Attached files

| file | filename |

|---|---|

| 8-K - 8-K - COUSINS PROPERTIES INC | a8-k3q15.htm |

| EX-99.1 - EXHIBIT 99.1 - COUSINS PROPERTIES INC | a8-kpressreleaseex9913q15.htm |

Q3 2015 SUPPLEMENTAL INFORMATION

1

TABLE OF CONTENTS | ||

Key Performance Metrics | |

Funds From Operations - Detail | |

Portfolio Statistics | |

Office Leasing Activity | |

Office Lease Expirations | |

Top 20 Office Tenants | |

Tenant Industry Diversification | |

Investment Activity | |

Land Inventory | |

Debt Schedule | |

Non-GAAP Financial Measures - Calculations and Reconciliations | |

Non-GAAP Financial Measures - Discussion | |

Certain matters discussed in this news release are “forward-looking statements” within the meaning of the federal securities laws and are subject to uncertainties and risk. These include, but are not limited to, the availability and terms of capital and financing; the ability to refinance indebtedness as it matures; the failure of purchase, sale, or other contracts to ultimately close; the failure to achieve anticipated benefits from acquisitions or dispositions; the potential dilutive effect of any common stock offerings; the failure to achieve benefits from any repurchase of the Company's common stock; the availability of buyers and adequate pricing with respect to the disposition of assets; risks related to the geographic concentration of our portfolio, including (but not limited to) metropolitan Houston and Atlanta; risk related to the industry concentration of our portfolio, including (but not limited to) the energy industry; risks and uncertainties related to national and local economic conditions, the real estate industry in general, and the commercial real estate markets in particular; changes to the Company's strategy with regard to land and other non-core holdings that require impairment losses to be recognized; leasing risks, including the ability to obtain new tenants or renew expiring tenants, and the ability to lease newly developed and/or recently acquired space; the adverse change in the financial condition of one or more of its major tenants; volatility in interest rates and insurance rates; the availability of sufficient investment opportunities; competition from other developers or investors; the risks associated with real estate developments and acquisitions (such as zoning approval, receipts of required permits, construction delays, cost overruns, and leasing risk); the loss of key personnel; the potential liability for uninsured losses, condemnation, or environmental issues; the potential liability for a failure to meet regulatory requirements; the financial condition and liquidity of, or disputes with, joint venture partners; any failure to comply with debt covenants under credit agreements; any failure to continue to qualify for taxation as a real estate investment trust; and other risks detailed from time to time in the Company’s filings with the Securities and Exchange Commission, including those described in Part I, Item 1A of the Company’s Annual Report on Form 10-K/A for the year ended December 31, 2014. The words “believes,” “expects,” “anticipates,” “estimates,” "plans,” “may,” “intend,” “will,” or similar expressions are intended to identify forward-looking statements. Although the Company believes that its plans, intentions and expectations reflected in any forward-looking statement are reasonable, the Company can give no assurance that such plans, intentions or expectations will be achieved. Such forward-looking statements are based on current expectations and speak as of the date of such statements. The Company undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of future events, new information or otherwise, except as required under U.S. federal securities laws.

Cousins Properties Incorporated | Q3 2015 Supplemental Information | |

KEY PERFORMANCE METRICS | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

Property Statistics | ||||||||||||||||||||

Consolidated Operating Properties | 14 | 13 | 13 | 13 | 12 | 12 | 13 | 13 | 12 | 12 | ||||||||||

Consolidated Rentable Square Feet (in thousands) | 12,255 | 12,132 | 12,132 | 12,633 | 13,034 | 13,034 | 13,407 | 13,407 | 12,563 | 12,563 | ||||||||||

Unconsolidated Operating Properties | 9 | 9 | 9 | 9 | 5 | 5 | 5 | 5 | 6 | 6 | ||||||||||

Unconsolidated Rentable Square Feet (in thousands) | 3,468 | 3,468 | 3,468 | 3,468 | 3,129 | 3,129 | 3,129 | 3,129 | 3,431 | 3,431 | ||||||||||

Total Operating Properties | 23 | 22 | 22 | 22 | 17 | 17 | 18 | 18 | 18 | 18 | ||||||||||

Total Rentable Square Feet (in thousands) | 15,723 | 15,600 | 15,600 | 16,101 | 16,163 | 16,163 | 16,536 | 16,536 | 15,994 | 15,994 | ||||||||||

Office Leasing Activity (1) | ||||||||||||||||||||

Net Leased during the period (square feet in thousands) | 1,256 | 369 | 317 | 550 | 637 | 1,874 | 441 | 521 | 770 | 1,732 | ||||||||||

Net Rent (per square foot) | $18.54 | $21.05 | $22.39 | $22.99 | $24.10 | $22.88 | $18.93 | $23.23 | $23.42 | $21.44 | ||||||||||

Total Leasing Costs (per square foot) | (5.25) | (5.91) | (5.02) | (6.18) | (5.54) | (5.71) | (4.62) | (6.27) | (5.83) | (5.64) | ||||||||||

Net Effective Rent (per square foot) | $13.29 | $15.14 | $17.37 | $16.81 | $18.56 | $17.17 | $14.31 | $16.96 | $17.59 | $15.80 | ||||||||||

Change in Second Generation Net Rent | 12.9 | % | 12.7 | % | 48.4 | % | 36.3 | % | 43.8 | % | 38.0 | % | 33.6 | % | 43.8 | % | 28.1 | % | 36.2 | % |

Change in Cash-Basis Second Generation Net Rent | (3.6 | )% | (0.4 | )% | 33.3 | % | 7.6 | % | 27.7 | % | 19.7 | % | 8.0 | % | 32.8 | % | 14.1 | % | 18.9 | % |

Same Property Information (2) | ||||||||||||||||||||

Percent Leased (period end) | 90.7 | % | 90.7 | % | 91.0 | % | 91.6 | % | 91.2 | % | 91.2 | % | 91.7 | % | 91.7 | % | 91.8 | % | 91.8 | % |

Weighted Average Occupancy | 90.1 | % | 89.9 | % | 89.8 | % | 89.9 | % | 89.3 | % | 89.7 | % | 91.5 | % | 90.4 | % | 90.6 | % | 90.6 | % |

Change in Net Operating Income (over prior year period) | 4.6 | % | 2.2 | % | 7.7 | % | 3.6 | % | 0.6 | % | 3.6 | % | 5.2 | % | 1.6 | % | 1.1 | % | 2.6 | % |

Change in Cash-Basis Net Operating Income (over prior year period) | 3.9 | % | 10.2 | % | 15.0 | % | 12.8 | % | 11.1 | % | 12.3 | % | 15.9 | % | 5.2 | % | 1.2 | % | 7.0 | % |

Development Pipeline | ||||||||||||||||||||

Estimated Project Costs (in thousands) (3) | $283,600 | $181,075 | $181,075 | $182,575 | $226,575 | $226,575 | $100,475 | $161,975 | $306,500 | $306,500 | ||||||||||

Estimated Project Costs (3) / Total Undepreciated Assets | 9.8 | % | 6.1 | % | 6.0 | % | 5.6 | % | 6.6 | % | 6.6 | % | 2.9 | % | 4.6 | % | 8.6 | % | 8.6 | % |

Market Capitalization (4) | ||||||||||||||||||||

Common Stock Price (period end) | $10.30 | $11.47 | $12.45 | $11.95 | $11.42 | $11.42 | $10.60 | $10.38 | $9.22 | $9.22 | ||||||||||

Common Shares Outstanding (period end in thousands) | 189,666 | 198,423 | 198,474 | 216,509 | 216,513 | 216,513 | 216,470 | 216,686 | 214,671 | 214,671 | ||||||||||

Equity Market Capitalization (in thousands) | $1,953,560 | $2,275,912 | $2,471,001 | $2,587,283 | $2,472,578 | $2,472,578 | $2,294,582 | $2,249,201 | $1,979,267 | $1,979,267 | ||||||||||

Preferred Stock (in thousands) | 94,775 | 94,775 | — | — | — | — | — | — | — | — | ||||||||||

Debt (in thousands) | 858,583 | 814,016 | 890,093 | 895,618 | 1,007,502 | 1,007,502 | 1,067,376 | 1,075,013 | 1,006,764 | 1,006,764 | ||||||||||

Total Market Capitalization (in thousands) | $2,906,918 | $3,184,703 | $3,361,094 | $3,482,901 | $3,480,080 | $3,480,080 | $3,361,958 | $3,324,214 | $2,986,031 | $2,986,031 | ||||||||||

Cousins Properties Incorporated | 3 | Q3 2015 Supplemental Information |

KEY PERFORMANCE METRICS | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

Credit Ratios (4) | ||||||||||||||||||||

Debt/Total Market Capitalization | 29.5 | % | 25.6 | % | 26.5 | % | 25.7 | % | 29.0 | % | 29.0 | % | 31.7 | % | 32.3 | % | 33.7 | % | 33.7 | % |

Debt/Total Undepreciated Assets | 30.0 | % | 27.6 | % | 29.5 | % | 27.5 | % | 29.5 | % | 29.5 | % | 30.7 | % | 30.5 | % | 28.3 | % | 28.3 | % |

Fixed Charges Coverage | 2.64 | 3.56 | 4.00 | 4.61 | 4.98 | 4.27 | 4.67 | 4.54 | 5.19 | 4.80 | ||||||||||

Debt/Annualized EBITDA | 4.72 | 4.31 | 4.48 | 4.37 | 4.05 | 4.05 | 4.77 | 4.86 | 4.02 | 4.34 | ||||||||||

Dividend Information (4) | ||||||||||||||||||||

Common Dividend per Share | $0.18 | $0.075 | $0.075 | $0.075 | $0.075 | $0.30 | $0.08 | $0.08 | $0.08 | $0.24 | ||||||||||

FFO Payout Ratio | 35.3 | % | 39.3 | % | 41.6 | % | 39.0 | % | 31.4 | % | 37.3 | % | 37.8 | % | 38.3 | % | 33.0 | % | 36.2 | % |

FAD Payout Ratio | 61.6 | % | 61.1 | % | 69.4 | % | 68.9 | % | 51.1 | % | 61.6 | % | 67.8 | % | 71.5 | % | 54.8 | % | 63.9 | % |

Operations Ratios (4) | ||||||||||||||||||||

Annualized General and Administrative Expenses/Total Undepreciated Assets | 0.76 | % | 0.76 | % | 0.76 | % | 0.62 | % | 0.40 | % | 0.58 | % | 0.40 | % | 0.67 | % | 0.33 | % | 0.47 | % |

Additional Information (4) | ||||||||||||||||||||

Straight Line Rental Revenue | $12,826 | $7,648 | $5,001 | $4,169 | $5,275 | $22,093 | $6,285 | $5,786 | $4,623 | $16,694 | ||||||||||

Above and Below Market Rents Amortization | $3,785 | $1,952 | $2,027 | $1,933 | $2,135 | $8,047 | $2,030 | $1,973 | $2,030 | $6,033 | ||||||||||

Second Generation Capital Expenditures | $16,414 | $3,295 | $7,317 | $12,023 | $12,419 | $35,054 | $12,020 | $13,259 | $14,208 | $39,487 | ||||||||||

(1) See Office Leasing Activity on page 13 herein for additional detail and explanations.

(2) Same Property Information is derived from the pool of office properties, as defined, in the period originally reported. See Same Property Performance on page 12 and Non-GAAP Financial Measures - Calculations and Reconciliations on page 25 for additional information.

(3) Cousins' share of development expenditures.

(4) See Non-GAAP Financial Measures - Calculations and Reconciliations.

Cousins Properties Incorporated | 4 | Q3 2015 Supplemental Information |

KEY PERFORMANCE METRICS | ||

(1) Total rentable square feet is based on the total portfolio.

(2) Office properties only.

Note: See additional information included herein for calculations, definitions, and reconciliations to GAAP financial measures.

