Attached files

| file | filename |

|---|---|

| EX-31.1 - SECTION 302 CERTIFICATION - Hyatt Hotels Corp | exhibit311-33116.htm |

| EX-32.1 - SECTION 906 CERTIFICATION - Hyatt Hotels Corp | exhibit321-33116.htm |

| EX-31.2 - SECTION 302 CERTIFICATION - Hyatt Hotels Corp | exhibit312-33116.htm |

| EX-32.2 - SECTION 906 CERTIFICATION - Hyatt Hotels Corp | exhibit322-33116.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

Form 10-Q

(Mark One)

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 2016

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 001-34521

HYATT HOTELS CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

Delaware | 20-1480589 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

71 South Wacker Drive 12th Floor, Chicago, Illinois | 60606 | |

(Address of Principal Executive Offices) | (Zip Code) | |

(312) 750-1234

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check One):

Large accelerated filer | x | Accelerated filer | ¨ | ||

Non-accelerated filer | ¨ | Smaller reporting company | ¨ | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of April 29, 2016, there were 24,742,779 shares of the registrant’s Class A common stock, $0.01 par value, outstanding and 109,628,962 shares of the registrant’s Class B common stock, $0.01 par value, outstanding.

HYATT HOTELS CORPORATION

QUARTERLY REPORT ON FORM 10-Q

FOR THE PERIOD ENDED MARCH 31, 2016

TABLE OF CONTENTS

PART I – FINANCIAL INFORMATION | ||

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II – OTHER INFORMATION | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements.

HYATT HOTELS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME

(In millions of dollars, except per share amounts)

(Unaudited)

Three Months Ended | |||||||

March 31, 2016 | March 31, 2015 | ||||||

REVENUES: | |||||||

Owned and leased hotels | $ | 516 | $ | 509 | |||

Management and franchise fees | 107 | 105 | |||||

Other revenues | 9 | 7 | |||||

Other revenues from managed properties | 457 | 433 | |||||

Total revenues | 1,089 | 1,054 | |||||

DIRECT AND SELLING, GENERAL, AND ADMINISTRATIVE EXPENSES: | |||||||

Owned and leased hotels | 389 | 384 | |||||

Depreciation and amortization | 81 | 79 | |||||

Other direct costs | 6 | 5 | |||||

Selling, general, and administrative | 88 | 94 | |||||

Other costs from managed properties | 457 | 433 | |||||

Direct and selling, general, and administrative expenses | 1,021 | 995 | |||||

Net gains and interest income from marketable securities held to fund operating programs | 1 | 8 | |||||

Equity earnings (losses) from unconsolidated hospitality ventures | 2 | (6 | ) | ||||

Interest expense | (17 | ) | (17 | ) | |||

Gain on sale of real estate | — | 8 | |||||

Other loss, net | (4 | ) | (18 | ) | |||

INCOME BEFORE INCOME TAXES | 50 | 34 | |||||

PROVISION FOR INCOME TAXES | (16 | ) | (12 | ) | |||

NET INCOME | 34 | 22 | |||||

NET INCOME ATTRIBUTABLE TO NONCONTROLLING INTERESTS | — | — | |||||

NET INCOME ATTRIBUTABLE TO HYATT HOTELS CORPORATION | $ | 34 | $ | 22 | |||

EARNINGS PER SHARE—Basic | |||||||

Net income | $ | 0.25 | $ | 0.15 | |||

Net income attributable to Hyatt Hotels Corporation | $ | 0.25 | $ | 0.15 | |||

EARNINGS PER SHARE—Diluted | |||||||

Net income | $ | 0.25 | $ | 0.15 | |||

Net income attributable to Hyatt Hotels Corporation | $ | 0.25 | $ | 0.15 | |||

See accompanying notes to condensed consolidated financial statements.

1

HYATT HOTELS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(In millions of dollars)

(Unaudited)

Three Months Ended | |||||||

March 31, 2016 | March 31, 2015 | ||||||

Net income | $ | 34 | $ | 22 | |||

Other comprehensive income (loss), net of taxes: | |||||||

Foreign currency translation adjustments, net of tax expense of $- and $- for the three months ended March 31, 2016 and March 31, 2015, respectively | 24 | (55 | ) | ||||

Unrealized gains (losses) on available for sale securities, net of tax (benefit) expense of $(3) and $- for the three months ended March 31, 2016 and March 31, 2015, respectively | (4 | ) | 2 | ||||

Other comprehensive income (loss) | 20 | (53 | ) | ||||

COMPREHENSIVE INCOME (LOSS) | 54 | (31 | ) | ||||

COMPREHENSIVE INCOME ATTRIBUTABLE TO NONCONTROLLING INTERESTS | — | — | |||||

COMPREHENSIVE INCOME (LOSS) ATTRIBUTABLE TO HYATT HOTELS CORPORATION | $ | 54 | $ | (31 | ) | ||

See accompanying notes to condensed consolidated financial statements.

2

HYATT HOTELS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(In millions of dollars, except share and per share amounts)

(Unaudited)

March 31, 2016 | December 31, 2015 | ||||||

ASSETS | |||||||

CURRENT ASSETS: | |||||||

Cash and cash equivalents | $ | 771 | $ | 457 | |||

Restricted cash | 73 | 96 | |||||

Short-term investments | 55 | 46 | |||||

Receivables, net of allowances of $16 and $15 at March 31, 2016 and December 31, 2015, respectively | 328 | 298 | |||||

Inventories | 16 | 12 | |||||

Prepaids and other assets | 160 | 152 | |||||

Prepaid income taxes | 59 | 63 | |||||

Total current assets | 1,462 | 1,124 | |||||

Investments | 332 | 327 | |||||

Property and equipment, net | 4,023 | 4,031 | |||||

Financing receivables, net of allowances | 20 | 20 | |||||

Goodwill | 129 | 129 | |||||

Intangibles, net | 546 | 547 | |||||

Deferred tax assets | 305 | 301 | |||||

Other assets | 1,082 | 1,112 | |||||

TOTAL ASSETS | $ | 7,899 | $ | 7,591 | |||

LIABILITIES AND EQUITY | |||||||

CURRENT LIABILITIES: | |||||||

Current maturities of long-term debt | $ | 265 | $ | 328 | |||

Accounts payable | 135 | 141 | |||||

Accrued expenses and other current liabilities | 516 | 516 | |||||

Accrued compensation and benefits | 96 | 122 | |||||

Total current liabilities | 1,012 | 1,107 | |||||

Long-term debt | 1,441 | 1,042 | |||||

Other long-term liabilities | 1,446 | 1,447 | |||||

Total liabilities | 3,899 | 3,596 | |||||

Commitments and contingencies (see Note 11) | |||||||

EQUITY: | |||||||

Preferred stock, $0.01 par value per share, 10,000,000 shares authorized and none outstanding as of March 31, 2016 and December 31, 2015 | — | — | |||||

Class A common stock, $0.01 par value per share, 1,000,000,000 shares authorized, 25,157,815 issued and outstanding at March 31, 2016, and Class B common stock, $0.01 par value per share, 441,623,374 shares authorized, 109,628,962 shares issued and outstanding at March 31, 2016. Class A common stock, $0.01 par value per share, 1,000,000,000 shares authorized, 26,604,687 issued and outstanding at December 31, 2015, and Class B common stock, $0.01 par value per share, 441,623,374 shares authorized, 109,628,962 shares issued and outstanding at December 31, 2015 | 1 | 1 | |||||

Additional paid-in capital | 1,882 | 1,931 | |||||

Retained earnings | 2,323 | 2,289 | |||||

Accumulated other comprehensive loss | (210 | ) | (230 | ) | |||

Total stockholders’ equity | 3,996 | 3,991 | |||||

Noncontrolling interests in consolidated subsidiaries | 4 | 4 | |||||

Total equity | 4,000 | 3,995 | |||||

TOTAL LIABILITIES AND EQUITY | $ | 7,899 | $ | 7,591 | |||

See accompanying notes to condensed consolidated financial statements.

