Attached files

| file | filename |

|---|---|

| EX-32.1 - EXHIBIT 32.1 - SELLAS Life Sciences Group, Inc. | gale20160630ex321.htm |

| EX-31.2 - EXHIBIT 31.2 - SELLAS Life Sciences Group, Inc. | gale20160630ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - SELLAS Life Sciences Group, Inc. | gale20160630ex311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________________________

FORM 10-Q

________________________________

ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2016

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-33958

Galena Biopharma, Inc.

(Exact name of registrant as specified in its charter)

________________________________

Delaware | 20-8099512 | |

(State of incorporation) | (I.R.S. Employer Identification No.) | |

2000 Crow Canyon Place, Suite 380, San Ramon, CA 94583

(855) 855-4253

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

________________________________

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter time that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

Large accelerated filer | ¨ | Accelerated filer | ý | |||

Non-accelerated filer | ¨ | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): ¨ Yes ý No

As of July 31, 2016, Galena Biopharma, Inc. had outstanding 213,968,953 shares of common stock, $0.0001 par value per share, exclusive of treasury shares.

GALENA BIOPHARMA, INC.

FORM 10-Q - Quarterly Report

For the Quarter Ended June 30, 2016

TABLE OF CONTENTS

Part No. | Item No. | Description | Page No. | ||

I | |||||

1 | |||||

Condensed Consolidated Balance Sheets as of June 30, 2016 (unaudited) and December 31, 2015 | |||||

Condensed Consolidated Statements of Operations (unaudited) for the three and six months ended June 30, 2016 and 2015 | |||||

Condensed Consolidated Statement of Stockholders' Equity (unaudited) for the six months ended June 30, 2016 | |||||

Condensed Consolidated Statements of Cash Flows (unaudited) for the six months ended June 30, 2016 and 2015 | |||||

2 | |||||

3 | |||||

4 | |||||

II | |||||

1 | Legal Proceedings | ||||

1A | Risk Factors | ||||

6 | |||||

EX-31.1 | |||||

EX-31.2 | |||||

EX-32.1 | |||||

1

PART I FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

GALENA BIOPHARMA, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts in thousands, except share and per share data)

June 30, 2016 | December 31, 2015 | ||||||

(Unaudited) | |||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 19,590 | $ | 29,730 | |||

Restricted cash | 24,401 | 401 | |||||

Litigation settlement insurance recovery | — | 21,700 | |||||

Prepaid expenses and other current assets | 1,210 | 1,398 | |||||

Current assets of discontinued operations, net | 83 | 392 | |||||

Total current assets | 45,284 | 53,621 | |||||

Equipment and furnishings, net | 259 | 335 | |||||

In-process research and development | 12,864 | 12,864 | |||||

GALE-401 rights | 9,255 | 9,255 | |||||

Goodwill | 5,898 | 5,898 | |||||

Deposits and other assets | 218 | 171 | |||||

Total assets | $ | 73,778 | $ | 82,144 | |||

LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

Current liabilities: | |||||||

Accounts payable | $ | 1,273 | $ | 1,597 | |||

Accrued expenses and other current liabilities | 4,703 | 5,292 | |||||

Litigation settlement payable | 5,100 | 25,000 | |||||

Fair value of warrants potentially settleable in cash | 9,264 | 14,518 | |||||

Current portion of long-term debt | 23,157 | 4,739 | |||||

Current liabilities of discontinued operations | 3,727 | 5,925 | |||||

Total current liabilities | 47,224 | 57,071 | |||||

Deferred tax liability | 5,418 | 5,418 | |||||

Contingent purchase price consideration | 815 | 6,142 | |||||

Total liabilities | 53,457 | 68,631 | |||||

Commitments and contingencies | |||||||

Stockholders’ equity: | |||||||

Preferred stock, $0.0001 par value; 5,000,000 shares authorized; no shares issued and outstanding | — | — | |||||

Common stock, $0.0001 par value; 275,000,000 shares authorized, 182,996,385 shares issued and 182,321,385 shares outstanding at June 30, 2016; 162,581,753 shares issued and 161,906,753 shares outstanding at December 31, 2015 | 18 | 15 | |||||

Additional paid-in capital | 314,639 | 296,730 | |||||

Accumulated deficit | (290,487 | ) | (279,383 | ) | |||

Less treasury shares at cost, 675,000 shares | (3,849 | ) | (3,849 | ) | |||

Total stockholders’ equity | 20,321 | 13,513 | |||||

Total liabilities and stockholders’ equity | $ | 73,778 | $ | 82,144 | |||

See accompanying notes to condensed consolidated financial statements.

2

GALENA BIOPHARMA, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Amounts in thousands, except share and per share data)

(Unaudited)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Operating expenses: | |||||||||||||||

Research and development | $ | 6,175 | $ | 7,197 | $ | 11,618 | $ | 13,022 | |||||||

General and administrative | 3,117 | 1,886 | 6,642 | 4,973 | |||||||||||

Total operating expenses | 9,292 | 9,083 | 18,260 | 17,995 | |||||||||||

Operating loss | (9,292 | ) | (9,083 | ) | (18,260 | ) | (17,995 | ) | |||||||

Non-operating income (expense): | |||||||||||||||

Litigation settlements | (1,800 | ) | — | (1,800 | ) | — | |||||||||

Change in fair value of warrants potentially settleable in cash | 14,392 | (4,267 | ) | 10,520 | (3,115 | ) | |||||||||

Interest expense, net | (519 | ) | (207 | ) | (611 | ) | (432 | ) | |||||||

Change in fair value of the contingent purchase price liability | 5,497 | 83 | 5,327 | (238 | ) | ||||||||||

Total non-operating income (expense), net | 17,570 | (4,391 | ) | 13,436 | (3,785 | ) | |||||||||

Income (loss) from continuing operations | 8,278 | (13,474 | ) | (4,824 | ) | (21,780 | ) | ||||||||

Loss from discontinued operations | (2,889 | ) | (2,186 | ) | (6,280 | ) | (4,417 | ) | |||||||

Net income (loss) | $ | 5,389 | $ | (15,660 | ) | $ | (11,104 | ) | $ | (26,197 | ) | ||||

Net income (loss) per common share: | |||||||||||||||

Basic and diluted net income (loss) per share, continuing operations | $ | 0.05 | $ | (0.08 | ) | $ | (0.03 | ) | $ | (0.15 | ) | ||||

Basic and diluted net loss per share, discontinued operations | $ | (0.02 | ) | $ | (0.02 | ) | $ | (0.03 | ) | $ | (0.03 | ) | |||

Basic and diluted net income (loss) per share | $ | 0.03 | $ | (0.10 | ) | $ | (0.06 | ) | $ | (0.18 | ) | ||||

Weighted-average common shares outstanding: basic | 182,034,593 | 161,383,398 | 180,703,456 | 148,647,581 | |||||||||||

Weighted-average common shares outstanding: diluted | 185,477,330 | 161,383,398 | 180,703,456 | 148,647,581 | |||||||||||

See accompanying notes to condensed consolidated financial statements.

3

GALENA BIOPHARMA, INC.

CONDENSED CONSOLIDATED STATEMENT OF STOCKHOLDERS' EQUITY

(Amounts in thousands, except share amounts)

(Unaudited)

Common Stock | Additional Paid-In Capital | Accumulated Deficit | Treasury Stock | Total | ||||||||||||||||||

Shares Issued | Amount | |||||||||||||||||||||

Balance at December 31, 2015 | 162,581,753 | $ | 15 | $ | 296,730 | $ | (279,383 | ) | $ | (3,849 | ) | $ | 13,513 | |||||||||

Issuance of common stock | 19,772,727 | 3 | 20,186 | — | — | 20,189 | ||||||||||||||||

Common stock warrants issued in connection with January 2016 common stock offering | — | — | (5,590 | ) | — | — | (5,590 | ) | ||||||||||||||

Common stock warrants issued in connection with debt financing | — | — | 1,139 | — | — | 1,139 | ||||||||||||||||

Issuance of common stock upon exercise of warrants | 408,058 | — | 557 | — | — | 557 | ||||||||||||||||

Issuance of common stock in connection with employee stock purchase plan | 67,017 | — | 78 | — | — | 78 | ||||||||||||||||

Stock-based compensation for directors and employees | — | — | 1,278 | — | — | 1,278 | ||||||||||||||||

Exercise of stock options | 166,830 | — | 261 | — | — | 261 | ||||||||||||||||

Net loss | — | — | — | (11,104 | ) | — | (11,104 | ) | ||||||||||||||

Balance at June 30, 2016 | 182,996,385 | $ | 18 | $ | 314,639 | $ | (290,487 | ) | $ | (3,849 | ) | $ | 20,321 | |||||||||

See accompanying notes to condensed consolidated financial statements.

