Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - ELAH Holdings, Inc. | rely-ex321_7.htm |

| EX-32.2 - EX-32.2 - ELAH Holdings, Inc. | rely-ex322_6.htm |

| EX-31.2 - EX-31.2 - ELAH Holdings, Inc. | rely-ex312_9.htm |

| EX-31.1 - EX-31.1 - ELAH Holdings, Inc. | rely-ex311_10.htm |

| EX-21 - EX-21 SUBSIDIARIES - ELAH Holdings, Inc. | rely-ex21_393.htm |

| EX-16.1 - EX-16.1 - ELAH Holdings, Inc. | rely-ex161_399.htm |

| EX-23.2 - EX-23.2 CONSENT OF SQUAR MILNER - ELAH Holdings, Inc. | rely-ex232_397.htm |

| EX-23.1 - EX-23.1 CONSENT OF EY - ELAH Holdings, Inc. | rely-ex231_398.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

þ |

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the Fiscal Year Ended December 31, 2015

or

|

¨ |

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number 001-08007

REAL INDUSTRY, INC.

(Exact Name of Registrant as Specified in its Charter)

|

Delaware |

|

46-3783818 |

|

(State or Other Jurisdiction of |

|

(I.R.S. Employer |

|

15301 Ventura Boulevard, Suite 400 |

|

(805) 435-1255 |

|

(Address of Principal Executive Offices) (Zip Code) |

|

(Registrant’s Telephone Number, including Area Code) |

Securities Registered Pursuant to Section 12(b) of the Act:

None

Securities Registered Pursuant to Section 12(g) of the Act:

(Title of Each Class)

Common Stock, $0.001 par value

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act of 1933. ¨ Yes þ No

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes þ No

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þ Yes ¨ No

Indicate by checkmark whether the Registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). þ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Securities Exchange Act of 1934.

|

¨ Large Accelerated Filer |

|

þ Accelerated Filer |

|

|

|

|

|

¨ Non-Accelerated Filer (Do not check if a smaller reporting company) |

|

¨ Smaller Reporting Company |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). ¨ Yes þ No

The aggregate market value of the Registrant’s common stock held by non-affiliates of the Registrant was $275,093,684 on June 30, 2015, the last business day of the Registrant’s most recently completed second fiscal quarter, based on the closing sales price of the Registrant’s common stock on the Nasdaq Stock Exchange, on that date. Shares of the Registrant’s common stock held by each officer, director and each person known to the Registrant to own 10% or more of the outstanding voting power of the Registrant, as of that date, have been excluded since such persons may be deemed to be affiliates. This determination of affiliate status is not a determination for any other purpose.

On February 29, 2016, 29,232,368 shares of the Registrant’s common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates by reference certain information from the Registrant’s definitive proxy statement for the 2016 Annual Meeting of Stockholders to be filed with the Securities and Exchange Commission on or before April 30, 2016.

ANNUAL REPORT ON FORM 10-K

For the Fiscal Year Ended December 31, 2015

TABLE OF CONTENTS

|

|

|

|

Page |

||

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Item 1. |

|

1 |

|

||

|

Item 1A. |

|

8 |

|

||

|

Item 1B. |

|

23 |

|

||

|

Item 2. |

|

24 |

|

||

|

Item 3. |

|

24 |

|

||

|

Item 4. |

|

25 |

|

||

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Item 5. |

|

26 |

|

||

|

Item 6. |

|

29 |

|

||

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

30 |

|

|

|

Item 7A. |

|

51 |

|

||

|

Item 8. |

|

53 |

|

||

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

53 |

|

|

|

Item 9A. |

|

53 |

|

||

|

Item 9B. |

|

56 |

|

||

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Item 10. |

|

57 |

|

||

|

Item 11. |

|

57 |

|

||

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

57 |

|

|

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

|

57 |

|

|

|

Item 14. |

|

57 |

|

||

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Item 15. |

|

58 |

|

||

SAFE HARBOR STATEMENT UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

Certain statements in this Annual Report on Form 10-K for the fiscal year ended December 31, 2015 (the “Annual Report”), including, without limitation, matters discussed under Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (“MD&A”) should be read in conjunction with the consolidated financial statements, related notes, and other detailed information included elsewhere in this Annual Report. We are including this cautionary statement to make applicable and take advantage of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Certain statements that are not historical fact are forward-looking statements. These forward-looking statements can be identified by the use of words such as “believes,” “anticipates,” “expects,” “intends,” “plans,” “projects,” “strategy,” “estimates,” “assumes,” “may,” “should,” “will,” “likely,” “could” or other similar expressions. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause actual results, performance or achievements to differ materially from the forward-looking statements. These forward-looking statements are based on our current beliefs, intentions and expectations. These statements are neither guarantees nor indicative of future performance. Important assumptions and other important factors that could cause changes in our financial condition or results of operations or could cause actual results to differ materially from those forward-looking statements include, but are not limited to:

|

|

· |

changes in domestic and international demand for recycled aluminum, including in the automotive, consumer packaging, aerospace, building and construction, steel, and durable goods manufacturing industries; |

|

|

· |

the cyclical nature of the aluminum industry, material adverse changes in the aluminum industry or end-use segments, such as global and regional supply and demand conditions for aluminum and aluminum products, and changes in our customers’ industries; |

|

|

· |

commodity price fluctuations in the aluminum market and our ability to enter into effective commodity derivatives or arrangements to effectively manage our exposure to such commodity price fluctuations; |

|

|

· |

our ability to use United States (“U.S.”) federal and state net operating loss tax carryforwards (“U.S. NOLs”) and recognize future tax benefits, including in connection with the sale of NABCO, the Real Alloy Acquisition, and the Financings (each as defined below); |

|

|

· |

the servicing of, and the high leverage associated with, the indebtedness from the Financings, security interests in the assets associated with such indebtedness, and compliance with the terms of the indebtedness, including the restrictive covenants that constrain the operation of our business and the businesses of our subsidiaries; |

|

|

· |

disruption in relationships with customers, employees and suppliers relating to the Real Alloy Business (as defined below) and our other businesses as a result of the Real Alloy Acquisition; |

|

|

· |

our ability to successfully identify, acquire and integrate additional companies and businesses that perform and meet expectations after completion of such acquisitions; |

|

|

· |

our ability to achieve future profitability; |

|

|

· |

our ability to control operating costs and other expenses; |

|

|

· |

our ability to secure additional financing; |

|

|

· |

our dependence, as a holding company, on funding from our operating subsidiaries; |

|

|

· |

general economic conditions may be worse than expected; |

|

|

· |

competition among other companies with whom we compete may increase significantly; |

|

|

· |

the loss of key personnel or the ability to cost-effectively attract, retain and motivate key personnel; |

|

|

· |

our ability to maintain effective disclosure controls and procedures and internal control over financial reporting to ensure timely, effective and accurate financial reporting; |

|

|

· |

changes in accounting policies and practices, as may be adopted by regulatory agencies and other organizations, including without limitation the Securities and Exchange Commission (“SEC or “Commission”) and the Financial Accounting Standards Board (“FASB”); |

|

|

· |

changes in laws or government regulations or policies affecting our current business operations and/or the legacy businesses related to residential mortgage lending and servicing, which are now a part of discontinued operations; |

|

|

· |

the impact of current or new litigation matters, or changes in litigation strategies brought against us in our current businesses, or the former businesses of our subsidiary SGGH, LLC (“SGGH”); |

1

|

|

· |

other factors, risks and uncertainties described in this Annual Report under Part I, Item 1A “Risk Factors,” as may be supplemented in our other filings with the Commission from time to time. |

All forward-looking statements set forth herein are qualified by these cautionary statements and are made only as of the date hereof. We undertake no obligation to update or revise the information contained herein including, without limitation, any forward-looking statements whether as a result of new information, subsequent events or circumstances, or otherwise, unless otherwise required by law.

