Attached files

| file | filename |

|---|---|

| EX-32 - CERTIFICATION - Omagine, Inc. | f10k2015ex32_omagineinc.htm |

| EX-31 - CERTIFICATION - Omagine, Inc. | f10k2015ex31_omagineinc.htm |

| EX-10.36 - THE MASRAF AL RAYAN TERM SHEET - Omagine, Inc. | f10k2015ex10xxxvi_omagine.htm |

| EX-10.37 - THE MURABAHA FACILITY AGREEMENT BETWEEN OMAGINE LLC AND MASRAF AL RAYAN BANK - Omagine, Inc. | f10k2015ex10xxxvii_omagine.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

Commission File Number 0-17264

Omagine, Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 20-2876380 | |

| (State of incorporation) | (I.R.S. Employer | |

| Identification Number) |

136 Madison Avenue, 5th Floor, New York, NY 10016

(Address of Principal Executive Offices)

Registrant's telephone number and area code: (212) 563-4141

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $.001 par value

(Title of Class)

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933, as amended ("Securities Act"). ☐ Yes ☒ No

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Exchange Act of 1934 (the "Act"). ☐ Yes ☒ No

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Act during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by a check mark whether the Registrant has submitted electronically and posted on its corporate Website every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

The aggregate market value of the 11,970,255 shares of voting stock held by non-affiliates of the Registrant (based upon the average of the high and low bid prices) on June 30, 2015, the last day of the Registrant's most recently completed second quarter, was $26,933,075. (SEE Item 5: "Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities").

As of April 13, 2016, the Registrant had outstanding 19,744,034 shares of Common Stock, par value $.001 per share ("Common Stock").

Documents Incorporated By Reference

None

| Omagine, Inc. | ||

| Table of Contents to the Annual Report on Form 10-K | ||

| Fiscal Year Ended December 31, 2015 | ||

| 2 |

Some of the statements contained in this report that are not statements of historical facts constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, notwithstanding that such statements are not specifically identified as such. These forward-looking statements are based on current expectations and projections about future events. The words “estimates,” “projects,” “plans,” “believes,” “expects,” “anticipates,” “intends,” “targeted,” “continue,” “remain,” “will,” “should,” “may” and other similar expressions, or the negative or other variations thereof, as well as discussions of strategy that involve risks and uncertainties (such as the Al Rayan Bank Loan discussed in this report), are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. Examples of forward-looking statements include but are not limited to statements about or relating to: (i) future revenues, expenses, income or loss, cash flow, earnings or loss per share, the payment or nonpayment of dividends, capital structure and other financial items, (ii) plans, objectives and expectations of Omagine, Inc. or its subsidiary Omagine LLC or the managements or Boards of Directors thereof, (iii) the Company’s business plans, products or services, (iv) future economic or financial performance, and (v) assumptions underlying such statements. Forecasts, projections and assumptions contained and expressed herein were reasonably based on information available to the Company at the time so furnished and as of the date of this report. All such forecasts, projections and assumptions are subject to significant uncertainties and contingencies, many of which are beyond the Company's control, and no assurance can be given that such forecasts, projections or assumptions will be realized. No assurances can be given regarding the achievement of future results, as our actual results may differ materially from our projected future results as a result of the risks we face, and actual future events may differ from anticipated future events because of the assumptions underlying the forward-looking statements that have been made regarding such anticipated events.

Factors that may cause actual results, our performance or achievements, or industry results, to differ materially from those contemplated by such forward-looking statements include without limitation:

| ● | the uncertainty associated with political events in the Middle East and North Africa (the “MENA Region”) in general, including the ongoing civil disorder and military activities in the MENA Region; |

| ● | the success or failure of Omagine’s efforts to secure additional financing, including project financing for the Omagine Project; |

| ● | oversupply of residential and/or commercial property inventory in the Oman real estate market or other adverse conditions in such market; |

| ● | the impact of MENA Region or international economies and/or future events (including natural disasters) on the Oman economy, on Omagine’s business or operations, on tourism within or into Oman, on the oil and natural gas businesses in Oman and on other major industries operating within the Omani market; |

| ● | deterioration or malaise in economic conditions, including the continuing destabilizing factors associated with the recent rapid decline in the price of crude oil on international markets; |

| ● | inflation, interest rates, movements in interest rates, securities market and monetary fluctuations; |

| ● | threatened and ongoing acts of war, civil or political unrest, terrorism or political instability in the MENA Region; or |

| ● | the ability to attract and retain skilled employees. |

Potential investors are cautioned not to place undue reliance on any such forward-looking statements, which speak only as of the date hereof. Omagine undertakes no obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

| 3 |

PART I

Introduction

Omagine, Inc. (“Omagine” or the ”Registrant”) was incorporated in Delaware in October 2004 and is a holding company which conducts substantially all its operations through its 60% owned subsidiary Omagine LLC, an Omani limited liability corporation (“LLC”) and its wholly-owned subsidiary Journey of Light, Inc., a New York corporation (“JOL”). Omagine, JOL and LLC are collectively referred to herein as the ”Company”.

In November 2009, Omagine organized LLC as a wholly owned subsidiary under the laws of the Sultanate of Oman (”Oman”) to design, develop, own and operate our initial project – a mixed-use tourism and real estate project named the “Omagine Project” (See “The Omagine Project” below). In October 2014, LLC and the Government of Oman (the “Government”) signed an agreement (the “Development Agreement” or “DA”) for the development in Oman by LLC of the Omagine Project (See: Exhibits 10.7 and 99.1 and “The Development Agreement and the Usufruct Agreement”, below).

Omagine initially capitalized LLC at Omani Rials (“OMR”) 20,000 [$52,000] and in 2011 Omagine’s 100% ownership of LLC was reduced to 60% pursuant to a shareholders’ agreement (the “Shareholder Agreement”) signed in May 2011 by Omagine, JOL and three new LLC minority investors (See: Exhibit 10.6 and “The Shareholder Agreement” below).

As of the date hereof, the shareholders of Omagine LLC (the “LLC Shareholders”) are:

| i. | Omagine, Inc. and | |

| ii. | Royal Court Affairs (“RCA”), an organization representing the personal interests of His Majesty Sultan Qaboos bin Said, the ruler of Oman, and | |

| iii. | Two subsidiaries of Consolidated Contractors International Company, SAL (“CCIC”). CCIC is a 65 year old Lebanese multi-national company headquartered in Athens, Greece having approximately five and one-half (5.5) billion U.S. dollars in annual revenue, one hundred thirty thousand (130,000) employees worldwide and operating subsidiaries in among other places, every country in the MENA Region. The two CCIC subsidiaries which are LLC shareholders are: a. Consolidated Contracting Company S.A. (“CCC-Panama”), a wholly owned subsidiary of CCIC and its investment arm, and b. Consolidated Contractors Oman Company LLC (“CCC-Oman”), CCIC’s operating subsidiary in Oman which is a construction company with approximately 13,000 employees. |

CCC-Panama and CCC-Oman are sometimes referred to collectively in this report as “CCC”.

The Present State of Affairs – An Overview:

As has been widely reported by the international media and press, during 2015 and early 2016 the price of crude oil worldwide dropped very suddenly from over $100 per barrel to about $30 per barrel. Almost all countries in the MENA Region are dependent on the sale of crude oil to support their economies and their government spending programs.

This was by no means catastrophic (there are 100s of billions of dollars of savings still in sovereign reserve funds throughout the region), but it was by all means a very, very challenging environment for the MENA Region governments and for the companies of all types – especially contractors – operating in the MENA region.

Almost all local banking institutions in the MENA Region are dependent on large deposits from oil and gas sales by governments into their institutions in order to provide the normally excess liquidity apparent in the local banking system prior to the recent dramatic worldwide drop in oil prices. With the sudden fall in deposits from oil sales, bank liquidity at local banking institutions in the GCC and wider MENA Region came under immense pressure as deposits fell dramatically while simultaneously governments became large borrowers (where they were not before). Such sudden and large government borrowings from commercial banking institutions began to crowd out commercial borrowing capacity for private companies. The largest banks of course weathered this storm more handily then the mid-size or smaller banks.