4

GALENA BIOPHARMA, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in thousands)

(Unaudited)

For the Six Months Ended June 30, | ||||||||

2016 | 2015 | |||||||

Cash flows from operating activities: | ||||||||

Cash flows from continuing operating activities: | ||||||||

Net loss from continuing operations | $ | (4,824 | ) | $ | (21,780 | ) | ||

Adjustment to reconcile net loss to net cash used in operating activities: | ||||||||

Depreciation and amortization expense | 777 | 181 | ||||||

Non-cash stock-based compensation | 1,278 | 759 | ||||||

Change in fair value of common stock warrants | (10,520 | ) | 3,115 | |||||

Change in fair value of contingent consideration | (5,327 | ) | 238 | |||||

Changes in operating assets and liabilities: | ||||||||

Prepaid expenses and other assets | 141 | 256 | ||||||

Litigation settlement insurance recovery | 21,700 | — | ||||||

Litigation settlement payable | (19,900 | ) | — | |||||

Accounts payable | (324 | ) | (825 | ) | ||||

Accrued expenses and other current liabilities | (589 | ) | (1,380 | ) | ||||

Net cash used in continuing operating activities | (17,588 | ) | (19,436 | ) | ||||

Cash flows from discontinued operating activities: | ||||||||

Net loss from discontinued operations | (6,280 | ) | (4,417 | ) | ||||

Changes in operating assets and liabilities attributable to discontinued operations | (839 | ) | 437 | |||||

Net cash used in discontinued operating activities | (7,119 | ) | (3,980 | ) | ||||

Net cash used in operating activities | (24,707 | ) | (23,416 | ) | ||||

Cash flows from investing activities: | ||||||||

Cash paid for purchase of equipment and furnishings | (6 | ) | (34 | ) | ||||

Net cash used in continuing investing activities | (6 | ) | (34 | ) | ||||

Selling costs paid for sale of commercial assets | (1,050 | ) | — | |||||

Cash paid for commercial assets | — | (534 | ) | |||||

Net cash used in discontinued investing activities | (1,050 | ) | — | (534 | ) | |||

Net cash used in investing activities | (1,056 | ) | (568 | ) | ||||

Cash flows from financing activities: | ||||||||

Net proceeds from issuance of common stock | 20,189 | 47,416 | ||||||

Net proceeds from exercise of stock options | 261 | 1 | ||||||

Proceeds from exercise of warrants | 233 | — | ||||||

Proceeds from common stock issued in connection with ESPP | 78 | 110 | ||||||

Net proceeds from issuance of long-term debt | 23,641 | — | ||||||

Minimum cash covenant on long-term debt | (24,000 | ) | — | |||||

Principal payments on long-term debt | (4,779 | ) | (1,914 | ) | ||||

Net cash provided by financing activities | 15,623 | 45,613 | ||||||

Net (decrease) increase in cash and cash equivalents | (10,140 | ) | 21,629 | |||||

Cash and cash equivalents at the beginning of period | 29,730 | 23,650 | ||||||

Cash and cash equivalents at end of period | $ | 19,590 | $ | 45,279 | ||||

Supplemental disclosure of cash flow information: | ||||||||

Cash received during the periods for interest | $ | 49 | $ | 2 | ||||

Cash paid during the periods for interest | $ | 606 | $ | 312 | ||||

Supplemental disclosure of non-cash investing and financing activities: | ||||||||

Fair value of warrants issued in connection with common stock recorded as cost of equity | $ | 5,590 | $ | 10,296 | ||||

Reclassification of warrant liabilities upon exercise | $ | 324 | $ | — | ||||

5

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. Business and Basis of Presentation

Overview

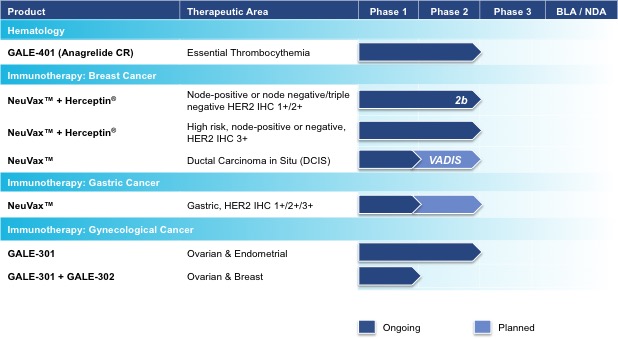

Galena Biopharma, Inc. (“we,” “us,” “our,” “Galena” or the “Company”) is a biopharmaceutical company committed to the development and commercialization of hematology and oncology therapeutics that address unmet medical needs. The Company’s pipeline consists of multiple mid- to late-stage clinical assets, including our hematology asset, GALE-401, our novel cancer immunotherapy programs including NeuVax™ (nelipepimut-S), GALE-301 and GALE-302. GALE-401 is a controlled release version of the approved drug anagrelide for the treatment of elevated platelets in patients with myeloproliferative neoplasms. GALE-401 has completed a Phase 2 trial and we are advancing the asset into a pivotal trial. NeuVax is currently in multiple Phase 2 trials. GALE-301 is in a Phase 2a clinical trial in ovarian and endometrial cancers and in a Phase 1b clinical trial given sequentially with GALE-302.

We are seeking to build value for shareholders through pursuit of the following objectives:

• | Developing hematology and oncology assets through clinical development, targeting areas of unmet medical need. Our hematology asset is targeting the treatment of patients with essential thrombocythemia (ET) to reduce elevated platelet counts. Our immunotherapy programs are currently targeting two key areas: secondary prevention intended to significantly decrease the risk of disease recurrence in breast, gastric, and ovarian cancers; and primary prevention intended to cease or delay ductal carcinoma in situ (DCIS) from becoming invasive breast cancer. |

• | Expand our development pipeline by enhancing the clinical and geographic footprint of our technologies. We intend to accomplish this through the initiation of new clinical trials and potentially through the acquisition of additional development programs. |

• | Leverage partnerships and collaborations, as well as investigator-sponsored trial arrangements, to maximize the scope of potential clinical opportunities in a cost effective and efficient manner. |

6

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

Basis of Presentation and Significant Accounting Policies

The accompanying consolidated financial statements included herein have been prepared by Galena pursuant to the generally accepted accounting principles (GAAP). Unless the context otherwise indicates, references in these notes to the “Company,” “we,” “us” or “our” refer (i) to Galena, our wholly owned subsidiaries, Apthera, Inc., or “Apthera,” and our wholly owned subsidiary, Mills Pharmaceuticals, LLC or "Mills."

At June 30, 2016, the Company’s capital resources consisted of cash and cash equivalents of $19.6 million not including $24.4 million of restricted cash. The Company will need to continue to incur significant expenses to advance our development portfolio and will need to raise additional capital to finance such activities.

On July 13, 2016, we closed the sale to certain institutional investors of 28,000,000 shares of common stock at a purchase price per share of $0.45 in a registered direct offering, and warrants to purchase up to 14,000,000 shares of common stock with an exercise price of $0.65 per share in a concurrent private placement. The warrants are initially exercisable six months and one day following issuance and have a term of five years from the date of issuance. The net proceeds to Galena after deducting placement agent fees and estimated offering expenses were approximately $11.7 million. The Company intends to use the net proceeds from this offering to fund its clinical trials of its product candidates, to augment its working capital, and for general corporate purposes. The current unrestricted cash and cash equivalents as of the date of this filing will fund the Company's operations for at least six months.

