Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - Manning & Napier, Inc. | exhibit311_q42015form10-k.htm |

| EX-32.1 - EXHIBIT 32.1 - Manning & Napier, Inc. | exhibit321_q42015form10-k.htm |

| EX-23.1 - EXHIBIT 23.1 - Manning & Napier, Inc. | exhibit231_q42015form10-k.htm |

| EX-21.1 - EXHIBIT 21.1 - Manning & Napier, Inc. | exhibit211_q42015form10-k.htm |

| EX-32.2 - EXHIBIT 32.2 - Manning & Napier, Inc. | exhibit322_q42015form10-k.htm |

| EX-31.2 - EXHIBIT 31.2 - Manning & Napier, Inc. | exhibit312_q42015form10-k.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

___________________________________

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-35355

___________________________________

MANNING & NAPIER, INC.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 45-2609100 (I.R.S. Employer Identification No.) | |

290 Woodcliff Drive Fairport, New York | 14450 | |

(Address of principal executive offices) | (Zip code) | |

(585) 325-6880

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange in which registered | |

Class A common stock, $0.01 par value per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act:

None

___________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | x | |

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the registrant's common equity held by non-affiliates of the registrant (assuming for purposes of this computation only that the directors and executive officers may be affiliates) at June 30, 2015, which was the last business day of the registrant’s most recently completed second fiscal quarter was approximately $145.2 million based on the closing price of $9.97 for one share of common stock, as reported on the New York Stock Exchange on that date.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

Class | Outstanding at March 10, 2016 | |

Class A common stock, $0.01 par value per share | 14,735,130 | |

Class B common stock, $0.01 par value per share | 1,000 | |

___________________________________

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement for its 2016 Annual Meeting of Stockholders to be held June 16, 2016 are incorporated by reference into Part III of this Form 10-K.

TABLE OF CONTENTS

Page | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

In this Annual Report on Form 10-K, “we”, “our”, “us”, the “Company”, “Manning & Napier” and the “Registrant” refers to Manning & Napier, Inc. and, unless the context otherwise requires, its direct and indirect subsidiaries and predecessors on a consolidated basis.

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, which reflect our views with respect to, among other things, our operations and financial performance. Words like “believes,” “expects,” “may,” “estimates,” “will,” “should,” “could,” “intends,” “plans,” or “anticipates” or the negative thereof or other variations thereon or comparable terminology, are used to identify forward-looking statements, although not all forward-looking statements contain these words. Although we believe that we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know about our business and operations, there can be no assurance that our actual results will not differ materially from what we expect or believe. Some of the factors that could cause our actual results to differ materially from our expectations or beliefs are disclosed in the “Risk Factors” as well as other sections of this report which include, without limitation: changes in securities or financial markets or general economic conditions; a decline in the performance of the Company’s products; client sales and redemption activity; any loss of an executive officer or key personnel; changes in our business related to strategic acquisitions and other transactions; and changes of government policy or regulations. All forward-looking statements speak only as of the date on which they are made and we undertake no duty to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

ii

PART I

Item 1. Business.

Overview

Manning & Napier, Inc. is an independent investment management firm that provides a broad range of investment solutions through separately managed accounts, mutual funds, and collective investment trust funds, as well as a variety of consultative services that complement its investment process. Founded in 1970, we offer equity, fixed income and alternative strategies, as well as a range of blended asset portfolios, such as life cycle funds. Headquartered in Fairport, New York, we serve a diversified client base of high net worth individuals and institutions, including 401(k) plans, pension plans, Taft-Hartley plans ("Taft-Hartley"), endowments and foundations.

Since our inception, we have taken the view that an active, team-based approach to portfolio management is the best way to manage risk for clients as market conditions change. Across our variety of equity, fixed income and blended asset portfolios, our goal is to provide competitive absolute returns over full market cycles. We employ disciplined processes that seek to avoid areas of speculation by focusing on investments with strong fundamentals at reasonable prices or stable fundamentals at attractive prices. To ensure a focus on absolute returns, we employ a compensation structure for our research team that rewards positive and above benchmark results and penalizes negative and below benchmark results. This active, absolute-returns based approach requires flexibility to invest where opportunities are and avoid speculation, regardless of the allocations within a comparative benchmark.

Initially, this approach helped us build a client base of high net worth individuals, small business owners and middle market institutions, and we maintain these relationships in many targeted geographic regions. This foundation allowed us to expand our business to serve the needs of larger institutions, investment consultants and other intermediaries.

A key aspect of our client service approach is a commitment to internal subject matter experts that can provide consultative services beyond investment management, which we believe helps us attract new clients and build close relationships through multiple service touch points and a solutions-oriented approach. We have designed solutions that are specific to our clients’ needs, such as our family wealth management service and trust services. This service oriented approach combined with competitive long-term investment performance across portfolios, has allowed us to achieve a high average annual separate account retention rate. For the ten-year period ending December 31, 2015, our average annual separate account retention rate was 95%.

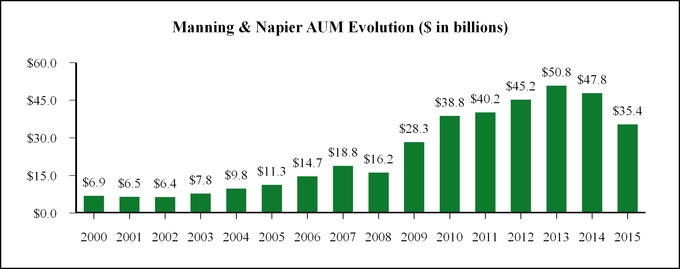

Our commitment to team-based research, an absolute return focus and a flexible process that is benchmark-agnostic have been central to our success, and we believe are distinctive within the industry. Over the course of our 45+ year history our mutual funds have earned several industry accolades, including a finalist ranking for Morningstar’s international manager of the decade during the 2000s and multiple Lipper awards. Several of our investment strategies have value-added track records over multiple decades, which has led to strong growth in our total discretionary assets under management ("AUM") over the long-term. However, our active approach causes us to be out of favor relative to benchmarks and/or peers over shorter time periods. As of December 31, 2015, 28% of our total mutual fund AUM rated by Morningstar were in funds rated at least four stars, and 97% were in funds that were rated at least three stars. These short-term periods can lead to changes in AUM trends over time. The following chart reflects our AUM as of December 31 for each year since 2000.

1

We offer our investment management capabilities primarily through direct sales to high net worth individuals and institutions, as well as through third-party intermediaries, platforms and institutional investment consultants. As of December 31, 2015, our investment management offerings include 40 distinct separate account composites and 65 mutual funds and collective investment trusts.

Our separate accounts are primarily distributed through our Direct Channel, where our representatives form relationships with high net worth individuals, middle market institutions or large institutions that are working with a consultant. To a lesser extent, we also obtain a portion of our separate account distribution via third parties, either through our Intermediary Channel where national brokerage firm representatives or independent financial advisors select our separate account strategies for their clients, or through our Platform/Sub-Advisory Channel, where unaffiliated registered investment advisors approve our strategies for their product platforms. Our separate account products are a primary driver of our blended asset portfolios for high net worth and middle market institutional clients and financial intermediaries. In contrast, larger institutions and unaffiliated registered investment advisor platforms are a driver of our separate account equity portfolios.

