Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-35462

Vantiv, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 26-4532998 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

8500 Governor’s Hill Drive

Symmes Township, OH 45249

(Address of principal executive offices)

Registrant's telephone number, including area code: (513) 900-5250

Securities registered pursuant to 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Class A Common Stock, $0.00001 par value | New York Stock Exchange | |

Securities registered pursuant to 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer o | |

Non-accelerated filer o | Smaller reporting company o | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

As of June 30, 2015 (the last business day of the registrant's most recently completed second fiscal quarter), the aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant was $5.5 billion.

As of December 31, 2015, there were 155,488,326 shares of the registrant’s Class A common stock outstanding and 35,042,826 shares of the registrant’s Class B common stock outstanding.

Documents Incorporated by Reference: |

Portions of the registrant's definitive Proxy Statement for the 2016 Annual Meeting of Stockholders are incorporated by reference in Part III of this Annual Report on Form 10-K as indicated. Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant's fiscal year ended December 31, 2015.

VANTIV, INC.

FORM 10-K

For the Fiscal Year Ended December 31, 2015

TABLE OF CONTENTS

Page | |

2

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, including the sections entitled "Management’s Discussion and Analysis of Financial Condition and Results of Operations" and "Risk Factors," contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. All statements other than statements of historical fact, including statements regarding our future results of operations and financial position, our business strategy and plans, our objectives for future operations, and any statements of a general economic or industry specific nature, are forward-looking statements. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. Words such as "anticipate," "estimate," "expect," "project," "plan," "intend," "believe," "may," "will," "continue," "could," "should," "can have," "likely," or the negative or plural of these words and similar expressions are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe, based on information currently available to our management, may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in the "Risk Factors" section of this report. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the future events and trends discussed in this report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

You should not rely upon forward-looking statements as predictions of future events. The events and circumstances reflected in the forward-looking statements may not be achieved or occur. Although we believe that the expectations and assumptions reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. We undertake no obligation to publicly update any forward-looking statement after the date of this report, whether as a result of new information, future developments or otherwise, or to conform these statements to actual results or revised expectations, except as may be required by law.

3

PART I

Item 1. Business

Vantiv, Inc., a Delaware corporation, is a holding company that conducts its operations through its majority-owned subsidiary, Vantiv Holding, LLC ("Vantiv Holding"). Vantiv, Inc., Vantiv Holding and their subsidiaries are referred to collectively as the "Company," "Vantiv," "we," "us" or "our," unless the context requires otherwise.

Business and Client Description

Vantiv is a leading payment processor differentiated by an integrated technology platform, breadth of distribution and superior cost structure. According to the Nilson Report, we are the second largest merchant acquirer and the largest PIN debit acquirer by number of transactions in the United States. Our integrated technology platform is differentiated from our competitors' multiple platform architectures. It enables us to efficiently provide a comprehensive suite of services to merchants and financial institutions of all sizes as well as to innovate, develop and deploy new services, while providing us with significant economies of scale. Our broad and varied distribution includes multiple sales channels, such as our direct and indirect sales forces and referral partner relationships, which provide us with a growing and diverse client base of merchants and financial institutions. We believe this combination of attributes provides us with competitive advantages that generate strong growth and profitability by enabling us to efficiently manage, update and maintain our technology, to utilize technology integration and value-added services to expand our new sales and distribution, and to realize significant operating leverage.

We offer a broad suite of payment processing services that enable our clients to meet their payment processing needs through a single provider, including in omni-channel environments that span point-of-sale, ecommerce and mobile devices. We enable merchants of all sizes to accept and process credit, debit and prepaid payments and provide them supporting value-added services, such as security solutions and fraud management, information solutions, and interchange management. We also provide mission critical payment services to financial institutions, such as card issuer processing, payment network processing, fraud protection, card production, prepaid program management, ATM driving and network gateway and switching services that utilize our proprietary Jeanie PIN debit payment network.

Merchant Services

We have a broad and diversified merchant client base. Our merchant client base includes approximately 800,000 merchant locations across the United States. In 2015, we processed approximately 19.0 billion transactions for these merchants. Our merchant client base has low client concentration and is heavily weighted in non-discretionary everyday spend categories, such as grocery and pharmacy, and includes large national retailers, including ten of the top 25 national retailers by revenue in 2014. We provide a comprehensive suite of payment processing services to our merchant services clients. We authorize, clear, settle and provide reporting for electronic payment transactions, as further discussed below.

Acquiring and Processing. We provide merchants with a broad range of credit, debit and prepaid payment processing services. We give them the ability to accept and process Visa, MasterCard, American Express, Discover and PIN debit network card transactions originated at the point of sale as well as for ecommerce and mobile transactions. This service includes all aspects of card processing, including authorization and settlement, customer service, chargeback and retrieval processing and network fee and interchange management.

Value-added Services. We offer value-added services that help our clients operate and manage their businesses including omni-channel acceptance, prepaid services and gift card solutions. We also provide security solutions such as point-to-point encryption and tokenization both at the point of sale and for ecommerce transactions.

Financial Institution Services

Our financial institution client base is also generally well diversified and includes approximately 1,400 financial institutions, including regional banks, community banks, credit unions and regional PIN debit networks. In 2015, we processed approximately 4.0 billion transactions for these financial institutions. We generally focus on small to mid-sized institutions with less than $15 billion in assets. Smaller financial institutions generally do not have the scale or infrastructure typical of large institutions and are more likely to outsource their payment processing needs. We provide integrated card issuer processing, payment network processing and value-added services to our financial institutions clients. These services are discussed further below.

4

Integrated Card Issuer and Processing. We process and service credit, debit, ATM and prepaid transactions. We process and provide statement production, collections and inbound/outbound call centers. Our card processing solution includes processing and other services such as card portfolio analytics, program strategy and support, fraud and security management and chargeback and dispute services. We also offer processing for specialized accounts, such as business cards, home equity lines of credit and health savings accounts. We provide authorization support in the form of online or batch settlement, as well as real-time transaction research capability and archiving and daily and monthly cardholder reports for statistical analysis.

Value-added Services. We provide additional services to our financial institution clients that complement our issuing and processing services. These services include fraud protection, card production, prepaid cards, ATM driving, portfolio optimization, data analytics and card program marketing. We also provide network gateway and switching services that utilize our Jeanie PIN network. Our Jeanie network offers real-time electronic payment, network bill payment, single point settlement, shared deposit taking and customer select PINs. Our Jeanie network includes approximately 7,600 ATMs, 26 million cardholders and 710 member financial institution clients.