Additional funding was received July 13, 2016 upon the closing of an underwritten registered direct offering of our common stock and a private placement of warrants for net proceeds of $11.7 million to the Company. Additional funding sources that are, or in certain circumstances may be, available to the Company, include 1) approximately $24 million of restricted cash associated with our $25.5 million sale of Debentures by amending the current agreement with the holder to reduce the minimum cash covenant as detailed in Note 4; 2) a Purchase Agreement with Lincoln Park Capital, LLC; and 3) At Market Issuance Sales Agreements (ATM) with FBR & Co. (formerly MLV & Co. LLC) and Maxim Group LLC. The Purchase Agreement and ATM are unavailable to the Company until 75 days after the closing of our July 2016 financing. The Company cannot provide assurances that its plans will not change or that changed circumstances will not result in the depletion of its capital resources more rapidly than it currently anticipates. The Company is seeking and will need to raise additional capital, whether through a sale of equity or debt securities, a strategic business, the establishment of other funding facilities, licensing arrangements, asset sales or other means, in order to continue the development of the Company's product candidates and to support its other ongoing activities. However, the Company cannot be certain that it will be able to raise additional capital on favorable terms, or at all, which raises substantial doubt about the Company’s ability to continue as a going concern. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Discontinued Operations — As described in Note 11, during the quarter ended September 30, 2015 the Company met the relevant criteria for reporting the commercial operations as held for sale and in discontinued operations, pursuant to FASB Topic 205-20, Presentation of Financial Statements - Discontinued Operations, and FASB Topic 360, Property, Plant, and Equipment. During the quarter ended December 31, 2015, the Company completed the sale of the commercial products and the related assets.

Uses of Estimates in Preparation of Financial Statements — The preparation of these consolidated financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ materially from those estimates.

Principles of Consolidation — The consolidated financial statements include the accounts of Galena and its wholly owned subsidiaries. All material intercompany accounts have been eliminated in consolidation.

7

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

Reclassifications — Certain prior year amounts have been reclassified to conform to current year presentation. These reclassifications had no effect on net loss per share. The Company has reclassified the financial information for the three and six months ended June 30, 2015 to present the Company's commercial business as discontinued operations in the accompanying financial statements as the commercial business was divested in the fourth quarter of 2015.

Cash and Cash Equivalents — The Company considers all highly liquid debt instruments with an original maturity of 90 days or less to be cash equivalents. Cash equivalents consist primarily of amounts invested in money market accounts and demand deposits.

Restricted Cash — Restricted cash consists of certificates of deposit on hand with the Company’s financial institutions as collateral for its corporate credit cards and the minimum cash covenant per the Company's outstanding Debentures as described in Note 4.

Fair Value of Financial Instruments — The carrying amounts reported in the balance sheet for cash equivalents, accounts receivable, accounts payable, and capital leases approximate their fair values due to their short-term nature and market rates of interest.

Equipment and Furnishings — Equipment and furnishings are stated at cost and depreciated using the straight-line method based on the estimated useful lives (generally three to five years) of the related assets.

Goodwill and Intangible Assets — Goodwill and indefinite-lived intangible assets are not amortized but are tested annually for impairment at the reporting unit level, or more frequently if events and circumstances indicate impairment may have occurred. Factors the Company considers important that could trigger an interim review for impairment include, but are not limited to, the following:

• | Significant changes in the manner of its use of acquired assets or the strategy for its overall business; |

•Significant negative industry or economic trends;

•Significant decline in stock price for a sustained period; and

•Significant decline in market capitalization relative to net book value.

Goodwill and other intangible assets with indefinite lives are evaluated for impairment first by a qualitative assessment to determine the likelihood of impairment. If it is determined that impairment is more likely than not, the Company will then proceed to the two step impairment test. The first step is to compare the fair value of the reporting unit to the carrying amount of the reporting unit. If the carrying amount exceeds the fair value, a second step must be followed to calculate impairment. Otherwise, if the fair value of the reporting unit exceeds the carrying amount, the goodwill is not considered to be impaired as of the measurement date. In its review of the carrying value of the goodwill for its single reporting unit and its indefinite-lived intangible assets, the Company determines fair values of its goodwill using the market approach, and its indefinite-lived intangible assets using the income approach.

Intangible assets not considered indefinite-lived are reviewed for impairment when facts or circumstances suggest that the carrying value of these assets may not be recoverable. The Company’s policy is to identify and record impairment losses, if necessary, on intangible assets when events and circumstances indicate that the assets might be impaired and the undiscounted cash flows estimated to be generated by those assets are less than the carrying amounts.

In connection with the interim analysis of the PRESENT Phase 3 clinical trial and subsequent close down of the trial, the Company performed an impairment analysis of the intangible asset and goodwill. The fair value was determined to exceed to the carrying amount as of June 30, 2016 based on the other ongoing and and planned trials with NeuVax. As a result, no impairment was deemed necessary to these assets as of June 30, 2016.

8

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

Acquisitions and In-Licensing — For all in-licensed products and technologies, we perform an analysis to determine whether we hold a variable interest or a controlling financial interest in a variable interest entity. On the basis of our interpretations and conclusions, we determine whether the acquisition falls under the purview of variable interest entity accounting and if so, consider the necessity to consolidate the acquisition. As of June 30, 2016, we determined there were no variable interest entities required to be consolidated.

We also perform an analysis to determine if the assets and liabilities acquired in an acquisition qualify as a "business." The excess of the purchase price over the fair value of the net assets acquired can only be recognized as goodwill in a business combination. The Company completes its valuation analysis no later than twelve months from the date of the acquisition.

Contingent Purchase Price Consideration — Contingent consideration in business combinations is recorded at the estimated fair value as of the acquisition date. The fair value of the contingent consideration is re-measured at each reporting period with any adjustments in fair value included in our consolidated statement of comprehensive loss.

Patents and Patent Application Costs — Although the Company believes that its patents and underlying technology have continuing value, the amount of future benefits to be derived from the patents is uncertain. Patent costs are, therefore, expensed as incurred.

Litigation Settlement Payable and Insurance Recoveries — There can be a significant time lag between the time that legal fees are incurred and the insurance reimbursement available to offset the related costs. The legal costs are recorded in the period they are incurred, and the insurance recoveries for those costs are recorded in the period when the insurance reimbursement is deemed probable.

Share-based Compensation — The Company follows the provisions of the FASB ASC Topic 718, Compensation — Stock Compensation (“ASC 718”), which requires the measurement and recognition of compensation expense for all stock-based payment awards made to employees, non-employee directors, and consultants, including stock options and warrants. Stock compensation expense based on the grant date fair value estimated in accordance with the provisions of ASC 718 is recognized as an expense over the requisite service period.

For stock options and warrants granted as consideration for services rendered by non-employees, the Company recognizes compensation expense in accordance with the requirements of FASB ASC Topic 505-50 (“ASC 505-50”), Equity Based Payments to Non- Employees. Non-employee option and warrant grants that do not vest immediately upon grant are recorded as an expense over the vesting period. At the end of each financial reporting period prior to vesting, the value of these options and warrants, as calculated using the Black-Scholes option-pricing model, is re-measured using the fair value of the Company’s common stock and the non-cash compensation recognized during the period is adjusted accordingly. Since the fair market value of options and warrants granted to non-employees is subject to change in the future, the amount of the future compensation expense will include fair value re-measurements until the stock options are fully vested.

Research and Development Expenses — Research and development costs are expensed as incurred. Included in research and development costs are wages, benefits and other operating costs, facilities, supplies, external services and overhead related to our research and development departments, and clinical trial expenses.

Clinical trial expenses include direct costs associated with contract research organizations (CROs), as well as patient-related costs at sites at which our trials are being conducted. Direct costs associated with our CROs are generally payable on a time and materials basis, or when certain enrollment and monitoring milestones are achieved. Expense related to a milestone is recognized in the period in which the milestone is achieved or in which we determine that it is more likely than not that it will be achieved.