Our mutual funds and collective investment trusts are primarily distributed through financial intermediaries, including brokers, financial advisors, retirement plan advisors and platform relationships. We also obtain a portion of our mutual fund and collective investment trust distribution through our direct sales representatives, in particular within the defined contribution and institutional marketplace. Our mutual fund and collective investment trust products are an important driver of our blended asset class portfolios, in particular with 401(k) plan sponsors, advisors and recordkeepers that select our funds as default options for participants. In addition, financial intermediaries, mutual fund advisory programs and retail platforms are a driver of equity strategies within our mutual fund offerings.

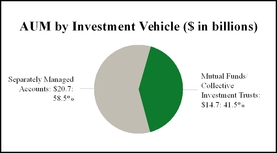

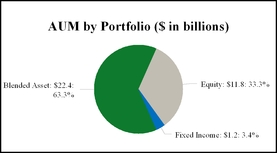

Our AUM as of December 31, 2015 by investment vehicle and portfolio were as follows:

Recent Developments

In December of 2015, we announced the agreement to acquire a majority interest in Rainier Investment Management, LLC ("Rainier"), an active investment management firm with more than $3 billion in AUM. Under the terms of the transaction, key professionals will maintain a 25% ownership stake in Rainier, with Manning & Napier owning the remaining 75%. The transaction is expected to close in the first half of 2016, subject to customary regulatory approvals and closing conditions.

Our Strategy

Our approach for continued success is focused on the strategies described below.

Maintain a Strong, Team-Based Research Engine

With a research department of over 70 investment professionals, we are committed to a team-based approach to portfolio management to ensure that success can be repeated over time. All of our investment products are managed by a team, so that stability of process takes precedence over any individual personality. Our Senior Research Group, which consists of long-tenured members of the research department, maintains oversight responsibility for our investment disciplines and policies. We take a home-grown approach to maintaining this strong research engine. Analysts begin their employment with us as Research Assistants or Associates, and progress to the Analyst level only after learning our process and disciplines in a role that supports the portfolio management teams. We believe this ensures consistency with our time-tested philosophies and also provides a source of future analysts to address growth and turnover.

2

Over time and as product development warrants, we may add to our research team or supplement that team with additional investment professionals through corporate development activities. In 2014, we acquired an alternative investment manager and integrated the research professionals into our existing team to enhance our alternatives capabilities. In December of 2015, we announced our intention to acquire a majority interest in Rainier in part to expand the product set available to our clients. The investment teams of both Manning & Napier and Rainier will remain autonomous, and the transaction will not result in changes to either firm's investment personnel or processes.

Broad, Multi Channel Distribution Team

We continue to focus on the depth of our multi-channel distribution structure, which includes both direct and intermediary channels. Within our direct and intermediary channels, we recognize the growing influence and specialization of retirement plan advisors. To address this opportunity, we have established a specific Defined Contribution Investment Only wholesaling team to focus their sales efforts on retirement specialist advisors, who work with small-to-mid market defined contribution plans. In these channels, we believe we have a competitive advantage that allows us to offer our multi-asset class strategies, including our life cycle and retirement target mutual fund and collective trust products. Non-retirement plan advisors have and will continue to be focused on wealth management investment solutions.

Within our direct channel, our high-touch distribution strategy has allowed us to build strong relationships over time. We continuously look to opportunistically enhance our direct distribution sales force domestically. Beyond deepening these current channels and territories, we continue to look at ways to expand our global distribution, including leveraging our current relationships in Europe and expanding into new markets.

Innovative Product Development

We are committed to on-going development of products and consultative services in response to current and prospective client needs. Today's market environment presents new challenges for investors. Historically low yields on fixed income securities, the potential for rising interest rates and future inflation, and continued global uncertainty have created an investing landscape that requires new solutions to meeting objectives. We understand that we must stay relevant and competitive by ensuring that we are consistently providing innovative solutions that address today's challenges.

We have approximately $30 million invested in seed capital to our investment teams as of December 31, 2015 across more than fifteen products, including equity, fixed income and alternative strategies. Over the last two years, we have seen five of those seeded products reach a three year track record, including our Emerging Markets and Global Quality equity strategies as well as our Global Fixed Income, Strategic Income Conservative and Strategic Income Moderate strategies. In addition, our intent to acquire a majority interest in Rainier during 2016 will add several equity products to our product set, including small-to-mid cap, mid cap and large cap U.S. equity offerings as well as an international small cap equity strategy.

Enhanced Consultative Services

Offering consultative services alongside our team-based, process-driven investment management has been a source of both new business and client retention over our history. Currently, we offer a variety of consultative services to individual and institutional clients, including estate and tax planning, asset/liability modeling for defined benefit pension plans, retirement and health plan design analysis for employers, and donor relations and planned giving services for endowment and foundation clients.

Many of these services are offered through our Client Analytics Group, which consists of internal consultants whose primary responsibilities include working with prospective and current clients to solve investment and planning-related problems. This group includes several chartered financial analysts, certified financial planners, an accredited investment fiduciary and professionals with law and masters degrees.

We also offer practice management concepts and tools to both wealth advisors and retirement plan advisors to assist in their new business and service efforts, and certain technology-driven products and services aimed at the middle market employer marketplace to assist both employers and employees with their health and wealth planning.

Products and Services

We manage a variety of equity, fixed income, alternative and blended asset strategies, using primarily traditional asset classes such as stocks and bonds. These strategies may include a mix of the different vehicles we offer, including separate accounts, mutual funds, and collective investment trusts. Our goal is to help our clients meet their investment objectives by providing competitive positive returns over full stock market cycles, including both bull and bear market environments. Three key elements of our investment process help to keep us focused on that goal:

• | Team-Based Research. Our analysts and economists work together to understand market opportunities from both a broad, macro level and a more detailed industry and company level. This combination of both "top-down" and "bottom-up" research allows us to identify trends, themes and company specific investment opportunities across the |

3

globe, and has been a key factor in our success. The use of a team rather than an individual to manage strategies means we emphasize repeatable processes over personalities.

• | A Focus on Absolute Returns. Whether investing in a country, industry or individual company, we hold a strong belief that price matters. We are focused on helping our clients avoid permanent loss of capital over their time horizon, which is different than day-to-day volatility, which could in fact present opportunities. We believe that active management has consistently been the most appropriate and relevant investment strategy to achieve these goals across changing market environments. To that end, we believe we have aligned the incentives of our analysts with the goals of our clients by structuring our analyst compensation system such that returns that are both negative and below benchmarks produce a negative bonus the analyst has to offset before earning a positive bonus. The analysts earn their largest bonus, which could be multiples of their salary and the largest part of their total compensation, when they earn returns that are both positive and above benchmarks for our clients. We believe this focus on price has provided capital preservation in many valuation-based bear markets during our history, and reduces the risk of permanent, downside price fluctuation from our buy price. |

• | Flexibility to be Benchmark Agnostic. The flexibility to invest across sectors, countries and asset classes allows us to focus on companies we view as having greater upside potential than downside risk, and allows us to have a broad enough opportunity set to freely navigate away from areas of excess or speculation without limiting the number of investment opportunities. While this approach may often result in our strategies having meaningfully different allocations and exposures when compared to market benchmarks, we believe this type of differentiation is necessary to manage risk in many environments. |

Sales and Distribution

We distribute our products and services through direct sales to high net worth individuals, middle market institutions and larger institutional clients that are working with consultants. In addition, we have dedicated efforts to sell through financial intermediaries and platforms. In identifying prospective new business, we focus on individuals and institutions that have long-term objectives and needs, and are looking for a partner in addressing those objectives. We believe our problem-solving approach fosters strong relationships, and our focus on communicating our investment process helps to manage long-term expectations and minimize AUM turnover.

