Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Ready Capital Corp | v445096_8k.htm |

Investor Presentation July 2016 Exhibit 99.1

Disclaimer Forward - Looking Statements ▪ This presentation contains statements that constitute “forward - looking statements,” as such term is defined in Section 27A of th e Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and such statements are intended to be covered by the safe harbors provid ed by the same. These statements are based on current expectations and beliefs of management of Sutherland Asset Management Corporation (“SAM”) and ZAIS Financial Corp. (“ZFC”) an d a re subject to a number of trends and uncertainties that could cause actual results to differ materially from those described in the forward - looking statements; neith er SAM nor ZFC can give any assurance that expectations will be attained. ▪ Factors that could cause actual results to differ materially from expectations include, but are not limited to, the risk that th e merger will not be consummated within the expected time period or at all; the occurrence of any event, change or other circumstances that could give rise to the termination of the m erg er agreement; the inability to obtain stockholder approvals relating to the merger or the failure to satisfy the other conditions to completion of the merger; fluctuations in the adjust ed book value per share of the shares of both SAM and ZFC; risks related to disruption of management attention from the companies’ ongoing business operations due to the proposed merge r; the effect of the announcement of the proposed merger on SAM’s and ZFC’s operating results and businesses generally; the outcome of any legal proceedings relating to the me rge r; changes in future loan production; the ability to retain key managers of GMFS; availability of suitable investment opportunities; changes in interest rates; changes in the yie ld curve; changes in prepayment rates; the availability and terms of financing; general economic conditions; market conditions; conditions in the market for mortgage - related investments; l egislative and regulatory changes that could adversely affect the businesses of ZFC and SAM; and other factors, including those set forth in the Risk Factors section of ZFC’s most rec ent Annual Report on Form 10 - K and Quarterly Report on Form 10 - Q filed with the U.S. Securities and Exchange Commission (the “SEC”), and other reports filed by ZFC with the SEC, co pies of which are available on the SEC’s website, www.sec.gov. Neither SAM nor ZFC assumes any responsibility for information relating to the other, and neither ZFC nor SAM un der takes any obligation to update these statements for revisions or changes after the date of this presentation, except as required by law. Additional Information About the Merger ▪ In connection with the merger, ZFC filed a registration statement on Form S - 4 (File No. 333 - 211251) with the SEC that included a preliminary joint proxy statement/prospectus, and will file other relevant documents concerning the proposed merger. The registration statement has not yet been declared effec tiv e by the SEC and is subject to revisions, some of which may be significant. The registration statement and joint proxy statement/prospectus contain important information about the pro posed merger and related matters. BEFORE MAKING ANY VOTING OR INVESTMENT DECISION, INVESTORS ARE URGED TO READ THE DEFINITIVE JOINT PROXY STATEMENT/PROSPECTUS AND ANY OTHER DOCUMENTS TO BE FILED WITH THE SEC IN CONNECTION WITH THE MERGER OR INCORPORATED BY REFERENCE IN THE DEFINITIVE JOINT PROXY STATEMENT/PROSPECTUS BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT ZFC, SAM AND THE MERGER. ▪ Investors and stockholders of ZFC and SAM may obtain free copies of the registration statement and other relevant documents f ile d by ZFC with the SEC (as they become available) through the website maintained by the SEC at www.sec.gov. Copies of the documents filed by ZFC with the SEC are also availabl e f ree of charge on ZFC’s website at www.zaisfinancial.com . ZFC stockholders may also contact ZFC Investor Services for additional information by calling 212 - 827 - 3773 or emailing mmeek@ mww.com. ▪ This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall the re be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such ju ris diction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended. Participants in Solicitation Relating to the Merger ▪ ZFC, SAM and their respective directors and executive officers may be deemed to be participants in the solicitation of proxie s f rom ZFC’s and SAM’s stockholders in respect of the proposed merger. Information regarding ZFC’s directors and executive officers can be found in ZFC’s Annual Report on Form 10 - K f iled with the SEC on March 10, 2016, as amended by its Form 10 - K/A filed on April 29, 2016. Information regarding SAM’s directors and executive officers can be found in ZFC’s r egistration statement on Form S - 4 filed with the SEC. Additional information regarding the interests of such potential participants will be included in the joint proxy statem ent /prospectus and other relevant documents filed with the SEC in connection with the merger if and when they become available. These documents are available free of charge on the SEC' s w ebsite and from ZFC or SAM, as applicable, using the sources indicated above. 2

▪ ZFC will become a diversified commercial mortgage REIT with a unique focus on small balance commercial (“SBC”) conventional and owner occupied loans including Small Business Administration (“SBA”) ▪ The combined company will operate four primary segments: 1) SAM: acquires and manages distressed SBC loans (1) 2) ReadyCap Commercial: wholly - owned subsidiary of SAM, which originates SBC loans ▪ Originated $421.7 million of SBC loans in 2015 and $235.1 million YTD 2016 3) ReadyCap Lending: wholly - owned subsidiary of SAM, which originates and services SBA loans ▪ Granted Preferred Lender Status by the SBA in Q4 2015; originated $24.0 million since inception ▪ Serviced $1.2 billion as of March 31, 2016 ▪ Holds 1 of only 14 non - bank SBA licenses issued in the U.S. (acquired platform and portfolio from CIT in 2014) 4) GMFS: wholly - owned subsidiary of ZFC which originates, sells and services residential mortgage loans ▪ Originated $1.8 billion in 2015 and $432.1 million YTD March 2016 (excluding reverse mortgages); serviced an MSR portfolio of $4.4 billion in UPB as of March 31, 2016 Combined Business Overview Executive Summary 3 Transaction Highlights x Creates a REIT with an expanded capital base of over $560 million in stockholder’s equity to be deployed into attractive small balance commercial real estate assets, which include newly originated and distressed legacy mortgages x Ability to generate compelling risk - adjusted returns with a focus on the underserved and fragmented small balance commercial mortgage market x Uniquely positioned to source high yielding assets from acquisitions and self - originated products driving growth x Creates a highly scalable, fully integrated REIT platform generating small balance commercial assets through multiple origina tio n channels (1) Since 2008 and through March 31, 2016, Waterfall has acquired more than 9,000 SBC and SBA loans with aggregate UPB of approximately $3.5 billion for an aggregate purchase price of approximately $2.6 billion.

Executive Summary (cont’d) 4 ▪ In October 2015, ZAIS Financial Corp (“ZFC”) launched a strategic review and conducted a full process, with the assistance of Ho ulihan Lokey ▪ The process resulted in ZFC and Sutherland Asset Management (“SAM”) entering a definitive merger agreement on April 6, 2016, subsequently amended on May 9, 2016 (the “Merger”) ▪ ZFC contacted 63 potential strategic and financial buyers as part of its strategic review ▪ ZFC determined that liquidation was challenging and did not maximize stockholder value ▪ ZFC received 3 proposals, 2 of which did not ascribe any immediate value to GMFS ▪ Only SAM submitted an offer for the entire company ▪ In June 2016, a ZFC Investor owning 4.8% of the common shares outstanding filed a Schedule13D (1) opposing the merger ▪ The key point put forth by the ZFC Investor is that liquidation of 100% of the assets of ZFC at near book value will yield sh are holders more cash than a merger (1) As of 6/15/16 per Schedule 13D filing.

