Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - Pendrell Corp | d74578dex232.htm |

| EX-31.2 - EX-31.2 - Pendrell Corp | d74578dex312.htm |

| EX-31.1 - EX-31.1 - Pendrell Corp | d74578dex311.htm |

| EX-10.25 - EX-10.25 - Pendrell Corp | d74578dex1025.htm |

| EX-23.1 - EX-23.1 - Pendrell Corp | d74578dex231.htm |

| EX-32.1 - EX-32.1 - Pendrell Corp | d74578dex321.htm |

| EX-21.1 - EX-21.1 - Pendrell Corp | d74578dex211.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2015 |

Or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-33008

PENDRELL CORPORATION

(Exact name of registrant as specified in its charter)

| Washington | 98-0221142 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

2300 Carillon Point, Kirkland, Washington 98033

(Address of principal executive offices including zip code)

(425) 278-7100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Class A common stock, par value $0.01 per share | The Nasdaq Global Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer, accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x.

As of June 30, 2015, the aggregate market value of common stock held by non-affiliates of the registrant was approximately $237,203,993

As of February 26, 2016, the registrant had 214,311,266 shares of Class A common stock and 53,660,000 shares of Class B common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Definitive Proxy Statement for its 2016 Annual Meeting of Shareholders are incorporated by reference in Part III of this Form 10-K.

Table of Contents

PENDRELL CORPORATION

2015 ANNUAL REPORT ON FORM 10-K

| Page | ||||||

| PART I. | ||||||

| Item 1. | 1 | |||||

| Item 1A. | 4 | |||||

| Item 1B. | 11 | |||||

| Item 2. | 11 | |||||

| Item 3. | 11 | |||||

| Item 4. | 13 | |||||

| PART II. | ||||||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 14 | ||||

| Item 6. | 16 | |||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

18 | ||||

| Item 7A. | 28 | |||||

| Item 8. | 29 | |||||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

58 | ||||

| Item 9A. | 58 | |||||

| Item 9B. | 60 | |||||

| PART III. | ||||||

| Item 10. | 60 | |||||

| Item 11. | 60 | |||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 60 | ||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence |

60 | ||||

| Item 14. | 60 | |||||

| PART IV. | ||||||

| Item 15. | 61 | |||||

| Signatures | 62 | |||||

Table of Contents

This Annual Report on Form 10-K (“Form 10-K”) contains certain forward-looking statements regarding future events and our future operating results that are subject to the safe harbors created under the Securities Act of 1933, as amended (“Securities Act”), and the Securities Exchange Act of 1934, as amended (“Exchange Act”). These statements may include words such as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “will,” “should,” “likely” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. All of these forward-looking statements are subject to risks and uncertainties that could cause our actual results to differ materially from those contemplated by the relevant forward-looking statements. Factors that might cause or contribute to such a difference include, but are not limited to, those discussed under “Item 1A of Part I – Risk Factors” and elsewhere in this Form 10-K. The forward-looking statements included in this document are made only as of the date of this report, and we undertake no obligation to publicly update these forward-looking statements to reflect subsequent events or circumstances.

| Item 1. | Business. |

Overview

Pendrell Corporation (“Pendrell”), with its consolidated subsidiaries, is referred to as “us,” “we,” or the “Company.” Pendrell has, for the past four years, invested in, acquired and monetized intellectual property (“IP”) rights. We are continuing our efforts to monetize our IP assets. We are also evaluating our IP investments to determine whether retention or disposition is appropriate. We no longer advise clients on IP strategies and transactions.

Pendrell was originally incorporated in 2000 as New ICO Global Communications (Holdings) Limited, a Delaware corporation. In July 2011, we changed our name to Pendrell Corporation. On November 14, 2012, we reincorporated from Delaware to Washington. Our principal executive office is located at 2300 Carillon Point, Kirkland, Washington 98033, and our telephone number is (425) 278-7100. Our website address is www.pendrell.com. The information contained in or that can be accessed through our website is not part of this Form 10-K.

Our Business

Revenue Generating Activities

We generate revenues by licensing and selling our IP rights to others. Prior to 2016, we also generated revenue by advising clients on various IP matters. Our subsidiaries hold patents that support four IP licensing programs that we own and manage: (i) digital media, (ii) digital cinema, (iii) wireless technologies, and (iv) memory and storage technologies.

Our digital media program is supported by patents and patent applications designed to protect against unauthorized duplication and use of digital content that is transferred from a source to one or more electronic devices. The majority of our digital media patents and patent applications came to us through our October 2011 purchase of a 90.1% interest in ContentGuard Holdings, Inc. (“ContentGuard”), where we partnered with Time Warner to expand the development and licensing of ContentGuard’s portfolio of digital rights management (“DRM”) technologies. Our digital media licensees include manufacturers, distributors and providers of consumer products, including Amazon, Casio Hitachi Mobile Communications, DirecTV, Fujitsu, LG Electronics, Microsoft Corporation, Nokia, Panasonic, Pantech, Sharp, Sony, Toshiba, Technicolor, S.A., Time Warner and Xerox Corporation. Other companies that manufacture, distribute or provide DRM-enabled consumer products and that we believe use ContentGuard’s innovations, including Apple, Google, HTC, Huawei, Motorola Mobility and Samsung (the “ContentGuard Defendants”), did not take a license to our digital media assets, which prompted us to file claims against them for patent infringement.

1

Table of Contents

Our digital cinema program is supported by patents and patent applications designed to protect against unauthorized creation, duplication and use of digital cinema content that is authored and distributed to movie theaters globally, many of which also came to us through our acquisition of ContentGuard. Potential digital cinema licensees include distributors and exhibitors of digital content, including motion picture producers, motion picture distributors and equipment vendors. We launched our digital cinema program in June 2013, and have engaged in licensing discussions with leading feature film studios.

Our wireless technologies program is supported by U.S. and foreign patents and patent applications, many of which enable key functionality in cellular and digital wireless devices and infrastructure. These patents and patent applications were developed by leading innovators in the wireless space, including Philips, IBM and ETRI, and cover key innovations in the cellular industry and digital wireless arena. Key technologies covered include 3G (e.g., W-CDMA, HSDPA, HSUPA), 4G (e.g., LTE, VoLTE), Bluetooth, Wi-Fi, and NFC technologies. Potential licensees include suppliers, manufacturers, distributors, and providers of wireless devices and infrastructure, including manufacturers and distributors of handsets, tablets, laptops, and other connected devices. We launched our wireless technologies program in Fall 2012, but have not yet generated material revenue through the program.

Our memory and storage technologies program is supported by patents and patent applications, the majority of which were acquired from Nokia Corporation in March 2013, of which 81 have been declared by Nokia to be essential to standards that are applicable to memory and storage technologies used in electronic devices. These patents cover embedded memory components and storage subsystems. Potential licensees include flash memory component suppliers, solid state disk manufacturers and device vendors. We commenced discussions with potential licensees in late 2013, and subsequently entered into two license agreements with leading technology companies in 2014 and another license with a leading technology company in early 2015.

We typically license our patents via agreements that cover entire patent portfolios or large segments of portfolios. We expect licensing negotiations with prospective licensees to take approximately 12 to 24 months, and perhaps longer, measured from inception of technical discussions regarding the scope of our patents. If we are unable to secure reasonable, negotiated licenses, we may resort to litigation to enforce our IP rights. For example, in late 2013 and early 2014, ContentGuard asserted infringement claims against the ContentGuard Defendants. Those claims resulted in two separate jury trials in the Eastern District of Texas during the fall of 2015. Both juries determined that the patents asserted by ContentGuard are valid, but both juries also concluded that the ContentGuard Defendants did not infringe the asserted patents. We are appealing both verdicts. However, as a result of the verdicts, we evaluated the financial statement carrying value of our entire IP portfolio. This evaluation resulted in an $82.3 million impairment of our IP, as well as a $21.2 million impairment of goodwill.

