Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - Jones Lang LaSalle Income Property Trust, Inc. | exhibit312may122016.htm |

| EX-32.1 - EXHIBIT 32.1 - Jones Lang LaSalle Income Property Trust, Inc. | exhibit321may122016.htm |

| EX-32.2 - EXHIBIT 32.2 - Jones Lang LaSalle Income Property Trust, Inc. | exhibit322may122016.htm |

| EX-31.1 - EXHIBIT 31.1 - Jones Lang LaSalle Income Property Trust, Inc. | exhibit311may122016.htm |

______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________________

FORM 10-Q

_________________________________

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2016

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 000-51948

_________________________________

Jones Lang LaSalle Income Property Trust, Inc.

(Exact name of registrant as specified in its charter)

_________________________________

Maryland | 20-1432284 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

333 West Wacker Drive, Chicago IL, 60606

(Address of principal executive offices, including Zip Code)

(312) 897-4000

(Registrant’s telephone number, including area code)

N/A

(Former name or former address, if changed since last report)

_________________________________

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer.

Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

Non-accelerated filer | x | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ¨ NO x

The number of shares of the registrant’s Common Stock, $.01 par value, outstanding on May 12, 2016 were 48,531,906 shares of Class A Common Stock, 30,411,785 shares of Class M Common Stock, 7,320,485 of Class A-I Common Stock, 5,118,410 of Class M-I Common Stock and 6,387,184 shares of Class D Common Stock.

______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Jones Lang LaSalle Income Property Trust, Inc.

INDEX

PAGE NUMBER | |

2

Item 1. Financial Statements.

Jones Lang LaSalle Income Property Trust, Inc.

CONSOLIDATED BALANCE SHEETS

$ in thousands, except per share amounts

The abbreviation “VIEs” above means consolidated Variable Interest Entities.

March 31, 2016 | December 31, 2015 | |||||||

(Unaudited) | ||||||||

ASSETS | ||||||||

Investments in real estate: | ||||||||

Land (including from VIEs of $32,645 and $32,645, respectively) | $ | 249,991 | $ | 251,331 | ||||

Buildings and equipment (including from VIEs of $187,824 and $187,505, respectively) | 889,830 | 889,307 | ||||||

Less accumulated depreciation (including from VIEs of $(24,304) and $(23,146), respectively) | (81,265 | ) | (75,245 | ) | ||||

Net property and equipment | 1,058,556 | 1,065,393 | ||||||

Investment in unconsolidated real estate affiliates | 103,338 | 103,003 | ||||||

Net investments in real estate | 1,161,894 | 1,168,396 | ||||||

Cash and cash equivalents (including from VIEs of $13,616 and $13,365, respectively) | 160,293 | 34,739 | ||||||

Restricted cash (including from VIEs of $890 and $666, respectively) | 1,727 | 1,227 | ||||||

Tenant accounts receivable, net (including from VIEs of $1,495 and $1,724, respectively) | 4,164 | 3,500 | ||||||

Deferred expenses, net (including from VIEs of $146 and $118, respectively) | 9,861 | 10,022 | ||||||

Acquired intangible assets, net (including from VIEs of $8,911 and $9,208, respectively) | 83,070 | 86,471 | ||||||

Deferred rent receivable, net (including from VIEs of $951 and $852, respectively) | 10,642 | 9,445 | ||||||

Prepaid expenses and other assets (including from VIEs of $287 and $373, respectively) | 9,536 | 5,978 | ||||||

TOTAL ASSETS | $ | 1,441,187 | $ | 1,319,778 | ||||

LIABILITIES AND EQUITY | ||||||||

Mortgage notes and other debt payable, net (including from VIEs of $141,706 and $141,972, respectively) | $ | 518,107 | $ | 485,178 | ||||

Accounts payable and other accrued expenses (including from VIEs of $1,888 and $2,058, respectively) | 18,284 | 17,235 | ||||||

Distributions payable | 9,445 | 8,633 | ||||||

Accrued interest (including from VIEs of $562 and $560, respectively) | 1,699 | 1,659 | ||||||

Accrued real estate taxes (including from VIEs of $888 and $802, respectively) | 3,562 | 1,925 | ||||||

Advisor fees payable | 1,082 | 3,241 | ||||||

Acquired intangible liabilities, net | 16,245 | 16,984 | ||||||

TOTAL LIABILITIES | 568,424 | 534,855 | ||||||

Commitments and contingencies | — | — | ||||||

Equity: | ||||||||

Class A common stock: $0.01 par value; 200,000,000 shares authorized; 44,847,501 and 37,092,768 shares issued and outstanding at March 31, 2016 and December 31, 2015, respectively | 448 | 371 | ||||||

Class M common stock: $0.01 par value; 200,000,000 shares authorized; 29,134,965 and 27,909,411 shares issued and outstanding at March 31, 2016 and December 31, 2015, respectively | 291 | 279 | ||||||

Class A-I common stock: $0.01 par value; 200,000,000 shares authorized; 6,788,479 and 6,116,812 shares issued and outstanding at March 31, 2016 and December 31, 2015, respectively | 68 | 61 | ||||||

Class M-I common stock: $0.01 par value; 200,000,000 shares authorized; 3,912,988 and 3,356,619 shares issued and outstanding at March 31, 2016 and December 31, 2015, respectively | 39 | 34 | ||||||

Class D common stock: $0.01 par value; 200,000,000 shares authorized; 6,319,475 and 7,787,823 shares issued and outstanding at March 31, 2016 and December 31, 2015, respectively | 63 | 78 | ||||||

Additional paid-in capital (net of offering costs of $30,596 and $26,911 as of March 31, 2016 and December 31, 2015, respectively) | 1,146,482 | 1,051,230 | ||||||

Accumulated other comprehensive loss | (1,820 | ) | (2,327 | ) | ||||

Distributions to stockholders | (160,733 | ) | (151,277 | ) | ||||

Accumulated deficit | (122,214 | ) | (123,700 | ) | ||||

Total Jones Lang LaSalle Income Property Trust, Inc. stockholders’ equity | 862,624 | 774,749 | ||||||

Noncontrolling interests | 10,139 | 10,174 | ||||||

Total equity | 872,763 | 784,923 | ||||||

TOTAL LIABILITIES AND EQUITY | $ | 1,441,187 | $ | 1,319,778 | ||||

See notes to consolidated financial statements.

3

Jones Lang LaSalle Income Property Trust, Inc.

CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME

$ in thousands, except share and per share amounts

(Unaudited)

Three months ended March 31, 2016 | Three months ended March 31, 2015 | ||||||||

Revenues: | |||||||||

Minimum rents | $ | 23,570 | $ | 17,650 | |||||

Tenant recoveries and other rental income | 5,776 | 4,075 | |||||||

Total revenues | 29,346 | 21,725 | |||||||

Operating expenses: | |||||||||

Real estate taxes | 3,722 | 2,845 | |||||||

Property operating | 5,192 | 4,465 | |||||||

Provision for doubtful accounts | 135 | 125 | |||||||

Property general and administrative | 328 | 165 | |||||||

Advisor fees | 3,028 | 1,638 | |||||||

Company level expenses | 606 | 687 | |||||||

Acquisition expenses | 180 | 133 | |||||||

Depreciation and amortization | 9,009 | 6,564 | |||||||

Total operating expenses | 22,200 | 16,622 | |||||||

Operating income | 7,146 | 5,103 | |||||||

Other income and (expenses): | |||||||||

Interest expense | (5,961 | ) | (4,227 | ) | |||||

Equity in income of unconsolidated affiliates | 335 | 180 | |||||||

Gain on disposition of property and extinguishment of debt | 40 | 29,009 | |||||||

Total other income and (expenses) | (5,586 | ) | 24,962 | ||||||

Net income | 1,560 | 30,065 | |||||||

Less: Net income attributable to the noncontrolling interests | (74 | ) | (6,553 | ) | |||||

Net income attributable to Jones Lang LaSalle Income Property Trust, Inc. | $ | 1,486 | $ | 23,512 | |||||

Net income attributable to Jones Lang LaSalle Income Property Trust, Inc. per share-basic and diluted | $ | 0.02 | $ | 0.48 | |||||

Weighted average common stock outstanding-basic and diluted | 87,274,769 | 49,162,338 | |||||||

Other comprehensive gain (loss): | |||||||||

Foreign currency translation adjustment | 507 | (692 | ) | ||||||

Total other comprehensive gain (loss) | 507 | (692 | ) | ||||||

Net comprehensive income | $ | 1,993 | $ | 22,820 | |||||

See notes to consolidated financial statements.