Executive Summary (cont’d) 5 ▪ Certain ZFC assets can be liquidated with cash proceeds distributed to shareholders (via a dividend); liquidation of other as set s is more challenging ▪ As of March 31, 2016, ~40% of ZFC equity value is in its Residential Mortgage Banking Segment, operating through GMFS, which the ZFC Investor claims can be sold (in a liquidation scenario) or that proceeds could be distributed to shareholders by leveraging m ort gage - servicing rights (“MSRs”) (in a liquidating trust scenario) ▪ The assumption that $16 in cash per share can be achieved through liquidation is incorrect as the contingent claim on GMFS (subject to “tolling agreement” recently extended to 12/31/16 ) severely restricts the ability to sell the mortgage banking operations or distribute cash via asset sale or increased leverage ▪ With potential litigation, creditors’ rights represent a legal obstacle to both asset sales and distributions of sale proceed s ▪ Other restrictions exist that prohibit GMFS from up - streaming cash, including minimum net worth covenants included in warehouse financing arrangements and limitations on changes in net worth with respect to Fannie/Freddie/Ginnie seller - servicer licenses ▪ Due to the overhang of the potential claims at GMFS, the mortgage company is not reasonably saleable at the current time, and ZF C lacks the ability to distribute cash to stockholders from liquidating certain mortgage banking assets ▪ Liquidating the ZFC non - GMFS assets and liabilities are estimated to produce $9.19 per share, implying that the combined company must trade at 21% of book value to be economically indifferent to the liquidation value – implies a 43% dividend yield (1) (1) Based on average cash and stock consideration to ZFC stockholders and a dividend based on SAM LTM ROAE of 9% and 100% payout ratio. We believe the Merger is a compelling transaction and represents the best overall outcome for ZFC stockholders

11.8% 11.3% 10.4% 9.1% 8.9% 8.6% 8.4% 8.1% ZFC ARI SAM CLNY STWD BXMT LADR ACRE 1.03x 0.89x 0.60x 0.80x 1.00x 1.20x Jul - 13 Mar - 14 Oct - 14 May - 15 Dec - 15 Jul - 16 Commercial Residential Commercial 3 - Year Average: 1.07x Residential 3 - Year Average: 0.86x Investor Concern #1 6 The analysis of the newly merged entity is based upon overly optimistic and unrealistic assumptions . The new entity will trade substantially below ZFC’s assumptions and likely below the current ZFC share price . Investor Concern # 1 : Response : Historical Price to Book Value Per Share Source: SNL Financial and Fact Set, Market data as of 7/28/16. Note: Commercial includes STWD, CLNY, ARI, BXMT, ACRE, and LADR. Residential includes: NLY, AGNC, ARR, CYS, CMO, ANH, ORC, TWO, CIM, MFA, IVR, MTGE, NYMT, EFC, WMC, MITT, AI, DX, OAKS, EARN, and ZFC. (1) Represents the ROAE for the last twelve months ended 3/31/16. (2) SAM dividend yield calculated as Q1’16 annualized declared dividend to common stockholders divided by Q1’16 book value per s har e. Most Recent Quarter Dividend Yield (2) Return on Average Equity (Last Twelve Months (1) ) 11.1% 10.8% 9.0% 9.0% 8.6% 8.1% 8.0% 7.8% (2.9%) Pro Forma ▪ The combined company’s balance sheet will consist of mainly senior commercial mortgage loans, similar to how SAM balance sheet is structured today ▪ On average, the commercial mortgage REIT peer group trades at 1 . 03 x P/BV ▪ On a pro forma basis, the combined company has the second highest LTM ROAE amongst commercial mortgage REITs and SAM’s current dividend yield ranks second highest among its commercial mortgage REIT peer set ▪ Recent trades of SAM stock reflect trades on a 144 a exchange maintained by one dealer and, as such, are highly illiquid and should not be considered as an accurate indication of how the combined company will trade post - transaction (i . e . , on the NYSE) ▪ In the last 3 months only 1 % of SAM’s outstanding shares have traded

Investor Concern #2 7 Zais management has not adequately considered other strategic alternatives which would result in greater value and more certainty for shareholders . We calculate $ 16 of distributable cash is available at present to ZFC shareholders . Investor Concern # 2 : Response : ▪ In October 2015, ZFC conducted a strategic review, contacting 63 strategic and financial buyers, with the assistance of Houli han Lokey ▪ In November 2015, ZFC received 14 proposals for various transactions involving all or a part of the company ▪ After a review of all of the bids received, ZFC decided to invite 3 parties to the second round to complete further due dilig enc e ▪ In January 2016, ZFC received proposals from the 3 parties that were invited to the second round ▪ Party A submitted a proposal for a purchase price of $90 million to acquire ZFC exclusive of GMFS ▪ Party B submitted a proposal to acquire ZFC’s conduit loans, RMBS portfolio, re - performing loan portfolio and GMFS, but proposed a $65 million holdback in the form of an escrow until final resolution of potential indemnification claims arising o ut of sales of mortgage loans by GMFS from 1999 to 2006 (“potential claims”) ▪ SAM submitted an indication of interest which proposed that ZFC acquire SAM in a stock for stock merger, with an exchange ratio being computed based on the companies’ respective book value ▪ ZFC, and its board, concluded that a merger would maximize shareholder value due to some of the limitations with a liquidatio n ▪ With potential litigation, creditors’ rights represent a legal obstacle to both asset sales and distributions of sale proceed s ▪ Other restrictions exist that prohibit GMFS from up - streaming cash, including minimum net worth covenants included in warehouse financing arrangements and limitations on changes in net worth with respect to Fannie/Freddie/ Ginnie seller - servicer licenses We calculate only ~$9 of cash per share would be distributable in the short - term in a liquidation scenario – potential value to be realized from GMFS would be discounted and subject to distribution restrictions

