Attached files

| file | filename |

|---|---|

| EX-21.1 - EXHIBIT 21.1 - Western Refining Logistics, LP | wnrl-ex211.htm |

| EX-32.2 - EXHIBIT 32.2 - Western Refining Logistics, LP | wnrl-ex322.htm |

| EX-31.2 - EXHIBIT 31.2 - Western Refining Logistics, LP | wnrl-ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - Western Refining Logistics, LP | wnrl-ex311.htm |

| EX-32.1 - EXHIBIT 32.1 - Western Refining Logistics, LP | wnrl-ex321.htm |

| EX-23.1 - EXHIBIT 23.1 - Western Refining Logistics, LP | wnrl-ex231consentofindepen.htm |

| EX-12.1 - EXHIBIT 12.1 - Western Refining Logistics, LP | wnrl-ex121ratioofearningst.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2015 | ||

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from _____ to _____ | ||

Commission File Number: 001-36114

WESTERN REFINING LOGISTICS, LP

(Exact name of registrant as specified in its charter)

Delaware | 46-3205923 | |

(State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization) | Identification No.) | |

123 W. Mills Avenue, Suite 200 | 79901 | |

El Paso, Texas | (Zip Code) | |

(Address of principal executive offices) | ||

Registrant’s telephone number, including area code: (915) 534-1400

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Units Representing Limited Partner Interests | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer þ | Non-accelerated filer o | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant computed based on the New York Stock Exchange closing price on June 30, 2015 (the last business day of the registrant’s most recently completed second fiscal quarter) was $466,071,205.

As of February 19, 2016, there were 24,446,384 common units and 22,811,000 subordinated units outstanding.

WESTERN REFINING LOGISTICS, LP

TABLE OF CONTENTS

PART I | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | Changes In and Disagreements with Accountants on Accounting and Financial Disclosure | |

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

EX-12.1 | ||

EX-21.1 | ||

EX-23.1 | ||

EX-31.1 | ||

EX-31.2 | ||

EX-32.1 | ||

EX-32.2 | ||

EX-101 | ||

References in this report to “Western Refining Logistics, LP,” “WNRL,” and “we,” “our,” “us,” the “Partnership” or like terms used in context of periods on or after October 16, 2013, refer to Western Refining Logistics, LP and its subsidiaries.

EXPLANATORY NOTE

Western Refining Logistics, LP is a publicly-traded Delaware limited partnership that commenced operations on October 16, 2013 in connection with its initial public offering (the "Offering") of 15,812,500 common units. In conjunction with the Offering, Western Refining, Inc. ("Western") and certain of its subsidiaries contributed to us the majority of the logistics assets that we currently operate.

On October 15, 2014, WNRL purchased all of the outstanding limited liability company interests of Western Refining Wholesale, LLC ("WRW") from Western for $320 million in cash and 1,160,092 common units (the "Wholesale Acquisition"). This purchase was a transaction between entities under common control and transferred substantially all of WRW's operations from Western to WNRL.

On October 30, 2015, WNRL acquired a segment of the TexNew Mex Pipeline system from Western that currently extends from our crude oil station in Star Lake, New Mexico, in the Four Corners region to our T station in Eddy County, New Mexico (the "TexNew Mex Pipeline System"). We also acquired an 80,000 barrel crude oil storage tank located at our crude oil pumping station in Star Lake, New Mexico and certain other related assets ("TexNew Mex Pipeline Acquisition"). We acquired these assets in exchange for $170 million in cash, 421,031 common units representing limited partner interests in WNRL and 80,000 units of a newly created class of limited partner interests in WNRL, referred to as the "TexNew Mex Units." This transaction was between entities under common control.

The financial position, results of operations and operating statistics of our accounting predecessor for the contributed logistics assets for periods prior to October 16, 2013 are contained herein. In addition, our accounting predecessor contains the financial position and results of operations of the TexNew Mex Pipeline System assets that were not contributed at the time of the Offering. We refer to the financial position, results of operations and operating statistics of these contributed and non-contributed assets, for periods prior to October 16, 2013 as the "WNRL Predecessor."

The information contained herein for the WNRL Predecessor and WNRL has been retrospectively adjusted to include the historical results of the WRW assets acquired for periods prior to the effective date of the Wholesale Acquisition. We refer to the collective entity of the WNRL Predecessor with the retrospective adjustment for the Wholesale Acquisition as our "Predecessor" for periods prior to October 16, 2013. The results of WNRL contain the retrospective adjustment for the Wholesale Acquisition and the TexNew Mex Pipeline Acquisition beginning October 16, 2013, the date WNRL commenced operations. Because the WNRL Predecessor has always contained the financial position and results of operations and operating statistics of the TexNew Mex Pipeline System, the retrospective adjustments related to the TexNew Mex Pipeline Acquisition are applied to WNRL only.

See Note 3, Initial Public Offering and Note 4, Acquisitions, in the Notes to Consolidated Financial Statements included in this annual report for detailed information.

FORWARD-LOOKING STATEMENTS

Certain statements included throughout this Annual Report on Form 10-K and in particular under the sections entitled Item 1. Business, Item 3. Legal Proceedings and Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations relating to matters that are not historical fact are forward-looking statements that represent management’s beliefs and assumptions based on currently available information. These forward-looking statements relate to matters such as our industry including the regulation of our industry, the expected outcomes of legal proceedings involving us or Western, business strategy, future operations, acquisition opportunities, volatility of crude oil prices, gross margins, volumes, taxes, capital expenditures, liquidity and capital resources, sources of financing for acquisitions, maintenance and capital expenditures, distributions and other financial and operating information. Forward-looking statements give our current expectations, contain projections of results of operations or of financial condition or forecasts of future events. We have used the words “anticipate,” “assume,” “believe,” “budget,” “continue,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “plan,” “position,” “potential,” “predict,” “project,” “strategy,” “will,” “future” and similar terms and phrases to identify forward-looking statements in this report.

Forward-looking statements reflect our current expectations regarding future events, results or outcomes. These expectations may or may not be realized. Some of these expectations may be based upon assumptions or judgments that prove to be incorrect or that are affected by unknown risks or uncertainties. Consequently, no forward-looking statements can be guaranteed. In addition, our business and operations involve numerous risks and uncertainties, many that are beyond our control

1

that could result in our expectations not being realized or otherwise materially affect our financial condition, results of operations and cash flows.

When considering these forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this Form 10-K. Actual events, results and outcomes may differ materially from our expectations due to a variety of factors. Although it is not possible to predict or identify all of these factors, they include, among others, the following:

• | changes in the business strategy or activity levels of Western that may be impacted by a variety of factors, including changes in crack spreads, changes in the spread between WTI crude oil and WTS crude oil, also known as the sweet/sour spread and changes in the spread between WTI crude oil and Dated Brent crude oil and between WTI Cushing crude oil and WTI Midland crude oil, and Western's pending merger with Northern Tier Energy LP ("Northern Tier"); |

• | changes in general economic conditions, including the price volatility of crude oil; |

• | competitive conditions in our industry; |

• | actions taken by third-party operators, processors and transporters; |

• | the demand for crude oil, refined and other products and transportation and storage services; |

• | the supply of crude oil in the regions in which we and Western operate; |

• | interest rates; |

• | labor relations; |

• | changes in the availability and cost of capital; |

• | changes in tax status; |

• | operating hazards, natural disasters, weather-related delays, casualty losses and other matters, including those that may result in a force majeure event under our commercial agreements with Western, that may be beyond our control; |

• | the effects of existing and future laws and governmental regulations and the manner in which they are interpreted and implemented; |

• | changes in insurance markets impacting costs and the level and types of coverage available; |

• | disruptions due to equipment interruption or failure at our facilities, Western’s facilities or third-party facilities on which our business is dependent; |

• | our ability to successfully implement our business plan; |

• | the effects of future litigation; and |

• | other factors discussed in more detail under Part I. - Item 1A Risk Factors of this report that are incorporated herein by this reference. |

Any one of these factors or a combination of these factors could materially affect our financial condition, results of operations or cash flows and could influence whether any forward-looking statements ultimately prove to be accurate. You are urged to consider these factors carefully in evaluating any forward-looking statements and are cautioned not to place undue reliance on these forward-looking statements.

