Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒ |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2015 |

||

|

OR |

||

|

☐ |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-9025

VISTA GOLD CORP.

(Exact Name of Registrant as Specified in its Charter)

|

British Columbia |

|

98-0542444 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

Suite 5, 7961 Shaffer Parkway |

|

|

|

Littleton, Colorado |

|

80127 |

|

(Address of Principal Executive Offices) |

|

(Zip Code) |

(720) 981-1185

(Registrant’s Telephone Number, including Area Code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

|

Title of Each Class |

Name of Each Exchange on Which Registered |

|

|

|

|

Common Shares without par value |

NYSE MKT |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐No☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐No☒

Indicate by checkmark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒No ☐

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒No ☐

Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part II of this Form 10-K or any amendment to the Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “Accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (Check one):

Large Accelerated Filer ☐ Accelerated Filer ☐ Non-Accelerated Filer ☐Smaller Reporting Company ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐No☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $27,005,000

The number of shares of the Registrant’s Common Stock outstanding as of February 15, 2016 was 82,883,562.

Documents incorporated by reference: To the extent herein specifically referenced in Part III, portions of the Registrant’s Definitive Proxy Statement on Schedule 14A for the 2014 Annual General Meeting of Shareholders are incorporated herein. See Part III.

|

|

Page |

| 1 | |

| 6 | |

| 6 | |

| 6 | |

| 6 | |

| 9 | |

| 13 | |

| 20 | |

| 20 | |

| 35 | |

| 35 | |

| 36 | |

|

ITEM 6. SELECTED FINANCIAL DATA |

NA |

|

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

38 |

|

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

NA |

| 46 | |

|

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

66 |

| 66 | |

| 67 | |

|

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE |

67 |

| 67 | |

| 67 | |

| 67 | |

| 68 | |

| 68 | |

CAUTIONARY NOTE TO U.S. INVESTORS REGARDING ESTIMATES OF MEASURED, INDICATED AND INFERRED RESOURCES AND PROVEN AND PROBABLE RESERVES

The terms “mineral reserve”, “proven mineral reserve” and “probable mineral reserve” are Canadian mining terms defined in Canadian National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) – CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended (the “CIM Definition Standards”). These definitions differ from the definitions in the United States Securities and Exchange Commission (“SEC”) Industry Guide 7 (“SEC Industry Guide 7”) under the United States Securities Act of 1933, as amended (the “Securities Act”). Under SEC Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report reserves, the three-year historical average price is used in any reserve or cash flow analysis to designate reserves, and the primary environmental analysis or report must be filed with the appropriate governmental authority.

In addition, the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in and required to be disclosed by NI 43-101; however, these terms are not defined terms under SEC Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that all or any part of a mineral deposit in these categories will ever be converted into reserves. “Inferred mineral resources” have a great amount of uncertainty as to their existence, and great uncertainty as to their economic, technical and legal feasibility. It cannot be assumed that all, or any part, of an inferred mineral resource will ever be upgraded to a higher category. Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically, technically or legally mineable. Disclosure of “contained ounces” in a resource is permitted disclosure under Canadian regulations; however, the SEC normally only permits issuers to report mineralization that does not constitute “reserves” by SEC standards as in place tonnage and grade without reference to unit measures.

Accordingly, information contained in this report and the documents incorporated by reference herein contain descriptions of our mineral deposits that may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

The term “mineralized material” as used in this annual report on Form 10-K, although permissible under SEC Industry Guide 7, does not indicate “reserves” by SEC Industry Guide 7 standards. We cannot be certain that any part of the mineralized material will ever be confirmed or converted into SEC Industry Guide 7 compliant “reserves”. Investors are cautioned not to assume that all or any part of the mineralized material will ever be confirmed or converted into reserves or that mineralized material can be economically or legally extracted.

“acid rock drainage (ARD)” results from the interaction of meteoric water with oxidizing sulfide minerals.

“arsenopyrite” means an iron arsenic sulfide. It is the most common arsenic mineral and the primary ore of arsenic metal.

“assay” means to test ores or minerals by chemical or other methods for the purpose of determining the amount of valuable metals contained.

“bedding” means the characteristic structure of sedimentary rock in which layers of different composition, grain size or arrangement are layered one on top of another in a sequence with oldest on the bottom and youngest at the top.

“bismuthinite” means a mineral consisting of bismuth sulfide; it is an ore for bismuth.

“chalcopyrite” means a brass-yellow colored sulfide of copper and iron. It is a copper mineral.

1

“claim” means a mining title giving its holder the right to prospect, explore for and exploit minerals within a defined area.

“clastic” refers to sedimentary rock (such as shale or siltstone) or sediment. An accumulation of transported weathered debris.

“comminution” means the process in which solid materials are broken into small fragments by crushing, grinding, and other processes.

“conglomerate” refers to clastic sedimentary rock that contains large (greater than two millimeters in diameter) rounded particles. The space between the pebbles is generally filled with smaller particles and/or a chemical cement that binds the rock together.

“cut-off grade” means the grade below which mineralized material will be considered waste.

“deposit” is an informal term for an accumulation of mineralized material.

“exploration stage enterprise” refers to an issuer engaged in the search for mineral deposits (reserves) which are not in either the development or production stage, per SEC Industry Guide 7. A development stage enterprise is engaged in the preparation of an established, commercially minable deposit (reserve) which is not in the production stage. A production stage enterprise is engaged in the exploitation of commercially viable mineral deposits (reserves).

“facies” means the characteristics of a rock mass that reflects its depositional environment.

“fault” means a fracture in rock along which there has been displacement of the two sides parallel to the fracture.

“feasibility study” is a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of realistically assumed mining, processing, metallurgical, economic, marketing, legal, environmental, social and governmental considerations together with any other relevant operational factors and detailed financial analysis, that are necessary to demonstrate at the time of reporting that extraction is reasonably justified or economically viable. The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project. The confidence level of the study will be higher than that of a pre-feasibility study.

“felsic” is a term used to describe an igneous rock that has a large percentage of light-colored minerals such as quartz, feldspar and muscovite. Felsic rocks are generally rich in silicon and aluminum and contain only small amounts of magnesium and iron.

“ferruginous” means containing iron oxides or rust.

“foliation” means planar arrangement of structural or textural features in any rock type.

“fold” is a bend or flexure in a rock unit or series of rock units caused by crust movements.

“g Au/tonne” or “g Au/t” means grams of gold per tonne.

“galena” means a lead sulfide mineral commonly found in hydrothermal veins; it is the primary ore of lead.

“geosyncline” means a major trough or downwarp of the Earth’s crust, in which great thicknesses of sedimentary and/or volcanic rocks have accumulated.

“granitoid” means a variety of coarse grained plutonic rock similar to granite, which are composed predominantly of feldspar or quartz.

2

“greywackes” means fine-grained sandstone generally characterized by its hardness, dark color and poorly sorted angular grains of quarts, feldspar and small rock fragments set in a compact, clay-fine matrix.

“heap leach” means a gold extraction method that percolates a cyanide solution through ore heaped on an impermeable pad or base.

“hornfels” refers to nonfoliated metamorphic rock that is typically formed by contact metamorphism around igneous intrusions.

“indicated mineral resource” and “indicated resource” means “indicated mineral resource” as defined by the CIM in the CIM Definition Standards and is that part of a mineral resource for which quantity, grade or quality, densities, shape and physical characteristics can be estimated with sufficient confidence to allow the appropriate application of technical and economic parameters in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation. An indicated mineral resource has a lower level of confidence than that applying to a measured mineral resource and may only be converted to a probable mineral reserve.