Integrated Technology Platform

Our integrated technology platform provides our merchant and financial institution clients with differentiated payment processing solutions and provides us with significant strategic and operational benefits. Our clients access our processing solutions primarily through a single point of service, which is easy to use and enables our clients to acquire additional services as their business needs evolve. Small and mid-sized merchants are able to easily connect to our integrated technology platform using our application process interfaces, or APIs, software development kits, or SDKs, and other tools we make available to technology partners, which we believe enhances our capacity to sell to such merchants. Our integrated technology platform allows us to collect, manage and analyze data across both our Merchant Services and our Financial Institution Services segments that we can then package into information solutions for our clients. It provides insight into market trends and opportunities as they emerge, which enhances our ability to innovate and develop new value-added services, including security solutions and fraud management, and it allows us to easily deploy new solutions that span the payment processing value chain, such as ecommerce and mobile services, which are high growth market opportunities. It is highly scalable, which enables us to efficiently manage, update and maintain our technology, increase capacity and speed, and realize significant operating leverage. We believe our integrated technology platform is a key differentiator from payment processors that operate on multiple technology platforms and provides us with a significant competitive advantage.

Sales and Marketing

Our integrated technology platform enables us to provide a comprehensive suite of services to merchants and financial institutions of all sizes. We distribute our services through multiple sales channels that enable us to efficiently and effectively target a growing and diverse client base of merchants and financial institutions. Our sales channels include direct and indirect sales forces as well as referral partner relationships within our Merchant Services and Financial Institution Services segments as described below.

Merchant Services. We distribute our comprehensive suite of services to a broad range of merchants, including difficult to reach small and mid-sized merchants, through multiple sales channels as further discussed below.

• | Direct: Includes a national sales force that targets large national merchants, a regional and mid-market sales team that sells solutions to merchants and third party reseller clients, and a telesales operation that targets small and mid-sized merchants. |

• | Indirect: Includes Independent Sales Organizations (ISOs) that target small and mid-sized merchants. |

• | Merchant Bank: Includes referral partner relationships with financial institutions that target their financial services customers as merchant referrals to us. |

• | Integrated Payments (IP): Includes referral partner relationships with independent software vendors (ISVs), value-added resellers (VARs), and payment facilitators that target their technology customers as merchant referrals to us. |

• | eCommerce: Includes a sales force that targets internet retail, online services and direct marketing merchants. |

These sales channels utilize multiple strategies and leverage relationships with referral partners that sell our solutions to small and mid-sized merchants. We offer certain of our services on a white-label basis which enables them to be marketed under our partners' brand. We select referral partners that enhance our distribution and augment our services with complimentary offerings. We believe our sales structure provides us with broad geographic coverage and access to various industries and verticals.

5

Financial Institution Services. We distribute our services by utilizing direct sales forces as well as a diverse group of referral partner relationships. These sales channels utilize multiple strategies and leverage relationships with core processors that sell our solutions to small and mid-sized financial institutions. We offer certain of our services on a white-label basis which enables them to be marketed under our client's brand. We select resellers that enhance our distribution and augment our services with complementary offerings. Our relationships with core processors are necessary for developing the processing environments required by our financial institution clients. Many of our core processing relationships are non-contractual and continue for so long as an interface between us and the core processor is needed to accommodate one or more common financial institution customers.

Our sales teams in both Merchant Services and Financial Institution Services are paid a combination of base salary and commission. As of December 31, 2015, we had approximately 1,000 full-time employees participating in sales and marketing, including sales support personnel. Commissions paid to our sales force are based upon a percentage of revenue from new business and cross-selling to existing clients. Residual payments to our referral partners are based upon a percentage of revenues earned from referred business. For the year ended December 31, 2015, combined sales force commissions and residual payments represent approximately 75% of total sales and marketing expenses, or $376.6 million.

Our History

We have a 40 year history of providing payment processing services. We operated as a business unit of Fifth Third Bank ("Fifth Third") until June 2009 when we separated as a stand-alone company, established our own organization, headquarters, brand, growth strategy and completed our initial public offering ("IPO") in March 2012. Since the separation, we have made substantial investments, including several key acquisitions, to enhance our integrated technology platform and reorganize our business to better align it with our market opportunities and broaden our geographic footprint beyond the markets traditionally served by Fifth Third Bank.

Industry Background

Electronic Payments

Electronic payments in the United States have evolved into a large and growing market with favorable secular trends that continue to increase the adoption and use of card-based payment services, such as those for credit, debit and prepaid cards.

This growth is driven by the shift from cash and checks towards card-based and other electronic forms of payment due to their greater convenience, security, enhanced services and rewards and loyalty features. We believe changing demographics and emerging trends, such as the adoption of new technologies and business models, including ecommerce, mobile commerce and prepaid services, will also continue to drive growth in electronic payments.

Payment Processing Industry

The payment processing industry is comprised of various processors that create and manage the technology infrastructure that enables electronic payments. Payment processors help merchants and financial institutions develop and offer electronic payment solutions to their customers, facilitate the routing and processing of electronic payment transactions and manage a range of supporting security, value-added and back office services. In addition, many large banks manage and process their card accounts in-house. This is collectively referred to as the payment processing value chain.

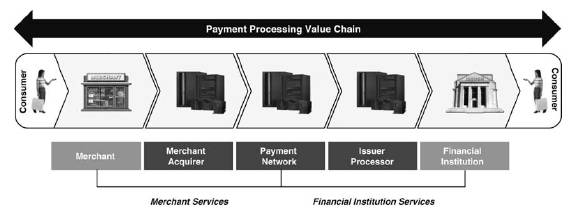

Many payment processors specialize in providing services in discrete areas of the payment processing value chain, which can result in merchants and financial institutions using payment processing services from multiple providers. A limited number of payment processors have capabilities or offer services in multiple parts of the payment processing value chain. We provide solutions across the payment processing value chain as a merchant acquirer, payment network, and as an issuer processor, primarily by utilizing our integrated technology platform to enable our clients to easily access a broad range of payment processing services as illustrated below:

6

The payment processing value chain encompasses three key types of processing:

• | Merchant Acquiring Processing. Merchant acquiring processors sell electronic payment acceptance, processing and supporting services to merchants and third-party resellers. These processors route transactions originated by consumer transactions with the merchant, including in omni-channel environments that span point-of-sale, ecommerce and mobile devices, to the appropriate payment networks for authorization, known as "front-end" processing, and then ensure that each transaction is appropriately cleared and settled into the merchant's bank account, known as "back-end" processing. Many of these processors also provide specialized reporting, back office support, risk management and other value-added services to merchants. Merchant acquirers charge merchants based on a percentage of the value of each transaction on a per transaction basis. Merchant acquirers pay the payment network processors a routing fee per transaction and pass through interchange fees to the issuing financial institution. |