As of December 31, 2015, we have nearly 60 sales and distribution professionals, with an average of approximately 18 years of industry experience. Our Managing Director of Sales, who has been with us since 1993, oversees 13 direct institutional and regional sales representatives. Our Managing Director of Regional Sales and Managing Director of Intermediary Distribution, who have respectively been with us for 17 and 6 years, report to our Managing Director of Sales and help to manage our various sales and service representatives. Specifically, our direct national sales representatives cover large, multiple state territories prospecting large plans. Our direct regional sales representatives cover smaller territories and pursue both individual and middle market institutional business opportunities, and our regional service representatives focus on servicing individual and small institutional clients. Our Intermediary Channel includes external and internal wholesalers, separately covering retirement plan advisors and wealth management advisors, and key account representatives. Lastly, we have Portfolio Strategists who are primarily responsible for consultant relations.

Sales representatives have different areas of focus in terms of client type, product and vehicle, but are highly knowledgeable about the investment markets, our investment process and our product and service offerings, so as to lessen the need for our research department personnel to assist in bringing new relationships on board. Our sales representatives are responsible for generating new business as well as maintaining existing business. Referrals are an important source of new business in both our direct and intermediary marketing efforts. To assist the sales representatives, we have over 30 service professionals who are responsible for responding to client requests and questions.

Our separate accounts are primarily distributed by direct sales representatives that market to individuals and institutions in defined territories within North America. Our regional sales representatives form separate account relationships with high net worth individuals that own businesses, sit on boards of endowments or foundations, or are generally well-connected in their communities, and leverage those relationships to obtain middle market, institutional separate account business. Our high net worth and middle market separate account clients also often use the consultative services of our Client Analytics Group, which includes a variety of planning services. Our regional sales representatives focus more on large institutional mandates across the United States. We obtain a smaller portion of our separate account business through our external and internal wholesalers, who work with intermediaries, including national brokerage firm representatives and independent financial advisors working with high net worth individuals, and unaffiliated registered investment advisor platforms that select our strategies for inclusion in their investment programs.

Our mutual funds and collective investment trusts are distributed through intermediaries, platforms and investment consultants, as well as direct to institutional clients. Our internal and external wholesale professionals are focused on distributing through retirement plan advisors who work with defined contribution plans, as well as through brokers and

4

advisors who work with retail clients. Our consultant relations specialists are dedicated to building relationships with investment consultants. The primary responsibilities of these individuals are to educate consultants, platform providers and advisors on our investment products and process and to ensure our products are among those considered for placement within mutual fund advisory programs, on platforms’ approved lists and in active searches conducted by consultants. Our direct institutional and regional sales representatives also contribute to mutual fund and collective investment trust distribution through sales and servicing of fund vehicles to large market retirement plan sponsors and institutions.

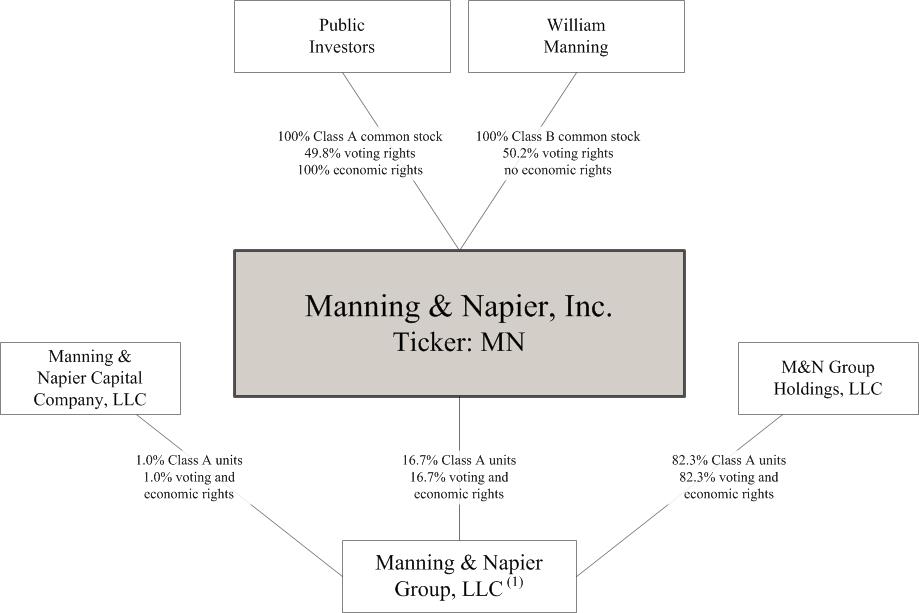

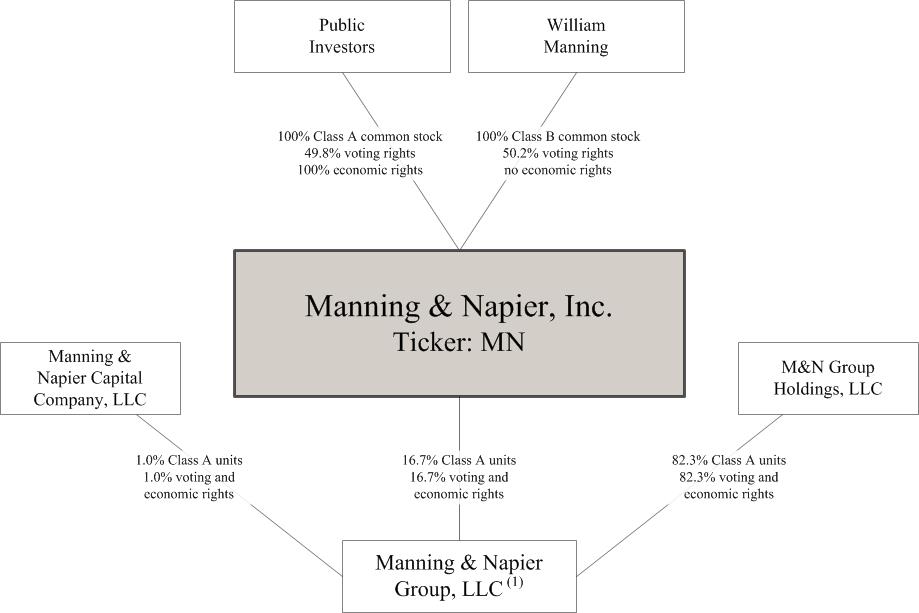

Structure

The Company was incorporated in 2011 as a Delaware corporation, and is the sole managing member of Manning & Napier Group, LLC and its subsidiaries (“Manning & Napier Group”), a holding company for the investment management businesses conducted by its operating subsidiaries. The diagram below depicts our organization structure as of December 31, 2015.

