Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - BLOUNT INTERNATIONAL INC | a2015form10-kex21.htm |

| EX-4.H - EXHIBIT 4.H - BLOUNT INTERNATIONAL INC | a2015form10-kex4h.htm |

| EX-23.2 - EXHIBIT 23.2 - BLOUNT INTERNATIONAL INC | a2015form10-kex232.htm |

| EX-32.1 - EXHIBIT 32.1 - BLOUNT INTERNATIONAL INC | a2015form10-kex321.htm |

| EX-31.2 - EXHIBIT 31.2 - BLOUNT INTERNATIONAL INC | a2015form10-kex312.htm |

| EX-31.1 - EXHIBIT 31.1 - BLOUNT INTERNATIONAL INC | a2015form10-kex311.htm |

| EX-32.2 - EXHIBIT 32.2 - BLOUNT INTERNATIONAL INC | a2015form10-kex322.htm |

| EX-23.1 - EXHIBIT 23.1 - BLOUNT INTERNATIONAL INC | a2015form10-kex231.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015.

Or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the transition period from to

Commission file number 001-11549

BLOUNT INTERNATIONAL, INC.

(Exact name of registrant as specified in its charter)

Delaware | 63 0780521 | |

(State of Incorporation) | (I.R.S. Employer Identification No.) | |

4909 SE International Way, Portland, Oregon | 97222-4679 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (503) 653-8881

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, $.01 par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months. ¨ Yes x No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company (as defined in Rule 12b-2 of the Exchange Act).

Large accelerated filer | o | Accelerated filer | x | |||

Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company | o | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

At June 30, 2015, the aggregate market value of the voting and non-voting common stock held by non-affiliates, computed by reference to the last sales price $10.92 as reported by the New York Stock Exchange, was $363,191,086 (affiliates being, for these purposes only, directors, executive officers, and holders of more than 10% of the registrant’s Common Stock).

The number of shares outstanding of $0.01 par value common stock as of March 4, 2016 was 48,250,363 shares.

DOCUMENTS INCORPORATED BY REFERENCE

None.

BLOUNT INTERNATIONAL, INC. AND SUBSIDIARIES

Table of Contents | Page | |

Item 1 | ||

Item 1A | ||

Item 1B | ||

Item 2 | ||

Item 3 | ||

Item 4 | ||

Item 5 | ||

Item 6 | ||

Item 7 | ||

Item 7A | ||

Item 8 | ||

Item 9 | ||

Item 9A | ||

Item 9B | ||

Item 10 | ||

Item 11 | ||

Item 12 | ||

Item 13 | ||

Item 14 | ||

Item 15 | ||

2

PART I

ITEM 1. BUSINESS

Overview. Blount International, Inc. (“Blount” or the “Company”) is a global industrial company. The Company designs, manufactures, and markets equipment, replacement and component parts, and accessories for professionals and consumers in select end-markets under our proprietary brand names. We also manufacture and market such items to original equipment manufacturers (“OEMs”) under private label brand names. We specialize in manufacturing cutting parts and equipment used in forestry, lawn, and garden; farming, ranching, and agricultural; and construction applications. We also purchase products manufactured by other suppliers that are aligned with the markets we serve and market them, typically under one of our brands, through our global sales and distribution network. Our products are sold in more than 110 countries and approximately 51% of our 2015 sales were shipped to customers outside of the United States of America (“U.S.”). Our Company is headquartered in Portland, Oregon, and we have manufacturing operations in the U.S., Brazil, Canada, China, and France. In addition, we operate marketing, sales, and distribution centers in Europe, North America, South America, and the Asia-Pacific region.

We operate in two primary business segments: the Forestry, Lawn, and Garden (“FLAG”) segment and the Farm, Ranch, and Agriculture (“FRAG”) segment. The FLAG segment manufactures and markets cutting chain, guide bars, and drive sprockets for chain saw use, and lawnmower and other cutting blades for outdoor power equipment. In addition, the FLAG segment manufactures cutting chain, guide bars, drive sprockets, and lawnmower and other cutting blades that are marketed to OEM customers. The FLAG segment also purchases replacement parts and accessories from other manufacturers and markets them, primarily under our brands, to our FLAG customers through our global sales and distribution network.

The Company’s FRAG segment designs, manufactures, assembles and markets attachments and implements for tractors in a variety of mowing, cutting, clearing, material handling, landscaping and grounds maintenance applications, as well as log splitters, post-hole diggers, self-propelled lawnmowers, attachments for off-highway construction equipment applications, and other general purpose tractor attachments. In addition, the FRAG segment manufactures a variety of agricultural equipment cutting blade parts that are marketed primarily to OEM customers. The FRAG segment also purchases replacement parts and accessories from other manufacturers and markets them, primarily under our brands, to our FRAG customers through our sales and distribution network.

The Company also operates a concrete cutting and finishing ("CCF") equipment business that is reported within the Corporate and Other category. This business manufactures and markets diamond cutting chain, assembles and markets concrete cutting chain saws, and purchases other concrete cutting products that are marketed to the construction and water utility industries.

Forestry, Lawn, and Garden Segment

Forestry Products. These products are sold primarily under the Oregon®, Carlton®, and KOX™ brands, as well as under private label brands for certain OEM customers. Manufactured product lines include a broad range of cutting chain, chain saw guide bars, and cutting chain drive sprockets used on portable gasoline and electric chain saws and on mechanical timber harvesting equipment. We also purchase and market replacement parts and other accessories for the forestry market, including chain saw engine replacement parts, safety equipment and clothing, lubricants, maintenance tools, hand tools, and other accessories used in forestry applications. We also market a line of electric and cordless electric chain saws under the Oregon® brand.

Lawn and Garden Products. These products are sold under the Oregon® brand name, as well as private labels for certain OEM and retail customers. Manufactured product lines include lawnmower and edger cutting blades designed to fit a wide variety of machines and cutting conditions, cutting blades for grass-cutting equipment, and garden tiller tines. We also purchase and market various cutting attachments, replacement parts, and accessories for the lawn and garden market, such as cutting line for line trimmers, air filters, spark plugs, lubricants, wheels, belts, grass bags, maintenance tools, hand tools, and accessories to service the lawn and garden equipment industry. We also market a line of cordless electric tools including a string trimmer, hedge trimmer, and pole saw under the Oregon® brand name.

Our FLAG products are sold both under our own proprietary brands and under private label brands to OEM customers for use on new chain saws and lawn and garden equipment, and to professionals and consumers as replacement parts through distributors, dealers, and mass merchants. During 2015, approximately 75% of FLAG segment sales were to the replacement market, with the remainder sold to OEMs.

Industry Overview. Our competitors for FLAG products include Ariens, Briggs & Stratton, Fisher Barton, Husqvarna, Jaekel, John Deere, MTD, Northern Tool, OEM Products, Rotary, Stens, Stihl, and TriLink, among others. We work with our OEM customers to improve the design and specifications of cutting chain, guide bars, and lawnmower blades used as original

3

equipment on their products. We also supply products or components to some of our competitors. In addition, new and existing competitors in recent years have expanded capacity or contracted with suppliers in China and other low-cost manufacturing locations, which has increased competition and pricing pressure, particularly for consumer-grade cutting chain and guide bars.

We believe we are the world’s largest producer of cutting chain for chain saws. Oregon®, Carlton®, and KOX branded cutting chain and related products are used by professional loggers, farmers, arborists, and homeowners. We believe we are a leading manufacturer of guide bars and drive sprockets for chain saws. Our OEM customers include the majority of the world’s chain saw manufacturers, and we also produce replacement cutting chain and guide bars to fit virtually every chain saw sold today, and virtually all saw chain timber harvesting equipment in use today. We believe we are a leading supplier of lawnmower blades in Europe. Additionally, our lawnmower blades are used by many of the world’s leading power equipment producers, and our Oregon® branded replacement blades and lawnmower-related parts and accessories are used by commercial landscape companies and homeowners.