• | Payment Network Processing. Payment network processors, such as Visa, MasterCard and PIN debit payment networks, sell electronic payment network routing and support services to financial institutions that issue cards and merchant acquirers that provide transaction processing. Depending on their market position and network capabilities, these providers route credit, debit and prepaid card transactions from merchant acquiring processors to the financial institution that issued the card, and they ensure that the financial institution's authorization approvals are routed back to the merchant acquiring processor and that transactions are appropriately settled between the merchant's bank and the card-issuing financial institution. These providers also provide specialized risk management and other value-added services to financial institutions. Payment networks charge merchant acquiring processors and issuing financial institutions routing fees per transaction and monthly or annual maintenance fees and assessments. |

• | Issuer Card Processing. Issuer card processors sell electronic payment issuing, processing and supporting services to financial institutions. These providers authorize transactions received from the payment networks and ensure that each transaction is appropriately cleared and settled from the originating card account. These companies also provide specialized program management, reporting, outsourced customer service, back office support, risk management and other value-added services to financial institutions. Card processors charge issuing financial institutions fees based on the number of transactions processed and the number of cards that are managed. |

7

Emerging Trends and Opportunities in the Payment Processing Industry

The payment processing industry will continue to adopt new technologies, develop new products and services, evolve new business models and experience new market entrants and changes in the regulatory environment. In the near-term, as merchants and financial institutions seek services that help them enhance their own offerings to consumers, including acceptance and issuance of Europay-MasterCard-Visa (EMV) chip-based cards, other security and fraud management services, information services, and support for omni-commerce environments, we believe that payment processors may seek to develop additional capabilities and expand across the payment processing value chain to meet these demands and capture additional data and provide additional value per transaction. To facilitate this expansion and deliver more robust service offerings, we believe that payment processors will need to develop greater control over and integration of their technology platforms, to enable them to deliver and differentiate their offerings from other providers.

We believe that emerging, alternative electronic payment technologies will be adopted by merchants and other businesses. As a result, non-financial institution enterprises, such as mobile payment providers, internet, retail and social media companies, could become more active participants in the development of these alternative electronic payment technologies and facilitate the convergence of retail, online, mobile and social commerce applications, representing an attractive growth opportunity for the industry. We believe that payment processors that have an integrated business, provide solutions across the payment processing value chain and utilize broad distribution capabilities will be best positioned to provide processing services for emerging alternative electronic payment technologies and to successfully partner with new market entrants.

Competition

Merchant Services

Our competitors include financial institutions and well-established payment processing companies, including Bank of America Merchant Services, Chase Paymentech Solutions, Elavon Inc. (a subsidiary of U.S. Bancorp), First Data Corporation, Global Payments, Inc., Heartland Payment Systems, Inc., Total System Services, Inc. and WorldPay US, Inc. in our Merchant Services segment. Furthermore, we are facing new competitive pressure from non-traditional payments processors and other parties entering the payments industry, such as PayPal, Google, Apple, Alibaba and Amazon, who may compete in one or more of the functions performed in processing merchant transactions. The most significant competitive factors in this segment are price, breadth of features and functionality, data security, system performance and reliability, scalability, service capability and brand.

Financial Institution Services

In our Financial Institution Services segment, competitors include Fidelity National Information Services, Inc., First Data Corporation, Fiserv, Inc., Total System Services, Inc. and Visa Debit Processing Service. In addition to competition with direct competitors, we also compete with the capabilities of many larger potential clients to conduct their key payment processing applications in-house. The most significant competitive factors in this segment are price, system performance and reliability, breadth of services and functionality, data security, scalability, flexibility of infrastructure and servicing capability.

Our Strategy

We plan to grow our business over the course of the next few years, depending on market conditions, by continuing to execute on the following four key strategies:

• | Invest in and leverage our integrated business model and technology platform to strengthen and protect our core business; |

• | Broaden and deepen our distribution channels to grow our merchant and financial institutions client base; |

• | Differentiate through value-added services that address evolving client demands and provide additional cross-selling opportunities, including security and fraud management, information services, ease of connection and delivery, and support for omni-channel environments; and |

• | Enter new geographic markets through strategic partnerships or acquisitions that enhance our distribution channels, client base, and service capabilities. |

8

Financial Highlights

Revenue for the year ended December 31, 2015, increased 23% to $3,159.9 million from $2,577.2 million in 2014. Income from operations for the year ended December 31, 2015, increased 38% to $434.4 million from $314.7 million in 2014. Net income for the year ended December 31, 2015, increased 24% to $209.2 million from $169.0 million in 2014. Net income attributable to Vantiv, Inc. for the year ended December 31, 2015, increased 18% to $147.9 million from $125.3 million in 2014.

The following tables provide a summary of the results for our two segments, Merchant Services and Financial Institution Services, for the years ended December 31, 2015, 2014 and 2013.

Year Ended December 31, | |||||||||||

2015 | 2014 | 2013 | |||||||||

(dollars in thousands) | |||||||||||

Merchant Services | |||||||||||

Total revenue | $ | 2,656,906 | $ | 2,100,367 | $ | 1,639,157 | |||||

Network fees and other costs | 1,321,312 | 1,033,801 | 801,463 | ||||||||

Net revenue | 1,335,594 | 1,066,566 | 837,694 | ||||||||

Sales and marketing | 478,736 | 367,998 | 286,200 | ||||||||

Segment profit | $ | 856,858 | $ | 698,568 | $ | 551,494 | |||||

Non-financial data: | |||||||||||

Transactions (in millions) | 18,959 | 16,262 | 13,333 | ||||||||

Year Ended December 31, | |||||||||||

2015 | 2014 | 2013 | |||||||||

(dollars in thousands) | |||||||||||

Financial Institution Services | |||||||||||

Total revenue | $ | 503,032 | $ | 476,836 | $ | 468,920 | |||||

Network fees and other costs | 156,890 | 140,864 | 133,978 | ||||||||

Net revenue | 346,142 | 335,972 | 334,942 | ||||||||

Sales and marketing | 25,213 | 28,355 | 25,844 | ||||||||

Segment profit | $ | 320,929 | $ | 307,617 | $ | 309,098 | |||||

Non-financial data: | |||||||||||

Transactions (in millions) | 4,032 | 3,815 | 3,613 | ||||||||

Refer to "Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations" for more details.

Regulation

Various aspects of our business are subject to U.S. federal, state and local regulation. Failure to comply with regulations may result in the suspension or revocation of licenses or registrations, the limitation, suspension or termination of services and/or the imposition of civil and criminal penalties, including fines. Certain of our services are also subject to rules set by various payment networks, such as Visa and MasterCard. Many of these regulations and rules are more fully described below.

