Attached files

| file | filename |

|---|---|

| EX-32 - CERTIFICATION - IMMUCELL CORP /DE/ | f10q0915ex32_immucell.htm |

| EX-31 - CERTIFICATION - IMMUCELL CORP /DE/ | f10q0915ex31_immucell.htm |

| EX-10.1 - SUPPLY AGREEMENT BETWEEN THE COMPANY AND PLAS-PAK INDUSTRIES, INC. DATED AS OF OCTOBER 14, 2015. - IMMUCELL CORP /DE/ | f10q0915ex10i_immucell.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2015

001-12934

(Commission file number)

ImmuCell Corporation

(Exact name of registrant as specified in its charter)

| Delaware | 01-0382980 | |

| (State of Incorporation) | (I.R.S. Employer Identification No.) |

|

| 56 Evergreen Drive, Portland, ME | 04103 | |

| (Address of principal executive office) | (Zip Code) |

(207) 878-2770

(Registrant's telephone number)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | Non-accelerated filer ☐ | Smaller reporting company ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of shares of the Registrant’s common stock outstanding at November 9, 2015 was 3,055,034.

ImmuCell Corporation

TABLE OF CONTENTS

September 30, 2015

PART I: FINANCIAL INFORMATION

| ITEM 1. | Financial Statements | |

| Balance Sheets as of September 30, 2015 and December 31, 2014 | 2 | |

| Statements of Operations for the three-month and nine-month periods ended September 30, 2015 and 2014 | 3 | |

| Statements of Comprehensive Income (Loss) for the three-month and nine-month periods ended September 30, 2015 and 2014 | 4 | |

| Statements of Stockholders’ Equity for the nine-month periods ended September 30, 2015 and 2014 | 5 | |

| Statements of Cash Flows for the nine-month periods ended September 30, 2015 and 2014 | 6 | |

| Notes to Unaudited Financial Statements | 7-15 | |

| ITEM 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 16-24 |

| ITEM 3. | Quantitative and Qualitative Disclosures about Market Risk | 25 |

| ITEM 4. | Controls and Procedures | 25 |

| PART II: OTHER INFORMATION | ||

| ITEMS 1 THROUGH 6 | 26-32 | |

| Signature | 33 | |

| - 1 - |

ImmuCell Corporation

PART

1. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

BALANCE SHEETS

| (Unaudited)

As of September 30, 2015 | As

of December 31, 2014 | |||||||

| ASSETS | ||||||||

| CURRENT ASSETS: | ||||||||

| Cash and cash equivalents | $ | 2,469,087 | $ | 850,028 | ||||

| Short-term investments | 3,720,000 | 2,489,000 | ||||||

| Accounts receivable, net | 789,214 | 1,005,292 | ||||||

| Inventory | 864,444 | 945,755 | ||||||

| Prepaid expenses and other assets | 275,559 | 148,399 | ||||||

| Current portion of deferred tax asset | 69,011 | 30,463 | ||||||

| Total current assets | 8,187,315 | 5,468,937 | ||||||

| PROPERTY, PLANT AND EQUIPMENT, net | 4,955,614 | 3,837,647 | ||||||

| LONG-TERM INVESTMENTS | 487,000 | 496,000 | ||||||

| LONG-TERM PORTION OF DEFERRED TAX ASSET | 543,602 | 1,230,340 | ||||||

| OTHER ASSETS, net | 49,615 | 18,930 | ||||||

| TOTAL ASSETS | $ | 14,223,146 | $ | 11,051,854 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| CURRENT LIABILITIES: | ||||||||

| Accounts payable and accrued expenses | $ | 545,927 | $ | 851,677 | ||||

| Current portion of bank debt | 133,959 | 150,382 | ||||||

| Deferred revenue | 0 | 6,690 | ||||||

| Total current liabilities | 679,886 | 1,008,749 | ||||||

| LONG-TERM LIABILITIES: | ||||||||

| Long-term portion of bank debt | 3,126,004 | 745,920 | ||||||

| Interest rate swaps | 118,773 | 38,817 | ||||||

| Total long-term liabilities | 3,244,777 | 784,737 | ||||||

| TOTAL LIABILITIES | 3,924,663 | 1,793,486 | ||||||

| STOCKHOLDERS’ EQUITY: | ||||||||

| Common stock, $0.10 par value per share, 8,000,000 shares authorized, 3,261,148 shares issued as of September 30, 2015 and December 31, 2014 | 326,115 | 326,115 | ||||||

| Capital in excess of par value | 10,144,794 | 10,042,305 | ||||||

| Accumulated surplus (deficit) | 349,865 | (574,567 | ) | |||||

| Treasury stock, at cost, 206,114 and 234,114 shares as of September 30, 2015 and December 31, 2014, respectively | (450,901 | ) | (512,154 | ) | ||||

| Accumulated other comprehensive loss | (71,390 | ) | (23,331 | ) | ||||

| Total stockholders’ equity | 10,298,483 | 9,258,368 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 14,223,146 | $ | 11,051,854 | ||||

The accompanying notes are an integral part of these financial statements.

| - 2 - |

ImmuCell Corporation

(Unaudited)

STATEMENTS OF OPERATIONS

For the Three-Month Periods Ended | For the Nine-Month Periods Ended | |||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| Product sales | $ | 2,472,428 | $ | 1,770,129 | $ | 7,534,281 | $ | 5,391,599 | ||||||||

| Costs of goods sold | 860,526 | 692,233 | 2,940,881 | 2,285,285 | ||||||||||||

| Gross margin | 1,611,902 | 1,077,896 | 4,593,400 | 3,106,314 | ||||||||||||

| Sales and marketing expenses | 381,740 | 373,595 | 1,086,928 | 921,588 | ||||||||||||

| Administrative expenses | 301,566 | 302,216 | 941,417 | 873,866 | ||||||||||||

| Product development expenses | 301,746 | 361,232 | 904,170 | 1,716,114 | ||||||||||||

| Operating expenses | 985,052 | 1,037,043 | 2,932,515 | 3,511,568 | ||||||||||||

| NET OPERATING INCOME (LOSS) | 626,850 | 40,853 | 1,660,885 | (405,254 | ) | |||||||||||

| Other expenses, net | 15,111 | 11,246 | 27,059 | 38,633 | ||||||||||||

| INCOME (LOSS) BEFORE INCOME TAXES | 611,739 | 29,607 | 1,633,826 | (443,887 | ) | |||||||||||

| Income tax expense (benefit) | 260,447 | 19,277 | 709,394 | (146,101 | ) | |||||||||||

| NET INCOME (LOSS) | $ | 351,292 | $ | 10,330 | $ | 924,432 | $ | (297,786 | ) | |||||||

| Weighted average common shares outstanding: | ||||||||||||||||

| Basic | 3,052,175 | 3,027,034 | 3,038,111 | 3,026,990 | ||||||||||||

| Diluted | 3,188,349 | 3,105,832 | 3,162,620 | 3,026,990 | ||||||||||||

| NET INCOME (LOSS) PER SHARE: | ||||||||||||||||

| Basic | $ | 0.12 | $ | 0.00 | $ | 0.30 | $ | (0.10 | ) | |||||||

| Diluted | $ | 0.11 | $ | 0.00 | $ | 0.29 | $ | (0.10 | ) | |||||||

The accompanying notes are an integral part of these financial statements.

| - 3 - |

ImmuCell Corporation

(Unaudited)

STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

For the Three-Month Periods Ended | For the Nine-Month Periods Ended | |||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| Net income (loss) | $ | 351,292 | $ | 10,330 | $ | 924,432 | $ | (297,786 | ) | |||||||

| Other comprehensive (loss) income: | ||||||||||||||||

| Interest rate swaps, before taxes | (81,767 | ) | 8,347 | (79,956 | ) | 322 | ||||||||||

| Income tax applicable to interest rate swaps | 32,620 | (3,330 | ) | 31,897 | (129 | ) | ||||||||||

| Other comprehensive (loss) income, net of taxes | (49,147 | ) | 5,017 | (48,059 | ) | 193 | ||||||||||

| Total comprehensive income (loss) | $ | 302,145 | $ | 15,347 | $ | 876,373 | $ | (297,593 | ) | |||||||

The accompanying notes are an integral part of these financial statements.

| - 4 - |

ImmuCell Corporation

(Unaudited)