Cousins Properties Incorporated | 5 | Q3 2015 Supplemental Information |

FUNDS FROM OPERATIONS - SUMMARY | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

(in thousands, except per share amounts) | ||||||||||||||||||||

Net Operating Income | ||||||||||||||||||||

Office | 122,503 | 47,598 | 48,821 | 52,691 | 57,441 | 206,551 | 56,734 | 59,269 | 59,328 | 175,331 | ||||||||||

Other | 15,577 | 2,420 | 2,467 | 2,421 | 1,812 | 9,122 | 1,319 | 1,505 | 1,488 | 4,312 | ||||||||||

Total Net Operating Income | 138,080 | 50,018 | 51,288 | 55,112 | 59,253 | 215,673 | 58,053 | 60,774 | 60,816 | 179,643 | ||||||||||

Sales Less Cost of Sales | 1,464 | 160 | 1,373 | 82 | 2,295 | 3,910 | 810 | (324 | ) | 3,016 | 3,502 | |||||||||

Fee Income | 10,890 | 2,339 | 2,025 | 1,803 | 6,353 | 12,520 | 1,816 | 1,704 | 1,686 | 5,206 | ||||||||||

Other Income | 8,693 | 1,943 | 2,484 | 559 | 415 | 5,401 | 407 | 238 | 845 | 1,490 | ||||||||||

Reimbursed Expenses | (5,216 | ) | (932 | ) | (988 | ) | (783 | ) | (949 | ) | (3,652 | ) | (1,111 | ) | (717 | ) | (686 | ) | (2,514 | ) |

General and Administrative Expenses | (21,940 | ) | (5,695 | ) | (5,756 | ) | (5,022 | ) | (3,499 | ) | (19,972 | ) | (3,595 | ) | (5,936 | ) | (2,971 | ) | (12,502 | ) |

Interest Expense | (29,672 | ) | (9,012 | ) | (8,813 | ) | (8,660 | ) | (9,989 | ) | (36,474 | ) | (9,498 | ) | (9,696 | ) | (9,518 | ) | (28,712 | ) |

Other Expenses | (11,217 | ) | (678 | ) | (917 | ) | (1,170 | ) | (2,059 | ) | (4,824 | ) | (476 | ) | (431 | ) | (307 | ) | (1,214 | ) |

Income Tax Benefit (Provision) | 23 | 12 | 9 | (1 | ) | — | 20 | — | — | — | — | |||||||||

Depreciation and Amortization of Non-Real Estate Assets | (787 | ) | (196 | ) | (213 | ) | (244 | ) | (260 | ) | (913 | ) | (471 | ) | (374 | ) | (414 | ) | (1,259 | ) |

Preferred Stock Dividends and Original Issuance Costs | (12,664 | ) | (1,777 | ) | (4,708 | ) | — | — | (6,485 | ) | — | — | — | — | ||||||

FFO | 77,134 | 36,182 | 35,784 | 41,676 | 51,560 | 165,204 | 45,935 | 45,238 | 52,467 | 143,640 | ||||||||||

Weighted Average Shares - Basic | 144,255 | 191,739 | 198,440 | 209,839 | 216,511 | 204,216 | 216,568 | 216,630 | 216,261 | 216,485 | ||||||||||

Weighted Average Shares - Diluted | 144,420 | 191,952 | 198,702 | 210,111 | 216,733 | 204,460 | 216,754 | 216,766 | 216,374 | 216,625 | ||||||||||

FFO per Share - Basic and Diluted | 0.53 | 0.19 | 0.18 | 0.20 | 0.24 | 0.81 | 0.21 | 0.21 | 0.24 | 0.66 | ||||||||||

Cousins Properties Incorporated | 6 | Q3 2015 Supplemental Information |

FUNDS FROM OPERATIONS - DETAIL | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

(in thousands, except per share amounts) | ||||||||||||||||||||

Net Operating Income | ||||||||||||||||||||

Office Consolidated Properties | ||||||||||||||||||||

Greenway Plaza | 24,606 | 18,202 | 19,295 | 20,356 | 19,526 | 77,379 | 18,403 | 18,916 | 19,544 | 56,863 | ||||||||||

Post Oak Central | 15,593 | 5,564 | 5,886 | 6,032 | 5,955 | 23,437 | 6,675 | 6,516 | 6,495 | 19,686 | ||||||||||

Northpark Town Center | — | — | — | — | 5,794 | 5,794 | 5,825 | 5,651 | 5,127 | 16,603 | ||||||||||

191 Peachtree Tower | 16,040 | 4,198 | 4,650 | 4,115 | 4,046 | 17,009 | 4,082 | 4,060 | 4,173 | 12,315 | ||||||||||

Fifth Third Center | — | — | — | 2,196 | 3,435 | 5,631 | 3,641 | 3,709 | 3,770 | 11,120 | ||||||||||

Promenade | 9,568 | 2,772 | 2,792 | 3,030 | 2,841 | 11,435 | 3,542 | 3,581 | 3,623 | 10,746 | ||||||||||

The American Cancer Society Center | 11,539 | 2,992 | 3,022 | 3,329 | 3,030 | 12,373 | 3,114 | 3,206 | 3,039 | 9,359 | ||||||||||

Colorado Tower | — | — | — | — | — | — | 328 | 1,797 | 2,268 | 4,393 | ||||||||||

816 Congress Avenue | 4,029 | 1,536 | 1,740 | 1,862 | 1,854 | 6,992 | 1,858 | 2,117 | 2,156 | 6,131 | ||||||||||

North Point Center East | 5,909 | 1,606 | 1,564 | 1,471 | 1,435 | 6,076 | 1,537 | 1,633 | 1,691 | 4,861 | ||||||||||

Meridian Mark Plaza | 4,111 | 908 | 1,008 | 898 | 914 | 3,728 | 918 | 954 | 946 | 2,818 | ||||||||||

The Points at Waterview | 1,876 | 415 | 329 | 348 | 356 | 1,448 | 410 | 507 | 486 | 1,403 | ||||||||||

Other (2) | 9,353 | 4,032 | 3,380 | 4,139 | 3,740 | 15,291 | 1,770 | 2,133 | 1,366 | 5,269 | ||||||||||

Subtotal - Office Consolidated | 102,624 | 42,225 | 43,666 | 47,776 | 52,926 | 186,593 | 52,103 | 54,780 | 54,684 | 161,567 | ||||||||||

Office Unconsolidated Properties | ||||||||||||||||||||

Terminus 100 | 6,892 | 1,973 | 1,875 | 1,831 | 1,876 | 7,555 | 1,922 | 1,754 | 1,780 | 5,456 | ||||||||||

Terminus 200 | 4,278 | 1,235 | 1,466 | 1,449 | 1,354 | 5,504 | 1,436 | 1,442 | 1,575 | 4,453 | ||||||||||

Emory University Hospital Midtown Medical Office Tower | 3,874 | 998 | 962 | 1,008 | 992 | 3,960 | 987 | 996 | 992 | 2,975 | ||||||||||

Gateway Village (1) | 1,208 | 302 | 302 | 302 | 302 | 1,208 | 302 | 302 | 302 | 906 | ||||||||||

Other | (61 | ) | (15 | ) | (12 | ) | (15 | ) | (9 | ) | (51 | ) | (5 | ) | (5 | ) | (5 | ) | (15 | ) |

Subtotal - Office Unconsolidated | 16,191 | 4,493 | 4,593 | 4,575 | 4,515 | 18,176 | 4,642 | 4,489 | 4,644 | 13,775 | ||||||||||

Discontinued Operations | 3,688 | 880 | 562 | 340 | — | 1,782 | (11 | ) | — | — | (11 | ) | ||||||||

Total Office Net Operating Income | 122,503 | 47,598 | 48,821 | 52,691 | 57,441 | 206,551 | 56,734 | 59,269 | 59,328 | 175,331 | ||||||||||

Other | ||||||||||||||||||||

Consolidated Properties (2) | 1,293 | 402 | 407 | 396 | 178 | 1,383 | (24 | ) | 12 | — | (12 | ) | ||||||||

Unconsolidated Properties | ||||||||||||||||||||

Emory Point Apartments (Phase 1) | 2,300 | 1,118 | 1,181 | 1,200 | 1,148 | 4,647 | 1,071 | 1,244 | 1,213 | 3,528 | ||||||||||

Emory Point Retail (Phase 1) | 1,211 | 321 | 312 | 257 | 190 | 1,080 | 281 | 255 | 222 | 758 | ||||||||||

Emory Point Retail (Phase 2) | — | — | — | — | — | — | — | — | 56 | 56 | ||||||||||

Emory Point Apartments (Phase 2) (3) | — | — | — | — | — | — | — | — | 1 | 1 | ||||||||||

Other (2) | 8,061 | 567 | 562 | 569 | 295 | 1,993 | (6 | ) | (6 | ) | (4 | ) | (16 | ) | ||||||

Subtotal - Other | 11,572 | 2,006 | 2,055 | 2,026 | 1,633 | 7,720 | 1,346 | 1,493 | 1,488 | 4,327 | ||||||||||

Discontinued Operations | 2,712 | 12 | 5 | (1 | ) | 1 | 19 | (3 | ) | — | — | (3 | ) | |||||||

Total Other Net Operating Income | 15,577 | 2,420 | 2,467 | 2,421 | 1,812 | 9,122 | 1,319 | 1,505 | 1,488 | 4,312 | ||||||||||

Total Net Operating Income | 138,080 | 50,018 | 51,288 | 55,112 | 59,253 | 215,673 | 58,053 | 60,774 | 60,816 | 179,643 | ||||||||||

Cousins Properties Incorporated | 7 | Q3 2015 Supplemental Information |

FUNDS FROM OPERATIONS - DETAIL | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

(in thousands, except per share amounts) | ||||||||||||||||||||

Sales Less Cost of Sales | ||||||||||||||||||||

Land Sales Less Cost of Sales - Consolidated | 1,353 | 160 | 1,326 | 82 | 135 | 1,703 | 810 | (566 | ) | 978 | 1,222 | |||||||||

Land Sales Less Cost of Sales - Unconsolidated | 111 | — | 47 | — | 2,160 | 2,207 | — | 242 | 2,038 | 2,280 | ||||||||||

Total Sales Less Cost of Sales | 1,464 | 160 | 1,373 | 82 | 2,295 | 3,910 | 810 | (324 | ) | 3,016 | 3,502 | |||||||||

Fee Income | ||||||||||||||||||||

Management Fees (3) | 7,223 | 1,315 | 1,446 | 1,203 | 1,118 | 5,082 | 1,503 | 1,184 | 1,128 | 3,815 | ||||||||||

Development Fees | 3,102 | 937 | 541 | 571 | 5,216 | 7,265 | 308 | 461 | 531 | 1,300 | ||||||||||

Leasing & Other Fees | 565 | 87 | 38 | 29 | 19 | 173 | 5 | 59 | 27 | 91 | ||||||||||

Total Fee Income | 10,890 | 2,339 | 2,025 | 1,803 | 6,353 | 12,520 | 1,816 | 1,704 | 1,686 | 5,206 | ||||||||||

Other Income | ||||||||||||||||||||

Termination Fees | 2,952 | 1,843 | 2,210 | 280 | 240 | 4,573 | 193 | 28 | 499 | 720 | ||||||||||

Termination Fees - Discontinued Operations | — | — | 2 | — | — | 2 | — | — | — | |||||||||||

Interest and Other Income | 5,213 | 72 | 44 | 116 | 29 | 261 | 55 | 22 | 222 | 299 | ||||||||||

Interest and Other Income - Discontinued Operations | 15 | — | — | 8 | (4 | ) | 4 | — | — | — | — | |||||||||

Other - Unconsolidated | 513 | 28 | 228 | 155 | 150 | 561 | 159 | 188 | 124 | 471 | ||||||||||

