Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 CERTIFICATIONS UNDER SECTION 906 - DENBURY INC | dnr-20160331xex32.htm |

| 10-Q - PDF OF FORM 10-Q - DENBURY INC | dnr-20160331x10q.pdf |

| EX-10.A - EXHIBIT 10(A) 2016 TSR PERFORMANCE AWARD (EQUITY PORTION) - DENBURY INC | dnr-20160331xex10a.htm |

| EX-10.B - EXHIBIT 10(B) 2016 TSR PERFORMANCE AWARD (CASH PORTION) - DENBURY INC | dnr-20160331xex10b.htm |

| EX-10.C - EXHIBIT 10(C) 2016 EBITDAX PERFORMANCE AWARD (EQUITY PORTION) - DENBURY INC | dnr-20160331xex10c.htm |

| EX-10.D - EXHIBIT 10(D) 2016 EBITDAX PERFORMANCE AWARD (CASH PORTION) - DENBURY INC | dnr-20160331xex10d.htm |

| EX-10.E - EXHIBIT 10(E) 2016 OIL PRICE CHANGE VS. TSR PERFORMANCE AWARD - DENBURY INC | dnr-20160331xex10e.htm |

| EX-10.F - EXHIBIT 10(F) DENBURY RESOURCES SEVERANCE PROTECTION PLAN - DENBURY INC | dnr-20160331xex10f.htm |

| EX-31.A - EXHIBIT 31(A) CEO CERTIFICATION UNDER SECTION 302 - DENBURY INC | dnr-20160331xex31a.htm |

| EX-31.B - EXHIBIT 31(B) CFO CERTIFICATION UNDER SECTION 302 - DENBURY INC | dnr-20160331xex31b.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

þ Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the quarterly period ended March 31, 2016

OR

o Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from _______ to ________

Commission file number: 001-12935

DENBURY RESOURCES INC.

(Exact name of registrant as specified in its charter)

Delaware | 20-0467835 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

5320 Legacy Drive, Plano, TX | 75024 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: | (972) 673-2000 | |

Not applicable

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

Class | Outstanding at April 30, 2016 | |

Common Stock, $.001 par value | 350,593,956 | |

Denbury Resources Inc.

Table of Contents

Page | ||||

2

Denbury Resources Inc.

Unaudited Condensed Consolidated Balance Sheets

(In thousands, except par value and share data)

March 31, | December 31, | |||||||

2016 | 2015 | |||||||

Assets | ||||||||

Current assets | ||||||||

Cash and cash equivalents | $ | 8,252 | $ | 2,812 | ||||

Accrued production receivable | 95,934 | 100,413 | ||||||

Trade and other receivables, net | 87,228 | 87,924 | ||||||

Derivative assets | 72,798 | 142,846 | ||||||

Other current assets | 8,763 | 10,005 | ||||||

Total current assets | 272,975 | 344,000 | ||||||

Property and equipment | ||||||||

Oil and natural gas properties (using full cost accounting) | ||||||||

Proved properties | 10,296,792 | 10,245,195 | ||||||

Unevaluated properties | 902,990 | 894,948 | ||||||

CO2 properties | 1,186,607 | 1,187,458 | ||||||

Pipelines and plants | 2,293,102 | 2,293,219 | ||||||

Other property and equipment | 405,039 | 408,194 | ||||||

Less accumulated depletion, depreciation, amortization and impairment | (9,982,733 | ) | (9,653,205 | ) | ||||

Net property and equipment | 5,101,797 | 5,375,809 | ||||||

Other assets | 163,775 | 166,555 | ||||||

Total assets | $ | 5,538,547 | $ | 5,886,364 | ||||

Liabilities and Stockholders’ Equity | ||||||||

Current liabilities | ||||||||

Accounts payable and accrued liabilities | $ | 186,715 | $ | 253,197 | ||||

Oil and gas production payable | 79,765 | 87,337 | ||||||

Derivative liabilities | 25,005 | — | ||||||

Current maturities of long-term debt | 32,917 | 32,481 | ||||||

Total current liabilities | 324,402 | 373,015 | ||||||

Long-term liabilities | ||||||||

Long-term debt, net of current portion | 3,222,497 | 3,245,114 | ||||||

Asset retirement obligations | 142,101 | 138,919 | ||||||

Deferred tax liabilities, net | 742,148 | 837,263 | ||||||

Other liabilities | 26,121 | 27,484 | ||||||

Total long-term liabilities | 4,132,867 | 4,248,780 | ||||||

Commitments and contingencies (Note 7) | ||||||||

Stockholders’ equity | ||||||||

Preferred stock, $.001 par value, 25,000,000 shares authorized, none issued and outstanding | — | — | ||||||

Common stock, $.001 par value, 600,000,000 shares authorized; 354,340,533 and 354,541,626 shares issued, respectively | 354 | 355 | ||||||

Paid-in capital in excess of par | 2,356,069 | 2,353,134 | ||||||

Accumulated deficit | (1,228,039 | ) | (1,042,882 | ) | ||||

Treasury stock, at cost, 3,734,768 and 3,124,311 shares, respectively | (47,106 | ) | (46,038 | ) | ||||

Total stockholders’ equity | 1,081,278 | 1,264,569 | ||||||

Total liabilities and stockholders’ equity | $ | 5,538,547 | $ | 5,886,364 | ||||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

3

Denbury Resources Inc.

Unaudited Condensed Consolidated Statements of Operations

(In thousands, except per share data)

Three Months Ended March 31, | ||||||||

2016 | 2015 | |||||||

Revenues and other income | ||||||||

Oil, natural gas, and related product sales | $ | 187,803 | $ | 297,470 | ||||

CO2 sales and transportation fees | 6,272 | 6,972 | ||||||

Interest income and other income | 769 | 3,207 | ||||||

Total revenues and other income | 194,844 | 307,649 | ||||||

Expenses | ||||||||

Lease operating expenses | 102,447 | 141,084 | ||||||

Marketing and plant operating expenses | 13,194 | 11,685 | ||||||

CO2 discovery and operating expenses | 607 | 947 | ||||||

Taxes other than income | 20,092 | 26,679 | ||||||

General and administrative expenses | 33,901 | 46,280 | ||||||

Interest, net of amounts capitalized of $5,780 and $8,409, respectively | 42,171 | 40,099 | ||||||

Depletion, depreciation, and amortization | 77,366 | 149,958 | ||||||

Commodity derivatives expense (income) | 22,826 | (83,076 | ) | |||||

Gain on debt extinguishment | (94,991 | ) | — | |||||

Write-down of oil and natural gas properties | 256,000 | 146,200 | ||||||

Other expenses | 1,544 | — | ||||||

Total expenses | 475,157 | 479,856 | ||||||

Loss before income taxes | (280,313 | ) | (172,207 | ) | ||||

Income tax benefit | (95,120 | ) | (64,461 | ) | ||||

Net loss | $ | (185,193 | ) | $ | (107,746 | ) | ||

Net loss per common share | ||||||||

Basic | $ | (0.53 | ) | $ | (0.31 | ) | ||

Diluted | $ | (0.53 | ) | $ | (0.31 | ) | ||

Dividends declared per common share | $ | — | $ | 0.0625 | ||||

Weighted average common shares outstanding | ||||||||

Basic | 347,235 | 350,688 | ||||||

Diluted | 347,235 | 350,688 | ||||||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

4

Denbury Resources Inc.

Unaudited Condensed Consolidated Statements of Comprehensive Operations

(In thousands)

Three Months Ended March 31, | ||||||||

2016 | 2015 | |||||||

Net loss | $ | (185,193 | ) | $ | (107,746 | ) | ||

Other comprehensive income, net of income tax: | ||||||||

Interest rate lock derivative contracts reclassified to income, net of tax of $0 and $11, respectively | — | 17 | ||||||

Total other comprehensive income | — | 17 | ||||||

Comprehensive loss | $ | (185,193 | ) | $ | (107,729 | ) | ||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

5

Denbury Resources Inc.

