Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - EZCORP INC | a2016-q210qxex312_3312016.htm |

| EX-31.1 - EXHIBIT 31.1 - EZCORP INC | a2016-q210qxex311_3312016.htm |

| EX-32.1 - EXHIBIT 32.1 - EZCORP INC | a2016-q210qxex321_3312016.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2016

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 0-19424

EZCORP, INC.

(Exact name of registrant as specified in its charter)

Delaware | 74-2540145 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

2500 Bee Cave Road, Rollingwood, Texas | 78746 |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (512) 314-3400

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | x |

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

APPLICABLE ONLY TO CORPORATE ISSUERS:

The only class of voting securities of the registrant issued and outstanding is the Class B Voting Common Stock, par value $.01 per share, all of which is owned by an affiliate of the registrant. There is no trading market for the Class B Voting Common Stock.

As of May 2, 2016, 50,976,110 shares of the registrant’s Class A Non-voting Common Stock, par value $.01 per share, and 2,970,171 shares of the registrant’s Class B Voting Common Stock, par value $.01 per share, were outstanding.

EZCORP, Inc.

INDEX TO FORM 10-Q

PART I — FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

EZCORP, Inc. CONDENSED CONSOLIDATED BALANCE SHEETS (in thousands, except share and per share amounts) | |||||||||||

March 31, 2016 | March 31, 2015 | September 30, 2015 | |||||||||

(Unaudited) | |||||||||||

Assets: | |||||||||||

Current assets: | |||||||||||

Cash and cash equivalents | $ | 75,336 | $ | 138,173 | $ | 59,124 | |||||

Restricted cash | 13,817 | 47,909 | 15,137 | ||||||||

Pawn loans | 140,195 | 127,929 | 159,964 | ||||||||

Consumer loans, net | 26,362 | 55,529 | 36,533 | ||||||||

Pawn service charges receivable, net | 27,626 | 24,909 | 30,852 | ||||||||

Consumer loan fees and interest receivable, net | 13,226 | 13,063 | 19,802 | ||||||||

Inventory, net | 126,446 | 116,144 | 124,084 | ||||||||

Income taxes receivable | 557 | 52,234 | 45,175 | ||||||||

Prepaid expenses and other current assets | 32,505 | 32,383 | 21,076 | ||||||||

Total current assets | 456,070 | 608,273 | 511,747 | ||||||||

Investment in unconsolidated affiliate | 56,677 | 94,510 | 56,182 | ||||||||

Property and equipment, net | 64,962 | 102,252 | 75,594 | ||||||||

Restricted cash, non-current | 2,308 | 2,880 | 2,883 | ||||||||

Goodwill | 254,782 | 344,931 | 327,460 | ||||||||

Intangible assets, net | 40,197 | 49,674 | 41,263 | ||||||||

Non-current consumer loans, net | 62,673 | 79,860 | 75,824 | ||||||||

Deferred tax asset, net | 77,125 | 35,213 | 69,121 | ||||||||

Other assets, net | 19,655 | 60,041 | 42,985 | ||||||||

Total assets (1)(3) | $ | 1,034,449 | $ | 1,377,634 | $ | 1,203,059 | |||||

Liabilities, temporary equity and equity: | |||||||||||

Current liabilities: | |||||||||||

Current maturities of long-term debt | $ | 82,174 | $ | 71,471 | $ | 74,345 | |||||

Current capital lease obligations | — | 93 | — | ||||||||

Accounts payable and other accrued expenses | 85,836 | 89,711 | 107,871 | ||||||||

Other current liabilities | 2,595 | 6,230 | 15,384 | ||||||||

Customer layaway deposits | 11,370 | 10,484 | 10,470 | ||||||||

Income taxes payable | 6,632 | — | — | ||||||||

Total current liabilities | 188,607 | 177,989 | 208,070 | ||||||||

Long-term debt, less current maturities, net | 252,808 | 344,960 | 297,166 | ||||||||

Deferred gains and other long-term liabilities | 2,751 | 7,673 | 6,157 | ||||||||

Total liabilities (2)(4) | 444,166 | 530,622 | 511,393 | ||||||||

Commitments and contingencies (Note 11) | |||||||||||

Temporary equity: | |||||||||||

Class A Non-voting Common Stock, subject to possible redemption at $10.06 per share; none as of March 31, 2016 and 1,168,456 shares issued and outstanding at redemption value as of March 31, 2015 and September 30, 2015 | — | 11,696 | 11,696 | ||||||||

Redeemable noncontrolling interest | (1,229 | ) | 16,827 | 3,235 | |||||||

Total temporary equity | (1,229 | ) | 28,523 | 14,931 | |||||||

Stockholders’ equity: | |||||||||||

Class A Non-voting Common Stock, par value $.01 per share; shares authorized: 100 million as of March 31, 2016 and 2015 and September 30, 2015; issued and outstanding: 50,989,430 as of March 31, 2016; 50,681,477 as of March 31, 2015; and 50,726,289 as of September 30, 2015 | 510 | 506 | 507 | ||||||||

Class B Voting Common Stock, convertible, par value $.01 per share; 3 million shares authorized; issued and outstanding: 2,970,171 | 30 | 30 | 30 | ||||||||

Additional paid-in capital | 312,569 | 329,973 | 307,080 | ||||||||

Retained earnings | 341,538 | 522,541 | 423,137 | ||||||||

Accumulated other comprehensive loss | (62,805 | ) | (34,561 | ) | (54,019 | ) | |||||

EZCORP, Inc. stockholders’ equity | 591,842 | 818,489 | 676,735 | ||||||||

Noncontrolling interest | (330 | ) | — | — | |||||||

Total equity | 591,512 | 818,489 | 676,735 | ||||||||

Total liabilities, temporary equity and equity | $ | 1,034,449 | $ | 1,377,634 | $ | 1,203,059 | |||||

See accompanying notes to unaudited interim condensed consolidated financial statements.

1

Assets and Liabilities of Consolidated Variable Interest Entities (See Note 16)

(1) Our consolidated assets as of March 31, 2016 and 2015 and September 30, 2015 include the following assets of our consolidated variable interest entities:

March 31, 2016 | March 31, 2015 | September 30, 2015 | |||||||||

(Unaudited) | |||||||||||

(in thousands) | |||||||||||

Restricted cash | $ | 397 | $ | 2,084 | $ | 1,361 | |||||

Consumer loans, net | 6,607 | 14,826 | 5,846 | ||||||||

Consumer loan fees and interest receivable, net | 3,559 | 3,577 | 6,399 | ||||||||

Non-current consumer loans, net | 17,245 | 32,511 | 27,162 | ||||||||

Total assets | $ | 27,808 | $ | 52,998 | $ | 40,768 | |||||

(2) Our consolidated liabilities as of March 31, 2016 and 2015 and September 30, 2015 include the following liabilities of our consolidated variable interest entities:

March 31, 2016 | March 31, 2015 | September 30, 2015 | ||||||||||

(Unaudited) | ||||||||||||

(in thousands) | ||||||||||||

Accounts payable and other accrued expenses | $ | 6,065 | $ | 3,153 | $ | 4,313 | ||||||

Current maturities of long-term debt | 37,177 | 48,246 | 42,017 | * | ||||||||

Long-term debt, less current maturities | 13,704 | 51,888 | 31,247 | * | ||||||||

Total liabilities | $ | 56,946 | $ | 103,287 | $ | 77,577 | ||||||

* | This amount has been revised from the originally filed amount due to an immaterial reclassification error between current and non-current amounts as of September 30, 2015. The consolidated amounts previously reported in the balance sheet were correct. |

Assets and Liabilities of Grupo Finmart Securitization Trust (See Note 16)

(3) Our consolidated assets as of March 31, 2016 and 2015 and September 30, 2015 include the following assets of Grupo Finmart's securitization trust that can only be used to settle its liabilities:

March 31, 2016 | March 31, 2015 | September 30, 2015 | |||||||||

(Unaudited) | |||||||||||

(in thousands) | |||||||||||

Restricted cash | $ | 4,869 | $ | 21,835 | $ | 12,033 | |||||

Consumer loans* | 39,453 | 34,803 | 36,845 | ||||||||

Consumer loan fees and interest receivable, net | 7,424 | 5,182 | 6,067 | ||||||||

Restricted cash, non-current | 196 | 119 | 197 | ||||||||

Total assets | $ | 51,942 | $ | 61,939 | $ | 55,142 | |||||

* | These amounts include the current and non-current portions of active consumer loans considered to be performing under the terms of the Grupo Finmart securitization trust. These balances, which represent the total collateral that can be used to settle the liabilities of the securitization trust, exclude loan loss allowances as described in Note 13, and are presented on a net basis in the condensed consolidated balance sheets including allowances. |

(4) Our consolidated liabilities as of March 31, 2016 and 2015 and September 30, 2015 include the following liabilities for which the creditors of Grupo Finmart's securitization trust do not have recourse to the general credit of EZCORP, Inc.:

March 31, 2016 | March 31, 2015 | September 30, 2015 | |||||||||

(Unaudited) | |||||||||||

(in thousands) | |||||||||||

Long-term debt, less current maturities | $ | 33,613 | $ | 44,837 | $ | 40,493 | |||||

See accompanying notes to unaudited interim condensed consolidated financial statements.