________________________

________________________(1) | The operating subsidiaries of Manning & Napier Group include Manning & Napier Advisors, LLC, Manning & Napier Alternative Opportunities, LLC, Perspective Partners LLC, Manning & Napier Information Services, LLC, Manning & Napier Benefits, LLC, Manning & Napier Investor Services, Inc. and Exeter Trust Company. |

As of December 31, 2015, we had 474 employees, including William Manning, our Chairman and controlling stockholder, and other current employee-owners, most of whom are based in Fairport, New York. Collectively, these owners and former employee-owners own approximately 83.3% of our operating subsidiary, Manning & Napier Group. We believe that our culture of employee ownership aligns our interests with those of our clients and shareholders by delivering strong long-term investment performance and solutions.

Competition

Historically, we have competed to attract assets to manage principally on the basis of:

• | a broad portfolio and service offering that provides solutions for our clients; |

5

• | the disciplined and repeatable nature of our team-based investment processes; |

• | the quality of the service we provide to our clients and the duration of our relationships with them; |

• | our pricing compared to other investment management products offered; |

• | the tenure and continuity of our management and team-based investment professionals; and |

• | our long-term investment track record. |

Our ability to continue to compete effectively will also depend upon our ability to retain our current investment professionals and employees and to attract highly qualified new investment professionals and employees. We compete in all aspects of our business with a large number of investment management firms, commercial banks, broker-dealers, insurance companies and other financial institutions.

Regulation

Our business is subject to extensive regulation in the United States at the federal level and, to a lesser extent, the state level, as well as by self-regulatory organizations and regulations outside the United States. Under certain of these laws and regulations, agencies that regulate investment advisers have broad administrative powers, including the power to limit, restrict or prohibit an investment adviser from carrying on its business in the event that it fails to comply with such laws and regulations. Possible sanctions that may be imposed include the suspension of individual employees, limitations on engaging in certain lines of business for specified periods of time, revocation of investment adviser and other registrations, censures and fines.

SEC Regulation

Manning & Napier Advisors, LLC ("MNA") is registered with the U.S. Securities and Exchange Commission, or SEC, as investment advisers under the U.S. Investment Advisers Act of 1940, as amended, ("the Advisers Act"). Additionally, the Manning & Napier Fund, Inc., (the "Fund"), and several of the third-party investment companies we sub-advise are registered under the U.S. Investment Company Act of 1940, (the "1940 Act"). The Advisers Act and the 1940 Act, together with the SEC’s regulations and interpretations thereunder, impose substantive and material restrictions and requirements on the operations of advisers and mutual funds. The SEC is authorized to institute proceedings and impose sanctions for violations of the Advisers Act and the 1940 Act, ranging from fines and censures to termination of an adviser’s registration.

As an investment adviser, we have a fiduciary duty to our clients. The SEC has interpreted these duties to impose standards, requirements and limitations on, among other things:

• | trading for proprietary, personal and client accounts; |

• | allocations of investment opportunities among clients; |

• | use of soft dollars; |

• | execution of transactions; and |

• | recommendations to clients. |

We manage accounts for all of our clients on a discretionary basis, with authority to buy and sell securities for each portfolio, select broker-dealers to execute trades and negotiate brokerage commission rates. In connection with these transactions, we receive soft dollar credits from broker-dealers that have the effect of reducing certain of our expenses. All of our soft dollar arrangements are intended to be within the safe harbor provided by Section 28(e) of the U.S. Securities Exchange Act of 1934, as amended, (the "Exchange Act".) If our ability to use soft dollars were reduced or eliminated as a result of statutory amendments or new regulations, our operating expenses would increase.

As a registered adviser, we are subject to many additional requirements that cover, among other things:

• | disclosure of information about our business to clients; |

• | maintenance of formal policies and procedures; |

• | maintenance of extensive books and records; |

• | restrictions on the types of fees we may charge; |

• | custody of client assets; |

• | client privacy; |

• | advertising; and |

6

• | solicitation of clients. |

The SEC has authority to inspect any investment adviser and typically inspects a registered adviser periodically to determine whether the adviser is conducting its activities (i) in accordance with applicable laws, (ii) consistent with disclosures made to clients and (iii) with adequate policies, procedures and systems to ensure compliance.

For the year ended December 31, 2015, 32% of our revenues were derived from our advisory services to investment companies registered under the 1940 Act, including 32% derived from our advisory services to the Fund. The 1940 Act imposes significant requirements and limitations on a registered fund, including with respect to its capital structure, investments and transactions. While we exercise broad discretion over the day-to-day management of the business and affairs of the Fund and the investment portfolios of the Fund and the funds we sub-advise, our own operations are subject to oversight and management by each fund’s board of directors. Under the 1940 Act, a majority of the directors must not be “interested persons” with respect to us (sometimes referred to as the “independent director” requirement). The responsibilities of the board include, among other things, approving our investment management agreement with the Fund; approving other service providers; determining the method of valuing assets; and monitoring transactions involving affiliates. Our investment management agreements with the Fund may be terminated by the funds on not more than 60 days’ notice, and are subject to annual renewal by the Fund board after their initial term.

The 1940 Act also imposes on the investment adviser to a mutual fund a fiduciary duty with respect to the receipt of the adviser’s investment management fees. That fiduciary duty may be enforced by the SEC through administrative action or litigation by investors in the fund pursuant to a private right of action.

Under the Advisers Act, our investment management agreements may not be assigned without the client’s consent. Under the 1940 Act, investment management agreements with registered funds (such as the mutual funds we manage) terminate automatically upon assignment. The term “assignment” is broadly defined and includes direct assignments as well as assignments that may be deemed to occur upon the transfer, directly or indirectly, of a controlling interest in us.

Manning & Napier Investor Services ("MNBD"), our SEC-registered broker-dealer subsidiary, is subject to the SEC’s Uniform Net Capital Rule, which requires that at least a minimum part of a registered broker-dealer’s assets be kept in relatively liquid form. As of December 31, 2015, MNBD was in compliance with its net capital requirements.

ERISA-Related Regulation

We are a fiduciary under the Employee Retirement Income Security Act of 1974, as amended, or ERISA, with respect to assets that we manage for benefit plan clients subject to ERISA. ERISA, regulations promulgated thereunder and applicable provisions of the Internal Revenue Code of 1986, as amended, impose certain duties on persons who are fiduciaries under ERISA, prohibit certain transactions involving ERISA plan clients and provide monetary penalties for violations of these prohibitions.

The fiduciary duties under ERISA may be enforced by the U.S. Department of Labor by administrative action or litigation and by our benefit plan clients pursuant to a private right of action. In addition, the IRS may assess excise taxes against us if we engage in prohibited transactions on behalf of or with our benefit plan clients.

CFTC/NFA Regulation

MNA is registered with the Commodity Futures Trading Commission, or CFTC, as a commodity pool operator ("CPO") and is also a member of the National Futures Association, or NFA. The CFTC and NFA each administer a regulatory system covering futures contracts and various other financial instruments in which certain of our clients may invest.

New Hampshire Banking Regulation

Exeter Trust Company is a state-chartered non-depository trust company subject to the laws of the State of New Hampshire and the regulations promulgated thereunder by the New Hampshire Bank Commissioner.

