Attached files

| file | filename |

|---|---|

| EX-32.1 - EX-32.1 - MARKETAXESS HOLDINGS INC | mktx-ex321_8.htm |

| EX-21.1 - EX-21.1 - MARKETAXESS HOLDINGS INC | mktx-ex211_6.htm |

| EX-31.2 - EX-31.2 - MARKETAXESS HOLDINGS INC | mktx-ex312_7.htm |

| EX-31.1 - EX-31.1 - MARKETAXESS HOLDINGS INC | mktx-ex311_9.htm |

| EX-32.2 - EX-32.2 - MARKETAXESS HOLDINGS INC | mktx-ex322_11.htm |

| EX-23.1 - EX-23.1 - MARKETAXESS HOLDINGS INC | mktx-ex231_10.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

|

þ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

|

¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 001-34091

MARKETAXESS HOLDINGS INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

52-2230784 |

|

(State of incorporation) |

|

(IRS Employer Identification No.) |

|

|

|

|

|

299 Park Avenue, New York, New York |

|

10171 |

|

(Address of principal executive offices) |

|

(Zip Code) |

(212) 813-6000

(Registrant’s telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

|

Title of each class: |

|

Name of each exchange on which registered: |

|

Common Stock, par value $0.003 per share |

|

NASDAQ Global Select Market |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

|

þ |

|

Accelerated filer |

|

¨ |

|

|

|

|

|

|||

|

Non-accelerated filer |

|

¨ (Do not check if a smaller reporting company) |

|

Smaller reporting company |

|

¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The aggregate market value of the shares of common stock held by non-affiliates of the registrant as of June 30, 2015 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $3.4 billion computed by reference to the last reported sale price on the NASDAQ Global Select Market on that date. For purposes of this calculation, affiliates are considered to be officers, directors and holders of 10% or more of the outstanding common stock of the registrant on that date. The registrant had 37,308,457 shares of common stock, 1,004,608 of which were held by affiliates, outstanding on that date.

As of February 22, 2016, the aggregate number of shares of the registrant’s common stock outstanding was 37,522,515.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for the 2016 Annual Meeting of Stockholders are incorporated by reference into Items 10, 11, 12, 13 and 14 of Part III of this Form 10-K.

2015 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

|

|

|

|

|

Page |

|

|

|

|

||

|

|

|

|||

|

Item 1: |

|

|

3 |

|

|

Item 1A: |

|

|

18 |

|

|

Item 1B: |

|

|

36 |

|

|

Item 2: |

|

|

36 |

|

|

Item 3: |

|

|

36 |

|

|

Item 4: |

|

|

36 |

|

|

|

|

|

||

|

|

|

|||

|

Item 5: |

|

|

37 |

|

|

Item 6: |

|

|

39 |

|

|

Item 7: |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

42 |

|

Item 7A: |

|

|

60 |

|

|

Item 8: |

|

|

62 |

|

|

Item 9: |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

88 |

|

Item 9A: |

|

|

88 |

|

|

Item 9B: |

|

|

88 |

|

|

|

|

|

||

|

|

|

|||

|

Item 10: |

|

|

89 |

|

|

Item 11: |

|

|

89 |

|

|

Item 12: |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

89 |

|

Item 13: |

|

Certain Relationships and Related Transactions and Director Independence |

|

89 |

|

Item 14: |

|

|

89 |

|

|

|

|

|

||

|

|

|

|||

|

Item 15: |

|

|

90 |

|

2

Forward-Looking Statements

This report contains certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements may be identified by words such as “expects,” “intends,” “anticipates,” “plans,” “believes,” “seeks,” “estimates,” “will,” or words of similar meaning and include, but are not limited to, statements regarding the outlook for our future business and financial performance. Forward-looking statements are based on management’s current expectations and assumptions, which are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. It is routine for our internal projections and expectations to change as the year or each quarter in the year progresses, and therefore it should be clearly understood that the internal projections and beliefs upon which we base our expectations may change prior to the end of each quarter or the year. Although these expectations may change, we are under no obligation to revise or update any forward-looking statements contained in this report. Our company policy is generally to provide our expectations only once per quarter, and not to update that information until the next quarter. Actual future events or results may differ, perhaps materially, from those contained in the projections or forward-looking statements. Factors that could cause or contribute to such differences include those discussed below and elsewhere in this report, particularly in Item 1A “Risk Factors.”

MarketAxess Holdings Inc. (the “Company” or “MarketAxess”) operates a leading electronic trading platform that enables fixed-income market participants to efficiently trade corporate bonds and other types of fixed-income instruments using our patented trading technology. Our over 1,000 active participant firms include broker-dealer clients, investment advisers, mutual funds, insurance companies, public and private pension funds, bank portfolios and hedge funds. Our approximately 100 broker-dealer market-maker clients provide liquidity on the platform and include most of the leading broker-dealers in global fixed-income trading. Through our Open TradingTM initiative, we also execute certain bond transactions between and among institutional investor and broker-dealer clients on a matched principal basis by serving as counterparty to both the buyer and the seller in trades which then settle through a third-party clearing broker. We provide fixed-income market data, analytics and compliance tools that help our clients make trading decisions. We also provide trade matching and regulatory transaction reporting services to the securities markets. In addition, we provide technology solutions and professional consulting services to fixed-income industry participants.

Our multi-dealer trading platform allows our institutional investor clients to simultaneously request competing, executable bids or offers from our broker-dealer clients and execute trades with the broker-dealer of their choice from among those that choose to respond. We offer our broker-dealer clients a solution that enables them to efficiently reach our institutional investor clients for the distribution and trading of bonds. Our trading platform provides access to global liquidity in U.S. high-grade corporate bonds, emerging markets and high-yield bonds, European bonds, U.S. agency bonds, credit derivatives and other fixed-income securities.

Our Open TradingTM protocols allow our broker-dealer and institutional investor clients to interact in an all-to-all trading environment. These innovative technology solutions are designed to increase the number of potential trading counterparties on our electronic trading platform and create a menu of solutions to address different trade sizes and bond liquidity characteristics.

The majority of our revenues are derived from commissions for trades executed on our platform and distribution fees that are billed to our broker-dealer clients on a monthly basis. We also derive revenues from information and post-trade services, technology products and services, investment income and other income. Our expenses consist of employee compensation and benefits, depreciation and amortization, technology and communication expenses, professional and consulting fees, occupancy, marketing and advertising and other general and administrative expenses.

Traditionally, bond trading has been a manual process, with product and price discovery conducted over the telephone between two or more parties. This traditional process has a number of shortcomings resulting primarily from the lack of a central trading facility for these securities, which makes it difficult to match buyers and sellers for particular issues. Many corporate bond trading participants use e-mail and other electronic means of communication for trading corporate bonds. While this has addressed some of the shortcomings associated with traditional corporate bond trading, we believe that the process is still hindered by limited liquidity, limited price transparency, significant transaction costs, compliance and regulatory challenges, and difficulty in executing numerous trades at one time.

