Attached files

| file | filename |

|---|---|

| EX-12.1 - EXHIBIT 12.1 - ALLEGHENY TECHNOLOGIES INC | fy201510k121.htm |

| EX-32.1 - EXHIBIT 32.1 - ALLEGHENY TECHNOLOGIES INC | fy201510-k321.htm |

| EX-31.1 - EXHIBIT 31.1 - ALLEGHENY TECHNOLOGIES INC | fy201510-k311.htm |

| EX-21.1 - EXHIBIT 21.1 - ALLEGHENY TECHNOLOGIES INC | fy201510k211.htm |

| EX-31.2 - EXHIBIT 31.2 - ALLEGHENY TECHNOLOGIES INC | fy201510-k312.htm |

| EX-23.1 - EXHIBIT 23.1 - ALLEGHENY TECHNOLOGIES INC | fy201510k231.htm |

| EX-10.33 - EXHIBIT 10.33 - ALLEGHENY TECHNOLOGIES INC | fy201510k1033.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2015

OR

¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission file number 1-12001

ALLEGHENY TECHNOLOGIES INCORPORATED

(Exact name of registrant as specified in its charter)

Delaware | 25-1792394 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

1000 Six PPG Place, Pittsburgh, Pennsylvania | 15222-5479 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (412) 394-2800

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, $0.10 Par Value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the Registrant is well known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | x | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

On February 12, 2016, the Registrant had outstanding 108,912,564 shares of its Common Stock.

The aggregate market value of the Registrant’s voting stock held by non-affiliates at June 30, 2015 was approximately $3.3 billion, based on the closing price per share of Common Stock on June 30, 2015 of $30.20 as reported on the New York Stock Exchange. Shares of Common Stock known by the Registrant to be beneficially owned by directors and officers of the Registrant subject to the reporting and other requirements of Section 16 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are not included in the computation. The Registrant, however, has made no determination that such persons are “affiliates” within the meaning of Rule 12b-2 under the Exchange Act.

Documents Incorporated By Reference

Selected portions of the Proxy Statement for the Annual Meeting of Stockholders to be held on May 6, 2016 are incorporated by reference into Part III of this Report.

1

INDEX

Page Number | |

2

PART I

Item 1. Business

The Company

Allegheny Technologies Incorporated is a Delaware corporation with its principal executive offices located at 1000 Six PPG Place, Pittsburgh, Pennsylvania 15222-5479, telephone number (412) 394-2800, Internet website address http://www.atimetals.com. References to “Allegheny Technologies,” “ATI,” the “Company,” the “Registrant,” “we,” “our” and “us” and similar terms mean Allegheny Technologies Incorporated and its subsidiaries, unless the context otherwise requires.

Our Business

We are one of the largest and most diversified specialty materials and components producers in the world. Our high-value products include titanium and titanium alloys, nickel-based alloys and specialty steels, precision forgings, castings and machined components, zirconium and related alloys, precision and engineered stainless steel strip, and grain-oriented electrical steel. Our standard products include specialty stainless sheet, stainless steel sheet, and stainless steel plate. Our specialty materials are produced in a wide range of alloys and product forms and are selected for use in applications that demand materials having exceptional hardness, toughness, strength, resistance to heat, corrosion or abrasion, or a combination of these characteristics. ATI is a fully integrated supplier from raw material (for titanium sponge) and melt (for other specialty alloy systems) through highly engineered finished components.

ATI’s strategic vision is to be an aligned and integrated specialty materials and components company. Our strategies target the products and global growth markets that require and value ATI’s technical and manufacturing capability leadership. These differentiated products serve key global markets including aerospace and defense, oil & gas/chemical & hydrocarbon processing industry, electrical energy, medical and automotive, and sales to these key global markets represented 79% of total 2015 sales.

We have undertaken a multi-phase program over several years to enhance and expand our capabilities to produce premium specialty materials aimed at these strategic, global markets. We are near the end of this multi-year cycle of capital expenditures on major strategic investments. Since 2004, we have transformed ATI by investing $4.7 billion in capital expenditures and acquisitions. This program has included acquisitions to forward integrate into producing forgings, castings and components, construction and qualification of facilities to backward integrate into producing our own titanium sponge to ensure a stable source of supply, and expanding manufacturing capabilities for producing specialty materials and components that enable ATI to continue to innovate and develop new products to maintain our technological advantage in these differentiated markets. These investments have included expansions of our premium titanium alloy melt and remelt capability; nickel-based alloy and superalloy melt and remelt capability; titanium and specialty alloy plate production capability; and premium titanium and nickel-based superalloy forging capability. Also, we purchased assets that added advanced nickel-based alloy and titanium alloy powders to our product portfolio. In 2014, we acquired precision flowform process technologies to produce thin-walled components in net or near-net shapes across multiple alloy systems, and we acquired capabilities for precision machining parts and components to expand our ability to product finished specialty materials parts and components and reinforce our important aerospace supply chain role.

We made significant progress in 2015 in qualifying and fully integrating several long-term strategic capital projects, including what we believe to be the world’s most advanced and powerful Hot-Rolling and Processing Facility (HRPF) in the specialty materials flat-rolled products industry. The HRPF was fully integrated into our manufacturing operations in 2015, and is a critical part of our strategy to transform our flat-rolled products business into a more competitive and consistently profitable business. The HRPF is designed to:

• | Significantly expand our product offering capabilities, shorten manufacturing cycle times, reduce inventory requirements, and improve the cost structure of our flat-rolled products business. |

• | Provide unsurpassed manufacturing capability and versatility in the production of a wide range of flat-rolled specialty metals, including ATI’s diversified product mix of nickel-based and specialty alloys, titanium and titanium alloys, zirconium alloys, Precision Rolled Strip® products, and stainless sheet and coiled plate products. |

• | Process high-strength carbon steel alloys. We expect to partner with, or provide conversion services for, producers of these carbon steel products. |

Additionally, the premium-quality (PQ) qualification process for our products used in jet engine rotating parts made with titanium sponge produced by our Rowley, UT facility was completed in the second quarter 2015. This marked the completion

3

of a journey from the 2009 commencement of operations that fully qualifies Rowley as a PQ titanium sponge producer for all applications.

These strategic capital projects have been multi-year accomplishments that are expected to begin providing a return on our invested capital after extensive construction and qualification phases. We believe these investments strengthen and enhance ATI’s leadership position in the production of advanced specialty materials.

Strategic end use markets for our products include:

Aerospace and Defense. We are a world leader in the production of premium titanium alloys, nickel-based and cobalt-based alloys and superalloys, and vacuum-melted specialty alloys used in the manufacture of components for both commercial and military jet engines, as well as replacement parts for those engines. We also produce titanium alloys, vacuum-melted specialty alloys, and high-strength stainless alloys for use in commercial and military airframes, airframe components and missiles.

Titanium and titanium alloys are critical metals in aerospace and defense applications. They possess an extraordinary combination of properties, including superior strength-to-weight ratio, elevated temperature resistance, low coefficient of thermal expansion, and extreme corrosion resistance. These metals are used to produce jet engine components such as blades, vanes, discs, and casings, and airframe components such as structural members, landing gear, hydraulic systems, and fasteners. The latest and next-generation airframes and jet engines use increasing amounts of titanium and titanium alloys in component parts in order to minimize weight and maximize fuel efficiency.