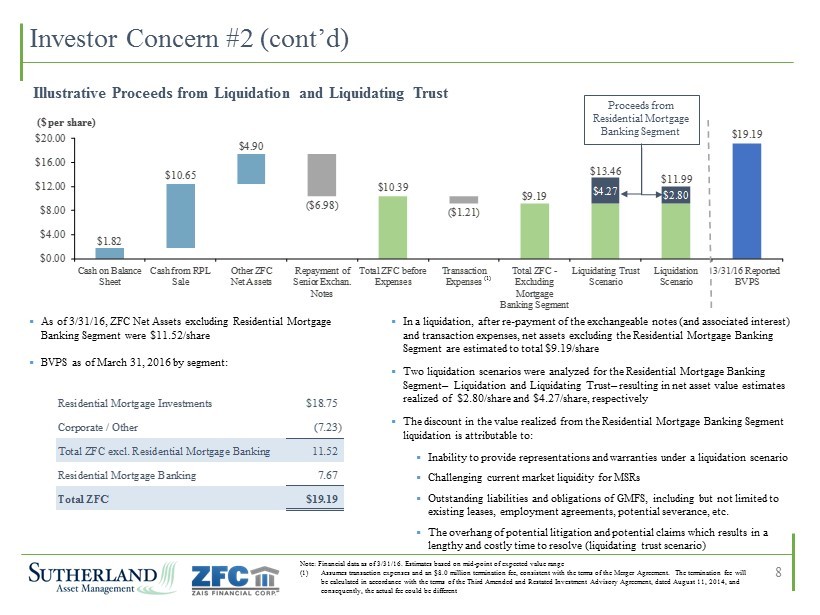

$1.82 $10.39 $9.19 $19.19 $10.65 $4.90 ($6.98) ($1.21) $4.27 $2.80 $0.00 $4.00 $8.00 $12.00 $16.00 $20.00 Cash on Balance Sheet Cash from RPL Sale Other ZFC Net Assets Repayment of Senior Exchan. Notes Total ZFC before Expenses Transaction Expenses Total ZFC - Excluding Mortgage Banking Segment Liquidating Trust Scenario Liquidation Scenario 3/31/16 Reported BVPS ($ per share) $13.46 $11.99 Investor Concern #2 (cont’d) 8 ▪ As of 3/31/16, ZFC Net Assets excluding Residential Mortgage Banking Segment were $11.52/share ▪ BVPS as of March 31, 2016 by segment: Illustrative Proceeds from Liquidation and Liquidating Trust Note: Financial data as of 3/31/16. Estimates based on mid - point of expected value range (1) Assumes transaction expenses and an $8.0 million termination fee, consistent with the terms of the Merger Agreement. The te rmination fee will be calculated in accordance with the terms of the Third Amended and Restated Investment Advisory Agreement, dated August 11, 201 4, and consequently, the actual fee could be different Proceeds from Residential Mortgage Banking Segment ▪ In a liquidation, after re - payment of the exchangeable notes (and associated interest) and transaction expenses, net assets excluding the Residential Mortgage Banking Segment are estimated to total $9.19/share ▪ Two liquidation scenarios were analyzed for the Residential Mortgage Banking Segment – Liquidation and Liquidating Trust – resulting in net asset value estimates realized of $2.80/share and $4.27/share, respectively ▪ The discount in the value realized from the Residential Mortgage Banking Segment liquidation is attributable to: ▪ Inability to provide representations and warranties under a liquidation scenario ▪ Challenging current market liquidity for MSRs ▪ Outstanding liabilities and obligations of GMFS, including but not limited to existing leases, employment agreements, potential severance, etc. ▪ The overhang of potential litigation and potential claims which results in a lengthy and costly time to resolve (liquidating trust scenario) (1) Residential Mortgage Investments $18.75 Corporate / Other (7.23) Total ZFC excl. Residential Mortgage Banking 11.52 Residential Mortgage Banking 7.67 Total ZFC $19.19

Investor Concern #2 (cont’d) 9 Note: All figures in thousands except for per share amounts. (1) Based on pro forma 3/31/16 financials. Value Per Share figures represent the average consideration received per share. (2) Represents the book value received by ZFC stockholders. (3) Based on pro forma combined company BVPS of $17.05 and assumes a dividend based on SAM LTM ROAE of 9% and 100% payout ratio. Commentary Consideration Received by ZFC Stockholders (1) Consideration per Share Received by ZFC Stockholders at Various Pro Forma Company Trading Levels (1) Pro Forma Company Price to BVPS Multiple: 0.50x 0.60x 0.70x 0.80x 0.90x 1.00x Cash Consideration Per Share $7.23 $7.23 $7.23 $7.23 $7.23 $7.23 Stock Consideration Per Share 4.66 5.59 6.53 7.46 8.39 9.32 Total Consideration Per Share $11.89 $12.82 $13.76 $14.69 $15.62 $16.55 Implied Dividend Yield (3) 18.0% 15.0% 12.9% 11.3% 10.0% 9.0% ZFC Close Price (7/28/16): $13.59 Liquidation Analysis: $11.99 Liquidating Trust Analysis: $13.46 ▪ The liquidation and liquidating trust analyses are estimated to generate $11.99 of cash per share and $13.46 of cash per share, respectively ▪ While estimated to generate $11.99 per share in a liquidation (including $2.80 per share from GMFS), it remains highly unlikely that ZFC could distribute proceeds from the Residential Mortgage Banking Segment due to the potential claims at GMFS ▪ The liquidating trust analysis assumes that the potential claim is resolved at a future date, but the length of time and the cost incurred is highly uncertain ▪ The combined company would have to trade at 0.51x P/BV for ZFC stockholders to be indifferent between the liquidation scenario and executing the Merger and at 0.67x P/BV to be indifferent to the liquidating trust scenario Cash Stock Portion (1) Portion (2) Total Value Received $64,331 $82,963 $147,294 Shares 8,898 8,898 8,898 Value Per Share $7.23 $9.32 $16.55 % of Consideration 43.7% 56.3% 100.0%

Investor Concern #2 (cont’d) 10 ▪ Time needed to liquidate the trust and resolve potential claims is highly uncertain ▪ Based on similar sub - prime RMBS litigation cases, legal resolution may be a multi - year process ▪ Spinning GMFS off as a standalone public company may impair its value ▪ Under liquidation, counterparties may choose to limit/adjust/withdraw credit facilities provided to GMFS, limiting the compan y’s ability to originate loans ▪ Earnings may be impacted by substantial incremental costs associated with operating as a standalone company ▪ Key staff retention may be difficult in context of uncertainty surrounding disposition of contingent claim as a standalone en tit y (and third ownership change in 3 - years) ▪ In particular, loan production staff would be at risk ▪ GMFS could face difficulties as a microcap publicly - traded company with limited public float ▪ Valuations of publicly - traded mortgage companies remains depressed; uncertainty under what price and terms GMFS could be sold Challenges Associated with a Liquidating Trust In addition to the challenges outlined in a liquidation scenario, even further challenges would be presented if ZFC pursued a strategy of liquidating ZFC assets and liabilities and putting GMFS into a liquidating trust until the resolution of certain lia bilities

Investor Concern #3 11 Zais Board and management are conflicted in recommending the merger as the management company stands to benefit at shareholder’s expense . ▪ There is no conflict of interest as a termination fee is payable to ZFC’s manager in the event of a liquidation or the propos ed transaction ▪ The negotiated termination fee of $8.0 million as part of the transaction is less than the contractual amount due under the management agreement of $8.6 million (1) ▪ The merger decision was made by ZFC’s Board of Directors, comprised of a majority of independent directors ▪ The termination fee will be shared by the shareholders of the combined company ▪ ZFC’s pro rata split will be approximately 24% (based on pre - tender pro rata ownership) ▪ Legacy ZFC shareholders effectively pay $1.9 million of the $8.0 million ▪ A termination fee would be due following the decision to liquidate; therefore, liquidating ZFC assets and putting GMFS into a liquidating trust would not result in a lower termination fee Investor Concern # 3 : Response : (1) The termination fee will be calculated in accordance with the terms of the Third Amended and Restated Investment Advisory Ag reement, dated August 11, 2014, and consequently, the actual fee could be different

