Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - WASHINGTON FEDERAL INC | wafdex3209302015.htm |

| EX-31.2 - EXHIBIT 31.2 - WASHINGTON FEDERAL INC | wafdex31209302015.htm |

| EX-13 - EXHIBIT 13 - WASHINGTON FEDERAL INC | a9302015annualreportex13.htm |

| EX-23.1 - EXHIBIT 23.1 - WASHINGTON FEDERAL INC | wafdex231dtconsent09302015.htm |

| EX-3.1 - EXHIBIT 3.1 - WASHINGTON FEDERAL INC | wafdex31restatedarticlesof.htm |

| EX-31.1 - EXHIBIT 31.1 - WASHINGTON FEDERAL INC | wafdex31109302015.htm |

United States

Securities and Exchange Commission

Washington, D.C. 20549

____________________________________

FORM 10-K

____________________________________

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2015. | |

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | |

_____________________________________

Washington Federal, Inc.

(Exact name of registrant as specified in its charter)

_____________________________________

Washington | 91-1661606 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

425 Pike Street, Seattle, Washington 98101

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (206) 624-7930

_____________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each Class Name of each exchange on which registered

Common Stock, $1.00 par value per share NASDAQ Stock Market

Securities registered pursuant to section 12(g) of the Act:

None

____________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the registrant's common stock ("Common Stock") held on March 31, 2015, by non-affiliates was $2,046,569,111 based on the NASDAQ Stock Market closing price of $21.805 per share on that date. This is based on 93,857,790 shares of Common Stock that were issued and outstanding on this date, which excludes 1,230,504 shares held by all directors and executive officers of the Registrant.

At December 2, 2015, there were 93,038,843 shares of Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents incorporated by reference and the Part of Form 10-K into which the document is incorporated:

(1) Portions of the Registrant’s Annual Report to Stockholders for the fiscal year ended September 30, 2015, are incorporated into Part II, Items 5-8 and Part III, Item 12 of this Form 10-K.

(2) Portions of the Registrant’s definitive proxy statement for its Annual Meeting of Stockholders to be held on January 20, 2016 are incorporated into Part III, Items 10-14 of this Form 10-K.

PART I

We make statements in this Annual Report on Form 10-K that constitute forward-looking statements. Words such as “expects,” “anticipates,” “believes,” “estimates,” “intends,” “forecasts,” “projects” and other similar expressions or future or conditional verbs such as “will,” “should,” “would” and “could” are intended to help identify such forward-looking statements. These statements are not historical facts, but instead represent current expectations, plans or forecasts of the Company and are based on the beliefs and assumptions of the management of the Company and the information available to management at the time that these disclosures were prepared. The Company intends for all such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and the provisions of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements are not guarantees of future results or performance and involve certain risks, uncertainties and assumptions that are difficult to predict and often are beyond the Company's control. Actual outcomes and results may differ materially from those expressed in, or implied by, the Company's forward-looking statements.

You should not place undue reliance on any forward-looking statement and should consider the following uncertainties and risks, as well as the risks and uncertainties discussed elsewhere in this report, including under Item 1A. “Risk Factors,” and in any of the Company's other subsequent Securities and Exchange Commission filings, which could cause our future results to differ materially from the plans, objectives, goals, estimates, intentions, and expectations expressed in forward-looking statements:

• | a deterioration in economic conditions, including declines in the real estate market and home sale volumes and financial stress on borrowers as a result of the uncertain economic environment; |

• | the severe effects of the continued economic downturn, including high unemployment rates and declines in housing prices and property values, in our primary market areas; |

• | the effects of and changes in monetary and fiscal policies of the Board of Governors of the Federal Reserve System and the U.S. Government; |

• | fluctuations in interest rate risk and changes in market interest rates; |

• | the Company's ability to make accurate assumptions and judgments about the collectability of its loan portfolio, including the creditworthiness of its borrowers and the value of the assets securing these loans; |

• | the Company's ability to successfully complete merger and acquisition activities and realize expected strategic and operating efficiencies associated with such activities; |

• | legislative and regulatory limitations, including those arising under the Dodd-Frank Wall Street Reform Act and potential limitations in the manner in which we conduct our business and undertake new investments and activities; |

• | the ability of the Company to obtain external financing to fund its operations or obtain this financing on favorable terms; |

• | changes in other economic, competitive, governmental, regulatory, and technological factors affecting the Company's markets, operations, pricing, products, services and fees; |

• | the success of the Company at managing the risks involved in the foregoing and managing its business; and |

• | the timing and occurrence or non-occurrence of events that may be subject to circumstances beyond the Company's control. |

All forward-looking statements speak only as of the date on which such statements are made, and Washington Federal undertakes no obligation to update or revise any forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events, changes to future operating results over time, or the impact of circumstances arising after the date the forward-looking statement was made.

2

Item 1. | Business |

General

Washington Federal, Inc., formed in November 1994, is a Washington corporation headquartered in Seattle, Washington. The Company is a bank holding company that conducts its operations through a federally-insured national bank subsidiary, Washington Federal, National Association (“Bank”). As used throughout this document, the terms “Washington Federal” or the “Company” refer to Washington Federal, Inc. and its consolidated subsidiaries and the term "Bank" refers to the operating subsidiary Washington Federal, National Association.

The Bank is a national bank that began operations in Washington as a state-chartered mutual company in 1917. In 1935, the Company converted to a federal charter and became a member of the Federal Home Loan Bank (“FHLB”) system. On November 9, 1982, Washington Federal converted from a federal mutual to a federal capital stock savings association. On July 17, 2013, the Bank converted from a federal savings association to a national bank charter with the Office of the Comptroller of the Currency (the "OCC") and is now a national bank; at the same time, Washington Federal, which had previously been a savings and loan holding company, became a bank holding company under the Bank Holding Company Act (the "BHCA").

The Company's fiscal year end is September 30th. All references to 2015, 2014 and 2013 represent balances as of September 30, 2015, September 30, 2014 and September 30, 2013, respectively, or activity for the fiscal years then ended.

The business of the Bank consists primarily of attracting deposits from the general public and investing these funds in loans of various types, including first lien mortgages on single-family dwellings, construction loans, land acquisition and development loans, loans on multi-family and other income producing properties, home equity loans and business loans. It also invests in certain United States government and agency obligations and other investments permitted by applicable laws and regulations. Washington Federal has 247 branches located in Washington, Oregon, Idaho, Arizona, Utah, Nevada, New Mexico and Texas. Through its subsidiaries, the Company is also engaged in real estate investment and insurance brokerage activities.

The principal sources of funds for the Company's activities are retained earnings, loan repayments (including prepayments), net deposit inflows, repayments and sales of investments and borrowings. Washington Federal's principal sources of revenue are interest on loans and interest and dividends on investments. Its principal expenses are interest paid on deposits, credit costs, general and administrative expenses, interest on borrowings and income taxes.

The Company's growth has been generated both internally and as a result of 19 acquisitions. Six of those acquisitions involved government assistance in some form.

Certain branches of Bank of America, National Association. During the fiscal year 2014, the Bank acquired 74 branches from Bank of America, National Association. This included: effective as of the close of business on October 31, 2013, 11 branches located in New Mexico; effective as of the close of business on December 6, 2013, 40 branches that are located in Eastern Washington, Oregon, and Idaho; and effective as of the close of business on May 2, 2014, 23 branches that are located in Arizona and Nevada. The combined acquisitions provided $1.9 billion in deposit accounts, $13 million of loans, and $25 million in branch properties. The Bank paid a 1.99% premium on the total deposits and received $1.8 billion in cash from the transactions. The operating results of the Company include the operating results produced by the first eleven branches for the period from November 1, 2013 to September 30, 2015, for the additional forty branches from December 7, 2013 to September 30, 2015, and for the most recent twenty-three branches from May 3, 2014 to September 30, 2015.

South Valley Bancorp, Inc. Effective November 1, 2012, the Bank acquired South Valley Bancorp, Inc. and it's wholly owned subsidiary, South Valley Bank & Trust ("SVBT"), was merged into the Bank. The acquisition provided $361 million of net loans, $108 million of loans covered by an FDIC loss-sharing agreement, $736 million of deposit accounts, including $533 million in transaction deposit accounts and 24 branch locations in Central and Southern Oregon. Total consideration paid at closing was $44 million, including $34 million of Washington Federal common stock and $10 million of cash resulting from the collection of certain earn-out assets. The operating results of the Company include the operating results produced by the acquired assets and assumed liabilities for the period November 1, 2012 to September 30, 2015.

Western National Bank. Effective December 16, 2011, the Bank acquired certain assets and liabilities, including most of the loans and deposits, of Western National Bank, headquartered in Phoenix, Arizona (“WNB”) from the Federal Deposit Insurance Corporation (“FDIC”) in an FDIC assisted transaction. Under the terms of the Purchase and Assumption Agreement, the Bank and the FDIC agreed to a discount of $53 million on net assets and no loss sharing provision or premium on deposits. WNB operated three full-service offices in Arizona. The Bank acquired certain assets with a book value of $177 million, including $143 million in loans and $7 million in foreclosed real estate, and selected liabilities with a book value of $153 million, including $136 million in deposits.

