Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION - BLUE DOLPHIN ENERGY CO | bdco_ex321.htm |

| EX-31.2 - CERTIFICATION - BLUE DOLPHIN ENERGY CO | bdco_ex312.htm |

| EX-31.1 - CERTIFICATION - BLUE DOLPHIN ENERGY CO | bdco_ex311.htm |

| EX-32.2 - CERTIFICATION - BLUE DOLPHIN ENERGY CO | bdco_ex322.htm |

| EX-21.1 - LIST OF SUBSIDIARIES OF BLUE DOLPHIN - BLUE DOLPHIN ENERGY CO | bdco_ex211.htm |

| EX-23.1 - CONSENT OF UHY LLP - BLUE DOLPHIN ENERGY CO | bdco_ex231.htm |

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

FORM 10-K

(Mark One)

|

[ Ö ]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the fiscal year ended December 31, 2015

or

|

[ ]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to .

Commission File No. 0-15905

BLUE DOLPHIN ENERGY COMPANY

(Exact name of registrant as specified in its charter)

|

Delaware

|

73-1268729

|

|

|

State or other jurisdiction of incorporation or organization

|

(I.R.S. Employer Identification No.)

|

|

801 Travis Street, Suite 2100

Houston, Texas

|

77002

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

(713) 568-4725

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

|

|

Common Stock, par value $0.01 per share

|

OTCQX

|

Securities registered pursuant to Section 12(g) of the Act:

|

(Title of class)

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [ Ö ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [ Ö ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ Ö ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ Ö ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ Ö ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Act.

Large accelerated filer [ ] Accelerated filer [ ] Non-accelerated filer [ ] Smaller Reporting Company [ Ö ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [ Ö ]

The aggregate market value of shares of common stock held by non-affiliates of the registrant was $10,000,310 based on the number of shares of common stock held by non-affiliates and the last reported sale price of the registrant's common stock on December 31, 2015.

|

Number of shares of common stock, par value $0.01 per share outstanding as of March 30, 2016: 10,453,802

|

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

INTRODUCTION

This Annual Report on Form 10-K is a document that U.S. public companies file with the Securities and Exchange Commission (“SEC”) every year. Part I of the Annual Report provides a general overview of our business, including relevant risk factors. Part II of the Annual Report contains financial information and management’s discussion and analysis of our financial condition and results of operations. We hope investors will find it useful to have all of this information in a single document.

Within this Annual Report, “Blue Dolphin,” “we,” “our,” and “us” are used interchangeably to refer to Blue Dolphin Energy Company or to Blue Dolphin Energy Company and its subsidiaries, as appropriate to the context. Information in this Annual Report is current as of the filing date, unless otherwise specified.

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

In this Annual Report, and from time to time throughout the year, we share our expectations for our future performance. These forward-looking statements include statements about our business plans; our expected financial performance, including the anticipated effect of strategic actions; previously reported material weakness in our internal control over financial reporting; economic, political and market conditions; and other factors that could affect our future results of operations or financial position, including, without limitation, statements under the sections entitled “Part I, Item 1. Business,” “Part I, Item 3. Legal Proceedings” and “Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations”. Any statements we make that are not matters of current reportage or historical fact should be considered forward-looking. Such statements often include words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “will,” and similar expressions. By their nature, these types of statements are uncertain and are not guarantees of our future performance. Our forward-looking statements represent our estimates and expectations at the time that we make them. However, circumstances change constantly, often unpredictably, and investors should not place undue reliance on these statements. Many events beyond our control will determine whether our expectations will be realized. We disclaim any current intention or obligation to revise or update any forward-looking statements, or the factors that may affect their realization, whether in light of new information, future events or otherwise, and investors should not rely on us to do so. In the interests of our investors, and in accordance with the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, “Part I, Item 1A. Risk Factors” within this Annual Report explains some of the important reasons that actual results may be materially different from those that we anticipate.

Remainder of Page Intentionally Left Blank

2

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

GLOSSARY OF SELECTED OIL AND GAS TERMS

The following are abbreviations and definitions of certain terms used in this Annual Report, which are commonly used in the oil and gas industry:

|

Atmospheric gas oil (“AGO”). The heaviest product boiled by a crude distillation unit operating at atmospheric pressure. This fraction ordinarily sells as distillate fuel oil, either in pure form or blended with cracked stocks. In-blends atmospheric gas oil, usually serves as the premium quality component used to lift lesser streams to the standards of saleable furnace oil or diesel engine fuel. Certain ethylene plants, called heavy oil crackers, can take AGO as feedstock.

Barrel (“Bbl”). One stock tank barrel, or 42 U.S. gallons of liquid volume, used in reference to oil or other liquid hydrocarbons.

Blending. The physical mixture of a number of different liquid hydrocarbons to produce a finished product with certain desired characteristics. Products can be blended in-line through a manifold system, or batch blended in tanks and vessels. In-line blending of gasoline, distillates, jet fuel and kerosene is accomplished by injecting proportionate amounts of each component into the main stream where turbulence promotes thorough mixing. Additives, including octane enhancers, metal deactivators, anti-oxidants, anti-knock agents, gum and rust inhibitors, and detergents, are added during and/or after blending to result in specifically desired properties not inherent in hydrocarbons.

Barrels per Day (“Bpd”). A measure of oil output, represented by the number of barrels of oil produced in a single day.

Based on operating days.

Capacity utilization rate. A percentage measure that indicates the amount of available capacity that is being used at a facility.

Complexity. A numerical score that denotes, for a given refinery, the extent, capability, and capital intensity of the refining processes downstream of the crude oil distillation unit. The higher a refinery’s complexity, the greater the refinery’s capital investment and number of operating units used to separate feedstock into fractions, improve their quality, and increase the production of higher-valued products. Refinery complexities range from the relatively simple crude oil distillation unit (“topping unit”), which has a complexity of 1.0, to the more complex deep conversion (“coking”) refineries, which have a complexity of 12.0.

Condensate. Liquid hydrocarbons that are produced in conjunction with natural gas. Condensate is chemically more complex than liquefied petroleum gas. Although condensate is sometimes similar to crude oil, it is usually lighter.

Crude oil. A mixture of thousands of chemicals and compounds, primarily hydrocarbons. Crude oil quality is measured in terms of density (light to heavy) and sulfur content (sweet to sour). Crude oil must be broken down into its various components by distillation before these chemicals and compounds can be used as fuels or converted to more valuable products.

Crude oil distillation unit. The refinery processing unit where initial crude oil distillation takes place. See also definition of topping unit.

Cut. One or more crude oil compounds that vaporize and are extracted within a certain temperature range during the crude distillation process.

Depropanizer unit. A distillation column that is used to isolate propane from a mixture containing butane and other heavy components.

Desalting. Removal of salt from crude oil. Desalting is preferably performed prior to commercialization of the crude; must be performed prior to refining.

|

Distillates. The result of crude distillation and therefore any refined oil product. Distillate is more commonly used as an abbreviated form of middle distillate. There are mainly four (4) types of distillates: (i) very light oils or light distillates (e.g., natural gasoline, kerosene, and light and heavy naphtha), (ii) light oils or middle distillates (e.g., kerosene, light and heavy diesel), (iii) medium oils, and (iv) heavy fuel oils, such as our heavy oil-based mud blendstock (“HOBM”).