Our nickel-based alloys and superalloys and specialty alloys are also widely used in aerospace and defense applications. Nickel-based alloys and superalloys remain extremely strong at high temperatures and resist degradation under extreme conditions. Typical aerospace applications for nickel-based alloys and superalloys and advanced powder alloys include jet engine shafts, discs, blades, vanes, rings and casings. The next generation and future-generation jet engines use new generations of nickel-based superalloys and advanced powder alloys in large part due to increased fuel efficiency requirements that require hotter-burning engines. Our specialty alloys include vacuum-melted maraging steels used in the manufacture of aircraft landing gear and structural components, as well as jet engine components.

Our titanium alloy, nickel-based alloy, and specialty alloy precision forgings are used for hot-section components for jet engines, structural components for aircraft, helicopters, launch vehicles, and other demanding applications. We are a world leader in isothermal and hot-die forging technologies for advanced aerospace components. We produce highly sophisticated components that have differing mechanical properties in different parts of the same piece for greater resistance to fatigue and temperature effects. ATI provides a full range of post-forging inspection, machining and finishing services with the certified quality needed to meet demanding application requirements. ATI has the technology, equipment and know-how to cast titanium parts in some of the largest sizes and most complex shapes currently being manufactured for aerospace applications. ATI’s advanced manufacturing capabilities offer OEMs the freedom to design components with intricate geometries, cored passageways, cast-in features and sculpted surfaces.

ATI’s powder metal technology delivers extreme alloy compositions and refined microstructures that offer increased performance and longer useful lives in high-temperature aerospace environments. Powder metal technology boosts the efficiency of jet engines. Powder delivers the most uniform grain structure achievable, in near-net shapes, to cut reject rates and costs in highly machined components.

We continuously seek to develop innovative new alloys to better serve the needs of this end use market. For example, ATI’s 718Plus® nickel-based superalloy, Rene 65 near-powder superalloy, and our powder alloys have won significant share in the current and next-generation jet engines.

Oil and Gas and Chemical and Hydrocarbon Processing Industry. The environments in which oil and gas can be found in commercial quantities have become more challenging, involving deep offshore wells, high pressure and high temperature conditions in sour wells and unconventional sources, such as shale oil and gas, and oil sands. Challenging offshore environments are in deepwater remote locations that are further off the continental shelf, including arctic and tropical locations, often one mile or more below the water’s surface, and up to two miles below the ocean floor. The requirements for equipment that can operate for up to 30 years in these environments are the specialty materials that we produce.

Both of our business segments produce specialty materials that are critical to the oil and gas industry and the chemical and hydrocarbon processing industry. Our specialty materials, including titanium and titanium alloys, nickel-based alloys, zirconium alloys, stainless and duplex alloys and other specialty alloys have the strength, wear corrosion-resistant properties necessary for difficult environments.

4

Our Datalloy2® and DatalloyHP™ specialty stainless is used for non-magnetic drill collars that enable the most advanced directional and horizontal drilling techniques to be guided to the exact position desired for the reservoir. We have developed a family of duplex alloys, including ATI 2003® and ATI 2102® lean duplex alloys, for use in subsea and deepwater oil and gas applications. Several of our strip, plate and cast products are NORSOK qualified. The NORSOK standards are developed by the Norwegian petroleum industry and are intended to identify materials used in oil and gas applications that are safe and cost-effective.

Electrical Energy. Our specialty materials are widely used in the global electrical power generation and distribution industry.We believe energy needs and environmental policies and the electrification of developing countries will continue to drive demand for our specialty materials and products for use in this industry.

For electrical power generation, our specialty materials, including corrosion-resistant alloys (CRAs), are used in coal, nuclear, and natural gas applications. In coal-fired plants, our CRAs are used for pipe, tube, and heat exchanger applications in water systems in addition to pollution control scrubbers. Our CRAs are also used in water systems, fuel cladding components, and process equipment for nuclear power plants. For nuclear power plants, we are an industry pioneer in producing reactor-grade zirconium and hafnium alloys used in nuclear fuel cladding and structural components. We have developed NushieldTM products, a new line of borated stainless alloys that begin with our advanced powder metals and are used for spent nuclear fuel applications. We are a technology leader for large diameter nickel-based superalloys used in natural gas land-based turbines for power generation. For renewable energy generation, our alloys are used for solar, fuel cell and geothermal applications.

The electrical power distribution market is served by our grain-oriented electrical steel (GOES) products, which are used in distribution and power transformer applications, where low loss magnetic properties are important. Significant global excess capacity and challenging market conditions, including the increasingly stringent transformer efficiency standards and a market shift to high permeability GOES products, resulted in the announced idling of GOES production in December 2015, which is expected to be completed by April 2016. ATI’s future participation in the electrical power distribution market will be dependent on market conditions and our ability to earn an acceptable return on invested capital for these products.

Medical. ATI’s advanced specialty materials are used in medical device products that save and enhance the quality of lives.

Our zirconium-niobium, titanium- and cobalt-based alloys are used for knees, hips and other prosthetic devices. These replacement devices offer the potential of lasting much longer than previous implant options.

Our biocompatible nickel-titanium shape memory alloy is used for stents to support collapsed or clogged blood vessels. Reduced in diameter for insertion, these stents expand to the original tube-like shape due to the metal’s superelasticity. Our ultra fine diameter (0.002 inch/0.051 mm) titanium wire is used for screens to prevent blood clots from entering critical areas of the body. In addition, our titanium bar and wire are used to make surgical screws for bone repairs.

Manufacturers of magnetic resonance imaging (MRI) devices rely on our niobium superconducting wire to help produce electromagnetic fields that allow physicians to safely scan the body’s soft tissue.

Automotive. For automobiles, nickel-based alloys, stainless steel and other ATI specialty materials are the choice for powertrain and structural parts, exhaust system and emission control parts, gaskets, air bag inflator housings, windshield wipers and blades, fuel systems, fasteners, hose clamps, gaskets and other components. Stainless steel is also used on exterior trim for its bright appearance and for internal components for its corrosion resistance.

ATI’s advanced nickel-based alloys and specialty alloys in flat-rolled products are used primarily in engine and exhaust applications in the automotive market. Global demand is expected to grow for our high-value precision and engineered strip for automotive applications such as gaskets, hose clamps, and turbo chargers. As automotive engine operating temperatures get hotter as a result of turbochargers, we bring our expertise in aerospace alloys to the automotive market and alloy mix continues to trend favorably. Our HRPF provides the capability to produce these high-value alloys in wider and longer coils.

We also provide a variety of heat-resistant and corrosion-resistant automotive exhaust alloys. Again, in this application we focus on those exhaust applications that are closer to the engine where exhaust temperatures are highest and corrosion resistance is most severe.

5

Business Segments

We operate in the following two business segments, which accounted for the following percentages of total revenues of $3.72 billion, $4.22 billion, and $4.04 billion for the years ended December 31, 2015, 2014, and 2013, respectively.

2015 | 2014 | 2013 | |||||||

High Performance Materials & Components | 53 | % | 48 | % | 48 | % | |||

Flat Rolled Products | 47 | % | 52 | % | 52 | % | |||

Information with respect to our business segments is presented below and in Note 16 of the notes to the consolidated financial statements.

High Performance Materials & Components Segment

Our High Performance Materials & Components segment produces, converts and distributes a wide range of high performance materials, including titanium and titanium-based alloys, nickel- and cobalt-based alloys and superalloys, zirconium and related alloys including hafnium and niobium, advanced powder alloys and other specialty materials, in long product forms such as ingot, billet, bar, rod, wire, shapes and rectangles, and seamless tubes, plus precision forgings and castings, components and machined parts. These products are designed for the high performance requirements of such major end markets as aerospace and defense (engines and airframes), oil & gas/chemical & hydrocarbon processing industry, electrical energy, and medical. We are integrated from raw materials (titanium sponge) to melt, remelt, finish processing, forging, investment casting, and machining in our titanium and titanium alloys, and zirconium and hafnium alloy products. Most of the products in this segment are sold directly to end-use customers, and a significant portion of our High Performance Materials & Components segment products are sold under multi-year agreements.

