Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Petco Holdings Inc | d42894dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on September 24, 2015

Registration No. 333-206436

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

PETCO HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 5990 | 46-1075492 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

10850 Via Frontera,

San Diego, California 92127

(858) 453-7845

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

James Myers

Chief Executive Officer

10850 Via Frontera,

San Diego, California 92127

(858) 453-7845

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Thomas Holden, Esq. Patrick O’Brien, Esq. Ropes & Gray LLP 3 Embarcadero Center San Francisco, California 94111-4006 (415) 315-6300 |

Darragh J. Davis, Esq. Vice President, General Counsel & Corporate Secretary 10850 Via Frontera, San Diego, California 92127 (858) 453-7845 |

Jeffrey D. Karpf, Esq. Helena K. Grannis, Esq. Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, New York 10006 (212) 225-2000 |

Approximate date of commencement of proposed sale to public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ¨ |

Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated September 24, 2015

Preliminary prospectus

Shares

Petco Holdings, Inc.

Common Stock

$ per share

This is the initial public offering of our common stock. The selling stockholders identified in this prospectus are offering shares. We will not receive any of the proceeds from the sale of the shares being sold by the selling stockholders. We currently expect the initial public offering price to be between $ and $ per share of common stock.

The selling stockholders have granted the underwriters an option to purchase up to additional shares of our common stock.

We have applied to list our common stock on under the symbol “ .”

| Per share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds to selling stockholders before expenses |

$ | $ | ||||||

| (1) | See “Underwriting” for additional information regarding underwriting compensation. |

Investing in our common stock involves risk. See “Risk Factors” beginning on page 20.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to investors on or about , 2015.

| Goldman, Sachs & Co. | BofA Merrill Lynch | J.P. Morgan | ||||

| Credit Suisse | Deutsche Bank Securities | Morgan Stanley | Wells Fargo Securities | Jefferies | ||||

| TPG Capital BD, LLC | Piper Jaffray | Stifel | Cantor Fitzgerald & Co. | Guggenheim Securities | Nomura | |||||

Prospectus dated , 2015

Table of Contents

Table of Contents

| Page | ||||

| 1 | ||||

| 20 | ||||

| 40 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| 45 | ||||

| 47 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

51 | |||

| 72 | ||||

| 89 | ||||

| 99 | ||||

| 128 | ||||

| 130 | ||||

| 134 | ||||

| 138 | ||||

| 140 | ||||

| Certain Material United States Federal Income Tax Considerations for Non-U.S. Holders |

142 | |||

| 147 | ||||

| 150 | ||||

| 155 | ||||

| 155 | ||||

| 155 | ||||

| F-1 | ||||

We are responsible for the information contained in this prospectus and in any free writing prospectus we prepare or authorize. Neither we, the selling stockholders nor the underwriters have authorized anyone to provide you with different information, and neither we, the selling stockholders nor the underwriters take responsibility for any other information others may give you. We are not, and the selling stockholders and underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than its date.

i

Table of Contents

INDUSTRY AND MARKET DATA

This prospectus includes market data and forecasts with respect to the pet food, supplies and services industry. Although we are responsible for all of the disclosure contained in this prospectus, in some cases we rely on and refer to market data and certain industry forecasts that were obtained from third-party surveys, market research, consultant surveys, publicly available information and industry publications and surveys that we believe to be reliable. Unless otherwise indicated, all market and industry data and other statistical information and forecasts contained in this prospectus are based on independent industry publications, government publications, reports by market research firms or other published independent sources, such as Packaged Facts, and other externally obtained data that we believe to be reliable. Some market and industry data, and statistical information and forecasts, are also based on management’s estimates, which are derived from our review of internal surveys as well as the independent sources referred to above. Any such market data, information or forecast may prove to be inaccurate because of the method by which we obtain it or because it cannot always be verified with complete certainty given the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties, including those discussed under the caption “Risk Factors.” As a result, although we believe that these sources are reliable, we have not independently verified the information.

TRADEMARKS AND SERVICE MARKS

Petco® is a registered trademark of Petco Animal Supplies, Inc. and Petco Animal Supplies Stores, Inc. Unleashed by Petco®, Healthier Pets. Happier People. Better World.®, Drs. Foster Smith®, WholePets® and Vetco® are registered trademarks of Petco Animal Supplies Stores, Inc. Pals Rewards™ and What We Feed Them Matters™ are trademarks of Petco Animal Supplies Stores, Inc. All other product and company names are trademarks of their respective owners.

Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus are listed without the ®, SM and TM symbols.

ii

Table of Contents

This summary highlights information contained in other parts of this prospectus. Because it is only a summary, it does not contain all of the information that you should consider before investing in shares of our common stock and it is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere in this prospectus. Unless the context requires otherwise, references in this prospectus to the “Company,” “Petco,” “we,” “us” and “our” refer to Petco Holdings, Inc. and its consolidated subsidiaries. “Petco Animal Supplies” refers to Petco Animal Supplies, Inc., our wholly owned subsidiary, and “Petco Stores” refers to Petco Animal Supplies Stores, Inc., our wholly owned indirect subsidiary. “Drs. Foster and Smith” refers to Drs. Foster Smith™. We report on the basis of a 52- or 53-week fiscal year, which ends on the Saturday closest to January 31. References to “fiscal year” mean the year in which that fiscal year began. For example, fiscal 2014 ended January 31, 2015, fiscal 2013 ended February 1, 2014 and fiscal 2012 ended February 2, 2013. Fiscal 2012 contained 53 weeks, while fiscal 2013 and fiscal 2014 contained 52 weeks. You should read the entire prospectus, especially “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements” and our financial statements and the related notes, before deciding to buy shares of our common stock.

Our Company

We believe in the powerful bond between humans and their pets. Our promise is to nurture connections between pets and their parents for better lives together. We strive to be the trusted partner of choice for pet parents, offering a fun, engaging and educational customer experience at more than 1,400 convenient store locations across the country and through our websites. We are a leading omnichannel specialty retailer of pet food, supplies, services and companion animals in the United States, with one of the largest selections of premium pet brands and services available to pet lovers. We offer purposeful products comprising what we believe are among the most trusted and authentic brands in the pet industry, many of which are not currently sold or carried by our closest pet specialty competitor.

With over 50 years of history, our goal is to offer our customers the merchandise, services and advice to help ensure that their pets enjoy the best nutrition and the highest quality of life in loving homes. We support pet parents who view their pets as extensions of their family. We believe this “humanization” trend drives demand for premium products and services, leading to higher levels of spending per pet. Our omnichannel business model helps nurture these powerful relationships between people and their pets. This is our vision: Healthier Pets. Happier People. Better World.

As of August 1, 2015, we operated 1,409 stores across all 50 states, the District of Columbia and Puerto Rico and an additional 13 stores through our joint venture in Mexico. We have two retail formats: Petco, our flagship retail store format, and Unleashed by Petco (“Unleashed”), a smaller format and up-scale urban lifestyle concept, which enable us to capitalize on real estate opportunities in a variety of urban, suburban and rural markets across the country. We offer a robust suite of in-store services that we believe appeal to discerning pet parents. These services, which cannot be replicated online, include grooming and dog training as well as low-cost vaccination and preventative wellness services, and we continue to expand and enhance our services offerings to address this fast-growing market segment. Our stores are complemented by the largest ecommerce platform in specialty pet retail, which includes Petco.com, DrsFosterSmith.com, Liveaquaria.com and Unleashed.com, and we have one of the most followed pet brands on social media.