9

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

The invoicing from clinical trial sites can lag several months. We accrue these site costs based on our estimate of upfront set-up costs upon the screening of the first patient at each site, and the patient related costs based on our knowledge of patient enrollment status at each site.

Income Taxes — The Company recognizes liabilities or assets for the deferred tax consequences of temporary differences between the tax basis of assets or liabilities and their reported amounts in the financial statements in accordance with FASB ASC 740-10, Accounting for Income Taxes (“ASC 740-10”). These temporary differences will result in taxable or deductible amounts in future years when the reported amounts of the assets or liabilities are recovered or settled. ASC 740-10 requires that a valuation allowance be established when management determines that it is more likely than not that all or a portion of a deferred asset will not be realized. The Company evaluates the realizability of its net deferred income tax assets and valuation allowances as necessary, at least on an annual basis. During this evaluation, the Company reviews its forecasts of income in conjunction with other positive and negative evidence surrounding the realizability of its deferred income tax assets to determine if a valuation allowance is required. Adjustments to the valuation allowance will increase or decrease the Company’s income tax provision or benefit. The recognition and measurement of benefits related to the Company’s tax positions requires significant judgment, as uncertainties often exist with respect to new laws, new interpretations of existing laws, and rulings by taxing authorities. Differences between actual results and the Company’s assumptions or changes in the company’s assumptions in future periods are recorded in the period they become known.

There was no income tax expense or benefit for the three and six month periods ended June 30, 2016 and 2015. We continue to maintain a full valuation allowance against our net deferred tax assets.

Concentrations of Credit Risk — Financial instruments that potentially subject the Company to significant concentrations of credit risk consist principally of cash and cash equivalents. The Company maintains cash balances in several accounts with two banks, which at times are in excess of federally insured limits. As of June 30, 2016, the Company’s cash equivalents were invested in money market mutual funds. The Company’s investment policy does not allow investment in any debt securities rated less than “investment grade” by national ratings services. The Company has not experienced any losses on its deposits of cash and cash equivalents. The Company maintains significant cash and cash equivalents at two financial institutions that are in excess of federally insured limits.

Comprehensive Loss — Comprehensive loss consists of our net loss, with no other comprehensive income items for the periods presented.

Effect of Recent Accounting Pronouncements

In February 2016, the FASB issued Accounting Standards Update No. 2016-02, Leases ("ASU 2016-02"). ASU 2016-02 provides accounting guidance for both lessee and lessor accounting models. Among other things, lessees will recognize a right-of-use asset and a lease liability for leases with a duration of greater than one year. For income statement purposes, ASU 2016-02 will require leases to be classified as either operating or finance. Operating leases will result in straight-line expense while finance leases will result in a front-loaded expense pattern. The new standard will be effective for us on January 1, 2019 and will be adopted using a modified retrospective approach which will require application of the new guidance at the beginning of the earliest comparative period presented. We are currently evaluating the effect that the updated standard will have on our consolidated financial statements and related disclosures, however, we anticipate recognition of additional assets and corresponding liabilities related to leases on our balance sheet upon adoption.

In March 2016, the FASB issued Accounting Standards Update No. 2016-09, Compensation-Stock Compensation ("ASU 2016-09"). ASU 2016-09 changes several aspects of the accounting for share-based payment transactions including the income tax consequences, classification of awards as either equity or liabilities, employee tax withholding, calculation of shares for use in diluted earnings per share, and classification on the statement of cash flows. The new standard will be effective for us on January 1, 2017. Early adoption is available. We are currently evaluating the effect that the updated standard will have on our consolidated financial statements and related disclosures.

10

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

2. Fair Value Measurements

The Company follows ASC 820, Fair Value Measurements and Disclosures, (“ASC 820”) for the Company’s financial assets and liabilities that are re-measured and reported at fair value at each reporting period, and are re-measured and reported at fair value at least annually using a fair value hierarchy that is broken down into three levels. Level inputs are defined as follows:

Level 1 — quoted prices in active markets for identical assets or liabilities.

Level 2 — other significant observable inputs for the assets or liabilities through corroboration with market data at the measurement date.

Level 3 — significant unobservable inputs that reflect management’s best estimate of what market participants would use to price the assets or liabilities at the measurement date.

The Company categorized its cash equivalents as Level 1. The valuations for Level 1 were determined based on a “market approach” using quoted prices in active markets for identical assets. Valuation of these assets does not require a significant degree of judgment. The Company categorized its warrants potentially settleable in cash as Level 2 inputs. The warrants are measured at market value on a recurring basis and are being marked to market each quarter-end until they are completely settled. The warrants are valued using an appropriate pricing model, using assumptions consistent with our application of ASC 718. The contingent purchase price consideration is categorized as Level 3 inputs and is measured at its estimated fair value on a recurring basis and is adjusted at each quarter-end until it is completely settled. The contingent purchase price consideration is valued based on the expected timing of milestones, the expected probability of success for each milestone and discount rates based on a corporate debt interest rate index publicly issued.

The following tables present information about our assets and liabilities measured at fair value on a recurring basis in the condensed consolidated balance sheets (in thousands):

Description | June 30, 2016 | Quoted Prices In Active Markets (Level 1) | Significant Other Observable Inputs (Level 2) | Unobservable Inputs (Level 3) | |||||||||||

Assets: | |||||||||||||||

Cash equivalents | $ | 18,169 | $ | 18,169 | $ | — | $ | — | |||||||

Total assets measured and recorded at fair value | $ | 18,169 | $ | 18,169 | $ | — | $ | — | |||||||

Liabilities: | |||||||||||||||

Warrants potentially settleable in cash | $ | 9,264 | $ | — | $ | 9,264 | $ | — | |||||||

Contingent purchase price consideration | 815 | — | — | 815 | |||||||||||

Total liabilities measured and recorded at fair value | $ | 10,079 | $ | — | $ | 9,264 | $ | 815 | |||||||

Description | December 31, 2015 | Quoted Prices In Active Markets (Level 1) | Significant Other Observable Inputs (Level 2) | Unobservable Inputs (Level 3) | |||||||||||

Assets: | |||||||||||||||

Cash equivalents | $ | 29,171 | $ | 29,171 | $ | — | $ | — | |||||||

Total assets measured and recorded at fair value | $ | 29,171 | $ | 29,171 | $ | — | $ | — | |||||||

Liabilities: | |||||||||||||||

Warrants potentially settleable in cash | $ | 14,518 | $ | — | $ | 14,518 | $ | — | |||||||

Contingent purchase price consideration | 6,142 | — | — | 6,142 | |||||||||||

Total liabilities measured and recorded at fair value | $ | 20,660 | $ | — | $ | 14,518 | $ | 6,142 | |||||||

11

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

The Company did not transfer any financial instruments into or out of Level 3 classification during the six months ended June 30, 2016 and 2015. A reconciliation of the beginning and ending Level 3 liabilities for the six months ended June 30, 2016 is as follows (in thousands):

Fair Value Measurements Using Significant Unobservable Inputs (Level 3) | |||

Balance, January 1, 2016 | $ | 6,142 | |

Change in the estimated fair value of the contingent purchase price consideration | (5,327 | ) | |

Balance at June 30, 2016 | $ | 815 | |

The fair value of the contingent purchase price consideration is measured at the end of each reporting period using Level 3 inputs in a probability-weighted, discounted cash-outflow model. The significant unobservable assumptions include the probability of achieving each milestone, the date we expect to reach the milestone, and a determination of present value factors used to discount future expected cash outflows. The change in the estimated fair value of the contingent purchase price consideration during the quarter ended June 30, 2016 reflects an adjusted probability and time line for the potential approval of NeuVax associated with the Phase 2 combination trial with trastuzumab. Previously, the valuation was measured using the probability and time line of the Phase 3 PRESENT trial, which was stopped in June 2016 due to futility as recommended by the Independent Data Monitoring Committee ("IDMC").

See Note 7 for discussion of the Level 2 liabilities relating to warrants accounted for as liabilities.