Total Other Income | 8,693 | 1,943 | 2,484 | 559 | 415 | 5,401 | 407 | 238 | 845 | 1,490 | ||||||||||

Reimbursed Expenses | (5,216 | ) | (932 | ) | (988 | ) | (783 | ) | (949 | ) | (3,652 | ) | (1,111 | ) | (717 | ) | (686 | ) | (2,514 | ) |

General and Administrative Expenses | (22,460 | ) | (5,695 | ) | (5,756 | ) | (5,022 | ) | (3,499 | ) | (19,972 | ) | (3,595 | ) | (5,936 | ) | (2,971 | ) | (12,502 | ) |

Interest Expense | ||||||||||||||||||||

Consolidated Debt | ||||||||||||||||||||

The American Cancer Society Center | (8,813 | ) | (2,158 | ) | (2,175 | ) | (2,192 | ) | (2,185 | ) | (8,710 | ) | (2,131 | ) | (2,147 | ) | (2,164 | ) | (6,442 | ) |

Post Oak Central | (2,618 | ) | (2,044 | ) | (2,036 | ) | (2,028 | ) | (2,019 | ) | (8,127 | ) | (2,010 | ) | (2,001 | ) | (1,992 | ) | (6,003 | ) |

Promenade | (1,568 | ) | (1,223 | ) | (1,216 | ) | (1,209 | ) | (1,202 | ) | (4,850 | ) | (1,194 | ) | (1,187 | ) | (1,180 | ) | (3,561 | ) |

Unsecured Credit Facility | (2,260 | ) | (575 | ) | (616 | ) | (705 | ) | (1,458 | ) | (3,354 | ) | (966 | ) | (1,072 | ) | (1,089 | ) | (3,127 | ) |

191 Peachtree Tower | (3,483 | ) | (861 | ) | (861 | ) | (861 | ) | (861 | ) | (3,444 | ) | (861 | ) | (861 | ) | (861 | ) | (2,583 | ) |

816 Congress Avenue | — | — | — | — | (709 | ) | (709 | ) | (817 | ) | (818 | ) | (817 | ) | (2,452 | ) | ||||

Meridian Mark Plaza | (1,587 | ) | (393 | ) | (391 | ) | (390 | ) | (388 | ) | (1,562 | ) | (387 | ) | (385 | ) | (384 | ) | (1,156 | ) |

The Points at Waterview | (903 | ) | (221 | ) | (219 | ) | (217 | ) | (215 | ) | (872 | ) | (213 | ) | (211 | ) | (209 | ) | (633 | ) |

Other | (995 | ) | (65 | ) | (66 | ) | (65 | ) | (38 | ) | (234 | ) | — | — | — | — | ||||

Capitalized | 518 | 373 | 610 | 850 | 919 | 2,752 | 903 | 813 | 1,023 | 2,739 | ||||||||||

Subtotal - Consolidated | (21,709 | ) | (7,167 | ) | (6,970 | ) | (6,817 | ) | (8,156 | ) | (29,110 | ) | (7,676 | ) | (7,869 | ) | (7,673 | ) | (23,218 | ) |

Unconsolidated Debt | ||||||||||||||||||||

Terminus 100 | (3,193 | ) | (879 | ) | (875 | ) | (872 | ) | (868 | ) | (3,494 | ) | (865 | ) | (861 | ) | (857 | ) | (2,583 | ) |

Terminus 200 | (1,369 | ) | (390 | ) | (390 | ) | (390 | ) | (390 | ) | (1,560 | ) | (390 | ) | (390 | ) | (390 | ) | (1,170 | ) |

Emory University Hospital Midtown Medical Office Tower | (1,358 | ) | (334 | ) | (334 | ) | (334 | ) | (334 | ) | (1,336 | ) | (334 | ) | (334 | ) | (333 | ) | (1,001 | ) |

Emory Point | (867 | ) | (242 | ) | (244 | ) | (247 | ) | (241 | ) | (974 | ) | (233 | ) | (242 | ) | (265 | ) | (740 | ) |

Other | (1,176 | ) | — | — | — | — | — | — | — | — | — | |||||||||

Subtotal - Unconsolidated | (7,963 | ) | (1,845 | ) | (1,843 | ) | (1,843 | ) | (1,833 | ) | (7,364 | ) | (1,822 | ) | (1,827 | ) | (1,845 | ) | (5,494 | ) |

Total Interest Expense | (29,672 | ) | (9,012 | ) | (8,813 | ) | (8,660 | ) | (9,989 | ) | (36,474 | ) | (9,498 | ) | (9,696 | ) | (9,518 | ) | (28,712 | ) |

Cousins Properties Incorporated | 8 | Q3 2015 Supplemental Information |

FUNDS FROM OPERATIONS - DETAIL | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

(in thousands, except per share amounts) | ||||||||||||||||||||

Other Expenses | ||||||||||||||||||||

Noncontrolling Interests | (1,671 | ) | (156 | ) | (129 | ) | (92 | ) | (47 | ) | (424 | ) | — | — | — | — | ||||

Property Taxes and Other Holding Costs | (1,570 | ) | (271 | ) | (276 | ) | (288 | ) | (388 | ) | (1,223 | ) | (287 | ) | (242 | ) | (141 | ) | (670 | ) |

Predevelopment & Other | (492 | ) | (229 | ) | (363 | ) | (146 | ) | (1,309 | ) | (2,047 | ) | (106 | ) | (187 | ) | (147 | ) | (440 | ) |

Acquisition and Related Costs | (7,484 | ) | (22 | ) | (149 | ) | (644 | ) | (315 | ) | (1,130 | ) | (83 | ) | (2 | ) | (19 | ) | (104 | ) |

Total Other Expenses | (11,217 | ) | (678 | ) | (917 | ) | (1,170 | ) | (2,059 | ) | (4,824 | ) | (476 | ) | (431 | ) | (307 | ) | (1,214 | ) |

Income Tax Provision (Benefit) | 23 | 12 | 9 | (1 | ) | — | 20 | — | — | — | — | |||||||||

Depreciation and Amortization of Non-Real Estate Assets | ||||||||||||||||||||

Consolidated | (753 | ) | (185 | ) | (201 | ) | (232 | ) | (249 | ) | (867 | ) | (423 | ) | (374 | ) | (414 | ) | (1,211 | ) |

Unconsolidated | (34 | ) | (11 | ) | (12 | ) | (12 | ) | (11 | ) | (46 | ) | (48 | ) | — | — | (48 | ) | ||

Total Non-Real Estate Depreciation and Amoritization | (787 | ) | (196 | ) | (213 | ) | (244 | ) | (260 | ) | (913 | ) | (471 | ) | (374 | ) | (414 | ) | (1,259 | ) |

Preferred Stock Dividends and Original Issuance Costs | (12,664 | ) | (1,777 | ) | (4,708 | ) | — | — | (6,485 | ) | — | — | — | — | ||||||

FFO | 77,134 | 36,182 | 35,784 | 41,676 | 51,560 | 165,204 | 45,935 | 45,238 | 52,467 | 143,640 | ||||||||||

Weighted Average Shares - Basic | 144,255 | 191,739 | 198,440 | 209,839 | 216,511 | 204,216 | 216,568 | 216,630 | 216,261 | 216,485 | ||||||||||

Weighted Average Shares - Diluted | 144,420 | 191,952 | 198,702 | 210,111 | 216,733 | 204,460 | 216,754 | 216,766 | 216,374 | 216,625 | ||||||||||

FFO per Share - Basic and Diluted | 0.53 | 0.19 | 0.18 | 0.20 | 0.24 | 0.81 | 0.21 | 0.21 | 0.24 | 0.66 | ||||||||||

Note: Amounts may differ slightly from other schedules contained herein due to rounding. | |||||||||||||||||

(1) The Company receives an 11.46% current return on its $10.4 million investment in Gateway Village and recognizes this amount as NOI from this venture. See Joint Venture Information included herein for further details. | |||||||||||||||||

(2) Represents NOI for properties sold in prior periods. | |||||||||||||||||

(3) Management Fees include reimbursement of expenses that are included in the "Reimbursed Expenses" line item. | |||||||||||||||||

Cousins Properties Incorporated | 9 | Q3 2015 Supplemental Information |

PORTFOLIO STATISTICS | ||

Company's Share | ||||||||||||||||||||||||||||||

Property Description | Metropolitan Area | Rentable Square Feet | Financial Statement Presentation | Company's Ownership Interest | End of Period Leased 3Q15 | End of Period Leased 2Q15 | Weighted Average Occupancy 3Q15 | Weighted Average Occupancy 2Q15 | % of Total Net Operating Income (1) | Property Level Debt ($000) | ||||||||||||||||||||

Office | ||||||||||||||||||||||||||||||

Greenway Plaza (2) | Houston | 4,348,000 | Consolidated | 100 | % | 89.3 | % | 89.6 | % | 88.8 | % | 89.4 | % | 33 | % | $ | — | |||||||||||||

Post Oak Central (2) | Houston | 1,280,000 | Consolidated | 100 | % | 96.0 | % | 95.2 | % | 95.1 | % | 95.2 | % | 11 | % | 182,618 | ||||||||||||||

Colorado Tower | Austin | 373,000 | Consolidated | 100 | % | 100.0 | % | 98.4 | % | 73.4 | % | 59.7 | % | 4 | % | — | ||||||||||||||

816 Congress | Austin | 435,000 | Consolidated | 100 | % | 95.2 | % | 94.4 | % | 85.1 | % | 85.7 | % | 3 | % | 85,000 | ||||||||||||||

The Points at Waterview (3) | Dallas | 203,000 | Consolidated | 100 | % | 92.0 | % | 92.0 | % | 92.0 | % | 92.0 | % | 1 | % | 14,171 | ||||||||||||||

Texas | 6,639,000 | 52 | % | 281,789 | ||||||||||||||||||||||||||

Northpark Town Center (2) | Atlanta | 1,528,000 | Consolidated | 100 | % | 85.2 | % | 88.0 | % | 86.0 | % | 91.1 | % | 9 | % | — | ||||||||||||||

191 Peachtree Tower | Atlanta | 1,225,000 | Consolidated | 100 | % | 93.9 | % | 93.8 | % | 88.7 | % | 86.2 | % | 7 | % | 100,000 | ||||||||||||||

Promenade | Atlanta | 777,000 | Consolidated | 100 | % | 94.2 | % | 93.5 | % | 90.6 | % | 89.9 | % | 6 | % | 108,899 | ||||||||||||||

The American Cancer Society Center | Atlanta | 996,000 | Consolidated | 100 | % | 86.5 | % | 84.0 | % | 86.5 | % | 84.4 | % | 5 | % | 129,794 | ||||||||||||||

Terminus 100 | Atlanta | 656,000 | Unconsolidated | 50 | % | 90.9 | % | 90.0 | % | 90.3 | % | 90.0 | % | 3 | % | 64,917 | ||||||||||||||

North Point Center East (2) | Atlanta | 540,000 | Consolidated | 100 | % | 92.1 | % | 95.8 | % | 92.6 | % | 93.3 | % | 3 | % | — | ||||||||||||||

Terminus 200 | Atlanta | 566,000 | Unconsolidated | 50 | % | 92.2 | % | 92.2 | % | 87.8 | % | 87.8 | % | 3 | % | 41,000 | ||||||||||||||

Meridian Mark Plaza | Atlanta | 160,000 | Consolidated | 100 | % | 97.7 | % | 97.8 | % | 97.9 | % | 98.2 | % | 2 | % | 25,088 | ||||||||||||||

Emory University Hospital Midtown Medical Office Tower | Atlanta | 358,000 | Unconsolidated | 50 | % | 98.8 | % | 100.0 | % | 100.0 | % | 100.0 | % | 2 | % | 37,322 | ||||||||||||||