“inferred mineral resource” and “inferred resource” means “inferred mineral resource” as defined by the CIM in the CIM Definition Standards and is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An inferred mineral resource has a lower level of confidence than that applying to an indicated mineral resource and must not be converted to a mineral reserve. It is reasonably expected that the majority of inferred mineral resources could be upgraded to indicated mineral resources with continued exploration.

“intrusion” refers to an igneous rock body that formed from magma that forced its way into, through or between subsurface rock units.

“intrusives” refers to igneous rocks that crystallize below the earth’s surface.

“ironstone” is a sedimentary rock, either deposited directly as a ferruginous sediment or created by chemical replacement, that contains a substantial proportion of an iron compound from which iron either can be or once was smelted commercially.

“joint” means a fracture in a rock along which there has been no displacement.

“measured mineral resource” means “measured mineral resource” as defined by the CIM in the CIM Definition Standards and is that part of a mineral resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with confidence sufficient to allow the application of technical and economic parameters to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation. A measured mineral resource has a higher level of confidence than that applying to either an indicated mineral resource or an inferred mineral resource. It may be converted to a proven mineral reserve or to a probable mineral reserve.

“mica” any of a group of phyllosilicate minerals having similar chemical compositions and highly perfect basal cleavage.

“mineral reserve” means the economically mineable part of a measured mineral resource and/or indicated mineral resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at pre-feasibility or feasibility level as appropriate that include application of mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified.

3

“mineral resource” means a concentration or occurrence of solid material of economic interest in or on the earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a mineral resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling.

“mineralization” means the concentration of valuable minerals within a body of rock.

“mineralized material” under SEC Industry Guide 7 is a mineralized body that has been delineated by appropriately spaced drilling and/or underground sampling to support a sufficient tonnage and average grade of metal(s). Such a deposit does not qualify as a reserve until a comprehensive evaluation based upon unit cost, grade, recoveries, and other material factors conclude legal and economic feasibility. Mineralized material is equivalent to measured plus indicated mineral resources but does not include inferred mineral resources.

“mudstone” is a fine grained sedimentary rock whose original constituents were clays or muds.

“ore” means material containing minerals in such quantity, grade and chemical composition that they can be economically extracted.

“oxide” means mineralized rock in which some of the original minerals have been oxidized (i.e., combined with oxygen). Oxidation tends to make the ore more porous and permits a more complete permeation of cyanide solutions so that minute particles of gold in the interior of the minerals will be more readily dissolved.

“preliminary economic assessment” and “PES” as defined by NI 43-101 is a study, other than a pre-feasibility study or feasibility study, that includes an economic analysis of the potential viability of mineral resources.

“preliminary feasibility study”, “PFS” and “pre-feasibility study” as defined by the CIM is a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the realistically assumed mining, processing, metallurgical, economic, marketing, legal, environmental, social and government considerations and the evaluation of any other relevant factors which are sufficient for a qualified person, acting reasonably, to determine if all or part of the mineral resource may be converted to a mineral reserve at the time of reporting. A pre-feasibility study is at a lower confidence level than a feasibility study.

“probable reserves” under SEC Industry Guide 7 means reserves for which quantity and grade and/or quality are computed from information similar to that used for proven reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven reserves, is high enough to assume continuity between points of observation.

“probable mineral reserves” as defined by the CIM in the CIM Definition Standards is the economically mineable part of an indicated and, in some circumstances, a measured mineral resource. The confidence in the mining, processing, metallurgical, economic, and other relevant factors applying to a probable mineral reserve is lower than that applying to a proven mineral reserve.

“proven reserves” under SEC Industry Guide 7 means reserves for which (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling and (b) the sites for inspection, sampling and measurement are spaced so closely and the geologic character is so well defined that size, shape, depth and mineral content of reserves are well established.

“proven mineral reserves”, as defined by the CIM in the CIM Definition Standards, is the economically mineable part of a measured mineral resource A proven mineral reserve implies a high degree of confidence in the mining, processing, metallurgical, economic and other relevant factors.

4

“pyrrhotite” means a bronze-colored magnetic ferrous sulfide mineral consisting of iron and sulfur.

“pyrite” means a pale brass-yellow colored iron sulfide mineral consisting of iron and sulfur.

“qualified person” as defined under NI 43-101 means an individual who (a) is an engineer or geoscientist with a university degree, or equivalent accreditation, in an area of geoscience, or engineering, relating to mineral exploration or mining; (b) has at least five years of experience in mineral exploration, mine development or operation, or mineral project assessment or any combination of these that is relevant to his or her professional degree or area of practice; (c) has experience relevant to the subject matter of the mineral project and the technical report; (d) is in good standing with a professional association; and (e) in the case of a professional association in a foreign jurisdiction, has a membership designation that (i) requires attainment of a position of responsibility in their profession that requires the exercise of independent judgment; and (ii) requires (A) a favorable, confidential peer evaluation of the individual’s character, professional judgment, expertise and ethical fitness; or (B) a recommendation for membership by at least two peers, and demonstrated prominence or expertise in the field of mineral exploration or mining. Note: a professional association is a self-regulatory organization of engineers, geoscientists or both that, among other criteria, requires compliance with the professional standards of competence and ethics established by the organization and has disciplinary powers over its members.

“recovery” means that portion of the metal contained in the ore that is successfully extracted by processing and is expressed as a percentage.

“sampling” means selecting a fractional, but representative, part of a mineral deposit for analysis.

“schist” is a metamorphic rock containing abundant particles of mica, characterized by strong foliation and originating from a metamorphism in which directed pressure played a significant role.

“sediment” means solid material settled from suspension in a liquid.

“sedimentary rock” means rock formed from the accumulation and consolidation of sediment, usually in layered deposits.

“shale” is a fine grained, clastic sedimentary rock composed of mud that is a mix of flakes of clay minerals and tiny fragments (silt-sized particles) or other minerals, especially quartz and calcite.

“silicified” means to become converted into or impregnated with silica.

“siltstone” is a sedimentary rock that has a grain size in the silt range, finer than sandstone and coarser than claystones.

“sphalerite” means a zinc sulfide mineral commonly found in hydrothermal veins; it is the primary ore of zinc.

“strike” when used as a noun, means the direction, course or bearing of a vein or rock formation measured on a level surface and, when used as a verb, means to take such direction, course or bearing.

“sulfide” means a compound of sulfur and some other element. From a metallurgical perspective, sulfide rock is primary ore that has not been oxidized. Both ore and waste may contain sulfide minerals.

“tailings” means material rejected from a mill after most of the valuable minerals have been extracted.

“tonne” means a metric tonne and has the weight of 1,000 kg or 2,204.6 pounds.

“tpd” means tonnes per day.

“tuffs” are a type of rock consisting of consolidated volcanic ash ejected from vents during a volcanic eruption.

5

“vein” means a fissure, fault or crack in a rock filled by minerals that have traveled upwards from some deep source.

“waste” means rock lacking sufficient grade and/or other characteristics of ore.

In this annual report on Form 10-K, unless the context otherwise requires, the terms “we”, “us”, “our”, “Vista”, “Vista Gold”, or the “Company” refer to Vista Gold Corp. and its subsidiaries.