Through our disclosed multi-dealer Request For Quote (“RFQ”) trading functionality, our institutional investor clients can determine prices available for a security, a process called price discovery, and then trade those securities directly with our broker-dealer clients. The price discovery process includes the ability to view indicative prices from the broker-dealer clients’ inventory available on our platform, access to real-time pricing information and analytical tools (including spread-to-Treasury data, search capabilities and independent third-party credit research) available on our BondTickerTM service and the ability to request executable bids and offers simultaneously from all of our participating broker-dealer clients during the trade process. On average, institutional

3

investor clients receive several bids or offers from broker-dealer clients in response to trade inquiries. However, some trade inquiries may not receive any bids or offers.

Our services relating to trade execution include single and multiple-dealer inquiries; list trading, which is the ability to request bids and offers on multiple bonds at the same time; and swap trading, which is the ability to request an offer to purchase one bond and a bid to sell another bond, in a manner such that the two trades will be executed simultaneously, with payment based on the price differential of the bonds. Once a trade is completed on our platform, the broker-dealer client and institutional investor client may settle the trade with the assistance of our automated post-trade messaging, which facilitates the communication of trade acknowledgment and allocation information between our institutional investor and broker-dealer clients.

According to the Federal Reserve, outstanding U.S. high-grade corporate bond debt has increased approximately 52% from year-end 2008 to September 30, 2015, the most recent date available. During this same period, financial market regulators have increased capital requirements for bank-owned broker-dealers holding corporate bond inventory. As a result, corporate bond debt owned by institutional investors has increased, while the available base of capital for dealer market making has declined. Partly as a result of these trends, overall secondary turnover as a percentage of corporate debt outstanding has been falling, causing all market participants to look for new electronic trading solutions to improve liquidity and turnover. We have responded with a series of new Open TradingTM protocols designed to allow our broker-dealer and institutional investor clients to interact in an all-to-all trading environment. During 2015, we completed approximately 180,000 trades utilizing our Open Trading™ solutions, an increase of 134% compared to 2014.

Typically, we are not a party to the trades that occur on our platform between institutional investor clients and broker-dealer clients; rather, we serve as an intermediary between broker-dealers and institutional investors, enabling them to meet, agree on a price and then transact with each other. However, in connection with our Open Trading™ or other anonymous protocols, we execute bond transactions between and among institutional investor and broker-dealer clients on a matched principal basis by serving as counterparty to both the buyer and the seller in matching back-to-back trades which are then settled through a third-party clearing broker.

Our broker-dealer clients accounted for approximately 97% of the underwriting of newly-issued U.S. corporate bonds and approximately 79% of the underwriting of newly issued European corporate bonds in 2015. We believe these broker-dealers also represent the principal source of secondary market liquidity in the other markets in which we operate. Secondary market liquidity refers to the ability of market participants to buy or sell a security quickly and in large volume subsequent to the original issuance of the security, without substantially affecting the price of the security. In addition to trading fixed-income securities by traditional means, including the telephone and e-mail, our broker-dealer clients use proprietary single-dealer systems and other trading platforms, as well as our electronic trading platform. We believe that the traditional means of trading remain the manner in which the majority of bonds are traded between institutional investors and broker-dealers.

In 2015, our volume in U.S. high-grade corporate bonds represented approximately 16.8% of the total estimated adjusted U.S. high-grade corporate bond volume, as reported by the Financial Industry Regulatory Authority (“FINRA”) Trade Reporting and Compliance Engine (“TRACE”). We adjusted the reported U.S. high-grade TRACE volumes to eliminate the increased reporting of affiliate back-to-back trades by certain broker-dealers that occurred from April 2014 through October 2015 and the inclusion of 144A securities in reported TRACE volumes beginning on July 1, 2014. TRACE facilitates the mandatory reporting of over-the-counter (“OTC”) secondary market transactions in eligible fixed-income securities in the U.S., including trading between institutional investors and broker-dealers, as well as inter-dealer and retail trading. All broker-dealers that are FINRA member firms have an obligation to report transactions in corporate bonds to TRACE under a set of rules approved by the Securities and Exchange Commission (“SEC”). We provide both the reported and adjusted U.S. high-grade TRACE volumes on our website. We believe that the adjusted estimated volumes provide a more accurate comparison to prior period reporting.

Through our Trax® brand, we provide trade matching and regulatory transaction reporting services for European securities and market and reference data across a range of fixed-income products. Trax provides the Company with an expanded set of technology solutions ahead of incoming pre-and post-trade transparency mandates from the Markets in Financial Instruments Directive (“MiFID”) II in Europe.

Industry Background

Fixed-income securities are issued by corporations, governments and other entities, and pay a pre-set absolute or relative rate of return. As of September 30, 2015, the most recent date available, there were approximately $39.6 trillion principal amount of fixed-income securities outstanding in the U.S. market, including $8.2 trillion principal amount of U.S. corporate bonds, according to the Securities Industry and Financial Markets Association (“SIFMA”). The estimated average daily trading volume of U.S. corporate bonds, as measured by TRACE, was $24.0 billion in 2015. Primary dealer holdings of U.S. corporate bonds (investment-grade and high-yield) as reported by the Federal Reserve Bank of New York were $8.7 billion as of December 31, 2015. This represents less than one day of trading volume as measured by TRACE.

4

U.S. High-Grade Corporate Bond Market

The U.S. corporate bond market consists of three broad categories of securities: investment-grade debt (so-called “high-grade”), which typically refers to debt rated BBB- or better by Standard & Poor’s or Baa3 or better by Moody’s Investor Service; debt rated below investment-grade (so-called “high-yield”), which typically refers to debt rated lower than BBB- by Standard & Poor’s or Baa3 by Moody’s Investor Service; and debt convertible into equity (so-called “convertible debt”). We use the terms high-grade debt and investment-grade debt interchangeably in this Annual Report on Form 10-K.

The U.S. high-grade corporate bond market represents the largest subset of the U.S. corporate bond market. FINRA includes over 46,000 unique securities in the list of TRACE-eligible bonds, representing the majority of the daily trading volume of high-grade bonds. According to the Federal Reserve, U.S. high-grade corporate bond debt outstanding has increased approximately 26.0% from $6.5 trillion at year-end 2010 to $8.2 trillion at September 30, 2015. Over the last four years, high-grade corporate bond issuance was over $1.0 trillion each year, exceeding pre-financial crisis levels. Notwithstanding the growth in the total amount of debt outstanding, turnover (which is the total amount traded as a percentage of the amount outstanding for the bonds that traded) is below credit-crisis lows. The trading volume of U.S. high-grade corporate bonds as reported by TRACE increased to approximately $4.0 trillion for the year ended December 31, 2015, compared to $3.7 trillion and $3.6 trillion for the years ended December 31, 2014 and 2013, respectively. We believe that the low level of turnover is an indicator of liquidity challenges in the credit markets.

Prior to regulatory reforms such as Basel III and regulations under The Dodd–Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), dealer balance sheets were relatively elastic, so dealers were able to facilitate trading in most fixed-income products without dramatic price moves. The regulatory reforms enacted after the global financial crisis resulted in greater capital and liquidity requirements for dealers, which impacted market liquidity and diminished risk appetite by market intermediaries. The Volcker Rule, which limits proprietary trading by banks, has also had an impact on dealer inventories and the ability of dealers to act as effective market-makers. As a result, we believe market participants require new solutions to increase liquidity and we have responded with our Open Trading™ protocols, designed to allow our broker-dealer and institutional investor clients to interact in an all-to-all trading environment.