2

EZCORP, Inc. CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS | |||||||||||||||

Three Months Ended March 31, | Six Months Ended March 31, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

(Unaudited) | |||||||||||||||

(in thousands, except per share amounts) | |||||||||||||||

Revenues: | |||||||||||||||

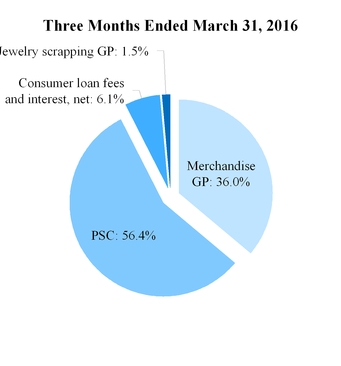

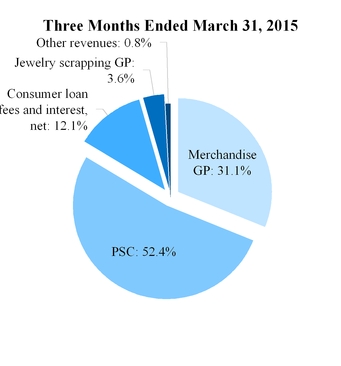

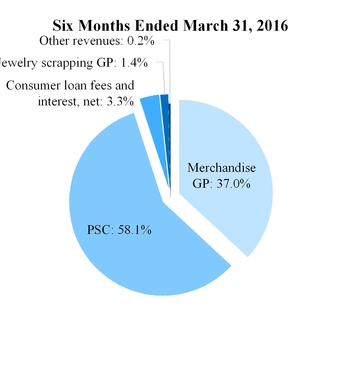

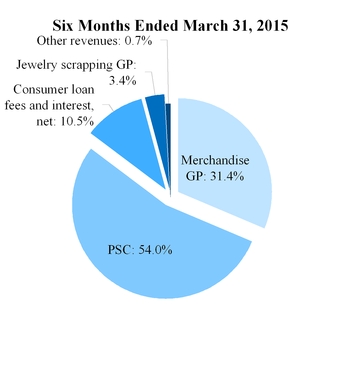

Merchandise sales | $ | 109,343 | $ | 107,852 | $ | 217,927 | $ | 217,491 | |||||||

Jewelry scrapping sales | 12,780 | 18,399 | 22,401 | 36,933 | |||||||||||

Pawn service charges | 64,130 | 59,470 | 130,724 | 124,397 | |||||||||||

Consumer loan fees and interest | 15,616 | 18,544 | 28,804 | 37,515 | |||||||||||

Other revenues | 30 | 910 | 497 | 1,565 | |||||||||||

Total revenues | 201,899 | 205,175 | 400,353 | 417,901 | |||||||||||

Merchandise cost of goods sold | 68,332 | 72,492 | 134,591 | 144,970 | |||||||||||

Jewelry scrapping cost of goods sold | 11,085 | 14,354 | 19,161 | 29,029 | |||||||||||

Consumer loan bad debt | 8,683 | 4,761 | 21,286 | 13,276 | |||||||||||

Net revenues | 113,799 | 113,568 | 225,315 | 230,626 | |||||||||||

Operating expenses: | |||||||||||||||

Operations | 80,282 | 77,190 | 165,888 | 157,277 | |||||||||||

Administrative | 15,621 | 14,800 | 35,604 | 27,352 | |||||||||||

Depreciation and amortization | 7,082 | 8,095 | 15,141 | 16,103 | |||||||||||

Loss on sale or disposal of assets | 649 | 387 | 682 | 643 | |||||||||||

Restructuring | 218 | 704 | 1,910 | 726 | |||||||||||

Total operating expenses | 103,852 | 101,176 | 219,225 | 202,101 | |||||||||||

Operating income | 9,947 | 12,392 | 6,090 | 28,525 | |||||||||||

Interest expense | 8,449 | 11,296 | 17,641 | 23,330 | |||||||||||

Interest income | (127 | ) | (512 | ) | (267 | ) | (1,043 | ) | |||||||

Equity in net (income) loss of unconsolidated affiliate | (1,877 | ) | 3,678 | (3,932 | ) | 1,484 | |||||||||

Impairment of goodwill | 73,921 | — | 73,921 | — | |||||||||||

Other expense | 89 | 1,862 | 959 | 2,621 | |||||||||||

(Loss) income from continuing operations before income taxes | (70,508 | ) | (3,932 | ) | (82,232 | ) | 2,133 | ||||||||

Income tax expense | 6,189 | 362 | 2,493 | 3,626 | |||||||||||

Loss from continuing operations, net of tax | (76,697 | ) | (4,294 | ) | (84,725 | ) | (1,493 | ) | |||||||

(Loss) income from discontinued operations, net of tax | (1,094 | ) | 4,731 | (1,332 | ) | 11,608 | |||||||||

Net (loss) income | (77,791 | ) | 437 | (86,057 | ) | 10,115 | |||||||||

Net loss from continuing operations attributable to noncontrolling interest | (3,666 | ) | (906 | ) | (4,458 | ) | (2,840 | ) | |||||||

Net (loss) income attributable to EZCORP, Inc. | $ | (74,125 | ) | $ | 1,343 | $ | (81,599 | ) | $ | 12,955 | |||||

Basic (loss) earnings per share attributable to EZCORP, Inc.: | |||||||||||||||

Continuing operations | $ | (1.33 | ) | $ | (0.06 | ) | $ | (1.46 | ) | $ | 0.02 | ||||

Discontinued operations | (0.02 | ) | 0.09 | (0.02 | ) | 0.22 | |||||||||

Basic (loss) earnings per share | $ | (1.35 | ) | $ | 0.03 | $ | (1.48 | ) | $ | 0.24 | |||||

Diluted (loss) earnings per share attributable to EZCORP, Inc.: | |||||||||||||||

Continuing operations | $ | (1.33 | ) | $ | (0.06 | ) | $ | (1.46 | ) | $ | 0.02 | ||||

Discontinued operations | (0.02 | ) | 0.09 | (0.02 | ) | 0.22 | |||||||||

Diluted (loss) earnings per share | $ | (1.35 | ) | $ | 0.03 | $ | (1.48 | ) | $ | 0.24 | |||||

Weighted-average shares outstanding: | |||||||||||||||

Basic | 54,843 | 54,184 | 54,869 | 53,915 | |||||||||||

Diluted | 54,843 | 54,184 | 54,869 | 53,972 | |||||||||||

Net (loss) income from continuing operations attributable to EZCORP, Inc. | $ | (73,031 | ) | $ | (3,388 | ) | $ | (80,267 | ) | $ | 1,347 | ||||

Net (loss) income from discontinued operations attributable to EZCORP, Inc. | (1,094 | ) | 4,731 | (1,332 | ) | 11,608 | |||||||||

Net (loss) income attributable to EZCORP, Inc. | $ | (74,125 | ) | $ | 1,343 | $ | (81,599 | ) | $ | 12,955 | |||||

See accompanying notes to unaudited interim condensed consolidated financial statements.

3

EZCORP, Inc. CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS | |||||||||||||||

Three Months Ended March 31, | Six Months Ended March 31, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

(Unaudited) | |||||||||||||||

(in thousands) | |||||||||||||||

Net (loss) income | $ | (77,791 | ) | $ | 437 | $ | (86,057 | ) | $ | 10,115 | |||||

Other comprehensive income (loss): | |||||||||||||||

Foreign currency translation loss, net of income tax (expense) benefit for our investment in unconsolidated affiliate of ($752) and $1,851 for the three and six-months ended March 31, 2016, respectively, and ($199) and $220 for the three and six-months ended March 31, 2015, respectively | (2,204 | ) | (6,897 | ) | (9,144 | ) | (27,999 | ) | |||||||

Cash flow hedges: | |||||||||||||||

Amounts reclassified from accumulated other comprehensive loss | — | 35 | 22 | 387 | |||||||||||

Other comprehensive loss, net of tax | (2,204 | ) | (6,862 | ) | (9,122 | ) | (27,612 | ) | |||||||

Comprehensive loss | $ | (79,995 | ) | $ | (6,425 | ) | $ | (95,179 | ) | $ | (17,497 | ) | |||

Attributable to noncontrolling interest: | |||||||||||||||

Net loss | (3,666 | ) | (906 | ) | (4,458 | ) | (2,840 | ) | |||||||

Foreign currency translation loss | (272 | ) | (825 | ) | (337 | ) | (3,227 | ) | |||||||

Amounts reclassified from accumulated other comprehensive loss | — | 8 | 1 | 94 | |||||||||||

Comprehensive loss attributable to noncontrolling interest | (3,938 | ) | (1,723 | ) | (4,794 | ) | (5,973 | ) | |||||||

Comprehensive loss attributable to EZCORP, Inc. | $ | (76,057 | ) | $ | (4,702 | ) | $ | (90,385 | ) | $ | (11,524 | ) | |||

See accompanying notes to unaudited interim condensed consolidated financial statements.