4

Jones Lang LaSalle Income Property Trust, Inc.

CONSOLIDATED STATEMENT OF EQUITY

$ in thousands, except share and per share amounts

(Unaudited)

Common Stock | Additional Paid In Capital | Accumulated Other Comprehensive Loss | Distributions to Stockholders | Accumulated Deficit | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||||

Shares | Amount | ||||||||||||||||||||||||||||||

Balance, January 1, 2016 | 82,263,433 | $ | 823 | $ | 1,051,230 | $ | (2,327 | ) | $ | (151,277 | ) | $ | (123,700 | ) | $ | 10,174 | $ | 784,923 | |||||||||||||

Issuance of common stock | 11,377,875 | 113 | 128,657 | — | — | — | — | 128,770 | |||||||||||||||||||||||

Repurchase of shares | (2,637,900 | ) | (27 | ) | (29,720 | ) | — | — | — | — | (29,747 | ) | |||||||||||||||||||

Offering costs | — | — | (3,685 | ) | — | — | — | — | (3,685 | ) | |||||||||||||||||||||

Net income | — | — | — | — | — | 1,486 | 74 | 1,560 | |||||||||||||||||||||||

Other comprehensive income | — | — | — | 507 | — | — | — | 507 | |||||||||||||||||||||||

Cash contributions from noncontrolling interests | — | — | — | — | — | — | 20 | 20 | |||||||||||||||||||||||

Cash distributed to noncontrolling interests | — | — | — | — | — | — | (129 | ) | (129 | ) | |||||||||||||||||||||

Distributions declared per share ($0.12) | — | — | — | — | (9,456 | ) | — | — | (9,456 | ) | |||||||||||||||||||||

Balance, March 31, 2016 | 91,003,408 | $ | 909 | $ | 1,146,482 | $ | (1,820 | ) | $ | (160,733 | ) | $ | (122,214 | ) | $ | 10,139 | $ | 872,763 | |||||||||||||

See notes to consolidated financial statements.

5

Jones Lang LaSalle Income Property Trust, Inc.

CONSOLIDATED STATEMENTS OF CASH FLOWS

$ in thousands (Unaudited)

See notes to consolidated financial statements.

Three months ended March 31, 2016 | Three months ended March 31, 2015 | |||||||

CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

Net income | $ | 1,560 | $ | 30,065 | ||||

Adjustments to reconcile income to net cash provided by operating activities: | ||||||||

Depreciation and amortization | 8,602 | 6,267 | ||||||

Gain on disposition of property and extinguishment of debt | (40 | ) | (29,009 | ) | ||||

Provision for doubtful accounts | 135 | 125 | ||||||

Straight line rent | (1,347 | ) | (276 | ) | ||||

Equity in income of unconsolidated affiliates | (335 | ) | (180 | ) | ||||

Net changes in assets, liabilities and other | (637 | ) | (290 | ) | ||||

Net cash provided by operating activities | 7,938 | 6,702 | ||||||

CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

Proceeds from sale of real estate investments and fixed assets | 7,371 | 119,706 | ||||||

Capital improvements and lease commissions | (4,135 | ) | (1,450 | ) | ||||

Investment in unconsolidated real estate affiliates | — | (73 | ) | |||||

Loan escrows | (500 | ) | 1,092 | |||||

Net cash provided by investing activities | 2,736 | 119,275 | ||||||

CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

Issuance of common stock | 120,554 | 48,399 | ||||||

Repurchase of shares | (29,747 | ) | (14,294 | ) | ||||

Offering costs | (3,437 | ) | (2,139 | ) | ||||

Distributions to stockholders | (2,869 | ) | (2,735 | ) | ||||

Distributions paid to noncontrolling interests | (129 | ) | (10,891 | ) | ||||

Contributions received from noncontrolling interests | 20 | 329 | ||||||

Deposits for loan commitments | (1,115 | ) | (344 | ) | ||||

Payment on credit facility | (30,000 | ) | — | |||||

Proceeds from mortgage notes and other debt payable | 62,800 | — | ||||||

Debt issuance costs | (874 | ) | (28 | ) | ||||

Payment on early extinguishment of debt | — | (711 | ) | |||||

Principal payments on mortgage notes and other debt payable | (448 | ) | (80,683 | ) | ||||

Net cash provided by (used in) financing activities | 114,755 | (63,097 | ) | |||||

Net increase in cash and cash equivalents | 125,429 | 62,880 | ||||||

Effect of exchange rates | 125 | (125 | ) | |||||

Cash and cash equivalents at the beginning of the period | 34,739 | 32,211 | ||||||

Cash and cash equivalents at the end of the period | $ | 160,293 | $ | 94,966 | ||||

Supplemental disclosure of cash flow information: | ||||||||

Interest paid | $ | 5,189 | $ | 4,132 | ||||

Non-cash activities: | ||||||||

Write-offs of receivables | $ | 12 | $ | 52 | ||||

Write-offs of retired assets and liabilities | 373 | (288 | ) | |||||

Change in liability for capital expenditures | (309 | ) | 1,081 | |||||

Deposit of holdback proceeds from sale of real estate investments | — | 1,847 | ||||||

Net liabilities transferred at sale of real estate investment | — | 973 | ||||||

Change in issuance of common stock receivable | 2,441 | (294 | ) | |||||

Change in accrued offering costs | 248 | 718 | ||||||

6

Jones Lang LaSalle Income Property Trust, Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

$ in thousands, except per share amounts

NOTE 1—ORGANIZATION

General

Except where the context suggests otherwise, the terms “we,” “us,” “our” and the “Company” refer to Jones Lang LaSalle Income Property Trust, Inc. The terms “Advisor” and “LaSalle” refer to LaSalle Investment Management, Inc.

Jones Lang LaSalle Income Property Trust, Inc. is an externally managed, non-listed, daily valued perpetual-life real estate investment trust ("REIT") that owns and manages a diversified portfolio of apartment, industrial, office, retail and other properties located primarily in the United States. We expect over time that our real estate portfolio will be further diversified on a global basis through the acquisition of additional properties outside of the United States and will be complemented by investments in real estate-related debt and equity securities. We were incorporated on May 28, 2004 under the laws of the State of Maryland. We believe that we have operated in such a manner to qualify to be taxed as a REIT for federal income tax purposes commencing with the taxable year ended December 31, 2004, when we first elected REIT status. As of March 31, 2016, we owned interests in a total of 53 properties, 52 of which are located in 14 states and one of which is located in Canada.

From our inception to October 1, 2012, we raised equity proceeds through private offerings of shares of our common stock. On October 1, 2012, the Securities and Exchange Commission (the "SEC") declared effective our Registration Statement on Form S-11 with respect to our continuous public offering of up to $3,000,000 in any combination of Class A and Class M shares of common stock (the "Initial Public Offering"). Affiliates of our sponsor, Jones Lang LaSalle Incorporated ("JLL" or our "Sponsor"), currently have invested an aggregate of $50,200 through purchases of shares of our common stock. As of January 15, 2015, the date our Initial Public Offering terminated, we had raised aggregate gross proceeds from the sale of shares of our Class A and Class M common stock in our Initial Public Offering of $268,981.

On January 16, 2015, our follow-on Registration Statement on Form S-11 was declared effective by the SEC (Commission File No. 333-196886) with respect to our continuous public offering of up to $2,700,000 in any combination of shares of our Class A, Class M, Class A-I and Class M-I common stock, consisting of up to $2,400,000 of shares offered in our primary offering and up to $300,000 in shares offered pursuant to our distribution reinvestment plan (the “First Extended Public Offering”). We reserve the right to terminate the First Extended Public Offering at any time and to extend the First Extended Public Offering term to the extent permissible under applicable law. As of March 31, 2016, we have raised aggregate gross proceeds from the sale of shares of our Class A, Class M, Class A-I and Class M-I shares in our First Extended Public Offering of $482,580.

On June 19, 2014, we began a private offering of up to $400,000 in any combination of our Class A-I, Class M-I and Class D shares of common stock (the "Initial Private Offering"). Upon the SEC declaring the registration statement for our First Extended Public Offering effective, we terminated the Initial Private Offering. As of January 15, 2015, we had raised aggregate gross proceeds from the sale of shares of our Class A-I, Class M-I and Class D common stock in our Initial Private Offering of approximately $43,510. On March 3, 2015, we commenced a new private offering (the "Follow-on Private Offering") of up to $350,000 in shares of our Class D common stock with indefinite duration. As of March 31, 2016, we have raised aggregate gross proceeds from the sale of our Class D shares in our Follow-on Private Offering of $50,082.