Unaudited Condensed Consolidated Statements of Cash Flows

(In thousands)

Three Months Ended March 31, | ||||||||

2016 | 2015 | |||||||

Cash flows from operating activities | ||||||||

Net loss | $ | (185,193 | ) | $ | (107,746 | ) | ||

Adjustments to reconcile net loss to cash flows from operating activities | ||||||||

Depletion, depreciation, and amortization | 77,366 | 149,958 | ||||||

Write-down of oil and natural gas properties | 256,000 | 146,200 | ||||||

Deferred income taxes | (95,115 | ) | (66,036 | ) | ||||

Stock-based compensation | 859 | 7,849 | ||||||

Commodity derivatives expense (income) | 22,826 | (83,076 | ) | |||||

Receipt on settlements of commodity derivatives | 72,227 | 148,465 | ||||||

Gain on debt extinguishment | (94,991 | ) | — | |||||

Amortization of debt issuance costs and discounts | 3,306 | 2,221 | ||||||

Other, net | (416 | ) | (2,359 | ) | ||||

Changes in assets and liabilities, net of effects from acquisitions | ||||||||

Accrued production receivable | 4,479 | 33,636 | ||||||

Trade and other receivables | 812 | 16,828 | ||||||

Other current and long-term assets | 1,437 | (6,136 | ) | |||||

Accounts payable and accrued liabilities | (53,548 | ) | (83,248 | ) | ||||

Oil and natural gas production payable | (7,572 | ) | (17,716 | ) | ||||

Other liabilities | (448 | ) | (1,076 | ) | ||||

Net cash provided by operating activities | 2,029 | 137,764 | ||||||

Cash flows from investing activities | ||||||||

Oil and natural gas capital expenditures | (65,692 | ) | (162,192 | ) | ||||

CO2 capital expenditures | (315 | ) | (14,855 | ) | ||||

Pipelines and plants capital expenditures | (635 | ) | (12,455 | ) | ||||

Other | (312 | ) | (3,076 | ) | ||||

Net cash used in investing activities | (66,954 | ) | (192,578 | ) | ||||

Cash flows from financing activities | ||||||||

Bank repayments | (696,000 | ) | (595,000 | ) | ||||

Bank borrowings | 831,000 | 665,000 | ||||||

Repurchases of senior subordinated notes | (55,521 | ) | — | |||||

Cash dividends paid | (387 | ) | (22,068 | ) | ||||

Other | (8,727 | ) | (10,250 | ) | ||||

Net cash provided by financing activities | 70,365 | 37,682 | ||||||

Net increase (decrease) in cash and cash equivalents | 5,440 | (17,132 | ) | |||||

Cash and cash equivalents at beginning of period | 2,812 | 23,153 | ||||||

Cash and cash equivalents at end of period | $ | 8,252 | $ | 6,021 | ||||

See accompanying Notes to Unaudited Condensed Consolidated Financial Statements.

6

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

Note 1. Basis of Presentation

Organization and Nature of Operations

Denbury Resources Inc., a Delaware corporation, is an independent oil and natural gas company with operations focused in two key operating areas: the Gulf Coast and Rocky Mountain regions. Our goal is to increase the value of our properties through a combination of exploitation, drilling and proven engineering extraction practices, with the most significant emphasis relating to CO2 enhanced oil recovery operations.

Interim Financial Statements

The accompanying unaudited condensed consolidated financial statements of Denbury Resources Inc. and its subsidiaries have been prepared in accordance with the rules and regulations of the Securities and Exchange Commission (“SEC”) and do not include all of the information and footnotes required by accounting principles generally accepted in the United States for complete financial statements. These financial statements and the notes thereto should be read in conjunction with our Annual Report on Form 10-K for the year ended December 31, 2015 (the “Form 10-K”). Unless indicated otherwise or the context requires, the terms “we,” “our,” “us,” “Company” or “Denbury,” refer to Denbury Resources Inc. and its subsidiaries.

Accounting measurements at interim dates inherently involve greater reliance on estimates than at year end, and the results of operations for the interim periods shown in this report are not necessarily indicative of results to be expected for the year. In management’s opinion, the accompanying unaudited condensed consolidated financial statements include all adjustments of a normal recurring nature necessary for a fair statement of our consolidated financial position as of March 31, 2016, our consolidated results of operations for the three months ended March 31, 2016 and 2015, and our consolidated cash flows for the three months ended March 31, 2016 and 2015.

Reclassifications

Certain prior period amounts have been reclassified to conform to the current year presentation. On the Unaudited Condensed Consolidated Balance Sheets, beginning “Other current assets,” “Deferred tax liabilities, net,” “Paid-in capital in excess of par” and “Accumulated deficit” have been adjusted for changes related to (1) the accounting for excess tax benefits and forfeitures associated with share-based payment transactions, (2) debt issuance costs associated with our senior subordinated notes have been reclassified from “Other assets” to “Long-term debt, net of current portion” and (3) deferred tax assets have been reclassified from “Deferred tax assets, net” to “Deferred tax liabilities, net.” Such reclassifications were made as a result of our adoption of new accounting pronouncements described in Recent Accounting Pronouncements – Recently Adopted below and had no impact on our previously reported net income or cash flows.

Net Loss per Common Share

Basic net loss per common share is computed by dividing the net loss attributable to common stockholders by the weighted average number of shares of common stock outstanding during the period. Diluted net loss per common share is calculated in the same manner, but includes the impact of potentially dilutive securities. Potentially dilutive securities consist of stock options, stock appreciation rights (“SARs”), nonvested restricted stock and nonvested performance-based equity awards. For the three months ended March 31, 2016 and 2015, there were no adjustments to net loss for purposes of calculating basic and diluted net loss per common share.

7

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

The following is a reconciliation of the weighted average shares used in the basic and diluted net loss per common share calculations for the periods indicated:

Three Months Ended | ||||||

March 31, | ||||||

In thousands | 2016 | 2015 | ||||

Basic weighted average common shares outstanding | 347,235 | 350,688 | ||||

Potentially dilutive securities | ||||||

Restricted stock, stock options, SARs and performance-based equity awards | — | — | ||||

Diluted weighted average common shares outstanding | 347,235 | 350,688 | ||||

Basic weighted average common shares exclude shares of nonvested restricted stock. As these restricted shares vest, they will be included in the shares outstanding used to calculate basic net loss per common share (although time-vesting restricted stock is issued and outstanding upon grant).

The following securities could potentially dilute earnings per share in the future, but were excluded from the computation of diluted net loss per share, as their effect would have been antidilutive:

Three Months Ended | ||||||

March 31, | ||||||

In thousands | 2016 | 2015 | ||||

Stock options and SARs | 7,412 | 10,507 | ||||

Restricted stock and performance-based equity awards | 5,097 | 2,948 | ||||

Write-Down of Oil and Natural Gas Properties

The net capitalized costs of oil and natural gas properties are limited to the lower of unamortized cost or the cost center ceiling. The cost center ceiling is defined as (1) the present value of estimated future net revenues from proved oil and natural gas reserves before future abandonment costs (discounted at 10%), based on the average first-day-of-the-month oil and natural gas price for each month during a 12-month rolling period prior to the end of a particular reporting period; plus (2) the cost of properties not being amortized; plus (3) the lower of cost or estimated fair value of unproved properties included in the costs being amortized, if any; less (4) related income tax effects. Our future net revenues from proved oil and natural gas reserves are not reduced for development costs related to the cost of drilling for and developing CO2 reserves nor those related to the cost of constructing CO2 pipelines, as those costs have previously been incurred by the Company. Therefore, we include in the ceiling test, as a reduction of future net revenues, that portion of our capitalized CO2 costs related to CO2 reserves and CO2 pipelines that we estimate will be consumed in the process of producing our proved oil and natural gas reserves. The fair value of our oil and natural gas derivative contracts is not included in the ceiling test, as we do not designate these contracts as hedge instruments for accounting purposes. The cost center ceiling test is prepared quarterly.

As a result of the precipitous and continuing decline in NYMEX oil prices since the fourth quarter of 2014, the rolling first-day-of-the-month average oil price for the preceding 12 months, after adjustments for market differentials by field, has fallen throughout 2015 and the first quarter of 2016, from $79.55 per Bbl for the first quarter of 2015 to $44.03 per Bbl for the first quarter of 2016. In addition, the first-day-of-the-month average natural gas price for the preceding 12 months, after adjustments for market differentials by field, was $3.95 per Mcf for the first quarter of 2015 and $2.22 per Mcf for the first quarter of 2016. These falling prices have led to our recognizing full cost pool ceiling test write-downs of $256.0 million and $146.2 million during the three months ended March 31, 2016 and March 31, 2015, respectively.

Recent Accounting Pronouncements

Recently Adopted

Stock Compensation. In March 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2016-09, Improvements to Employee Share-Based Payment Accounting (“ASU 2016-09”). ASU 2016-09

8

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

simplifies the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities, and classification on the statement of cash flows. The amendments in this ASU are effective for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years, and early adoption is permitted. The standard contains various amendments, each requiring a specific method of adoption, and designates whether each amendment should be adopted using a retrospective, modified retrospective, or prospective transition method. Effective January 1, 2016, we adopted ASU 2016-09. The amendments within ASU 2016-09 related to the timing of when excess tax benefits are recognized and accounting for forfeitures were adopted using a modified retrospective method. In accordance with this method, we recorded a cumulative-effect adjustment in our Unaudited Condensed Consolidated Balance Sheet as of December 31, 2015, relating to the timing of recognition of excess tax benefits, representing a $15.7 million reduction to beginning “Accumulated deficit” with the offset to “Deferred tax liabilities, net” ($14.8 million) and “Other current assets” ($0.8 million). We also recorded a cumulative-effect adjustment in our Unaudited Condensed Consolidated Balance Sheet as of December 31, 2015, to reflect actual forfeitures versus the previously-estimated forfeiture rate, representing a $0.4 million reduction to beginning “Accumulated deficit” with the offset to “Paid-in capital in excess of par.” The amendments within ASU 2016-09 related to the recognition of excess tax benefits and tax shortfalls in the income statement and presentation of excess tax benefits on the statement of cash flows were adopted prospectively, with no adjustments made to prior periods.