2

Overview

Real Industry, Inc. (“Real Industry,” the “Company,” “we,” “us” or “our”) is a Delaware holding company that operates through subsidiaries. Our business focus is supporting the performance of Real Alloy, a global leader in aluminum recycling and our single largest operating business today, and to make acquisitions of additional operating companies. We seek to acquire meaningful ownership stakes in businesses with talented and experienced management teams, strong customer relationships, and sustainable competitive advantages. We regularly consider acquisitions of businesses that operate in undervalued industries, as well as businesses that we believe are in transition or are otherwise misunderstood by the marketplace. Post-acquisition, we expect to operate our businesses as autonomous subsidiaries, as we do with Real Alloy. We anticipate that we will continue to use our securities to pursue value-enhancing acquisitions and leverage our considerable tax assets, as well as support the needs of our existing operating segments, as necessary.

A key element to our business strategy is utilizing our considerable U.S. NOLs by becoming a significantly profitable enterprise. Our NOLs were predominantly generated by the legacy businesses of Fremont General Corporation (“Fremont”), and as of December 31, 2015, we have U.S. NOLs of approximately $871.8 million, which begin to expire if not used before our 2027 tax year. The ultimate realization of our deferred tax assets, including our U.S. NOLs, depends on our ability to generate future U.S. taxable income through the implementation of our business plan.

Transformation of Real Industry

During the first quarter of 2015, the Company underwent a considerable transformation. On January 9, 2015, we completed the sale of North American Breaker Co., LLC (“NABCO”), previously the primary business within our subsidiary SGGH. On February 27, 2015, we acquired and began operating the global recycling and specification alloys business (the “Real Alloy Business” operated as Real Alloy Holding, Inc. or “Real Alloy”) of Aleris Corporation (“Aleris”) for total consideration of $554.5 million (the “Real Alloy Acquisition”). A portion of the proceeds of the sale of NABCO were used to fund the Real Alloy Acquisition.

The closing of the Real Alloy Acquisition was the culmination of a series of equity and debt financing transactions that began in the fourth quarter of 2014, raising the capital required to fund the Real Alloy Acquisition and pay transaction costs as summarized below (collectively, the “Financings”):

|

|

· |

In October 2014, Real Industry issued 0.3 million shares of common stock at $10.00 per share in a private placement providing gross proceeds of $3.0 million; |

|

|

· |

In December 2014, Real Industry issued approximately 4.4 million shares of common stock at $6.50 per share in an underwritten public offering providing gross proceeds of $28.5 million; |

|

|

· |

In January 2015, Real Alloy issued $305.0 million in senior secured notes due January 2019 (the “Senior Secured Notes”) at a price of 97.206% of the principal amount, providing gross proceeds of $296.5 million; |

|

|

· |

In February 2015, Real Industry issued approximately 9.8 million shares of common stock to existing stockholders in a stapled rights offering (the “Rights Offering”), providing gross proceeds of $55.0 million; |

|

|

· |

In February 2015, certain operating subsidiaries of Real Alloy entered into new credit facilities, including a $110.0 million asset-based lending facility (the “Asset-Based Facility”) and a €50.0 million factoring facility (the “Factoring Facility”); and |

|

|

· |

In February 2015, Real Industry issued 25,000 shares of non-participating preferred stock (the “Redeemable Preferred Stock”) to Aleris, with a liquidation value of $25.0 million. |

The Real Alloy Acquisition was a transformative event for the Company, both in terms of size and substance. We have devoted significant time and attention to integrating and incorporating the Real Alloy Business into the Company, even as a largely stand-alone operating entity. For more information on the details of the Real Alloy Acquisition and the Financings for such transaction, please see Note 1—Business and Operations and Note 3—Business Combinations in the notes to the consolidated financial statements in Part IV, Item 15 of this Annual Report.

2015 – Other Corporate Milestones

On April 21, 2015, our common stock began trading on the Nasdaq Stock Market (“NASDAQ”) under the symbol “RELY.”

1

At our 2015 Annual Meeting of Stockholders on May 28, 2015, our stockholders approved an amendment to our charter to change our name to Real Industry, Inc., we expanded the size of our board of directors (“Board”) to seven members, and a new independent registered public accounting firm was approved.

In June 2015, Real Industry became a member of the Russell Global®, Russell 2000® and Russell Microcap® indexes.

In October 2015, we filed a $700.0 million shelf registration statement on Form S-3 (the “Shelf Registration Statement”) replacing the September 2013 registration statement on Form S-3 that had availability of approximately $200.0 million of registered securities.

Corporate History and Structure

Real Industry, Inc. is the successor to Signature Group Holdings, Inc., a Delaware corporation (“Signature Delaware”), which on January 2, 2014, completed a holding company reorganization and reincorporation from Nevada to Delaware (the “Reincorporation”). The Reincorporation was completed to take advantage of the benefits of Delaware corporate law and to provide a better organizational structure for our future acquisitions and the management of existing operations. To accomplish this, in late 2013, Signature Group Holdings, Inc. a Nevada corporation (“Signature Nevada”) formed SGH Holdco, Inc., a Delaware corporation, and its subsidiary, SGGH. In the Reincorporation, following the approval of Signature Nevada’s stockholders, Signature Nevada merged with and into SGGH, with Signature Nevada ceasing to exist and SGGH continuing as the surviving entity and as a wholly owned subsidiary of SGH Holdco, Inc., which concurrent with the merger, was renamed Signature Group Holdings, Inc. In the Reincorporation, each outstanding share of common stock of Signature Nevada was automatically converted into one share of common stock of Signature Delaware. In May 2015, Signature Delaware was renamed Real Industry, Inc.

Signature Nevada was originally incorporated as Fremont in 1972. Prior to its bankruptcy filing in June 2008, Fremont operated as a financial services holding company. On June 11, 2010 (the “Reorganization Date”), Fremont completed a plan of reorganization and emerged from a nearly two-year reorganization under Chapter 11 bankruptcy proceedings (the “Bankruptcy Proceedings”) as a renamed public company, with significant cash resources and a substantial amount of U.S. NOLs.

After the Reorganization Date, Signature Nevada was repositioned through the divestiture of non-core legacy assets, the settlement and resolution of a significant number of legacy legal actions, and it made select investments through a former specialty lending business segment and acquired NABCO.