Dodd-Frank Act

In July 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 was signed into law in the United States. The Dodd-Frank Act has resulted in significant structural and other changes to the regulation of the financial services industry. Among other things, the Dodd-Frank Act established the Consumer Financial Protection Bureau, or CFPB, to regulate consumer financial services, including many offered by our clients.

The Dodd-Frank Act provided two immediately effective, self-executing statutory provisions limiting the ability of payment card networks to impose certain restrictions. The first provision allows merchants to set minimum dollar amounts (not

9

to exceed $10) for the acceptance of a credit card (and allows federal governmental entities and institutions of higher education to set maximum amounts for the acceptance of credit cards). The second provision allows merchants to provide discounts or incentives to entice consumers to pay with cash, checks, debit cards or credit cards, as the merchant prefers.

Separately, the "Durbin Amendment" to the Dodd-Frank Act provided that interchange fees that a card issuer or payment network receives or charges for debit transactions will now be regulated by the Federal Reserve and must be "reasonable and proportional" to the cost incurred by the card issuer in authorizing, clearing and settling the transaction. In addition, the Durbin Amendment contains prohibitions on network exclusivity and merchant routing restrictions.

Banking Regulation

Fifth Third Bank beneficially owns an equity interest representing approximately 18.4% of Vantiv Holding's voting power and equity interests (through their ownership of Vantiv Holding Class B units) and 18.4% of the voting interest in Vantiv, Inc. (through their ownership of our Class B common stock). Fifth Third Bank is an Ohio state-chartered bank and a member of the Federal Reserve System and is supervised and regulated by the Federal Reserve and the Ohio Division of Financial Institutions, or ODFI. Fifth Third Bank is a wholly-owned indirect subsidiary of Fifth Third Bancorp, which is a bank holding company, or BHC, which has elected to be treated as a financial holding company, or FHC, and is supervised and regulated by the Federal Reserve under the Bank Holding Company Act of 1956, as amended, or BHC Act.

We continue to be deemed to be controlled by Fifth Third Bancorp and Fifth Third Bank for bank regulatory purposes and, therefore, remain subject to supervision and regulation by the Federal Reserve under the BHC Act and by the ODFI under applicable federal and state banking laws until Fifth Third Bancorp and Fifth Third Bank are no longer deemed to control us for bank regulatory purposes, which we do not generally have the ability to control and which will generally not occur until Fifth Third Bank has significantly reduced its equity interest in us, as well as certain other factors, including the extent to which we continue to maintain material business relationships with Fifth Third Bancorp and Fifth Third Bank. The ownership level at which the Federal Reserve would consider us no longer controlled by Fifth Third Bank for bank regulatory purposes will generally depend on the circumstances at that time and could be less than 5%. The circumstances and other factors that the Federal Reserve will consider will include, among other things, the extent of our relationships with Fifth Third Bank, including the various agreements entered into at the time of the separation from Fifth Third Bank and the Amended and Restated Vantiv Holding Limited Liability Company Agreement.

Because of the foregoing, in certain circumstances, prior approval of the Federal Reserve or the ODFI may be required before Fifth Third Bancorp, Fifth Third Bank or their subsidiaries for bank regulatory purposes, including us, can engage in permissible activities. The Federal Reserve has broad powers to approve, deny or refuse to act upon applications or notices for us to conduct new activities, acquire or divest businesses or assets, or reconfigure existing operations. Additionally, it may be difficult for us to engage in activities abroad or invest in a non-U.S. company. We and Fifth Third Bank may seek to engage in offshore activities through various entities and structures, each of which may require prior regulatory approval, the receipt of which cannot be assured, as well as continued banking regulation and limitations. The Federal Reserve and the ODFI have substantial discretion in this regard. We will need Fifth Third Bank's cooperation to form and operate any such entity for offshore activities, and the regulatory burdens imposed upon Fifth Third Bank may be too extensive to justify its establishment or continuation. If, after such an entity is formed, we or Fifth Third Bank are at any time unable to comply with any applicable regulatory requirements, the Federal Reserve or ODFI may impose additional limitations or restrictions on Fifth Third Bank's or our operations, which could potentially force us to limit the activities or dispose of the entity.

For as long as we are deemed to be controlled by Fifth Third Bancorp and Fifth Third Bank for bank regulatory purposes, we are subject to regulation, supervision, examination and potential enforcement action by the Federal Reserve and the ODFI and to certain banking laws, regulations and orders. Fifth Third Bancorp and Fifth Third Bank are required to file reports with the Federal Reserve and the ODFI on our behalf, and we are subject to examination by the Federal Reserve and the ODFI for the purposes of determining, among other things, our financial condition, the adequacy of our risk management and the financial and operational risks that we pose to the safety and soundness of Fifth Third Bank and Fifth Third Bancorp, and our compliance with federal and state banking laws applicable to us and our relationship and transactions with Fifth Third Bancorp and Fifth Third Bank. The Federal Reserve has broad authority to take enforcement actions against us if it determines that we are engaged in or are about to engage in unsafe or unsound banking practices or are violating or are about to violate a law, rule or regulation, or a condition imposed by or an agreement with, the Federal Reserve, and any enforcement actions taken against Fifth Third Bancorp or Fifth Third Bank may result in regulatory actions being applied to us or our activities in certain circumstances, even if the enforcement actions are unrelated to our conduct or business. For the most serious violations under federal banking laws, the Federal Reserve may impose civil money penalties and criminal penalties.

10

As a condition to Fifth Third Bank's investment in us, we are required under the Amended and Restated Vantiv Holding Limited Liability Company Agreement to limit our activities to those activities permissible for a national bank. Accordingly, under the Amended and Restated Vantiv Holding Limited Liability Company Agreement: (i) we are required to notify Fifth Third Bank before we engage in any activity, by acquisition, investment, organic growth or otherwise, that may reasonably require Fifth Third Bank or an affiliate of Fifth Third Bank to obtain regulatory approval, so that Fifth Third Bank can determine whether the new activity is permissible, permissible subject to regulatory approval or impermissible; and (ii) if a change in the scope of our business activities causes the ownership of our equity not to be legally permissible for Fifth Third Bank without first obtaining regulatory approvals, then we must use reasonable best efforts to assist Fifth Third Bank in obtaining the regulatory approvals, and if the change in the scope of our business activities is impermissible for Fifth Third Bank, then we will not engage in such activity.