Income Taxes. In November 2015, the FASB issued ASU 2015-17, Income Taxes (“ASU 2015-17”). ASU 2015-17 simplifies the presentation of deferred income taxes and requires deferred tax assets and liabilities to be classified as noncurrent in the balance sheet. The amendments in this ASU are effective for fiscal years beginning after December 15, 2016, and interim periods within those fiscal years, and early adoption is permitted. Entities can transition to the standard either retrospectively to each period presented or prospectively. Effective January 1, 2016, we adopted ASU 2015-17, which has been applied retrospectively for all comparative periods presented. Accordingly, current deferred tax assets of $1.5 million have been reclassified from “Deferred tax assets, net” to “Deferred tax liabilities, net” in our Unaudited Condensed Consolidated Balance Sheet as of December 31, 2015. The adoption of ASU 2015-17 did not have an impact on our consolidated results of operations or cash flows.

Debt Issuance Costs. In April 2015, the FASB issued ASU 2015-03, Interest – Imputation of Interest: Simplifying the Presentation of Debt Issuance Costs (“ASU 2015-03”). ASU 2015-03 requires debt issuance costs related to a recognized debt liability to be presented as a direct reduction of the carrying amount of that debt in the balance sheet, consistent with the presentation of debt discounts. The amendments in this ASU are effective for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years. Entities are required to apply the guidance on a retrospective basis to each period presented as a change in accounting principle. In August 2015, the FASB issued ASU 2015-15, Interest – Imputation of Interest: Simplifying the Presentation of Debt Issuance Costs (“ASU 2015-15”) which amends ASU 2015-03 to clarify the presentation and subsequent measurement of debt issuance costs associated with line of credit arrangements, such that entities may continue to apply current practice. Effective January 1, 2016, we adopted ASU 2015-03 and ASU 2015-15, which have been applied retrospectively for all comparative periods presented. Accordingly, debt issuance costs associated with our senior subordinated notes of $32.8 million have been reclassified from “Other assets” to “Long-term debt, net of current portion” in our Unaudited Condensed Consolidated Balance Sheet as of December 31, 2015. The adoption of ASU 2015-03 and ASU 2015-15 did not have an impact on our consolidated results of operations or cash flows.

Not Yet Adopted

Leases. In February 2016, the FASB issued ASU 2016-02, Leases (“ASU 2016-02”). ASU 2016-02 amends the guidance for lease accounting to require lease assets and liabilities to be recognized on the balance sheet, along with additional disclosures regarding key leasing arrangements. The amendments in this ASU are effective for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years, and early adoption is permitted. Entities must adopt the standard using a modified retrospective transition and apply the guidance to the earliest comparative period presented, with certain practical expedients that entities may elect to apply. Management is currently assessing the impact the adoption of ASU 2016-02 will have on our consolidated financial statements.

Revenue Recognition. In May 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers (“ASU 2014-09”). ASU 2014-09 amends the guidance for revenue recognition to replace numerous, industry-specific requirements. The core principle of the ASU is that an entity should recognize revenue for the transfer of goods or services equal to the amount that it expects to be entitled to receive for those goods or services. The ASU implements a five-step process for customer contract revenue recognition that focuses on transfer of control, as opposed to transfer of risk and rewards. The amendment also requires enhanced disclosures regarding the nature, amount, timing and uncertainty of revenues and cash flows arising from contracts with

9

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

customers. In August 2015, the FASB issued ASU 2015-14, Revenue from Contracts with Customers (“ASU 2015-14”) which amends ASU 2014-09 and delays the effective date for public companies, such that the amendments in the ASU are effective for reporting periods beginning after December 15, 2017, and early adoption will be permitted for periods beginning after December 15, 2016. In March 2016, the FASB issued ASU 2016-08, Revenue from Contracts with Customers (“ASU 2016-08”) which clarifies the implementation guidance on principal versus agent considerations. Entities can transition to the standard either retrospectively to each period presented or as a cumulative-effect adjustment as of the date of adoption. Management is currently assessing the impact the adoption of ASU 2014-09, ASU 2015-14 and ASU 2016-08 will have on our consolidated financial statements.

Note 2. Long-Term Debt

The following long-term debt and capital lease obligations were outstanding as of the dates indicated:

March 31, | December 31, | |||||||

In thousands | 2016 | 2015 | ||||||

Senior Secured Bank Credit Agreement | $ | 310,000 | $ | 175,000 | ||||

6⅜% Senior Subordinated Notes due 2021 | 396,000 | 400,000 | ||||||

5½% Senior Subordinated Notes due 2022 | 1,207,745 | 1,250,000 | ||||||

4⅝% Senior Subordinated Notes due 2023 | 1,094,000 | 1,200,000 | ||||||

Other Subordinated Notes, including premium of $6 and $7, respectively | 2,256 | 2,257 | ||||||

Pipeline financings | 209,399 | 211,766 | ||||||

Capital lease obligations | 65,817 | 71,324 | ||||||

Total | 3,285,217 | 3,310,347 | ||||||

Issuance costs on senior subordinated notes | (29,803 | ) | (32,752 | ) | ||||

Total, net of debt issuance costs on senior subordinated notes | 3,255,414 | 3,277,595 | ||||||

Less: current obligations | (32,917 | ) | (32,481 | ) | ||||

Long-term debt and capital lease obligations | $ | 3,222,497 | $ | 3,245,114 | ||||

The ultimate parent company in our corporate structure, Denbury Resources Inc. (“DRI”), is the sole issuer of all of our outstanding senior subordinated notes. DRI has no independent assets or operations. Each of the subsidiary guarantors of such notes is 100% owned, directly or indirectly, by DRI, and the guarantees of the notes are full and unconditional and joint and several; any subsidiaries of DRI that are not subsidiary guarantors of such notes are minor subsidiaries.

Senior Secured Bank Credit Facility

In December 2014, we entered into an Amended and Restated Credit Agreement with JPMorgan Chase Bank, N.A., as administrative agent, and other lenders party thereto (the “Bank Credit Agreement”). The Bank Credit Agreement is a senior secured revolving credit facility with a maturity date of December 9, 2019. As of April 18, 2016, in connection with our May 2016 borrowing base redetermination requirement, we have reduced our borrowing base and lender commitments to $1.05 billion, with the next such redetermination scheduled for November 2016.

In order to provide more flexibility in managing our balance sheet, the credit extended by our lenders, and continuing compliance with maintenance financial covenants in this low oil price environment, we have entered into three amendments to the Bank Credit Agreement between May 2015 and April 2016 that have modified the Bank Credit Agreement as follows:

• | for 2016 and 2017, the maximum permitted ratio of consolidated total net debt to consolidated EBITDAX covenant has been suspended and replaced by a maximum permitted ratio of consolidated senior secured debt to consolidated EBITDAX covenant of 3.0 to 1.0 (currently, only debt under our Bank Credit Agreement is considered consolidated senior secured debt for purposes of this ratio); |

• | for 2016 and 2017, a new covenant has been added to require a minimum permitted ratio of consolidated EBITDAX to consolidated interest charges of 1.25 to 1.0; |

• | beginning in the first quarter of 2018, the ratio of consolidated total net debt to consolidated EBITDAX covenant will be reinstated, utilizing an annualized EBITDAX amount for the first quarter of 2018 and building to a trailing four quarters |

10

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

by the end of 2018, with the maximum permitted ratios being 6.0 to 1.0 for the first quarter ending March 31, 2018, 5.5 to 1.0 for the second quarter ending June 30, 2018, and 5.0 to 1.0 for the third and fourth quarters ending September 30 and December 31, 2018, and returning to 4.25 to 1.0 for the first quarter ending March 31, 2019;

• | allows for the incurrence of up to $1.0 billion of junior lien debt (subject to customary requirements); |

• | limits unrestricted cash and cash equivalents to $225 million if more than $250 million of borrowings are outstanding under the Bank Credit Agreement; and |

• | limits the amount spent on repurchases of our senior subordinated notes to $225 million. |

Additionally, such amendments provide for the following changes to the Bank Credit Agreement: (1) increases the applicable margin for ABR Loans and LIBOR Loans by 75 basis points such that the margin for ABR Loans now ranges from 1% to 2% per annum and the margin for LIBOR Loans now ranges from 2% to 3% per annum, (2) increases the commitment fee rate to 0.50%, and (3) provides for semi-annual scheduled redeterminations of the borrowing base in May and November of each year. As of March 31, 2016, we were in compliance with all debt covenants under the Bank Credit Agreement. The weighted average interest rate on borrowings outstanding as of March 31, 2016, under the Bank Credit Agreement was 2.4%.