In order to preserve the availability of our U.S. NOLs, our Amended and Restated Bylaws include trading restrictions (the “Tax Benefit Preservation Provision”) that imposes on any persons who own, or as a result of a transaction would own, 4.9-percent or more of our common stock in order to reduce the risk that any change in ownership might limit our ability to utilize the U.S. NOLs under Section 382 of the Internal Revenue Code of 1986, as amended (the “Tax Code”), and thereby suffer limitations on our ability to utilize our U.S. NOLs in the future. For more information on the Tax Benefit Preservation Provision, see “Risk Factors—Risks Related to Our Business—Our ability to use our U.S. NOLs to offset future U.S. taxable income may be limited as a result of past events, the Financings, the Real Alloy Acquisition or the other financings, or as the result of future acquisitions or other issuances or transfers of our common stock.” Additionally, we have a Rights Agreement, dated October 23, 2007, as amended, between Fremont and Computershare NA, as successor to Mellon Investor Services LLC, as Rights Agent (the “Rights Agreement”), which was adopted to protect the value of our U.S. NOLs and continues to remain in effect. The Rights Agreement was approved by the Company’s shareholders through the Reincorporation.

Business and Management Strategy

Our business strategy is to take meaningful ownership positions in operating companies that leverage the strengths of our platform, including our status as a public company, our sizable tax assets, and the experience of our executive management team. We seek to acquire companies with sustainable competitive advantages. In considering acquisition opportunities, we seek businesses with management teams that have shown success through business cycles, and have defensible market positions. We regularly consider acquisitions in what we view as undervalued industries, as well as businesses with values we believe to be misunderstood by the marketplace. In all cases we seek opportunities that will be accretive to our earnings.

We believe the Real Alloy Acquisition is consistent with this strategy. For more information on the business operations of Real Alloy, please refer to “Our Segments—RANA and RAEU” in this Item 1. Given our present size and operations, the Real Alloy Acquisition represents a transformative transaction for the Company. During 2015, our management team worked closely with the Real Alloy management team to integrate and incorporate the Real Alloy Business into the Company, even as a largely stand-alone business unit, and certain members of our management will continue to focus on this transition until it is complete. Further, we are working closely with Real Alloy management to accomplish the business objectives and operating strategies of Real Alloy.

2

Beyond the Real Alloy Acquisition, we expect to continue to evaluate acquisition opportunities as permitted by the terms of the Financings, and these may or may not have a strategic relationship with Real Alloy. Potential transactions are typically identified by our chief executive officer (“CEO”), but may be sourced by members of the management team, Board, and others connected with the Company. The bulge bracket investment banks on Wall Street, as well as regional firms, and other organizations around the country, routinely approach Real Industry with acquisition opportunities. Our CEO and management screen such ideas and determine whether to engage in a process. During the second half of 2015, after the Real Alloy Acquisition was closed and the integration efforts were well underway, we recommenced our acquisition efforts, reviewed more than a dozen potential acquisitions, and devoted significant management resources to four such opportunities. We incurred approximately $0.6 million of diligence and advisory costs and expenses, unrelated to Real Alloy, during the year ended December 31, 2015.

Similar to the Real Alloy Acquisition, we expect that most, if not all of our future acquisitions would be separately financed in the credit markets and we anticipate structuring any such financings to minimize the impact on our other businesses. We structured the Financings for the Real Alloy Acquisition, including our stapled Rights Offering, with a view to minimizing ownership shift in our common stock and allowing our existing stockholders the ability to avoid dilution as we grow. At the holding company level, we may enter into financing arrangements, issue securities in secondary offerings, rights offerings or private placements, or provide other financial support under terms that would limit us from additional acquisitions until such financing arrangements are repaid.

In conjunction with our business strategy of making acquisitions, as described above, our management strategy involves proactive strategic, financial and operational support for the management and operations of our business units. Particular areas in which we may provide assistance to our business units include:

|

|

· |

recruiting and retaining talented managers to lead our businesses; |

|

|

· |

monitoring financial and operational performance, instilling consistent financial discipline, and supporting management in the development and implementation of information systems to effectively achieve these goals; |

|

|

· |

assisting management in the development of their analyses and pursuit of prudent organic growth strategies; |

|

|

· |

evaluating capital investments to expand geographic reach, increase capacity, or otherwise grow service or product offerings; |

|

|

· |

identifying and working with management to execute attractive acquisition opportunities in their respective sector or industry; and |

|

|

· |

implementing our Six Sigma, lean operations framework across all subsidiaries. |

As part of our business and operating strategy, we may dispose of businesses or assets we own from time to time via sale, liquidation or other means when attractive opportunities arise that outweigh the potential future value we believe such businesses or assets can bring to us. As such, our decision to dispose of businesses or assets is based on our belief that doing so will increase stockholder value.

As an entity seeking to acquire well-performing companies, we compete in a diverse market with a wide spectrum of capital providers, including private equity funds, investment banks, public and private funds, hedge funds, and high net worth individuals and their family offices. Additionally, we compete with operating companies who seek to make acquisitions for strategic purposes. Real Industry’s existing and potential competitors for acquisitions may be larger, may have easier access to financing sources and a greater ability to issue equity capital in the market generally, may have greater technical and marketing resources, may possess industry-specific overlaps with potential targets, and may have longer standing reputations in the marketplace for acquisitions.

Our Segments – RANA and RAEU

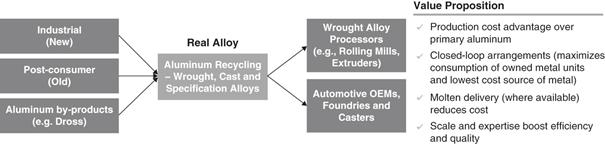

Real Alloy is a global leader in third-party aluminum recycling, which includes the processing of scrap aluminum and by-products and the manufacturing of wrought, cast, and specification or foundry alloys. Real Alloy offers a broad range of products and services to wrought alloy processors, automotive original equipment manufacturers, foundries, and casters. Industries served include automotive, consumer packaging, aerospace, building and construction, steel, and durable goods. Real Alloy delivers recycled metal in liquid or solid form according to customer specifications. Real Alloy’s facilities are capable of processing industrial (new) scrap, post-consumer (old/obsolete) scrap, and various aluminum by-products, giving it a great degree of flexibility in reclaiming high-quality recycled aluminum. Real Alloy currently operates eighteen facilities strategically located throughout North America and six facilities in Germany, Norway, and Wales.

3

Real AlloyWe have two reportable segments, both related to the Real Alloy Business: Real Alloy North America (“RANA”) and Real Alloy Europe (“RAEU”). We are only including the results of operations for these two reportable segments for the period from the acquisition date, February 27, 2015, to December 31, 2015, or approximately ten months, in any performance metric noted as “for the year ended December 31, 2015.”

RANA includes aluminum melting, processing, recycling, and alloying activities conducted in eighteen facilities located in the United States, Canada and Mexico. RANA services customers serving end-uses related to automotive, consumer packaging, construction, transportation, and steel. Approximately 53.8% of RANA’s invoiced sales volume was used in automotive applications in the year ended December 31, 2015. For the year ended December 31, 2015, RANA reported $711.4 million of revenues, representing 62.1% of the Company’s consolidated revenues.

Similar to RANA, RAEU’s operations primarily convert aluminum scrap, dross and other alloying agents, as needed, and deliver the recycled metal in ingot or molten form to customers from six facilities located in Germany, Norway and Wales. RAEU supplies the European automobile industry, which represented approximately 72.0% of this segment’s invoiced sales volume in the year ended December 31, 2015, and other aluminum producers and manufacturers serving other European aluminum industries. For the year ended December 31, 2015, RAEU reported $434.2 million of revenues, representing 37.9% of the Company’s consolidated revenues.

