Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 CERTIFICATION - SPECTRANETICS CORP | ex31212312015.htm |

| EX-10.89 - EXHIBIT 10.89 LEASE - SPECTRANETICS CORP | ex108912312015.htm |

| EX-32.2 - EXHIBIT 32.2 CERTIFICATION - SPECTRANETICS CORP | ex32212312015.htm |

| EX-32.1 - EXHIBIT 32.1 CERTIFICATION - SPECTRANETICS CORP | ex32112312015.htm |

| EX-21.1 - EXHIBIT 21.1 SUBSIDIARIES - SPECTRANETICS CORP | ex211subsidiaries2015.htm |

| EX-12.1 - EXHIBIT 12.1 RATIO OF EARNINGS TO FIXED CHARGES - SPECTRANETICS CORP | ex121ratioofearningstofixe.htm |

| EX-23.1 - EXHIBIT 23.1 CERTIFICATION OF INDEPENDENT AUDITORS - SPECTRANETICS CORP | ex231certificationofindepe.htm |

| EX-31.1 - EXHIBIT 31.1 CERTIFICATION - SPECTRANETICS CORP | ex31112312015.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the year ended December 31, 2015 | |

or | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | |

Commission file number 0-19711

THE SPECTRANETICS CORPORATION

(Exact name of Registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 84-0997049 (I.R.S. Employer Identification No.) |

9965 Federal Drive

Colorado Springs, Colorado 80921

(Address of principal executive offices and zip code)

Registrant’s Telephone Number, Including Area Code:

(719) 633-8333

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $.001 par value

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes o No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes o No x

The aggregate market value of the voting stock of the Registrant, as of June 30, 2015, the last business day of the registrant’s most recently completed second fiscal quarter was $963,268,366, as computed by reference to the closing sale price of the voting stock held by non-affiliates on such date. As of February 22, 2016, there were outstanding 42,699,239 shares of Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s definitive Proxy Statement for its 2016 Annual Meeting of Stockholders, to be filed with the Securities and Exchange Commission not later than April 29, 2016, are incorporated by reference into Part III as specified herein.

TABLE OF CONTENTS

PART I | ||

PART II | ||

PART III | ||

PART IV | ||

ii

PART I

The information in this annual report on Form 10-K includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, and is subject to the safe harbor created by that section. Forward-looking statements in this report or incorporated herein by reference constitute our expectations or forecasts of future events as of the date this report was filed with the Securities and Exchange Commission and are not statements of historical fact. You can identify these statements by the fact that they do not relate strictly to historical or current facts. Such statements may include words such as “anticipate,” “will,” “estimate,” “seek,” “expect,” “project,” “intend,” “should,” “plan,” “believe,” “hope,” and other words and terms of similar meaning in connection with any discussion of, among other things, future operating or financial performance, strategic initiatives and business strategies, regulatory or competitive environments, our intellectual property and product development. You are cautioned not to place undue reliance on these forward-looking statements and to note they speak only as of the date hereof. Factors that could cause actual results to differ materially from those set forth in the forward-looking statements are in the risk factors listed from time to time in our filings with the SEC and those set forth in Item 1A, “Risk Factors.” We disclaim any intention or obligation to update or revise any financial projections or forward-looking statements due to new information or other events. Some industry and market data in this annual report on Form 10-K are based on independent industry publications, including those generated by the Millennium Research Group and IMS Health, or other publicly available information. This information involves several assumptions and limitations. Although we believe that each source is reliable as of its respective date, we have not independently verified the accuracy or completeness of this information. Certain percentage amounts included herein may not add due to rounding.

ITEM 1. Business

The Company

We develop, manufacture, market and distribute single-use medical devices used in minimally invasive procedures within the cardiovascular system. Our products are used to cross, prepare, and treat arterial blockages in the legs and heart and to remove pacemaker and defibrillator cardiac leads. We believe that the diversified nature of our business allows us to respond to a wide range of physician and patient needs. The innovative products and services we offer are divided into three categories:

• | Vascular Intervention (“VI”): Our broad portfolio of VI devices consists of laser and aspiration catheters, AngioSculpt® scoring balloon catheters, which are the specialty balloon market leader, support catheters, and the Stellarex™ drug-coated balloon (“DCB”) catheters. |

• | Lead Management (“LM”): We are a global leader in devices for the removal of pacemaker and defibrillator cardiac leads. Our primary LM devices consist of our excimer laser sheaths, non-laser mechanical sheaths and cardiac lead management accessories for the removal of pacemaker and defibrillator cardiac leads. |

• | Laser, service, and other: Our proprietary excimer laser system, the CVX-300®, is the only laser system approved in the United States, Europe, Japan and Canada for use in multiple minimally invasive cardiovascular procedures. We sell, rent and service our CVX-300 laser systems. |

On January 27, 2015, we acquired certain assets and liabilities related to Covidien LP’s Stellarex™ (“Stellarex”) over the wire percutaneous transluminal angioplasty balloon catheter with a paclitaxel coated balloon. The Stellarex DCB platform is designed to treat peripheral arterial disease and currently is cleared for use in Europe. Stellarex uses EnduraCoat™ technology, a durable, uniform coating designed to prevent drug loss during transit and facilitate controlled, efficient drug delivery to the treatment site.

1

On June 30, 2014, we completed our acquisition of AngioScore Inc., the U.S. market leader in specialty scoring balloon catheters. AngioScore develops, manufactures and markets the AngioSculpt scoring balloon catheter for the treatment of peripheral and coronary disease. The AngioSculpt catheter combines a semi-compliant balloon with a nitinol scoring element to address specific limitations of conventional balloon angioplasty catheters and rotational atherectomy. The AngioSculpt technology platform includes three models of coronary catheters and one model of peripheral catheters of various sizes and lengths. AngioScore is also developing the Drug-Coated AngioSculpt (“DCAS”), which is expected to be the world’s first drug-coated scoring balloon to treat coronary disease.

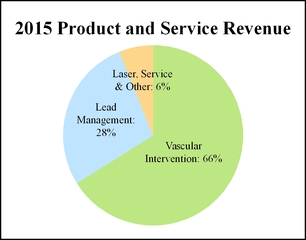

Our disposable devices include VI and LM products. For the year ended December 31, 2015, our disposable products generated 94% of our consolidated revenue, of which VI accounted for 66% and LM accounted for 28%. The remainder of our revenue is derived from sales and rental of our laser systems and related service.

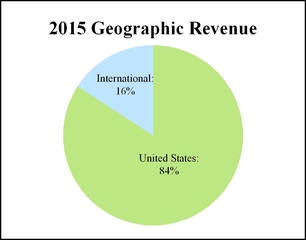

Our two operating segments are United States Medical and International Medical. United States Medical includes direct sales operations in the United States and Canada. International Medical includes our sales presence in over 65 countries outside of the U.S. and Canada, including our direct sales operations in certain countries in Europe and Puerto Rico and a network of approximately 60 distributors. Total international revenue in 2015 was 16% of our consolidated revenue.