Emerging Markets Bond Market

We define the emerging markets bond market generally to include U.S. dollar, Euro or local currency denominated bonds issued by sovereign entities or corporations domiciled in a developing country. These issuers are typically located in Latin America, Asia, or Central and Eastern Europe. Examples of countries we classify as emerging markets include: Argentina, Brazil, Colombia, Mexico, Peru, the Philippines, Russia, Turkey and Venezuela.

The institutional investor base for emerging markets bonds includes many crossover investors from the high-yield and high-grade investment areas. Institutional investors have been drawn to emerging markets bonds by their high returns and high growth potential. The average daily trading volume of emerging markets debt, as reported by the Emerging Markets Trade Association for the quarter ended September 30, 2015, the most recent date available, was $6.7 billion of external markets debt and $11.0 billion of local markets debt.

Crossover and High-Yield Bond Market

We define the high-yield bond market generally to include all debt rated lower than BBB- by Standard & Poor’s or Baa3 by Moody’s Investor Service. We define the crossover market to include any debt issue rated below investment-grade by one agency but investment-grade by the other. The total amount of high-yield corporate bonds yearly issuance as reported by SIFMA decreased by 16.3% to $260.5 billion in 2015 from $311.4 billion in 2014, primarily due to the risk aversion among corporate bond investors that severely limited the ability of high-yield issuers to raise new debt. The average daily trading volume of high-yield bonds as measured by TRACE for the year ended December 31, 2015 was approximately $8.1 billion.

European High-Grade Corporate Bond Market

The European high-grade corporate bond market consists of a broad range of products, issuers and currencies. We define the European high-grade corporate bond market generally to consist of bonds intended to be distributed to European investors, primarily bonds issued by European corporations, excluding bonds that are issued by corporations domiciled in an emerging markets country and excluding most government bonds that trade in Europe. Examples include:

|

|

· |

bonds issued by European corporations, denominated in any currency; |

|

|

· |

bonds generally denominated in Euros, U.S. dollars or Pounds Sterling, excluding bonds that are issued by corporations domiciled in an emerging market; |

|

|

· |

bonds issued by supra-national organizations (entities that include a number of central banks or government financial authorities, such as the World Bank), agencies and governments located in Europe, generally denominated in Euros, |

5

|

|

U.S. dollars or Pounds Sterling, provided that such currency is not the currency of the country where the bond was issued; and |

|

|

· |

floating-rate notes issued by European corporations. |

We believe that the European high-grade corporate bond market is impacted by many of the same factors as the U.S. high-grade corporate bond market.

U.S. Agency Bond Market

We define the U.S. agency bond market to include debt issued by a U.S. government-sponsored enterprise. Some prominent issuers of agency bonds are the Federal National Mortgage Association and Federal Home Loan Mortgage Corporation. The total amount of U.S. agency bonds outstanding was approximately $2.0 trillion as of September 30, 2015 as reported by SIFMA. The average daily trading volume of U.S. agency bonds (excluding mortgage-backed securities) as measured by TRACE declined from approximately $10.2 billion at December 31, 2011 to $5.0 billion for the year ended December 31, 2015.

Credit Derivative Market

Credit derivatives are contracts on an underlying asset that transfer risk and return from one party to another without transferring ownership of the underlying asset, allowing market participants to obtain credit protection or assume credit exposure associated with a broad range of issuers of fixed-income securities and other debt obligations. Among the most significant requirements of the derivatives section of the Dodd-Frank Act are mandatory clearing of certain derivatives transactions (“swaps”) through regulated central clearing organizations and mandatory trading of those swaps through either regulated exchanges or swap execution facilities (“SEFs”), in each case, subject to certain key exceptions. We operate a swap execution facility pursuant to the U.S. Commodity Futures Trading Commission’s (“CFTC”) rules and we list certain credit derivatives for trading by U.S. persons and other participants on our SEF. The U.S. Securities and Exchange Commission (“SEC”) has not yet finalized its rules for security-based SEFs that would govern the execution of single-name credit derivatives, nor has it published a timetable for the finalization and implementation of such rules. According to The Depository Trust & Clearing Corporation Trade Information Warehouse, the average daily trading volume of credit derivatives for the year ended December 31, 2015 was approximately $86.0 billion.

Trade Matching and Regulatory Transaction Reporting Services

In Europe, the first MiFID set best-execution requirements for trades and mandated that financial firms submit to their local regulators detailed end-of-day reports, including the time and price of a trade, the counterparty involved and whether it was a purchase or sale. Firms must either become so-called approved reporting mechanisms (“ARMs”) or use one of the approved providers, such as our Trax® ARM to submit such reports. In the U.K., required transactions are reported to the Financial Conduct Authority (“FCA”). MiFID II will increase the number of fields that must be reported to regulators and we expect the demand for experienced regulatory trade reporting service providers to increase over the next several years.

Trade matching enables counterparties to agree the terms of a trade shortly after execution, reducing the risk of errors and a trade failing during settlement. In 2014, the Central Securities Depositories Regulation shortened the securities settlement cycle for all cash securities, including corporate bonds, across the European Union (“EU”) to no later than two days after the date on which a trade is executed, referred to as a T+2 settlement cycle. We believe that the move to T+2 settlement increased the need for trade matching services, such as those provided by our Trax® brand in Europe.

Our Competitive Strengths

Our electronic trading platform provides solutions to some of the shortcomings of traditional bond trading methods. The benefits of our solution are demonstrable throughout the trading cycle:

|

|

· |

Pre-trade — In the pre-trade period, our platform assists our participants by providing them with value-added services, such as real time and historical trade price information, liquidity and turnover analytics, bond reference data and trade order matching alerts; |

|

|

· |

Trade — Our innovative electronic trading platform enables our participants to, among other things, request and receive single and multiple security trade execution, with access to broad and unique sources of liquidity from our growing network of participating firms, and the ability to choose from a wide menu of electronic trading protocols to address different trade sizes and liquidity characteristics; and |

|

|

· |

Post-trade — Following the execution of a trade, our platform supports all of the essential tools and functionalities to enable our participants to realize the full benefits of electronic trading and demonstrate best execution, including real-time trade details, straight-through processing (“STP”), account allocations, automated audit trails, regulatory trade reporting, trade detail matching, and transaction cost analysis. |

6

We believe that we are well positioned to strengthen our market position in electronic trading in our existing products and to extend our presence into new products and services by capitalizing on our competitive strengths, including:

Significant Trading Volumes with Participation by Leading Broker-Dealers and Institutional Investors

Our electronic trading platform provides access to the liquidity provided through the participation on our platform of over 1,000 active institutional investor and broker-dealer clients, including substantially all of the leading broker-dealers in global fixed-income trading. We believe these broker-dealers represent the principal source of secondary market liquidity for U.S. high-grade corporate bonds, emerging markets and high-yield bonds, European high-grade corporate bonds and the other markets in which we operate. Our broker-dealer clients are motivated to continue to utilize our platform due to the presence on the platform of our large network of institutional investor clients.