STATEMENTS OF STOCKHOLDERS’ EQUITY

| Common Stock $0.10 Par Value | Capital in Excess of | Accumulated (Deficit) | Treasury Stock | Accumulated Other Comprehensive | Total Stockholders’ | |||||||||||||||||||||||||||

| Shares | Amount | Par Value | Surplus | Shares | Amount | (Loss) | Equity | |||||||||||||||||||||||||

| Balance as of December 31, 2014 | 3,261,148 | $ | 326,115 | $ | 10,042,305 | $ | (574,567 | ) | 234,114 | $ | (512,154 | ) | $ | (23,331 | ) | $ | 9,258,368 | |||||||||||||||

| Net income | 0 | 0 | 0 | 924,432 | 0 | 0 | 0 | 924,432 | ||||||||||||||||||||||||

| Other comprehensive (loss), net of taxes | 0 | 0 | 0 | 0 | 0 | 0 | (48,059 | ) | (48,059 | ) | ||||||||||||||||||||||

| Exercise of stock options | 0 | 0 | 58,957 | 0 | (28,000 | ) | 61,253 | 0 | 120,210 | |||||||||||||||||||||||

| Tax benefits related to stock options | 0 | 0 | 25,707 | 0 | 0 | 0 | 0 | 25,707 | ||||||||||||||||||||||||

| Stock-based compensation | 0 | 0 | 17,825 | 0 | 0 | 0 | 0 | 17,825 | ||||||||||||||||||||||||

| Balance as of September 30, 2015 | 3,261,148 | $ | 326,115 | $ | 10,144,794 | $ | 349,865 | 206,114 | $ | (450,901 | ) | $ | (71,390 | ) | $ | 10,298,483 | ||||||||||||||||

| Common

Stock $0.10 Par Value | Capital in Excess of | Accumulated | Treasury Stock | Accumulated

Other Comprehensive | Total Stockholders’ | |||||||||||||||||||||||||||

| Shares | Amount | Par Value | Deficit | Shares | Amount | (Loss) | Equity | |||||||||||||||||||||||||

| Balance as of December 31, 2013 | 3,261,148 | $ | 326,115 | $ | 10,011,339 | $ | (407,408 | ) | 235,114 | $ | (514,341 | ) | $ | (19,836 | ) | $ | 9,395,869 | |||||||||||||||

| Net (loss) | 0 | 0 | 0 | (297,786 | ) | 0 | 0 | 0 | (297,786 | ) | ||||||||||||||||||||||

| Other comprehensive income, net of taxes | 0 | 0 | 0 | 0 | 0 | 0 | 193 | 193 | ||||||||||||||||||||||||

| Exercise of stock options | 0 | 0 | 962 | 0 | (1,000 | ) | 2,188 | 0 | 3,150 | |||||||||||||||||||||||

| Stock-based compensation | 0 | 0 | 22,265 | 0 | 0 | 0 | 0 | 22,265 | ||||||||||||||||||||||||

| Balance as of September 30, 2014 | 3,261,148 | $ | 326,115 | $ | 10,034,566 | $ | (705,194 | ) | 234,114 | $ | (512,153 | ) | $ | (19,643 | ) | $ | 9,123,691 | |||||||||||||||

The accompanying notes are an integral part of these financial statements.

| - 5 - |

ImmuCell Corporation

(Unaudited)

STATEMENTS OF CASH FLOWS

For the Nine-Month Periods Ended | ||||||||

| 2015 | 2014 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||

| Net income (loss) | $ | 924,432 | $ | (297,786 | ) | |||

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | ||||||||

| Depreciation | 378,475 | 330,796 | ||||||

| Amortization | 2,074 | 2,158 | ||||||

| Deferred income taxes | 680,087 | (146,401 | ) | |||||

| Stock-based compensation | 17,825 | 22,265 | ||||||

| (Gain) loss on disposal of fixed assets | (3,984 | ) | 4,519 | |||||

| Changes in: | ||||||||

| Receivables | 216,078 | 67,846 | ||||||

| Inventory | 81,311 | 167,062 | ||||||

| Prepaid expenses and other assets | (127,160 | ) | (185,676 | ) | ||||

| Accounts payable and accrued expenses | (92,332 | ) | 78,992 | |||||

| Deferred revenue | (6,690 | ) | 6,690 | |||||

| Net cash provided by operating activities | 2,070,116 | 50,465 | ||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | ||||||||

| Purchase of property, plant and equipment | (1,772,091 | ) | (520,142 | ) | ||||

| Maturities of investments | 2,489,000 | 2,489,000 | ||||||

| Purchases of investments | (3,711,000 | ) | (2,985,000 | ) | ||||

| Proceeds from sale of fixed assets | 66,215 | 0 | ||||||

| Net cash (used for) investing activities | (2,927,876 | ) | (1,016,142 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||

| Proceeds from debt issuance | 2,500,000 | 0 | ||||||

| Debt principal repayments | (136,339 | ) | (141,647 | ) | ||||

| Debt issuance costs | (32,759 | ) | 0 | |||||

| Proceeds from exercise of stock options | 120,210 | 3,150 | ||||||

| Tax benefits related to stock options | 25,707 | 0 | ||||||

| Net cash provided by (used for) financing activities | 2,476,819 | (138,497 | ) | |||||

| NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | 1,619,059 | (1,104,174 | ) | |||||

| BEGINNING CASH AND CASH EQUIVALENTS | 850,028 | 2,270,385 | ||||||

| ENDING CASH AND CASH EQUIVALENTS | $ | 2,469,087 | $ | 1,166,211 | ||||

| INCOME TAXES PAID | $ | 3,600 | $ | 1,752 | ||||

| INTEREST EXPENSE PAID | $ | 38,324 | $ | 44,771 | ||||

| NON-CASH ACTIVITIES: | ||||||||

| Change in capital expenditures included in accounts payable and accrued expenses | $ | (213,418 | ) | $ | 84,031 | |||

| Net change in fair value of interest rate swaps | $ | 48,059 | $ | (193 | ) | |||

The accompanying notes are an integral part of these financial statements.

| - 6 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements

| 1. | BUSINESS OPERATIONS |

ImmuCell Corporation (the Company) is a growing animal health company whose purpose is to create scientifically-proven and practical products that result in a measurable economic impact on animal health and productivity in the dairy and beef industries. The Company was originally incorporated in Maine in 1982 and reincorporated in Delaware in 1987, in conjunction with its initial public offering of common stock. We market products that provide immediate immunity to newborn dairy and beef cattle. We are developing product line extensions of our existing products and are in the late stages of developing a new product that addresses mastitis, the most significant cause of economic loss to the dairy industry. The Company is subject to certain risks associated with its stage of development including dependence on key individuals, competition from other larger companies, the successful sale of existing products and the development and acquisition of additional commercially viable products with appropriate regulatory approvals, where applicable. These and other risks to our company are further detailed under PART II: OTHER INFORMATION, ITEM 1A – RISK FACTORS.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

| (a) | Basis of presentation |

We have prepared the accompanying unaudited financial statements reflecting all adjustments, all of which are of a normal recurring nature, that are, in our opinion, necessary in order to ensure that the financial statements are not misleading. We follow accounting standards set by the Financial Accounting Standards Board (FASB). The FASB sets generally accepted accounting principles (GAAP) that we follow to ensure we consistently report our financial condition, results of operations, earnings per share and cash flows. References to GAAP in these footnotes are to the FASB Accounting Standards Codification™ (Codification). Certain prior year accounts have been reclassified to conform with the 2015 financial statement presentation. Certain information and footnote disclosures normally included in the annual financial statements have been condensed or omitted. Accordingly, we believe that although the disclosures are adequate to ensure that the information presented is not misleading, these financial statements should be read in conjunction with the financial statements for the year ended December 31, 2014 and the notes thereto, contained in our Annual Report on Form 10-K as filed with the Securities and Exchange Commission (SEC).

| (b) | Cash, Cash Equivalents, Short-Term Investments and Long-Term Investments |

We consider all highly liquid investment instruments that mature within three months of their purchase dates to be cash equivalents. Cash equivalents are principally invested in securities backed by the U.S. government. Certain cash balances in excess of Federal Deposit Insurance Corporation (FDIC) limits of $250,000 per financial institution per depositor are maintained in money market accounts at financial institutions that are secured, in part, by the Securities Investor Protection Corporation. Amounts in excess of these FDIC limits per bank that are not invested in securities backed by the U.S. government aggregated $1,968,787 and $566,637 as of September 30, 2015 and December 31, 2014, respectively. Short-term investments are classified as held to maturity and are comprised principally of certificates of deposit that mature in more than three months from their purchase dates and not more than twelve months from the balance sheet date. Long-term investments are classified as held to maturity and are comprised principally of certificates of deposit that mature in more than twelve months from the balance sheet date. Short-term and long-term investments are held at different financial institutions that are insured by the FDIC, within the FDIC limits per financial institution. See Note 3.