As of March 31, 2016, 44,847,501 shares of Class A common stock, 29,134,965 shares of Class M common stock, 6,788,479 shares of Class A-I common stock, 3,912,988 shares of Class M-I common stock, and 6,319,475 shares of Class D common stock were outstanding and held by a total of 8,468 stockholders.

LaSalle acts as our advisor pursuant to the second amended and restated advisory agreement between the Company and LaSalle (the “Advisory Agreement”). On May 10, 2016, we renewed our Advisory Agreement with our Advisor for a one-year term expiring on June 5, 2017. Our Advisor, a registered investment advisor with the SEC, has broad discretion with respect to our investment decisions and is responsible for selecting our investments and for managing our investment portfolio pursuant to the terms of the Advisory Agreement. LaSalle is a wholly-owned, but operationally independent subsidiary of JLL, a New York Stock Exchange-listed global financial and professional services firm specializing in commercial real estate services. We have no employees, as all operations are managed by our Advisor. Our executive officers are employees of and compensated by our Advisor.

7

NOTE 2—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation and Principles of Consolidation

The accompanying consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“GAAP”), the instructions to Form 10-Q and Rule 10-01 of Regulation S-X and include the accounts of our wholly-owned subsidiaries, consolidated variable interest entities ("VIE") and the unconsolidated investment in real estate affiliate accounted for under the equity method of accounting. We consider the authoritative guidance of accounting for investments in common stock, investments in real estate ventures, investors accounting for an investee when the investor has the majority of the voting interest but the minority partners have certain approval or veto rights, determining whether a general partner or general partners as a group controls a limited partnership or similar entity when the limited partners have certain rights and the consolidation of VIEs in which we own less than a 100% interest. All significant intercompany balances and transactions have been eliminated in consolidation.

Parenthetical disclosures are shown on our Consolidated Balance Sheets regarding the amounts of VIE assets and liabilities that are consolidated. As of March 31, 2016, our VIEs include The District at Howell Mill, The Edge at Lafayette, Campus Lodge Tampa, Grand Lakes Marketplace and Townlake of Coppell due to the limited partnership structures and our partners having limited participation rights and no kick out rights. The creditors of our VIEs do not have general recourse to us. Prior to new consolidation guidance adopted on January 1, 2016, Grand Lakes Marketplace and Townlake of Coppell were not classified as VIEs. VIE disclosures as of December 31, 2015 on our Consolidated Balance Sheets have been updated to include Grand Lakes Marketplace and Townlake of Coppell for comparative purposes.

Noncontrolling interests represent the minority members’ proportionate share of the equity in our VIEs. At acquisition, the assets, liabilities and noncontrolling interests were measured and recorded at the estimated fair value. Noncontrolling interests will increase for the minority members’ share of net income of these entities and contributions and decrease for the minority members’ share of net loss and distributions. As of March 31, 2016, noncontrolling interests represented the minority members’ proportionate share of the equity of the entities listed above as VIEs.

The accompanying unaudited interim consolidated financial statements have been prepared in accordance with the accounting policies described in the consolidated financial statements and related notes included in our Form 10-K filed with the SEC on March 10, 2016 (our “2015 Form 10-K”) and should be read in conjunction with such consolidated financial statements and related notes. The following notes to these interim consolidated financial statements highlight changes to the notes included in the December 31, 2015 audited consolidated financial statements included in our 2015 Form 10-K and present interim disclosures as required by the SEC.

The interim financial data as of March 31, 2016 and for the three months ended March 31, 2016 and 2015 is unaudited. In our opinion, the interim data includes all adjustments, consisting only of normal recurring adjustments, necessary for a fair statement of the results for the interim periods.

Allowance for Doubtful Accounts

An allowance for doubtful accounts is provided against the portion of accounts receivable and deferred rent receivable that is estimated to be uncollectible. Such allowance is reviewed periodically based upon our recovery experience. At March 31, 2016 and December 31, 2015, our allowance for doubtful accounts was $436 and $312, respectively.

Deferred Expenses

Deferred expenses consist of lease commissions. Lease commissions are capitalized and amortized over the term of the related lease as a component of depreciation and amortization expense. Accumulated amortization of deferred expenses at March 31, 2016 and December 31, 2015 was $1,583 and $1,234, respectively.

Acquisitions

We have allocated a portion of the purchase price of our acquisitions to acquired intangible assets, which include acquired in-place lease intangibles, acquired above-market in-place lease intangibles and acquired ground lease intangibles, which are reported net of accumulated amortization of $24,632 and $21,660 at March 31, 2016 and December 31, 2015, respectively, on the accompanying Consolidated Balance Sheets. The acquired intangible liabilities represent acquired below-market in-place leases, which are reported net of accumulated amortization of $4,109 and $3,364 at March 31, 2016 and December 31, 2015, respectively, on the accompanying Consolidated Balance Sheets.

8

Assets and Liabilities Measured at Fair Value

The Financial Accounting Standards Board’s (“FASB”) guidance for fair value measurement and disclosure states that fair value is an exit price, representing the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. As such, fair value is a market-based measurement that should be determined based on assumptions that market participants would use in pricing an asset or liability. As a basis for considering assumptions, authoritative guidance establishes a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value as follows:

• | Level 1—Inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that we have access to at the measurement date. |

• | Level 2—Observable inputs, other than quoted prices included in level 1 that are observable for the asset or liability, either directly or indirectly. Level 2 inputs are those in markets for which there are few transactions, the prices are not current, little public information exists or instances where prices vary substantially over time or among brokered market makers. |

• | Level 3—Unobservable inputs for the asset or liability. Unobservable inputs are those inputs that reflect our own assumptions that market participants would use to price the asset or liability based on the best available information. |

The authoritative guidance requires the disclosure of the fair value of our financial instruments for which it is practicable to estimate that value. The guidance does not apply to all balance sheet items. Market information as available or present value techniques have been utilized to estimate the amounts required to be disclosed. Since such amounts are estimates, there can be no assurance that the disclosed value of any financial instrument could be realized by immediate settlement of the instrument.

Partnership interests accounted for under the fair value option are stated at the fair value of our ownership in the partnership. The fair value is recorded based upon changes in the net asset value of the limited partnership as determined from the financial statements of the limited partnership. During the three months ended March 31, 2016, we recorded unrealized changes in fair value classified within the Level 3 category of $223 in our investment in NYC Retail Portfolio (see Note 4-Unconsolidated Real Estate Affiliates).

We have estimated the fair value of our mortgage notes and other debt payable reflected in the accompanying Consolidated Balance Sheets at amounts that are based upon an interpretation of available market information and valuation methodologies (including discounted cash flow analysis with regard to fixed rate debt) for similar loans made to borrowers with similar credit ratings and for the same maturities. The fair value of our mortgage notes payable using Level 2 inputs was $5,810 and $927 higher than the aggregate carrying amounts at March 31, 2016 and December 31, 2015, respectively. Such fair value estimates are not necessarily indicative of the amounts that would be realized upon disposition of our mortgage notes payable.

Derivative Financial Instruments

We record all derivatives on the Consolidated Balance Sheets at fair value in prepaid expenses and other assets or accounts payable and other accrued expenses. Changes in the fair value of our derivatives are recorded as a component of interest expense on our Consolidated Statements of Operations and Comprehensive Income as we have not designated our derivative instruments as hedges. Our objective in using interest rate derivatives is to manage our exposure to interest rate movements. To accomplish this objective, we use interest rate caps and swaps.

As of March 31, 2016, we had the following outstanding interest rate derivatives related to managing our interest rate risk:

Interest Rate Derivative | Number of Instruments | Notional Amount | ||||

Interest Rate Caps | 6 | $ | 97,930 | |||

Interest Rate Swaps | 3 | 71,400 | ||||

The fair value of our interest rate caps and swaps represent liabilities of $653 and $153 at March 31, 2016 and December 31, 2015, respectively.

9

Use of Estimates

The preparation of consolidated financial statements in conformity with GAAP requires us to make estimates and assumptions. These estimates and assumptions impact the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. For example, significant estimates and assumptions have been made with respect to useful lives of assets, recoverable amounts of receivables, fair value of derivatives and real estate assets, initial valuations and related amortization periods of deferred costs and intangibles, particularly with respect to property acquisitions. Actual results could differ from those estimates.

NOTE 3—PROPERTY

The primary reason we make acquisitions of real estate investments in the apartment, industrial, office, retail and other property sectors is to invest capital contributed by stockholders in a diversified portfolio of real estate assets. There were no consolidated properties acquired during the three months ended March 31, 2016.