3

Pursuant to the purchase and assumption agreement with the FDIC, the Company received a cash payment from the FDIC for $30 million. The operating results of the Company include the operating results produced by the acquired assets and assumed liabilities for the period December 16, 2011 to September 30, 2015.

Charter Bank. Effective October 14, 2011, the Bank acquired six branch locations, four in Albuquerque, New Mexico, and two in Santa Fe, New Mexico, from Charter Bank. The acquisition provided $255 million of deposits were acquired for a premium of $1.1 million. The operating results of the Company include the operating results produced by the assumed liabilities for the period October 14, 2011 to September 30, 2015.

The Bank is subject to extensive regulation, supervision and examination by the OCC, its primary federal regulator, the Bureau of Consumer Financial Protection ("CFPB") and the FDIC, which insures its deposits up to applicable limits. Washington Federal, as a bank holding company, is subject to extensive regulation, supervision and examination by the Board of Governors of the Federal Reserve System (" Federal Reserve"). The CFPB has broad authority to regulate providers of credit, payment and other consumer financial products and services and to bring actions to enforce federal consumer protection legislation as necessary.

The regulatory structure gives the regulatory authorities extensive discretion in connection with their supervisory and enforcement activities. Any change in such regulation, whether by the OCC, the FDIC, the Federal Reserve, the CFPB or the U.S. Congress, could have a significant impact on the Company and its operations. See “Regulation” section below.

4

Average Statements of Financial Condition | ||||||||||||||||||||||||||||||||

Year Ended September 30, | ||||||||||||||||||||||||||||||||

2015 | 2014 | 2013 | ||||||||||||||||||||||||||||||

Average Balance | Interest | Average Rate | Average Balance | Interest | Average Rate | Average Balance | Interest | Average Rate | ||||||||||||||||||||||||

(In thousands) | ||||||||||||||||||||||||||||||||

Assets | ||||||||||||||||||||||||||||||||

Loans (1) | $ | 8,598,435 | $ | 437,002 | 5.08 | % | $ | 7,997,565 | $ | 430,850 | 5.39 | % | $ | 7,818,781 | $ | 454,915 | 5.82 | % | ||||||||||||||

Mortgage-backed securities | 3,073,180 | 71,392 | 2.32 | 3,275,846 | 80,260 | 2.45 | 2,582,247 | 48,520 | 1.88 | |||||||||||||||||||||||

Investment securities (2) | 1,634,441 | 20,318 | 1.24 | 1,866,560 | 20,964 | 1.12 | 1,446,493 | 12,492 | .86 | |||||||||||||||||||||||

FHLB & FRB stock | 138,443 | 1,841 | 1.33 | 168,078 | 1,623 | .97 | 155,773 | 364 | .23 | |||||||||||||||||||||||

Total interest-earning assets | 13,444,499 | 530,553 | 3.95 | % | 13,308,049 | 533,697 | 4.01 | % | 12,003,294 | 516,291 | 4.30 | % | ||||||||||||||||||||

Other assets | 1,102,599 | 969,654 | 945,137 | |||||||||||||||||||||||||||||

Total assets | $ | 14,547,098 | $ | 14,277,703 | $ | 12,948,431 | ||||||||||||||||||||||||||

Liabilities and Stockholders’ Equity | ||||||||||||||||||||||||||||||||

Checking accounts | $ | 2,458,314 | 1,036 | .04 | % | $ | 1,888,478 | 1,259 | .07 | % | $ | 1,244,149 | 936 | .08 | % | |||||||||||||||||

Passbook and statement accounts | 659,938 | 660 | .10 | 558,146 | 607 | .11 | 377,581 | 566 | .15 | |||||||||||||||||||||||

Insured money market accounts | 2,541,137 | 3,631 | .14 | 2,323,460 | 4,574 | .20 | 1,881,866 | 4,280 | .23 | |||||||||||||||||||||||

Certificate accounts (time deposits) | 4,944,916 | 45,606 | .92 | 5,420,812 | 51,966 | .96 | 5,479,541 | 62,010 | 1.13 | |||||||||||||||||||||||

Repurchase agreements with customers | 52,382 | 121 | .23 | 46,905 | 118 | .25 | 37,913 | 111 | .29 | |||||||||||||||||||||||

FHLB advances | 1,848,904 | 66,018 | 3.57 | 1,955,205 | 69,553 | 3.56 | 1,905,479 | 68,256 | 3.58 | |||||||||||||||||||||||

Securities sold under agreements to repurchase | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||

Total interest-bearing liabilities | 12,505,591 | 117,072 | .94 | % | 12,193,006 | 128,077 | 1.05 | % | 10,926,529 | 136,159 | 1.25 | % | ||||||||||||||||||||

Other liabilities | 88,912 | 114,746 | 99,746 | |||||||||||||||||||||||||||||

Total liabilities | 12,594,503 | 12,307,752 | 11,026,275 | |||||||||||||||||||||||||||||

Stockholders’ equity | 1,952,595 | 1,969,951 | 1,922,156 | |||||||||||||||||||||||||||||

Total liabilities and stockholders’ equity | $ | 14,547,098 | $ | 14,277,703 | $ | 12,948,431 | ||||||||||||||||||||||||||

Net interest income/Interest rate spread | $ | 413,481 | 3.01 | % | $ | 405,620 | 2.96 | % | $ | 380,132 | 3.05 | % | ||||||||||||||||||||

Net interest margin (3) | 3.08 | % | 3.05 | % | 3.17 | % | ||||||||||||||||||||||||||

___________________

(1) | The average balance of loans includes nonaccruing loans and covered loans, interest on which is recognized on a cash basis. It also includes net accretion of deferred loan fees and costs of $29.7 million, $27.8 million and $26.4 million for years 2015, 2014 and 2013, respectively. |

(2) | Includes cash equivalents and non MBS investments, such as U.S. agency obligations, mutual funds, corporate bonds, and municipal bonds. |

(3) | Net interest income divided by average interest-earning assets. |

5

Lending Activities

General. The Company's net portfolio of loans totaled $9.2 billion at September 30, 2015, representing approximately 63% of its total assets. The Bank's lending activity is concentrated in the origination of loans secured by real estate, including long-term fixed-rate and adjustable-rate mortgage loans, adjustable-rate construction loans, adjustable-rate land development loans, fixed-rate and adjustable rate multi-family loans and fixed-rate and adjustable rate business loans.

The following table sets forth the composition of the Bank’s gross loan portfolio, by loan type, as of September 30 for the years indicated.

2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||||||||||||||||

Amount | % | Amount | % | Amount | % | Amount | % | Amount | % | |||||||||||||||||||||||||

(In thousands) | ||||||||||||||||||||||||||||||||||

Loans (excluding covered loans): | ||||||||||||||||||||||||||||||||||

Single-family residential | $ | 5,670,959 | 57.8 | % | $ | 5,572,244 | 92.6 | % | $ | 5,373,950 | 64.3 | % | $ | 5,779,264 | 70.2 | % | $ | 6,218,878 | 70.6 | % | ||||||||||||||

Construction – speculative (2) | 200,509 | 2.0 | 140,060 | 1.6 | 130,778 | 1.6 | 131,526 | 1.6 | 140,459 | 1.6 | ||||||||||||||||||||||||

Construction – custom (2) | 396,307 | 4.0 | 385,824 | 4.3 | 302,722 | 3.6 | 211,690 | 2.6 | 279,851 | 3.2 | ||||||||||||||||||||||||

Land – acquisition and development (1) | 96,679 | 1.0 | 80,359 | 0.9 | 81,660 | 1.0 | 128,379 | 1.6 | 200,692 | 2.3 | ||||||||||||||||||||||||

Land – consumer lot loans | 106,815 | 1.1 | 111,130 | 1.3 | 124,984 | 1.5 | 141,844 | 1.7 | 163,146 | 1.9 | ||||||||||||||||||||||||

Multi-family | 1,129,045 | 11.6 | 920,285 | 10.4 | 835,598 | 10.0 | 710,741 | 8.6 | 700,673 | 8.0 | ||||||||||||||||||||||||

Commercial Real Estate | 1,152,652 | 11.7 | 752,957 | 8.5 | 625,293 | 7.5 | 406,364 | 4.9 | 303,442 | 3.2 | ||||||||||||||||||||||||

Commercial & Industrial | 657,222 | 6.7 | 434,088 | 4.9 | 326,450 | 3.9 | 166,115 | 2.0 | 109,332 | 1.2 | ||||||||||||||||||||||||

HELOC | 139,692 | 1.4 | 134,455 | 1.5 | 133,631 | 1.6 | 126,942 | 1.5 | 115,092 | 1.2 | ||||||||||||||||||||||||

Consumer | 197,481 | 2.0 | 138,315 | 1.6 | 55,479 | 0.7 | 63,471 | 0.8 | 67,509 | 0.1 | ||||||||||||||||||||||||

Total non-covered loans | $ | 9,747,361 | 99.3 | $ | 8,669,717 | 97.6 | $ | 7,990,545 | 95.7 | $ | 7,866,336 | 95.5 | $ | 8,299,074 | 94.4 | |||||||||||||||||||

Covered loans | 75,909 | 0.7 | 213,203 | 2.4 | 362,248 | 4.3 | 373,455 | 4.5 | 495,358 | 5.6 | ||||||||||||||||||||||||

GROSS LOANS | 9,823,270 | 100.0 | % | 8,882,920 | 100.0 | % | 8,352,793 | 100.0 | % | 8,239,791 | 100.0 | % | 8,794,432 | 100.0 | % | |||||||||||||||||||

Less LIP, Allowance, net def. fees & discounts | (652,636 | ) | (558,122 | ) | (528,816 | ) | (499,417 | ) | (476,372 | ) | ||||||||||||||||||||||||

NET LOANS | $ | 9,170,634 | $ | 8,324,798 | $ | 7,823,977 | $ | 7,740,374 | $ | 8,318,060 | ||||||||||||||||||||||||

6

The following table summarizes the Company’s total loan portfolio, excluding covered loans, due for the periods indicated as of September 30, 2015 based on their contractual terms to maturity or repricing. Amounts are presented prior to deduction of discounts, premiums, loans in process, deferred net loan origination fees and allowance for loan losses.