▪ The ZFC vote process has been constructed in strict compliance with Maryland law and the Company’s Articles of Incorporation ▪ The merger transaction is subject to a vote by ZFC stockholders on whether they authorize the issuance of shares – they have the right to vote as they choose ▪ ZFC will be holding a Stockholders Meeting whereby its stockholders may vote pursuant to Sections 2 - 504, 2 - 506 and 2 - 507 of the Corporations and Associations Code of Maryland and NYSE requirements ▪ Transitioning assets from residential to commercial mortgages should create shareholder value as commercial mortgage REITs trade higher on a price - to - book - value basis ▪ A larger, more scaled REIT should have better access to capital/funding and can participate in larger deals which all benefit shareholders ▪ From a total return perspective, SAM has performed in line with commercial mortgage and outperformed residential mortgage REITs Investor Concern #4 12 ZFC is effectively being merged into a REIT three times its size with the surviving entity, Sutherland, having a completely different investment strategy and new investment manager . If put to a vote, we question whether this transaction would be approved by ZFC’s shareholders Investor Concern # 4 : Response :

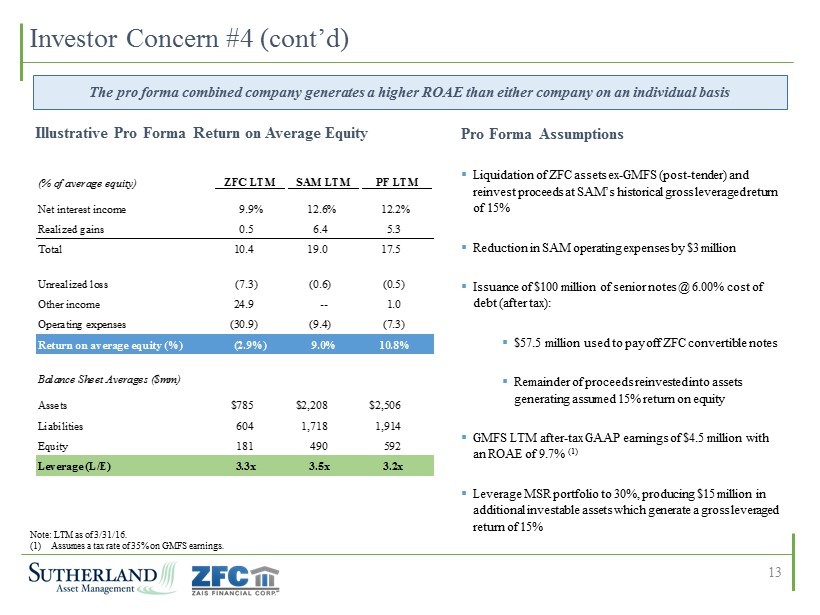

Note: LTM as of 3/31/16. (1) Assumes a tax rate of 35% on GMFS earnings. Investor Concern #4 (cont’d) 13 Pro Forma Assumptions ▪ Liquidation of ZFC assets ex - GMFS (post - tender) and reinvest proceeds at SAM’s historical gross leveraged return of 15% ▪ Reduction in SAM operating expenses by $3 million ▪ Issuance of $100 million of senior notes @ 6.00% cost of debt (after tax): ▪ $57.5 million used to pay off ZFC convertible notes ▪ Remainder of proceeds reinvested into assets generating assumed 15% return on equity ▪ GMFS LTM after - tax GAAP earnings of $4.5 million with an ROAE of 9.7% (1) ▪ Leverage MSR portfolio to 30%, producing $15 million in additional investable assets which generate a gross leveraged return of 15% Illustrative Pro Forma Return on Average Equity The pro forma combined company generates a higher ROAE than either company on an individual basis (% of average equity) ZFC LTM SAM LTM PF LTM Net interest income 9.9% 12.6% 12.2% Realized gains 0.5 6.4 5.3 Total 10.4 19.0 17.5 Unrealized loss (7.3) (0.6) (0.5) Other income 24.9 -- 1.0 Operating expenses (30.9) (9.4) (7.3) Return on average equity (%) (2.9%) 9.0% 10.8% Balance Sheet Averages ($mm) Assets $785 $2,208 $2,506 Liabilities 604 1,718 1,914 Equity 181 490 592 Leverage (L/E) 3.3x 3.5x 3.2x

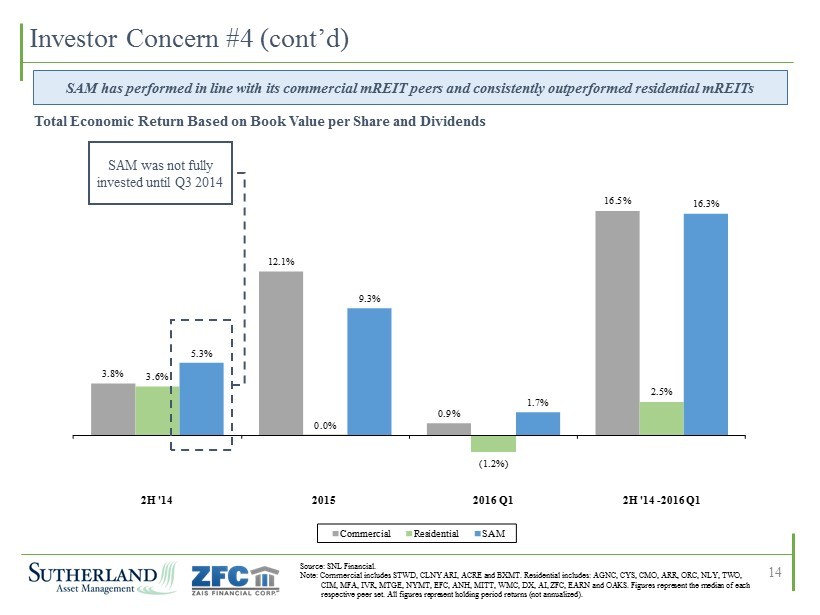

Source: SNL Financial. Note: Commercial includes STWD, CLNY ARI, ACRE and BXMT. Residential includes: AGNC, CYS, CMO, ARR, ORC, NLY, TWO, CIM, MFA, IVR, MTGE, NYMT, EFC, ANH, MITT, WMC, DX, AI, ZFC, EARN and OAKS. Figures represent the median of each respective peer set. All figures represent holding period returns (not annualized). 14 3.8% 12.1% 0.9% 16.5% 3.6% 0.0% (1.2%) 2.5% 5.3% 9.3% 1.7% 16.3% 2H '14 2015 2016 Q1 2H '14 - 2016 Q1 Commercial Residential SAM Investor Concern #4 (cont’d) SAM was not fully invested until Q3 2014 Total Economic Return Based on Book Value per Share and Dividends SAM has performed in line with its commercial mREIT peers and consistently outperformed residential mREITs