Georgia | 6,806,000 | 40 | % | 507,020 | ||||||||||||||||||||||||||

Fifth Third Center | Charlotte | 698,000 | Consolidated | 100 | % | 93.9 | % | 85.1 | % | 83.6 | % | 82.7 | % | 6 | % | — | ||||||||||||||

Gateway Village | Charlotte | 1,065,000 | Unconsolidated | 50 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | — | % | 11,071 | ||||||||||||||

North Carolina | 1,763,000 | 6 | % | 11,071 | ||||||||||||||||||||||||||

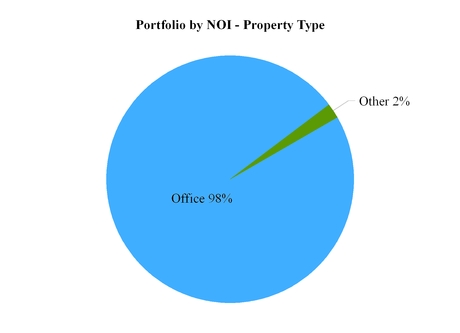

Total Office Properties | 15,208,000 | 98 | % | $ | 799,880 | |||||||||||||||||||||||||

Other | ||||||||||||||||||||||||||||||

Emory Point Apartments (Phase 1) (4) | Atlanta | 404,000 | Unconsolidated | 75 | % | 96.2 | % | 92.6 | % | 94.9 | % | 91.9 | % | 2 | % | $ | 36,123 | |||||||||||||

Emory Point Retail (Phase 1) | Atlanta | 80,000 | Unconsolidated | 75 | % | 76.8 | % | 82.0 | % | 80.9 | % | 82.0 | % | — | % | 7,399 | ||||||||||||||

Emory Point Retail (Phase 2) | Atlanta | 45,000 | Unconsolidated | 75 | % | 69.1 | % | — | % | 51.3 | % | — | % | — | % | 4,404 | ||||||||||||||

Emory Point Apartments (Phase 2) (4) | Atlanta | 257,000 | Unconsolidated | 75 | % | 34.2 | % | — | % | 24.2 | % | — | % | — | % | 24,958 | ||||||||||||||

Total Other | 786,000 | 2 | % | 72,884 | ||||||||||||||||||||||||||

Total Portfolio | 15,994,000 | 100 | % | $ | 872,764 | |||||||||||||||||||||||||

(1) | Net Operating Income represents the Company's share of rental property revenues less rental property operating expenses. Calculation is based on amounts for the three months ended September 30, 2015. | |||||||||||||||||||||||||||||

(2) | Contains multiple buildings that are grouped together for reporting purposes. | |||||||||||||||||||||||||||||

(3) | On October 1, 2015, The Points at Waterview mortgage note was repaid in full without penalty. | |||||||||||||||||||||||||||||

(4) | Phase 1 consists of 443 units and Phase 2 consists of 307 units. | |||||||||||||||||||||||||||||

Cousins Properties Incorporated | 10 | Q3 2015 Supplemental Information |

PORTFOLIO STATISTICS | ||

Cousins Properties Incorporated | 11 | Q3 2015 Supplemental Information |

SAME PROPERTY PERFORMANCE (1) | ||

Net Operating Income ($ in thousands) | |||||||||||||||||

Three Months Ended | |||||||||||||||||

September 30, 2015 | September 30, 2014 | June 30, 2015 | 3Q15 vs. 3Q14 % Change | 3Q15 vs. 2Q15 % Change | |||||||||||||

Property Revenues (2) | $ | 77,753 | $ | 76,899 | $ | 76,692 | 1.1 | % | 1.4 | % | |||||||

Property Operating Expenses (2) | 33,106 | 32,734 | 32,825 | 1.1 | % | 0.9 | % | ||||||||||

Property Net Operating Income | $ | 44,647 | $ | 44,165 | $ | 43,867 | 1.1 | % | 1.8 | % | |||||||

% of Total Property Net Operating Income | 73.4 | % | 80.1 | % | 72.2 | % | |||||||||||

Cash Basis Property Revenues (3) | $ | 74,181 | $ | 73,319 | $ | 72,772 | 1.2 | % | 1.9 | % | |||||||

Cash Basis Property Operating Expenses (4) | 33,093 | 32,736 | 32,831 | 1.1 | % | 0.8 | % | ||||||||||

Cash Basis Property Net Operating Income | $ | 41,088 | $ | 40,583 | $ | 39,941 | 1.2 | % | 2.9 | % | |||||||

% of Total Property Cash Basis Net Operating Income | 75.2 | % | 81.7 | % | 74.6 | % | |||||||||||

End of Period Leased | 91.8 | % | 93.4 | % | 91.7 | % | |||||||||||

Weighted Average Occupancy | 90.6 | % | 90.9 | % | 90.4 | % | |||||||||||

Nine Months Ended | |||||||||||||

September 30, 2015 | September 30, 2014 | % Change | |||||||||||

Property Revenues (2) | $ | 228,009 | $ | 222,370 | 2.5 | % | |||||||

Property Operating Expenses (2) | 96,168 | 93,894 | 2.4 | % | |||||||||

Property Net Operating Income | $ | 131,841 | $ | 128,476 | 2.6 | % | |||||||

Cash Basis Property Revenues (3) | $ | 216,003 | $ | 205,932 | 4.9 | % | |||||||

Cash Basis Property Operating Expenses (4) | 96,165 | 93,901 | 2.4 | % | |||||||||

Cash Basis Property Net Operating Income | $ | 119,838 | $ | 112,031 | 7.0 | % | |||||||

(1) | Same Properties include office properties that were operational and stabilized on January 1, 2014, excluding properties subsequently sold. Properties included in this reporting period are as follows: |

Greenway Plaza The American Cancer Society Center Terminus 200 | |

Post Oak Central Promenade Meridian Mark Plaza | |

The Points at Waterview Terminus 100 Emory University Hospital Midtown Medical Office Tower | |

191 Peachtree Tower North Point Center East Gateway Village | |

(2) | Property Revenues and Expenses include results for the Company and its share of unconsolidated joint ventures. |

(3) | Cash Basis Same Property Revenues include that of the Company and its share of unconsolidated joint ventures. It represents Property Revenues, excluding straight-line rents, amortization of lease inducements and amortization of acquired above and below market rents. |

(4) | Cash Basis Same Property Operating Expenses include that of the Company and its share of unconsolidated joint ventures. It represents Property Operating Expenses, excluding straight-line ground rent expense and amortization of above and below market ground rent expense. |

Cousins Properties Incorporated | 12 | Q3 2015 Supplemental Information |

OFFICE LEASING ACTIVITY(1) | ||

Three Months Ended September 30, 2015 | Nine Months Ended September 30, 2015 | ||||||||||||||||||||||||||||||

New | Renewal | Expansion | Total | New | Renewal | Expansion | Total | ||||||||||||||||||||||||

Gross leased (square feet) | 827,275 | 1,879,717 | |||||||||||||||||||||||||||||

Less: Leases less than one year, amenity leases, percentage rent leases, storage leases, intercompany leases, and license agreements | (57,266 | ) | (147,521) | ||||||||||||||||||||||||||||

Net leased (square feet) | 617,469 | 129,531 | 23,009 | 770,009 | 918,097 | 743,631 | 70,468 | 1,732,196 | |||||||||||||||||||||||

Number of transactions | 18 | 12 | 5 | 35 | 46 | 49 | 14 | 109 | |||||||||||||||||||||||

Lease term (years) (2)(3) | 5.88 | 9.13 | 7.42 | 7.48 | 7.71 | 6.43 | 5.80 | 6.84 | |||||||||||||||||||||||

Net rent (per square foot) (2)(3)(4) | $ | 22.56 | $ | 24.58 | $ | 21.85 | $ | 23.42 | $ | 21.98 | $ | 21.04 | $ | 22.39 | $ | 21.44 | |||||||||||||||

Total leasing costs (per square foot) (2)(3)(5) | (6.21 | ) | (5.28 | ) | (6.75 | ) | (5.83 | ) | (6.44 | ) | (5.13 | ) | (6.09 | ) | (5.64 | ) | |||||||||||||||

Net effective rent (per square foot) (2)(3) | $ | 16.35 | $ | 19.30 | $ | 15.10 | $ | 17.59 | $ | 15.54 | $ | 15.91 | $ | 16.30 | $ | 15.80 | |||||||||||||||

Second generation leased square feet (3)(6) | 182,124 | 894,621 | |||||||||||||||||||||||||||||

Increase in second generation net rent (3)(4)(6) | 28.1 | % | 36.2 | % | |||||||||||||||||||||||||||

Increase in cash basis second generation net rent(3)(6)(7) | 14.1 | % | 18.9 | % | |||||||||||||||||||||||||||

(1) Excludes apartment and retail leasing. | |||||||||||||||||||||||||||||||

(2) Excludes NCR lease of 485,000 square feet due to final financial terms not being determined until construction completion. | |||||||||||||||||||||||||||||||

(3) Weighted average. | |||||||||||||||||||||||||||||||

(4) Represents straight-lined net rent per square foot (operating expenses deducted from gross leases) over the lease term. | |||||||||||||||||||||||||||||||

(5) Includes tenant improvements, external leasing commissions, and free rent. | |||||||||||||||||||||||||||||||

(6) Excludes leases executed for spaces that were vacant upon acquisition, new leases in a development property, and leases for spaces that have been vacant for one year or more. | |||||||||||||||||||||||||||||||

(7) Represents increase in net rent at the end of term paid by the prior tenant compared to net rent at beginning of term paid by the current tenant. For early renewals, represents increase in net rent at the end of the term of the original lease compared to net rent at the beginning of the extended term of the lease. | |||||||||||||||||||||||||||||||

Cousins Properties Incorporated | 13 | Q3 2015 Supplemental Information |

OFFICE LEASE EXPIRATIONS | ||

Lease Expirations by Year

Year of Expiration | Square Feet Expiring (1) | % of Leased Space | Annual Contractual Rents ($000's) (1)(2) | % of Total Annual Contractual Rents | Annual Contractual Rent/Sq. Ft. (2) | ||||||||||||

2015 | 226,648 | 1.8 | % | $ | 3,508 | 1.1 | % | $ | 15.48 | ||||||||

2016 | 1,211,065 | 9.5 | % | 23,475 | 7.7 | % | 19.38 | ||||||||||

2017 | 896,752 | 7.1 | % | 19,251 | 6.3 | % | 21.47 | ||||||||||

2018 | 1,147,662 | 9.0 | % | 24,245 | 8.0 | % | 21.13 | ||||||||||

2019 | 1,094,785 | 8.6 | % | 27,304 | 9.0 | % | 24.94 | ||||||||||

2020 | 866,941 | 6.8 | % | 20,056 | 6.6 | % | 23.13 | ||||||||||

2021 | 1,157,918 | 9.1 | % | 29,122 | 9.5 | % | 25.15 | ||||||||||

2022 | 1,311,347 | 10.3 | % | 30,620 | 10.0 | % | 23.35 | ||||||||||

2023 | 1,568,191 | 12.4 | % | 35,423 | 11.6 | % | 22.59 | ||||||||||

2024 &Thereafter | 3,226,786 | 25.4 | % | 92,101 | 30.2 | % | 28.54 | ||||||||||

Total | 12,708,095 | 100.0 | % | $ | 305,105 | 100.0 | % | $ | 24.01 | ||||||||

Lease Expirations Greater than 100,000 Square Feet Through Year End 2018

Expiration Date | Tenant | Market | Building | Square Feet Expiring (1) | ||||||

December 2016 | Bank of America | Charlotte | Gateway Village | 514,396 | ||||||

December 2018 | Apache Corporation | Houston | Post Oak Central | 524,342 | ||||||

(1) Company's share.

(2) Annual Contractual Rent shown is the rate in the year of expiration. It includes the minimum contractual rent paid by the tenant which may or may not include a base year of operating expenses depending upon the terms of the lease.