Approximately 70% of High Performance Materials & Components segment revenue is derived from the aerospace and defense market. Demand for our products is driven primarily by the commercial aerospace cycle. Large aircraft and aircraft engines are manufactured by a small number of companies, such as The Boeing Company, Airbus S.A.S. (an Airbus Group company), Bombardier Aerospace (a division of Bombardier Inc.), and Embraer (Empresa Brasileira de Aeronáutica S.A.) for airframes, and GE Aviation (a division of General Electric Company), Rolls-Royce plc, Pratt & Whitney (a division of United Technologies Corporation), Snecma (SAFRAN Group), and various joint ventures that manufacture jet engines. These companies and their suppliers form a substantial part of our customer base in this business segment. The loss of one or more of our customers in the aerospace and defense market could have a material adverse effect on ATI’s results of operations and financial condition.

Principal competitors in the High Performance Materials & Components segment include Berkshire Hathaway Inc., for nickel-based alloys and superalloys and specialty steel alloys, titanium and titanium-based alloys, precision forgings and investment castings through its recent acquisition of Precision Castparts Corporation and subsidiaries; Alcoa Inc., for titanium and titanium-based alloys and precision forgings through its recent acquisitions of RTI International Metals, Inc. and Firth Rixson; Carpenter Technology Corporation for nickel-based alloys and superalloys and specialty steel alloys; VSMPO-AVISMA for titanium and titanium-based alloys; and Aubert & Duval for precision forgings.

Flat Rolled Products Segment

Our Flat Rolled Products segment produces, converts and distributes stainless steel, nickel-based alloys, specialty alloys, and titanium and titanium-based alloys, in a variety of product forms including plate, sheet, engineered strip, and Precision Rolled Strip® products, as well as grain-oriented electrical steel. The major end markets for our flat-rolled products are oil & gas/ chemical & hydrocarbon processing industry, electrical energy, automotive, food processing equipment and appliances, construction and mining, electronics, communication equipment and computers, and aerospace and defense. The operations in this segment are ATI Flat Rolled Products and the Chinese joint venture company known as Shanghai STAL Precision Stainless Steel Company Limited (STAL), in which we hold a 60% interest. Segment results also include our 50% interest in the industrial titanium joint venture known as Uniti LLC.

Stainless steel, nickel-based alloys and titanium sheet products are used in a wide variety of industrial and consumer applications. In 2015, approximately 55% by volume of our stainless sheet products were sold to independent service centers, which have slitting, cutting or other processing facilities, with the remainder sold directly to end-use customers.

Engineered strip and very thin Precision Rolled Strip products, which are under 0.015 inches thick, are used by customers to fabricate a variety of products primarily in the automotive, construction, and electronics markets. In 2015, approximately 95% by volume of our engineered strip and Precision Rolled Strip products were sold directly to end-use customers or through our own distribution network, with the remainder sold to independent service centers.

6

Stainless steel, nickel-based alloy and titanium plate products are primarily used in industrial markets. In 2015, approximately 40% by volume of our plate products were sold to independent service centers, with the remainder sold directly to end-use customers.

Grain-oriented electrical steel (GOES) is used in power transformers where electrical conductivity and magnetic properties are important. Nearly all of our grain-oriented electrical steel products are sold directly to end-use customers.

Competition in the Flat Rolled Products segment includes domestic stainless steel competitors AK Steel Corporation, North American Stainless, and Outokumpu Stainless USA, LLC, as well as imports from numerous Chinese producers, Ta Chen International Corporation of Taiwan, and Aperam, based in Europe. Competitors for nickel-based alloys and superalloys and specialty steel alloys include Haynes International and VDM Metals GmbH. Competitors for GOES include AK Steel Corporation and imports from China, Russia, Japan, Korea, and various European Union countries.

Significant global overcapacity for stainless steel and GOES flat-rolled products has intensified the price competition in this segment over the last several years. Some of our foreign competitors are either directly or indirectly subsidized by governments. In 1999, the United States imposed anti-dumping and countervailing duties on dumped and subsidized imports of stainless steel sheet and strip in coils and stainless steel plate in coils from companies in ten foreign countries. The anti-dumping and countervailing duty orders were reviewed in 2011 by the U.S. Department of Commerce and the U.S. International Trade Commission to determine whether the orders should remain in place for another five years. The agencies decided that eight such orders against five countries will continue in effect. Additionally, on February 12, 2016, ATI and the three domestic stainless steel competitors filed antidumping and countervailing duty petitions concurrently with the U.S. Department of Commerce and the U.S International Trade Commission, charging that unfairly traded imports of stainless steel sheet and strip from the People’s Republic of China are causing material injury to the domestic stainless steel industry. We continue to monitor imports from foreign producers for appropriate action.

In December 2015, we announced rightsizing actions to better align our ATI Flat Rolled Products operations to the challenging market conditions for our commodity products. Such actions included the idling of the standard stainless melt shop and sheet finishing operations at the Midland, PA facility, which was completed in January 2016, and the idling of the GOES operations in Western PA, including the Bagdad, PA facility, which is expected to be completed by April 2016. The future restart of the Midland and GOES operations, respectively, will depend on future business conditions and our ability to earn an acceptable return on invested capital on products manufactured at these operations.

Raw Materials and Supplies

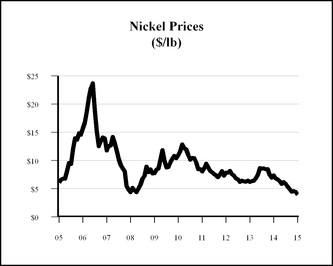

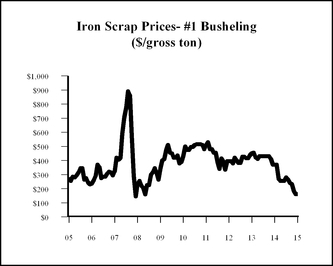

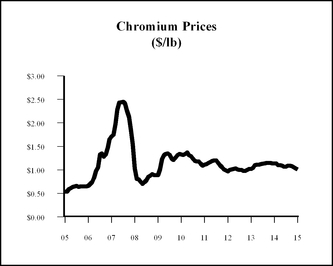

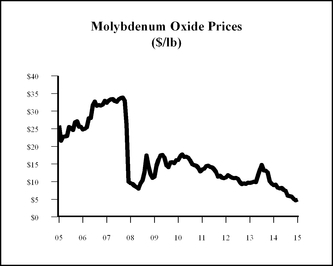

Substantially all raw materials and supplies required in the manufacture of our products are available from more than one supplier and the sources and availability of raw materials essential to our businesses are currently adequate. The principal raw materials we use in the production of our specialty materials are scrap (including iron-, nickel-, chromium-, titanium-, and molybdenum-bearing scrap), nickel, titanium sponge, zirconium sand and sponge, ferrochromium, ferrosilicon, molybdenum and molybdenum alloys, manganese and manganese alloys, cobalt, niobium, vanadium and other alloying materials.