3. Accrued Expenses and Other Current Liabilities

Accrued expenses and other current liabilities consist of the following (in thousands):

June 30, 2016 | December 31, 2015 | ||||||

Clinical trial costs | $ | 3,208 | $ | 3,294 | |||

Professional fees | 560 | 435 | |||||

Compensation and related benefits | 935 | 1,535 | |||||

Interest expense | — | 28 | |||||

Accrued expenses and other current liabilities | $ | 4,703 | $ | 5,292 | |||

12

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

4. Long-term Debt

On May 8, 2013, we entered into a loan and security agreement with Oxford Finance LLC, as collateral agent, and related lenders under which we borrowed the first tranche of $10 million (the "Loan"). The Loan payment terms include 12 months of interest-only payments at the fixed coupon rate of 8.45%, followed by 30 months of amortization of principal and interest until maturity in November 2016. In connection with the Loan, we paid the lender a 1% cash facility fee and a 5.5% cash final payment and granted to the lenders seven-year warrants to purchase up to 182,186 shares of our common stock at an exercise price of $2.47, which equaled a 20-day average market price of our common stock prior to the date of the grant. On May 10, 2016, the Company prepaid the outstanding principal amount and cash final payment.

On May 10, 2016, the Company entered into a Securities Purchase Agreement, with certain purchasers pursuant to which the Company sold, at a 6.375% original issue discount, a total of $25,530,000 Senior Secured Debentures (the “Debentures”) and warrants to purchase up to 2.0 million shares of the Company's common stock. Net proceeds to the Company from sale of the Debentures, after payment of commissions and legal fees, were approximately $23,400,000. The Debentures mature November 10, 2018, accrue interest at 9% per year, and do not contain any conversion features into shares of our common stock. The Company intends to use the net proceeds from this offering to fund the costs associated with the close down of the Phase 3 PRESENT study of NeuVax and other clinical trials of our product candidates and to augment its working capital and for general corporate purposes.

The Debentures carry an interest only period of six months following which the holder shall have the rights, at its option, to require the Company to redeem up to $1,100,000 per month of the outstanding principal amount of these Debentures. Interest is payable at the end of each month based on the outstanding principal.

The Company is required to promptly, but in any event no more than three trading days after the holder delivers a redemption notice to the Company, pay the applicable redemption amount in cash or, at the Company’s election and subject to certain conditions, in shares of the Company's common stock. If the Company elects to pay the redemption amount in shares of its common stock, then the shares will be delivered at the lesser of A) 7.5% discount to the average of the 3 lowest volume weighted average prices over the prior 20 trading days or B) a 7.5% discount to the prior trading day’s volume weighted average price. The Company may only opt for payment in shares of common stock if certain equity conditions are met. The Company, at its option, may also force the holder to redeem up to double the monthly redemption principal amount of the Debentures but not less than the monthly payment.

Based on the recommendation of the IDMC to stop the PRESENT Trial, the holder has the right to require the Company to prepay in cash all, or any portion, of the outstanding principal amount of this Debenture funded in cash by the holder on the closing date, plus all accrued and unpaid interest. If the holder elects such prepayment of the Debentures, then the number of shares subject to the warrants issued to the holder will be reduced in proportion to the percentage of principal required and accrued interest to be prepaid by the Company. The Purchaser received 1 million warrants upon the closing on the sale of the Debentures at an exercise price of $1.51, maturing 5 years from issuance. Additionally, the Purchasers received 1 million warrants upon the Company's public company announcement of the interim analysis on June 29, 2016 at an exercise price of $0.43. As of June 30, 2016 and the date of this filing, the holder had not exercised its right to require the Company to prepay in cash all, or any portion, of the outstanding principal amount of the Debentures. The holder's right to require the Company to prepay the outstanding principal amount expires 30 trading days after June 29, 2016, the announcement date of the recommendation of the IDMC. Therefore as of June 30, 2016 the Debentures, net of unamortized discounts, are presented as current liabilities on the condensed consolidated balance sheet.

The Company’s obligations under the Debenture can be accelerated in the event the Company undergoes a change in control and other customary events of default. In the event of default and acceleration of the Company’s obligations, the Company would be required to pay all amounts of principal and interest then outstanding under the Debenture in cash. The Company’s obligations under the Debentures are secured under a Security Agreement by a senior lien on all of the Company’s assets, including all of the Company’s interests in its consolidated subsidiaries. Until the holder exercises its right to require the Company to prepay some or all of the loan, the Company must also maintain a minimum of $24.0 million in cash, which is included in restricted cash as of June 30, 2016.

13

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

Armentum Partners, LLC (the “Placement Agent”) acted as the placement agent in the offering of the Debentures and the Company agreed to pay the Placement Agent a fee equal to 2% of the funds received from the sale of the Debentures. The Company paid half of the placement fee upon funding with the remaining payable at such time as the IDMC recommended in favor of the continuation of the PRESENT Trial or the holder waives the Company’s obligation to prepay the Debenture as a result of the IDMC’s recommendation.

5. Legal Proceedings, Commitments and Contingencies

Legal Proceedings

On December 3, 2015, we agreed in principle to resolve and settle the consolidated shareholder derivative action, In re Galena Biopharma, Inc. Derivative Litigation, Civil Action No. 3:14-cv-00382-SI, pending in the United States District Court for the District of Oregon against us and certain of our current and former officers and directors. On April 21, 2016, the District Court of Oregon held the final approval hearing of the settlement with the derivative plaintiffs after which the District Court continued the final approval hearing until June 23, 2016 and requested the parties submit additional briefing by June 9, 2016 on the fee request by the derivative plaintiffs’ attorneys. Following the hearing on June 23, 2016, on June 24, 2016, the U.S. District Court for the District of Oregon entered a final order and judgment in In re Galena Biopharma, Inc. Derivative Litigation, granting final approval to the settlement.

On the same day, the Court also issued an opinion and order awarding attorney’s fees of $4.5 million plus costs, which will be paid by our insurance carriers. The settlement includes a payment of $15 million in cash by our insurance carriers, which we used to fund a portion of the class action settlement, and cancellation of 1,200,000 outstanding director stock options. The settlement also requires that we adopt and implement certain corporate governance measures. The settlement does not include any admission of wrongdoing or liability on the part of us or the individual defendants and includes a full release of us and the current and former officers and directors in connection with the allegations made in the consolidated federal derivative actions and state court derivative actions.

On December 3, 2015, we also agreed in principal to resolve and settle the securities putative class action lawsuit, In re Galena Biopharma, Inc. Securities Litigation, Civil Action No. 3:14-cv-00367-SI, pending against us, certain of our current and former officers and directors and other defendants in the United States District Court for the District of Oregon. Following the hearing on June 23, 2016, on June 24, 2016, the U.S. District Court for the District of Oregon entered a final order and partial judgment in In re Galena Biopharma, Inc. Securities Litigation, granting final approval of the settlement. On the same day, the Court also issued an opinion and order awarding attorney’s fees of $4.5 million plus costs, which is paid out of the settlement funds. The settlement agreement provides for a payment of $20 million to the class and the dismissal of all claims against us and our current and former officers and directors in connection with the consolidated federal securities class actions. Of the $20 million settlement payment to the class, $16.7 million was paid by our insurance carriers and $2.3 million in cash was paid by us on July 1, 2016, along with $1 million in shares of our common stock (480,053 shares) paid by us on July 6, 2016. We will be responsible for defense costs and any settlements or judgments incurred for any related opt-out lawsuits. As of June 30, 2016 our insurance carriers paid $21.7 million. The Company paid $2.3 million in cash and $1 million in common stock on July 1, 2016.

In July 2016, we have resolved claims brought by shareholders that relate to the securities litigation mentioned above in one case for $150,000 plus $150,000 in shares (291,262) of our common stock, and in another case for $1.5 million in shares of our common stock (3,366,750 shares). The shares issued in connection with such settlements are included in the secondary offering filed on July 25, 2016. The settlements do not include any admission of wrongdoing or liability on the part of us or any of the current or former directors and officers and includes a full release of us and the current and former directors and officers in connection with the allegations made. We are not aware of any other claims made by shareholders who have opted out of the securities litigation.