The above description of our Bank Credit Agreement financial covenants and the changes provided for within the three amendments are qualified by the express language and defined terms contained in the Bank Credit Agreement, the First Amendment to the Bank Credit Agreement dated May 4, 2015, the Second Amendment to the Bank Credit Agreement dated February 17, 2016, and the Third Amendment to the Bank Credit Agreement dated April 18, 2016, each of which are filed as exhibits to our periodic reports filed with the SEC.

2016 Repurchases of Senior Subordinated Notes

During February and March 2016, we repurchased a total of $4.0 million in aggregate principal amount of our 6⅜% Senior Subordinated Notes due 2021 (the “2021 Notes”), $42.3 million in aggregate principal amount of our 5½% Senior Subordinated Notes due 2022 (the “2022 Notes”), and $106.0 million in aggregate principal amount of our 4⅝% Senior Subordinated Notes due 2023 (the “2023 Notes”) in open-market transactions for a total purchase price of $55.5 million, excluding accrued interest. In connection with these transactions, we recognized a $95.0 million gain on extinguishment, net of unamortized debt issuance costs written off. As of May 4, 2016, an additional $169.5 million may be spent on senior subordinated notes repurchases under the Bank Credit Agreement.

Note 3. Income Taxes

We evaluate our estimated annual effective income tax rate based on current and forecasted business results and enacted tax laws on a quarterly basis and apply this tax rate to our ordinary income or loss to calculate our estimated tax liability or benefit. As of March 31, 2016, we had $34.5 million of deferred tax assets associated with State of Louisiana net operating losses. As the result of a new tax law enacted in the State of Louisiana effective June 30, 2015, which limits a company’s utilization of certain deductions, including our net operating loss carryforwards, we recognized tax valuation allowances totaling $33.6 million during 2015 and an additional $0.9 million during the first quarter of 2016 to reduce the carrying value of our deferred tax assets. The valuation allowances will remain until the realization of future deferred tax benefits are more likely than not to become utilized.

As of March 31, 2016, we had an unrecognized tax benefit of $5.4 million related to an uncertain tax position. The unrecognized tax benefit was recorded during the fourth quarter of 2015 as a direct reduction of the associated deferred tax asset and, if recognized, would not materially affect our annual effective tax rate. The tax benefit from an uncertain tax position will only be recognized if it is more likely than not that the tax position will be sustained upon examination by the taxing authorities, based upon the technical merits of the position. We currently do not expect a material change to the uncertain tax position within the next 12 months. Our policy is to recognize penalties and interest related to uncertain tax positions in income tax expense; however, no such amounts were accrued related to the uncertain tax position as of March 31, 2016.

Note 4. Stockholders’ Equity

Dividends

During the first three quarters of 2015, the Company’s Board of Directors declared quarterly cash dividends of $0.0625 per common share, with dividends totaling $22.1 million paid to stockholders during the three months ended March 31, 2015. In

11

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

September 2015, in light of the continuing low oil price environment and our desire to maintain our financial strength and flexibility, the Company’s Board of Directors suspended our quarterly cash dividend.

Note 5. Commodity Derivative Contracts

We do not apply hedge accounting treatment to our oil and natural gas derivative contracts; therefore, the changes in the fair values of these instruments are recognized in income in the period of change. These fair value changes, along with the settlements of expired contracts, are shown under “Commodity derivatives expense (income)” in our Unaudited Condensed Consolidated Statements of Operations.

Historically, we have entered into various oil and natural gas derivative contracts to provide an economic hedge of our exposure to commodity price risk associated with anticipated future oil and natural gas production and to provide more certainty to our future cash flows. We do not hold or issue derivative financial instruments for trading purposes. Generally, these contracts have consisted of various combinations of price floors, collars, three-way collars, fixed-price swaps and fixed-price swaps enhanced with a sold put. The production that we hedge has varied from year to year depending on our levels of debt, financial strength and expectation of future commodity prices.

We manage and control market and counterparty credit risk through established internal control procedures that are reviewed on an ongoing basis. We attempt to minimize credit risk exposure to counterparties through formal credit policies, monitoring procedures and diversification, and all of our commodity derivative contracts are with parties that are lenders under our Bank Credit Agreement (or affiliates of such lenders). As of March 31, 2016, all of our outstanding derivative contracts were subject to enforceable master netting arrangements whereby payables on those contracts can be offset against receivables from separate derivative contracts with the same counterparty. It is our policy to classify derivative assets and liabilities on a gross basis on our balance sheets, even if the contracts are subject to enforceable master netting arrangements.

12

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

The following table summarizes our commodity derivative contracts as of March 31, 2016, none of which are classified as hedging instruments in accordance with the Financial Accounting Standards Board Codification (“FASC”) Derivatives and Hedging topic:

Months | Index Price | Volume (Barrels per day) | Contract Prices ($/Bbl) | |||||||||||||||||||||||

Range (1) | Weighted Average Price | |||||||||||||||||||||||||

Swap | Sold Put | Floor | Ceiling | |||||||||||||||||||||||

Oil Contracts: | ||||||||||||||||||||||||||

2016 Enhanced Swaps (2) | ||||||||||||||||||||||||||

Apr – June | NYMEX | 2,000 | $ | 90.35 | – | 90.35 | $ | 90.35 | $ | 68.00 | $ | — | $ | — | ||||||||||||

Apr – June | LLS | 6,000 | 93.30 | – | 93.50 | 93.38 | 70.00 | — | — | |||||||||||||||||

2016 Fixed-Price Swaps | ||||||||||||||||||||||||||

Apr – June | NYMEX | 11,500 | $ | 60.30 | – | 63.75 | $ | 61.84 | $ | — | $ | — | $ | — | ||||||||||||

Apr – June | LLS | 3,500 | 64.20 | – | 66.15 | 64.99 | — | — | — | |||||||||||||||||

July – Sept | NYMEX | 16,500 | 36.25 | – | 40.65 | 38.24 | — | — | — | |||||||||||||||||

July – Sept | LLS | 7,000 | 37.24 | – | 42.15 | 39.61 | — | — | — | |||||||||||||||||

Oct – Dec | NYMEX | 23,000 | 36.25 | – | 40.00 | 37.97 | — | — | — | |||||||||||||||||

Oct – Dec | LLS | 7,000 | 37.24 | – | 41.00 | 39.16 | — | — | — | |||||||||||||||||

2016 Three-Way Collars (3) | ||||||||||||||||||||||||||

Apr – June | NYMEX | 2,000 | $ | 85.00 | – | 95.50 | $ | — | $ | 68.00 | $ | 85.00 | $ | 95.50 | ||||||||||||

Apr – June | LLS | 2,000 | 88.00 | – | 98.25 | — | 70.00 | 88.00 | 98.25 | |||||||||||||||||

2016 Collars | ||||||||||||||||||||||||||

Apr – June | NYMEX | 5,000 | $ | 55.00 | – | 72.25 | $ | — | $ | — | $ | 55.00 | $ | 71.01 | ||||||||||||

Apr – June | LLS | 2,000 | 58.00 | – | 73.00 | — | — | 58.00 | 73.00 | |||||||||||||||||

July – Sept | NYMEX | 4,500 | 55.00 | – | 72.65 | — | — | 55.00 | 71.22 | |||||||||||||||||

July – Sept | LLS | 3,000 | 58.00 | – | 74.30 | — | — | 58.00 | 73.85 | |||||||||||||||||

2017 Fixed-Price Swaps | ||||||||||||||||||||||||||

Jan – Mar | NYMEX | 20,000 | $ | 41.15 | – | 44.35 | $ | 42.39 | $ | — | $ | — | $ | — | ||||||||||||

Jan – Mar | LLS | 9,000 | 42.35 | – | 45.60 | 43.51 | — | — | — | |||||||||||||||||

(1) | Ranges presented for fixed-price swaps and enhanced swaps represent the lowest and highest fixed prices of all open contracts for the period presented. For collars and three-way collars, ranges represent the lowest floor price and highest ceiling price for all open contracts for the period presented. |

(2) | An enhanced swap is a fixed-price swap contract combined with a sold put feature (at a lower price) with the same counterparty. The value associated with the sold put is used to increase or enhance the fixed price of the swap. At the contract settlement date, (1) if the index price is higher than the swap price, we pay the counterparty the difference between the index price and swap price for the contracted volumes, (2) if the index price is lower than the swap price but at or above the sold put price, the counterparty pays us the difference between the index price and the swap price for the contracted volumes and (3) if the index price is lower than the sold put price, the counterparty pays us the difference between the swap price and the sold put price for the contracted volumes. |

(3) | A three-way collar is a costless collar contract combined with a sold put feature (at a lower price) with the same counterparty. The value received for the sold put is used to enhance the contracted floor and ceiling price of the related collar. At the contract settlement date, (1) if the index price is higher than the ceiling price, we pay the counterparty the difference between the index price and ceiling price for the contracted volumes, (2) if the index price is between the floor and ceiling price, no settlements occur, (3) if the index price is lower than the floor price but at or above the sold put price, the counterparty pays us the difference between the index price and the floor price for the contracted volumes and (4) if the index price is lower than the sold put price, the counterparty pays us the difference between the floor price and the sold put price for the contracted volumes. |