In both RANA and RAEU, Real Alloy conducts business with its customers primarily through tolling arrangements and buy/sell arrangements. Under tolling arrangements, customers pay a fee to convert their own aluminum scrap or by-products into usable recycled metal. Tolling arrangements provide Real Alloy benefits through commodity price risk reduction, earnings stability, and consistent returns on invested capital given the reduced working capital needs associated with tolling. Under buy/sell arrangements, scrap units are purchased in the open market, including from scrap dealers, customers and other producers, and the scrap is processed and sold as wrought or cast alloys to customer specifications. Real Alloy invoiced approximately 375.4 thousand metric tonnes (“kt”) in North America and 176.1 kt in Europe through tolling arrangements, which represented 54.8% of its overall volume for the year ended December 31, 2015, and invoiced approximately 299.9 kt in North America and 155.6 kt in Europe through buy/sell arrangements, which represented 45.2% of its overall volume during the same period. The buy/sell portion of Real Alloy’s business has a much more significant impact on reported revenues and cost of sales compared to tolling arrangements, as the cost of metal is included in both figures.

Real Alloy is a trusted partner in the aluminum recycling industry and has long-standing relationships with a diverse customer base, including many blue-chip multinational companies. Many of Real Alloy’s customers, and all of its top ten customers, have closed-loop arrangements under which customers provide aluminum scrap and by-products generated by their operations, and their scrap and by-products are converted into usable recycled aluminum metal that is returned. Typically, closed-loop arrangements utilize tolling arrangements, though they can also be facilitated through buy/sell arrangements. Closed-loop arrangements benefit customers by enabling them to maximize utilization of their own metal (which is usually their lowest cost alternative), optimize operational efficiencies, and minimize by-product waste. The closed-loop business model also allows Real Alloy to be highly integrated into its customers’ supply chains, further strengthening customer relationships.

Real Alloy’s well-maintained facilities have been equipped with a broad range of pre-processing equipment, such as shredders, dryers and mills, thereby increasing flexibility and enabling it to process multiple grades of scrap and by-products to optimize metal purchases and minimize input costs. Its ability to effectively source and use diverse types of scrap allows Real Alloy to improve business performance. Increased flexibility in raw material input mix improves margins and is expected to help to insulate Real Alloy in periods of unfavorable market conditions while creating significant benefits during upcycles. Additionally, Real Alloy’s centralized purchasing function within each of its operating regions, combined with its broad geographic footprint, allows it to leverage its scale and purchasing expertise to secure the lowest cost aluminum scrap available.

4

With its extensive footprint and strategically located facilities in North America and Europe, Real Alloy effectively and efficiently serves both its global blue-chip customers and its regional and local customers. Most of its operations are located near customers’ facilities, allowing for closed-loop arrangements, as discussed above, and making Real Alloy an integral part of its customers’ supply chain. At twelve facilities, this close proximity allows Real Alloy to deliver “just-in-time” molten metal for direct use in customers’ operations, which differentiates Real Alloy from many of its competitors. In 2015, 41% of Real Alloy’s volume was delivered in molten metal form. This capability is a significant competitive advantage as it enables maximum production efficiency, reduces costs, and reinforces the integrated nature of its customer relationships. With its multi-location operation, aluminum scrap or by-products can be taken from a customer in one location, with recycled metal delivered back to that same customer in a different location and/or as a different alloy.

Real Alloy’s scale, broad geographic footprint across two continents and comprehensive product and service offerings positions it to capitalize on favorable industry trends. Unlike other metals, aluminum is infinitely recyclable without any loss of quality, thus making recycled, or secondary aluminum, just as desirable and usable as primary aluminum. This characteristic, coupled with increasing global demand for aluminum and long-term secular growth in key end-markets, provides a positive macro environment for Real Alloy’s growth plans. According to the Freedonia Group, global aluminum demand is projected to grow 5.4% annually from 2012 to 2022. More specifically, in the automotive sector, which represented approximately 59.8% of Real Alloy’s volumes for the year ended December 31, 2015, aluminum consumption is expected to grow by over 17% annually from 2012 to 2017, largely driven by the “lightweighting” of vehicles to meet new regulatory standards. In addition to growing demand in Real Alloy’s key end-markets, demand for recycled aluminum is expected to grow at a faster rate than primary aluminum production in North America and Europe, which is largely driven by the cost and energy efficiency of recycling aluminum. By 2022, secondary aluminum production is expected to comprise nearly 50% of all aluminum production in North America and Europe.

Real Alloy’s operations were shaped through a series of acquisitions, organic growth, and divestitures over the past 30+ years. Prior to ownership by Real Industry and Aleris, much of the recycling and specification alloys business was part of IMCO Recycling Inc. From 2005 through 2007, Aleris completed purchases of several companies, including Alumitech, Inc. and Wabash Alloys, LLC, to enhance its recycling and specification alloys portfolio.

The financial performance of Real Alloy is determined, in part, by the volume of metal processed and invoiced. Increased production volume will normally result in lower per unit costs, while higher invoiced volumes will normally result in additional revenue and associated margins. A significant component of revenue is derived from the price of aluminum scrap, which is a commodity that changes based on both macro and micro economic supply and demand conditions, and which is generally passed through to customers. Revenues and margin percentages are also subject to fluctuation based on the percentage of customer-owned metal tolled or processed. Increased processing under such tolling agreements results in lower revenues and generally also results in higher gross profit margin and net earnings margin compared to buy/sell arrangements. Tolling agreements reduce exposure to the risk of changing metal prices and working capital requirements. Although tolling agreements are beneficial in these ways, the percentage of Real Alloy’s capacity under these agreements is limited by the amount of metal their customers own and the extent they are willing to enter into such arrangements.

In addition to focusing on tolling relationships and carefully managing the size of its commercial inventory position related to its buy/sell business, Real Alloy also utilizes various derivative financial instruments designed to reduce the impact of changing aluminum prices on these net physical purchases and sales, particularly in its European operations. A portion of its buy/sell business is executed based on published indices, which often do not correlate with an index and, therefore, are not hedged. Real Alloy’s risk management practices reduce, but do not eliminate exposure to changing aluminum prices. While these practices limit exposure to unfavorable aluminum price changes, they also limit Real Alloy’s ability to benefit from favorable price changes.

Margins are impacted by the fees charged to customers to process their metal, by “scrap spreads,” which represents the difference between the purchase price of the aluminum scrap Real Alloy buys and its selling prices, and by conversion costs. Aluminum scrap prices tend to be determined regionally and are typically impacted by supply and demand dynamics. While aluminum scrap prices may trend in a similar direction as primary aluminum prices, the extent of price movements is not highly correlated and can cause unpredictable movements in metal spreads of aluminum scrap versus primary aluminum. Real Alloy’s operations are more significantly impacted by scrap spreads, which they strive to maximize by utilizing all grades of aluminum scrap and optimizing metal blends and plant loadings. Additionally, recycling operations are labor intensive and require a significant amount of energy (primarily natural gas and electricity) to melt aluminum scrap or primary aluminum, which is referred to as “conversion costs.”