Our stores are at the heart of our customer engagement strategy, showcasing our love for pets and providing opportunities for our associates to deliver high-quality service and knowledgeable advice

1

Table of Contents

to customers. Based on measures of unaided brand awareness and our Net Promoter Score, the Petco brand is widely recognized and highly recommended. To capitalize on our trusted brand and drive engagement with pet parents, we empower our sales associates to provide solutions for customers in the areas of pet nutrition, behavior and services. We utilize the rich customer insights gathered from our Pals loyalty card database to help guide our customer engagement strategy. This database included 19.1 million active members (which we define as members having made a purchase in the last twelve months) and captured 87% of our total sales in fiscal 2014. We believe our highly trained sales associates, together with our data-driven customer engagement model, promote regular return visits of our customers and help establish Petco as a one stop shop for all pet needs.

We have made substantial investments in our omnichannel retail model to position us for continued growth and success in the evolving pet industry. We operate our ecommerce business in-house, utilizing fulfillment processes which are integrated with our network of distribution centers. In recent years, we have made significant investments in our infrastructure to further optimize our business platform. Additionally, these investments include integrating new technology across stores, web and mobile experiences to complement our advanced in-house ecommerce fulfillment processes; a new advanced Customer Relationship Management (“CRM”) system to manage our Pals loyalty program; and the opening of our fifth main distribution center in Reno, Nevada to support our western U.S. store expansion and ecommerce businesses.

The $74 billion pet industry continues to thrive. We estimate that there are more than 6 million new pet households since 2007, while pet ownership among millennial households was 59% in 2014 compared to 50% in 2010, according to Packaged Facts. We believe pet humanization and ownership trends will continue to drive outsized growth of the pet services and premium offerings market segments compared to other portions of the pet industry. We plan to continue to invest in our business to maintain our leading position in the fastest-growing segments of the pet food, supplies and services industry. As a leading pet specialty retailer of natural and organic pet food brands, we believe we are well-positioned to capitalize on these favorable industry trends and take additional market share from grocery and discount stores.

Under the leadership of our experienced management team, we have taken several actions to strengthen our market position and enhance our growth potential. These actions include:

| • | refreshing our stores to make them more appealing and engaging to our customers; |

| • | expanding and refining our assortment of premium pet food and private label products; |

| • | enhancing the range, experience and quality of the robust suite of services offered in our stores; |

| • | developing an additional store format, Unleashed, which enables us to access a broader range of markets, customers and real estate; |

| • | building an industry-leading, comprehensive ecommerce platform, including pet pharmacy and prescription offerings; and |

| • | establishing a model for international growth through our joint venture in Mexico. |

We have established a track record of strong and consistent financial performance, achieving more than 20 consecutive years of net sales growth through various economic cycles. Key financial highlights include:

| • | achieving positive comparable sales growth for our 21 most recent consecutive quarters, and averaging 3.5% of comparable sales growth annually from fiscal 2005 to fiscal 2014; |

2

Table of Contents

| • | growing our store base from 779 stores under the Petco banner as of the end of fiscal 2005 to 1,251 stores under the Petco banner and 122 stores under the Unleashed banner as of the end of fiscal 2014, representing a compound annual growth rate (“CAGR”) of 6.6% on our total store base; |

| • | increasing the share of our net sales attributable to ecommerce from 1.2% in fiscal 2005 to 8.5% during the first two quarters of fiscal 2015, which includes our operations since our acquisition of Drs. Foster and Smith; |

| • | increasing net sales from $1,996 million for fiscal 2005 to $3,995 million for fiscal 2014, representing a CAGR of 8.0%; |

| • | increasing net income from $22 million for fiscal 2010 to $75 million for fiscal 2014, representing a CAGR of 35.3%; and |

| • | increasing Adjusted EBITDA from $320 million for fiscal 2010 to $457 million for fiscal 2014, representing a CAGR of 9.3%, and increasing Adjusted Net Income from $46 million for fiscal 2010 to $103 million for fiscal 2014, representing a CAGR of 22.6%. |

Adjusted EBITDA and Adjusted Net Income are financial measures that are not presented in accordance with U.S. generally accepted accounting principles (“GAAP”). For a discussion of our use of Adjusted EBITDA and Adjusted Net Income and reconciliations to net income, and historical comparable sales growth, please refer to “Summary Historical Consolidated Financial Data” and “Selected Historical Consolidated Financial Data.”

Our Industry

We compete in the highly attractive U.S. pet industry (including food, supplies, veterinary services and non-medical services), which was a $74 billion industry in 2014 and is projected to grow to $92 billion in 2019, representing a 4.3% CAGR, according to Packaged Facts. From 2014 to 2019, Packaged Facts forecasts that non-veterinary pet services, pet food and pet supplies will grow at a CAGR of 6.2%, 3.8% and 3.0%, respectively. The pet food, supplies and services market is highly fragmented, spread across superstores, discount stores, supermarkets, independent pet retailers and online retailers, with an increasing number of pet-owning households choosing to shop the pet specialty channel.

The pet specialty channel (which includes retail chains but not local independent pet stores) is the second largest channel with 24% market share in 2014, according to Packaged Facts. We estimate growth in this channel has outpaced that in the overall market with a 7.5% CAGR from 2005 to the end of 2014 compared to the U.S. pet industry’s 5.0% CAGR over the same period. As of June 2015, we estimate that we had approximately 16% of the total U.S. pet specialty chain and independent retail market share, based on total number of locations.

| * | Online includes ecommerce sales of brick and mortar market participants, including Petco. |

3

Table of Contents

The pet industry is characterized by the following trends that we believe positively impact our competitive positioning:

| • | Stable, defensive sector with continued attractive consumer trends. The pet industry has consistently demonstrated resilience across economic cycles, driven in part by the replenishment nature of consumable products and services such as pet food, grooming and veterinary services. Packaged Facts estimates that pet ownership has climbed to 63.8 million households in 2014 (or 54% of U.S. households), up from 61.2 million households in 2010 (or 53% of U.S. households). Spending on pets has consistently increased, even during the last recession, and is projected to reach $77.0 billion in 2015, up from $62.7 billion in 2010 and $47.2 billion in 2005, with average household spending of approximately $1,150 per year at the end of 2014. |

| * | Represents internal estimates for 2005 to 2008, and Packaged Facts data from 2009 to 2015E. |

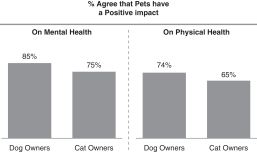

| • | Continued expansion of the pet humanization trend. At the forefront of the pet industry’s momentum is pet humanization, the trend in which passionate and loyal pet parents view their pets as family and strive to provide better care for their pets through premium food, supplies and services. The pet humanization trend is demonstrated by results of a 2014 survey of pet owners conducted by Packaged Facts, set forth in the following charts: |

|

|

We believe this humanization trend leads many pet parents to seek to provide high-quality care for their pets with premium food, supplies and services, which is further increasing spending in the pet industry as 68% of dog owners and 63% of cat owners reported in the 2014 survey that they enjoy purchasing pet products that pamper their pets. The trend is also driving increased spending on non-medical services such as grooming and training, which Packaged Facts forecasts to be the highest growth-rate sub-sector in the pet industry, at a 6.2% CAGR from 2014 to 2019. In addition, as pet parents increasingly use social media as a means to personify and share their pets with others, we believe pet-focused content in social media will continue to accelerate the humanization trend.