The drop in crude oil prices was not only just a large drop – it was an extremely sudden, rapid and unexpected drop. Government budgets were slashed across the region; contractors’ payments were delayed; and many government sponsored projects were postponed, delayed or cancelled. As with the banks, the largest contractors weathered this storm more readily then the mid-size or smaller contractors. CCIC is a very large multi-national contractor with significant financial resources ($5+ billion in annual revenue and 130,000 + employees) but they too had to adjust accordingly to the present economic realities. Moreover, Omagine LLC is not a government sponsored project – but is a private company.

Pursuant to the Shareholder Agreement:

| 4 |

| Ø | A “Financing Agreement” is a legally binding agreement between LLC and an investment fund, lender or other person, pursuant to which such investment fund, lender or other person agrees to provide debt financing for the first phase or for any or all phases of the Omagine Project, and |

| Ø | The first “Financing Agreement Date” is the day upon which LLC and a bank, investment fund, lender or other person first execute and deliver a Financing Agreement”), and |

| Ø | The “Contract Date” is the day on which LLC and CCC-Oman execute a contract (the “CCC Contract”) appointing CCC-Oman as the general contractor for the Omagine Project. |

Between November 2015 and the date hereof:

| Ø | On November 9, 2015, LLC received a term sheet from Masraf Al Rayan (the “Qatari Bank”) outlining the terms of a proposed agreement (the “Al Rayan Loan Agreement”) between LLC and the Qatari Bank pursuant to which the Qatari Bank would agree to provide $25 million of debt financing to LLC (the “Al Rayan Bank Loan”) to finance the first phase of the design and construction of the Omagine Project (the “First Phase”). See Exhibit 10.36. |

| Ø | On November 29, 2015, LLC and the Qatari Bank signed a definitive agreement with respect to the Al Rayan Bank Loan. See Exhibit 10.37. |

| Ø | On December 4, 2015, Omagine LLC management met with the president of CCIC and senior CCIC executives in Athens, Greece and presented the Al Rayan Loan Agreement which was happily received by all and it was agreed that we would finalize the CCC Contract as soon as possible and that CCC-Oman and CCC-Panama would then make their Deferred Investments into Omagine LLC. |

| Ø | Between December 2015 and the date hereof, we have held multiple meetings with CCIC, CCC-Oman and RCA in Muscat, Dubai, Athens, Abu Dhabi and London in an effort to conclude the foregoing arrangements and sign the CCC Contract. All parties are willing but the reality of the current economic scene and the effect it is having on bank liquidity and therefor on future requirements that LLC will have for construction financing (“Project Finance”) was well recognized by all LLC shareholders. |

| Ø | As previously disclosed, LLC management, the LLC Shareholders, (and their financial and operations advisers) estimate that the future Project Finance requirement will be between approximately $350 to $400 million --- but importantly this Project Finance agreement does not need to be in place for at least another 12 months from now after the design, masterplanning and engineering studies and associated tasks (the “Initial Activities”) are completed. |

| Ø | Also as previously disclosed, LLC management, the LLC Shareholders and their financial and operations advisers estimate that the budget to undertake and substantially complete the Initial Activities over the next 12 to 18 months is approximately $20 million. |

| Ø | Members of LLC management are presently in London and Athens for a series of parallel and conclusive meetings with the CCIC, RCA and our London lawyers (CMS) and other financial and operations advisers – all of whom are cooperatively working together – to do the necessary to bring the Omagine Project to an early start and to a successful conclusion. |

| Ø | Extensive financial negotiations and legal re-drafting of multiple versions of the CCC Contract and of the Amended & Restated Shareholder Agreement have occurred during this December 2015 to the present time period as a result of and in tandem with each other for the sole purpose of assuring this project is undertaken and completed as envisioned by all the LLC Shareholders. |

| Ø | Everyone is aligned to do the necessary to make this happen – in spite of the present challenging economic environment in the region. |

| Ø | In this regard, and importantly, given the present liquidity issues at local banks, the matter of project construction debt financing (“Project Finance”) is an issue that now moved to the forefront of all developer’s and contractor’s agendas (from its previously more relaxed and deferred position). The required Project Finance for the Omagine Project – or any project – is not really needed until after the masterplanning and design phase is complete or near complete (in our case, the $20 to $25 million First Phase). Given present economic strains however, developers and contractors are well advised to seek to lock up a Project Finance commitment early on rather than waiting to start a syndication at a later date in the First Phase process (in our case approximately 8 to 12 months after starting the First Phase). |

| Ø | Further in this regard, as an exercise in caution, management re-opened its earlier informal contacts with several Chinese contractors active in the GCC. Subsequently in February 2016, management traveled to Beijing and Hong Kong, China where we held high level discussions with the headquarters’ executive leadership of two of China’s leading building contractors – each of which is multiple times the size of CCIC. These discussions are well advanced at present and negotiations with the larger of the two Chinese contractors are at an advanced stage. |

| Ø | The proposal being discussed with each of such Chinese contractor is identical and includes a requirement for the award of the Omagine Project construction contract to the Chinese contractor (as a sub-contractor to CCC-Oman) if, and only if, BOTH of the following conditions are fulfilled: (i) an investment into LLC by the contractor (or its parent company), and (ii) the Chinese contractor (or its parent company) must arrange for the Project Finance for the Omagine Project. |

| Ø | Chinese banks have no such liquidity issue as mentioned above and they are moreover encouraged and directed by the Chinese Government to support their overseas Chinese contractors in this manner. Management is presently cautiously optimistic that it can arrange a transaction involving both CCIC and one of the Chinese contractors which will be beneficial to all parties concerned. No assurance however can be given at this time that management will be successful in this endeavor. |

| Ø | Management has had discussions with Masraf Al Rayan throughout and although the Al Rayan Loan Agreement is still valid and on offer as of the date hereof, no assurance can be given as of the date hereof that the Al Rayan Bank Loan will continue to remain on offer or that it actually will be utilized by LLC. [See: “The Al Rayan Bank Loan” and “The First Phase”, below]. |

| Ø | An agreement has been reached with CCIC regarding a new structure of the CCC Contract whereby CCC-Oman would be the general contractor and the Managing Contractor (but not necessarily the actual builder) and would oversee and manage the Chinese sub-contractor and CCIC would be paid a fixed fee for this. Any and all other sub-contracts will be awarded based on a competitive sealed-bidding process managed by LLC (in which CCC-Oman may participate where they felt they could be competitive – e.g. earth works, infrastructure, building cores, etc.) – but if CCC-Oman did any actual construction work their fixed supervision fee would be waived for that portion of the work. |

| Ø | But the matter of financing the Initial Activities remained and this has now been resolved by CCIC voluntarily agreeing to (i) advance $10 million of its $16 million CCC-Oman investment immediately upon signing of the CCC Contract (even if we don’t access the Masraf Al Rayan Loan), and (ii) stepping aside from its CCC-Panama investment and allowing the Chinese contractor (or other investor) to take up this 10% equity in LLC (at a higher price than CCC-Panama would have had to invest), and (iii) amending all existing agreements as required and signing the CCC Contract and amended Shareholder Agreement as may be required to accomplish all of the foregoing. |

| Ø | In short, CCIC has agreed to take substantial risk to advance the Omagine Project’s early implementation and successful conclusion. Management views this as a very reasonable outcome. Management is at this moment crafting & drafting all the required contracts and agreements with its lawyers, CCIC and RCA to memorialize the foregoing and intends to stay continuously at this process without interruption from now until its expected conclusion in the next few weeks. |

| 5 |

While the circuitous and extended negotiations above are rather frustrating, our shareholders should be aware that such negotiations were not unreasonable given the present economic environment caused by the drop of oil prices – and in this case where the contractor is also an investor, the complications are more pronounced since the contractor is entitled to be assured of its future payments. While not unexpected, such negotiations have apparently concluded in a win-win situation for all concerned, thanks in no small part to the Company’s willingness to finance the continued obligations of LLC when it was not legally obligated to do so – and CCIC’s willingness to step into the breach at a crucial time.

