Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - ARROW ELECTRONICS INC | a201510kex21.htm |

| EX-4.(A)(X) - EXHIBIT 4.(A)(X) - ARROW ELECTRONICS INC | arwexhibit4ax.htm |

| EX-31.(I) - EXHIBIT 31.(I) - ARROW ELECTRONICS INC | arwexhibit31iq415.htm |

| EX-32.(L) - EXHIBIT 32.(I) - ARROW ELECTRONICS INC | arwexhibit32iq415.htm |

| EX-32.(LL) - EXHIBIT 32.(II) - ARROW ELECTRONICS INC | arwexhibit32iiq415.htm |

| EX-31.(II) - EXHIBIT 31.(II) - ARROW ELECTRONICS INC | arwexhibit31iiq415.htm |

| EX-10.(C)(II) - EXHIBIT 10.(C)(II) - ARROW ELECTRONICS INC | arwexhibit10ciifebruary220.htm |

| EX-10.(M) - EXHIBIT 10.(M) - ARROW ELECTRONICS INC | arwexhibit10mfebruary22016.htm |

| EX-10.(A)(I) - EXHIBIT 10.(A)(I) - ARROW ELECTRONICS INC | arwexhibit10aifebruary22016.htm |

| EX-23 - EXHIBIT 23 - ARROW ELECTRONICS INC | a201510kex23.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-4482

ARROW ELECTRONICS, INC.

(Exact name of registrant as specified in its charter)

New York | 11-1806155 |

(State or other jurisdiction of | (I.R.S. Employer |

incorporation or organization) | Identification Number) |

9201 East Dry Creek Road, Centennial, Colorado | 80112 |

(Address of principal executive offices) | (Zip Code) |

(303) 824-4000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, $1 par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act (check one):

Large accelerated filer x | Accelerated filer o |

Non-accelerated filer o (do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of voting stock held by non-affiliates of the registrant as of the last business day of the registrant's most recently completed second fiscal quarter was $5,352,842,897.

There were 90,943,344 shares of Common Stock outstanding as of February 1, 2016.

DOCUMENTS INCORPORATED BY REFERENCE

The definitive proxy statement related to the registrant's Annual Meeting of Shareholders, to be held May 12, 2016 is incorporated by reference in Part III to the extent described therein.

TABLE OF CONTENTS

PART I | |||

Item 1. | Business. | ||

Item 1A. | Risk Factors. | ||

Item 1B. | Unresolved Staff Comments. | ||

Item 2. | Properties. | ||

Item 3. | Legal Proceedings. | ||

Item 4. | Mine Safety Disclosures. | ||

PART II | |||

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. | ||

Item 6. | Selected Financial Data. | ||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations. | ||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk. | ||

Item 8. | Financial Statements and Supplementary Data. | ||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. | ||

Item 9A. | Controls and Procedures. | ||

Item 9B. | Other Information. | ||

PART III | |||

Item 10. | Directors, Executive Officers and Corporate Governance. | ||

Item 11. | Executive Compensation. | ||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | ||

Item 13. | Certain Relationships and Related Transactions, and Director Independence. | ||

Item 14. | Principal Accounting Fees and Services. | ||

PART IV | |||

Item 15. | Exhibits and Financial Statement Schedules. | ||

Signatures | |||

2

PART I

Item 1. Business.

Arrow Electronics, Inc. (the "company" or "Arrow") is a global provider of products, services, and solutions to industrial and commercial users of electronic components and enterprise computing solutions. The company has one of the world’s broadest portfolios of product offerings available from leading electronic components and enterprise computing solutions suppliers, coupled with a range of services, solutions and tools that help industrial and commercial customers introduce innovative products, reduce their time to market, and enhance their overall competitiveness. Arrow was incorporated in New York in 1946 and serves over 100,000 customers.

Arrow's diverse worldwide customer base consists of original equipment manufacturers ("OEMs"), contract manufacturers ("CMs"), and other commercial customers. These customers include manufacturers of industrial equipment (such as machine tools, factory automation, and robotic equipment) and consumer products serving industries ranging from telecommunications, automotive and transportation, aerospace and defense, medical, professional services, and alternative energy, among others. Customers also include value-added resellers ("VARs") of enterprise computing solutions.

The company maintains over 300 sales facilities and 40 distribution and value-added centers in 53 countries, serving over 85 countries. Through this network, Arrow guides innovation forward by helping its customers deliver new technologies, new materials, new ideas, and new electronics that impact the business community and consumers.

The company has two business segments, the global components business and the global enterprise computing solutions ("ECS") business. The company distributes electronic components to OEMs and CMs through its global components business segment and provides enterprise computing solutions to VARs through its global ECS business segment. For 2015, approximately 62% of the company's sales were from the global components business segment, and approximately 38% of the company's sales were from the global ECS business segment. The financial information about the company's business segments and geographic operations is found in Note 16 of the Notes to the Consolidated Financial Statements.

The company's financial objectives are to grow sales faster than the market, increase the markets served, grow profits faster than sales, and increase return on invested capital. To achieve its objectives, the company seeks to capture significant opportunities to grow across products, markets, and geographies. To supplement its organic growth strategy, the company continually evaluates strategic acquisitions to broaden its product and value-added service offerings, increase its market penetration, and expand its geographic reach.

Global Components

Global components markets and distributes electronic components and provides a comprehensive range of value-added capabilities throughout the entire life cycle of technology products and services. The company provides customers with the ability to deliver the latest technologies to the market through design engineering, global marketing and integration, global logistics and supply chain management. The company offers the convenience of accessing, from a single source, multiple technologies and products from its suppliers with rapid or scheduled deliveries. Additionally, the company offers expertise in reverse logistics, asset management, and asset recovery to maximize value at the end of a product’s life cycle. Most of the company's customers require delivery of their orders on schedules or volumes that are generally not available on direct purchases from manufacturers.

As one of the largest providers of electronic components and related services in the world, global components covers the world's largest electronics markets - the Americas, EMEA (Europe, Middle East, and Africa), and Asia Pacific regions. The Americas include operations in Argentina, Brazil, Canada, Mexico, and the United States. In the EMEA region, the global components business segment operates in Austria, Belgium, Czech Republic, Denmark, Egypt, Estonia, Finland, France, Germany, Hungary, Israel, Italy, the Netherlands, Norway, Poland, Portugal, Romania, the Russian Federation, Slovakia, Slovenia, South Africa, Spain, Sweden, Switzerland, Turkey, Ukraine, and the United Kingdom. In the Asia Pacific region, the global components business segment operates in Australia, China, Hong Kong, India, Indonesia, Japan, Malaysia, New Zealand, Philippines, Singapore, Taiwan, Thailand, and Vietnam.

Within the global components business segment, approximately 66% of the company's sales consist of semiconductor products and related services; approximately 19% consist of passive, electro-mechanical, and interconnect products, consisting primarily of capacitors, resistors, potentiometers, power supplies, relays, switches, and connectors; approximately 10% consist of computing and memory; and approximately 5% consist of other products and services.