4

Table of Contents

| • | High growth rate in premium pet food. As the trend of healthy human food consumption has grown, there has been a corresponding focus on nutritious options for pets. Specifically, natural food, with simple core ingredients, has driven increased spending on pet food. The higher demand for natural food products and more specialized formulas for different life-stages, breed sizes, special needs and diet types has fueled premiumization in the pet food industry, leading to the faster growth of products with higher net sales per unit. This premiumization trend has impacted all market segments and product types in the pet food industry. |

| • | Favorable demographic trends with millennials and higher-income households representing a growth opportunity. Pet ownership among the technology savvy millennial generation (age 18 to 29) was 59% of households in 2014 compared to 50% of households in 2010. Our market research indicates that millennials have higher average intended pet spend compared to baby boomers (age 50 to 68), with 76% of millennials indicating that they would splurge on certain items for pets compared to 50% of boomers. In addition, millennials, who tend to live in more dense urban locations, favor online shopping and social media, which represent additional growth avenues. A significant percentage of pet care and pet food sales also come from households with incomes of over $70,000, according to Packaged Facts. These favorable demographics represent a source for continued long-term industry growth, particularly within pet specialty. |

| • | Shift to specialty retailers. Pet specialty chains comprised 24% of the $43.8 billion in U.S. retail pet product sales in 2014, with discount merchandisers (31%) and grocery (18%) as significant competitors. We believe the pet specialty channel will gain market share from discount merchandisers and grocery, driven by the availability of knowledgeable associates; broader assortments of pet-related products; channel-specific foods and treats; service offerings such as grooming, training and vaccination; millennial customer preference for the specialty experience; and the availability of live animals and adoptions. Moreover, we believe that continued expansion of larger specialty chains, with size and scale leverage, will put increasing pressure on the highly fragmented independent pet specialty retailers. |

| • | Growing importance of omnichannel retailing in the pet industry. In recent years, pet food and pet supply sales have experienced significant growth in the pet specialty and ecommerce channels. Although Packaged Facts estimates that the ecommerce share of total expenditures in the pet food and supply industry was only 4% as of the end of 2014, it is growing rapidly, which we believe is being driven by online convenience, free shipping and reliable delivery advantages. In a recent Packaged Facts survey, nearly 31% of pet parents reported buying pet products online more frequently than they used to, up from only 14% in 2011. As the ecommerce segment grows, we believe the ability to provide an integrated, omnichannel experience by providing customers with the ability to shop for, and manage the needs of, their pets anytime and anywhere will be a competitive advantage over both ecommerce-only retailers and smaller independent retailers. As part of the omnichannel retail experience, we expect channel boundaries to blur, but physical stores will continue to support the vast majority of the market, especially key offerings such as pet services. |

As a result of these major industry trends, we believe that the pet industry will continue to be an attractive, dynamic and growing part of the overall U.S. economy. We also believe that pet parents are increasingly looking for specialty pet retailers, both in-store and online, with the knowledge and expertise to holistically address the health and well-being of their pets and the scale to remain convenient and price competitive on a broad selection of pet products and services.

5

Table of Contents

Our Competitive Strengths

We believe that we will continue to capitalize on attractive industry dynamics as a result of the following key competitive strengths:

Nationally recognized and trusted brand authority in pet retailing. We have one of the most widely recognized brands in the pet industry. We believe unaided brand awareness for Petco is over 70% as of the end of the second quarter of fiscal 2015. Our customers are strong advocates, as demonstrated by our Net Promoter Score (a measure of loyalty based on whether our Pals customers would recommend our stores to a friend or family member), which has consistently increased since implementing the program in 2012 to a score of approximately 75, comparable to other leading retail brands. We believe our long history of service to pet parents has driven brand authenticity and trust with our customers.

Our brand recognition is driven in large part by the scale of our store presence. We are the largest specialty pet retailer in the United States by total number of stores, with over 1,400 stores covering all 50 states, the District of Columbia and Puerto Rico. We also recently successfully expanded into Mexico with a joint venture with Grupo Gigante and currently have 13 Petco stores with plans to open additional stores in the future.

We believe that the scale of our national store footprint provides us with several advantages over smaller chains and independents in maintaining our brand authority, including product purchasing power, integrated marketing efforts and advertising scale, more convenient locations for customers, overall effectiveness in associate training and more robust omnichannel capabilities.

Broad and innovative product and service offerings. We have one of the broadest assortments of pet products and services, including exclusive and private label brands and natural and organic foods.

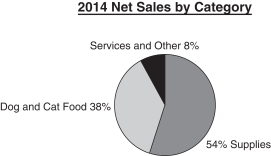

| • | Supplies and companion animal sales represented approximately 54% of our total sales in fiscal 2014. Our supplies offerings combine an extensive assortment, high level of quality and unique offerings through preferred vendor relationships and private label product lines. The companion animals we sell in our stores, which include birds, reptiles, aquatic life and other small animals, and in-store adoption centers also help us to initiate pet parent relationships and acquire long-term customers, in addition to creating a fun and engaging in-store shopping experience. |

| • | Food and consumables represented approximately 38% of our total sales during fiscal 2014. We are well-positioned to capitalize on the premium food trend by providing an extensive assortment of natural and organic pet brands, including leading natural brands that are currently not carried by our closest pet specialty competitor. |

| • | Services represented approximately 8% of our total sales in fiscal 2014. We complement our pet food and merchandise offerings with in-store grooming and training offerings to address the humanization-related increased demand for pet services. We complement these core services with our Vetco mobile vaccination in-store clinics, which supported over 80% of our locations as of the end of fiscal 2014. |

We believe that as a result of the actions we have taken to refine our product and service offerings, we are well-positioned to maximize our exposure to the fastest-growing segments of the pet industry. We believe the quality and breadth of our product offerings, combined with the services we offer, make Petco a leading retail destination and drive customer loyalty.

6

Table of Contents

A differentiated customer engagement approach. At the core of our business model is a focus on creating a genuine, supportive long-term relationship with the pet parent. We accomplish this through our knowledgeable in-store associates, interactive store experiences, customer rewards program and targeted marketing. We use years of customer insights from our 19.1 million active Pals loyalty card member database to train our in-store associates to generate high-content discussions with customers about pet nutrition, behavior and services. This consultative approach is even more involved around companion animal purchase and adoption activities. A key to our store environments has been improving store navigation through enhanced visual merchandising and display, right-sizing of categories and brands through space optimization, as well as innovation around new “shop in shops” like fun and fashion accessories, health and wellness, and natural, all of which are high-growth categories. We are not simply transaction-focused, but strive to create an interactive customer experience that drives regular return visits and establishes Petco as a one stop shop for all pet needs. Our customer data, gathered through our Pals loyalty program, demonstrates the high frequency and value of our best customers. For example, the top 10% of our Pals database customers on average visit Petco 18 times per year and spend an average of $856 per year. We also utilize our six-million customer e-mail database to contact customers with informational, promotional and loyalty-related direct marketing. We track our overall progress in customer engagement through our Net Promoter Score framework, which has demonstrated improving scores since its implementation in 2012. We believe our highly trained sales associates and data-driven customer engagement model have been effective in driving the quality of the shopping experience and visits to our stores.