| (c) | Inventory |

Inventory includes raw materials, work-in-process and finished goods and is recorded at the lower of cost, on the first-in, first-out method, or market (net realizable value). Work-in-process and finished goods inventories include materials, labor and manufacturing overhead. See Note 4.

| (d) | Trade Receivables |

Trade receivables are carried at the original invoice amount less an estimate made for doubtful collection. Management determines the allowance for doubtful accounts on a monthly basis by identifying troubled accounts and by using historical experience applied to an aging of accounts. Trade receivables are written off when deemed uncollectible. Recoveries of trade receivables previously written off are recorded as income when received. A trade receivable is considered to be past due if any portion of the receivable balance is outstanding for more than 30 days. Interest is charged on past due trade receivables. See Note 5.

| - 7 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements (continued)

| (e) | Property, Plant and Equipment |

We depreciate property, plant and equipment on the straight-line method by charges to operations in amounts estimated to expense the cost of the assets from the date they are first put into service to the end of the estimated useful lives of the assets. The cost of our building (which was acquired in 1993) and the 2001 and 2007 additions thereto are being depreciated through 2023. We are depreciating the building addition that was completed during the first quarter of 2015 over twenty-five years. Related building improvements are depreciated over ten year periods. Large and durable fixed assets are depreciated over their useful lives that are generally estimated to be five to ten years. Other fixed assets and computer equipment are depreciated over their useful lives that are generally estimated to be five and three years, respectively. See Note 7.

| (f) | Intangible Assets |

We amortize intangible assets on the straight-line method by charges to operations in amounts estimated to expense the cost of the assets from the date they are first put into service to the end of the estimated useful lives of the assets. In connection with certain credit facilities entered into during the third quarters of 2010 and 2015, we incurred debt issue costs of $26,489 and $32,759, respectively, which costs are being amortized to other expenses, net over the terms of the credit facilities. See Notes 6 and 9.

We continually assess the realizability of these assets in accordance with the impairment provisions of Codification Topic 360, Accounting for the Impairment or Disposal of Long-Lived Assets. If an impairment review is triggered, we evaluate the carrying value of long-lived assets by determining if impairment exists based on estimated undiscounted future cash flows over the remaining useful life of the assets and comparing that value to the carrying value of the assets. If the carrying value of the asset is greater than the estimated future cash flows, the asset is written down to its estimated fair value. The cash flow estimates that are used contain our best estimates, using appropriate and customary assumptions and projections at the time. We also review the estimated useful life of intangible assets at the end of each reporting period, making any necessary adjustments.

| (g) | Disclosure of Fair Value of Financial Instruments and Concentration of Risk |

Financial instruments consist mainly of cash, cash equivalents, short-term investments, long-term investments, accounts receivable, accounts payable, bank debt and interest rate swaps. Financial instruments that potentially subject the Company to concentrations of credit risk are principally cash, cash equivalents, short-term investments, long-term investments and accounts receivable. We make short-term and long-term investments in financial instruments that are insured by the FDIC. We account for fair value measurements in accordance with Codification Topic 820, Fair Value Measurements and Disclosures, which defines fair value, establishes a framework for measuring fair value and requires additional disclosures about fair value measurements. The estimated fair value of cash, cash equivalents, short-term investments, long-term investments, accounts receivable and accounts payable approximate their carrying value due to their short maturities. The estimated fair value of bank debt approximates its carrying value because the interest rates are variable. Interest rate swaps are carried at fair value. See Note 9.

Concentration of credit risk with respect to accounts receivable is principally limited to certain customers to whom we make substantial sales. To reduce risk, we routinely assess the financial strength of our customers and, as a consequence, believe that our accounts receivable credit risk exposure is limited. We maintain an allowance for potential credit losses, but historically we have not experienced significant credit losses related to an individual customer or groups of customers in any particular industry or geographic area.

We believe that supplies and raw materials for the production of our products are available from more than one vendor or farm. Our policy is to maintain more than one source of supply for the components used in our products. However, there is a risk that we could have difficulty in efficiently acquiring essential supplies.

| (h) | Interest Rate Swap Agreements |

All derivatives are recognized on the balance sheet at their fair value. We entered into interest rate swap agreements in 2010 and 2015. On the dates the agreements were entered into, we designated the derivatives as hedges of the variability of cash flows to be paid related to our long-term debt. The agreements have been determined to be highly effective in hedging the variability of identified cash flows, so changes in the fair market value of the interest rate swap agreements are recorded as comprehensive income (loss), until earnings are affected by the variability of cash flows (e.g. when periodic settlements on a variable-rate asset or liability are recorded in earnings). We formally documented the relationship between the interest rate swap agreements and the related hedged items. We also formally assess, both at the interest rate swap agreements’ inception and on an ongoing basis, whether the agreements are highly effective in offsetting changes in cash flow of hedged items. See Note 9.

| - 8 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements (continued)

| (i) | Revenue Recognition |

We recognize revenue in accordance with Staff Accounting Bulletin (SAB) No. 104, “Revenue Recognition”. SAB No. 104 requires that four criteria are met before revenue is recognized. These include i) persuasive evidence that an arrangement exists, ii) delivery has occurred or services have been rendered, iii) the seller’s price is fixed and determinable and iv) collectability is reasonably assured. We recognize revenue at the time of shipment (including to distributors) for substantially all products, as title and risk of loss pass to the customer on delivery to the common carrier after concluding that collectability is reasonably assured. We recognize service revenue at the time the service is performed.

| (j) | Expense Recognition |

Advertising costs are expensed when incurred, which is generally during the month in which the advertisement is published. Advertising expenses amounted to $27,545 and $15,844 during the three-month periods ended September 30, 2015 and 2014, respectively, and $72,539 and $42,915 during the nine-month periods ended September 30, 2015 and 2014, respectively. All product development expenses are expensed as incurred, as are all related patent costs.

| (k) | Income Taxes |

We account for income taxes in accordance with Codification Topic 740, Income Taxes, which requires that we recognize a current tax liability or asset for current taxes payable or refundable and a deferred tax liability or asset for the estimated future tax effects of temporary differences and carryforwards to the extent they are realizable. We believe it is more likely than not that the deferred tax assets will be realized through future taxable income and future tax effects of temporary differences between book income and taxable income. Accordingly, we have not established a valuation allowance for the deferred tax assets. Codification Topic 740-10 clarifies the accounting for income taxes by prescribing a minimum recognition threshold that a tax position must meet before being recognized in the financial statements. In the ordinary course of business, there are transactions and calculations where the ultimate tax outcome is uncertain. In addition, we are subject to periodic audits and examinations by the Internal Revenue Service and other taxing authorities. We have evaluated the positions taken on our filed tax returns. We have concluded that no uncertain tax positions exist as of September 30, 2015. Although we believe that our estimates are reasonable, actual results could differ from these estimates. See Note 11.

| (l) | Stock-Based Compensation |

We account for stock-based compensation in accordance with Codification Topic 718, Compensation-Stock Compensation, which generally requires us to recognize non-cash compensation expense for stock-based payments using the fair-value-based method. The fair value of each stock option grant has been estimated on the date of grant using the Black-Scholes option pricing model. Accordingly, we recorded compensation expense pertaining to stock-based compensation of $6,342 and $4,974 during the three-month periods ended September 30, 2015 and 2014, respectively, and $17,825 and $22,265 during the nine-month periods ended September 30, 2015 and 2014, respectively, which resulted in a decrease to income before income taxes of less than $0.01 per share during each of the periods reported. Codification Topic 718 requires us to reflect gross tax savings resulting from tax deductions in excess of expense reflected in our financial statements as a financing cash flow.

| (m) | Net Income (Loss) Per Common Share |

Net Income (Loss) per common share has been computed in accordance with Codification Topic 260-10, Earnings Per Share. The basic Net Income per share has been computed by dividing Net Income by the weighted average number of common shares outstanding during this period. Diluted Net Income per share has been computed by dividing Net Income by the weighted average number of shares outstanding during the period plus all outstanding stock options with an exercise price that is less than the average market price of the common stock during the period less the number of shares that could have been repurchased at this average market price with the proceeds from the hypothetical stock option exercises. The Net (Loss) per common share in 2014 has been computed by dividing the Net (Loss) by the weighted average number of common shares outstanding during the period, without giving consideration to outstanding stock options because the impact would be anti-dilutive.