Our IP revenue generation activities are not limited to licensing and litigation. Patents that we believe may generate greater value through a sales transaction may be sold. Although our revenue may occur in different forms, we regard our IP monetization activities as integrated and not separate revenue streams.

Product Development Activities

In early 2015, we suspended further development of the Provitro™ proprietary micro-propagation technology and related laboratory processes that were designed to facilitate production on a commercial scale of certain plants, particularly timber bamboo. Near the end of 2015, we discontinued efforts to further develop ephemeral photo and messaging applications. Neither of these product initiatives generated revenue, and we are not currently pursuing any other product initiatives.

Business Outlook

From 2011 through 2015, we focused on acquiring and growing companies that developed or possessed unique, innovative technologies that could be licensed to third parties or could provide a competitive advantage

2

Table of Contents

to products we were developing. During 2015, we moderated those efforts and reduced our costs by eliminating certain positions, abandoning certain patent assets that do not support our existing licensing programs, and lowering facilities costs. We are continuing to reduce costs in 2016.

We have explored and continue to explore investment opportunities that are not premised on the value of IP, with the goal of investing our capital in operating companies that can generate solid, stable income streams. Due to high valuations that we attribute to inexpensive and widely available capital, we did not acquire any such operating companies in 2015. With the cost of capital rising in early 2016, we may encounter more suitable opportunities in 2016, and we therefore intend to increase our exploratory activity while keeping our costs contained.

Although our focus may evolve away from companies that develop or possess unique, innovative technologies, we will continue to dedicate effort and resources to generate revenue from our existing IP assets.

Competition

Due to the unique nature of our IP rights, we do not compete directly with other patent holders or patent applicants. However, to the extent that multiple parties seek royalties on the same product or service, we might as a practical matter compete for a share of reasonable royalties from manufacturers and distributors.

As we pursue opportunities that are not premised on the value of IP, we may compete with well-capitalized companies pursuing those same opportunities.

Divestiture of Satellite Assets

When we were formed in 2000, our intent was to develop and operate a next generation global mobile satellite communications system. In 2011, we started selling assets associated with the satellite business, including our interests in DBSD North America, Inc. and its subsidiaries (collectively referred to as “DBSD”) to DISH Network Corporation for $325 million, from which we recognized a gain of approximately $301 million associated with the disposition. During 2012, we divested the remaining vestiges of our satellite business, including the sale of our remaining medium earth orbit (“MEO”) satellites and related equipment and our real property in Brazil, the transfer to a liquidating trust (the “Liquidating Trust”) of certain former subsidiaries associated with the satellite business (the “International Subsidiaries”) to address the winding down of the International Subsidiaries, and the settlement of our litigation with The Boeing Company (“Boeing”).

The 2012 divestiture and the corresponding transfer to the Liquidating Trust of the International Subsidiaries triggered tax losses of approximately $2.4 billion, which we believe can be carried forward for up to twenty years. Under the sales agreement for the MEO assets, the Company is entitled to a substantial portion of any proceeds generated from the resale of the MEO assets. In January 2015, the party that acquired the MEO assets from the Company resold the MEO assets and as a result, the Company received $3.9 million during 2015, which has been recorded in gain on contingencies in the statement of operations for the year ended December 31, 2015. On February 23, 2016, the buyer received the final scheduled payment for the MEO assets, which will result in the Company’s recognition of an additional $2.0 million gain on contingency in the first quarter of 2016.

Employees

As of December 31, 2015, on a consolidated basis, we had the equivalent of 16 full-time employees located in Washington, California, Finland and Texas.

Available Information

The address of our website is www.pendrell.com. You can find additional information about us and our business on our website. We make available on this website, free of charge, our annual reports on Form 10-K,

3

Table of Contents

quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, as soon as reasonably practicable after we electronically file or furnish such materials to the Securities and Exchange Commission (“SEC”). You may read and copy this Form 10-K at the SEC’s public reference room at 100 F Street, NE, Washington, DC 20549-0102. Information on the operation of the public reference room can be obtained by calling the SEC at 1-800-SEC-0330. These filings are also accessible on the SEC’s website at www.sec.gov.

We also make available on our website in a printable format the charters for certain of our various Board of Director committees, including the Audit Committee, the Compensation Committee and the Nominating and Governance Committee, and our Code of Conduct and Ethics in addition to our Articles of Incorporation, Bylaws and Tax Benefits Preservation Plan. This information is available in print without charge to any shareholder who requests it by sending a request to Pendrell Corporation, 2300 Carillon Point, Kirkland, Washington 98033, Attn: Corporate Secretary. The material on our website is not incorporated into or part of this Form 10-K.

| Item 1A. | Risk Factors. |

The risks below address some of the factors that may affect our future operating results and financial performance. If any of the following risks develop into actual events, then our business, financial condition, results of operations or prospects could be materially adversely affected.

Risks Related to our Patents and Monetization Activities

Success of our licensing efforts depends on our ability to enter into new license agreements or otherwise enforce our intellectual property rights.

IP licensing revenues are dependent on our ability to enter into new license agreements with, or otherwise enforce our intellectual property rights against, users of our patented inventions. If users refuse to sign or renew license agreements, we may need to resort to litigation or other measures to compel the payment of fair consideration, which to date has not been effective, and may not be effective in the future. This risk applies not only to new license agreements, but to existing license agreements with fixed expiration dates. If we fail to sign or renew license agreements on terms that are favorable to us or obtain favorable outcomes through litigation or other enforcement actions, the value of our IP could be further impaired.

Revenue opportunities from our IP monetization efforts are limited.

Patents have finite lives. Our IP portfolio currently consists of patents that expire between 2016 and 2033. If we fail to develop or acquire new patentable inventions prior to the expiration of our patents, our IP revenue opportunities will be limited.

We may have a limited number of prospective licensees.

The patent portfolios that we own are applicable to only a limited number of prospective licensees. As such, if we are unable to enter into licenses with this limited group, licensing revenue will be adversely impacted. For instance, if the trial results in the Google Litigation and Apple Litigation (as such terms are defined below in Item 3 of Part I) are affirmed on appeal, there will be very few mobile device manufacturers that have not either signed a license with ContentGuard or otherwise resolved ContentGuard’s claims against them.

Our licensing cycle is lengthy, and our licensing efforts may be unsuccessful.

The process of licensing to customers can be lengthy, sometimes spanning a number of years. We have incurred and expect to incur significant legal and sales expenses prior to entering into license agreements and generating license revenues. We also expect to spend considerable resources educating prospective licensees on

4

Table of Contents

the benefits of a license arrangement with us. As such, we may incur significant losses in any particular period before any associated revenue is generated. Moreover, if our portfolio is not demonstrably applicable to prospective licensees’ products or services, whether due to poor quality, lack of breadth or otherwise, parties may refuse to enter into license agreements.

Enforcement proceedings may be costly and ineffective and could lead to impairment of our IP assets.