Well-positioned store base and flexible real estate strategy. We have developed two store formats that enable us to appeal to a broad range of customers in different markets and locations. As of August 1, 2015, we had 1,283 Petco stores in urban, suburban and rural markets that generally range from 6,000 to 15,000 square feet and average 14,000 square feet. As of August 1, 2015, we also operated 126 Unleashed stores in or around urban markets, which average 5,000 square feet and are designed to have particular appeal to the millennial customer. The physical look of our stores has kept pace with investments across our chain to ensure that they are well-maintained and that we continue to innovate and improve our in-store experience. Approximately 46% of our stores have been remodeled, and 76% of our retail footprint has been opened or remodeled, since fiscal 2010. Our flexible store model enables us to appeal to a broad range of customers at different life stages and in urban, suburban and rural markets, which we believe enhances our growth prospects in each of these markets.

Leading omnichannel capabilities. We have the largest integrated ecommerce offering in pet specialty retail, with Petco.com, DrsFosterSmith.com, Liveaquaria.com and Unleashed.com collectively generating over $185 million in total net sales during the first two quarters of fiscal 2015. While in 2014 approximately 4% of overall pet food and supplies spending in the pet industry (excluding services) was attributable to ecommerce, the portion of our net sales generated through our websites was approximately 8.5% during the first two quarters of fiscal 2015. Petco.com recreates the in-store experience by focusing on a fun, content-driven shopping experience for online customers. We offer leading convenience capabilities with our broad national footprint and ecommerce capabilities, including our repeat delivery service for consumables and supplies and our recent partnership with Instacart, which provides same-day delivery of Petco products in major U.S. cities. We acquired DrsFosterSmith.com in fiscal 2015, which enables us to offer a complementary assortment of online pet pharmacy, prescription food and therapeutic, health and wellness products. In 2015, DrsFosterSmith.com was among the top ten most trustworthy websites in the country according to the Online Trust Alliance. Our sites collectively have 2.5 million active customers and provide us with a substantial base for direct marketing efforts to help facilitate repeat visits to stores and online

7

Table of Contents

purchases. Combined with our flexible store format, we seek to utilize our ecommerce capabilities to provide a seamless, integrated experience focused on quality, customer service and convenience.

Proven and experienced management team. We have an experienced and proven management team of successful retail industry veterans. Our Chief Executive Officer and Chairman of our Board of Directors, Jim Myers, has spent his entire 25-year retail career with Petco. Our Executive Vice President and Chief Financial Officer, Michael Nuzzo, has over 15 years of retail experience and brings extensive financial and operational experience from both GNC Holdings and Abercrombie & Fitch. Brad Weston, our President and Chief Merchandising Officer, with 27 years of experience in the retail industry, has served at Petco for three years, having previously served as Senior Vice President and Chief Merchandising Officer at Dick’s Sporting Goods for five years. Our management team has delivered consistent top- and bottom-line results throughout business cycles and has developed and implemented a number of initiatives to strengthen our future competitive positioning and growth prospects.

Our Growth Strategy

We grew our net sales at a CAGR of 8.0% from fiscal 2010 to fiscal 2014, while the pet industry as a whole grew at a CAGR of 4.1% during the same period. We believe our continued focus on the high-growth segments of the pet industry will enable us to continue to outpace the overall growth of the pet industry. We believe our competitive strengths, combined with our strategic investments in our business, position us to capitalize on industry drivers. Key elements of our future growth strategy are detailed below.

Increase core business comparable sales growth.

Continue to elevate our customer engagement efforts. We view our customer engagement model as a significant competitive advantage, and we continue to find ways to improve our approach, both online and in stores, to fuel increased sales growth. Our engagement efforts focus on each stage of the customer lifecycle, from early engagement welcome emails to growth- and retention-based brand initiatives and event-based campaigns to win back customer appreciation and reactivation efforts. We see opportunities to improve the cross-selling of merchandise and services through a mix of promotional and informational messaging, including by offering more customized e-mails to our Pals members to more effectively generate return visits. We are also exploring an opportunity to generate cross-selling synergies between our Petco and Drs. Foster and Smith customer bases. We are a leader among pet specialty retailers in social media, with millions of members, fans, and followers across Facebook, Twitter, Instagram, Pinterest and other social media outlets. Social media engagement enables us to effectively reach our customers, particularly millennial customers who on average significantly outpace baby boomers in omnichannel shopping habits and pet accessory “splurge” tendencies. Overall, we seek to be at the forefront of the shift to more individualized marketing and customer engagement, creating a loyalty-based, lifetime value proposition for pet parents that increases visit frequency and per trip expenditure levels.

Convert more customers to premium pet food buyers. The pet food category is a key driver of traffic for our stores and our websites that offer food products. For example, the total average size of transactions including food purchases was approximately 34% higher than non-food purchases during the second quarter of fiscal 2015. Pals members purchasing food during the second quarter of fiscal 2015 also made an average of approximately 3.1 trips to our stores during the quarter, compared to approximately 1.8 average trips made by Pals members who did not purchase food during the quarter.

8

Table of Contents

As pet parents are often resistant to switching pet foods, we designed our most recent advertising campaign—“what we feed them matters”—around inspiring pet parents to think critically about nutrition. In fiscal 2015 we also launched our Petco in-store demo program, which offers free pet food samples and nutritional information on brands and pet nutrition alternatives. The advertising campaign and demo program are supported by enhanced in-store associate training on nutrition conversations with customers.

With our high-quality, broad assortment of premium and natural pet food, as well as our integrated product and services offerings and compelling in-store and online experience, we are well-positioned to drive sales growth and increase customer retention by converting customers to our differentiated assortment of premium pet food brands. Although we generally do not have formal exclusivity agreements with our vendors, several of these brands are not carried by our closest competitors. Many of these brands are innovative and new, helping differentiate our product offering, further reinforcing the Petco brand as an authority in pet retailing. These brand offerings are typically higher margin due to their natural and premium qualities. We are consistently enhancing our offerings by establishing new relationships with brands we believe recognize our ability to help build brand awareness for their products and leverage the premium pricing opportunities of the specialty pet channel.

Increase penetration of pet services. Pet services is one of the fastest-growing segments in pet specialty retail with a projected CAGR of 6.2% from 2014 to 2019. While our services net sales grew at nearly twice the projected growth rate of the pet services industry in fiscal 2014, it represented only 7.7% of our total fiscal 2014 net sales. We have taken a number of steps to expand and enhance our services offerings to enable us to continue to outpace the overall pet services industry and to capitalize on this key sales growth driver. We use our many on-site pet services offerings to create the feel of an in-store theater, which we believe provides our customers with an experiential shopping environment that builds and promotes customer loyalty. We believe our services offerings distinguish us from other ecommerce and pet retailers. Our services are an important component of driving the in-store experience for our customers and enhancing the frequency of customer visits and total expenditures. For example, based on recent analysis, our dog-grooming customers generally visit our stores 50% more often than our average store customer, with close to double the amount spent per year (including grooming spend).

In fiscal 2014, we introduced a new store format and remodel design that positions services front and center within an overall health and wellness theme. We have also made changes to our management and employee compensation structures to drive further growth of our pet services business. We plan to further integrate vaccination services through our in-house Vetco business. We believe these investments position us well to continue to gain market share in the pet services industry.