During the three months ended March 31, 2016 and 2015, we incurred $180 and $133, respectively, of acquisition expenses recorded on the Consolidated Statements of Operations and Comprehensive Income.

2016 Dispositions

On March 1, 2016, we sold 36 Research Park Drive for approximately $7,900 less closing costs. We recorded a gain on the sale of the property in the amount of $40.

NOTE 4—UNCONSOLIDATED REAL ESTATE AFFILIATES

Fair Value Option Investment

NYC Retail Portfolio

On December 8, 2015, a wholly-owned subsidiary of the Company acquired an approximate 28% interest in a newly formed limited partnership, Madison NYC Core Retail Partners, L.P., which acquired an approximate 49% interest in entities that own 15 retail properties located in the greater New York City area (the “NYC Retail Portfolio”), the result of which is that we own an approximate 14% interest in the NYC Retail Portfolio. The purchase price for such portion was approximately $85,600 including closing costs. The NYC Retail Portfolio contains approximately 2,700,000 square feet across urban infill locations in Manhattan, Brooklyn, Queens, the Bronx, Staten Island and New Jersey.

At acquisition we made the election to account for our interest in the NYC Retail Portfolio under the fair value option. Our investment in the NYC Retail Portfolio will be presented on our Consolidated Balance Sheets within investments in unconsolidated real estate affiliates. Changes in the fair value of our investment as well as cash distributions received will be recorded on our Consolidated Statements of Operations and Comprehensive Income within equity in income of unconsolidated affiliates. As of March 31, 2016 and December 31, 2015, the carrying amount of our investment in the NYC Retail Portfolio was $85,291 and $85,068, respectively. During the three months ended March 31, 2016 we recorded a $223 increase in fair value of our investment in the NYC Retail Portfolio and received no cash distributions. For the year ended December 31, 2015 we recorded no changes in fair value of our investment in the NYC Retail Portfolio and received no cash distributions.

Equity Method Investment

Chicago Parking Garage

On December 23, 2014, we acquired a condominium interest in Chicago Parking Garage, a 366 stall, multi-level parking facility located in a large mixed-use property in Chicago, Illinois for approximately $16,900 using cash on hand. In accordance with authoritative guidance, Chicago Parking Garage is accounted for as an investment in an unconsolidated real estate affiliate. At March 31, 2016 and December 31, 2015, the carrying amount of our investment in Chicago Parking Garage was $18,047 and $17,935, respectively.

10

NOTE 5—MORTGAGE NOTES AND OTHER DEBT PAYABLE

Mortgage notes and other debt payable have various maturities through 2027 and consist of the following:

Mortgage notes and other debt payable | Maturity Date | Interest Rate | Amount payable as of | |||||||||

March 31, 2016 | December 31, 2015 | |||||||||||

Mortgage notes payable (1) (2) | October 1, 2016 - March 1, 2027 | 2.49% - 6.14% | $ | 521,330 | $ | 487,615 | ||||||

Net debt premium on assumed debt and debt issuance costs | (3,223 | ) | (2,437 | ) | ||||||||

Mortgage notes and other debt payable, net | $ | 518,107 | $ | 485,178 | ||||||||

(1) | On February 17, 2016, we entered into a $40,000 mortgage note payable on Monument IV at Worldgate. The mortgage note is for seven years and bears a floating interest rate equal to LIBOR plus 1.75%. We entered into an interest rate swap for this loan which fixed the interest rate at 3.13% for the seven year term. |

(2) | On March 17, 2016, we entered into a $22,800 mortgage note payable on 140 Park Avenue. The mortgage note is for five years and bears a floating interest rate equal to LIBOR plus 1.75%. We entered into an interest rate swap for this loan which fixed the interest rate at 3.00% for the five year term. |

Aggregate future principal payments of mortgage notes payable as of March 31, 2016 are as follows:

Year | Amount | |||

2016 | $ | 32,850 | ||

2017 | 81,366 | |||

2018 | 19,994 | |||

2019 | 11,309 | |||

2020 | 50,431 | |||

Thereafter | 325,380 | |||

Total | $ | 521,330 | ||

Line of Credit

On June 8, 2015, we extended our existing $40,000 revolving line of credit agreement with Bank of America, N.A. The line of credit has a two-year term with a one-year extension at our option and bears interest based on LIBOR plus a spread ranging from 1.35% to 2.10%, depending on our leverage ratio (1.35% spread at March 31, 2016). The line of credit also contains an accordion feature that allows us to increase the facility to $100,000, which we exercised in December 2015. We intend to use the line of credit to cover short-term capital needs, for new property acquisitions and working capital. We may not draw funds on our line of credit if we (i) experience a material adverse effect, which is defined to include, among other things, (a) a material adverse effect upon the operations, business, assets, liabilities or financial condition of the Company, taken as a whole; (b) a material impairment of the rights and remedies of any lender under any loan document or the ability of any loan party to perform its obligations under any loan document; or (c) a material adverse effect upon the legality, validity, binding effect or enforceability against any loan party of any loan document to which it is a party or (ii) are in default, as that term is defined in the agreement, including a cross default under certain other loan agreements and/or guarantees entered into by the Company or its subsidiaries. As of March 31, 2016, we believe no material adverse effects had occurred. Our line of credit does require us to meet certain customary debt covenants which include a maximum leverage ratio, a minimum debt service coverage ratio as well as maintaining minimum amounts of equity and liquidity. As of March 31, 2016 and December 31, 2015, we had $0 and $30,000, respectively, borrowings outstanding on the revolving line of credit.

At March 31, 2016, we were in compliance with all debt covenants.

Debt Issuance Costs

Debt issuance costs are capitalized and amortized over the terms of the respective agreements as a component of interest expense. Accumulated amortization of debt issuance costs at March 31, 2016 and December 31, 2015 was $2,301 and $2,107, respectively. Upon implementing FASB Accounting Standard Update 2015-03, Simplifying the Presentation of Debt Issuance Costs during the period ended March 31, 2016, we reclassified $2,914 of net debt issuance costs from Deferred expenses, net to Mortgage notes and other debt payable, net on our Consolidated Balance Sheet as of December 31, 2015.

11

NOTE 6—COMMON STOCK

We have five classes of common stock authorized as of March 31, 2016, Class A, Class M, Class A-I, Class M-I, and Class D. The fees payable to LaSalle Investment Management Distributors, LLC, an affiliate of our Advisor and the dealer manager for our offerings (the "Dealer Manager"), with respect to each outstanding share of each class, as a percentage of NAV, are as follows:

Selling Commission (1) | Dealer Manager Fee (2) | |||

Class A Shares | up to 3.5% | 1.05% | ||

Class M Shares | None | 0.30% | ||

Class A-I Shares | up to 1.5% | 0.30% | ||

Class M-I Shares | None | 0.05% | ||

Class D Shares (3) | up to 1.0% | None | ||

(1) | Selling commissions are paid on the date of purchase. |

(2) | Dealer manager fees are accrued daily on a continuous basis equal to 1/365th of the stated fee. |

(3) | Shares of Class D common stock are only being offered pursuant to a private offering. |

The selling commission and dealer manager fee are offering costs and are recorded as a reduction of additional paid in capital.

Stock Transactions

The stock transactions for each of our classes of common stock for the three months ended March 31, 2016 were as follows:

Shares of Class A Common Stock | Shares of Class M Common Stock | Shares of Class A-I Common Stock | Shares of Class M-I Common Stock | Shares of Class D Common Stock | |||||||||||

Balance, December 31, 2015 | 37,092,768 | 27,909,411 | 6,116,812 | 3,356,619 | 7,787,823 | ||||||||||

Issuance of common stock | 7,848,394 | 2,120,944 | 769,098 | 556,369 | 83,070 | ||||||||||

Repurchase of shares | (93,661 | ) | (895,390 | ) | (97,431 | ) | — | (1,551,418 | ) | ||||||

Balance, March 31, 2016 | 44,847,501 | 29,134,965 | 6,788,479 | 3,912,988 | 6,319,475 | ||||||||||

Stock Issuances

The stock issuances for our classes of shares, including those issued through our distribution reinvestment plan, for the three months ended March 31, 2016 were as follows:

Three months ended | ||||||

March 31, 2016 | ||||||

# of shares | Amount | |||||

Class A Shares | 7,848,394 | $ | 88,984 | |||

Class M Shares | 2,120,944 | 23,882 | ||||

Class A-I Shares | 769,098 | 8,703 | ||||

Class M-I Shares | 556,369 | 6,266 | ||||

Class D Shares | 83,070 | 935 | ||||

Total | $ | 128,770 | ||||

Share Repurchase Plan

Our share repurchase plan allows stockholders, subject to a one-year holding period, with certain exceptions, to request that we repurchase all or a portion of their shares on a daily basis at that day's NAV per share, limited to 5% of aggregate Company NAV per quarter. For the three months ended March 31, 2016, we repurchased 2,637,900 shares of common stock. During the three months ended March 31, 2015, we repurchased 1,342,088 shares of common stock.