Our business strategy emphasizes:

• | Saving lives and limbs: We focus on inventing and delivering technology that enables physicians to complete procedures confidently and successfully, as well as treating cardiovascular disease and its complications. We want patients to live life fully, free from health conditions that stand in the way. |

• | Proven solutions: At Spectranetics, we focus on proven algorithms of treatment for the most complex and challenging cardiovascular cases. |

• | Expanding our reach: We thoughtfully invest to broaden our solutions portfolio and deliver answers to complex diseases through: |

▪ | organic growth through new product development; |

▪ | new clinical indications for our existing products; |

▪ | continued execution of our commercial, educational, and clinical programs; |

▪ | acquisitions that leverage our current customer base and expand our portfolio of products; |

▪ | capitalizing on our expanded U.S. sales force in both VI and LM; and |

▪ | continued global expansion. |

2

Vascular Intervention Products

We are dedicated to helping physicians cross, prepare and treat complex clinical challenges of peripheral and coronary artery disease. We provide a comprehensive portfolio of clinical solutions designed to eradicate restenosis, modify all plaque and reduce amputations. We partner with physicians to successfully treat challenging vascular conditions at every stage.

Peripheral Vascular Intervention Products

Peripheral artery disease (“PAD”) is characterized by clogged or obstructed arteries in the lower extremities. The resulting lack of blood flow can cause leg pain, cramping and weakness, and lead to tissue loss or, in very extreme cases, amputation. PAD is a global pandemic estimated to impact over 200 million people in the world, growing 25% from 2000 to 2010. In the U.S. and Europe alone, 25 million people are afflicted with PAD; however, only 10 million of these patients suffer from typical symptoms such as leg pain while walking or resting. PAD patients are underdiagnosed and undertreated with as few as one million patients receiving endovascular treatment each year, according to internal estimates using leading market research data. Of these patients, an estimated 875,000 are treated with percutaneous transluminal angioplasty (“PTA”) or stents while an estimated 125,000 patients are treated with atherectomy. An additional 400,000 to 500,000 PAD patients annually undergo bypass surgery or amputation in the U.S. and Europe.

Research shows that nearly half of all amputations occur without appropriate diagnostics and consideration of minimally invasive treatment options, leading to unnecessary amputations. This has a tremendous impact on patient quality of life, five-year mortality and healthcare economics. According to internal estimates, reducing amputations by 25% could save $3 billion in treatment and follow-up costs annually in the U.S. alone.

We believe that physicians, including interventional cardiologists, vascular surgeons, and interventional radiologists, prefer minimally invasive solutions to treat PAD when appropriate for the patient. Our focus and core competency is providing solutions for three complex conditions in PAD: chronic total occlusions (“CTO”), in-stent restenosis (“ISR”), and critical limb ischemia (“CLI”). We provide sound clinical solutions to cross, prepare and treat the lesion, thereby restoring blood flow and delivering the best long term outcomes for our customers’ patients.

Crossing the Lesion

Spectranetics is the U.S. market leader in support catheters, according to IMS Health data. To treat PAD, a physician must first cross the lesion with an interventional guidewire. Physicians encounter a CTO, which is a complete or near-complete blockage of a blood vessel, in approximately 40% of PAD procedures and as high as 80% in advanced CLI cases. The interventional procedure, whether atherectomy, balloon dilation, or stent placement, cannot occur without first crossing the lesion. Our crossing solutions products support vascular access in the arterial system to enable both coronary and peripheral interventions. Our primary crossing solutions products include the Quick-Cross™, Quick-Cross Select, and Quick-Cross Extreme. These solutions provide directional support, transmission, columnar strength, and the ability to gain access into difficult branched anatomy.

Preparing the Vessel

Our laser atherectomy and AngioSculpt specialty scoring balloon catheter vessel preparation technologies are a core part of our business. Vessel preparation can be advantageous to maximize the benefit of vascular treatments, whether stents, DCBs or covered stent platforms. We believe that our vessel preparation portfolio of products is uniquely aligned to overcome the complex challenges our physician customers routinely face.

Laser atherectomy has been approved or cleared by the Food and Drug Administration (“FDA”) for peripheral stenoses and occlusions, both as a stand-alone treatment and as an adjunctive treatment with other

3

therapies, such as balloons and stents. In the periphery, laser catheters are often used as an alternative to stents and other atherectomy devices. Our Turbo-Elite™, Turbo-Tandem™ and Turbo-Power™ catheters are approved to treat stenoses and occlusions within the arteries of the leg both above and below the knee.

We offer our laser catheters in sizes ranging from 0.9 to 2.5 millimeters in diameter, enabling physicians to treat both smaller and larger diameter arteries. Our single-use laser catheters contain up to 250 small-diameter, flexible optical fibers that can access difficult to reach peripheral and coronary anatomy and produce evenly distributed laser energy at the tip of the catheter. We believe our laser system and Turbo-Elite, Turbo-Tandem and Turbo-Power catheter technology offer several patient benefits, including a minimally invasive alternative to bypass surgery and amputation, predictable outcomes in addressing PAD, short procedure time and a robust safety profile. Our laser catheter is inserted into an artery through a small incision and then guided to the site of the blockage or lesion under x-ray guidance using conventional angioplasty tools. When the tip of the laser catheter has been placed at the site of the blockage or lesion, the physician activates the laser to ablate the lesion. Our laser generates minimal heat and is a contact ablation laser that only ablates materials within 50 microns (approximately the width of a human hair) ahead of the laser tip. It can break down the molecular bonds of plaque, moderate calcium and thrombus into particles, most of which are smaller than red blood cells, without significant thermal damage to surrounding tissue.

The acquisition of AngioScore expanded our portfolio of products for both vessel preparation and vessel treatment. The AngioSculpt scoring balloon catheter combines a semi-compliant balloon with a nitinol scoring element to address specific limitations of conventional balloon angioplasty catheters, including a lower occurrence of flow-limiting dissections and balloon slippage. It is often used for the vessel preparation of complex lesions in the arteries of the leg, including predilation of highly calcified, diffuse or complex de novo, restenotic and ISR lesions. The AngioSculpt peripheral scoring balloon platform includes catheters of various sizes and lengths to treat PAD both above and below the knee.

In July 2014, we launched the 200 mm length AngioSculpt scoring balloon catheters, which incorporate 200 mm balloons in diameters of 4.0, 5.0 and 6.0 mm with a novel scoring element specifically designed for these longer balloons. The devices are particularly useful in preparing and/or final dilation of the typical complex and long lesions found above the knee. In 2015, we launched 7 and 8 mm diameter AngioSculpt scoring balloons for use in larger vessels of the leg such as the common femoral and iliac arteries. The device is also used to open hemodialysis access sites, particularly those lesions that are resistant to plain old balloon angioplasty and require higher pressure dilation. It is believed that as many as 20% of revision endovascular treatments involve these more complex lesions.

Treating the Vessel

Physicians typically treat PAD by using balloon angioplasty (either a scoring balloon, DCB or PTA), or by placing a stent (either drug-coated, bare metal or covered). The acquisition of AngioScore in 2014 augmented our portfolio of products to treat vascular lesions. AngioSculpt peripheral scoring balloon catheters can be used for treatment of many lesion types, including highly calcified lesions, non-stent zones, and in-stent or native-vessel restenotic disease.

The acquisition of the Stellarex DCB in January 2015 further complemented our portfolio of products to treat PAD. Stellarex uses EnduraCoat technology, a durable, uniform coating designed to prevent drug loss during transit and facilitate controlled, efficient drug delivery to the treatment site. Stellarex received Conformité Européene (“CE”) mark in the European Union in December 2014. In 2015, Spectranetics completed enrollment in the ILLUMENATE Pivotal clinical study, a prospective, randomized controlled, multicenter study designed to assess the clinical performance of Stellarex. Completion of enrollment is a significant step toward FDA premarket approval, which we expect will be filed after one-year follow-up visits with all patients are completed.

4

Differentiated Solutions for Treatment of Important and Complex PAD Patients

We have uniquely aligned our portfolio to deliver meaningful solutions to treat complex conditions including ISR and CLI.