14

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

The litigation settlements are summarized as follow as of June 30, 2016 (in thousands)

Amount | |||

Class action settlement | $ | 20,000 | |

Derivative settlement | 5,000 | ||

Shareholders securities litigation settlements | $ | 1,800 | |

Total settlements | $ | 26,800 | |

Paid by the insurance carriers | $ | 21,700 | |

Payable by the company in cash (paid in July 2016) | 2,450 | ||

Payable by the company in common stock (paid in July 2016) | 2,650 | ||

Total settlements | $ | 26,800 | |

We are aware that the SEC is investigating certain matters relating to the use of certain outside investor-relations professionals by us and other public companies. We have been in contact with the SEC staff through our counsel and are cooperating with the investigation and in discussions with the SEC staff to resolve the investigation.

A federal investigation of two of the high-prescribing physicians for Abstral has resulted in the criminal prosecution of the two physicians for alleged violations of the federal False Claims Act and other federal statutes. The criminal trial is set for October 2016. We have received a trial subpoena for documents in connection with that investigation and we have been in contact with the U.S. Attorney’s Office for the Southern District of Alabama, which is handling the criminal trial, and are cooperating in the production of documents. On April 28, 2016, a second superseding indictment was filed in the criminal case, which added additional information about the defendant physicians and provided information regarding the facts and circumstances involving a rebate agreement between the Company and the defendant physicians’ pharmacy as well as their ownership of our stock. Certain former employees have received trial subpoenas to appear at the trial and provide oral testimony. We have agreed to reimburse those former employees’ attorney’s fees. To our knowledge, we are not a target or subject of that investigation.

There also have been federal and state investigations of a company that has a product that competes with Abstral in the same therapeutic class, and we have learned that the FDA and other governmental agencies are investigating our Abstral promotion practices. On December 16, 2015, we received a subpoena issued by the U.S. Attorney’s Office in District of New Jersey requesting the production of a broad range of documents pertaining to our marketing and promotional practices for Abstral. We have been in contact with the U.S. Attorney’s Office for the District of New Jersey and are cooperating in the production of the requested documents. We are unable to predict whether we could become subject to legal or administrative actions as a result of these matters, or the impact of such matters. If we are found to be in violation of the False Claims Act, Anti-Kickback Statute, Patient Protection and Affordable Care Act, or any other applicable state or any federal fraud and abuse laws, we may be subject to penalties, such as civil and criminal penalties, damages, fines, or an administrative action of exclusion from government health care reimbursement programs. We can make no assurances as to the time or resources that will need to be devoted to these matters or their outcome, or the impact, if any, that these matters or any resulting legal or administrative proceedings may have on our business or financial condition.

15

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

6. Stockholders’ Equity

Preferred Stock — The Company has authorized up to 5,000,000 shares of preferred stock, $0.0001 par value per share, for issuance. The preferred stock will have such rights, preferences, privileges and restrictions, including voting rights, dividend rights, conversion rights, redemption privileges and liquidation preferences, as shall be determined by the Company’s Board of Directors upon its issuance. To date, the Company has not issued any preferred shares.

Common Stock — The Company has authorized up to 275,000,000 shares of common stock, $0.0001 par value per share, for issuance. On July 14, 2016, shareholders approved a 75,000,000 share increase to the Company's authorized shares of common stock up to 350,000,000 shares.

November 2014 Purchase Agreement with Lincoln Park Capital, LLC - On November 18, 2014, the Company entered into a purchase agreement with Lincoln Park Capital, LLC (LPC), pursuant to which the Company has the right to sell to LPC up to $50 million in shares of the Company's common stock, subject to certain limitations and conditions over the 36 month term of the purchase agreement. Pursuant to the purchase agreement, LPC initially purchased 2.5 million shares of the Company's common stock at $2.00 per share and the Company issued 631,221 shares of common stock to LPC as a commitment fee, which was recorded as a cost of capital. As a result of this initial issuance, the Company received initial net proceeds of $4.9 million, after deducting commissions and other offering expenses. In addition to LPC’s initial purchase of our common stock under the purchase agreement, during the first quarter of 2015, we received net proceeds of $4.4 million from LPC’s subsequent purchases of a total of 2.7 million shares of our common stock, excluding the commitment fee shares. There were no sales of our common stock under the LPC purchase agreement during the six months ended June 30, 2016.

At Market Issuance Sales Agreements - On May 24, 2013 the Company entered into At Market Issuance Sales Agreements (ATM) with FBR & Co. (formerly MLV & Co. LLC) and Maxim Group LLC (the Agents). From time to time during the term of the ATM, we may issue and sell through the Agents, shares of our common stock, and the Agents collect a fee equal to 3% of the gross proceeds from the sale of shares, up to a total limit of $20 million in gross proceeds. The ATM is available to the Company until it is terminated by the Agents or the Company. During the first quarter of 2015, we received $2.3 million in net proceeds from the sale of 1.4 million shares of our common stock through the ATM. There were no sales of our common stock under the ATM during the six months ended June 30, 2016.

March 2015 Underwritten Public Offering - On March 18, 2015 the Company closed an underwritten public offering of 24,358,974 units at a price to the public of $1.56 per unit for gross proceeds of $38 million (the "March 2015 Offering"). Each unit consists of one share of common stock, and a warrant to purchase 0.50 of a share of common stock at an exercise price of $2.08 per share. The March 2015 Offering included an over-allotment option for the underwriters to purchase an additional 3,653,846 shares of common stock and/or warrants to purchase up to 1,826,923 shares of common stock. On March 18, 2015, the underwriters exercised their over-allotment option to purchase warrants to purchase an aggregate of 1,826,923 shares of common stock. On April 10, 2015, the underwriters exercised their over-allotment option to purchase 3,653,846 shares of common stock for additional net proceeds of $5.4 million. The total net proceeds of the March 2015 Offering, including the exercise of the over-allotment option to purchase the warrants, were $40.8 million, after deducting underwriting discounts and commissions and offering expenses payable by the Company.

January 2016 Underwritten Public Offering - On January 12, 2016 the Company closed an underwritten public offering of 19,772,727 units at a price to the public of $1.10 per unit for gross proceeds of $21.8 million (the "January 2016 Offering"). Each unit consists of one share of common stock, and a warrant to purchase 0.60 of a share of common stock at an exercise price of $1.42 per share. The January 2016 Offering included an over-allotment option for the underwriters to purchase an additional 2,965,909 shares of common stock and/or warrants to purchase up to 1,779,545 shares of common stock. On January 12, 2016, the underwriters exercised their over-allotment option to purchase warrants to purchase an aggregate of 1,779,545 shares of common stock. The underwriters did not exercise their over-allotment option to purchase 2,965,909 shares of our common stock. The total net proceeds of the January 2016 Offering, including the exercise of the over-allotment option to purchase the warrants, were $20.2 million, after deducting underwriting discounts and commissions and offering expense paid by the Company.

16

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

Shares of common stock for future issuance are reserved for as follows (in thousands):

As of June 30, 2016 | ||

Warrants outstanding | 37,418 | |

Stock options outstanding | 10,309 | |

Options reserved for future issuance under the Company’s 2007 Incentive Plan | 10,923 | |

Shares reserved for future issuance under the Employee Stock Purchase Plan | 461 | |

Total reserved for future issuance | 59,111 | |

7. Warrants

The following is a summary of warrant activity for the six months ended June 30, 2016 (in thousands):

January 2016 Warrants | March 2015 Warrants | September 2013 Warrants | December 2012 Warrants | Other Equity Financing Warrants | Warrants issued to Consultants and Debtors | Total | ||||||||||||||

Outstanding, January 1, 2016 | — | 14,006 | 3,973 | 3,031 | 816 | 482 | 22,308 | |||||||||||||

Issued | 13,643 | — | — | — | — | 2,000 | 15,643 | |||||||||||||

Exercised | — | — | — | — | (502 | ) | — | (502 | ) | |||||||||||

Expired | — | — | — | — | (31 | ) | — | (31 | ) | |||||||||||

Outstanding, June 30, 2016 | 13,643 | 14,006 | 3,973 | 3,031 | 283 | 2,482 | 37,418 | |||||||||||||

Expiration | January 2021 | March 2020 | September 2018 | December 2017 | Varies 2016-2017 | Varies 2014-2021 | ||||||||||||||

Warrants consist of warrants potentially settleable in cash, which are liability-classified warrants, and equity-classified warrants.