Distillation. The first step in the refining process whereby crude oil and condensate is heated at atmospheric pressure in the base of a distillation tower. As the temperature increases, the various compounds vaporize in succession at their various boiling points and then rise to prescribed levels within the tower according to their densities, from lightest to heaviest. They then condense in distillation trays and are drawn off individually for further refining. Distillation is also used at other points in the refining process to remove impurities. Lighter products produced in this process can be further refined in a catalytic cracking unit or reforming unit. Heavier products, which cannot be vaporized and separated in this process, can be further distilled in a vacuum distillation unit or coker.

Distillation tower. A tall column-like vessel in which crude oil and condensate is heated and its vaporized components distilled by means of distillation trays.

Exchanger (heat exchanger). A device used to transfer heat from one process liquid to another.

Feedstocks. Crude oil and other hydrocarbons, such as condensate and/or intermediate products, that are used as basic input materials in a refining process. Feedstocks are transformed into one or more finished products.

Fractionation. The separation of crude oil and condensate into its more valuable and usable components through distillation.

Field. An area consisting of a single reservoir or multiple reservoirs all grouped on or related to the same individual geological structural feature and/or stratigraphic condition.

Finished petroleum products. Materials or products which have received the final increments of value through processing operations, and which are being held in inventory for delivery, sale, or use.

Heat exchanger. See definition for exchanger.

Intermediate petroleum products. A petroleum product that might require further processing before it is saleable to the ultimate consumer. This further processing might be done by the producer or by another processor. Thus, an intermediate petroleum product might be a final product for one company and an input for another company that will process it further.

Jet fuel. A high-quality kerosene product primarily used in aviation. Kerosene-type jet fuel (including Jet A and Jet A-1) has a carbon number distribution between about 8 and 16 carbon atoms per molecule; wide-cut or naphtha-type jet fuel (including Jet B) has between about 5 and 15 carbon atoms per molecule. Jet fuel is a white product, so-called because it is transparent.

Kerosene. A middle distillate fraction of crude oil that is produced at higher temperatures than naphtha and lower temperatures than gas oil. It is usually used as jet turbine fuel and sometimes for domestic cooking, heating, and lighting.

|

3

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

|

Leasehold interest. The interest of a lessee under an oil and gas lease.

Light crude. A liquid petroleum that has a low density and flows freely at room temperature. It has a low viscosity, low specific gravity, and a high API gravity due to the presence of a high proportion of light hydrocarbon fractions.

Liquefied petroleum gas (“LPG”). Manufactured during the refining of crude oil and condensate; burns relatively cleanly with no soot and very few sulfur emissions.

Low sulfur diesel. Not to be confused with ultra low sulfur diesel, low sulfur diesel contains a maximum 500 ppm sulfur.

MMcf. One million cubic feet; a measurement of gas volume only.

Naphtha. A refined or partly refined light distillate fraction of crude oil. Blended further or mixed with other materials it can make high-grade motor gasoline or jet fuel. It is also a generic term applied to the lightest and most volatile petroleum fractions.

Net revenue interest. The percentage of production to which the owner of a working interest is entitled.

Non-road, locomotive and marine diesel (“NRLM”). Used in locomotive, marine and non-road diesel engines and equipment, such as farm or construction equipment. Commonly referred to as “off-road” diesel. In the U.S., the EPA fuel standard for “off-road” vehicles was progressively lowered from low sulfur diesel (500 ppm sulfur) to ultra low sulfur diesel (15 ppm sulfur).

Overriding royalty interest. An interest in oil and gas produced at the surface, free of the expense of production that is in addition to the usual royalty interest reserved to the lessor in an oil and gas lease.

Petroleum. A naturally occurring flammable liquid consisting of a complex mixture of hydrocarbons of various molecular weights and other liquid organic compounds. The name petroleum covers both the naturally occurring unprocessed crude oils and petroleum products that are made up of refined crude oil.

Parts per Million “(ppm”). Represents the mass of a chemical or contaminate per unit volume of water.

Product slate. The type of refined petroleum products produced by the refining process.

Propane. A by-product of natural gas processing and petroleum refining. Propane is one of a group of liquefied petroleum gases. The others include butane, propylene, butadiene, butylene, isobutylene and mixtures thereof. See definition of liquefied petroleum gas.

Recommissioning. While commissioning of a new plant facility or refinery helps ensure correct operation of its major systems when first installed, recommissioning helps to restore an existing plant facility or refinery to its originally intended operating performance or capacity. Both processes comprise the integrated application of a set of engineering techniques and procedures to check, inspect and test every operational component of the project, from individual functions such as instruments and equipment, up to complex amalgamations, such as modules, subsystems and systems.

|

Refined petroleum products. Refined petroleum products are derived from crude oil and condensate that have been processed through various refining methods. The resulting products include gasoline, home heating oil, jet fuel, diesel, lubricants and the raw materials for fertilizer, chemicals, and pharmaceuticals. Following the refining process, the products are transported to terminals or local distribution centers for sale to various end-users and consumers.

Refinery. Within the oil and gas industry, a refinery is an industrial processing plant where crude oil and condensate is separated and transformed into marketable refined petroleum products.

Separation. The separation of the different hydrocarbons present in crude oil and condensate depending on their respective boiling ranges. This process takes place in a distillation column.

Sour crude. Crude oil containing sulfur content of more than 0.5%.

Stabilizer unit. A distillation column intended to remove the lighter boiling compounds, such as butane or propane from a product.

Sweet crude. Crude oil containing sulfur content of less than 0.5%.

Sulfur. Present at various levels of concentration in many hydrocarbon deposits, such as petroleum, coal, or natural gas. Also produced as a byproduct of removing sulfur-containing contaminants from natural gas and petroleum. Some of the most commonly used hydrocarbon deposits are categorized according to their sulfur content, with lower sulfur fuels usually selling at a higher, premium price and higher sulfur fuels selling at a lower, or discounted, price.

Topping unit. A type of petroleum refinery that engages in only the first step of the refining process -- crude distillation. A topping unit uses atmospheric distillation to separate crude oil and condensate into constituent petroleum products. A topping unit has a refinery complexity range of 1.0 to 2.0.

Throughput. The volume processed through a unit or a refinery or transported through a pipeline.

Turnaround. Scheduled large-scale maintenance activity wherein an entire process unit is taken offline for a week or more for comprehensive revamp and renewal.

Ultra low sulfur diesel (“ULSD”). A cleaner-burning diesel fuel containing a maximum 15 ppm sulfur. Primarily used for highway vehicles. Commonly referred to as “on-road” diesel.

Undivided interest. A form of ownership interest in which more than one person concurrently owns an interest in the same oil and gas lease or pipeline and in which the interests of the parties are not specified whether by percentage or portion of the property.

West Texas Intermediate (“WTI”). A grade of crude oil used as a benchmark in oil pricing. Described as intermediate because of its relative mid-range density and mid-range sulfur content.

Working interest. The operating interest that gives the owner the right to drill, produce, and conduct operating activities on the property and receive a share of production after the corresponding percentage of operational costs and royalties are paid.

Yield. The percentage of refined petroleum products that is produced from crude oil and other feedstocks.

|

4

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

TABLE OF CONTENTS

|

PART I

|

6 | |

|

ITEM 1.

|

BUSINESS

|

6

|

|

ITEM 1A.

|

RISK FACTORS

|

17

|

|

ITEM 1B.

|

UNRESOLVED STAFF COMMENTS

|

25

|

|

ITEM 2.

|

PROPERTIES

|

25

|

|

ITEM 3.

|

LEGAL PROCEEDINGS

|

26

|

|

ITEM 4.

|

MINE SAFETY DISCLOSURES

|

26

|

|

PART II

|

27

|

|

|

ITEM 5.

|

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

27

|

|

ITEM 6.

|

SELECTED FINANCIAL DATA

|

27

|

|

ITEM 7.

|

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

28

|

|

ITEM 7A.

|

QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

41

|

|

ITEM 8.

|

FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

42

|

|

ITEM 9.

|

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

73

|

|

ITEM 9A.

|

CONTROLS AND PROCEDURES

|

73

|

|

ITEM 9B.

|

OTHER INFORMATION

|

74

|

|

PART III

|

75

|

|

|

ITEM 10.

|

DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

75

|

|

ITEM 11.

|

EXECUTIVE COMPENSATION

|

79

|

|

ITEM 12.