In-Stent Restenosis (“ISR”). Physicians frequently implant stents to open obstructed blood vessels in patients suffering from PAD. Although stents deliver improved overall outcomes compared to PTA treatment, it is common for a return of the blockage to occur within the stent (ISR), which is therapeutically challenging. Once ISR develops, there is a high recurrence rate, up to 65% within two years, after PTA treatment, which has long been considered the standard of care for treatment of ISR. In 2014, our Turbo-Tandem and Turbo-Elite products became the only atherectomy devices cleared by the FDA for the treatment of ISR. Our first in-industry randomized clinical trial data for atherectomy, EXCITE ISR, demonstrated superior safety and efficacy of laser atherectomy with adjunctive PTA compared with PTA alone. In the U.S. alone, it is estimated that as many as 115,000 patients require treatment for ISR each year.

In late 2015, we obtained FDA 510(k) clearance of our Turbo-Power laser atherectomy catheter, a next generation ISR solution with improved ease of use and delivering clinical superiority in ISR treatment when used with PTA versus PTA alone. Uniquely designed for ISR treatment, the Turbo-Power laser atherectomy catheter treats at the tip with vaporizing technology for maximal luminal gain. The device debulks the lesion in a single step and offers remote automatic rotation for precise directional control. As the only company with an ISR indication for femoral and popliteal arteries of the leg (“FemPop”), backed by Level 1 clinical evidence, and primary competitors contraindicated or not indicated, we believe that we are well-positioned to continue to deliver tools that advance care for patients suffering from ISR.

Critical Limb Ischemia (“CLI”). We estimate that up to half of all PAD procedures involve CLI, a condition defined by a range of symptoms, from pain at rest to the presence of ulcers, tissue loss or gangrene. Our products can prepare and treat multiple lesion morphologies, including plaque, calcium, restenotic tissue and thrombus. Because the disease of the lower leg is primarily a diffuse, occlusive disease, removal or debulking of the lesion may be necessary to restore robust blood flow. The Turbo-Elite catheters come in a range of sizes and are uniquely designed to safely prepare the long diffuse lesions commonly found in CLI patients. Our Turbo-Elite laser atherectomy catheter ablates at the tip and has a very low profile. These two important features allow the physician to safely reach deep into the arteries of the foot. The AngioSculpt PTA scoring balloon comes in a range of sizes tailored to the arteries of the lower leg and is particularly well suited to dilate the vessel while limiting the likelihood of a major dissection requiring stent placement.

Coronary Vascular Intervention Products

Specialty Scoring Balloons, Atherectomy and Thrombectomy. In the coronary market, our disposable catheters are used to cross, prepare and treat complex coronary artery disease (“CAD”) as an adjunctive treatment to traditional percutaneous coronary interventions (“PCI”) using balloons and stents. In total, we have nine coronary indications.

Our coronary atherectomy product portfolio, led by the ELCA™ laser ablation catheter, comprises a broad selection of proprietary laser catheters. Our seven approved coronary atherectomy indications for the vessel preparation and treatment of challenging coronary lesion subsets include occluded saphenous vein bypass grafts, ostial lesions, long lesions, moderately calcified stenoses, total occlusions traversable by guidewire, lesions with previously failed balloon angioplasty, and restenosis in bare metal stents prior to brachytherapy. In the coronary market, our laser catheters are used to prepare the vessel prior to placement of a stent, particularly in challenging lesion subsets.

5

With the acquisition of AngioScore in 2014, we expanded our ability to prepare and treat a variety of complex coronary diseases. The AngioSculpt scoring percutaneous transluminal coronary angioplasty (“PTCA”) balloon catheters are available in a range of sizes. The products are cleared to treat ISR and have an indication to treat complex type C lesions, which are the most difficult lesions to treat.

In the thrombus management market, we offer aspiration catheters, often used with other devices such as balloons and stents, to address thrombus-laden lesions. A thrombus, or clot, is an accumulation of blood coagulation large enough to block blood flow in the coronary, peripheral, or cerebral arteries. The thrombus may block the artery at the lesion location and can dislodge and travel further downstream in the arterial system. Depending on the location of the thrombus, arterial complications such as myocardial infarction in the coronary arteries, stroke in the brain, or acute limb ischemia in the extremities may occur. The thrombus management product line includes the QuickCat™ aspiration catheter, designed for quick deliverability and efficient thrombus removal from vessels in the arterial system.

Lead Management Products

We are a global leader in devices for the removal of pacemaker and defibrillation cardiac leads. The Heart Rhythm Society’s list of indications for lead extraction includes several well-defined scenarios involving non-functional leads, functional leads and venous occlusion. We believe that approximately 300,000 patients worldwide are indicated every year for a potential lead extraction as a result of an infection, classified by the Heart Rhythm Society as a Class I Indication for Extraction of Cardiac Leads, or a Class II Indication for Extraction of Cardiac Leads, which includes malfunction, system upgrade, venous occlusion, and other less common reasons. We believe that this results in a market potential of over $700 million with approximately 25% from Class I indications and approximately 75% from Class II indications. We believe that, although infection is a Class I indication for lead extraction, a majority of patients with cardiac device infection are not being treated. The near-term consequence of delayed device removal for infection is an increase in the mortality rate of such patients. Recognizing this, in 2009, the Heart Rhythm Society strengthened recommendations for extraction of infected leads.

We also believe that the majority of the Class II non-infected leads are capped and left in the body as a predominant mode of practice, based on physician perception of risk associated with removal and perception that abandoned leads are benign. We believe the long-term consequences associated with abandoned leads are more significant than generally believed and that clinical data, strongly supporting the safety of lead removal, will be instrumental in reshaping perceptions around this procedure as a mainstream treatment option for patients with devices.

Our primary Lead Management products include:

• | Spectranetics Laser Sheaths (GlideLight™ and SLS™ II). Spectranetics Laser Sheaths are laser-assisted lead removal devices designed to be used with our CVX-300 excimer laser system to extract implanted leads with minimal force. We believe that the advantages of laser lead extraction include low trauma to the surrounding veins, low occurrence of complication, effectiveness and time efficiency. |

• | Lead Locking Device (LLD™). Our Lead Locking Device product complements our laser sheath product line as an adjunctive mechanical tool. The LLD is a mechanical device that assists in the removal of leads by providing traction on the inner aspect of the leads, which are typically constructed of wire coils covered by insulating material. |

• | Mechanical Tools (TightRail™ Rotating Dilator Sheath and SightRail™ Manual Dilator Sheath). The TightRail and the SightRail mechanical lead extraction platforms expand physicians’ options for removing cardiac leads, and complement the laser-based technology that established our leading position in lead extraction. Both product platforms are cleared for use in the U.S. and Europe. |

6

In addition to our primary products mentioned above, in February 2016, we received 510(k) regulatory clearance for our Bridge™ Occlusion Balloon product. The Bridge is a balloon designed to dramatically reduce blood loss in the event of a tear in the superior vena cava during a lead extraction procedure. The device is designed to give the physician adequate time to safely transition the patient for surgical repair and to give the surgeon the benefit of a clear field of view to repair the tear. Although a superior vena cava tear is a rare occurrence, we believe that this product is an important innovation in an effort to accomplish our goal of eliminating mortality as a risk during lead extraction procedures.

Laser Equipment and Service

We sell or rent our CVX-300 excimer laser systems to hospitals and physicians’ offices, and our field service engineers service the laser systems on a periodic basis.