Although we believe the forward-looking statements we make in this report related to our plans, intentions and expectations are reasonable, we can provide no assurance that such plans, intentions or expectations will be achieved. These statements are based on assumptions made by us based on our experience and perception of historical trends, current conditions, expected future developments and other factors that we believe are appropriate in the circumstances. Such statements are subject to a number of risks and uncertainties, many that are beyond our control. The forward-looking statements included herein are made only as of the date of this report and we are not required to (and will not) update any information to reflect events or circumstances that may occur after the date of this report, except as required by applicable law.

2

PART I

Item 1. Business

Overview

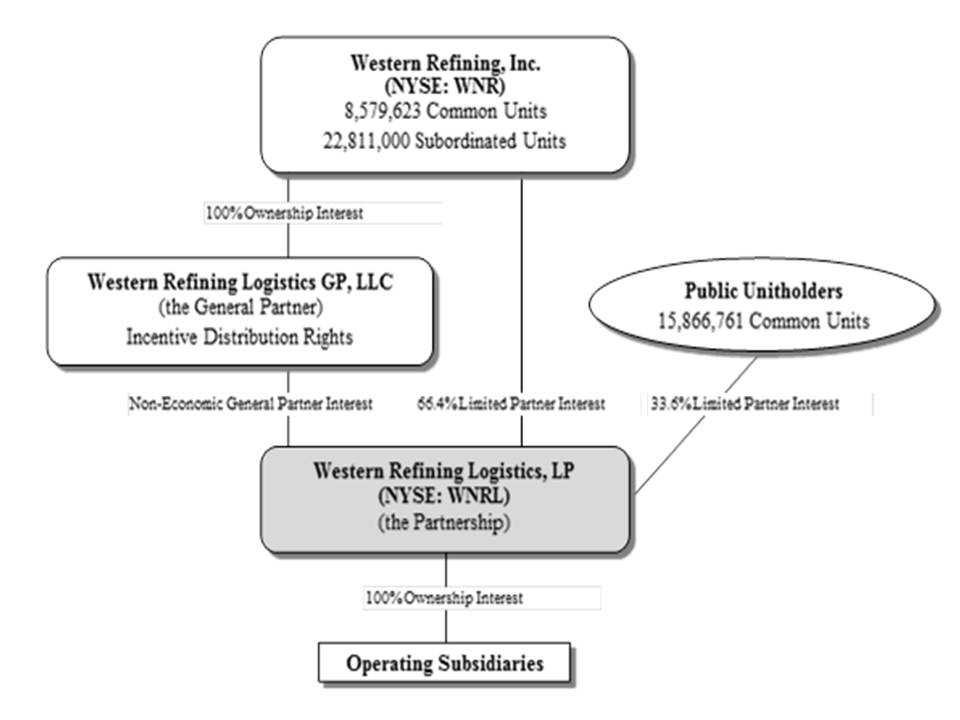

WNRL is a Delaware master limited partnership that commenced operations in October 2013. Western Refining Logistics GP, LLC ("WRGP"), our general partner holds all of the non-economic general partner interests in WNRL and is owned 100% by Western. On October 16, 2013, WNRL completed the Offering of 15,812,500 common units, after which Western's limited partner interest in WNRL was 65.3%. Our units trade on the New York Stock Exchange (“NYSE”) under the symbol “WNRL.”

WNRL is principally a fee-based, growth-oriented partnership that owns, operates, develops and acquires logistics and related assets and businesses to include terminals, storage tanks, pipelines and other logistics assets related to the terminalling, transportation, storage and distribution of crude oil and refined products. WNRL's assets and operations include 685 miles of pipelines, 8.2 million barrels ("bbls") of active storage capacity, distribution of wholesale petroleum products and crude oil trucking.

On October 15, 2014, we acquired all of the outstanding limited liability company interests of WRW, which owned substantially all of Western’s wholesale assets in the Southwest U.S. We acquired these interests in exchange for $320 million in cash and 1,160,092 of our common units. The issuance of these additional units to Western increased Western's limited partner interest in WNRL to 66.2%. We funded the cash payment through $269 million in new borrowings under our revolving credit facility and $51 million from cash on hand.

On October 30, 2015, WNRL acquired Western's TexNew Mex Pipeline System. We also acquired an 80,000 barrel crude oil storage tank located at our crude oil pumping station in Star Lake, New Mexico and certain other related assets. We acquired these assets in exchange for $170 million in cash, 421,031 common units representing limited partner interests in WNRL and 80,000 TexNew Mex Units.

The following simplified diagram depicts our organizational structure as of December 31, 2015:

3

All of our incentive distribution rights are held by our general partner and our units are held as follows:

Public Common Units | 33.6 | % |

Common Units held by Western | 18.2 | % |

Subordinated Units held by Western | 48.2 | % |

Non-Economic General Partner Interest held by Western Refining Logistics GP, LLC | — | |

TexNew Mex Units held by Western | — | |

Total | 100.0 | % |

We report our operating results in two business segments: logistics and wholesale. See Note 5, Segment Information, in the Notes to Consolidated Financial Statements included in this annual report for detailed information on our operating results by business segment.

• | We operate our logistics business under commercial and service agreements with Western, as described below, and we currently generate substantially all logistics segment revenues under fee-based agreements with Western. As a result of our fee-based arrangements with Western, we generally do not have exposure to variability in the prices of the hydrocarbons and other products we handle, although these risks indirectly influence our activities and results of operations over the long term. |

• | Our wholesale business operates under commercial and service agreements with Western, as described below, and sells refined products to third parties. Revenues, earnings and cash flows from our wholesale segment are primarily affected by the sales volumes and margins of gasoline, diesel fuel and lubricants sold. These margins are equal to the sales price, net of discounts, less total cost of sales and are measured on a cents per gallon ("cpg") basis. Factors that influence margins include local supply, demand and competition and the impact to margin of our commercial agreements with Western. |

We entered into the following agreements (the "Commercial Agreements") with Western that became effective in connection with the Offering and have initial ten-year terms:

• | Pipeline and Gathering Services Agreement: we entered into a pipeline and gathering services agreement, as amended, with Western under which we agreed to transport crude oil on our Permian Basin system primarily for use at Western’s El Paso refinery (the "El Paso Refinery") and on our Four Corners system primarily for use at Western’s Gallup refinery (the "Gallup Refinery"). |

In connection with the TexNew Mex Pipeline Acquisition, WNRL entered into Amendment No. 1 to the Pipeline and Gathering Services Agreement, dated as of October 16, 2013, with Western (the "Amendment to the Pipeline Agreement"). Among other things, the Amendment to the Pipeline Agreement amends the scope of the existing agreement to include the provision of storage services and a minimum volume commitment of 80,000 barrels of storage at the Star Lake storage tank. In this Amendment to the Pipeline Agreement, Western also committed to a minimum volume of 13,000 barrels per day ("bpd") throughput of crude oil on the TexNew Mex Pipeline for 10 years from the date of the Amendment to the Pipeline Agreement.

In connection with the TexNew Mex Pipeline Acquisition, our general partner adopted certain amendments to the First Amended and Restated Agreement of Limited Partnership of the Partnership by adopting the Second Amended and Restated Agreement of Limited Partnership (the “Second A&R Partnership Agreement”). The amendments contained in the Second A&R Partnership Agreement create a new class of partner interests in the Partnership, referred to as the TexNew Mex Units, and set forth the rights, preferences and obligations of the TexNew Mex Units.

The Second A&R Partnership Agreement provides for the creation of the “TexNew Mex Shared Segment” that will reflect the financial and operating results of the TexNew Mex Pipeline. The TexNew Mex Units are generally entitled to participate in 80% of the economics attributable to the TexNew Mex Shared Segment resulting from crude oil throughput on the TexNew Mex Pipeline above the 13,000 barrels per day contemplated by the commitment in the Amendment to the Pipeline Agreement. To the extent there is sufficient available cash from operating surplus under the Second A&R Partnership Agreement, the holder of the TexNew Mex Units will be entitled to receive a distribution equal to 80% of the excess of TexNew Mex Shared Segment Distributable Cash Flow over the TexNew Mex Base Amount (as such terms are defined in the Second A&R Partnership Agreement). The TexNew Mex Unit distributions are preferential to all other unit holder distributions.