4

EZCORP, Inc. CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS | |||||||

Six Months Ended March 31, | |||||||

2016 | 2015 | ||||||

(Unaudited) | |||||||

(in thousands) | |||||||

Operating activities: | |||||||

Net (loss) income | $ | (86,057 | ) | $ | 10,115 | ||

Adjustments to reconcile net (loss) income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 15,141 | 18,097 | |||||

Amortization of debt discount and consumer loan premium, net | 4,357 | 4,229 | |||||

Consumer loan loss provision | 18,662 | 14,023 | |||||

Deferred income taxes | (8,004 | ) | (5,536 | ) | |||

Impairment of goodwill | 73,921 | — | |||||

Amortization of deferred financing costs | 1,575 | 2,625 | |||||

Amortization of prepaid commissions | 7,754 | 6,200 | |||||

Other adjustments | (2,149 | ) | 380 | ||||

Loss on sale or disposal of assets | 682 | 950 | |||||

Stock compensation expense (benefit) | 2,149 | (1,928 | ) | ||||

(Income) loss from investment in unconsolidated affiliate | (3,932 | ) | 1,484 | ||||

Changes in operating assets and liabilities, net of business acquisitions: | |||||||

Service charges and fees receivable | 10,140 | 2,542 | |||||

Inventory | (993 | ) | 2,499 | ||||

Prepaid expenses, other current assets and other assets | (5,935 | ) | (16,949 | ) | |||

Accounts payable, other accrued expenses, deferred gains and other long-term liabilities | (12,112 | ) | (5,925 | ) | |||

Customer layaway deposits | 851 | 1,947 | |||||

Restricted cash | (4,860 | ) | (835 | ) | |||

Income taxes receivable | 51,250 | 4,427 | |||||

Payments of restructuring charges | (6,701 | ) | (2,962 | ) | |||

Dividends from unconsolidated affiliate | — | 2,407 | |||||

Net cash provided by operating activities | 55,739 | 37,790 | |||||

Investing activities: | |||||||

Loans made | (323,980 | ) | (417,014 | ) | |||

Loans repaid | 225,138 | 334,888 | |||||

Recovery of pawn loan principal through sale of forfeited collateral | 121,830 | 138,885 | |||||

Additions to property and equipment | (2,976 | ) | (15,934 | ) | |||

Acquisitions, net of cash acquired | (6,000 | ) | (4,750 | ) | |||

Investment in unconsolidated affiliate | — | (12,140 | ) | ||||

Proceeds from sale of assets | 26 | — | |||||

Net cash provided by investing activities | 14,038 | 23,935 | |||||

Financing activities: | |||||||

Payout of deferred consideration | (14,875 | ) | (6,000 | ) | |||

Repurchase of redeemable common stock issued due to acquisitions | (11,750 | ) | — | ||||

Proceeds from settlement of forward currency contracts | 3,557 | 2,313 | |||||

Change in restricted cash | 6,519 | 11,476 | |||||

Proceeds from bank borrowings, net of debt issuance costs | 14,302 | 69,384 | |||||

Payments on bank borrowings and capital lease obligations | (47,698 | ) | (51,677 | ) | |||

Net cash (used in) provided by financing activities | (49,945 | ) | 25,496 | ||||

Effect of exchange rate changes on cash and cash equivalents | (3,620 | ) | (4,373 | ) | |||

Net increase in cash and cash equivalents | 16,212 | 82,848 | |||||

Cash and cash equivalents at beginning of period | 59,124 | 55,325 | |||||

Cash and cash equivalents at end of period | $ | 75,336 | $ | 138,173 | |||

5

EZCORP, Inc. CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS | |||||||

Non-cash investing and financing activities: | |||||||

Pawn loans forfeited and transferred to inventory | $ | 122,709 | $ | 119,028 | |||

Issuance of common stock, subject to possible redemption, due to acquisition | — | 11,696 | |||||

Deferred consideration | — | 250 | |||||

See accompanying notes to unaudited interim condensed consolidated financial statements.

6

EZCORP, Inc. CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY | ||||||||||||||||||||||

Common Stock | Additional Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Loss | EZCORP, Inc. Stockholders’ Equity | ||||||||||||||||||

Shares | Par Value | |||||||||||||||||||||

(Unaudited, except balances as of September 30, 2015 and 2014) | ||||||||||||||||||||||

(in thousands) | ||||||||||||||||||||||

Balances as of September 30, 2014 | 53,585 | $ | 536 | $ | 332,264 | $ | 509,586 | $ | (10,082 | ) | $ | 832,304 | ||||||||||

Issuance of common stock related to 401(k) match | 1 | — | — | — | — | — | ||||||||||||||||

Stock compensation | — | — | (1,928 | ) | — | — | (1,928 | ) | ||||||||||||||

Release of restricted stock | 66 | — | — | — | — | — | ||||||||||||||||

Excess tax benefit from stock compensation | — | — | (167 | ) | — | — | (167 | ) | ||||||||||||||

Taxes paid related to net share settlement of equity awards | — | — | (196 | ) | — | — | (196 | ) | ||||||||||||||

Amounts reclassified from accumulated other comprehensive loss | — | — | — | — | 293 | 293 | ||||||||||||||||

Foreign currency translation adjustment | — | — | — | — | (24,772 | ) | (24,772 | ) | ||||||||||||||

Net income attributable to EZCORP, Inc. | — | — | — | 12,955 | — | 12,955 | ||||||||||||||||

Balances as of March 31, 2015 | 53,652 | $ | 536 | $ | 329,973 | $ | 522,541 | $ | (34,561 | ) | $ | 818,489 | ||||||||||

Balances as of September 30, 2015 | 53,696 | $ | 537 | $ | 307,080 | $ | 423,137 | $ | (54,019 | ) | $ | 676,735 | ||||||||||

Stock compensation | — | — | 5,954 | — | — | 5,954 | ||||||||||||||||

Release of restricted stock | 264 | 3 | — | — | — | 3 | ||||||||||||||||

Excess tax benefit from stock compensation | — | — | (372 | ) | — | — | (372 | ) | ||||||||||||||

Taxes paid related to net share settlement of equity awards | — | — | (93 | ) | — | — | (93 | ) | ||||||||||||||

Amounts reclassified from accumulated other comprehensive loss | — | — | — | — | 21 | 21 | ||||||||||||||||

Foreign currency translation adjustment | — | — | — | — | (8,807 | ) | (8,807 | ) | ||||||||||||||

Net loss attributable to EZCORP, Inc. | — | — | — | (81,599 | ) | — | (81,599 | ) | ||||||||||||||

Balances as of March 31, 2016 | 53,960 | $ | 540 | $ | 312,569 | $ | 341,538 | $ | (62,805 | ) | $ | 591,842 | ||||||||||

See accompanying notes to unaudited interim condensed consolidated financial statements.

7

EZCORP, Inc.

Notes to Interim Condensed Consolidated Financial Statements (Unaudited)

March 31, 2016

NOTE 1: ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Description of Business

We are a leading provider of pawn loans in the United States and Mexico and consumer loans in Mexico. In the United States and Mexico, we offer pawn loans, which are non-recourse loans collateralized by tangible property, and we sell merchandise, primarily collateral forfeited from pawn lending operations and used merchandise purchased from customers.

Through our 94%-owned subsidiary, Prestaciones Finmart, S.A.P.I. de C.V., SOFOM, E.N.R. ("Grupo Finmart"), headquartered in Mexico City, we offer unsecured installment loans to employees of various Mexican employers (principally federal, state and local government agencies), which are repaid through payroll deductions.

We also own approximately 32% of Cash Converters International Limited ("Cash Converters International"), based in Australia and publicly-traded on the Australian Stock Exchange, which franchises and operates a worldwide network of over 700 locations that provide pawn loans, short-term unsecured loans and other consumer finance products, and buy and sell second-hand goods, with significant store concentration in Australia and the United Kingdom.

Basis of Presentation

The accompanying unaudited interim condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all the information and footnotes required by generally accepted accounting principles for complete financial statements. Our management has included all adjustments it considers necessary for a fair presentation. These adjustments are of a normal, recurring nature except for those related to discontinued operations described in Note 2.

The accompanying financial statements should be read in conjunction with the condensed consolidated financial statements and notes included in our Annual Report on Form 10-K for the year ended September 30, 2015. The balance sheet as of September 30, 2015 has been derived from the audited financial statements at that date but does not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. Our business is subject to seasonal variations, and operating results for the three and six-months ended March 31, 2016 (the "current quarter" and "current six-months," respectively) are not necessarily indicative of the results of operations for the full fiscal year.