Purchase prices of certain principal raw materials have been volatile. As a result, our operating results may be subject to significant fluctuation. We use raw materials surcharge and index mechanisms to offset the impact of changes in raw material costs; however, competitive factors in the marketplace may limit our ability to institute such mechanisms, and there can be a delay between the change in the price of raw materials and the impact of such mechanisms. For example, in 2015 we used approximately 95 million pounds of nickel; therefore a hypothetical change of a $1.00 per pound increase in nickel prices would result in increased costs of approximately $95 million. We also used approximately 800 million pounds of ferrous scrap in the production of our flat-rolled products; a hypothetical change of a $0.01 per pound increase would result in increased costs of approximately $8 million.

While we have increased our manufacturing capacity to produce titanium sponge, the major raw material for our titanium products, a portion of our needs, together with certain other raw materials, such as nickel, cobalt, and ferrochromium, are available to us and our specialty materials industry competitors primarily from foreign sources. Some of these foreign sources are located in countries that may be subject to unstable political and economic conditions, which could disrupt supplies or affect the price of these materials.

We purchase our nickel requirements principally from producers in Australia, Canada, Norway, Russia, and the Dominican Republic. Zirconium raw materials are primarily purchased from the United States and China. Cobalt is purchased primarily from producers in Canada. More than 80% of the world’s reserves of ferrochromium are located in South Africa, Zimbabwe, Albania, and Kazakhstan. Niobium is purchased primarily from producers in Brazil. We also purchase titanium sponge from sources in Russia, Kazakhstan, and Japan.

7

Export Sales and Foreign Operations

Direct international sales represented approximately 42% of our total annual sales in 2015, 38% of our total sales in 2014, and 39% of our total sales in 2013. These figures include direct export sales by our U.S.-based operations to customers in foreign countries, which accounted for approximately 33% of our total sales in 2015, 28% of our total sales in 2014, and 29% of our total sales in 2013. Our overseas sales, marketing and distribution efforts are aided by our international marketing and distribution offices, ATI Europe, ATI Europe Distribution, and ATI Asia, or by independent representatives at various locations throughout the world. We believe that at least 50% of ATI’s 2015 sales were driven by global markets when we consider exports of our customers. Direct sales by geographic area in 2015, and as a percentage of total sales, were as follows:

(In millions) | |||||||

United States | $ | 2,142.6 | 58 | % | |||

Europe | 809.2 | 21 | % | ||||

Asia | 503.9 | 14 | % | ||||

Canada | 154.5 | 4 | % | ||||

South America, Middle East and other | 109.4 | 3 | % | ||||

Total sales | $ | 3,719.6 | 100 | % | |||

Our High Performance Materials & Components segment has manufacturing capabilities for melting, remelting, forging and finishing nickel-based alloys and specialty alloys in the United Kingdom, and manufacturing capabilities for precision forging and machining in Poland, primarily serving the construction, transportation and aerospace markets. Within our Flat Rolled Products segment, our STAL joint venture in the People’s Republic of China produces Precision Rolled Strip products, which enables us to offer these products more effectively to markets in China and other Asian countries. Our Uniti LLC joint venture allows us to offer titanium products to industrial markets more effectively worldwide.

Backlog, Seasonality and Cyclicality

Our backlog of confirmed orders was approximately $1.5 billion at December 31, 2015 and $1.7 billion at December 31, 2014. We expect that approximately 85% of confirmed orders on hand at December 31, 2015 will be filled during the year ending December 31, 2016. Backlog of confirmed orders of our High Performance Materials & Components segment was approximately $1.3 billion at December 31, 2015 and $1.4 billion at December 31, 2014. We expect that approximately 85% of the confirmed orders on hand at December 31, 2015 for this segment will be filled during the year ending December 31, 2016. Backlog of confirmed orders of our Flat Rolled Products segment was approximately $0.2 billion at December 31, 2015 and $0.3 billion at December 31, 2014. We expect that all of the confirmed orders on hand at December 31, 2015 for this segment will be filled during the year ending December 31, 2016.

Generally, our sales and operations are not seasonal. However, demand for our products is cyclical over longer periods because specialty materials customers operate in cyclical industries and are subject to changes in general economic conditions and other factors both external and internal to those industries.

Research, Development and Technical Services

We believe that our research and development capabilities give ATI an advantage in developing new products and manufacturing processes that contribute to the profitable growth potential of our businesses on a long-term basis. We conduct research and development at our various operating locations both for our own account and, on a limited basis, for customers on a contract basis. Research and development expenditures for the years ended December 31, 2015, 2014, and 2013 included the following:

(In millions) | 2015 | 2014 | 2013 | |||||||||

Company-Funded: | ||||||||||||

High Performance Materials & Components | $ | 10.0 | $ | 12.9 | $ | 11.7 | ||||||

Flat Rolled Products | 4.0 | 4.3 | 4.3 | |||||||||

Corporate | 0.2 | 0.2 | 0.1 | |||||||||

$ | 14.2 | $ | 17.4 | $ | 16.1 | |||||||

Customer-Funded: | ||||||||||||

High Performance Materials & Components | $ | 1.5 | $ | 2.7 | $ | 2.7 | ||||||

Total Research and Development | $ | 15.7 | $ | 20.1 | $ | 18.8 | ||||||

8

Our research, development and technical service activities are closely interrelated and are directed toward cost reduction and process improvement, process control, quality assurance and control, system development, the development of new manufacturing methods, the improvement of existing manufacturing methods, the improvement of existing products, and the development of new products.

We own hundreds of United States patents, many of which are also filed under the patent laws of other nations. Although these patents, as well as our numerous trademarks, technical information, license agreements, and other intellectual property, have been and are expected to be of value, we believe that the loss of any single such item or technically related group of such items would not materially affect the conduct of our business.

Environmental, Health and Safety Matters

We are subject to various domestic and international environmental laws and regulations that govern the discharge of pollutants, and disposal of wastes, and which may require that we investigate and remediate the effects of the release or disposal of materials at sites associated with past and present operations. We could incur substantial cleanup costs, fines, civil or criminal sanctions, third party property damage or personal injury claims as a result of violations or liabilities under these laws or non-compliance with environmental permits required at our facilities. We are currently involved in the investigation and remediation of a number of our current and former sites as well as third party sites.

We consider environmental compliance to be an integral part of our operations. We have a comprehensive environmental management and reporting program that focuses on compliance with applicable federal, state, regional and local environmental laws and regulations. Each operating company has an environmental management system that includes mechanisms for regularly evaluating environmental compliance and managing changes in business operations while assessing environmental impact.

Our Corporate Guidelines for Business Conduct and Ethics address compliance with environmental laws as well as employment and workplace safety laws, and also describe our commitment to equal opportunity and fair treatment of employees. We continued to focus on safety across ATI’s operations during 2015. As a result of our continuing focus on and commitment to safety, in 2015 our OSHA Total Recordable Incident Rate was 1.88 and our Lost Time Case Rate was 0.29, which improved versus 2014 and which we believe to be competitive with world-class performance for our industry.

Employees

We have approximately 9,200 full-time employees, of which approximately 15% are located outside the United States. Approximately 50% of our workforce is covered by various collective bargaining agreements, predominantly with the United Steel, Paper and Forestry, Rubber, Manufacturing, Energy, Allied & Industrial Service Workers International Union, AFL-CIO, CLC (“USW”). The collective bargaining agreements between ATI and the USW at many of our Flat Rolled Products segment facilities, and at two High Performance Materials & Components segment facilities located in Albany, OR and Lockport, NY, expired on June 30, 2015. Due to the lack of progress in ongoing contract negotiations, we issued a lockout notice involving more than 2,000 workers at various facilities which took effect August 15, 2015. We have and will continue to operate the affected facilities and continue serving customer needs with our salaried and non-union employees and temporary professional staffing until the contract negotiations are resolved. On February 22, 2016, we reached a tentative agreement with the bargaining committee of the USW on a new labor contract, which would end the lockout. The contract is subject to ratification by USW members.