Warrants classified as liabilities

Liability-classified warrants consist of warrants to purchase common stock issued in connection with equity financings in January 2016, March 2015, September 2013, December 2012, April 2011, March 2011, and March 2010. These warrants are potentially settleable in cash and were determined not to be indexed to our common stock.

The estimated fair value of outstanding warrants accounted for as liabilities is determined at each balance sheet date. Any decrease or increase in the estimated fair value of the warrant liability since the most recent balance sheet date is recorded in the condensed consolidated statement of operations as other income (expense). The fair value of the warrants is estimated using an appropriate pricing model with the following inputs:

As of June 30, 2016 | |||||||||||||||||||||||

January 2016 Warrants | March 2015 Warrants | September 2013 Warrants | December 2012 Warrants | April 2011 Warrants | March 2010 Warrants | ||||||||||||||||||

Strike price | $ | 1.42 | $ | 2.08 | $ | 2.50 | $ | 1.75 | $ | 0.65 | $ | 1.92 | |||||||||||

Expected term (years) | 4.52 | 3.72 | 2.22 | 1.48 | 0.81 | 0.25 | |||||||||||||||||

Volatility % | 113.70 | % | 122.36 | % | 139.26 | % | 167.41 | % | 218.93 | % | 218.93 | % | |||||||||||

Risk-free rate % | 0.94 | % | 0.82 | % | 0.61 | % | 0.51 | % | 0.42 | % | 0.19 | % | |||||||||||

17

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

As of December 31, 2015 | |||||||||||||||||||||||

March 2015 Warrants | September 2013 Warrants | December 2012 Warrants | April 2011 Warrants | March 2011 Warrants* | March 2010 Warrants | ||||||||||||||||||

Strike price | $ | 2.08 | $ | 2.50 | $ | 1.83 | $ | 0.65 | $ | 0.65 | $ | 2.02 | |||||||||||

Expected term (years) | 4.22 | 2.72 | 1.98 | 1.31 | 0.18 | 1.00 | |||||||||||||||||

Volatility % | 75.85 | % | 74.70 | % | 76.37 | % | 65.60 | % | 47.98 | % | 71.41 | % | |||||||||||

Risk-free rate % | 1.58 | % | 1.24 | % | 1.05 | % | 0.77 | % | — | % | — | % | |||||||||||

*The March 2011 warrants expired in March 2016. The March 2010 warrants do not expire until September 2016.

The expected volatility assumptions are based on the Company's implied volatility in combination with the implied volatilities of similar publicly traded entities. The expected life assumption is based on the remaining contractual terms of the warrants. The risk-free rate is based on the zero coupon rates in effect at the time of valuation. The dividend yield used in the pricing model is zero, because the Company has no present intention to pay cash dividends.

The changes in fair value of the warrant liability for the six months ended June 30, 2016 were as follows (in thousands):

January 2016 Warrants | March 2015 Warrants | September 2013 Warrants | December 2012 Warrants | April 2011 Warrants | Other Equity Financing Warrants | Total | |||||||||||||||||||||

Warrant liability, January 1, 2016 | $ | — | $ | 10,337 | $ | 1,933 | $ | 1,565 | $ | 537 | $ | 146 | $ | 14,518 | |||||||||||||

Fair value of warrants issued | 5,590 | — | — | — | — | — | 5,590 | ||||||||||||||||||||

Fair value of warrants exercised | — | — | — | — | (278 | ) | (46 | ) | (324 | ) | |||||||||||||||||

Change in fair value of warrants | (1,515 | ) | (6,668 | ) | (1,148 | ) | (909 | ) | (184 | ) | (96 | ) | (10,520 | ) | |||||||||||||

Warrant liability, June 30, 2016 | $ | 4,075 | $ | 3,669 | $ | 785 | $ | 656 | $ | 75 | $ | 4 | $ | 9,264 | |||||||||||||

Warrants classified as equity

Equity-classified warrants consist of warrants issued in connection with consulting services provided to us and warrants issued in connection with debt financings. On May 10, 2016 upon closing on the sale of Debentures, we granted the holder warrants to purchase up to 1,000,000 shares of common stock at an exercise price of $1.51. The warrants were valued using an appropriate pricing model. The fair value assumptions for the grant included a volatility of 77.13%, expected term of five and five tenths years, risk-free rate of 1.26%, and a dividend rate of 0.00%. The fair value of the warrants granted was $0.87 per share. These warrants are recorded in equity at fair value upon issuance. Additionally, on June 29, 2016 upon closing on the public announcement of the interim analysis of the PRESENT trial, we granted the holder warrants to purchase up to 1,000,000 shares of common stock at an exercise price of $0.43.The warrants were valued using an appropriate pricing model. The fair value assumptions for the grant included a volatility of 106.63%, expected term of 5.5 years, risk-free rate of 1.35%, and a dividend rate of 0.00%. The fair value of the warrants granted was $0.27 per share. These warrants are recorded in equity at fair value upon issuance.

18

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

8. Stock-Based Compensation

Options to Purchase Shares of Common Stock — The Company follows the provisions ASC 718, which requires the measurement and recognition of compensation expense for all share-based payment awards made to employees, non-employee directors, including employee stock options. Stock compensation expense based on the grant date fair value estimated in accordance with the provisions of ASC 718 is recognized as an expense over the requisite service period.

For stock options and warrants granted in consideration for services rendered by non-employees, the Company recognizes compensation expense in accordance with the requirements of ASC Topic 505-50. Non-employee option and warrant grants that do not vest immediately upon grant are recorded as an expense over the vesting period. At the end of each financial reporting period prior to vesting, the value of these options and warrants, as calculated using the Black-Scholes option-pricing model, is re-measured using the fair value of the Company’s common stock and the non-cash compensation recognized during the period is adjusted accordingly. Since the fair market value of options and warrants granted to non-employees is subject to change in the future, the amount of the future compensation expense will include fair value re-measurements until the stock options and warrants are fully vested.

The following table summarizes the components of stock-based compensation expense in the condensed consolidated statements of comprehensive loss for the three and six months ended June 30, 2016 and 2015, respectively (in thousands):

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Research and development | $ | 108 | $ | 93 | $ | 235 | $ | 170 | |||||||

General and administrative | 514 | 296 | 1,043 | 590 | |||||||||||

Total stock-based compensation from continuing operations | $ | 622 | $ | 389 | $ | 1,278 | $ | 760 | |||||||

The Company uses the Black-Scholes option-pricing model and the following weighted-average assumptions to determine the fair value of all its stock options granted:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||

Risk free interest rate | 1.41 | % | 1.69 | % | 1.41 | % | 1.50 | % | |||

Volatility | 76.30 | % | 73.32 | % | 75.63 | % | 74.20 | % | |||

Expected lives (years) | 6.25 | 5.76 | 6.25 | 6.09 | |||||||

Expected dividend yield | — | % | — | % | — | % | — | % | |||

The weighted-average fair value of options granted during the three and six months ended June 30, 2016 were $1.36 per share and $0.86 per share, respectively.

19

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

The Company’s expected common stock price volatility assumption is based upon the Company's own implied volatility in combination with the implied volatility of a basket of comparable companies. The expected life assumptions for employee grants were based upon the simplified method provided for under ASC 718-10, which averages the contractual term of the Company’s options of ten years with the average vesting term of four years for an average of six years. The expected life assumptions for non-employees were based upon the contractual term of the option. The dividend yield assumption is zero, because the Company has never paid cash dividends and presently has no intention to do so. The risk-free interest rate used for each grant was also based upon prevailing short-term interest rates. The Company has estimated an annualized forfeiture rate of 15% for options granted to its employees, 8% for options granted to senior management and zero for non-employee directors. The Company will record additional expense if the actual forfeitures are lower than estimated and will record a recovery of prior expense if the actual forfeiture rates are higher than estimated.