| - 9 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements (continued)

Three-Month

Period | Nine-Month

Period | |||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| Weighted average number of shares outstanding | 3,052,175 | 3,027,034 | 3,038,111 | 3,026,990 | ||||||||||||

| Effect of dilutive stock options | 136,174 | 78,798 | 124,509 | 0 | ||||||||||||

| Diluted number of shares outstanding | 3,188,349 | 3,105,832 | 3,162,620 | 3,026,990 | ||||||||||||

| Stock options outstanding as of September 30th not included in the calculation because the effect would be anti-dilutive | 0 | 85,000 | 3,000 | 251,000 | ||||||||||||

| (n) | Use of Estimates |

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the period. Actual amounts could differ from those estimates.

| (o) | New Accounting Pronouncement |

In May 2014, the FASB issued Accounting Standards Update No. 2014-09, Revenue from Contracts with Customers (ASU 2014-09), which requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. ASU 2014-09 will replace most existing revenue recognition guidance in U.S. GAAP when it becomes effective. ASU 2014-09 was initially effective for the Company on January 1, 2017. Early application was not permitted. In July 2015, the FASB approved a one-year deferral in the effective date to January 1, 2018, with the option of applying the standard on the original effective date. ASU 2014-09 permits the use of either the retrospective or cumulative effect transition method. We have evaluated the effect that ASU 2014-09 would have on our financial statements and related disclosures. We expect that ASU 2014-09 will have no significant effect on our ongoing financial reporting, but we continue to evaluate this pending accounting standard.

| 3. | CASH, CASH EQUIVALENTS, SHORT-TERM INVESTMENTS AND LONG-TERM INVESTMENTS |

Cash, cash equivalents, short-term investments and long-term investments consisted of the following:

As of September 30, 2015 | As of December 31, 2014 | Increase (Decrease) | ||||||||||

| Cash and cash equivalents | $ | 2,469,087 | $ | 850,028 | $ | 1,619,059 | ||||||

| Short-term investments | 3,720,000 | 2,489,000 | 1,231,000 | |||||||||

| Subtotal | 6,189,087 | 3,339,028 | 2,850,059 | |||||||||

| Long-term investments | 487,000 | 496,000 | (9,000 | ) | ||||||||

| Total | $ | 6,676,087 | $ | 3,835,028 | $ | 2,841,059 | ||||||

| 4. | INVENTORY |

Inventory consisted of the following:

As of September 30, 2015 | As of December 31, 2014 | Increase (Decrease) | ||||||||||

| Raw materials | $ | 337,538 | $ | 306,444 | $ | 31,094 | ||||||

| Work-in-process | 468,059 | 355,745 | 112,314 | |||||||||

| Finished goods | 58,847 | 283,566 | (224,719 | ) | ||||||||

| Total | $ | 864,444 | $ | 945,755 | $ | (81,311 | ) | |||||

| - 10 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements (continued)

| 5. | ACCOUNTS RECEIVABLE |

Accounts receivable consisted of the following:

As of September 30, 2015 | As of December 31, 2014 | (Decrease) Increase | ||||||||||

| Trade accounts receivable, gross | $ | 783,547 | $ | 1,004,990 | $ | (221,443 | ) | |||||

| Accumulated allowance for bad debt and product returns | (16,958 | ) | (16,194 | ) | (764 | ) | ||||||

| Trade accounts receivable, net | 766,589 | 988,796 | (222,207 | ) | ||||||||

| Other receivables | 22,625 | 16,496 | 6,129 | |||||||||

| Accounts receivable, net | $ | 789,214 | $ | 1,005,292 | $ | (216,078 | ) | |||||

| 6. | PREPAID EXPENSES AND OTHER ASSETS |

Prepaid expenses and other assets consisted of the following:

As of September 30, 2015 | As of December 31, 2014 | Increase (Decrease) | ||||||||||

| Prepaid expenses and other assets | $ | 234,628 | $ | 133,119 | $ | 101,509 | ||||||

| Security deposits | 40,931 | 15,280 | 25,651 | |||||||||

| Current subtotal | 275,559 | 148,399 | 127,160 | |||||||||

| Debt issue costs | 59,248 | 26,489 | 32,759 | |||||||||

| Accumulated amortization of debt issue costs | (18,553 | ) | (16,479 | ) | (2,074 | ) | ||||||

| Security deposits | 8,920 | 8,920 | 0 | |||||||||

| Long-term subtotal | 49,615 | 18,930 | 30,685 | |||||||||

| Total | $ | 325,174 | $ | 167,329 | $ | 157,845 | ||||||

| 7. | PROPERTY, PLANT AND EQUIPMENT |

Property, plant and equipment consisted of the following, at cost:

As of September 30, 2015 | As of December 31, 2014 | Increase (Decrease) | ||||||||||

| Laboratory and manufacturing equipment | $ | 3,602,690 | $ | 3,522,465 | $ | 80,225 | ||||||

| Building and improvements | 4,579,852 | 2,969,891 | 1,609,961 | |||||||||

| Office furniture and equipment | 569,567 | 470,607 | 98,960 | |||||||||

| Construction in progress(1) | 738,282 | 1,270,672 | (532,390 | ) | ||||||||

| Land | 72,807 | 50,000 | 22,807 | |||||||||

| Property, plant and equipment, gross | 9,563,198 | 8,283,635 | 1,279,563 | |||||||||

| Accumulated depreciation | (4,607,584 | ) | (4,445,988 | ) | (161,596 | ) | ||||||

| Property, plant and equipment, net | $ | 4,955,614 | $ | 3,837,647 | $ | 1,117,967 | ||||||

(1)As of December 31, 2014, construction in progress consisted of a building addition that was completed during the first quarter of 2015. As of September 30, 2015, construction in progress consisted principally of partial payments towards new manufacturing equipment.

| - 11 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements (continued)

| 8. | ACCOUNTS PAYABLE AND ACCRUED EXPENSES |

Accounts payable and accrued expenses consisted of the following:

As of September 30, 2015 | As of December 31, 2014 | (Decrease) Increase | ||||||||||

| Accounts payable – capital | $ | 37,965 | $ | 251,383 | $ | (213,418 | ) | |||||

| Accounts payable – trade | 178,542 | 204,810 | (26,268 | ) | ||||||||

| Accrued payroll | 134,466 | 145,176 | (10,710 | ) | ||||||||

| Accrued clinical studies | 68,428 | 131,945 | (63,517 | ) | ||||||||

| Accrued professional fees | 55,462 | 42,250 | 13,212 | |||||||||

| Accrued other | 71,064 | 76,113 | (5,049 | ) | ||||||||

| Total | $ | 545,927 | $ | 851,677 | $ | (305,750 | ) | |||||

| 9. | BANK DEBT |

We have in place certain credit facilities with TD Bank, N.A. (a wholly owned subsidiary of TD Financial Group, which is a multinational bank with approximately $944 billion in assets and over 22 million clients worldwide) which are secured by substantially all of our assets. Proceeds from the $1,000,000 mortgage note were received during the third quarter of 2010. Based on a 15-year amortization schedule, a balloon principal payment of approximately $451,885 will be due during the third quarter of 2020. Proceeds from the $2,500,000 mortgage note were received during the third quarter of 2015. Based on a 20-year amortization schedule, a balloon principal payment of approximately $1,550,007 will be due during the third quarter of 2025. We hedged our interest rate exposure on these mortgage notes with interest rate swap agreements that effectively converted floating interest rates based on the one-month LIBOR plus a bank profit margin to the fixed rates of 6.04% and 4.38%, respectively. As of September 30, 2015, the variable rates on these two mortgage notes were 3.46% and 2.45%, respectively. All derivatives are recognized on the balance sheet at their fair value. At the time of the closings and thereafter, the agreements were determined to be highly effective in hedging the variability of the identified cash flows and have been designated as cash flow hedges of the variability in the hedged interest payments. Changes in the fair value of the interest rate swap agreements are recorded in other comprehensive income (loss), net of taxes. The original notional amounts of the interest rate swap agreements of $1,000,000 and $2,500,000 amortize in accordance with the amortization of the mortgage notes. The notional amount of the interest rate swaps was $3,259,963 as of September 30, 2015. Payments required by the interest rate swaps totaled $5,112 and $5,538 during the three-month periods ended September 30, 2015 and 2014, and $15,549 and $16,726 during the nine-month periods ended September 30, 2015 and 2014, respectively. As the result of our decision to hedge this interest rate risk, we recorded other comprehensive (loss) income, net of taxes, in the amount of ($49,147) and $5,017 during the three-month periods ended September 30, 2015 and 2014, and ($48,059) and $193 during the nine-month periods ended September 30, 2015 and 2014, respectively, which reflects the change in the fair value of the interest rate swap assets (liabilities), net of taxes. The fair values of the interest rate swaps have been determined using observable market-based inputs or unobservable inputs that are corroborated by market data. Accordingly, the interest rate swaps are classified as level 2 within the fair value hierarchy provided in Codification Topic 820, Fair Value Measurements and Disclosures. Proceeds from a $600,000 note bearing interest at 4.25% were received during the first quarter of 2011. This note was repaid during the third quarter of 2015. The $500,000 line of credit is available as needed and has been extended through May 31, 2016 and is renewable annually thereafter. The line of credit was unused as of September 30, 2015 and December 31, 2014. Interest on any borrowings against the line of credit would be variable at the higher of 4.25% per annum or the one-month LIBOR plus 3.5% per annum. These credit facilities are subject to certain financial covenants. We are in compliance with all applicable covenants as of September 30, 2015. Principal payments due under debt outstanding as of September 30, 2015 are reflected in the following table by the year that payments are due:

| - 12 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements (continued)

| Period | $1,000,000 Mortgage Note | $2,500,000 Mortgage Note | Total | |||||||||

| Three months ending December 31, 2015 | $ | 14,043 | $ | 19,371 | $ | 33,414 | ||||||

| Year ending December 31, 2016 | 57,384 | 78,456 | 135,840 | |||||||||

| Year ending December 31, 2017 | 61,056 | 82,308 | 143,364 | |||||||||

| Year ending December 31, 2018 | 64,876 | 86,097 | 150,973 | |||||||||

| Year ending December 31, 2019 | 68,908 | 89,997 | 158,905 | |||||||||

| After December 31, 2019 | 493,696 | 2,143,771 | 2,637,467 | |||||||||

| Total | $ | 759,963 | $ | 2,500,000 | $ | 3,259,963 | ||||||

| 10. | OTHER EXPENSES, NET |

Other expenses, net, consisted of the following:

Three-Month

Periods | Nine-Month

Periods | |||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| Interest income | $ | (4,461 | ) | $ | (3,912 | ) | $ | (10,634 | ) | $ | (11,607 | ) | ||||

| Interest expense | 15,084 | 14,514 | 41,039 | 44,148 | ||||||||||||

| Other | 4,488 | 644 | (3,346 | ) | 6,092 | |||||||||||

| Other expenses, net | $ | 15,111 | $ | 11,246 | $ | 27,059 | $ | 38,633 | ||||||||

| 11. | INCOME TAXES |

Our income tax expense (benefit) aggregated $260,447 and $19,277 (amounting to 43% and 65% of our income (loss) before income taxes) for the three-month periods ended September 30, 2015 and 2014, respectively, and $709,394 and ($146,101) (amounting to 43% and 33% of our income (loss) before income taxes) for the nine-month periods ended September 30, 2015 and 2014, respectively. As of December 31, 2014, we have state net operating loss carryforwards of approximately $1,920,000 that expire in 2028 through 2031, if not utilized before then, and federal net operating loss carryforwards of approximately $1,750,000 that expire in 2029 through 2034, if not utilized before then. Additionally, we have general business tax credit carryforwards of approximately $220,000 that expire in 2027 through 2034, if not utilized before then, which effectively protects approximately $549,000 in taxable income (assuming a 40% tax rate) from taxes, which can be utilized only after all net operating loss carryforwards are utilized. The $965,000 licensing payment that we made during the fourth quarter of 2004 was treated as an intangible asset and is being amortized over 15 years, for tax return purposes only. Approximately $1,112,000 of our investment to produce the Drug Substance (our Active Pharmaceutical Ingredient, Nisin) for Mast Out® was expensed as incurred for our books. Included in this amount is approximately $820,000 that was capitalized and is being depreciated over statutory periods for tax return purposes only.

Deferred tax assets are recognized only when it is probable that sufficient taxable income will be available in future periods against which deductible temporary differences and credits may be utilized. However, the amount of the deferred tax asset could be reduced if projected income is not achieved due to various factors, such as unfavorable business conditions. If projected income is not expected to be achieved, we would decrease the deferred tax asset to the amount that we believe can be realized.

Net operating loss carryforwards, credits, and other tax attributes are subject to review and possible adjustment by the Internal Revenue Service. Section 382 of the Internal Revenue Code contains provisions that could place annual limitations on the future utilization of net operating loss carryforwards and credits in the event of a change in ownership of the Company, as defined.

The Company files income tax returns in the U.S. federal jurisdiction and several state jurisdictions. With few exceptions, the Company is no longer subject to income tax examinations by tax authorities for years before 2011. We currently have no tax examinations in progress. We also have not paid additional taxes, interest or penalties as a result of tax examinations nor do we have any unrecognized tax benefits for any of the periods in the accompanying financial statements.

| - 13 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements (continued)

| 12. | COMMITMENTS AND CONTINGENT LIABILITIES |

Our bylaws, as amended, in effect provide that the Company will indemnify its officers and directors to the maximum extent permitted by Delaware law. In addition, we make similar indemnity undertakings to each director through a separate indemnification agreement with that director. The maximum payment that we may be required to make under such provisions is theoretically unlimited and is impossible to determine. We maintain directors’ and officers’ liability insurance, which may provide reimbursement to the Company for payments made to, or on behalf of, officers and directors pursuant to the indemnification provisions. Our indemnification obligations were grandfathered under the provisions of Codification Topic 460, Guarantees. Accordingly, we have recorded no liability for such obligations as of September 30, 2015. Since our incorporation, we have had no occasion to make any indemnification payment to any of our officers or directors for any reason.

As of September 30, 2015, we had committed approximately $728,000 to capital expenditures, $576,000 to the production of inventory and an additional $261,000 to other obligations.

We enter into agreements with third parties in the ordinary course of business under which we are obligated to indemnify such third parties from and against various risks and losses. The precise terms of such indemnities vary with the nature of the agreement. In many cases, we limit the maximum amount of our indemnification obligations, but in some cases those obligations may be theoretically unlimited. We have not incurred material expenses in discharging any of these indemnification obligations, and based on our analysis of the nature of the risks involved, we believe that the fair value of the liabilities potentially arising under these agreements is minimal. Accordingly, we have recorded no liabilities for such obligations as of September 30, 2015.

The development, manufacturing and marketing of animal health care products entails an inherent risk that liability claims will be asserted against us. We feel that we have reasonable levels of liability insurance to support our operations.

| 13. | COMMON STOCK RIGHTS PLAN |

During the second quarter of 2015, we amended our Common Stock Rights Plan by removing a provision that prevented a new group of directors elected following the emergence of an Acquiring Person (an owner of more than 20% of our stock) from controlling the Rights Plan by maintaining exclusive authority over the Rights Plan with pre-existing directors. We did this because such provisions have come to be viewed with disfavor by Delaware courts.

| 14. | SEGMENT AND SIGNIFICANT CUSTOMER INFORMATION |

We principally operate in the business segment described in Note 1. Pursuant to Codification Topic 280, Segment Reporting, we operate in one reportable business segment, that being the development, acquisition, manufacture and sale of products that improve the health and productivity of cows for the dairy and beef industries. Almost all of our internally funded product development expenses are in support of such products. The significant accounting policies of this segment are described in Note 2.

Our primary customers for the majority of our product sales (85% and 84% for the three-month periods ended September 30, 2015 and 2014, and 83% and 82% for the nine-month periods ended September 30, 2015 and 2014, respectively) are in the U.S. dairy and beef industries. Product sales to international customers, who are also in the dairy and beef industries, aggregated 6% and 11% of our total product sales for the three-month periods ended September 30, 2015 and 2014, respectively, and 13% for both of the nine-month periods ended September 30, 2015 and 2014. Sales to significant customers that amounted to 10% or more of total product sales are detailed in the following table:

| Three-Month

Periods Ended September 30, | Nine-Month

Periods Ended September 30, | |||||||||||||||

| 2015 | 2014 | 2015 | 2014 | |||||||||||||

| Animal Health International, Inc.(1) | 39 | % | 34 | % | 41 | % | 37 | % | ||||||||

| MWI Animal Health(2) | 22 | % | 23 | % | 21 | % | 22 | % | ||||||||

| - 14 - |

ImmuCell Corporation

Notes to Unaudited Financial Statements (continued)

Accounts receivable due from significant customers amounted to the percentages of total trade accounts receivable as detailed in the following table:

As of September 30, 2015 | As of December 31, 2014 | |||||||

| Animal Health International, Inc.(1) | 37 | % | 45 | % | ||||

| MWI Animal Health(2) | 25 | % | 26 | % | ||||

| TCS Biosciences, Ltd. | 13 | % | * | |||||

(1)During

June 2015, Patterson Companies, Inc. (NASDAQ: PDCO) acquired Animal Health International, Inc.