Total | Less than 1 Year | 1 to 5 Years | After 5 Years | ||||||||||||

(In thousands) | |||||||||||||||

Single-family residential | $ | 5,670,959 | $ | 169,651 | $ | 449,015 | $ | 5,052,293 | |||||||

Construction – speculative | 200,509 | 191,989 | 6,337 | 2,183 | |||||||||||

Construction – custom | 396,307 | 308,114 | 86,323 | 1,870 | |||||||||||

Land – acquisition and development | 96,679 | 91,973 | 516 | 4,190 | |||||||||||

Land – consumer lot loans | 106,815 | 11,107 | 16,743 | 78,965 | |||||||||||

Multi-family | 1,129,045 | 138,293 | 790,064 | 200,688 | |||||||||||

Commercial real estate | 1,152,652 | 622,279 | 270,749 | 259,624 | |||||||||||

Commercial & industrial | 657,222 | 345,446 | 125,499 | 186,277 | |||||||||||

HELOC | 139,692 | 139,477 | 215 | — | |||||||||||

Consumer | 197,481 | 90,759 | 24,170 | 82,552 | |||||||||||

$ | 9,747,361 | $ | 2,109,088 | $ | 1,769,631 | $ | 5,868,642 | ||||||||

Loans maturing after one year: | |||||||||||||||

Adjustable-rate | $ | 1,606,271 | |||||||||||||

Fixed-rate | 6,032,003 | ||||||||||||||

Total | $ | 7,638,274 | |||||||||||||

The original contractual loan payment period for residential mortgage loans originated by the Company normally ranges from 15 to 30 years. Experience during recent years has indicated that, because of prepayments in connection with refinancing and sales of property, residential loans have a weighted average life of four to ten years.

Lending Programs and Policies. The Bank's principal lending activity is the origination of real estate mortgage loans to purchase or refinance single-family residences. The Bank also originates a significant number of multi-family residential and commercial loans, along with construction and land development loans. At September 30, 2015, single-family residential loans totaled $5.7 billion, or 57.8% of the Bank's gross loan portfolio; construction- speculative loans totaled $201 million, or 2.0% of the Bank's gross loan portfolio; construction - custom loans totaled $396 million, or 4.0% of the Bank's gross loan portfolio; land acquisition and development loans totaled $97 million, or 1.0% of the Bank's gross loan portfolio; land - consumer lot loans totaled $107 million, or 1.1% of the Bank's gross loan portfolio; multi-family loans totaled $1.1 billion, or 11.6% of the Bank's gross loan portfolio; commercial real estate loans totaled $1.2 billion, or 11.7% of the Bank's gross loan portfolio; commercial and industrial loans totaled $657 million, or 6.7% of the Bank's gross loan portfolio; HELOC loans totaled $140 million, or 1.4% of the Bank's gross loan portfolio and consumer loans totaled $197 million, or 2.0% of the Bank's gross loan portfolio.

Single-family residential loans. The Bank primarily originates 30 year fixed-rate loans secured by single-family residences. Moreover, it is the Bank's general policy to include in the documentation evidencing its conventional mortgage loans a due-on-sale clause, which facilitates adjustment of interest rates on such loans when the property securing the loan is sold or transferred.

All of the Bank's mortgage lending is subject to written, nondiscriminatory underwriting standards, loan origination procedures and lending policies prescribed by the Company's Board of Directors. Property valuations are required on all real estate loans. Appraisals are prepared by independent appraisers approved by the Bank's management, and reviewed by the Bank's staff. Property evaluations are sometimes utilized in lieu of appraisals on single-family real estate loans of $250,000 or less and are reviewed by the Bank's staff. Detailed loan applications are obtained to determine the borrower's ability to repay and the more significant items on these applications are verified through the use of credit reports, financial statements or written confirmations.

Depending on the size of the loan involved, a varying number of officers of the Bank must approve the application before the loan can be granted. Federal guidelines limit the amount of a real estate loan made to a specified percentage of the value of the property securing the loan, as determined by an evaluation at the time the loan is originated. This is referred to as the loan-to-value ratio. Maximum loan-to-value ratios for each type of real estate loan are established by the Company's Board of Directors.

7

When establishing general reserves for loans with loan-to-value ratios exceeding 80% that are not insured by private mortgage insurance, the Bank considers the additional risk inherent in these products, as well as their relative loan loss experience, and provides reserves when deemed appropriate. The total balance for loans with loan-to-value ratios exceeding 80% at origination as of September 30, 2015, was $529 million, with allocated reserves of $10.6 million.

Construction loans. The Bank originates construction loans to finance construction of single-family and multi-family residences as well as commercial properties. These loans to builders are generally indexed to the "prime rate" and normally have maturities of two years or less. Loans made to individuals for construction of their home generally are 30 year fixed rate loans. The Bank's policies provide that for residential construction loans, loans may be made for 85% or less of the appraised value of the property upon completion. As a result of activity over the past four decades, the Bank believes that builders of single-family residences in its primary market areas consider it to be a construction lender of choice. Because of this history, the Bank has developed a staff with in-depth land development and construction experience and working relationships with selected builders based on their operating histories and financial stability.

Construction lending involves a higher level of risk than single-family residential lending due to the concentration of principal in a limited number of loans and borrowers, and the effects of general economic conditions in the homebuilding industry. Moreover, a construction loan can involve additional risks because of the inherent difficulty in estimating both a property's value at completion of the project and the estimated cost (including interest) of the project.

Land loans. The Bank's land development loans are of a short-term nature and are generally made for 75% or less of the appraised value of the unimproved property. Funds are disbursed periodically at various stages of completion as authorized by the Company's personnel. The interest rate on these loans generally adjusts daily in accordance with a designated index.

Land development loans involve a higher degree of credit risk than long-term financing on owner-occupied real estate. Mitigation of risk of loss on a land development loan is dependent largely upon the accuracy of the initial estimate of the property's value at completion of development compared to the estimated cost (including interest) of development and the financial strength of the borrower.

The Bank's permanent land loans (also called consumer lot loans) are generally made on improved land, with the intent of building a primary or secondary residence. These loans are limited to 80% or less of the appraised value of the property, up to a maximum loan amount of $350,000. The interest rate on permanent land loans is generally fixed for 20 years.

Multi-family residential loans. Multi-family residential (five or more dwelling units) loans generally are secured by multi-family rental properties, such as apartment buildings. In underwriting multi-family residential loans, the Bank considers a number of factors, which include the projected net cash flow to the loan's debt service requirement, the age and condition of the collateral, the financial resources and income level of the borrower and the borrower's experience in owning or managing similar properties. Multi-family residential loans are originated in amounts up to 80% of the appraised value of the property securing the loan.

Loans secured by multi-family residential real estate generally involve a greater degree of credit risk than single-family residential loans and carry larger loan balances. This increased credit risk is a result of several factors, including the concentration of principal in a limited number of loans and borrowers, the effects of general economic conditions on income-producing properties, and the increased difficulty of evaluating and monitoring these types of loans. Furthermore, the repayment of loans secured by multi-family mortgages typically depends upon the successful operation of the related real estate property. If the cash flow from the project is reduced, the borrower's ability to repay the loan may be impaired. The Bank seeks to minimize these risks through its underwriting policies, which require such loans to be qualified at origination on the basis of the property's income and debt service ratio. The Bank generally limits its multi-family residential loans to $10.0 million on any one loan.

It is the Bank's policy to obtain title insurance ensuring that it has a valid first lien on the mortgaged real estate serving as collateral. Borrowers must also obtain hazard insurance prior to closing and, when required by regulation, flood insurance. Borrowers may be required to advance funds on a monthly basis, together with each payment of principal and interest, to a mortgage escrow account from which the Bank makes disbursements for items such as real estate taxes, hazard insurance premiums and private mortgage insurance premiums when due.