We do recognize the exceptionally unusual (and we believe temporary) economic circumstances under which CCIC is operating in the MENA Region today. They have construction operations in every country in the MENA Region – and are suffering greatly from delayed payments of huge amounts – from a variety of governments in the region. Recently CCIC (because of its size and strength) negotiated a several hundred million USD stand-by credit line to cushion itself against such delays in payment from its ongoing contracts across the entire MENA region.

We expect that this sudden business cycle change will eventually right itself as all market participants adapt to the new realities but we are of the present opinion that, being faced with no path, we believe that (assuming the foregoing agreements are executed as described), the Company has succeeded in creatively making a path where none had apparently previously existed.

Pursuant to the Shareholder Agreement as presently in effect the occurrence of both (i) the Financing Agreement Date, and (ii) the Contract Date, are the two conditions precedent (“Conditions Precedent”) to the obligations of RCA and CCC to make their final cash investments into LLC in the aggregate combined amount of OMR 26,628,125 [$69,233,125] (the “Deferred Cash Investments”). As of the date hereof all of the LLC shareholders have previously made cash and non-cash investments into LLC and the Financing Agreement Date has occurred. When the final Condition Precedent (the occurrence of the Contract Date) is satisfied, RCA and CCC will be then obligated to make the Deferred Cash Investments into LLC (as may be amended as indicated above). Notwithstanding the foregoing however, it is possible, even likely, that the Shareholder Agreement will be amended to accommodate the present economic conditions such that the Deferred Investments may be made over a period more in line with LLC’s actual cash requirements.

The following table illustrates the equity investments by the LLC Shareholders:

| Shareholder Equity Investments into Omagine LLC | ||||||

| Omagine, Inc. | Royal Court Affairs | Consolidated Contractors | ||||

| Omani Rials | US Dollars | Omani Rials | US Dollars | Omani Rials | US Dollars | |

| Initial cash equity investment at inception | OMR 20,000 | $ 52,000 | ||||

| Additional cash equity investment at signing of Shareholder Agreement | OMR 70,000 | $ 182,000 | OMR 37,500 | $ 97,500 | OMR 22,500 | $ 58,500 |

| Additional cash equity investment before the first Financing Agreement Date | OMR 210,000 | $ 546,000 | ||||

| Additional non-cash equity investment of Land Rights on registration of the Usufruct Agreement* | OMR 276,666,667 | $ 718,614,000 | ||||

| Additional cash equity investment (Deferred Cash Investments)** | OMR 7,640,625 | $ 19,865,625 | OMR 18,987,500 | $ 49,367,500 | ||

| Total Equity Investment into LLC per Shareholder | OMR 300,000 | $ 780,000 | OMR 284,344,792 | $ 738,577,125 | OMR 19,010,000 | $ 49,426,000 |

| * | The Omani Rial is pegged to the U.S. Dollar and as such its value relative to the U.S. Dollar normally exhibits very minimal fluctuation between approximately $2.597 and $2.60 U.S. Dollars to 1 Omani Rial. In its initial recording of the Land Rights in its September 30, 2015 consolidated financial statement, the Company utilized an exchange rate of $2.5974 U.S. Dollars to 1 Omani Rial which was based on the July 7, 2015 XE Currency Converter. The exchange rate based on the December 8, 2015 XE Currency Converter is $2.5982 U.S. Dollars to 1 Omani Rial. For presentation purposes, all conversions of Omani Rials to U.S. Dollars in this Report are, unless otherwise stated to the contrary, calculated at one (1) Omani Rial being equivalent to two United States Dollars and sixty cents ($2.60). See: “The Land Rights” and “Critical Accounting Policies”, below. |

| ** | The Deferred Cash Investments are to be invested when the Conditions Precedent are satisfied; the Shareholder Agreement terms and conditions relative to the timing of the Deferred Cash Investments may be amended; all other investments listed have been made as of the date hereof (See: “LLC Capital Structure” below). |

In order to bring the Omagine Project to its present state, Omagine expended (i) in excess of approximately $21 million of Pre-Development Expenses through the October 2014 DA signing date, and (ii) an additional approximately $6.2 million since the October 2014 DA signing date, to finance LLC’s pre-development activities. As of January 31, 2016, Omagine has paid pre-development expenses of approximately $27.2 million on behalf of Omagine LLC. All such pre-development expenses will be liabilities of LLC reimbursable to Omagine, Inc. in accordance with the terms of the Shareholder Agreement (as may likely be amended) (See: “Pre-Development Expenses / Post-DA Pre-Development Expenses”, below).

| 6 |

| LLC Expenses paid by Omagine, Inc. | ||||

| US Dollars | ||||

| Pre-Development Expenses (pre-DA) | $ | 20,996,707 | ||

| Post-DA Pre-Development Expenses | $ | 6,191,303 | ||

| Total Reimbursable Expenses | $ | 27,188,010 |

The Company is focused on entertainment, hospitality and real estate development opportunities in the Middle East and North Africa (the “MENA Region”) and on the design and development of distinctive tourism destinations. The Company presently concentrates the majority of its efforts on the business of LLC and specifically on the Omagine Project.

Omagine, Inc. has 19,744,034 shares of its Common Stock issued and outstanding as of April 13, 2016.

The Omagine Project

The Omagine Project is a mixed-use tourism and residential real estate project. Subject to normal and customary scheduling changes during its development and construction (and to the current delayed start date), the Omagine Project is planned to be completed in late 2021. It is being developed on one million square meters (equal to 100 hectares or approximately 245 acres) of beachfront land (the “Existing Land”) facing the Gulf of Oman just west of Oman’s capital city of Muscat and approximately six miles from Muscat International Airport. Present development plans envision the creation of approximately a net additional 106,000 square meters of “Reclaimed Land” which together with the Existing Land will comprise approximately 1,106,000 square meters of land (the “Project Land”). The Omagine Project will require substantial Project Finance to complete (See: “The Present State of Affairs – An Overview”, above and “The Shareholder Agreement”, “LLC Capital Structure” and “Financial Advisor”, below).

The Omagine Project is planned to be an elegant integration of cultural, scientific, heritage, entertainment and residential components, including seven pearl shaped (20 meter diameter) buildings (the “Pearls”) located along an open boardwalk with associated entertainment exhibitions; an amphitheater and stage; green landscaped spaces; a canal; an enclosed harbor and marina; boat slips and docking facilities; retail shops; a variety of restaurants, cafes and entertainment venues; a five-star resort hotel; a four-star hotel; and possibly an additional three or four-star hotel; shopping and retail establishments integrated with the hotels; commercial office buildings; and more than two thousand elegant residences to be developed for sale by LLC. The ethos of the project is entertainment and elegance and the Company expects that the Pearls will become “the Landmark” for the Sultanate of Oman.

Non-Omani persons are not permitted to purchase land in Oman unless such land is located within an Integrated Tourism Project (“ITC”). The Government has designated the Omagine Project as an ITC and has issued a license to LLC (an “ITC License”) thereby permitting the sale by LLC to any person, including any non-Omani person of the freehold title to the Project Land and to properties developed on the Project Land. Since the Omagine Project will contain significant hotel, retail, commercial, and entertainment elements, LLC’s business operations are expected over time to encompass real estate development, hospitality, entertainment and property management.

| 7 |

The Development Agreement and the Usufruct Agreement

Omagine’s 60% owned subsidiary, LLC, signed a Development Agreement with the Government of Oman in October 2014 for the development in Oman by LLC of the Omagine Project. The legal effectiveness of the DA was conditional upon its ratification by Oman’s Ministry of Finance which Ratification occurred in March 2015. On July 1, 2015 (the “Operative Date”), the Government and LLC entered into the UA with respect to the Land Rights over the land constituting the “Omagine Site”. The Operative Date is the date from which all time periods for the execution by LLC of various tasks enumerated in the DA are to be measured (See Exhibits 10.8 and 99.2). Management currently expects, based on informal discussions with Government officials, that the Operative Date will be further extended once we finalize our negotiations and agreements with CCIC and/or one of the aforementioned Chinese contractors or after we conclude any other such similar arrangement.