Weather and natural disasters can influence our FLAG sales cycle. For example, severe weather patterns and events, such as hurricanes, tornadoes, and storms, generally result in greater chain saw use and, therefore, stronger sales of cutting chain and guide bars. Temperature patterns also drive the demand for firewood, which in turn drives the demand for our cutting chain and other forestry products. Changes in home heating costs can drive the demand for firewood, which in turn affects the demand for our forestry products. Seasonal rainfall plays a role in demand for our lawnmower blades and other lawn and garden equipment products. Above-average rainfall drives greater demand for products in this category, while drought conditions tend to reduce demand for these products. Similarly, changes in housing starts can drive the demand for lumber, which also affects the demand for our forestry products. General economic conditions also drive demand in other markets for timber, including pulp and paper, packaging, lumber, and furniture.

Within the FLAG segment the largest volume raw material we purchase is cold-rolled strip steel, which we obtain from multiple intermediate steel processors, but which can also be obtained from other sources. Changes in the price of steel can have a significant effect on the manufactured cost of our products and on the gross margin we earn from the sale of these products, particularly in the short-term.

Our profitability in the FLAG segment is also affected by changes in foreign currency exchange rates, changes in economic and political conditions in the various markets in which we operate, and changes in the regulatory environment in various jurisdictions. For additional information regarding the FLAG segment, see Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Note 19 to the Consolidated Financial Statements.

Farm, Ranch, and Agriculture Segment

Equipment and Tractor Attachment Products. These products are sold under the AlitecTM, CF®, Gannon®, Oregon®, SpeeCo®, WainRoy®, and Woods® brand names, as well as under private label brands for certain of our OEM and retail customers. Product lines include attachments for tractors in a variety of mowing, cutting, clearing, material handling, landscaping and grounds maintenance applications, as well as log splitters, post-hole diggers, self-propelled lawnmowers, snow blowers, attachments for off-highway construction equipment applications, and other general purpose tractor attachments.

OEM and Aftermarket Parts. These products are sold under the SpeeCo®, TISCO®, Tru-Power®, Vintage Iron®, and WoodsCare™ brand names, as well as under private label brands for certain of our OEM and retail customers. The FRAG segment manufactures a variety of attachment cutting blade component parts sold to OEM customers for inclusion in original equipment, and as replacement parts. Additional product lines purchased from other manufacturers include tractor linkage, electrical, engine and hydraulic replacement parts, agricultural equipment replacement parts, and other accessories used in the agriculture and construction equipment markets.

Industry Overview. Competitors for our equipment and tractor attachment products include AGCO, Alamo Group, Champion, Doosan, Dover, Great Plains, John Deere, Koch Industries, Kubota, and MTD, among others. Competitors for our OEM and aftermarket parts include A&I, Herschel, Kondex, and SMA, among others. In recent years, suppliers in China and other low-cost manufacturing locations have increased productive capacity, particularly for tractor accessory parts, which has increased competition and pressure on pricing in North America.

We believe we are a leading supplier of log splitters, tractor attachments, including rotary cutters and finish mowers, 3-point linkage parts, implements, and tractor repair parts in North America. Our products are used by large commodity and livestock farmers, small farmers, rural property owners, commercial landscape and yard care maintenance operators, construction contractors, and municipalities.

4

To help us compete in our markets, we have reduced costs by utilizing global sourcing for key components and products. In addition, we believe we are an industry leader in product innovation and design in certain of our product categories. We also believe our long-standing relationships with key national retailers in North America have helped us maintain, or grow, our market share for certain of our product lines.

Weather can influence our FRAG sales cycle. For example, seasonal rainfall plays a role in demand for our agricultural and grounds maintenance products. Above-average rainfall drives greater demand for products in this category, while drought conditions tend to reduce demand for these products. Extreme cold weather can influence the agricultural planting and growing cycle, which in turn can affect demand for our agricultural products. Increases in home heating fuel costs and changes in temperature patterns can also drive the demand for firewood, which in turn drives the demand for our log splitters. Finally, demand for our FRAG products is affected by housing starts, crop prices, and disposable and farm income levels for our end customers.

Increases in raw material prices, particularly for steel, can negatively affect profit margins in our FRAG business, especially in the short-term. Fluctuations in foreign currency exchange rates and transportation costs can also affect our profitability as we source a significant amount of our components from Asia and ship them to the U.S. for assembly and distribution. Our industry is highly competitive, making pricing pressure a potential threat to sustaining profit margins. For additional information regarding the FRAG segment, see Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Note 19 to the Consolidated Financial Statements.

Concrete Cutting and Finishing Products

We operate a business in the specialized concrete cutting and finishing market. These products are sold primarily under the ICS® and Pentruder(R) brands, as well as under private label brands for certain OEM customers. The principal product lines are proprietary diamond-segmented cutting chains, which are used on gasoline, hydraulic, and electric powered concrete and utility pipe cutting saws and equipment. We also market and distribute branded gasoline and hydraulic powered concrete and utility pipe cutting chain saws as well as high-performance concrete cutting systems to our customers, which include contractors, rental equipment companies, construction equipment dealers, and utilities, primarily in the U.S. and Europe. We also market circular saw blades and other concrete cutting and finishing products to our customers. The power heads for the gasoline powered saws are manufactured for us by third parties. Competition primarily comes from other manufacturers of concrete cutting saws, including Husqvarna and Stihl. We also supply diamond-segmented chain to certain of these competitors. We believe we are a market leader in diamond chain cutting products.

Corporate Operations

We maintain a centralized administrative staff at our headquarters in Portland, Oregon. This centralized administrative staff provides the executive leadership for the Company, as well as accounting, finance, human resources, information technology, and supply chain services, administration of various health and welfare plans, risk management and insurance services, supervision of the Company’s capital structure, and oversight of the regulatory, compliance, and legal functions. Operating expenses of this central administrative function are included in selling, general, and administrative expenses (“SG&A”) in the Consolidated Statements of Income (Loss). The cost of providing certain shared services is allocated to our business segments using various allocation drivers such as employee headcount, software licenses, purchase volume, shipping volume, sales revenue, square footage, and other factors.

Merger Agreement

On December 9, 2015, we entered into a definitive agreement (the "Merger Agreement") to be acquired by affiliates of American Securities LLC (“American Securities”) and P2 Capital Partners, LLC (“P2 Capital Partners”) in an all-cash transaction valued at approximately $855 million, including the assumption of debt. Under the terms of the Merger Agreement, upon the consummation of the transaction, Blount stockholders will receive $10.00 in cash, without interest, for each share of Blount common stock they hold.

The independent members of Blount’s Board of Directors (the "Board") unanimously approved the proposed transaction based upon the unanimous recommendation of a Special Committee, which was comprised of independent directors and advised by its own financial and legal advisers.

The consummation of the transaction, which is structured as a one-step merger with Blount continuing as the surviving corporation (the “Merger”) and a wholly owned subsidiary of ASP Blade Intermediate Holdings, Inc., an affiliate of American Securities ("Parent"), is expected to occur during the second quarter of fiscal year 2016, and remains subject to receipt of

5

certain required regulatory approvals, the approval of the holders of a majority of the outstanding shares of Blount common stock, and the satisfaction or waiver of other customary closing conditions. The meeting at which Blount stockholders will vote on the adoption of the Merger Agreement is currently scheduled to take place on April 7, 2016. We cannot assure you that the proposed Merger will be completed, nor can we predict the exact timing of the completion of the proposed Merger, because it is subject to the satisfaction of various conditions, many of which are outside our control. If the proposed Merger is consummated, Blount common stock will cease to be traded on the New York Stock Exchange and we will no longer be a publicly-traded company.