We may choose to pursue litigation or other enforcement action to protect our intellectual property rights, such as the Apple Litigation and Google Litigation. Enforcement proceedings are typically protracted and complex, and might require cooperation of inventors and others who are unwilling or unable to assist with enforcement. Litigation also involves several stages, including the potential for a prolonged appeals process. The costs are typically substantial, and the outcomes are unpredictable. As occurred during our fourth quarter in 2015, we might receive rulings or judgments, or enter into licenses or settlement agreements, that compel us to revalue the IP assets that we are enforcing, which in turn might result in a reduction to the financial statement carrying value of such assets through a corresponding impairment charge. Enforcement actions will likely divert our managerial, technical, legal and financial resources from business operations. In certain cases, we may conclude that these costs and risks outweigh the potential benefits that would arise from successful enforcement, in which event we may opt not to pursue enforcement.

Our business could be negatively impacted by product composition and future innovation.

Our licensing revenues have been generated from manufacturers and distributors of products that use our patented inventions. Our business prospects could be negatively impacted if prospective licensees do not use our inventions in their products, or if they later modify their products to eliminate use of our inventions. Moreover, changes in technology or customer requirements could alter product composition and render our patented inventions obsolete or unmarketable.

Our staff reductions could harm our IP monetization efforts.

As we continue to explore investment opportunities that are not premised on the value of IP, we have significantly reduced our IP licensing and legal staff. The smaller staff might be less capable of pursuing and concluding IP license transactions. Even if our remaining team effectively pursues IP license transactions, certain users of our patented inventions might conclude that we will be less diligent in protecting our rights, and therefore may be reluctant to engage in licensing discussions. This in turn might render enforcement of our rights more time-consuming and costly.

Challenges to the validity or enforceability of our key patents could significantly harm our business.

Our assets include patents that are integral to our business and revenues. Prospective licensees or competitors may challenge the validity, scope, enforceability and ownership of our patents. Their challenges may include review requests in the relevant patent and trademark office, such as the inter partes review and covered business method proceedings initiated by ZTE, Apple and Google. Review proceedings are costly and time-consuming, and we cannot predict their outcome or consequences. Such proceedings may narrow the scope of our claims or may cancel some or all of our claims. If some or all of our patent claims are canceled, we could be prevented from enforcing or earning future revenues from such patents. Even if our claims are not canceled, enforcement actions against alleged infringers may be stayed pending resolution of reviews, or courts or tribunals reviewing our patent claims could make findings adverse to our interests based on facts presented in review proceedings. Irrespective of outcome, review challenges may result in substantial legal expenses and diversion of management’s time and attention away from our other business operations, including our ability to evaluate and acquire other businesses. Adverse decisions could impair the value of our inventions or result in a loss of our proprietary rights and may adversely affect our results of operations and our financial position.

5

Table of Contents

Changes in patent law could adversely impact our business.

Patent laws may continue to change, and may alter protections afforded to owners of patent rights, impose additional enforcement risks, increase the costs of enforcement, or increase our licensing cycles. For instance, during 2013 and 2015, legislative initiatives were introduced to address perceived patent abuses by non-practicing entities. Even if legislative initiatives do not directly impact our business, such initiatives might encourage manufacturers to infringe our IP rights, lengthen our licensing cycles, increase the likelihood that we will litigate to enforce our IP rights, or make it more difficult and expensive to license our patents or enforce our patents against parties using our inventions without a license. Moreover, increased focus on the growing number of patent-related lawsuits may result in legislative changes which increase our costs and related risks of asserting patent enforcement actions.

Changes of interpretations of patent law could adversely impact our business.

Our success in review and enforcement proceedings relies in part on the historically consistent application of patent laws and regulations. Interpretations of patent laws and regulations by the courts and applicable regulatory bodies have evolved, and may continue to evolve, particularly with the introduction of new laws and regulations. Changes or potential changes in judicial interpretation could have a negative impact on our ability to monetize our patent rights.

Risks Related to our Acquisition Activities

We may over-estimate the value of assets or businesses we acquire.

We make investments from which we intend to generate a return. We estimate the value of these investments prior to acquisition, using both objective and subjective methodologies. If we over-estimate such value, we may not generate desired returns on our investment, or we may need to adjust the value of the investments to fair value and record a corresponding impairment charge, either of which could adversely affect our results of operations and our financial position.

We may not capitalize on acquired assets.

Even if we accurately value the investments we make, we must succeed in generating a return on the investments. Our success in generating a return depends on effective efforts of our employees and outside professionals. If we do not generate desired returns on our investments or if we are compelled to adjust the value of the investments to fair value and record a corresponding impairment charge, it could adversely affect our results of operations and our financial position.

We may pursue other acquisition or investment opportunities that do not yield desired results.

We intend to continue investigating potential acquisitions that support our business objectives and strategy. Acquisitions are time-consuming, complex and costly. The terms of acquisition agreements tend to be heavily negotiated. As a result, we may incur significant transactional expenses, regardless of whether or not acquisitions are consummated. Moreover, the integration of acquired companies prompts significant challenges, and we can provide no assurances that the integration of acquired businesses with our business will result in the realization of the full benefits we anticipate from such acquisitions. Investigating businesses and assets and integrating newly acquired businesses or assets may be costly and time-consuming, and such activities could divert our attention from other business concerns. In addition, we might lose key employees while integrating new organizations. Acquisitions could also result in potentially dilutive issuances of equity securities or the incurrence of debt, the assumption or incurrence of contingent liabilities, possible impairment charges related to goodwill or other intangible assets or other unanticipated events or circumstances, any of which could negatively impact our financial position. We might not be successful in integrating acquired businesses and might not achieve desired revenues and cost benefits.

6

Table of Contents

The financing of our acquisition activities could threaten our ability to use NOLs to offset future taxable income.

We have substantial historical net operating losses (“NOLs”) for United States federal income tax purposes. As explained in greater detail below, our use of our NOLs will be significantly limited if we undergo a “Tax Ownership Change,” as defined in Section 382 of the Internal Revenue Code. If and to the extent we finance acquisitions through the sale or issuance of stock, we will likely cause an ownership shift that increases the possibility that a future Tax Ownership Change might occur. If a Tax Ownership Change occurs, we will be permanently unable to use most of our NOLs.

We rely on representations, warranties and opinions from third parties that might not be accurate.

When we acquire assets or businesses or establish relationships with inventors or strategic partners, we may rely on representations and warranties made by third parties. We also may rely on opinions of lawyers and other professionals. We may not have the opportunity to independently investigate and verify the facts upon which such representations, warranties and opinions are made. By relying on these representations, warranties and opinions, we may be exposed to unforeseen liabilities that could have a material adverse effect on our operating results and financial condition.

Risks Related to our Operations

Our financial and operating results have been and may continue to be uneven.

Our operating results may fluctuate and, as such, our operating results are difficult to predict. You should not rely on quarterly or annual comparisons of our results of operations as an indication of our future performance. Factors that could cause our operating results to fluctuate during any period or that could adversely affect our operating results include the timing of license and sales agreements, compliance with such agreements, the terms and conditions for payment under those agreements, our ability to protect and enforce our intellectual property rights, costs of enforcement, changes in demand for products that incorporate our inventions, the time period between commencement and completion of license negotiations or enforcement proceedings, revenue recognition principles, and changes in accounting policies.

Our revenues have not and may not offset our operating expenses.

Through the first quarter of 2015, we acquired IP assets and expanded the reach and scope of our IP business. We also incurred expenses to hire new personnel, including employees for IP services, patent research and analysis, development of reporting systems and general and administrative functions and to pay legal fees for IP enforcement activities. As a result, our costs exceeded our revenues, and although we substantially scaled back our expansion efforts and our costs in 2015, we anticipate that costs may continue to exceed revenues. If we are not successful in generating revenue that is sufficient to offset our expenses, our financial position will be negatively impacted.