Cousins Properties Incorporated | 14 | Q3 2015 Supplemental Information |

OFFICE LEASE EXPIRATIONS | ||

Note: Company's share

Cousins Properties Incorporated | 15 | Q3 2015 Supplemental Information |

TOP 20 OFFICE TENANTS | ||

Tenant (1) | Company's Share of Square Footage | Company's Share of Annualized Base Rent | Percentage of Total Company's Share of Annualized Base Rent (2) | Average Remaining Lease Term (Years) (3) | |||||

1 | Occidental Oil & Gas Corp. | 961,491 | $ | 18,366,458 | 7% | 11 | |||

2 | Apache Corporation | 524,342 | 9,092,950 | 4% | 3 | ||||

3 | Invesco Management Group, Inc. | 400,332 | 6,626,873 | 3% | 8 | ||||

4 | Bank of America (4) | 865,872 | 6,253,505 | 3% | 3 | ||||

5 | McGuire Woods, LLP | 198,648 | 5,617,946 | 2% | 11 | ||||

6 | Deloitte LLP | 259,998 | 5,397,558 | 2% | 9 | ||||

7 | Transocean Offshore Deepwater | 264,002 | 5,241,160 | 2% | 7 | ||||

8 | American Cancer Society, Inc. | 275,198 | 4,829,991 | 2% | 7 | ||||

9 | Smith Gambrell & Russell | 159,136 | 4,767,099 | 2% | 6 | ||||

10 | Stewart Information Services | 235,290 | 4,068,203 | 2% | 4 | ||||

11 | US South Communications | 219,659 | 3,977,498 | 2% | 6 | ||||

12 | Internap Network Services | 120,298 | 3,521,033 | 1% | 5 | ||||

13 | Direct Energy | 197,422 | 2,996,984 | 1% | 8 | ||||

14 | National Union Fire Insurance | 105,362 | 2,891,242 | 1% | 3 | ||||

15 | Northside Hospital | 99,185 | 2,855,822 | 1% | 7 | ||||

16 | MedAssets Supply Chain Systems, LLC | 120,660 | 2,717,827 | 1% | 15 | ||||

17 | Wells Fargo Bank, N.A. | 94,215 | 2,438,183 | 1% | 5 | ||||

18 | Gulf South Pipeline Company LP | 98,616 | 2,366,784 | 1% | 9 | ||||

19 | Parsley Energy, L.P. | 73,843 | 2,141,447 | 1% | 9 | ||||

20 | Emory University | 86,496 | 2,116,824 | 1% | 13 | ||||

Total Top 20 | 5,360,065 | $ | 98,285,387 | 40% | 7 | ||||

(1) | In some cases, the actual tenant may be an affiliate of the entity shown. | ||||||||

(2) | Annualized Base Rent represents the annualized minimum rent paid by the tenant as of the date of this report. If the tenant is in a free rent period as of the date of this report, Annualized Base Rent represents the annualized minimum contractual rent the tenant will pay in the first month it is required to pay rent which may or may not include a base year of operating expenses depending upon the terms of the lease. | ||||||||

(3) | Weighted average. | ||||||||

(4) | A portion of the Company's economic exposure for this tenant is limited to a fixed return through a joint venture arrangement. | ||||||||

Note: | This schedule includes tenants whose leases have commenced and/or have taken occupancy. Leases that have been signed but have not commenced are excluded from this schedule. | ||||||||

Cousins Properties Incorporated | 16 | Q3 2015 Supplemental Information |

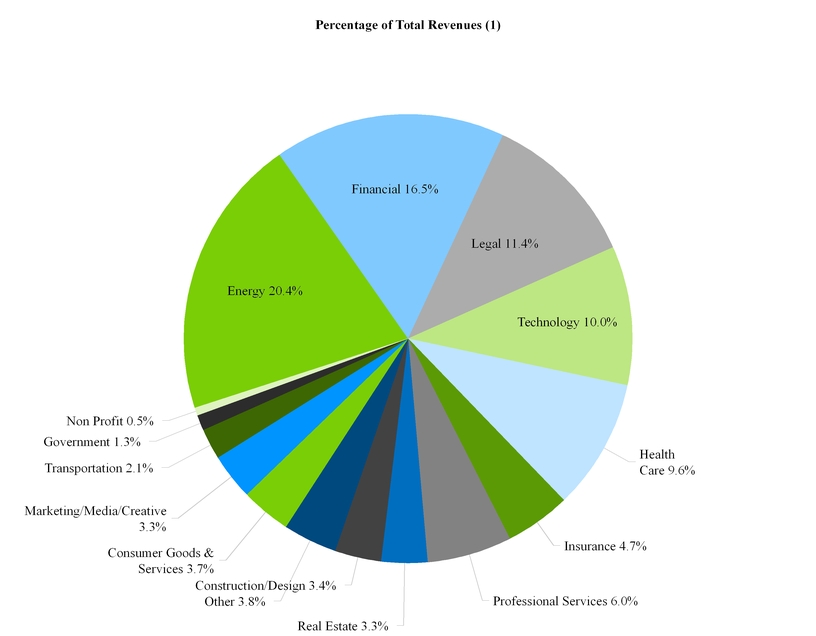

TENANT INDUSTRY DIVERSIFICATION | ||

(1) Based on total portfolio holdings.

Cousins Properties Incorporated | 17 | Q3 2015 Supplemental Information |

INVESTMENT ACTIVITY | ||

Completed Property Acquisitions

Property | Type | Metropolitan Area | Company's Ownership Interest | Timing | Square Feet | Gross Purchase Price ($ in thousands) | |||||||||

2014 | |||||||||||||||

Fifth Third Center | Office | Charlotte | 100.0% | 3Q | 698,000 | $ | 215,000 | ||||||||

Northpark Town Center | Office | Atlanta | 100.0% | 4Q | 1,528,000 | 348,000 | |||||||||

2013 | |||||||||||||||

Post Oak Central | Office | Houston | 100.0% | 1Q | 1,280,000 | 230,900 | |||||||||

Terminus 200 | Office | Atlanta | 50.0% | 1Q | 566,000 | 164,000 | |||||||||

816 Congress | Office | Austin | 100.0% | 2Q | 435,000 | 102,400 | |||||||||

Greenway Plaza | Office | Houston | 100.0% | 3Q | 4,348,000 | 950,000 | |||||||||

777 Main | Office | Fort Worth | 100.0% | 3Q | 980,000 | 160,000 | |||||||||

2012 | |||||||||||||||

2100 Ross | Office | Dallas | 100.0% | 3Q | 844,000 | 59,200 | |||||||||

2011 | |||||||||||||||

Promenade | Office | Atlanta | 100.0% | 4Q | 775,000 | 134,700 | |||||||||

11,454,000 | $ | 2,364,200 | |||||||||||||

Completed Property Developments

Project | Type | Metropolitan Area | Company's Ownership Interest | Timing | Square Feet | Project Cost ($ in thousands) | |||||||||

2015 | |||||||||||||||

Colorado Tower | Office | Austin | 100.0% | 1Q | 373,000 | $ | 126,100 | ||||||||

Emory Point - Phase 2 | Mixed | Atlanta | 75.0% | 3Q | 302,000 | 75,400 | |||||||||

2013 | |||||||||||||||

Emory Point - Phase 1 | Mixed | Atlanta | 75.0% | 4Q | 484,000 | 102,300 | |||||||||

2012 | |||||||||||||||

Mahan Village | Retail | Tallahassee | 50.5% | 4Q | 147,000 | 25,800 | |||||||||

1,306,000 | $ | 329,600 | |||||||||||||

Cousins Properties Incorporated | 18 | Q3 2015 Supplemental Information |

INVESTMENT ACTIVITY | ||

Completed Property Dispositions

Property | Type | Metropolitan Area | Company's Ownership Interest | Timing | Square Feet | Gross Sales Price ($ in thousands) | |||||||||

2015 | |||||||||||||||

2100 Ross | Office | Dallas | 100.0% | 3Q | 844,000 | $ | 131,000 | ||||||||

2014 | |||||||||||||||

600 University Park Place | Office | Birmingham | 100.0% | 1Q | 123,000 | 19,700 | |||||||||

Lakeshore Park Plaza | Office | Birmingham | 100.0% | 3Q | 197,000 | 25,000 | |||||||||

Mahan Village | Retail | Florida | 50.5% | 4Q | 147,000 | 29,500 | |||||||||

Cousins Watkins LLC | Retail | Other | 50.5% | 4Q | 339,000 | 79,500 | |||||||||

777 Main | Office | Fort Worth | 100.0% | 4Q | 980,000 | 167,000 | |||||||||

2013 | |||||||||||||||

Terminus 100 | Office | Atlanta | 100.0% | 1Q | 656,000 | 209,200 | |||||||||

Tiffany Springs MarketCenter | Retail | Kansas City | 88.5% | 3Q | 238,000 | 53,500 | |||||||||

The Avenue Murfreesboro | Retail | Nashville | 50.0% | 3Q | 752,000 | 164,000 | |||||||||

CP Venture Two LLC | Retail | Other | 10.3% | 3Q | 934,000 | 226,100 | |||||||||

CP Venture Five LLC | Retail | Other | 11.5% | 3Q | 1,179,000 | 296,200 | |||||||||

Inhibitex | Office | Atlanta | 100.0% | 4Q | 51,000 | 8,300 | |||||||||

2012 | |||||||||||||||

The Avenue Collierville | Retail | Memphis | 100.0% | 2Q | 511,000 | 55,000 | |||||||||

Galleria 75 | Office | Atlanta | 100.0% | 2Q | 111,000 | 9,200 | |||||||||

Ten Peachtree Place | Office | Atlanta | 50.0% | 2Q | 260,000 | 45,300 | |||||||||

The Avenue Web Gin | Retail | Atlanta | 100.0% | 4Q | 322,000 | 59,600 | |||||||||

The Avenue Forsyth | Retail | Atlanta | 88.5% | 4Q | 524,000 | 119,000 | |||||||||

Cosmopolitan Center | Office | Atlanta | 100.0% | 4Q | 51,000 | 7,000 | |||||||||

Palisades West | Office | Austin | 50.0% | 4Q | 373,000 | 64,800 | |||||||||

Presbyterian Medical Plaza | Office | Charlotte | 11.5% | 4Q | 69,000 | 4,500 | |||||||||

2011 | |||||||||||||||

King Mill | Industrial | Atlanta | 75.0% | 4Q | 796,000 | 28,300 | |||||||||

Lakeside Ranch | Industrial | Dallas | 100.0% | 4Q | 749,000 | 28,400 | |||||||||

One Georgia Center | Office | Atlanta | 88.5% | 3Q | 376,000 | 48,600 | |||||||||

Jefferson Mill | Industrial | Atlanta | 75.0% | 1Q | 459,000 | 22,000 | |||||||||

11,041,000 | $ | 1,900,700 | |||||||||||||

Cousins Properties Incorporated | 19 | Q3 2015 Supplemental Information |

DEVELOPMENT PIPELINE (1) | ||

Project | Type | Metropolitan Area | Company's Ownership Interest | Project Start Date | Number of Apartment Units/Square Feet | Estimated Project Cost (2) ($ in thousands) | Project Cost Incurred to Date (2) ($ in thousands) | Percent Leased | Percent Occupied | Initial Occupancy | Estimated Stabilization (5) | |||||||||||||||||||||

Research Park V | Office | Austin, TX | 100 | % | 4Q14 | 173,000 | $ | 45,000 | $ | 26,797 | — | % | — | % | 1Q16 | (3 | ) | 1Q17 | ||||||||||||||

Carolina Square | Mixed | Chapel Hill, NC | 50 | % | 2Q15 | 123,000 | 8,643 | |||||||||||||||||||||||||

Office | 159,000 | 39 | % | — | % | 2Q17 | (3 | ) | 2Q18 | |||||||||||||||||||||||

Apartments | 246 | — | % | — | % | 2Q17 | (4 | ) | 2Q18 | |||||||||||||||||||||||

Retail | 43,000 | — | % | — | % | 2Q17 | (4 | ) | 2Q18 | |||||||||||||||||||||||

NCR | Office | Atlanta, GA | 100 | % | 3Q15 | 485,000 | 200,000 | 26,030 | 100 | % | — | % | 1Q18 | (3 | ) | 1Q18 | ||||||||||||||||

Total | $ | 368,000 | $ | 61,470 | ||||||||||||||||||||||||||||

(1) This schedule shows projects currently under active development through the substantial completion of construction. Amounts included in the estimated project cost column represent the estimated costs of the project through stabilization. Significant estimation is required to derive these costs and the final costs may differ from these estimates. The projected stabilization dates are also estimates and are subject to change as the project proceeds through the development process.