Expand private label product sales. Our private label offering of pet supplies accounted for 15% of our net sales in fiscal 2014 and from fiscal 2010 to fiscal 2014 we grew our private label sales at a CAGR of 7.1%. We have an established infrastructure for developing, introducing and fostering growth in private label products, including a dedicated sourcing office in Asia, established in 2007. We intend to increase our private label sales by increasing penetration of existing brands such as You & Me, Well & Good, Sophresh, Bowl Mates and Bootique. We also intend to continue to expand our offering of new products and brands, including by opportunistically licensing additional brands. We also have an opportunity to leverage our Drs. Foster and Smith brand for developing veterinarian-approved product lines that can support both our online and store merchandising initiatives. We believe growing our private label sales will enhance overall net sales growth and drive gross margin rate benefit.

9

Table of Contents

Expand our integrated omnichannel model.

Continue to open profitable new stores. We believe our compelling product offering, leading customer engagement and the success of our flexible format stores across a broad range of geographic regions and population densities creates a significant opportunity to profitably increase our store count. Our flexible format stores, which generally range from 4,000 to 15,000 square feet, permit us to enter a wide range of markets to capitalize on attractive growth opportunities. For example, our smaller format Unleashed stores provide a differentiated market fill-in opportunity in urban centers. Our Petco store model has attractive economics for urban, suburban and more rural market settings. Based on our internal estimates, there are 800 to 900 additional locations in the United States that fit our performance requirements for new stores.

In addition, through our joint venture in Mexico with Grupo Gigante, we have successfully expanded the Petco store brand into Mexico, where we currently have 13 stores and plan to open additional stores in the future. Our initial performance in Mexico has greatly exceeded our internal expectations and creates a model for further potential international expansion.

Link stores, web and mobile in an integrated digital platform. We intend to utilize our leading digital presence, customer engagement programs such as Pals and new technology implementation to grow our omnichannel leadership position and acquire market share in the evolving pet retail landscape. Our strategy includes the following initiatives:

| • | Our Petco.com and DrsFosterSmith.com websites are already leading ecommerce banners. We expect our new 2015 IBM web platform implementation to enhance our advanced digital capabilities that will facilitate channel offerings like repeat delivery. |

| • | We are installing a new technology and communications infrastructure at our stores and equipping store associates with tablet devices to enable in-store online orders from our websites, known as “extended aisle.” We are also upgrading our in-store services scheduling technology to enhance our ability to generate repeat visits and cross-sell health and wellness merchandise. We expect this technology investment will enable future online-to-store links and give us additional flexibility for taking and fulfilling customer transactions. |

| • | We plan to continue to expand our same day delivery service partnership with Instacart, which currently offers 13,000 Petco stock-keeping units (“SKUs”) to customers in over 50 cities, including New York, Boston, Chicago, San Francisco and Los Angeles. |

Align organizational incentives to drive omnichannel growth. We believe that aligning incentives, training and communication programs to support omnichannel is as important as digital asset implementation to driving significant net sales growth. For example, we are augmenting incentive programs for our store organization to also reward in-store efforts to generate online sales. We believe that if our employees have an equal incentive to foster a strong customer relationship any time through any channel, we can drive an overall higher total company net sales growth rate.

Drive operational excellence.

Invest in new innovative revenue driving capabilities. We have a history of making strategic investments in systems, infrastructure, and complementary businesses to drive growth. Our management team has a disciplined focus and advanced return-on-investment framework for capital

10

Table of Contents

allocation decisions related to new stores, distribution facilities, and home office assets. We also regularly evaluate business acquisition opportunities in the pet industry. Overall, we seek to remain close to new and emerging business trends in the industry and take a measured approach to assessing their potential growth value to Petco.

Drive cost optimization in order to re-allocate resources to new growth opportunities. We continually seek to optimize our business model by rationalizing our cost structure and investing in future growth drivers. We have a track record of more than 20 years of profitable net sales growth and a continued focus on our expense base. Through a comprehensive assessment of our cost structure, we have identified additional cost saving opportunities in several areas, including cost of goods sold, operating expenses, distribution efficiency and corporate general and administrative expenses. We believe these opportunities for additional savings can result in further margin and profitability expansion and help us to maintain our long track-record of profitable net sales growth.

Utilize the Petco Foundation to drive organizational mission. The Petco Foundation, a separately incorporated 501(c)(3) nonprofit organization, invests in ground-breaking animal welfare work and finds homes for more than 400,000 pets last year through our Think Adoption First program in support of our mission to find a home for animals in need. The Petco Foundation is a significant factor in facilitating pet ownership and is aligned with our mission of making sure pets enjoy the best nutrition and the highest quality of life in loving homes. Since we believe that operational excellence is largely culturally influenced, the Petco Foundation serves as a meaningful employee rallying point that creates significant opportunities for continued success.

Risks Related to Our Business

An investment in our common stock involves a high degree of risk. Among these important risks are the following:

| • | general economic factors or failure to successfully predict and respond to changing consumer trends and demand could materially adversely affect our sales, results of operations and cash flow; |

| • | competition, including Internet-based competition, could negatively impact our business; |

| • | any damage to our reputation or our brand could materially adversely affect our business, financial condition and results of operations; |

| • | we may not be able to successfully execute our expansion strategy, including our international expansion, or manage and sustain our recent growth; |

| • | the loss of any of our key merchandise vendors, or of our exclusive distribution arrangements with certain of our vendors, would negatively impact our business; |

| • | product recalls and product liability exposure, as well as changes in product safety and other consumer protection laws, could increase our costs and otherwise restrict our operations; |

| • | breaches of, or interruptions in, our data security and information systems could disrupt or business and expose us to risk of loss; and |

| • | our substantial indebtedness could adversely affect our financial condition and limit our ability to pursue our growth strategy. |

See “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.”

11

Table of Contents

Our Sponsors

TPG. TPG Global, LLC (together with its affiliates, “TPG”) is a leading global private investment firm founded in 1992 with more than $74 billion of assets under management as of June 30, 2015, and offices in San Francisco, Fort Worth, Austin, Beijing, Dallas, Hong Kong, Houston, London, Luxembourg, Melbourne, Moscow, Mumbai, New York, São Paulo, Shanghai, Singapore, Tokyo and Toronto. TPG has extensive experience with global public and private investments executed through leveraged buyouts, recapitalizations, spinouts, growth investments, joint ventures and restructurings. The firm’s investments span a variety of industries, including healthcare, financial services, travel and entertainment, technology, energy, industrials, retail, consumer, real estate and media and communications.

LGP. Founded in 1989 and based in Los Angeles, Leonard Green & Partners (‘‘LGP,” and together with TPG, the “Sponsors”) is one of the nation’s leading private equity firms. LGP frequently invests in companies that are leaders in their markets, including The Container Store, Shake Shack, Whole Foods Market, Jetro Cash & Carry, Activision, CHG Healthcare and Life Time Fitness. The firm invests in traditional buyouts, going-private transactions, recapitalizations, growth capital investments, corporate carve-outs and selective public equity and debt positions. LGP has a long history of investing in the pet sector, including its investment in VCA, a nationwide veterinarian hospital chain that went public in 2001.

We are party to certain agreements with the Sponsors and their affiliates, including a stockholders’ agreement pursuant to which the Sponsors and other stockholders have rights with respect to the designation of director nominees and a management services agreement pursuant to which affiliates of the Sponsors provide management, consulting and other services to us from time to time. Pursuant to the management services agreement, we will pay an aggregate of $ million upon its termination in connection with this offering. See “Certain Relationships and Related Party Transactions.”