The DA and UA are the contracts that govern the design, development, construction, management and ownership of the Omagine Project, the use and sale by LLC of the Project Land, and the Government’s and LLC’s rights and obligations with respect to the Omagine Project. In the event of any conflict between the terms and conditions of the DA and the terms and conditions of the UA, the terms and conditions of the DA control (See Exhibits 10.7, 99.1, 10.8 and 99.2). The term of the DA is 20 years and the term of the UA is 50 years (renewable) commencing from the Operative Date. The UA, and the DA provisions relevant to the UA, survive the expiration of the term of the DA.

The Land Rights owned by LLC give it extensive rights over the Project Land including the right to sell such Project Land on a freehold basis. On July 2, 2015, the UA was registered by the Government which registration legally perfected LLC’s ownership of the Land Rights (See: Exhibits 10.8 and 99.2). LLC may use, control, develop, retain, operate and/or sell the approximately 1.1 million square meters of Project Land to itself or to third parties. The DA obligates LLC to pay the Government twenty-five (25) Omani Rials ($65) for each square meter of Project Land purchased directly by LLC or sold by LLC to any third party (the “Land Price”). The average valuation for the Land Rights (net of such Land Price is OMR 276,666,667 ($718,614,000) (See: “The Land Rights”, below).

The five year period commencing on the Operative Date is a rent free period (the “Rent Free Period”) and thereafter LLC will pay annual rent to the Government (the “Land Rent”) based on only the built but unsold commercial area (excluding the residential area) of the Omagine Project (approximately 150,000 sq. meters) or approximately OMR 45,000 ($117,000) per year based on the current annual per square meter fee of OMR 0.300 ($0.78). No Land Rent is due or owing during the Rent Free Period and no Land Rent is ever due or owing with respect to plots of Project Land (i) on which there is a residential building, or (ii) on which there is not a substantially completed non-residential building (i.e. Project Land that is open space, roads, building work-in-progress, etc. are rent-free).

The continued legal effectiveness of the DA subsequent to the Operative Date is dependent upon certain milestone dates being achieved (any or all of which may be extended or waived by the Government): (1) LLC’s delivery to the Government by June 30, 2016 of a term sheet with lenders for the financing of the First Phase, any other phase or all of the Project, [this condition is now satisfied by the term sheet which LLC has received from the Qatari Bank] (2) LLC’s submission to the Ministry of Tourism of a social impact assessment by March 31, 2016 and the Government’s approval thereof by June 30, 2016 (this condition 2 is not yet satisfied and is expected to be extended as mentioned above if and when the Operative Date is extended), (3) the Government’s approval by June 30, 2016 of the development control plan for the Omagine Project, and (4) the transformation of LLC into a joint stock company by June 30, 2016. Company management has had informal discussions with the concerned government officials and management is confident that given the present economic conditions referred to above (of which the Government is keenly aware), the Company will be granted an extension of time on many of such due dates similar to the extension of the Operative Date to July1. 2016 already previously granted by the Government.

Pursuant to the DA, LLC must substantially complete the construction of the seven Pearl buildings and one hotel (the “Minimum Build Obligation” or “MBO”) by June 30, 2020 (the “MBO Completion Date”), as such date may be amended or extended per the DA. The DA imposes no performance timelines on LLC with respect to completing the development or construction of elements of the Omagine Project other than the MBO but the completion of the MBO will require LLC to obtain the necessary Project Finance to do so. Any material breach by LLC of its obligation to perform the MBO would constitute an event of default under the DA. The DA specifies that the principal construction contract (i.e. the CCC Contract) should be executed by June 30, 2016. LLC is required to provide written notice to the Government in certain circumstances, such as LLC’s change in an anticipated milestone date that would result in a substantial achievement of work to occur later than 60 days after such milestone date. Such notice has been communicated both verbally and in writing to the appropriate government officials in recent discussions with them.

Company management initiated a fast-track development strategy in October 2014 and as a result, Omagine has undertaken and financed many pre-development activities on behalf of LLC subsequent to the DA signing and through the date hereof (See: “Pre-Development Expenses / Post-DA Pre-Development Expenses”, and “The Success Fee” below). Notwithstanding the foregoing, the Omagine Project has been delayed beyond where we had expected to be at this point due to Project Finance discussions referred to above as a result of the present economic conditions affecting local banking liquidity. See: “The Present State of Affairs – An Overview”, above.

| 8 |

Non-Omani persons (such as expatriates living and working in Oman) are not permitted by Omani law to purchase land or residences in Oman outside of an ITC. The Government’s designation and licensing of the Omagine Project as an ITC therefore permits LLC to sell the freehold title to Project Land and properties which are developed on Project Land to any Omani or non-Omani individual or juristic person worldwide. Properties within an ITC enjoy a premium price relative to properties not in an ITC. Any Project Land or buildings remaining unsold at the expiration of the 50 year Usufruct Term will revert to the Government. LLC does not anticipate that there will be any such unsold properties at the expiration of the 50 year Usufruct Term.

The foregoing summary of some of the terms of the DA and of the UA does not purport to be complete and it is qualified in its entirety by reference to the full texts of such agreements. The full text of the Development Agreement is attached hereto as Exhibits 10.7 and 99.1. The full text of the Usufruct Agreement is attached hereto as Exhibits 10.8 and 99.2 and also contained in Schedule 2A of the Development Agreement.

The Land Rights

The value of the Project Land has been determined by three highly experienced professional valuation firms in accordance with the requirements and procedures specified for such a valuation by (i) the Royal Institution of Chartered Surveyors (“RICS”) of London, England, and (ii) International Financial Reporting Standards (“IFRS”). Each of the three firms has a worldwide brand in the real estate valuation business.

| • | In November 2014, LLC engaged the Oman office of Savills (http://www.savills.com/ (“Savills”) operating as Arabian Real Estate LLC (http://www.savills.om). Savills provides real estate services from over 600 offices worldwide, is listed on the London Stock Exchange, and is a FTSE 250 Index company. |

| • | In December 2014, LLC engaged DTZ International Ltd., a Dubai, UAE firm with extensive experience in Oman (http://www.dtzglobal.com) (“DTZ”). DTZ is one of the top three global commercial real estate service companies, with more than 28,000 employees operating across more than 260 offices in 50 countries and $63 billion in transaction volume. |

| • | In January 2015, LLC engaged Jones Lang LaSalle, UAE Limited, Dubai Branch (http://www.jll-mena.com/mena/en-gb/locations/Our-locations-in-MENA/dubai) (“JLL”). JLL has 53,000 employees operating across more than 230 offices in 80 countries. |

The Savills and DTZ final valuation reports were received by LLC in January 2015. The JLL final valuation report was received by LLC in July 2015. The Company is of the opinion that JLL’s valuation is flawed and most probably represents a statistical outlier. In an abundance of caution however, management has nevertheless determined to include the JLL valuation in its calculation of the average value of LLC’s Land Rights. The Land Rights valuations by the three aforementioned firms are summarized in the table below:

| Land Rights Valuation | ||

| Valuation Firm | Omani Rials | |

| Savills | OMR 295,000,000 | |

| DTZ | OMR 385,000,000 | |

| JLL | OMR 150,000,000 | |

| Average | OMR 276,666,667 | |

| 9 |

The Accounting Treatment for the Land Rights

Omagine and JOL prepare their financial statements in accordance with accounting principles generally accepted in the United States (“US GAAP”) and the Company prepares its consolidated financial statements in accordance with US GAAP. LLC’s financial statements are prepared in accordance with International Financial Reporting Standards (“IFRS”).

LLC has land under development valued at 276,666,667 Omani Rials. Based on a $2.5974 per 1 Omani Rial exchange rate, the Company recorded this land under development in its financial statements at $718,614,000 and the Company has allocated this amount as follows: 188,963,334 Omani Rials ($490,813,363 based on a $2.5974 per 1 Omani Rial exchange rate) to inventory; and 87,703,333 Omani Rials ($227,800,637 based on a $2.5974 per 1 Omani Rial exchange rate) to property. This land under development was purchased by LLC on July 2, 2015 pursuant to the terms of the Shareholder Agreement whereby an LLC shareholder subscribed for 663,750 LLC Shares at a purchase price equal to the value of the Land Rights. Since the Land Rights represented a non-cash payment-in-kind for the LLC Shares, it was necessary to value the Land Rights.