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

81

|

|

ITEM 13.

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE

|

82

|

|

ITEM 14.

|

PRINCIPAL ACCOUNTING FEES AND SERVICES

|

83

|

|

PART IV

|

84

|

|

|

ITEM 15.

|

EXHIBITS, FINANCIAL STATEMENT SCHEDULES

|

84

|

|

SIGNATURES

|

92

|

5

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

PART I

ITEM 1. BUSINESS

Nature of Operations

We are primarily an independent refiner and marketer of petroleum products. Our primary asset is a 15,000 bpd crude oil and condensate processing facility that is located in Nixon, Texas (the “Nixon Facility”). As part of our refinery business segment, we conduct petroleum storage and terminaling operations under third-party lease agreements at the Nixon Facility. We also own and operate pipeline assets and have leasehold interests in oil and gas properties.

Structure and Management

We were formed as a Delaware corporation in 1986. We are currently controlled by Lazarus Energy Holdings, LLC (“LEH”), which owns approximately 81% of our common stock, par value $0.01 per share (the “Common Stock). LEH manages and operates all of our properties pursuant to an Operating Agreement (the “Operating Agreement”). Jonathan P. Carroll is Chairman of the Board of Directors (the “Board”), Chief Executive Officer and President of Blue Dolphin, as well as a majority owner of LEH. See “Part II, Item 8. Financial Statements and Supplementary Data – Note (9) Accounts Payable, Related Party,” “Note (12) Long-Term Debt,” and “Note (20) Commitments and Contingencies – Financing Agreements” of this Annual Report for additional disclosures related to the Operating Agreement, Jonathan P. Carroll, and LEH.

Our operations are conducted through the following operating subsidiaries:

|

·

|

Lazarus Energy, LLC, a Delaware limited liability company (“LE”);

|

|

·

|

Lazarus Refining & Marketing, LLC, a Delaware limited liability company (“LRM”);

|

|

·

|

Blue Dolphin Pipe Line Company, a Delaware corporation;

|

|

·

|

Blue Dolphin Petroleum Company, a Delaware corporation; and

|

|

·

|

Blue Dolphin Services Co., a Texas corporation.

|

Refinery Operations

Overview

The Nixon Facility is situated on approximately 56 acres in Nixon, Wilson County, Texas. The Nixon Facility consists of a distillation unit, naphtha stabilizer unit, depropanizer unit, and related loading and unloading facilities and utilities. At December 31, 2015, the site contained approximately 398,000 bbls of crude oil, condensate, and refined petroleum product storage capacity. We are currently constructing an additional 700,000 bbls of petroleum storage capacity at the Nixon Facility. When construction is complete, total crude oil, condensate, and refind petroleum product storage capacity at the Nixon Facility will exceed 1,000,000 bbls.

The existing Nixon Facility was built in 1980, with a processing capacity of 15,000 bpd. The refinery operated intermittently under various owners from 1980 to 1992. The refinery sat dormant from 1992 until acquired by LE in 2006. LE refurbished the facility, replaced certain key components, and placed the refinery back in service in 2012.

The Nixon Facility is located in the Eagle Ford Shale region of South-Central Texas, among a high concentration of oil and gas properties. Management closely monitors and adjusts the yields of the Nixon Facility’s most profitable refined petroleum products, utilizes an inventory risk management policy to reduce commodity price risk, and tightly manages refinery operating expenses in an effort to maximize refining margins. Under our inventory risk management policy, Genesis Energy, LLC (“Genesis”) may, but is not required to, use derivative instruments when certain of our refined petroleum product inventories exceed certain thresholds.

6

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

Refining Industry Overview

Crude oil refining is the process of separating the hydrocarbons present in crude oil into usable or refined petroleum products such as naphtha, diesel, jet fuel and other products. Crude oil refining is primarily a margin-based business where both crude oil and refined petroleum products are commodities with prices that can fluctuate independently for short periods due to supply, demand, transportation and other factors. In order to increase profitability, or improve margins, it is important for a crude oil refinery to maximize the yields of higher value petroleum products and to minimize the costs of feedstocks and operating expenses. There are also a number of operational efficiencies that can be deployed to improve margins. These include selecting the appropriate crude oil or condensate to fulfill anticipated product demand, increasing the amount and value of refined petroleum products processed from the crude oil or condensate, reducing downtime for maintenance, repair and investment, developing valuable by-products or production inputs out of materials that are typically discarded, and adjusting utilization rates.

Crude oil and condensate supply and demand dynamics vary by region, creating differentiated margin opportunities based on the refinery’s location. The Nixon Facility is located in the Gulf Coast region of the U.S., which is represented by the Energy Information Administration as Petroleum Administration for Defense District 3 (“PADD 3”).

A refinery's product slate depends on the refinery's configuration and the type of crude oil and/or condensate being refined, and can be adjusted based on market demand. Although an increase or decrease in the price for crude oil generally results in a similar increase or decrease in prices for refined petroleum products, there is normally a time lag in the realization of the similar increase or decrease in prices for refined petroleum products. The effect of changes in crude oil prices on a refinery’s results of operations depends, in part, on how quickly and how fully refined petroleum products prices adjust to reflect these changes.

Nixon Facility Process Summary

With a current capacity of 15,000 bpd, the Nixon Facility is considered a “topping unit” because it is primarily comprised of a crude distillation unit, the first stage of the crude oil refining process. The Nixon Facility’s current level of complexity allows us to refine crude oil and condensate into finished and intermediate petroleum products. Our jet fuel is sold in nearby markets, and our intermediate products, including LPG, naphtha, HOBM, and AGO are sold to wholesalers and nearby refineries for further blending and processing. The Nixon Facility uses light crude oil and condensate sourced in the Eagle Ford Shale as feedstock.

Remainder of Page Intentionally Left Blank

7

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

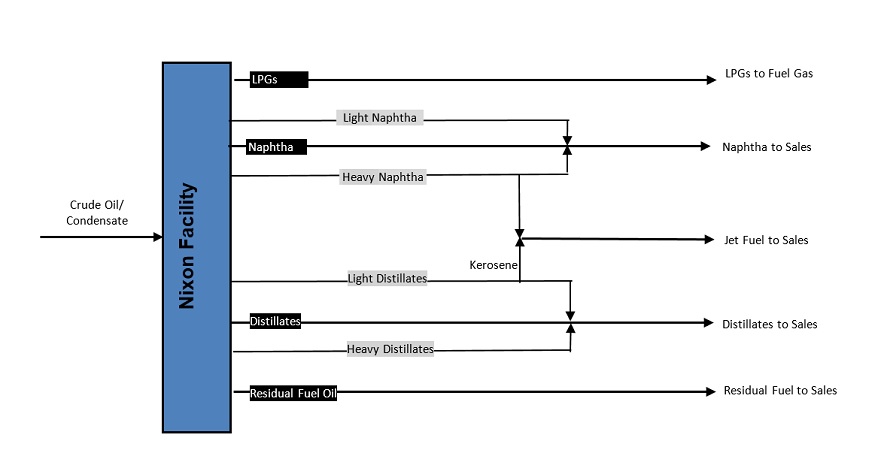

The below diagram represents a high level overview of the current crude oil and condensate refining process at the Nixon Facility.