The Merger Agreement provides that we are required to pay a termination fee to Parent if (i) the Merger Agreement is terminated so that we can enter into an agreement with respect to a “superior proposal” (as defined in the Merger Agreement), (ii) the Merger Agreement is terminated by Parent due to a change of recommendation with respect to the Merger Agreement by the Board or the Special Committee or (iii) each of the following three events occurs:

• | prior to the adoption of the Merger Agreement by our stockholders, the Merger Agreement is terminated by us or Parent because the Merger has not been consummated by the termination date (June 4, 2016) or because our stockholders have not adopted the Merger Agreement; |

• | any person has made (and has not subsequently withdrawn prior to the event giving rise to such termination) a proposal to acquire more than 75% of our common stock or assets after the date of the Merger Agreement but prior to such termination; and |

• | within 12 months after such termination, we enter into a definitive agreement with respect to such acquisition proposal, or a transaction contemplated by such acquisition proposal is otherwise consummated within 12 months of such termination. |

The termination fee payable (a) would have been in an amount equal to approximately $7.3 million if such fee had been payable in connection with the termination of the Merger Agreement due to (I) our entry into an agreement with respect to, or (II) a change of the Board’s or Special Committee’s recommendation as a result of, an acquisition proposal first received from an “excluded party” (as defined in the Merger Agreement) on or before March 9, 2016, and (b) is in an amount equal to

approximately $14.7 million if payable in accordance with the terms of the Merger Agreement other than under the circumstances described in (a) above. As described further in the definitive proxy statement relating to the Merger, which we filed with the SEC on March 9, 2016, there were no “excluded parties” under the Merger Agreement because we did not receive any acquisition proposals during the “go-shop” period provided for by the Merger Agreement. Accordingly, if a termination fee becomes payable by us in accordance with the terms of the Merger Agreement, it will be in an amount equal to approximately $14.7 million.

The Merger Agreement also provides that Parent will be required to pay us a reverse termination fee of $39.1 million (which obligation has been guaranteed by affiliates of each of American Securities and P2 Capital Partners) if the Merger Agreement is terminated by us because of Parent's uncured breach of the Merger Agreement or because Parent has not closed the Merger within two business days of the date the closing of the Merger should have occurred under the Merger Agreement despite our standing ready, willing and able to consummate the Merger during such two business day period.

We have entered into an agreement with P2 Capital Partners and certain of its affiliates, which collectively own approximately 14.99% of our outstanding shares, whereby P2 Capital Partners and such affiliates have agreed to vote their shares in accordance with the recommendation of the Board with respect to the proposed Merger. If we take action with respect to a “superior proposal” (as defined in the Merger Agreement), P2 Capital Partners and its affiliates have agreed to vote all of their shares in favor of an all-cash superior proposal and to vote their shares for or against other superior proposals in the same proportion as our stockholders (other than American Securities, P2 Capital Partners, members of our management or Board, or any of their respective affiliates).

Intellectual Property

Our proprietary brands include Alitec™, Carlton®, CF™, EuroMAX®, FORCE4®, Fusion®, Gannon™, Gator™, Gator Mulcher®, ICS®, INTENZ®, Jet-Fit®, Magnum Edger™, Oregon®, PBL™, PowerGrit®, PowerSharp®, Power-Match®, PowerNow™, PowerPro™, RentMAX™, SealPro®, SpeeCo®, SpeedHook®, Silverstreak®, Tiger®, Tisco®, Tru-Power®, Vintage Iron™, WainRoy®, Windsor®, Woods®, Woods Batwing™, Woods BrushBull™, Woods Mow'n Machine™, and WoodsCare™. All of these are registered, pending, or common trademarks of Blount and its subsidiaries in the U.S. and/or other countries.

The Company holds a number of patents, trademarks, and other intellectual property that are important to our business. From time to time we are involved in disputes, some of which lead to litigation, either in defense of our intellectual property or cases

6

where others have alleged that we have infringed on their intellectual property rights. See further discussion under Item 1A, Risk Factors, within the heading “Litigation – We may have litigation liabilities that could result in significant costs to us.”

Capacity Utilization

Based on a five-day, three-shift work week, average capacity utilization is estimated as follows:

Capacity Utilization | Year Ended December 31, | ||||||||

2015 | 2014 | 2013 | |||||||

Forestry, lawn, and garden | 79 | % | 86 | % | 74 | % | |||

Farm, ranch, and agriculture | 33 | % | 41 | % | 34 | % | |||

Concrete cutting and finishing | 71 | % | 75 | % | 69 | % | |||

The Company expects to meet future sales demand growth by utilizing excess capacity at existing facilities. Future expansion of capacity will be made through both productivity enhancements and capital investment at existing facilities as well as potential capital investment in additional FLAG locations. We have undertaken recent facility consolidation actions to streamline operations and reduce costs. During 2013 we closed a FLAG manufacturing facility near Portland, OR and consolidated the manufacturing operations into our other facilities. During 2014 we closed a small lawnmower blade manufacturing facility in Mexico and consolidated the manufacturing operations in our Kansas City, MO location. In the third quarter of 2015, the Company took certain actions to reduce its global headcount and lower operating costs in response to weak market conditions and lower 2015 sales.

The FRAG segment facilities are normally operated on a five-day, one-shift basis, which was the case during 2013, 2014, and 2015.

Sales Order Backlog

Our sales order backlog was as follows:

Sales Order Backlog | As of December 31, | |||||||||||

(Amounts in thousands) | 2015 | 2014 | 2013 | |||||||||

Forestry, lawn, and garden | $ | 114,493 | $ | 140,063 | $ | 150,850 | ||||||

Farm, ranch, and agriculture | 19,539 | 28,783 | 31,355 | |||||||||

Concrete cutting and finishing | 401 | 273 | 434 | |||||||||

Total sales order backlog | $ | 134,433 | $ | 169,119 | $ | 182,639 | ||||||

The total sales order backlog as of December 31, 2015 is expected to be completed and shipped within twelve months.

Employees

At December 31, 2015, we employed approximately 4,000 individuals. None of our U.S. employees belong to a labor union. The number of foreign employees who belong to labor unions is not significant. Certain of our foreign locations participate with worker councils which perform functions similar to a labor union. Certain other foreign locations participate with industry trade groups that negotiate certain policies and procedures for the general industry or with employer worker councils. We believe our relations with our employees are satisfactory, and we have not experienced any significant labor-related work stoppages in the last three years.

Environmental Matters

The Company’s operations are subject to comprehensive U.S. and foreign laws and regulations relating to the protection of the environment, including those governing discharges of pollutants into the air, ground, and water, the management and disposal of hazardous substances, and the cleanup of contaminated sites. Permits and environmental controls are required for certain of these operations, including those required to prevent or reduce air and water pollution, and our permits are subject to modification, renewal, and revocation by issuing authorities.

7

On an ongoing basis, we incur capital and operating costs to comply with environmental laws and regulations, as summarized in the following table.