References to C$ refer to Canadian currency, A$ to Australian currency and $ to United States currency. All dollars amounts are expressed in thousands of dollars except references to per ounce and per share amounts.

|

To Convert Imperial Measurement Units |

|

To Metric Measurement Units |

|

Multiply by |

|

|

Acres |

|

Hectares |

|

0.4047 |

|

|

Feet |

|

Meters |

|

0.3048 |

|

|

Miles |

|

Kilometers |

|

1.6093 |

|

|

Tons (short) |

|

Tonnes |

|

0.9071 |

|

|

Gallons |

|

Liters |

|

3.785 |

|

|

Ounces (troy) |

|

Grams |

|

31.103 |

|

|

Ounces (troy) per ton (short) |

|

Grams per tonne |

|

34.286 |

|

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report, including all exhibits hereto and any documents that are incorporated by reference as set forth on the face page under “Documents incorporated by reference”, contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 and forward-looking information under Canadian securities laws that are intended to be covered by the safe harbor created by such legislation. All statements, other than statements of historical facts, included in this annual report on Form 10-K, our other filings with the SEC and Canadian securities commissions and in press releases and public statements by our officers or representatives that address activities, events or developments that we expect or anticipate will or may occur in the future are forward-looking statements and forward-looking information, including, but not limited to, such things as those listed below:

|

· |

the Company’s ability to sustain its fixed costs at $1,400 to $1,600 per quarter for the foreseeable future; |

|

· |

the ability to fund the Company’s currently planned programs into 2018; |

|

· |

the potential monetization of our non-core assets, including our mill equipment which is for sale; |

|

· |

our expectation that future R&D grants from the Government of Australia, if any, will be significantly smaller than those received in 2015; |

|

· |

our belief that we will obtain Environmental Protection and Biodiversity Conservation Act 1999 authorization in early 2016; |

|

· |

our belief that we have positioned the Company to judiciously pursue near-term value creating opportunities; |

|

· |

the nature and magnitude of future discretionary programs, if any, and the availability of funding for such programs; |

|

· |

our ability to quickly advance Mt Todd (defined in “Item 1: Business” below) to development when economic conditions permit; |

|

· |

estimates of future operating and financial performance; |

6

|

· |

potential funding requirements and sources of capital, including near-term sources of additional cash; |

|

· |

our expectation that the Company will continue to incur losses and will not pay dividends for the foreseeable future; |

|

· |

our intention to continue cost management efforts; |

|

· |

our expectation that market conditions will not improve for the foreseeable future; |

|

· |

our expectation that raising capital for mining companies without producing assets will continue to be difficult for the foreseeable future, and the potential impact of this on our ability to raise capital in sufficient amounts on reasonable terms; |

|

· |

our planned deferral of significant development programs until market conditions improve; |

|

· |

our potential ability to generate proceeds from operations or the disposition of our assets; |

|

· |

the timing, performance and results of feasibility studies; |

|

· |

plans and anticipated effects of holding 4.9% of the outstanding Midas Gold Shares (defined in “Item 1: Business” below); |

|

· |

our potential entry into agreements to find, lease, purchase, option or sell mineral interests; |

|

· |

plans for evaluation and advancement of Mt Todd; |

|

· |

our ability to raise sufficient capital (approximately $2,500) to complete a feasibility study of Mt Todd; |

|

· |

our ability to complete the Mt Todd feasibility study within six months of commencement; |

|

· |

the feasibility of Mt Todd; |

|

· |

our expectation of Mt Todd’s impact, including environmental and economic impacts; |

|

· |

plans and estimates concerning potential project exploration and development, including the use of high pressure grinding roll crushers and access to a water supply, as well as the ability to obtain required permits; |

|

· |

our belief that we are in compliance in all material respects with applicable mining, health, safety and environmental statutes and regulations in all of the jurisdictions in which we operate; |

|

· |

our belief that we maintain reasonable amounts of insurance; |

|

· |

estimates of mineral reserves and mineral resources; |

|

· |

our intention to seek partners to advance the Guadalupe de los Reyes project; |

|

· |

potential changes in regulations or taxation initiatives; |

|

· |

our belief that adopting the guidelines proposed by the Financial Accounting Standards Board in 2016 will not materially impact our financial statements; and |

|

· |

our expectation that we will continue to be a passive foreign investment company (“PFIC”). |

7

Forward-looking statements and forward-looking information have been based upon our current business and operating plans, as approved by the Company’s Board of Directors (the “Board”); our cash and other funding requirements and timing and sources thereof; results of pre-feasibility and feasibility studies, mineral resource and reserve estimates, preliminary economic assessments and exploration activities; advancements of the Company’s required permitting processes; current market conditions and project development plans. The words “estimate,” “plan,” “anticipate,” “expect,” “intend,” “believe,” “will,” “may” and similar expressions are intended to identify forward-looking statements and forward-looking information. These statements involve known and unknown risks, uncertainties, assumptions and other factors which may cause our actual results, performance or achievements to be materially different from any results, performance or achievements expressed or implied by such forward-looking statements and forward-looking information. These factors include risks such as:

|

· |

our ability to raise additional capital or raise funds from the sale of non-core assets on favorable terms, if at all; |

|

· |

pre-feasibility and feasibility study results and preliminary assessment results and the accuracy of estimates and assumptions on which they are based; |

|

· |

resource and reserve estimate results, the accuracy of such estimates and the accuracy of sampling and subsequent assays and geologic interpretations on which they are based; |

|

· |

technical and operational feasibility and the economic viability of deposits; |

|

· |

our ability to obtain, renew or maintain the necessary authorizations and permits for Mt Todd, including its development plans and operating activities; |

|

· |

the timing and results of a feasibility study on Mt Todd; |

|

· |

delays in commencement of construction at Mt Todd; |

|

· |

our ability to secure the permits for Mt Todd; |

|

· |

increased costs that affect our operations or our financial condition; |

|

· |

our reliance on third parties to fulfill their obligations under agreements with us; |

|

· |

whether projects not managed by us will comply with our standards or meet our objectives; |

|

· |

a shortage of skilled labor, equipment and supplies; |

|

· |

whether our acquisition, exploration and development activities, as well as the realization of the market value of our assets, will be commercially successful and whether any transactions we enter into will maximize the realization of the market value of our assets; |

|

· |

trading price of our securities and our ability to raise funds in new share offerings due to future sales of common shares in the public or private market; |

|

· |

the lack of cash dividend payments by us; |

|

· |

the success of future joint ventures, partnerships and other arrangements relating to our properties; |

|

· |

industry consolidation which could result in the acquisition of a control position in the Company for less than fair value; |

|

· |

the market price of the securities held by us; |

|

· |

our ability to timely monetize our Midas Gold Shares; |

|

· |

perception of potential environmental impact of Mt Todd; |

|

· |

reclamation liabilities, including reclamation requirements at Mt Todd; |

|

· |

our history of losses from operations; |

|

· |

future water supply issues at Mt Todd; |

8

|

· |

litigation or other legal claims; |

|

· |

environmental lawsuits; |

|

· |

lack of adequate insurance to cover potential liabilities; |

|

· |

our ability to attract, retain and hire key personnel; |

|

· |

fluctuations in the price of gold; |

|

· |

volatility in our stock price; |

|

· |

inherent hazards of mining exploration, development and operating activities; |

|

· |

the accuracy of calculations of mineral reserves, mineral resources and mineralized material fluctuations therein based on metal prices, and inherent vulnerability of the ore and recoverability of metal in the mining process; |

|

· |

changes in environmental regulations to which our exploration and development operations are subject; |

|

· |

changes in climate change regulations could result in increased operating costs; |

|

· |

intense competition in the mining industry; |

|

· |

potential challenges to the title to our mineral properties; |

|

· |

political and economic instability in Mexico; |

|

· |

tax initiatives on domestic and international levels; |

|

· |

fluctuation in foreign currency values; and |

|

· |

our likely status as a PFIC for U.S. federal tax purposes. |

For a more detailed discussion of such risks and other important factors that could cause actual results to differ materially from those in such forward-looking statements and forward-looking information, please see “Item 1A. Risk Factors” below in this annual report on Form 10-K. Although we have attempted to identify important factors that could cause actual results to differ materially from those described in forward-looking statements and forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that these statements will prove to be accurate as actual results and future events could differ materially from those anticipated in the statements. Except as required by law, we assume no obligation to publicly update any forward-looking statements and forward-looking information, whether as a result of new information, future events or otherwise.