5

The third-party aluminum recycling industry is highly fragmented, with a few participants in North America and in Europe operating multiple facilities, and many smaller aluminum recyclers that are single plant, family-owned businesses. We believe Real Alloy is the largest third-party aluminum recycler in both North America and Europe. Historically, Real Alloy has competed effectively because of its extensive global footprint, significant production flexibility, superior range of products and services, operational efficiency and flexibility, knowledgeable and experienced management team, well-invested and strategically located facilities, and operational economies of scale. Real Alloy’s main competitors in North America are Scepter Inc., Smelter Service Corporation, Tennessee Aluminum Processors, Inc., Owl’s Head Alloys Inc., Imperial Aluminum, Superior Aluminum Alloys, LLC, Allied Metal Company, Audubon Metals LLC, Spectro Alloys Corporation, Beck Aluminum Corporation, and Timco, a division of TST Inc. Main competitors in Europe are Oetinger Aluminum, AMAG Austria Metall AG, Raffmetal SpA, Trimet Aluminum, and Befesa. Many of Real Alloy’s customers also recycle their own scrap. In the future, such customers may increase the amount of scrap they recycle, and other customers may recycle their own scrap, in lieu of using third-party recycling services.

Raw Materials and Supplies

The buy/sell portion of Real Alloy’s business requires the purchase of aluminum scrap, primary aluminum, and hardeners. Metallics (primary aluminum metal, aluminum scrap, and aluminum dross) represent the largest component of Real Alloy’s cost of sales. The availability and price of these raw materials depends on a number of factors outside of the control of Real Alloy, including general economic conditions, international demand for metallics and internal recycling activities by primary aluminum producers and other consumers of aluminum. Real Alloy purchases its raw materials from a wide spectrum of aluminum scrap dealers, primary aluminum producers, and other intermediaries. During the year ended December 31, 2015, no supplier provided more than 10% of Real Alloy’s metal purchases. The top ten suppliers represented approximately 22% of total metal purchases in 2015.

Energy Supplies

Real Alloy’s operations are dependent on natural gas and electricity, which represent the third largest component of cost of sales after metal and labor costs. Real Alloy purchases the majority of its natural gas and electricity on a spot-market basis. In an effort to acquire the most favorable energy costs, Real Alloy secures a portion of its natural gas and electricity at fixed price commitments. Real Alloy uses forward contracts, as well as contractual price escalators, and pass through mechanics in customer contracts, to reduce the risks associated with natural gas requirements.

Patents and Other Intellectual Property

Real Alloy holds patents registered in the U.S. and other countries relating to its business. In addition to patents, it also possesses other intellectual property, including trademarks, trade names, know-how, developed technology and trade secrets. Although we believe these intellectual property rights are important to the operations of Real Alloy, we do not consider any single patent, trademark, trade name, know-how, developed technology, trade secret or any group of patents, trademarks, trade names, know-how, developed technology or trade secrets to be material to Real Alloy as a whole.

Seasonality

Demand for certain of Real Alloy’s products can be seasonal, depending on market demand related to its automotive customers and rolling mill customers that serve automotive manufacturers. Additionally, Real Alloy’s margins can be influenced by weather due to its impact on scrap availability. Specifically, in regions subject to freezing temperatures and snowfall, the aluminum scrap supply can become temporarily limited during the winter months, putting pressure on margins.

Employees

As of December 31, 2015, Real Alloy had a total of approximately 1,700 employees, including approximately 1,100 in North America and 600 in Europe. Approximately 21% of our U.S. employees and substantially all of our non-U.S. employees are covered by collective bargaining agreements. We believe employee relations are satisfactory.

6

Real Alloy’s operations are subject to U.S. federal, state, and local, and foreign environmental laws and regulations, which govern, among other things, air emissions, wastewater discharges, the handling, storage, and disposal of hazardous substances and wastes, the investigation or remediation of contaminated sites, and employee health and safety. These laws can impose joint and several liability for releases, or threatened releases, of hazardous substances upon statutorily defined parties, including Real Alloy, regardless of fault or the lawfulness of the original activity or disposal. Given the changing nature of environmental legal requirements, Real Alloy may be required, from time to time, to install additional pollution control equipment, make process changes, or take other environmental control measures at some of its facilities to meet future requirements. Currently, and from time to time, Real Alloy is a party to notices of violation brought by environmental agencies concerning laws governing air emissions.

Our aggregate accrual for environmental matters was $16.0 million as of December 31, 2015, including $4.3 million classified in accrued liabilities in the consolidated balance sheets. See Note 3—Business Combinations and Note 23—Commitments and Contingencies in the notes to consolidated financial statements included in Part IV, Item 15 for additional information about environmental obligations assumed in the Real Alloy Acquisition and environmental matters as of December 31, 2015, respectively.

In addition, we have asset retirement obligations of $5.0 million as of December 31, 2015, for costs related to the future removal of asbestos, ongoing monitoring of landfill closure, and underground storage tanks at various facilities, all of which were assumed in the Real Alloy Acquisition. Asset retirement costs identified after the acquisition date are capitalized as long-lived assets (asset retirement cost), and are amortized over the remaining useful life of the related asset. See Note 2—Financial Statement Presentation and Significant Accounting Policies, Note 3—Business Combinations, and Note 11—Asset Retirement Obligations in the notes to consolidated financial statements included in Part IV, Item15 of this Annual Report for additional information about asset retirement obligations.

The processing of scrap generates solid waste in the form of salt cake and baghouse dust. For RANA, salt cake is further processed for recycling at milling operations or disposed of in landfills. For RAEU, salt cake is processed for recycling, but is not disposed of in landfills. Baghouse dust is disposed of in landfills in North America and in underground deposits in Europe. If salt cake was ever classified as a hazardous waste in the U.S., the costs to manage and dispose of salt cake would increase, which could result in significant increased expenditures.

Financial Information about Geographic Areas

The chief operating decision-maker (“CODM”), our CEO, evaluates Real Alloy largely by geographic area. Our reporting segments of RANA and RAEU have been accordingly created representing the Real Alloy businesses in North America and Europe. See Note 19—Segment and Geographic Information in the notes to consolidated financial statements included in Part IV, Item 15 of this Annual Report for additional information about our segments.

Other Business Units of Corporate and Other

As a holding company, we report the administrative, financial and human resource activities related to the oversight of our business segment and units, implementation of our acquisition strategies, maintenance of our public company status and management of our discontinued operations as “Corporate and Other.” As of December 31, 2015, our corporate staff was comprised of eleven individuals none of which are under a collective bargaining agreement and management believes its relationships are good. The holding company plans to charge its business segments management fees for providing oversight and for certain direct and indirect expenses incurred on their behalf. In the case of Real Alloy, for the ten month period ended December 31, 2015, $2.5 million of management fees were charged. Such charges are excluded from Real Alloy’s Adjusted EBITDA, as management excludes such costs when assessing segment performance.

Corporate and Other also includes the assets, liabilities, and results of operations of operating segments that do not meet the criteria of a reportable segment, generally as a result of the size of the segment, including Cosmedicine, LLC (“Cosmedicine”) and Signature Credit Partners, Inc. (“SCP”). Cosmedicine is a 90.0% owned specialty cosmetics company that re-launched a line of prestige skin care products and regimens, including lotions, crèmes and sunscreen in the second half of 2015. Cosmedicine owns the intellectual property and proprietary product formulations of a line of anti-aging skin care and skin protection products. Cosmedicine reported sales of less than $0.1 million in 2015, which were exclusively through its e-commerce channel. SCP was the primary component of a former reportable segment, Special Situations. As of December 31, 2015, SCP has assets of approximately $1.6 million. Management does not expect to deploy additional capital in SCP and expects to generate less than $0.1 million of revenues annually until the remaining mortgage loans receivable portfolio runs off.