Commercial and industrial loans. The Bank makes various types of business loans to customers in its market area for working capital, acquiring real estate, equipment or other business purposes, such as acquisitions. The terms of these loans generally range from less than one year to a maximum of ten years. The loans are either negotiated on a fixed-rate basis or carry adjustable interest rates indexed to the Libor rate, prime rate or another market rate.

Commercial loans are based upon Management's assessment of the borrower's ability and willingness to repay along with an evaluation of secondary repayment sources such as the value and marketability of collateral. Most such loans are extended to closely held businesses and the personal guaranty of the principals is usually obtained. Commercial loans have a relatively high risk of default compared to residential real estate loans. Pricing of commercial loans is based on the credit risk of the borrower with consideration

8

given to the overall relationship of the borrower, including deposits. The acquisition of business deposits is an important focus of this business line. The Bank provides a full line of treasury management products to support the depository needs of our clients.

Consumer loans. The Bank's $197.5 million consumer loan portfolio consists of approximately $167.1 million in prime quality student loans acquired from an independent financial investment firm that retains 1% of each loan, plus various other consumer loans acquired through acquisitions. The acquired consumer loans include home improvement loans made through third party originators that bear interest at rates of 10% and higher. Due to the nature of these loans, the average charge-off rate has been 3-5% per year. After extensive review of this program, the Bank decided in fiscal 2009 to cease origination of these consumer loans, as the risk profile did not match with the Bank's long-term business plan. The Bank will continue to service the portfolio until the balances are repaid.

Home equity loans. The Bank extends revolving lines of credit to consumers that are secured by a first or second mortgage on a single family residence. The interest rates on these loans adjust monthly indexed to prime. Total loan-to-value ratios when combined with any underlying first liens are limited to 80% or less. Loan terms are a ten year draw period followed by a fifteen year amortization period.

Origination and Purchase of Loans. The Bank has general authority to lend anywhere in the United States; however, its primary lending areas are within the states of Washington, Oregon, Idaho, Arizona, Utah, Nevada, New Mexico and Texas. Loan originations come from a number of sources. Residential loan originations result from referrals from real estate brokers, walk-in customers, purchasers of property in connection with builder projects that are financed by the Bank, mortgage brokers and refinancings for existing customers. Business purpose loans are obtained primarily by direct solicitation of borrowers and ongoing relationships.

The Bank also purchases loans and mortgage-backed securities when lending rates and mortgage volume for new loan originations in its market area do not fulfill its needs. SFR loan originations, over the past few years were lower than historical levels due to the low interest rate environment and excessive government participation in the mortgage market. However, as can be seen in the table below, that trend has turned around in the last couple of years.

The table below shows total loan origination, purchase and repayment activities on loans of the Bank for the years indicated.

2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||

(In thousands) | |||||||||||||||||||

Loans originated (1): | |||||||||||||||||||

Single-family residential | $ | 705,741 | $ | 696,999 | $ | 707,310 | $ | 539,222 | $ | 557,902 | |||||||||

Construction – speculative | 263,532 | 170,539 | 173,446 | 146,494 | 126,042 | ||||||||||||||

Construction – custom | 365,220 | 359,073 | 304,156 | 210,308 | 289,113 | ||||||||||||||

Land – acquisition & development | 78,818 | 53,960 | 22,590 | 21,323 | 14,957 | ||||||||||||||

Land – consumer lot loans | 21,422 | 12,441 | 14,324 | 13,169 | 9,968 | ||||||||||||||

Multi-family | 349,442 | 239,352 | 309,636 | 189,692 | 122,618 | ||||||||||||||

Commercial real estate | 600,610 | 258,367 | 163,577 | 87,471 | 18,120 | ||||||||||||||

Commercial & industrial | 642,309 | 332,871 | 225,809 | 143,849 | 134,940 | ||||||||||||||

HELOC | 74,455 | 47,054 | 44,872 | 38,750 | 33,711 | ||||||||||||||

Consumer | 1,966 | 1,359 | 315 | — | 219 | ||||||||||||||

Total loans originated | 3,103,515 | 2,172,015 | 1,966,035 | 1,390,278 | 1,307,590 | ||||||||||||||

Loans purchased (2) | 279,936 | 211,228 | 646,408 | 129,670 | 400 | ||||||||||||||

Loan principal repayments | (2,418,547 | ) | (1,857,597 | ) | (2,353,061 | ) | (1,964,593 | ) | (1,822,128 | ) | |||||||||

Net change in loans in process, discounts, etc. (3) | (119,068 | ) | (24,825 | ) | (175,779 | ) | (133,041 | ) | (125,979 | ) | |||||||||

Net loan activity increase (decrease) | $ | 845,836 | $ | 500,821 | $ | 83,603 | $ | (577,686 | ) | $ | (640,117 | ) | |||||||

Beginning balance | $ | 8,324,798 | $ | 7,823,977 | $ | 7,740,374 | $ | 8,318,060 | $ | 8,958,177 | |||||||||

Ending balance | $ | 9,170,634 | $ | 8,324,798 | $ | 7,823,977 | $ | 7,740,374 | $ | 8,318,060 | |||||||||

___________________

(1) | Includes undisbursed loan in process and does not include savings account loans, which were not material during the periods indicated. |

(2) | Includes non-covered loans acquired through acquisitions and whole loan purchases. |

(3) Includes non-cash transactions

9

Interest Rates, Loan Fees and Service Charges. Interest rates charged by the Bank on mortgage loans are primarily determined by the competitive loan rates offered in its lending areas and in the secondary market. Mortgage loan rates reflect factors such as general interest rates, the supply of money available to the industry and the demand for such loans. These factors are in turn affected by general economic conditions, the regulatory programs and policies of federal and state agencies, changes in tax laws and governmental budgetary programs and Federal Reserve monetary policy.

The Bank receives fees for originating loans in addition to various fees and charges related to existing loans, including prepayment charges, late charges and assumption fees. In making one-to-four- family home mortgage loans, the Bank normally charges an origination fee and as part of the loan application, the borrower pays the Bank for out-of-pocket costs, such as the appraisal fee, whether or not the borrower closes the loan. The interest rate charged is normally the prevailing rate at the time the loan application is approved and accepted. In the case of construction loans, the Bank normally charges an origination fee. Loan origination fees and other terms of multi-family residential loans are individually negotiated.

Non-performing Assets. When a borrower violates a condition of a loan, the Bank attempts to cure the default by contacting the borrower. In most cases, defaults are cured promptly. If the default is not cured within an appropriate time frame, typically 90 days, the Bank may institute appropriate action to collect the loan, such as making demand for payment or initiating foreclosure proceedings on the collateral. If foreclosure occurs, the collateral will typically be sold at public auction and may be purchased by the Company.

Loans are placed on nonaccrual status when, in the judgment of management, the probability of collection of interest or principal is deemed to be insufficient to warrant further accrual. When a loan is placed on nonaccrual status, previously accrued but unpaid interest is deducted from interest income. The Bank does not accrue interest on loans 90 days past due or more. See Note A to the Consolidated Financial Statements included in Item 8 hereof for additional information.

The Company will consider modifying the interest rate and terms of a loan if it determines that a modification is deemed to be the best option available for collection in full or to minimize the loss to the Bank. Most loans restructured in troubled debt restructurings ("TDRs") are accruing and performing loans where the borrower has proactively approached the Bank about a modification due to temporary financial difficulties. Each request is individually evaluated for merit and likelihood of success. The modification of these loans is typically a payment reduction through a rate reduction of from 100 to 200 bps for a specific term, usually six to twelve months. Interest-only payments may also be approved during the modification period. Principal forgiveness generally is not an available option for restructured loans. As of September 30, 2015, single-family residential loans comprised 86% of restructured loans. The Bank reserves for restructured loans within its allowance for loan loss methodology by taking into account the following performance indicators: 1) time since modification, 2) current payment status and 3) geographic market conditions.

Real estate acquired by foreclosure or deed-in-lieu thereof (“REO” or “Real Estate Owned”) is classified as real estate held for sale until it is sold or transferred to Real Estate Held for Investment (“REHI”). When property is acquired, it is recorded at the fair market value less estimated selling costs at the date of acquisition. Interest accrual ceases on the date of acquisition and all costs incurred in maintaining the property from that date forward are expensed as incurred. Costs incurred for the improvement or development of such property are capitalized. See Note A to the Consolidated Financial Statements included in Item 8 hereof for additional information.

10

The following table sets forth information regarding restructured and non-accrual loans and REO held by the Bank at the dates indicated.