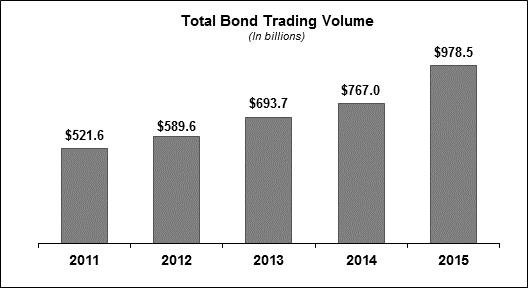

Our total bond trading volume increased from $521.6 billion in 2011 to $978.5 billion in 2015, as indicated below:

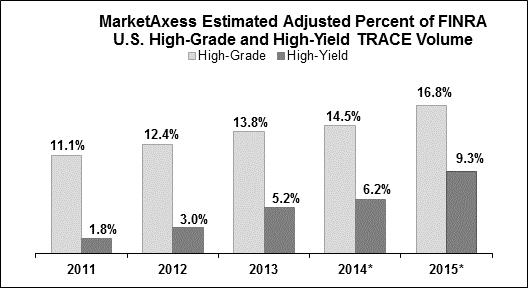

Our adjusted estimated share of U.S. high-grade and high-yield corporate bond volume for 2015 was approximately 16.8% and 9.3%, respectively. Our estimated market share from 2011 to 2015 is shown in the chart below:

*Adjusted by us to eliminate the increased reporting of affiliated back-to-back trades to FINRA by certain broker-dealers that occurred from April 2014 through October 2015 and the inclusion of 144A securities in reported TRACE volumes beginning on July 1, 2014.

7

Execution Benefits to Clients

Benefits to Institutional Investor Clients

We believe we provide numerous benefits to our institutional investor clients over traditional fixed-income trading methods, including:

Competitive Prices. By enabling institutional investors to simultaneously request bids or offers from our broker-dealer clients, we believe our electronic trading platform creates an environment that motivates our broker-dealer clients to provide competitive prices and gives institutional investors confidence that they are obtaining a competitive price. For typical MarketAxess multi-dealer corporate bond inquiries, the range of competitive spread-to-Treasury responses is approximately 9 basis points (a basis point is 1/100 of 1% in yield). As an example of the potential cost savings to institutional investors, a one basis point savings on a $1 million face amount trade of a bond with 10 years to maturity translates to aggregate savings of approximately $800.00. We believe our Open TradingTM protocols enhance our institutional investor clients’ ability to obtain a competitive price by allowing all of our Open TradingTM participants to interact in an all-to-all trading environment, thereby increasing the potential sources of liquidity for each participant, as well as the likelihood of receiving a competitive price response.

Improved Cost Efficiency. We believe that we provide improved efficiency by reducing the time and labor required to conduct broad product and price discovery. Single-security and multi-security (bid or offer lists) inquiries can be efficiently conducted with multiple broker-dealers. In addition, our BondTickerTM service eliminates the need for manually-intensive phone calls or e-mail communication to gather, sort and analyze information concerning historical transaction prices.

Benefits to Broker-Dealer Clients

We also provide substantial benefits to our broker-dealer clients over traditional fixed-income trading methods, including:

Greater Sales Efficiency. We offer our broker-dealer clients broad connectivity with our institutional investor clients. Through this connectivity, our broker-dealer clients are able to efficiently display their indications of interest to buy and sell various securities. We also enable broker-dealers to broaden their distribution by participating in transactions to which they otherwise may not have had access. In addition, the ability to post prices and electronically execute on straightforward trades enables bond sales professionals at broker-dealer firms to focus their efforts on higher value-added trades and more complex transactions.

More Efficient Inventory Management. The posting of inventory to, and the ability to respond to inquiries from, a broad pool of institutional investors, creates an increased opportunity for broker-dealers to identify demand for their inventory, particularly in less liquid securities. As a result, we believe they can achieve enhanced bond inventory turnover, which may limit credit exposure.

Benefits to Both Institutional Investor and Broker-Dealer Clients

We offer additional benefits over traditional fixed-income trading methods that are shared by both institutional investor and broker-dealer clients, including:

Transparent Pricing on a Range of Securities. Institutional investors and broker-dealer clients can search bonds in inventory based on combinations of issuer, issue, rating, maturity, spread-to-Treasury, size and dealer providing the listing, in a fraction of the time it takes to do so manually. Clients can also request executable bids and offers on our electronic trading platform on any debt security in a database of corporate bonds, although there can be no assurance as to the number of market participants who will choose to provide an executable price. Our platform transmits bid and offer requests in real-time to other participants, who may respond with executable prices within the time period specified by the requestor. Through our Open Trading™ protocols, participants may also elect to display live requests for bids or offers anonymously to all other users of our electronic trading platform, in order to create broader visibility of their inquiry among market participants and increase the likelihood that the request results in a trade. We believe that broader participation in client inquiries will result in more trade matches and lower transaction costs.

Greater Trading Accuracy. Our electronic trading platform includes verification mechanisms at various stages of the execution process which result in greater accuracy in the processing, confirming and clearing of trades between institutional investor and broker-dealer clients. These verification mechanisms are designed to ensure that our broker-dealer and institutional investor clients are sending accurate trade messages by providing multiple opportunities to verify they are trading the correct bond, at the agreed-upon price and size. Our platform assists our institutional investor clients in automating the transmittal of order tickets from the portfolio manager to the trader, and from the trader to back-office personnel. This automation provides more timely execution and a reduction in the likelihood of errors that can result from manual entry of information into different systems.

Efficient Risk Monitoring and Compliance. Institutional investors and their regulators are increasingly focused on ensuring that best execution is achieved for fixed-income trades. Our electronic trading platform offers both institutional investors and broker-dealers an automated audit trail for each stage in the trading cycle. This enables compliance personnel to review information relating to trades more easily and with greater reliability. Trade information, including time, price and spread-to-Treasury, is stored securely

8

and automatically on our electronic trading platform. This data represents a valuable source of information for our clients’ compliance personnel. Importantly, we believe the automated audit trail, together with the competitive pricing that is a feature of our electronic trading platform, gives fiduciaries the ability to demonstrate that they have achieved best execution on behalf of their clients.

Other Service Offerings

In addition to services directly related to the execution of trades, we offer our clients several other services, including:

Information Services. The information and analytical tools we provide to our clients help them make investment and trading decisions. Our BondTickerTM service provides access to real-time and historical price, yield and MarketAxess estimated spread-to-Treasuries for publicly disseminated TRACE-eligible bonds. BondTickerTM combines publicly-available TRACE data with the prices for trades executed on our U.S. high-grade electronic trading platform, integrating the two data sources and providing real-time TRACE data with associated analytical tools that are not otherwise available. Our electronic trading platform allows institutional investors to compile, sort and use information to discover investment opportunities that might have been difficult or impossible to identify using a manual information-gathering process or other electronic services.

Through our Trax® brand, we provide a range of information solutions for financial services firms, utilizing quotes contributed by market participants and leveraging our trade matching and regulatory transaction reporting services for European securities. We provide market participants with access to pricing, liquidity and volume data on over 50,000 unique fixed-income securities. We also provide access to securities reference data on approximately 300,000 fixed-income securities.

Post-Trade Services. Our Trax® service provides post-trade, pre-settlement trade matching and regulatory reporting for the European markets. It allows subscribers to match and report trades in a range of capital market instruments, including bonds, derivatives, equities and swaps. Following the implementation of the T+2 settlement cycle for transferable securities in European markets, subscribers can use Trax® to match trades on trade date and help reduce settlement risk. Trax® has approximately 100 clients, including broker-dealers, hedge funds and investment banks. The Trax® platform processed over 1.0 billion transactions in 2015.