Example represents a simplified plant configuration. The specific configuration will vary based on various market and operational factors.

Refinery Operations Business Strategy

We plan to continue improving the Nixon Facility in order to support near-term performance. In 2015, we announced plans to expand the Nixon Facility by constructing additional petroleum storage tanks, as well as purchasing, refurbishing, and redeploying idle refinery equipment. Potential benefits of the Nixon Facility expansion plan include:

|

·

|

generating additional revenue from leasing product and crude storage to third parties;

|

|

·

|

having crude and product storage to support refinery throughput and future expansion of up to 30,000 bbls per day; and

|

|

·

|

increasing the processing capacity and complexity of the Nixon Facility.

|

During 2015, we secured $35.0 million in 19 year financing for the Nixon Facility expansion project. To date, we have:

|

(i)

|

completed refurbishment of the naphtha stabilizer and depropanizer units, which improve the overall quality of the naphtha that we produce and help increase the capacity utilization rate of the Nixon Facility;

|

|

(ii)

|

purchased idle refinery equipment, including, among others, a Merox unit, vacuum tower, prefrac tower unit, and LPG fractionator, which may, over time, be refurbished for use at the Nixon Facility;

|

|

(iii)

|

continued debottlenecking efforts, which improve production and efficiency;

|

|

(iv)

|

completed construction of an additional 100,000 bbls of petroleum storage tanks at the Nixon Facility; and

|

8

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

|

(v)

|

made smaller, impactful capital improvements to the Nixon Facility, including refurbishment of the wastewater system, and construction of a new parking area, new access roads, drainage, and tank firewalls.

|

We are currently constructing an additional 700,000 bbls of petroleum storage capacity at the Nixon Facility. When construction is complete, total crude oil, condensate, and refined petroleum product storage capacity at the Nixon Facility will exceed 1,000,000 bbls.

Raw Material Supply

The primary input for the Nixon Facility is crude oil and condensate sourced from the Eagle Ford Shale. As a result of the declining price of crude oil and condensate from late 2014 through 2015, our average crude oil and condensate costs were lower. However, the number of barrels of crude oil and condensate that we processed increased year over year by 317,601 bbls, or nearly 8%, from 3,862,351 bbls for the year ended December 31, 2014, to 4,179,952 bbls for the year ended December 31, 2015.

According to the Energy Information Administration’s January 2016 Short-Term Energy Outlook, there is still high uncertainty in the crude oil price outlook, and crude oil prices are expected to remain low as supply continues to outpace demand in 2016 and more crude oil is placed into storage. With regard to domestic production, although there was a significant decline in total rig counts in 2015, rig counts have largely stabilized in the core counties of the Bakken, Eagle Ford, Niobrara, and Permian. In these areas, falling costs and ongoing technological and process improvements in rig, labor, and well productivity are anticipated to lead to faster rates of well completions and less-rapid production declines relative to other areas. The ongoing gains in learning-by-doing, cost reductions, and rig and well productivity are expected to enhance the economic viability of these areas as well as to be disseminated to other regions, incrementally reducing the breakeven costs of production in more marginal areas.

Crude Oil and Condensate Supply

We purchase the light crude oil and condensate for the Nixon Facility pursuant to an exclusive Crude Oil Supply and Throughput Services Agreement (the “Crude Supply Agreement”) with GEL TEX Marketing, LLC (“GEL”), an affiliate of Genesis. We have the ability to purchase crude oil and condensate from other suppliers with the prior consent of GEL. All crude oil and condensate supplied pursuant to the Crude Supply Agreement is paid for pursuant to the terms of the Joint Marketing Agreement. In addition, we have granted GEL right of first refusal to use three petroleum storage tanks at the Nixon Facility during the term of the Crude Supply Agreement. See “Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Relationship with Genesis” of this Annual Report for more information related to the Crude Supply Agreement.

Subject to certain termination rights, the Crude Supply Agreement had an initial term of three years. The initial term ended in August 2014. However, in October 2013, LE entered into a Letter Agreement Regarding Certain Advances and Related Agreements with GEL and Milam Services, Inc. (“Milam”) (the “October 2013 Letter Agreement”), effective in October 2013. In accordance with the terms of the October 2013 Letter Agreement, LE agreed not to terminate the Crude Supply Agreement and GEL agreed to automatically renew the Crude Supply Agreement at the end of the initial term for successive one year periods until August 2019 unless sooner terminated by GEL with 180 days prior written notice.

Crude oil and condensate is currently received at the Nixon Facility by truck and stored in tanks. The Nixon Facility property is crossed by a crude oil and condensate pipeline owned by Koch Pipeline Company. The pipeline represents a potential future opportunity to receive crude oil and condensate at the Nixon Facility, which could reduce trucking costs.

Electrical Power Supply

A regional electric cooperative supplies electrical power to the Nixon Facility.

Fuel Supply

Fuel gas (LPGs) that are produced at the Nixon Facility are used as fuel within the refinery. In addition, small amounts of propane are occasionally acquired for use in starting-up the Nixon Facility.

9

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

Turnaround and Refinery Reliability

We are committed to the safe and efficient operation of the Nixon Facility. Turnarounds are used to repair, restore, refurbish or replace refinery equipment such as vessels, tanks, reactors, piping, rotating equipment, instrumentation, electrical equipment, heat exchangers and fired heaters. Typically a refinery undergoes a major facility turnaround every three to five years. Since the Nixon Facility is still in the recommissioning phase, one or more of the units may require additional unscheduled downtime for unanticipated maintenance or repairs that are more frequent than our scheduled turnarounds.

Petroleum Refining Market and Competition

The principal competitive factors affecting refineries are crude oil and other feedstock costs, capacity utilization rates, refinery operating expenses, refined petroleum products mix, and product distribution/transportation costs. Many of our principal competitors are larger, independent refining or multinational integrated oil companies (such as Valero, Chevron, ExxonMobil, Shell and ConocoPhillips). These competitors are often better able to withstand volatile market conditions, compete on the basis of price, obtain crude oil in times of shortage and bear the economic risk inherent in all phases of the refining industry because of their larger capitalization, diversified operations, multiple locations, and larger refinery complexities. We compete primarily on the basis of cost. Due to the low complexity of our simple “topping unit” refinery, we can be relatively nimble in adjusting our refined petroleum products slate as a result of changing commodity prices, market demand, and refinery operating costs.

Refining Operations Customers

Customers for our refined petroleum products include distributors, wholesalers and refineries primarily in the lower portion of the Texas Triangle (the Houston - San Antonio - Dallas/Fort Worth area). We have bulk term contracts, including month-to-month, six months, and up to five year terms, in place with most of our customers. Certain of our contracts require us to sell fixed quantities and/or minimum quantities of intermediate and finished petroleum products and many of these arrangements are subject to periodic renegotiation, which could result in us receiving higher or lower relative prices for our refined petroleum products. See “Part II, Item 8. Financial Statements and Supplementary Data – Note (14) Concentration of Risk” of this Annual Report for disclosures related to significant customers.

Pipeline Transportation

Our pipeline transportation operations involve the gathering and transportation of oil and natural gas for producers/shippers operating offshore in the vicinity of our pipelines, as well as leasehold interests in oil and natural gas properties, in the Gulf of Mexico. Our pipeline transportation operations represented less than 1% of total revenue for the years ended December 31, 2015 and 2014.