Overview

Vista Gold Corp. and its subsidiaries (collectively, “Vista,” the “Company,” “we,” “our,” or “us”) are engaged in the gold mining industry. We are focused on the evaluation, acquisition, exploration and advancement of gold exploration and potential development projects which may lead to gold production or value adding strategic transactions such as earn-in right agreements, option agreements, royalty agreements, leases to third parties, joint venture arrangements with other mining companies, or outright sales of assets for cash and/or other consideration. We look for opportunities to improve the value of our gold projects through exploration drilling and/or technical studies focused on optimizing previous engineering work.

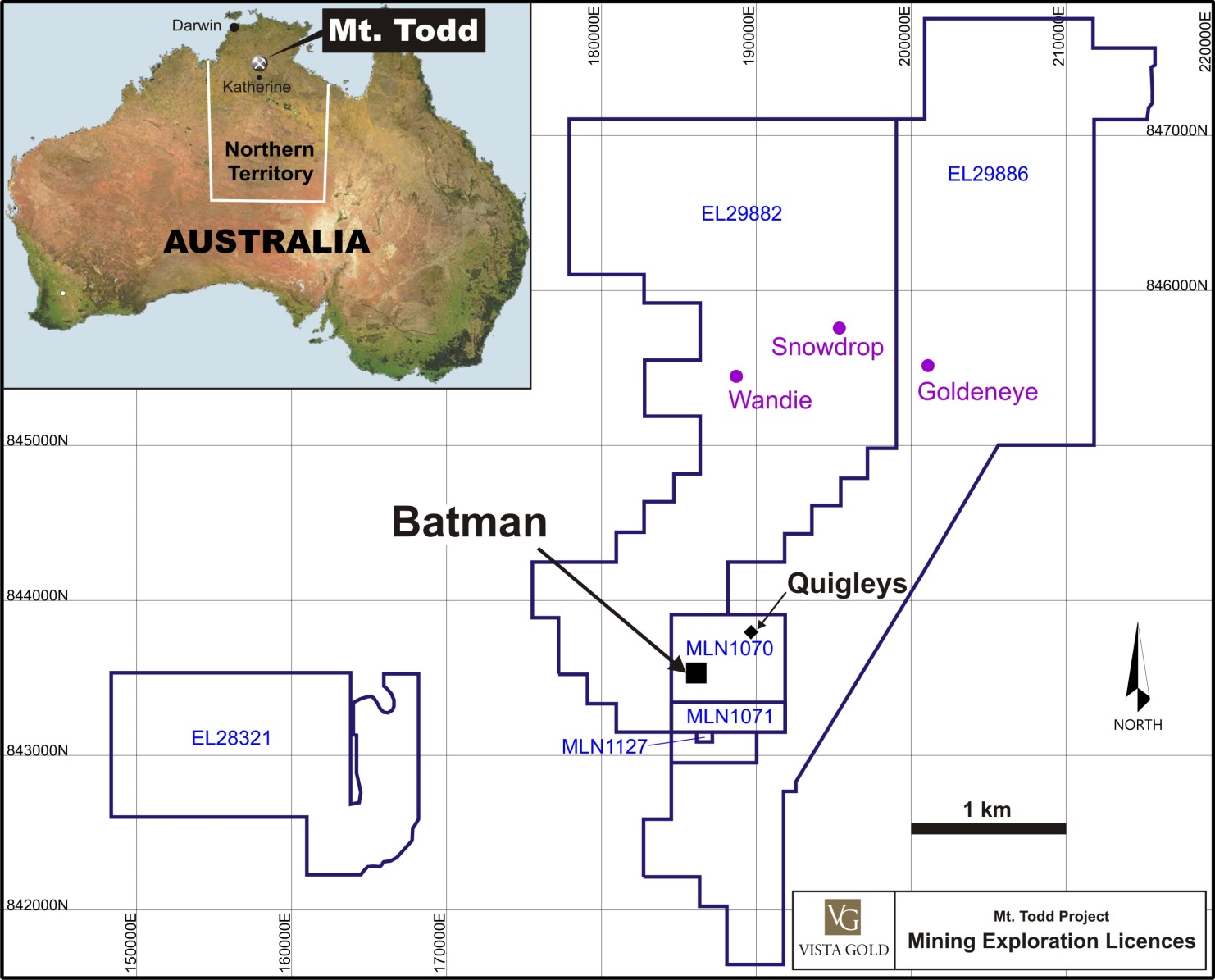

The Company’s flagship asset is its 100% owned Mt Todd gold project (“Mt Todd”) in Northern Territory (“NT”), Australia. Completion of a feasibility study or the development of the project is not justified at this time due to the current low gold price. With the completion of the environmental impact statement (“EIS”) in 2014 and the previous completion of a significant amount of the project engineering and design, much of which is contained in the previously

9

released preliminary feasibility study, management believes that the permitting risk is substantially reduced and the potential development timeline at Mt Todd is well defined. We believe that we are well positioned, subject to sustained improvement in gold prices, to move forward quickly with the completion of the Mt Todd feasibility study. At the time the May 2013 PFS was completed, because of the high level of detail in the work completed for the study, it was estimated that the feasibility study could be completed within six months of its start at a cost of approximately $2,500.

We do not currently generate cash flows from mining operations. The prices for gold equities, particularly those with early stage projects, have decreased significantly during the past few years, and capital raising on reasonable terms has become more difficult for mining companies which do not have producing assets. These market conditions are expected to continue for the foreseeable future, and could affect our ability to raise sufficient capital to advance Mt Todd on reasonable terms, if at all.

Since 2013 we have raised sufficient cash to operate our business without share dilution, and we have significantly reduced our costs to strengthen our balance sheet and mitigate the effects of these difficult markets. We believe we have sufficient cash to fund our currently planned programs into 2018, while retaining opportunities to access additional financing from non-dilutive sources such as the sale of our used mill equipment and monetization of other non-core assets.

We plan to continue to evaluate and execute programs that could position us to quickly advance Mt Todd to development when economic conditions permit. In addition, with our improved treasury and strong management team we are in a position to judiciously evaluate and pursue other near-term value creating opportunities.