7

Discontinued operations presents the financial condition and results of operations of the businesses and operations of our subsidiary SGGH that have been sold, or have been discontinued, including NABCO and certain of Fremont’s former operations where SGGH is still engaged in various legal proceedings. See “Legal Proceedings” in Note 23—Commitments and Contingencies in the notes to consolidated financial statements in Part IV, Item 15 of this Annual Report for more information about the material legal proceedings in which SGGH is involved, all of which are related to Fremont’s former operations. During the first quarter of 2015, NABCO was sold for a pretax gain of $39.7 million and, as a result of a strategic shift in operations, its results of operations have been reclassified to discontinued operations for all periods presented.

As of December 31, 2015, discontinued operations has $0.3 million of assets and $0.8 million of liabilities. See Note 20—Discontinued Operations for additional information about our discontinued operations.

Available Information: Website Access to Periodic Reports

The following information can be found on Real Industry’s website at www.realindustryinc.com:

|

|

· |

the most recent Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as soon as reasonably practicable after the reports have been filed with the Commission. Copies of all of Real Industry’s Form 10-Ks, Form 10-Qs and other reports filed with the Commission can also be obtained from the Commission’s website at https://www.sec.gov; |

|

|

· |

information relating to corporate governance at Real Industry, including our Code of Conduct (for directors and all employees, including executive officers), which also complies with the definition of a “code of ethics” set forth in Section 406(c) of the Sarbanes-Oxley Act of 2002, as required by NASDAQ’s corporate governance requirements. We intend to disclose any amendments to or waivers from these governance documents on our Internet website, in lieu of disclosure on Form 8-K in accordance with Item 5.05(c) of Form 8-K; |

|

|

· |

information about membership on Board committees, as well as the charters of standing committees of the Board; and |

|

|

· |

information relating to transactions in Real Industry’s securities by its directors, executive officers and significant stockholders reportable on Forms 3, 4 and 5, and Schedules 13D and 13G. |

The information contained on our Internet website is not incorporated herein.

Additionally, copies of any of this information will be provided, free of charge, upon written request to the Company’s principal executive offices, Real Industry, Inc., Investor Relations, 15301 Ventura Boulevard, Suite 400, Sherman Oaks, California 91403, or by email request to investor.relations@realindustryinc.com. Our telephone number is (805) 435-1255.

Before deciding to purchase, hold or sell our common stock, you should carefully consider the risks described below in addition to other information contained in this Annual Report and in our other filings with the SEC, including our subsequent reports on Forms 10-Q and 8-K. The risks and uncertainties described below are in addition to risks that apply to most businesses and are not the only ones we face. The order in which the risks appear is not intended as an indication of their relative weight, likelihood or importance. Additional risks and uncertainties that are not presently known to us or that we currently deem immaterial may also affect our business. If any of these known or unknown risks or uncertainties actually occurs, our business, financial condition, results of operations and/or liquidity could be materially and adversely affected. In that event, the market price for our common stock will likely decline and you may lose all or part of your investment.

Risks Related to the Real Alloy Acquisition and the Financings

Following the consummation of the Real Alloy Acquisition, we and Real Alloy have and continue to incur significant cost, time, effort, and attention on integration and the development of necessary support related to its carve-out from Aleris. These may hinder our ability to realize the expected benefits of the Real Alloy Acquisition. We are a holding company and Real Alloy represents a significantly larger operating business than any other business owned by Real Industry. Real Alloy operated substantially on a stand-alone basis from Aleris and maintained its own sales, marketing, product development, manufacturing, and other administrative teams; however, it did receive support from Aleris with respect to legal, purchasing, information technology (“IT”), tax, and certain other financial and operating services such as human resources (“HR”), insurance, and treasury services.

8

While we are operating Real Alloy predominantly as a stand-alone business with substantially the same organizational structure, operations, management team, employees, and locations as were present prior to the Real Alloy Acquisition, the success of the Real Alloy Acquisition will substantially depend on our ability to integrate Real Alloy into Real Industry and support its business needs, as well as effectively manage this significantly larger business. Challenges may include: i) integrating Real Alloy into our accounting and financial reporting system and functions; ii) developing, adapting and maintaining operating and administrative support systems historically provided by Aleris on which Real Alloy has relied, including legal, purchasing, IT, tax, HR, insurance, and treasury services; and iii) Real Alloy’s ability to adapt to our policies, procedures and support systems, including internal controls.

The incorporation of, and development of the necessary support for, Real Alloy could be a lengthy process, requiring substantial expenditures by Real Industry, as well as significant time, effort and attention from the management teams and key employees of both Real Industry and Real Alloy. Such demands could divert needed resources from both businesses. Further, these challenges could result in the loss of key employees, disruption of the ongoing businesses and relationships with customers, suppliers and other third-parties, diversion of management and corporate attention to integration issues, tax costs and inefficiencies, and inconsistencies in standards, controls, IT systems, accounting systems, procedures, policies, Sarbanes-Oxley controls, and other administrative systems. If any of these factors limit our ability to integrate Real Alloy successfully or on a timely basis, we may not achieve the strategic, operational, financial, and other benefits anticipated to result from the Real Alloy Acquisition to the fullest extent, on a timely basis or at all.

For a period following the closing of the Real Alloy Acquisition, we and Real Alloy will be subject to business uncertainties that could adversely affect our and their businesses. Delays in integrating the business could exacerbate these uncertainties and have adverse effects. Uncertainties about the effect of the Real Alloy Acquisition on the employees and customers of both Real Industry and Real Alloy may have an adverse effect on Real Alloy and, consequently, us. Although we and Real Alloy have taken, and continue to take, steps to reduce the potential adverse effects during the integration period, these uncertainties may impair our and Real Alloy’s ability to attract, retain and motivate key personnel. These uncertainties could cause customers, suppliers and others that deal with Real Alloy, and to a lesser degree, our business, to seek to change their existing business relationships. Alternatively, it could cause third-parties who are considering doing business with us or Real Alloy to delay taking action until the Real Alloy Acquisition is fully integrated. Employee retention could be reduced during the integration of the Real Alloy Acquisition, as employees of Real Industry or Real Alloy may experience uncertainty about their future duties or roles. If, despite retention and business partner management efforts, we or Real Alloy lose key employees or customer/supplier relationships because of concerns relating to the uncertainty and difficulty of the integration process or a desire not to remain with Real Industry or Real Alloy, the business, operations, prospects and financial results of the Company could be harmed.

With the completion of the Real Alloy Acquisition, we operate a substantially larger entity in an industry and at locations in which we have not operated, and we are subject to additional regulations, risks and uncertainties that we have not previously faced. These could exceed our expectations and have a negative impact on our financial condition and results of operations. Following the consummation of the Real Alloy Acquisition, the size of the Company and our primary operating segments have changed substantially compared with our previous operations. As a result, any risk or uncertainty that is significant to Real Alloy, including those discussed below under “Risks Related to Real Alloy,” will also be significant to us and could have a negative effect on our financial condition and results of operations.

If Real Alloy is unable to maintain compliance with U.S. federal, state, and local, and foreign regulatory requirements, we could incur substantial costs, including fines, civil penalties, and criminal sanctions or costs associated with upgrades to improve facilities or changes in manufacturing processes in order to achieve and maintain regulatory compliance. While we intend to operate Real Alloy largely as a stand-alone business, our results of operations, financial condition and stock price will largely depend on Real Alloy’s ability to handle its business risks and uncertainties. These risks and uncertainties may exceed our expectations, and it may take time for us to mitigate them.