(2) Amount represents 100% of the estimated project cost. The Research Park V project is being funded 100% by the Company. Carolina Square will be funded with a combination of equity from the partners and up to $80 million from a construction loan, which has no outstanding balance as of September 30, 2015.

(3) Represents the quarter which the Company estimates the first office square feet to be occupied.

(4) Represents the quarter which the Company estimates the first apartment/retail space to be occupied.

(5) Stabilization represents the earlier of the quarter within which the Company estimates it will achieve 90% economic occupancy or one year from initial occupancy.

Cousins Properties Incorporated | 20 | Q3 2015 Supplemental Information |

LAND INVENTORY | ||

Metropolitan Area | Company's Ownership Interest | Total Developable Land (Acres) | Company's Share | |||||||||

Commercial | ||||||||||||

North Point | Atlanta | 100.0% | 32 | |||||||||

Wildwood Office Park | Atlanta | 50.0% | 22 | |||||||||

The Avenue Forsyth-Adjacent Land | Atlanta | 100.0% | 10 | |||||||||

NCR Phase II (3) | Atlanta | 100.0% | 1 | |||||||||

Georgia | 65 | |||||||||||

Victory Center | Dallas | 75.0% | 3 | |||||||||

Texas | 3 | |||||||||||

Commercial Land Held (Acres) | 68 | 57 | ||||||||||

Cost Basis of Commercial Land Held | $ | 39,364 | $ | 20,577 | ||||||||

Residential (1) | ||||||||||||

Paulding County | Atlanta | 50.0% | 478 | |||||||||

Callaway Gardens (2) | Atlanta | 100.0% | 218 | |||||||||

Georgia | 696 | |||||||||||

Padre Island | Corpus Christi | 50.0% | 15 | |||||||||

Texas | 15 | |||||||||||

Residential Land Held (Acres) | 711 | 465 | ||||||||||

Cost Basis of Residential Land Held | $ | 11,899 | $ | 8,363 | ||||||||

Grand Total Land Held (Acres) | 779 | 522 | ||||||||||

Grand Total Cost Basis of Land Held | $ | 51,263 | $ | 28,940 | ||||||||

(1) Residential represents land that may be sold to third parties as lots or in large tracts for residential or commercial development.

(2) Company's ownership interest is shown at 100% as Callaway Gardens is owned in a joint venture which is consolidated with the Company. See Joint Venture Information included herein for further details.

(3) Represents land adjacent to the NCR development project. Upon completion of the NCR development project, NCR is required to pay rent on this land.

Cousins Properties Incorporated | 21 | Q3 2015 Supplemental Information |

DEBT SCHEDULE | ||

Company's Share of Debt Maturities and Principal Payments | ||||||||||||||||||||||||||||||||||||||||

Description (Interest Rate Base, if not fixed) | Company's Ownership Interest | Rate at End of Quarter | Maturity Date | 2015 | 2016 | 2017 | 2018 | 2019 | Thereafter | Total | Company's Share Recourse (1) | |||||||||||||||||||||||||||||

Consolidated Debt | ||||||||||||||||||||||||||||||||||||||||

Floating Rate Debt | ||||||||||||||||||||||||||||||||||||||||

Credit Facility, Unsecured (LIBOR + 1.10%-1.45%; $500mm facility)(2) | 100.0 | % | 1.29 | % | 5/28/19 | $ | — | $ | — | $ | — | $ | — | $134,000 | $ | — | $134,000 | $134,000 | ||||||||||||||||||||||

Total Floating Rate Debt | — | — | — | — | 134,000 | — | 134,000 | 134,000 | ||||||||||||||||||||||||||||||||

Fixed Rate Debt | ||||||||||||||||||||||||||||||||||||||||

The Points at Waterview (3) | 100.0 | % | 5.66 | % | 1/1/16 | 146 | 14,025 | — | — | — | — | 14,171 | — | |||||||||||||||||||||||||||

The American Cancer Society Center (4) | 100.0 | % | 6.45 | % | 9/1/17 | 452 | 1,834 | 127,508 | — | — | — | 129,794 | — | |||||||||||||||||||||||||||

191 Peachtree Tower | 100.0 | % | 3.35 | % | 10/1/18 | — | 1,305 | 2,013 | 96,682 | — | — | 100,000 | — | |||||||||||||||||||||||||||

Meridian Mark Plaza | 100.0 | % | 6.00 | % | 8/1/20 | 110 | 456 | 484 | 514 | 546 | 22,978 | 25,088 | — | |||||||||||||||||||||||||||

Post Oak Central | 100.0 | % | 4.26 | % | 10/1/20 | 848 | 3,485 | 3,636 | 3,794 | 3,959 | 166,896 | 182,618 | — | |||||||||||||||||||||||||||

Promenade | 100.0 | % | 4.27 | % | 10/1/22 | 695 | 2,862 | 2,986 | 3,116 | 3,252 | 95,988 | 108,899 | — | |||||||||||||||||||||||||||

816 Congress | 100.0 | % | 3.75 | % | 11/1/24 | — | 128 | 1,568 | 1,628 | 1,690 | 79,986 | 85,000 | — | |||||||||||||||||||||||||||

Total Fixed Rate Debt | 2,251 | 24,095 | 138,195 | 105,734 | 9,447 | 365,848 | 645,570 | — | ||||||||||||||||||||||||||||||||

Total Consolidated Debt | 2,251 | 24,095 | 138,195 | 105,734 | 143,447 | 365,848 | 779,570 | 134,000 | ||||||||||||||||||||||||||||||||

Unconsolidated Debt | ||||||||||||||||||||||||||||||||||||||||

Floating Rate Debt | ||||||||||||||||||||||||||||||||||||||||

Emory Point (LIBOR + 1.75%) | 75.0 | % | 1.94 | % | 10/9/16 | — | 43,522 | — | — | — | — | 43,522 | — | |||||||||||||||||||||||||||

Emory Point II (LIBOR + 1.85%, $46mm facility) | 75.0 | % | 2.04 | % | 10/9/16 | — | 29,362 | — | — | — | — | 29,362 | 2,936 | |||||||||||||||||||||||||||

Carolina Square (LIBOR + 1.90%, $79.8mm facility) (5) | 50.0 | % | 2.09 | % | 5/1/18 | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||

Total Floating Rate Debt | — | 72,884 | — | — | — | — | 72,884 | 2,936 | ||||||||||||||||||||||||||||||||

Fixed Rate Debt | ||||||||||||||||||||||||||||||||||||||||

Gateway Village (6) | 50.0 | % | 6.41 | % | 12/1/16 | 2,303 | 8,768 | — | — | — | — | 11,071 | — | |||||||||||||||||||||||||||

Terminus 100 | 50.0 | % | 5.25 | % | 1/1/23 | 309 | 1,277 | 1,346 | 1,418 | 1,494 | 59,073 | 64,917 | — | |||||||||||||||||||||||||||

Terminus 200 | 50.0 | % | 3.79 | % | 1/1/23 | — | 559 | 770 | 800 | 831 | 38,040 | 41,000 | — | |||||||||||||||||||||||||||

Emory University Hospital Midtown Medical Office Tower | 50.0 | % | 3.50 | % | 6/1/23 | 179 | 732 | 758 | 785 | 813 | 34,055 | 37,322 | — | |||||||||||||||||||||||||||

Total Fixed Rate Debt | 2,791 | 11,336 | 2,874 | 3,003 | 3,138 | 131,168 | 154,310 | — | ||||||||||||||||||||||||||||||||

Total Unconsolidated Debt | 2,791 | 84,220 | 2,874 | 3,003 | 3,138 | 131,168 | 227,194 | 2,936 | ||||||||||||||||||||||||||||||||

Total Debt | $ | 5,042 | $ | 108,315 | $ | 141,069 | $ | 108,737 | $ | 146,585 | $ | 497,016 | $ | 1,006,764 | $ | 136,936 | ||||||||||||||||||||||||

Total Maturities (7) | $ | — | $ | 86,909 | $ | 127,508 | $ | 96,682 | $ | 134,000 | $ | 472,361 | $ | 917,460 | ||||||||||||||||||||||||||

% of Maturities | —% | 9% | 14% | 11% | 15% | 51% | 100% | |||||||||||||||||||||||||||||||||

Floating and Fixed Rate Debt Analysis

Total Debt ($) | Total Debt (%) | Weighted Average Interest Rate | Weighted Average Maturity (Yrs.) | ||||||||||

Floating Rate Debt | $ | 206,884 | 21 | % | 1.53 | % | 2.7 | ||||||

Fixed Rate Debt | 799,880 | 79 | % | 4.58 | % | 5.2 | |||||||

Total Debt | $ | 1,006,764 | 100 | % | 3.95 | % | 4.7 | ||||||

(1) Non-recourse loans are subject to customary carve-outs.

(2) Total borrowing capacity of the Credit Facility at September 30, 2015 was $500 million. The spread over LIBOR at September 30, 2015 was 1.10%.

(3) On October 1, 2015, this note was prepaid in full without penalty.

(4) The real estate and other assets of this property are restricted under a loan agreement such that these assets are not available to settle other debts of the Company.

(5) The Company and Northwood Ravin will each guarantee 12.5% of the outstanding loan amount. See Joint Venture information for further details on the Carolina Square venture structure.

(6) See Joint Venture Information for further details on the Gateway Village venture structure. Based on the structure of the venture and the nature of the related debt, the Company excludes the Gateway Village debt in certain of its leverage calculations.

(7) Maturities include lump sum principal payments due at the maturity date. Maturities do not include scheduled principal payments due prior to the maturity date.