Environmental Compliance Costs | Year Ended December 31, | |||||||||||

(Amounts in thousands) | 2015 | 2014 | 2013 | |||||||||

Expenses attributed to environmental compliance | $ | 2,200 | $ | 2,000 | $ | 1,500 | ||||||

Capital expenditures attributed to environmental compliance | 900 | 500 | 700 | |||||||||

Total attributed to environmental compliance | $ | 3,100 | $ | 2,500 | $ | 2,200 | ||||||

We expect to spend between $2.0 million and $3.0 million per year in capital and operating costs over the next three years for environmental compliance and anticipate continued spending at a similar level in subsequent years. The actual cost to comply with environmental laws and regulations may be greater than these estimated amounts.

In the manufacture of our products, we use certain chemicals and processes, including chrome and paints applied to some of our products, and oils used on metal-working machinery. Some of our current and former manufacturing facilities are located on properties with a long history of industrial use, including the use of hazardous substances. For certain of our former facilities, we retained responsibility for past environmental matters under certain conditions and pursuant to the terms of the agreements by which we sold the properties to third party purchasers. In addition, from time to time third parties have asserted claims against us for environmental remediation at former sites despite the absence of a contractual obligation. We have identified soil and groundwater contamination from these historical activities at certain of our current and former facilities, which we are currently investigating, monitoring, and in some cases, remediating. We have recognized the estimated costs of remediation in the Consolidated Financial Statements for all known contaminations that require remediation by us. As of December 31, 2015, the total recorded liability for environmental remediation was $2.0 million. Management believes that costs incurred to investigate, monitor, and remediate known contamination at these sites will not have a material adverse effect on our business, financial condition, results of operations or cash flows. We cannot be sure, however, that we have identified all existing contamination on our current and former properties, or that our estimated costs will be adequate to fully remediate the known contamination, or that our operations will not cause contamination in the future. As a result, we could incur material future costs to clean up environmental contamination.

From time to time we may be identified as a potentially responsible party under the U.S. Comprehensive Environmental Response, Compensation and Liability Act or similar state statutes with respect to sites at which we may have disposed of wastes. The U.S. Environmental Protection Agency (or an equivalent state agency) can either (a) allow potentially-responsible parties to conduct and pay for a remedial investigation and feasibility study and remedial action or (b) conduct the remedial investigation and action on its own and then seek reimbursement from the parties. Each party can be held liable for all of the costs, but the parties can then bring contribution actions against each other or potentially responsible third parties. As a result, we may be required to expend amounts on such remedial investigations and actions, which amounts cannot be determined at the present time, but which may ultimately prove to be material to the Consolidated Financial Statements.

In recent years, climate change has been discussed in various forums throughout the world. We do not believe that climate change has had a significant impact on our business operations or results to this point, but we cannot be sure of the potential effects to our business from any future changes in regulations or laws concerning climate change. Any new regulations limiting the amount of timber that could be harvested would most likely have a negative impact on our sales of forestry products. If climate change were to result in significant shifts in crops grown in agricultural regions, or prolonged significant changes in weather patterns, it could adversely affect our agricultural product business.

For additional information regarding certain environmental matters, see Note 15 to the Consolidated Financial Statements.

Financial Information about Industry Segments and Foreign and Domestic Operations

For financial information about industry segments and foreign and domestic operations, see Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and Note 19 to the Consolidated Financial Statements.

Seasonality

The Company’s operations are somewhat seasonal in nature. Year-over-year and quarter-over-quarter operating results are impacted by economic and business trends within the respective industries in which we compete, as well as by seasonal weather patterns and the occurrence of natural disasters and storms. Shipping and sales volume for some of the Company’s products vary based upon the time of year, but the overall impact of seasonality is generally not significant.

8

Research and Development Activities

See Note 1 to the Consolidated Financial Statements for information about our research and development activities.

Available Information

Our website address is www.blount.com. You may obtain electronic copies of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, all amendments to those reports, and other U.S. Securities and Exchange Commission (“SEC”) filings by accessing the Investor Relations section of the Company’s website under the heading “SEC Filings”. These reports are available on our Investor Relations website as soon as reasonably practicable after we electronically file them with the SEC.

Once filed with the SEC, such documents may be read and/or copied at the SEC’s Public Reference Room at 100 F Street NE, Washington, DC 20549. Information regarding the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an internet site at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers, including Blount, who file electronically with the SEC.

ITEM 1A. RISK FACTORS

Risks and Uncertainties Associated with the Proposed Merger—There are a number of risks and uncertainties associated with the proposed Merger.

On December 9, 2015, we entered into the Merger Agreement, which provides for the acquisition of Blount by affiliates of American Securities and P2 Capital Partners. The transaction is structured as a one-step merger with Blount as the surviving corporation. A number of risks and uncertainties are associated with the proposed Merger. For example, there can be no assurance that the conditions to the closing of the proposed Merger will be satisfied or, to the extent permitted, waived, including receipt of certain required regulatory approvals, the adoption of the Merger Agreement by Blount stockholders, the absence of any legal prohibitions, the accuracy of the representations and warranties of the parties under the Merger Agreement, compliance by the parties with their respective obligations under the Merger Agreement and the absence of a Company material adverse effect. Parent is also not required to consummate the proposed Merger until after the completion of a marketing period described in the Merger Agreement for the debt financing it is using to fund a portion of the merger consideration.

Other events may also occur, which could delay or result in the failure to consummate the proposed Merger, including litigation relating to the proposed Merger or the failure of Parent to obtain the necessary debt financing provided for by the commitment letters received in connection with the proposed Merger. If the proposed Merger is not consummated for any reason, Blount stockholders will not receive the consideration that Parent has agreed to pay upon the consummation of the proposed Merger, and the price of Blount common stock may decrease to the extent that its current market price reflects an assumption that the proposed Merger will be consummated. Such price decrease may be significant.

Additionally, we are currently subject to certain "no shop" provisions in the Merger Agreement that, subject to certain exceptions, limit our ability to discuss, facilitate or commit to third-party acquisition proposals to acquire all or a significant part of the Company. In addition, we will be required to pay a termination fee of approximately $14.7 million to Parent if (a) the Merger Agreement is terminated so that we can enter into an agreement with respect to a “superior proposal” (as defined in the Merger Agreement), (b) the Merger Agreement is terminated by Parent due to a change of recommendation with respect to the Merger Agreement by the Board or the Special Committee or (c) each of the following three events occurs:

• | prior to the adoption of the Merger Agreement by our stockholders, the Merger Agreement is terminated by us or Parent because the Merger has not been consummated by the termination date (June 4, 2016) or because our stockholders have not adopted the Merger Agreement; |

• | any person has made (and has not subsequently withdrawn prior to the event giving rise to such termination) a proposal to acquire more than 75% of our common stock or assets after the date of the Merger Agreement but prior to such termination; and |

• | within 12 months after such termination, we enter into a definitive agreement with respect to such acquisition proposal, or a transaction contemplated by such acquisition proposal is otherwise consummated within 12 months of such termination. |

9

These provisions might discourage a third party that has an interest in acquiring all or a significant part of the Company from considering or proposing an acquisition, even if the party were prepared to pay consideration with a higher per share cash or market value than the cash value to be received in the proposed Merger, or might result in a potential competing acquirer proposing to pay a lower price than it might otherwise have proposed to pay because of the added expense of the termination fee.

Furthermore, pending the closing of the proposed Merger, the Merger Agreement also restricts us from engaging in certain actions without Parent's consent, which could prevent us from pursuing opportunities that may arise prior to the closing of the proposed Merger and may be beneficial to our future performance.

If the proposed Merger is completed, we will no longer exist as a public company and Blount stockholders will forego any increase in our value that might have otherwise resulted from our possible future growth.

Business Impact of the Proposed Merger—Our business could be adversely impacted as a result of uncertainty related to the proposed Merger or by the failure to consummate the proposed Merger.