Corporate Information

The Spectranetics Corporation is a Delaware corporation formed in 1984. Our principal executive offices are located at 9965 Federal Drive, Colorado Springs, Colorado 80921. Our telephone number is (719) 633-8333.

Our corporate website is www.spnc.com. A link to a third-party website is provided at our corporate website to access our SEC filings free of charge promptly after such material is electronically filed with, or furnished to, the SEC. We do not intend for information found on our website to be part of this document.

Research and Development

We believe research and development investments are critical to increasing our revenue and revenue growth rate. Our product development and technology teams are focused on developing additional disposable devices addressing the VI and LM markets, and further developing our laser system. We believe in the near-term our primary research and development effort and expense will be within our DCB programs, Stellarex and DCAS. Our team of research scientists, engineers and technicians, supported by third-party research and engineering organizations, performs substantially all of our research and development activities. Our research and development expense, which also includes clinical studies costs, regulatory costs, and royalty costs, totaled $64.4 million in 2015, $28.7 million in 2014 and $22.1 million in 2013.

Clinical Trials

We sponsor and support clinical investigations to evaluate patient safety and clinical efficacy, and to advance adoption and support regulatory approval or clearance for new product initiatives. Our clinical and regulatory departments are focused on developing the necessary clinical data to achieve initial regulatory approval or clearance, and expanded indications for our existing and emerging products around the world. The goal of a clinical trial is to meet the primary endpoint, which measures clinical effectiveness and may also provide information about the performance and safety of a device, which are the bases for FDA approval or clearance. Primary endpoints for clinical trials are selected based on the proposed intended use of the medical device. Results in clinical trials form the basis for approval or clearance of the product, but results in clinical practice may be somewhat less favorable than in a trial, because there may be variables in clinical practice that are controlled in the clinical trial setting.

7

Current and Recent Clinical Trials

The trials listed below represent the significant trials we are currently conducting or have recently conducted. This is not a complete listing of every trial conducted or underway. We may not complete some or all of the trials underway, and the clinical results of the completed trials may not be favorable, or even if favorable, they may not be sufficient to support approval or clearance of a new device or a new indication for a currently approved or cleared device.

Stellarex DCB ILLUMENATE

The Stellarex DCB platform is being evaluated in five clinical studies, including one Investigational Device Exemption (“IDE”) trial in the United States and four international trials. The Stellarex DCB received CE mark to be marketed in the European Union in December 2014, and we launched the product in Europe in late January 2015. It is not approved in the U.S., where it is currently limited to investigational use.

In March 2015, findings from the ILLUMENATE First-in-Human (“FIH”) study, a prospectIve, controlled, multi-center, open, singLe arm study for the treatment of subjects presenting de novo occLUded/stenotic or re-occluded/restenotic lesions of the superficial feMoral or poplitEal arteries using a paclitaxel-coated percutaNeous Angioplasty catheTEr, were posted in Catheterization and Cardiovascular Interventions, a publication of the Society for Cardiovascular Angiography and Interventions.

In addition to the FIH study, which is now complete, the Stellarex DCB is currently being studied in four active above-the-knee ILLUMENATE clinical trials:

The ILLUMENATE Pharmacokinetic Study is a prospectIve, singLe-arm, muLti-center, pharmacokinetic study to evalUate treatMent of obstructive supErficial femoral artery or popliteal lesioNs with A novel pacliTaxel-coatEd percutaneous angioplasty balloon and has an enrollment of 25 subjects at two sites.

The ILLUMENATE Pivotal Trial is a prospectIve, randomized, singLe-blind, U.S. muLti-center study to evalUate treatMent of obstructive supErficial femoral artery or popliteal lesioNs with A novel pacliTaxel-coatEd percutaneous angioplasty balloon and has an enrollment of 300 subjects at 45 sites.

The ILLUMENATE European Randomized Trial is a prospectIve, randomized, multi-center, singLe-blind study for the treatment of subjects presenting with de novo occLUded/stenotic or re-occluded/restenotic lesions of the supErficial feMoral poplitEal arteries using a paclitaxel-coated or bare percutaNeous transluminal Angioplasty balloon catheTEr and has an enrollment of 328 subjects at 30 sites.

The ILLUMENATE Global Registry is a prospectIve, singLe-arm, global muLti-center study to evalUate treatMent of obstructive supErficial femoral artery or popliteal lesioNs with A novel pacliTaxel-coatEd percutaneous angioplasty balloon with an enrollment of 371 subjects at 65 sites.

These five clinical trials will be used to evaluate the safety and effectiveness of the Stellarex DCB platform and are intended to support U.S. and Canada regulatory approval. We cannot predict the outcome of the active ILLUMENATE clinical trials, and the outcome of the FIH study is not predictive of the outcome of any other trials. There is no assurance that the ongoing trials will support approval, and there is no assurance that our anticipated time frame will be met.

In January 2016, we announced that we expect to release clinical data related to our ILLUMENATE clinical trials during the course of 2016. Our initial clinical data release will be an interim analysis of 12-month data on a subset of the patients enrolled in the ILLUMENATE Global Registry. In addition to this data, we will be

8

presenting the full 12-month data from each of the ILLUMENATE Pivotal Trial and ILLUMENATE European Randomized Trial.

Stellarex DCB Future Studies

Spectranetics will sponsor a large, multicenter registry in Europe in 2016, referred to as the Stellarex Vascular e-Registry (“SAVER”). In addition, we will support physician-initiated studies to evaluate long and calcified lesions, beginning in 2016.

EXCITE ISR

The EXCImer Laser Randomized Controlled Study for the Treatment of Femoropopliteal arteries (above and behind the knee) ISR (“EXCITE ISR”) study, granted by the FDA in 2011, incorporated a 2:1 randomization plan, comparing laser ablation using our Turbo-Tandem and Turbo-Elite laser ablation devices followed by adjunctive balloon angioplasty with balloon angioplasty alone as a control. The primary endpoint is freedom from TLR through six months following the procedure. The primary safety endpoint is freedom from major adverse events (“MAE”), such as death, major amputation, or TLR, at 30 days following the procedure.

ISR occurs when a previously placed stent becomes occluded, or blocked. We designed the treatment-to-control EXCITE ISR study to investigate the safety and efficacy of treatment with laser atherectomy in subjects with ISR, and the study was adequately powered based on hypothesized results.

In March 2014, we announced early termination of the EXCITE ISR study, achieving statistically significant results in both safety and efficacy. We met the endpoints of the study based on the enrollment of 250 patients versus the 318 patients originally planned.

In July 2014, we announced FDA 510(k) clearance of Turbo-Tandem and Turbo-Elite for the treatment of peripheral ISR in bare nitinol stents, when used in conjunction with percutaneous transluminal angioplasty. FDA clearance was based on the EXCITE ISR clinical findings.

In January 2015, the initial results of the EXCITE ISR trial were published in the Journal of the American College of Cardiology; Cardiovascular Interventions. Also in January 2015, the complete six month results of the EXCITE ISR trial were presented at the Leipzig Interventional Course (“LINC”) conference.

In November 2015, we received FDA 510(k) clearance of our peripheral atherectomy product, the Turbo-Power laser atherectomy catheter, for the treatment of ISR. In addition to our Turbo-Tandem and Turbo-Elite products, these products are now the only atherectomy devices cleared by the FDA for the treatment of ISR.