Vista Gold Corp. was originally incorporated on November 28, 1983 under the name “Granges Exploration Ltd.” It amalgamated with Pecos Resources Ltd. during June 1985 and continued as Granges Exploration Ltd. In June 1989, Granges Exploration Ltd. changed its name to Granges Inc. Granges Inc. amalgamated with Hycroft Resources & Development Corporation during May 1995 and continued as Granges Inc. Effective November 1996, Da Capo Resources Ltd. and Granges, Inc. amalgamated under the name “Vista Gold Corp.” and, effective December 1997, Vista Gold continued from British Columbia to the Yukon Territory, Canada under the Business Corporations Act (Yukon Territory). On June 11, 2013, Vista Gold continued from the Yukon Territory, Canada to the Province of British Columbia, Canada under the Business Corporations Act (British Columbia). The current addresses, telephone and facsimile numbers of our offices are:

|

Executive Office |

|

Registered and Records Office |

|

Suite 5 - 7961 Shaffer Parkway |

|

1200 Waterfront Centre – 200 Burrard Street |

|

Littleton, Colorado, USA 80127 |

|

Vancouver, British Columbia, Canada V7X 1T2 |

|

Telephone: (720) 981-1185 |

|

Telephone: (604) 687-5744 |

|

Facsimile: (720) 981-1186 |

|

Facsimile: (604) 687-1415 |

10

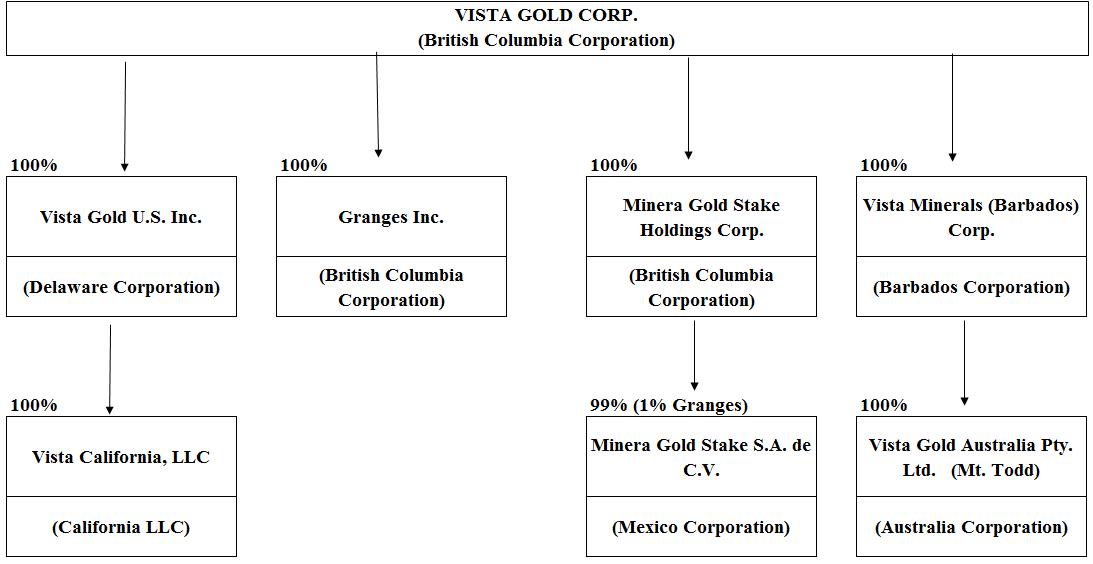

Corporate Organization Chart

The name, place of incorporation, continuance or organization and percent of equity securities that we own or control as of February 15, 2016 for each of its subsidiaries is set out below.

Employees

As of December 31, 2015, we had 13 employees globally. In addition, we use consultants with specific skills to assist with various aspects of our project evaluation, due diligence, corporate governance and property management.

Geographic and Segment Information

We have one reportable segment, consisting of evaluation, acquisition and exploration activities which are focused principally in Australia and North America. We evaluate, acquire, explore and advance gold exploration and potential development projects, which may lead to gold production or value adding strategic transactions. These activities are focused principally in Australia and North America. We reported no operating revenues during the years ended December 31, 2015 and 2014. Geographic location of mineral properties and plant and equipment is provided in Notes 4 – Mineral Properties and 5 – Plant and Equipment to our Consolidated Financial Statements under the section heading “Item 8. Financial Statements and Supplementary Data” below

Significant Developments in 2015

In 2015, the Company received an A$13,470 ($10,220) Research & Development (“R&D”) Tax Incentive refund, net of costs to prepare and file. These amounts were paid under the Australian Government’s R&D Tax Incentive Program, a program designed to encourage industry to engage in R&D activities that benefit Australia; and relate to costs we incurred during the 2012 and 2013 fiscal years for qualifying R&D programs. This R&D Tax Incentive program is a self-assessment process, and as such, the Australian Government has the right to review the qualifying programs and expenditures for a period of four years.

In March 2015, we sold 8,000,000 Midas Gold Corp. common shares (“Midas Gold Shares”) for net proceeds of $2,772.

11

In January 2015, the Company amended the payment terms for the sale of its 100% interest in the Los Cardones gold project in Baja California Sur, Mexico. Under the amended terms the Company accepted a final payment of $2,994, net of legal costs, for the project.

See the section heading “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations – Financial Position, Liquidity and Capital Resources”, below.

Reclamation

We generally will be required to mitigate long-term environmental impacts by stabilizing, contouring, re-sloping and revegetating various portions of a site after mining and mineral processing operations are completed. These reclamation efforts would be conducted in accordance with detailed plans, which must be reviewed and approved by the appropriate regulatory agencies.

The Mt Todd site was not reclaimed when the mine closed in the late 1990’s. Liability for the reclamation of the environmental conditions existing prior to Vista’s involvement with the project remains the responsibility of the NT Government until 30 days after we have provided notice to the NT Government that we intend to take over and assume the management, operation and rehabilitation of Mt Todd. Vista will not give such notice until a production decision has been made, the project is fully permitted to construct the mine, and the necessary financing for construction has been arranged.

Government Regulation

Our exploration and development activities are subject to various national, state, provincial and local laws and regulations in the United States, Mexico, Australia, and other jurisdictions, which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances and other matters. We have obtained or have pending applications for those licenses, permits or other authorizations currently required to conduct our exploration and other programs. We believe that we are in compliance in all material respects with applicable mining, health, safety and environmental statutes and regulations in all of the jurisdictions in which we operate. Management of the Company is not aware of any current orders or directions relating to us with respect to the foregoing laws and regulations.

Australia Laws

Mineral projects in the Northern Territory are subject to Australian federal and Northern Territory laws and regulations regarding environmental matters and the discharge of hazardous wastes and materials. As with all mining projects, Mt Todd would be expected to have a variety of environmental impacts should development proceed. We are required under Australian laws and regulations (federal, state and territorial) to acquire permits and other authorizations before Mt Todd can be developed and mined. In Australia, environmental legislation plays a significant role in the mining industry. Various environmental documents, such as the Mt Todd EIS, covering studies on inter alia, air, water, pollution, hazardous and toxic wastes, reclamation of mining area, etc., must be prepared and submitted to the Northern Territory Minister for Mines & Energy and Environment and the Australian Government Minister For Sustainability, Environment, Water, Population and Communities for approval. During September 2014, the EIS for Mt Todd was approved. The Environmental Protection Agency of the Northern Territory Government (“NTEPA”) has advised that it has assessed the environmental impacts of the Mt Todd gold mine and concluded that it can proceed, subject to a number of recommendations which are outlined in the assessment report. We must also comply with Aboriginal heritage legislation requirements, which require heritage survey work to be undertaken prior to the commencement of mining operations. All these recommendations/conditions may result in the occurrence of significant pre-production costs and may delay potential production at Mt Todd.