The proposed Merger could cause disruptions to our business or our business relationships, which could have an adverse impact on our results of operations. For example, our employees may experience uncertainty about their future roles with us, which may adversely affect our ability to hire and retain key personnel. Parties with which we have business relationships may experience uncertainty as to the future of such relationships and may delay or defer certain business decisions, seek alternative relationships with third parties or seek to alter their present business relationships with us. Parties with whom we otherwise may have sought to establish business relationships may seek alternative relationships with third parties. In addition, our management team and other employees are devoting significant time and effort to activities related to the proposed Merger.

We have incurred and will continue to incur significant costs, expenses and fees for professional services and other transaction costs in connection with the proposed Merger, and many of these fees and costs are payable regardless of whether or not the proposed Merger is consummated. In the event the proposed Merger is not consummated for any reason, or the timing of its consummation is delayed, our operating results may be adversely affected as a result of the incurrence of these significant additional expenses and the diversion of management attention.

In addition, if the proposed Merger is not completed, we may experience negative reactions from the financial markets and from our customers, suppliers, and employees. We also could be subject to litigation related to any failure to complete the proposed Merger or to enforcement proceedings commenced against us to attempt to force us to perform our obligations under the Merger Agreement.

Interests of Certain Executive Officers and Directors—Certain of our executive officers and directors have interests in the proposed Merger that may be different from, or in addition to, the interests of Blount stockholders generally.

Certain of our executive officers and directors have interests in the proposed Merger that may be different from, or in addition to, the interests of Blount stockholders generally. The interests of our directors and executive officers in the proposed Merger are described in detail in the definitive proxy statement regarding the proposed Merger, which we filed with the SEC on March 9, 2016.

Competition—Competition may result in decreased sales, operating income, and cash flows.

The markets in which we operate are competitive. We believe that design features, product quality, product performance, customer service, delivery lead times, and price are the principal factors considered by our customers. Some of our competitors may have, or may develop, greater financial resources, lower costs, superior technology, more favorable operating conditions, or may require lower returns on capital invested than we do. For example, our competitors have expanded capacity and contracted with suppliers located in China and other low-cost manufacturing locations as a means to lower costs. Although we have also established a manufacturing facility in China, international competition from emerging economies has nevertheless been formidable and has, in some cases, negatively affected our business through the introduction of lower competitive pricing in our markets. We may not be able to compete successfully with our existing or any new competitors, and the competitive pressures we face may result in decreased sales, operating income, and cash flows. Competitors could also obtain knowledge of our proprietary manufacturing techniques and processes and reduce our competitive advantage by copying such techniques and processes. Certain of our customers also compete with us with certain products in selected markets, and they may expand their production and marketing of competing products in the future.

10

Key Customers—Loss of one or more key customers would substantially decrease our sales.

In 2015, none of our customers individually accounted for 10% or more of our total sales and our top five customers accounted for 19.1%, of our total sales. While we expect these business relationships to continue, the loss of any of these key customers, or a substantial portion of their business, would most likely significantly decrease our sales, operating income, and cash flows. Certain customers may also decide to self-manufacture various components that we currently sell to them, which would have an adverse effect on our business. For example, one of our customers, the Husqvarna Group, has announced its plan to manufacture certain cutting chain, which we have historically supplied to them, and we expect this change will result in a reduction in our sales, operating income, and cash flows.

Key Suppliers and Raw Materials Costs—The loss of a few key suppliers or increases in raw materials costs could substantially decrease our sales or increase our costs.

We purchase raw materials, components, and parts from a limited number of suppliers that meet our quality criteria. We generally do not operate under long-term written supply contracts with our suppliers. Although alternative sources of supply are available, the sudden elimination or disruption of certain suppliers could result in manufacturing delays, an increase in costs, a reduction in product quality, and a possible loss of sales in the short-term. In 2015, we purchased $13.0 million in products from our largest supplier and $46.3 million in products and raw materials from our top five suppliers.

Some raw materials, in particular cold-rolled strip steel, are subject to price volatility over periods of time. In 2015 we purchased $79.2 million of steel. In addition to steel raw material, we also purchase components and sub-assemblies that are made with steel, and prices for these items are subject to steel price volatility risk. We have entered into purchase contracts with certain suppliers to stabilize near-term pricing on a portion of our steel purchases, but we have not entered into any derivative instruments to hedge against the price volatility of any raw materials. It has been our experience that raw material price increases are sometimes difficult to recover from our customers in the short-term through increased pricing. We estimate that a 10% change in the price of steel purchased as raw material, without a corresponding increase in selling prices, would have increased 2015 loss before income taxes by $7.9 million.

Foreign Sales and Operations—We have substantial foreign sales, operations, and property, which could be adversely affected as a result of changes in local economic or political conditions, fluctuations in foreign currency exchange rates, unexpected changes in regulatory environments, or potentially adverse tax consequences.

In 2015, approximately 51% of our sales were shipped to customers outside of the U.S. International sales and operations are subject to inherent risks, including changes in local economic or political conditions, instability of government institutions, the imposition of currency exchange restrictions, unexpected changes in legal and regulatory environments, nationalization of private property, and potentially adverse tax consequences. Under some circumstances, these factors could result in significant declines in international sales or loss of assets.

Some of our sales and expenses are denominated in local currencies that are affected by fluctuations in foreign currency exchange rates in relation to the U.S. Dollar. Historically, our principal local currency exposures have been related to manufacturing costs and expenses in Brazil, Canada, and China, and local currency sales and expenses in Europe, South America, Canada, and China. From time to time, we manage some of our exposure to currency exchange rate fluctuations through derivative products. However, such derivative products merely reduce the short-term volatility of currency fluctuations, and do not eliminate their effects over the long-term. We estimate the year-over-year movement of foreign currency exchange rates from 2014 to 2015, whereby the U.S. Dollar strengthened in relation to most foreign currencies, decreased our sales by $42.0 million and increased our operating income by $0.6 million from the translation of foreign currency denominated transactions into U.S. Dollars. Any change in the exchange rates of currencies in jurisdictions into which we sell products or incur significant expenses could result in a significant decrease in reported sales and operating income. For example, we estimate that a 10% stronger Canadian Dollar in relation to the U.S. Dollar would have increased our operating loss by $5.0 million in 2015. We estimate that a 10% weaker Euro in relation to the U.S. Dollar would have reduced our sales by $9.5 million and increased our operating loss by $1.2 million in 2015.

Also, approximately 55% of our foreign sales in 2015 were denominated in U.S. Dollars. We may see a decline in sales during periods of a strengthening U.S. Dollar, which can make our prices less competitive in international markets. We attribute much of the 2015 decline in sales unit volume to the impact on competitive pricing from the stronger U.S. Dollar. Furthermore, if the U.S. Dollar strengthens against foreign currencies, it becomes more costly for foreign customers to pay their U.S. Dollar receivable balances owed to us. They may have difficulty in repaying these amounts, and in turn, our bad debt expense may increase.

11

In addition, we own substantial manufacturing facilities outside the U.S. As of December 31, 2015, 48%, or 857,555 of the total square feet of our owned facilities are located outside of the U.S., and 26% of our leased square footage is located outside the U.S. This foreign-based property, plant, and equipment ("PP&E") is subject to inherent risks for the reasons cited above. Loss of these facilities or restrictions on our ability to use them would have an adverse effect on our manufacturing and distribution capabilities and would result in reduced sales, operating income, and cash flows.

Sanctions by the U.S. government against certain companies and individuals in Russia and Ukraine may hinder our ability to conduct business with potential or existing customers and vendors in these countries.