Sales and Marketing

Our primary goal is to increase the global use of our vascular and cardiovascular products in new and existing accounts. We seek to educate and train physicians and institutions regarding the safety, efficacy, ease of use and growing number of disease states treated by our VI and LM product portfolios. Through published studies of clinical applications and training initiatives, we share clinical outcomes with customers and potential customers to demonstrate that our products are proven safe and effective.

U.S. Sales and Marketing

During 2014, we nearly doubled our sales and marketing team through planned expansion and the acquisition of AngioScore. We further augmented our marketing team with the acquisition of Stellarex in 2015. Due to differentiated selling strategies and physician specialties, our U.S. sales organization is divided into two

9

strategic groups, one focusing on VI and the other on LM. This strategic segmentation allows our sales teammates to better understand the needs of the customers within their respective product lines. Our VI commercial team works with interventional cardiologists, vascular surgeons and interventional radiologists who perform vascular procedures on a more regular basis utilizing a wider range of treatment options. Our LM commercial team works with electrophysiologists and cardiac surgeons who perform lead extraction procedures.

Our VI and LM educational sessions include hands-on training with a unique simulation system. The simulation technology augments traditional procedural training for physicians on the use of our products by permitting hands-on practice with extraction tools, catheter navigation and laser simulation techniques in multiple case scenarios in a virtual operating environment.

Our field team in the U.S. includes field service engineers who are responsible for the installation of lasers and participation in the training program at each site. The field service engineers also perform ongoing service on the lasers placed under our various rental programs.

Our marketing team supports our two U.S. sales organizations, the Stellarex DCB program and global product development initiatives. Our team includes marketing and product managers responsible for all marketing activities for each of our core businesses. Our marketing activities are designed to support our direct sales teams and include branding, sales enablement tools, advertising and product publicity in trade journals, newsletters, continuing education programs, public relations and attendance at trade shows and professional association meetings.

International Sales and Marketing

We have a sales presence in over 65 countries outside of the U.S., including our direct sales operations in certain countries in Europe and Puerto Rico and a network of approximately 60 distributors. We also have a global marketing presence in key markets internationally that drives commercial execution of our full line of products to our direct international sales force and distributor partners. We sell substantially all of our products internationally, including Stellarex, which we sell in Europe; however, Stellarex is not approved in the U.S., where it is currently limited to investigational use. Total international revenue in 2015 was $39.3 million, or 16% of our consolidated revenue. This represents an increase of $1.8 million, or 5% (17% on a constant currency basis), over 2014 international revenue of $37.5 million. See the “Non-GAAP Financial Measures” section in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for a discussion of our use of the constant currency financial measure. For further discussion of our International Medical segment and our financial information by geographic areas, please see Note 11, “Segment and Geographic Reporting,” of the consolidated financial statements in Part IV, Item 15 of this annual report.

We market and sell our products in Europe, the Middle East and Russia through our wholly-owned subsidiary, Spectranetics International, B.V., and its wholly-owned international subsidiaries and through distributors. We conduct international business in Japan and an expanding set of countries in the Asia Pacific and Latin America regions through distributors.

Foreign sales may be subject to certain risks, including export/import licenses, tariffs, foreign exchange rate fluctuations, other trade regulations and foreign medical regulations and reimbursement. Tariff and trade policies, domestic and foreign tax and economic policies, exchange rate fluctuations and international monetary conditions have not significantly affected our business.

Competition

The medical device industry is highly competitive, subject to rapid change and significantly affected by new product introductions and other activities of industry participants. Our primary competitors are manufacturers of products used in competing therapies to cross, prepare and treat disease within the peripheral and coronary

10

markets, such as mechanical methods to remove arterial blockages, balloon angioplasty and stents, specialty balloon angioplasty alternatives to our specialty scoring balloons, bypass surgery and amputation. Primary competitors include Medtronic, Boston Scientific Corporation, C.R. Bard, Inc., QT Vascular–Singapore, Biotronik and Cardiovascular Systems, Inc. In the lead management market, we compete with Cook Medical, Inc., as well as Biotronik internationally. There has been consolidation in the industry, and we expect that to continue.

Manufacturing

We manufacture substantially all of our products. We have vertically integrated a number of manufacturing processes in an effort to provide increased quality and reliability of the components used in the manufacturing processes. Many of our manufacturing processes are proprietary. We believe that our level of manufacturing integration allows us to better control lead time, costs, quality and process advancements, to accelerate new product development cycle time, to provide greater design flexibility, and to scale manufacturing, should market demand increase.

We manufacture a significant number of our disposable products and all of our CVX-300 laser systems at our corporate headquarters in Colorado Springs, Colorado. We maintain manufacturing capabilities at another location in Colorado Springs for business continuity contingency planning purposes. We manufacture the AngioSculpt products at our facility in Fremont, California. The Stellarex products are manufactured in a separate facility, also located in Fremont, California.

Our manufacturing facilities are subject to periodic inspections and audits by federal, state, international, and other regulatory authorities, including inspections by the FDA and audits by our Notified Body (currently the British Standards Institution (“BSI”)), which is authorized by the European Commission (“EC”) to conduct such audits on behalf of the European Union (“EU”). Most raw materials, components and subassemblies used in our products are purchased from outside suppliers and are generally readily available from multiple sources, and a minority of our products is single sourced.

During 2015, we have undergone external quality system audits and factory safety inspections, some of which resulted in Form 483 notices. We cannot assure you that material nonconformities will not be identified in the future, or that the FDA will not issue us any “it has come to our attention” or warning letters based on the promotion or manufacturing of any of our products.

Patents and Proprietary Rights

We hold numerous issued U.S. patents and trademarks and have rights to additional U.S. patents under license agreements in the name of The Spectranetics Corporation and AngioScore, Inc. We also hold issued patents and trademarks in other countries. In addition, we also have pending U.S. and international patent applications that cover numerous inventions, including general features of the laser system, our catheters, our scoring balloon technology platform, the coatings of our DCB platform, and other technologies, as well as pending trademark applications.

It is our policy to require our employees and consultants to execute confidentiality agreements upon the commencement of an employment or consulting relationship with us. Each agreement provides that all confidential information developed or made known to the individual during the relationship will be kept confidential and not disclosed to third parties except in specified circumstances. In the case of employees, the agreements provide that all inventions developed by the individual pursuant to their employment are our exclusive property. These agreements may not provide meaningful protection if unauthorized use or disclosure of such information occurs.

We also rely on trade secrets and unpatented know how to protect our proprietary technology and may be vulnerable to competitors who attempt to copy our products or gain access to our trade secrets and know how.

11

We are party to license agreements under which we license patents covering certain aspects of our products. For example, we have an amended vascular laser angioplasty catheter license agreement with SurModics, Inc., under which SurModics has granted us a worldwide non-exclusive license to use a lubricious coating that is applied to our products using certain SurModics patents. We pay SurModics royalties as a specified percentage of net sales of products using its patents, subject to a quarterly minimum royalty. The license agreement expires on the later of the expiration of the last licensed patent or the fifteenth anniversary of the date a licensed product is first sold unless terminated earlier (1) by either party if the other party is involved with insolvency, dissolution or bankruptcy proceedings, (2) by us upon 90 days’ advance written notice, or (3) by SurModics upon 60 days’ advance written notice if we have failed to perform our obligations under the agreement and have not cured such breach during such 60-day period, or if the royalties we pay SurModics are not greater than specified levels. In 2015, we incurred royalties of approximately $1.2 million to SurModics under this license agreement.