Failure to effectively manage the composition of our employee base could strain our business.

Our success depends, in large part, on continued contributions of our key managers and employees, many of whom are highly skilled and would be difficult to replace. Our success also depends on the ability of our personnel to function effectively, both individually and as a group. Recently, we terminated the employment of certain individuals (including IP consultants) whose roles we believe were unnecessary to advance our current and anticipated business strategies. If we misjudged our ongoing personnel needs or lose any of our remaining senior managers or key personnel, it could lead to dissatisfaction among our clients or licensees, which could slow our growth or result in a loss of business. Moreover, if we fail to manage the composition of our employee base effectively or otherwise strain our relationships with our personnel, our business and financial results may be materially harmed.

7

Table of Contents

If we need financing and cannot obtain financing on favorable terms, our business may suffer.

We have relied on revenues from clients and licensees and existing cash reserves to finance our operations. If we deploy a significant portion of our capital or encounter unforeseen difficulties in the future that deplete our capital resources more rapidly than anticipated, we may need to obtain additional financing. Financing might not be available on favorable terms, if at all, may dilute our existing shareholders, and may prompt us to pursue structural changes that could impact shareholder concentration and liquidity. If we fail to obtain additional capital as and when needed, such failure could have a material adverse impact on our business, results of operations and financial condition.

Future changes in standards, rules, practices or interpretation may impact our financial results.

We prepare our consolidated financial statements in accordance with accounting principles generally accepted in the United States of America. These principles are subject to interpretations by the SEC and various accounting bodies. In addition, we are subject to various taxation rules in many jurisdictions. The existing taxation rules are generally complex, voluminous, frequently changing and often ambiguous. Changes to existing taxation rules, changes to the financial accounting standards, or any changes to the interpretations of these standards or rules, or changes in practices under these standards and rules, may adversely affect our reported financial results or the way we conduct our business.

Unauthorized use or disclosure of our confidential information could adversely affect our business.

We rely primarily on a combination of license agreements, nondisclosure agreements, other contractual relationships and patent, trademark, trade secret and copyright laws to protect our confidential and proprietary information, our technology and our intellectual property. We cannot be certain that these protections have not been and will not be breached, that we will be able to timely detect unauthorized use or transfer of our trade secrets or intellectual property, that we will have adequate remedies for any breach, or that our trade secrets will not otherwise become known or be independently discovered by competitors. If we are unable to detect in a timely manner the unauthorized use or disclosure of our proprietary or other confidential information or if we are unable to enforce our rights under our agreements or applicable laws, the misappropriation of such information could harm our business.

Our company has an evolving business model, which raises doubt about our ability to increase our revenues and grow our business.

We have recently shifted our principal focus away from the IP business and are evaluating opportunities that provide more reliable cash flow with greater growth potential. As a result of our evolving business model, our opportunities must be considered in light of the risks, expenses, and difficulties frequently encountered by companies in an early stage of development. We may not be successful in addressing such risks, and the failure to do so could have a material adverse effect on our business, operating results and financial condition. There can be no assurance that we will be able to increase our revenues and otherwise grow our business as we execute on new business opportunities in the future.

Risks Related to our Tax Losses

We cannot be certain that our tax losses will be available to offset future taxable income.

A significant portion of our NOLs were triggered when we disposed of our satellite assets. We believe these NOLs can be carried forward to offset certain future taxable income. However, the NOLs have not been audited or otherwise validated by the Internal Revenue Service (“IRS”). We cannot assure you that we would prevail if the IRS were to challenge the amount or our use of the NOLs. If the IRS were successful in challenging our NOLs, all or some amount of our NOLs would not be available to offset future taxable income which would result in an increase to our future income tax liability. The NOL carryforward period begins to expire in 2025

8

Table of Contents

with the bulk of our NOLs expiring in 2032. If the tax laws are amended to limit or eliminate our ability to carry forward our NOLs for any reason, or to lower income tax rates, the value of our NOLs may be significantly reduced.

An Ownership Change under Section 382 of the Internal Revenue Code may significantly limit our ability to use NOLs to offset future taxable income.

Our use of our NOLs will be significantly limited if we undergo a Tax Ownership Change. Broadly, a Tax Ownership Change will occur if, over a three-year testing period, the percentage of our stock, by value, owned by one or more 5% shareholder increases by more than 50 percentage points. For purposes of this test, shareholders that own less than 5% of our stock are aggregated into one or more separate “public groups,” each of which is treated as a 5% shareholder. In general, shares traded within a public group are not included in the Tax Ownership Change test. Despite our adoption of certain protections against a Tax Ownership Change (such as our Tax Benefits Preservation Plan), we cannot control the trading activity of our significant shareholders. If shareholders acquire or divest their shares in a manner or at times that do not account for the loss-limiting provisions of the Internal Revenue Code or regulations adopted thereunder, a Tax Ownership Change could occur. If a Tax Ownership Change occurs, we will be permanently unable to use most of our NOLs.

Our NOLs cannot be used to offset the Personal Holding Company tax.

The Internal Revenue Code imposes an additional tax on the undistributed income of a Personal Holding Company (“PHC”). In general, a corporation is classified as a PHC if 50% or more of its outstanding shares, measured by value, are owned directly or indirectly by five or fewer individual shareholders at any time during the second half of a calendar year (“Concentrated Ownership”) and at least 60% of its adjusted ordinary gross income is Personal Holding Company Income (“PHCI”). Broadly, PHCI includes items such as dividends, interest, rents and royalties, among others. Pendrell or ContentGuard may meet the Concentrated Ownership test in 2016. Also, it is possible that action or inaction by our significant shareholders or by Time Warner (the 10% owner of ContentGuard) could cause Pendrell or ContentGuard to meet the Concentrated Ownership test. If Pendrell or ContentGuard meet the Concentrated Ownership test and generate positive net PHCI, Pendrell or ContentGuard will be subject to the PHC tax on undistributed net PHCI. The PHC tax, which is in addition to the income tax, is currently levied at 20% of the net PHCI not distributed to the corporation’s shareholders.

Our NOLs cannot be used to completely offset the Alternative Minimum Tax or other taxes.

We may also be subject to the corporate Alternative Minimum Tax (“AMT”) in a year in which we have net taxable income because the AMT cannot be completely offset by available NOLs, as losses carried forward generally can offset no more than 90% of a corporation’s AMT liability. In addition, our federal NOLs will not shield us from foreign withholding taxes, state and local income taxes, or revenue-based taxes incurred in jurisdictions that impose such taxes.

Our ability to utilize our NOLs is dependent on the generation of future taxable income.

Our ability to utilize our NOLs is dependent upon the generation of future taxable income before the expiration of the carry forward period attributable to the NOLs, which begin to expire in 2025. We did not generate taxable income in 2013, 2014 or 2015, and we may not generate sufficient taxable income in future years to use the NOLs before they begin expiring.

Risks Related to Our Class A Common Stock

If we are delisted from Nasdaq, our ability to access the capital markets could be negatively impacted.