We are currently controlled, and after this offering is completed will continue to be controlled, by the Sponsors and certain other significant stockholders. Upon completion of this offering, investment funds affiliated with the Sponsors and certain other significant stockholders will beneficially own % of our outstanding common stock (or % if the underwriters exercise in full their option to purchase additional shares from the selling stockholders). As long as the Sponsors and other significant stockholders own or control at least a majority of our outstanding voting power, they will have the ability to exercise substantial control over all corporate actions requiring stockholder approval, irrespective of how our other stockholders may vote, including the election and removal of directors and the size of our board, any amendment of our certificate of incorporation or bylaws, or the approval of any merger or other significant corporate transaction, including a sale of substantially all of our assets. Even if their ownership falls below 50%, the Sponsors and other significant stockholders will continue to be able to strongly influence or effectively control our decisions.

The Sponsors’ interests may not align with the interests of our other stockholders. The Sponsors are in the business of making investments in companies and may acquire and hold interests in businesses that compete directly or indirectly with us. The Sponsors may also pursue acquisition opportunities that may be complementary to our business, and, as a result, those acquisition opportunities may not be available to us. See “Risks Related to Our Common Stock and this Offering— Our Sponsors and certain other significant stockholders will continue to have significant influence over us after this offering, including control over decisions that require the approval of stockholders, which could limit your ability to influence the outcome of matters submitted to stockholders for a vote.”

12

Table of Contents

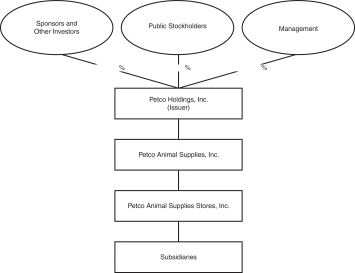

Corporate Information and Structure

Petco Holdings, Inc. is a Delaware corporation that was formed in October 2012 in connection with a corporate restructuring to support the Company’s capital structure. Its only material assets are the shares of the equity of Petco Animal Supplies, Inc., a Delaware corporation, which is the holder of 100% of the equity of Petco Animal Supplies Stores, Inc., a Delaware corporation. Petco Holdings, Inc. does not conduct any operations other than with respect to its direct and indirect ownership of its subsidiaries and conducts all of its business through Petco Animal Supplies and its subsidiaries. Our principal executive offices are located at 10850 Via Frontera, San Diego, California 92127, and our telephone number at that location is (858) 453-7845. Our website address is www.petco.com. Our website is included as an inactive textual reference only and our website and the information contained on our website do not constitute a part of this prospectus.

The following chart shows our simplified organizational structure immediately following the consummation of this offering assuming no exercise of the underwriters’ option to purchase additional shares:

13

Table of Contents

THE OFFERING

| Common stock offered by the selling stockholders |

shares. |

| Common stock to be outstanding after this offering |

shares. |

| Option to purchase additional shares of common stock |

additional shares from the selling stockholders. |

| Use of proceeds |

We will not receive any of the proceeds from the sale of shares by the selling stockholders. See “Use of Proceeds. |

| Dividend policy |

Our Board of Directors does not currently intend to pay dividends on our common stock. However, we expect to reevaluate our dividend policy on a regular basis following the offering and may, subject to compliance with the covenants contained in our credit facilities and other considerations, determine to pay dividends in the future. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources” and “Description of Indebtedness” for restrictions on our ability to pay dividends. |

| Risk factors |

You should read the “Risk Factors” section of this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

| Stock exchange listing and proposed symbol |

We have applied to list our common stock on under the symbol “ .” |

| Conflicts of interest |

Certain affiliates of TPG Capital BD, LLC, an underwriter in this offering, will own in excess of 10% of our issued and outstanding common stock following this offering. In addition, these affiliates of TPG Capital BD, LLC, as selling stockholders, will receive more than 5% of the net proceeds of this offering. As a result of the foregoing relationships, TPG Capital BD, LLC is deemed to have a “conflict of interest” within the |

14

Table of Contents

| meaning of FINRA Rule 5121. Accordingly, this offering will be made in compliance with the applicable provisions of FINRA Rule 5121. Pursuant to that rule, the appointment of a qualified independent underwriter is not necessary in connection with this offering. In accordance with FINRA Rule 5121(c), no sales of the shares will be made to any discretionary account over which TPG Capital BD, LLC exercises discretion without the prior specific written approval of the account holder. See “Underwriting—Conflicts of Interest.” |

The number of shares of common stock to be outstanding after this offering is based on shares of common stock outstanding as of , 2015 and excludes the following:

| • | shares of common stock issuable upon exercise of stock options outstanding as of , 2015 at a weighted average exercise price of $ per share; |

| • | that number of shares of common stock issuable upon exercise of a warrant to purchase shares of common stock, exercisable in connection with this offering, determined by dividing $ by the average closing price of a share of our common stock as reported on for the first 30 consecutive trading days commencing on the effective date of this offering; |

| • | shares of common stock underlying restricted stock units (“RSUs”) subject to future vesting requirements as of , 2015; and |

| • | shares of common stock reserved for future issuance under our equity incentive plans as of , 2015. |

Unless otherwise indicated, this prospectus reflects and assumes the following:

| • | an initial public offering price of $ per share, the midpoint of the price range set forth on the cover page of this prospectus; |

| • | the adoption of our restated certificate of incorporation and our amended and restated bylaws, to be effective upon the closing of this offering; |

| • | no exercise by the underwriters of their option to purchase up to additional shares of our common stock in this offering; and |

| • | for all periods, a for reverse split of our common stock effected on , 2015. |

15

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following table sets forth summary historical consolidated financial data for the periods presented and at the dates indicated below. We have derived the balance sheet data as of January 31, 2015 and February 1, 2014 and the statement of income and comprehensive income and cash flow data for fiscal years 2014, 2013 and 2012 from our audited consolidated financial statements included elsewhere in this prospectus. We have derived the balance sheet data as of August 1, 2015 and August 2, 2014 and the statement of income and comprehensive income and cash flow data for the 26-week period ended August 1, 2015 and August 2, 2014 from our unaudited interim condensed consolidated financial statements, included elsewhere in this prospectus.

Historical results are not necessarily indicative of the results to be expected for future periods and operating results for the 26 weeks ended August 1, 2015 are not necessarily indicative of the results that may be expected for the fiscal year ending January 30, 2016. The following information should be read in conjunction with the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the notes thereto contained elsewhere in this prospectus.