3

HYATT HOTELS CORPORATION AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In millions of dollars)

(Unaudited)

Three Months Ended | |||||||

March 31, 2016 | March 31, 2015 | ||||||

CASH FLOWS FROM OPERATING ACTIVITIES: | |||||||

Net income | $ | 34 | $ | 22 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 81 | 79 | |||||

Deferred income taxes | (1 | ) | 3 | ||||

Equity (earnings) losses from unconsolidated hospitality ventures, net of distributions received | (1 | ) | 6 | ||||

Foreign currency losses | — | 7 | |||||

Gain on sale of real estate | — | (8 | ) | ||||

Working capital changes and other | (62 | ) | (94 | ) | |||

Net cash provided by operating activities | 51 | 15 | |||||

CASH FLOWS FROM INVESTING ACTIVITIES: | |||||||

Purchases of marketable securities and short-term investments | (85 | ) | (157 | ) | |||

Proceeds from marketable securities and short-term investments | 83 | 175 | |||||

Contributions to investments | (15 | ) | (12 | ) | |||

Capital expenditures | (38 | ) | (61 | ) | |||

Proceeds from sale of real estate, net of cash disposed | — | 69 | |||||

Sales proceeds transferred from escrow to cash and cash equivalents | 29 | — | |||||

(Increase) decrease in restricted cash—investing | (12 | ) | 18 | ||||

Other investing activities | 26 | 9 | |||||

Net cash (used in) provided by investing activities | (12 | ) | 41 | ||||

CASH FLOWS FROM FINANCING ACTIVITIES: | |||||||

Proceeds from long-term debt, net of issuance costs of $4 and $0, respectively | 426 | — | |||||

Repayments of long-term debt | (95 | ) | — | ||||

Repurchase of common stock | (63 | ) | (187 | ) | |||

Other financing activities | (4 | ) | (6 | ) | |||

Net cash provided by (used in) financing activities | 264 | (193 | ) | ||||

EFFECT OF EXCHANGE RATE CHANGES ON CASH | 11 | 15 | |||||

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | 314 | (122 | ) | ||||

CASH AND CASH EQUIVALENTS—BEGINNING OF YEAR | 457 | 685 | |||||

CASH AND CASH EQUIVALENTS—END OF PERIOD | $ | 771 | $ | 563 | |||

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | |||||||

Cash paid during the period for interest | $ | 33 | $ | 32 | |||

Cash paid during the period for income taxes | $ | 16 | $ | 18 | |||

Non-cash investing activities are as follows: | |||||||

Change in accrued capital expenditures | $ | 4 | $ | (6 | ) | ||

See accompanying notes to condensed consolidated financial statements.

4

HYATT HOTELS CORPORATION AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(amounts in millions of dollars, unless otherwise indicated)

(Unaudited)

1. ORGANIZATION

Hyatt Hotels Corporation, a Delaware corporation, and its consolidated subsidiaries (collectively "Hyatt Hotels Corporation") provide hospitality services on a worldwide basis through the development, ownership, operation, management, franchising and licensing of hospitality related businesses. We develop, own, operate, manage, franchise, license or provide services to a portfolio of properties consisting of full service hotels, select service hotels, resorts and other properties, including timeshare, fractional and other forms of residential or vacation properties. As of March 31, 2016, (i) we operated or franchised 296 full service hotels, comprising 117,998 rooms throughout the world, (ii) we operated or franchised 316 select service hotels, comprising 43,574 rooms, of which 296 hotels are located in the United States, and (iii) our portfolio of properties included 6 franchised all inclusive Hyatt-branded resorts, comprising 2,401 rooms. Our portfolio of properties operates in 53 countries around the world and we hold ownership interests in certain of these properties.

As used in these Notes and throughout this Quarterly Report on Form 10-Q, (i) the terms "Company," "HHC," "we," "us," or "our" mean Hyatt Hotels Corporation and its consolidated subsidiaries and (ii) the term "portfolio of properties" refers to hotels and other properties or residential ownership units that we develop, own, operate, manage, franchise, license or provide services to, including under our Park Hyatt, Grand Hyatt, Hyatt Regency, Hyatt, Andaz, Hyatt Centric, The Unbound Collection by Hyatt, Hyatt Place, Hyatt House, Hyatt Ziva, Hyatt Zilara and Hyatt Residence Club brands.

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") for interim financial information, the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all information or footnotes required by GAAP for complete annual financial statements. As a result, this Quarterly Report on Form 10-Q should be read in conjunction with the Consolidated Financial Statements and accompanying Notes in our Annual Report on Form 10-K for the fiscal year ended December 31, 2015 (the "2015 Form 10-K").

We have eliminated all intercompany accounts and transactions in our condensed consolidated financial statements. We consolidate entities under our control, including entities where we are deemed to be the primary

beneficiary.

Management believes that the accompanying condensed consolidated financial statements reflect all adjustments, which are all of a normal recurring nature, considered necessary for a fair presentation of the interim periods.

2. RECENTLY ISSUED ACCOUNTING STANDARDS

Adopted Accounting Standards—In April 2015, the Financial Accounting Standards Board ("FASB") released Accounting Standards Update No. 2015-03 ("ASU 2015-03"), Interest - Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs. ASU 2015-03 requires that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The provisions of ASU 2015-03 are effective for interim periods and fiscal years beginning after December 15, 2015. We adopted the standard on January 1, 2016, and as a result we reclassified $5 million of debt issuance costs previously included in other assets to long-term debt on our condensed consolidated financial statements as of December 31, 2015.

Future Adoption of Accounting Standards—In May 2014, the FASB released Accounting Standards Update No. 2014-09 ("ASU 2014-09"), Revenue from Contracts with Customers (Topic 606). ASU 2014-09 provides a single, comprehensive revenue recognition model for contracts with customers. In August 2015, the FASB released Accounting Standards Update No. 2015-14 ("ASU 2015-14"), Revenue from Contracts with Customers (Topic 606): Deferral of the Effective Date. ASU 2015-14 delays the effective date of ASU 2014-09 by one year, making it effective for interim periods and fiscal years beginning after December 15, 2017, with early adoption permitted as of the original effective date. The Company is currently evaluating the impact of adopting ASU 2014-09.

5

In January 2016, the FASB released Accounting Standards Update No. 2016-01 ("ASU 2016-01"), Financial Instruments - Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities. ASU 2016-01 revises the accounting for equity investments, financial liabilities under the fair value option, and the presentation and disclosure requirements for financial instruments. The provisions of ASU 2016-01 are effective for interim periods and fiscal years beginning after December 15, 2017. The Company is currently evaluating the impact of adopting ASU 2016-01.

In February 2016, the FASB released Accounting Standards Update No. 2016-02 ("ASU 2016-02"), Leases (Topic 842). ASU 2016-02 requires lessees to record lease contracts on the balance sheet by recognizing a right-of-use asset and lease liability. The provisions of ASU 2016-02 are effective for interim periods and fiscal years beginning after December 15, 2018, with early adoption permitted. The Company is currently evaluating the impact of adopting ASU 2016-02.

In March 2016, the FASB released Accounting Standards Update No. 2016-09 ("ASU 2016-09"), Compensation-Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting. ASU 2016-09 simplifies the accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities, and classification on the statement of cash flows. The provisions of ASU 2016-09 are effective for interim periods and fiscal years beginning after December 15, 2016, with early adoption permitted. The Company is currently evaluating the impact of adopting ASU 2016-09.

3. EQUITY AND COST METHOD INVESTMENTS

We have investments that are recorded under both the equity and cost methods. These investments are considered to be an integral part of our business and are strategically and operationally important to our overall results. Our equity and cost method investment balances recorded at March 31, 2016 and December 31, 2015 are as follows:

March 31, 2016 | December 31, 2015 | ||||||

Equity method investments | $ | 309 | $ | 304 | |||

Cost method investments | 23 | 23 | |||||

Total investments | $ | 332 | $ | 327 | |||

The following table presents summarized financial information for all unconsolidated ventures in which we hold an investment that is accounted for under the equity method:

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Total revenues | $ | 284 | $ | 244 | |||

Gross operating profit | 70 | 60 | |||||

Income (loss) from continuing operations | 20 | (13 | ) | ||||

Net income (loss) | 20 | (13 | ) | ||||

4. MARKETABLE SECURITIES

We hold marketable securities to fund certain operating programs and for investment purposes. We periodically transfer cash and cash equivalents to time deposits, highly liquid and transparent commercial paper, corporate notes and bonds, and U.S. government obligations and obligations of other government agencies for investment purposes.