The market price of our common stock has been volatile, may continue to be volatile, and may be affected by factors different from those affecting our shares prior to the Real Alloy Acquisition. The market price of our common stock has experienced, and may continue to experience, significant volatility. During 2015, our stock price ranged from $5.90 to $13.50. Our previous businesses differ significantly from Real Alloy in several ways, including size, industry, geographic area, and applicable regulations. As a result, the results of operations following the Real Alloy Acquisition and the market price of our shares of common stock may be affected by factors different from those previously affecting our results of operations prior to the Real Alloy Acquisition. In addition, the Company conducted multiple offerings of common stock as part of the Financings, for the Real Alloy Acquisition and general corporate purposes, which may have depressed the market price of our common stock as a result of dilution. The Company may conduct further offerings in the future, and any additional equity offering could dilute our stockholders’ ownership in the Company.

9

The Real Alloy Acquisition may not be accretive to earnings and if not accretive, may cause dilution to our earnings per share. We currently anticipate that the Real Alloy Acquisition will be accretive to our earnings in 2016. This expectation is based on our preliminary estimates, which may change materially. We may encounter additional or unforeseen transaction and integration-related costs, or we may fail to realize all of the anticipated benefits of the Real Alloy Acquisition. Any of these factors could cause a decrease in our earnings per share or decrease or delay the expected accretive effect of the Real Alloy Acquisition and contribute to a decrease in the price of our common stock.

The Real Alloy Acquisition may expose us to unknown or contingent liabilities for which we will not be adequately indemnified. The entities acquired in the Real Alloy Acquisition may have unknown or contingent liabilities, including liabilities for failure to comply with environmental and other laws and regulations, and for litigation or other claims. While the Real Alloy purchase agreement includes indemnification provisions, the total amount of indemnification related to breaches of representations, warranties and covenants is generally capped at $67.0 million, excluding breaches of certain fundamental representations, and representations relating to taxes and Title IV of ERISA, and, generally, Aleris is not obligated to indemnify us until the aggregate amount of all losses exceeds $3 million. However, certain scheduled environmental matters are subject to a deductible of approximately $23.9 million. Based on these provisions we may incur material liabilities for the past activities of Real Alloy. Such liabilities and related legal or other costs and/or resulting reputational damage could negatively impact our business, financial condition and results of operations.

We have issued $25.0 million in Redeemable Preferred Stock to Aleris as partial consideration in the Real Alloy Acquisition, which shares have superior rights to our common stock. In connection with the Real Alloy Acquisition, we issued $25.0 million of newly created Redeemable Preferred Stock to Aleris to be held in an escrow to secure Aleris’ indemnification obligations under the Real Alloy purchase agreement. The Redeemable Preferred Stock could have a material impact on the rights of our common stockholders in terms of dividends, repurchases and redemptions by, or in the event of a liquidation of, the Company.

We will pay quarterly dividends on the Redeemable Preferred Stock, increasing from 7% for the first eighteen months after the issue date, to 8% for the next twelve months, to 9% thereafter, with dividends payable in kind for the first two years, and thereafter in cash. Other than dividends or distributions payable on our common stock in shares of common stock, the Redeemable Preferred Stock ranks superior to our common stock in the payment of accrued and accumulated dividends, declaration and payment of new dividends and distributions, and making of redemptions. In addition, without the consent of the holders of a majority of the Redeemable Preferred Stock, we are prohibited from paying dividends on our common stock until February 27, 2017.

The Redeemable Preferred Stock generally has no voting rights, except, among other customary matters, for any merger (unless the Redeemable Preferred Stock remains outstanding or is purchased at the liquidation preference), for any acquisition valued at more than 5% of the consolidated assets of the Company (so long as at least $10.0 million in aggregate principal amount of Redeemable Preferred Stock remain outstanding), or (until February 27, 2017) for the declaration or payment of cash dividends on common stock or generally the purchase, redemption or acquisition of common stock.

Our debt agreements as of December 31, 2015 and future debt financing arrangements into which we or our subsidiaries may otherwise enter, may contain various covenants that limit our ability to take certain actions and also require us to meet financial maintenance tests. Failure of these tests or to comply with these limits could have a material adverse effect on our operations, business and financial results. As of December 31, 2015, we had approximately $331.1 million of indebtedness outstanding, which was entirely related to Real Alloy. Further, Real Alloy has additional borrowing capacity under the Asset-Based Facility and Factoring Facility. Interest costs related to this indebtedness, together with the dividends on the Redeemable Preferred Stock, will be substantial. The Senior Secured Notes, the Asset-Based Facility, the Factoring Facility and the Redeemable Preferred Stock, and the instruments governing our other future indebtedness contain, or may contain, certain customary restrictions, covenants, provisions for mandatory repayment upon the occurrence of certain events, and provisions for events of default that will require us or Real Alloy to satisfy certain financial tests and maintain certain financial ratios, restrict our or Real Alloy’s ability to engage in specified types of transactions, and otherwise limit the distributions of funds from Real Alloy to us. This overall leverage and the terms of our financing arrangements could:

|

|

· |

limit the ability to pay dividends, especially from Real Alloy, and future subsidiaries, to us; |

|

|

· |

make it more difficult to satisfy obligations under the terms of this indebtedness; |

|

|

· |

limit the ability to refinance this indebtedness on terms acceptable to Real Alloy, us, or at all; |

|

|

· |

limit the flexibility to plan for and adjust to changing business and market conditions in the industries in which we or Real Alloy operate and increase the vulnerability to general adverse economic and industry conditions; |

10

|

|

· |

restrict sales of key assets; |

|

|

· |

limit the ability to substantially change our business or enter into new lines of business; |

|

|

· |

limit the ability to obtain additional financing for working capital, to fund growth or acquisitions or for general corporate purposes, even when necessary to maintain adequate liquidity, particularly if any ratings assigned to our debt securities by rating organizations were revised downward; or |

|

|

· |

cause a competitive disadvantage and may reduce our flexibility in responding to increased competition. |

In addition, the restrictive covenants in the Senior Secured Notes and Asset-Based Facility and certain other indebtedness require us or could require us to maintain specified financial ratios and satisfy other financial conditions and tests. Our ability to meet those financial ratios, conditions and tests will depend on our ongoing financial and operating performance, which, in turn, will be subject to economic conditions and to financial, market, and competitive factors, many of which are beyond our control. A breach of any of these covenants could result in a default under the instruments governing our indebtedness.

With respect to the Real Alloy Acquisition, challenges with integration, the industry, operations and other business, market and acquisition-related risks, as well as various uncertainties and events beyond our control, could affect our ability to comply with such restrictions and covenants. Failure to comply with any of the restrictions and covenants in our existing or future financing arrangements could result in a default under those arrangements and under other arrangements containing cross-default provisions.

Upon the occurrence of an event of default under any such financing arrangement, the relevant lenders could assess increased interest rates, accelerate the maturity of the debt or foreclose upon any collateral securing the debt. In this event, we may lack sufficient funds or other resources to satisfy all of our obligations. In addition, any limitations imposed by financing agreements on our ability to incur additional debt or to take other actions could significantly impair our ability to obtain other financing.