Environmental Regulation

Our projects are subject to various federal, state and local laws and regulations governing protection of the environment. These laws are continually changing and, in general, are becoming more restrictive. Our policy is to conduct business in

12

a way that safeguards public health and the environment. We believe that our operations are conducted in material compliance with applicable laws and regulations.

Changes to current local, state or federal laws and regulations in the jurisdictions where we operate could require additional capital expenditures and increased operating and/or reclamation costs. We are unable to predict what additional legislation, if any, might be proposed or enacted, and additional regulatory requirements could impact the economics of our projects.

During 2015, none of our project sites had any material non-compliance occurrences with any applicable environmental regulations.

Competition

We compete with other mining companies in connection with the acquisition, exploration, financing and development of gold properties. There is competition for the limited number of gold acquisition and exploration opportunities, some of which is with other companies having substantially greater financial resources than we have. As a result, we may have difficulty acquiring attractive gold projects at reasonable prices. We use consultants and compete with other mining companies for the man hours of consulting time required to complete our studies. We also compete with other mining companies for mining engineers, geologists and other skilled personnel in the mining industry and for exploration and development services.

Gold Price History

The price of gold is volatile and is affected by numerous factors, all of which are beyond our control, such as the sale or purchase of gold by various central banks and financial institutions, inflation, recession, fluctuation in the relative values of the U.S. dollar and foreign currencies, changes in global gold demand and political and economic conditions.

The following table presents the high, low and average afternoon fixed prices in U.S. dollars for an ounce of gold on the London Bullion Market over the past five years:

|

Year |

|

High |

|

Low |

|

Average |

|

|||

|

2011 |

|

$ |

1,895 |

|

$ |

1,319 |

|

$ |

1,571 |

|

|

2012 |

|

|

1,792 |

|

|

1,540 |

|

|

1,669 |

|

|

2013 |

|

|

1,694 |

|

|

1,192 |

|

|

1,411 |

|

|

2014 |

|

|

1,385 |

|

|

1,142 |

|

|

1,266 |

|

|

2015 |

|

|

1,296 |

|

|

1,049 |

|

|

1,160 |

|

|

2016 (to February 15, 2016) |

|

|

1,241 |

|

|

1,077 |

|

|

1,126 |

|

Data Source: www.kitco.com

Available Information

We make available, free of charge, on or through our Internet website, at www.vistagold.com, our annual report on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the U.S. Securities Exchange Act of 1934. Our Internet website and the information contained therein or connected thereto are not intended to be, and are not, incorporated into this annual report on Form 10-K.

An investment in our securities involves a high degree of risk. The risks described below are not the only ones facing the Company or otherwise associated with an investment in our securities. Additional risks not presently known to us or which we currently consider immaterial may also adversely affect our business. If any of the following risks actually occur, our business, financial condition and operating results could be materially adversely affected.

13

Operating Risks

We cannot be assured that Mt Todd is feasible or that a feasibility study will accurately forecast operating results.

Mt Todd is our principal asset. Our future profitability depends largely on the economic feasibility of the project. Before arranging financing for Mt Todd, we will have to complete a feasibility study. There can be no assurance that the results of the feasibility study will be positive or that such study will be completed when expected. If the Mt Todd feasibility study is favorable, and if the project can be financed, there is no assurance that actual production rates, revenues, capital and operating costs at Mt Todd will not vary unfavorably from the estimates and assumptions included in the feasibility study.

Mt Todd requires substantial capital investment and we may be unable to raise sufficient capital on favorable terms or at all.

The construction and operation of Mt Todd will require significant capital. Our ability to raise sufficient capital will depend on several factors, including a favorable feasibility study, acquisition of the requisite permits, macroeconomic conditions, and future gold prices. Uncontrollable factors such as lower gold prices, unanticipated operating or permitting challenges, perception of environmental impact, illiquidity in the debt markets or a further dislocation in the gold mining equity markets as experienced in recent years, could prohibit our ability to finance Mt Todd on acceptable terms, if at all.

If we decide to construct the mine at Mt Todd, we will be assuming certain reclamation obligations resulting in a material financial obligation.

The Mt Todd site was not reclaimed when the original mine closed. Although we are not currently responsible for the reclamation of these historical disturbances, we will accept full responsibility for them if and when we make a decision to finance and construct the mine and we provide 30 days notice to NT Government of our intention to take over and assume the management, operation and rehabilitation of Mt Todd. At that time, we will be required to provide a bond in a form satisfactory to the NT Government (in whose jurisdiction Mt Todd is located) that would cover the prospective expense of the reclamation of the property. In addition, the regulatory authorities may increase reclamation and bonding requirements from time to time. The satisfaction of these bonding requirements and continuing or future reclamation obligations will require a significant amount of capital.

We may not be able to get the required permits to begin construction at Mt Todd in a timely manner or at all.

Any delay in acquiring the requisite permits, or failure to receive required governmental approvals could delay or prevent the start of construction of Mt Todd. If we are unable to acquire permits to mine the property, then the project cannot be developed and operated; in addition the property will have no reserves under SEC Industry Guide 7 and NI 43-101, which would result in an impairment of the carrying value of the project.

There may be other delays in the construction of Mt Todd.

Delays in commencement of construction could result from factors such as availability and performance of engineering and construction contractors, suppliers and consultants; availability of required equipment; and availability of capital. Any delay in the performance of any one or more of the contractors, suppliers, consultants or other persons on which we depend, or lack of availability of required equipment, or delay or failure to receive required governmental approvals, or financing could delay or prevent commencement of construction at Mt Todd. There can be no assurance of whether or when construction at Mt Todd will start or that the necessary personnel, equipment or supplies will be available to the Company if and when construction is started.

14

Increased costs could impede our ability to become profitable.

Costs at any particular mining location frequently are subject to variation due to a number of factors, such as changing ore grade, changing metallurgy, and revisions to mine plans in response to the physical shape and location of the ore body. In addition, costs are affected by the price of commodities, fuel, electricity, operating supplies and labor. These costs are at times subject to volatile price movements, including increases that could make future production at Mt Todd less profitable or uneconomic. This could have a material adverse effect on our financial condition, cash flows and results of operations.

We cannot be assured that we will have an adequate water supply at Mt Todd.

Water at Mt Todd is expected to be provided from a fresh water reservoir which is fed by seasonal rains. Insufficient rainfall, or drought-like conditions in the area feeding the reservoir could limit or extinguish this water supply, and insufficient water resources may not be available leading to operations stopping until the water supply is replenished.

We could be subject to litigation or other legal claims.

Our assets or our business activities may be subject to disputes that may result in litigation or other legal claims. We may be required to respond to or defend against these claims which will divert resources away from our principal business. There can be no assurance that our defense of such claims would be successful, and we may be required to make material settlements. This could have a material adverse effect on our financial condition and cash flows, results of operations, and corporate reputation.

We rely on third parties to fulfill their obligations under agreements.