In December 2009, we entered into a license agreement with Peter Rentrop, M.D. As part of the agreement, we received a worldwide, exclusive license to certain patents and patent applications owned by Dr. Rentrop, which, in general, apply to laser catheters with a tip diameter less than one millimeter. We pay Dr. Rentrop royalties of a specified percentage of net sales of products using his patents subject to a quarterly minimum royalty. The license agreement expires in January 2020, unless terminated earlier in accordance with its terms. In 2015, we incurred royalties of approximately $2.0 million to Dr. Rentrop under this license agreement.

In March 2010, AngioScore entered into a development and license agreement with InnoRa GmbH, Ulrich Speck and Bruno Scheller. As part of the agreement, AngioScore received an exclusive license to certain InnoRa intellectual property related to drug coatings of certain balloon catheters in the field of the treatment of coronary artery disease and peripheral arterial disease, and AngioScore obtained ownership of any new technology developed under the agreement. AngioScore pays InnoRa royalties of a specified percentage of net sales of products developed under the agreement. The exclusive rights granted by InnoRa are subject to AngioScore meeting certain milestones. If AngioScore does not satisfy the milestones, then the exclusive license rights will convert to a non-exclusive license, and AngioScore will license certain new technology developed under the agreement to InnoRa. In 2015, AngioScore did not incur royalties under this license agreement.

Third-Party Reimbursement

U.S. Third-Party Reimbursement

Our CVX-300 excimer laser system and related disposable devices are generally purchased by hospitals, which then bill various third-party payers for the healthcare services provided to their patients. These payers include Medicare, Medicaid and private insurance payers. The Centers for Medicare and Medicaid Services (“CMS”) administers the federal Medicare program. Medicare policies and payment rates depend on the setting in which the services are performed. Private payers are influenced by Medicare coverage and payment methodologies.

Hospitals are reimbursed for inpatient services by Medicare under the Inpatient Prospective Payment System (“IPPS”). Payment is made to the hospital through the Medicare Severity Diagnosis Related Group (“MS-DRG”) methodology. MS-DRGs classify discharges into groups with similar clinical characteristics that are expected to require similar resource utilization. MS-DRG assignment for a patient’s hospitalization is based on the patient’s reason for admission, discharge diagnoses, and procedures performed during the inpatient stay. Hospitals are paid a fixed payment that is designed to be inclusive of all supplies, devices, and overhead associated with the stay. IPPS does not separately reimburse for the actual cost of the medical device used or for the services provided. Hospitals performing inpatient procedures using our technology are paid the applicable MS-DRG payment rate for the inpatient stay.

For outpatient hospital services, payments are also made under a prospective payment system, the Outpatient Prospective Payment System (“OPPS”). Payments are based on Ambulatory Payment Classifications

12

(“APCs”), under which each procedure is categorized. Most procedures are assigned to APCs with other procedures that are clinically and resource comparable.

An ambulatory surgery center (“ASC”) is a center not attached to a hospital where surgical procedures are performed at which patients have a recovery of less than 24 hours. The payment methodology uses relative weights based on the OPPS. Medicare pays ASCs for covered surgical procedures. The payment includes ASC facility services furnished in connection with the covered procedure. In 2013, lower extremity revascularization procedures in ASCs were designated by Medicare as covered procedures.

Besides payments made to hospitals and ASCs for procedures using our technology, Medicare makes separate payments to physicians for their professional services. Payments to physicians are made under the national Medicare Physician Fee Schedule (“MPFS”). National payment rates are assigned based on the Resource Based Relative Value System (“RBRVS”). Payment is adjusted for geographic location and place of service. Lower extremity revascularization procedures have been designated by Medicare as covered procedures in office-based labs and inpatient and outpatient sites of service since 2011.

Hospital outpatient and physician services are reported with the Healthcare Common Procedure Coding System (“HCPCS”), which includes the AMA Current Procedural Terminology (“CPT”). Cardiac lead extraction procedures are typically reported with the current code sets describing lead removal. Percutaneous coronary and peripheral vascular laser atherectomy procedures are reported with the current code sets that describe coronary atherectomy and percutaneous endovascular revascularization.

Most third-party payers cover and reimburse for procedures using our products.

International Third-Party Reimbursement

Market acceptance of our products in international markets is dependent in part upon the availability of reimbursement from healthcare payment systems. Reimbursement and healthcare payment systems in international markets vary significantly by country. The main types of healthcare payment systems in international markets are government-sponsored healthcare and private insurance. Countries with government-sponsored healthcare, such as the United Kingdom, have a centralized, nationalized healthcare system. New devices are brought into the system through negotiations between departments at individual hospitals at the time of budgeting. In most foreign countries, there are also private insurance systems that may offer payments for alternative therapies.

Government Regulation

Overview of Medical Device Regulation

Our products are medical devices subject to extensive regulation by the FDA under the Federal Food, Drug, and Cosmetic Act (“FDCA”). FDA regulations govern, among other things, the following activities we perform:

• | product design, development, manufacture and testing; |

• | product labeling; |

• | product storage; |

• | premarket clearance or approval; |

• | advertising and promotion; |

• | product sales and distribution; and |

• | post-market safety reporting. |

To be commercially distributed in the United States, non-exempt medical devices must receive either approval through a Premarket Approval (“PMA”) or be found to be substantially equivalent to an already marketed

13

510(k) cleared device through a Premarket Notification 510(k) from the FDA prior to marketing and distribution under the FDCA.

510(k) Clearance Premarket Notification Pathway. To obtain 510(k) clearance, a manufacturer must submit a Premarket Notification 510(k) application demonstrating that the proposed device is substantially equivalent in intended use and in safety and effectiveness to a previously 510(k) cleared device or a device in commercial distribution before May 28, 1976.

PMA Pathway. A high risk device not eligible for 510(k) clearance must follow the PMA pathway, which requires valid scientific evidence providing a reasonable assurance of the safety and effectiveness of the device to the FDA’s satisfaction.

A PMA application must provide extensive preclinical and clinical trial data and also information about the device and its components regarding, among other things, device design, manufacturing and labeling. As part of the PMA review, the FDA will typically inspect the manufacturer’s facilities for compliance with Quality System Regulations (“QSR”), which impose elaborate testing, control, documentation and other quality assurance procedures. After initial PMA approval, changes in design, manufacturing, labeling and other changes often require prior FDA approval.

Postmarket. After a device is placed on the market, numerous regulatory requirements apply. These include: FDA labeling regulations that prohibit manufacturers from promoting products for unapproved or “off-label” uses; the Medical Device Reporting regulation, which requires that manufacturers report to the FDA if their device may have caused or contributed to a death or serious injury or malfunctioned in a way that would likely cause or contribute to a death or serious injury if it recurred; and the Reports of Corrections and Removals regulation, which requires manufacturers to report recalls and field actions to the FDA if initiated to reduce a risk to health posed by the device or to remedy a violation of the FDCA.

Labeling and promotional activities are also subject to scrutiny by the FDA and, in certain instances, by the Federal Trade Commission (“FTC”). The FDA and FTC actively enforce regulations prohibiting marketing of products for unapproved uses.

International Regulations. International sales of our products are subject to foreign regulations, including health and medical safety regulations. The regulatory review process varies from country to country. Many countries also impose product standards, packaging and labeling requirements and import restrictions on devices.

The Medical Device Directive (“MDD”) is a directive that covers the regulatory requirements for medical devices in the European Union, and upon successful completion, the MDD process results in the approval to apply for a CE mark. The Company has received CE mark registration for the majority of our current products. The CE mark indicates a product is certified for sale throughout the European Union and that the manufacturer of the product complies with applicable safety and quality standards.