Insurance-Related Regulation

Manning & Napier Benefits, LLC is a registered insurance broker in multiple states including the District of Columbia and, as such, is subject to various state insurance and health-related rules and regulations.

Non-U.S. Regulation

In addition to the extensive regulation our investment management industry is subject to in the United States, we are also subject to regulation by various Canadian regulatory authorities in the Canadian provinces where we operate pursuant to exemptions from registration. We are authorized to act as a non-resident sub-advisory investment manager to collective investment vehicles in Ireland. Our business is also subject to the rules and regulations of the more than 30 countries in which we currently buy and sell portfolio investments.

Employees

As of December 31, 2015, we had 474 employees, most of whom are based in Fairport, New York. None of our employees are subject to a collective bargaining agreement. We believe that relations with our employees are good. We strive to attract and retain the best talent in the industry.

7

Available Information

All annual, quarterly and current reports, and amendments to those reports, proxy statements and other filings we file or furnish with the SEC are available free of charge from the SEC’s website at http://www.sec.gov/ or from the Public Reference Room at 100 F Street N.E., Washington, D.C. 20549; 1-800-SEC-0330.

We also make the documents listed above available without charge through the Investor Relations section of our website at http://ir.manning-napier.com/. Such documents are available as soon as reasonably practicable after electronic filing of the material with the SEC.

Item 1A. Risk Factors.

Risks Related to our Business

Our revenues are dependent on the market value and composition of our AUM, all of which are subject to fluctuation due to factors outside of our control.

We derive the majority of our revenue from investment management fees, typically calculated as a percentage of the market value of our AUM. As a result, our revenues are dependent on the value and composition of our AUM, all of which are subject to fluctuation due to many factors, including:

• | Declines in prices of securities in our portfolios. The prices of the securities held in the portfolios we manage may decline due to any number of factors beyond our control, including, among others, declining stock or commodities markets, changes in interest rates, a general economic downturn, political uncertainty or acts of terrorism. The U.S. and global financial markets continue to be subject to uncertainty and instability. Such factors could cause an unusual degree of volatility and price declines for securities in the portfolios we manage. |

• | Redemptions and other withdrawals. Our clients generally may withdraw their funds at any time, on very short notice and without any significant penalty. A substantial portion of our revenue is derived from investment advisory agreements that are terminable by clients upon short notice or no notice and investors in the mutual funds we advise can redeem their investments in those funds at any time without prior notice. Also, new clients and portfolios may not have the same client retention characteristics as we have experienced in the past. In addition, in a declining stock market, the pace of redemptions could accelerate. |

• | Investment performance. Our ability to deliver strong investment performance depends in large part on our ability to identify appropriate investment opportunities in which to invest client assets. If we are unable to identify sufficient appropriate investment opportunities for existing and new client assets on a timely basis, our investment performance could be adversely affected. The risk that sufficient appropriate investment opportunities may be unavailable is influenced by a number of factors including general market conditions. If our portfolios perform poorly, even over the short-term, as compared with our competitors or applicable third-party benchmarks, or the rankings of mutual funds we manage decline, we may lose existing AUM and have difficulty attracting new assets. |

If any of these factors cause a decline in our AUM, it would result in lower investment management revenues. If our revenues decline without a commensurate reduction in our expenses, our net income will be reduced and our business will be adversely affected.

We derive substantially all of our revenues from contracts and relationships that may be terminated upon short or no notice.

We derive substantially all of our revenues from investment advisory and sub-advisor agreements, all of which are terminable by clients upon short notice or no notice and without any significant penalty. Our investment management agreements with mutual funds, as required by law, are generally terminable by the funds’ board of directors or a vote of the majority of the funds’ outstanding voting securities on not more than 60 days’ written notice. After an initial term, each fund’s investment management agreement must be approved and renewed annually by such fund’s board, including by its independent members. In addition, all of our separate account clients and some of the pooled investment vehicles, including mutual funds, that we sub-advise have the ability to re-allocate all or any portion of the assets that we manage away from us at any time with little or no notice. These investment management agreements and mutual fund and collective investment trust client

8

relationships may be terminated or not renewed for any number of reasons. The decrease in revenues that could result from the termination of a material client relationship or group of client relationships could have an adverse effect on our business.

Our portfolios may not obtain attractive returns under certain market conditions or at all.

The goal of our investment process is to provide competitive absolute returns over full market cycles. Accordingly, our portfolios may not perform well compared to benchmarks or other investment managers’ strategies during certain periods of time or under certain market conditions. Short-term underperformance may negatively affect our ability to retain clients and attract new clients. We are likely to be most out of favor when the markets are running on positive or negative price momentum and market prices become disconnected from underlying investment fundamentals. During and shortly following such periods of relative under performance, we are likely to see our highest levels of client turnover, even if our absolute returns are positive. Loss of client assets and the failure to attract new clients could adversely affect our revenues and growth.

The loss of key investment professionals or members of our senior management team could have an adverse effect on our business.

We depend on the skills and expertise of qualified investment professionals and our success depends on our ability to retain key employees, including members of our senior management team. Our investment professionals possess substantial experience in investing and have been primarily responsible for the historically attractive investment performance we have achieved. We particularly depend on our executive officers as well as senior members of our research department. The loss of any of these key individuals could limit our ability to successfully execute our business strategy and could have an adverse effect on our business.

Any of our investment or management professionals may resign at any time, subject to various covenants not to compete with us. In addition, employee-owners are subject to additional covenants not to compete.

Competition for qualified investment, management, marketing and client service professionals is intense and we may fail to attract and retain qualified personnel in the future. Our ability to attract and retain our named executive officers and other key employees will depend heavily on the amount and structure of compensation and opportunities for equity ownership we offer. We utilize a compensation structure that uses a combination of cash and equity-based incentives as appropriate. However, our compensation may not be effective to recruit and retain the personnel we need, especially if our equity-based compensation does not return significant value to employees. Any cost-reduction initiative or adjustments or reductions to compensation could negatively impact our ability to retain key personnel. In addition, changes to our management structure, corporate culture and corporate governance arrangements could negatively impact our ability to retain key personnel.

We may be required to reduce the fees we charge, or our fees may decline due to changes in our AUM composition, which could have an adverse effect on our profit margins and results of operations.

Our current fee structure may be subject to downward pressure due to a variety of factors, including a trend in recent years toward lower fees in the investment management industry. We may be required to reduce fees with respect to both the separate accounts we manage and the mutual funds and collective trust funds we advise. In addition, we may charge lower fees to attract future new business as compared to our existing business, which may result in us having to reduce our fees with respect to our existing business accordingly. The investment management agreements pursuant to which we advise mutual funds are terminable on short notice and, after an initial term, are subject to an annual process of review and renewal by the funds’ boards. As part of that annual review process, the fund board considers, among other things, the level of compensation that the fund has been paying us for our services, and that process may result in the renegotiation of our fee structure or increase our obligations, thus increasing the cost of our performance. Any fee reductions on existing or future new business could have an adverse effect on our profit margins and results of operations.

Our AUM is concentrated in certain portfolios.