• | Terminalling, Transportation and Storage Services Agreement: we entered into a terminalling, transportation and storage services agreement, as amended, with Western under which we agreed to, among other things, distribute products produced at Western’s refineries, connect Western’s refineries to third-party pipelines and systems and provide fee-based asphalt terminalling and processing services. At our network of crude oil and refined products |

4

terminals and related assets and storage facilities, we charge Western fees for crude oil, blendstock and refined product storage, shipments into and out of storage and additive and blending services. At our asphalt plant and terminal in El Paso and our three stand-alone asphalt terminals, we charge Western fees for asphalt storage, shipments into and out of asphalt storage and asphalt processing and blending services.

The fees under each of these agreements are indexed for inflation and apply only to services WNRL provides to Western. These agreements include provisions that permit Western to suspend, reduce or terminate its obligations under the applicable agreement if certain events occur. These events include Western deciding to permanently or indefinitely suspend refining operations at either of its refineries as well as certain extraordinary events beyond the control of us or Western that would prevent us from performing required services under the applicable agreement.

We entered into the following Commercial Agreements that became effective in connection with the Wholesale Acquisition and have initial ten-year terms with Western:

• | Product Supply Agreement: we entered into a product supply agreement, as amended, under which Western supplies, and we purchase, approximately 79,000 bpd of refined products for sale to our wholesale customers. The agreement includes product pricing based upon OPIS or Platts indices on the day of delivery. The agreement also contains, subject to certain exceptions, a covenant restricting Western's ability to compete in certain wholesale activities in the Southwest. The agreement provides for make-up payments to the Partnership in any month that the Partnership’s average margin on non-delivered rack sales is below a per gallon threshold. |

• | Fuel Distribution and Supply Agreement: we entered into a fuel distribution and supply agreement under which Western has agreed to purchase a minimum of 645,000 bbls per month of branded and unbranded motor fuels for its retail and automated commercial fueling sites (cardlocks) at a price equal to our product cost at each terminal, plus actual transportation costs, plus a margin of $0.03 per gallon. Under the fuel distribution agreement, a subsidiary of Western is obligated to offer us the first opportunity to satisfy all of its incremental branded and unbranded motor fuel requirements. |

• | Crude Oil Trucking Transportation Services Agreement: we entered into a crude oil trucking transportation services agreement, as amended, under which Western has agreed to utilize our crude oil trucks to haul a minimum of 1.525 million bbls of crude oil each month. Western pays a flat rate per barrel based on the distance between the applicable pick-up and delivery points plus monthly fuel adjustments and customary applicable surcharges. |

Western will remain obligated under the Commercial Agreements even if Western no longer controls our general partner.

We entered into a services agreement, as amended, with Western under which Western provides certain personnel for operational services under our supervision in support of our pipeline and gathering assets and terminalling and storage facilities. We reimburse Western for the cost of these services, including routine and emergency maintenance and repair services, routine operational activities, routine administrative services, construction and related services and other services as we and Western may mutually agree. Western prepares a maintenance, operating and capital budget on an annual basis subject to our approval. Western submits actual expenditures to us monthly for reimbursement. Under the agreement, Western indemnifies us from any claims, losses or liabilities that we incur, including third-party claims, arising from Western’s performance of the agreement to the extent caused by Western’s breach of contract, gross negligence or willful misconduct. We have agreed to indemnify Western from any claims, losses or liabilities that Western incurs, including any third-party claims, arising from Western’s performance of the agreement or from our breach of the agreement, except to the extent such claims, losses or liabilities are caused by Western’s breach of contract, gross negligence or willful misconduct.

We have also entered in an omnibus agreement with Western through which Western provides, and we in turn reimburse Western, for certain general and administrative services (this reimbursement is in addition to certain expenses of our general partner and its affiliates that are reimbursed under our partnership agreement and services agreement), as well as certain other direct or allocated costs and expenses incurred by Western on our behalf. Western has also indemnified us for certain environmental and other liabilities, and we have indemnified Western for events and conditions associated with our operations and for environmental liabilities related to our assets. The omnibus agreement generally terminates if we or our general partner experience change in control.

See Note 22, Related Party Transactions, in the Notes to Consolidated Financial Statements included in this annual report for detailed information on our agreements with Western.

5

Our Assets and Operations

Logistics Segment

Our logistics assets consist of pipeline and gathering infrastructure and terminalling, transportation and storage assets in the Southwestern portion of the U.S., including approximately 685 miles of pipelines and approximately 8.2 million bbls of active storage capacity, as well as other assets. Most of our assets are integral to the operations of the El Paso refinery and the Gallup refinery. We generate substantially all of our logistics revenue from fees charged for services provided to Western under the logistics Commercial Agreements.

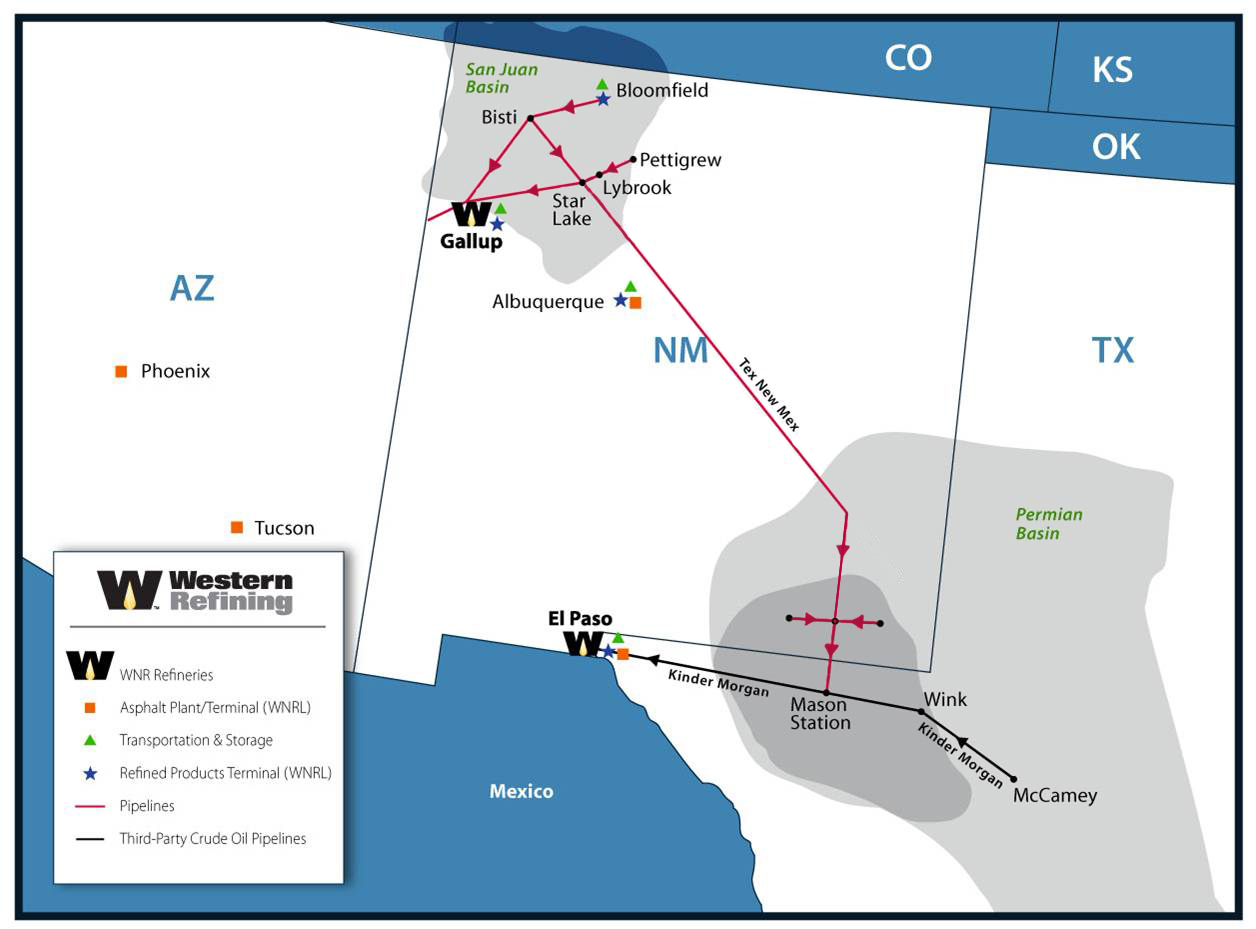

The following map depicts the locations of our assets (not to scale):