As of June 30, 2016, there was $3,755,000 of unrecognized compensation cost related to outstanding options that is expected to be recognized as a component of the Company’s operating expenses over a weighted-average period of 2.79 years.

As of June 30, 2016, an aggregate of 26,500,000 shares of common stock were reserved for issuance under the Company’s 2007 Incentive Plan, including 10,309,000 shares subject to outstanding common stock options granted under the plan. On July 14, 2016, the shareholders approved the 2016 Incentive Plan into which the available shares in the 2007 Incentive Plan were transferred. There are 10,923,000 shares available for future grants based on adjustments in the 2016 Incentive Plan. The administrator of the plan determines the terms when an option may become exercisable. Vesting periods of options granted to date have not exceeded four years. The options will expire, unless previously exercised, no later than ten years from the grant date.

The following table summarizes option activity of the Company:

Total Number of Shares (In Thousands) | Weighted Average Exercise Price | Aggregate Intrinsic Value (In Thousands) | ||||||||

Outstanding at January 1, 2016 | 13,262 | $ | 2.58 | |||||||

Granted | 166 | 1.27 | ||||||||

Exercised | (167 | ) | 1.57 | $ | 56 | |||||

Canceled | (2,952 | ) | 3.07 | $ | — | |||||

Outstanding at June 30, 2016 | 10,309 | $ | 2.44 | $ | — | |||||

Options exercisable at June 30, 2016 | 5,970 | $ | 2.97 | $ | — | |||||

The aggregate intrinsic values of outstanding and exercisable options at June 30, 2016 were calculated based on the closing price of the Company’s common stock as reported on The NASDAQ Capital Market on June 30, 2016 of $0.47 per share. The aggregate intrinsic value equals the positive difference between the closing fair market value of the Company’s common stock and the exercise price of the underlying options.

20

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

9. Net Income (Loss) Per Share

Basic and diluted earnings per share are calculated as follows:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

Numerator: | |||||||||||||||

Net income (loss) (in thousands) | $ | 5,389 | $ | (15,660 | ) | $ | (11,104 | ) | $ | (26,197 | ) | ||||

Denominator: | |||||||||||||||

Weighted average number of common shares outstanding | 182,034,593 | 161,383,398 | 180,703,456 | 148,647,581 | |||||||||||

Effect of dilutive securities | |||||||||||||||

Stock options | 677,279 | — | — | — | |||||||||||

Warrants | 2,765,458 | — | — | — | |||||||||||

Dilutive potential common shares | 3,442,737 | — | — | — | |||||||||||

Shares used in calculating diluted earnings per share | 185,477,330 | 161,383,398 | 180,703,456 | 148,647,581 | |||||||||||

Basic net income (loss) per share | $ | 0.03 | $ | (0.10 | ) | $ | (0.06 | ) | $ | (0.18 | ) | ||||

Diluted net income (loss) per share | $ | 0.03 | $ | (0.10 | ) | $ | (0.06 | ) | $ | (0.18 | ) | ||||

The following table sets forth the potentially dilutive common shares excluded from the calculation of net income (loss) per common share because their inclusion would be anti-dilutive (in thousands):

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||

Warrants to purchase common stock | 21,517 | 22,308 | 37,418 | 22,308 | |||||||

Options to purchase common stock | 6,442 | 11,411 | 10,309 | 11,411 | |||||||

Total | 27,959 | 33,719 | 47,727 | 33,719 | |||||||

21

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

10. License Agreements

As part of its business, the Company enters into licensing agreements with third parties that often require milestone and royalty payments based on the progress of the licensed assets through development and commercial stages. Milestone payments may be required, for example, upon approval of the product for marketing by a regulatory agency, and the Company may be required to make royalty payments based upon a percentage of net sales of the product. The expenditures required under these arrangements in any period may be material and are likely to fluctuate from period to period.

These arrangements sometimes permit the Company to unilaterally terminate development of the product and thereby avoid future contingent payments; however, the Company is unlikely to cease development if the compound successfully achieves clinical testing objectives.

On January 12, 2014, we acquired worldwide rights to anagrelide controlled release (CR) formulation, which we renamed GALE-401, through our acquisition of Mills Pharmaceuticals, LLC ("Mills") and Mills became a wholly owned subsidiary. GALE-401 contains the active ingredient anagrelide, an FDA-approved product that has been in use since the late 1990s for the treatment of essential thrombocythemia (ET). Mills holds an exclusive license to develop and commercialize anagrelide CR formulation, pursuant to a license agreement with BioVascular, Inc. Under the terms of the license agreement, Mills has agreed to pay BioVascular, Inc. a mid-to-low single digit royalty on net revenue from the sale of licensed products as well as future cash milestone payments based on the achievement of specified regulatory milestones. Mills is also responsible for patent prosecution and maintenance. BioVascular has advised the Company of an alleged breach of the BioVascular agreement which the Company has denied. Both parties are discussing the dispute and it is anticipated that the dispute will be resolved.

On November 19, 2015, the Company and Sentynl Therapeutics Inc., a Delaware corporation (“Sentynl”), entered into and closed upon an Asset Purchase Agreement (the “Purchase Agreement”), pursuant to which the Company agreed to sell to Sentynl and Sentynl agreed to purchase from the Company, certain assets of the Company related to and including its Abstral® (fentanyl) sublingual tablets product (“Abstral”). The assets sold and assigned to Sentynl pursuant to the Purchase Agreement included all of the Company’s rights and interests in the Asset Purchase Agreement by and between the Company and Orexo AB (“Orexo”) dated March 15, 2013, and the License Agreement by and between the Company and Orexo dated March 18, 2013 (collectively, the “Orexo Agreements”). The Company’s future obligations under the Orexo Agreements were assumed by Sentynl pursuant to such assignment. In connection with such assignment, Orexo released the Company from any future obligations under the Orexo Agreements. The Purchase Agreement further provides that the Company will continue to be responsible for any pre-closing liabilities and obligations related to Abstral, as well for certain channel liabilities and rebates related to Abstral for a period of time post-closing.

The total potential consideration payable to the Company under the Purchase Agreement is $12 million, comprised of an $8 million upfront payment and up to an aggregate of $4 million, consisting of two one-time payments based on Sentynl's achievement of "net sales" of Abstral in amounts ranging from $25 million to $35 million.

On December 17, 2015, the Company and Midatech Pharma PLC, a public limited company organized under the laws of England and Wales (“Midatech”), entered into an Asset Purchase Agreement (the “Purchase Agreement”), pursuant to which the Company agreed to sell to Midatech and Midatech agreed to purchase from the Company, certain assets of the Company related to and including its Zuplenz® (ondansetron) Oral Soluble Film (“Zuplenz”). The assets to be sold and assigned to Midatech pursuant to the Purchase Agreement include all of the Company’s rights and interests in the License and Supply Agreement by and between the Company and MonoSol Rx, LLC (“MonoSol”) dated July 17, 2014 (the “MonoSol License”). The Company’s future obligations under the MonoSol agreement will be assumed by Midatech pursuant to such assignment. The Purchase Agreement further provides that the Company will continue to be responsible for any pre-closing liabilities and obligations related to Zuplenz, as well for certain rebates and channel liabilities related to Zuplenz for a period of time post-closing. The transaction was completed on December 24, 2015.

22

GALENA BIOPHARMA, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - Continued

(Unaudited)

The total potential consideration payable to the Company under the Purchase Agreement is $29.75 million, comprised of an $3.75 million upfront payment upon the closing and up to an aggregate of $26 million, consisting of four one-time payments based on Midatech's achievement of "net sales" of Zuplenz in amounts ranging from $12 million to $70 million.

Through a separate agreement with MonoSol entered into on December 16, 2015 (the “MonoSol License Amendment”), (i) the Company and MonoSol agreed to amend the MonoSol License in order to reduce the number of field representatives that the Company is required to maintain with respect to Zuplenz, and (ii) the Company paid MonoSol $900,000 of the upfront fee payable to the Company under the Purchase Agreement and 20% of any future milestone payments received by the Company under the Purchase Agreement.