6

Marketable Securities Held to Fund Operating Programs—At March 31, 2016 and December 31, 2015, total marketable securities held to fund operating programs, which are recorded at fair value and included on the condensed consolidated balance sheets, were as follows:

March 31, 2016 | December 31, 2015 | ||||||

Marketable securities held by the Hyatt Gold Passport Fund | $ | 393 | $ | 384 | |||

Marketable securities held to fund deferred compensation plans (Note 9) | 332 | 333 | |||||

Marketable securities held to fund our captive insurance company | 78 | 82 | |||||

Total marketable securities held to fund operating programs | $ | 803 | $ | 799 | |||

Less current portion of marketable securities held for operating programs included in cash and cash equivalents, short-term investments, and prepaids and other assets | (143 | ) | (121 | ) | |||

Marketable securities held to fund operating programs included in other assets | $ | 660 | $ | 678 | |||

Net gains and interest income from marketable securities held to fund operating programs on the condensed consolidated statements of income includes realized and unrealized gains (losses) and interest income, net related to the following:

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Hyatt Gold Passport Fund | $ | 1 | $ | 1 | |||

Deferred compensation plans | — | 7 | |||||

Total net gains and interest income from marketable securities held to fund operating programs | $ | 1 | $ | 8 | |||

Our captive insurance company holds marketable securities which have been classified as available for sale ("AFS") and are invested in U.S. government agencies, time deposits and corporate debt securities. We have classified these investments as current or long-term, based on their contractual maturity dates, which range from 2016 through 2021. During the three months ended March 31, 2016, we recorded insignificant unrealized gains (losses), net related to these AFS securities on the condensed consolidated statements of comprehensive income (loss).

Marketable Securities Held for Investment Purposes—At March 31, 2016 and December 31, 2015, our total marketable securities held for investment purposes, which are recorded at fair value and included on the condensed consolidated balance sheets, were as follows:

March 31, 2016 | December 31, 2015 | ||||||

Interest bearing money market funds | $ | 49 | $ | 5 | |||

Time deposits | 30 | 30 | |||||

Preferred shares | 328 | 335 | |||||

7

Fair Value—As of March 31, 2016 and December 31, 2015, we had the following financial assets measured at fair value on a recurring basis:

March 31, 2016 | Cash and Cash Equivalents | Short-term Investments | Prepaids and Other Assets | Other Assets | |||||||||||||||

Level One - Quoted Prices in Active Markets for Identical Assets | |||||||||||||||||||

Interest bearing money market funds | $ | 58 | $ | 58 | $ | — | $ | — | $ | — | |||||||||

Mutual funds | 332 | — | — | — | 332 | ||||||||||||||

Level Two - Significant Other Observable Inputs | |||||||||||||||||||

Time deposits | 47 | — | 37 | — | 10 | ||||||||||||||

U.S. government obligations | 132 | — | — | 38 | 94 | ||||||||||||||

U.S. government agencies | 79 | — | 17 | 12 | 50 | ||||||||||||||

Corporate debt securities | 181 | — | 1 | 44 | 136 | ||||||||||||||

Mortgage-backed securities | 26 | — | — | 7 | 19 | ||||||||||||||

Asset-backed securities | 24 | — | — | 7 | 17 | ||||||||||||||

Municipal and provincial notes and bonds | 3 | — | — | 1 | 2 | ||||||||||||||

Level Three - Significant Unobservable Inputs | |||||||||||||||||||

Preferred shares | 328 | — | — | — | 328 | ||||||||||||||

Total | $ | 1,210 | $ | 58 | $ | 55 | $ | 109 | $ | 988 | |||||||||

December 31, 2015 | Cash and Cash Equivalents | Short-term Investments | Prepaids and Other Assets | Other Assets | |||||||||||||||

Level One - Quoted Prices in Active Markets for Identical Assets | |||||||||||||||||||

Interest bearing money market funds | $ | 18 | $ | 18 | $ | — | $ | — | $ | — | |||||||||

Mutual funds | 333 | — | — | — | 333 | ||||||||||||||

Level Two - Significant Other Observable Inputs | |||||||||||||||||||

Time deposits | 45 | — | 38 | — | 7 | ||||||||||||||

U.S. government obligations | 131 | — | — | 32 | 99 | ||||||||||||||

U.S. government agencies | 83 | — | 6 | 10 | 67 | ||||||||||||||

Corporate debt securities | 168 | — | 2 | 36 | 130 | ||||||||||||||

Mortgage-backed securities | 26 | — | — | 6 | 20 | ||||||||||||||

Asset-backed securities | 27 | — | — | 7 | 20 | ||||||||||||||

Municipal and provincial notes and bonds | 3 | — | — | 1 | 2 | ||||||||||||||

Level Three - Significant Unobservable Inputs | |||||||||||||||||||

Preferred shares | 335 | — | — | — | 335 | ||||||||||||||

Total | $ | 1,169 | $ | 18 | $ | 46 | $ | 92 | $ | 1,013 | |||||||||

During the three months ended March 31, 2016 and March 31, 2015, there were no transfers between levels of the fair value hierarchy. Our policy is to recognize transfers in and transfers out as of the end of each quarterly reporting period. We currently do not have non-financial assets or non-financial liabilities that are required to be measured at fair value on a recurring basis.

8

We invest a portion of our cash into short-term interest bearing money market funds that have a maturity of less than ninety days. Consequently, the balances are recorded in cash and cash equivalents. The funds are held with open-ended registered investment companies and the fair value of the funds are classified as Level One as we are able to obtain market available pricing information on an ongoing basis. The fair value of our mutual funds are classified as Level One as they trade with sufficient frequency and volume to enable us to obtain pricing information on an ongoing basis. Time deposits are recorded at par value, which approximates fair value and are classified as Level Two. The remaining securities, other than our investment in preferred shares, are classified as Level Two due to the use and weighting of multiple market inputs being considered in the final price of the security. Market inputs include quoted market prices from active markets for identical securities, quoted market prices for identical securities in inactive markets, and quoted market prices in active and inactive markets for similar securities.

Preferred shares—During the year ended December 31, 2013, we invested $271 million in Playa Hotels & Resorts B.V. ("Playa") for redeemable, convertible preferred shares. Hyatt has the option to convert its preferred shares into shares of common stock at any time through the later of the second anniversary of the closing of our investment or an initial public offering by Playa. The preferred investment is redeemable at Hyatt's option in August 2021. In the event of an initial public offering or other equity issuance by Playa, Hyatt has the option to request that Playa redeem up to $125 million of preferred shares. As a result, we have classified the preferred investment as an AFS debt security, which is remeasured quarterly at fair value on the condensed consolidated balance sheets through other comprehensive income (loss). The fair value of the preferred shares was:

2016 | 2015 | ||||||

Fair value at January 1 | $ | 335 | $ | 280 | |||

Gross unrealized gains | — | 2 | |||||

Gross unrealized losses | (7 | ) | — | ||||

Fair value at March 31 | $ | 328 | $ | 282 | |||

Due to the lack of availability of market data, the preferred shares are classified as Level Three. We estimated the fair value of the Playa preferred shares using an option-pricing model. This model requires that we make certain assumptions regarding the expected volatility, term, risk-free interest rate over the expected term, dividend yield and enterprise value. Financial forecasts were used in the computation of the enterprise value using the income approach, based on assumed revenue growth rates and operating margin levels. The risks associated with achieving these forecasts were assessed in selecting the appropriate weighted-average cost of capital.

A summary of the significant assumptions used to estimate the fair value of our preferred shares as of March 31, 2016 and December 31, 2015 are as follows:

March 31, 2016 | December 31, 2015 | ||||

Expected term | 0.5 years | 0.75 years | |||

Risk-free Interest Rate | 0.39 | % | 0.57 | % | |

Volatility | 48.0 | % | 46.0 | % | |

Dividend Yield | 12.0 | % | 12.0 | % | |

There is inherent uncertainty in our assumptions, and fluctuations in these assumptions will result in different estimates of fair value. The significant unobservable assumptions driving the value of the preferred shares are the enterprise value and the expected term. A 10% increase or decrease in the enterprise value primarily driven by the weighted-average cost of capital assumption and financial forecasts may cause the fair value to fluctuate by approximately $20 million. Independent of the enterprise value, a 0.5 year change in the expected term assumption may cause the fair value to fluctuate by approximately $21 million.

Held-to-Maturity Debt Securities—As of March 31, 2016 and December 31, 2015, we have investments in held-to-maturity debt securities of $25 million, which are investments in third-party entities that own certain of our hotels. The amortized cost of our investments approximates fair value. The securities are mandatorily redeemable between 2020 and 2025.

9

5. FINANCING RECEIVABLES

Financing receivables at March 31, 2016 and December 31, 2015 are as follows:

March 31, 2016 | December 31, 2015 | ||||||

Unsecured financing to hotel owners | $ | 122 | $ | 120 | |||

Less allowance for losses | (100 | ) | (98 | ) | |||

Less current portion included in receivables, net | (2 | ) | (2 | ) | |||

Total long-term financing receivables, net | $ | 20 | $ | 20 | |||

During the year ended December 31, 2015, all of our outstanding secured financing receivables to hotel owners were settled.