12

Distribution Reinvestment Plan

Pursuant to our distribution reinvestment plan, holders of shares of any class of our common stock may elect to have their cash distributions reinvested in additional shares of our common stock at the NAV per share applicable to the class of shares being purchased on the distribution date. For the three months ended March 31, 2016, we issued 513,733 shares of common stock for $5,775 under the distribution reinvestment plan. For the three months ended March 31, 2015, we issued 224,956 shares of common stock for $2,410 under the distribution reinvestment plan.

Earnings Per Share (“EPS”)

Basic per share amounts are based on the weighted average of shares outstanding of 87,274,769 for the three months ended March 31, 2016 and 49,162,338 for the three months ended March 31, 2015. We have no dilutive or potentially dilutive securities.

Organization and Offering Costs

Organization and offering costs include, but are not limited to, legal, accounting and printing fees and personnel costs of our Advisor (including reimbursement of personnel costs for our executive officers prior to the commencement of the offerings) attributable to our organization, preparation of the registration statement, registration and qualification of our common stock for sale with the SEC and in the various states and filing fees incurred by our Advisor. LaSalle agreed to fund our organization and offering expenses through January 16, 2015, which is the date the SEC declared our registration statement effective for the First Extended Public Offering, following which time we commenced reimbursing LaSalle over 36 months for organization and offering costs incurred prior to the commencement date of the First Extended Public Offering. Following the First Extended Public Offering commencement date, we began paying directly or reimbursing LaSalle if it pays on our behalf any organization and offering costs incurred during the First Extended Public Offering period (other than selling commissions and dealer manager fees) as and when incurred. After the termination of the First Extended Public Offering, our Advisor has agreed to reimburse us to the extent that the organization and offering costs that we incur exceed 15% of our gross proceeds from the First Extended Public Offering. Organization costs are expensed, whereas offering costs are recorded as a reduction of capital in excess of par value. As of March 31, 2016 and December 31, 2015, LaSalle had paid $2,044 and $2,009, respectively, of organization and offering costs on our behalf which we had not yet reimbursed. These costs are included in Accounts payable and other accrued expenses.

NOTE 7—RELATED PARTY TRANSACTIONS

Effective as of October 1, 2012, we entered into a first amended and restated advisory agreement with LaSalle, pursuant to which we pay a fixed advisory fee of 1.25% of our NAV calculated daily. The Advisory Agreement allows for a performance fee to be earned for each share class based on the total return of that share class during the calendar year. The performance fee is calculated as 10% of the return in excess of 7% per annum. On May 10, 2016, we renewed our Advisory Agreement with our Advisor for a one year term expiring on June 5, 2017.

The fixed advisory fees for the three months ended March 31, 2016 and 2015 were $3,028 and $1,638, respectively. There were no performance fees for the three months ended March 31, 2016 and 2015. Included in Advisor fees payable at March 31, 2016 and December 31, 2015 were $1,082 and $3,241 of fixed advisory fee and performance fee expenses, respectively.

We pay Jones Lang LaSalle Americas, Inc. (“JLL Americas”), an affiliate of our Advisor, for property management, leasing, mortgage brokerage and sales brokerage services performed at various properties we own, on terms no less favorable than we could receive from other third party service providers. For the three months ended March 31, 2016 and 2015, JLL Americas was paid $83 and $74, respectively, for property management and leasing services. During the three months ended March 31, 2016, we paid JLL Americas $114 in loan placement fees related to the mortgage note payable on 140 Park Avenue and $197 in sales brokerage fees for the 36 Research Park Drive property sale.

We pay the Dealer Manager selling commissions and dealer manager fees in connection with our offerings. For the three months ended March 31, 2016 and 2015, we paid the Dealer Manager selling commissions and dealer manager fees totaling $2,342 and $978, respectively. A majority of the selling commissions and dealer manager fees are reallowed to participating broker-dealers.

As of March 31, 2016 and December 31, 2015, we owed $2,044 and $2,009, respectively, for organization and offering costs paid by LaSalle (see Note 6-Common Stock). These costs are included in Accounts payable and other accrued expenses.

13

NOTE 8—COMMITMENTS AND CONTINGENCIES

We are involved in various claims and litigation matters arising in the ordinary course of business, some of which involve claims for damages. Many of these matters are covered by insurance, although they may nevertheless be subject to deductibles or retentions. Although the ultimate liability for these matters cannot be determined, based upon information currently available, we believe the ultimate resolution of such claims and litigation will not have a material adverse effect on our financial position, results of operations or liquidity.

From time to time, we have entered into contingent agreements for the acquisition and financing of properties. Such acquisitions and financings are subject to satisfactory completion of due diligence or meeting certain leasing or occupancy thresholds.

We are subject to fixed ground lease payments on South Beach Parking Garage of $94 per year until September 30, 2016. The fixed amount will increase on September 30, 2016 and every five years thereafter by the lesser of 12% or the cumulative CPI over the previous five year period. We are also subject to a variable ground lease payment calculated as 2.5% of revenue. The lease expires September 30, 2041 and has a ten-year renewal option.

The operating agreement for Townlake of Coppell allows the unrelated third party joint venture partner, owning a 10% interest, to put their interest to us at a market determined value for a period of 90 days beginning in 2018.

14

NOTE 9—SEGMENT REPORTING

We have five operating segments: apartment, industrial, office, retail and other properties. Consistent with how we review and manage our properties, the financial information summarized below is presented by operating segment and reconciled to net income for the three months ended March 31, 2016 and 2015.

Apartment | Industrial | Office | Retail | Other | Total | |||||||||||||||||||

Assets as of March 31, 2016 | $ | 210,688 | $ | 291,422 | $ | 277,423 | $ | 392,281 | $ | 22,240 | $ | 1,194,054 | ||||||||||||

Assets as of December 31, 2015 | 211,532 | 292,730 | 281,582 | 392,718 | 21,981 | 1,200,543 | ||||||||||||||||||

Three Months Ended March 31, 2016 | ||||||||||||||||||||||||

Revenues: | ||||||||||||||||||||||||

Minimum rents | $ | 5,610 | $ | 4,834 | $ | 7,113 | $ | 5,944 | $ | 69 | $ | 23,570 | ||||||||||||

Tenant recoveries and other rental income | 299 | 1,540 | 1,117 | 2,136 | 684 | 5,776 | ||||||||||||||||||

Total revenues | $ | 5,909 | $ | 6,374 | $ | 8,230 | $ | 8,080 | $ | 753 | $ | 29,346 | ||||||||||||

Operating expenses: | ||||||||||||||||||||||||

Real estate taxes | $ | 614 | $ | 1,095 | $ | 829 | $ | 1,056 | $ | 128 | $ | 3,722 | ||||||||||||

Property operating | 1,797 | 413 | 1,664 | 1,109 | 209 | 5,192 | ||||||||||||||||||

Provision for doubtful accounts | 11 | — | — | 124 | — | 135 | ||||||||||||||||||

Total segment operating expenses | $ | 2,422 | $ | 1,508 | $ | 2,493 | $ | 2,289 | $ | 337 | $ | 9,049 | ||||||||||||

Operating income - Segments | $ | 3,487 | $ | 4,866 | $ | 5,737 | $ | 5,791 | $ | 416 | $ | 20,297 | ||||||||||||

Capital expenditures by segment | $ | 410 | $ | 415 | $ | 3,236 | $ | 363 | $ | — | $ | 4,424 | ||||||||||||

Reconciliation to net income | ||||||||||||||||||||||||

Operating income - Segments | $ | 20,297 | ||||||||||||||||||||||

Property general and administrative | 328 | |||||||||||||||||||||||

Advisor fees | 3,028 | |||||||||||||||||||||||

Company level expenses | 606 | |||||||||||||||||||||||

Acquisition expenses | 180 | |||||||||||||||||||||||

Depreciation and amortization | 9,009 | |||||||||||||||||||||||

Operating income | $ | 7,146 | ||||||||||||||||||||||

Other income and (expenses): | ||||||||||||||||||||||||

Interest expense | $ | (5,961 | ) | |||||||||||||||||||||

Equity in income of unconsolidated affiliates | 335 | |||||||||||||||||||||||

Gain on disposition of property and extinguishment of debt | 40 | |||||||||||||||||||||||