13

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

Note 6. Fair Value Measurements

The FASC Fair Value Measurement topic defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (often referred to as the “exit price”). We utilize market data or assumptions that market participants would use in pricing the asset or liability, including assumptions about risk and the risks inherent in the inputs to the valuation technique. These inputs can be readily observable, market corroborated or generally unobservable. We primarily apply the income approach for recurring fair value measurements and endeavor to utilize the best available information. Accordingly, we utilize valuation techniques that maximize the use of observable inputs and minimize the use of unobservable inputs. We are able to classify fair value balances based on the observability of those inputs. The FASC establishes a fair value hierarchy that prioritizes the inputs used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurement) and the lowest priority to unobservable inputs (Level 3 measurement). The three levels of the fair value hierarchy are as follows:

• | Level 1 – Quoted prices in active markets for identical assets or liabilities as of the reporting date. |

• | Level 2 – Pricing inputs are other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable as of the reported date. Level 2 includes those financial instruments that are valued using models or other valuation methodologies. Instruments in this category include non-exchange-traded oil derivatives that are based on NYMEX pricing and fixed-price swaps that are based on regional pricing other than NYMEX (e.g., Light Louisiana Sweet). The fixed-price swap features of our enhanced swaps are valued using a discounted cash flow model based upon forward commodity price curves. Our costless collars and the sold put features of our enhanced oil swaps and three-way collars are valued using the Black-Scholes model, an industry standard option valuation model that takes into account inputs such as contractual prices for the underlying instruments, maturity, quoted forward prices for commodities, interest rates, volatility factors and credit worthiness, as well as other relevant economic measures. Substantially all of these assumptions are observable in the marketplace throughout the full term of the instrument, can be derived from observable data or are supported by observable levels at which transactions are executed in the marketplace. |

• | Level 3 – Pricing inputs include significant inputs that are generally less observable. These inputs may be used with internally developed methodologies that result in management’s best estimate of fair value. At March 31, 2016, instruments in this category include non-exchange-traded enhanced swaps, costless collars and three-way collars that are based on regional pricing other than NYMEX (e.g., Light Louisiana Sweet). The valuation models utilized for enhanced swaps, costless collars and three-way collars are consistent with the methodologies described above; however, the implied volatilities utilized in the valuation of Level 3 instruments are developed using a benchmark, which is considered a significant unobservable input. An increase or decrease of 100 basis points in the implied volatility inputs utilized in our fair value measurement would result in a change of approximately $14 thousand in the fair value of these instruments as of March 31, 2016. |

We adjust the valuations from the valuation model for nonperformance risk, using our estimate of the counterparty’s credit quality for asset positions and our credit quality for liability positions. We use multiple sources of third-party credit data in determining counterparty nonperformance risk, including credit default swaps.

14

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

The following table sets forth, by level within the fair value hierarchy, our financial assets and liabilities that were accounted for at fair value on a recurring basis as of the periods indicated:

Fair Value Measurements Using: | ||||||||||||||||

In thousands | Quoted Prices in Active Markets (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | ||||||||||||

March 31, 2016 | ||||||||||||||||

Assets | ||||||||||||||||

Oil derivative contracts – current | $ | — | $ | 49,758 | $ | 23,040 | $ | 72,798 | ||||||||

Total Assets | $ | — | $ | 49,758 | $ | 23,040 | $ | 72,798 | ||||||||

Liabilities | ||||||||||||||||

Oil derivative contracts – current | $ | — | $ | 25,005 | $ | — | $ | 25,005 | ||||||||

Total Liabilities | $ | — | $ | 25,005 | $ | — | $ | 25,005 | ||||||||

December 31, 2015 | ||||||||||||||||

Assets | ||||||||||||||||

Oil derivative contracts – current | $ | — | $ | 90,012 | $ | 52,834 | $ | 142,846 | ||||||||

Total Assets | $ | — | $ | 90,012 | $ | 52,834 | $ | 142,846 | ||||||||

Since we do not apply hedge accounting for our commodity derivative contracts, any gains and losses on our assets and liabilities are included in “Commodity derivatives expense (income)” in the accompanying Unaudited Condensed Consolidated Statements of Operations.

Level 3 Fair Value Measurements

The following table summarizes the changes in the fair value of our Level 3 assets and liabilities for the three months ended March 31, 2016 and 2015:

Three Months Ended | ||||||||

March 31, | ||||||||

In thousands | 2016 | 2015 | ||||||

Fair value of Level 3 instruments, beginning of period | $ | 52,834 | $ | 188,446 | ||||

Fair value adjustments on commodity derivatives | 281 | 25,085 | ||||||

Payment (receipts) on settlements of commodity derivatives | (30,075 | ) | (48,516 | ) | ||||

Fair value of Level 3 instruments, end of period | $ | 23,040 | $ | 165,015 | ||||

The amount of total gains for the period included in earnings attributable to the change in unrealized gains relating to assets still held at the reporting date | $ | 133 | $ | 23,099 | ||||

We utilize an income approach to value our Level 3 enhanced swaps, costless collars and three-way collars. We obtain and ensure the appropriateness of the significant inputs to the calculation, including contractual prices for the underlying instruments, maturity, forward prices for commodities, interest rates, volatility factors and credit worthiness, and the fair value estimate is prepared and reviewed on a quarterly basis. The following table details fair value inputs related to implied volatilities utilized in the valuation of our Level 3 oil derivative contracts:

15

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

Fair Value at 3/31/2016 (in thousands) | Valuation Technique | Unobservable Input | Volatility Range | |||||||

Oil derivative contracts | $ | 23,040 | Discounted cash flow / Black-Scholes | Volatility of Light Louisiana Sweet for settlement periods beginning after March 31, 2016 | 26.9% – 38.0% | |||||

Other Fair Value Measurements

The carrying value of our loans under our Bank Credit Agreement approximate fair value, as they are subject to short-term floating interest rates that approximate the rates available to us for those periods. We use a market approach to determine fair value of our fixed-rate long-term debt using observable market data. The fair values of our senior subordinated notes are based on quoted market prices. The estimated fair value of our debt as of March 31, 2016 and December 31, 2015, excluding pipeline financing and capital lease obligations, was $1,487.4 million and $1,119.0 million, respectively. We have other financial instruments consisting primarily of cash, cash equivalents, short-term receivables and payables that approximate fair value due to the nature of the instrument and the relatively short maturities.

Note 7. Commitments and Contingencies

We are involved in various lawsuits, claims and regulatory proceedings incidental to our businesses. We are also subject to audits for various taxes (income, sales and use, and severance) in the various states in which we operate, and from time to time receive assessments for potential taxes that we may owe. While we currently believe that the ultimate outcome of these proceedings, individually and in the aggregate, will not have a material adverse effect on our financial position, results of operations or cash flows, litigation is subject to inherent uncertainties. Although a single or multiple adverse rulings or settlements could possibly have a material adverse effect on our finances, we only accrue for losses from litigation and claims if we determine that a loss is probable and the amount can be reasonably estimated.

NGS Sub Corp., Evolution, et al v. Denbury Onshore, LLC

In March 2015, Evolution Petroleum Corporation (together with its subsidiaries, “Evolution”), the parent of the entity which sold Denbury Onshore, LLC (“Denbury Onshore”), a subsidiary of Denbury Resources Inc. (“DRI” and together with Denbury Onshore, “Denbury”), its original interest in Delhi Field, filed an amended petition in a lawsuit which has been pending in the 133rd Judicial District Court in Houston, Harris County, Texas since December 2013. Originally, that lawsuit involved ongoing disputes between Denbury and Evolution regarding the terms of the purchase documents under which Denbury Onshore bought its original Delhi Field interest, including disputes regarding allocation of costs in determining “payout” as defined in the agreements, and the extent and terms of assignment of reversionary interests in the unit back to Evolution following payout, along with related contractual terms. The amended petition added allegations of negligence and gross negligence against Denbury in connection with the June 2013 Delhi Field release of well fluids, and for the first time Evolution estimated its damages attributable to its allegations in the case as exceeding $200 million. The amended petition also added a claim for unspecified punitive damages. In Denbury’s answer and counterclaim, we have denied Evolution’s claims, alleged breach of contract by Evolution for failing to convey the full interest for which we paid and for violating our preferential purchase rights, and asked for a declaratory judgment as to various purchase document terms, including those pertaining to the determination of payout, the assignment of provisions of the documents, and cost sharing. Denbury has also filed a Motion for Summary Judgment seeking dismissal of Evolution’s tort claims for negligence and gross negligence.

Discovery is ongoing in the case, and the case is currently set for trial in July 2016. We believe that Evolution’s claims and requests for damages in this matter are without merit and we intend to vigorously pursue our requested relief under the purchase documents.