Allowance for Losses and Impairments—The following tables summarize the activity in our financing receivables allowance for the three months ended March 31, 2016 and March 31, 2015:

Secured Financing | Unsecured Financing | Total | |||||||||

Allowance at January 1, 2016 | $ | — | $ | 98 | $ | 98 | |||||

Provisions | — | 1 | 1 | ||||||||

Other Adjustments | — | 1 | 1 | ||||||||

Allowance at March 31, 2016 | $ | — | $ | 100 | $ | 100 | |||||

Secured Financing | Unsecured Financing | Total | |||||||||

Allowance at January 1, 2015 | $ | 13 | $ | 87 | $ | 100 | |||||

Provisions | — | 2 | 2 | ||||||||

Other Adjustments | — | (1 | ) | (1 | ) | ||||||

Allowance at March 31, 2015 | $ | 13 | $ | 88 | $ | 101 | |||||

Credit Monitoring—Our unsecured financing receivables are as follows:

March 31, 2016 | |||||||||||||||

Gross Loan Balance (Principal and Interest) | Related Allowance | Net Financing Receivables | Gross Receivables on Non-Accrual Status | ||||||||||||

Loans | $ | 15 | $ | — | $ | 15 | $ | — | |||||||

Impaired loans (1) | 60 | (60 | ) | — | 60 | ||||||||||

Total loans | 75 | (60 | ) | 15 | 60 | ||||||||||

Other financing arrangements | 47 | (40 | ) | 7 | 40 | ||||||||||

Total unsecured financing receivables | $ | 122 | $ | (100 | ) | $ | 22 | $ | 100 | ||||||

(1) The unpaid principal balance was $43 million and the average recorded loan balance was $59 million as of March 31, 2016.

December 31, 2015 | |||||||||||||||

Gross Loan Balance (Principal and Interest) | Related Allowance | Net Financing Receivables | Gross Receivables on Non-Accrual Status | ||||||||||||

Loans | $ | 15 | $ | — | $ | 15 | $ | — | |||||||

Impaired loans (2) | 58 | (58 | ) | — | 58 | ||||||||||

Total loans | 73 | (58 | ) | 15 | 58 | ||||||||||

Other financing arrangements | 47 | (40 | ) | 7 | 40 | ||||||||||

Total unsecured financing receivables | $ | 120 | $ | (98 | ) | $ | 22 | $ | 98 | ||||||

10

Fair Value—We estimated the fair value of financing receivables which are classified as Level Three in the fair value hierarchy to be approximately $22 million as of March 31, 2016 and December 31, 2015. During the three months ended March 31, 2016 and March 31, 2015, there were no transfers between levels of the fair value hierarchy.

6. ACQUISITIONS AND DISPOSITIONS

During the three months ended March 31, 2016 and March 31, 2015, we did not have any acquisitions.

Dispositions—During the three months ended March 31, 2016, we did not have any dispositions.

Hyatt Regency Indianapolis—During the three months ended March 31, 2015, we sold Hyatt Regency Indianapolis for $69 million, net of closing costs, to an unrelated third party, and entered into a long-term franchise agreement with the owner of the property. The sale resulted in a pre-tax gain of $8 million, which has been recognized in gain on sale of real estate on our condensed consolidated statements of income during the three months ended March 31, 2015. The operating results and financial position of this hotel prior to the sale remain within our owned and leased hotels segment.

As a result of certain dispositions, we have agreed to provide indemnifications to third-party purchasers for certain liabilities incurred prior to sale and for breach of certain representations and warranties made during the sales process, such as representations of valid title, authority, and environmental issues that may not be limited by a contractual monetary amount. These indemnification agreements survive until the applicable statutes of limitation expire, or until the agreed upon contract terms expire.

7. INTANGIBLE ASSETS

The following is a summary of intangible assets at March 31, 2016 and December 31, 2015:

March 31, 2016 | Weighted- Average Useful Lives in Years | December 31, 2015 | ||||||||

Management and franchise agreement intangibles | $ | 522 | 25 | $ | 535 | |||||

Lease related intangibles | 133 | 111 | 136 | |||||||

Advanced booking intangibles | 12 | 5 | 12 | |||||||

Brand intangible | 7 | — | 7 | |||||||

Other | 7 | 12 | 8 | |||||||

681 | 698 | |||||||||

Less accumulated amortization | (135 | ) | (151 | ) | ||||||

Intangibles, net | $ | 546 | $ | 547 | ||||||

Amortization expense relating to intangible assets for the three months ended March 31, 2016 and March 31, 2015 was as follows:

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Amortization expense | $ | 7 | $ | 8 | |||

8. DEBT

Long-term debt, net of current maturities, at March 31, 2016 and December 31, 2015, was $1,441 million and $1,042 million, respectively.

Senior Notes—During the three months ended March 31, 2016, we issued $400 million of 4.850% senior notes due 2026, at an issue price of 99.920% (the "2026 Notes"). We received net proceeds of $396 million from the sale of the 2026 Notes, after deducting discounts and offering expenses of approximately $4 million. We intend to use the net proceeds for general corporate purposes, including to pay for the redemption of the 2016 Notes (as

11

defined below). Interest on the 2026 Notes is payable semi-annually on March 15 and September 15 of each year, beginning on September 15, 2016.

The 2026 Notes, together with our $250 million of 3.875% senior notes due 2016 (the "2016 Notes"), $196 million of 6.875% senior notes due 2019 (the "2019 Notes"), $250 million of 5.375% senior notes due 2021 (the "2021 Notes"), and $350 million of 3.375% senior notes due 2023 (the "2023 Notes"), are collectively referred to as the "Senior Notes."

Senior Secured Term Loan—During the three months ended March 31, 2016, we repaid the senior secured term loan related to Hyatt Regency Lost Pines Resort and Spa of $64 million.

Debt Redemption—During the three months ended March 31, 2016, we gave notice to redeem our outstanding 2016 Notes, of which an aggregate principal amount of $250 million was outstanding as of March 31, 2016. See Note 18.

Fair Value—We estimated the fair value of debt, excluding capital leases, which consists of our Senior Notes, bonds and other long-term debt. Our Senior Notes and bonds are classified as Level Two due to the use and weighting of multiple market inputs in the final price of the security. Market inputs include quoted market prices from active markets for identical securities, quoted market prices for identical securities in inactive markets, and quoted market prices in active and inactive markets for similar securities. We estimated the fair value of our other long-term debt instruments using discounted cash flow analysis based on current market inputs for similar types of arrangements. Based upon the lack of availability of market data, we have classified our other long-term debt as Level Three. The primary sensitivity in these calculations is based on the selection of appropriate discount rates. Fluctuations in these assumptions will result in different estimates of fair value. During the three months ended March 31, 2016 and March 31, 2015, there were no transfers between levels of the fair value hierarchy.

Asset (Liability) | |||||||||||||||||||

March 31, 2016 | |||||||||||||||||||

Carrying Value | Fair Value | Quoted Prices in Active Markets for Identical Assets (Level One) | Significant Other Observable Inputs (Level Two) | Significant Unobservable Inputs (Level Three) | |||||||||||||||

Debt, excluding capital lease obligations | $ | (1,690 | ) | $ | (1,791 | ) | $ | — | $ | (1,709 | ) | $ | (82 | ) | |||||

Asset (Liability) | |||||||||||||||||||

December 31, 2015 | |||||||||||||||||||

Carrying Value | Fair Value | Quoted Prices in Active Markets for Identical Assets (Level One) | Significant Other Observable Inputs (Level Two) | Significant Unobservable Inputs (Level Three) | |||||||||||||||

Debt, excluding capital lease obligations | $ | (1,354 | ) | $ | (1,421 | ) | $ | — | $ | (1,277 | ) | $ | (144 | ) | |||||

9. LIABILITIES

Other long-term liabilities at March 31, 2016 and December 31, 2015 consist of the following:

March 31, 2016 | December 31, 2015 | ||||||

Deferred gains on sales of hotel properties | $ | 362 | $ | 367 | |||

Deferred compensation plans | 332 | 333 | |||||

Hyatt Gold Passport Fund | 275 | 280 | |||||

Guarantee liabilities (see Note 11) | 113 | 120 | |||||

Other | 364 | 347 | |||||

Total | $ | 1,446 | $ | 1,447 | |||

Accrued expenses and other current liabilities includes $174 million and $166 million of liabilities related to the Hyatt Gold Passport Fund at March 31, 2016 and December 31, 2015, respectively.