3

Over the past three years, the global components business segment completed 16 strategic acquisitions to broaden its product and service offerings, to further expand its geographic reach in the Asia Pacific region, and to increase its digital capabilities to meet the evolving needs of customers and suppliers. These acquisitions also expanded the company's global components business segment's portfolio of products and services across the full product lifecycle including new product development, reverse logistics, and electronics asset disposition.

Global ECS

The company's global ECS business segment is a leading value-added provider of comprehensive computing solutions and services. Global ECS’ portfolio of computing solutions includes datacenter, cloud, security, and analytics solutions. Global ECS brings broad market access, extensive supplier relationships, scale and resources to help its VARs meet the needs of their end-users. Global ECS works with VARs to tailor complex IT solutions for their end-users. Customers have access to various services including engineering and integration support, warehousing and logistics, marketing resources, and authorized hardware and software training. Global ECS’ suppliers benefit from demand creation, speed to market, and efficient supply chain management. For these suppliers, global ECS is the aggregation point to over 20,000 VARs.

Global ECS operates in 32 countries around the world, largely in the Americas, EMEA, and the Asia Pacific regions. The Americas include operations in the United States, Canada, and Brazil. In the EMEA region, the global ECS business segment operates in Austria, Belgium, Czech Republic, Denmark, Estonia, Finland, France, Germany, Hungary, Iceland, Ireland, Israel, Italy, Latvia, Lithuania, Luxembourg, Morocco, the Netherlands, Norway, Poland, Portugal, Spain, Sweden, Switzerland, the United Arab Emirates, and the United Kingdom. The Asia Pacific region includes offices in Australia, New Zealand, and Singapore.

Within the global ECS business segment, approximately 39% consist of software, 35% of the company's sales consist of storage, 9% consist of proprietary servers, 9% consist of industry standard servers, and 8% consist of other products and services.

Over the past three years, the global ECS business segment completed 4 strategic acquisitions to further expand its geographic reach and its portfolio of products. Aligned with the vision of guiding innovation forward in the IT channel, the company is investing in emerging and adjacent markets, such as managed services and unified computing, within the ECS business.

Customers and Suppliers

The company and its affiliates serve over 100,000 industrial and commercial customers. Industrial customers range from major OEMs and CMs to small engineering firms, while commercial customers primarily include VARs and OEMs. No single customer accounted for more than 2% of the company's 2015 consolidated sales.

The company’s sales teams focus on an extensive portfolio of products and services to support customers’ material management and production needs, including connecting customers to the company’s field application engineers that provide technical support and serve as a gateway to the company’s supplier partners. The company’s sales representatives generally focus on a specific customer segment, particular product lines or a specific geography, and provide end-to-end product offerings and solutions with an emphasis on helping customers introduce innovative products, reduce their time to market, and enhance their overall competitiveness.

Substantially all of the company's sales are made on an order-by-order basis, rather than through long-term sales contracts. As such, the nature of the company's business does not provide visibility of material forward-looking information from its customers and suppliers beyond a few months.

No single supplier accounted for more than 7% of the company's consolidated sales in 2015. The company believes that many of the products it sells are available from other sources at competitive prices. However, certain parts of the company's business, such as the company's global ECS business segment, rely on a limited number of suppliers with the strategy of providing focused support, extensive product knowledge, and customized service to suppliers and VARs. Most of the company's purchases are pursuant to distributor agreements, which are typically non-exclusive and cancelable by either party at any time or on short notice.

Distribution Agreements

Generally, our agreements with manufacturers protect us against the potential write-down of inventories due to technological change or manufacturers' price reductions. Write-downs of inventories to market value are based upon contractual provisions, which typically provide certain protections to the company for product obsolescence and price erosion in the form of return privileges, scrap allowances, and price protection. Under the terms of the related distributor agreements and assuming the company complies with certain conditions, such suppliers are required to credit the company for reductions in manufacturers' list prices.

4

As of December 31, 2015, this type of arrangement covered approximately 57% of the company's consolidated inventories. In addition, under the terms of many such agreements, the company has the right to return to the manufacturer, for credit, a defined portion of those inventory items purchased within a designated period of time.

A manufacturer, which elects to terminate a distribution agreement, is generally required to purchase from the company the total amount of its products carried in inventory. As of December 31, 2015, this type of repurchase arrangement covered approximately 61% of the company's consolidated inventories.

While these inventory practices do not wholly protect the company from inventory losses, the company believes that they currently provide substantial protection from such losses.

Competition

The company operates in a highly competitive environment, both in the United States and internationally. The company competes with other large multinational and national electronic components and enterprise computing solutions distributors, as well as numerous other smaller, specialized competitors who generally focus on narrower markets, products, or particular sectors. The company also competes for customers with its suppliers. The size of the company's competitors vary across markets sectors, as do the resources the company has allocated to the sectors in which it does business. Therefore, some of the company's competitors may have a more extensive customer and/or supplier base than the company in one or more of its market sectors. There is significant competition within each market sector and geography served that creates pricing pressure and the need to improve services. Other competitive factors include rapid technological changes, product availability, credit availability, speed of delivery, ability to tailor solutions to customer needs, quality and depth of product lines and training, as well as service and support provided by the distributor to the customer.

The company also faces competition from companies entering or expanding into the logistics and product fulfillment, electronic catalog distribution, and e-commerce supply chain services markets. As the company seeks to expand its business into new areas in order to stay competitive in the market, the company may encounter increased competition from its current and/or new competitors.

The company believes that it is well equipped to compete effectively with its competitors in all of these areas due to its comprehensive product and service offerings, highly-skilled work force, and global distribution network.

Employees

The company and its affiliates employed approximately 18,500 employees worldwide as of December 31, 2015.

Available Information

The company files its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Proxy Statements, and other documents with the U.S. Securities and Exchange Commission ("SEC") under the Securities Exchange Act of 1934. A copy of any document the company files with the SEC is available for review at the SEC's public reference room, 100 F Street, N.E., Washington, D.C. 20549. The SEC is reachable at 1-800-SEC-0330 for further information on the public reference room. The company's SEC filings are also available to the public on the SEC's Web site at http://www.sec.gov and through the New York Stock Exchange ("NYSE"), 20 Broad Street, New York, New York 10005, on which the company's common stock is listed.

A copy of any of the company's filings with the SEC, or any of the agreements or other documents that constitute exhibits to those filings, can be obtained by request directed to the company at the following address and telephone number:

Arrow Electronics, Inc.

9201 East Dry Creek Road

Centennial, Colorado 80112

(303) 824-4000

Attention: Corporate Secretary

The company also makes these filings available, free of charge, through its website (http://www.arrow.com) as soon as reasonably practicable after the company files such material with the SEC. The company does not intend this internet address to be an active link or to otherwise incorporate the contents of the website into this Annual Report on Form 10-K.