Total other income and (expenses) | $ | (5,586 | ) | |||||||||||||||||||||

Net income | $ | 1,560 | ||||||||||||||||||||||

Reconciliation to total consolidated assets as of March 31, 2016 | ||||||||||||||||||||||||

Assets per reportable segments | $ | 1,194,054 | ||||||||||||||||||||||

Corporate level assets | 247,133 | |||||||||||||||||||||||

Total consolidated assets | $ | 1,441,187 | ||||||||||||||||||||||

Reconciliation to total consolidated assets as of December 31, 2015 | ||||||||||||||||||||||||

Assets per reportable segments | $ | 1,200,543 | ||||||||||||||||||||||

Corporate level assets | 119,235 | |||||||||||||||||||||||

Total consolidated assets | $ | 1,319,778 | ||||||||||||||||||||||

15

Apartment | Industrial | Office | Retail | Other | Total | |||||||||||||||||||

Three Months Ended March 31, 2015 | ||||||||||||||||||||||||

Revenues: | ||||||||||||||||||||||||

Minimum rents | $ | 4,900 | $ | 3,139 | $ | 6,172 | $ | 3,369 | $ | 70 | $ | 17,650 | ||||||||||||

Tenant recoveries and other rental income | 247 | 752 | 1,083 | 1,211 | 782 | 4,075 | ||||||||||||||||||

Total revenues | $ | 5,147 | $ | 3,891 | $ | 7,255 | $ | 4,580 | $ | 852 | $ | 21,725 | ||||||||||||

Operating expenses: | ||||||||||||||||||||||||

Real estate taxes | $ | 511 | $ | 560 | $ | 780 | $ | 843 | $ | 151 | $ | 2,845 | ||||||||||||

Property operating | 1,827 | 199 | 1,655 | 525 | 259 | 4,465 | ||||||||||||||||||

Provision for doubtful accounts | 19 | — | 1 | 105 | — | 125 | ||||||||||||||||||

Total segment operating expenses | $ | 2,357 | $ | 759 | $ | 2,436 | $ | 1,473 | $ | 410 | $ | 7,435 | ||||||||||||

Operating income - Segments | $ | 2,790 | $ | 3,132 | $ | 4,819 | $ | 3,107 | $ | 442 | $ | 14,290 | ||||||||||||

Capital expenditures by segment | $ | 136 | $ | — | $ | 316 | $ | 70 | $ | 24 | $ | 546 | ||||||||||||

Reconciliation to net income | ||||||||||||||||||||||||

Operating income - Segments | $ | 14,290 | ||||||||||||||||||||||

Property general and administrative | 165 | |||||||||||||||||||||||

Advisor fees | 1,638 | |||||||||||||||||||||||

Company level expenses | 687 | |||||||||||||||||||||||

Acquisition expenses | 133 | |||||||||||||||||||||||

Depreciation and amortization | 6,564 | |||||||||||||||||||||||

Operating income | $ | 5,103 | ||||||||||||||||||||||

Other income and (expenses): | ||||||||||||||||||||||||

Interest expense | $ | (4,227 | ) | |||||||||||||||||||||

Equity in income of unconsolidated affiliate | 180 | |||||||||||||||||||||||

Gain on disposition of property and extinguishment of debt | 29,009 | |||||||||||||||||||||||

Total other income and (expenses) | $ | 24,962 | ||||||||||||||||||||||

Net income | $ | 30,065 | ||||||||||||||||||||||

16

NOTE 10—DISTRIBUTIONS PAYABLE

On March 8, 2016, our board of directors approved a gross dividend for the first quarter of 2016 of $0.12 per share to stockholders of record as of March 30, 2016. The dividend was paid on May 2, 2016. Class A, Class M, Class A-I, Class M-I and Class D stockholders received $0.12 per share, less applicable class-specific fees, if any.

NOTE 11— RECENTLY ISSUED ACCOUNTING PRONOUNCEMENTS

In May 2014, the FASB issued Accounting Standard Update 2014-09 Revenue from Contracts with Customers, that will use a five step model to recognize revenue from customer contracts in an effort to increase consistency and comparability throughout global capital markets and across industries. The model will identify the contract, identify any separate performance obligations in the contract, determine the transaction price, allocate the transaction price and recognize revenue when the performance obligation is satisfied. The new standard will replace most existing revenue recognition in GAAP when it becomes effective for us on January 1, 2018. We have not yet selected a transition method nor have we determined the effect of the standard on our ongoing financial reporting.

In January 2016, the FASB issued Accounting Standard Update 2016-01 Financial Instruments - Overall: Recognition and Measurement of Financial Assets and Financial Liabilities. The new standard requires equity investments (except those accounted for under the equity method of accounting, or those that result in consolidation of the investee) to be measured at fair value with changes in fair value recognized in net income, requires public business entities to use the exit price notion when measuring the fair value of financial instruments for disclosure purposes, requires separate presentation of financial assets and financial liabilities by measurement category and form of financial asset, and eliminates the requirement for public business entities to disclose the method(s) and significant assumptions used to estimate the fair value that is required to be disclosed for financial instruments measured at amortized cost. The standard will become effective for reporting periods beginning after December 15, 2017, with early adoption permitted. We are in the process of evaluating the impact of this new guidance.

In February 2016, the FASB issued Accounting Standard Update 2016-02 Leases (ASC 842), which sets out the principles for the recognition, measurement, presentation and disclosure of leases for both parties to a contract (i.e. lessees and lessors). The new standard requires lessors to account for leases using an approach that is substantially equivalent to existing guidance for sales-type leases, direct financing leases and operating leases. The new standard requires lessees to apply a dual approach, classifying leases as either finance or operating leases based on the principle of whether or not the lease is effectively a financed purchase by the lessee. This classification will determine whether lease expense is recognized based on an effective interest method or on a straight line basis over the term of the lease. A lessee is also required to record a right-of-use asset and a lease liability for all leases with a term of greater than 12 months regardless of their classification. Leases with a term of 12 months or less will be accounted for similar to existing guidance for operating leases today. The update is expected to impact our consolidated financial statements as we have certain operating and land lease arrangements for which we are the lessee. ASC 842 supersedes the previous leases standard, ASC 840 Leases. The standard is effective on January 1, 2019, with early adoption permitted. We are in the process of evaluating the impact of this new guidance.

NOTE 12—SUBSEQUENT EVENTS

On April 1, 2016, we acquired San Juan Medical Center, a newly constructed 40,000 square foot medical office building located in San Juan Capistrano, California, for approximately $26,390. The property is 100% leased to four tenants. The acquisition was funded with cash on hand.

On April 11, 2016, we acquired Tampa Distribution Center, a 386,000 square foot industrial building located in Tampa, Florida, for approximately $28,240. The property is 100% leased to two tenants. The acquisition was funded with cash on hand.

On May 10, 2016, our board of directors approved a gross dividend for the second quarter of 2016 of $0.12 per share to stockholders of record as of June 29, 2016. The dividend will be paid on or around August 1, 2016. Class A, Class M, Class A-I, Class M-I and Class D stockholders will receive $0.12 per share, less applicable class-specific fees, if any.

On May 10, 2016, we renewed the Advisory Agreement with our Advisor for one year. The term of the Advisory Agreement is for one year from its effective date of June 5, 2016, subject to renewals by our board of directors for an unlimited number of successive one-year periods. The Advisory Agreement may be terminated without penalty (1) immediately by us for “cause,” upon the bankruptcy of our Advisor or upon a material breach of the agreement by our Advisor, (2) upon 60 days’ written notice by us without cause upon the vote of a majority of our independent directors, or (3) upon 60 days’ written notice by our Advisor. “Cause” is defined in the Advisory Agreement to mean fraud, criminal conduct, willful misconduct or willful or negligent breach of fiduciary duty by our Advisor in connection with performing its duties.