12

10. INCOME TAXES

The effective income tax rates for the three months ended March 31, 2016 and March 31, 2015, were 31.7% and 35.3%, respectively. Our effective tax rate decreased for the three months ended March 31, 2016 compared to the three months ended March 31, 2015, primarily due to the tax impact of global transfer pricing changes implemented during the fourth quarter of 2015.

Unrecognized tax benefits were $108 million and $110 million at March 31, 2016 and December 31, 2015, respectively, of which $24 million and $21 million, respectively, would impact the effective tax rate if recognized.

11. COMMITMENTS AND CONTINGENCIES

In the ordinary course of business, we enter into various commitments, guarantees, surety bonds, and letter of credit agreements, which are discussed below:

Commitments—As of March 31, 2016, we are committed, under certain conditions, to lend or invest up to $166 million, net of any related letters of credit, in various business ventures.

Performance Guarantees—Certain of our contractual agreements with third-party owners require us to guarantee payments to the owners if specified levels of operating profit are not achieved by their hotels.

Our most significant performance guarantee relates to four managed hotels in France that we began managing in the second quarter of 2013 ("the four managed hotels in France"), which has a term of 7 years, with approximately 4.25 years remaining, and does not have an annual cap. The remaining maximum exposure related to our performance guarantees at March 31, 2016 was $419 million, of which €344 million ($392 million using exchange rates as of March 31, 2016) related to the four managed hotels in France.

We had total net guarantee liabilities of $97 million at March 31, 2016 and December 31, 2015, which included $76 million and $81 million recorded in other long-term liabilities, $22 million and $16 million in accrued expenses and other current liabilities and $1 million and $0 in receivables on our condensed consolidated balance sheets, respectively. Our total guarantee liabilities are comprised of the fair value of the guarantee obligation liabilities recorded upon inception, net of amortization and any separate contingent liabilities, net of cash payments. Performance guarantee expense or income and income from amortization of the guarantee obligation liabilities are recorded in other loss, net on the condensed consolidated statements of income, see Note 17.

The following table details the total performance guarantee liability (inclusive of the initial guarantee liability, net of amortization and the contingent liability, net of cash payments):

The Four Managed Hotels in France | Other Performance Guarantees | All Performance Guarantees | ||||||||||||||||||||||

2016 | 2015 | 2016 | 2015 | 2016 | 2015 | |||||||||||||||||||

Beginning balance, January 1 | $ | 93 | $ | 106 | $ | 4 | $ | 5 | $ | 97 | $ | 111 | ||||||||||||

Amortization of initial guarantee obligation liability into income | (8 | ) | (2 | ) | — | — | (8 | ) | (2 | ) | ||||||||||||||

Performance guarantee expense, net | 19 | 16 | — | — | 19 | 16 | ||||||||||||||||||

Net (payments) receipts during the period | (14 | ) | 1 | (1 | ) | (1 | ) | (15 | ) | — | ||||||||||||||

Foreign currency exchange, net | 4 | (13 | ) | — | — | 4 | (13 | ) | ||||||||||||||||

Ending balance, March 31 | $ | 94 | $ | 108 | $ | 3 | $ | 4 | $ | 97 | $ | 112 | ||||||||||||

Additionally, we enter into certain management contracts where we have the right, but not an obligation, to make payments to certain hotel owners if their hotels do not achieve specified levels of operating profit. If we choose not to fund the shortfall, the hotel owner has the option to terminate the management contract. As of March 31, 2016 and December 31, 2015, there were no amounts recorded on our condensed consolidated balance sheets related to these performance test clauses.

13

Debt Repayment Guarantees—We have entered into various debt repayment guarantees primarily related to our unconsolidated hospitality ventures and certain managed hotels. As of March 31, 2016, we had a $37 million liability representing the carrying value of these guarantees, net of amortization within other long-term liabilities on our condensed consolidated balance sheets. Included within debt guarantees are the following:

Property Description | Maximum Guarantee Amount | Amount Recorded at March 31, 2016 | Amount Recorded at December 31, 2015 | Year of Guarantee Expiration | ||||||||||

Hotel properties in India | $ | 170 | $ | 26 | $ | 27 | 2020 | |||||||

Hotel property in Brazil | 74 | 3 | 4 | 2020 | ||||||||||

Vacation ownership property | 34 | — | — | 2016 | ||||||||||

Hotel property in Minnesota | 25 | 2 | 2 | 2021 | ||||||||||

Hotel property in Arizona | 23 | 3 | 3 | 2019 | ||||||||||

Hotel property in Hawaii | 15 | 3 | 3 | 2017 | ||||||||||

Hotel property in Colorado | 15 | — | — | 2016 | ||||||||||

Other | 21 | — | — | various, through 2020 | ||||||||||

Total Debt Repayment Guarantees | $ | 377 | $ | 37 | $ | 39 | ||||||||

With respect to certain debt repayment guarantees related to unconsolidated hospitality ventures, the Company has agreements with its respective partners that require each partner to pay a pro rata portion of the guarantee amount based on each partner’s ownership percentage. In relation to the vacation ownership property debt repayment guarantee, for which we no longer have an investment in the unconsolidated venture, we have the ability to fully recover from third parties any amounts we may be required to fund. Assuming successful enforcement of these agreements with our respective partners and third parties, our maximum exposure under the various debt repayment guarantees as of March 31, 2016 would be $260 million. Additionally, with respect to the debt repayment guarantee associated with the hotel properties in India, we have the contractual right to recover all amounts funded under the guarantee from the unconsolidated hospitality venture, in which we have a 50% ownership interest. Furthermore, under certain conditions as stated in the hospitality ventures' operating agreements, we have the right to force the sale of the hotel properties in India in order to recover any amounts funded under the guarantee.

Insurance—The Company obtains commercial insurance for potential losses for general liability, workers' compensation, automobile liability, employment practices, crime, property and other miscellaneous coverages. A portion of the risk is retained on a self insurance basis primarily through a U.S. based and licensed captive insurance company that is a wholly owned subsidiary of Hyatt and generally insures our deductibles and retentions. Reserve requirements are established based on actuarial projections of ultimate losses. Losses estimated to be paid within twelve months are $36 million and $35 million as of March 31, 2016 and December 31, 2015, respectively, and are classified within accrued expenses and other current liabilities on our condensed consolidated balance sheets, while losses expected to be payable in later periods are $61 million and $57 million as of March 31, 2016 and December 31, 2015, respectively, and are included in other long-term liabilities on our condensed consolidated balance sheets. At March 31, 2016, standby letters of credit amounting to $7 million have been issued to provide collateral for the estimated claims, which are guaranteed by us. For further discussion, see the "—Letters of Credit" section of this footnote.

At March 31, 2016, we have a $3 million liability related to our estimated exposure for a cyber security malware issue that occurred in 2015. We maintain a separate cyber security insurance policy with a deductible of $3 million and expect our exposure to exceed our deductible but be significantly less than our maximum insurance coverage.

Collective Bargaining Agreements—At March 31, 2016, approximately 26% of our U.S. based employees were covered by various collective bargaining agreements, generally providing for basic pay rates, working hours, other conditions of employment and orderly settlement of labor disputes. Generally, labor relations have been maintained in a normal and satisfactory manner, and we believe that our employee relations are good.

Surety Bonds—Surety bonds issued on our behalf totaled $23 million as of March 31, 2016 and primarily relate to workers’ compensation, taxes, licenses and utilities related to our lodging operations.

14

Letters of Credit—Letters of credit outstanding on our behalf as of March 31, 2016 totaled $227 million, which relate to our ongoing operations and securitization of our performance under our debt repayment guarantee associated with the hotel properties in India, which is only called upon if we default on our guarantee. The $227 million letters of credit outstanding do not reduce the available capacity under our revolving credit facility.

Capital Expenditures—As part of our ongoing business operations, significant expenditures are required to complete renovation projects that have been approved.

Other—We act as general partner of various partnerships owning hotel properties subject to mortgage indebtedness. These mortgage agreements generally limit the lender’s recourse to security interests in the assets financed and/or other assets of the partnership(s) and/or the general partner(s) thereof.

In conjunction with financing obtained for our unconsolidated hospitality ventures, we may provide standard indemnifications to the lender for loss, liability or damage occurring as a result of our actions or actions of the other hospitality venture owners.

We are subject, from time to time, to various claims and contingencies related to lawsuits, taxes and environmental matters, as well as commitments under contractual obligations. Many of these claims are covered under current insurance programs, subject to deductibles. We reasonably recognize a liability associated with commitments and contingencies when a loss is probable and reasonably estimable. Although the ultimate liability for these matters cannot be determined at this point, based on information currently available, we do not expect that the ultimate resolution of such claims and litigation will have a material effect on our condensed consolidated financial statements.