Our business strategy includes entering into agreements with third-parties (“Partners”) which may earn the right to obtain a majority interest in certain of our projects, in part by managing the respective project. Whether or not we hold a majority interest in a respective project, our Partner(s) may: (i) have economic or business interests or goals that are inconsistent with or opposed to ours; (ii) exercise veto rights to block actions that we believe to be in the best interests of the project; (iii) take action contrary to our policies or objectives; or (iv) as a result of financial or other difficulties, be unable or unwilling to fulfill their obligations under the respective joint venture, option, earn-in right or other agreement(s), such as contributing capital for the expansion or maintenance of projects. Any one or a combination of these could result in liabilities for us and/or could adversely affect the value of the related project(s) and, by association, damage our reputation and consequently our ability to acquire or advance other projects and/or attract future co-venturers.

Our exploration and development interests are subject to evolving environmental regulations.

Our property and royalty interests are subject to environmental regulation. Environmental legislation is becoming more restrictive in some countries or jurisdictions in a manner that will require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects and a heightened degree of responsibility for companies and their officers, directors and employees. There is no assurance that future changes in environmental regulation, if any, will not adversely affect our interests. Currently, our property and royalty interests are subject to government environmental regulations in Australia, Indonesia, Mexico and the U.S.

We could be subject to environmental lawsuits.

Neighboring landowners and other third parties could file claims based on environmental statutes and common law for personal injury and property damage allegedly caused by the release of hazardous substances or other waste material into the environment on or around our properties. There can be no assurance that our defense of such claims would be successful. This could have a material adverse effect on our business prospects, financial condition, results of operation, and corporate reputation.

15

There may be challenges to our title to mineral properties.

There may be challenges to our title to our mineral properties. If there are title defects with respect to any of our properties, we may be required to compensate other persons or perhaps reduce our interest in the affected property. Also, in any such case, the investigation and resolution of title issues could divert Company resources from our core strategies.

Our property and royalty interests in Mexico and Indonesia are subject to risks from political and economic instability.

We have property and royalty interests in Mexico and Indonesia that may be affected by risks associated with political or economic instability in those countries. The risks include, but are not limited to, military repression, extreme fluctuations in currency exchange rates, labor instability or militancy, mineral title irregularities and high rates of inflation. In addition, changes in mining or investment policies or shifts in political attitude in these countries may adversely affect our business. We may be affected in varying degrees by government regulation with respect to restrictions on production, price controls, export controls, income taxes, expropriation of property, maintenance of claims, environmental legislation, land use, land claims of local people, water use and mine safety. The effect of these factors cannot be accurately predicted.

Financial and Business Risks

A substantial or extended decline in gold prices would have a material adverse effect on the value of our assets, on our ability to raise capital and could result in lower than estimated economic returns.

The value of our assets, our ability to raise capital and our future economic returns are substantially dependent on the price of gold. The gold price fluctuates on a daily basis and is affected by numerous factors beyond our control. Factors tending to influence gold prices include:

|

· |

gold sales or leasing by governments and central banks or changes in their monetary policy, including gold inventory management and reallocation of reserves; |

|

· |

speculative short positions taken by significant investors or traders in gold; |

|

· |

the relative strength of the U.S. dollar; |

|

· |

expectations of the future rate of inflation; |

|

· |

interest rates; |

|

· |

changes to economic activity in the United States, China, India and other industrialized or developing countries; |

|

· |

geopolitical conflicts; |

|

· |

changes in jewelry, investment or industrial demand; |

|

· |

changes in supply from production, disinvestment and scrap; and |

|

· |

forward sales by producers in hedging or similar transactions. |

A substantial or extended decline in the gold price could:

|

· |

negatively impact our ability to raise capital on favorable terms, or at all; |

|

· |

jeopardize the development of Mt Todd; |

|

· |

reduce our existing estimated mineral resources and reserves by removing ores from these estimates that could not be economically processed at the lower gold price; |

|

· |

reduce the potential for future revenues from gold projects in which we have an interest; |

|

· |

reduce funds available to operate our business; and |

|

· |

reduce the market value of our assets, including our investment in Midas Gold Shares. |

Industry consolidation could result in the acquisition of a control position in the Company for less than fair value.

Consolidation within the industry is a growing trend. As a result of the broad market and industry factors including the price of gold, we believe the current market value of our common stock does not reflect the fair value of the Company’s

16

assets. These conditions could result in the acquisition of a control position, or attempted acquisition of a control position in the Company at what we believe to be less than fair value. This could result in substantial costs to us, divert our management’s attention and resources. A completed acquisition could result in realized losses of shareholder value.

We have a history of losses, and we do not expect to generate earnings from operations or pay dividends in the near term.

We are an exploration stage enterprise. As such, we devote our efforts to exploration, analysis and, if warranted, development of our projects. We do not currently produce gold and do not currently generate operating earnings from gold production. We finance our business activities principally by issuing equity and/or debt, and selling non-core assets. In addition, during 2015 we received refunds related to the Australian Government’s Research and Development Tax Incentive Program (“R&D Refunds”).

We have incurred losses in all periods since 1998, except for the year ended December 31, 2011, during which we recorded non-cash net gains, and the year ended December 31, 2015 during which we recorded gains related to R&D Refunds. We expect to continue to incur losses for the foreseeable future. We have no history of paying cash dividends and we do not expect to pay cash dividends or to make any similar distribution in the foreseeable future.

We may be unable to raise additional capital on favorable terms, if at all.

Our exploration and, if warranted, development activities and the construction and start-up of any mining operation require substantial amounts of capital. In order to develop Mt Todd, and/or to acquire attractive gold projects, we will have to raise additional funds from the sale of non-core assets and / or external sources. There can be no assurance that we will be successful in selling non-core assets or that additional financing will be available at all or on acceptable terms. If we cannot raise sufficient additional financing, we may have to substantially reduce or cease operations.

Our exploration and development activities or any acquisition activities may not be commercially successful.

Substantial expenditures are required to acquire gold properties, to establish mineral reserves through drilling and analysis, to develop metallurgical processes to extract metal from the ore and to develop the mining and processing facilities and infrastructure at any site chosen for mining. We cannot be assured that any mineral reserves or mineral resources acquired, established or discovered will be in sufficient quantities to justify commercial operations or that the funds invested in them will ever be recovered.

We face intense competition in the mining industry.

The mining industry is intensely competitive in all of its phases. Some of our competitors are much larger, established mining companies with greater financial and technical resources than ours. We compete with other mining companies for attractive mining claims, for capital, for equipment and supplies, for outside services and for qualified managerial and technical employees. Competition for capital has reduced the amount of capital available and increased the associated cost of raising capital. If we are unable to raise sufficient capital, we will be unable to execute exploration and development programs or such programs may be reduced in scope, which is what we have done at Mt Todd, for example. Competition for equipment and supplies could result in shortage of necessary supplies and/or increased costs. Competition for outside services could result in increased costs, reduced quality of service and/or delays in completing services. If we cannot successfully retain or attract qualified employees, our ability to advance the development of Mt Todd, to attract necessary financing, to meet all of our environmental and regulatory responsibilities, or to take opportunities to improve our business, could be negatively affected. This could have a material adverse effect on our results of operations, cash flows, financial condition and corporate reputation.

The occurrence of events for which we are not insured may affect our cash flow and overall profitability.

We maintain insurance policies that mitigate certain risks related to our operations. This insurance is maintained in amounts that we believe to be reasonable based on the circumstances surrounding each identified risk. However, we may elect not to have insurance for certain risks because of the high premiums associated with insuring those risks or for

17

various other reasons; in other cases, insurance may not be available for certain risks. We do not insure against political risk. Occurrence of events for which we are not insured could result in significant losses that could materially adversely affect our financial condition and our ability to fund our business.