Three expert real estate valuation companies were engaged by LLC to independently value the Land Rights in accordance with the professional standards specified by RICS and IFRS. The average of the three Land Rights valuations was OMR 276,666,667. (See: “The Land Rights”, above and Exhibits 99.4, 99.5 and 99.6).

Since the 276,666,667 Omani Rial value of the Land Rights is substantial, LLC retained the services of PricewaterhouseCoopers LLP (“PwC”) to provide its written analysis and report to LLC with respect to the correct IFRS accounting method LLC should use to record the 276,666,667 Omani Rial Land Rights value in its IFRS compliant financial statements. PwC did not advise on the valuation of the Land Rights (as determined by Savills, DTZ and JLL), but only on the correct accounting LLC should use to record such Land Rights valuation in LLC’s financial statements in accordance with IFRS. PwC’s written report was received by LLC in August 2015. Promptly thereafter, LLC consulted with its independent auditor, Deloitte & Touche (M.E.) & Co. LLC (“Deloitte”) with respect to the matter, and Deloitte’s written technical analysis report (which agreed with PwC’s analysis) was received by LLC in November 2015.

The Land Rights over the Project Land are extensive, are closely akin to ownership rights and include the right to sell such land on a freehold basis. The Land Rights are virtually equivalent to ownership rights and like any asset, if its value were to become impaired for any reason (including any contractual reason pursuant to the DA requirements), a reserve for such impairment would need to be established at such time. Both PwC and Deloitte independently concluded that the Land Rights should be recorded as capital and as tangible assets (work-in-process inventory and land) on LLC’s financial statements. With respect to the Company’s consolidated financial statements, the Company’s independent auditor in the U.S. has likewise concurred that pursuant to US GAAP, the Land Rights should be recorded as capital, inventory and land.

In determining the proper amounts to be allocated to inventory and to land, LLC calculated the percentage (x) by dividing (y) the area of the land LLC presently plans definitively to sell, by (z) the total area of the Project Land, and then multiplying that percentage (x) by 276,666,667 Omani Rials to get the number (N) for inventory. The amount to be allocated to property was then calculated by subtracting N from 276,666,667 Omani Rials. Using its detailed internal financial model, management calculated (x) to be equal to 68.3%, thereby making the inventory number (N) equal to 188,963,334 Omani Rials ($490,813,363 based on a $2.5974 per 1 Omani Rial exchange rate) and the property number equal to 87,703,333 Omani Rials ($227,800,637 based on a $2.5974 per 1 Omani Rial exchange rate). In its consolidated financial statements therefore, the Company has allocated the value of the Land Rights between (i) land under development which is held for sale (inventory), and (ii) land under development which is held for investment (PP&E). As more precise land use percentages emerge during and after the masterplanning and construction of the Omagine Project, the percentage allocations for the value of the Land Rights may be reclassified to distinguish between the land underlying properties that we will own and operate and those which we will own and lease.

The Shareholder Agreement

Pursuant to the provisions of the Shareholder Agreement the LLC Shareholders subscribed for an aggregate of 4,800,000 LLC Shares in consideration for:

| i. | an aggregate cash investment of OMR 26,968,125 [$70,117,125] in exchange for 4,136,250 LLC Shares (the “Cash Investment”), and |

| ii. | a non-cash investment of the Land Rights in exchange for 663,750 LLC Shares. |

| 10 |

Investments into LLC

Upon organizing Omagine LLC in 2009, Omagine made an initial cash investment into LLC of OMR 20,000 [$52,000] in consideration for the issuance to Omagine of 200,000 LLC Shares.

Pursuant to the Shareholder Agreement as presently in effect (which is likely to be amended):

| i. | Before the DA was signed and after the execution of the Shareholder Agreement, the LLC Shareholders purchased an aggregate of 1,300,000 LLC Shares for an aggregate cash investment of OMR 130,000 [$338,000], as follows: |

| a) | Omagine purchased an additional 700,000 LLC Shares for OMR 70,000 [$182,000] in cash, and | |

| b) | RCA purchased 375,000 LLC Shares for OMR 37,500 [$97,500] in cash, and | |

| c) | CCC-Panama purchased 150,000 LLC Shares for OMR 15,000 [$39,000] in cash, and | |

| d) | CCC-Oman purchased 75,000 LLC Shares for OMR 7,500 [$19,500] in cash, and | |

| ii. | After the DA was signed (October 2014) but before the first Financing Agreement Date, Omagine completed the purchase of an additional 2,100,000 LLC Shares for OMR 210,000 [$546,000] in cash, and |

| iii. | On July 2, 2015, RCA purchased an additional 663,750 LLC Shares in consideration for the non-cash payment of the Land Rights valued at OMR 276,666,667 [$718,614,000], and |

| iv. | Upon the signing of the CCC Contract, RCA, CCC-Oman and CCC-Panama will (except as may be amended pursuant to ongoing negotiations) be obligated to invest the “Deferred Cash Investments” into LLC in the aggregate amount of OMR 26,628,125 [$69,233,125], as follows See: “The Present State of Affairs – An Overview”, above.: |

| a) | CCC-Panama will purchase 350,000 additional LLC Shares for OMR 12,658,333 [$32,911,666] in cash, and |

| b) | CCC-Oman will purchase 175,000 additional LLC Shares for OMR 6,329,167 [$16,455,834] in cash, and |

| c) | RCA will purchase 211,250 additional LLC Shares for OMR 7,640,625 [$19,865,625] in cash. |

The occurrence of the Contract Date is the sole remaining Condition Precedent to the obligations of RCA and CCC to make the Deferred Cash Investments into LLC in the aggregate amount of $69,233,125. As of the date hereof management is hopeful that all parties to the Shareholder agreement will agree shortly to an amended and restated shareholder agreement whereby sufficient funding is supplied to LLC to carry out its planned Phase One activities and an appropriate CCC Contract can be negotiated and signed. But no assurance can be given at this time that such will occur until it actually occurs. Management cautions however that such proposed amended Shareholder Agreement may not materialize and the CCC Contract process presently underway may prove to be unsuccessful. (See: “The CCC Contract” and “The Al Rayan Bank Loan”, below).

Pre-Development Expenses / Post-DA Pre-Development Expenses

To finance the Omagine Project’s pre-development activities, Omagine has expended:

| (i) | up to and through the October 2014 DA signing date, $20,996,707 of pre-development expenses, $7,146,441 of which are non-cash stock option expenses (the “Pre-Development Expense Amount”), and |

| (ii) | subsequent to the October 2014 DA signing date up to and through January 31, 2016, an additional $6,191,303 of pre-development expenses, $3,115,191 of which are non-cash stock option expenses (the “Post-DA Pre-Development Expenses”). |

As of January 31, 2016, Omagine has paid pre-development expenses (some of which are non-cash stock option expenses) of $27,188,010 on behalf of Omagine LLC. All such pre-development expenses will be liabilities of LLC reimbursable in full to Omagine, Inc. in accordance with the provisions of the Shareholder Agreement (as may be amended).

Prior to the DA being signed, Omagine incurred significant costs related to marketing, planning, concept design, re-design, feasibility studies, engineering, financing, promotions, capital raising, travel, legal fees, consulting and professional fees, other general and administrative activities and similar such activities including preparing and making presentations to the Government and to potential investors and all other activities and matters associated with the negotiation and conclusion of the DA with the Government (collectively, the ”Pre-Development Expenses”). The Shareholder Agreement defines the “Pre-Development Expense Amount” as the total amount of such Pre-Development Expenses incurred before the DA was signed by the Government and LLC on October 2, 2014.

| 11 |

The $20,996,707 Pre-Development Expense Amount will be recorded on the books of LLC as a liability payable to Omagine in accordance with the provisions of the Shareholder Agreement (as may be amended).

The Shareholder Agreement defines the date subsequent to the Financing Agreement Date when LLC draws down the first amount of debt financing as the “Draw Date”. Fifty percent (50%) of the Pre-Development Expense Amount will be paid to Omagine on or within ten (10) days after the Draw Date and the remaining fifty percent (50%) will be paid to Omagine in five equal annual installments beginning on the first anniversary of the Draw Date. The $6,191,303 of Post-DA Pre-Development Expenses are payable to Omagine from LLC on demand (but as a practical matter, not until LLC has the financial capacity to do so).