5

Executive Officers

The following table sets forth the names, ages, and the positions held by each of the executive officers of the company as of February 5, 2016:

Name | Age | Position |

Michael J. Long | 57 | Chairman, President, and Chief Executive Officer |

Andrew S. Bryant | 60 | Chief Operating Officer, Arrow Global Enterprise Computing Solutions and Global Components |

Sean J. Kerins | 53 | President, Arrow Global Enterprise Computing Solutions |

Andy King | 52 | President, Arrow Global Components |

Vincent P. Melvin | 52 | Senior Vice President, Chief Information Officer |

M. Catherine Morris | 57 | Senior Vice President, Chief Strategy Officer |

Paul J. Reilly | 59 | Executive Vice President, Finance and Operations, and Chief Financial Officer |

Gregory P. Tarpinian | 54 | Senior Vice President, General Counsel, and Secretary |

Gretchen K. Zech | 46 | Senior Vice President, Global Human Resources |

Set forth below is a brief account of the business experience during the past five years of each executive officer of the company.

Michael J. Long has been Chairman of the Board of Directors and Chief Executive Officer of the company for more than five years. He has been a Director and President of the company for more than five years.

Andrew S. Bryant was appointed Chief Operating Officer of the Arrow Global Enterprise Computing Solutions and Global Components businesses in May 2014. Prior thereto he served as the President of Arrow Global Enterprise Computing Solutions for more than five years.

Sean J. Kerins was appointed President of Arrow Global Enterprise Computing Solutions in May 2014. Prior thereto he served as President of North America Enterprise Computing Solutions from July 2010 to May 2014.

Andy King was appointed President of Arrow Global Components in November 2015. Prior thereto he served as President of EMEA Components from November 2013 to November 2015 and Vice President of Sales in EMEA Components from November 2011 to November 2013. He also served as the VP of EMEA Marketing and Engineering from November 2010 to November 2011.

Vincent P. Melvin was appointed Senior Vice President of the company in December 2013. Prior thereto he served as Vice President of the company from September 2006 to December 2013. He has been the Chief Information Officer of the company for more than five years.

M. Catherine Morris has been Senior Vice President and Chief Strategy Officer of the company for more than five years.

Paul J. Reilly has been Executive Vice President, Finance and Operations, and Chief Financial Officer of the company for more than five years.

Gregory P. Tarpinian was appointed Senior Vice President, General Counsel, and Secretary of the company effective January 2015. Prior thereto he served as the Vice President of Legal Affairs for more than five years.

Gretchen K. Zech was appointed Senior Vice President of Global Human Resources of the company in November 2011. Prior to joining Arrow she served as Senior Vice President, Human Resources, for Dex One Corporation (formerly known as R.H. Donnelley Corporation) from June 2006 to November 2011. R.H. Donnelley Corporation filed for reorganization under Chapter 11 of the United States Bankruptcy Code in May 2009 and emerged as Dex One Corporation in January 2010.

6

Item 1A. Risk Factors.

Described below and throughout this report are certain risks that the company's management believes are applicable to the company's business and the industry in which it operates. If any of the described events occur, the company's business, results of operations, financial condition, liquidity, or access to the capital markets could be materially adversely affected. When stated below that a risk may have a material adverse effect on the company's business, it means that such risk may have one or more of these effects. There may be additional risks that are not presently material or known. There are also risks within the economy, the industry, and the capital markets that could materially adversely affect the company, including those associated with an economic recession, inflation, a global economic slowdown, and those associated with customers' inability or refusal to pay for the products and services provided by the company. There are also risks associated with the occurrence of natural disasters such as tsunamis, hurricanes, tornadoes, and floods. These factors affect businesses generally, including the company's customers and suppliers and, as a result, are not discussed in detail below except to the extent such conditions could materially affect the company and its customers and suppliers in particular ways. Included below are some risks pertaining to specific government regulation, however, not all regulations applicable to the company or unanticipated regulation changes (such as changes in tax regulations in the various geographies we operate) have been described. The continuing expansion of government laws and regulations, some that may apply specifically to the company's industry and others to the market generally, as well as any actions taken by activist investors, could negatively impact the company's profitability.

If the company is unable to maintain its relationships with its suppliers or if the suppliers materially change the terms of their existing agreements with the company, the company's business could be materially adversely affected.

A substantial portion of the company's inventory is purchased from suppliers with which the company has entered into non-exclusive distribution agreements. These agreements are typically cancelable on short notice (generally 30 to 90 days). Certain parts of the company's business, such as the company's global ECS business, rely on a limited number of suppliers. To the extent that the company's significant suppliers reduce the amount of products they sell through distribution, are unwilling to continue to do business with the company, or are unable to continue to meet or significantly alter their obligations, the company's business could be materially adversely affected. In addition, to the extent that the company's suppliers modify the terms of their contracts with the company, limit supplies due to capacity constraints, or other factors, there could be a material adverse effect on the company's business.

The competitive pressures the company faces could have a material adverse effect on the company's business.

The company operates in a highly competitive international environment. The company competes with other large multinational and national electronic components and enterprise computing solutions distributors, as well as numerous other smaller, specialized competitors who generally focus on narrower markets, products, or particular sectors. The company also competes for customers with its suppliers. The size of the company's competitors vary across market sectors, as do the resources the company has allocated to the sectors in which it does business. Therefore, some of the company's competitors may have a more extensive customer and/or supplier base than the company in one or more of its market sectors. There is significant competition within each market sector and geography that creates pricing pressure and the need for constant attention to improve services. Other competitive factors include rapid technological changes, product availability, credit availability, speed of delivery, ability to tailor solutions to customer needs, quality and depth of product lines and training, as well as service and support provided by the distributor to the customer. The Company also faces competition from companies entering or expanding into the logistics and product fulfillment, catalog distribution, and e-commerce supply chain services markets. As the company seeks to expand its business into new areas in order to stay competitive in the market, such as in the area of the "Internet of Things," the company may encounter increased competition from its current and/or new competitors. The company's failure to maintain and enhance its competitive position could have a material adverse effect on its business.

Products sold by the company may be found to be defective and, as a result, warranty and/or product liability claims may be asserted against the company, which may have a material adverse effect on the company.

The company sells its components at prices that are significantly lower than the cost of the equipment or other goods in which they are incorporated. As a result, the company may face claims for damages (such as consequential damages) that are disproportionate to the revenues and profits it receives from the components involved in the claims. While the company typically has provisions in its supplier agreements that hold the supplier accountable for defective products, and the company and its suppliers generally exclude consequential damages in their standard terms and conditions, the company's ability to avoid such liabilities may be limited as a result of differing factors, such as the inability to exclude such damages due to the laws of some of the countries where it does business. The company's business could be materially adversely affected as a result of a significant quality or performance issue in the products sold by the company, if it is required to pay for the associated damages. Although the company

7

currently has product liability insurance, such insurance is limited in coverage and amount. Further, when relying on contractual liability exclusions, the company could lose customers if their claims are not addressed to their satisfaction.

Declines in value and other factors pertaining to the company's inventory could materially adversely affect its business.

The market for the company's products and services is subject to rapid technological change, evolving industry standards, changes in end-market demand, oversupply of product, and regulatory requirements, which can contribute to the decline in value or obsolescence of inventory. Although most of the company's suppliers provide the company with certain protections from the loss in value of inventory (such as price protection and certain rights of return), the company cannot be sure that such protections will fully compensate it for the loss in value, or that the suppliers will choose to, or be able to, honor such agreements. For example, many of the company's suppliers will not allow products to be returned after they have been held in inventory beyond a certain amount of time, and, in most instances, the return rights are limited to a certain percentage of the amount of product the company purchased in a particular time frame. All of these factors pertaining to inventory could have a material adverse effect on the company's business.