Cousins Properties Incorporated | 22 | Q3 2015 Supplemental Information |

DEBT SCHEDULE | ||

Cousins Properties Incorporated | 23 | Q3 2015 Supplemental Information |

JOINT VENTURE INFORMATION (1) | ||

Cash Flows to Cousins | Financial Statement Presentation | |||||||||

Joint Ventures | Properties | Operating | Capital Transactions/Other | GAAP Accounting | ||||||

EP I LLC | Emory Point (Phase I) | 75% of operating cash flows. | 75% of proceeds. | Recognize 75% of net income from venture. | Unconsolidated | |||||

EP II LLC | Emory Point (Phase II) | 75% of operating cash flows. | 75% of proceeds. | Recognize 75% of net income from venture. | Unconsolidated | |||||

Crawford Long-CPI, LLC | Emory University Hospital Midtown Medical Office Tower | 50% of operating cash flows. | 50% of proceeds. | Recognize 50% of net income from venture. | Unconsolidated | |||||

Charlotte Gateway Village LLC | Gateway Village | Preferred return on investment of 11.46%. | 50% of proceeds after partner receives $66.8 million until a 17% leveraged IRR. Thereafter, 20% of remaining proceeds. | Recognize 11.46% of invested capital each period. | Unconsolidated | |||||

Terminus Office Holdings LLC | Terminus 100, Terminus 200 | 50% of operating cash flows until partner receives an agreed upon return. Thereafter, receive an additional promoted interest if certain return thresholds are met. | Same as operating cash flow. | Recognize 50% of net income from venture. | Unconsolidated | |||||

Carolina Square Holdings LP | Carolina Square | 50% of operating cash flows. | 50% of proceeds. | Recognize 50% of net income from venture. | Unconsolidated | |||||

HICO Victory Center LP (2) | Land/ Future Office Development | Cousins funds 75% of land and 50% of other expenses in predevelopment stage. | Same as operating cash flow. | Recognize 50% of net income from joint venture. | Unconsolidated (2) | |||||

CL Realty, L.L.C. | Land | 50% of operating cash flows. | 50% of proceeds. | Recognize 50% of net income from venture. | Unconsolidated | |||||

Temco Associates, LLC | Land | 50% of operating cash flows. | 50% of proceeds. | Recognize 50% of net income from venture. | Unconsolidated | |||||

Wildwood Associates | Land | 50% of operating cash flows. | 50% of proceeds. | Recognize 50% of net income from venture. | Unconsolidated | |||||

Cousins/Callaway LLC | Land | The first $2.0 million of cash flows; 77% of the next $17.7 million of cash flows; 50% of remaining cash flows until a 20% IRR; 40% of remaining cash flows until a 25% IRR; 25% of remainder. | Same as operating cash flow. | Recognize revenues and expenses as if a wholly-owned property. Recognize noncontrolling interest based on amounts earned by partner. | Consolidated | |||||

(1) This schedule includes information on joint venture investments of the Company that have properties under active development, active operations, or have significant assets.

(2) If the partners decide to construct an office building, the economics of the venture will adjust such that Cousins owns at least 90% of the venture. At that time, the Company expects the venture to be consolidated.

Cousins Properties Incorporated | 24 | Q3 2015 Supplemental Information |

NON-GAAP FINANCIAL MEASURES - CALCULATIONS AND RECONCILIATIONS | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

2nd Generation TI & Leasing Costs & Building CAPEX: | ||||||||||||||||||||

Office | ||||||||||||||||||||

Second Generation Leasing Related Costs | 12,139 | 2,745 | 5,388 | 12,023 | 11,031 | 31,187 | 11,513 | 12,294 | 10,941 | 34,748 | ||||||||||

Second Generation Building Improvements | 3,814 | 550 | 1,929 | — | 1,388 | 3,867 | 507 | 965 | 3,267 | 4,739 | ||||||||||

15,954 | 3,295 | 7,317 | 12,023 | 12,419 | 35,054 | 12,020 | 13,259 | 14,208 | 39,487 | |||||||||||

Net Operating Income | ||||||||||||||||||||

Office Consolidated Properties | 102,624 | 42,225 | 43,666 | 47,776 | 52,926 | 186,593 | 52,103 | 54,780 | 54,685 | 161,568 | ||||||||||

Other Consolidated Properties | 1,299 | 402 | 409 | 396 | 178 | 1,385 | (24 | ) | 10 | — | (14 | ) | ||||||||

Net Operating Income - Consolidated | 103,923 | 42,627 | 44,075 | 48,172 | 53,104 | 187,978 | 52,079 | 54,790 | 54,685 | 161,554 | ||||||||||

Rental Property Revenues | 194,420 | 77,484 | 80,034 | 86,857 | 99,535 | 343,910 | 90,033 | 96,177 | 96,016 | 282,226 | ||||||||||

Rental Property Operating Expenses | (90,497 | ) | (34,857 | ) | (35,959 | ) | (38,685 | ) | (46,434 | ) | (155,934 | ) | (37,954 | ) | (41,387 | ) | (41,331 | ) | (120,672 | ) |

Net Operating Income - Consolidated | 103,923 | 42,627 | 44,075 | 48,172 | 53,101 | 187,976 | 52,079 | 54,790 | 54,685 | 161,554 | ||||||||||

Income from Discontinued Operations | ||||||||||||||||||||

Rental Property Revenues | 10,552 | 1,356 | 967 | 601 | 4 | 2,927 | 4 | — | — | 4 | ||||||||||

Rental Property Operating Expenses | (4,163 | ) | (464 | ) | (402 | ) | (262 | ) | (2 | ) | (1,128 | ) | (18 | ) | — | — | (18 | ) | ||

Net Operating Income | 6,389 | 892 | 565 | 339 | 2 | 1,799 | (14 | ) | — | — | (14 | ) | ||||||||

Termination Fees | — | — | 2 | — | — | 2 | — | — | — | — | ||||||||||

Interest and Other Income (Expense) | 15 | — | — | 8 | (4 | ) | 3 | — | (6 | ) | 6 | — | ||||||||

FFO from Discontinued Operations | 6,404 | 892 | 567 | 349 | (2 | ) | 1,804 | (14 | ) | (6 | ) | 6 | (14 | ) | ||||||

Third Party Management and Leasing Revenues | 76 | — | — | — | — | — | — | — | — | — | ||||||||||

Third Party Management and Leasing Expenses | (97 | ) | — | — | (1 | ) | (1 | ) | (2 | ) | — | — | — | — | ||||||

FFO from Third Party Management and Leasing | (21 | ) | — | — | (1 | ) | (1 | ) | (2 | ) | — | — | — | — | ||||||

FFO from Discontinued Operations | 6,383 | 892 | 567 | 348 | (3 | ) | 1,802 | (14 | ) | (6 | ) | 6 | (14 | ) | ||||||

Depreciation and Amortization of Real Estate | (3,086 | ) | — | — | — | — | — | — | — | — | ||||||||||

Income from Discontinued Operations | 3,297 | 892 | 567 | 348 | (3 | ) | 1,804 | (14 | ) | (6 | ) | 6 | (14 | ) | ||||||

Income (Loss) from Unconsolidated Joint Ventures | ||||||||||||||||||||

Net Operating Income | ||||||||||||||||||||

Office Properties | 16,195 | 4,493 | 4,593 | 4,575 | 4,515 | 18,176 | 4,642 | 4,489 | 4,644 | 13,775 | ||||||||||

Other Properties | 11,572 | 2,006 | 2,055 | 2,026 | 1,633 | 7,720 | 1,346 | 1,495 | 1,487 | 4,328 | ||||||||||

Net Operating Income | 27,767 | 6,499 | 6,648 | 6,601 | 6,148 | 25,896 | 5,988 | 5,984 | 6,131 | 18,103 | ||||||||||

Residential Lot, Outparcel and Tract Sales Less Cost of Sales | 115 | — | 5 | — | 2,160 | 2,165 | — | 242 | 2,038 | 2,280 | ||||||||||

Other Sales Less Cost of Sales | (4 | ) | — | 42 | — | — | 42 | — | — | — | — | |||||||||

Termination Fees | 19 | — | 72 | — | 113 | 185 | 120 | 28 | 271 | 419 | ||||||||||

Interest Expense | (7,963 | ) | (1,845 | ) | (1,843 | ) | (1,843 | ) | (1,833 | ) | (7,364 | ) | (1,822 | ) | (1,827 | ) | (1,845 | ) | (5,494 | ) |

Other Expense | 513 | 28 | 203 | 155 | 150 | 536 | 68 | 106 | 12 | 186 | ||||||||||

Depreciation and Amortization of Non-Real Estate Assets | (34 | ) | (11 | ) | (12 | ) | (12 | ) | (11 | ) | (46 | ) | — | — | — | — | ||||

Cousins Properties Incorporated | 25 | Q3 2015 Supplemental Information |

NON-GAAP FINANCIAL MEASURES - CALCULATIONS AND RECONCILIATIONS | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

Funds from Operations - Unconsolidated Joint Ventures | 20,413 | 4,671 | 5,115 | 4,901 | 6,727 | 21,414 | 4,354 | 4,533 | 6,607 | 15,494 | ||||||||||

Gain on Sale of Depreciated Investment Properties, net | 60,344 | (387 | ) | — | — | 2,154 | 1,767 | — | — | — | — | |||||||||

Depreciation and Amortization of Real Estate | (13,435 | ) | (2,998 | ) | (3,088 | ) | (2,870 | ) | (2,957 | ) | (11,913 | ) | (2,743 | ) | (2,772 | ) | (2,891 | ) | (8,406 | ) |

Net Income from Unconsolidated Joint Ventures | 67,322 | 1,286 | 2,027 | 2,031 | 5,924 | 11,268 | 1,611 | 1,761 | 3,716 | 7,088 | ||||||||||

Market Capitalization | ||||||||||||||||||||

Common Stock price at Period End | 10.30 | 11.47 | 12.45 | 11.95 | 11.42 | 11.42 | 10.60 | 10.38 | 9.22 | 9.22 | ||||||||||

Number of Common Shares Outstanding at Period End | 189,666 | 198,423 | 198,474 | 216,509 | 216,513 | 216,513 | 216,470 | 216,686 | 214,671 | 214,671 | ||||||||||

Common Stock Capitalization | 1,953,560 | 2,275,912 | 2,471,001 | 2,587,283 | 2,472,578 | 2,472,578 | 2,294,582 | 2,249,201 | 1,979,267 | 1,979,267 | ||||||||||

Preferred Stock Series B Price at Liquidation Value | 94,775 | 94,775 | — | — | — | — | — | — | — | — | ||||||||||

Preferred Stock at Liquidation Value | 94,775 | 94,775 | — | — | — | — | — | — | — | — | ||||||||||

Debt | 630,094 | 587,442 | 665,852 | 671,074 | 792,344 | 792,344 | 847,948 | 849,772 | 779,570 | 779,570 | ||||||||||

Share of Unconsolidated Debt | 228,489 | 226,574 | 224,241 | 224,544 | 215,158 | 215,158 | 219,428 | 225,241 | 227,194 | 227,194 | ||||||||||

Debt (2) | 858,583 | 814,016 | 890,093 | 895,618 | 1,007,502 | 1,007,502 | 1,067,376 | 1,075,013 | 1,006,764 | 1,006,764 | ||||||||||

Total Market Capitalization | 2,906,918 | 3,184,703 | 3,361,094 | 3,482,901 | 3,480,080 | 3,480,080 | 3,361,958 | 3,324,214 | 2,986,031 | 2,986,031 | ||||||||||

EBITDA (2) | ||||||||||||||||||||

FFO | 77,134 | 36,182 | 35,784 | 41,676 | 51,560 | 165,204 | 45,935 | 45,238 | 52,467 | 143,640 | ||||||||||

Interest Expense | 29,672 | 9,012 | 8,813 | 8,660 | 9,989 | 36,474 | 9,498 | 9,696 | 9,518 | 28,712 | ||||||||||

Non-Real Estate Depreciation and Amortization | 787 | 196 | 213 | 244 | 260 | 913 | 423 | 374 | 414 | 1,211 | ||||||||||

Income Tax Provision (Benefit) | (23 | ) | (12 | ) | (9 | ) | 1 | — | (20 | ) | — | — | — | — | ||||||

Gain on Sale of Third Party Management & Leasing Business | 787 | (7 | ) | — | (5 | ) | 15 | 3 | — | — | — | — | ||||||||

Acquisition and Related Costs | 77,134 | 22 | 149 | 644 | 315 | 1,130 | 83 | 2 | 19 | 104 | ||||||||||

Preferred Stock Dividends and Original Issuance Costs | 29,672 | 1,777 | 4,708 | — | — | 6,485 | — | — | — | — | ||||||||||

EBITDA (2) | 787 | 47,170 | 49,658 | 51,220 | 62,139 | 210,189 | 55,939 | 55,310 | 62,418 | 173,667 | ||||||||||

Credit Ratios | ||||||||||||||||||||

Debt (2) | 858,583 | 814,016 | 890,093 | 895,618 | 1,007,502 | 1,007,502 | 1,067,376 | 1,075,013 | 1,006,764 | 1,006,764 | ||||||||||