As of December 31, 2015, 64% of our AUM was invested in products that comprise our blended asset portfolio. As a result, a substantial portion of our operating results depends upon the performance of these products, and our ability to retain client assets in such products. If a significant portion of the investors in our blended asset portfolio decide to withdraw their investments or terminate their investment management agreements for any reason, including poor investment performance or adverse market conditions, our revenues from these portfolios would decline, which could have an adverse effect on our earnings and financial condition.

Several of our portfolios involve investing principally in the securities of non-U.S. companies, which involve foreign currency exchange risk, and tax, political, social and economic uncertainties and risks.

9

As of December 31, 2015, approximately 30% of our AUM across all of our portfolios was invested in securities of non-U.S. companies. Fluctuations in foreign currency exchange rates could negatively affect the returns of our clients who are invested in these strategies. In addition, an increase in the value of the U.S. dollar relative to non-U.S. currencies is likely to result in a decrease in the U.S. dollar value of our AUM, which, in turn, could result in lower revenue since we report our financial results in U.S. dollars.

Investments in non-U.S. issuers may also be affected by tax positions taken in countries or regions in which we are invested as well as political, social and economic uncertainty. Declining tax revenues may cause governments to assert their ability to tax the local gains and/or income of foreign investors (including our clients), which could adversely affect clients’ interests in investing outside their home markets. Many financial markets are not as developed, or as efficient, as the U.S. financial markets and, as a result, those markets may have limited liquidity and higher price volatility and may lack established regulations. Liquidity may also be adversely affected by political or economic events, government policies, social or civil unrest within a particular country, and our ability to dispose of an investment may also be adversely affected if we increase the size of our investments in smaller non-U.S. issuers. Non-U.S. legal and regulatory environments, including financial accounting standards and practices, may also be different, and there may be less publicly available information about such companies. These risks could adversely affect the performance of our strategies that are invested in securities of non-U.S. issuers and may be particularly acute in the emerging or less developed markets in which we invest.

The growth we have experienced historically has been and may continue to be difficult to sustain, and we may have difficulty managing our growth effectively.

The growth in our AUM we have experienced historically has been and may continue to be difficult to sustain. The future growth of our business will depend on, among other things:

• | our success in achieving desired investment performance from our portfolios; |

• | our ability to deal with changing market conditions; |

• | our ability to retain key investment professionals; |

• | our ability to attract investment professionals as necessary; |

• | our ability to devote sufficient resources to maintaining existing portfolios and to selectively develop new portfolios; |

• | our ability to maintain and extend our distribution capabilities; |

• | our ability to successfully consummate and integrate strategic acquisitions; |

• | our ability to maintain adequate financial and business controls; and |

• | our ability to comply with new legal and regulatory requirements arising in response to both the increased sophistication of the investment management industry and the significant market and economic events of the last few years. |

Unless our growth results in an increase in our revenues that is proportionate to the increase in our costs associated with this growth, our future profitability will be adversely affected. In addition, failure to successfully diversify into new asset classes may adversely affect our growth strategy and our future profitability.

The historical returns of our existing portfolios may not be indicative of their future results or of the portfolios we may develop in the future.

The historical returns of our portfolios and the ratings and rankings we or the mutual funds that we advise have received in the past should not be considered indicative of the future results of these portfolios or of any other portfolios that we may develop in the future. The investment performance we achieve for our clients varies over time and the variance can be wide. The ratings and rankings we or the mutual funds we advise have received are typically revised monthly. The historical performance and ratings and rankings included in this report are as of December 31, 2015 and for periods then ended except where otherwise stated. The performance we have achieved and the ratings and rankings received at subsequent dates and for subsequent periods may be higher or lower and the difference could be material. Our portfolios’ returns have benefited during some periods from investment opportunities and positive economic and market conditions. In other periods, general economic and market conditions have negatively affected our portfolios’ returns. These negative conditions may occur again, and in the future we may not be able to identify and invest in profitable investment opportunities within our current or future portfolios.

We may elect to pursue growth in the United States and abroad through acquisitions or joint ventures, which would expose us to risks inherent in assimilating new operations, expanding into new jurisdictions, and making non-controlling minority investments in other entities.

10

In order to maintain and enhance our competitive position, we may review and pursue acquisition and joint venture opportunities. We cannot assure we will identify and consummate any such transactions on acceptable terms or have sufficient resources to accomplish such a strategy. In addition, any strategic transaction can involve a number of risks, including:

• | additional demands on our staff; |

• | unanticipated problems regarding integration of investor account and investment security recordkeeping, operating facilities and technologies, and new employees; |

• | adverse effects in the event acquired intangible assets or goodwill become impaired; |

• | the existence of liabilities or contingencies not disclosed to or otherwise known by us prior to closing such a transaction; and |

• | dilution to our public stockholders if we issue shares of our Class A common stock, or units of Manning & Napier Group with exchange rights, in connection with future acquisitions. |

We depend in part on third-party intermediaries to market our portfolios and help service our client base.

Our ability to attract additional assets to manage is in part dependent on our access to third-party intermediaries. We gain access to mutual fund investors and some retail and institutional clients through third parties, including mutual fund platforms and financial intermediaries. As of December 31, 2015, the largest relationship we have with a third party represents approximately 5.0% of our total AUM and the mutual fund platform representing the largest portion of our fund assets represents an additional 1.8% of our total AUM. We compensate most of the intermediaries through which we gain access to investors in our mutual funds by paying fees, most of which are based on a percentage of assets invested in our mutual funds through that intermediary and with respect to which that intermediary provides services. These intermediaries and their client bases may not continue to be accessible to us on terms we consider commercially reasonable, or at all. Limiting or the total absence of such access could have an adverse effect on our results of operations. In addition, the service levels provided by these intermediaries may increase under certain trading and servicing models and could result in increased fees charged by the intermediary. Many of these intermediaries have internal manager due diligence teams that review and evaluate our products and our firm from time to time. Poor evaluations of a particular product, portfolio or us as an investment management firm, or decreased demand for our active investment style or mutual fund vehicles, may result in client withdrawals or may impair our ability to attract new assets through these intermediaries. In addition, the industry trends toward consolidation in the broker-dealer industry may lead to reduced distribution access and increases in fees we are required to pay to intermediaries. If such increased fees should be required, refusal to pay them could restrict our access to those client bases while paying them could adversely affect our profitability.

Our efforts to establish new portfolios or new products or services may be unsuccessful and could negatively impact our results of operations and our reputation.

As part of our growth strategy, we may seek to take advantage of opportunities to develop new portfolios consistent with our philosophy of managing portfolios to meet our clients’ objectives and using a team-based investment approach. The costs associated with establishing a new portfolio initially likely will exceed the revenues that the portfolio generates. If any such new portfolio performs poorly or fails to attract sufficient assets to manage, our results of operations could be negatively impacted. Further, a new portfolio’s poor performance may negatively impact our reputation and the reputation of our other portfolios within the investment community. In addition, we have developed and may seek from time to time to develop new products and services to take advantage of opportunities involving technology, insurance, participant and plan sponsor education and other products beyond investment management. The development of these products and services could involve investment of financial and management resources and may not be successful in developing client relationships, which could have an adverse effect on our business. The cost to develop these products initially will likely exceed the revenue they generate. If establishing new portfolios or offering new products or services requires hiring new personnel, to the extent we are unable to recruit and retain sufficient personnel, we may not be successful in further diversifying our portfolios, client assets and business, which could have an adverse effect on our business and future prospects.