The Success Fee

The Shareholder Agreement defines the Success Fee as being equal to ten (10) million dollars. Pursuant to the terms of the Shareholder Agreement as presently in effect, on the first Financing Agreement Date, the Success Fee is to be recorded on the books of LLC as a liability payable to Omagine. The ten (10) million dollar Success Fee will be paid to Omagine in five annual two (2) million dollar installments beginning on or within ten (10) days after the Draw Date. These dates may be amended and pushed out to a further date after the first Financing Agreement Date as a result of ongoing discussions which have not yet been concluded.

Omagine, may at its option, agree to a different schedule for the payments associated with the Pre-Development Expense Amount and/or the Success Fee until LLC is in a financial position to make such payments and Omagine may likewise, at its option, refrain from demanding payment of the Post-DA Pre-Development Expenses until LLC is in a financial position to make such payment.

As of the date hereof, Omagine continues to incur Post-DA Pre-Development Expenses on behalf of LLC for the activities undertaken by or on behalf of LLC during the Immediate Post-DA Period in order to advance the development schedule for the Omagine Project prior to concluding our ongoing discussions with CCC regarding the timing of its Deferred Investment. The 2011 Shareholder Agreement is, of course, silent with respect to the 2014, 2015 and 2016 Post-DA Pre-Development Expenses. Management expects that the other LLC Shareholders (CCC and RCA) will recognize Omagine’s extraordinary and voluntary assistance to LLC during the Immediate Post-DA Period and that Omagine will be reimbursed by LLC for the Post-DA Pre-Development Expenses as promptly as LLC is able to do so subsequent to its receiving additional financing.

LLC Capital Structure

As of the date hereof the LLC Shareholders have made:

| (i) | cash investments totaling OMR 360,000 [$936,000] (of which OMR 300,000 [$780,000] was invested by Omagine), and |

| (ii) | a non-cash investment of the Land Rights valued at OMR 276,666,667 ($718,614,000), |

for a total investment to date of OMR 277,026,667 ($720,269,334). LLC is presently capitalized as follows:

| Investment | ||||||||||||||

| Shareholder | Omani Rials | US Dollars | ||||||||||||

| Omagine | OMR | 300,000 | $ | 780,000 | ||||||||||

| RCA | OMR | 276,704,167 | $ | 718,711,500 | ||||||||||

| CCC-Panama | OMR | 15,000 | $ | 39,000 | ||||||||||

| CCC-Oman | OMR | 7,500 | $ | 19,500 | ||||||||||

| Total: | OMR | 277,026,667 | $ | 719,550,000 | ||||||||||

As a result of the post-DA further investment into LLC of cash by Omagine and Land Rights by RCA, LLC is obligated to issue a further 2,100,000 LLC Shares to Omagine and a further 663,750 LLC Shares to RCA.

As of the date hereof, the ownership percentages of LLC as registered at MOC&I are as follows:

| LLC Shareholder | % Ownership |

| Omagine | 60% |

| RCA | 25% |

| CCC-Panama | 10% |

| CCC-Oman | 5% |

| Total: | 100% |

| 12 |

Absent an amendment to the Shareholder Agreement which is expected to occur, upon the CCC Contract being signed, CCC and RCA will be obligated to make further cash investments into LLC in the aggregate amount of OMR 26,628,125 [$69,233,125]. Based on present discussions these amounts will be modified. (See: “The Present State of Affairs – An Overview”, above.)

The Transformation

At some time prior to June 30, 2016 or at such later date as may be agreed by the relevant parties, LLC intends to transform its corporate structure from a limited liability company into a joint-stock company (the “Transformation”). Assuming (a) no further LLC equity sales are made, (b) Omagine LLC is transformed into Omagine SAOC, (c) the Contract Date has occurred, and (d) all Deferred Cash Investments are paid in full, then Omagine SAOC would then be capitalized as follows:

| Omagine SAOC | ||||||||||||||||

| Investment | ||||||||||||||||

| Shareholder | LLC Shares | Percent Ownership | Omani Rials | US Dollars | ||||||||||||

| Omagine | 3,000,000 | 60% | OMR | 300,000 | $ | 780,000 | ||||||||||

| RCA | 1,250,000 | 25% | OMR | 284,344,792 | $ | 739,296,459 | ||||||||||

| CCC-Panama (or New Investor) | 500,000 | 10% | OMR | 12,673,333 | $ | 32,950,666 | ||||||||||

| CCC-Oman | 250,000 | 5% | OMR | 6,336,667 | $ | 16,475,334 | ||||||||||

| Total: | 5,000,000 | 100% | OMR | 303,654,792 | $ | 789,502,459 | ||||||||||

Neither CCC nor RCA is an affiliate of Omagine. The Shareholder Agreement also specifies, among other things, the corporate governance and management policies of LLC and it provides for the LLC shares presently owned by JOL to be transferred to Omagine subsequent to the signing of the DA. We presently expect this share transfer to occur at the time of the Transformation of LLC into a joint stock company.

The foregoing summary of the terms of the Shareholder Agreement does not purport to be complete and is qualified in its entirety by reference to the full text of the Shareholder Agreement attached hereto as Exhibit 10.6.

The Al Rayan Bank Loan

During 2015 management has conducted a multitude of investor presentations across the MENA Region with potential LLC equity investors including sovereign funds, investment funds and high net-worth individuals. Several of these investors expressed interest in becoming shareholders of LLC but in all such cases, management concluded that the percentage of LLC equity required by such investors was excessive and much too dilutive to the LLC Shareholders (and indirectly dilutive to our Omagine shareholders via their 60% ownership of LLC).

As of the date hereof, in order to finance the First Phase in the most efficient and effective way which involved zero direct or indirect shareholder dilution:

| i. | LLC management concluded a $25 million Financing Agreement on November 29, 2015 with Masraf Al Rayan, an Islamic Bank in the State of Qatar, |

| ii | LLC attempted to finalize the CCC Contract but was delayed in this effort (See: “The Present State of Affairs – An Overview”, above, and |

LLC management remains in contact with the Qatari Bank and believes that the Al Rayan Bank Loan will remain available to LLC for the near foreseeable future. No assurances can be given that such discussions with the Qatari Bank will be conclusive or that the Al Rayan Bank Loan will actually be made. Investors and shareholders should not rely on such Al Rayan Bank Loan being made until it is actually finalized and the proceeds are actually delivered to LLC.

| 13 |

The proposed $25 million Al Rayan Bank Loan is subject to the definitive Al Rayan Loan Agreement which contains several conditions precedent that must be satisfied before LLC can receive the $25 million proceeds of the Al Rayan Bank Loan. One of the conditions precedent is that the Al Rayan Bank Loan be secured by a $25 million cash deposit in an LLC account at the Qatari Bank. Assuming the CCC Contract is signed, RCA and CCC will be then obligated to make their Deferred Cash Investments into LLC in the aggregate amount of approximately $69 million after which LLC will then deposit $25 million in its account at the Qatari Bank to secure the Al Rayan Bank Loan and the condition precedent with respect to LLC’s right to draw down the $25 million of debt financing will be satisfied.

This somewhat cumbersome structure is a result of the multi-stage legal structure of the investments and debt financing required by the Shareholder Agreement which were structured in 2011 such that the Deferred Cash Investments did not have to be invested into LLC until the First Phase of the Omagine Project’s development and construction was financed and ready to begin.

Pursuant to the Shareholder Agreement, unless amended as is presently under discussion, the obligations of RCA and CCC to make their Deferred Cash Investments into LLC in the aggregate amount of approximately $69 million is presently contingent upon only the signing of the CCC Contract. CCC and LLC are presently negotiating a CCC Contract calling for CCC-Oman to provide a $10 million portion of its Deferred Cash Investment at the time of execution of the CCC Contract and CCC-Panama to withdraw as an LLC investor in favor of a new investor yet to be determined.