Straight-Through Processing. STP refers to the integration of systems and processes to automate the trade process from end-to-end — trade execution, confirmation and settlement — without the need for manual intervention. Our electronic trading platform provides broker-dealers and institutional investors with the ability to automate portions of their transaction processing requirements, improving accuracy and efficiency. Through electronic messaging, institutional investors can submit inquiries to, and receive electronic notices of execution from us, in industry standard protocols, complete with all relevant trade details. Institutional investors can download trade messages, allocate trades to the sub-accounts on whose behalf the trades were made and send the allocations to broker-dealers for confirmation.

Technology Products and Services. We provide technology solutions and professional consulting services to fixed-income industry participants. Technology projects have ranged from enhancing regional broker-dealer systems to developing full-fledged globally integrated trading networks.

Robust, Scalable Technology

We have developed proprietary technology that is highly secure, fault-tolerant and provides adequate capacity for our current operations, as well as for substantial growth. Our highly scalable systems are designed to accommodate additional volume, products and clients with relatively little modification and low incremental costs.

Proven Innovator with an Experienced Management Team

Since our inception, we have been an innovator in the fixed-income securities markets. The members of our management team average more than 20 years of experience in the securities industry. We have consistently sought to benefit participants in the markets we serve by attempting to replicate the essential features of fixed-income trading, including the existing relationships between broker-dealers and their institutional investor clients, while applying technology to eliminate weaknesses in traditional trading methods. In recent years, MarketAxess was awarded “OTC Trading Platform of the Year” by Global Capital, “SEF of the Year” by Risk Magazine, and “2015 Best Trading and Execution Technology” by Alt Credit Intelligence.

Some of the innovations we have introduced to electronic trading include:

|

|

· |

the first multi-dealer disclosed trading platform for U.S. high-grade corporate bonds; |

|

|

· |

the first electronic Treasury benchmarking for U.S. high-grade corporate bond trades; |

|

|

· |

BondTickerTM, our information services product, combining TRACE bond data with MarketAxess data and analytical tools; |

9

|

|

· |

bid and offer list technology for corporate bond trading, enabling institutional investors to request executable prices for multiple securities simultaneously; |

|

|

· |

the first disclosed client to multi-dealer trading platform for credit derivative indices; |

|

|

· |

public Market Lists for corporate bonds, giving institutional investors the ability to display their bid and offer lists anonymously to the entire MarketAxess trading community; and |

|

|

· |

Axess All™, the first intra-day trade tape for the European fixed income market. |

Independence

We believe the current regulatory environment creates competitive advantages for independent companies like us that are less prone to conflicts of interest. As an independent company, we are free to make business and trading protocol decisions with the best interests of both our institutional investor and broker-dealer clients in mind. We are also able to attract industry leaders with valuable skills and insights to our independent Board of Directors.

Our Strategy

Our objective is to provide the leading global electronic trading platform for fixed-income securities, connecting broker-dealers and institutional investors more easily and efficiently, while offering a broad array of information, trading and technology services to market participants across the trading cycle. The key elements of our strategy are:

Enhance the Liquidity of Securities Traded on Our Platform and Broaden Our Client Base in Our Existing Markets

We intend to further enhance the liquidity of securities traded on our leading electronic, multi-dealer to client fixed-income platform. Our ability to innovate and efficiently add new functionality and product offerings to the MarketAxess platform will help us deepen our market share with our existing clients, as well as expand our client base, which we believe will, in turn, lead to even further increases in the liquidity of the securities provided by our broker-dealer clients and available on our platform. We will seek to increase the amount of cross-regional activity by our institutional investor clients on our electronic trading platform, subject to regulatory requirements.

Leverage our Existing Client Network and Technology to Increase Counterparties and Improve Liquidity

Due to regulatory changes that have caused significant reductions in primary dealer corporate bond balance sheets, our broker-dealer and institutional investor clients need new and innovative electronic trading solutions to promote secondary market liquidity. We intend to continue to develop and deploy a wide range of electronic trading protocols to complement our traditional request-for-quote model. These Open Trading™ protocols increase potential trading counterparties by allowing broker-dealers and institutional investors to interact in an all-to-all trading environment. During 2015, we completed approximately 180,000 trades using our Open Trading™ solutions.

Leverage our Existing Technology and Client Relationships to Expand into New Sectors of the Fixed-Income Securities Market

We intend to leverage our technology, as well as our strong broker-dealer and institutional investor relationships, to deploy our electronic trading platform into additional product segments within the fixed-income securities markets and deliver fixed-income securities-related technical services and products. Due in part to our highly scalable systems, we believe we will be able to enter new markets efficiently.

Continue to Strengthen and Expand our Trade-Related Service Offerings

We plan to continue building our existing service offerings so that our electronic trading platform is more fully integrated into the workflow of our broker-dealer and institutional investor clients. We expect to continue to add functionality to enhance the ability of our clients to achieve a fully automated, end-to-end straight-through processing solution (automation from trade initiation to settlement). We also plan to expand and enhance the trade matching and regulatory transaction reporting services provided by Trax® in Europe to enable our clients to comply with their heightened obligations pursuant to MiFID II.

Expand our Data and Information Services Offerings

We regularly add new content and analytical capabilities to BondTicker™ in order to improve the value of the information we provide to our clients. We plan to expand the data service offering provided by Trax® in Europe, with additional content related to trading volume and pricing. For example, we recently launched Axess All™, the first intra-day trade tape for the European fixed income market. Axess All™ is sourced from over 30,000 bond transactions processed daily by Trax® through its post-trade services

10

and includes aggregated volume and pricing for the most actively traded European fixed income instruments. We intend to continue to widen the user base of our data products and to continue adding new content and analytical capabilities. As the use of our electronic trading platform continues to grow, we believe that the amount and value of our proprietary trading data will also increase, further enhancing the value of our information services offerings to our clients.

Pursue Select Acquisitions and Strategic Alliances

We plan to continue to increase and supplement our internal growth by entering into strategic alliances, or acquiring businesses or technologies, that will enable us to enter new markets, provide new products or services, or otherwise enhance the value of our platform to our clients.

The acquisition of Xtrakter Limited (“Xtrakter”) in February 2013 provided us with an expanded set of technology solutions ahead of incoming pre-and post-trade transparency mandates from MiFID II in Europe. In April 2013, we entered into a strategic alliance with BlackRock, Inc. (“Blackrock”) to create a unified, open trading solution designed to help reduce liquidity fragmentation and improve pricing across the U.S. cash credit markets. In January 2015, we expanded our strategic alliance with BlackRock to include the European cash credit markets.

MarketAxess Electronic Trading Platform

Key Trading Functionalities

The key trading functionalities are detailed below.

Single Inquiry Trading Functionality

We offer institutional investors the ability to request bids or offers in a single inquiry from an unlimited number of our broker-dealer clients in all of our key trading products. Our platform allows institutional investors to view bids and offers from one or more of our broker-dealer clients while permitting each party to know the identity of its counter-party throughout the trading process. This disclosed inquiry trading functionality combines the strength of existing offline client/dealer relationships with the efficiency and transparency of an electronic trading platform. Institutional investors can obtain bids or offers on any security posted in inventory or included in the database available on our platform.