Pipeline and Gathering

Our pipeline and gathering assets are strategically positioned to support crude oil supply options for the El Paso refinery and the Gallup refinery as well as third parties and consist of crude oil pipelines and gathering assets located primarily in the Delaware Basin in the Permian Basin area of West Texas and Southern New Mexico (the "Delaware Basin") and in the Four Corners area of Northwestern New Mexico. Through these systems, we gather and transport crude oil by pipeline and trucks from various production locations to Western’s refineries utilizing approximately 685 miles of pipeline, 31 crude oil storage tanks with a total combined active shell storage capacity of approximately 828,000 bbls, eight truck loading and unloading locations and 15 pump stations.

Our pipeline and gathering assets consist of the following:

• | Permian Basin System. Our Permian Basin system includes our Delaware Basin system and other crude oil gathering assets in West Texas. The primary components of our Permian Basin system include: |

• | Delaware Basin System. Our Delaware Basin system includes approximately 39 miles of 10-inch and 12-inch mainlines located in Southeast New Mexico and West Texas and handles crude oil produced in the Delaware Basin. The Main 12-inch pipeline and the East 10-inch pipeline were placed into service in July 2013. The West 10-inch pipeline was placed into service in August 2013. The Delaware Basin system is designed to handle up to 154,000 bpd, comprised of a mainline capacity of 100,000 bpd and truck unloading capacity of 54,000 bpd and is operated from a central control station located in Bloomfield, New Mexico. Its primary components include: |

• | Main 12-inch Pipeline. This 12-inch crude oil pipeline is approximately 20 miles in length and connects our Mason Station crude oil facility to our T Station crude oil facility; |

6

• | West 10-inch Pipeline and CR-285 Crude Oil Station. This 10-inch crude oil pipeline is approximately 7 miles in length and has a capacity in excess of 75,000 bpd. It extends westward from our T Station crude oil facility. This west segment of the system includes a four-bay truck loading and unloading location and associated storage permitting truck deliveries of up to 24,000 bpd; |

• | East 10-inch Pipeline and CR-1 Crude Oil Station. This 10-inch crude oil pipeline is approximately 12 miles in length and has a capacity in excess of 75,000 bpd. It extends eastward from our T Station crude oil facility. This east segment of the system includes a four-bay truck loading and unloading location and associated storage permitting truck deliveries of up to 24,000 bpd; |

• | T Station Crude Oil Facility. Our T Station crude oil facility operates as a station for aggregating crude oil deliveries from the West 10-inch pipeline and East 10-inch pipeline and contains a staging tank with a combined shell storage capacity of 30,000 bbls; and |

• | Mason Station Crude Oil Facility. Our Mason Station crude oil facility is located in Reeves County, Texas and receives crude oil produced in Southern New Mexico and West Texas. This facility consists of three 80,000 bbl crude oil storage tanks, a nine-bay truck loading and unloading location and eleven automatic custody transfer units. This facility has a capacity of up to 54,000 bpd by truck and a capacity of up to 100,000 bpd from our Main 12-inch pipeline. Our Mason Station crude oil facility is connected to Kinder Morgan Energy Partners, LP's ("Kinder Morgan") Mason Junction pump station that injects crude oil into the Kinder Morgan Wink pipeline for delivery to Western’s El Paso Refinery or the Bobcat Pipeline. |

• | Other Permian Basin Crude Gathering Assets. We own other crude gathering assets in West Texas that handle crude oil produced in the Permian Basin with an aggregate capacity of approximately 8,000 bpd. |

• | McCamey Crude Oil Station. Our McCamey crude oil station is located in Upton County, Texas and receives crude oil produced in West Texas. This station consists of a four-bay truck rack and crude receipt tanks. This facility has a capacity of up to 5,700 bpd by truck. Our McCamey crude oil station is connected to Plains All American Pipeline, LP’s (“Plains”) McCamey crude oil terminal that either injects crude oil into the Kinder Morgan Wink pipeline for delivery to the El Paso refinery or into Plains’ McCamey crude oil terminal for delivery to Midland, Texas; and |

• | Riverbend 4-inch Gathering Pipeline. Our four-inch crude oil pipeline is approximately three miles in length and connects the Riverbend crude oil tanks in Crane County, Texas owned by third parties to the Kinder Morgan Wink pipeline for delivery to the El Paso refinery via Kinder Morgan’s Cordona Lake gathering system. |

• | Four Corners System. Our Four Corners system includes approximately 256 miles of pipeline in Northwestern New Mexico that gather and transport crude oil and condensate produced in the San Juan and Paradox Basin areas of Colorado, New Mexico and Utah (referred to, collectively as, “Four Corners area crude oil”) and deliver it to the Gallup refinery or into our TexNew Mex Pipeline System. This Four Corners area crude oil is received at our Bloomfield terminal and at crude oil stations we own located in Bisti, Lybrook, Pettigrew and Star Lake, New Mexico. This system has a delivery capacity of up to approximately 31,600 bpd to the Gallup refinery. The Four Corners system’s primary components include: |

• | San Juan 6-inch Pipeline. This six-inch crude oil pipeline is approximately 17 miles in length, connects our Bloomfield terminal to our Bisti crude oil station and handles Four Corners area crude oil; |

• | West 6-inch Pipeline. This six-inch crude oil pipeline is approximately 77 miles in length, connects our Bisti crude oil station to the Gallup refinery and handles Four Corners area crude oil; |

• | TexNew Mex 16" Pipeline Segment. This portion of the 16-inch crude pipeline is approximately 43 miles in length, connects our Bisti crude oil station to our Star Lake crude oil station and handles Four Corners area crude oil; |

• | East 6-inch Pipeline. This six-inch crude oil pipeline is approximately 105 miles in length, connects our Pettigrew crude oil station to our Star Lake crude oil station and also the Gallup refinery and handles Four Corners area crude oil; |

• | Wingate 4-inch NGL Pipeline. This four-inch natural gas liquids ("NGL") pipeline is approximately 14 miles in length and connects Western's NGL plant located in Gallup to the Gallup refinery. It transports NGLs for the Gallup refinery; and |

• | Other. The Bisti, Star Lake, Lybrook and Pettigrew Stations combine to have 16 crude oil storage and breakout tanks with a total combined capacity of approximately 485,400 bbls; four truck receipt locations and a connection point with the Navajo Nation Oil and Gas Company's Running Horse pipeline. |

7

• | TexNew Mex Pipeline System, including 76 mile extension. Our TexNew Mex pipeline extends approximately 299 miles from our crude oil station in Star Lake, New Mexico in the Four Corners area to near Maljamar, New Mexico in the Delaware Basin. In addition, a 76 mile pipeline was constructed to connect the TexNew Mex 16-inch pipeline from Maljamar to our Delaware Basin system. |

The following tables provide certain information regarding our pipeline and gathering assets:

Summary of Assets | ||||||

Length (miles) | Capacity | |||||

Mainline Movements (bpd) | ||||||

Delaware Basin | 39 | 100,000 | ||||

Four Corners (1) | 256 | 58,800 | ||||

TexNew Mex | 375 | 70,000 | ||||

Total | 228,800 | |||||

Gathering (Truck Offloading) (bpd) | ||||||

Mason Station | — | 54,000 | ||||

CR-285 (2) (3) | — | 24,000 | ||||

CR-1 (3) | — | 24,000 | ||||

McCamey Station | — | 5,700 | ||||

Four Corners | — | 22,800 | ||||

Total Gathering Capacity | 130,500 | |||||

Pipeline Tank Storage (bbls) | ||||||

Delaware Basin | — | 342,851 | ||||

Four Corners | — | 485,351 | ||||

Total Pipeline Tank Storage | 828,202 | |||||

(1) | The total capacity to transport crude oil to the Gallup refinery on the West 6-inch and East 6-inch pipelines is 31,600 bpd. |

(2) | Placed into service in August 2013. |

(3) | These volumes ship on the Delaware Basin mainline and are included in the 100,000 bpd capacity. |

Terminalling, Transportation, Storage and Distribution

Our terminalling, transportation and storage assets support crude oil supply and refined product distribution for the El Paso refinery and the Gallup refinery as well as third parties and primarily consist of storage tanks, terminals, transportation and other assets located in El Paso, Texas; Gallup, Bloomfield and Albuquerque, New Mexico and Phoenix and Tucson, Arizona. These assets include crude oil, feedstock, blendstock, refined product and asphalt storage tanks with a total combined shell storage capacity of approximately 7.4 million bbls, truck loading racks, railcar loading racks, pump stations and pipeline and related logistics assets to service Western’s operations.