2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||

(In thousands) | |||||||||||||||||||

Performing restructured loans | $ | 289,587 | $ | 350,653 | $ | 391,415 | $ | 403,238 | $ | 320,018 | |||||||||

Non-Performing restructured loans | 13,126 | 24,090 | 24,281 | 30,040 | 57,478 | ||||||||||||||

Total restructured loans | 302,713 | 374,743 | 415,696 | 433,278 | 377,496 | ||||||||||||||

Non-accrual loans: | |||||||||||||||||||

Single-family residential | 59,074 | 74,067 | 100,460 | 131,193 | 126,624 | ||||||||||||||

Construction – speculative | 754 | 1,477 | 4,560 | 10,634 | 15,383 | ||||||||||||||

Construction – custom | 732 | — | — | 539 | 635 | ||||||||||||||

Land – Acquisition & development | — | 811 | 2,903 | 13,477 | 37,339 | ||||||||||||||

Land – consumer lot loans | 1,273 | 2,637 | 3,337 | 5,149 | 8,843 | ||||||||||||||

Multi-family | 2,558 | 1,742 | 6,573 | 4,185 | 7,664 | ||||||||||||||

Commercial real estate | 2,176 | 5,106 | 11,736 | 7,653 | 11,380 | ||||||||||||||

Commercial & industrial | — | 7 | 477 | 16 | 1,679 | ||||||||||||||

HELOC | 563 | 795 | 263 | 198 | 481 | ||||||||||||||

Consumer | 680 | 789 | 990 | 383 | 437 | ||||||||||||||

Total non-accrual loans (1) | 67,810 | 87,431 | 131,299 | 173,427 | 210,465 | ||||||||||||||

Total REO (2) | 57,191 | 55,072 | 72,925 | 80,800 | 129,175 | ||||||||||||||

Total REHI(3) | 3,576 | 4,808 | 9,392 | 18,678 | 30,654 | ||||||||||||||

Total non-performing assets | 128,577 | 147,311 | 213,616 | 272,905 | 370,294 | ||||||||||||||

Total non-performing assets and performing restructured loans | $ | 418,164 | $ | 497,964 | $ | 605,031 | $ | 676,143 | $ | 690,312 | |||||||||

Total non-performing assets and restructured loans as a percent of total assets | 2.87 | % | 3.37 | % | 4.62 | % | 5.42 | % | 5.14 | % | |||||||||

Total non-performing assets to total assets | 0.88 | % | 1.00 | % | 1.63 | % | 2.19 | % | 2.76 | % | |||||||||

___________________

(1) | Had these loans performed according to their original contract terms, the Bank would have recognized interest income of approximately $6,410,000 in 2015. In addition to the nonaccrual loans reflected in the above table, at September 30, 2015, the Bank had $99,246,928 of loans that were less than 90 days delinquent but that were classified as substandard for one or more reasons. If these loans were deemed nonperforming, the Company's ratio of total nonperforming assets and restructured loans as a percent of total assets would have been 3.55% at September 30, 2015. For a discussion of the Company's policy for placing loans on nonaccrual status, see Note A to the Consolidated Financial Statements included in Item 8 hereof. |

(2) | Total REO includes real estate held for sale acquired in settlement of loans or acquired from purchased institutions in settlement of loans. Excludes covered REO. |

(3) | Total REHI includes real estate held for investment acquired in settlement of loans. |

11

The following table analyzes the Bank’s allowance for loan losses at the dates indicated.

September 30, | |||||||||||||||||||

2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||

(In thousands) | |||||||||||||||||||

Beginning balance | $ | 114,591 | $ | 116,741 | $ | 133,147 | $ | 160,926 | $ | 163,094 | |||||||||

Charge-offs: | |||||||||||||||||||

Single-family residential | 5,524 | 8,529 | 20,947 | 53,789 | 38,465 | ||||||||||||||

Construction – speculative | 388 | 949 | 1,446 | 4,916 | 13,197 | ||||||||||||||

Construction – custom | — | — | 481 | — | 237 | ||||||||||||||

Land – Acquisition & development | 38 | 541 | 3,983 | 16,978 | 39,797 | ||||||||||||||

Land – consumer lot loans | 459 | 658 | 1,363 | 2,670 | 4,196 | ||||||||||||||

Multi-family | — | — | 1,043 | 1,393 | 1,950 | ||||||||||||||

Commercial real estate | 1,711 | 105 | 747 | 814 | 1,593 | ||||||||||||||

Commercial & industrial loans | 3,354 | 826 | 1,145 | 249 | 4,733 | ||||||||||||||

HELOC | 66 | 48 | 163 | 232 | 939 | ||||||||||||||

Consumer | 3,060 | 3,443 | 2,783 | 3,538 | 4,602 | ||||||||||||||

14,600 | 15,099 | 34,101 | 84,579 | 109,709 | |||||||||||||||

Recoveries: | |||||||||||||||||||

Single-family residential | 13,403 | 17,684 | 9,416 | 8,164 | 3,072 | ||||||||||||||

Construction – speculative | 120 | 97 | 501 | 711 | 2,143 | ||||||||||||||

Construction – custom | — | — | — | — | — | ||||||||||||||

Land – Acquisition & development | 207 | 3,071 | 4,105 | 1,341 | 2,271 | ||||||||||||||

Land – consumer lot loans | 221 | 22 | 40 | — | — | ||||||||||||||

Multi-family | 220 | — | 171 | 504 | 71 | ||||||||||||||

Commercial real estate | 735 | 33 | 17 | 225 | 328 | ||||||||||||||

Commercial & industrial loans | 1,374 | 5,043 | 95 | 2,366 | 1,925 | ||||||||||||||

HELOC | 2 | — | — | 66 | 185 | ||||||||||||||

Consumer | 3,688 | 3,513 | 2,000 | 1,480 | 1,429 | ||||||||||||||

19,970 | 29,463 | 16,345 | 14,857 | 11,424 | |||||||||||||||

Net charge-offs (recoveries) | (5,370 | ) | (14,364 | ) | 17,756 | 69,722 | 98,285 | ||||||||||||

Transfer to unfunded commitments | (175 | ) | (2,910 | ) | — | — | — | ||||||||||||

Provision for (reversal of) reserve for covered loans | (2,244 | ) | 2,244 | — | (3,766 | ) | 3,766 | ||||||||||||

Provision for (reversal of) loan loss reserve | (10,713 | ) | (15,848 | ) | 1,350 | 45,709 | 92,351 | ||||||||||||

Ending balance (1) | $ | 106,829 | $ | 114,591 | $ | 116,741 | $ | 133,147 | $ | 160,926 | |||||||||

Ratio of net charge-offs (recoveries) to average loans outstanding | (0.06 | )% | (0.18 | )% | 0.23 | % | 0.87 | % | 1.14 | % | |||||||||

___________________

(1) This does not include a reserve for unfunded commitments of $3,085,000; $2,910,000; and $3,444,000 for the years ended 2015, 2014, and 2013, respectively.

12

The following table sets forth the allocation of the Bank’s allowance for loan losses at the dates indicated.

September 30, | ||||||||||||||||||||||||||||||||||

2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||||||||||||||||

Amount | %(1) | Amount | %(1) | Amount | %(1) | Amount | %(1) | Amount | %(1) | |||||||||||||||||||||||||

(In thousands) | ||||||||||||||||||||||||||||||||||

Allowance allocation: | ||||||||||||||||||||||||||||||||||

Single-family residential | $ | 47,450 | 57.8 | % | $ | 62,763 | 62.6 | % | $ | 64,184 | 64.3 | % | $ | 81,815 | 70.2 | % | $ | 83,307 | 70.6 | % | ||||||||||||||

Construction – speculative | 6,680 | 2.0 | 6,742 | 1.6 | 8,407 | 1.6 | 12,060 | 1.6 | 13,828 | 1.6 | ||||||||||||||||||||||||

Construction – custom | 990 | 4.0 | 1,695 | 4.3 | 882 | 3.6 | 347 | 2.6 | 623 | 3.2 | ||||||||||||||||||||||||

Land – acquisition & development | 5,753 | 1.0 | 5,592 | .9 | 9,165 | 1.0 | 15,598 | 1.6 | 32,719 | 2.3 | ||||||||||||||||||||||||

Land – consumer lot loans | 2,946 | 1.1 | 3,077 | 1.3 | 3,552 | 1.5 | 4,937 | 1.7 | 5,520 | 1.9 | ||||||||||||||||||||||||

Multi-family | 5,304 | 11.6 | 4,248 | 10.4 | 3,816 | 10.0 | 5,280 | 8.6 | 7,623 | 8.0 | ||||||||||||||||||||||||

Commercial real estate | 8,953 | 11.7 | 7,548 | 8.5 | 5,595 | 7.5 | 1,956 | 4.9 | 4,331 | 3.5 | ||||||||||||||||||||||||

Commercial & industrial | 24,980 | 6.7 | 16,527 | 4.9 | 16,614 | 3.9 | 7,626 | 2.0 | 5,099 | 1.2 | ||||||||||||||||||||||||

HELOC | 835 | 1.4 | 928 | 1.5 | 1,002 | 1.6 | 965 | 1.5 | 1,139 | 1.3 | ||||||||||||||||||||||||

Consumer | 2,938 | 2.0 | 3,227 | 1.6 | 3,524 | 0.7 | 2,563 | 0.8 | 2,971 | 0.8 | ||||||||||||||||||||||||