12. EQUITY

Stockholders’ Equity and Noncontrolling Interests—The following table details the equity activity for the three months ended March 31, 2016 and March 31, 2015, respectively.

Stockholders’ equity | Noncontrolling interests in consolidated subsidiaries | Total equity | |||||||||

Balance at January 1, 2016 | $ | 3,991 | $ | 4 | $ | 3,995 | |||||

Net income | 34 | — | 34 | ||||||||

Other comprehensive income | 20 | — | 20 | ||||||||

Repurchase of common stock | (63 | ) | — | (63 | ) | ||||||

Employee stock plan issuance | 1 | — | 1 | ||||||||

Share-based payment activity | 13 | — | 13 | ||||||||

Balance at March 31, 2016 | $ | 3,996 | $ | 4 | $ | 4,000 | |||||

Stockholders’ equity | Noncontrolling interests in consolidated subsidiaries | Total equity | |||||||||

Balance at January 1, 2015 | $ | 4,627 | $ | 4 | $ | 4,631 | |||||

Net income | 22 | — | 22 | ||||||||

Other comprehensive loss | (53 | ) | — | (53 | ) | ||||||

Repurchase of common stock | (187 | ) | — | (187 | ) | ||||||

Employee stock plan issuance | 1 | — | 1 | ||||||||

Share-based payment activity | 12 | — | 12 | ||||||||

Balance at March 31, 2015 | $ | 4,422 | $ | 4 | $ | 4,426 | |||||

15

Accumulated Other Comprehensive Loss—The following table details the accumulated other comprehensive loss activity for the three months ended March 31, 2016 and March 31, 2015, respectively.

Balance at January 1, 2016 | Current period other comprehensive income (loss) before reclassification | Amount Reclassified from Accumulated Other Comprehensive Loss | Balance at March 31, 2016 | ||||||||||||

Foreign currency translation adjustments | $ | (257 | ) | $ | 24 | $ | — | $ | (233 | ) | |||||

Unrealized gains (losses) on AFS securities | 39 | (4 | ) | — | 35 | ||||||||||

Unrecognized pension cost | (7 | ) | — | — | (7 | ) | |||||||||

Unrealized losses on derivative instruments | (5 | ) | — | — | (5 | ) | |||||||||

Accumulated Other Comprehensive Income (Loss) | $ | (230 | ) | $ | 20 | $ | — | $ | (210 | ) | |||||

Balance at January 1, 2015 | Current period other comprehensive income (loss) before reclassification | Amount Reclassified from Accumulated Other Comprehensive Loss | Balance at March 31, 2015 | ||||||||||||

Foreign currency translation adjustments | $ | (155 | ) | $ | (55 | ) | $ | — | $ | (210 | ) | ||||

Unrealized gains on AFS securities | 6 | 2 | — | 8 | |||||||||||

Unrecognized pension cost | (5 | ) | — | — | (5 | ) | |||||||||

Unrealized losses on derivative instruments | (6 | ) | — | — | (6 | ) | |||||||||

Accumulated Other Comprehensive Loss | $ | (160 | ) | $ | (53 | ) | $ | — | $ | (213 | ) | ||||

Share Repurchase—During 2016, 2015, and 2014, the Company's board of directors authorized the repurchase of up to $250 million, $400 million and $700 million, respectively, of the Company's common stock. These repurchases may be made from time to time in the open market, in privately negotiated transactions, or otherwise, including pursuant to a Rule 10b5-1 plan, at prices that the Company deems appropriate and subject to market conditions, applicable law and other factors deemed relevant in the Company's sole discretion. The common stock repurchase program applies to the Company’s Class A common stock and/or the Company’s Class B common stock. The common stock repurchase program does not obligate the Company to repurchase any dollar amount or number of shares of common stock and the program may be suspended or discontinued at any time.

During the three months ended March 31, 2016 and March 31, 2015, the Company repurchased 1,527,750 and 3,192,629 shares of common stock, respectively. These shares of common stock were repurchased at a weighted-average price of $41.37 and $58.67 per share, respectively, for an aggregate purchase price of $63 million and $187 million, respectively, excluding related expenses that were insignificant in both periods. The shares repurchased during the three months ended March 31, 2016 represented approximately 1% of the Company's total shares of common stock outstanding as of December 31, 2015. The shares repurchased during the three months ended March 31, 2015 represented approximately 2% of the Company's total shares of common stock outstanding as of December 31, 2014. The shares of Class A common stock that were repurchased on the open market were retired and returned to the status of authorized and unissued shares while the shares of Class B common stock that were repurchased were retired and the total number of authorized Class B shares was reduced by the number of shares repurchased. As of March 31, 2016, we had $316 million remaining under the share repurchase authorization.

16

13. STOCK-BASED COMPENSATION

As part of our Long-Term Incentive Plan, we award Stock Appreciation Rights ("SARs"), Restricted Stock Units ("RSUs"), Performance Share Units ("PSUs") and Performance Vesting Restricted Stock ("PSSs") to certain employees. Compensation expense and unearned compensation presented below exclude amounts related to employees of our managed hotels and other employees whose payroll is reimbursed, as this expense has been and will continue to be reimbursed by our third-party hotel owners and is recorded on the lines other revenues from managed properties and other costs from managed properties on our condensed consolidated statements of income. Compensation expense included in selling, general, and administrative expense on our condensed consolidated statements of income related to these awards for the three months ended March 31, 2016 and March 31, 2015 are as follows:

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

SARs | $ | 7 | $ | 7 | |||

RSUs | 8 | 8 | |||||

PSUs and PSSs | 1 | 1 | |||||

Total stock-based compensation recorded within selling, general, and administrative expenses | $ | 16 | $ | 16 | |||

SARs—Each vested SAR gives the holder the right to the difference between the value of one share of our Class A common stock at the exercise date and the value of one share of our Class A common stock at the grant date. Vested SARs can be exercised over their life as determined by the plan. All SARs have a 10-year contractual term, are settled in shares of our Class A common stock and are accounted for as equity instruments.

During the three months ended March 31, 2016, the Company granted 924,424 SARs to employees with a weighted-average grant date fair value of $14.52. The fair value of each SAR was estimated on the grant date using the Black-Scholes-Merton option-pricing model.

RSUs—Each vested RSU will be settled with a single share of our Class A common stock, with the exception of insignificant portions of certain awards which will be settled in cash. The value of the stock-settled RSUs is based on the fair value of our Class A common stock as of the grant date. In certain situations we also grant cash-settled RSUs which are recorded as a liability instrument. During the three months ended March 31, 2016, the Company granted a total of 444,629 RSUs (an insignificant portion of which are cash-settled RSUs) to employees which, with respect to stock-settled RSUs, had a weighted-average grant date fair value of $47.36.

PSUs and PSSs—The Company has granted both PSUs and PSSs to certain executive officers.

The number of PSUs that will ultimately vest and be paid out in Class A common stock depends upon the performance of the Company at the end of the applicable three year performance period relative to the applicable performance target. During the three months ended March 31, 2016, the Company granted to its executive officers a total of 111,620 PSUs, with a weighted-average grant date fair value of $47.36. The performance period is a three year period beginning January 1, 2016 and ending December 31, 2018. The PSUs will vest at the end of the performance period only if the performance threshold is met; there is no interim performance metric.

The number of PSSs that will ultimately vest with no further restrictions on transfer depends upon the performance of the Company at the end of the applicable three year performance period relative to the applicable performance target. The PSSs vest in full if the maximum performance metric is achieved. At the end of the performance period, the PSSs that do not vest will be forfeited. The PSSs will vest at the end of the performance period only if the performance threshold is met; there is no interim performance metric.

Our total unearned compensation for our stock-based compensation programs as of March 31, 2016 was $8 million for SARs, $24 million for RSUs and $5 million for PSUs and PSSs, which will be recorded to compensation expense over the next three years with respect to SARs and RSUs, with a limited portion of the SAR and RSU awards extending to four years, and over the next two years with respect to PSUs and PSSs.

17

14. RELATED-PARTY TRANSACTIONS

In addition to those included elsewhere in the notes to the condensed consolidated financial statements, related-party transactions entered into by us are summarized as follows:

Leases—Our corporate headquarters have been located at the Hyatt Center in Chicago, Illinois, since 2005. A subsidiary of the Company holds a master lease for a portion of the Hyatt Center and has entered into sublease agreements with certain related parties. Future expected sublease income for this space from related parties is $5 million.