We currently derive a portion (approximately 1.8% in 2015) of our revenue from Russia and Ukraine, and have a sales and distribution office in Russia. Recently, the U.S. government imposed sanctions through several executive orders restricting U.S. companies from conducting business with specified Russian and Ukrainian individuals and companies. While we believe that the executive orders currently do not preclude us from conducting business with our current customers in Russia and Ukraine, the sanctions imposed by the U.S. government may be expanded in the future and restrict our activities with them. If we are unable to conduct business with new or existing customers or pursue opportunities in Russia or Ukraine, our sales, operating income, and cash flows, could be adversely affected.

Weather—Sales of many of our products are affected by weather patterns and the occurrence of natural disasters.

Sales of many of our products are influenced by weather patterns that are clearly outside our control. For example, drought conditions tend to reduce the demand for agricultural and yard care products, such as tractor attachments and lawnmower blades, and conversely, plentiful rain conditions stimulate demand for these products. Extreme cold weather can affect the agricultural cycle and adversely affect our business. For example, during 2015, harsh winter conditions in North America delayed the spring planting season and adversely affected our FRAG agricultural attachment sales. Conversely, cold winter weather can stimulate demand for our forestry and log splitter products. Natural disasters such as hurricanes, typhoons, and ice and wind storms that knock down trees can stimulate demand for our forestry and log splitter products. Conversely, a relative lack of severe weather and natural disasters can result in reduced demand for these same products.

Financial Leverage and Debt—Due to our financial leverage, we could have difficulty operating our business and satisfying our debt obligations.

As of December 31, 2015, we have $582.7 million of total liabilities, including $379.0 million of debt. Our debt leverage is significant, and may have important consequences for us, including the following:

• | A significant portion of our cash flow from operations is dedicated to the payment of interest expense and required principal repayments, which reduces the funds that would otherwise be available to fund operations and future business opportunities. Cash interest and mandatory debt principal payments totaled $29.2 million during 2015. |

• | A substantial decrease in net operating income and cash flows or a substantial increase in expenses may make it difficult for us to meet our debt service requirements or force us to modify our operations. |

• | Our financial leverage may make us more vulnerable to economic downturns and competitive pressures. |

• | Our ability to obtain additional or replacement financing for working capital, capital expenditures, or other purposes, may be impaired, or such financing may not be available on terms favorable to us under current market conditions for credit. Our current senior credit facilities mature on May 5, 2020. |

We have available borrowing capacity under the revolving portion of our senior credit facilities of $43.9 million as of December 31, 2015. If we or any of our subsidiaries incur additional indebtedness, the risks outlined above could worsen. Our ability to make payments on our indebtedness and to fund planned capital expenditures and research and product development efforts will depend on our ability to generate cash in the future. Our ability to generate cash, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory, and other factors that are beyond our control.

Our historical financial results have been, and we anticipate that our future financial results will continue to be, subject to fluctuations in customer orders, sales, operating results, and cash flows. Our business may not be able to generate sufficient cash flow from our operations or future borrowings may not be available to us in an amount sufficient to enable us to service our indebtedness or to fund our other liquidity needs. An inability to pay our debts would require us to pursue one or more alternative capital raising strategies, such as selling assets, refinancing or restructuring our indebtedness, or selling equity capital. However, alternative strategies may not be feasible at the time or may not prove adequate, which could cause us to default on our obligations and would impair our liquidity. Also, some alternative strategies would require the prior consent of our secured lenders, which we may not be able to obtain. See also Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

12

Restrictive Covenants—The terms of our indebtedness contain a number of restrictive covenants, the breach of any of which could result in acceleration of payment of our senior credit facilities.

A breach of any of our restrictive debt covenants could result in acceleration of our obligations to repay our debt. An acceleration of our repayment obligations under our senior credit facilities could result in a payment or distribution of substantially all of our assets to our secured lenders, which would materially impair our ability to operate our business as a going concern. In addition, our senior credit facility agreement, among other things, restricts and/or limits our and certain of our subsidiaries’ ability to:

• | incur debt; |

• | guarantee indebtedness of others; |

• | pay dividends on our stock; |

• | repurchase our stock; |

• | pursue business acquisitions; |

• | make certain types of investments; |

• | use assets as security in other transactions; |

• | sell certain assets or merge with or into other companies; |

• | enter into sale and leaseback transactions; |

• | enter into certain types of transactions with affiliates; |

• | enter into certain new businesses; and |

• | make certain payments in respect of subordinated indebtedness. |

In addition, the senior credit facilities require us to maintain certain financial ratios and satisfy certain financial condition tests, which may require that we take actions to reduce debt or to act in a manner contrary to our business objectives. Our ability to meet those financial ratios and tests could be affected by events beyond our control, and there can be no assurance that we will continue to meet those ratios and tests. A breach of any of these covenants could, if uncured, constitute an event of default under the senior credit facilities. Upon the occurrence of an event of default under the senior credit facilities, the lenders could elect to declare all amounts outstanding under the senior credit facilities, together with any accrued interest and commitment fees, to be immediately due and payable. If we and certain of our subsidiaries were unable to repay those amounts, the lenders under the senior credit facilities could enforce the guarantees from the guarantors and proceed against the collateral securing the senior credit facilities. The assets of Blount, Inc., our wholly-owned subsidiary and issuer of the debt under our senior credit facilities, and the applicable guarantors could be insufficient to repay in full that indebtedness and our other indebtedness. See also Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Assets Pledged as Security on Credit Facilities—The majority of our assets and the capital stock of our wholly-owned subsidiary Blount, Inc. are pledged to secure obligations under our senior credit facilities.

The Company and all of its domestic subsidiaries other than Blount, Inc. guarantee Blount, Inc.’s obligations under the senior credit facilities. The obligations under the senior credit facilities are collateralized by a first priority security interest in substantially all of the assets of Blount, Inc. and its domestic subsidiaries, as well as a pledge of all of Blount, Inc.’s capital stock held by Blount International, Inc. and all of the stock of domestic subsidiaries held by Blount, Inc. Blount, Inc. has also pledged 65% of the stock of its direct non-domestic subsidiaries as additional collateral. An event of default under our senior credit facilities could trigger our lenders’ contractual rights to enforce their security interests in these assets.

Litigation—We may have litigation liabilities that could result in significant costs to us and, in the case of stockholder litigation relating to the proposed Merger, could delay or prevent the proposed Merger.

Our historical and current business operations have experienced a number of litigation matters, including litigation involving personal injury or death, as a result of alleged design or manufacturing defects of our products, and litigation involving alleged patent infringement. Certain of these liabilities relate to our discontinued operations and were retained by us under terms of the relevant divestiture agreements. Some of the product liability claims made against us seek significant or unspecified damages for serious personal injuries for which there are retentions or deductible amounts under our insurance policies. In the future, we may face additional lawsuits, and it is difficult to predict the amount and type of litigation that we may face. Litigation, insurance, and other related costs could result in future liabilities that are significant and that could significantly reduce our operating income, cash flows, and cash balances.