Covered loans | — | 0.7 | 2,244 | 2.4 | — | 4.3 | — | 4.5 | 3,766 | 5.6 | ||||||||||||||||||||||||

Unallocated | — | — | — | — | — | |||||||||||||||||||||||||||||

Total allowance for loan losses (2) | $ | 106,829 | 100 | % | $ | 114,591 | 100 | % | $ | 116,741 | 100 | % | $ | 133,147 | 100 | % | $ | 160,926 | 100 | % | ||||||||||||||

___________________

(1) | Represents the total amount of the loan category as a percentage of total loans outstanding. |

(2) | This does not include a reserve for unfunded commitments of $3,085,000; $2,910,000; and $3,444,000 for the years ended 2015, 2014, and 2013, respectively. |

The Bank maintains an allowance for loan losses to absorb losses inherent in the loan portfolio. The amount of this allowance is based on ongoing, quarterly assessments of the probable and estimable losses inherent in the loan portfolio. The Bank’s method for assessing the appropriateness of the allowance is to apply a loss percentage factor to the different loan types. The loss percentage factor is made up of two parts - the historical loss factor (“HLF”) and the qualitative loss factor (“QLF”). The HLF takes into account historical charge-offs by loan type. The Company uses an average of historical loss rates for each loan category multiplied by a loss emergence period. The QLF are based on management's continuing evaluation of the pertinent factors underlying the quality of the loan portfolio, including changes in the size and composition of the loan portfolio, actual loan loss experience, current economic conditions, collateral values, geographic concentrations, seasoning of the loan portfolio, specific industry conditions, and the duration of the current business cycle. These factors are considered by loan type. Specific allowances are established in cases where management has identified conditions or circumstances related to a loan that management believes indicate the probability that a loss has been incurred. The Bank has also established a reserve for unfunded commitments.

As part of the process for determining the adequacy of the allowance for loan losses, management reviews the loan portfolio for specific weaknesses and considers the above mentioned factors. The recovery of the carrying value of loans is susceptible to future market conditions beyond the Bank's control, which may result in losses or recoveries differing from those provided. In those cases, a portion of the allowance is then allocated to reflect the estimated loss exposure.

13

Investment Activities

As a national association, the Bank is obligated to maintain adequate liquidity and does so by holding cash and cash equivalents and by investing in securities. These investments may include, among other things, certain certificates of deposit, repurchase agreements, bankers’ acceptances, loans to financial institutions whose deposits are federally-insured, federal funds, United States government and agency obligations and mortgage-backed securities.

The following table sets forth the composition of the Bank’s investment portfolio at the dates indicated.

September 30, | |||||||||||||||||||||||

2015 | 2014 | 2013 | |||||||||||||||||||||

Amortized Cost | Fair Value | Amortized Cost | Fair Value | Amortized Cost | Fair Value | ||||||||||||||||||

(In thousands) | |||||||||||||||||||||||

U.S. government and agency obligations | $ | 486,968 | $ | 482,464 | $ | 729,299 | $ | 731,943 | $ | 534,792 | $ | 533,975 | |||||||||||

Mutual Fund Investments | 100,422 | 101,952 | 100,500 | 101,387 | 100,500 | 101,237 | |||||||||||||||||

Corporate Bonds | 506,172 | 505,800 | 505,741 | 509,007 | 449,750 | 452,015 | |||||||||||||||||

State and political subdivisions | 23,970 | 27,123 | 20,402 | 23,681 | 20,422 | 22,545 | |||||||||||||||||

Agency pass-through certificates | 2,788,003 | 2,797,938 | 3,109,904 | 3,083,726 | 2,900,066 | 2,834,025 | |||||||||||||||||

Other commercial MBS | 103,131 | 102,706 | 98,851 | 98,916 | — | — | |||||||||||||||||

$ | 4,008,666 | $ | 4,017,983 | $ | 4,564,697 | $ | 4,548,660 | $ | 4,005,530 | $ | 3,943,797 | ||||||||||||

The investment portfolio at September 30, 2015 was categorized by maturity as follows:

Amortized Cost | Wtd Avg Yield | |||||

(In thousands) | ||||||

Due in less than 1 year | $ | 25,287 | 0.55 | % | ||

Due after 1 year through 5 years | 518,707 | 1.25 | ||||

Due after 5 years through 10 years | 220,374 | 1.51 | ||||

Due after 10 years | 3,244,298 | 2.74 | ||||

$ | 4,008,666 | 2.47 | % | |||

Sources of Funds

General. Deposits are the primary source of the Bank’s funds for use in lending and other general business purposes. In addition to deposits, Washington Federal derives funds from loan repayments, advances from the FHLB, other borrowings, and from investment repayments and sales. Loan repayments are a relatively stable source of funds, while deposit inflows and outflows are influenced by general interest rates, money market conditions, the availability of FDIC insurance and the market perception of the Company’s financial stability. Borrowings may be used on a short-term basis to compensate for reductions in normal sources of funds, such as deposit inflows at lower than projected levels. Borrowings may also be used on a longer-term basis to support expanded activities and to manage interest rate risk.

Deposits. The Bank relies on a mix of deposit types, including business and personal checking accounts, term certificates of deposit, and other savings deposit alternatives that have no fixed term, such as money market accounts and passbook savings accounts The Bank offers several consumer checking account products, both interest bearing and non-interest bearing. Three business checking accounts are offered. Two are targeted to small businesses with relatively simple and straightforward banking needs. Larger, more complex business depositors are provided with an account that prices monthly based on the volume and type of activity. Savings and money market accounts are offered to both businesses and consumers, with interest paid after certain threshold amounts are exceeded.

Certificates with a maturity of one year or less have penalties for premature withdrawal equal to 90 days of interest. When the maturity is greater than one year but less than four years, the penalty is 180 days of interest. When the maturity is greater than four years, the penalty is 365 days interest. Early withdrawal penalties during 2013, 2014 and 2015 amounted to approximately $548,000, $552,000 and $546,000, respectively.

14

The Bank’s deposits are obtained primarily from residents of Washington, Oregon, Idaho, Arizona, Utah, Nevada, New Mexico and Texas. The Bank does not advertise for deposits outside of these states.

The following table sets forth certain information relating to the Company’s deposits at the dates indicated.

September 30, | |||||||||||||||||||

2015 | 2014 | 2013 | |||||||||||||||||

Amount | Rate | Amount | Rate | Amount | Rate | ||||||||||||||

(In thousands) | (In thousands) | (In thousands) | |||||||||||||||||

Balance by interest rate: | |||||||||||||||||||

Checking accounts | $2,555,766 | .06 | % | $2,331,170 | .06 | % | $1,247,885 | .08 | % | ||||||||||

Passbook and statement accounts | 700,794 | .10 | 622,546 | .10 | 404,937 | .15 | |||||||||||||

Money market accounts | 2,564,318 | .13 | 2,536,971 | .18 | 1,888,020 | .23 | |||||||||||||

5,820,878 | 5,490,687 | 3,540,842 | |||||||||||||||||

Fixed-rate certificates: | |||||||||||||||||||

Under 2.00% | 4,303,475 | 4,524,158 | 4,716,427 | ||||||||||||||||

2.00% to 2.99% | 501,409 | 602,683 | 631,256 | ||||||||||||||||

3.00% to 3.99% | 5,156 | 98,610 | 175,549 | ||||||||||||||||

4.00% to 4.99% | 150 | 146 | 25,335 | ||||||||||||||||

5.00% to 5.99% | 635 | 644 | 862 | ||||||||||||||||

4,810,825 | 5,226,241 | 5,549,429 | |||||||||||||||||

$ | 10,631,703 | $ | 10,716,928 | $ | 9,090,271 | ||||||||||||||

The following table sets forth, by various interest rate categories, the amount of certificates of deposit of the Company at September 30, 2015, which mature during the periods indicated.

Maturing in | |||||||||||||||||||||||||||

1 to 3 Months | 4 to 6 Months | 7 to 12 Months | 13 to 24 Months | 25 to 36 Months | 37 to 60 Months | Total | |||||||||||||||||||||

(In thousands) | |||||||||||||||||||||||||||

Fixed-rate certificates: | |||||||||||||||||||||||||||

Under 2.00% | $ | 895,807 | $ | 944,771 | $ | 849,548 | $ | 744,034 | $ | 318,816 | $ | 550,499 | $ | 4,303,475 | |||||||||||||

2.00% to 2.99% | 34,772 | 35,683 | 101,306 | 323,727 | 1,730 | 4,191 | 501,409 | ||||||||||||||||||||

3.00 to 3.99% | 28 | 118 | 47 | 996 | 68 | 3,899 | 5,156 | ||||||||||||||||||||

4.00 to 4.99% | — | 69 | 52 | 14 | 3 | 12 | 150 | ||||||||||||||||||||

5.00 to 5.99% | — | — | 111 | 22 | 500 | 2 | 635 | ||||||||||||||||||||

Total | $ | 930,607 | $ | 980,641 | $ | 951,064 | $ | 1,068,793 | $ | 321,117 | $ | 558,603 | $ | 4,810,825 | |||||||||||||

Historically, a significant number of certificate holders roll over their balances into new certificates of the same term at the Bank’s then current rate. To ensure a continuity of this trend, the Bank expects to continue to offer market rates of interest. Its ability to retain maturing deposits in certificate accounts is difficult to project; however, the Bank is confident that by competitively pricing these certificates, levels deemed appropriate by management can be achieved on a continuing basis.