Investor Concern #5 15 The mortgage litigation risk Sutherland is inheriting from GMFS will likely cause Sutherland to trade at a greater discount to book value . Investor Concern # 5 : Response : ▪ On a pro - forma basis, GMFS will represent only 10% of combined company equity so will have a limited impact on overall valuation ▪ Indemnifications put in place during the sale of GMFS to ZFC from its former owners, including a private fund managed by Waterfall Asset Management (“Waterfall”), will transfer to SAM ▪ The existing reserves and escrow amounts related to any potential ligation claim will remain in place after the acquisition ▪ As a result of this merger, SAM will be a public company with a separate board who will undertake whatever legal actions appropriate to protect shareholder value; SAM is separate and distinct from the private fund managed by Waterfall, the prior owners of GMFS ▪ As compared to liquidation, the acquisition by SAM will preserve GMFS value due to the following: ▪ With increased scale, if any GMFS litigation were to arise, the combined company would be able to better manage this issue with a larger capital base ▪ Being part of a larger organization with over $500M capital mitigates the potential loss of warehouse financing (critical to operations) and/or counterparty credit with the mortgage regulatory agencies associated with the potential litigation ▪ SAM intends to maintain GMFS as a core business (cross - selling its commercial loan products) thereby avoiding the substantial potential discount on sale of GMFS associated with liquidation

Investor Concern #6 16 The new manager is proposing to significantly increase management fees by adding an incentive fee whereby management will receive 15 % of the annual return in excess of 8 % . The increase in management fees will likely cause Sutherland to trade at a larger discount, further eroding shareholder value . Investor Concern # 6 : Response : Base Management Fee Mgmt. Fee Basis Incentive Fee Incentive Fee Hurdle Incentive Fee Payment Structure Termination Fee 1.5% on SE ≤ $500 million (2) plus 1.0% on SE > $500 million Stockholders’ equity 15.0% 8.0% (1) 50% stock / 50% cash 3x the average annual base management fee and incentive fee received during the 24 months prior 1.5% Stockholders’ equity 20.0% 8.0% 50% stock / 50% cash 3x the average annual base management fee and incentive fee received during the 24 months prior 1.5% Stockholders’ equity NA NA NA 3x the average annual base management fee during the 24 months prior 1.5% Stockholders’ equity 20.0% 8.0% 100% cash 3x the average annual base management fee and incentive fee received during the 24 - months prior 1.5% Market capitalization 20.0% 7.0% 100% cash 3x the average annual base management fee and incentive fee received during the 24 months prior 1.5% Stockholders’ equity NA NA NA 3x the average annual base management fee during the 24 months prior Source: Company SEC filings. Note: Waterfall will enter into a new 3 - year management agreement. Incentive distributions, if any, will be based on the trailin g 4 - quarter core earnings. Until there is sufficient history, the prior quarters will be annualized. Management believes this increases transparency versus using core ear nings prior to the merger of ZFC and SAM. (1) Incentive distribution equal to 15% of the difference between the trailing 4 - quarter core earnings and the product of the 8% hur dle rate and outstanding shares multiplied by the weighted average issue price of $17.45 per share assuming an exchange ratio of 0.8455. (2) Management fee equal to 1.5% per annum of Stockholders' Equity up to $500 million and 1.00% per annum of Stockholders' Equity in excess of $500 million ▪ The management fee is consistent with other commercial mortgage REITs and should not cause the combined company to trade differently from its peers ▪ Unlike residential mortgage REITs (which conduct primarily leveraged investment in MBS) incentive fees are common for commercial mortgage REITs (which are operating entities engaged in commercial lending) ▪ SAM’s management terms are in line or more favorable to stockholders vs . other commercial mortgage REITs ▪ The incentive fee is paid partially in stock which aligns the interests of the manager with shareholders ▪ Further, the incentive fee is calculated off capital at the price at which it was raised (i . e . , $ 17 . 45 per share, after giving effect to the exchange ratio), rather than book value ( 1 ) ▪ The combined company Base Management Fee is lower than that currently paid by ZFC

Investor Concern #7 17 ZFC expects shareholders to incur over $ 6 million in costs to complete the merger, greater than 5 % of the ZFC market capitalization . Investor Concern # 7 : ▪ As of March 31, 2016, ZFC has already incurred $2.8 million in Merger related costs with remaining transaction fees expected to be $3.5 million – comparable expenses are expected under a liquidation or liquidating trust scenario ▪ The majority of the professional services expenses associated with the merger will also be incurred in a liquidation scenario ; i n liquidation, expenses may increase if the timetable to completion extends ▪ There is a fee to terminate ZFC’s existing manager payable under a Merger or liquidation ▪ In a liquidation, the termination fee of $8.6 million due to ZFC’s existing manager would be borne solely by ZFC stockholders (1) ▪ In the Merger scenario, this fee is shared pro forma among ZFC ($1.9 million) and SAM ($6.1 million) shareholders, making the Merger more attractive Response : (1) The termination fee will be calculated in accordance with the terms of the Third Amended and Restated Investment Advisory Agr eem ent, dated August 11, 2014, and consequently, the actual fee could be different.