Total Market Capitalization | 2,906,918 | 3,184,703 | 3,361,094 | 3,482,901 | 3,480,080 | 3,480,080 | 3,361,958 | 3,324,214 | 2,986,031 | 2,986,031 | ||||||||||

Debt (2) / Total Market Capitalization | 29.5 | % | 25.6 | % | 26.5 | % | 25.7 | % | 29.0 | % | 29.0 | % | 31.7 | % | 32.3 | % | 33.7 | % | 33.7 | % |

Total Assets - Consolidated | 2,273,206 | 2,294,038 | 2,280,243 | 2,533,660 | 2,667,330 | 2,667,330 | 2,684,661 | 2,637,607 | 2,635,397 | 2,635,397 | ||||||||||

Accumulated Depreciation - Consolidated | 257,151 | 319,865 | 355,711 | 376,832 | 400,593 | 400,593 | 435,939 | 470,360 | 542,084 | 542,084 | ||||||||||

Undepreciated Assets - Unconsolidated (2) | 441,928 | 446,890 | 492,640 | 459,931 | 450,535 | 450,535 | 454,835 | 466,438 | 482,606 | 482,606 | ||||||||||

Less: Investment in Unconsolidated Joint Ventures | (107,082 | ) | (107,106 | ) | (111,164 | ) | (111,353 | ) | (100,498 | ) | (100,498 | ) | (100,821 | ) | (103,665 | ) | (103,470 | ) | (103,470 | ) |

Total Undepreciated Assets (2) | 2,865,203 | 2,953,687 | 3,017,430 | 3,259,070 | 3,417,960 | 3,417,960 | 3,474,614 | 3,523,306 | 3,556,617 | 3,556,617 | ||||||||||

Debt (2) | 858,583 | 814,016 | 890,093 | 895,618 | 1,007,502 | 1,007,502 | 1,067,376 | 1,075,013 | 1,006,764 | 1,006,764 | ||||||||||

Debt (2) / Total Undepreciated Assets (2) | 30.0 | % | 27.6 | % | 29.5 | % | 27.5 | % | 29.5 | % | 29.5 | % | 30.7 | % | 30.5 | % | 28.3 | % | 28.3 | % |

Cousins Properties Incorporated | 26 | Q3 2015 Supplemental Information |

NON-GAAP FINANCIAL MEASURES - CALCULATIONS AND RECONCILIATIONS | ||

2013 | 2014 1st | 2014 2nd | 2014 3rd | 2014 4th | 2014 | 2015 1st | 2015 2nd | 2015 3rd | 2015 YTD | |||||||||||

Interest Expense | 29,672 | 9,012 | 8,813 | 8,660 | 9,989 | 36,474 | 9,498 | 9,696 | 9,518 | 28,712 | ||||||||||

Scheduled Principal Payments | 7,032 | 2,445 | 2,430 | 2,460 | 2,501 | 9,836 | 2,493 | 2,477 | 2,507 | 7,477 | ||||||||||

Preferred Stock Dividends | 10,008 | 1,777 | 1,178 | — | — | 2,955 | — | — | — | — | ||||||||||

Fixed Charges | 46,712 | 13,234 | 12,421 | 11,120 | 12,490 | 49,265 | 11,991 | 12,173 | 12,025 | 36,189 | ||||||||||

EBITDA | 123,142 | 47,170 | 49,658 | 51,220 | 62,139 | 210,189 | 55,939 | 55,310 | 62,418 | 173,667 | ||||||||||

Fixed Charges Coverage Ratio (2) | 2.64 | 3.56 | 4.00 | 4.61 | 4.98 | 4.27 | 4.67 | 4.54 | 5.19 | 4.80 | ||||||||||

Debt (2) | 858,583 | 814,016 | 890,093 | 895,618 | 1,007,502 | 1,007,502 | 1,067,376 | 1,075,013 | 1,006,764 | 1,006,764 | ||||||||||

Annualized EBITDA (3) | 181,728 | 188,680 | 198,632 | 204,880 | 248,556 | 248,556 | 223,756 | 221,240 | 250,260 | 231,752 | ||||||||||

Debt (2) / Annualized EBITDA (3) | 4.72 | 4.31 | 4.48 | 4.37 | 4.05 | 4.05 | 4.77 | 4.86 | 4.02 | 4.34 | ||||||||||

Dividend Information | ||||||||||||||||||||

Cash Common Dividends | 27,192 | 14,232 | 14,882 | 16,236 | 16,213 | 61,563 | 17,349 | 17,328 | 17,334 | 52,011 | ||||||||||

FFO | 77,134 | 36,182 | 35,784 | 41,676 | 51,560 | 165,204 | 45,935 | 45,238 | 52,467 | 143,640 | ||||||||||

FFO Payout Ratio | 35.3 | % | 39.3 | % | 41.6 | % | 39.0 | % | 31.4 | % | 37.3 | % | 37.8 | % | 38.3 | % | 33.0 | % | 36.2 | % |

FFO | 77,134 | 36,182 | 35,784 | 41,676 | 51,560 | 165,204 | 45,935 | 45,238 | 52,467 | 143,640 | ||||||||||

Straight Line Rental Revenue | (12,826 | ) | (7,648 | ) | (5,001 | ) | (4,169 | ) | (5,275 | ) | (22,093 | ) | (6,285 | ) | (5,786 | ) | (4,623 | ) | (16,694 | ) |

Above and Below Market Rents | (3,785 | ) | (1,952 | ) | (2,027 | ) | (1,933 | ) | (2,135 | ) | (8,047 | ) | (2,030 | ) | (1,973 | ) | (2,030 | ) | (6,033 | ) |

Second Generation CAPEX | (16,414 | ) | (3,295 | ) | (7,317 | ) | (12,023 | ) | (12,419 | ) | (35,054 | ) | (12,020 | ) | (13,259 | ) | (14,208 | ) | (39,487 | ) |

FAD (2) | 44,109 | 23,286 | 21,439 | 23,551 | 31,731 | 100,010 | 25,600 | 24,220 | 31,606 | 81,426 | ||||||||||

Common Dividends | 27,192 | 14,232 | 14,882 | 16,236 | 16,213 | 61,563 | 17,349 | 17,328 | 17,334 | 52,011 | ||||||||||

FAD Payout Ratio (2) | 61.6 | % | 61.1 | % | 69.4 | % | 68.9 | % | 51.1 | % | 61.6 | % | 67.8 | % | 71.5 | % | 54.8 | % | 63.9 | % |

Operations Ratios | ||||||||||||||||||||

Total Undepreciated Assets (2) | 2,865,203 | 2,953,687 | 3,017,430 | 3,259,070 | 3,417,960 | 3,417,960 | 3,474,614 | 3,523,306 | 3,556,617 | 3,556,617 | ||||||||||

Annualized General and Administrative Expenses (4) / Total Undepreciated Assets | 0.76 | % | 0.76 | % | 0.76 | % | 0.62 | % | 0.40 | % | 0.58 | % | 0.40 | % | 0.67 | % | 0.33 | % | 0.47 | % |

Cousins Properties Incorporated | 27 | Q3 2015 Supplemental Information |

NON-GAAP FINANCIAL MEASURES - CALCULATIONS AND RECONCILIATIONS | ||

Three Months Ended ($ in thousands) | Nine Months Ended | |||||||||||||||||||

September 30, 2015 | September 30, 2014 | June 30, 2015 | September 30, 2015 | September 30, 2014 | ||||||||||||||||

Rental Property Revenues | ||||||||||||||||||||

Same Property | $ | 77,753 | $ | 76,899 | $ | 76,692 | $ | 228,009 | $ | 222,370 | ||||||||||

Non-Same Property | 28,001 | 20,227 | 28,529 | 81,975 | 53,372 | |||||||||||||||

$ | 105,754 | $ | 97,126 | $ | 105,221 | $ | 309,984 | $ | 275,742 | |||||||||||

Rental Property Operating Expenses | ||||||||||||||||||||

Same Property | $ | 33,106 | $ | 32,734 | $ | 32,825 | $ | 96,168 | $ | 93,894 | ||||||||||

Non-Same Property | 11,834 | 9,280 | 11,623 | 34,175 | 25,432 | |||||||||||||||

$ | 44,940 | $ | 42,014 | $ | 44,448 | $ | 130,343 | $ | 119,326 | |||||||||||

Rental Property Revenues | ||||||||||||||||||||

Consolidated Properties | $ | 96,016 | $ | 86,857 | $ | 96,177 | $ | 282,226 | $ | 244,375 | ||||||||||

Discontinued Operations | — | 601 | — | 4 | 2,923 | |||||||||||||||

Share of Unconsolidated Joint Ventures | 9,738 | 9,668 | 9,044 | 27,754 | 28,444 | |||||||||||||||

$ | 105,754 | $ | 97,126 | $ | 105,221 | $ | 309,984 | $ | 275,742 | |||||||||||

Rental Property Operating Expenses | ||||||||||||||||||||

Consolidated Properties | $ | 41,331 | $ | 38,685 | $ | 41,387 | $ | 120,672 | $ | 109,501 | ||||||||||

Discontinued Operations | — | 260 | — | 18 | 1,126 | |||||||||||||||

Share of Unconsolidated Joint Ventures | 3,609 | 3,069 | 3,061 | 9,653 | 8,700 | |||||||||||||||

$ | 44,940 | $ | 42,014 | $ | 44,448 | $ | 130,343 | $ | 119,327 | |||||||||||

Cash Basis Rental Property Revenues | ||||||||||||||||||||

Rental Property Revenues | $ | 105,754 | $ | 97,126 | $ | 105,221 | $ | 309,984 | $ | 275,742 | ||||||||||

Less: Straight Line Rent | 4,623 | 4,169 | 5,786 | 16,694 | 16,818 | |||||||||||||||

Less: Other | 1,526 | 1,551 | 1,456 | 4,517 | 4,753 | |||||||||||||||

$ | 99,605 | $ | 91,406 | $ | 97,979 | $ | 288,773 | $ | 254,171 | |||||||||||

Cash Basis Rental Property Revenues | ||||||||||||||||||||

Same Property | $ | 74,181 | $ | 73,319 | $ | 72,772 | $ | 216,003 | $ | 205,932 | ||||||||||

Non-Same Property | 25,424 | 18,087 | 25,207 | 72,770 | 48,239 | |||||||||||||||

$ | 99,605 | $ | 91,406 | $ | 97,979 | $ | 288,773 | $ | 254,171 | |||||||||||

Cash Basis Rental Property Operating Expenses | ||||||||||||||||||||

Rental Property Operating Expenses | $ | 44,940 | $ | 42,014 | $ | 44,448 | $ | 130,343 | $ | 119,327 | ||||||||||

Non-Cash Ground Rent Expense | — | 3 | 19 | (58 | ) | 9 | ||||||||||||||

$ | 44,940 | $ | 42,017 | $ | 44,467 | $ | 130,285 | $ | 119,336 | |||||||||||

Cash Basis Rental Property Operating Expenses | ||||||||||||||||||||

Same Property | $ | 33,093 | $ | 32,736 | $ | 32,831 | $ | 96,165 | $ | 93,901 | ||||||||||

Non-Same Property | 11,847 | 9,281 | 11,636 | 34,120 | 25,435 | |||||||||||||||

$ | 44,940 | $ | 42,017 | $ | 44,467 | $ | 130,285 | $ | 119,336 | |||||||||||

(1) Amounts may differ slightly from other schedules contained herein due to rounding. | ||||||||||||||||||||

(2) Includes Company share of unconsolidated joint ventures. | ||||||||||||||||||||

(3) Annualized represents quarter amount annualized. | ||||||||||||||||||||

(4) Quarter figures annualized represent quarter amount annualized, year-to-date represents year-to-date annualized. | ||||||||||||||||||||

Cousins Properties Incorporated | 28 | Q3 2015 Supplemental Information |

NON-GAAP FINANCIAL MEASURES - DISCUSSION | ||