ASAP and Holding Bin Trading Functionalities

We offer both ASAP (“as soon as possible”) and Holding Bin trading protocols. In the Holding Bin trading protocol, institutional investor clients set the time when they would like all of the broker-dealers’ prices or spreads returned to them, in order to have the ability to see all executable prices available at the same time. In the ASAP trading protocol, institutional investor clients see each broker-dealer’s price or spread as soon as it is entered by the broker-dealer.

List Trading Functionality

We offer institutional investors the ability to request bids or offers on a list of up to 40 bonds depending on the market. This facilitates efficient trading for institutional investors such as investment advisors, mutual funds and hedge funds. Institutional investors are able to have multiple lists executable throughout the trading day, enabling them to manage their daily cash flows, portfolio duration, and credit and sector exposure.

Market Lists

We offer institutional investors and broker-dealers the ability to display live requests for bids and offers anonymously to the entire MarketAxess trading community through our Market List functionality, thereby creating broader visibility of their inquiry among market participants and increasing the likelihood that the request results in a trade. Bond trades executed pursuant to this anonymous Open Trading™ protocol are conducted with MarketAxess on a matched principal basis.

Open Markets

Open Markets is an order book-style price discovery process that gives clients the ability to view anonymous indications of interest from both broker-dealer clients and institutional investor clients’ inventory on our platform. Through the aggregated indication of interest inventory, clients can search for bonds of interest and engage in electronic transactions on a bilateral basis or anonymously through MarketAxess on a matched principal basis. Each line item of inventory represents an indicative bid and/or offer on a particular bond issue by a particular client. To transact in a specific bond that does not appear in inventory, institutional investors can easily search our database and submit an online inquiry to their chosen broker-dealers (or to all Open Trading™ participants on our platform), who can respond with live, executable prices.

11

Click-to-Trade

Our click-to-trade functionality allows our investor clients to initiate an inquiry with a single click on stacks of distinctly displayed dealer bids and offers. In support of this functionality, pools of dealers stream attributable pricing for each instrument. Click-to-trade is offered alongside our existing RFQ product and allows pre-trade price discovery and fast-track execution. Although currently limited to credit derivatives, U.S. Treasuries and emerging markets, click-to-trade functionality may be applied to trading of other market sectors.

Session-based matching protocols

We have the ability to offer a session-based matching protocol for bonds that allows counterparties to trade at mid-market prices.

SEF Trading for Credit Derivatives

We offer a range of functionality for electronic trading of CFTC regulated credit derivatives on our SEF in compliance with the CFTC’s requirements. This includes an RFQ system that allows participants to send anonymous or disclosed RFQs, as well as an order book, which enables market participants to trade anonymously with all other market participants.

Central Limit Order Book

We have offered central limit order book (“CLOB”) style trading for bonds in the past. We currently provide a CLOB only for credit derivatives. While the characteristics of the corporate bond market have not been conducive to continuous trading (as in equity markets), we believe there is a sub-set of actively traded bonds that could benefit from CLOB trading.

Key Trading Products

U.S. High-Grade Corporate Bonds

Our U.S. high-grade corporate bond business consists of U.S. dollar-denominated investment-grade debt issued by corporations for distribution in the U.S. Both domestic and foreign institutional investors have access to U.S. high-grade corporate bond trading on our electronic trading platform. Our 2015 trading volume in the U.S. high-grade corporate bond market was $577.6 billion.

In the U.S. high-grade corporate bond market, 72 broker-dealers utilize our platform, including all of the top 20 broker-dealers as ranked by 2015 U.S. corporate bond new-issue underwriting volume. Our broker-dealer clients accounted for approximately 97% of the underwriting of newly-issued U.S. corporate bonds in 2015. More than 750 active institutional investor firms use our platform to trade U.S. high-grade corporate bonds.

Emerging Markets Bonds

Seventy-four of our broker-dealer clients and more than 650 active institutional investor firms use our platform to trade emerging markets bonds. These institutional investor clients are predominantly located in the U.S. and Europe. The emerging markets countries whose bonds were most frequently traded on our platform in 2015 were Mexico, Brazil, Russia, Turkey, South Africa, Columbia, China, and Indonesia. We also enable our institutional investor clients to transact local currency denominated bonds issued by sovereign entities or corporations in countries that include Argentina, Brazil and Mexico. Our 2015 trading volume in the emerging market bond market was $145.6 billion.

Crossover and High-Yield Bonds

Seventy-one of our broker-dealer clients and more than 700 active institutional investor firms use our platform to trade crossover and high-yield bonds. Trading in crossover and high-yield bonds uses many of the same features available in our U.S. high-grade corporate bond offering. Our 2015 trading volume in the high-yield bond market was $114.0 billion.

Eurobonds

We offer secondary trading functionality in U.S. dollar- and Euro-denominated European corporate bonds to our broker-dealer and institutional investor clients. We also offer our clients the ability to trade in other European high-grade corporate bonds, including bonds issued in Pounds Sterling, floating rate notes, European government bonds and bonds denominated in non-core currencies. We offered the first platform in Europe with a multi-dealer disclosed counterparty trading capability for corporate bonds. Our 2015 trading volume in the Eurobond bond market was $75.5 billion.

In the Eurobond credit market, defined as including European high-grade, high-yield and government bonds, 36 broker-dealers utilize our platform, including all of the top 20 broker-dealers as ranked by 2015 European corporate new-issue underwriting volume. More than 300 active institutional investor firms use our platform to trade European bonds.

12

U.S. Agency Bonds

Forty-three of our broker-dealer clients and approximately 300 active institutional investor firms use our platform to trade U.S. agency bonds. Trading in U.S. agency bonds uses many of the same features available in our U.S. high-grade corporate bond offering.

Credit Derivatives

MarketAxess offers a complete solution for the trading of clearable and non-clearable credit derivative instruments, including indices, single-name swaps and index options. Through our CFTC-registered SEF, we offer trading of credit derivative indices and credit options to approximately 150 market participants. We support the trading of single-name credit derivatives through our traditional RFQ protocol, as well as through a CLOB.

Information and Post-Trade Services

Information Services

BondTickerTM provides real-time TRACE data and enhances it with MarketAxess trade data and analytical tools in order to provide professional market participants with a comprehensive set of corporate bond price information. The data includes trade time and sales information, including execution prices, as well as MarketAxess-estimated spread-to-Treasuries, for trades disseminated by the TRACE system. The data also includes actual execution prices and spread-to-Treasury levels for U.S. high-grade corporate bond trades executed on the MarketAxess platform. BondTickerTM is currently the source of corporate bond trading information for The Wall Street Journal in the U.S.

BondTickerTM allows institutional investors to search for and sort bonds based upon specific criteria, such as volume, time/date of transaction, spread change, issuer or security. This search function allows institutional investors to compile information relating to potential securities trades in a fraction of the time that it takes to manually compile this information from disparate sources or other electronic databases, including direct TRACE feeds.

BondTickerTM also contains pricing information on a broad selection of European fixed-income securities. European pricing information is provided by Trax’s end-of-day pricing feed, XM2M.