The company is subject to environmental laws and regulations that could materially adversely affect its business.

A number of jurisdictions in which the company's products are sold have enacted laws addressing environmental and other impacts from product disposal, use of hazardous materials in products, use of chemicals in manufacturing, recycling of products at the end of their useful life, and other related matters. These laws prohibit the use of certain substances in the manufacture of the company's products and impose a variety of requirements for modification of manufacturing processes, registration, chemical testing, labeling, and other matters. Failure to comply with these laws or any other applicable environmental regulations could result in fines or suspension of sales. Additionally, these directives and regulations may result in the company having non-compliant inventory that may be less readily salable or have to be written off.

Some environmental laws impose liability, sometimes without fault, for investigating or cleaning up contamination on or emanating from the company's currently or formerly owned, leased, or operated property, as well as for damages to property or natural resources and for personal injury arising out of such contamination. As the distribution business, in general, does not involve the manufacture of products, it is typically not subject to significant liability in this area. However, there may be occasions, including through acquisitions, where environmental liability arises. Two sites for which the company assumed responsibility as part of the Wyle Electronics ("Wyle") acquisition are known to have environmental issues, one at Norco, California and the other at Huntsville, Alabama. The company was also named as a defendant in a private lawsuit filed in connection with alleged contamination at a small industrial building formerly leased by Wyle Laboratories in El Segundo, California. The lawsuit was settled, but the possibility remains that government entities or others may attempt to involve the company in further characterization or remediation of groundwater issues in the area. The presence of environmental contamination could also interfere with ongoing operations or adversely affect the company's ability to sell or lease its properties. The discovery of contamination for which the company is responsible, the enactment of new laws and regulations, or changes in how existing requirements are enforced, could require the company to incur costs for compliance or subject it to unexpected liabilities.

Expansion into the electronic asset disposition market has broadened the company's risk profile.

The company has expanded into the electronics asset disposition business, pursuant to which it provides services related to electronic devices being disposed of by business customers. These services include, the cleansing of storage devices from customer equipment and either recycling it through resale or disposing of it in an environmentally compliant manner. The company may also hold equipment in order to protect and preserve customer data. If the company does not meet its contractual and regulatory obligations with respect to such data, it could be subject to financial damages, penalties, and damage to reputation. Also, the company's or its subcontractors' failure to comply with applicable environmental laws and regulations in disposing of the equipment could result in liability. Such environmental liability may be joint and several, meaning that the company could be held responsible for more than its share of the liability involved. To the extent that company fails to comply with its obligations and such failure is not covered by insurance, the company's business could be adversely affected.

The company may not have adequate or cost-effective liquidity or capital resources.

The company requires cash or committed liquidity facilities for general corporate purposes, such as funding its ongoing working capital, acquisition, and capital expenditure needs, as well as to refinance indebtedness. At December 31, 2015, the company had cash and cash equivalents of $273.1 million. In addition, the company currently has access to committed credit lines and an asset securitization program of $2.4 billion, of which the company had outstanding borrowings of $147.0 million at December 31, 2015. The company's ability to satisfy its cash needs depends on its ability to generate cash from operations and to access the

8

financial markets, both of which are subject to general economic, financial, competitive, legislative, regulatory, and other factors that are beyond its control.

The company may, in the future, need to access the financial markets to satisfy its cash needs. The company's ability to obtain external financing is affected by various factors including general financial market conditions and the company's debt ratings. Further, any increase in the company's level of debt, change in status of its debt from unsecured to secured debt, or deterioration of its operating results may cause a reduction in its current debt ratings. Any downgrade in the company's current debt rating or tightening of credit availability could impair the company's ability to obtain additional financing or renew existing credit facilities on acceptable terms. Under the terms of any external financing, the company may incur higher financing expenses and become subject to additional restrictions and covenants. For example, the company's existing debt agreements contain restrictive covenants, including covenants requiring compliance with specified financial ratios, and a failure to comply with these or any other covenants may result in an event of default. The company's lack of access to cost-effective capital resources, an increase in the company's financing costs, or a breach of debt covenants could have a material adverse effect on the company's business.

The agreements governing some of the company's financing arrangements contain various covenants and restrictions that limit some of management's discretion in operating the business and could prevent the company from engaging in some activities that may be beneficial to its business.

The agreements governing the company's financings contain various covenants and restrictions that, in certain circumstances, could limit its ability to:

• | grant liens on assets; |

• | make investments; |

• | merge, consolidate, or transfer all or substantially all of its assets; |

• | incur additional debt; or |

• | engage in certain transactions with affiliates. |

As a result of these covenants and restrictions, the company may be limited in how it conducts its business and may be unable to raise additional debt, compete effectively, or make investments.

The company's failure to have long-term sales contracts may have a material adverse effect on its business.

Most of the company's sales are made on an order-by-order basis, rather than through long-term sales contracts. The company generally works with its customers to develop non-binding forecasts for future orders. Based on such non-binding forecasts, the company makes commitments regarding the level of business that it will seek and accept, the inventory that it purchases, and the levels of utilization of personnel and other resources. A variety of conditions, both specific to each customer and generally affecting each customer's industry may cause customers to cancel, reduce, or delay orders that were either previously made or anticipated, file for bankruptcy protection or fail, or default on their payments. Generally, customers cancel, reduce, or delay purchase orders and commitments without penalty. The company seeks to mitigate these risks, in some cases, by entering into noncancelable/nonreturnable sales agreements, but there is no guarantee that such agreements will adequately protect the company. Significant or numerous cancellations, reductions, delays in orders by customers, loss of customers, and/or customer defaults on payments could materially adversely affect the company's business.

The company's revenues originate primarily from the sales of semiconductor, PEMCO (passive, electro-mechanical and interconnect), IT hardware and software products, the sales of which are traditionally cyclical.

The semiconductor industry historically has experienced fluctuations in product supply and demand, often associated with changes in technology and manufacturing capacity and subject to significant economic market upturns and downturns. Sales of semiconductor products and related services represented approximately 41%, 42%, and 41% of the company's consolidated sales in 2015, 2014, and 2013, respectively. The sale of the company's PEMCO products closely tracks the semiconductor market. Accordingly, the company's revenues and profitability, particularly in its global components business segment, tend to closely follow the strength or weakness of the semiconductor market. Further, economic weakness could cause a decline in spending in information technology, which could have a negative impact on the company's ECS business. A cyclical downturn in the technology industry could have a material adverse effect on the company's business and negatively impact its ability to maintain historical profitability levels.

9

The company's non-U.S. sales represent a significant portion of its revenues, and consequently, the company is exposed to risks associated with operating internationally.