13

Additionally, we and the members of our Board (including Joshua L. Collins, the chairman of our Board and our chief executive officer, and David A Willmott, our president and chief operating officer, both in their capacities as officers and members of our Board) have been named as defendants in litigation relating to the Merger Agreement and the proposed Merger. American Securities, P2 Capital Partners and certain of their respective affiliates, and Goldman, Sachs & Co., financial advisor to our Board in connection with the proposed Merger (“Goldman Sachs”), have also been named as defendants. The litigation plaintiff has alleged that (1) the individual defendants breached their fiduciary duties of care and loyalty in connection with their negotiation and approval of the Merger Agreement, (2) the individual defendants breached their fiduciary duty of disclosure by filing a preliminary proxy statement that fails to disclose and/or misrepresents material information and (3) P2 Capital Partners, one of P2 Capital Partners’ affiliates and Goldman Sachs aided and abetted such alleged breaches of fiduciary duties. The plaintiff has asked the court to, among other things, (i) preliminarily and permanently enjoin the defendants from proceeding with the proposed Merger on the current terms, and (ii) in the event that the proposed Merger is consummated, rescind the proposed Merger or grant rescissory damages. Further lawsuits may be filed in connection with the proposed Merger. The closing of the proposed Merger is subject to the satisfaction or waiver of the condition that no order, judgment, injunction, award, decree or writ of any governmental entity of competent jurisdiction has been issued and continues in effect that prohibits, restrains, enjoins or renders illegal the consummation of the proposed Merger. If any lawsuits are successful in obtaining an injunction prohibiting the parties from completing the proposed Merger on the agreed-upon terms, such injunction may prevent the completion of the proposed Merger in the expected time frame or altogether.

See also Item 3, Legal Proceedings, and Note 15 to the Consolidated Financial Statements.

Environmental Matters—We face potential exposure to environmental liabilities and costs.

We are subject to various U.S. and foreign environmental laws and regulations relating to the protection of the environment, including those governing discharges of pollutants into the air and water, the management and disposal of hazardous substances, and the cleanup of contaminated sites. Violations of, or liabilities incurred under, these laws and regulations could result in an assessment of significant costs to us, including civil or criminal penalties, claims by third parties for personal injury or property damage, requirements to investigate and remediate contamination, and the imposition of natural resource damages. Furthermore, under certain environmental laws, current and former owners and operators of contaminated property or parties who sent waste to a contaminated site can be held liable for cleanup, regardless of fault or the lawfulness of the disposal activity at the time it was performed. This potential exposure to environmental liabilities and costs can apply to both our current and former operating facilities, including those related to our discontinued operations.

Future events, such as the discovery of additional contamination or other information concerning releases of hazardous substances at our or other sites affected by our actions, changes in existing environmental laws or their interpretation, including changes related to climate change, and more rigorous enforcement by regulatory authorities may require additional expenditures by us to modify operations, install pollution control equipment, investigate and monitor contamination at sites, clean contaminated sites, or curtail our operations. These expenditures could significantly reduce our net income and cash flows. See also Item 1, Business-Environmental Matters, Item 3, Legal Proceedings, and Note 15 to the Consolidated Financial Statements.

General Economic Factors—We are subject to general economic factors that are largely out of our control, any of which could, among other things, result in a decrease in sales, net income, and cash flows, and an increase in our interest or other expenses.

Our business is subject to a number of general economic factors, many of which are largely out of our control, which may, among other effects, result in a decrease in sales, net income, and cash flows, and an increase in our interest or other expenses. These factors include recessionary economic cycles and downturns in customers’ business cycles, as well as downturns in the principal regional economies where our operations are located. Economic conditions may adversely affect our customers’ business levels and the amount of products that they need. Furthermore, customers encountering adverse economic conditions may have difficulty in paying for our products and actual bad debts may exceed our allowance for bad debts. World-wide economic conditions may also adversely affect our suppliers and they may not be able to provide us with the goods and services we need on a timely basis, which could adversely affect our ability to manufacture and sell our products. Our senior credit facility borrowings are at variable interest rates. Increases in market reference interest rates could increase our interest expense payable under the senior credit facilities to levels in excess of what we currently expect. We estimate that an increase in our average interest rates in 2015 of 100 basis points would have increased our interest expense by $4.6 million. In addition, fluctuations in the market values of equity and debt securities held in the Company’s pension plan assets can adversely affect the funded status of our defined benefit pension plans. The expense and funding requirements for these plans may increase in the future as a result of reduced values of the plan assets. Changes in reference interest rates can also have a significant effect on the measurement of post-employment benefit plan obligations and the related expense recognized. Furthermore, terrorist

14

activities, anti-terrorist efforts, war, or other armed conflicts involving the U.S. or its interests abroad may result in a downturn in the U.S. and global economies and exacerbate the risks to our business described in this paragraph.

Key Employees—The loss of key employees could adversely affect our manufacturing efficiency.

Many of our manufacturing processes require a high level of expertise. For example, we build our own complex dies for use in cutting and shaping steel into components for our products. The design and manufacture of such dies are highly dependent on the expertise of key employees. We have also developed numerous proprietary manufacturing techniques that rely on the expertise of key employees. Our manufacturing efficiency and cost could be adversely affected if we are unable to retain these key employees or continue to train them or their replacements. Uncertainties associated with the proposed Merger may cause a loss of management or other key employees.

Common Stock Price—The price of our common stock may fluctuate significantly, and stockholders could lose all or part of their investment.

Volatility in the market price of our common stock may prevent stockholders from being able to sell their shares at or above the price paid for the shares. The market price of our common stock could fluctuate significantly for various reasons that include:

• | failure to complete the proposed Merger, or a significant delay in completing the proposed Merger; |

• | our quarterly or annual earnings or those of other companies in our industries; |

• | the public’s reaction to events and results contained in our press releases, our other public announcements, and our filings with the SEC; |

• | changes in earnings estimates or recommendations by research analysts who track our common stock or the stock of other comparable companies; |

• | changes in general conditions in the U.S. and global economies, financial markets, or the industries we market our products to, including those resulting from war, incidents of terrorism, changes in technology or competition, or responses to such events; |

• | sales of common stock by our largest stockholders, directors, or executive officers; and |

• | the other factors described in these “Risk Factors.” |

In addition, the stock market and our common stock have historically experienced price and volume fluctuations. This volatility has had a significant impact on the market price of securities issued by many companies, including companies in our industries. The changes in prices frequently appear to occur without regard to the operating performance of these companies. For example, over the preceding two-year period, our highest closing stock price has exceeded our lowest closing stock price by 250.0%. The price of our common stock could fluctuate based upon factors that have little or nothing to do with our Company, and these fluctuations could materially reduce our stock price.

Common Stock Sales—Future sales of our common stock in the public market could lower our stock price.

Ownership and control of our common stock is concentrated in a relatively small number of institutional investors. As of December 31, 2015, approximately 48% of our outstanding common stock was owned or controlled by our five largest stockholders. If the proposed Merger does not close as anticipated, we may sell additional shares of common stock in subsequent public offerings. Additionally, other stockholders with significant holdings of our common stock may sell large amounts of shares they own in a secondary or open market stock offering. We may also issue additional shares of common stock to finance future transactions. We cannot predict the size of future issuances of our common stock or the effect, if any, that future issuances and sales of shares of our common stock will have on the market price of our common stock. Sales of substantial amounts of our common stock (including shares issued in connection with an acquisition or shares sold by existing stockholders), or the perception that such sales could occur, may adversely affect the prevailing market price of our common stock.

Disruptions in Shipping—A prolonged disruption in transportation logistics could affect our ability to import critical components and to ship our products to customers.

We rely on third party vendors for a substantial portion of our shipping needs, including both obtaining raw materials and products from suppliers and delivering our products to customers, and a significant amount of our shipping is via ocean transport. A significant disruption in transportation logistics could disrupt our ability to obtain raw materials and products from suppliers, and in turn disrupt our ability to manufacture our products and sell them to our customers. Significant disruption of shipping could adversely affect our operating results and cash flows, and could increase our transportation costs.

15

Computer Transaction Processing—An information technology system failure or breach of security may adversely affect our business.