BondTickerTM is integrated directly into the MarketAxess electronic trading platform and can be seamlessly accessed, either when viewing securities inventory or when launching an inquiry. BondTickerTM is also available through the Internet for non-trading professional market participants, including, among others, research analysts and rating agencies, who can log in and access the information via a browser-based interface.

We provide BondTickerTM as an ancillary service to our trading clients and also to other industry participants. We derive revenues from our BondTickerTM service by charging for seat licenses per user at our broker-dealer and institutional investor clients, through distribution agreements with other information service providers and through bulk data sales to third parties. Seat license fees are waived for clients that transact a sufficient volume of trades through MarketAxess.

We also offer a comprehensive set of reports designed to review and monitor credit trading activity for institutional investor clients. These reports utilize extensive TRACE information and have a flexible interface to run and save in a variety of formats for both compliance and management reporting. For example, the best execution report provides a view of the savings generated by trading on our electronic trading platform and offers a quantitative measure of the value of price discovery from multiple dealers. The report allows clients to monitor performance against their own best execution policy. Our compliance product provides a printed history of each inquiry submitted through the MarketAxess trading platform.

Through our Trax® brand, we provide a range of information solutions for financial services firms, utilizing quotes contributed by participants and leveraging our trade matching and regulatory transaction reporting services for European securities. We recently launched Axess All™, the first intra-day trade tape for the European fixed income market. Axess All™ is sourced from over 30,000 bond transactions processed daily by Trax® through its post-trade services and includes aggregated volume and pricing for the most actively traded European fixed income instruments.

Post-Trade Services

Our Trax® service provides post-trade, pre-settlement trade matching and regulatory transaction reporting services for the European OTC markets. Subscribers use the Trax® platform to match and report trades in a range of capital market instruments, including bonds, derivatives, equities and swaps. Trax® has approximately 100 clients, including broker-dealers, hedge funds and investment banks. The Trax® platform processed over 1.0 billion transactions in 2015.

13

Straight-Through Processing and APIs

Straight-through processing refers to the integration of systems and processes to automate the trade process from end-to-end — trade execution, confirmation and settlement — without the need for manual intervention. There are two elements of straight-through processing: internal straight-through processing and external straight-through processing. Internal straight-through processing relates to the trade and settlement processes that are internal to an industry participant. For example, in the case of an institutional investor, this includes authorization of orders, placement of orders with broker-dealers, receipt of execution details and allocation of trades. External straight-through processing refers to connecting seamlessly to all external counterparts in the trading and settlement process.

Automation by way of straight-through processing improves efficiency throughout the trade cycle. We provide broker-dealers and institutional investors with a range of tools that facilitate straight-through processing, including order upload, easy-to-use online allocation tools and pre- and post-trade messaging features that enable institutional investors to communicate electronically between front- and back-office systems, thereby integrating the order, portfolio management and accounting systems of our broker-dealer and institutional investor clients in real time. Our straight-through processing tools can be customized to meet specific needs of clients. We continue to build industry partnerships to assist our clients in creating connectivity throughout the trade cycle. Through these partnerships, we are increasingly providing solutions that can quickly be deployed within our clients’ trading operations.

Usage of our straight-through processing tools increased significantly during the last several years. The number of investor client STP connections increased to 518 as of December 31, 2015. In addition, many of our broker-dealer clients use our Application Programming Interfaces (“API”) services for pre-trade, trade negotiation and post-trade services to improve efficiency and reduce errors in processing.

Sales and Marketing

We promote our products and services using a variety of direct and indirect sales and marketing strategies. Our sales force is responsible for client acquisition activity and for increasing use of our trading platform and information and post-trade services by our existing clients. Their goal is to train and support existing and new clients on how to use our system and to educate them as to the benefits of utilizing an electronic fixed-income trading platform. We employ various strategies, including advertising, direct marketing, promotional mailings, and participation in industry conferences and media engagement, to increase awareness of our brand and our electronic trading platform. For example, we have worked with The Wall Street Journal to establish BondTickerTM as the source of information for its daily corporate bond and high-yield tables. A similar process also exists for our Trax® post-trade business, employing both direct and indirect sales methods.

Competition

The industry that we participate in is highly competitive and we expect competition to intensify in the future. We face four main areas of competition:

|

|

· |

Telephone and Direct Electronic Communications — We compete with bond trading business conducted over the telephone, e-mail or instant messaging between broker-dealers and their institutional investor clients. Institutional investors have historically purchased fixed-income securities by telephoning or otherwise communicating via e-mail or instant messaging with bond sales professionals at one or more broker-dealers and inquiring about the price and availability of individual bonds. This remains the manner in which the majority of corporate bonds are still traded between institutional investors and broker-dealers. |

|

|

· |

Other electronic trading platforms — There are numerous other electronic trading platforms currently in existence, including several that have only commenced, or announced an intention to launch, operations in the last twelve months. Among others, Bloomberg and TradeWeb operate- multi-dealer to institutional investor trading platforms for both fixed-income securities and derivatives. The New York Stock Exchange also offers exchange-style trading for corporate bonds. In addition, some broker-dealers and institutional investors operate proprietary electronic trading systems that enable institutional investors to trade directly with a broker-dealer, and/or with other institutional investors over an electronic medium. As we expand our business into new products, we will likely come into more direct competition with other electronic trading platforms or firms offering traditional services. |

|

|

· |

Market data and information vendors — Several large market data and information providers currently have a data and analytics relationship with virtually every institutional firm. Some of these entities, including Bloomberg, currently offer varying forms of electronic trading of fixed-income securities, mostly on a single-dealer basis. Some of these entities have announced their intention to expand their electronic trading platforms or to develop new platforms. These entities are currently direct competitors to our information services business and already are or may in the future become direct competitors to our electronic trading platform. |

14

|

|

· |

Other approved regulatory mechanisms — We compete with other approved regulatory mechanisms in Europe that have the FCA’s ARM designation and provide post-trade matching and regulatory transaction reporting services, including the London Stock Exchange’s UnaVista. |

Competitors, including companies in which some of our clients have invested, have developed electronic trading platforms or have announced their intention to explore the development of electronic trading platforms that compete or will compete with us. Furthermore, some of our clients have made, and may in the future continue to make, investments in or enter into agreements with other businesses that directly or indirectly compete with us.

In general, we compete on the basis of a number of key factors, including:

|

|

· |

broad network of broker-dealer and institutional investor clients using our electronic trading platform; |

|

|

· |

liquidity provided by the participating broker-dealers and, to a growing extent, by other institutional investors; |

|

|

· |

magnitude and frequency of price improvement; |

|

|

· |

enhancing the quality and speed of execution; |

|

|

· |

compliance benefits; |

|

|

· |

total transaction costs; |

|

|

· |

technology capabilities, including the reliability and ease of use of our electronic trading platform; and |

|

|

· |

range of products, protocols and services offered. |

We believe that our ability to grow volumes and revenues will largely depend on our performance with respect to these factors.

Our competitive position is also enhanced by the familiarity and integration of our broker-dealer and institutional investor clients with our electronic trading platform and other systems. We have focused on the unique aspects of the credit markets we serve in the development of our platform, working closely with our clients to provide a system that is suited to their needs.