Environmental Regulations. We are also subject to certain federal, state and local regulations regarding environmental protection and hazardous substance controls, among others. Compliance with such environmental regulations has not had a material effect on our capital expenditures or competitive position.

Corporate Compliance and Corporate Integrity Agreement. We have processes, policies and procedures designed to maintain compliance with applicable federal, state and foreign laws and regulations governing our operations.

In December 2009, to resolve a federal investigation, we entered a five-year Corporate Integrity Agreement with the Office of Inspector General of the United States Department of Health and Human Services (“OIG”). On

14

April 13, 2015, the Company’s monitor under the Corporate Integrity Agreement (“CIA”) with the OIG notified the Company that the CIA had been completed.

Product Liability Insurance

Our business entails the risk of product liability claims. We maintain product liability insurance for $25 million per occurrence with an annual aggregate maximum of $25 million.

Employees

As of December 31, 2015, we had 892 full time employees worldwide, an increase from 753 at December 31, 2014, primarily due to the Stellarex acquisition. We believe that we have a good relationship with our employees.

15

ITEM 1A. Risk Factors

Risks related to our business and industry

We may be unable to compete successfully with larger companies in our highly competitive industry.

The medical device industry is highly competitive. Our primary competitors are manufacturers of products used in competing therapies within the peripheral and coronary atherectomy and lead management markets, such as:

• | atherectomy and thrombectomy, using mechanical methods to remove arterial blockages; |

• | balloon angioplasty and stents; |

• | specialty balloon angioplasty, such as scoring balloons, pillowing balloons, cutting balloons and drug-coated balloons; |

• | bypass surgery; |

• | amputation; and |

• | mechanical lead removal tools. |

We believe that the primary competitive factors in the interventional coronary and peripheral markets include:

• | the ability to treat a variety of lesions safely and effectively as demonstrated by credible clinical data; |

• | ease of use; |

• | the impact of managed care practices, related reimbursement to the healthcare provider and procedure costs; |

• | size and effectiveness of sales forces; and |

• | research and development capabilities. |

Many of our competitors have substantially greater financial, manufacturing, marketing and technical resources than we do. There has been consolidation in the industry, and we expect that to continue. Larger competitors may have substantially larger sales and marketing operations than we do. This may allow those competitors to spend more time with potential customers and to focus on a larger number of potential customers, which gives them a significant advantage over our sales and marketing team and our international distributors in making sales. At times, we have experienced significant sales personnel turnover, and sales personnel turnover could be an issue in the future.

Larger competitors may also have broader product lines, which enables them to offer customers bundled purchase contracts and quantity discounts. These competitors may have more experience than we have in research and development, marketing, manufacturing, preclinical testing, conducting clinical trials, obtaining FDA and foreign regulatory approvals and marketing approved products. Our competitors may discover technologies and techniques, or enter into partnerships and collaborations, to develop competing products that are more effective or less costly than our products or the products we may develop. This may render our technology or products obsolete or noncompetitive. Academic institutions, government agencies, and other public and private research organizations may seek patent protection regarding potentially competitive products or technologies and may establish exclusive collaborative or licensing relationships with our competitors. Our competitors may be better equipped than we are to respond to competitive pressures. Competition will likely intensify.

Technological change may adversely affect sales of our products and may cause our products to become obsolete.

The medical device market is characterized by extensive research and development and rapid technological change. We derive most of our revenue from the sale of our disposable catheters. Technological progress or new developments in our industry could adversely affect sales of our products. Our products could be rendered obsolete because of future innovations by our competitors or others in the treatment of cardiovascular disease.

16

We may be unable to sustain our revenue growth.

Our ability to continue to increase our revenue in future periods will depend on our ability to successfully penetrate our target markets and increase sales of our VI products (including our AngioSculpt products) and LM products and generate significant sales from our Stellarex DCB catheters and new and improved products we introduce, which will, in turn, depend in part on our success in growing our customer base and obtaining reorders from those customers. New products will also need to be developed and approved or cleared by the FDA and foreign regulatory agencies to sustain revenue growth in our markets. Additional clinical data and new products may be necessary to grow revenue. We may not be able to generate, sustain, or increase revenue on a quarterly or annual basis. If we cannot achieve or sustain revenue growth for an extended period, our financial results will be adversely affected and our stock price may decline.

Our products may not achieve or maintain market acceptance.

Even if we obtain FDA approval or clearance of our products, or new indications for our products, market acceptance of our products in the healthcare community, including physicians, patients and third-party payers, depends on many factors, including:

• | our ability to provide incremental clinical and economic data that shows the safety and clinical efficacy and cost effectiveness of, and patient benefits from, our products; |

• | the availability of alternative treatments; |

• | whether our products are included on insurance company formularies; |

• | the willingness and ability of patients and the healthcare community to adopt new technologies; |

• | the convenience and ease of use of our products relative to other treatment methods; |

• | the pricing and reimbursement of our products relative to other treatment methods; and |

• | the marketing and distribution support for our products. |

Even if we obtain all necessary FDA approvals and clearances, any of our products may fail to achieve market acceptance. If we do not educate physicians about PAD and the need to address cardiac device infection through lead removal and the existence of our products, these products may not gain market acceptance, as many physicians do not routinely screen for PAD while screening for coronary artery disease and are not aware of the need to remove and replace coronary leads when treating cardiac device infections. If our products achieve market acceptance, they may not maintain that market acceptance over time if competing products or technologies are introduced that are received more favorably or are more cost effective. Our Lead Management products are used, in part, to remove advisory leads, which are leads for which a physician advisory has been issued by the manufacturer of the lead. When the advisory leads are extracted or become inactive, the market for our Lead Management products will be reduced. Failure to achieve or maintain market acceptance would limit our ability to generate revenue and would have a material adverse effect on our business, financial condition, and results of operations.

If we do not achieve our projected development and commercialization goals, our business may be harmed.

For planning, we estimate the timing of the accomplishment of various scientific, clinical, regulatory and other product development and commercialization goals, which we sometimes refer to as milestones. These milestones may include the commencement or completion of scientific studies and clinical trials and the submission of regulatory filings. From time to time, we publicly announce the expected timing of some of these milestones. We base these milestones on a variety of assumptions, which are subject to numerous risks and uncertainties. There is a risk we will not achieve these milestones on a timely basis or at all. Even if we achieve these milestones, the actual timing of the achievement of these milestones can vary dramatically compared to our estimates, often for reasons beyond our control, depending on numerous factors, including:

• | the rate of progress, costs and results of our clinical trials and research and development activities; |

• | our ability to identify and enroll patients who meet clinical trial eligibility criteria; |

17

• | the extent of scheduling conflicts with participating physicians and clinical institutions; |

• | adverse reactions reported during clinical trials or commercialization; |

• | the ability of our products to meet the standards for clearance or approval; |

• | the receipt of IDE approvals, marketing approvals and clearances by our competitors and by us from the FDA and other regulatory agencies; and |

• | other actions by regulators, including actions related to a class of products. |

If we do not meet these milestones for our products or if we are delayed in achieving these milestones, the development and commercialization of new products, modifications of existing products or sales of existing products for new approved indications may be prevented or delayed, which could damage our reputation or materially adversely affect our business. Even if we achieve a milestone for a product, market acceptance for the product is not assured.

We have a history of losses and may not return to profitability.

We incurred net losses from our inception in 1984 until 2000, and again in 2002, 2006, from 2008 to 2010 and from 2013 to 2015. At December 31, 2015, we had accumulated $194.6 million in net losses since inception. We may not be profitable in the future.