We rely on information technology systems to manage our operations and transact our business. An information technology system failure due to computer viruses, internal or external security breaches, power interruptions, hardware failures, fire, natural disasters, human error, or other causes could disrupt our operations and prevent us from being able to process transactions with our customers, operate our manufacturing facilities, and properly report those transactions in a timely manner. A significant, protracted information technology system failure may result in a material adverse effect on our financial condition, results of operations, or cash flows.

In recent years we have increased the volume of sales transactions processed over the Internet. As a result, sensitive information about our customers is stored in electronic media. If unauthorized access to this information were gained, we could be subject to penalties or claims by our customers, which could have an adverse effect on our business.

Material Weaknesses—Management’s determination that material weaknesses exists in our internal controls over financial reporting could have a material adverse impact on our ability to produce timely and accurate financial statements.

The Sarbanes-Oxley Act requires that we report annually on the effectiveness of our internal controls over financial reporting. We must conduct an assessment of our internal controls to allow management to report on, and our independent registered public accounting firm to attest to, our internal controls over financial reporting, as required by Section 404 of the Sarbanes-Oxley Act. Our management concluded that material weaknesses in our internal control over financial reporting existed and that internal control over financial reporting was not effective as of December 31, 2014. As a result of these material weaknesses, management also determined that our disclosure controls and procedures were not fully effective as of December 31, 2014.

In connection with our compliance efforts during the three years ended December 31, 2015, we have incurred substantial accounting, information technology, internal audit, external audit, and other expenses, as well as significant management time and resources, to remediate these material weaknesses. As of December 31, 2015, our material weaknesses in internal control over financial reporting have been remediated. Our future assessment, or the future assessment by our independent registered public accounting firm, may reveal new material weaknesses in our internal controls. Whether new material weaknesses in internal control over financial reporting are discovered or not, we expect to continue to incur significant expenses in our compliance efforts.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

Our corporate headquarters occupy executive offices at 4909 SE International Way, Portland, Oregon 97222. Cutting chain, guide bar, and drive sprocket manufacturing facilities within our FLAG business segment are located in Portland, Oregon; Curitiba, Brazil; Guelph, Canada; and Fuzhou, China. Lawnmower and other cutting blade manufacturing facilities within our FLAG business segment are located in Kansas City, Missouri and Civray, France. A small lawnmower blade manufacturing facility in Queretaro, Mexico was closed in January 2014. Assembly of log splitters and post-hole diggers within our FRAG business segment occurs in leased facilities in Kansas City, Missouri. Tractor attachment, construction attachment, riding lawnmowers, and other product manufacturing plants within our FRAG business segment are located in Oregon, Illinois; Kronenwetter, Wisconsin; Sioux Falls, South Dakota; and Civray, France. Sales offices and distribution centers are located in Coppell, Texas; Curitiba, Brazil; several locations in Europe; Fuzhou, China; Guelph, Canada; Nishi-ku, Yokohama, Japan; Kansas City, Missouri; Moscow, Russia; Nashville, Tennessee; Oregon, Illinois; Portland, Oregon; Rockford, Illinois; Sparks, Nevada; and Strongsville, Ohio. The FRAG segment also leases office space in Golden, Colorado with design, engineering, sales, and marketing functions.

16

In the opinion of management, all of these facilities are in relatively good condition, are currently in normal operation, and are generally suitable and adequate for the business activity conducted therein. The approximate square footage of facilities located at our principal properties as of December 31, 2015 is as follows:

Properties as of December 31, 2015 | Area in Square Feet | |||||

Owned | Leased | |||||

Forestry, Lawn, and Garden segment | 1,217,000 | 511,600 | ||||

Farm, Ranch, and Agriculture segment | 533,200 | 630,500 | ||||

Corporate and Other | 50,800 | 41,400 | ||||

Total | 1,801,000 | 1,183,500 | ||||

ITEM 3. LEGAL PROCEEDINGS

For information regarding legal proceedings, see Note 15 to the Consolidated Financial Statements.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

17

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

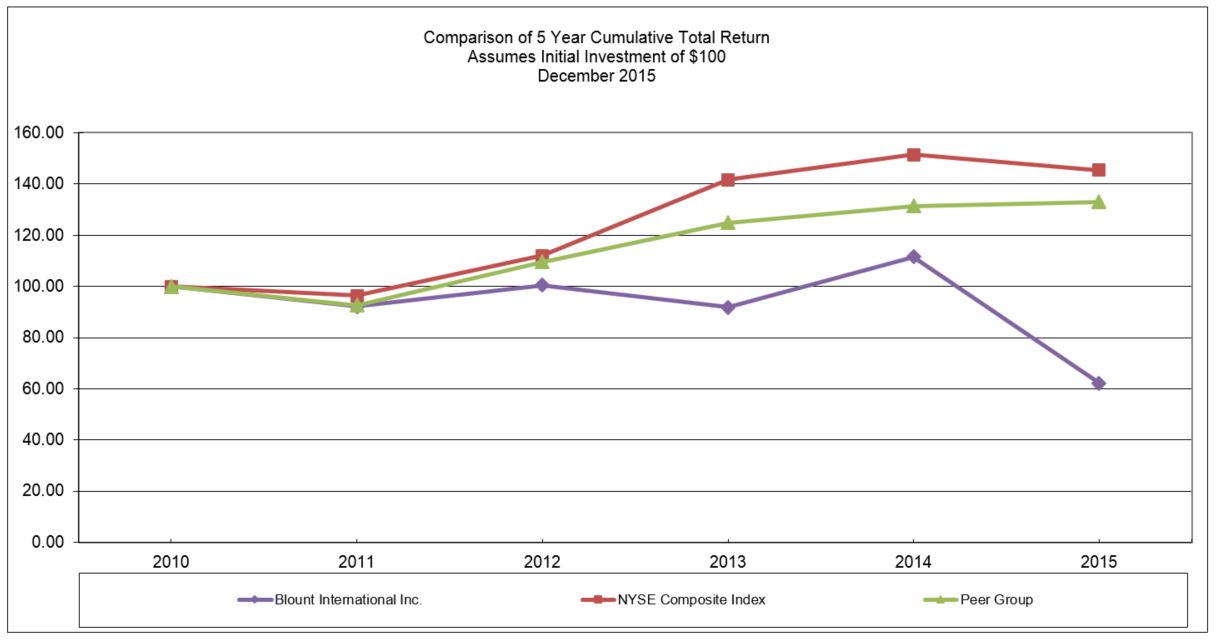

The Company’s common stock is traded on the New York Stock Exchange (ticker “BLT”). Cash dividends have not been declared for the Company’s common stock since 1999. The Company’s senior credit facility agreement limits the amount available to pay dividends or repurchase Company stock. See Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, for further discussion. The Company had approximately 5,200 stockholders of record as of December 31, 2015. See information about the Company’s stock compensation plans in Note 18 to the Consolidated Financial Statements and also in Item 12, Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. See also information about the proposed Merger affecting the price of our common stock in Item 1, Business, and Item 1A, Risk Factors.

The Company has not sold any registered or unregistered securities during the three year period ended December 31, 2015.

On August 6, 2014, the Board authorized a share repurchase program of the Company's common stock up to an aggregate maximum of $75.0 million through December 31, 2016. Through December 31, 2015 the Company had repurchased 1,684,688 shares at a total cost of $24.4 million, leaving a remaining authorization of $50.6 million for future purchases. This share repurchase program does not obligate Blount to acquire any particular amount of common stock, and it may be suspended at any time at the Company's discretion. As part of the Merger Agreement, the Company has agreed to not repurchase additional shares without Parent's consent.