Design, Development & Construction:

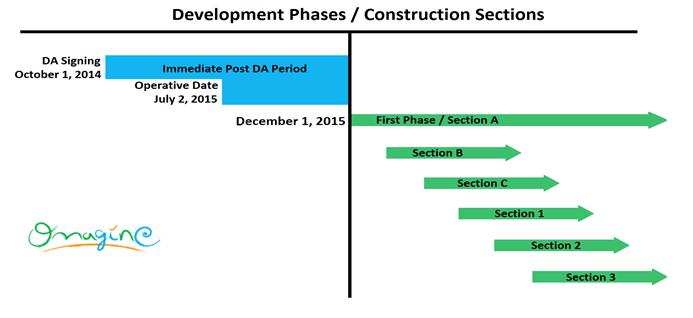

The design, development and construction of the Omagine Project is divided into various phases (each, a “Phase”) and the CCC Contract (as previously and presently drafted) further sub-divides the construction portion of the Omagine Project’s development into various sections (each, a “Section”). Sections may be either “Lettered Sections” which will be priced based on a pre-agreed Schedule of Rates (“SOR”) or “Numbered Sections” which will be priced based on a fixed lump sum basis. All Sections are part of and occur within a Phase (See; “The CCC Contract”, below). The illustration below is indicative only of phased development of the Omagine Project and the December 1, 2015 date will now likely be pushed forward to a date on or before June 1, 2016.

The Immediate Post-DA Period

The Immediate Post-DA Period is the time period between the DA signing and the first Financing Agreement Date. The execution of many initial activities during this period by LLC required the parallel launching by LLC management of many diverse efforts and processes on multiple fronts immediately after the DA Execution Date of October 2, 2014 and continuing through the date hereof. This early initiative fast track strategy (financed entirely by Omagine) greatly benefited LLC to date in many ways, among which are:

| 14 |

| 1. | the DA was Ratified by the Government; |

| 2. | the UA was signed and registered with the Government; |

| 3. | the Operative Date of July 1, 2015 replaced both the Execution Date of October 2, 2014 and the Effective Date of March 11, 2015 referenced in the DA; |

| 4. | three separate valuation studies and reports were commissioned and the valuation of the Land Rights was completed; |

| 5. | expert accounting analyses and reports were received from PwC, Deloitte and the Company’s independent auditor regarding LLC’s purchase of the Land Rights and the recording thereof in LLC’s and the Company’s financial statements; |

| 6. | LLC booked OMR 276,666,667 of new equity which is also reflected in the Company’s consolidated financial statements; |

| 7. | a cost accounting budgetary framework to be used during the development, construction and marketing of the Omagine Project was created by an independent accounting and finance consultant; |

| 8. | an expert IT consultant was selected to architect and install the IT framework and solutions we intend to implement across LLC and the Company and across the Omagine Project’s “smart city” environment; |

| 9. | an independent third party update to our feasibility study was commissioned and completed; |

| 10. | an update of LLC’s internal financial model by specialist real estate investment bankers and advisers was commissioned and completed; |

| 11. | confirmation from banks in Oman (but not from banks outside of Oman) that the value of the Land Rights can be used as collateral to support the Syndicated Bank Financing was received; |

| 12. | the “Brand Identity” and associated brand pillar components and uniform brand messaging platform we intend to implement for Omagine, LLC and the Omagine Project were created; |

| 13. | LLC’s strategic plan was completed; |

| 14. | multiple meetings with, and multiple iterations of proposals and presentations from major mission-critical project consultants (architects, designers, master-planners, engineers, program managers, quantity surveyors, real estate advisers, hospitality advisers, hotel management companies, financial advisers and others) have been received, reviewed and analyzed by management and selections of many consultants have been made by management; |

| 15. | candidates for ten senior LLC executive positions have been recruited, interviewed and selected; |

| 16. | extensive and multiple presentations and meetings with potential LLC equity investors in six MENA Region countries, Europe, Asia and the U.S. were conducted and while most offers were declined by LLC, negotiations with several selected strategic investors are still ongoing; |

| 17. | extensive and multiple presentations and meetings with local, regional and international banks in Oman, the MENA Region and Europe with respect to the provision of Syndicated Bank Financing have occurred and these discussions and negotiations are ongoing with Chinese and U.S based banks since the onset of the above mentioned liquidity squeeze in GCC banks; |

| 18. | Multiple drafts of the CCC Contract have been created and the final attempt to close this transaction is now underway after many delays, and |

| 19. | several other contracts for mission-critical consultants are presently being prepared, |

| 20. | parallel negotiations with two multi-billion dollar Chinese contractor / investors are underway and such talks require Project Finance for the Omagine Project to be included in any offer to LLC, |

| 21. | CCC and LLC are presently negotiating a CCC Contract calling for CCC-Oman to provide a $10 million portion of its Deferred Cash Investment at the time of execution of the CCC Contract. |

The execution of this LLC fast-track strategy during the Immediate Post-DA Period was meant to expedite the execution of the First Phase, which is now delayed for lack of the RCA and CCIC Deferred investments being made as originally contemplated by the Shareholder Agreement. The Immediate Post-DA Period is now essentially completed and the First Phase of development and construction of the Omagine Project is ready to begin. Shortly as soon as the necessary approximately $20 to $25 million of financing therefor is secured.

| 15 |

The CCC Contract

Descriptions of the draft CCC Contract as previously disclosed are no longer accurate or operative as we have now agreed to a management type General Contractor agreement with CCC-Oman based on a flat fee. We have not yet agreed all the details of this agreement and management is meeting in Athens from April 15, 2015 onward until such time as this draft is finalized.

If agreement is reached with CCC, management will proceed to London to meet with its lawyers for a final review; then present the draft to RCA for its consent and approval; and then return to Athens and/or Muscat to execute and sign the CCC Contract

Notwithstanding the foregoing and given our recent experience, management can give no assurance whatsoever at this time that the CCC Contract will in fact be signed at all. We will report further on these negotiations and developments with CCC as they unfold in the next few weeks.

If successfully agreed, the CCC Contract will be based on internationally accepted contracting standards promulgated by the International Federation of Consulting Engineers (“FIDIC”) and will contain a set of industry standard performance parameters, incentives and penalties to ensure Omagine LLC’s interests are protected and that value is delivered.

Such a contract approach conceivably could have CCC perform as construction manager in addition to general contractor with liability for the quality and scheduled performance off all sub-contractors as is now under discussion. CCC would have the ability to be part of the tendering process for any Section of the project as described below but would not earn its flat fee for any such Section it actually constructed rather than managed.

LLC would manage the tendering and competitive process and would choose any of the subcontractors, however CCC would be responsible for managing such subcontractors. CCC regularly employs various subcontractors for its numerous projects and that approach for the Omagine Project under the CCC Contract would include such subcontractors for which there is an ample supply of qualified choices in Oman. CCC and LLC management remain willing partners - and foresee the conclusion of the CCC contract process in due course after which it will be presented to the LLC Shareholders for their consideration and expected approval. The CCC Contract is one of the cornerstone agreements for the Omagine Project and the many considerations are both complex and interconnected with investment considerations.

The CCC Contract will still call for the construction work required for the entire Omagine Project is sub-divided into Sections. Each Section will then be executed by a sub-contractor to CCC-Oman pursuant to the relevant written “Notice to Proceed” issued by LLC with respect to such Section. The Notice to Proceed for any Section contains the relevant design and specifications for the work comprising that Section as well as any Section specific instructions or information.

Sections for which detailed design and specification criteria are not usually required for the work involved (e.g.: fencing, surveying, soil testing, earthworks, dredging, site leveling, etc. [collectively, the “Enabling Works”] are referred to as “Lettered Sections” and they are labeled as Section A, Section B, Section C, Section D, etc.

Sections for which a high level of detailed design and precise specification criteria are usually or always required for the work involved - and for which such design and specifications are very important to LLC in order to assure itself of the desired design outcomes [e.g.: buildings, building foundations, roads, landscaping, underground facilities for parking, storage or utilities, above and below ground construction of buildings and all manner of horizontal or vertical permanent structures, fixtures and elements of the Omagine Project (collectively, the “Permanent Works”)] are referred to as “Numbered Sections” and they are labeled as Section 1, Section 2, Section 3, Section 4, etc.