Available Information

Our Internet website address is http://www.atimetals.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as well as proxy and information statements and other information that we file, are available free of charge through our Internet website as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the United States Securities and Exchange Commission (“SEC”). Our Internet website and the content contained therein or connected thereto are not intended to be incorporated into this Annual Report on Form 10-K. You may read and copy materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet website at http://www.sec.gov, which contains reports, proxy and information statements and other information that we file electronically with the SEC.

9

Executive Management, Including Executive Officers under Federal Securities Laws

The following are members of the Company’s executive management, including executive officers under the federal securities laws, as of February 15, 2016:

Name | Age | Title | ||

Richard J. Harshman | 59 | Chairman, President and Chief Executive Officer | ||

Patrick J. DeCourcy | 53 | Senior Vice President, Finance and Chief Financial Officer | ||

Hunter R. Dalton | 61 | Executive Vice President, Strategic Growth Initiatives | ||

John D. Sims | 56 | Executive Vice President, High Performance Materials and Components Segment | ||

Robert S. Wetherbee | 56 | Executive Vice President, ATI Flat Rolled Products Group | ||

Elliot S. Davis | 54 | Senior Vice President, General Counsel, Chief Compliance Officer and Corporate Secretary | ||

Kevin B. Kramer | 56 | Senior Vice President, Chief Commercial and Marketing Officer | ||

Elizabeth C. Powers | 56 | Senior Vice President, Chief Human Resources Officer | ||

Karl D. Schwartz | 52 | Vice President, Controller and Chief Accounting Officer | ||

All individuals in the above table are subject to the reporting and other requirements of Section 16 of the Securities Exchange Act of 1934, as amended.

Set forth below are descriptions of the business backgrounds for the past five years of the Company’s executive officers and management.

Richard J. Harshman became Chairman, President and Chief Executive Officer in May 2011. Mr. Harshman was President and Chief Operating Officer from 2010 to May 2011. Prior to that, he served as Executive Vice President, Finance and Chief Financial Officer from 2003 to 2010.

Patrick J. DeCourcy, has served as Senior Vice President, Finance and Chief Financial Officer since December 2013. He was Interim Chief Financial Officer from July 2013 to December 2013. From 2011 to July 2013, Mr. DeCourcy provided assistance to ATI executive management with business integration and strategic investments and was Senior Director, Strategic Projects and Business Integration, from March 2012 to July 2013. From 2000 to 2010, he served as Vice President, Finance and Administration of ATI Specialty Materials.

Hunter R. Dalton has served as Executive Vice President, Strategic Growth Initiatives since August 2015. He was Executive Vice President, ATI High Performance Specialty Materials Group from May 2011 to August 2015, and was President, ATI Specialty Materials from 2008 to August 2015. Previously, he served as Group President, ATI Long Products from 2008 to May 2011. From 2003 to 2008, Mr. Dalton served as Senior Vice President of Sales and Marketing for ATI Specialty Materials.

John D. Sims has served as Executive Vice President, High Performance Materials and Components Segment since August 2015. He was Executive Vice President, ATI High Performance Components Group from September 2013 to August 2015 and President, ATI Forged Products from September 2013 to April 2014. Previously, he was Executive Vice President, Primary Titanium Operations, and Engineered Alloys and Products beginning in February 2013. Prior to that, Mr. Sims served as Executive Vice President, Primary Metals and Exotic Alloys from May 2011 to February 2013 and President, Specialty Alloys & Components from 2008 to February 2013. Previously, he was Group President, ATI Primary Metals and Exotic Alloys from February 2011 to May 2011.

Robert S. Wetherbee began serving as Executive Vice President, ATI Flat Rolled Products group in January 2015. He served as President, ATI Flat Rolled Products beginning April 1, 2014. Prior to that, Mr. Wetherbee was President and Chief Executive Officer of Minerals Technologies, Inc. from March 2013 until February 2014. Mr. Wetherbee was President of ATI’s tungsten materials business from 2010 through 2012. Previously, he was Vice President of Market Strategy of Alcoa Inc. from 2006 through 2009.

Elliot S. Davis became Senior Vice President, General Counsel, Chief Compliance Officer and Corporate Secretary in May 2011. Previously, Mr. Davis was Vice President and General Counsel from 2010 to May 2011. Mr. Davis served as Assistant General Counsel from 2008, when he joined the Company, to 2010. Prior to that, Mr. Davis was a partner of the law firm K&L Gates LLP, where he practiced for nearly 20 years in its corporate, mergers and acquisitions and securities group.

Kevin B. Kramer was named Senior Vice President, Chief Commercial and Marketing Officer when he joined the Company in February 2014. Prior to joining ATI, Mr. Kramer was President - Stoneridge Wiring Division and Vice President of Stoneridge, Inc., from May 2012 through January 2014. Previously, Mr. Kramer worked for Alcoa, Inc. from 2004 until 2012, where he had served as President - Growth Initiatives and President - Wheel and Transportation Products.

10

Elizabeth C. Powers joined ATI in November 2014 as Senior Vice President, Chief Human Resources Officer. Ms. Powers served as Vice President, Human Resources and Chief Administrative Officer for Dresser-Rand Group, Inc. from 2010 until 2012 and from 2005 to 2009. She was named Vice President, Human Resources of Dresser-Rand Group in 2004. From 2012 until she joined ATI, Ms. Powers worked in academia. In 2009 and 2010, Ms. Powers worked in the public policy and non-profit sectors.

Karl D. Schwartz is Vice President, Controller and Chief Accounting Officer and has served in that role since January 2016. Previously, he was Controller and Chief Accounting Officer from May 2011 to January 2016, and Controller and Principal Accounting Officer from 2010 to May 2011. Prior to that, Mr. Schwartz was Assistant Controller beginning in 2002, when he joined the Company.

Item 1A. Risk Factors

There are inherent risks and uncertainties associated with our business that could adversely affect our operating performance and financial condition. Set forth below are descriptions of those risks and uncertainties that we currently believe to be material, but the risks and uncertainties described are not the only risks and uncertainties that could affect our business. See the discussion under “Forward-Looking Statements” in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, in this Annual Report on Form 10-K.

Cyclical Demand for Products. The cyclical nature of the industries in which our customers operate causes demand for our products to be cyclical, creating potential uncertainty regarding future profitability. Various changes in general economic conditions may affect the industries in which our customers operate. These changes could include decreases in the rate of consumption or use of our customers’ products due to economic downturns. Other factors that may cause fluctuation in our customers’ positions are changes in market demand, lower overall pricing due to domestic and international overcapacity, currency fluctuations, lower priced imports and increases in use or decreases in prices of substitute materials. As a result of these factors, our profitability has been and may in the future be subject to significant fluctuation.

Worldwide economic conditions deteriorated significantly in the recent past and could remain weak in the future. These conditions have had, and may continue to have, an adverse effect on demand for our customers’ products and, in turn, on demand for our products. If these conditions persist or worsen, our results of operations and financial condition could be materially adversely affected.