At September 30, 2015, the Bank had $420,963,000 of certificates of deposit in amounts of $250,000 or more outstanding, maturing as follows: $71,093,000 within 3 months; $112,670,000 over 3 months through 6 months; $30,464,000 over 6 months through 12 months; and $206,736,000 thereafter.

15

The following table sets forth the customer account and customer repurchase activities of the Company for the years indicated.

September 30, | |||||||||||

2015 | 2014 | 2013 | |||||||||

(In thousands) | |||||||||||

Deposits | $ | 3,770,598 | $ | 3,995,756 | $ | 3,568,826 | |||||

Acquired deposits | — | 1,853,798 | 735,000 | ||||||||

Withdrawals | (3,906,877 | ) | (4,281,421 | ) | (3,858,076 | ) | |||||

Net increase (decrease) in deposits before interest credited | (136,279 | ) | 1,568,133 | 445,750 | |||||||

Interest credited | 51,054 | 58,524 | 67,903 | ||||||||

Net increase (decrease) in customer accounts | $ | (85,225 | ) | $ | 1,626,657 | $ | 513,653 | ||||

Borrowings. The Bank obtains advances from the FHLB upon the security of the FHLB capital stock it owns and certain of its loans, provided certain standards related to credit worthiness have been met. See “Regulation-Washington Federal-Federal Home Loan Bank System” below. Such advances are made pursuant to several different credit programs. Each credit program has its own interest rate and range of maturities, and the FHLB prescribes acceptable uses to which the advances pursuant to each program may be put, as well as limitations on the size of such advances. Depending on the program, such limitations are based either on a fixed percentage of assets or the Company's credit worthiness. The FHLB is required to review its credit limitations and standards at least annually. FHLB advances have, from time to time, been available to meet seasonal and other withdrawals of savings accounts and to expand the Bank's lending program. The Company had $1.8 billion of FHLB advances outstanding at September 30, 2015.

The Bank may need to borrow funds for short periods of time to meet day-to-day financing needs. In these instances, funds are borrowed from other financial institutions or the Federal Reserve, for periods generally ranging from one to seven days at the then current borrowing rate. At September 30, 2015, the Bank had no such short-term borrowings.

The Bank also offers two forms of repurchase agreements to its customers. One form has an interest rate that floats like that of a money market deposit account. The other form has a fixed rate and is offered in a minimum denomination of $100,000. Both forms are fully collateralized by securities. These obligations are not insured by FDIC and are classified as borrowings for regulatory purposes. The Bank had $56.3 million of such agreements outstanding at September 30, 2015.

16

The following table presents certain information regarding borrowings of the Bank for the years indicated.

September 30, | |||||||||||

2015 | 2014 | 2013 | |||||||||

(In thousands) | |||||||||||

FHLB advances: | |||||||||||

Average balance outstanding | $ | 1,848,904 | $ | 1,955,205 | $ | 1,905,479 | |||||

Maximum amount outstanding at any month-end during the period | 1,930,000 | 2,083,226 | 1,930,000 | ||||||||

Weighted-average interest rate during the period (1) | 3.57 | % | 3.56 | % | 3.57 | % | |||||

Securities sold to customers under agreements to repurchase: | |||||||||||

Average balance outstanding | $ | 52,382 | $ | 46,905 | $ | 37,913 | |||||

Maximum amount outstanding at any month-end during the period | 62,315 | 51,615 | 46,128 | ||||||||

Weighted-average interest rate during the period (1) | 0.23 | % | 0.25 | % | 0.29 | % | |||||

Total average borrowings: | $ | 1,901,286 | $ | 2,002,110 | $ | 1,943,392 | |||||

Weighted-average interest rate on total average borrowings (1) | 3.48 | % | 3.42 | % | 3.51 | % | |||||

___________________

(1) | Interest expense divided by average daily balances. |

Other Ratios

The following table sets forth certain ratios related to the Company for the periods indicated.

September 30, | ||||||||

2015 | 2014 | 2013 | ||||||

Return on assets (1) | 1.10 | % | 1.10 | % | 1.17 | % | ||

Return on equity (2) | 8.21 | 7.99 | 7.88 | |||||

Average equity to average assets | 13.42 | 13.80 | 14.84 | |||||

Dividend payout ratio (3) | 32.14 | 26.45 | 24.83 | |||||

___________________

(1) | Net income divided by average total assets. |

(2) | Net income divided by average equity. |

(3) | Dividends paid per share divided by net income per share. |

17

Rate/Volume Analysis

The table below sets forth certain information regarding changes in interest income and interest expense of the Company for the years indicated. For each category of interest-earning asset and interest-bearing liability, information is provided on changes attributable to: (1) changes in volume (changes in volume multiplied by old rate) and (2) changes in rate (changes in rate multiplied by old average volume). The change in interest income and interest expense attributable to changes in both volume and rate has been allocated proportionately to the change due to volume and the change due to rate.

September 30, | |||||||||||||||||||||||||||||||||||

2015 vs. 2014 Increase (Decrease) Due to | 2014 vs. 2013 Increase (Decrease) Due to | 2013 vs. 2012 Increase (Decrease) Due to | |||||||||||||||||||||||||||||||||

Volume | Rate | Total | Volume | Rate | Total | Volume | Rate | Total | |||||||||||||||||||||||||||

(In thousands) | (In thousands) | (In thousands) | |||||||||||||||||||||||||||||||||

Interest income: | |||||||||||||||||||||||||||||||||||

Loan portfolio | $ | 30,507 | $ | (24,355 | ) | $ | 6,152 | $ | 10,399 | $ | (34,464 | ) | $ | (24,065 | ) | $ | (11,925 | ) | $ | (17,993 | ) | $ | (29,918 | ) | |||||||||||

Mortgage-backed securities | (4,941 | ) | (3,927 | ) | (8,868 | ) | 15,032 | 16,708 | 31,740 | (15,610 | ) | (32,012 | ) | (47,622 | ) | ||||||||||||||||||||

Investments (1) | (2,594 | ) | 2,166 | (428 | ) | 4,291 | 5,440 | 9,731 | 2,370 | 1,190 | 3,560 | ||||||||||||||||||||||||

All interest-earning assets | 22,972 | (26,116 | ) | (3,144 | ) | 29,722 | (12,316 | ) | 17,406 | (25,165 | ) | (48,815 | ) | (73,980 | ) | ||||||||||||||||||||

Interest expense: | |||||||||||||||||||||||||||||||||||

Customer accounts | 1,879 | (9,349 | ) | (7,470 | ) | 8,670 | (18,049 | ) | (9,379 | ) | 2,673 | (21,709 | ) | (19,036 | ) | ||||||||||||||||||||

FHLB advances and other borrowings | (3,358 | ) | (177 | ) | (3,535 | ) | 2,340 | (1,043 | ) | 1,297 | (26,997 | ) | (11,057 | ) | (38,054 | ) | |||||||||||||||||||

All interest-bearing liabilities | (1,479 | ) | (9,526 | ) | (11,005 | ) | 11,010 | (19,092 | ) | (8,082 | ) | (24,324 | ) | (32,766 | ) | (57,090 | ) | ||||||||||||||||||

Change in net interest income | $ | 24,451 | $ | (16,590 | ) | $ | 7,861 | $ | 18,712 | $ | 6,776 | $ | 25,488 | $ | (841 | ) | $ | (16,049 | ) | $ | (16,890 | ) | |||||||||||||

___________________

(1) | Includes interest on cash equivalents and dividends on stock of the FHLB of Des Moines and FRB of San Francisco. |

18

Interest Rate Risk

The primary source of income for the Company is net interest income, which is the difference between the interest income generated by our interest-earning assets and the interest expense incurred for our interest-bearing liabilities. The level of net interest income is a function of the average balances of our interest-earning assets and liabilities and the spread between the yield on such assets and the cost of such liabilities. These factors are influenced by both the pricing and mix of our interest-earning assets and our interest-bearing liabilities. Typically, if the interest rates on our interest-bearing liabilities increase at a faster pace than the interest rates on our interest-earning assets, the result could be a reduction in net interest income and with it, a reduction in our earnings.

During the past year, interest rates on our earning assets and our interest-bearing liabilities have both declined. The rates on earning assets have declined 6 bps which is less than the reduction in costs of interest-bearing liabilities of 10 bps, so the net interest margin has increased to 3.08% compared to 3.05% in the prior year.