16

Denbury Resources Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

Note 8. Additional Balance Sheet Details

Accounts Payable and Accrued Liabilities

March 31, | December 31, | |||||||

In thousands | 2016 | 2015 | ||||||

Accrued interest | $ | 44,201 | $ | 48,908 | ||||

Accounts payable | 32,688 | 30,477 | ||||||

Accrued lease operating expenses | 30,169 | 37,549 | ||||||

Taxes payable | 17,717 | 32,438 | ||||||

Accrued compensation | 14,403 | 46,780 | ||||||

Accrued exploration and development costs | 13,500 | 20,892 | ||||||

Other | 34,037 | 36,153 | ||||||

Total | $ | 186,715 | $ | 253,197 | ||||

Note 9. Subsequent Event

During the first week of May 2016, we entered into privately negotiated exchange agreements to exchange $922.5 million in aggregate principal amount of our outstanding 2021 Notes, 2022 Notes and 2023 Notes for $531.2 million in aggregate principal amount of new 9% Senior Secured Second Lien Notes due 2021 and 36.9 million shares of Denbury common stock. The transactions are currently expected to close May 10, 2016, subject to customary closing conditions.

17

Denbury Resources Inc.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis should be read in conjunction with our Unaudited Condensed Consolidated Financial Statements and Notes thereto included herein and our Consolidated Financial Statements and Notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2015 (the “Form 10-K”), along with Management’s Discussion and Analysis of Financial Condition and Results of Operations contained in the Form 10-K. Any terms used but not defined herein have the same meaning given to them in the Form 10-K. Our discussion and analysis includes forward-looking information that involves risks and uncertainties and should be read in conjunction with Risk Factors under Item 1A of Part II of this report, along with Forward-Looking Information at the end of this section for information on the risks and uncertainties that could cause our actual results to be materially different than our forward-looking statements.

OVERVIEW

Denbury is an independent oil and natural gas company with operations focused in two key operating areas: the Gulf Coast and Rocky Mountain regions. Our goal is to increase the value of our properties through a combination of exploitation, drilling and proven engineering extraction practices, with the most significant emphasis relating to CO2 enhanced oil recovery operations.

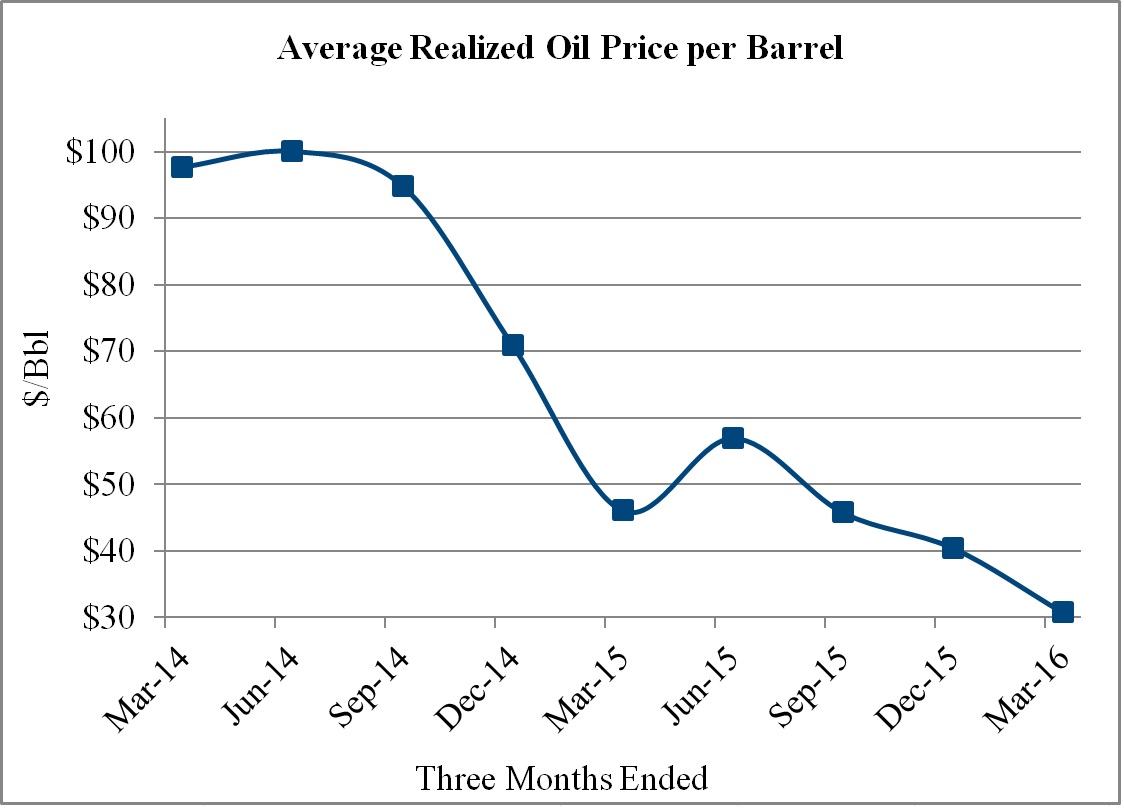

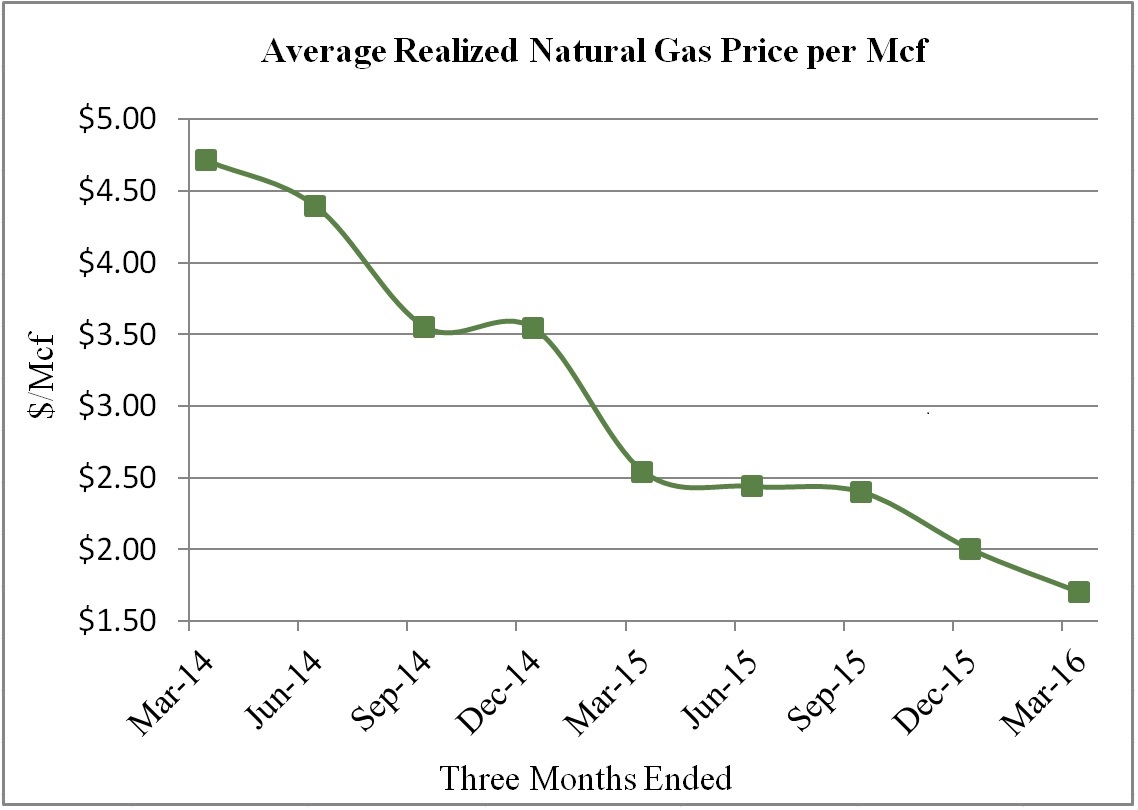

Oil Price Decline and Impact on Our Business. Oil prices generally constitute the single largest variable in our operating results. Oil prices have historically been volatile, with NYMEX prices ranging from $35 to $111 per Bbl over the last three calendar years, and prices have declined dramatically since the fourth quarter of 2014 to less than $27 per Bbl in January 2016, the lowest level in over 13 years. The following charts illustrate the fluctuations in our realized oil and natural gas prices, excluding the impact of commodity derivative settlements, during 2014, 2015 and the first quarter of 2016.