Volatility of Raw Material Costs. Most of our inventory is valued utilizing the LIFO costing methodology. Inventory of our non-U.S. operations is valued using average cost or FIFO methods. Under the LIFO inventory valuation method, changes in the cost of raw materials and production activities are recognized in cost of sales in the current period even though these material and other costs may have been incurred at significantly different values due to the length of time of our production cycle. In a period of rising prices, cost of sales expense recognized under LIFO is generally higher than the cash costs incurred to acquire the inventory sold. Conversely, in a period of declining raw material prices, cost of sales recognized under LIFO is generally lower than cash costs incurred to acquire the inventory sold. Generally, over time based on overall inflationary trends in raw materials, labor and overhead costs, the use of the LIFO inventory valuation method will result in a LIFO inventory valuation reserve, as the higher current period costs are included in cost of sales and the balance sheet carrying value of inventory is reduced.

The prices for many of the raw materials we use have been extremely volatile during the past several years. Since we value most of our inventory utilizing the LIFO inventory costing methodology, a fall in raw material costs results in a benefit to operating results by reducing cost of sales and increasing the inventory carrying value, while conversely, a rise in raw material costs has a negative effect on our operating results by increasing cost of sales while lowering the carrying value of inventory. For example, for the year ended December 31, 2015, the effect of falling raw material costs on our LIFO inventory valuation method resulted in cost of sales that were $131.6 million lower than what would have been recognized under the FIFO costing methodology to value our inventory.

Due primarily to persistent raw material deflation over the last several years, we are in an unusual situation of having a LIFO inventory balance that exceeds replacement cost. In cases where inventory at FIFO cost is lower than the LIFO carrying value, a write-down of the inventory to market may be required, subject to a lower of cost or market evaluation. In applying the lower of cost or market principle, market means current replacement cost, subject to a ceiling (market value shall not exceed net realizable value) and a floor (market shall not be less than net realizable value reduced by an allowance for a normal profit margin). We evaluate product lines on a quarterly basis to identify inventory values that exceed estimated net realizable value. The calculation of a resulting reserve, if any, is recognized as an expense in the period that the need for the reserve is identified.

Due to the long lead times required to manufacture many of our products, volatility in raw material prices exposes us to cash costs that may not be fully recovered through surcharge and index pricing mechanisms.

11

Product Pricing. From time-to-time, reduced demand, intense competition and excess manufacturing capacity have resulted in reduced prices, excluding raw material surcharges, for many of our products. These factors have had and may have an adverse impact on our revenues, operating results and financial condition.

Although inflationary trends in recent years have been moderate, during most of the same period certain critical raw material costs, such as nickel, titanium sponge, chromium, and molybdenum and scrap containing iron, nickel, titanium, chromium, and molybdenum have been volatile. While we have been able to mitigate some of the adverse impact of volatile raw material costs through raw material surcharges or indices to customers, rapid changes in raw material costs may adversely affect our results of operations.

We change prices on certain of our products from time-to-time. The ability to implement price increases is dependent on market conditions, economic factors, raw material costs and availability, competitive factors, operating costs and other factors, some of which are beyond our control. The benefits of any price increases may be delayed due to long manufacturing lead times and the terms of existing contracts.

Risks Associated with Commercial Aerospace. A significant portion of the sales of our High Performance Materials & Components segment represents products sold to customers in the commercial aerospace industry. The commercial aerospace industry has historically been cyclical due to factors both external and internal to the airline industry. These factors include general economic conditions, airline profitability, consumer demand for air travel, varying fuel and labor costs, execution of projected build rates, price competition, and international and domestic political conditions such as military conflict and the threat of terrorism. The length and degree of cyclical fluctuation are influenced by these factors and therefore are difficult to predict with certainty. Demand for our products in this segment is subject to these cyclical trends. A downturn in the commercial aerospace industry has had, and may in the future have, an adverse effect on the prices at which we are able to sell these and other products, and our results of operations, business and financial condition could be materially adversely affected.

Risks Associated with Strategic Capital Projects. From time-to-time, we undertake strategic capital projects in order to enhance, expand and/or upgrade our facilities and operational capabilities. For instance, over the last several years we have undertaken major expansions of our titanium and premium-melt nickel-based alloy, superalloy and specialty alloy production capabilities, and finished product commissioning of a new advanced specialty materials hot-rolling and processing facility. Our ability to achieve the anticipated increased revenues or otherwise realize acceptable returns on these investments or other strategic capital projects that we may undertake is subject to a number of risks, many of which are beyond our control, including a variety of market, operational, permitting, and labor-related factors. In addition, the cost to implement any given strategic capital project ultimately may prove to be greater than originally anticipated. If we are not able to achieve the anticipated results from the implementation of any of our strategic capital projects, or if we incur unanticipated implementation costs or delays, our results of operations and financial position may be materially adversely affected.

Dependence on Critical Raw Materials Subject to Price and Availability Fluctuations. We rely to a substantial extent on third parties to supply certain raw materials that are critical to the manufacture of our products. Purchase prices and availability of these critical raw materials are subject to volatility. At any given time we may be unable to obtain an adequate supply of these critical raw materials on a timely basis, on price and other terms acceptable, or at all.

If suppliers increase the price of critical raw materials, we may not have alternative sources of supply. In addition, to the extent that we have quoted prices to customers and accepted customer orders for products prior to purchasing necessary raw materials, or have existing contracts, we may be unable to raise the price of products to cover all or part of the increased cost of the raw materials.

The manufacture of some of our products is a complex process and requires long lead times. As a result, we may experience delays or shortages in the supply of raw materials. If unable to obtain adequate and timely deliveries of required raw materials, we may be unable to timely manufacture sufficient quantities of products. This could cause us to lose sales, incur additional costs, delay new product introductions, or suffer harm to our reputation.

We acquire certain important raw materials that we use to produce specialty materials, including nickel, zirconium, niobium, chromium, cobalt, and titanium sponge, from foreign sources. Some of these sources operate in countries that may be subject to unstable political and economic conditions. These conditions may disrupt supplies or affect the prices of these materials.

Availability of Energy Resources. We rely upon third parties for our supply of energy resources consumed in the manufacture of our products. The prices for and availability of electricity, natural gas, oil and other energy resources are subject to volatile market conditions. These market conditions often are affected by political and economic factors beyond our control. Disruptions in the supply of energy resources could temporarily impair the ability to manufacture products for customers. Further, increases in energy costs, or changes in costs relative to energy costs paid by competitors, has and may continue to

12

adversely affect our profitability. To the extent that these uncertainties cause suppliers and customers to be more cost sensitive, increased energy prices may have an adverse effect on our results of operations and financial condition.

Risks Associated with Environmental Matters. We are subject to various domestic and international environmental laws and regulations that govern the discharge of pollutants, and disposal of wastes, and which may require that we investigate and remediate the effects of the release or disposal of materials at sites associated with past and present operations. We could incur substantial cleanup costs, fines and civil or criminal sanctions, third party property damage or personal injury claims as a result of violations or liabilities under these laws or non-compliance with environmental permits required at our facilities. We are currently involved in the investigation and remediation of a number of our current and former sites as well as third party sites. We also could be subject to future laws and regulations that govern greenhouse gas emissions and various matters related to climate change, which could increase our operating costs.

With respect to proceedings brought under the federal Superfund laws, or similar state statutes, we have been identified as a potentially responsible party (PRP) at approximately 42 of such sites, excluding those at which we believe we have no future liability. Our involvement is limited or de minimis at approximately 25 of these sites, and the potential loss exposure with respect to 12 individual sites is not considered to be material.

We are a party to various cost-sharing arrangements with other PRPs at most of the sites. The terms of the cost-sharing arrangements are subject to non-disclosure agreements as confidential information. Nevertheless, the cost-sharing arrangements generally require all PRPs to post financial assurance of the performance of the obligations or to pre-pay into an escrow or trust account their share of anticipated site-related costs. In addition, the Federal government, through various agencies, is a party to several such arrangements.