We are subject to regulation and enforcement by the CFPB, created by the Dodd-Frank Act, because we are an affiliate of Fifth Third Bank for bank regulatory purposes and because we are a service provider to insured depository institutions with assets of $10 billion or more in connection with their consumer financial products and to entities that are larger participants in markets for consumer financial products and services such as prepaid cards. CFPB rules, examinations and enforcement actions may require us to adjust our activities and may increase our compliance costs. In addition to rulemaking authority over several enumerated federal consumer financial protection laws, the CFPB is authorized to issue rules prohibiting unfair, deceptive or abusive acts or practices by persons offering consumer financial products or services and those, such as us, who are service providers to such persons, and has authority to enforce these consumer financial protection laws and CFPB rules.

Collection Services State Licensing

Ancillary to our credit card processing business, we are subject to the Fair Debt Collection Practices Act and various similar state laws. We are authorized in 19 states to engage in debt administration and debt collection activities on behalf of some of our card issuing financial institution clients through calls and letters to the debtors in those states. We may seek licenses in other states to engage in similar activities in the future.

Association and Network Rules

While not legal or governmental regulation, we are subject to the network rules of Visa, MasterCard and other payment networks. The payment networks routinely update and modify their requirements. On occasion, we have received notices of non-compliance and fines, which have typically related to excessive chargebacks by a merchant or data security failures. Our failure to comply with the networks' requirements or to pay the fines they impose could cause the termination of our registration and require us to stop providing payment processing services.

Privacy and Information Security Regulations

We provide services that may be subject to privacy laws and regulations of a variety of jurisdictions. Relevant federal privacy laws include the Gramm-Leach-Bliley Act of 1999, which applies directly to a broad range of financial institutions and indirectly, or in some instances directly, to companies that provide services to financial institutions. These laws and regulations restrict the collection, processing, storage, use and disclosure of personal information, require notice to individuals of privacy practices and provide individuals with certain rights to prevent the use and disclosure of protected information. These laws also impose requirements for safeguarding and proper destruction of personal information through the issuance of data security standards or guidelines. In addition, there are state laws restricting the ability to collect and utilize certain types of information such as Social Security and driver's license numbers. Certain state laws impose similar privacy obligations as well as obligations to provide notification of security breaches of computer databases that contain personal information to affected individuals, state officers and consumer reporting agencies and businesses and governmental agencies that own data.

Processing and Back-Office Services

As a provider of electronic data processing and back-office services to financial institutions we are also subject to regular oversight and examination by the Federal Financial Institutions Examination Council (FFIEC), an interagency body of the FDIC, the Office of the Comptroller of the Currency, the Federal Reserve, the National Credit Union Administration and the CFPB. In addition, independent auditors annually review several of our operations to provide reports on internal controls for our clients' auditors and regulators. We are also subject to review under state laws and rules that regulate many of the same activities that are described above, including electronic data processing and back-office services for financial institutions and use of consumer information.

11

Anti-Money Laundering and Counter Terrorist Regulation

Our business is subject to U.S. federal anti-money laundering laws and regulations, including the Bank Secrecy Act, as amended by the USA PATRIOT Act of 2001, which we refer to collectively as the BSA. The BSA, among other things, requires money services businesses to develop and implement risk-based anti-money laundering programs, report large cash transactions and suspicious activity and maintain transaction records.

We are also subject to certain economic and trade sanctions programs that are administered by the Treasury Department's Office of Foreign Assets Control, or OFAC, that prohibit or restrict transactions to or from or dealings with specified countries, their governments and, in certain circumstances, their nationals, narcotics traffickers, and terrorists or terrorist organizations, as well as similar anti-money laundering, counter terrorist financing and proceeds of crime laws applicable to movements of currency and payments through electronic transactions and to dealings with certain specified persons.

We continually develop new compliance programs and enhance existing ones to monitor and address legal and regulatory requirements and developments.

Federal Trade Commission Act and Other Laws Impacting Our and our Customers' Business

All persons engaged in commerce, including, but not limited to, us and our merchant and financial institution customers are subject to Section 5 of the Federal Trade Commission Act prohibiting unfair or deceptive acts or practices, or UDAP. In addition, there are other laws, rules and or regulations, including the Telemarketing Sales Act and the Unlawful Internet Gambling Enforcement Act of 2006, that may directly impact the activities of our merchant customers and in some cases may subject us, as the merchant's payment processor, to litigation, investigations, fees, fines and disgorgement of funds in the event we are deemed to have aided and abetted or otherwise provided the means and instrumentalities to facilitate the illegal activities of the merchant through our payment processing services. Various federal and state regulatory enforcement agencies including the Federal Trade Commission, or FTC, and the states' attorneys general have authority to take action against nonbanks that engage in UDAP or violate other laws, rules and regulations.

As a result of the increasingly uncertain regulatory and judicial environment surrounding Daily Fantasy Sports, we have decided to suspend processing for these transactions. Revenue from Daily Fantasy Sports is not material to our business or to our Merchant segment. If there is greater regulatory and judicial clarity, we may re-enter the space in the future. In the meantime, we remain firmly committed to processing for online and land-based gaming operators, including state lotteries and other regulated gaming activities where the regulatory and judicial framework are more clearly established.

Prepaid Services

Prepaid card programs managed by us are subject to various federal and state laws and regulations, which may include laws and regulations related to consumer and data protection, licensing, consumer disclosures, escheat, anti-money laundering, banking, trade practices and competition and wage and employment. For example, most states require entities engaged in money transmission in connection with the sale of prepaid cards to be licensed as a money transmitter with, and subject to examination by, that jurisdiction's banking department. In the future, we may have to obtain state licenses to expand our distribution network for prepaid cards, which licenses we may not be able to obtain. Furthermore, the Credit Card Accountability Responsibility and Disclosure Act of 2009 and the Federal Reserve's Regulation E impose requirements on general-use prepaid cards, store gift cards and electronic gift certificates. These laws and regulations are sometimes inconsistent and subject to judicial and regulatory challenge and interpretation, and therefore the extent to which these laws and rules have application to, and their impact on, us, financial institutions, merchants or others could change. Prepaid services may also be subject to the rules and regulations of Visa, MasterCard and other payment networks with which we and the card issuers do business. The programs in place to process these products generally may be modified by the payment networks in their discretion and such modifications could also impact us, financial institutions, merchants and others.

We are also registered with the Financial Crimes Enforcement Network of the U.S. Department of the Treasury, or FinCEN, as a "money services business-provider of prepaid access" and are subject to examination and review by FinCEN, primarily with respect to anti-money laundering issues.

Other

We are subject to the Housing Assistance Tax Act of 2008, which requires information returns to be made for each calendar year by merchant acquiring entities. In addition, we are subject to U.S. federal and state unclaimed or abandoned

12

property (escheat) laws in the United States which require us to turn over to certain government authorities the property of others we hold that has been unclaimed for a specified period of time such as account balances that are due to a merchant following discontinuation of its relationship with us.