Appendix

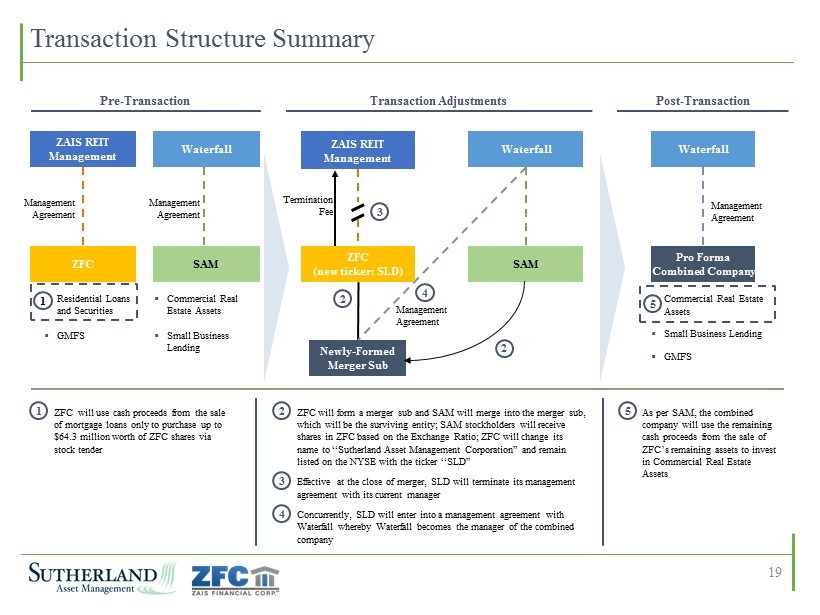

▪ As per SAM, the combined company will use the remaining cash proceeds from the sale of ZFC’s remaining assets to invest in Commercial Real Estate Assets Transaction Structure Summary Waterfall SAM Pro Forma Combined Company ZAIS REIT Management ZFC Management Agreement Pre - Transaction Post - Transaction Transaction Adjustments Management Agreement ▪ ZFC will use cash proceeds from the sale of mortgage loans only to purchase up to $64.3 million worth of ZFC shares via stock tender ▪ Residential Loans and Securities ▪ GMFS 2 1 ▪ Commercial Real Estate Assets ▪ Small Business Lending Waterfall SAM ZAIS REIT Management Management Agreement Newly - Formed Merger Sub 2 3 4 ▪ ZFC will form a merger sub and SAM will merge into the merger sub, which will be the surviving entity; SAM stock holders will receive shares in ZFC based on the Exchange Ratio; ZFC will change its name to “Sutherland Asset Management Corporation” and remain listed on the NYSE with the ticker “SLD” ▪ Effective at the close of merger, SLD will terminate its management agreement with its current manager ▪ Concurrently, SLD will enter into a management agreement with Waterfall whereby Waterfall becomes the manager of the combined company Waterfall Management Agreement ▪ Commercial Real Estate Assets ▪ Small Business Lending ▪ GMFS 1 5 5 ZFC (new ticker: SLD) Termination Fee 2 3 4 19

Calculation of Exchange Ratio and Tender Offer Price Source: ZFC S - 4 dated 7/18/16. (1) Per merger agreement. 20 ZFC (as of 3/31/16) ZFC Book Value $170,842,741 Less: Transaction costs (3,500,000) Less: Book Value Adjustment (15,000,000) ZFC Adjusted Book Value $152,342,741 Shares Outstanding 8,897,800 A ZFC Adjusted Book Value per Share $17.12 B SAM (as of 3/31/16) SAM Book Value (before preferred stock redemption) $489,808,000 Less: Transaction Costs (4,000,000) Less: Preferred Stock (125,000) SAM Adjusted Book Value $485,683,000 Shares Outstanding 33,550,940 C SAM Adjusted Book Value per Share $14.48 D Exchange Ratio 0.8455x E = D / B # shares issued based on pro-forma exchange ratio C x E 28,367,319 F Total shares A + F 37,265,119 G Pro-rata ownership - ZFC (pre-tender) A / G 23.9% H Pro-rata ownership - SAM (pre-tender) 100% - H 76.1% Pro-rata adjustments to TO price H x (-$8.0mm - $3.9mm) ($2,833,725) I Pro-rata adjustments to TO price per share I / A ($0.32) J Tender Offer price before applying 95% factor B + J $16.80 K Tender Offer price K x 95% $15.96 (1)

Name Background Thomas E. Capasse Jack J. Ross Frederick C. Herbst, CPA Thomas Buttacavoli Management Team of the Combined Company ▪ CEO and Chairman of SAM ▪ Manager and Co - Founder of Waterfall Asset Management ▪ 34 years of structured credit experience globally ▪ Co - founded Merrill Lynch’s ABS group in the 1980’s ▪ President and Director of SAM ▪ Manager and Co - Founder of Waterfall Asset Management ▪ 31 years of ABS and structured credit experience ▪ Co - founded Merrill Lynch’s ABS group in the 1980’s ▪ CFO of SAM ▪ Managing Director of Waterfall Asset Management ▪ Previously served as CFO of Arbor Realty Trust (NYSE: ABR) and Clayton Holdings (NASD: CLAY) ▪ Chief Investment Officer of SAM ▪ Manager and Managing Director of Waterfall Asset Management ▪ Previously served as a structured finance analyst at Licent Capital, strategic planning analyst at BNY Capital Markets and Financial Analyst at Merrill Lynch 21 Chief Executive Officer Chairman President Chief Financial Officer Chief Investment Officer Source: ZFC S - 4 dated 7/18/16.

Board of Directors of the Combined Company Name Background Thomas E. Capasse Jack J. Ross Frank P. Filipps Todd M. Sinai J. Mitchell Reese David L. Holman ▪ Manager and Co - Founder of Waterfall Asset Management ▪ 34 years of structured credit experience globally ▪ Co - founded Merrill Lynch’s ABS group in the 1980’s ▪ Manager and Co - Founder of Waterfall Asset Management ▪ 31 years of ABS and structured credit experience ▪ Co - founded Merrill Lynch’s ABS group in the 1980’s ▪ Served as Chairman and CEO of Clayton Holdings. And Radian Group ▪ Director of Impac Mortgage Holdings since 1995, and Director of Orchid Island Capital since 2013 ▪ Professor of Real Estate and Business Economics and Public Policy at Wharton ▪ Holds a Ph.D. in Economics from MIT, and B.A. in Economics and Math from Yale ▪ Currently serves as a Managing Member of Cintra Capital ▪ Previously served as a Managing Director of The Carlyle Group, where he headed the firm’s U.S. venture capital fund ▪ Previously served as a Partner, and the Americas Director of Accounting Standards at Ernst & Young ▪ Director of ZFC, Chair of ZFC Audit Committee 22 Chief Executive Officer Chairman President Director (SAM Designee) Director (SAM Designee) Director (SAM Designee) Director (ZAIS Financial Designee) Source: ZFC S - 4 dated 7/18/16.