Risks Related to Real Industry as a Holding Company

Our financial condition and results of operations will depend on our ability to acquire and integrate businesses that perform and meet expectations after closing. A key element of our business strategy involves the acquisition and integration of profitable operating businesses. We may experience challenges identifying, financing, consummating and integrating such acquisitions. Competition exists in the market for the acquisition of profitable operating companies. We may not be able to find suitable acquisition opportunities that are available at attractive valuations, if at all. Even if we do find suitable acquisition opportunities, we may not be able to consummate the acquisitions on commercially acceptable terms, as suitable financing arrangements may not be available on acceptable terms, on a timely basis, or at all.

Even if we are successful in completing additional acquisitions, these could require significant investments of capital, management attention, and integration effort. We may also encounter difficulties in assimilating and integrating the operations, personnel, technologies, products, and information systems of acquired companies, and retaining key personnel. We may also incur significant goodwill impairment charges in the future. Acquisitions could disrupt relationships with existing customers, suppliers, and strategic partners of the newly acquired entities and may create other contractual, intellectual property, or employment issues. The acquisition of another company or business may also require us to enter into a business or geographic market in which we have little or no prior experience. These challenges could disrupt our ongoing business, distract our management and employees, harm our reputation and increase our operating costs, and these challenges could be magnified as the size of the acquisition increases.

There can be no assurance that we will be able to consummate any future acquisitions or that, if consummated, we will realize the benefits anticipated from these acquisitions. Even if we are able to grow and build our operations, any failure to manage our growth effectively could have a material adverse effect on our business, financial condition, results of operations and prospects.

11

We have experienced substantial losses from continuing operations in recent years and may experience losses in the future. Although we reported net earnings for the year ended December 31, 2014, primarily as a result of NABCO’s operations, for the years ended December 31, 2015, 2014, 2013, 2012 and 2011, we reported losses from continuing operations of $31.7 million, $0.1 million, $14.2 million, $7.4 million and $9.9 million, respectively. Since emerging from Bankruptcy Proceedings in 2010, we have continued to have significant operating costs at corporate, including compensation, legal, professional and other outside services expenses, occupancy, and other general and administrative expenses. While we believe we made significant progress in reducing our operating costs at corporate since summer 2013, following the sale of NABCO and the consummation of the Real Alloy Acquisition, the nature of our operations and our operating costs have changed significantly. Therefore, we may experience operating losses and net losses in the future, which could make it difficult to fund our operations, finance acquisitions and achieve our business plan, any of which could cause the market price of our common stock to decline.

Our ability to use our U.S. NOLs to offset future U.S. taxable income may be limited as a result of past events, the Financings, the Real Alloy Acquisition or other financings, or as the result of future acquisitions or other issuances or transfers of our common stock. As of December 31, 2015, we reported U.S. NOLs of approximately $871.8 million, which will begin to expire if not used before the tax year ending December 31, 2027. For accounting purposes, a valuation allowance is required to reduce our potential deferred tax assets if it is determined that it is more likely than not that all or some portion of such assets will not be realized due to the lack of sufficient taxable income. As a result of uncertainties about the timing and amount of future U.S. taxable income, we have a full valuation allowance of $382.4 million recorded against our deferred tax assets as of December 31, 2015, and expect to continually review and evaluate the valuation allowance in future periods.

Our ability to fully utilize our existing U.S. NOLs could be limited or eliminated as a result of changes in U.S. federal tax laws and regulations or should we: i) be found by the Internal Revenue Service (“IRS”) to not be able to avail ourselves of Section 382(l)(5) of the Tax Code in connection with the Plan of Reorganization; ii) undergo an “ownership change” as described under Section 382 of the Tax Code; iii) be deemed to have abandoned an active business; or iv) not return to profitability or be only marginally profitable in the future.

Although we cannot assure you that the IRS will agree with our position, we believe that, as of Fremont’s emergence from Bankruptcy Proceedings, Signature Nevada, its successor, and after the Reincorporation in 2014, Real Industry as successor in interest to Signature Delaware has met the criteria under Section 382(l)(5) of the Tax Code to be able to utilize its U.S. NOLs to offset future taxable income, if any.

Our ability to utilize our U.S. NOLs, however, will be subject to significant limitation for U.S. federal income tax purposes if the Company undergoes an “ownership change” as defined in Section 382 of the Tax Code. For this purpose, an “ownership change” is generally defined as greater than a 50% change in equity ownership by value, over a rolling three-year period. We may experience an ownership change in the future as a result of changes in our common stock ownership, which would result in a limitation on our ability to utilize our U.S. NOLs. Separately, any changes to tax rules or the interpretation of tax rules could negatively impact our ability to recognize benefits from our U.S. NOLs.

While there is no guarantee that the IRS will agree with our position, we believe that the Financings and the Real Alloy Acquisition did not result in an ownership change for purposes of Section 382 of the Tax Code. The Company received an opinion letter (the “Section 382 Opinion Letter”) from its U.S. tax counsel, Blank Rome LLP, substantially to the effect that the Financings and Real Alloy Acquisition should not result in an “ownership change” for U.S. federal income tax purposes and that the Company may use its U.S. NOLs to offset future U.S. taxable income generated by Real Alloy. The Section 382 Opinion Letter is restricted to the precise terms described therein and the Company or its stockholders may engage in subsequent transactions that would result in an “ownership change.” Additionally, the Company adopted the Tax Benefit Preservation Provision in order to protect stockholder value by preserving our U.S. NOLs. There is no guarantee, however, that the Tax Benefit Preservation Provision will be effective in protecting our U.S. NOLs and other tax assets.

The amount of our U.S. NOLs has not been audited or otherwise validated by the IRS. The IRS could challenge the amount of our U.S. NOLs and other tax assets, which could result in an increase in our liability for income taxes in the future. Further, our U.S. NOLs only have value to the extent we generate U.S. taxable income. If we are unable to generate U.S. taxable income prior to the expiration of the U.S. NOLs, or if we are only marginally profitable during such period, we will be limited in our ability to utilize the tax benefits related to our U.S. NOLs. There can be no assurance that we will have sufficient U.S. taxable income to be able to utilize our U.S. NOLs prior to their expiration. Finally, the use of U.S. NOLs is subject to various tax laws and regulations and the changes in such or the interpretations thereof.

12

Funding for our future acquisitions and operations could increase our liabilities, trigger negative tax consequences or dilute, or rank preferentially to, our stockholders. We intend to fund any future acquisition through a mix of our available cash, the sale of equity securities in private placements or in registered offerings under our Shelf Registration Statement declared effective on October 21, 2015, rights offerings to existing stockholders, and debt financings. Utilizing these funding sources can result in increased debt or contingent liabilities, adverse tax consequences or substantial capital commitments. Any of these events could negatively impact our financial condition and results of operations and could cause the price of our common stock to decline.

We currently have 9,235,000 shares of blank check preferred stock available for issuance and $700.0 million of securities available for issuance under the Shelf Registration Statement. In order to fund our future operations or acquisitions, we may sell equity securities or convertible debt securities, which securities could have rights, preferences and privileges senior to our existing stockholders. In such event, future security holders could be entitled to dividends, liquidation or other transaction preferences, or voting rights that are not provided to our existing common stockholders. Further, with or without preferential terms, future issuances of securities could result in dilution to our stockholders.