* * * * * *

17

Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

$ in thousands, except per share amounts

Cautionary Note Regarding Forward-Looking Statements

This Quarterly Report on Form 10-Q may contain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), regarding, among other things, our plans, strategies and prospects, both business and financial. Forward-looking statements include, but are not limited to, statements that represent our beliefs concerning future operations, strategies, financial results or other developments. Forward-looking statements can be identified by the use of forward-looking terminology such as, but not limited to, “may,” “should,” “expect,” “anticipate,” “estimate,” “would be,” “believe,” or “continue” or the negative or other variations of comparable terminology. Because these forward-looking statements are based on estimates and assumptions that are subject to significant business, economic and competitive uncertainties, many of which are beyond our control or are subject to change, actual results could be materially different. Although we believe that our plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, we cannot assure you that we will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date this Form 10-Q is filed with the SEC. Except as required by law, we do not undertake to update or revise any forward-looking statements contained in this Form 10-Q. Important factors that could cause actual results to differ materially from the forward-looking statements are disclosed in “Item 1A. Risk Factors,” “Item 1. Business” and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained in our 2015 Form 10-K and our periodic reports filed with the SEC.

Management Overview

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) is intended to help the reader understand our results of operations and financial condition. This MD&A is provided as a supplement to, and should be read in conjunction with, our consolidated financial statements and the accompanying notes to the consolidated financial statements appearing elsewhere in this Form 10-Q. All references to numbered Notes are to specific notes to our Consolidated Financial Statements beginning on page 7 of this Form 10-Q, and the descriptions referred to are incorporated into the applicable portion of this section by reference. References to “base rent” in this Form 10-Q refer to cash payments made under the relevant lease(s), excluding real estate taxes and certain property operating expenses that are paid by us and are recoverable under the relevant lease(s) and exclude adjustments for straight-line rent revenue and above- and below-market lease amortization.

The discussions surrounding our Consolidated Properties refer to our wholly or majority owned and controlled properties, which as of March 31, 2016, were comprised of:

Apartment

• | Station Nine Apartments, |

• | The Edge at Lafayette, |

• | Campus Lodge Tampa, |

• | Townlake of Coppell (acquired in 2015) and |

• | AQ Rittenhouse (acquired in 2015). |

Industrial

• | Kendall Distribution Center, |

• | Norfleet Distribution Center, |

• | Joliet Distribution Center, |

• | Suwanee Distribution Center, |

• | South Seattle Distribution Center, |

• | Grand Prairie Distribution Center, |

• | Charlotte Distribution Center, |

• | DFW Distribution Center (acquired in 2015) and |

• | O'Hare Industrial Portfolio (acquired in 2015). |

18

Office

• | Monument IV at Worldgate, |

• | 111 Sutter Street, |

• | 14600 Sherman Way, |

• | 14624 Sherman Way, |

• | Railway Street Corporate Centre and |

• | 140 Park Avenue (acquired in 2015). |

Retail

• | The District at Howell Mill, |

• | Grand Lakes Marketplace, |

• | Oak Grove Plaza, |

• | Rancho Temecula Town Center, |

• | Skokie Commons (acquired in 2015), |

• | Whitestone Market (acquired in 2015) and |

• | Maui Mall (acquired in 2015). |

Other

• | South Beach Parking Garage. |

Sold Properties

• | Cabana Beach San Marcos (sold in 2015), |

• | Cabana Beach Gainesville (sold in 2015), |

• | Campus Lodge Athens (sold in 2015), |

• | Campus Lodge Columbia (sold in 2015) and |

• | 36 Research Park Drive (sold in 2016). |

Discussions surrounding our Unconsolidated Properties refer to properties owned through joint venture arrangements or condominium interests, which were comprised of the Chicago Parking Garage and the NYC Retail Portfolio as of March 31, 2016. Our investment in the NYC Retail Portfolio was acquired on December 8, 2015. We elected the fair value option to account for this investment.

Our primary business is the ownership and management of a diversified portfolio of apartment, industrial, office, retail and other properties primarily located in the United States. It is expected that over time our real estate portfolio will be further diversified on a global basis and will be complemented by investments in real estate-related assets.

We are managed by our Advisor, LaSalle Investment Management, Inc., a subsidiary of our Sponsor, Jones Lang LaSalle Incorporated (NYSE: JLL), a leading global financial and professional services firm that specializes in commercial real estate. We hire property management and leasing companies to provide the on-site, day-to-day management and leasing services for our properties. When selecting a property management or leasing company for one of our properties, we look for service providers that have a strong local market or industry presence, create portfolio efficiencies, have the ability to develop new business for us and will provide a strong internal control environment that will comply with our Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley”) internal control requirements. We currently use a mix of property management and leasing service providers that include large national real estate service firms, including an affiliate of our Advisor and smaller local firms.

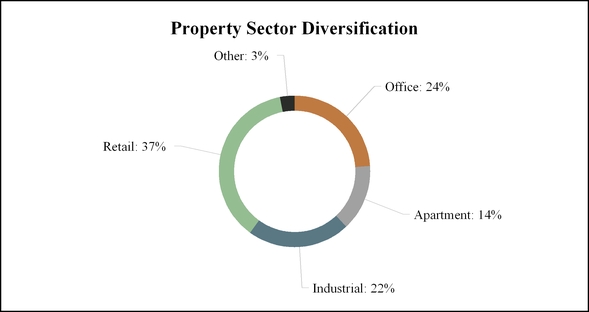

We seek to minimize risk and maintain stability of income and principal value through broad diversification across property sectors and geographic markets and by balancing tenant lease expirations and debt maturities across the real estate portfolio. Our diversification goals also take into account investing in sectors or regions we believe will create returns consistent with our investment objectives. Under normal conditions, we intend to pursue investments principally in well-located, well-leased properties within the apartment, industrial, office, retail and other sectors. We expect to actively manage the mix of properties and markets over time in response to changing operating fundamentals within each property sector and to changing economies and real estate markets in the geographic areas considered for investment. When consistent with our investment objectives, we also seek to maximize the tax efficiency of our investments through like-kind exchanges and other tax planning strategies.

19

The following charts summarize our portfolio diversification by property sector and geographic region based upon the fair value of our properties. These tables provide examples of how our Advisor evaluates our real estate portfolio when making investment decisions.

Estimated Percent of Fair Value as of March 31, 2016:

20

Seasonality

For our two student-oriented apartments, the majority of our leases commence mid-August and terminate the last day of July. These dates generally coincide with the commencement of the universities’ fall academic term and the completion of the subsequent summer school session. In certain cases we enter into leases for less than the full academic year, including nine-month or shorter-term leases. As a result, cash flows may be reduced during the summer months at properties having lease terms shorter than 12 months. The annual releasing cycle results in significant turnover in the tenant population from year to year. Accordingly, certain property revenues and operating expenses tend to be seasonal in nature, and therefore not incurred ratably over the course of the year. Prior to the commencement of each new lease period, mostly during the first two weeks of August, we prepare the units for new incoming tenants. Other than revenue generated by in-place leases for returning tenants, we do not generally recognize lease revenue during this period, referred to as the “Turn,” as we have no leases in place. In addition, during the Turn we incur significant expenses making our units ready for occupancy, which we recognize immediately. This lease Turn period results in seasonality impacts on our operating results during the second and third quarter of each year.

With the exception of our student-oriented apartments described above, our investments are not materially impacted by seasonality, despite certain of our retail tenants being impacted by seasonality. Percentage rents (rents computed as a percentage of tenant sales) that we earn from investments in retail properties may, in the future, be impacted by seasonality.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires us to make estimates and assumptions. These estimates and assumptions impact the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. For example, significant estimates and assumptions have been made with respect to the useful lives of assets, recoverable amounts of receivables, fair value of derivatives and real estate assets, initial valuations and related amortization periods of deferred costs and intangibles, particularly with respect to property acquisitions. Actual results could differ from those estimates.

Critical Accounting Policies

This MD&A is based upon our consolidated financial statements, which have been prepared in accordance with GAAP. The preparation of these consolidated financial statements requires management to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses. Management bases its estimates on historical experience and assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions. We believe there have been no significant changes during the three months ended March 31, 2016 to the items that we disclosed as our critical accounting policies and estimates under “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in our 2015 Form 10-K.

Initial Valuations and Estimated Useful Lives or Amortization Periods for Real Estate Investments and Intangibles

These estimates are particularly important as they are used for the allocation of purchase price between depreciable and non-depreciable real estate and other identifiable intangibles, including above, below and at-market leases. As a result, the impact of these estimates on our operations could be substantial. Significant differences in annual depreciation or amortization expense may result from the differing useful life or amortization periods related to such purchased assets and liabilities.

Impairment of Long-Lived Assets

Our estimate of the expected future cash flows used in testing for impairment is highly subjective and based on, among other things, our estimates regarding future market conditions, rental rates, occupancy levels, costs of tenant improvements, leasing commissions and other tenant concessions, assumptions regarding the residual value of our properties at the end of our anticipated holding period, discount rates and the length of our anticipated holding period. These assumptions could differ materially from actual results. If our strategy changes or if market conditions otherwise dictate a reduction in the holding period and an earlier sale date, an impairment loss could be recognized and such loss could be material.