(2)During March 2015, AmerisourceBergen Corporation (NYSE:

ABC) acquired MWI Animal Health.

*Amount is less than 10%.

| 15. | RELATED PARTY TRANSACTIONS |

Dr. David S. Tomsche (Chair of our Board of Directors) is a controlling owner of Leedstone Inc. (formerly Stearns Veterinary Outlet, Inc.), a domestic distributor of ImmuCell products (First Defense®, Wipe Out® Dairy Wipes, and CMT) and of J-t Enterprises of Melrose, Inc., an exporter. His affiliated companies purchased $452,207 and $283,287 of products from ImmuCell during the nine-month periods ended September 30, 2015 and 2014, respectively, on terms consistent with those offered to other distributors of similar status. We made marketing-related payments of $3,222 and $6,355 to these affiliate companies during the nine-month periods ended September 30, 2015 and 2014, respectively. Our accounts receivable (subject to standard and customary payment terms) due from these affiliated companies aggregated $12,864 and $18,796 as of September 30, 2015 and December 31, 2014, respectively.

| 16. | EMPLOYEE BENEFITS |

We have a 401(k) savings plan (the Plan) in which all employees completing one month of service with the Company are eligible to participate. Participants may contribute up to the maximum amount allowed by the Internal Revenue Service. Since August 2012 we have matched 100% of the first 3% of each employee’s salary that is contributed to the Plan and 50% of the next 2% of each employee’s salary that is contributed to the Plan. Under this matching plan, we paid $17,102 and $17,117 into the plan for the three-month periods ended September 30, 2015 and 2014, respectively, and $54,157 and $47,920 for the nine-month periods ended September 30, 2015 and 2014, respectively.

| 17. | SUBSEQUENT EVENTS |

We have adopted the disclosure provisions of Codification Topic 855-10-50-1, Subsequent Events, which provides guidance to establish general standards of accounting for and disclosures of events that occur after the balance sheet date but before financial statements are issued. Codification Topic 855-10-50-1 requires additional disclosures only, and therefore did not have an impact on our financial condition, results of operations, earnings per share or cash flows. Entities are required to disclose the date through which subsequent events were evaluated as well as the rationale for why that date was selected. Public entities must evaluate subsequent events through the date that financial statements are issued. Accordingly, we have evaluated subsequent events through the time of filing on November 12, 2015, the date we have issued this Quarterly Report on Form 10-Q. This disclosure should alert all users of financial statements that an entity has not evaluated subsequent events after that date in the set of financial statements being presented.

During the fourth quarter of 2015, we entered into a revised agreement with Plas-Pak Inc. of Norwich, Connecticut covering the supply of plastic syringes used to deliver Mast Out®, effective through the year ending December 31, 2020. On October 28, 2015, we filed a registration statement on Form S-3 with the SEC for the potential issuance of up to $10,000,000 in equity (subject to certain limitations). We filed Pre-Effective Amendment No. 1 on November 5, 2015, and our registration statement became effective on November 10, 2015. During the fourth quarter of 2015, our Board of Directors voted to exercise an option to acquire land nearby to our existing Portland facility for a potential site for a Mast Out® production facility for $238,000 (less the $23,800 option payment that was paid during the third quarter of 2015).

| - 15 - |

ImmuCell Corporation

ITEM 2 - MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Financial Condition

We aim to capitalize on the significant growth in sales of First DefenseÒ and to revolutionize the mastitis treatment paradigm. Our strategy is focused on developing and selling products that improve animal health and productivity in the dairy and beef industries. These product opportunities are generally less expensive to develop than the human health product opportunities that we had worked on during the 1990’s. We have funded most of our product development expenses principally from our gross margin on product sales. Our cumulative investment of approximately $21,653,000 during the 16.75 year period that began January 1, 1999 (the year we elected to change our strategic focus from human to animal health products) and ended September 30, 2015 was offset, in part, by $4,130,000 in licensing revenue, technology sales and grant income. Having largely completed the significant clinical studies for Mast OutÒ, we reduced product development expenses during 2012, as anticipated, and were profitable during 2012 and 2013. These product development expenses increased again, as we invested in a small-scale Nisin production facility, resulting in a net loss during the first half of 2014, which was large enough to result in a net loss for the year ended December 31, 2014. After completing this investment, we returned to profitable results during the second half of 2014 and have continued to be profitable during the first nine months of 2015.

We had approximately $6,676,000 in available cash, cash equivalents, short-term investments and long-term investments as of September 30, 2015. The table below summarizes the changes in selected, key balance sheet items (in thousands, except for percentages):

As of September 30, | As of December 31, | Increase | ||||||||||||||

| 2015 | 2014 | $ | % | |||||||||||||

| Cash, cash equivalents, short-term investments and long-term investments | $ | 6,676 | $ | 3,835 | $ | 2,841 | 74 | % | ||||||||

| Net working capital | 7,507 | 4,460 | 3,047 | 68 | ||||||||||||

| Total assets | 14,223 | 11,052 | 3,171 | 29 | ||||||||||||

| Stockholders’ equity | $ | 10,298 | $ | 9,258 | $ | 1,040 | 11 | % | ||||||||

Net cash provided by operating activities amounted to $2,070,000 during the nine-month period ended September 30, 2015 compared to net cash provided by operating activities of $50,000 during the nine-month period ended September 30, 2014. Net cash provided by operating activities amounted to $2,322,000 during the twelve-month period ended September 30, 2015 compared to net cash provided by operating activities of $134,000 during the twelve-month period ended September 30, 2014. Capital investments of $1,772,000 during the nine-month period ended September 30, 2015 compared to capital investments of $520,000 during the nine-month period ended September 30, 2014. Together with gross margin earned from ongoing product sales, we believe that we have sufficient capital resources to meet our working capital requirements and to finance our ongoing business operations during at least the next twelve months, but we do not currently have sufficient capital to fund the contemplated investment in a commercial-scale production facility for Mast Out®.

During the third quarters of 2010 and 2015, we agreed to terms of certain credit facilities with TD Bank, N.A., which are secured by substantially all of our assets including our building which was independently appraised at $4,180,000 in connection with the 2015 financing. As of September 30, 2015, our outstanding bank debt balance was approximately $3,260,000. We have a $500,000 line of credit that is available as needed. We chose debt financing at this time in order to take advantage of what we believe to be historically low interest rates, which may trend higher in the future.

On October 28, 2015, we filed a registration statement on Form S-3 with the SEC for the potential issuance of up to $10,000,000 in equity (subject to certain limitations). This registration statement became effective on November 10, 2015. This would allow us to raise equity at a time that we may determine the market conditions are favorable. Under this form of registration statement, we are limited to raising gross proceeds of no more than one-third of the market capitalization of our common stock (as determined by the high price within the preceding 60 days leading up to a sale of securities) held by non-affiliates (non-insiders) of the Company. This limit was approximately $4,760,000, based on the closing price of $6.53 per share as of November 3, 2015. While we may use the net proceeds from any sale of securities to fund our growth plans and other general corporate purposes, we anticipate that a primary use of the net proceeds would be to fund a significant portion of the cost of building and equipping a pharmaceutical facility to produce the Drug Substance (the Active Pharmaceutical Ingredient, which is our pharmaceutical-grade Nisin) for Mast OutÒ.