Acquisition, Disposition and Restructuring Activities

Consistent with our growth strategy, we are continuously engaged in discussions with potential sellers of assets, including LEH, our majority stockholder, regarding the possible purchase of assets and operations that are strategic and complementary to our existing operations. These acquisition efforts may involve participation by us in processes that have been made public and involve a number of potential buyers, commonly referred to as “auction” processes, as well as situations in which we believe we are the only potential buyer or one of a limited number of potential buyers in negotiations with the potential seller. These acquisition efforts often involve assets and operations which, if acquired, could have a material effect on our financial condition and results of operations and require special financing. The closing of any transaction for which we have entered into a definitive agreement will be subject to customary and other closing conditions, which may not ultimately be satisfied or waived. Accordingly, we can give no assurance that any anticipated acquisition efforts will be successful. Although we expect acquisitions to be accretive in the long-term, there can be no assurance that such expectations will ultimately be realized.

10

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

In February 2013, the Board established a Master Limited Partnership (“MLP”) Conversion special committee to oversee a potential conversion of Blue Dolphin from a Delaware “C” corporation to a Delaware MLP. Due to a less hospitable financing market, MLPs were negatively impacted during 2015. The special committee is continuing to evaluate the market. There can be no assurance that the special committee’s review will lead to a proposal for a conversion or restructuring of Blue Dolphin, or if a proposal is made, that such a proposed transaction will be approved or consummated.

Insurance and Risk Management

Our operations are subject to significant hazards and risks inherent in crude oil and condensate refining operations and in the transportation and storage of crude oil and condensate, as well as intermediate and finished petroleum products. We have property damage and business interruption coverage at the Nixon Facility, as well as business interruption coverage for 24 months from the date of the loss, subject to a deductible with a 45 day waiting period. Our property damage insurance has deductibles ranging from $5,000 to $500,000. In addition, we have a full suite of insurance policies covering workers compensation, general liability, directors’ and officers’ liability, environmental liability, and other business risks. These are supported by safety and other risk management programs. See also, “Part I, Item 1A. Risk Factors – Risks Related to Our Business” in this Annual Report.

Governmental Regulation

Our operations and properties are subject to extensive and complex federal, state, and local environmental, health, and safety statutes, regulations, and ordinances. These rules govern, among other things, the generation, storage, handling, use and transportation of petroleum, solid wastes, hazardous wastes, and hazardous substances; the emission and discharge of materials into the environment and environmental protection; waste management; characteristics and composition of diesel and other fuels; and the monitoring, reporting and control of greenhouse gas emissions. These laws impose certain obligations on our operations, including requiring the acquisition of permits and authorizations to conduct regulated activities, restricting the manner in which regulated activities are conducted, limiting the quantities and types of materials that may be released into the environment, and requiring the monitoring of releases of materials into the environment.

Failure to comply with environmental, health or safety laws and our permits or other authorizations issued under such laws could result in fines, civil or criminal penalties or other sanctions, injunctive relief compelling the installation of additional controls, or a revocation of our permits and the shutdown of our facilities.

We cannot predict the extent to which additional environmental, health, and safety laws will be enacted in the future, or how existing or future laws will be interpreted with respect to our operations. Many environmental, health, and safety laws and regulations are becoming increasingly stringent. The cost of compliance with and governmental enforcement of environmental, health, and safety laws may increase in the future. We may be required to make significant capital expenditures or incur increased operating costs to achieve compliance with applicable environmental, health, and safety laws. This Governmental Regulation section should be read in conjunction with “Part I, Item 1A. Risk Factors” of this Annual Report, which discuss our expectations regarding future events, results or outcomes based on currently available information.

Air Emissions

Toxic Air Pollutants. The federal Clean Air Act (the “CAA”) is a comprehensive law that regulates toxic air pollutants from stationary and mobile sources. Among other things, the law authorizes the Environmental Protection Agency (the “EPA”) to establish National Ambient Air Quality Standards to protect public health and public welfare and to regulate emissions of hazardous air pollutants. The CAA, as well as corresponding state laws and regulations regarding emissions of pollutants into the air, affect our crude oil and condensate processing operations and impact certain emissions sources located offshore. Under the CAA, facilities that emit volatile organic compounds (“VOCs”) or nitrogen oxides face increasingly stringent regulations.

Refineries, which are major stationary sources of Hazardous Air Pollutants (“HAPs”), have historically been high-visibility targets for enforcement by the EPA under the CAA. In August 1995, the EPA implemented the National Standards for Hazardous Air Pollutants for petroleum refineries. These standards require petroleum refineries to meet emission standards reflecting the application of the maximum achievable control technology. The affected sources at petroleum refineries are defined to include all process vents, storage vessels, marine tank vessel loading operations, gasoline rack operations, equipment leaks, and wastewater treatment systems located at the refinery. In order to meet emission standards, we are required to obtain permits, as well as test, monitor, report, and implement control requirements.

11

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

In February 2007, the EPA finalized a rule to reduce HAPs from mobile sources. Mobile Source Air Toxics (“MSAT”) regulations established stringent new controls on gasoline, passenger vehicles, and gas cans to further reduce emissions of mobile source air toxics. The EPA has continued to adopt MSAT emission control programs to further reduce HAPs from mobile sources, including sulfur control requirements in gasoline and diesel transportation fuels. New sulfur control standards required most refineries to produce transportation fuels for highway use at or below 15 ppm sulfur for “on-road” diesel and 30 ppm sulfur for gasoline. “Off-road” diesel requirements were also reduced to 15 ppm sulfur in June 2014. We no longer produce transportation-related diesel fuel products. In May 2014, we ceased production of NRLM, a transportation-related diesel fuel product. In June 2014, we began producing HOBM, a non-transportation lubricant blend product. The shift in product slate from NRLM to HOBM was the result of the EPA’s new sulfur control requirements. “Topping units,” like the Nixon Facility, typically lack a desulfurization process unit to lower sulfur content levels within the range required by the EPA’s new sulfur control standards, and integration of such a desulfurization unit generally requires additional permitting and significant capital upgrades. We can still produce and sell diesel with sulfur content levels above the EPA’s new sulfur control standards in the U.S. as a feedstock to other refineries and blenders and to other countries as a finished petroleum product.

In August 2015, the EPA proposed a suite of requirements in an effort to further reduce air pollution, provide greater certainty about CAA permitting requirements, and combat climate change. These proposals include: (i) building on the 2012 New Source Performance Standards for VOC emissions to reduce methane and add emission reduction requirements, (ii) drafting control technique guidelines to reduce VOC emissions from existing equipment and processes, and (iii) clarifying permitting requirements. Final rules on these new proposals are not expected until sometime in 2016.

Greenhouse Gas Emissions. In 2007, the U.S. Supreme Court held in Massachusetts vs. EPA that emission of Greenhouse Gases (“GHGs”) may be regulated as an air pollutant under the CAA. In December 2009, the EPA published its findings that GHGs, including carbon dioxide and methane, are contributing to the warming of the Earth’s atmosphere and other climatic conditions, presenting a potential danger to public health and the environment. By allowing the regulation of GHGs under the CAA, the EPA’s findings also indirectly impacted many other carbon-intensive industries, which would potentially become subject to federal New Source Review Prevention of Significant Deterioration (“PSD”) and Title V permitting requirements under the CAA (the “CAA Permitting Requirements”).