Our common stock is listed for trading on the Nasdaq Global Select Market (“Nasdaq”). We must satisfy Nasdaq’s continued listing requirements, including, among other things, Listing Rule 5450(a)(1) (the “Listing

9

Table of Contents

Rule”), which requires listed companies to maintain a minimum closing bid price of $1.00 per share. On September 24, 2015, the closing bid price of our Class A Common Stock fell below $1.00 and has remained below $1.00. On November 5, 2015, Nasdaq notified us that we do not comply with the Listing Rule and that we have 180 days to comply with the Listing Rule. We may regain compliance if the price of our Class A Common Stock closes at $1.00 per share or more for a minimum of 10 consecutive business days at any time during the 180 day cure period. If we fail to comply with the Listing Rule within that time period, and fail to extend the compliance time period, Nasdaq may delist our stock, in which case our stock (i) may be more thinly traded, making it more difficult for our shareholders to sell shares, (ii) may experience greater price volatility, and (iii) may not attract analyst coverage, all of which may result in a lower stock price. In addition, delisting could harm our ability to raise capital through financing sources on terms acceptable to us, or at all, and result in the potential loss of confidence by investors, increased employee turnover, and fewer business development opportunities.

If we remedy our Class A common stock price deficiency with a reverse stock split, our Class A common stock price might decrease.

In order to regain compliance with the Listing Rule, we may need to implement a reverse stock split. A reverse stock split could decrease the trading volume in our Class A common stock, which could cause the price of the Class A common stock to decrease following the reverse stock split.

Future sales of our Class A common stock could depress the market price.

The average trading volume of our Class A common stock is low in relation to the number of outstanding shares of Class A common stock. As a result, the market price of our Class A common stock could decline as a result of sales of a large number of shares. These sales might also make it more difficult for us to sell shares in the future at a time and price that we deem appropriate.

A sale of a large number of shares by our largest shareholders could depress the market price of our Class A common stock.

A small number of our shareholders hold a majority of our Class A common stock and our Class B common stock, which is convertible at the option of the holders into Class A common stock. The sale or prospect of the sale of a substantial number of these shares could have an adverse effect on the market price of our Class A common stock.

The interests of our controlling shareholder may conflict with the interests of other Class A holders.

Eagle River Satellite Holdings, LLC, together with its affiliates Eagle River Investments, LLC, Eagle River, Inc. and Eagle River Partners, LLC (collectively, “Eagle River”) controls approximately 65% of the voting power of our outstanding capital stock. As a result, Eagle River has control over the outcome of matters requiring shareholder approval, including the election of directors, amendments to our governing documents, the adoption or prevention of mergers, consolidations or sales of all or substantially all of our assets, or control changes. Eagle River is not restricted or prohibited from competing with us.

We are a “controlled company” within the meaning of the Nasdaq Marketplace Rules and, as a result, will qualify for, and may rely on, exemptions from certain corporate governance requirements.

Eagle River controls approximately 65% of the voting power of our outstanding capital stock. As a result, we are a “controlled company” within the meaning of the Nasdaq corporate governance standards, and therefore may elect not to comply with certain Nasdaq corporate governance requirements, including (i) the requirement that a majority of the board of directors consist of independent directors, (ii) the requirement that the compensation of officers be determined, or recommended to the board of directors for determination, by a majority of the independent directors or a compensation committee comprised solely of independent directors,

10

Table of Contents

and (iii) the requirement that director nominees be selected, or recommended for the board of directors’ selection, by a majority of the independent directors or a nominating committee comprised solely of independent directors with a written charter or board resolution addressing the nomination process. We do not currently rely on any of these exemptions, but reserve the right to do so in the future. If we choose to do so, our shareholders may not have the same protections afforded to shareholders of companies that are subject to all of the Nasdaq corporate governance requirements.

Our Tax Benefits Preservation Plan (“Tax Benefits Plan”), as well as certain provisions in our restated articles of incorporation, may discourage takeovers, which could affect the rights of holders of our Class A common stock.

Our Tax Benefits Plan is intended to act as a deterrent against any person or group acquiring or otherwise obtaining beneficial ownership of more than 4.9% of our securities without the approval of our board of directors. In addition, our articles of incorporation require us to take all necessary and appropriate action to protect certain rights of our common shareholders, including voting, dividend and conversion rights and rights in the event of a liquidation, merger, consolidation or sale of substantially all of our assets. Our articles of incorporation also provide that we will not avoid or seek to avoid the observance or performance of those rights by charter amendment, entry into an inconsistent agreement or reorganization, recapitalization, transfer of assets, consolidation, merger, dissolution or the issuance or sale of securities. The rights protected by these provisions of the articles of incorporation include our Class B common shareholders’ right to ten votes per share on matters submitted to a vote of our shareholders and option to convert each share of Class B common stock into one share of Class A common stock. The provisions of the Tax Benefits Plan and our articles of incorporation could discourage takeovers of our company, which could adversely affect the rights of our shareholders.

| Item 1B. | Unresolved Staff Comments. |

None.

| Item 2. | Properties. |

Our corporate headquarters are located in Kirkland, Washington, where we lease 8,050 square feet in Kirkland under a lease which expires on July 31, 2019. We currently sublease 2,882 square feet of that space and occupy the remaining 5,198 square feet.

Additionally, we have a lease for 2,995 square feet of office space in Plano, Texas which expires December 31, 2018.

We believe our facilities are adequate for our current business and operations.

| Item 3. | Legal Proceedings. |

ContentGuard Enforcement Actions—On December 18, 2013, ContentGuard filed a patent infringement lawsuit against Amazon.com, Inc., Apple Inc., Huawei Device USA, Inc. and Motorola Mobility LLC in the Eastern District of Texas (“EDTX”), in which ContentGuard alleged that these entities infringed and continue to infringe nine of its patents by making, using, selling or offering for sale certain mobile communication and computing devices (the “Apple Litigation”). On January 17, 2014, ContentGuard filed an amended complaint in the Apple Litigation adding certain affiliates of the original defendants, along with HTC Corporation, HTC America Inc., Samsung Electronics Co., Ltd., Samsung Electronics America, Inc. and Samsung Telecommunications America, LLC (collectively, “Samsung”). On January 31, 2014, Google Inc. (“Google”) filed a declaratory judgment suit in the Northern District of California alleging that Google does not infringe the nine patents asserted in the Apple Litigation. On February 5, 2014, ContentGuard filed a patent infringement action in the EDTX against Google, in which ContentGuard alleged that Google has infringed and continues to

11

Table of Contents

infringe the same nine patents (the “Google Litigation”). From and after April 2014, the presiding judge in the EDTX has administered the cases in parallel.

Amazon Settlement. In August 2015, ContentGuard settled its claims against Amazon by granting to Amazon a license to use the ContentGuard patents. In connection with the settlement, ContentGuard released Amazon from the Apple Litigation. The settlement and license with Amazon is not impacted by the adverse jury findings in the Apple Litigation and Google Litigation that are described below.

DirecTV Settlement. In August 2014, DirecTV intervened in the Apple Litigation and thereby became an additional defendant, against whom ContentGuard asserted additional infringement claims. In January 2016, ContentGuard settled its claims against DirecTV by granting to DirecTV a license to use the ContentGuard patents. In connection with the settlement, ContentGuard released DirecTV from the Apple Litigation. The settlement and license with DirecTV is not impacted by the adverse jury findings in the Apple Litigation and Google Litigation that are described below.

Google and Samsung Verdict. On September 23, 2015, a jury in the Google Litigation found that the patents asserted against Google and Samsung in the Apple Litigation and Google Litigation are valid, but that Samsung products and Google products accused in the litigation do not infringe the patents. The judge entered judgment consistent with the verdict on October 13, 2015. The non-infringement decision, if not reversed or overturned in post-trial practice or on appeal, applies to all defendants in the Google Litigation and Apple Litigation that manufacture, sell or distribute Android devices that run Google Play services. If the verdict and judgment are not overturned, we will be liable for approximately $0.5 million of court costs and expenses incurred by Google and Samsung in the defense of the Google Litigation.