| - 16 - |

ImmuCell Corporation

During the third quarter of 2013, our Board of Directors approved the aggregate investment of approximately $3,000,000 in two projects. The first investment involved acquiring processing equipment and modifying a portion of our facility to produce the Drug Substance at small-scale as part of the Mast OutÒ product development initiative. These expenses were not capitalized because this plant is not expected to support commercial sales. This project was substantially completed during the third quarter of 2014. This specifically targeted increase in product development expenses resulted in a net loss during the first six months of 2014. The purpose of this investment is discussed in greater detail under “Product Development Expenses” below. The second investment involved acquiring manufacturing equipment and constructing a two-story addition to our facility, providing us with approximately 7,100 square feet of cold storage, production and warehouse space to increase our commercial production capacity for First DefenseÒ and other products. Additionally, this investment allows us to better integrate the production of the Drug Substance at small-scale into our operations. This project was initiated at the end of the third quarter of 2014 and was substantially completed during the first quarter of 2015. These expenses have been capitalized as they support the commercial sale of our existing products. The following table details the spending on these two projects:

| Expenses | Capital Expenditures | Total Expenses and Capital Expenditures | ||||||||||

| Three-month period ended December 31, 2013 | $ | 110,000 | $ | 21,000 | $ | 131,000 | ||||||

| Year ended December 31, 2014 | 973,000 | 1,492,000 | 2,465,000 | |||||||||

| Nine-month period ended September 30, 2015 | 9,000 | 414,000 | 423,000 | |||||||||

| Total investment | $ | 1,092,000 | $ | 1,927,000 | $ | 3,019,000 | ||||||

Separately, as of October 1, 2015, we had additional authorization from our Board of Directors to spend up to approximately $1,095,000 on new manufacturing equipment and other routine and necessary capital expenditures. This investment is in addition to the $1,145,000 that we invested in related capital expenditures during the first nine months of 2015. Most of this 2015 investment is intended to pay for the acquisition of First DefenseÒ production equipment necessary to increase our liquid processing capacity by approximately 50% and our freeze-drying capacity by approximately 100%. We completed the investment to increase our liquid processing capacity during the fourth quarter of 2015, and the investment to increase our freeze-drying capacity is proceeding on schedule and is expected to be completed before the end of the first quarter of 2016. These investments, together with the 7,100 square foot facility addition, described above, are necessary to increase our manufacturing capacity to fill our current backlog of First DefenseÒ orders and to meet the increased sales demand that we are experiencing.

Results of Operations

Product Sales

Our total product sales during the three-month period ended September 30, 2015 increased by 40%, or $702,000, to $2,472,000 from $1,770,000 during the three-month period ended September 30, 2014. Our total product sales during the nine-month period ended September 30, 2015 increased by 40%, or $2,143,000 to $7,534,000 from $5,392,000 during the nine-month period ended September 30, 2014. Our total product sales during the twelve-month period ended September 30, 2015 increased by 40%, or $2,789,000, to $9,740,000 from $6,951,000 during the twelve-month period ended September 30, 2014. This sales growth has exceeded our current production capacity and created a backlog of orders for First DefenseÒ aggregating approximately $1,554,000 as of September 30, 2015. This backlog of orders has persisted since the first quarter of 2015. We believe that some of our customers may now be increasing their orders in an attempt to secure increased inventory levels. This could explain why the amount of the order backlog has not been reduced materially, despite our increasing inventory production levels. During the three-month period ended September 30, 2015, domestic product sales increased by 45%, or $667,000, and international sales increased by 13%, or $36,000, in comparison to the three-month period ended September 30, 2014. During the nine-month period ended September 30, 2015, domestic product sales increased by 41%, or $1,836,000, and international sales increased by 35%, or $307,000, in comparison to the nine-month period ended September 30, 2014. The growth in international sales is primarily being experienced in Canada.

| - 17 - |

ImmuCell Corporation

Growth in sales of our lead product, First DefenseÒ and related product line extensions, is driving the increase in our total product sales. First DefenseÒ and related product line extensions continue to benefit from wide acceptance by dairy and beef producers as an effective tool to prevent bovine enteritis (scours) in newborn calves. We believe that our increased investment in sales and marketing personnel is helping us introduce First DefenseÒ and related product line extensions to new customers. We launched a new communications campaign at the end of 2010 that continues to emphasize how the unique ability of First DefenseÒ to provide Immediate ImmunityTM generates a dependable return on investment for dairy and beef producers. Preventing newborn calves from becoming sick immediately after birth helps them to reach their genetic potential and reduces the reliance on antibiotic treatments. By our estimation, calf scours can cost the calf industry approximately $740 million per year (approximately $328 million to the dairy industry and $412 million to the beef industry). Our market research suggests that we captured approximately 38% of the market segment comprised of the four leading USDA-approved scours preventative products during the twelve-month period ended September 30, 2015. In light of the challenging market conditions faced by our customers (i.e. lower milk prices, deteriorated milk-to-feed price ratio, etc.), there can be no assurance that this level of growth and contribution to profitability can be sustained. We generally held our product selling prices without increase during the seven-year period ended December 31, 2007. During the first quarter of 2008, we implemented a modest increase to the selling price of First Defense®. We did not implement another price increase until the third quarter of 2014. We implemented a price increase for the tube delivery format of our First Defense Technology™ in a gel solution (as described below) during the second quarter of 2015. This pricing strategy recognizes that while selling a premium-priced product, we must be very efficient with our manufacturing costs to maintain a healthy gross margin.

Competition for resources that dairy producers allocate to their calf enterprises has been increased by the many new products that have been introduced to the market. Our sales are normally seasonal, with higher sales expected during the first quarter. Warm and dry weather reduces the producer’s perception of the need for a disease preventative product like First DefenseÒ, but heat stress on calves caused by extremely hot summer weather can increase the incidence of scours. Harsher winter weather benefits our sales. The animal health distribution segment has been aggressively consolidating over the last few years. Larger distributors have been acquiring smaller distributors. Our two largest distributors have been acquired by larger companies. Beef herd numbers were reduced because of the 2012 drought conditions in many parts of North America. This has resulted in an increase in the value of newborn calves today, as producers re-build their herd levels. Such an upswing increases a producer’s likelihood to invest in First DefenseÒ for their calf crop. Our product sales benefited from the relatively strong prices of cows and calves, as well as a stable to moderately lower cost of feed, despite a decrease in milk prices since 2014. We believe that our sales have also benefited from a lack of supply in the market of a competitive product sold by Elanco Animal Health during the early part of 2015.

We are selling product line extensions of First DefenseÒ under the description First Defense TechnologyTM, which is a unique whey protein concentrate that is processed utilizing our proprietary milk protein purification methods, for the nutritional and feed supplement markets without disease prevention claims approved by the U.S. Department of Agriculture (USDA). Through our First Defense TechnologyTM, we are selling concentrated whey proteins in different formats. During the first quarter of 2011, we initiated sales of First Defense TechnologyTM in a bulk powder format (no capsule), which is delivered with a scoop and mixed with colostrum for feeding to calves. During the fourth quarter of 2011, Milk Products, LLC of Chilton, Wisconsin launched commercial sales of their product, Ultra StartÒ 150 Plus, and other private label brands of colostrum replacers with First Defense TechnologyTM Inside. During the first quarter of 2012, we initiated a limited launch of a tube delivery format of our First Defense TechnologyTM in a gel solution. Sales of these new product formats have increased steadily since launch.

| - 18 - |

ImmuCell Corporation

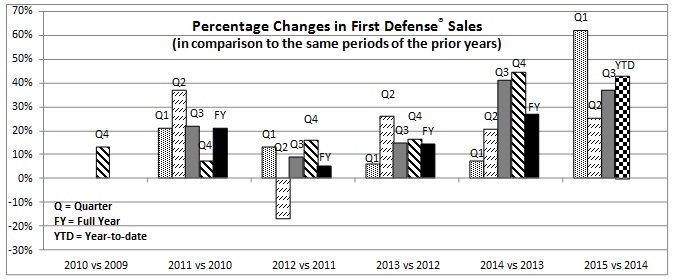

Sales of First DefenseÒ and related product line extensions aggregated 88% and 90% of our total product sales during the three-month periods ended September 30, 2015 and 2014, respectively. These sales increased by 37%, or $585,000, during the three-month period ended September 30, 2015 in comparison to the same period in 2014. These sales aggregated 92% and 90% of our total product sales during the nine-month periods ended September 30, 2015 and 2014, respectively. These sales increased by 43%, or $2,079,000, during the nine-month period ended September 30, 2015 in comparison to the same period in 2014. Sales of First DefenseÒ and related product line extensions increased by 27%, 14% and 5% during the years ended December 31, 2014, 2013 and 2012, respectively, in comparison to the immediately prior years. During the three-month period ended September 30, 2015, domestic sales of First DefenseÒ and related product line extensions increased by 45%, and international sales decreased by 22% in comparison to the three-month period ended September 30, 2014. During the nine-month period ended September 30, 2015, domestic sales of this product line increased by 45%, and international sales increased by 32% in comparison to the nine-month period ended September 30, 2014. This new level of sales demand has exceeded our current production capacity and available inventory, resulting in a backlog of orders as of September 30, 2015. We completed the investment to increase our liquid processing capacity by approximately 50% during the fourth quarter of 2015, and the investment to increase our freeze-drying capacity by approximately 100% is proceeding on schedule and is expected to be completed before the end of the first quarter of 2016. With the single exception of the second quarter of 2012, we have realized consistently positive sales growth of First DefenseÒ and related product line extensions during nineteen of the last twenty quarters (including the last thirteen consecutive quarters) in comparison to the same quarters of the prior year, as demonstrated in the following table:

We also sell topical wipes (our second leading source of animal health product sales) that are pre-moistened with a Nisin-based formulation in two product formats. Since 1999, we have been selling Wipe OutÒ Dairy Wipes for use in preparing the teat area of a cow for milking. We are competing aggressively on selling price against less expensive products and alternative teat sanitizing methods. We believe that the sales growth potential for Wipe OutÒ Dairy Wipes is limited. During the first quarter of 2013, we initiated sales of Nisin-based wipes for pets in a 120-count canister (Preva™ wipes) to Bayer HealthCare Animal Health of St. Joseph, Missouri for commercial sales to pet owners through their veterinarians. Sales of our topical wipes increased by 60% during the three-month period ended September 30, 2015 and decreased by 16% during the nine-month period ended September 30, 2015 in comparison to the same periods during 2014. Sales of our topical wipes aggregated approximately 4% and 3% of total product sales during the three-month and nine-month periods ending September 30, 2015, respectively.

Sales of our California Mastitis Test (CMT) (our third leading source of animal health product sales) decreased by 12% during the three-month period ended September 30, 2015 and increased by 41% during the nine-month period ended September 30, 2015 in comparison to the same periods during 2014. Sales of CMT aggregated approximately 1% and 2% of total product sales during the three-month and nine-month periods ended September 30, 2015, respectively.

We make and sell bulk reagents for Isolate™ (formerly known as Crypto-Scan®), which is a drinking water test that is sold by our distributor in Europe. Sales of Isolate™ increased by 46% during the nine-month period ended September 30, 2015 in comparison to the same period in 2014. Sales of these bulk reagents aggregated approximately 7% and 3% of total product sales during the three-month and nine-month periods ended September 30, 2015, respectively.

| - 19 - |

ImmuCell Corporation

Gross Margin

Changes in the gross margin from product sales are summarized in the following tables for the respective periods (in thousands, except for percentages):

For the Three-Month

Periods | Increase | |||||||||||||||

| 2015 | 2014 | Amount | % | |||||||||||||

| Gross margin | $ | 1,612 | $ | 1,078 | $ | 534 | 50 | % | ||||||||

| Percent of product sales | 65 | % | 61 | % | 4 | % | 7 | % | ||||||||

For

the Nine-Month Periods | Increase | |||||||||||||||

| 2015 | 2014 | Amount | % | |||||||||||||

| Gross margin | $ | 4,593 | $ | 3,106 | $ | 1,487 | 48 | % | ||||||||

| Percent of product sales | 61 | % | 58 | % | 3 | % | 6 | % | ||||||||

For the Twelve-Month Periods Ended September 30, | Increase | |||||||||||||||

| 2015 | 2014 | Amount | % | |||||||||||||

| Gross margin | $ | 5,936 | $ | 3,714 | $ | 2,222 | 60 | % | ||||||||

| Percent of product sales | 61 | % | 53 | % | 8 | % | 14 | % | ||||||||

Our objective for the foreseeable future is to maintain the full-year gross margin percentage over 50%, and we have achieved this objective during all of the periods being reported. The gross margin as a percentage of product sales was 59% and 51% during the years ended December 31, 2014 and 2013, respectively. We reduced production output during the last six months of 2013 in order to upgrade and increase our freeze-drying capacity by approximately 50%. During this period, we used more expensive subcontractors temporarily, which resulted in an increase in our cost of goods sold during that period. This production slow-down resulted in a few, short delays in shipping customer orders of First DefenseÒ during the first quarter of 2014. This investment was completed during the fourth quarter of 2013, and our gross margin percentage was again in line with historical norms during 2014. A number of other factors account for the variability in our costs, resulting in some fluctuations in gross margin percentages from quarter to quarter. The gross margin on First DefenseÒ is affected by biological yields from our raw material, which do vary over time. Like most U.S. manufacturers, we have been experiencing increases in the cost of raw materials that we purchase. The costs for production of First DefenseÒ and Wipe OutÒ Dairy Wipes have increased due to increased labor costs and other expenses associated with our efforts to sustain compliance with current Good Manufacturing Practice (cGMP) regulations in our production processes. We have been able to minimize the impact of these cost increases by implementing yield improvements. Product mix also affects gross margin in that we earn a higher gross margin on First DefenseÒ and a much lower gross margin on Wipe OutÒ Dairy Wipes.

Sales and Marketing Expenses

Sales and marketing expenses during the three-month period ended September 30, 2015 increased by approximately 2%, or $8,000, to $382,000 in comparison to $374,000 during the three-month period ended September 30, 2014, amounting to 15% and 21% of product sales during the 2015 and the 2014 periods, respectively. These expenses during the nine-month period ended September 30, 2015 increased by approximately 18%, or $165,000, to $1,087,000 in comparison to $922,000 during the nine-month period ended September 30, 2014, amounting to 14% and 17% of product sales during the 2015 and the 2014 periods, respectively. We continue to leverage the efforts of our small sales force by using veterinary distributors. These expenses have increased due principally to a strategic decision to invest more to grow First DefenseÒ sales. Our sales and marketing team currently consists of one vice president and five regional managers. Our inside sales and customer service representative performs most of the order entry and inside sales duties, and our facility manager processes most shipments. This investment may have created, at least in part, our recent increase in product sales. Our current budgetary objective in 2015 is to invest up to 20% of product sales in sales and marketing expenses on an annual basis.

Administrative Expenses

Administrative expenses were essentially unchanged at approximately $302,000 during the three-month periods ended September 30, 2015 and 2014. These expenses increased by approximately 8%, or $68,000, to $941,000 during the nine-month period ended September 30, 2015 as compared to $874,000 during the nine-month period ended September 30, 2014. We strive to be efficient with these expenses while funding costs associated with complying with the Sarbanes-Oxley Act of 2002 and other costs associated with being a publicly-held company. Prior to 2014, we had limited our investment in investor relations spending. Beginning in the second quarter of 2014, we initiated an investment in a more actively managed investor relations program. Additionally, we continue to provide full disclosure of the status of our business and financial condition in three quarterly reports and one annual report each year, as well as in Current Reports on Form 8-K when legally required or deemed appropriate by management. Additional information about us is available in our annual Proxy Statement. All of these reports are filed with the SEC and are available on-line or upon request to the Company.

| - 20 - |

ImmuCell Corporation

Product Development Expenses

Product development expenses decreased by 16%, or $59,000, to $302,000 during the three-month period ended September 30, 2015 as compared to $361,000 during the same period in 2014. These expenses decreased by 47%, or $812,000, to $904,000 during the nine-month period ended September 30, 2015 as compared to $1,716,000 during the same period in 2014. Product development expenses aggregated 12% and 20% of product sales during the three-month periods ended September 30, 2015 and 2014, and 12% and 32% of product sales during the nine-month periods ended September 30, 2015 and 2014, respectively. The majority of our product development budget is focused on the development of Mast OutÒ, a Nisin-based intramammary treatment of subclinical mastitis in lactating dairy cows. During the 15.75 year period that began on January 1, 2000 (the year we began the development of Mast OutÒ) and ended on September 30, 2015, we invested an aggregate of approximately $11,612,000 in the development of Mast OutÒ. This estimated allocation to Mast OutÒ reflects only direct expenses and includes no allocation of product development or administrative overhead expenses. Approximately $2,891,000 of this investment was offset by product licensing revenues and grant income related to Mast OutÒ.

Nisin, the same active ingredient contained in our topical wipe products, is an antibacterial peptide known to be effective against most Gram-positive and some Gram-negative bacteria. Nisin is a well characterized substance, having been used in food preservation applications for over 50 years. Food-grade Nisin, however, cannot be used in pharmaceutical applications because of its low purity. Our Nisin technology includes methods to achieve pharmaceutical-grade purity. In our pivotal effectiveness study of Mast OutÒ, statistically significant cure rates were associated with a statistically significant reduction in milk somatic cell count, which is an important measure of milk quality.