These condensed consolidated financial statements include the accounts of EZCORP, Inc. and its consolidated subsidiaries (collectively, "EZCORP"). All intercompany accounts and transactions have been eliminated in consolidation.

To determine if we hold a controlling financial interest in an entity, we first evaluate if we are required to apply the variable interest entity ("VIE") model to the entity; otherwise, the entity is evaluated under the voting interest model. Where we hold current or potential rights that give us the power to direct the activities of a VIE that most significantly impact the VIE's economic performance combined with a variable interest that gives us the right to receive potentially significant benefits or the obligation to absorb potentially significant losses, we have a controlling financial interest in that VIE. Rights held by others to remove the party with power over the VIE are not considered unless one party can exercise those rights unilaterally. Grupo Finmart has completed several transfers of consumer loans to various securitization trusts. We consolidate those securitization entities under the VIE model as described in Note 16.

We account for our investment in our unconsolidated affiliate Cash Converters International using the equity method.

There have been no changes in significant accounting policies as described in our Annual Report on Form 10-K for the year ended September 30, 2015, other than those described below.

8

Recasting of Certain Prior Period Information

Certain reclassifications of prior period amounts have been made to conform to the current period presentation. These reclassifications, other than those pertaining to the recasting of prior period segment information and discontinued operations discussed in our Annual Report on Form 10-K for the year ended September 30, 2015 and the adoption of Financial Accounting Standards Board ("FASB") Accounting Standards Updates ("ASU") discussed below, primarily include the following:

• | Removal of historical corporate overhead allocations totaling $3.9 million and $8.2 million for the three and six-months ended March 31, 2015, respectively, from segment level "Operations" expense and inclusion in corporate "Administrative" expense. These allocations were reclassified to provide greater clarity into the results of our segment operations. These changes primarily impacted Note 12 with no net impact on our consolidated financial position, results of operations or cash flows. |

• | Reclassification of "Prepaid income taxes" to "Income taxes receivable" of $7.9 million as of September 30, 2015 to conform to current period presentation. |

Use of Estimates and Assumptions

The preparation of these financial statements requires us to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses and related disclosure of contingent assets and liabilities. On an ongoing basis, we evaluate our estimates and judgments, including those related to revenue recognition, inventory, loan loss allowances, long-lived and intangible assets, share-based compensation, income taxes, contingencies and litigation. We base our estimates on historical experience, observable trends and various other assumptions that we believe are reasonable under the circumstances. We use this information to make judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ materially from these estimates under different assumptions or conditions.

Recently Adopted Accounting Policies

Simplification of Adjustments to Provisional Amounts Identified During a Measurement Period

In September 2015, the FASB issued ASU 2015-16, Business Combinations (Topic 805). This ASU requires reporting entities to recognize adjustments to provisional amounts that are identified during the measurement period in the reporting period in which the adjustment amounts are determined, with the effect on earnings of changes in depreciation, amortization, or other income effects, if any, as a result of the change to the provisional amounts, calculated as if the accounting had been completed at the acquisition date. The provisions of this ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015. Early adoption is permitted. A reporting entity should apply the amendment prospectively to adjustments to provisional amounts that occur after the date of adoption. We early adopted ASU 2015-16 during the current quarter to reduce the cost and complexity of accounting for and reporting business combinations. There was no material impact of adopting ASU 2015-16 on our consolidated financial position, results of operations or cash flows.

Share-Based Awards with Performance Targets that could be Achieved after the Requisite Service Period

In June 2014, the FASB issued ASU 2014-12, Compensation — Stock Compensation (Topic 718): Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period. This ASU requires reporting entities to recognize compensation costs for share-based awards with performance targets in the period in which it becomes probable that the performance targets will be achieved and should represent the compensation cost attributable to the periods for which the requisite service has already been rendered. The provisions of this ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015. Early adoption is permitted. A reporting entity may apply the amendment prospectively or retrospectively. We early adopted ASU 2015-16 during the current quarter and applied the amendments prospectively to all awards granted or modified after the effective date. There was no material impact of adopting ASU 2014-12 on our consolidated financial position, results of operations or cash flows.

Classification of Deferred Tax Assets

In November 2015, the FASB issued ASU 2015-17, Income Taxes (Topic 740): Balance Sheet Classification of Deferred Taxes. This ASU requires reporting entities to classify deferred income taxes as non-current on the condensed consolidated balance sheets. Deferred income taxes were previously required to be classified as current or non-current on the condensed consolidated balance sheets. The provisions of this ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016. Early adoption is permitted. A reporting entity may apply the amendment prospectively or retrospectively. We early adopted ASU 2015-17 during the three-months ended December 31, 2015 on a retrospective basis. The impact of adopting ASU 2015-17 on our current period condensed consolidated financial statements was the classification of all deferred tax assets as non-current in addition to the reclassification of current "Deferred tax asset, net" to non-current

9

"Deferred tax asset, net" as of March 31, 2015 and September 30, 2015 of $24.4 million and $44.1 million, respectively, within the condensed consolidated balance sheets to conform to the current period presentation. Other than these reclassifications, the adoption of ASU 2015-17 did not have an impact on our consolidated financial position, results of operations or cash flows.

Presentation of Debt Issuance Costs

In April 2015, the FASB issued ASU 2015-03, Interest — Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs. This ASU requires reporting entities to record costs paid to third parties that are directly related to issuing debt, and that otherwise would not be incurred, as a deduction to the corresponding debt for presentation purposes. In addition, in August 2015, FASB issued ASU 2015-15, Interest — Imputation of Interest (Subtopic 835-30): Presentation and Subsequent Measurement of Debt Issuance Costs Associated with Line-of-Credit Arrangements-Amendments to SEC Paragraphs Pursuant to Staff Announcement at the June 18, 2015 Emerging Issues Task Force ("EITF") Meeting. Given the absence of authoritative guidance within ASU 2015-03 for debt issuance costs related to line-of-credit arrangements, ASU 2015-15 states the SEC staff would not object to an entity deferring and presenting debt issuance costs as an asset and subsequently amortizing the deferred debt issuance costs ratably over the term of the line-of-credit arrangement, regardless of whether there are any outstanding borrowings on the line-of-credit arrangement. The provisions of each ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015. Early adoption is permitted for each. A reporting entity should apply each amendment retrospectively. We early adopted ASU 2015-03 during the three-months ended December 31, 2015 on a retrospective basis. The impact of adopting ASU 2015-03 on our current period condensed consolidated financial statements was the classification of all deferred financing costs as a deduction to the corresponding debt in addition to the reclassification of deferred financing costs in "Intangible assets, net" to "Long-term debt less current maturities, net" as of March 31, 2015 and September 30, 2015 of $11.4 million and $9.2 million, respectively, within the condensed consolidated balance sheets to conform to the current period presentation. Other than these reclassifications and additional disclosures, the adoption of ASU 2015-03 did not have an impact on our consolidated financial position, results of operations or cash flows.

Reporting Discontinued Operations

In April 2014, the FASB issued ASU 2014-08, Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360) — Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity. This ASU provides guidance for the reporting of discontinued operations if (1) a component or group of components of an entity meets the criteria in FASB Accounting Standards Codification ("ASC") Paragraph 205-20-45-1E to be classified as held for sale; (2) the component of an entity or group of components of an entity is disposed of by sale; or (3) the component of an entity or group of components of an entity is disposed of other than by sale (for example, by abandonment or in a distribution to owners in a spinoff). Among other disclosures, ASU 2014-08 requires an entity to present, for each comparative period, the assets and liabilities of a disposal group that includes a discontinued operation separately in the asset and liability sections, respectively, of the statement of financial position. ASU 2014-08 is effective prospectively for (1) all disposals of components that occur within annual periods beginning on or after December 15, 2014, and interim periods within those years; and (2) all businesses or nonprofit activities that, on acquisition, are classified as held for sale that occur within annual periods beginning on or after December 15, 2014, and interim periods within those years. There was no impact of adopting ASU 2014-08 on our consolidated financial position, results of operations or cash flows.

Recently Issued Accounting Pronouncements

In March 2016, the FASB issued ASU 2016-09, Compensation — Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting. This ASU simplifies several aspects of the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities, and classification on the statement of cash flows. The provisions of this ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016. Early adoption is permitted. A reporting entity should apply the amendment using transition guidance for each aspect of the ASU. We are in the process of evaluating the impact of adopting ASU 2016-09 on our financial position, results of operations and cash flows.