SAM Company Overview

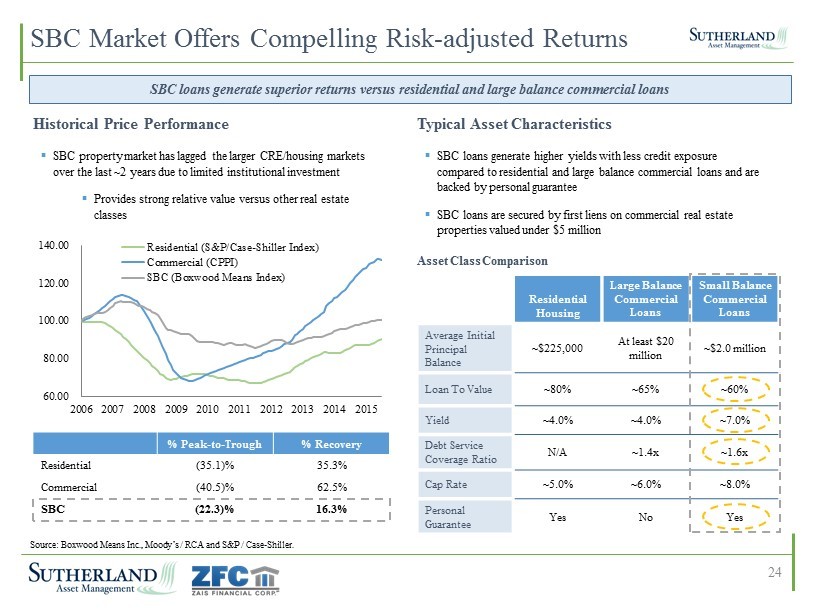

Residential Housing Large Balance Commercial Loans Small Balance Commercial Loans Average Initial Principal Balance ~$225,000 At least $20 million ~$2.0 million Loan To Value ~80% ~65% ~60% Yield ~4.0% ~4.0% ~7.0% Debt Service Coverage Ratio N/A ~1.4x ~1.6x Cap Rate ~5.0% ~6.0% ~8.0% Personal Guarantee Yes No Yes 60.00 80.00 100.00 120.00 140.00 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Residential (S&P/Case-Shiller Index) Commercial (CPPI) SBC (Boxwood Means Index) % Peak - to - Trough % Recovery Residential (35.1)% 35.3% Commercial (40.5)% 62.5% SBC (22.3)% 16.3% SBC Market Offers Compelling Risk - adjusted Returns ▪ SBC property market has lagged the larger CRE/housing markets over the last ~2 years due to limited institutional investment ▪ Provides strong relative value versus other real estate classes Historical Price Performance Asset Class Comparison Source: Boxwood Means Inc., Moody’s / RCA and S&P / Case - Shiller. SBC loans generate superior returns versus residential and large balance commercial loans Typical Asset Characteristics ▪ SBC loans generate higher yields with less credit exposure compared to residential and large balance commercial loans and are backed by personal guarantee ▪ SBC loans are secured by first liens on commercial real estate properties valued under $5 million 24

25 Small Balance Commercial Property Overview Investor owned retail strip mall – 10 unit property, Snellville, GA Owner - occupied franchise – 2,400 sqft, Daytona, FL Investor owned multifamily - 10 unit property, Los Angeles, CA Owner - occupied medical office – 3,100 sqft, Arlington, TX

SAM Business Overview 26 Loan Acquisition Business Origination Business(es) Conventional Loans Bridge Loans Freddie Mac SBL Program SBA 7(a) Booking Entity: Sutherland ReadyCap Commercial ReadyCap Lending Principal Business Activity / Secured by: Acquires pools of performing, sub - performing, and non - performing SBC loans from banks, other lenders, the FDIC, special servicers and others First mortgages on investor - owned commercial, multi - family or mixed - use properties. Multifamily properties with five units or more First mortgages on owner - occupied commercial properties that are 75% guaranteed by the SBA Typical Size: $500K - $10M $750K - $10M $1M to $15M $1M to $5M Up to $5M Rate: Fixed / floating Fixed / floating Fixed / floating Fixed / floating Typically floating Original Term: 5 - 30 years (18 - 36 months hold) 5 - 10 years 24 - 36 months 5 - 20 years 25 years Amortization: Fully amortizing 15 - 30 years Interest only Up to 30 years Fully amortizing Personal Guarantee: Typically Personal and / or carve - out guarantee Personal and / or carve - out guarantee No Yes Loan Assets (1) $1.2B $245.3M $707.8M Stockholders’ Equity (1) $335.2M $77.4M $76.7M Funding Strategy Credit Facilities and Securitizations Credit Facilities and Securitizations Guaranteed portion (75%) sold to unaffiliated parties, non - guaranteed portion retained (1) As of 3/31/2016.

27 SAM Economics by Business Line Acquired Portfolio Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015 Unlevered yield 8.5% 9.9% 8.9% 9.7% 9.1% Cost of funds 4.4 % 4.1 % 4.1 % 4.0 % 4.5 % Net interest spread 4.1 % 5.8 % 4.8 % 3.7 % 4.6 % Leverage ratio 3.3x 2.6x 2.8x 2.2x 2.0x Levered yield 22.2% 25.0% 22.3% 22.5% 18.2% SBC Conventional and Investor Originations Unlevered yield 7.4% 6.3% 5.8% 5.8% 5.5% Cost of funds 4.3 % 3.6 % 3.1 % 3.3 % 3.1 % Net interest spread 3.1 % 2.7 % 2.7 % 2.5 % 2.4 % Leverage ratio 2.4x 2.7x 2.4x 2.7x 2.2x Levered yield 15.0% 13.5% 12.3% 12.5% 10.8% SBA Originations, Acquisitions and Servicing Unlevered yield 6.7% 5.1% 7.1% 11.4% 12.9% Cost of funds 3.2 % 3.1 % 3.4 % 5.2 % 4.7 % Net interest spread 3.5 % 2.0 % 3.7 % 6.2 % 8.2 % Leverage ratio 7.0x 7.7x 8.7x 3.2x 2.0x Levered yield 31.2% 21.1% 39.3% 31.3% 29.0%

Sourcing Strategy: Acquisition and Origination Acquired Loans ▪ Top 5 acquirer of SBC loans since crisis ▪ Since 2008 and through March 31, 2016, Waterfall has reviewed approximately 254,000 performing, sub - performing and non - performing SBC and SBA loans, priced approximately 129,000 of these loans and acquired more than 9,000 SBC and SBA loans with aggregate UPB of approximately $3.5 billion for an aggregate purchase price of approximately $2.6 billion ▪ Waterfall has also acquired more than $483.1 million in UPB of SBC ABS notes over this time period ▪ Represents 33.0% of SAM’s equity allocation ▪ ReadyCap Lending is a market leader in SBA 7(a) loan origination and servicing ▪ ReadyCap Lending holds one of only 14 non - bank SBLC licenses which provides a unique advantage in origination and acquisition of 7(a) loans. Of the 14 license holders, only four are actively originating ▪ The Company commenced ReadyCap Lending SBA 7(a) originations in 3Q15 ▪ Represents 21.8% of SAM’s equity allocation Originated Loans SAM either acquires a loan or originates a loan through its ReadyCap businesses ▪ ReadyCap Commercial is a TRS and market - leading nationwide originator, focused solely on providing SBC loans (First mortgage loans, "Mini - perm" loans, Bridge loans, and Mezzanine loans) ▪ Originated more than $1.0 billion in loans across 31 states since inception in Sep. 2012 ▪ Represents 45.2% of SAM’s equity allocation 28