In March 2010, an EPA final decision allowed the EPA to continue applying its existing interpretation of capturing pollutants under CAA Permitting Requirements. In May 2010, the EPA set GHG emissions thresholds to define when permits under the CAA Permitting Requirements are required for new and existing industrial facilities (the “2010 Tailoring Rule”). Emissions from small farms, restaurants, and all but the very largest commercial facilities are not covered by the 2010 Tailoring Rule. The 2010 Tailoring Rule established a schedule that: (i) initially focused on the largest stationary sources with the most CAA permitting experience, (ii) then expanded to cover the largest stationary sources of GHG that may not have been previously covered by the CAA for other pollutants, and (iii) finally described the EPA’s plan for any additional steps in this process. Without this tailoring rule, the lower emissions thresholds would have taken effect automatically for GHGs in January 2011, leading to dramatic increases in the number of required permits. The EPA phased in the 2010 Tailoring Rule in two initial steps:

|

-

|

Step 1 (January 2, 2011 – June 30, 2011). Only stationary sources then subject to the PSD permitting program (i.e., those that are newly-constructed or modified in a way that significantly increases emissions of a pollutant other than GHGs) were subject to permitting requirements for their GHG emissions under PSD. Similarly for the Title V permitting program, only stationary sources then subject to the program (i.e., newly constructed or existing major stationary sources for a pollutant other than GHGs) were subject to Title V permitting requirements for GHG. During this time, no stationary sources were subject to CAA permitting requirements due solely to GHG emissions.

|

12

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

|

-

|

Step 2 (July 1, 2011 to June 30, 2013). Step 2 built on Step 1. In this phase, PSD permitting requirements covered for the first time new construction projects that emit GHG emissions of at least 100,000 tons per year even if they did not exceed the permitting thresholds for any other pollutant. Modifications at existing facilities that increased GHG emissions by at least 75,000 tons per year were subject to permitting requirements, even if they did not significantly increase emissions of any other pollutant. In Step 2, operating permit requirements did, for the first time, apply to stationary sources based on their GHG emissions even if they did not apply based on emissions of any other pollutant. Facilities that emitted at least 100,000 tons per year carbon dioxide equivalent were subject to Title V permitting requirements.

|

Under the 2010 Tailoring Rule, the EPA committed to undertake another rulemaking to add a Step 3 for phasing in GHG permitting and potentially discuss whether certain smaller stationary sources could be permanently excluded from permitting.

In December 2010, the EPA issued a series of rules that put the necessary regulatory framework in place to ensure that: (i) industrial facilities could get CAA permits covering their GHG emissions when needed, and (ii) facilities emitting GHGs at levels below those to be established in a final rule tailoring the requirements would not need to obtain CAA permits. In July 2012, the EPA issued a final 2010 Tailoring Rule Step 3, which retained existing GHG permitting thresholds that were established in Steps 1 and 2 of the 2010 Tailoring Rule. Further, since the EPA and state permitting authorities did not have the opportunity to develop and implement streamlining approaches, it was determined that it was not appropriate to apply CAA Permitting Requirements to additional, smaller stationary sources of GHG emissions.

In August 2015, the EPA issued a good cause final rule to remove portions of its CAA Permitting that were initially promulgated under Step 2 of the 2010 Tailoring Rule, of which the Court of Appeals for the District of Columbia Circuit specifically identified as vacated in the Coalition for Responsible Regulation vs. EPA Amended Judgment that followed the U.S. Supreme Court decision in Utility Air Regulatory Group vs. EPA.

Although we are not currently subject to reporting requirements under GHG-related regulations, the future adoption of any regulations that require reporting of GHGs or otherwise limit emissions of GHGs from the Nixon Facility could require us to incur significant costs and expenses or changes in operations, which could adversely affect our operations and financial condition.

Renewable Fuels

Pursuant to the Energy Policy Act of 2005 and the Energy Independence and Security Act of 2007, the EPA issued Renewable Fuels Standards (“RFS”) that require the blending of biofuels into transportation fuel. Since the compliance mechanism for RFS - Renewable Identification Numbers (“RINs”) – would have created a burden on the Nixon Facility related to its NRLM production through May 2014, we applied for an extension of the temporary exemption afforded small refineries through December 31, 2010 under the CAA Section 211(o)(9)(B). In September 2014, the EPA granted the Nixon Facility a small refinery exemption from RFS requirements for 2013 and 2014. We no longer produce transportation-related diesel fuel products. In May 2014, we ceased production of NRLM, a transportation-related diesel fuel product. In June 2014, we began producing HOBM, a non-transportation lubricant blend product.

Hazardous Waste

The Comprehensive Environmental Response, Compensation, and Liability Act (“CERCLA”) provides a federal "superfund" to clean up uncontrolled or abandoned hazardous waste sites, as well as accidents, spills, and other emergency releases of pollutants and contaminants into the environment. The law authorizes two kinds of response actions: (i) short-term removals, where actions may be taken to address releases or threatened releases requiring prompt response, and (ii) long-term remedial response actions, that permanently and significantly reduce the dangers associated with releases or threats of releases of hazardous substances that are serious, but not immediately life threatening. These actions can be conducted only at sites listed on the EPA's National Priorities List.

13

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

In October 2014, the EPA finalized an amendment to the “All Appropriate Inquiries” (“AAI”) rule. As a result of the amendment, ASTM E-1527-05: Standard Practice for Environmental Site Assessments is no longer adequate to establish landowner and lender liability protections under CERCLA. This means that ASTM E-1527-05 no longer establishes a CERCLA defense. Site buyers, sellers, and lenders will now need to ensure that an AAI is conducted under the newer 2013 ASTM standard. As of the filing of this Annual Report, neither we nor any of our predecessors have been designated as a potentially responsible party under CERCLA or a similar state statute.

The Resource Conservation and Recovery Act (“RCRA”) and comparable state and local laws impose requirements related to the handling, storage, treatment and disposal of solid and hazardous wastes. Our refining operations generate petroleum product wastes, solid wastes, and ordinary industrial wastes, such as from paint and solvents, that are regulated under RCRA and state law. Certain wastes generated by the Nixon Facility are currently exempt from regulation as hazardous wastes, but are subject to non-hazardous waste regulations. In the future these wastes could be designated as hazardous wastes under RCRA or other applicable statutes and therefore may become subject to more rigorous and costly requirements.

In January 2015, the EPA published a final Definition of Solid Waste (“DSW”) rule that distinguished between a waste and a recyclable material under the RCRA. This definition is used to determine the threshold question of whether a given material is regulated as a solid or hazardous waste under RCRA or is instead a recyclable material exempt from regulation. The new DSW rule took effect six months after publication in the Federal Register.

The Nixon Facility has been used for refining activities for many years. Although prior owners and operators may have used operating and waste disposal practices that were standard in the industry at the time, petroleum hydrocarbons and various wastes may have been released on or under the Nixon Facility site. A 2008 third-party environmental study determined that petroleum hydrocarbon and VOC concentrations were below Tier 1 protective concentration levels (“PCLs”). However, RCRA-8 metals were found to be above Tier 1 PCLs. An additional third-party study determined that metal concentrations from the soil would not leach beyond groundwater concentrations exceeding their respective PCLs. As a result, groundwater resources would not be threatened and no further reporting was required.

Water Discharges

Stormwater from the Nixon Facility is tested and discharged pursuant to applicable stormwater permits. Process wastewater from the Nixon Facility is tested and discharged to a nearby municipal treatment facility pursuant to applicable process wastewater permits. Wastewater from our offshore facilities, including our oil and natural gas pipelines and anchor platform, are tested and discharged pursuant to applicable produced water permits.