Interest rate risk arises in part due to the Bank's significant holdings of fixed-rate single-family home loans, which are longer-term than the customer accounts that constitute its primary liabilities. Accordingly, assets do not usually respond as quickly to changes in interest rates as liabilities. In the absence of action by Management, net interest income can be expected to decline when interest rates rise and to expand when interest rates fall. Shortening the maturity or repricing of the investment portfolio is one action that management can take. The composition of the investment portfolio was 41% variable rate and 59% fixed rate as of September 30, 2015 to provide some protection against the potential for rising rates. In addition, the Bank is producing more short term or variable rate loans and has increased less rate sensitive transaction accounts to 45% of the deposit portfolio.

The Company's balance sheet strategy, in conjunction with low operating costs, has allowed the Company to manage interest rate risk, within guidelines established by the Board of Directors, through all interest rate cycles. Although a significant change in market interest rates could adversely affect net interest income of the Company, the Company's interest rate risk approach has never resulted in the recording of a monthly operating loss. It is management's objective to grow the dollar amount of net interest income, through the rate cycles, acknowledging that there will be some periods of time when that will not be feasible.

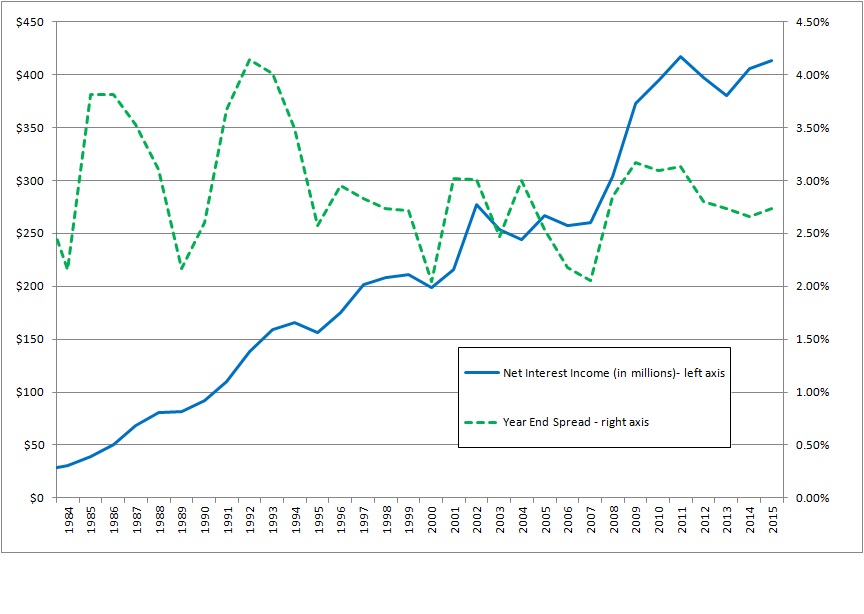

The chart below shows the volatility of our period end net interest spread (dotted line which is measured against the right axis) compared to the relatively consistent growth in net interest income (solid line which is measured against the left axis). As noted above, this consistency is accomplished by managing the size and composition of the balance sheet through different rate cycles.

19

The following table shows the estimated repricing periods for earning assets and paying liabilities.

Repricing Period | |||||||||||||||

Within One Year | After 1 year - before 6 Years | Thereafter | Total | ||||||||||||

As of September 30, 2015 | (In thousands) | ||||||||||||||

Earning Assets (1) | $ | 4,857,276 | $ | 4,730,256 | $ | 3,925,481 | $ | 13,513,013 | |||||||

Paying Liabilities | (6,804,769 | ) | (3,619,159 | ) | (2,043,780 | ) | (12,467,708 | ) | |||||||

Excess (Liabilities) Assets | $ | (1,947,493 | ) | $ | 1,111,097 | $ | 1,881,701 | ||||||||

Excess as % of Total Assets | (13.40 | )% | |||||||||||||

Policy limit for one year excess | (20.00 | )% | |||||||||||||

(1) Asset repricing period includes estimated prepayments based on historical activity

At September 30, 2015, the Company had approximately $1.9 billion more liabilities than assets subject to repricing in the next year, which amounted to a negative maturity gap of 13.40% of total assets, approximately the same gap as the prior year. The excess of liabilities relative to assets that will be repricing within the next year subjects the Company to decreasing net interest income should interest rates rise. However, if management were to take steps to change the size and/or mix of the balance sheet or slow the repricing of deposit rates upward, rising rates might not cause a decrease in net interest income.

The following table shows the potential impact of rising interest rates on net income for one year. The Bank's focus is primarily on the impact of rising rates, given the negative gap position which implies that generally when rates fall income should increase and when rates increase income is at risk to decrease (assuming no change in the size or composition of the balance sheet).

It is important to note that this is not a forecast or prediction of future events, but is used as a tool for measuring potential risk. This analysis assumes zero balance sheet growth and a constant percentage composition of assets and liabilities.

Potential Impact on Net Income | |||||||

Basis Point Increase in Interest Rates | As of 09/30/15 | As of 09/30/14 | |||||

(In thousands) | |||||||

100 | $ | (413 | ) | $ | 448 | ||

200 | (9,288 | ) | (6,190 | ) | |||

300 | (22,292 | ) | (14,745 | ) | |||

Actual results will differ from the assumptions used in this model, as management monitors and adjusts both the size and the composition of the balance sheet in order to respond to changing interest rates. In a rising rate environment, it is likely that the Company will grow its balance sheet to offset margin compression that may occur. Improvement in the net income sensitivity during the year are the result of changing our loan and deposit mix toward shorter term and/or floating rate instruments.

20

Another method used to quantify interest rate risk is the net portfolio value (“NPV”) analysis. This analysis calculates the difference between the present value of interest-bearing liabilities and the present value of expected cash flows from interest-earning assets and off-balance-sheet contracts. The following tables set forth an analysis of the Company’s interest rate risk as measured by the estimated changes in NPV resulting from instantaneous and sustained parallel shifts in the yield curve (measured in 100-basis-point increments). The improvement in the net portfolio value sensitivity during the year is due to shorter estimated lives of our assets and a higher beginning net portfolio value position. Comparing the NPV with no change in interest rates from September 30, 2015 to the prior year end, NPV decreased $27.3 million or 1%.

These are expressed as a percentage of assets in the table below.

September 30, 2015

Change in Interest Rates | Estimated NPV Amount | Estimated (Decrease) in NPV Amount | NPV as % of Assets | ||||||||||

(Basis Points) | (In thousands) | (In thousands) | |||||||||||

300 | $ | 1,852,417 | $ | (874,372 | ) | 14.03 | % | ||||||

200 | 2,190,841 | (535,948 | ) | 15.91 | |||||||||

100 | 2,500,300 | (226,490 | ) | 17.45 | |||||||||

No change | 2,726,790 | — | 18.39 | ||||||||||

September 30, 2014

Change in Interest Rates | Estimated NPV Amount | Estimated (Decrease) in NPV Amount | NPV as % of Assets | ||||||||||

(Basis Points) | (In thousands) | (In thousands) | |||||||||||

300 | $ | 1,803,038 | $ | (954,076 | ) | 13.68 | % | ||||||

200 | 2,158,694 | (598,421 | ) | 15.68 | |||||||||

100 | 2,448,453 | (268,661 | ) | 17.35 | |||||||||

No change | 2,754,114 | — | 18.53 | ||||||||||

As of September 30, 2015 and 2014, the Company was in compliance with all of its interest rate risk policy guidelines.

Subsidiaries

Washington Federal, Inc. is a bank holding company that conducts its primary business through its only directly-owned subsidiary, the Bank. The Bank has a national bank charter with the OCC. The Bank has four active wholly owned subsidiaries which are discussed further below.

WAFD Insurance Group, Inc. is incorporated under the laws of the state of Washington and is an insurance agency that offers a full line of individual and business insurance policies to customers of the Company, as well as to the general public.

Statewide Mortgage Services Company is incorporated under the laws of the state of Washington. It holds and markets real estate held for investment. As of September 30, 2015, Statewide Mortgage Services held $3,576,000 of real estate held for investment and $10,555,886 of property and land.

Washington Services, Inc. is incorporated under the laws of the state of Washington. It holds certain branch properties and equipment and also acts as a trustee under deeds of trust as to which the Bank is beneficiary. As of September 30, 2015, Washington Services, Inc. held $199,246 of property and equipment.

First Mutual Sales Finance, Inc.is incorporated under the laws of the State of Delaware. It services consumer loans. The Board of Directors of the Company have approved the merger of this wholly owned subsidiary into the Bank effective November 13, 2015 subject to regulatory approval.

21

Employees

As of September 30, 2015, the Company had approximately 1,838 employees, including the full-time equivalent of 41 part-time employees and its service corporation employees. None of these employees are represented by a collective bargaining agreement, and the Company has enjoyed harmonious relations with its personnel.

Regulation

Set forth below is a brief description of certain laws and regulations that relate to the regulation of the Company and the Bank. The description of these laws and regulations, and descriptions of laws and regulations contained elsewhere herein, do not purport to be complete and are qualified in their entirety by reference to applicable laws and regulations. Certain federal banking laws were amended by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”).

The Company

General. The Company is registered as a bank holding company and is subject to Federal Reserve regulation, examination, supervision and reporting requirements.