In 2015, 2014, and 2013, approximately 54%, 54%, and 53%, respectively, of the company's sales came from its operations outside the United States. As a result of the company's international sales and locations, its operations are subject to a variety of risks that are specific to international operations, including the following:

• | import and export regulations that could erode profit margins or restrict exports; |

• | the burden and cost of compliance with international laws, treaties, and technical standards and changes in those regulations; |

• | potential restrictions on transfers of funds; |

• | import and export duties and value-added taxes; |

• | transportation delays and interruptions; |

• | the burden and cost of compliance with complex multi-national tax laws and regulations; |

• | uncertainties arising from local business practices and cultural considerations; |

• | enforcement of the Foreign Corrupt Practices Act, or similar laws of other jurisdictions; |

• | foreign laws that potentially discriminate against companies which are headquartered outside that jurisdiction; |

• | volatility associated with sovereign debt of certain international economies; |

• | potential military conflicts and political risks; and |

• | currency fluctuations, which the company attempts to minimize through traditional hedging instruments. |

Furthermore, products the company sells which are either manufactured in the United States or based on U.S. technology ("U.S. Products") are subject to the Export Administration Regulations ("EAR") when exported and re-exported to and from all international jurisdictions, in addition to the local jurisdiction's export regulations applicable to individual shipments. Licenses or proper license exemptions may be required by local jurisdictions' export regulations, including EAR, for the shipment of certain U.S. Products to certain countries, including China, India, Russia, and other countries in which the company operates. Non-compliance with the EAR or other applicable export regulations can result in a wide range of penalties including the denial of export privileges, fines, criminal penalties, and the seizure of inventories. In the event that any export regulatory body determines that any shipments made by the company violate the applicable export regulations, the company could be fined significant sums and/or its export capabilities could be restricted, which could have a material adverse effect on the company's business.

Also, the company's operating income margins in the components business in the Asia/Pacific region tend to be lower than those in the other markets in which the company sells products and services. If sales in this market increased as a percentage of overall sales, consolidated operating income margins will be lower. The financial impact of lower operating income on returns on working capital is offset, in part, by lower working capital requirements. While the company has and will continue to adopt measures to reduce the potential impact of losses resulting from the risks of doing business abroad, it cannot ensure that such measures will be adequate and, therefore, could have a material adverse effect on its business.

When the company makes acquisitions, it may take on additional liabilities or not be able to successfully integrate such acquisitions.

As part of the company's history and growth strategy, it has acquired other businesses. Acquisitions involve numerous risks, including the following:

• | effectively combining the acquired operations, technologies, or products; |

• | unanticipated costs or assumed liabilities, including those associated with regulatory actions or investigations; |

• | not realizing the anticipated financial benefit from the acquired companies; |

• | diversion of management's attention; |

• | negative effects on existing customer and supplier relationships; and |

• | potential loss of key employees, especially those of the acquired companies. |

Further, the company has made, and may continue to make acquisitions of, or investments in new services, businesses or technologies to expand its current service offerings and product lines. Some of these may involve risks that may differ from those traditionally associated with the company's core distribution business, including undertaking product or service warranty responsibilities that in its traditional core business would generally reside primarily with its suppliers. If the company is not successful in mitigating or insuring against such risks, it could have a material adverse effect on the company's business.

10

The company's goodwill and identifiable intangible assets could become impaired, which could reduce the value of its assets and reduce its net income in the year in which the write-off occurs.

Goodwill represents the excess of the cost of an acquisition over the fair value of the assets acquired. The company also ascribes value to certain identifiable intangible assets, which consist primarily of customer relationships and trade names, among others, as a result of acquisitions. The company may incur impairment charges on goodwill or identifiable intangible assets if it determines that the fair values of the goodwill or identifiable intangible assets are less than their current carrying values. The company evaluates, on a regular basis, whether events or circumstances have occurred that indicate all, or a portion, of the carrying amount of goodwill or identifiable intangible assets may no longer be recoverable, in which case an impairment charge to earnings would become necessary.

Refer to Notes 1 and 3 of the Notes to the Consolidated Financial Statements and 'Critical Accounting Policies' in Management's Discussion and Analysis of Financial Condition and Results of Operations for further discussion of the impairment testing of goodwill and identifiable intangible assets.

A decline in general economic conditions or global equity valuations could impact the judgments and assumptions about the fair value of the company's businesses and the company could be required to record impairment charges on its goodwill or other identifiable intangible assets in the future, which could impact the company's consolidated balance sheet, as well as the company's consolidated statement of operations. If the company is required to recognize an impairment charge in the future, the charge would not impact the company's consolidated cash flows, current liquidity, or capital resources.

If the company fails to maintain an effective system of internal controls or discovers material weaknesses in its internal controls over financial reporting, it may not be able to report its financial results accurately or timely or detect fraud, which could have a material adverse effect on its business.

An effective internal control environment is necessary for the company to produce reliable financial reports and is an important part of its effort to prevent financial fraud. The company is required to annually evaluate the effectiveness of the design and operation of its internal controls over financial reporting. Based on these evaluations, the company may conclude that enhancements, modifications, or changes to internal controls are necessary or desirable. While management evaluates the effectiveness of the company's internal controls on a regular basis, these controls may not always be effective. There are inherent limitations on the effectiveness of internal controls, including collusion, management override, and failure in human judgment. In addition, control procedures are designed to reduce rather than eliminate financial statement risk. If the company fails to maintain an effective system of internal controls, or if management or the company's independent registered public accounting firm discovers material weaknesses in the company's internal controls, it may be unable to produce reliable financial reports or prevent fraud, which could have a material adverse effect on the company's business. In addition, the company may be subject to sanctions or investigation by regulatory authorities, such as the SEC or the NYSE. Any such actions could result in an adverse reaction in the financial markets due to a loss of confidence in the reliability of the company's financial statements, which could cause the market price of its common stock to decline or limit the company's access to capital.

Cyber security and privacy breaches may hurt the company’s business, damage its reputation, increase its costs, and cause losses.

The company’s information technology systems could be subject to invasion, cyber-attack, or data privacy breaches by employees, others with authorized access, and unauthorized persons. Such attacks could result in disruption to the company’s operations, loss or disclosure of, or damage to, the company’s or any of its customer’s or supplier’s data or confidential information. The company’s information technology systems security measures may also be breached due to employee error, malfeasance, or otherwise. Additionally, outside parties may attempt to fraudulently induce employees, customers or suppliers to disclose sensitive information in order to gain access to the company’s data and information technology systems. Any such breach could result in significant legal and financial exposure, damage to the company’s reputation, loss of competitive advantage, and a loss of confidence in the security of the company’s information technology systems that could potentially have an impact on the company’s business. Because the techniques used to obtain unauthorized access, disable or degrade, or sabotage the company’s information technology systems change frequently and often are not recognized until launched, the company may be unable to anticipate these techniques or to implement adequate preventive measures. Further, third parties, such as hosted solution providers, that provide services for the company’s operations, could also be a source of security risk in the event of a failure of their own security systems and infrastructure. In addition, sophisticated hardware and operating system software and applications that the company procures from third parties may contain defects in design or manufacture, including "bugs" and other problems that could unexpectedly interfere with the operation of the company’s information technology systems. Although the company has developed systems and processes that are designed to protect information and prevent data loss and other security breaches, including systems and processes designed

11

to reduce the impact of a security breach, such measures cannot provide absolute security. Such breaches, whether successful or unsuccessful, could result in the company incurring costs related to, for example, rebuilding internal systems, defending against litigation, responding to regulatory inquiries or actions, paying damages, or taking other remedial steps.