The First Phase, which includes among other things the construction activities to be enumerated in the Notice to Proceed for Lettered Section A of the CCC Contract (“Section A”), will require the approximately $25 million of financing which management planned to have been provided by the Al Rayan Bank Loan and the Deferred Cash Investments described above. This plan may now be modified by ongoing discussions with RCA and CCIC.

The amount that LLC will pay CCC-Oman for the construction of each Section by its sub-contractor will be individually negotiated and agreed per Section (an “Agreed Contract Amount”) prior to LLC issuing a written Notice to Proceed with respect to such Section. Each Agreed Contract Amount for a Section is subject to adjustment and finalization pursuant to the provisions of the CCC Contract into a final “Contract Price” after the relevant Section is completed.

| 16 |

The Agreed Contract Amount and final Contract Price for each Section is determined as follows:

i. For any Lettered Section, the Agreed Contract Amount is based on:

| a. | the quantities of work, materials and activities specified in the relevant Notice to Proceed as being required for the completion of such Lettered Section, and |

| b. | the unit pricing for such work, material or activity as memorialized in the agreed Schedule of Rates (“SOR”) attached to the relevant Notice to Proceed., and |

the final Contract Price for Lettered Sections will be calculated by direct observation, re-measurement and counting by LLC’s Quantity Surveyor of the units of work, materials and/or activities actually utilized to complete such Lettered Section.

It is anticipated that several Lettered Sections will be under construction simultaneously and/or in rapid succession as the required Enabling Works are identified and executed. During the First Phase LLC will pay CCC-Oman for all Lettered Sections its sub-contractors undertake based on the relevant Notices to Proceed, the SOR and the BOM.

ii. For any Numbered Section, the Agreed Contract Amount is the lump-sum fixed price for such Numbered Section stated in the relevant Notice to Proceed and such Agreed Contract Amount is the final Contract Price for such Numbered Section absent any adjustment thereto pursuant to a written “Variation Order” issued by LLC.

As part of the masterplanning, we will develop a phasing program for the entire project and as the design and/or specifications of any Section is sufficiently completed such that LLC can put it out for competitive bidding it will do so and CCC-Oman will manage and oversee the work of the successful bidder who will be a sub-contractor to CCC-Oman.

CCC-Oman will only commence construction activities on Sections after the competitive bids therefore are examined and a contract award is made by LLC.

It is anticipated that several Sections will be under construction simultaneously in an overlapping manner as the various designs and specifications for the various Sections are sequentially completed. Construction on Sections will continue until the conclusion of all Permanent Works constituting the Omagine Project are completed.

Section A which is part of the First Phase is presently estimated to have an Agreed Contract Amount of approximately $6 million. Further Lettered Sections may be added to the First Phase depending upon the site conditions encountered and the availability of the necessary financing at the time.

LLC plans to maintain a robust control of the design of each Section through to completion. LLC’s intention is to have CCC-Oman work closely with LLC and its masterplanner and architects to ensure that CCC’s constructability and value engineering advice are integrated into the final design for each Section.

Development Phases / Construction Sections / The Financing Agreement Date / The Deferred Cash Investments

It is anticipated that the Omagine Project will be developed in several phases and each such phase will likely include one or more Sections of construction. It is expected therefore that several tranches of project financing from banks or other financial institutions (including possibly the Al Rayan Bank Loan) will occur and several Financing Agreements will likely be executed during the course of the project’s phased development and construction. The first Financing Agreement Date occurred on November 29, 2015 with the signing of the Al Rayan Loan agreement. Until such other Financing Agreements are actually executed by the parties however, no assurance can be given that they actually will be so executed or that such project financing will be available to LLC. Each such further Financing Agreement, if any, is expected to coincide approximately with the beginning of a new development and construction phase, all of which phases will include design, marketing and one or more new Sections of construction activities. The closing of a tranche of Project Finance whether from banks, financial institutions or from Syndicated Bank Financing will each be likely memorialized by a separate Financing Agreement. The November 29, 2015 execution date of the first such Financing Agreement with Masraf Al Rayan is defined in the Shareholder Agreement as the “Financing Agreement Date”.

| 17 |

The earlier the Financing Agreement Date occurs, the better it was expected to be for LLC, the Omagine Project, and all concerned for a variety of reasons but this has now been complicated by present economic conditions in the MENA Region. (See: “The Present State of Affairs – An Overview”, above.) These anticipated early benefits to the Omagine Project are now unlikely to occur until the Deferred Investment question is resolved with CCIC – and even then the present liquidity squeeze in GCC banks which didn’t exist a year ago will likely have a negative impact on our Project Finance efforts.

LLC is presently exploring other possible Equity Sales and Debt Facilities in order to finance the First Phase as well as a possible increase in the scope of the First Phase activities including additional Lettered Sections as and if required. One of such Debt Facility presently under consideration by management is a secured loan from Omagine to LLC if and when sufficient funds are available to Omagine to make such loan. Like any other Debt Facility, this would also be memorialized by a Financing Agreement.

No assurance however can be given at this time as to whether the Company will be successful in arranging either Equity Sales or Debt Facilities or in closing the Al Rayan Bank Loan until such events actually happen.

Any reference in this report to a term or condition of the Development Agreement, the Usufruct Agreement and/or the Shareholders Agreement does not purport to be complete and is qualified in its entirety by reference to the full texts of such agreements. The full text of the Development Agreement is attached hereto as Exhibits 10.7 and 99.1. The full text of the Usufruct Agreement is attached hereto as Exhibits 10.8 and 99.2. The full text of the Shareholder Agreement is attached hereto as Exhibit 10.6.

The First Phase

The First Phase of the development and construction of the Omagine Project (including Lettered Section A) is presently budgeted at approximately $24 million and was ready to begin utilizing the Masraf Al Rayan loan but now must wait until adequate funding to finance this First Phase becomes available to LLC. In addition to the Section A construction activities, the First Phase includes the execution over the 10 to 12 months after its inception of the masterplan, design, engineering, administrative, marketing, and temporary and permanent construction work necessary for vertical construction to begin on Numbered Section 1.

Architectural, design and engineering activities are planned to continue over the next several years after inception of Phase One as the phased development of the project unfolds. The construction of the Permanent Works is expected to accelerate (provided adequate project financing therefor is available to LLC) as Notices to Proceed are issued for the construction of overlapping Numbered Sections following the sequential completion of the design work for such Numbered Sections.

Our present budget (subject to modification as required) for the First Phase of the development and construction of the Omagine Project is as follows:

| Omagine Project – First Phase (including Section A) | ||||

| First 12 Months of Development & Construction Operations – Cash Outflows in USD | ||||

| Description – Task | Annual | |||

| Executive & Financial Management | $ | 827,750 | ||

| Design, Engineering, Planning | $ | 9,006,985 | ||

| Construction Activities & Support Services | $ | 5,519,867 | ||

| Technology & Process Solutions (ERP) | $ | 1,568,750 | ||

| Sales & Marketing: | $ | 4,154,754 | ||

| Administrative & Support Services | $ | 2,061,755 | ||

| 12 Month Total | $ | 23,139,861 |

The approximately 12 month First Phase was planned and expected to begin in January 2016 but was delayed because of present economic conditions in the MENA Region. (See: “The Present State of Affairs – An Overview”, above.). During Phase One we plan to execute Section A and most probably additional Lettered Sections and LLC’s engineers, architects and designers will undertake the masterplanning, engineering and architectural design work for the Omagine Project (the “Design Work”). At the conclusion of the First Phase, the finished design for Numbered Section 1 is expected to be completed. Undertaking the First Phase is contingent upon the availability to LLC of the necessary project financing to do so, which as of the date hereof, has been definitively arranged with the Masraf Al Rayan Loan but such loan has not been accessed due to the present economic conditions in the MENA Region. (See: “The Present State of Affairs – An Overview”, above.).

| 18 |

Masterplanning / Equity Sales / Debt Facilities / Project Financing

The masterplanning of the Omagine Project is planned to occur during the First Phase. It is presently planned that as part of the First Phase - and in parallel with the masterplanning effort - that we will engage the hospitality, real estate, insurance and marketing consultants to execute various professional studies which will inform the masterplanning process and our business plan. These consultants and advisers all contribute to and inform the masterplanning and final design process for the Omagine Project.