In March 2016, the FASB issued ASU 2016-06, Derivatives and Hedging (Topic 815): Contingent Put and Call Options in Debt Instruments a consensus of the FASB Emerging Issues Task Force. This ASU clarifies what steps are required when assessing whether the economic characteristics and risks of call (put) options are clearly and closely related to the economic characteristics and risks of their debt hosts, which is one of the criteria for bifurcating an embedded derivative. The provisions of this ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2016. Early adoption is permitted. A reporting entity should apply the amendment modified retrospective basis to existing debt instruments as of the beginning of the fiscal year for which the amendments are effective. We are in the process of evaluating the impact of adopting ASU 2016-06 on our financial position, results of operations and cash flows.

10

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842). This ASU requires companies to generally recognize on the balance sheet operating and financing lease liabilities and corresponding right-of-use assets. The provisions of this ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018. Early adoption is permitted based upon guidance issued within the ASU. We anticipate adoption of this ASU on a modified retrospective basis using various practical expedients. We are in the process of evaluating the impact of adopting ASU 2016-02 on our financial position, results of operations and cash flows.

In January 2016, the FASB issued ASU 2016-01, Financial Instruments — Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities. This ASU makes targeted improvements to the accounting for, and presentation and disclosure of, financial assets and liabilities. The ASU further requires separate presentation of financial assets and financial liabilities by measurement category on the balance sheet or the accompanying notes to the financial statements. The provisions of this ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017. Early adoption is permitted based upon guidance issued within the ASU. A reporting entity should apply the amendment prospectively, with a cumulative-effect adjustment to the balance sheet as of the beginning of the fiscal year of adoption. We are in the process of evaluating the impact of adopting ASU 2016-01 on our financial position, results of operations and cash flows.

In May 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers (Topic 606). On August 12, 2015, the FASB issued ASU 2015-14, Revenue from Contracts with Customers (Topic 606) to defer the effective date to December 15, 2017 for annual reporting periods beginning after that date. The FASB also permitted early adoption of the standard, but not before the original effective date of December 15, 2016. The amendments in ASU 2014-09 will be added to the Accounting Standards Codification as Topic 606, Revenue from Contracts with Customers, and will supersede the revenue recognition requirements in Topic 605, Revenue Recognition, as well as some cost guidance in Subtopic 605-35, Revenue Recognition - Construction-Type and Production-Type Contracts. The core principle of ASU 2014-09 is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. To achieve this core principle, the guidance provides that an entity should apply the following steps: (1) identify the contract(s) with a customer; (2) identify the performance obligations in the contract; (3) determine the transaction price; (4) allocate the transaction price to the performance obligations in the contract; and (5) recognize revenue when, or as, the entity satisfies a performance obligation. Notably, the existing requirements for the recognition of a gain or loss on the transfer of non-financial assets that are not in a contract with a customer (e.g., assets within the scope of Topic 360, Property, Plant, and Equipment, and intangible assets within the scope of Topic 350, Intangibles — Goodwill and Other) are amended to be consistent with the guidance on recognition and measurement in ASU 2014-09. The new standard allows for two methods of adoption: (a) full retrospective adoption, meaning the standard is applied to all periods presented, or (b) modified retrospective adoption, meaning the cumulative effect of applying the new standard is recognized as an adjustment to the fiscal 2017 opening retained earnings balance. In April 2016 and March 2016, the FASB issued ASU 2016-10, Revenue from Contracts with Customers (Topic 606): Consensuses of the FASB Emerging Issues Task Force and ASU 2016-08, Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (Reporting Revenue Gross versus Net), respectively. ASU 2016-10 and ASU 2016-08 clarify identifying performance obligations and licensing implementation guidance and implementation guidance on principal versus agent considerations in ASU 2014-09, respectively, and are effective upon adoption of ASU 2014-09. We are evaluating the impact that will result from adopting ASU 2014-09 on our financial position, results of operations, and cash flows.

11

NOTE 2: DISCONTINUED OPERATIONS AND RESTRUCTURING

Discontinued Operations

During the fourth quarter of fiscal 2015, in the context of a transformational change in strategy following an intensive six-month review of all Company activities, we implemented a plan that included exiting our U.S. financial services business ("USFS"). During the fourth quarter of fiscal 2014, as part of our new strategy to concentrate on an integrated, customer-centric financial services model that is focused on our core businesses of pawn and unsecured payroll lending, we implemented a plan to exit our online lending businesses in the United States (EZOnline) and the United Kingdom (Cash Genie). These costs are included under "(Loss) income from discontinued operations, net of tax" in our condensed consolidated statements of operations.

The following table summarizes the pre-tax charges, inclusive of the charges presented in the accrued lease termination costs, severance costs and other costs rollforward below, pertaining to the above discontinued operations:

Three Months Ended March 31, 2016 | Three Months Ended March 31, 2015 | Six Months Ended March 31, 2016 | Six Months Ended March 31, 2015 | ||||||||||||

(in thousands) | |||||||||||||||

Other (a) | $ | 1,203 | $ | 4,025 | $ | 2,733 | $ | 4,025 | |||||||

(a) | Includes estimated costs related to employee severance and accelerated amortization of prepaid expenses and other assets in addition to a one-time charge of $3.3 million related to Cash Genie regulatory compliance recorded during the six-months ended March 31, 2015. The costs incurred during fiscal 2016 are primarily the result of final payments associated with the physical exit of USFS stores. |

Accrued lease termination costs, severance costs and other costs related to discontinued operations are included under "Accounts payable and other accrued expenses" in our condensed consolidated balance sheets and are primarily expected to be paid during fiscal 2016. Changes in these amounts during the three and six-months ended March 31, 2016 and 2015 are summarized as follows:

Three Months Ended March 31, 2016 | Three Months Ended March 31, 2015 | Six Months Ended March 31, 2016 | Six Months Ended March 31, 2015 | ||||||||||||

(in millions) | |||||||||||||||

Beginning balance (a) | $ | 9.0 | $ | 7.8 | $ | 16.9 | $ | 8.9 | |||||||

Charged to expense | 1.2 | 4.0 | 2.7 | 4.0 | |||||||||||

Cash payments | (2.0 | ) | (0.7 | ) | (11.5 | ) | (1.4 | ) | |||||||

Other (b) | (0.1 | ) | (0.9 | ) | — | (1.3 | ) | ||||||||

Ending balance | $ | 8.1 | $ | 10.2 | $ | 8.1 | $ | 10.2 | |||||||

(a) | Beginning balance as of September 30, 2015 includes a $10.5 million charge associated with the settlement of outstanding issues with the U.S. Consumer Financial Protection Bureau. We expect this amount to primarily be paid out during fiscal 2016; however ultimate settlement of certain portions may occur in fiscal 2017. |

(b) | Includes adjustments due to foreign currency effects and other individually immaterial adjustments. |

Total revenue included in "(Loss) income from discontinued operations, net of tax" in our condensed consolidated statements of operations for the three-months ended March 31, 2016 were nominal. Total revenue included in "(Loss) income from discontinued operations, net of tax" in our condensed consolidated statements of operations for the six-months ended March 31, 2016 was $2.1 million. Total revenue included in "(Loss) income from discontinued operations, net of tax" in our condensed consolidated statements of operations for the three and six-months ended March 31, 2015 was $36.5 million and $77.8 million, respectively. All revenue, expense and income reported in these condensed consolidated financial statements have been adjusted to reflect reclassification of all discontinued operations.

Restructuring

Fiscal 2015

During the fourth quarter of fiscal 2015, in the context of a transformational change in strategy following an intensive six-month review of all Company activities, we implemented a plan that included streamlining our structure and operating model to improve overall efficiency and reduce costs. The costs of streamlining our structure and operating model are included under "Restructuring" expenses in our condensed consolidated statements of operations and are allocated to certain of our segments as presented in Note 12.

12

The following table summarizes the pre-tax charges, inclusive of the charges presented in the changes in the balance of restructuring costs rollforward below:

Three Months Ended March 31, 2016 | Six Months Ended March 31, 2016 | ||||||

(in thousands) | |||||||

Other (a) | $ | 218 | $ | 768 | |||

Asset disposals | — | 323 | |||||

Lease termination costs | — | 819 | |||||

$ | 218 | $ | 1,910 | ||||

(a) | Includes costs related to employee severance and other. |

Accrued lease termination costs, severance costs and other costs related to restructuring are included under "Accounts payable and other accrued expenses" in our condensed consolidated balance sheets. Changes in these amounts during the three and six-months ended March 31, 2016 are summarized as follows:

Three Months Ended March 31, 2016 | Six Months Ended March 31, 2016 | ||||||

(in thousands) | |||||||

Beginning balance | $ | 6,718 | $ | 8,076 | |||

Charged to expense | 218 | 1,594 | |||||

Cash payments | (1,758 | ) | (3,800 | ) | |||

Other (a) | — | (692 | ) | ||||

Ending balance | $ | 5,178 | $ | 5,178 | |||

(a) | Includes other individually immaterial adjustments. |

The above amount includes accrued lease termination costs of $4.9 million that we expect to be partially offset by future sublease payments through 2029. The remaining other amounts accrued are expected to be paid during fiscal 2016.