Apple Verdict. On November 20, 2015, a jury in the Apple Litigation found that the patents asserted against Apple in the Apple Litigation are valid, but that Apple products accused in the litigation do not infringe the patents. The judge entered judgment consistent with the verdict in December 2015. If the verdict and judgment are not overturned, we will be liable for approximately $0.5 million of court costs and expenses incurred by Apple in the defense of the Apple Litigation.

Post-Trial Activities. ContentGuard is challenging the juries’ findings in the Google Litigation and Apple Litigation through motions for judgment as a matter of law (the “JMOL Motions”). The JMOL Motions will be reviewed and resolved by the presiding judge from the Google Litigation and Apple Litigation. If the JMOL Motions are unsuccessful, we intend to appeal the jury verdicts to the federal circuit court. We cannot predict the outcome of any post-trial activities in the Google Litigation or Apple Litigation.

IPR and CBM Petitions filed by Apple and Google—In December 2014, Apple filed with the USPTO twenty-nine inter partes review (“IPR”) petitions and three covered business method (“CBM”) petitions, through which Apple challenged the validity of all nine patents asserted in the Apple Litigation. Also in December 2014, Google filed three CBM petitions, challenging the validity of three of the nine asserted patents. Between March and July 2015, all of Apple’s IPR and CBM petitions were terminated or withdrawn. All but one of Google’s petitions were also terminated or withdrawn, leaving just one Google CBM petition, relating to patent number 7,774,280, that proceeded to trial before the USPTO’s Patent Trial and Appeal Board (“PTAB”). The trial took place on February 24, 2016, and we are waiting for the PTAB to issue its findings.

ZTE IPRs —In early 2012, ContentGuard and its subsidiaries filed lawsuits in United States and German courts, alleging that ZTE Corporation, ZTE (USA) Inc. and ZTE Deutschland GmbH (collectively “ZTE”) infringed and continue to infringe ContentGuard patents by making, using, selling or offering for sale certain mobile communication and computing devices. ZTE subsequently filed IPR petitions with the USPTO, challenging the validity of six U.S. patents asserted by ContentGuard against ZTE. The PTAB terminated proceedings with respect to two patents, both of which emerged with valid patent claims. ZTE’s claims against

12

Table of Contents

the other four patents went to trial. Following trial, the PTAB rejected ZTE’s remaining challenges, and confirmed the validity of all claims in the four patents. ZTE’s time for appeal expired with no appeals filed. Apple then challenged the same four patents in new IPRs, as described in the paragraph above, which the PTAB rejected. As a result, the favorable decisions of the PTAB, as against ZTE’s and Apple’s petitions, are final.

ZTE Enforcement Actions—In response to the claims filed against ZTE in Germany, in which ContentGuard Europe GmbH alleged infringement of three European patents, ZTE filed a nullity action against two of the patents and an opposition proceeding against the third patent. ZTE prevailed in the opposition proceeding, resulting in the revocation of one European patent, which ContentGuard has appealed. The infringement and nullity proceedings in Germany, along with all U.S. court actions, were “put to rest” or stayed as the result of a standstill agreement signed by ContentGuard and ZTE in December 2013. The standstill agreement has been extended through the end of the post-trial motion phase of the Google Litigation.

J&J Collection — In November 2012, we obtained an arbitration judgment in the U.K. against Jay and Jayendra (Pty), a South African corporation (“J&J Group”) for approximately $4.0 million. J&J Group submitted multiple appeals to the U.K. courts, the last of which was rejected in July 2013. In December 2014, we obtained an enforcement judgment against J&J Group from a South African court, and commenced collection efforts. In November 2015, we entered into a settlement agreement with the J&J Group whereby we received approximately $1.6 million, net of collection costs, in full and final settlement of all claims against the J&J Group. As a result, we recorded a gain of $1.6 million for the year ended December 31, 2015, which is included in gain on contingencies in the consolidated statements of operations.

| Item 4. | Mine Safety Disclosures. |

Not Applicable.

13

Table of Contents

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Market for Our Class A Common Stock

Our Class A common stock trades on the Nasdaq Global Select Market (“Nasdaq”) under the symbol “PCO.”

The table below sets forth the high and low sales prices of our Class A common stock in U.S. dollars for each of the periods presented. Stock prices represent amounts published on the Nasdaq Global Select Market. As of February 26, 2016, the closing sales price of our Class A common stock was $0.5713 per share.

| 2015 | 2014 | |||||||||||||||

| Period |

High | Low | High | Low | ||||||||||||

| First Quarter |

$ | 1.36 | $ | 0.99 | $ | 1.91 | $ | 1.34 | ||||||||

| Second Quarter |

$ | 1.45 | $ | 0.96 | $ | 1.85 | $ | 1.39 | ||||||||

| Third Quarter |

$ | 1.61 | $ | 0.72 | $ | 1.84 | $ | 1.31 | ||||||||

| Fourth Quarter |

$ | 0.80 | $ | 0.50 | $ | 1.67 | $ | 1.26 | ||||||||

As a result of our listing on Nasdaq, we must satisfy Nasdaq’s continued listing requirements, including, among other things, Listing Rule 5450(a)(1) (the “Listing Rule”), which requires listed companies to maintain a minimum closing bid price of $1.00 per share. On September 24, 2015, the closing bid price of our Class A Common Stock fell below $1.00 and has remained below $1.00. On November 5, 2015, we received written notice from the Listing Qualifications Department of Nasdaq stating that we are not currently in compliance with the Listing Rule based on the closing bid price of the Company’s Class A common stock for the 30 consecutive business days from September 24, 2015 to November 4, 2015. The notification does not result in the immediate delisting of our Class A common stock and our Class A common stock will continue to trade on the Nasdaq Global Market. Nasdaq has provided the Company a 180 calendar day period, or until May 3, 2016, to regain compliance with the minimum bid price requirement. To regain compliance, our Class A common stock must maintain a closing bid price of at least $1.00 per share for a minimum of ten consecutive business days during the 180-day compliance period.

As of February 26, 2016, there were approximately 390 record holders of our Class A common stock.

Market for Our Class B Common Stock

There is no established trading market for our Class B common stock, of which we have 53,660,000 shares outstanding with two holders of record. Each share of Class B common stock is convertible at any time at the option of its holder into one share of Class A common stock.

Dividends

We have never paid a cash dividend on shares of our equity securities. Unless we become subject to personal holding company tax, we do not intend to pay any cash dividends on our common shares during the foreseeable future. It is anticipated that future earnings, if any, from our operations will be used to finance growth.

Unregistered Sales of Equity Securities and Use of Proceeds

On December 31, 2015, we redeemed 92,500 shares of our Class A common stock as partial consideration for the sale of the Ovidian Group, LLC (“Ovidian”). The closing sales price of our Class A common stock on December 31, 2015, was $0.5011 per share.