Our fiscal year ends on the Saturday closest to January 31, resulting in fiscal years of either 52 or 53 weeks. All references to a fiscal year refer to the fiscal year ending on the Saturday closest to January 31 of the following year. For example, references to fiscal 2014 refer to the fiscal year beginning February 2, 2014 and ending January 31, 2015, references to fiscal 2013 refer to the fiscal year beginning February 2, 2013 and ending February 1, 2014 and references to fiscal 2012 refer to the fiscal year beginning January 28, 2012 and ending February 2, 2013. Fiscal 2014 and fiscal 2013 each include 52 weeks, and fiscal 2012 includes 53 weeks.

| Fiscal Year Ended | 26 Weeks Ended | |||||||||||||||||||

| (Dollars in thousands, except per share data) | January 31, 2015 (Fiscal 2014) |

February 1, 2014 (Fiscal 2013) |

February 2, 2013 (Fiscal 2012) |

August 1, 2015 |

August 2, 2014 |

|||||||||||||||

| (53 weeks) | (unaudited) | (unaudited) | ||||||||||||||||||

| Statement of operations data: |

||||||||||||||||||||

| Net sales |

$ | 3,995,368 | $ | 3,785,153 | $ | 3,528,030 | $ | 2,168,705 | $ | 1,941,408 | ||||||||||

| Cost of sales and occupancy costs |

2,778,427 | 2,601,855 | 2,403,065 | 1,514,751 | 1,351,611 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

1,216,941 | 1,183,298 | 1,124,965 | 653,954 | 589,797 | |||||||||||||||

| Selling, general and administrative expenses |

928,684 | 884,991 | 837,681 | 498,539 | 455,558 | |||||||||||||||

| Goodwill impairment charges |

7,753 | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income |

280,504 | 298,307 | 287,284 | 155,415 | 134,239 | |||||||||||||||

| Interest income |

(422 | ) | (119 | ) | (372 | ) | (199 | ) | (134 | ) | ||||||||||

| Interest expense |

159,292 | 157,143 | 128,123 | 78,345 | 79,955 | |||||||||||||||

| Loss on extinguishment of debt |

— | 3,810 | — | — | — | |||||||||||||||

| Other expenses |

— | 1,364 | 642 | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before income taxes and (income) loss from equity method investees |

121,634 | 136,109 | 158,891 | 77,269 | 54,418 | |||||||||||||||

| Income tax expense |

46,398 | 50,836 | 60,070 | 30,588 | 21,531 | |||||||||||||||

| (Income) Loss from equity method investees |

(106 | ) | 508 | — | (327 | ) | 96 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 75,342 | $ | 84,765 | $ | 98,821 | $ | 47,008 | $ | 32,791 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income per share attributable to common stockholders |

$ | $ | $ | $ | $ | |||||||||||||||

| Basic |

||||||||||||||||||||

| Diluted |

||||||||||||||||||||

| Weighted average common shares outstanding |

||||||||||||||||||||

| Basic |

||||||||||||||||||||

| Diluted |

||||||||||||||||||||

| Cash dividends declared per common share |

$ | — | $ | — | $ | $ | — | $ | — | |||||||||||

16

Table of Contents

| Fiscal Year Ended | 26 Weeks Ended | |||||||||||||||||||

| (Dollars in thousands, except per square foot) | January 31, 2015 (Fiscal 2014) |

February 1, 2014 (Fiscal 2013) |

February 2, 2013 (Fiscal 2012) |

August 1, 2015 |

August 2, 2014 |

|||||||||||||||

| (53 weeks) | (unaudited) | (unaudited) | ||||||||||||||||||

| Store data: |

||||||||||||||||||||

| Number of stores at period end |

1,383 | 1,314 | 1,230 | 1,409 | 1,364 | |||||||||||||||

| Comparable sales growth(1) |

1.8 | % | 4.9 | % | 7.6 | % | 2.9 | % | 0.8 | % | ||||||||||

| Rent expense(2) |

$ | 354,311 | $ | 334,964 | $ | 322,168 | $ | 183,206 | $ | 173,945 | ||||||||||

| Net sales per square foot(3) |

$ | 217.0 | $ | 213.4 | $ | 208.6 | $ | 115.4 | $ | 106.8 | ||||||||||

| As of | As of | |||||||||||||||||||

| (Dollars in thousands) | January 31, 2015 (Fiscal 2014) |

February 1, 2014 (Fiscal 2013) |

February 2, 2013 (Fiscal 2012) |

August 1, 2015 |

August 2, 2014 |

|||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||

| Balance sheet data (end of period): |

||||||||||||||||||||

| Cash and cash equivalents |

$ | 191,265 | $ | 135,793 | $ | 130,367 | $ | 57,948 | $ | 77,183 | ||||||||||

| Merchandise inventories |

393,808 | 386,240 | 334,521 | 453,497 | 408,756 | |||||||||||||||

| Working capital(4) |

250,326 | 235,281 | 173,088 | 183,513 | 218,415 | |||||||||||||||

| Fixed assets, net |

591,812 | 513,877 | 487,378 | 621,710 | 552,981 | |||||||||||||||

| Total assets |

2,706,981 | 2,543,754 | 2,462,073 | 2,835,797 | 2,589,315 | |||||||||||||||

| Total debt(5) |

2,268,211 | 2,238,048 | 2,240,942 | 2,316,253 | 2,233,185 | |||||||||||||||

| Net debt(6) |

2,076,946 | 2,102,255 | 2,110,575 | 2,258,305 | 2,156,002 | |||||||||||||||

| Stockholders’ deficit |

(330,338 | ) | (410,271 | ) | (512,123 | ) | (285,517 | ) | (370,935 | ) | ||||||||||

| Fiscal Year Ended | 26 Weeks Ended | |||||||||||||||||||

| (Dollars in thousands, except per square foot) | January 31, 2015 (Fiscal 2014) |

February 1, 2014 (Fiscal 2013) |

February 2, 2013 (Fiscal 2012) |

August 1, 2015 |

August 2, 2014 |

|||||||||||||||

| (53 weeks) | (unaudited) | (unaudited) | ||||||||||||||||||

| Other financial data: |

||||||||||||||||||||

| Net cash provided by (used for) Operating activities |

$ | 245,432 | $ | 164,553 | $ | 248,423 | $ | 92,503 | $ | 58,185 | ||||||||||

| Investing activities |

(213,728 | ) | (145,753 | ) | (178,416 | ) | (269,427 | ) | (109,123 | ) | ||||||||||

| Financing activities |

23,768 | (13,374 | ) | (61,659 | ) | 43,607 | (7,672 | ) | ||||||||||||

| Capital expenditures |

(191,627 | ) | (136,008 | ) | (160,160 | ) | (106,778 | ) | (101,810 | ) | ||||||||||

| Depreciation and amortization(7) |

130,791 | 115,929 | 106,922 | 69,226 | 61,661 | |||||||||||||||

| EBITDA(8) |

411,401 | 408,554 | 393,564 | 224,968 | 195,804 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA(8) |

$ | 456,808 | $ | 437,101 | $ | 420,377 | $ | 240,063 | $ | 208,931 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted Net Income(8) |

$ | 103,443 | $ | 99,376 | $ | 115,098 | $ | 56,153 | $ | 40,715 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | Comparable sales growth is for retail locations and ecommerce. A new store or website becomes comparable on the first day of the fiscal month following 12 full fiscal months of operation. Relocated stores become comparable stores on the first day of operation if original store was open longer than 12 full fiscal months. If, during the period presented, a store was closed, sales from that store are included up to the first day of the month of closing. See “Management’s Discussion and Analysis of Results of Operations and Financial Condition—How We Assess the Performance of our Business.” |

| (2) | Rent expense includes rent for stores and distribution centers and other small equipment leases. |

| (3) | Net sales per square foot is calculated by dividing net sales, including ecommerce sales, by total square footage as of the end of each fiscal year. |

| (4) | Working capital is defined as current assets less current liabilities. |

| (5) | Total debt includes obligations under our senior secured credit facilities, senior notes, senior payment-in-kind (“PIK”) toggle notes, capital lease and mortgage liabilities. |

| (6) | Net debt is defined as total debt less cash and cash equivalents. |

| (7) | Depreciation and amortization includes asset impairments and write-offs of $8.9 million, $2.3 million and $0.3 million for fiscal years 2014, 2013 and 2012, respectively. Asset impairments and write-offs for the 26-week period ending August 1, 2015 and August 2, 2014 included in depreciation and amortization were $1.8 million and $2.7 million, respectively. |

| (8) | EBITDA, Adjusted EBITDA and Adjusted Net Income are financial measures that are not defined under U.S. GAAP. We use these non-GAAP financial measures, and believe they enhance an investor’s understanding of our financial and operating performance from period to period, because they exclude certain material non-cash items, unusual or non-recurring items |