Also, global privacy legislation, enforcement, and policy activity are rapidly expanding and creating a complex compliance environment. The company’s failure to comply with federal, state, or international privacy related or data protection laws and regulations could result in proceedings against the company by governmental entities or others. Although the company has insurance coverage for protecting against cyber security risks, it may not be sufficient to cover all possible claims, and the company may suffer losses that could have a material adverse effect on its business.

The company relies heavily on its internal information systems, which, if not properly functioning, could materially adversely affect the company's business.

The company's current global operations reside on multiple technology platforms. The size and complexity of the company's computer systems make them potentially vulnerable to breakdown, malicious intrusion, and random attack. Because many of the company's systems consist of a number of legacy, internally developed applications, it can be harder to upgrade and may be more difficult to adapt to commercially available software.

The company is in process of implementing a global enterprise resource planning ("ERP") system to standardize its global components processes worldwide and adopt best-in-class capabilities. The conversion is substantially complete in the EMEA and Asia/Pacific regions, while the conversion in the Americas region is expected to be implemented over the next few years. The company has committed significant resources to this new ERP system, which replaces multiple legacy systems of the company. This conversion is extremely complex, in part, because of the wide range of processes and the multiple legacy systems that must be integrated globally. The company is using a controlled project plan that it believes will provide for the adequate allocation of resources. However, such a plan, or a divergence from it, may result in cost overruns, project delays, or business interruptions. During the conversion process, the company may be limited in its ability to integrate any business that it may want to acquire. Failure to properly or adequately address these issues could impact the company's ability to perform necessary business operations, which could materially adversely affect the company's business.

The company may be subject to intellectual property rights claims, which are costly to defend, could require payment of damages or licensing fees and could limit the company's ability to use certain technologies in the future.

Certain of the company's products and services include intellectual property owned primarily by the company's third party suppliers and, to a lesser extent, the company itself. Substantial litigation and threats of litigation regarding intellectual property rights exist in the semiconductor/integrated circuit, software and some service industries. From time to time, third parties (including certain companies in the business of acquiring patents not for the purpose of developing technology but with the intention of aggressively seeking licensing revenue from purported infringers) may assert patent, copyright and/or other intellectual property rights to technologies that are important to the company's business. In some cases, depending on the nature of the claim, the company may be able to seek indemnification from its suppliers for itself and its customers against such claims, but there is no assurance that it will be successful in obtaining such indemnification or that the company is fully protected against such claims. In addition, the company is exposed to potential liability for technology that it develops itself for which it has no indemnification protections. In any dispute involving products or services that incorporate intellectual property developed, licensed by the company, or obtained through acquisition, the company's customers could also become the target of litigation. The company is obligated in many instances to indemnify and defend its customers if the products or services the company sells are alleged to infringe any third party's intellectual property rights. Any infringement claim brought against the company, regardless of the duration, outcome, or size of damage award, could:

• | result in substantial cost to the company; |

• | divert management's attention and resources; |

• | be time consuming to defend; |

• | result in substantial damage awards; or |

• | cause product shipment delays. |

Additionally, if an infringement claim is successful the company may be required to pay damages or seek royalty or license arrangements, which may not be available on commercially reasonable terms. The payment of any such damages or royalties may significantly increase the company's operating expenses and harm the company's operating results and financial condition. Also, royalty or license arrangements may not be available at all. The company may have to stop selling certain products or using technologies, which could affect the company's ability to compete effectively.

12

The company may not be able to adequately anticipate, prevent or mitigate damage resulting from criminal and other illegal or fraudulent activities committed against it.

Global businesses like ours are facing increasing risks of criminal, illegal and other fraudulent acts. The evolving nature of such threats, in light of new and sophisticated methods used by criminals, including phishing, social engineering and forgery, are making it increasingly difficult for us to anticipate and adequately mitigate these risks. Although management believes internal controls are adequate to timely detect unauthorized cash disbursements so as to prevent a material misstatement of the company’s financial statements, these controls may not be adequate to safeguard the company’s cash assets from unauthorized transfers resulting from human error. In addition, designing and implementing measures to defend against, prevent and detect these types of activities are increasingly costly and invasive into the operations of the business. As a result, we could experience a material loss in the future to the extent that controls and other measures we implement to address these threats fail to prevent or detect such acts.

Compliance with government regulations regarding the use of "conflict minerals" may result in increased costs and risks to the company.

As part of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the "Act"), the SEC has promulgated disclosure requirements regarding the use of certain minerals, which are mined from the Democratic Republic of Congo and adjoining countries, known as conflict minerals. The disclosure rules were effective in May 2014. The company must publicly disclose the process it took to determine whether it manufactures (as defined in the Act) any products that contain conflict minerals. Customers typically rely on the company to provide critical data regarding the parts they purchase, including conflict mineral information. The company's material sourcing is broad-based and multi-tiered, and it is not able to easily verify the origins for conflict minerals used in all of the products it sells. The company has many suppliers and each provides conflict mineral information in a different manner, if at all. Accordingly, because the supply chain is complex, the company may face reputational challenges if it is unable to sufficiently verify the origins of conflict minerals used in its products. Additionally, customers may demand that the products they purchase be free of conflict minerals. This may limit the number of suppliers that can provide products in sufficient quantities to meet customer demand or at competitive prices.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

The company owns and leases sales offices, distribution centers, and administrative facilities worldwide. Its executive office is located in Centennial, Colorado and occupies a 129,000 square foot facility under a long-term lease expiring in 2017. The company owns 21 locations throughout the Americas, EMEA, and Asia Pacific regions and occupies approximately 450 additional locations under leases due to expire on various dates through 2026. The company believes its facilities are well maintained and suitable for company operations.

Item 3. Legal Proceedings.

Environmental and Related Matters

In connection with the purchase of Wyle in August 2000, the company acquired certain of the then outstanding obligations of Wyle, including Wyle's indemnification obligations to the purchasers of its Wyle Laboratories division for environmental clean-up costs associated with any then existing contamination or violation of environmental regulations. Under the terms of the company's purchase of Wyle from the sellers, the sellers agreed to indemnify the company for certain costs associated with the Wyle environmental obligations, among other things. As part of the settlement agreement the company accepted responsibility for any potential subsequent costs incurred related to the Wyle matters. The company is aware of two Wyle Laboratories facilities (in Huntsville, Alabama and Norco, California) at which contaminated groundwater was identified and will require environmental remediation. As further discussed in Note 15 of the Notes to the Consolidated Financial Statements, the Huntsville, Alabama site is being investigated by the company under the direction of the Alabama Department of Environmental Management. The Norco, California site is subject to a consent decree, entered in October 2003, between the company, Wyle Laboratories, and the California Department of Toxic Substance Control. In addition, the company was named as a defendant in several lawsuits related to the Norco facility and a third site in El Segundo, California which have now been settled to the satisfaction of the parties.