Our stock price may be volatile and your investment in our common stock could suffer a decline in value.

Broad market and industry factors may adversely affect the price of our common stock, regardless of our actual operating performance. Factors that could cause fluctuation in the price of our common stock may include, among other things:

|

· |

changes in financial estimates by us or by any securities analysts who might cover our stock; |

|

· |

stock market price and volume fluctuations of other publicly traded companies and, in particular, those that are in the mining industry; |

|

· |

speculation about our business in the press or the investment community; |

|

· |

conditions or trends in our industry or the economy generally; |

|

· |

changes in the prices of gold; |

|

· |

announcements by us or our competitors of significant acquisitions, strategic partnerships or divestitures; |

|

· |

additions or departures of key personnel; and |

|

· |

sales of our common stock, including sales by our directors, officers or significant stockholders. |

In the past, securities class action litigation has often been instituted against companies following periods of volatility in their stock price. This type of litigation could result in substantial costs to us and divert our management’s attention and resources.

Currency fluctuations may adversely affect our costs.

We have material property interests in Australia. Most costs in Australia are incurred in the local currency. The appreciation of the Australian dollar against the U.S. dollar effectively increases our cost of doing business in Australia. This could have the effect of increasing the amount of capital required to continue to explore and develop Mt Todd, and/or reducing the pace at which it is developed.

The Company is likely a “passive foreign investment company,” which will likely have adverse U.S. federal income tax consequences for U.S. shareholders.

U.S. shareholders of our common shares should be aware that the Company believes it was classified as a PFIC during the taxable year ended December 31, 2015, and based on current business plans and financial projections, management believes there is a significant likelihood that the Company will be a PFIC during the current taxable year. If the Company is a PFIC for any year during a U.S. shareholder’s holding period, then such U.S. shareholder generally will be required to treat any gain realized upon a disposition of Common Shares, or any so-called “excess distribution” received on their Common Shares, as ordinary income, and to pay an interest charge on a portion of such gain or distributions, unless the shareholder makes a timely and effective “qualified electing fund” (“QEF Election”) or a “mark-to-market” election with respect to the Common Shares. A U.S. shareholder who makes a QEF Election generally must report on a current basis its share of the net capital gain and ordinary earnings for any year in which the Company is PFIC, whether or not the Company distributes any amounts to its shareholders. U.S. shareholders should be aware that there can be no assurance that the Company will satisfy record keeping requirements that apply to a QEF Election, or that the Company will supply U.S. shareholders with information that such U.S. shareholders require to report under the QEF Election rules, in event that the Company is a PFIC and a U.S. shareholder wishes to make a QEF Election. Thus, U.S. shareholders may not be able to make a QEF Election with respect to their Common Shares. A U.S. shareholder who makes the mark-to-market election generally must include as ordinary income each year the excess of the fair market value of the Common Shares over the taxpayer’s basis therein. This paragraph is qualified in its entirety by the discussion below in “Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities - “Certain U.S. Federal Income Tax Considerations.” Each U.S. shareholder should consult his or her own tax advisor regarding the U.S. federal, U.S. state and local, and foreign tax consequences of the PFIC rules and the acquisition, ownership, and disposition of Common Shares.

18

Industry Risks

Calculations of mineral reserves and mineral resources are estimates only and subject to uncertainty.

The estimating of mineral reserves and mineral resources is an imprecise process and the accuracy of such estimates is a function of the quantity and quality of available data, the assumptions used and judgments made in interpreting engineering and geological information and estimating future capital and operating costs. There is significant uncertainty in any reserve or resource estimate, and the economic results of mining an ore deposit may differ materially from the estimates.

Feasibility studies are estimates only and subject to uncertainty.

Feasibility studies are used to determine the economic viability of an ore deposit, as are pre-feasibility studies and preliminary economic assessments. Feasibility studies are the most detailed studies and reflect a higher level of confidence in the estimated production rates, and capital and operating costs. Generally accepted levels of confidence are plus or minus 15% for feasibility studies, plus or minus 25-30% for pre-feasibility studies and plus or minus 35-40% for preliminary economic assessments. These levels reflect the levels of confidence that exist at the time the study is completed. Subsequent changes to metal prices, foreign exchange rates (if applicable), reclamation requirements, operating and capital costs may differ materially from these estimates.

Mining companies are increasingly required to consider and provide benefits to the communities and countries in which they operate, and are subject to extensive environmental, health and safety laws and regulations.

As a result of public concern about the real or perceived detrimental effects of economic globalization and global climate impacts, businesses in general, and the mining industry in particular, face increasing public scrutiny of their activities. These businesses are under pressure to demonstrate that, as they seek to generate satisfactory returns on investment to shareholders, other stakeholders, including employees, governments, indigenous peoples, communities surrounding operations and the countries in which they operate, benefit and will continue to benefit from their commercial activities. The potential consequences of these pressures include reputational damage, legal suits, increased costs, increased social investment obligations, difficulty in acquiring permits; and pressure to increase taxes and royalties payable to governments and communities.

Mining exploration, development and operating activities are inherently hazardous.

Mineral exploration involves many risks that even a combination of experience, knowledge and careful evaluation may not be able to overcome. Operations in which we have direct or indirect interests will be subject to all the hazards and risks normally incidental to exploration, development and production of gold and other metals, any of which could result in work stoppages, damage to property, physical harm and possible environmental damage. The nature of these risks is such that liabilities might exceed any liability insurance policy limits. It is also possible that the liabilities and hazards might not be insurable, or, we could elect not to be insured against such liabilities due to high premium costs or other reasons, in which event, we could incur significant costs that could have a material adverse effect on our financial condition.

Regulations and pending legislation involving climate change could result in increased operating costs.

Gold production is energy intensive, resulting in a significant carbon footprint. A number of governments and/or governmental bodies have introduced or are contemplating regulatory changes in response to various climate change interest groups and the potential impact of climate change. This type of legislation and possible future legislation and increased regulation regarding climate change could impose significant costs related to increased energy requirements, capital equipment, environmental monitoring and reporting and other costs to comply with such regulations.

19

Pending initiatives involving taxation could result in increased tax and operating costs.

There is growing attention from the media and the public on perceived international tax avoidance techniques which could result in escalating rates of poverty, inequality and unemployment in host countries. Initiatives like the Base Erosion and Profit Shifting project being led by the Organization for Economic Cooperation and Development aim to reform the system of international taxation to minimize international tax avoidance techniques. This initiative and possible future initiatives could result in increased tax expense and related compliance costs for future international mining operations.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

The following scientific and technical disclosures about Mt Todd have been reviewed and approved by Mr. John W. Rozelle, Senior Vice President of Vista. Mr. Rozelle is a qualified person as defined by NI 43-101.

Cautionary Note to U.S. Investors: This section and other sections of this annual report on Form 10-K contain the terms “measured mineral resources,” “indicated mineral resources,” “inferred mineral resources,” “proven mineral reserves,” and “probable mineral reserves” as defined in accordance with NI 43-101. Please note the following regarding these terms:

|

· |

“Measured mineral resources” and “indicated mineral resources” – we advise U.S. investors that although these terms are recognized and required by Canadian regulations, these terms are not defined in SEC Industry Guide 7 and the SEC does not normally permit such terms to be used in reports and registration statements filed with the SEC. U.S. investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into reserves. |

|

· |