We incurred significant costs in connection with the AngioScore and Stellarex acquisitions, and we have risks associated with integration of the AngioScore and Stellarex acquisitions.

We incurred significant transaction costs relating to the AngioScore and Stellarex acquisitions. Additionally, we have incurred and will continue to incur significant costs in connection with integrating the operations of AngioScore and Stellarex with our own. These costs are charged as an expense in the period incurred. We may not be able to predict the timing, nature and amount of all such costs. These integration costs could materially affect our results of operations in the period in which such charges are recorded. We may not achieve the planned eliminations of duplicative costs or realization of other efficiencies related to the integration of the business in the near term, or at all.

We do not have a history of acquiring businesses or assets of the size and complexity of AngioScore or Stellarex. The success of the acquisitions depends, in part, on our ability to successfully integrate AngioScore’s business and operations and fully realize the anticipated benefits and potential synergies from combining our business with AngioScore’s business and our ability to successfully integrate and operate the Stellarex assets and successfully launch the Stellarex products in Europe and receive approvals for the Stellarex products in other markets in a timely manner. If we are unable to achieve these objectives, the anticipated benefits and potential synergies of these acquisitions may not be realized fully or at all, or may take longer to realize than expected. Any failure to timely realize these anticipated benefits and potential synergies would have a material adverse effect on our business, operating results and financial condition.

We have made certain assumptions relating to the AngioScore and Stellarex acquisitions that have proven in the past and may prove in the future to be materially inaccurate.

We have made certain assumptions relating to the AngioScore and Stellarex acquisitions that relate to numerous matters, including:

• | projections of future revenue and revenue growth rates; |

• | the amount of goodwill and intangibles resulting from the acquisitions; |

• | certain other purchase accounting adjustments that are being recorded in our financial statements in connection with the acquisitions; |

• | our ability to maintain, develop and deepen relationships with customers; and |

• | other financial and strategic risks of the acquisitions. |

18

Certain assumptions relating to the AngioScore and Stellarex acquisitions may prove to be inaccurate. For example, for the year ended December 31, 2015, we failed to achieve the expected revenue growth with respect to the AngioScore acquisition. Our assumptions relating to the AngioScore and Stellarex acquisitions may be inaccurate in the future, which may result in our failure to realize the expected benefits of the acquisitions, failure to realize expected revenue growth rates, failure to receive product clearances or approvals in a timely manner or at all, higher than expected operating, transaction and integration costs, failure to integrate acquired personnel, loss of key employees, loss of key vendors, as well as general economic and business conditions that may adversely affect us following the acquisitions. If our assumptions regarding these acquisitions prove to be inaccurate and we cannot achieve or sustain revenue growth or we experience higher costs for an extended period, our financial results will be adversely affected and our stock price may decline.

If we make additional acquisitions, we could incur significant costs and encounter difficulties that harm our business.

We may acquire companies, products, or technologies in the future. If we engage in such acquisitions, we may incur significant transaction and integration costs and have difficulty integrating the acquired personnel, operations, products or technologies or otherwise realizing synergies or other benefits from the acquisitions. The integration process could result in the loss of key employees, loss of key customers, loss of key vendors, decreases in revenue and increases in operating costs, as well as the disruption of our business. Acquisitions may dilute our earnings per share, disrupt our ongoing business, distract our management and employees, increase our expenses, subject us to liabilities and increase our risk of litigation, all of which could harm our business. If we use cash to acquire companies, products or technologies, it may divert resources otherwise available for other purposes or increase our debt. If we use our common stock to acquire companies, products or technologies, we may experience a change of control or our stockholders may experience substantial dilution or both.

If we cannot obtain additional funding, we may be unable to make desirable acquisitions or fund expanding growth and operations.

We may require additional funds to make acquisitions of desirable companies, products or technologies, or fund expanding growth and operations. There can be no assurance that financing will be available in amounts or on terms acceptable to us, if at all. The inability to obtain additional capital may restrict our ability to grow and may reduce our ability to make desirable acquisitions. Any equity or convertible debt financing may result in substantial dilution to our existing stockholders.

If we do not manage our growth or control costs related to growth, our results of operations will suffer.

We intend to grow our business by expanding our customer base, sales force and product offerings, including through additional acquisitions or other business combinations. Growth could place significant strain on our management, employees, operations, operating and financial systems, and other resources. To accommodate significant growth, we could be required to open additional facilities, expand and improve our information systems and procedures and hire, train, motivate and manage a growing workforce, all of which would increase our costs. Our systems, facilities, procedures and personnel may not be adequate to support our future operations. Further, we may not maintain or accelerate our current growth, manage our expanding operations or achieve planned growth on a timely and profitable basis.

Litigation and other legal proceedings may adversely affect our business.

From time to time we are involved in legal proceedings relating to patent and other intellectual property matters, product liability claims, employee claims, tort or contract claims, federal regulatory investigations, securities class action, and other legal proceedings or investigations, which could have an adverse impact on our reputation, business and financial condition and divert the attention of our management from the operation of our

19

business. Litigation is inherently unpredictable and can result in excessive or unanticipated verdicts and/or injunctive relief that affect how we operate our business. We could incur judgments or enter into settlements of claims for monetary damages or for agreements to change the way we operate our business, or both. There may be an increase in the scope of these matters or there may be additional lawsuits, claims, proceedings or investigations in the future, which could have a material adverse impact on us. Adverse publicity about regulatory or legal action against us could damage our reputation and brand image, undermine our customers’ confidence and reduce long-term demand for our products, even if the regulatory or legal action is unfounded or not material to our operations.

We must indemnify officers and directors, including, in certain circumstances, former employees and directors, against all losses, including expenses, incurred by them in legal proceedings and advance their reasonable legal defense expenses, unless certain conditions apply. Insurance for claims of this nature does not apply in all such circumstances, may be denied or may not be adequate to cover all legal or other costs related to the proceeding. A prolonged uninsured expense and indemnification obligation could have a material adverse impact on us. From 2009 through 2013, we incurred more than $6 million in indemnification costs not covered by insurance for former employees charged in connection with a previously disclosed federal investigation. In connection with an action by a former director of AngioScore, a court held in August 2014 that AngioScore is required to advance the former director’s attorneys’ fees. In November 2015, the court granted in part our motion for summary judgment and ordered that TriReme is liable for 50% of advanced fees and costs, and must pay all fees and costs to be advanced moving forward until such fees and costs equal the fees and costs paid by AngioScore, and thereafter, the fees and costs will be advanced 50% by TriReme and 50% by AngioScore. A judge or jury could determine that AngioScore must ultimately pay the former director’s legal fees and costs defending against the breach of fiduciary duty and other claims, and the fees and costs associated with the dispute regarding indemnification, which could be material. As of December 31, 2015, AngioScore has incurred approximately $12.8 million in advancement costs, which may not be covered by insurance.

We have been named as a defendant in a securities class action lawsuit that may result in substantial costs and could divert management’s attention.

On August 27, 2015, a person purporting to represent a class of persons who purchased our securities between February 19, 2015 and July 23, 2015 filed a lawsuit against us and certain of our officers in the United States District Court for the District of Colorado. The lawsuit asserts claims under Sections 10(b) and 20 of the Securities Exchange Act of 1934, alleging that certain of our public statements concerning our projected revenue for 2015 were false and misleading. Plaintiff seeks unspecified monetary damages on behalf of the alleged class, interest, and attorney’s fees and costs of litigation. On December 18, 2015, the court appointed lead plaintiff and lead counsel in this matter.