17

Table of Contents

| that we do not expect to continue in the future and certain other adjustments we believe are not reflective of our ongoing operations and our performance. We also report Adjusted EBITDA, or variations of this metric required under the indentures and credit agreements governing our outstanding indebtedness, to our lenders and noteholders. Certain of our debt covenants use Adjusted EBITDA or variations of this metric, including covenants regarding amounts of permitted liens we may incur and restricted payments we may make. We believe that EBITDA, Adjusted EBITDA and Adjusted Net Income provide investors with a useful tool for assessing the comparability between periods of our ability to generate cash from operations sufficient to pay taxes, to service debt and to undertake capital expenditures. We use these metrics to measure our core financial and operating performance for business planning purposes, to assess our liquidity and to compare our performance to that of our competitors. In addition, we believe EBITDA, Adjusted EBITDA and Adjusted Net Income are measures commonly used by investors to evaluate companies in the pet industry. However, they are not presentations made in accordance with U.S. GAAP and the use of the terms EBITDA, Adjusted EBITDA and Adjusted Net Income vary from others in our industry. These financial measures are not intended to represent and should not be considered as alternatives to net income, operating income or any other performance measures derived in accordance with GAAP as measures of operating performance or operating cash flows or as measures of liquidity. |

| EBITDA, Adjusted EBITDA and Adjusted Net Income have important limitations as analytical tools and you should not consider them in isolation or as substitutes for analysis of our results as reported under GAAP. For example, these financial measures: |

| • | exclude certain tax payments that may reduce cash available to us; |

| • | do not reflect any cash capital expenditure requirements for the assets being depreciated and amortized that may have to be replaced in the future; |

| • | do not reflect changes in, or cash requirements for, our working capital needs; |

| • | do not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt; and |

| • | other companies in our industry may calculate these measures differently than we do, limiting their usefulness as comparative measures. |

| The table below illustrates a reconciliation of net income to EBITDA, Adjusted EBITDA and Adjusted Net Income for the periods presented: |

| Fiscal Year Ended | 26 Weeks Ended | |||||||||||||||||||

| (Dollars in thousands) | January 31, 2015 (Fiscal 2014) |

February 1, 2014 (Fiscal 2013) |

February 2, 2013 (Fiscal 2012) |

August 1, 2015 |

August 2, 2014 |

|||||||||||||||

| (53 weeks) | (unaudited) | (unaudited) | ||||||||||||||||||

| Net income |

$ | 75,342 | $ | 84,765 | $ | 98,821 | $ | 47,008 | $ | 32,791 | ||||||||||

| Interest expense, net |

158,870 | 157,024 | 127,751 | 78,146 | 79,821 | |||||||||||||||

| Income tax expense |

46,398 | 50,836 | 60,070 | 30,588 | 21,531 | |||||||||||||||

| Depreciation and amortization(1) |

130,791 | 115,929 | 106,922 | 69,226 | 61,661 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EBITDA |

$ | 411,401 | $ | 408,554 | $ | 393,564 | $ | 224,968 | $ | 195,804 | ||||||||||

| Stock compensation |

3,095 | 3,083 | 4,940 | 1,465 | 1,444 | |||||||||||||||

| Store pre-opening and closing costs(2) |

10,000 | 8,693 | 8,865 | 4,805 | 3,421 | |||||||||||||||

| Management fees(3) |

6,666 | 7,356 | 6,928 | 3,170 | 3,352 | |||||||||||||||

| Loss on debt extinguishment |

— | 3,810 | — | — | — | |||||||||||||||

| Term loan amendment fees(4) |

— | 1,364 | 642 | — | — | |||||||||||||||

| Relocation, retention, severance and other related miscellaneous costs |

9,999 | 3,733 | 5,239 | 3,360 | 4,814 | |||||||||||||||

| Other adjustments(5) |

15,647 | 508 | 199 | 2,295 | 96 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 456,808 | $ | 437,101 | $ | 420,377 | $ | 240,063 | $ | 208,931 | ||||||||||

| Depreciation and amortization |

(130,791 | ) | (115,929 | ) | (106,922 | ) | (69,226 | ) | (61,661 | ) | ||||||||||

| Interest expense, net |

(158,870 | ) | (157,024 | ) | (127,751 | ) | (78,146 | ) | (79,821 | ) | ||||||||||

| Loss on extinguishment of debt |

— | (3,810 | ) | — | — | — | ||||||||||||||

| Other expenses |

— | (1,364 | ) | (642 | ) | — | — | |||||||||||||

| Income taxes, adjusted(6) |

(63,704 | ) | (59,598 | ) | (69,964 | ) | (36,538 | ) | (26,734 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted Net Income |

$ | 103,443 | $ | 99,376 | $ | 115,098 | $ | 56,153 | $ | 40,715 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | Depreciation and amortization includes asset impairments and write-offs. |

18

Table of Contents

| (2) | The add-back of store pre-opening and closing costs are limited to $10.0 million in any four-quarter period, which is consistent with the requirements of reporting adjusted EBITDA under the indenture governing our senior notes. Uncapped pre-opening and closing costs for the fiscal year ended January 31, 2015 were $10.1 million. |

| (3) | Represent annual fees plus out of pocket expenses paid in accordance with a management services agreement with the Sponsors and certain other significant stockholders for management, consulting and other services. The management services agreement terminates in connection with this offering. See “Certain Relationships and Related Party Transactions—Management Services Agreement.” |

| (4) | Term loan amendment fees represent the portion of fees incurred to amend the term loan facility that were recorded as other expenses in the consolidated statements of income and comprehensive income. |

| (5) | Other adjustments include legal settlements, goodwill impairment, income / loss from equity method investees, acquisition & other non-recurring costs. |

| (6) | Represents income tax expense at the effective tax rate derived from our consolidated financial statements for the periods presented as applied to Adjusted EBITDA as defined above but including the impact of depreciation and amortization, interest expense, net, loss on extinguishment of debt and certain other expenses. |

19

Table of Contents

This offering and investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below together with all of the other information contained in this prospectus, including the section titled “Cautionary Note Regarding Forward-Looking Statements” and our consolidated financial statements and the related notes appearing at the end of this prospectus, before deciding to invest in our common stock. If any of the following risks actually occurs, our business, prospects, operating results and financial condition could suffer materially, the trading price of our common stock could decline and you could lose all or part of your investment. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or deemed to be material by us may impair our operations and performance.

Risks Related to Our Business

A decline in consumer spending or a change in consumer preferences or demographics could reduce our sales or profitability and adversely affect our business.

Our sales depend on consumer spending, which is influenced by factors beyond our control, including general economic conditions, the availability of discretionary income and credit, weather, consumer confidence and unemployment levels. We may experience declines in sales or changes in the types of products and services sold during economic downturns. Our business would be harmed by any material decline in the amount of consumer spending, which could reduce our sales, or a decrease in the sales of higher-margin products, such as certain of our supplies offerings, which could reduce our profitability and adversely affect our business.