14

Table of Contents

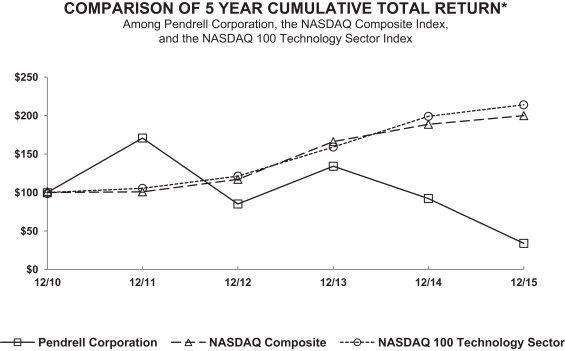

Performance Measurement Comparison

The following graph shows the total shareholder return as of the dates indicated of an investment of $100 in cash on December 31, 2010 for: (i) our Class A common stock; (ii) the Nasdaq Composite Index; and (iii) the Nasdaq 100 Technology Sector Index.

The stock price performance graph below is not necessarily indicative of future performance.

| *$100 invested on 12/31/10 in stock or index, including reinvestment of dividends. |

| Fiscal year ending December 31. |

| 12/10 | 12/11 | 12/12 | 12/13 | 12/14 | 12/15 | |||||||||||||||||||

| Pendrell Corporation |

100.00 | 170.67 | 84.67 | 134.00 | 92.00 | 33.41 | ||||||||||||||||||

| NASDAQ Composite |

100.00 | 100.53 | 116.92 | 166.19 | 188.78 | 199.95 | ||||||||||||||||||

| NASDAQ 100 Technology Sector |

100.00 | 105.21 | 121.15 | 158.80 | 198.87 | 213.99 | ||||||||||||||||||

15

Table of Contents

| Item 6. | Selected Financial Data. |

The following selected consolidated financial data should be read in conjunction with “Item 7— Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and accompanying notes included in this Form 10-K.

| Year Ended December 31, | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||||||

| Revenue(1) |

$ | 43,519 | $ | 42,534 | $ | 13,128 | $ | 33,775 | $ | 2,637 | ||||||||||

| Operating expenses: |

||||||||||||||||||||

| Cost of revenues(2) |

10,215 | 14,170 | 7,872 | 314 | — | |||||||||||||||

| Patent administration and related costs(2) |

2,668 | 6,386 | 4,405 | 3,655 | 193 | |||||||||||||||

| Patent litigation(2) |

13,076 | 9,880 | 4,564 | 2,538 | — | |||||||||||||||

| General and administrative(2) |

16,750 | 27,467 | 25,939 | 29,844 | 21,822 | |||||||||||||||

| Stock-based compensation |

4,507 | 9,405 | 12,345 | 8,597 | 5,369 | |||||||||||||||

| Amortization of intangibles |

13,939 | 15,929 | 15,864 | 13,471 | 1,986 | |||||||||||||||

| Impairment of intangibles and goodwill(3) |

103,499 | 11,013 | — | — | — | |||||||||||||||

| Gain on contract settlements(4) |

— | — | — | — | (4,735 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating expenses, net |

164,654 | 94,250 | 70,989 | 58,419 | 24,635 | |||||||||||||||

| Operating loss |

(121,135 | ) | (51,716 | ) | (57,861 | ) | (24,644 | ) | (21,998 | ) | ||||||||||

| Net interest income (expense)(5) |

103 | (99 | ) | (64 | ) | (2,245 | ) | (4,450 | ) | |||||||||||

| Gain on deconsolidation of subsidiaries(6) |

— | — | — | 48,685 | — | |||||||||||||||

| Gain on settlement of Boeing litigation(7) |

— | — | — | 10,000 | — | |||||||||||||||

| Gain associated with disposition of assets(8) |

— | — | — | 5,599 | 300,886 | |||||||||||||||

| Gain on Contingencies (9) |

6,095 | — | — | — | — | |||||||||||||||

| Other income (expense) |

(14 | ) | (16 | ) | (55 | ) | 1,588 | 1,223 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before income taxes |

(114,951 | ) | (51,831 | ) | (57,980 | ) | 38,983 | 275,661 | ||||||||||||

| Income tax benefit (expense)(10) |

(2,631 | ) | (6,303 | ) | — | 1,034 | 42,925 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

(117,582 | ) | (58,134 | ) | (57,980 | ) | 40,017 | 318,586 | ||||||||||||

| Net loss attributable to noncontrolling interest |

(7,902 | ) | (7,132 | ) | (2,918 | ) | (67 | ) | (274 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) attributable to Pendrell |

$ | (109,680 | ) | $ | (51,002 | ) | $ | (55,062 | ) | $ | 40,084 | $ | 318,860 | |||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Basic income (loss) per share attributable to Pendrell |

$ | (0.41 | ) | $ | (0.19 | ) | $ | (0.21 | ) | $ | 0.16 | $ | 1.26 | |||||||

| Diluted income (loss) per share attributable to Pendrell |

$ | (0.41 | ) | $ | (0.19 | ) | $ | (0.21 | ) | $ | 0.15 | $ | 1.23 | |||||||

| Total assets |

$ | 180,892 | $ | 304,104 | $ | 351,994 | $ | 381,415 | $ | 435,047 | ||||||||||

| Long-term obligations, including current portion of capital lease obligations(11) |

— | $ | 1,521 | $ | 6,695 | $ | 2,241 | $ | 76,406 | |||||||||||

| (1) | Prior to the acquisition of Ovidian and ContentGuard during the year ended December 31, 2011, we were a development stage enterprise and did not generate any revenue from operations. |

| (2) | Certain prior period amounts have been reclassified to conform to the current year presentation of expenses in our consolidated statements of operations, including the presentation of “cost of revenues” and “patent litigation” as separate captions; as such costs were previously included in “patent administration, litigation and related costs” and “general and administrative” in 2013 and prior years. |

| (3) | During the fourth quarter of the year ended December 31, 2015, we recorded a non-cash impairment charge of $103.5 million related to our patents, other intangible assets and goodwill. During the fourth quarter of the year ended December 31, 2014, we recorded a non-cash impairment charge of $11.0 million related to Provitro’s goodwill and proprietary micro-propagation technology. |

| (4) | During the year ended December 31, 2011, we recognized a $4.7 million gain associated with a reduction of our estimated liability for gateway obligations as a result of our agreement to purchase Deutsche Telekom AG’s claim against one of our subsidiaries. |

16

Table of Contents

| (5) | Prior to 2013, certain of our subsidiaries had agreements with operators of gateways for our MEO satellite system, some of which were capital leases. We continued to accrue expenses according to our subsidiaries’ contractual obligations until the liabilities were transferred to the Liquidating Trust on June 29, 2012, including interest costs resulting from capital lease obligations. |

| (6) | During the year ended December 31, 2012, we transferred our International Subsidiaries to the Liquidating Trust and recognized a gain of $48.7 million upon their deconsolidation. |

| (7) | We had been in litigation with Boeing regarding the development and launch of our former MEO satellites and related launch vehicles. In February 2009, the trial court entered judgment in our favor for approximately $603 million. On April 13, 2012, the California Court of Appeal overturned the judgment. The reversal was the culmination of a three year Court of Appeal process. The Court of Appeal also ordered us to reimburse Boeing for its appellate costs. On June 25, 2012, we settled our litigation against Boeing. As part of the settlement, we agreed to withdraw our petition for review to the California Supreme Court in exchange for a $10.0 million payment from Boeing and Boeing’s waiver of its right to appellate costs. The settlement agreement and mutual release between ourselves and Boeing fully released and discharged any and all claims between us and Boeing. As a result of the settlement agreement, we recorded a gain of $10.0 million during the year ended December 31, 2012. |

| (8) | In March 2011, upon the sale of our DBSD subsidiary for $325 million we recognized a $301 million gain associated with the disposition of DBSD and certain other assets pursuant to various agreements entered into with DISH Network. During the year ended December 31, 2012, we sold our real property located in Brazil for approximately $5.6 million. |