13

The company expects these environmental liabilities to be resolved over an extended period of time. Costs are recorded for environmental matters when it is probable that a liability has been incurred and the amount of the liability can be reasonably estimated. Accruals for environmental liabilities are adjusted periodically as facts and circumstances change, assessment and remediation efforts progress, or as additional technical or legal information becomes available. Environmental liabilities are difficult to assess and estimate due to various unknown factors such as the timing and extent of remediation, improvements in remediation technologies, and the extent to which environmental laws and regulations may change in the future. Accordingly, the company cannot presently fully estimate the ultimate potential costs related to these sites until such time as a substantial portion of the investigation at the sites is completed and remedial action plans are developed and, in some instances implemented. To the extent that future environmental costs exceed amounts currently accrued by the company, net income would be adversely impacted and such impact could be material.

As successor-in-interest to Wyle, the company is the beneficiary of various Wyle insurance policies that covered liabilities arising out of operations at Norco and Huntsville. To date, the company has recovered approximately $37.0 million from certain insurance carriers relating to environmental clean-up matters at the Norco site. The company is considering the best way to pursue its potential claims against insurers regarding liabilities arising out of operations at Huntsville. The resolution of these matters will likely take several years. The company has not recorded a receivable for any potential future insurance recoveries related to the Norco and Huntsville environmental matters, as the realization of the claims for recovery are not deemed probable at this time.

The company believes the settlement amount together with potential recoveries from various insurance policies covering environmental remediation and related litigation will be sufficient to cover any potential future costs related to the Wyle acquisition; however, it is possible unexpected costs beyond those anticipated could occur.

Tekelec Matter

In 2000, the company purchased Tekelec Europe SA ("Tekelec") from Tekelec Airtronic SA and certain other selling shareholders. Subsequent to the closing of the acquisition, Tekelec received a product liability claim in the amount of €11.3 million. The product liability claim was the subject of a French legal proceeding started by the claimant in 2002, under which separate determinations were made as to whether the products that are subject to the claim were defective and the amount of damages sustained by the purchaser. The manufacturer of the products also participated in this proceeding. The claimant has commenced legal proceedings against Tekelec and its insurers to recover damages in the amount of €3.7 million and expenses of €.3 million plus interest. In May 2012, the French court ruled in favor of Tekelec and dismissed the plaintiff's claims. In January 2015, the Court of Appeals confirmed the French court's ruling; however, the ruling remains subject to a final appeal by the plaintiff. The company believes that any amount in addition to the amount accrued by the company would not materially adversely impact the company's consolidated financial position, liquidity, or results of operations.

Antitrust Investigation

On January 21, 2014, the company received a Civil Investigative Demand in connection with an investigation by the Federal Trade Commission ("FTC") relating generally to the use of a database program (the “database program”) that has operated for more than ten years under the auspices of the Global Technology Distribution Council ("GTDC"), a trade group of which the company is a member. Under the database program, certain members of the GTDC who participate in the program provide sales data to a third party independent contractor chosen by the GTDC. The data is aggregated by the third party and the aggregated data is made available to the program participants. The company understands that other members participating in the database program have received similar Civil Investigative Demands.

In April 2014, the company responded to the Civil Investigative Demand. The Civil Investigative Demand merely sought information, and no proceedings have been instituted against any person. The company continues to believe that there has not been any conduct by the company or its employees that would be actionable under the antitrust laws in connection with its participation in the database program. Since this matter is at a preliminary stage, it is not possible to predict the potential impact, if any, of the Civil Investigative Demand or whether any actions may be instituted by the FTC against any person.

Other

From time to time, in the normal course of business, the company may become liable with respect to other pending and threatened litigation, environmental, regulatory, labor, product, and tax matters. While such matters are subject to inherent uncertainties, it is not currently anticipated that any such matters will materially impact the company's consolidated financial position, liquidity, or results of operations.

14

Item 4. Mine Safety Disclosures.

Not applicable.

15

PART II

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Market Information

The company's common stock is listed on the NYSE (trading symbol: "ARW"). The high and low sales prices during each quarter of 2015 and 2014 are as follows:

Year | High | Low | ||||

2015: | ||||||

Fourth Quarter | $ | 59.98 | $ | 51.60 | ||

Third Quarter | 59.27 | 50.79 | ||||

Second Quarter | 63.77 | 57.67 | ||||

First Quarter | 64.67 | 54.27 | ||||

2014: | ||||||

Fourth Quarter | $ | 59.43 | $ | 46.42 | ||

Third Quarter | 62.71 | 56.90 | ||||

Second Quarter | 60.81 | 54.40 | ||||

First Quarter | 58.52 | 48.82 | ||||

Record Holders

On February 1, 2016, there were approximately 1,647 shareholders of record of the company's common stock.

Dividend History

The company did not pay cash dividends on its common stock during 2015 or 2014. While from time to time the Board of Directors (the "Board") considers the payment of dividends on the common stock, the declaration of future dividends is dependent upon the company's earnings, financial condition, and other relevant factors, including debt covenants.

Equity Compensation Plan Information

The following table summarizes information, as of December 31, 2015, relating to the Omnibus Incentive Plan, which was approved by the company's shareholders and under which cash-based awards, non-qualified stock options, incentive stock options, stock appreciation rights, restricted stock, restricted stock units, performance shares, performance share units, covered employee annual incentive awards, and other stock-based awards may be granted.

Plan Category | Number of Securities to be Issued Upon Exercise of Outstanding Options, Warrants and Rights | Weighted-Average Exercise Price of Outstanding Options, Warrants and Rights | Number of Securities Remaining Available for Future Issuance | |||||||

Equity compensation plans approved by security holders | 3,607,360 | $ | 48.11 | 7,553,173 | ||||||

Total | 3,607,360 | $ | 48.11 | 7,553,173 | ||||||

16

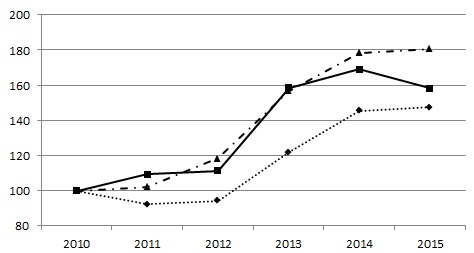

Performance Graph

The following graph compares the performance of the company's common stock for the periods indicated with the performance of the Standard & Poor's 500 Stock Index ("S&P 500 Stock Index") and the average performance of a group consisting of the company's peer companies ("Peer Group") on a line-of-business basis. The companies included in the Peer Group are Anixter International Inc., Avnet, Inc., Celestica Inc., Flextronics International Ltd., Ingram Micro Inc., Jabil Circuit, Inc., and Tech Data Corporation. The graph assumes $100 invested on December 31, 2010 in the company, the S&P 500 Stock Index, and the Peer Group. Total return indices reflect reinvestment of dividends and are weighted on the basis of market capitalization at the time of each reported data point.