We believe that we operate our businesses in compliance in all material respects with applicable environmental laws and regulations. However, from time-to-time, we are a party to lawsuits and other proceedings involving alleged violations of, or liabilities arising from, environmental laws. When our liability is probable and we can reasonably estimate our costs, we record environmental liabilities in our financial statements. In many cases, we are not able to determine whether we are liable or if liability is probable to reasonably estimate the loss or range of loss. Estimates of our liability remain subject to additional uncertainties, including the nature and extent of site contamination, available remediation alternatives, the extent of corrective actions that may be required, and the participation number and financial condition of other PRPs, as well as the extent of their responsibility for the remediation. We intend to adjust our accruals to reflect new information as appropriate. Future adjustments could have a material adverse effect on our results of operations in a given period, but we cannot reliably predict the amounts of such future adjustments. At December 31, 2015, our reserves for environmental matters totaled approximately $15 million. Based on currently available information, we do not believe that there is a reasonable possibility that a loss exceeding the amount already accrued for any of the sites with which we are currently associated (either individually or in the aggregate) will be an amount that would be material to a decision to buy or sell our securities. Future developments, administrative actions or liabilities relating to environmental matters, however, could have a material adverse effect on our financial condition or results of operations.

Risks Associated with Current or Future Litigation and Claims. A number of lawsuits, claims and proceedings have been or may be asserted against us relating to the conduct of our currently and formerly owned businesses, including those pertaining to product liability, patent infringement, commercial, government contracting, employment, employee and retiree benefits, taxes, environmental, health and safety and occupational disease, and stockholder and corporate governance matters. Due to the uncertainties of litigation, we can give no assurance that we will prevail on all claims made against us in the lawsuits that we currently face or that additional claims will not be made against us in the future. While the outcome of litigation cannot be predicted with certainty, and some of these lawsuits, claims or proceedings may be determined adversely to us, we do not believe that the disposition of any such pending matters is likely to have a material adverse effect on our financial condition or liquidity, although the resolution in any reporting period of one or more of these matters could have a material adverse effect on our results of operations for that period. Also, we can give no assurance that any other matters brought in the future will not have a material effect on our financial condition, liquidity or results of operations.

Labor Matters. We have approximately 9,200 full-time employees, of which approximately 15% are located outside the United States. Approximately 50% of our workforce is covered by various collective bargaining agreements, predominantly with the USW. At various times, our collective bargaining agreements expire and are subject to renegotiation. The collective bargaining agreements between ATI and the USW at many of our Flat Rolled Products segment facilities, and at two High Performance Materials & Components segment facilities located in Albany, OR and Lockport, NY, expired on June 30, 2015. Due to the lack of progress in ongoing contract negotiations, we issued a lockout notice involving more than 2,000 workers at various facilities which took effect August 15, 2015. On February 22, 2016, we reached a tentative agreement with the bargaining committee of the USW on a new labor contract, which would end the lockout. The contract is subject to ratification by USW members. Generally, collective bargaining agreements that expire may be terminated after notice by the union. After

13

termination, the union may authorize a strike. A labor dispute, which could lead to a strike, lockout, or other work stoppage by the employees covered by one or more of the collective bargaining agreements, could have a material adverse effect on production at one or more of our facilities and, depending upon the length of such dispute or work stoppage, on our operating results. There can be no assurance that we will succeed in concluding collective bargaining agreements to replace those that expire.

Export Sales. We believe that export sales will continue to account for a significant percentage of our future revenues. Risks associated with export sales include: political and economic instability, including weak conditions in the world’s economies; accounts receivable collection; export controls; changes in legal and regulatory requirements; policy changes affecting the markets for our products; changes in tax laws and tariffs; trade duties; and exchange rate fluctuations (which may affect sales to international customers and the value of profits earned on export sales when converted into dollars). Any of these factors could materially adversely affect our results for the period in which they occur.

Risks Associated with Retirement Benefits. At December 31, 2015, our U.S. qualified defined benefit pension plan was approximately 71% funded as calculated in accordance with U.S. generally accepted accounting principles, and we are not required to make any significant contributions to this plan in 2016. However, we may be required to fund the U.S. qualified defined benefit pension plan in the years beyond 2016 depending upon the value of plan investments and obligations in the future and changes in laws or regulations that govern pension plan funding. Depending on the timing and amount, a requirement that we fund our U.S. qualified defined benefit pension plan could have a material adverse effect on our results of operations and financial condition.

Risks Associated with Acquisition and Disposition Strategies. We intend to continue to strategically position our businesses in order to improve our ability to compete. Strategies we employ to accomplish this may include seeking new or expanding existing specialty market niches for our products, expanding our global presence, acquiring businesses complementary to existing strengths, and continually evaluating the performance and strategic fit of our existing business units. From time-to-time, management holds discussions with management of other companies to explore acquisitions, joint ventures, and other business combination opportunities as well as possible business unit dispositions. As a result, the relative makeup of the businesses comprising our Company is subject to change. Acquisitions, joint ventures, and other business combinations involve various inherent risks, such as: assessing accurately the value, strengths, weaknesses, contingent and other liabilities and potential profitability of acquisition or other transaction candidates; the potential loss of key personnel of an acquired business; our ability to achieve identified financial and operating synergies, growth or other benefits anticipated to result from an acquisition or other transaction; and unanticipated changes in business and economic conditions affecting an acquisition or other transaction. International acquisitions and other transactions could be affected by export controls, exchange rate fluctuations, domestic and foreign political conditions, changes in tax laws and a deterioration in domestic and foreign economic conditions.

Risks Associated with Information Technology. Information technology infrastructure is critical to supporting business objectives; failure of our information technology infrastructure to operate effectively could adversely affect our business. We depend heavily on information technology infrastructure to achieve our business objectives. If a problem occurs that impairs this infrastructure, the resulting disruption could impede our ability to record or process orders, manufacture and ship in a timely manner, or otherwise carry on business in the normal course. Any such events could cause us to lose customers or revenue and could require us to incur significant expense to remediate.

As we integrate, implement and deploy new information technology processes and information infrastructure across our operations, we could experience disruptions in our business that could have an adverse effect on our business, financial condition, results of operations and cash flow.

Cyber Security Threats. Increased global information technology threats, security requirements, vulnerabilities, and a rise in sophisticated and targeted international computer crime pose a risk to the security of our systems and networks and the confidentiality, availability and integrity of our data. We believe that ATI faces the threat of such cyber attacks due to the markets we serve, the products we manufacture, the locations of our operations, and global interest in our technology. Due to the evolving nature of cyber security threats, the scope and impact of any incident cannot be predicted. We continually work to safeguard our systems and mitigate potential risks. Despite our efforts to protect sensitive information and confidential and personal data, our facilities and systems and those of our third-party service providers may be vulnerable to security breaches. This could lead to disclosure, modification or destruction of proprietary and other key information, defective products, production downtimes, operational disruptions, and remediation costs, which in turn could adversely affect our reputation, competitiveness and results of operations.

14

Internal Controls Over Financial Reporting. Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Insurance. We have maintained various forms of insurance, including insurance covering claims related to our properties and risks associated with our operations. Our existing property and liability insurance coverages contain exclusions and limitations on coverage. From time-to-time, in connection with renewals of insurance, we have experienced additional exclusions and limitations on coverage, larger self-insured retentions and deductibles, and significantly higher premiums. As a result, in the future our insurance coverage may not cover claims to the extent that it has in the past and the costs that we incur to procure insurance may increase significantly, either of which could have an adverse effect on our results of operations.