The foregoing list of laws and regulations to which we are subject is not exhaustive, and the regulatory framework governing our operations changes continuously. The enactment of new laws and regulations may increasingly affect the operation of our business, directly and indirectly, which could result in substantial regulatory compliance costs, litigation expense, adverse publicity, the loss of revenue and decreased profitability.

Intellectual Property

We rely on a combination of intellectual property laws, confidentiality procedures and contractual provisions to protect our proprietary technology and our brand. We have registered, and applied for the registration of, U.S. and international trademarks, service marks, and domain names. Additionally, we have filed U.S. and international patent applications covering certain of our proprietary technology relating to payment solutions, transaction processing and other matters. Over time, we have assembled and continue to assemble a portfolio of patents, trademarks, service marks, copyrights, domain names and trade secrets covering our products and services. Intellectual property is a component of our ability to be a leading payment services provider and any significant impairment of, or third-party claim against, our intellectual property rights could harm our business or our ability to compete.

Employees

As of December 31, 2015, we had 3,313 employees. As of December 31, 2015, this included 896 Merchant Services employees, 84 Financial Institution Services employees, 863 IT employees, 960 operations employees and 510 general and administrative employees. None of our employees are represented by a collective bargaining agreement. We believe that relations with our employees are good.

Corporate Information

We are a Delaware corporation incorporated on March 25, 2009. We completed our initial public offering in March 2012 and our Class A common stock is listed on the New York Stock Exchange under the symbol "VNTV". Our principal executive offices are located at 8500 Governor's Hill Drive, Symmes Township, Ohio 45249, and our telephone number is (513) 900-4811. Our website address is www.vantiv.com.

Available Information

We are subject to the informational requirements of the Securities Exchange Act of 1934 and file or furnish reports, proxy statements, and other information with the U.S. Securities and Exchange Commission, or SEC. You can read our SEC filings over the Internet at the SEC's website at www.sec.gov. Our filings with the SEC, including our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments to those reports, also are available free of charge on the investors section of our website at http://investors.vantiv.com when such reports are available on the SEC's website. Further corporate governance information, including our certificate of incorporation, bylaws, governance guidelines, board committee charters, and code of business conduct and ethics, is also available on the investors section of our website.

You may also read and copy any document we file with the SEC at its public reference facilities at 100 F Street, NE, Room 1580, Washington, DC 20549. You may also obtain copies of the documents at prescribed rates by writing to the Public Reference Section at the SEC at 100 F Street, NE, Room 1580, Washington, DC 20549. Please call the SEC at 1-800-SEC-0330 for further information on the operation of the public reference facilities. The contents of the websites referred to above are not incorporated into this filing or in any other report or document we file with the SEC, and any references to these websites are intended to be inactive textual references only.

13

Item 1A. Risk Factors

Our business is subject to numerous risks. You should carefully consider the following risk factors and all other information contained in this Annual Report on Form 10-K and in our other filings with the SEC. Any of these risks could adversely affect our business, results of operations, financial condition and prospects.

Risks Related to Our Business

If we cannot keep pace with rapid developments, changes and consolidation occurring in our industry and provide new services to our clients, the use of our services could decline, reducing our revenues.

The electronic payments market in which we operate is characterized by rapid technological change, new product and service introductions, including ecommerce services, mobile payment applications, and prepaid services, evolving industry standards, changing customer and consumer needs, the entrance of non-traditional competitors and periods of increased consolidation. In order to remain competitive in this rapidly evolving market, we are continually involved in a number of projects to develop new and innovative services. These projects carry risks, such as cost overruns, delays in delivery, performance problems and lack of market acceptance of new or innovated services. Any delay in the delivery of new services or the failure to differentiate our services or to accurately predict and address market demand could render our services less desirable, or even obsolete, to our clients.

In addition, the new or innovated services we develop are designed to process very complex transactions and provide information on those transactions, all at very high volumes and processing speeds. Any failure to deliver reliable, effective and secure services that meet the expectations of our clients could result in increased costs and/or a loss in business and revenues that could reduce our earnings. If we are unable to develop, adapt to or access technological changes or evolving industry standards on a timely and cost effective basis, our business, financial condition and results of operations would be materially adversely affected.

The payment processing industry is highly competitive, and we compete with certain firms that are larger and that have greater financial resources. Such competition could adversely affect the transaction and other fees we receive from merchants and financial institutions, and as a result, our margins, business, financial condition and results of operations.

Our competitors include financial institutions and well-established payment processing companies, including Bank of America Merchant Services, Chase Paymentech Solutions, Elavon Inc. (a subsidiary of U.S. Bancorp), First Data Corporation, Global Payments, Inc., Heartland Payment Systems, Inc., Total System Services, Inc. and WorldPay US, Inc. in our Merchant Services segment, and Fidelity National Information Services, Inc., First Data Corporation, Fiserv, Inc., Total System Services, Inc. and Visa Debit Processing Service in our Financial Institution Services segment. With respect to our Financial Institutions Services segment, in addition to competition with direct competitors, we also compete with the capabilities of many larger potential clients to conduct their key payment processing applications in-house.

Many of our competitors also have substantially greater financial, technological and marketing resources than we have. In addition, our competitors that are financial institutions or are affiliated with financial institutions, may not incur the sponsorship costs we incur for registration with the payment networks. Accordingly, these competitors may be able to offer more attractive fees to our current and prospective clients or other services that we do not provide. Competition could result in a loss of existing clients, and greater difficulty attracting new clients. Furthermore, if competition causes us to reduce the fees we charge in order to attract or retain clients, there is no assurance we can successfully control our costs in order to maintain our profit margins. One or more of these factors could have a material adverse effect on our business, financial condition and results of operations.

Furthermore, we are facing new competitive pressure from non-traditional payments processors and other parties entering the payments industry, such as PayPal, Google, Apple, Alibaba and Amazon, who may compete in one or more of the functions performed in processing merchant transactions. These companies have significant financial resources and robust networks and are highly regarded by consumers. If these companies gain a greater share of total electronic payments transactions or if we are unable to successfully react to changes in the industry spurred by the entry of these new market participants, it could have a material adverse effect on our business, financial condition and results of operations.

14

Unauthorized disclosure of data, whether through cybersecurity breaches, computer viruses or otherwise, could expose us to liability, protracted and costly litigation and damage our reputation.