2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

Arrow Electronics | 100 | 109 | 111 | 158 | 169 | 158 |

Peer Group | 100 | 92 | 94 | 122 | 145 | 147 |

S&P 500 Stock Index | 100 | 102 | 118 | 157 | 178 | 181 |

Issuer Purchases of Equity Securities

During 2014, the company's Board approved the repurchase of up to $400 million ($200 million in May and December, respectively) of the company's common stock through a share-repurchase program. In September 2015, the company's Board approved an additional repurchase of up to $400 million of the company's common stock (collectively the "Share-Repurchase Programs").

The following table shows the share-repurchase activity for the quarter ended December 31, 2015:

Month | Total Number of Shares Purchased(a) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Program(b) | Approximate Dollar Value of Shares that May Yet be Purchased Under the Program | ||||||||||

September 27 through October 31, 2015 | — | $ | — | — | $ | 469,413,591 | ||||||||

November 1 through 28, 2015 | 1,565,710 | 58.27 | 1,565,710 | 378,177,246 | ||||||||||

November 29 through December 31, 2015 | 1,055,930 | 55.49 | 1,052,281 | 319,782,917 | ||||||||||

Total | 2,621,640 | 2,617,991 | ||||||||||||

17

(a) | Includes share repurchases under the Share-Repurchase Programs and those associated with shares withheld from employees for stock-based awards, as permitted by the Omnibus Incentive Plan, in order to satisfy the required tax withholding obligations. |

(b) | The difference between the "total number of shares purchased" and the "total number of shares purchased as part of publicly announced program" for the quarter ended December 31, 2015 is 3,649 shares, which relate to shares withheld from employees for stock-based awards, as permitted by the Omnibus Incentive Plan, in order to satisfy the required tax withholding obligations. The purchase of these shares were not made pursuant to any publicly announced repurchase plan. |

18

Item 6. Selected Financial Data.

The following table sets forth certain selected consolidated financial data and must be read in conjunction with the company's consolidated financial statements and related notes appearing elsewhere in this Annual Report on Form 10-K (dollars in thousands except per share data):

For the years ended December 31: | 2015 (a) | 2014 (b) | 2013 (c) | 2012 (d) | 2011 (e) | ||||||||||||||

Sales | $ | 23,282,020 | $ | 22,768,674 | $ | 21,357,285 | $ | 20,405,128 | $ | 21,390,264 | |||||||||

Operating income | $ | 824,482 | $ | 762,257 | $ | 693,500 | $ | 804,123 | $ | 908,843 | |||||||||

Net income attributable to shareholders | $ | 497,726 | $ | 498,045 | $ | 399,420 | $ | 506,332 | $ | 598,810 | |||||||||

Net income per share: | |||||||||||||||||||

Basic | $ | 5.26 | $ | 5.05 | $ | 3.89 | $ | 4.64 | $ | 5.25 | |||||||||

Diluted | $ | 5.20 | $ | 4.98 | $ | 3.85 | $ | 4.56 | $ | 5.17 | |||||||||

At December 31: | |||||||||||||||||||

Accounts receivable and inventories | $ | 8,627,908 | $ | 8,379,107 | $ | 7,937,046 | $ | 6,976,618 | $ | 6,446,027 | |||||||||

Total assets | 13,021,930 | 12,435,301 | 12,051,562 | 10,779,737 | 9,821,563 | ||||||||||||||

Long-term debt | 2,380,575 | 2,067,898 | 2,216,811 | 1,581,528 | 1,920,307 | ||||||||||||||

Shareholders' equity | 4,142,443 | 4,153,970 | 4,180,232 | 3,983,222 | 3,668,812 | ||||||||||||||

(a) | Operating income and net income attributable to shareholders include identifiable intangible asset amortization of $51.0 million ($41.3 million net of related taxes or $.44 and $.43 per share on a basic and diluted basis, respectively), and restructuring, integration, and other charges of $68.8 million ($51.3 million net of related taxes or $.54 per share on both a basic and diluted basis). Net income attributable to shareholders includes a loss on prepayment of debt of $2.9 million ($1.8 million net of related taxes or $.02 per share on both a basic and diluted basis), a gain on sale of investment of $2.0 million ($1.7 million net of related taxes or $.02 per share on both a basic and diluted basis), and a loss on investment of $3.0 million ($1.8 million net of related taxes or $.02 per share on both a basic and diluted basis). |

(b) | Operating income and net income attributable to shareholders include identifiable intangible asset amortization of $44.1 million ($36.0 million net of related taxes or $.36 per share on both a basic and diluted basis), restructuring, integration, and other charges of $39.8 million ($29.3 million net of related taxes or $.30 and $.29 per share on a basic and diluted basis, respectively), and a non-cash impairment charge associated with discontinuing the use of a trade name of $78.0 million ($47.9 million net of related taxes or $.49 and $.48 per share on a basic and diluted basis, respectively). Net income attributable to shareholders also includes a gain on sale of investment of $29.7 million ($18.3 million net of related taxes or $.19 and $.18 per share on a basic and diluted basis, respectively). |

(c) | Operating income and net income attributable to shareholders include identifiable intangible asset amortization of $36.8 million ($29.3 million net of related taxes or $.29 and $.28 per share on a basic and diluted basis, respectively), and restructuring, integration, and other charges of $92.7 million ($65.6 million net of related taxes or $.64 and $.63 per share on a basic and diluted basis, respectively). Net income attributable to shareholders also includes a loss on prepayment of debt of $4.3 million ($2.6 million net of related taxes or $.03 per share on both a basic and diluted basis), as well as an increase in the provision of income taxes of $20.8 million ($.20 per share on both a basic and diluted basis) and interest expense of $1.6 million ($1.2 million net of related taxes or $.01 per share on both a basic and diluted basis) relating to the settlement of certain international tax matters. |

(d) | Operating income and net income attributable to shareholders include identifiable intangible asset amortization of $36.5 million ($29.3 million net of related taxes or $.27 and $.26 per share on a basic and diluted basis, respectively), restructuring, integration, and other charges of $47.4 million ($30.7 million net of related taxes or $.28 per share on both a basic and diluted basis), and a gain of $79.2 million ($48.6 million net of related taxes or $.45 and $.44 per share on a basic and diluted basis, respectively) related to the settlement of a legal matter. |

(e) | Operating income and net income attributable to shareholders include identifiable intangible asset amortization of $35.4 million ($27.1 million net of related taxes or $.24 and $.23 per share on a basic and diluted basis, respectively), |

19

restructuring, integration, and other charges of $37.8 million ($28.1 million net of related taxes or $.25 and $.24 per share on a basic and diluted basis, respectively), and a charge of $5.9 million ($3.6 million net of related taxes or $.03 per share on both a basic and diluted basis) related to the settlement of a legal matter. Net income attributable to shareholders also includes a gain on bargain purchase of $1.1 million ($.7 million net of related taxes or $.01 per share on both a basic and diluted basis), a loss on prepayment of debt of $.9 million ($.5 million net of related taxes or $.01 per share on both a basic and diluted basis), and a net reduction in the provision for income taxes of $28.9 million ($.25 per share on both a basic and diluted basis) principally due to a reversal of a valuation allowance on certain deferred tax assets.

20

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

Overview