Our lenders may require us to provide additional collateral, which may restrict us from leveraging our assets as fully as desired, and reduce our liquidity, earnings and cash available for distribution to our shareholders.

Certain of our corporate assets are invested in products that we leverage. We are required to maintain cash held by brokers as collateral for managed futures. If the market value of these securities fluctuate, we may be required by the lender to provide additional collateral on minimal notice. Posting additional collateral will reduce our liquidity and limit our ability to leverage our assets, which could adversely affect our business. Additionally, we may be required to liquidate assets at a disadvantageous time, which could cause us to incur further losses and adversely affect our results of operations and financial condition, and may impair our ability to make distributions to our shareholders.

11

Our revolving credit agreement contains, and our future indebtedness may contain, various covenants that may limit our business activities.

Our revolving credit agreement contains financial and operating covenants that limit our business activities, including restrictions on our ability to incur additional indebtedness and pay dividends to our stockholders. For example, the agreement includes financial covenants requiring us not to exceed specified ratios of indebtedness to consolidated earnings before interest, taxes, depreciation and amortization (as defined in the agreements), or EBITDA, and interest expense to consolidated EBITDA. The failure to comply with any of these restrictions, or our inability to generate sufficient cash flow to service our debt, could result in an event of default, giving our lenders the ability to accelerate repayment of our obligations, which could adversely affect our business and financial condition. As of December 31, 2015, there was no outstanding principal amount due under the agreement and we believe we are in compliance with all of the covenants and other requirements set forth in the agreement.

Our failure to comply with investment guidelines set by our clients and limitations imposed by applicable law, could result in damage awards against us and a loss of our AUM, either of which could adversely affect our reputation, results of operations or financial condition.

When clients retain us to manage assets on their behalf, they generally specify certain guidelines regarding investment allocation that we are required to follow in managing their portfolios. We are also required to invest the mutual funds’ assets in accordance with limitations under the 1940 Act, and applicable provisions of the Internal Revenue Code of 1986, as amended. Other clients, such as plans subject to ERISA, or non-U.S. funds, require us to invest their assets in accordance with applicable law. Our failure to comply with any of these guidelines and other limitations could result in losses to clients or investors in our products which, depending on the circumstances, could result in our obligation to make clients whole for such losses. If we believed that the circumstances did not justify a reimbursement, or clients believed the reimbursement we offered was insufficient, clients could seek to recover damages from us, withdraw assets from our products or terminate their investment management agreement with us. Any of these events could harm our reputation and adversely affect our business.

A change of control of our company could result in termination of our investment advisory agreements.

Under the 1940 Act, each of the investment advisory agreements for SEC registered mutual funds that our affiliate, MNA, advises automatically terminates in the event of its assignment, as defined under the 1940 Act. If such an assignment were to occur, MNA could continue to act as adviser to any such fund only if that fund’s board of directors and stockholders approved a new investment advisory agreement, except in the case of certain of the funds that we sub-advise for which only board approval would be necessary. In addition, under the Advisers Act each of the investment advisory agreements for the separate accounts we manage may not be assigned without the consent of the client. An assignment may occur under the 1940 Act and the Advisers Act if, among other things, MNA undergoes a change of control. In certain other cases, the investment advisory agreements for the separate accounts we manage require the consent of the client for any assignment. If such an assignment occurs, we cannot be certain that MNA will be able to obtain the necessary approvals from the boards and stockholders of the mutual funds that it advises or the necessary consents from separate account clients.

Operational risks may disrupt our business, result in losses or limit our growth.

We are heavily dependent on the capacity and reliability of the communications, information and technology systems supporting our operations, whether developed, owned and operated by us or by third parties. Operational risks such as trading or operational errors or interruption of our financial, accounting, trading, compliance and other data processing systems, whether caused by fire, natural disaster or pandemic, power or telecommunications failure, act of terrorism or war or otherwise, could result in a disruption of our business, liability to clients, regulatory intervention or reputational damage, and thus adversely affect our business. Some types of operational risks, including, for example, trading errors, may be increased in periods of increased volatility, which can magnify the cost of an error. Although we have back-up systems in place, our back-up procedures and capabilities in the event of a failure or interruption may not be adequate, and the fact that we operate our business out of multiple physical locations may make such failures and interruptions difficult to address on a timely and adequate basis. As and if our client base, number of portfolios and/or physical locations increase, developing and maintaining our operational systems and infrastructure may become increasingly challenging, which could constrain our ability to expand our business. Any upgrades or expansions to our operations or technology to accommodate increased volumes of transactions or otherwise may require significant expenditures and may increase the probability that we will suffer system degradations and failures. We also depend on our headquarters in Fairport, New York, where a majority of our employees, administration and technology resources are located, for the continued operation of our business. Any significant disruption to our headquarters could have an adverse effect on our business.

We depend on third-party service providers for services that are important to our business, and an interruption or cessation of such services by any such service providers could have an adverse effect on our business.

We depend on a number of service providers, including custodial and clearing firms, and vendors of communications and networking products and services. We are not assured that these providers will be able to continue to provide these services in

12

an efficient manner or that they will be able to adequately expand their services to meet our needs. An interruption or malfunction in or the cessation of an important service by any third-party and our inability to make alternative arrangements in a timely manner, or at all, could have an adverse impact on our business, financial condition and operating results.

Employee misconduct could expose us to significant legal liability and reputational harm.

We operate in an industry in which integrity and the confidence of our clients are of critical importance. Accordingly, if any of our employees engage in illegal or suspicious activities or other misconduct, we could be subject to regulatory sanctions and suffer serious harm to our reputation, financial condition, client relationships and ability to attract new clients. For example, our business often requires that we deal with confidential information. If our employees were to improperly use or disclose this information, even if inadvertently, we could suffer serious harm to our reputation, financial condition and current and future business relationships. It is not always possible to deter employee misconduct, and the precautions we take to detect and prevent this activity may not always be effective. Misconduct by our employees, or even unsubstantiated allegations of misconduct, could result in an adverse effect on our reputation and our business.

Failure to implement effective information and cyber security policies, procedures and capabilities could disrupt operations and cause financial losses that could result in a decrease in earnings.

We are dependent on the effectiveness of our information and cyber security policies, procedures and capabilities to protect our computer and telecommunications systems and the data that reside on or are transmitted through them. An externally caused information security incident, such as a hacker attack, virus or worm, or an internally caused issue, such as failure to control access to sensitive systems, could materially interrupt business operations or cause disclosure or modification of sensitive or confidential client or competitive information and could result in material financial loss, loss of competitive position, regulatory actions, breach of client contracts, reputational harm or legal liability, which, in turn, could cause a decline in the Company’s earnings.

Failure to properly address conflicts of interest could harm our reputation, business and results of operations.

As we expand the scope of our business and our client base, we must continue to monitor and address any conflicts between our interests and those of our clients. The SEC and other regulators scrutinize potential conflicts of interest, and we have implemented procedures and controls that we believe are reasonably designed to address these issues. However, appropriately dealing with conflicts of interest is complex and if we fail, or appear to fail, to deal appropriately with conflicts of interest, we could face reputational damage, litigation or regulatory proceedings or penalties, any of which could adversely affect our reputation, business and results of operations.