We have responsibility for certain third parties, including merchants, ISOs, third party service providers and other agents, which we refer to collectively as associated participants, under Visa, MasterCard and other payment network rules and regulations. We and certain of our associated participants process, store and/or transmit sensitive data, such as names, addresses, social security numbers, credit or debit card numbers, driver’s license numbers and bank account numbers, and we have ultimate liability to the payment networks and member financial institutions that register us with Visa, MasterCard and other payment networks for our failure or the failure of our associated participants to protect this data in accordance with payment network requirements. The loss of merchant or cardholder data by us or our associated participants could result in significant fines and sanctions by the payment networks or governmental bodies. A significant cybersecurity breach could also result in payment networks prohibiting us from processing transactions on their networks or the loss of our financial institution sponsorship that facilitates our participation in the payment networks, which would have a material adverse effect on our business, financial condition and results of operations.

These concerns about security are increased when we transmit information over the Internet. The techniques used to obtain unauthorized access, disable or degrade service or sabotage systems change frequently and are often difficult to detect. We and our associated participants have been in the past and could be in the future, subject to breaches of security by hackers. In such circumstances, our encryption of data and other protective measures have not prevented and may not prevent unauthorized access service disruption or system sabotage. Although we have not incurred material losses or liabilities as a result of security breaches we or our associated participants have experienced, any future breach of our system or an associated participant could be material and harm our reputation, deter clients and potential clients from using our services, increase our operating expenses, expose us to uninsured losses or other liabilities, increase our risk of regulatory scrutiny, subject us to lawsuits, result in material penalties and fines under state and federal laws or by the payment networks, and adversely affect our continued payment network registration and financial institution sponsorship.

We cannot assure you that our arrangements with associated participants will prevent the unauthorized use or disclosure of data or that we would be reimbursed by associated participants in the event of unauthorized use or disclosure of data. Any such unauthorized use or disclosure of data could result in protracted and costly litigation, which could have a material adverse effect on our business, financial condition and results of operations.

Our systems and our third party providers’ systems may fail due to factors beyond our control, which could interrupt our service, cause us to lose business and increase our costs.

We depend on the efficient and uninterrupted operation of numerous systems, including our computer systems, software, data centers and telecommunications networks, as well as the systems of third parties, in order to provide services to our clients. Our systems and operations and those of our third party providers, could be exposed to damage or interruption from, among other things, fire, natural disaster, power loss, telecommunications failure, unauthorized entry, security breach, computer viruses, defects and development delays. Our property and business interruption insurance may not be adequate to compensate us for all losses or failures that may occur. Defects in our systems or those of third parties, errors or delays in the processing of payment transactions, telecommunications failures or other difficulties could result in loss of revenues and clients, reputational harm, additional operating expenses in order to remediate the failures, fines imposed by payment networks and exposure to other losses or other liabilities.

We may not be able to continue to expand our share of the existing payment processing markets or expand into new markets which would inhibit our ability to grow and increase our profitability.

Our future growth and profitability depend upon the growth of the markets in which we currently operate and our ability to increase our penetration and service offerings within these markets, as well as the emergence of new markets for our services and our ability to penetrate these new markets. It is difficult to attract new clients because of potential disadvantages associated with switching payment processing vendors, such as transition costs, business disruption and loss of accustomed functionality. We seek to overcome these factors by making investments to enhance the functionality of our software and differentiate our services. However, there can be no assurance that our efforts will be successful, and this resistance may adversely affect our growth.

Our expansion into new markets is also dependent upon our ability to adapt our existing technology and offerings or to develop new or innovative applications to meet the particular service needs of each new market. In order to do so, we will need to anticipate and react to market changes and devote appropriate financial and technical resources to our development efforts, and there can be no assurance that we will be successful in these efforts.

15

Furthermore, in response to market developments, we may expand into new geographical markets and foreign countries in which we do not currently have any operating experience. We cannot assure you that we will be able to successfully expand in such markets or internationally due to our lack of experience and the multitude of risks associated with global operations or lack of appropriate regulatory approval.

Any acquisitions, partnerships or joint ventures that we make could disrupt our business and harm our financial condition.

Acquisitions, partnerships and joint ventures are part of our growth strategy. We evaluate, and expect in the future to evaluate potential strategic acquisitions of, and partnerships or joint ventures with, complementary businesses, services or technologies. However, we may not be able to successfully identify suitable acquisition, partnership or joint venture candidates in the future. In addition, for purposes of the Bank Holding Company Act of 1956, as amended, or the BHC Act, we are deemed to be a subsidiary of Fifth Third Bank. For so long as we continue to be considered a subsidiary of a bank, we may only engage in activities that are permissible for the bank to engage in directly. These activities and restrictions may limit our ability to acquire other businesses, enter into other strategic transactions or expand into foreign countries.

If we do enter into acquisitions, partnerships and joint ventures, they may not provide us with the benefits we anticipate. We may not be able to successfully integrate any businesses, services or technologies that we acquire or with which we form a partnership or joint venture, or comply with applicable regulatory requirements. Furthermore, the integration of any acquisition, including our recent acquisitions, may divert management’s time and resources from our core business and disrupt our operations. Certain partnerships and joint ventures we make may also prevent us from competing for certain clients or in certain lines of business. To the extent we pay the purchase price of any acquisition in cash, it would reduce our cash reserves, and to the extent the purchase price is paid with our stock, it could be dilutive to our stockholders. To the extent we pay the purchase price with proceeds from the incurrence of debt, it would increase our already high level of indebtedness and could negatively affect our liquidity and restrict our operations.

If we fail to comply with the applicable requirements of the Visa, MasterCard or other payment networks, those payment networks could seek to fine us, suspend us or terminate our registrations through our financial institution sponsors. Fines could have a material adverse effect on our business, financial condition or results of operations, and if these registrations are terminated, we may not be able to conduct our business.

In order to provide our transaction processing services, we are registered through our bank sponsorships with the Visa, MasterCard and other payment networks as service providers for member institutions. We and many of our clients are subject to payment network rules. If we or our associated participants do not comply with the payment network requirements, the payment networks could seek to fine us, suspend us or terminate our registrations. We have occasionally received notices of noncompliance and fines, which have typically related to excessive chargebacks by a merchant or data security failures on the part of a merchant. If we are unable to recover fines from or pass through costs to our merchants or other associated participants, we would experience a financial loss. The termination of our registration, or any changes in the payment network rules that would impair our registration, could require us to stop providing payment network services to the Visa, MasterCard or other payment networks, which would have a material adverse effect on our business, financial condition and results of operations.

Changes in payment network rules or standards could adversely affect our business, financial condition and results of operations.

Payment network rules are established and changed from time to time by each payment network as they may determine in their sole discretion and with or without advance notice to their participants. In some cases, payment networks compete with us, and their ability to modify and enhance their rules in their sole discretion may provide them an advantage in selling or developing their own services that may compete directly or indirectly with our services. Any changes in payment network rules or standards or the way they are implemented could increase our cost of doing business or limit our ability to provide transaction processing services to or through our clients and have a material adverse effect on our business, financial condition and results of operations.