Fiscal 2014

During the fourth quarter of fiscal 2014, we conducted a company-wide operational review to realign our organization to streamline operations and create synergies and efficiencies. Restructuring charges related to this action are considered corporate costs and therefore are not allocated to specific segments. Changes in these amounts during the three and six-months ended March 31, 2016 and 2015 are summarized as follows:

Three Months Ended March 31, 2016 | Three Months Ended March 31, 2015 | Six Months Ended March 31, 2016 | Six Months Ended March 31, 2015 | ||||||||||||

(in thousands) | |||||||||||||||

Beginning balance | $ | — | $ | 3,858 | $ | 2,901 | $ | 6,121 | |||||||

Charged to expense | — | 726 | — | 726 | |||||||||||

Cash payments | — | (699 | ) | (2,901 | ) | (2,962 | ) | ||||||||

Ending Balance | $ | — | $ | 3,885 | $ | — | $ | 3,885 | |||||||

NOTE 3: ACQUISITIONS

On February 1, 2016, we acquired six pawn stores in the Houston, Texas area doing business under the "Pawn One" brand. The aggregate purchase price was $6.2 million in cash, inclusive of all ancillary arrangements, of which $3.2 million was recorded as goodwill in the U.S. Pawn segment. The acquisition was made as part of our continuing strategy to enhance our earnings over the long-term. The factors contributing to the recognition of goodwill were based on several strategic and synergistic benefits we expect to realize from the acquisition. These benefits include a greater presence in the Houston area, as well as the ability to further leverage our expense structure through increased scale. We expect no goodwill recorded as a result of the acquisition to be deductible for tax purposes. We have concluded that this acquisition was immaterial to our overall consolidated financial results and, therefore, have omitted the information that would otherwise be required by FASB ASC 805-10-50-2(h).

13

NOTE 4: EARNINGS PER SHARE

Components of basic and diluted (loss) earnings per share and excluded anti-dilutive potential common shares are as follows:

Three Months Ended March 31, | Six Months Ended March 31, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

(in thousands, except per share amounts) | |||||||||||||||

Net (loss) income from continuing operations attributable to EZCORP (A) | $ | (73,031 | ) | $ | (3,388 | ) | $ | (80,267 | ) | $ | 1,347 | ||||

Income (loss) from discontinued operations, net of tax (B) | (1,094 | ) | 4,731 | (1,332 | ) | 11,608 | |||||||||

Net (loss) income attributable to EZCORP (C) | $ | (74,125 | ) | $ | 1,343 | $ | (81,599 | ) | $ | 12,955 | |||||

Weighted-average outstanding shares of common stock (D) | 54,843 | 54,184 | 54,869 | 53,915 | |||||||||||

Dilutive effect of restricted stock* | — | — | — | 57 | |||||||||||

Weighted-average common stock and common stock equivalents (E) | 54,843 | 54,184 | 54,869 | 53,972 | |||||||||||

Basic (loss) earnings per share attributable to EZCORP: | |||||||||||||||

Continuing operations (A / D) | $ | (1.33 | ) | $ | (0.06 | ) | $ | (1.46 | ) | $ | 0.02 | ||||

Discontinued operations (B / D) | (0.02 | ) | 0.09 | (0.02 | ) | 0.22 | |||||||||

Basic (loss) earnings per share (C / D) | $ | (1.35 | ) | $ | 0.03 | $ | (1.48 | ) | $ | 0.24 | |||||

Diluted (loss) earnings per share attributable to EZCORP: | |||||||||||||||

Continuing operations (A / E) | $ | (1.33 | ) | $ | (0.06 | ) | $ | (1.46 | ) | $ | 0.02 | ||||

Discontinued operations (B / E) | (0.02 | ) | 0.09 | (0.02 | ) | 0.22 | |||||||||

Diluted (loss) earnings per share (C / E) | $ | (1.35 | ) | $ | 0.03 | $ | (1.48 | ) | $ | 0.24 | |||||

Potential common shares excluded from the calculation of diluted (loss) earnings per share: | |||||||||||||||

Restricted stock** | 1,608 | 273 | 1,545 | 6 | |||||||||||

Warrants*** | 14,317 | 14,317 | 14,317 | 14,317 | |||||||||||

Total potential common shares excluded | 15,925 | 14,590 | 15,862 | 14,323 | |||||||||||

* | As required by FASB ASC 260-10-45-19, amount excludes all potential common shares for periods when there is a loss from continuing operations. |

** | Includes antidilutive share-based awards as well as performance-based and market conditioned share-based awards that are contingently issuable, but for which the condition for issuance has not been met as of the end of the reporting period. |

*** | See Note 7 for discussion of the terms and conditions of these potential common shares. |

Weighted-average outstanding shares of common stock for the three and six-months ended March 31, 2016 include the impact of redeemable common stock repurchased as discussed in Note 9.

14

NOTE 5: STRATEGIC INVESTMENTS

As of March 31, 2016, we owned 151,948,000 shares, or approximately 32%, of our unconsolidated affiliate Cash Converters International. The following tables present summary financial information for Cash Converters International’s most recently reported results as of March 31, 2016 after translation to U.S. dollars:

December 31, | |||||||

2015 | 2014 | ||||||

(in thousands) | |||||||

Current assets | $ | 176,105 | $ | 200,682 | |||

Non-current assets | 143,466 | 157,737 | |||||

Total assets | $ | 319,571 | $ | 358,419 | |||

Current liabilities | $ | 68,857 | $ | 75,700 | |||

Non-current liabilities | 48,263 | 54,256 | |||||

Shareholders’ equity: | |||||||

Equity attributable to owners of the parent | 202,450 | 228,462 | |||||

Noncontrolling interest | 1 | 1 | |||||

Total liabilities and shareholders’ equity | $ | 319,571 | $ | 358,419 | |||

Half Year Ended December 31, | |||||||

2015 | 2014 | ||||||

(in thousands) | |||||||

Gross revenues | $ | 143,575 | $ | 167,206 | |||

Gross profit | 93,573 | 104,852 | |||||

Profit (loss) attributable to: | |||||||

Owners of the parent | $ | 11,483 | $ | (4,717 | ) | ||

Noncontrolling interest | — | (179 | ) | ||||

Profit (loss) for the year | $ | 11,483 | $ | (4,896 | ) | ||

NOTE 6: GOODWILL AND OTHER INTANGIBLE ASSETS

In accordance with FASB ASC 350-20-35, Goodwill — Subsequent Measurement, we test goodwill and intangible assets with an indefinite useful life for potential impairment annually, or more frequently when there are events or circumstances that indicate that it is more likely than not that an impairment exists. During the three-months ended March 31, 2016, we evaluated such events and circumstances and concluded that there were indicators of impairment under FASB ASC 350-20-35-3C. These indicators of impairment primarily included a continued decline in our stock price, as well as negative developments in bad debt experience at our Grupo Finmart segment. We performed a quantitative Step 1 analysis as of February 29, 2016 under FASB ASC 350-20-35 and determined that the fair value of each of our reporting units exceeded their carrying value, with the exception of our Grupo Finmart reporting unit. The fair values of each reporting unit were determined based on a discounted cash flow approach using significant unobservable inputs (Level 3) developed using company-specific information. During the quarter ended March 31, 2016, there were no material changes in the fair values of our U.S. Pawn and Mexico Pawn reporting units as compared to their carrying values. There is no goodwill attributable to our Other International reporting unit. We will further perform our required annual impairment test in the fourth quarter of our fiscal 2016.

The Step 1 analysis of our Grupo Finmart reporting unit yielded a valuation of $46.5 million. Under Step 2 of FASB ASC 350-20-35, we compared the fair value of the reporting unit to the fair value of the reporting unit's net assets and determined that all of the goodwill attributable to the Grupo Finmart reporting unit ($73.9 million), should be impaired. This impairment was recorded under "Impairment of goodwill" in the condensed consolidated statements of operations under the Grupo Finmart segment during the three-months ended March 31, 2016. No other assets held by Grupo Finmart were determined to be impaired as of March 31, 2016.

See Note 3 for additional information regarding goodwill acquired in business combinations during the three-months ended March 31, 2016.