Our terminalling, transportation and storage assets consist of the following:

• | El Paso Tank Farm. Our El Paso tank farm provides the El Paso refinery with storage, transfer and blending services required to support the refinery’s operations. The tank farm consists of storage tanks with an aggregate shell storage capacity of approximately 5.1 million bbls operating on land leased from Western under a 10-year agreement. The storage tanks handle refinery feedstock, jet fuel, gasoline, ultra-low sulfur diesel, blending components, crude oil, asphalt, slop oil and NGLs. Short pipelines on the tank farm transfer products to and from the refinery and storage tanks and ultimately to terminals or distribution pipelines. The El Paso tank farm also includes a rail loading facility located on the Burlington Northern Santa Fe and Union Pacific railroads and has railcar manifest loading capability. The rail loading facility handles asphalt, NGLs, feedstock, sulfuric acid and fuel oil. |

• | El Paso Refined Products Terminal. Our El Paso refined products terminal distributes refined products supplied by the El Paso refinery from a six-bay truck loading rack with a capacity to handle approximately 45,000 bpd of gasoline, diesel and jet fuel with associated ethanol, biodiesel and additive blending capabilities. The terminal includes storage tanks with a combined shell storage capacity of 74,900 bbls operating on land leased from Western under a 10-year agreement. The storage tanks handle gasoline, transmix, jet fuel, ultra-low sulfur diesel, bio-diesel, blending components and NGLs. |

8

• | Gallup Tank Farm. Our Gallup tank farm provides the Gallup refinery with storage and transfer services required to support the refinery’s operations. The tank farm consists of storage tanks with a combined shell storage capacity of approximately 887,100 bbls operating on land leased from Western under a 10-year agreement. The storage tanks handle refined products including ultra-low sulfur diesel, blending components, NGLs and gasoline and refinery feedstocks including crude oil, slop oil, intermediate feedstock and transmix. The Gallup tank farm also includes a railcar manifest loading facility located on the Burlington Northern Santa Fe railroad. The rail loading facility handles crude oil, intermediate feedstock, NGLs, fuel oil, ethanol and biodiesel. |

• | Gallup Refined Products Terminal. Our Gallup refined products terminal distributes refined products supplied by the Gallup refinery from a six-bay truck loading rack with a capacity to handle approximately 34,000 bpd of gasoline and ultra-low sulfur diesel with associated ethanol, biodiesel and additive blending capabilities. The terminal includes storage tanks with a combined active shell storage capacity of approximately 23,400 bbls operating on land leased from Western under a 10-year agreement. |

• | Bloomfield Terminal. Our Bloomfield terminal is a crude oil gathering and refined products distribution facility serving Western and third-party customers. The Bloomfield terminal includes storage tanks with combined shell storage capacity of approximately 675,900 bbls operating on land leased from Western under a 10-year agreement. The storage tanks handle Four Corners area crude oil, gasoline, ultra-low sulfur diesel and blending components. The terminal receives crude oil across a four-bay truck unloading rack, de-waters the crude oil and stores it for shipment on our San Juan 6-inch pipeline to our crude oil station in Bisti for further transport to the Gallup refinery. Our Bloomfield terminal distributes refined products for Western and third-party customers over a four-bay truck loading rack that has ethanol and additive blending capabilities. A pipeline from Artesia, New Mexico, owned by Holly Energy Partners LP provides primary supply to the terminal. The terminal also receives supply by trucks from other locations. |

• | Albuquerque Refined Products Terminal. Our Albuquerque refined products terminal distributes approximately 9,000 bpd of gasoline, diesel fuel and ethanol from a two-bay truck loading rack for Western and third-party customers. The truck loading rack has a capacity of up to approximately 27,500 bpd with associated ethanol and additive blending capabilities. The terminal includes storage tanks with a combined shell storage capacity of approximately 185,700 bbls operating on land that we own. The El Paso refinery supplies this terminal via the Magellan common carrier pipeline, owned by Magellan Midstream Partners, LP (“Magellan”), as well as by truck from the Gallup refinery, our Bloomfield terminal and other locations. Our Albuquerque refined products terminal is also capable of receiving ethanol by truck and rail. The rail loading facility is located on the Burlington Northern Santa Fe railroad. |

• | Asphalt Plant and Terminals. We provide fee-based asphalt terminalling and processing services at our asphalt plant and terminal in El Paso, as well as at three stand-alone asphalt terminals in Albuquerque, New Mexico and Phoenix and Tucson, Arizona. Our El Paso asphalt plant is located adjacent to the El Paso refinery. The plant has the ability to modify asphalt with polymer and polyphosphoric acid that allows for flexibility in meeting stringent performance grade asphalt specifications. The asphalt plant can process up to approximately 1,650 tons per day (“tpd”) of asphalt. The related El Paso asphalt terminal distributes asphalt to customers by rail (through its six rail locations) and by truck over a five-bay truck loading rack. Both the El Paso asphalt plant and the related terminal operate on land leased from Western under a 10-year agreement. Our three other asphalt terminals located in Albuquerque, New Mexico and Phoenix and Tucson, Arizona are throughput terminals for finished asphalt with an aggregate terminalling capacity of up to 2,250 tpd. The asphalt plant and terminals have a combined shell storage capacity of approximately 473,000 bbls. |

9

The following table describes the capacities of our terminal and storage assets:

Tank Shell Storage Capacity | ||

Crude Oil, Intermediates and Refined Products (bbls) | ||

El Paso Tank Farm | 5,065,600 | |

El Paso Refined Products Terminal | 74,900 | |

Gallup Tank Farm | 887,100 | |

Gallup Refined Products Terminal | 23,400 | |

Bloomfield Terminal | 675,900 | |

Albuquerque Refined Products Terminal | 185,700 | |

Total | 6,912,600 | |

Asphalt (tpd) | ||

El Paso Asphalt Plant | 202,000 | |

Albuquerque Asphalt Terminal | 38,500 | |

Tucson Asphalt Terminal | 208,700 | |

Phoenix Asphalt Terminal | 23,800 | |

Total | 473,000 | |

Wholesale Segment

Our wholesale business purchases substantially all of its petroleum fuels from Western and all of its lubricants and additional petroleum fuels from third-party suppliers. In addition to our sales to Western, our principal customers are retail fuel distributors and the mining, construction, utility, manufacturing, transportation, aviation and agricultural industries. We compete with other wholesale petroleum products distributors on product sales pricing and distribution services in the Southwest such as Pro Petroleum, Inc.; Southern Counties Fuels; Synergy Petroleum, LLC; SoCo Group, Inc.; C&R Distributing, Inc.; and Brewer Petroleum Services, Inc. Our sales and services to Western generally accounted for approximately 25% of our fuel volumes and 38% of our fuel trucking volumes for the year ended December 31, 2015. Among our third-party customers, sales to Kroger Company accounted for 23.5%, 23.0%, and 27.1% of consolidated net sales for the years ended December 31, 2015, 2014 and 2013, respectively.