Spill Prevention and Control

The federal Water Pollution Control Act of 1972, as amended, also known as the Clean Water Act (the “CWA”), and analogous state laws impose restrictions and stringent controls on the discharge of pollutants, including oil, into federal and state waters. These laws affect our crude oil and condensate processing operations and petroleum storage and terminaling operations, as well as our pipeline, facilities, and exploration and production assets. The CWA prohibits the discharge of pollutants into U.S. waters except as authorized by the terms of a permit issued by the EPA or a state agency with delegated authority. Spill prevention, control, and countermeasure requirements mandate the use of structures, such as berms and other secondary containment, to prevent hydrocarbons or other pollutants from reaching a jurisdictional body of water in the event of a spill or leak. Federal and state regulatory agencies can impose administrative, civil, and criminal penalties for non-compliance with discharge permits or other requirements of the CWA or analogous state laws and regulations.

The EPA covers inland oil spills. In June 2015, the EPA published a final rule expanding the definition of “Waters of the United States” under the CWA. The final rule does not expand federal jurisdiction. However, the final rule identifies waters that are specifically excluded from jurisdiction, including, among others, depressions incidental to mining or construction that may become filled with water, puddles, groundwater, and stormwater control features constructed to convey, treat, or store stormwater on dry land. See “Offshore Safety and Environmental Oversight” within this governmental regulation section for information on oil spills that occur in coastal waters.

14

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

Offshore Safety and Environmental Oversight

In addition to the CAA, our pipeline, exploration and production assets are also subject to the requirements of the Outer Continental Shelf Lands Act (the “OCSLA”). The OCSLA is administered by the Bureau of Ocean Energy Management (the “BOEM”) and the Bureau of Safety and Environmental Enforcement (the “BSEE”). The BOEM manages the nation's offshore resources in an environmentally and economically responsible way, including leasing, plan administration, environmental studies, National Environmental Policy Act analysis, resource evaluation, economic analysis, and the Renewable Energy Program. The BSEE enforces safety and environmental regulations, including permitting and research, inspections, offshore regulatory programs, oil spill response, and training and environmental compliance functions. With regard to oil spill response, the BSEE has partnered with the U.S. Coast Guard (“USCG”). In the event of an oil spill, the BSEE is responsible for monitoring and directing all efforts related to securing the source of the spill and re-establishing control over the facility. The USCG is responsible for monitoring and directing all efforts to mitigate a spill’s impact on the water, shoreline, or economic centers that could be impacted, as well as recovering any oil that has spilled. In response to the Deepwater Horizon explosion in 2010, the West Delta 32 explosion in 2012, and the resultant oil spills in the Gulf of Mexico, the BOEM and the BSEE have been more aggressive in proposing and implementing a number of reforms to offshore oil and gas regulations.

Spill Liability. The Oil Pollution Act of 1990 (the “OPA”) and the CWA, in connection with the OCSLA, impose liability on owners or operators of vessels and facilities that discharge harmful quantities of oil into the navigable waters of the U.S., adjoining shorelines, waters of the contiguous zone, or when the discharge may affect natural resources of the U.S. With limited exceptions, responsible parties are: (i) jointly and strictly liable for all removal costs incurred by a governmental authority and (ii) strictly liable for removal costs incurred by and damages to third parties affected by oil spills. Damages recovered from responsible parties include: injury or economic losses resulting from destruction of real or personal property, damages or loss of use of natural resources used for subsistence, lost tax revenue, royalties, rents, or net profit shares suffered by federal, state, or local governments due to injury to real or personal property, lost profits or impaired earning power because of injury to real or personal property or natural resources, and the net costs of providing increased or additional public services during or after removal activities.

In January 2015, the BOEM increased the offshore limit of liability for damages under the OPA from $75 million to $133.65 million, plus all clean-up costs, to reflect the significant increase in the Consumer Price Index. The onshore facilities limit of liability for damages under the OPA is $350 million plus all clean-up costs. A party cannot take advantage of the liability limits if the spill is caused by gross negligence or willful misconduct or resulted from a violation of federal safety, construction or operating regulations. If a party fails to report a spill or cooperate in the clean-up, liability limits do not apply.

The OPA requires responsible parties to provide proof of financial responsibility for potential spills The evidence of financial responsibility amount required is $35 million for certain types of offshore facilities located seaward of the seaward boundary of a state, including properties used for oil transportation. The BOEM’s January 2015 regulatory change did not affect the ongoing required coverage amount. We currently maintain the statutory $35 million coverage.

Spill Response. Pursuant to the OPA, the National Oil and Hazardous Substances Pollution Contingency Plan, more commonly called the National Contingency Plan, provides a blueprint for responding to both oil spills and hazardous substance releases. The National Contingency Plan requires, among other things, that responsible parties have an oil spill response plan in place. We currently have the required oil spill response plan in place.

Decommissioning Requirements. In order to cover the various obligations of lessees and rights-of-way holders operating in federal waters of the Gulf of Mexico, the BOEM generally requires that lessees and rights-of-way holders demonstrate financial strength and reliability according to regulations or post bonds or other acceptable assurances that such obligations will be satisfied, unless the BOEM exempts the lessee or rights-of-way holder from such financial assurance requirements. Such obligations include the cost of plugging and abandoning wells and decommissioning and removing platforms and pipelines at the end of production or service activities. Once plugging and abandonment work has been completed, the collateral backing the financial assurance is released by the BOEM.

In August 2014, the BOEM issued an Advanced Notice of Proposed Rulemaking outlining proposed changes to financial assurance requirements in order to modernize financial assurance and risk management and better address potential costs and liabilities of offshore energy development. Part of the Advanced Notice of Proposed Rulemaking includes the BOEM revising its supplemental bonding procedures by shifting from the current “waiver” model for self-insurance to a credit based model. Following a public comment period, the BOEM plans to publish a revised notice to lessees in 2016 that will outline new financial assurance requirements.

15

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

In August 2015, we received a letter from the BOEM requiring additional supplemental bonds or acceptable financial assurance of approximately $4.2 million for existing pipeline rights-of-way. We are currently working with the BOEM to develop a tailored plan to address the financial assurance requirements. There can be no assurance that the BOEM will accept a reduced amount of supplemental financial assurance or not require additional supplemental pipeline bonds related to our existing pipeline rights-of-way.

At December 31, 2015, we maintained approximately $0.9 million in credit and cash-backed rights-of-way bonds issued to the BOEM. At December 31, 2014, we maintained approximately $1.6 million in credit and cash-backed rights-of-way bonds issued to the BOEM. In December 2014, we completed work to abandon-in-place the pipeline associated with Right-of-Way Number OCS-G 08606. As a result, in November 2015, the BOEM released approximately $0.7 million in cash collateral backing this supplemental pipeline bond.

Offshore Safety. In October 2010, the BSEE issued The Workplace Safety Rule, which requires operators to employ a comprehensive safety and environmental management system (“SEMS”). Revisions to SEMS (“SEMS II”), which added several requirements to the original SEMS, became effective in June 2013. The purpose of SEMS II is to reduce human and organizational errors as root causes of work-related accidents and offshore spills, develop protocols as to who at the facility has the ultimate operational safety and decision-making authority, and establish procedures to provide all personnel with “stop work” authority. SEMS II must be periodically audited by an independent third party auditor approved by the BSEE. We currently have a SEMS II plan in place.

Health, Safety and Maintenance

We are subject to a number of federal and state laws and regulations related to the health and safety of workers pursuant to the Occupational Safety and Health Act of 1970. These laws and regulations are administered by the Occupational Safety and Health Administration (the “OSHA”) and, in states not participating in OSHA-approved state safety plans, comparable state regulatory bodies.