15

NOTE 7: LONG-TERM DEBT AND CAPITAL LEASE OBLIGATIONS

The following table presents our long-term debt instruments and balances under capital lease obligations outstanding as of March 31, 2016 and 2015 and September 30, 2015:

March 31, 2016 | March 31, 2015 | September 30, 2015 | |||||||||||||||||||||

Carrying Amount | Debt (Discount) and (Issuance Costs) | Carrying Amount | Debt (Discount) Premium and (Issuance Costs) | Carrying Amount | Debt (Discount) and (Issuance Costs) | ||||||||||||||||||

(in thousands) | |||||||||||||||||||||||

Recourse to EZCORP: | |||||||||||||||||||||||

2.125% Cash convertible senior notes due 2019 | $ | 192,565 | $ | (37,435 | ) | $ | 182,276 | $ | (47,724 | ) | $ | 187,471 | $ | (42,529 | ) | ||||||||

Cash convertible senior notes due 2019 embedded derivative | 3,219 | — | 27,215 | — | 10,505 | — | |||||||||||||||||

Capital lease obligations | — | — | 93 | — | — | — | |||||||||||||||||

Non-recourse to EZCORP*: | |||||||||||||||||||||||

8.2% Secured foreign currency debt up to $14 million due 2016 (a) (b) | 82 | (101 | ) | 2,044 | (451 | ) | 938 | (204 | ) | ||||||||||||||

14.5% Secured foreign currency debt up to $17 million due 2017 (a) | 17,393 | — | 19,682 | — | 17,567 | — | |||||||||||||||||

5.8% Consumer loans facility due 2019 (b) | 33,613 | (1,714 | ) | 44,837 | (2,989 | ) | 40,493 | (2,196 | ) | ||||||||||||||

8.5% Unsecured notes due 2015 | — | — | 12,329 | (187 | ) | 12,330 | (42 | ) | |||||||||||||||

10% Unsecured notes due 2015 | — | — | — | — | 1,500 | — | |||||||||||||||||

11% Unsecured notes due 2015 | — | — | 4,334 | — | 3,868 | — | |||||||||||||||||

17% Secured notes due 2015 consolidated from VIEs | — | — | 937 | — | — | — | |||||||||||||||||

10% Unsecured notes due 2016 | 1,500 | — | 844 | — | 1,885 | — | |||||||||||||||||

12% Secured notes due 2016 | — | — | 2,691 | 67 | 2,928 | — | |||||||||||||||||

13% Unsecured notes due 2016 | — | — | 656 | — | 1,171 | — | |||||||||||||||||

15% Unsecured notes due 2016 | 3,829 | — | — | — | 233 | — | |||||||||||||||||

15% Secured notes due 2016 consolidated from VIEs | 3,192 | — | 7,755 | — | 5,397 | — | |||||||||||||||||

18% Unsecured notes due 2016 | 5,797 | — | — | — | — | — | |||||||||||||||||

10% Unsecured notes due 2017 | 174 | — | — | — | — | — | |||||||||||||||||

11% Secured notes due 2017 consolidated from VIEs (c) | 37,901 | — | 76,545 | — | 56,113 | — | |||||||||||||||||

12% Secured notes due 2017 | 2,898 | — | — | — | — | — | |||||||||||||||||

13.5% Unsecured notes due 2017 | 5,797 | — | — | — | — | — | |||||||||||||||||

14.5% Secured notes due 2017 consolidated from VIEs | 9,788 | — | 14,897 | — | 11,754 | — | |||||||||||||||||

12.4% Secured notes due 2020 | 17,234 | (214 | ) | 19,389 | (358 | ) | 17,358 | (268 | ) | ||||||||||||||

Total | 334,982 | (39,464 | ) | 416,524 | (51,642 | ) | 371,511 | (45,239 | ) | ||||||||||||||

Less current portion | 82,174 | — | 71,564 | 67 | 74,345 | — | |||||||||||||||||

Total long-term debt and capital lease obligations | $ | 252,808 | $ | (39,464 | ) | $ | 344,960 | $ | (51,709 | ) | $ | 297,166 | $ | (45,239 | ) | ||||||||

* | Even though Grupo Finmart debt may be non-recourse to EZCORP, a default on more than $25 million of such debt could constitute an event of default under our Cash Convertible Notes (described below). See "Part II, Item 1A — Risk Factors." |

(a) | Maximum amounts of debt are translated from Mexican pesos to United States dollars as of the most current period end date in which outstanding debt is presented. |

(b) | Interest is charged at the Mexican Interbank Equilibrium rate (“TIIE”) plus an applicable margin. The rate presented is as of March 31, 2016. |

(c) | Grupo Finmart has entered into foreign exchange forward contracts to mitigate the VIE's currency risk, as described in Notes 15 and 16, and EZCORP has guaranteed the future cash outflows of the forward contracts. See "Part II, Item 1A — Risk Factors." |

2.125% Cash Convertible Senior Notes Due 2019

In June 2014 ("Original Issuance Date"), we issued $200 million aggregate principal amount of 2.125% Cash Convertible Senior Notes due 2019 (the “Cash Convertible Notes”). We granted the initial purchasers the option to purchase up to an additional $30 million aggregate principal amount of Cash Convertible Notes. That option was exercised in full on June 27,

16

2014, and we issued an additional $30 million principal amount of Cash Convertible Notes on July 2, 2014. All of the Cash Convertible Notes were issued pursuant to an indenture dated June 23, 2014 (the "Indenture") by and between us and Wells Fargo Bank, National Association, as the trustee. The Cash Convertible Notes were issued in a private offering and resold under Rule 144A under the Securities Act of 1933. The Cash Convertible Notes pay interest semi-annually in arrears at a rate of 2.125% per annum on June 15 and December 15 of each year, commencing December 15, 2014, and will mature on June 15, 2019 (the "Maturity Date").

Prior to December 15, 2018, the Cash Convertible Notes will be convertible only upon the occurrence of certain events and during certain periods, and thereafter, at any time prior to the close of business on the second scheduled trading day immediately preceding the Maturity Date. At maturity, the holders of the Cash Convertible Notes will be entitled to receive cash equal to the principal amount of the Cash Convertible Notes plus unpaid accrued interest.

The Cash Convertible Notes are unsubordinated unsecured obligations and rank senior in right of payment to any of our indebtedness that is expressly subordinated in right of payment to the Cash Convertible Notes, equal in right of payment with all of our other unsecured unsubordinated indebtedness, and effectively junior to all debt or other obligations (including trade payables) of our wholly-owned subsidiaries. The Indenture governing the Cash Convertible Notes does not contain any financial covenants.

We incurred transaction costs of approximately $8.8 million related to the issuance of the Cash Convertible Notes, which we recorded as deferred financing costs and have included as a deduction to the corresponding debt liability. Deferred financing costs are being amortized to interest expense using the effective interest method over the expected term of the Cash Convertible Notes.

Under the terms of our Cash Convertible Notes, payment of dividends requires a conversion rate adjustment equal to the conversion rate in effect immediately prior to the open of business on the ex-dividend date for such dividend multiplied by the last reported sale price of the Class A Non-voting Common Stock (“Class A Common Stock”) on the trading day immediately preceding the ex-dividend date for such dividend, divided by the difference between the last reported sale price of the Class A Common Stock on the trading day immediately preceding the ex-dividend date for such dividend and the amount in cash per share we distribute to all or substantially all holders of Class A Common Stock. Should we pay dividends in the future, our certificate of incorporation provides that cash dividends on common stock, when declared, must be declared and paid at the same per share amounts on both classes of stock. Any future determination to pay cash dividends will be at the discretion of our Board of Directors.

Cash Convertible Notes Embedded Derivative

We account for the cash conversion feature of the Cash Convertible Notes as a separate derivative instrument (the “Cash Convertible Notes Embedded Derivative”), which had a fair value of $46.5 million on the issuance date that was recognized as the original issue discount of the Cash Convertible Notes. This original issue discount is being amortized to interest expense over the term of the Cash Convertible Notes using the effective interest method. As of March 31, 2016 and 2015 and September 30, 2014, the Cash Convertible Notes Embedded Derivative was recorded as a non-current liability under "Long-term debt, less current maturities" in our condensed consolidated balance sheets, and will be marked to market in subsequent reporting periods. The classification of the Cash Convertible Notes Embedded Derivative liability as current or non-current on the condensed consolidated balance sheets corresponds with the classification of the net balance of the Cash Convertible Notes as discussed below.

The Cash Convertible Notes are convertible into cash, subject to satisfaction of certain conditions and during the periods described below, based on an initial "Conversion Rate" of 62.2471 shares of Class A Common Stock per $1,000 principal amount of Cash Convertible Notes (equivalent to an initial "Conversion Price" of approximately $16.065 per share of our Class A Common Stock). Upon conversion of a note, we will pay cash based on a daily conversion value calculated on a proportionate basis for each trading day in the applicable 80 trading day observation period as described in the Indenture. The conversion rate will not be adjusted for any accrued and unpaid interest.

Holders may surrender their Cash Convertible Notes for conversion into cash prior to December 15, 2018 only under the following circumstances (the “Early Conversion Conditions”): (1) during any fiscal quarter commencing after the fiscal quarter ending on September 30, 2014 (and only during such fiscal quarter), if the last reported sale price of our Class A Common Stock for at least 20 trading days (whether or not consecutive) during a period of 30 consecutive trading days ending on the last trading day of the immediately preceding fiscal quarter is greater than or equal to 130% of the conversion price on each applicable trading day; (2) during the five business day period after any five consecutive trading day period (the “measurement period”) in which the trading price, as defined in the Indenture, per $1,000 principal amount of notes for each trading day of the measurement period was less than 98% of the product of the last reported sale price of our Class A Common Stock and the conversion rate on such trading day; or (3) upon the occurrence of specified corporate events, as defined in the Indenture. On or

17

after December 15, 2018 until the close of business on the second scheduled trading day immediately preceding the Maturity Date, holders may convert their notes into cash at any time, regardless of the foregoing circumstances.