Our wholesale segment consists of the following operations:

Fuel Distribution

Our wholesale segment purchases petroleum fuels primarily from Western’s refining group and distributes these fuels. We have entered into a product supply agreement, as amended, with Western and certain of its affiliates, pursuant to which Western has agreed to sell, and we have agreed to buy, between 90% and 110% of 79,000 bpd of Western’s refined products based upon forecasts provided each month by us. The products are purchased according to a predetermined formula based upon OPIS or Platts indices on the day of delivery and the applicable terminal location. Western will provide us margin shortfall support for non-delivered rack sales. The product supply agreement contains customary payment terms that may be extended if our net working capital requirements grow significantly over time.

As part of this fuel distributions business, we have entered into a fuel distribution and supply agreement with Western. Under this arrangement, we are required to sell and deliver to Western, and Western is required to purchase and accept delivery from us, 645,000 bbls per month of branded and unbranded motor fuels to Western retail and cardlock locations in the Southwest. In exchange for the sale and delivery of branded and unbranded motor fuels, Western will pay us an amount equal to our product cost at each terminal, plus applicable taxes and fees, actual transportation costs and a margin of $0.03 per gallon. In the event that Western fails to purchase the committed volume of branded and unbranded motor fuels, Western will pay $0.03 per gallon for each gallon below the committed volume. Western will receive a credit for excess volumes purchased in subsequent months to the extent that shortfall payments were made in the prior twelve months. Our net cost per gallon will be determined based on the prices paid under the product supply agreement.

This business includes the operation of a fleet of finished products trucks that deliver a significant portion of the volumes sold by our wholesale segment.

10

Crude Trucking

Our wholesale segment operates a fleet of crude oil trucks, which are utilized to support crude oil supply options for the El Paso refinery and the Gallup refinery. We have entered into a crude oil trucking transportation services agreement, as amended, with Western under which we have agreed to, among other things, gather, transport and deliver crude oil from collection points in Colorado, New Mexico and Utah to the El Paso refinery and the Gallup refinery and their interconnected pipelines. Western has agreed to utilize our crude oil trucking fleet to transport a minimum volume of 1.525 million bbls per month.

In exchange for the gathering and transportation services performed under the crude trucking agreement, Western has agreed to pay us a flat rate per barrel (with market adjustments) based on the distance between the applicable pick-up and delivery points, plus monthly fuel adjustments and customary applicable surcharges.

Lubricants Distribution

Our wholesale segment purchases and distributes lubricants to various third-party customers. As part of this business, our wholesale segment operates several lubricants distribution facilities and a fleet of lubricants transports.

Environmental Regulation

General

Our operations are subject to extensive and periodically changing federal, state and local laws, regulations and ordinances relating to the protection of the environment. Among other things, these laws and regulations govern the emission or discharge of pollutants into or onto the land, air and water, the handling and disposal of solid and hazardous wastes, the remediation of contamination and protection of endangered and threatened species. Compliance with existing and anticipated environmental laws and regulations increases our overall cost of business, including our capital costs to develop, maintain, operate and upgrade equipment and facilities. We believe our facilities are in substantial compliance with applicable environmental laws and regulations. However, these laws and regulations are subject to changes, or to changes in the interpretation (including enforcement policies) of such laws and regulations, by regulatory authorities and continued and future compliance with such laws and regulations may require us to incur significant expenditures. Additionally, violation of environmental laws, regulations and permits can result in the imposition of significant administrative, civil and criminal penalties, injunctions limiting or prohibiting our operations, investigatory or remedial liabilities, or construction bans or delays in the development of additional facilities or equipment. In particular, a release of hydrocarbons or hazardous substances into the environment could, to the extent the event is not insured, subject us to substantial expenses, including costs to comply with applicable laws and regulations and to resolve claims by third parties for personal injury or property damage, or by the U.S. federal government or state governments for natural resources damages. This could directly and indirectly affect our business and may have an adverse impact on our financial position, results of operations and liquidity. We cannot currently determine the amounts of such future impact.

Indemnification

Under our omnibus agreement with Western, Western indemnifies us for all known and certain unknown environmental liabilities that are associated with the ownership or operation of our assets and due to occurrences on or before the closing of the Offering. Indemnification for any unknown environmental liabilities is limited to liabilities due to occurrences on or before the closing of the Offering and identified prior to the fifth anniversary of the closing of the Offering and will be subject to a deductible of $100,000 per claim. There is no limit on the amount for which Western indemnifies us under the omnibus agreement once we meet the deductible, if applicable. Western will also indemnify us for failure to obtain certain consents, licenses and permits necessary to conduct our business, including the cost of curing any such condition and litigation matters, in each case that are identified prior to the fifth anniversary of the closing of the Offering. These claims will be subject to an aggregate deductible of $200,000.

We have agreed to indemnify Western for environmental liabilities related to our assets to the extent Western is not required to indemnify us as described above. There is no limit on the amount for which we will indemnify Western under the omnibus agreement.

Under the separate contribution agreements related to the Wholesale Acquisition and the TexNew Mex Pipeline Acquisition, Western agreed to indemnify us with respect to liabilities related to certain historical assets and operations of WRW and the TexNew Mex Pipeline System that were not contributed to us in the respective acquisitions. In addition, Western made certain representations and warranties regarding the assets of WRW and the assets of the TexNew Mex Pipeline System, including with respect to environmental matters, and agreed to indemnify us for breaches of those representations and warranties, subject to specified deductibles, caps and other limitations.

11

Air Emissions and Climate Change

Our operations are subject to the Clean Air Act and its regulations and comparable state and local statutes and regulations in connection with air emissions from our operations. Under these laws, permits may be required before construction can commence on a new source of potentially significant air emissions and operating permits may be required for sources that are already constructed. These permits may require controls on our air emission sources and we may become subject to more stringent regulations requiring the installation of additional emission control technologies, the costs of which could be significant.

In addition, various legislative and regulatory measures to address greenhouse gas emissions (including carbon dioxide, methane and other gases) are in various phases of discussion or implementation, including reporting and permitting of greenhouse gas emissions and state and regional cap-and-trade programs. The impact of future regulatory and legislative developments, if adopted or enacted, including any cap-and-trade program or programs, is likely to result in increased compliance costs, increased utility costs, additional operating restrictions on our business and an increase in the cost of products generally. The extent and magnitude of that impact cannot be reliably or accurately estimated due to the present uncertainty regarding the additional measures and how they will be implemented. Some scientists have concluded that increasing concentrations of greenhouse gas in the Earth’s atmosphere may produce climate changes that have significant physical effects, such as increased frequency and severity of storms, droughts and floods and other climatic events. Such climatic events could have an adverse effect on our financial condition and results of operations.

Waste Management and Related Liabilities

Several of the environmental laws and regulations affecting our operations relate to the release of hazardous substances or solid wastes into soils, groundwater and surface water and include measures to control pollution of the environment. These laws generally regulate the generation, storage, treatment, transportation and disposal of solid and hazardous waste. They also require corrective action, including investigation and remediation, at a facility where such waste may have been released or disposed. Pursuant to our omnibus agreement, Western indemnifies us and will fund all of the costs of required remedial action for Western's known historical and legacy spills and releases and, subject to a deductible per claim of $100,000, for spills and releases, if any, existing but unknown at the time of closing of the Offering to the extent such existing but unknown spills and releases are identified within five years after closing of the Offering.

CERCLA. The Comprehensive Environmental Response, Compensation, and Liability Act ("CERCLA"), or the Superfund law, and analogous state laws, impose joint and several liability, without regard to fault or the legality of the original conduct, on certain classes of potentially responsible persons for releases of hazardous substances into the environment. These persons include the owner or operator of a site and companies that disposed or arranged for the disposal of the hazardous substances found at the site. By operation of law, if we are determined to be a potentially responsible person, we may be responsible under CERCLA for all or part of the costs required to clean up sites at which such materials are present, in addition to providing compensation for any natural resource damages. We have not been determined to be a potentially responsible party at any sites.