Political and Social Turmoil. The war on terrorism as well as political and social turmoil could put pressure on economic conditions in the United States and worldwide. These political, social and economic conditions could make it difficult for us, our suppliers, and our customers to forecast accurately and plan future business activities, and could adversely affect the financial condition of our suppliers and customers and affect customer decisions as to the amount and timing of purchases from us. As a result, our business, financial condition and results of operations could be materially adversely affected.

Risks Associated with Government Contracts. Some of our operating units perform contractual work directly or indirectly for the U.S. Government, which requires compliance with laws and regulations relating to the performance of Government contracts. Various claims (whether based on U.S. Government or Company audits and investigations or otherwise) could be asserted against us related to our U.S. Government contract work. Depending on the circumstances and the outcome, such proceedings could result in fines, penalties, compensatory and treble damages or the cancellation or suspension of payments under one or more U.S. Government contracts. Under government regulations, a company, or one or more of its operating divisions or units, can also be suspended or debarred from government contracts based on the results of investigations.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Our principal domestic facilities for our high performance materials include titanium sponge production, melting operations, and production facilities that include processing and finishing operations. Our titanium sponge production facility is located in Rowley, UT. Domestic melting operations are located in Monroe and Bakers, NC, and Lockport, NY (vacuum induction melting, vacuum arc re-melt, electro-slag re-melt, plasma melting), Richland, WA (electron beam melting), and Albany, OR (vacuum arc re-melt). Production of high performance materials, most of which are in long product form, takes place at our domestic facilities in Monroe and Bakers, NC, Lockport, NY, Richburg, SC, Albany, OR, and Oakdale, PA. Our production of zirconium and related specialty alloys takes place at facilities located in Millersburg, OR, Huntsville, AL, and Frackville, PA. Our production of highly engineered forgings, castings, and machined components takes place at facilities in Cudahy and Coon Valley, WI, East Hartford, CT, Albany, OR, Irvine, CA, Portland, IN, Lebanon, KY, Billerica, MA, and Salem, OR.

Our principal domestic locations for melting stainless steel and other flat-rolled specialty materials are located in Brackenridge, Midland, and Latrobe, PA. Hot-rolling is performed at our domestic facilities in Brackenridge and Washington, PA. Finishing of our flat-rolled products takes place at our domestic facilities located in Brackenridge, Bagdad, Vandergrift, Midland, Washington, Rochester, Monaca, and Zelienople, PA, and in Waterbury, CT, New Bedford, MA, Louisville, OH, and Bridgeview, IL.

Substantially all of our properties are owned, and three of our properties are subject to mortgages or similar encumbrances securing borrowings under certain industrial development authority financings.

We also own or lease facilities in a number of foreign countries, including France, Germany, the United Kingdom, Poland, and the People’s Republic of China. We own and/or lease and operate facilities for melting and re-melting, machining and bar mill operations, laboratories and offices located in Sheffield, England. We own highly engineered forging and machining operations in Stalowa Wola, Poland. Through our STAL joint venture, we operate facilities for finishing Precision Rolled Strip products in the Xin-Zhuang Industrial Zone, Shanghai, China.

Our executive offices, located in PPG Place in Pittsburgh, PA, are leased.

Although our facilities vary in terms of age and condition, we believe that they have been well maintained and are in sufficient condition for us to carry on our activities.

15

Item 3. Legal Proceedings

From time-to-time, we become involved in various lawsuits, claims and proceedings relating to the conduct of our current and formerly owned businesses, including those pertaining to product liability, patent infringement, commercial, government contracting, employment, employee and retiree benefits, taxes, environmental, health and safety and occupational disease, and stockholder and corporate governance matters. While we cannot predict the outcome of any lawsuit, claim or proceeding, our management believes that the disposition of any pending matters is not likely to have a material adverse effect on our financial condition or liquidity. The resolution in any reporting period of one or more of these matters, including those described above, however, could have a material adverse effect on our results of operations for that period.

On February 11, 2016, the National Labor Relations Board (NLRB) served a complaint on ATI that alleges that the Company violated the National Labor Relations Act in connection with its collective bargaining negotiations with the USW and by locking out its USW-represented employees effective August 15, 2015. On February 22, 2016, the Company and the USW bargaining committee reached a tentative agreement, which would end the lockout and which provides for withdrawal of the complaint by the NLRB. The contract is subject to ratification by USW members.

Information relating to legal proceedings is included in Note 21. Commitments and Contingencies of the Notes to Consolidated Financial Statements and incorporated herein by reference.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Common Stock Prices

Our common stock is traded on the New York Stock Exchange (symbol ATI). At February 4, 2016, there were 3,686 record holders of Allegheny Technologies Incorporated common stock. We paid a quarterly cash dividend of $0.08 per share of common stock outstanding for the fourth quarter of 2015 and $0.18 per share of common stock outstanding for the first three quarters of 2015 and all four quarters of 2014. The payment of dividends and the amount of such dividends depends upon matters deemed relevant by our Board of Directors, such as our results of operations, financial condition, cash requirements, future prospects, any limitations imposed by law, credit agreements or senior securities, and other factors deemed relevant and appropriate. Our Asset Based Lending (“ABL”) Revolving Credit Facility restricts our ability to pay dividends in certain circumstances. For more information on the restrictions under our ABL facility, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Financial Condition and Liquidity - Dividends.”

The ranges of high and low sales prices for shares of our common stock for the quarterly periods ended on the dates indicated were as follows:

2015 | March 31 | June 30 | September 30 | December 31 | ||||||||||||

High | $ | 35.10 | $ | 37.76 | $ | 31.02 | $ | 19.10 | ||||||||

Low | $ | 27.12 | $ | 29.05 | $ | 13.66 | $ | 10.15 | ||||||||

2014 | March 31 | June 30 | September 30 | December 31 | ||||||||||||

High | $ | 38.30 | $ | 45.26 | $ | 46.32 | $ | 36.99 | ||||||||

Low | $ | 29.74 | $ | 37.56 | $ | 36.74 | $ | 30.02 | ||||||||

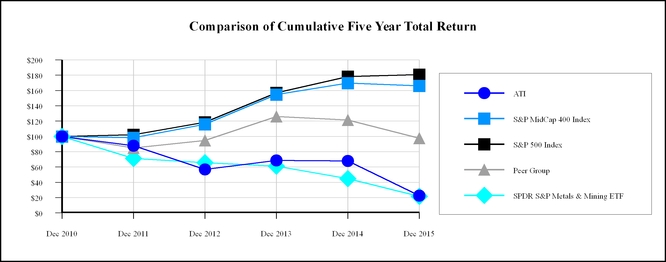

Cumulative Total Stockholder Return

The graph set forth below shows the cumulative total stockholder return (i.e., price change plus reinvestment of dividends) on our common stock from December 31, 2010 through December 31, 2015, as compared to (i) the S&P 500 Index, (ii) the S&P MidCap 400 Index and (iii) a Peer Group of companies. In recent years, we included the S&P 500 Index in our stock performance graphs because we were a component company of the S&P 500 and believed that it provided the most meaningful comparison to evaluate our cumulative total stockholder return. We are now including the S&P MidCap 400 Index because it is comprised of issuers currently having a market capitalization similar to ours now that we are a component company of that index. We do not intend to include the S&P 500 Index in our performance graph after this year absent a change in circumstances. We have included the SPDR S&P Metals and Mining Index ETF because our stock price trading and volatility trends with the performance of that index. We believe that the Peer Group of companies, which is defined below, is representative of companies in our industry that have served similar markets during the applicable periods. The total

16