If a holder elects to convert its Cash Convertible Notes in connection with certain make-whole fundamental changes, as that term is defined in the Indenture, that occur prior to the Maturity Date, we will in certain circumstances increase the conversion rate for Cash Convertible Notes converted in connection with such make-whole fundamental changes by a specified number of shares of Class A Common Stock. In addition, the conversion rate is subject to customary anti-dilution adjustments (for example, certain dividend distributions or tender or exchange offer of our Class A Common Stock).

Upon the occurrence of a fundamental change, as defined in the Indenture, holders may require us to repurchase for cash all or any portion of the then outstanding Cash Convertible Notes at a repurchase price equal to 100% of the principal amount of the notes to be repurchased, plus accrued and unpaid interest.

Impact of Early Conversion Conditions on Financial Statements

As of March 31, 2016, the Cash Convertible Notes were not convertible because the Early Conversion Conditions described above had not been met. Accordingly, the net balance of the Cash Convertible Notes was classified as a non-current liability in our condensed consolidated balance sheets as of March 31, 2016 and 2015 and September 30, 2015. The classification of the Cash Convertible Notes as current or non-current in the condensed consolidated balance sheets is evaluated at each balance sheet date and may change from time to time depending on whether any of the Early Conversion Conditions has been met.

If any of the Early Conversion Conditions is met in any future fiscal quarter, we would classify our net liability under the Cash Convertible Notes as a current liability in the condensed consolidated balance sheets as of the end of that fiscal quarter. If none of the Early Conversion Conditions have been met in a future fiscal quarter prior to the one year period immediately preceding the Maturity Date, we would classify our net liability under the Cash Convertible Notes as a non-current liability in the condensed consolidated balance sheets as of the end of that fiscal quarter. If the note holders elect to convert their Cash Convertible Notes prior to maturity, any unamortized discount and transaction costs will be expensed at the time of conversion. If the entire outstanding principal amount had been converted on March 31, 2016, we would have recorded an expense of $37.4 million associated with the conversion, comprised of $31.7 million of unamortized debt discount and $5.7 million of unamortized debt issuance costs. As of March 31, 2016, none of the note holders had elected to convert their Cash Convertible Notes.

Cash Convertible Notes Hedges

In connection with the issuance of the Cash Convertible Notes, we purchased cash-settled call options (the “Cash Convertible Notes Hedges”) in privately negotiated transactions with certain of the initial purchasers or their affiliates (in this capacity, the “Option Counterparties”). The Cash Convertible Notes Hedges provide us with the option to acquire, on a net settlement basis, approximately 14.3 million shares of our Class A Common Stock at a strike price of $16.065, which is equal to the number of shares of our Class A Common Stock that notionally underlie the Cash Convertible Notes and corresponds to the Conversion Price of the Cash Convertible Notes. The Cash Convertible Notes Hedges have an expiration date that is the same as the Maturity Date of the Cash Convertible Notes, subject to earlier exercise. The Cash Convertible Notes Hedges have customary anti-dilution provisions similar to the Cash Convertible Notes. If we exercise the Cash Convertible Notes Hedges, the aggregate amount of cash we will receive from the option counterparties to the Cash Convertible Notes Hedges will cover the aggregate amount of cash that we would be required to pay to the holders of the converted Cash Convertible Notes, less the principal amount thereof. As of March 31, 2016, we have not purchased any shares under the Cash Convertible Notes Hedges.

The aggregate cost of the Cash Convertible Notes Hedges was $46.5 million (or $21.3 million net of the total proceeds from the Warrants sold, as discussed below). The Cash Convertible Notes Hedges are accounted for as a derivative asset and are recorded in the condensed consolidated balance sheets at their estimated fair value under "Other assets, net." The Cash Convertible Notes Embedded Derivative liability and the Cash Convertible Notes Hedges asset will be adjusted to fair value each reporting period and unrealized gains and losses will be reflected in the condensed consolidated statements of operations. The Cash Convertible Notes Embedded Derivative and the Cash Convertible Notes Hedges are designed to have similar fair values. Accordingly, the changes in the fair values of these instruments are expected to offset and not have a net impact on the condensed consolidated statements of operations.

The classification of the Cash Convertible Notes Hedges asset as current or long-term on the condensed consolidated balance sheets corresponds with the classification of the Cash Convertible Notes, which is evaluated at each balance sheet date and may change from time to time depending on whether any of the Early Conversion Conditions has been met.

18

Cash Convertible Notes Warrants

In connection with the issuance of the Cash Convertible Notes, we also sold net-share-settled warrants (the “Warrants”) in privately negotiated transactions with the Option Counterparties for the purchase of up to approximately 14.3 million shares of our Class A Common Stock at a strike price of $20.83 per share, for total proceeds of $25.1 million, net of issuance costs, which was recorded as an increase in stockholders' equity. The Warrants have customary anti-dilution provisions similar to the Cash Convertible Notes. As a result of the Warrants, we will experience dilution to our diluted earnings per share if our average closing stock price exceeds $20.83 for any fiscal quarter. The Warrants expire on various dates from September 2019 through February 2020 and must be settled in net shares of our Class A Common Stock. Therefore, upon expiration of the Warrants, we will issue shares of Class A Common Stock to the purchasers of the Warrants that represent the value by which the price of the Class A Common Stock exceeds the strike price stipulated within the particular warrant agreement. As of March 31, 2016, there were 14.3 million warrants outstanding.

Cash Convertible Notes Interest Expense

Total interest expense attributable to the Cash Convertible Notes for the three-months ended March 31, 2016 and 2015 was $4.0 million and $3.8 million, respectively, comprised of contractual interest expense of $1.2 million and $1.2 million, respectively, and debt discount and deferred financing cost amortization of $2.8 million and $2.6 million, respectively. Total interest expense attributable to the Cash Convertible Notes for the six-months ended March 31, 2016 and 2015 was $7.7 million and $7.4 million, respectively, comprised of contractual interest expense of $2.4 million and $2.5 million, respectively, and debt discount and deferred financing cost amortization of $5.3 million and $4.9 million, respectively. The effective interest rate approximates 8% after inclusion of deferred financing costs upon adoption of ASU 2015-03, from the effective interest rate of approximately 7% during fiscal 2015.

As of March 31, 2016, the remaining unamortized issuance discount and costs will be amortized over the next three years assuming no early conversion.

Non-Recourse Debt to EZCORP

Non-recourse debt amounts in the table above represent Grupo Finmart’s third-party debt, including secured notes consolidated from VIEs. Amounts due in Mexican pesos are translated each reporting period. Effective interest rates approximate stated rates.

Secured Foreign Currency Debt, Secured Notes not Consolidated from VIEs and Unsecured Notes

Foreign currency debt and secured notes (not including secured notes consolidated from VIEs, which are discussed below) are secured by Grupo Finmart's loan portfolio or collateralized cash at Grupo Finmart’s option. As of March 31, 2016 and 2015, Grupo Finmart’s secured foreign currency debt and notes, excluding secured notes consolidated from VIEs, were secured by consumer loans totaling $36.5 million and $24.9 million, respectively, included in “Consumer loans, net” and “Non-current consumer loans, net” in our condensed consolidated balance sheets, and collateralized cash totaling $3.0 million and $19.2 million, respectively, included in “Restricted cash” and “Restricted cash, non-current” in our condensed consolidated balance sheets. All unsecured notes are collateralized with Grupo Finmart’s assets.

During the six-months ended March 31, 2016, Grupo Finmart issued $6.1 million of 13.5% unsecured notes due September 2016 (repayment term extended through 2017 during the three-months ended March 31, 2016), $6.1 million of 18% unsecured notes due September 2016 and $2.3 million of 20% unsecured notes due March 2016 (repaid in full during the three-months ended March 31, 2016). Amounts of debt issued are stated at exchange rates in effect at time of issuance.

During the six-months ended March 31, 2016, Grupo Finmart repaid the following amounts of debt that were outstanding as of September 30, 2015: the remaining $0.9 million 8.2% secured foreign currency debt due 2016; $12.3 million 8.5% unsecured notes due 2015; $1.5 million 10% unsecured notes due 2015; $3.9 million 11% unsecured notes due 2015; $2.9 million 12% secured notes due 2016; and $1.2 million 13% unsecured notes due 2016. Such amounts include the impact of foreign exchange effects and amortization of deferred costs. In addition, portions of other debt amounts still outstanding as of March 31, 2016 were repaid.

Notes Consolidated from VIEs