Our refinery operations are also subject to OSHA process safety management regulations. In 2007, the OSHA launched the National Emphasis Program for Petroleum Refineries (the “RNEP”), which requires inspections of all refineries for compliance with process safety management regulations. Under RNEP, the Nixon Facility is subject to inspections that may last from two to six months, including one to three months onsite. Inspectors primarily focus on process safety management implementation and recordkeeping. The Nixon Facility was inspected by OSHA in 2013. As a result of the inspection, we entered into an OSHA settlement agreement in 2014, complying with abatement certification provisions primarily related to documentation and notice posting requirements and paying a penalty totaling $38,500.

We operate a comprehensive safety, health and security program, with participation by personnel at all levels of the organization. We have developed comprehensive safety programs aimed at preventing OSHA recordable incidents. Despite our efforts to achieve excellence in our safety and health performance, there can be no assurances that there will not be accidents resulting in injuries or even fatalities. We routinely monitor our programs and consider improvements in our management systems.

Intellectual Property

We rely on intellectual property laws to protect our brand, as well as those of our subsidiaries. “Blue Dolphin Energy Company” is a registered trademark in the U.S. in name and logo form. “Petroport, Inc.” is a registered trademark in the U.S. in name form. In addition, “www.blue-dolphin-energy.com” is a registered domain name.

16

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

Personnel

We rely on the services of LEH pursuant to an Operating Agreement to manage our property and the property of our subsidiaries, including the Nixon Facility, in the ordinary course of business. LEH provides us with the following services under the Operating Agreement, among others:

|

·

|

Personnel serving in capacities equivalent to the capacities of corporate executive officers, including Chief Executive Officer and Chief Financial Officer, as well as general manager and environmental, health and safety personnel; and

|

|

·

|

Personnel providing administrative and professional services, including accounting, human resources, insurance, and regulatory compliance.

|

See “Part II, Item 8. Financial Statements and Supplementary Data - Note (9), Accounts Payable, Related Party” of this Annual Report for additional disclosures related to LEH.

Available Information

The Securities and Exchange Commission (the “SEC”) maintains and makes available public records, which includes reports filed by regulated companies and individuals, through conventional and electronic reading rooms. The SEC’s conventional reading room is located at 100 F Street, Northeast, Washington, D.C. 20549 and can be reached at (202) 551-8300. The SEC’s electronic reading room, which maintains records created by the SEC on or after November 1, 1996, is available online at http://www.sec.gov/foia/efoiapg.htm. Reports filed with the SEC by regulated entities and individuals are available at http://www.sec.gov/edgar/searchedgar/webusers.htm. We also make our public filings available on our website (http://www.blue-dolphin-energy.com) as soon as reasonably practicable after such material is filed, or furnished, to the SEC. A copy of our filings will also be furnished free of charge upon request.

ITEM 1A. RISK FACTORS

An investment in our Common Stock involves risks. In addition to the other information in this Annual Report and our other filings with the SEC, you should carefully consider the following risk factors in evaluating us and our business. The risks described below are not the only risks we face. Additional risks and uncertainties not specified herein, not currently known to us, or currently deemed to be immaterial may also materially adversely affect our business, financial condition, operating results and/or cash flows.

Any one of these factors or a combination of these factors could materially affect our future results of operations and could influence whether any forward-looking statements ultimately prove to be accurate. Our forward-looking statements are not guarantees of future performance, and actual results and future performance may differ materially from those suggested in any forward-looking statements. We do not intend to update these statements unless we are required to do so.

Risks Related to Our Business and Industry

The dangers inherent in oil and gas operations could expose us to potentially significant losses, costs or liabilities and reduce our liquidity.

Oil and gas operations are inherently subject to significant hazards and risks. These hazards and risks include, but are not limited to, fires, explosions, ruptures, blowouts, spills, third-party interference and equipment failure, any of which could result in interruption or termination of operations, pollution, personal injury and death, or damage to our assets and the property of others. These risks could harm our reputation and business, result in claims against us, and have a material adverse effect on our results of operations and financial condition.

The geographic concentration of our assets creates a significant exposure to the risks of the regional economy and other regional adverse conditions.

Our primary operating asset, the Nixon Facility, is located in Nixon, Texas in the Eagle Ford Shale and we market our refined petroleum products in a single, relatively limited geographic area. In addition, our onshore facilities assets are located in Freeport, Texas, and all of our pipelines, offshore facilities and oil and gas properties are located within the Gulf of Mexico. As a result, our operations are more susceptible to regional economic conditions than our more geographically diversified competitors. Any changes in market conditions, unforeseen circumstances or other events affecting the area in which our assets are located could have a material adverse effect on our business, financial condition, and results of operations. These factors include, among other things, changes in the economy, weather conditions, demographics, and population.

17

|

BLUE DOLPHIN ENERGY COMPANY

|

2015 FORM 10-K

|

Competition from companies having greater financial and other resources could materially and adversely affect our business and results of operations.

The refining industry is highly competitive. Our refining operations compete with domestic refiners and marketers in PADD 3 (Gulf Coast), domestic refiners in other PADD regions, and foreign refiners that import products into the U.S. Certain of our competitors have larger, more complex refineries and may be able to realize higher margins per barrel of production. Several of our principal competitors are integrated national or international oil companies that are larger and have substantially greater resources than we do and have access to proprietary sources of controlled crude oil production. Unlike these competitors, we obtain all of our feedstocks from a single supplier. Because of their integrated operations and larger capitalization, larger, more complex refineries may be more flexible in responding to volatile industry or market conditions, such as crude oil and other feedstocks supply shortages or commodity price fluctuations. If we are unable to compete effectively, we may lose existing customers or fail to acquire new customers.

Environmental laws and regulations could require us to make substantial capital expenditures to remain in compliance or to remediate current or future contamination that could give rise to material liabilities.

Our operations are subject to a variety of federal, state and local environmental laws and regulations relating to the protection of the environment, including those governing the emission or discharge of pollutants into the environment, product specifications and the generation, treatment, storage, transportation, disposal and remediation of solid and hazardous wastes. Violations of these laws and regulations or permit conditions can result in substantial penalties, injunctive orders compelling installation of additional controls, civil and criminal sanctions, permit revocations and/or facility shutdowns.

In addition, new environmental laws and regulations, new interpretations of existing laws and regulations, increased governmental enforcement of laws and regulations or other developments could require us to make additional unforeseen expenditures. Many of these laws and regulations are becoming increasingly stringent, and the cost of compliance with these requirements can be expected to increase over time. The requirements to be met, as well as the technology and length of time available to meet those requirements, continue to develop and change. These expenditures or costs for environmental compliance could have a material adverse effect on our results of operations, financial condition and profitability.

The Nixon Facility operates under a number of federal and state permits, licenses and approvals with terms and conditions containing a significant number of prescriptive limits and performance standards in order to operate. All of these permits, licenses, approvals, limits and standards require a significant amount of monitoring, record keeping and reporting in order to demonstrate compliance with the underlying permit, license, approval, limit or standard. Non-compliance or incomplete documentation of our compliance status may result in the imposition of fines, penalties and injunctive relief. Additionally, due to the nature of our refining processes, there may be times when we are unable to meet the standards and terms and conditions of our permits, licenses and approvals due to operational upsets or malfunctions, which may lead to the imposition of fines and penalties or operating restrictions that may have a material adverse effect on our ability to operate our facilities, and accordingly our financial performance.

We are subject to strict laws and regulations regarding personnel and process safety, and failure to comply with these laws and regulations could have a material adverse effect on our results of operations, financial condition and profitability.