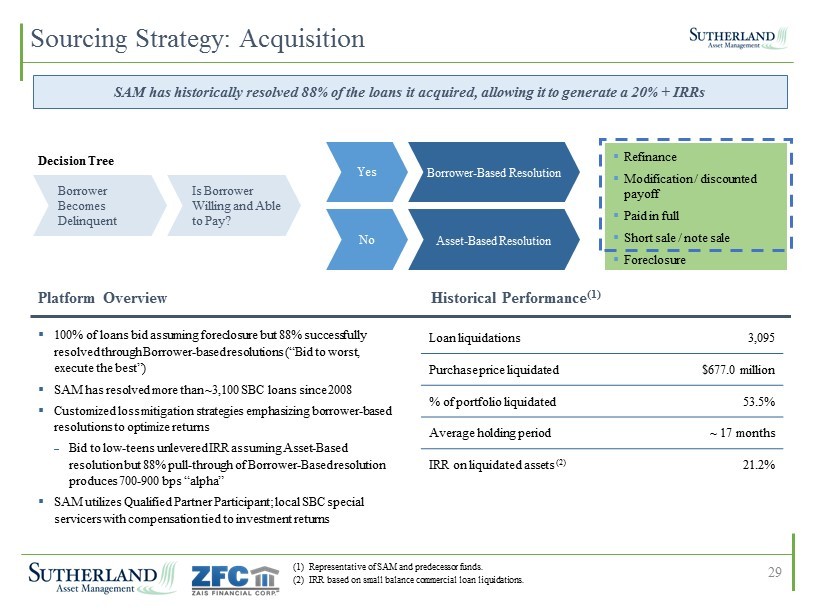

Yes No Borrower - Based Resolution Asset - Based Resolution Is Borrower Willing and Able to Pay? Borrower Becomes Delinquent Preferred Outcomes 88% ▪ Refinance ▪ Modification / discounted p ayoff ▪ Paid in full ▪ Short sale / note sale ▪ Foreclosure Decision Tree ▪ 100% of loans bid assuming foreclosure but 88% successfully resolved through Borrower - based resolutions (“Bid to worst, execute the best”) ▪ SAM has resolved more than ~ 3,100 SBC loans since 2008 ▪ Customized loss mitigation strategies emphasizing borrower - based resolutions to optimize returns – Bid to low - teens unlevered IRR assuming Asset - Based resolution but 88% pull - through of Borrower - Based resolution produces 700 - 900 bps “alpha” ▪ SAM utilizes Qualified Partner Participant; local SBC special servicers with compensation tied to investment returns Loan liquidations 3,095 Purchase price liquidated $677.0 million % of portfolio liquidated 53.5% Average holding period ~ 17 months IRR on liquidated assets (2) 21.2% (1) Representative of SAM and predecessor funds. (2) IRR based on small balance commercial loan liquidations. Sourcing Strategy: Acquisition Platform Overview Historical Performance (1) SAM has historically resolved 88% of the loans it acquired, allowing it to generate a 20% + IRRs 29

30 Geographically diversified SBC loan origination platform to drive future growth NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor NY008HT3 / 807214_1.wor Sourcing Strategy: Origination States with Funded Loans Headquarters Sales Offices Actively Recruiting ▪ SAM is well - positioned in key geographic markets to acquire and originate SBC loans ▪ Acquired more than $3.5 billion in SBC and SBA loans ▪ Originated more than $1.0 billion in SBC conventional and owner occupied loans ▪ ~$1.5 billion acquisition and origination pipeline

14% 12% 10% 8% 6% 5% 5% 3% 3% 34% Texas California Florida New York Arizona Georgia North Carolina Virginia Pennslyvania Other Portfolio Yield Analysis – Q1 2016 Investment Type Avg. Carrying Value (1) Gross Yield (2) Avg. Debt Cost (1) Debt Cost ROE Acquired portfolio $568,073 8.5% $437,030 4.4% 22.2% SBC investor origination portfolio $613,638 7.4% $434,333 4.3% 15.0% SBA Originations, Acquisitions & Servicing $691,518 6.7% $605,166 3.2% 31.2% Total $1,873,229 7.5% $1,476,529 3.9% 20.9% 36% 14% 14% 7% 6% 5% 4% 3% 2% 9% Retail Multi-Family Office Health Care Industrial Residential Mixed Use Single Family Business Assets Other Top Geographic Concentration (3) Collateral Diversification (3) (1) In thousands. (2) Excludes gains on early dispositions. (3) As determined by carrying value as of 3/31/16. Top 10 loan exposure as a % of gross assets. 31 Diversified Investment Portfolio 4% Top 10 Loans Top 10 Loan Exposure (3) Limited Geographical Concentration Risk Invests in a Variety of Property Types Top 10 Loans Make Up Less Than 5% of the Total Portfolio SAM’s asset portfolio is diversified across geographies and property types

SBA 7(a) Loan Sale Transaction Economics – An Example (1) Credit losses are shared pari passu with SBA guaranteed versus unguaranteed %. (2) Premiums above 10% split 50/50 with SBA. The average gross premium from RCL’s 2016 guaranteed sales is 13.96%. The additiona l 3 .96% (13.96% - 10%) is split with SBA. Key Assumptions for 7(a) Loan Example Loan Amount $1,000,000 Guaranteed Balance (1) 75.00% $750,000 Unguaranteed Balance 25.00% 250,000 Sales Premium (2) 10.00% 75,000 Securitization Advance Rate 70.00% 175,000 Sample Economics Return for SBA 7(a) Loan Gain on Sale of Guaranteed Balance $75,000 Income on Retained Portion $250,000 6.00% $15,000 Debt on Securitized Portion 175,000 4.00% 7,000 $75,000 $8,000 Servicing Fee on Guaranteed Balance Sold 1.00% 7,500 Annual Net Interest Income $15,500 Annual Return on Equity (excluding gain on sale) 20.7% 32

33 SAM Return on Equity – Q1 2016 (1) Core Earnings is a non - GAAP measure. Please refer to page 33 in the Appendix for a reconciliation of GAAP to Core Earnings. (2) ROE based on annualized return for quarter ended March 31, 2016. Business Line Levered Yield Equity Allocation Net ROE Core Earnings Acquisitions 22.2% 33.0% SBC Conventional Originations 15.0 45.2 SBA Originations, Acquisitions & Servicing 31.2 21.8 (3.8) (3.8) 1.6 2.5 (10.9) (10.9) (0.3) – 7.5% 8.7% Return on Equity 20.9% 20.9% Cash and Other Non-Earning Assets, Net Non-Earning Equity Realized & Unrealized Gains, Net Operating Expenses & Fees, Net Loss on Discontinued Operations (2) (2) (1)

SAM GAAP to Core Earnings Reconciliation 34 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4'15 Q1'16 Net income - U.S. GAAP after income taxes $13,236 $13,823 $9,742 $12,721 $13,387 $8,919 $9,113 Reconciling items: Unrealized (gain) loss on mortgage-backed securities 252 (415) (143) (377) 1,301 3,754 (2,001) Gain on sale of SBA license 0 0 0 0 (1,317) 0 3,051 Gain on sale of SBA mortgage loans held-for-investment 0 (1,700) 0 0 0 0 0 (Gain) loss on discontinued operations 998 497 1,045 (1,693) (386) 1,622 351 Total reconciling items 1,250 (1,618) 902 (2,070) (402) 5,376 1,401 Core earning before income taxes 14,486 12,205 10,644 10,651 12,985 14,295 10,514 Income tax adjustment - 680 - - 527 - - Core Earnings - Non U.S. GAAP $14,486 $12,885 $10,644 $10,651 $13,512 $14,295 $10,514 Core EPS - Non U.S. GAAP $0.44 $0.39 $0.32 $0.32 $0.40 $0.43 $0.31 (Dollars in thousands, except for per share amounts)