Our broker-dealer clients have invested in building API’s with us for inventory contributions, electronic trading, government bond benchmark pricing and post-trade messaging. We believe that we have successfully built deep roots with our broker-dealer clients, increasing our level of service to them while at the same time increasing their commitment to our services.

Furthermore, a significant number of our institutional investor firms have built interfaces to enable them to communicate electronically between our platform and their order, portfolio management and accounting systems. We believe that this increases the reliance of these institutional investor firms on our services and creates significant competitive barriers to entry.

Technology

The design and quality of our technology products are critical to our growth and our ability to execute our business strategy. Our electronic trading platform has been designed with secure, scalable client-server architecture that makes broad use of distributed computing to achieve speed, reliability and fault tolerance. The platform is built on industry-standard technologies and has been designed to handle many multiples of our current trading volume.

All critical server-side components, primarily our networks, application servers and databases, have backup equipment running in the event that the main equipment fails. This offers fully redundant system capacity to maximize uptime and minimize the potential for loss of transaction data in the event of an internal failure. We also seek to minimize the impact of external failures by automatically recovering connections in the event of a communications failure. The majority of our broker-dealer clients have redundant dedicated high-speed communication paths to our network in order to provide fast data transfer. Our security measures include industry-standard communications encryption.

We have designed our application with an easy-to-use, Windows-based interface. Our clients are able to access our electronic trading platform through a secure, single sign-on. Clients are also able to execute transactions over our platform directly from their order management systems. We provide users an automatic software update feature that does not require manual intervention.

Intellectual Property

We rely upon a combination of copyright, patent, trade secret and trademark laws, written agreements and common law to protect our proprietary technology, processes and other intellectual property. Our software code, elements of our electronic trading

15

platform, website and other proprietary materials are protected by copyright laws. We have been issued 13 patents covering our most significant trading protocols and other aspects of our trading system technology.

The written agreements upon which we rely to protect our proprietary technology, processes and intellectual property include agreements designed to protect our trade secrets. Examples of these written agreements include third party nondisclosure agreements, employee nondisclosure and inventions assignment agreements, and agreements with customers, contractors and strategic partners. Other written agreements upon which we rely to protect our proprietary technology, processes and intellectual property take many forms and contain provisions related to patent, copyright, trademark and trade secret rights.

We have obtained U.S. federal registration of the MarketAxess® name and logo, and the same mark and logo have been registered in several foreign jurisdictions. In addition, we have obtained U.S. federal registration for the marks AutoSpotting®, FrontPage®, Actives®, DealerAxess®, Trax®, Trade ON®, LiquidityBridge®, Axess 50® and associated designs and have a number of other registered trademarks and service marks. BondTickerTM, Open TradingTM, Axess AllTM, and MarketAxess Bid-Ask Spread Index (BASI) TM are trademarks we use, but they have not been registered.

In addition to our efforts to register our intellectual property, we believe that factors such as the technological and creative skills of our personnel, new product and service developments, frequent enhancements and reliability with respect to our services are essential to establishing and maintaining a technology and market leadership position.

Government Regulation

The securities industry and financial markets in the U.S. and elsewhere are subject to extensive regulation. As a matter of public policy, regulatory bodies in the U.S. and the rest of the world are charged with safeguarding the integrity of the securities and other financial markets and with protecting the interests of investors participating in those markets. Our active broker-dealer subsidiaries fall within the scope of their regulations.

Regulation of the U.S. Securities Industry and Broker-Dealers

In the U.S., the SEC is the governmental agency responsible for the administration of the federal securities laws. One of our U.S. subsidiaries, MarketAxess Corporation, is registered with the SEC as a broker-dealer and an alternative trading system operator. It is also a member of FINRA, a self-regulatory organization to which most broker-dealers belong. In addition, MarketAxess Corporation is a member of the Securities Investor Protection Corporation, which provides certain protection for clients’ accounts in the event of a liquidation of a broker-dealer to the extent any such accounts are held by the broker-dealer.

Additionally, MarketAxess Corporation is registered with certain states and the District of Columbia as a broker-dealer. The individual states and the District of Columbia are responsible for the administration of their respective “blue sky” laws, rules and regulations.

MarketAxess SEF Corporation, our wholly-owned U.S. subsidiary, operates as a SEF for the trading of certain credit derivatives subject to the CFTC’s jurisdiction, including certain index swaps subject to the CFTC’s ‘made available for trade’ determination that are required to be executed on a SEF or regulated exchange. The SEC has not yet finalized its rules for security-based SEFs, nor has it published a timetable for the finalization and implementation of such rules. No assurance can be given regarding when, whether or in what form the remaining rules regarding the new regulatory regime for the swaps marketplace will be finalized or implemented.

Various rules promulgated since the financial crisis could adversely affect our bank-affiliated broker-dealer clients’ ability to make markets in a variety of fixed-income securities, thereby negatively impacting the level of liquidity and pricing available on our trading platform. For example, while the recently adopted Volcker Rule does not apply directly to us, the Volcker Rule bans proprietary trading by banks and their affiliates. In addition, enhanced leverage ratios applicable to large banking organizations in the U.S. and Europe require such organizations to strengthen their balance sheets and may limit their ability or willingness to make markets on our trading platform. We cannot predict the extent to which these rules or any future regulatory changes may adversely affect our business and operations.

Regulation of the Non-U.S. Securities Industries and Investment Service Providers

The securities industry and financial markets in the U.K., the EU and elsewhere are subject to extensive regulation. Our principal regulator in the U.K. is the FCA. MarketAxess Europe Limited is registered as a Multilateral Trading Facility (“MTF”) with the FCA and is also a registered platform in Switzerland, Hong Kong and Singapore. Xtrakter is registered as an Approved Reporting Mechanism with the FCA and also has “recognized status” in France, the Netherlands and Belgium in connection with the submission of transaction reports to regulators.

16

The securities industry in the member states of the EU is regulated by agencies in each member state. EU measures provide for the mutual recognition of regulatory agencies and of prudential supervision making possible the grant of a single authorization for providers of investment services, which, in general, is valid throughout the EU. As an FCA approved MTF, MarketAxess Europe Limited receives the benefit of this authorization.

Similar to the U.S., regulatory bodies in Europe are developing new rules for the fixed-income markets. MiFID II and Markets in Financial Instruments Regulation (“MiFIR”) were approved in June 2014 and introduce changes in market structure designed to: (i) enhance pre- and post-trade transparency for fixed income instruments with the scope of requirements calibrated for liquidity, (ii) increase and enhance post-trade reporting obligations with a requirement to submit post-trade data to ARMs, (iii) ensure trading of certain derivatives occurs on regulated trading venues and (iv) establish a consolidated tape for trade data. While some of the rules and technical advice underpinning MiFID II have not yet been finalized, MiFID II will have a significant impact in these areas, as well as on corporate governance and investor protection. MiFID II and MiFIR are expected to take effect in January 2018. The final rules may have an adverse effect on our operations or our ability to provide our electronic trading platform in a manner that can successfully compete against other types of regulated and non-regulated venues for the fixed-income trading needs of our clients. In addition, MiFID II is expected to cause us to expend more significant compliance, business and technology resources, incur additional operational costs and create additional regulatory exposure for our trading and post-trade businesses. While we generally believe the net impact of the rules and regulations will be positive for our businesses, unintended consequences of the rules and regulations may adversely affect us in ways yet to be determined.