RCRA. We also generate solid wastes, including hazardous wastes, within the tank cleaning process that are subject to the requirements of the federal Resource Conservation and Recovery Act (“RCRA”) and comparable state statutes. While RCRA regulates both solid and hazardous wastes, it imposes strict requirements on the generation, storage, treatment, transportation and disposal of hazardous wastes. In the course of our operations, we generate petroleum product wastes and ordinary industrial wastes such as paint wastes, waste solvents and waste oils that are regulated as hazardous wastes. Certain materials generated in the exploration, development or production of crude oil and natural gas are excluded from RCRA’s hazardous waste regulations. However, it is possible that future changes in law or regulation could result in these wastes, including wastes currently generated by our operations, being designated as “hazardous wastes” and therefore subject to more rigorous and costly disposal requirements. Any such changes in laws and regulations could have a material adverse effect on our capital expenditures and operating expenses.

Hydrocarbon Wastes. We currently own and lease properties where hydrocarbons are being or for many years have been handled. Although operating and disposal practices that were standard in the industry at the time were utilized, hydrocarbons or other waste may have been disposed of or released on or under the properties owned or leased by us or on or under other locations where these wastes have been taken for disposal. These properties and wastes disposed thereon may be subject to CERCLA, RCRA and analogous state laws. Under these laws, we could be required to remove or remediate previously disposed wastes (including wastes disposed of or released by prior owners or operators), to clean up contaminated property (including contaminated groundwater) or to perform remedial operations to prevent further contamination, the costs of which could be significant.

12

Water

Our operations can result in the discharge of pollutants, including crude oil and other products that we handle, store or transport in the course of our operations. Regulations under the Water Pollution Control Act of 1972 (“Clean Water Act”), the Oil Pollution Act of 1990 (the "Oil Pollution Act" ) and state laws impose regulatory burdens on our operations. Spill prevention control and countermeasure ("SPCC") requirements of federal laws and some state laws require containment to mitigate or prevent contamination of navigable waters in the event of an oil overflow, rupture or leak.

In addition, the transportation and storage of crude oil and products over and adjacent to water involves risk and subjects us to the provisions of the Oil Pollution Act and related state requirements. In case of any such release, the Oil Pollution Act requires the responsible company to pay resulting removal costs and natural resource damages. We operate facilities and transport crude oil and products where releases in water of oil and hazardous substances could occur. We have implemented emergency oil response plans for all of our components and facilities covered by the Oil Pollution Act and we have established SPCC plans for facilities subject to Clean Water Act SPCC requirements.

Construction or maintenance of our pipelines, terminals and storage facilities may impact wetlands or surface waters that are regulated under the Clean Water Act by the U.S. Environmental Protection Agency (the "EPA") and the U.S. Army Corps of Engineers. Regulatory requirements governing wetlands (including associated mitigation projects) and surface water crossings may result in the delay of our pipeline projects while we obtain necessary permits and may increase the cost of new projects and maintenance activities.

Hazardous Materials Transportation Requirements

U.S. Department of Transportation (the "DOT") regulations affecting pipeline safety for certain of our pipelines require pipeline operators to implement measures designed to reduce the environmental impact of crude oil and product discharge from onshore crude oil and product pipelines. These regulations require operators to maintain comprehensive spill response plans, including extensive spill response training for pipeline personnel. In addition, the DOT regulations contain detailed specifications for pipeline operation and maintenance. We believe our operations are in compliance with these regulations. The DOT also has a pipeline integrity management rule, with which we believe we are in substantial compliance.

The Federal Motor Carrier Safety Administration of the DOT regulates safety standards and monitors drivers and equipment of commercial motor carrier fleets. Standards include vehicle and maintenance inspection requirements, limitations on the number of hours drivers may operate vehicles, and financial responsibility requirements. We believe that the operations of our fleet of crude oil and finished products truck transports are substantially in compliance with all related DOT regulations and safety requirements.

Employee Safety

We are subject to the requirements of the Occupational Safety and Health Act (“OSHA”) and comparable state statutes that regulate the protection of the health and safety of workers. In addition, the OSHA hazard communication standard requires that information be maintained about hazardous materials used or produced in operations and that this information be provided to employees, state and local government authorities and citizens. We believe that our operations are in substantial compliance with OSHA requirements, including general industry standards, record keeping requirements and monitoring of occupational exposure to regulated substances.

Employees

We are managed and operated by Western Refining Logistics GP, LLC, our general partner. As of December 31, 2015, we directly employed 562 employees through our wholesale subsidiary. Through our general partner's affiliates, we have 218 full-time employees as well as other employees who may provide services to us from time to time, all of whom are seconded to us pursuant to our services agreement with Western. These seconded employees provide operating, maintenance and other services under our direction, supervision and control with respect to the assets that our pipeline and terminalling subsidiaries own and operate. Other Western employees also may provide services to us from time to time.

13

Available Information

We file reports with the Securities and Exchange Commission (the "SEC"), including annual reports on Form 10-K, quarterly reports on Form 10-Q and other reports from time to time. The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. We are an electronic filer and the SEC’s Internet site at http://www.sec.gov contains the reports and other information filed electronically. We do not, however, incorporate any information on that website into this Form 10-K.

As required by Section 406 of the Sarbanes-Oxley Act of 2002, we have adopted a code of ethics that applies specifically to our Chief Executive Officer, Chief Financial Officer and Principal Accounting Officer. We have also adopted a Code of Business Conduct and Ethics applicable to all our directors, officers and employees. Those codes of ethics are posted on our website. Our website address is: http://www.wnrl.com. Within the time period required by the SEC and the NYSE, we will post any amendment to our code of ethics and any waiver applicable to any of our Chief Executive Officer, Chief Financial Officer and Principal Accounting Officer on our website. We make our website content available for informational purposes only. It should not be relied upon for investment purposes, nor is it incorporated by reference in this Form 10-K. We make our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports simultaneously to the electronic filings of those materials with, or furnishing of those materials to, the SEC available on our website under “Investor Relations,” free of charge. We also make hard copies of our complete audited financial statements available to unitholders, free of charge upon request.

14

Item 1A. | Risk Factors |

Limited partner interests are inherently different from capital stock of a corporation, although many of the business risks that we are subject to are similar to those that would be faced by a corporation engaged in similar businesses. Security holders and potential investors should carefully consider the following risk factors together with all of the other information included in this report. If any of the following risks were actually to occur, our business, financial condition, results of operations or cash flows could be materially adversely affected.

The risks described below are not the only ones that we face. Additional risks not presently known to us or that we currently deem immaterial individually or in the aggregate may also impair our business operations.

Risks Relating to Our Business

Western currently accounts for a substantial portion of our revenues and is one of our significant suppliers, and therefore we are subject to the business risks of Western. If Western changes its business strategy, is unable to satisfy its obligations under our commercial agreements for any reason or significantly reduces the volumes transported through our pipelines and gathering systems or handled at our terminals, our revenues would decline and our financial condition, results of operations, cash flows and ability to service our indebtedness would be adversely affected.

Western is the primary shipper on our pipelines and gathering systems, our primary customer for our terminalling and storage activities and a significant supplier to and customer of our wholesale business. As we expect to continue to derive a substantial portion of our logistics revenues and wholesale fuel supply from Western for the foreseeable future, we are subject to the risk of nonpayment or nonperformance by Western under our commercial agreements. Any event, whether in our existing areas of operation or otherwise, that materially and adversely affects Western’s financial condition, results of operations or cash flows may adversely affect our ability to service our indebtedness or make cash distributions. Accordingly, we are indirectly subject to the operational and business risks of Western, some of which are related to the following:

• | the price volatility of crude oil (including prolonged periods of low crude oil prices that could impact production growth of inland crude oil and reduce the amount of advantaged crude oil available and/or the discount of such crude oil), other feedstocks, refined products and fuel and utility services has had and may have a material adverse effect on Western’s earnings and cash flows; |

• | if the price of crude oil increases significantly or Western’s credit profile changes, or if Western is unable to access its revolving credit facility for borrowings or for letters of credit, Western’s liquidity and ability to purchase enough crude oil to operate its refineries at full capacity could be materially and adversely affected; |

• | Western’s hedging transactions may limit its gains and expose Western to other risks; |

• | Compliance with and changes in tax laws could adversely affect Western’s performance; |