21

Dealer Manager Fee Accounting

No authoritative GAAP guidance specifically addresses the accounting treatment for dealer manager fees. Dealer manager fees are accrued daily into our NAV based on a specified percentage for each publicly offered share class multiplied by the NAV of that share class at the end of each day. There are two acceptable accounting practices used by the industry to account for dealer manager fees in GAAP-based financial statements. The first practice involves accruing the liability for the dealer manager fees on a daily basis as offering costs, which are recorded as a reduction of capital in excess of par value. The second practice involves accruing all future dealer manager fees on the day the share of stock is sold, up to the maximum ten percent as allowed under applicable regulations. We have selected the first practice as our accounting policy. We selected the policy of accruing dealer manager fees on a daily basis because we are obligated to pay the fee every day that a share of common stock is outstanding until it has been repurchased or we have reached the ten percent limit. We believe dealer manager fees are offering costs and recorded as a reduction of capital in excess of par value as there are limited ongoing services required to be performed in order for the dealer manager fee to be paid to our Dealer Manager. In addition, the Dealer Manager reallows a majority of the dealer manager fee to participating broker-dealers who receive the fee as compensation for providing services to the stockholders. For common stock sold in the Initial Public Offering and First Extended Public Offering through March 31, 2016, we estimate we will pay out an additional $48,210 in offering costs, primarily in the form of dealer manager fees, which are not reflected on our Consolidated Balance Sheet as of March 31, 2016. We estimate these additional offering costs to be paid out over the next ten years.

22

Properties

Properties owned at March 31, 2016 are as follows:

Percentage Leased as of March 31, 2016 | ||||||||||

Property Name | Location | Acquisition Date | Ownership % | Net Rentable Square Feet | ||||||

Consolidated Properties: | ||||||||||

Apartment Segment: | ||||||||||

Station Nine Apartments | Durham, NC | April 16, 2007 | 100% | 312,000 | 95% | |||||

Townlake of Coppell (1) | Coppell, TX | May 22, 2015 | 90 | 351,000 | 93 | |||||

AQ Rittenhouse | Philadelphia, PA | July 30, 2015 | 100 | 92,000 | 84 | |||||

Student-oriented Apartment Communities: | ||||||||||

The Edge at Lafayette (1) | Lafayette, LA | January 15, 2008 | 78 | 207,000 | 97 | |||||

Campus Lodge Tampa (1) | Tampa, FL | February 29, 2008 | 78 | 477,000 | 99 | |||||

Industrial Segment: | ||||||||||

Kendall Distribution Center | Atlanta, GA | June 30, 2005 | 100 | 409,000 | 100 | |||||

Norfleet Distribution Center | Kansas City, MO | February 27, 2007 | 100 | 702,000 | 100 | |||||

Joliet Distribution Center | Joliet, IL | June 26, 2013 | 100 | 442,000 | 100 | |||||

Suwanee Distribution Center | Suwanee, GA | June 28, 2013 | 100 | 559,000 | 100 | |||||

South Seattle Distribution Center | ||||||||||

3800 1st Avenue | Seattle, WA | December 18, 2013 | 100 | 162,000 | 100 | |||||

3844 1st Avenue | Seattle, WA | December 18, 2013 | 100 | 101,000 | 100 | |||||

3601 2nd Avenue | Seattle, WA | December 18, 2013 | 100 | 60,000 | 100 | |||||

Grand Prairie Distribution Center | Grand Prairie, TX | January 22, 2014 | 100 | 277,000 | 100 | |||||

Charlotte Distribution Center | Charlotte, NC | June 27, 2014 | 100 | 347,000 | 100 | |||||

DFW Distribution Center | ||||||||||

4050 Corporate Drive | Grapevine, TX | April 15, 2015 | 100 | 441,000 | 100 | |||||

4055 Corporate Drive | Grapevine, TX | April 15, 2015 | 100 | 202,000 | 100 | |||||

O’Hare Industrial Portfolio | ||||||||||

200 Lewis | Wood Dale, IL | September 30, 2015 | 100 | 31,000 | 100 | |||||

1225 Michael Drive | Wood Dale, IL | September 30, 2015 | 100 | 109,000 | 100 | |||||

1300 Michael Drive | Wood Dale, IL | September 30, 2015 | 100 | 71,000 | 100 | |||||

1301 Mittel Drive | Wood Dale, IL | September 30, 2015 | 100 | 53,000 | 100 | |||||

1350 Michael Drive | Wood Dale, IL | September 30, 2015 | 100 | 56,000 | 100 | |||||

2501 Allan Drive | Elk Grove, IL | September 30, 2015 | 100 | 198,000 | 74 | |||||

2601 Allan Drive | Elk Grove, IL | September 30, 2015 | 100 | 124,000 | 100 | |||||

Office Segment: | ||||||||||

Monument IV at Worldgate | Herndon, VA | August 27, 2004 | 100 | 228,000 | 100 | |||||

111 Sutter Street | San Francisco, CA | March 29, 2005 | 100 | 286,000 | 85 | |||||

14600 Sherman Way | Van Nuys, CA | December 21, 2005 | 100 | 50,000 | 94 | |||||

14624 Sherman Way | Van Nuys, CA | December 21, 2005 | 100 | 53,000 | 89 | |||||

Railway Street Corporate Centre | Calgary, Canada | August 30, 2007 | 100 | 135,000 | 74 | |||||

140 Park Avenue | Florham Park, NJ | December 21, 2015 | 100 | 100,000 | 100 | |||||

Retail Segment: | ||||||||||

The District at Howell Mill (1) | Atlanta, GA | June 15, 2007 | 88 | 306,000 | 97 | |||||

Grand Lakes Marketplace (1) | Katy, TX | September 17, 2013 | 90 | 131,000 | 100 | |||||

Oak Grove Plaza | Sachse, TX | January 17, 2014 | 100 | 120,000 | 93 | |||||

Rancho Temecula Town Center | Temecula, CA | June 16, 2014 | 100 | 165,000 | 90 | |||||

Skokie Commons | Skokie, IL | May 15, 2015 | 100 | 97,000 | 97 | |||||

Whitestone Market | Austin, TX | September 30, 2015 | 100 | 145,000 | 100 | |||||

Maui Mall | Kahului, HI | December 22, 2015 | 100 | 235,000 | 92 | |||||

23

Other Segment: | ||||||||||

South Beach Parking Garage (2) | Miami, FL | January 28, 2014 | 100 | 130,000 | N/A | |||||

Unconsolidated Properties: | ||||||||||

Chicago Parking Garage (3) | Chicago, IL | December 23, 2014 | 100 | 167,000 | N/A | |||||

NYC Retail Portfolio (4) | NY/NJ | December 8, 2015 | 14 | 2,700,000 | 98 | |||||

(1) | We own an interest in the joint venture that owns a fee interest in this property. |

(2) | The parking garage contains 343 stalls. This property is owned subject to a ground lease. |

(3) | We own a condominium interest in the building that contains a 366 stall parking garage. |

(4) | We own an approximate 14% interest in a portfolio of 15 urban infill retail properties located in the greater New York City area. |

Operating Statistics

We generally hold investments in properties with high occupancy rates leased to quality tenants under long-term, non-cancelable leases. We believe these leases are beneficial to achieving our investment objectives. The following table shows our operating statistics by property type for our consolidated properties as of March 31, 2016:

Number of Properties | Total Area (Sq Ft) | % of Total Area | Occupancy % | Average Minimum Base Rent per Occupied Sq Ft (1) | ||||||||||||

Apartment | 5 | 1,438,000 | 18 | % | 95 | % | $ | 16.60 | ||||||||

Industrial | 18 | 4,345,000 | 54 | 99 | 4.29 | |||||||||||

Office | 6 | 852,000 | 11 | 90 | 34.50 | |||||||||||

Retail | 7 | 1,197,000 | 15 | 95 | 19.18 | |||||||||||

Other | 1 | 130,000 | 2 | N/A | N/A | |||||||||||

Total | 37 | 7,962,000 | 100 | % | 97 | % | $ | 11.54 | ||||||||

(1) | Amount calculated as in-place minimum base rent for all occupied space at March 31, 2016 and excludes any straight line rents, tenant recoveries and percentage rent revenues. |

As of March 31, 2016, our average effective annual rent per square foot, calculated as average minimum base rent per occupied square foot less tenant concessions and allowances, was $10.83 for our consolidated properties.

Recent Events and Outlook