| (9) | During the year ended December 31, 2015, we recorded a gain on contingency for the receipt of $3.9 million from the disposition of assets associated with our former satellite business and a gain of $1.6 million for the final settlement received from the J&J Group. See footnote 11- Gain on Contingencies for further discussion on gain of contingencies. |

| (10) | During the years ended December 31, 2015 and 2014, we recorded a tax provision of $4.1 million and $6.3 million, respectively, related to foreign taxes withheld on revenue generated from license agreements executed with third party licensees domiciled in a foreign jurisdiction. Additionally, during the year ended December 31, 2015, as a result of the impairment of certain indefinite-lived intangible assets, the deferred tax liability associated with these intangibles was decreased, resulting in a tax benefit of $1.5 million. During the year ended December 31, 2011, as a result of recording net deferred tax liabilities pursuant to the acquisition of ContentGuard, we were able to reduce a portion of our deferred tax valuation allowance resulting in a tax benefit of $40.7 million. |

| (11) | Long-term obligations consist primarily of deferred tax liabilities. Long-term obligations at December 31, 2013 also include an installment payment obligation arising from the 2013 acquisition of our memory and storage technologies portfolio and expense related to restricted stock awards that is required to be treated as a liability. Long-term obligations at December 31, 2011 also include capital lease obligations and income tax obligations associated with uncertain tax positions. |

17

Table of Contents

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

The following discussion and analysis should be read in conjunction with our consolidated financial statements and accompanying notes included elsewhere in this Form 10-K.

Special Note Regarding Forward-Looking Statements

With the exception of historical facts, the statements contained in this management’s discussion and analysis are “forward-looking” statements. All of these forward-looking statements are subject to risks and uncertainties that could cause our actual results to differ materially from those contemplated by the relevant forward-looking statements. Factors that might cause or contribute to such a difference include, but are not limited to, those discussed under “Item 1A of Part I—Risk Factors” and elsewhere in this Form 10-K. The forward-looking statements included in this document are made only as of the date of this report, and we undertake no obligation to publicly update these forward-looking statements to reflect subsequent events or circumstances.

Overview

For the past four years, through our consolidated subsidiaries, we have invested in, acquired and monetized IP rights. We have generated positive returns on certain IP assets, particularly our patents applicable to memory and storage technologies, but the overall performance of our IP business has been disappointing. Specifically, we have not generated revenue from a number of companies that we believe incorporate our digital rights management (“DRM”) inventions into their consumer products. Our inability to convince these companies to sign license agreements forced us to pursue time-consuming and expensive litigation. The litigation prompted two jury trials in the Fall of 2015. Both juries affirmed the validity of the DRM patents asserted by ContentGuard in the litigation, but also concluded that the named defendants did not infringe the asserted patents. We believe the process by which the juries made their non-infringement decisions and the substance of those decisions were defective, and are appealing both verdicts. Regardless of the outcome of the appeal process, the verdicts were significant setbacks to our IP initiatives. As a result of the verdicts, we evaluated the financial statement carrying value of our entire IP portfolio. This evaluation resulted in a combined $103.5 million impairment of our IP and goodwill.

We believe the results in our litigation reflect a growing unfavorable political and judicial climate for inventors, innovators and owners of IP. In light of that climate, we are shifting our primary focus to business opportunities that provide more reliable cash flow and greater growth potential. We have evaluated several opportunities with business owners and investment partners who see the benefits of working with a well-established, well-funded organization. Although we have not yet executed a formal agreement with any of these potential owners or partners, our discussions are ongoing. We will continue to take a thoughtful and measured approach to our evaluation of these opportunities.

Our focus on new business opportunities will not distract us from continuing to monetize our existing IP portfolios. We believe the licenses that we have signed in the past two years reflect the importance of our inventions, our leadership in the development of breakthrough next-generation solutions, and our commitment to entering into licenses on a reasonable and non-discriminatory basis.

To more efficiently support our business strategy, we have substantially reduced our costs and simplified our operations while retaining the resources we deem critical to the generation of revenue from our existing IP assets and the pursuit of new business opportunities. For example, in 2015, we divested certain businesses that did not generate reliable cash flow, including Ovidian and Provitro Biosciences LLC (“Provitro”), reduced the number of executive officers, and continued to abandon patents that do not support our existing licensing programs. As a result, we ended 2015 with overhead costs that were less than 2014 overhead costs, and we are continuing to reduce costs in 2016.

18

Table of Contents

If we successfully implement our business strategy, we believe we will realize value from our existing IP assets and generate more reliable cash flow, while maintaining a modest cost structure.

2015 Events

During the first quarter of 2015, we licensed our memory and storage patents to SK hynix Inc. to permit the manufacture and distribution of embedded Multimedia Cards (“eMMC”). The license covers more than 169 patents and patents pending, and enables SK hynix to use both standards essential and implementation technologies. Additionally, we signed a settlement and patent license agreement with Amazon in August 2015 related to our DRM patents and negotiated with DirecTV throughout the Fall of 2015, which resulted in a settlement and license in January 2016.

In early 2015, we suspended further development of the Provitro™ proprietary micro-propagation technology and related laboratory processes that are designed to facilitate production on a commercial scale of certain plants, particularly timber bamboo. We took an impairment charge equal to our unamortized investment in the Provitro™ technology and related goodwill, reducing their fair values from approximately $11.0 million to zero at December 31, 2014. Then, later in 2015, we reached agreement with Provitro’s minority partner to cancel the ownership interest in Provitro that we did not already own for nominal consideration, thereby leaving us with 100% ownership of Provitro. We then sold all of the Provitro assets, including the rights to the micro-propagation technology.

2014 Events

During 2014, we licensed our memory assets to two leading technology companies for the manufacture and sale of eMMC technologies. The license agreements yielded significant upfront license fees, and in one case the potential for future royalties.

2013 Events

In the first quarter of 2013, we acquired from Nokia Corporation 125 patents and patent applications worldwide, 81 of which have been declared by Nokia to be essential to standards that are applicable to memory and storage technologies used in electronic devices. In connection with the acquisition, we formed a wholly owned development company to continue innovation efforts in memory and storage technology begun by Nokia. Our resulting memory and storage technologies program has thus far generated three licenses.

Critical Accounting Policies

Critical accounting policies require difficult, subjective or complex judgments, often as a result of the need to make estimates about the effect of matters that are inherently uncertain. Our estimates and judgments are based on information available at the time the estimates and judgments are made. Actual results could differ materially from those estimates. We make estimates and judgments when accounting for, among other matters, business combinations, goodwill and intangible assets, revenue recognition, stock-based compensation, income taxes and contingencies, as more fully described below.

Business Combinations. We account for business combinations using the acquisition method and, accordingly, the identifiable assets acquired and liabilities assumed are recorded at their acquisition date fair values. This valuation requires management to make significant estimates and assumptions, especially with respect to intangible assets. Valuation methodologies may include the cost, market or income approach. Critical estimates in valuing intangible assets include but are not limited to estimates about: future expected cash flows from customers, proprietary technology, the acquired company’s brand awareness and market position and discount rates. Our estimates are based upon assumptions we believe to be reasonable, but which are inherently uncertain and unpredictable. Goodwill is calculated as the excess of the purchase price over the fair value of net assets, including the amount assigned to identifiable intangible assets. Subsequent changes to assets, liabilities,

19

Table of Contents