Equity Method Investments—We have equity method investments in entities that own properties for which we provide management and/or franchise services and receive fees. We recorded fees of $6 million and $5 million for the three months ended March 31, 2016 and March 31, 2015, respectively. As of March 31, 2016 and December 31, 2015, we had receivables due from these properties of $6 million. In addition, in some cases we provide loans (see Note 5) or guarantees (see Note 11) to these entities. Our ownership interest in these unconsolidated hospitality ventures generally varies from 24% to 70%. See Note 3 for further details regarding these investments.

Class B Share Repurchase—During the three months ended March 31, 2016, we repurchased 0 shares of Class B common stock. During the three months ended March 31, 2015, we repurchased 750,000 shares of Class B common stock for a weighted average price of $59.54 per share, for an aggregate purchase price of approximately $45 million. The shares repurchased represented approximately 0.5% of the Company's total shares of common stock outstanding prior to the repurchase. The shares of Class B common stock were repurchased in privately negotiated transactions from trusts for the benefit of certain Pritzker family members and limited partnerships owned indirectly by trusts for the benefit of certain Pritzker family members and were retired, thereby reducing the total number of shares outstanding and reducing the shares of Class B common stock authorized and outstanding by the repurchased share amount.

15. SEGMENT INFORMATION

Our reportable segments are components of the business which are managed discretely and for which discrete financial information is reviewed regularly by the chief operating decision maker to assess performance and make decisions regarding the allocation of resources. Our chief operating decision maker is the Chief Executive Officer. We define our reportable segments as follows:

• | Owned and leased hotels—This segment derives its earnings from owned and leased hotel properties located predominantly in the United States but also in certain international locations and for purposes of segment Adjusted EBITDA, includes our pro rata share of the Adjusted EBITDA of our unconsolidated hospitality ventures, based on our ownership percentage of each venture. |

• | Americas management and franchising—This segment derives its earnings primarily from a combination of hotel management and licensing of our portfolio of brands to franchisees located in the United States, Latin America, Canada and the Caribbean. This segment’s revenues also include the reimbursement of costs incurred on behalf of managed hotel property owners and franchisees with no added margin. These costs relate primarily to payroll costs at managed properties where the Company is the employer. These revenues and costs are recorded on the lines other revenues from managed properties and other costs from managed properties, respectively. The intersegment revenues relate to management fees that are collected from the Company’s owned hotels, which are eliminated in consolidation. |

• | ASPAC management and franchising—This segment derives its earnings primarily from a combination of hotel management and licensing of our portfolio of brands to franchisees located in Southeast Asia, as well as greater China, Australia, South Korea, Japan and Micronesia. This segment’s revenues also include the reimbursement of costs incurred on behalf of managed hotel property owners and franchisees with no added margin. These costs relate primarily to reservations, marketing and IT costs. These revenues and costs are recorded on the lines other revenues from managed properties and other costs from managed properties, respectively. The intersegment revenues relate to management fees that are collected from the Company’s owned hotels, which are eliminated in consolidation. |

• | EAME/SW Asia management—This segment derives its earnings primarily from hotel management of our portfolio of brands located primarily in Europe, Africa, the Middle East, India and Nepal, as well as countries along the Persian Gulf and the Arabian Sea. This segment’s revenues also include the reimbursement of |

18

costs incurred on behalf of managed hotel property owners with no added margin. These costs relate primarily to reservations, marketing and IT costs. These revenues and costs are recorded on the lines other revenues from managed properties and other costs from managed properties, respectively. The intersegment revenues relate to management fees that are collected from the Company’s owned hotels, which are eliminated in consolidation.

Our chief operating decision maker evaluates performance based on each segment’s revenue and Adjusted EBITDA. We define Adjusted EBITDA as net income attributable to Hyatt Hotels Corporation plus our pro-rata share of unconsolidated hospitality ventures Adjusted EBITDA based on our ownership percentage of each venture, adjusted to exclude equity earnings (losses) from unconsolidated hospitality ventures; stock-based compensation expense; gain on sale of real estate; other loss, net; depreciation and amortization; interest expense; and provision for income taxes.

Effective January 1, 2016, our definition of Adjusted EBITDA has been updated to exclude stock-based compensation expense, to facilitate comparison with our competitors. We have applied this change in the definition of Adjusted EBITDA to 2015 historical results to allow for comparability between the periods presented.

19

The table below shows summarized consolidated financial information by segment. Included within corporate and other are unallocated corporate expenses, license fees related to Hyatt Residence Club, and our co-branded credit card.

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

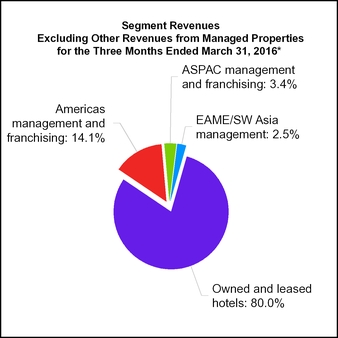

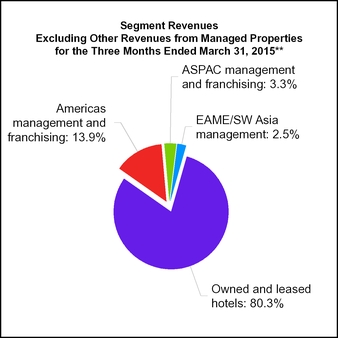

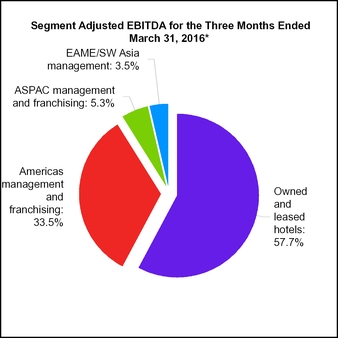

Owned and leased hotels | |||||||

Owned and leased hotels revenues | $ | 516 | $ | 509 | |||

Adjusted EBITDA | 131 | 124 | |||||

Depreciation and amortization | 68 | 71 | |||||

Americas management and franchising | |||||||

Management and franchise fees revenues | 91 | 88 | |||||

Other revenues from managed properties | 421 | 400 | |||||

Intersegment revenues (a) | 20 | 19 | |||||

Adjusted EBITDA | 76 | 73 | |||||

Depreciation and amortization | 5 | 5 | |||||

ASPAC management and franchising | |||||||

Management and franchise fees revenues | 22 | 21 | |||||

Other revenues from managed properties | 21 | 19 | |||||

Intersegment revenues (a) | — | — | |||||

Adjusted EBITDA | 12 | 12 | |||||

Depreciation and amortization | — | — | |||||

EAME/SW Asia management | |||||||

Management and franchise fees revenues | 16 | 16 | |||||

Other revenues from managed properties | 15 | 14 | |||||

Intersegment revenues (a) | 2 | 3 | |||||

Adjusted EBITDA | 8 | 7 | |||||

Depreciation and amortization | 1 | 1 | |||||

Corporate and other | |||||||

Revenues | 9 | 9 | |||||

Adjusted EBITDA | (33 | ) | (31 | ) | |||

Depreciation and amortization | 7 | 2 | |||||

Eliminations (a) | |||||||

Revenues | (22 | ) | (22 | ) | |||

Adjusted EBITDA | — | — | |||||

Depreciation and amortization | — | — | |||||

TOTAL | |||||||

Revenues | $ | 1,089 | $ | 1,054 | |||

Adjusted EBITDA | 194 | 185 | |||||

Depreciation and amortization | 81 | 79 | |||||

(a) | Intersegment revenues are included in the management and franchise fees revenues and eliminated in Eliminations. |

20

The table below provides a reconciliation of our consolidated Adjusted EBITDA to EBITDA and a reconciliation of EBITDA to net income attributable to Hyatt Hotels Corporation for the three months ended March 31, 2016 and March 31, 2015.