• | the risk of contract cancellation, non-renewal or failure to perform by Western’s customers and Western’s inability to replace such contracts and/or customers could have a material adverse effect on Western’s earnings and cash flows; |

• | Western’s indebtedness, including any indebtedness it may incur in the future, may limit its ability to obtain additional financing and Western may also face difficulties complying with the terms of its indebtedness agreements; |

• | covenants and events of default in Western’s debt instruments could limit its ability to undertake certain types of transactions and adversely affect its liquidity; |

• | Western has capital needs for which its internally generated cash flows and other sources of liquidity may not be adequate; |

• | future acquisitions by Western may reduce, rather than increase, its cash flows and the impacts of such acquisitions, together with any indebtedness incurred to fund such acquisitions, could have a negative impact on Western’s creditworthiness; |

• | the dangers inherent in Western’s operations could cause disruptions and could expose Western to potentially significant losses, costs or liabilities. Any significant interruptions in the operations of any of Western’s refineries could materially and adversely affect its business, financial condition, results of operations and cash flows; |

• | Western’s operations involve environmental risks that could give rise to material liabilities; |

• | Western may incur significant costs to comply with environmental, health and safety laws and regulations; |

• | Western could experience business interruptions caused by pipeline shutdowns or interruptions; |

15

• | a material decrease in the supply of crude oil available to Western’s refineries could significantly reduce its production levels; |

• | severe weather could interrupt the supply of some of Western’s feedstock for its refineries that could have a material adverse effect on its business, financial condition, results of operation and cash flows; |

• | Western could incur substantial costs or disruptions in its business if it cannot obtain or maintain necessary permits and authorizations; |

• | competition in the refining, marketing and retail industry is intense, and an increase in competition in the areas in which Western sells its refined and other products could adversely affect Western’s sales and profitability; |

• | Western’s business, financial condition, results of operations and cash flow may be materially adversely affected by a continued economic downturn; |

• | Western’s insurance policies do not cover all losses, costs or liabilities that Western may experience; |

• | Western could be subject to damages based on claims brought by its customers or lose customers as a result of a failure of its products to meet certain quality specifications; |

• | a substantial portion of Western’s refining workforce is unionized and Western may face labor disruptions that would interfere with their operations; |

• | if Western loses any of its key personnel, Western’s ability to manage its business could be negatively impacted; and |

• | terrorist attacks, cyber-attacks, threats of war or actual war may negatively affect Western’s operations, financial condition, results of operations, cash flows and prospects. |

Petroleum refining and marketing is highly competitive. Due to their geographic diversity, larger and more complex refineries, integrated operations and greater resources, some of Western’s competitors may be better able to withstand volatile market conditions, compete on the basis of price, obtain crude oil in times of shortage and bear the economic risk inherent in all phases of the refining industry. The El Paso refinery and the Gallup refinery primarily compete with Valero Energy Corp., Phillips 66 Company, Alon USA Energy, Inc., HollyFrontier Corporation, Tesoro Corporation, Chevron Products Company and Suncor Energy, Inc., as well as refineries in other regions of the country that serve the regions that Western serves through pipelines. Some areas where Western sells refined products are also supplied by various refined product pipelines. Any expansions or additional products supplied by these third-party pipelines could put downward pressure on refined product prices in these areas.

Western is not obligated to use our services with respect to volumes of crude oil or refined and other products in excess of the minimum volume commitments under its commercial agreements with us. In addition, the terms of Western’s obligations under those agreements are 10 years. If Western fails to use our assets and services after expiration of those agreements, or should our commercial agreements be invalidated for any reason, and we are unable to generate additional revenue from third parties, our ability to service our indebtedness may be materially and adversely affected. Furthermore, our commercial agreements with Western were not the result of arm’s-length negotiations and we may enter into future agreements with Western that are not the result of arm’s-length negotiations.

Additionally, Western may consider opportunities presented by third parties with respect to its refinery assets. These opportunities may include offers to purchase assets and joint venture propositions. Western may also change its refineries’ operations by developing new facilities, suspending or reducing certain operations, modifying or closing facilities or terminating operations. Changes may be considered to meet market demands, to satisfy regulatory requirements or environmental and safety objectives, to improve operational efficiency or for other reasons. Western actively manages its assets and operations, and therefore, changes of some nature, possibly material to its business relationship with us, are likely to occur at some point in the future. No such changes will be subject to our consent.

Furthermore, conflicts of interest may arise between Western and its affiliates, including our general partner and Western’s controlled subsidiary, Northern Tier, on the one hand, and us and our unitholders, on the other hand. We have no control over Western, our largest source of revenue and our primary customer, and Western may elect to pursue a business strategy that does not favor us and our business.

16

We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our general partner and its affiliates, to enable us to pay the minimum quarterly distribution to our unitholders.

We may not have sufficient available cash from operating surplus each quarter to enable us to pay the minimum quarterly distribution. The amount of cash we can distribute on our units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on, among other things:

• | the volume of crude oil and refined and other products we handle; |

• | the transportation, terminalling and storage fees with respect to volumes that we handle; |

• | our entitlement to payments associated with the minimum volume commitments under our commercial agreements with Western; |

• | timely payments by Western and our other customers; and |

• | prevailing economic conditions. |

In addition, the actual amount of cash we will have available for distribution will also depend on other factors, some of which are beyond our control, including:

• | the amount of our operating expenses and selling, general and administrative expenses, including our obligation to reimburse Western or our general partner in respect of those expenses, which obligation is not limited in amount under our partnership agreement, omnibus agreement or services agreement; |

• | the level of capital expenditures we make; |

• | the cost of acquisitions and organic growth projects, if any; |

• | our debt service requirements and other liabilities; |

• | fluctuations in our working capital needs; |

• | our ability to borrow funds and access capital markets; |

• | restrictions contained in our revolving credit facility and other debt service requirements; |

• | the amount of cash reserves established by our general partner; and |

• | other business risks affecting our cash levels. |

Western may suspend, reduce or terminate its obligations under each of our commercial agreements and our services agreement in some circumstances, which would have a material adverse effect on our financial condition, results of operations, cash flows and ability to service our indebtedness.

Our commercial agreements and services agreement with Western include provisions that permit Western to suspend, reduce or terminate its obligations under the applicable agreement if certain events occur. These events include a material breach of the agreement by us, or, in some cases, Western deciding to permanently or indefinitely suspend refining operations at one or more of its refineries, as well as our being subject to certain force majeure events that would prevent us from performing required services under the applicable agreement. Western has the discretion to make such decisions notwithstanding the fact that they may significantly and adversely affect us. For instance, under the commercial agreements entered into in connection with the Offering, if Western decides to permanently or indefinitely suspend, in full or in part, refining operations at a refinery for a period that will continue for at least twelve consecutive months, then it may terminate or proportionately reduce, as applicable, its obligations under the agreement on no less than twelve-months’ prior written notice to us, unless it publicly announces its intent to resume operations at the refinery at least two months prior to the expiration of the twelve-month notice period. Under the commercial agreements entered into in connection with the Offering and the Wholesale Acquisition, Western has the right to terminate such agreements with respect to any services for which performance will be suspended by a force majeure event for a period in excess specified periods ranging from six to twelve-months. Additionally, under the commercial agreements and the services agreement, Western has the right to terminate such agreements in the event of a material breach by us, subject to a specified cure period.

Generally, although Western is not entitled to claim a force majeure event under the commercial agreements, Western’s and our obligations under these agreements will be proportionately reduced or suspended to the extent that we are unable to perform under the agreements upon our declaration of a force majeure event. As defined in our commercial agreements and in the services agreement, force majeure events include any acts or occurrences that prevent services from being performed under the applicable agreement, including, but not limited to:

• | acts of God, or fires, floods or storms; |

17

• | compliance with orders of courts or any governmental authority; |

• | explosions, wars, terrorist acts, riots, strikes, lockouts or other industrial disturbances; |

• | accidental disruption of service; |

• | breakdown of machinery, storage tanks or pipelines and inability to obtain, or unavoidable delay in obtaining, material or equipment; and |

• | similar events or circumstances, so long as such events or circumstances are beyond the service provider’s reasonable control and could not have been prevented by the service provider’s due diligence. |