Three Months Ended | ||||||||||||||||||||||||||||||||||||||

Average realized prices | 3/31/14 | 6/30/14 | 9/30/14 | 12/31/14 | 3/31/15 | 6/30/15 | 9/30/15 | 12/31/15 | 3/31/16 | |||||||||||||||||||||||||||||

Oil price per Bbl | $ | 97.69 | $ | 100.04 | $ | 94.78 | $ | 70.80 | $ | 46.02 | $ | 56.92 | $ | 45.74 | $ | 40.41 | $ | 30.71 | ||||||||||||||||||||

Natural gas price per Mcf | 4.71 | 4.39 | 3.55 | 3.54 | 2.54 | 2.44 | 2.40 | 2.00 | 1.70 | |||||||||||||||||||||||||||||

As oil prices continued to decline in the first quarter of 2016 from already depressed levels, our focus remained on cost reductions and preserving liquidity. We continue to take steps to reduce our costs in all categories of our business, and we have made significant progress in that regard as demonstrated in our first quarter results discussed below. We have set our capital development budget (excluding capitalized interest) at $200 million for 2016, which we currently anticipate will primarily be funded with cash flow from operations, thus preserving our liquidity. One advantage we have in this environment is that our oil assets have relatively low decline rates, and therefore we anticipate that our production will decline by less than 10% in 2016, assuming the mid-point of our production guidance, even with our significantly reduced planned capital spending level. This decline rate is even lower if we exclude wells that we anticipate will be shut in for economic reasons. Lastly, we have hedged

18

Denbury Resources Inc.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

approximately half of our estimated production through the second quarter of 2017 in order to cover our current level of cash costs and to help mitigate any future price declines or sustained low oil prices.

During this period of reduced capital spending, we have continued to evaluate our assets with a goal of increasing the value of both existing assets and future projects by optimizing field operational and development plans, reducing CO2 injection volumes due to increased efficiency, and reducing costs such as power and workovers. Over the past year, we have reduced our CO2 injection volumes by 35% and our lease operating expenses by 27% when comparing the first quarters of 2015 and 2016. These initiatives aim to increase the profitability of our assets, making them more resilient to lower oil prices. Together, we believe these initiatives will help us manage through this low oil price environment and provide us with liquidity for the foreseeable future.

As more fully discussed under Capital Resources and Liquidity below, our banks recently completed their borrowing base redetermination under our senior secured bank credit facility, which resulted in a reduction in the banks’ commitment level under our facility from $1.5 billion to $1.05 billion. In addition, we entered into an amendment to our senior secured bank credit facility terms in February 2016 to relax certain of our financial covenants in 2016 and 2017, and we entered into another amendment in April 2016, which allows for up to $1.0 billion in junior lien debt capacity. As of March 31, 2016, we had $310.0 million drawn on our senior secured bank credit facility, leaving us with $680.7 million in availability under our bank line after adjusting for the recently revised commitment level. Borrowings under our senior secured bank credit facility increased from $175.0 million at December 31, 2015, due in part to $55.5 million utilized to purchase $152.3 million in aggregate principal amount of senior subordinated notes in open-market transactions, resulting in a net reduction of $96.7 million in our long-term debt (see Capital Resources and Liquidity – 2016 Repurchases of Senior Subordinated Notes below). The remaining portion of the increase in our senior secured bank credit facility balance from December 31, 2015 is primarily due to seasonal working capital outflows in the first quarter of 2016 associated with accrued compensation, ad valorem taxes and semi-annual interest payments on our senior subordinated notes.

Recent Debt Reduction Transactions. During February and March 2016, we reduced our outstanding long-term indebtedness through open-market purchases, and in May 2016 we entered into exchange agreements with a limited number of holders of our outstanding senior subordinated notes to exchange these notes for the Company’s 9% Senior Secured Second Lien Notes due 2021. The transactions are currently expected to close May 10, 2016, subject to customary closing conditions. See Capital Resources and Liquidity – 2016 Repurchases of Senior Subordinated Notes and 2016 Senior Subordinated Notes Exchange Agreements for further discussion.

Operating Highlights. Our financial results continue to be impacted by the decrease in realized oil prices as highlighted above, which decreased from an average of $46.02 per Bbl in the first quarter of 2015 to $30.71 in the first quarter of 2016. During the first quarter of 2016, we recognized a net loss of $185.2 million, or $0.53 per diluted common share, compared to a net loss of $107.7 million, or $0.31 per diluted common share, during the first quarter of 2015. The change in net loss between the first quarter of 2015 and 2016 was primarily due to the increase in the size of our full cost pool ceiling test write-down of our oil and natural gas properties, which totaled $256.0 million ($160.5 million net of tax) in the 2016 quarter (see Write-Down of Oil and Natural Gas Properties below), partially offset by a $95.0 million gain on debt extinguishment in the first quarter of 2016. Other significant changes between the first quarter of 2015 and 2016 were a $109.7 million (37%) decline in our oil and natural gas revenues between the periods, which was primarily oil-price related, and a $105.9 million decrease in commodity derivatives income, offset in part by a $72.6 million (48%) decrease in depletion, depreciation, and amortization, a $38.6 million (27%) reduction in lease operating expense, a $12.4 million (27%) decrease in general and administrative expenses, and a $6.6 million (25%) decrease in taxes other than income. The $105.9 million decrease in commodity derivatives income between the two periods was due to a $29.7 million increased loss associated with noncash fair value commodity adjustments and $76.2 million less in receipts from settlements of derivative contracts during the 2016 period.

We generated $2.0 million of cash flows from operating activities in the first quarter of 2016, compared to $164.9 million in the fourth quarter of 2015 and $137.8 million in the prior-year first quarter. These results include cash outflows for seasonal working capital changes of $54.8 million and $57.7 million during the three months ending March 31, 2016 and 2015, respectively, compared to cash inflows for working capital changes of $35.6 million during the three months ending December 31, 2015. The decrease in cash flows from operations between the first quarter of 2015 and 2016 was due primarily to lower oil prices, which caused a decrease in oil revenues, and approximately 51% lower receipts on derivative settlements, partially offset by reductions in lease operating expenses, general and administrative expenses, and taxes other than income.

19

Denbury Resources Inc.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

During the first quarter of 2016, our oil and natural gas production, which was 95% oil, averaged 69,351 BOE/d, compared to an average of 74,356 BOE/d produced during the first quarter of 2015 and 72,002 BOE/d during the fourth quarter of 2015. The year-over-year and sequential quarterly declines were primarily due to natural production declines based on our lower capital spending level, coupled with production shut in due to economics, as oil prices declined further during the quarter. We estimate that approximately 2,800 BOE/d of production was shut in as of March 31, 2016 attributable to uneconomic wells, resulting in a decrease to sequential quarterly production of approximately 1,100 BOE/d. We estimate that approximately one-half of the production currently shut in is profitable at $50 per Bbl, approximately two-thirds at $60 per Bbl, with the remainder requiring an oil price in excess of $60 per Bbl in order to be economic. See Results of Operations – Production for further discussion.

Our average realized oil price per barrel, excluding the impact of commodity derivative contracts, was $30.71 per Bbl during the first quarter of 2016, a decrease of 33% compared to $46.02 per Bbl realized during the first quarter of 2015 and a decrease of 24% compared to $40.41 per Bbl realized during the fourth quarter of 2015. The oil price we realized relative to NYMEX oil prices (our NYMEX oil price differential) was $3.02 per Bbl below NYMEX prices in the first quarter of 2016, compared to a negative $2.81 per-Bbl NYMEX differential in the first quarter of 2015 and a negative $1.74 per-Bbl NYMEX differential in the fourth quarter of 2015. The weakening in our oil price differential in comparison to its level in the first quarter of 2015 was principally due to weakening of our Light Louisiana Sweet (“LLS”) premium relative to NYMEX oil prices.

One of our primary focuses in the past few years has been to reduce costs throughout the organization, through a number of internal initiatives. As a result of these efforts, we have been able to make continued reductions in our lease operating expenses, and in the first quarter of 2016 these expenses were $16.23 per BOE, a 16% decrease on a sequential-quarter basis and a 23% decrease when compared to per-BOE levels in the first quarter of 2015. In addition, our recurring lease operating expenses per BOE decreased in each sequential quarter in 2014 and 2015 and decreased a total of 38% between fourth-quarter 2013 levels and those in the first quarter of 2016, with decreases realized in most categories of lease operating expenses, the most significant of which were workover costs, CO2 costs, power costs, and certain third-party contractor and vendor costs.

Write-Down of Oil and Natural Gas Properties. Due to a continued decline in the rolling first-day-of-the-month average oil and natural gas price for the preceding 12-month periods in 2015 and 2016, we recognized full cost pool ceiling test write-downs of $256.0 million and $146.2 million during the three months ended March 31, 2016 and March 31, 2015, respectively. See Note 1, Basis of Presentation – Write-Down of Oil and Natural Gas Properties, to the Unaudited Condensed Consolidated Financial Statements, and Results of Operations – Write-Down of Oil and Natural Gas Properties for additional information regarding the ceiling test.