16

If we cannot pass along to our merchants increases in interchange and other fees from payment networks, our operating margins would be reduced.

We pay interchange, assessment, transaction and other fees set by the payment networks to the card issuing financial institution and the payment networks for each transaction we process. From time to time, the payment networks increase the interchange fees and other fees that they charge payment processors and the financial institution sponsors. At their sole discretion, our financial institution sponsors have the right to pass any increases in interchange and other fees on to us and they have consistently done so in the past. We are generally permitted under the contracts into which we enter, and in the past we have been able to, pass these fee increases along to our merchants through corresponding increases in our processing fees. However, if we are unable to pass through these and other fees in the future, it could have a material adverse effect on our business, financial condition and results of operations.

If our agreements with financial institution sponsors and clearing service providers to process electronic payment transactions are terminated or otherwise expire and we are unable to renew existing or secure new sponsors or clearing service providers, we will not be able to conduct our business.

The Visa, MasterCard and other payment network rules require us to be sponsored by a member bank in order to process electronic payment transactions. Because we are not a bank, we are unable to directly access these payment networks. We are currently registered with the Visa, MasterCard and other payment networks through Fifth Third Bank and other sponsor banks. Our current agreement with Fifth Third Bank expires in June 2019. These agreements with Fifth Third Bank and other sponsors give them substantial discretion in approving certain aspects of our business practices, including our solicitation, application and qualification procedures for merchants and the terms of our agreements with merchants. Our financial institution sponsors’ discretionary actions under these agreements could have a material adverse effect on our business, financial condition and results of operations. We also rely on Fifth Third Bank and various other financial institutions to provide clearing services in connection with our settlement activities. Without these sponsorships or clearing services agreements, we would not be able to process Visa, MasterCard and other payment network transactions or settle transactions which would have a material adverse effect on our business, financial condition and results of operations. Furthermore, our financial results could be adversely affected if our costs associated with such sponsorships or clearing services agreements increase.

Increased merchant, financial institution or referral partner attrition and decreased transaction volume could cause our revenues to decline.

We experience attrition and declines in merchant and financial institution credit, debit or prepaid card processing volume resulting from several factors, including business closures, consolidations, loss of accounts to competitors, account closures that we initiate due to heightened credit risks, and reductions in our merchants' sales volumes. Our referral partners, many of which are not exclusive, such as merchant banks, ISVs, VARs, payment facilitators, ISOs and trade associations are strong contributors to our revenue growth in our Merchant Services segment. If an ISO or referral partner switches to another transaction processor, shuts down or becomes insolvent, we will no longer receive new merchant referrals from the ISO or referral partner, and we risk losing existing merchants that were originally enrolled by the ISO or referral partner. We cannot predict the level of attrition and decreased transaction volume in the future and our revenues could decline as a result of higher than expected attrition, which could have a material adverse effect on our business, financial condition and results of operations.

We are subject to economic and political risk, the business cycles and credit risk of our clients and the overall level of consumer, business and government spending, which could negatively impact our business, financial condition and results of operations.

The electronic payments industry depends heavily on the overall level of consumer, business and government spending. We are exposed to general economic conditions that affect consumer confidence, consumer spending, consumer discretionary income or changes in consumer purchasing habits. A sustained deterioration in general economic conditions, particularly in the United States, or increases in interest rates may adversely affect our revenues by reducing the number or average purchase amount of transactions made using electronic payments that we process. Furthermore, if economic conditions cause credit card issuers to tighten credit requirements, the negative effects on the use of electronic payments could be exacerbated. Since we have a certain amount of fixed and semi-fixed costs, including rent, debt service, processing contractual minimums and salaries, our ability to quickly adjust costs and respond to changes in our business and the economy is limited. As a result, changes in economic conditions could adversely impact our future revenues and profits.

17

In addition, a sustained deterioration in economic conditions could affect our merchants through a higher rate of closures or bankruptcies, resulting in lower revenues and earnings for us. In addition, our merchants and other associated participants are liable for any charges properly reversed by the card issuer on behalf of the cardholder and for any fines or penalties that may be assessed by payment networks. In the event that we are not able to collect such amounts from the associated participants, due to closure, insolvency or other reasons, we may be liable for any such charges.

Fraud by merchants or others could have a material adverse effect on our business, financial condition and results of operations.

We face potential liability for fraudulent electronic payment transactions initiated by merchants or other associated participants. Examples of merchant fraud include when a merchant or other party knowingly accepts payment by a stolen or counterfeit credit, debit or prepaid card, card number or other credentials records a false sales transaction utilizing a stolen or counterfeit card or credentials, processes an invalid card, or intentionally fails to deliver the merchandise or services sold in an otherwise valid transaction. In the event a dispute between a cardholder and a merchant is not resolved in favor of the merchant, the transaction is normally charged back to the merchant and the purchase price is credited or otherwise refunded to the cardholder. Failure to effectively manage risk and prevent fraud would increase our chargeback liability or other liability. In addition, beginning October 2015, merchants that cannot process EMV chip-based cards are held financially responsible for certain fraudulent transactions conducted using such cards. This will likely increase the amount of risk for merchants who are not yet EMV-compliant and could result in us having to seek increased chargebacks from such merchants. Increases in chargebacks or other liability could have a material adverse effect on our business, financial condition and results of operations.

A decline in the use of credit, debit or prepaid cards as a payment mechanism for consumers or adverse developments with respect to the payment processing industry in general could have a materially adverse effect on our business, financial condition and results of operations.

If consumers do not continue to use credit, debit or prepaid cards as a payment mechanism for their transactions or if there is a change in the mix of payments between cash, alternative currencies and technologies, credit, debit and prepaid cards, or the corresponding methodologies used for each, which is adverse to us, it could have a materially adverse effect on our business, financial condition and results of operations. Moreover, if there is an adverse development in the payments industry in general, such as new legislation or regulation that makes it more difficult for our clients to do business, our business, financial condition and results of operations may be adversely affected.

If Fifth Third Bank fails or is acquired by a third party, it could place certain of our material contracts at risk, decrease our revenue, and transfer the ultimate voting power of Fifth Third Bank’s stock ownership in us (including any shares of Class A common stock that may be issued in exchange for Fifth Third Bank’s units in Vantiv Holding) to a third party.

Fifth Third Bank accounted for approximately 3% of our revenue during the years ended December 31, 2015 and 2014, and is the provider of the services under our Clearing, Settlement and Sponsorship Agreement, Referral Agreement and Master Services Agreement. If Fifth Third Bank were to be placed into receivership or conservatorship, it could jeopardize our ability to generate revenue and conduct our business.