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Adjusted EBITDA | $ | 194 | $ | 185 | |||

Equity earnings (losses) from unconsolidated hospitality ventures | 2 | (6 | ) | ||||

Stock-based compensation expense (see Note 13) | (16 | ) | (16 | ) | |||

Gain on sale of real estate | — | 8 | |||||

Other loss, net (see Note 17) | (4 | ) | (18 | ) | |||

Pro rata share of unconsolidated hospitality ventures Adjusted EBITDA | (28 | ) | (23 | ) | |||

EBITDA | 148 | 130 | |||||

Depreciation and amortization | (81 | ) | (79 | ) | |||

Interest expense | (17 | ) | (17 | ) | |||

Provision for income taxes | (16 | ) | (12 | ) | |||

Net income attributable to Hyatt Hotels Corporation | $ | 34 | $ | 22 | |||

16. EARNINGS PER SHARE

The calculation of basic and diluted earnings per share, including a reconciliation of the numerator and denominator, are as follows:

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Numerator: | |||||||

Net income | $ | 34 | $ | 22 | |||

Net income attributable to noncontrolling interests | — | — | |||||

Net income attributable to Hyatt Hotels Corporation | $ | 34 | $ | 22 | |||

Denominator: | |||||||

Basic weighted average shares outstanding | 135,128,860 | 147,285,258 | |||||

Share-based compensation | 796,029 | 1,354,053 | |||||

Diluted weighted average shares outstanding | 135,924,889 | 148,639,311 | |||||

Basic Earnings Per Share: | |||||||

Net income | $ | 0.25 | $ | 0.15 | |||

Net income attributable to noncontrolling interests | — | — | |||||

Net income attributable to Hyatt Hotels Corporation | $ | 0.25 | $ | 0.15 | |||

Diluted Earnings Per Share: | |||||||

Net income | $ | 0.25 | $ | 0.15 | |||

Net income attributable to noncontrolling interests | — | — | |||||

Net income attributable to Hyatt Hotels Corporation | $ | 0.25 | $ | 0.15 | |||

The computations of diluted net income per share for the three months ended March 31, 2016 and March 31, 2015 do not include the following shares of Class A common stock assumed to be issued as stock-settled SARs and RSUs because they are anti-dilutive.

Three Months Ended March 31, | |||||

2016 | 2015 | ||||

SARs | — | 2,500 | |||

RSUs | 12,000 | — | |||

21

17. OTHER LOSS, NET

The table below provides a reconciliation of the components in other loss, net, for the three months ended March 31, 2016 and March 31, 2015, respectively.

Three Months Ended March 31, | |||||||

2016 | 2015 | ||||||

Performance guarantee expense, net (see Note 11) | $ | (19 | ) | $ | (16 | ) | |

Foreign currency losses, net | — | (7 | ) | ||||

Interest income | 1 | 2 | |||||

Depreciation recovery | 5 | 1 | |||||

Guarantee liability amortization (see Note 11) | 8 | 2 | |||||

Other | 1 | — | |||||

Other loss, net | $ | (4 | ) | $ | (18 | ) | |

18. SUBSEQUENT EVENTS

Pursuant to the notice of redemption on March 15, 2016, all of the Company’s outstanding 2016 Notes, of which an aggregate principal amount of $250 million was outstanding at March 31, 2016, were redeemed on April 11, 2016 for $254 million.

On April 25, 2016, we acquired Thompson Miami Beach for approximately $238 million, from a seller that is indirectly owned by a limited partnership affiliated with the brother of our Executive Chairman. We have rebranded this hotel as The Confidante, the newest addition to The Unbound Collection by Hyatt.

22

Item 2. Management's Discussion and Analysis of Financial Condition and Results of Operations.

This quarterly report contains "forward-looking statements" within the meaning of the Private Securities

Litigation Reform Act of 1995. These statements include statements about the Company's plans, strategies, financial performance, prospects or future events and involve known and unknown risks that are difficult to predict. As a result, our actual results, performance or achievements may differ materially from those expressed or implied by these forward-looking statements. In some cases, you can identify forward-looking statements by the use of words such as "may," "could," "expect," "intend," "plan," "seek," "anticipate," "believe," "estimate," "predict," "potential," "continue," "likely," "will," "would" and variations of these terms and similar expressions, or the negative of these terms or similar expressions. Such forward-looking statements are necessarily based upon estimates and assumptions that, while considered reasonable by us and our management, are inherently uncertain. Factors that may cause actual results to differ materially from current expectations include, but are not limited to: the factors discussed in our filings with the U.S. Securities and Exchange Commission, including our Annual Report on Form 10-K; general economic uncertainty in key global markets and a worsening of global economic conditions or low levels of economic growth; the rate and the pace of economic recovery following economic downturns; levels of spending in business and leisure segments as well as consumer confidence; declines in occupancy and average daily rate; limited visibility with respect to future bookings; loss of key personnel; hostilities, or fear of hostilities, including future terrorist attacks, that affect travel; travel-related accidents; natural or man-made disasters such as earthquakes, tsunamis, tornadoes, hurricanes, floods, oil spills, nuclear incidents and global outbreaks of pandemics or contagious diseases or fear of such outbreaks; our ability to successfully achieve certain levels of operating profits at hotels that have performance guarantees in favor of our third party owners; the impact of hotel renovations; our ability to successfully execute our common stock repurchase program; the seasonal and cyclical nature of the real estate and hospitality businesses; changes in distribution arrangements, such as through Internet travel intermediaries; changes in the tastes and preferences of our customers, including the entry of new competitors in the lodging business; relationships with colleagues and labor unions and changes in labor laws; financial condition of, and our relationships with, third-party property owners, franchisees and hospitality venture partners; the possible inability of our third-party owners, franchisees or development partners to access capital necessary to fund current operations or implement our plans for growth; risks associated with potential acquisitions and dispositions and the introduction of new brand concepts; the timing of acquisitions and dispositions; failure to successfully complete proposed transactions (including the failure to satisfy closing conditions or obtain required approvals); unforeseen terminations of our management or franchise agreements; changes in federal, state, local or foreign tax law; increases in interest rates and operating costs; foreign exchange rate fluctuations or currency restructurings; lack of acceptance of new brands or innovation; general volatility of the capital markets and our ability to access such markets; changes in the competitive environment in our industry, including as a result of industry consolidation, and the markets where we operate; cyber incidents and information technology failures; outcomes of legal or administrative proceedings; and violations of regulations or laws related to our franchising business. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements set forth above. Forward-looking statements speak only as of the date they are made, and we do not undertake or assume any obligation to update publicly any of these forward-looking statements to reflect actual results, new information or future events, changes in assumptions or changes in other factors affecting forward-looking statements, except to the extent required by applicable laws. If we update one or more forward-looking statements, no inference should be drawn that we will make additional updates with respect to those or other forward-looking statements.

The following discussion should be read in conjunction with the Company's Condensed Consolidated Financial Statements and accompanying Notes, which appear elsewhere in this Quarterly Report on Form 10-Q.

Executive Overview

We are a global hospitality company engaged in the development, ownership, operation, management, franchising and licensing of a portfolio of properties, including hotels, resorts and residential and vacation ownership properties around the world. As of March 31, 2016, our worldwide hotel portfolio consisted of 612 hotels (161,572 rooms), including:

• | 260 managed properties (86,717 rooms), all of which we operate under management agreements with third-party property owners; |

• | 280 franchised properties (46,560 rooms), all of which are owned by third parties that have franchise agreements with us and are operated by third parties; |

• | 34 owned properties (17,735 rooms) (including 1 consolidated hospitality venture), 1 capital leased property (171 rooms), and 7 operating leased properties (2,411 rooms), all of which we manage; |

23

• | 20 managed properties and 10 franchised properties owned or leased by unconsolidated hospitality ventures (7,978 rooms). |

Our worldwide property portfolio also includes:

• | 6 all inclusive resorts (2,401 rooms), all of which are owned and operated by an unconsolidated hospitality venture that has franchise agreements with us; |

• | 16 vacation ownership properties (1,038 units), all of which are licensed by Interval Leisure Group ("ILG") under the Hyatt Residence Club brand and operated by third parties, including ILG and its affiliates; and |

• | 18 residential properties (2,404 units), which consist of branded residences and serviced apartments. We manage all of the serviced apartments and those branded residential units that participate in a rental program with an adjacent Hyatt-branded hotel. |

We report our consolidated operations in U.S. dollars and manage our business within four reportable segments as described below:

• | Owned and leased hotels, which consists of our owned and leased full service and select service hotels and, for purposes of segment Adjusted EBITDA, our pro rata share of the Adjusted EBITDA of our unconsolidated hospitality ventures, based on our ownership percentage of each venture; |

• | Americas management and franchising, which consists of our management and franchising of properties located in the United States, Latin America, Canada and the Caribbean; |

• | ASPAC management and franchising, which consists of our management and franchising of properties located in Southeast Asia, as well as greater China, Australia, South Korea, Japan and Micronesia; and |

• | EAME/SW Asia management, which consists of our management of properties located primarily in Europe, Africa, the Middle East, India and Nepal, as well as countries along the Persian Gulf and the Arabian Sea. |

The results of our unallocated corporate overhead, license fees related to Hyatt Residence Club and Hyatt co-branded credit card are reported within corporate and other. See Note 15 for further discussion of our segment structure.