Impact of Commodity Price Decline on Proved Oil and Natural Gas Reserves Quantities. Declines in commodity prices may materially impact estimated quantities of proved reserves, as certain reserves may reach the point at which they become uneconomic to produce earlier than they would otherwise. The SEC requires proved reserves to be determined based on average first-day-of-the-month oil and natural gas prices for the trailing 12-month period. Using these prices, our total proved reserves at December 31, 2015, were 288.6 MMBOE, of which 98% was oil and 2% was natural gas. During 2015 and the first quarter of 2016, the average first-day-of-the-month NYMEX oil price used in estimating our proved reserves declined from $50.28 per Bbl at December 31, 2015, to $46.26 per Bbl at March 31, 2016, and for natural gas declined from $2.63 per MMBtu at December 31, 2015, to $2.45 per MMBtu at March 31, 2016. Although we had no significant change in our reserve quantities during the first quarter of 2016, based on current NYMEX futures prices, during 2016, we currently expect negative price revisions of less than 10% of our 2015 year-end proved reserves. The actual reserve revisions could occur for various reasons, including differences in actual commodity prices from commodity futures prices and changes in oil and natural gas price differentials, forecasted production rates, forecasted operating and capital costs, and changes in development plans, all of which are key assumptions in estimating proved oil and natural gas reserves.

CAPITAL RESOURCES AND LIQUIDITY

Overview. Our primary sources of capital and liquidity are our cash flows from operations and availability of borrowing capacity under our senior secured bank credit facility. Outstanding borrowings under our senior secured bank credit facility were $310.0 million as of March 31, 2016, compared to $175.0 million as of December 31, 2015. The $135.0 million increase in borrowings includes $55.5 million utilized to repurchase $152.3 million in aggregate principal amount of senior subordinated notes in open-market transactions, with the remainder primarily due to seasonal working capital outflows in the first quarter of 2016 associated with accrued compensation, ad valorem taxes and semi-annual interest payments on our senior subordinated notes. As a result of the significant reduction in oil prices discussed above and less advantageous hedge positions, our cash flow from

20

Denbury Resources Inc.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

operations has significantly decreased, from $137.8 million during the three months ended March 31, 2015 and $164.9 million during the three months ended December 31, 2015, to $2.0 million during the three months ended March 31, 2016.

The culmination of these factors places a significant priority on the preservation of cash and liquidity until oil prices improve. We have taken and will continue to take steps to lower our costs in all categories of our business, and we have made significant progress in that regard. We also amended our Bank Credit Agreement in the first quarter of 2016 to relax certain bank covenants through 2017 to address potential covenant compliance issues if oil prices remain at levels comparable to the first quarter of 2016. As of March 31, 2016, we had $310.0 million drawn on our senior secured bank credit facility, leaving us $680.7 million of current liquidity after consideration of $59.3 million of outstanding letters of credit and adjusting for the recently revised lender commitment level of $1.05 billion. This liquidity, coupled with our other cost saving and liquidity measures, should be sufficient to supplement our capital or operating cash outflows as needed until oil prices improve, which we believe will be in the next twelve to eighteen months. Based upon our current forecasted levels of production and costs, hedges in place as of May 2, 2016, and current oil commodity futures prices, we currently anticipate continuing to be in compliance with our bank covenants during 2016 and 2017.

To protect our liquidity, we have entered into additional oil swaps for the second half of 2016 and the first half of 2017, such that we now have approximately half of our estimated oil production hedged through the first half of 2017. While these prices are not sufficient to provide enough cash flow to grow our production, they do at least cover our most recent total cash costs which were in a per-barrel range in the low $30’s in the first quarter of 2016, including corporate overhead and interest, thereby minimizing the amount that would be required for day-to-day operations from our bank line.

Senior Secured Bank Credit Facility. As of March 31, 2016, we had $310.0 million of debt outstanding (based on a $1.05 billion commitment level from our banks) and $59.3 million in letters of credit on the senior secured bank credit facility. In order to provide more flexibility in managing our balance sheet, the credit extended by our lenders, and continuing compliance with maintenance financial covenants in this low oil price environment, we have entered into three amendments to the Bank Credit Agreement between May 2015 and April 2016 that have modified the Bank Credit Agreement as follows:

• | for 2016 and 2017, the maximum permitted ratio of consolidated total net debt to consolidated EBITDAX covenant has been suspended and replaced by a maximum permitted ratio of consolidated senior secured debt to consolidated EBITDAX covenant of 3.0 to 1.0 (currently, only debt under our Bank Credit Agreement is considered consolidated senior secured debt for purposes of this ratio); |

• | for 2016 and 2017, a new covenant has been added to require a minimum permitted ratio of consolidated EBITDAX to consolidated interest charges of 1.25 to 1.0; |

• | beginning in the first quarter of 2018, the ratio of consolidated total net debt to consolidated EBITDAX covenant will be reinstated, utilizing an annualized EBITDAX amount for the first quarter of 2018 and building to a trailing four quarters by the end of 2018, with the maximum permitted ratios being 6.0 to 1.0 for the first quarter ending March 31, 2018, 5.5 to 1.0 for the second quarter ending June 30, 2018, and 5.0 to 1.0 for the third and fourth quarters ending September 30 and December 31, 2018, and returning to 4.25 to 1.0 for the first quarter ending March 31, 2019; |

• | allows for the incurrence of up to $1.0 billion of junior lien debt (subject to customary requirements); |

• | limits unrestricted cash and cash equivalents to $225 million if more than $250 million of borrowings are outstanding under the Bank Credit Agreement; and |

• | limits the amount spent on repurchases of our senior subordinated notes to $225 million. |

For these financial performance covenant calculations as of March 31, 2016, our ratio of consolidated senior secured debt to consolidated EBITDAX was 0.36 to 1.0, our ratio of consolidated EBITDAX to consolidated interest charges was 4.71 to 1.0, and our current ratio was 4.99. Based upon our current forecasted levels of production and costs, hedges in place as of May 2, 2016, and current oil commodity futures prices, we currently anticipate continuing to be in compliance with our bank covenants during 2016 and 2017.

The above description of our Bank Credit Agreement financial covenants and the changes provided for within the three amendments are qualified by the express language and defined terms contained in the Bank Credit Agreement, the First Amendment to the Bank Credit Agreement dated May 4, 2015, the Second Amendment to the Bank Credit Agreement dated February 17, 2016 (the “Second Amendment”), and the Third Amendment to the Bank Credit Agreement dated April 18, 2016 (the “Third Amendment”), each of which are filed as exhibits to our periodic reports filed with the SEC.

21

Denbury Resources Inc.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

2016 Repurchases of Senior Subordinated Notes. During the first quarter of 2016, we repurchased a total of $152.3 million in aggregate principal amount of our existing senior subordinated notes in open-market transactions, consisting of $4.0 million in aggregate principal amount of our 6⅜% Senior Subordinated Notes due 2021 (the “2021 Notes”), $42.3 million in aggregate principal amount of our 5½% Senior Subordinated Notes due 2022 (the “2022 Notes”), and $106.0 million in aggregate principal amount of our 4⅝% Senior Subordinated Notes due 2023 (the “2023 Notes”) for a total purchase price of $55.5 million, excluding accrued interest. The repurchases were made at prices ranging from approximately 25% to 45% of the principal amount of the individual senior subordinated notes. In connection with these transactions, we recognized a $95.0 million gain on extinguishment, net of unamortized debt issuance costs written off. We currently estimate saving approximately $6 million in annual cash interest related to these repurchases, which takes into account the reduction in debt and the lower interest rate on our bank credit facility as compared to the senior subordinated notes. The Second Amendment limits the amount of these open-market repurchases of our senior subordinated notes to $225 million, so as of May 4, 2016, after taking these repurchases into account, we have an additional $169.5 million remaining to spend on senior subordinated notes repurchases.

2016 Senior Subordinated Notes Exchange Agreements. During the first week of May 2016, we entered into privately negotiated exchange agreements to exchange $126.6 million in aggregate principal amount of our 2021 Notes, $351.6 million in aggregate principal amount of our 2022 Notes, and $444.2 million in aggregate principal amount of our 2023 Notes for $531.2 million in aggregate principal amount of new 9% Senior Secured Second Lien Notes due 2021 plus 36.9 million shares of Denbury common stock. The transactions are currently expected to close May 10, 2016, subject to customary closing conditions. We expect to realize a minimal reduction in cash interest related to these transactions. Our Bank Credit Agreement allows for the incurrence of up to $1.0 billion of junior lien debt, so after taking these exchanges into account, we have an additional $468.8 million of junior lien debt capacity that remains available to us. Combined with the repurchases of senior subordinated notes in open-market transactions during February and March 2016, these transactions will result in a net reduction of the Company’s debt of approximately $488 million.

Capital Spending. We anticipate that our full-year 2016 capital budget, excluding capitalized interest and acquisitions, will be approximately $200 million, which includes approximately $55 million in capitalized internal acquisition, exploration and development costs and pre-production tertiary startup costs. This combined 2016 capital budget amount, excluding capitalized interest and acquisitions, is comprised of the following:

• | $100 million allocated for tertiary oil field expenditures; |

• | $35 million allocated for other areas, primarily non-tertiary oil field expenditures; |

• | $10 million to be spent on CO2 sources and pipeline construction; and |

• | $55 million for other capital items such as capitalized internal acquisition, exploration and development costs and pre-production tertiary startup costs. |