If our techniques for managing risk are ineffective, we may be exposed to material unanticipated losses.

In order to manage the significant risks inherent in our business, we must maintain effective policies, procedures and systems that enable us to identify, monitor and control our exposure to operational, legal and reputational risks. Our risk management methods may prove to be ineffective due to their design or implementation, or as a result of the lack of adequate, accurate or timely information or otherwise. If our risk management efforts are ineffective, we could suffer losses that could have an adverse effect on our financial condition or operating results. Additionally, we could be subject to litigation, particularly from our clients, and sanctions or fines from regulators. Our techniques for managing risks in client portfolios may not fully mitigate the risk exposure in all economic or market environments, or against all types of risk, including risks that we might fail to identify or anticipate.

The cost of insuring our business is substantial and may increase.

We believe our insurance costs are reasonable but they could fluctuate significantly from year to year. In addition, certain insurance coverage may not be available or may only be available at prohibitive costs. As we renew our insurance policies, we may be subject to additional costs resulting from rising premiums, the assumption of higher deductibles or co-insurance liability and, to the extent certain of our mutual funds purchase separate director and officer or errors and omissions liability coverage, an increased risk of insurance companies disputing responsibility for joint claims. Higher insurance costs and incurred deductibles, as with any expense, would reduce our net income.

Risks Related to our Industry

We are subject to extensive regulation.

We are subject to extensive regulation for our investment management business and operations, including regulation by the SEC under the 1940 Act and the Advisers Act, by the U.S. Department of Labor under ERISA, by the Financial Industry Regulatory Authority, Inc., or FINRA, by the National Futures Association and U.S. Commodity Futures Trading Commission. The U.S. mutual funds we advise are registered with and regulated by the SEC as investment companies under the 1940 Act. The Advisers Act imposes numerous obligations on investment advisers including record keeping, advertising and operating requirements, disclosure obligations and prohibitions on fraudulent activities. The 1940 Act imposes similar obligations, as well

13

as additional detailed operational requirements, on registered investment companies, which must be adhered to by their investment advisers. The U.S. mutual funds that we advise and our broker-dealer subsidiary are each subject to the USA PATRIOT Act of 2001, which requires them to know certain information about their clients and to monitor their transactions for suspicious financial activities, including money laundering. The U.S. Office of Foreign Assets Control, or OFAC, has issued regulations requiring that we refrain from doing business, or allow our clients to do business through us, in certain countries or with certain organizations or individuals on a list maintained by the U.S. government. In addition, Manning & Napier Benefits, LLC is a registered insurance broker with the New York State Insurance Department and, as such, is subject to various insurance and health-related rules and regulations.

Our failure to comply with applicable laws or regulations could result in fines, censure, suspensions of personnel or other sanctions, including revocation of our registration as an investment adviser. Even if a sanction imposed against us or our personnel is small in monetary amount, the adverse publicity arising from the imposition of sanctions against us by regulators could harm our reputation, result in withdrawal by our clients from our products and impede our ability to retain clients and develop new client relationships, which may reduce our revenues.

We face the risk of significant intervention by regulatory authorities, including extended investigation and surveillance activity, adoption of costly or restrictive new regulations and judicial or administrative proceedings that may result in substantial penalties. Among other things, we could be fined or be prohibited from engaging in some of our business activities. The requirements imposed by our regulators are designed to ensure the integrity of the financial markets and to protect customers and other third parties who deal with us, and are not designed to protect our stockholders. Accordingly, these regulations often serve to limit our activities, including through net capital, customer protection and market conduct requirements.

The regulatory environment in which we operate is subject to continual change, and regulatory developments designed to increase oversight could adversely affect our business.

The legislative and regulatory environment in which we operate has undergone significant changes in the recent past. We believe that significant regulatory changes in our industry are likely to continue on a scale that exceeds the historical pace of regulatory change, which is likely to subject industry participants to additional, more costly and generally more punitive regulation.

New laws or regulations, or changes in the enforcement of existing laws or regulations, applicable to us and our clients could adversely affect our business. Our ability to function in this environment will depend on our ability to constantly monitor and promptly react to legislative and regulatory changes. There have been a number of highly publicized regulatory inquiries that have focused on the investment management industry. These inquiries have resulted in increased scrutiny of the industry and new rules and regulations for mutual funds and investment managers. This regulatory scrutiny may limit our ability to engage in certain activities that might be beneficial to our shareholders. Further, adverse results of regulatory investigations of mutual fund, investment advisory and financial services firms could tarnish the reputation of the financial services industry generally and mutual funds and investment advisers more specifically, causing investors to avoid further fund investments or redeem their account balances. Redemptions would decrease our AUM, which would reduce our advisory revenues and net income.

Further, due to acts of serious fraud in the investment management industry and perceived lapses in regulatory oversight, U.S. and non-U.S. governmental and regulatory authorities may continue to increase regulatory oversight of our business. We may be adversely affected as a result of new or revised legislation or regulations imposed by the SEC, other U.S. governmental regulatory authorities or self-regulatory organizations that supervise the financial markets. We also may be adversely affected by changes in the interpretation or enforcement of existing laws and rules by these governmental authorities and self-regulatory organizations, as well as by U.S. courts. It is impossible to determine the extent of the impact of any new laws, regulations or initiatives that may be proposed, or whether any of the proposals will become law. Compliance with any new laws or regulations could make compliance more difficult and expensive and affect the manner in which we conduct business.

The investment management industry is intensely competitive.

The investment management industry is intensely competitive, with competition based on a variety of factors, including investment performance, investment management fee rates, recent trend towards favor for passive investment products, continuity of investment professionals and client relationships, the quality of services provided to clients, corporate positioning and business reputation, continuity of selling arrangements with intermediaries and differentiated products. A number of factors, including the following, serve to increase our competitive risks:

• | some competitors, including those with passive investment products and exchange traded funds, charge lower fees for their investment services than we do; |

• | a number of our competitors have greater financial, technical, marketing and other resources, more comprehensive name recognition and more personnel than we do; |

14

• | potential competitors have a relatively low cost of entering the investment management industry; |

• | the recent trend toward consolidation in the investment management industry, and the securities business in general, has served to increase the size and strength of a number of our competitors; |

• | some investors may prefer to invest with an investment manager that is not publicly traded based on the perception that a publicly traded asset manager may focus on the manager’s own growth to the detriment of investment performance for clients; |

• | some competitors may invest according to different investment styles or in alternative asset classes that the markets may perceive as more attractive than the portfolios we offer; |

• | some competitors may have more attractive investment returns due to current market conditions; |

• | some competitors may operate in a different regulatory environment than we do, which may give them certain competitive advantages in the investment products and portfolio structures that they offer; and |

• | other industry participants, hedge funds and alternative asset managers may seek to recruit our investment professionals. |

If we are unable to compete effectively, our revenues could be reduced and our business could be adversely affected.

The investment management industry faces substantial litigation risks, which could adversely affect our business, financial condition or results of operations or cause significant reputational harm to us.