Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - Resolute Forest Products Inc. | rfp-2015630xex312.htm |

| EX-32.2 - EXHIBIT 32.2 - Resolute Forest Products Inc. | rfp-2015630xex322.htm |

| EX-31.1 - EXHIBIT 31.1 - Resolute Forest Products Inc. | rfp-2015630xex311.htm |

| EX-32.1 - EXHIBIT 32.1 - Resolute Forest Products Inc. | rfp-2015630xex321.htm |

| EX-10.2 - EXHIBIT 10.2 - Resolute Forest Products Inc. | rfp-2015630xex102.htm |

| EX-10.3 - EXHIBIT 10.3 - Resolute Forest Products Inc. | rfp-2015630xex103.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

FOR THE QUARTERLY PERIOD ENDED JUNE 30, 2015

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

FOR THE TRANSITION PERIOD FROM TO

COMMISSION FILE NUMBER: 001-33776

RESOLUTE FOREST PRODUCTS INC.

(Exact name of registrant as specified in its charter)

Delaware | 98-0526415 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. employer identification number) |

111 Duke Street, Suite 5000; Montréal, Québec; Canada H3C 2M1 |

(Address of principal executive offices) (Zip Code) |

(514) 875-2515 |

(Registrant’s telephone number, including area code) |

(Former name, former address and former fiscal year, if changed since last report) |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

(Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No þ

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes þ No ¨

As of July 31, 2015, there were 91,306,132 shares of Resolute Forest Products Inc. common stock, $0.001 par value, outstanding.

RESOLUTE FOREST PRODUCTS INC.

TABLE OF CONTENTS

Page Number | ||

PART I. FINANCIAL INFORMATION | ||

Item 1. Financial Statements: | ||

PART II. OTHER INFORMATION | ||

PART I. | FINANCIAL INFORMATION |

ITEM 1. | FINANCIAL STATEMENTS |

RESOLUTE FOREST PRODUCTS INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited, in millions, except per share amounts)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||

2015 | 2014 | 2015 | 2014 | ||||||||||||||

Sales | $ | 926 | $ | 1,091 | $ | 1,846 | $ | 2,107 | |||||||||

Costs and expenses: | |||||||||||||||||

Cost of sales, excluding depreciation, amortization and distribution costs | 692 | 812 | 1,410 | 1,633 | |||||||||||||

Depreciation and amortization | 60 | 62 | 117 | 124 | |||||||||||||

Distribution costs | 118 | 134 | 231 | 254 | |||||||||||||

Selling, general and administrative expenses | 40 | 41 | 81 | 77 | |||||||||||||

Closure costs, impairment and other related charges | — | 52 | 6 | 62 | |||||||||||||

Net gain on disposition of assets | — | (2 | ) | — | (2 | ) | |||||||||||

Operating income (loss) | 16 | (8 | ) | 1 | (41 | ) | |||||||||||

Interest expense | (11 | ) | (11 | ) | (23 | ) | (23 | ) | |||||||||

Other income, net | 1 | 20 | 6 | 7 | |||||||||||||

Income (loss) before income taxes | 6 | 1 | (16 | ) | (57 | ) | |||||||||||

Income tax (provision) benefit | (10 | ) | (1 | ) | (20 | ) | 7 | ||||||||||

Net loss including noncontrolling interests | (4 | ) | — | (36 | ) | (50 | ) | ||||||||||

Net income attributable to noncontrolling interests | — | (2 | ) | (1 | ) | (2 | ) | ||||||||||

Net loss attributable to Resolute Forest Products Inc. | $ | (4 | ) | $ | (2 | ) | $ | (37 | ) | $ | (52 | ) | |||||

Net loss per share attributable to Resolute Forest Products Inc. common shareholders: | |||||||||||||||||

Basic | $ | (0.04 | ) | $ | (0.02 | ) | $ | (0.39 | ) | $ | (0.55 | ) | |||||

Diluted | (0.04 | ) | (0.02 | ) | (0.39 | ) | (0.55 | ) | |||||||||

Weighted-average number of Resolute Forest Products Inc. common shares outstanding: | |||||||||||||||||

Basic | 94.1 | 94.6 | 94.5 | 94.6 | |||||||||||||

Diluted | 94.1 | 94.6 | 94.5 | 94.6 | |||||||||||||

See accompanying notes to unaudited interim consolidated financial statements.

1

RESOLUTE FOREST PRODUCTS INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Unaudited, in millions)

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||

2015 | 2014 | 2015 | 2014 | ||||||||||||||

Net loss including noncontrolling interests | $ | (4 | ) | $ | — | $ | (36 | ) | $ | (50 | ) | ||||||

Other comprehensive (loss) income: | |||||||||||||||||

Unamortized prior service credits: | |||||||||||||||||

Change in unamortized prior service credits | (3 | ) | 45 | (8 | ) | 86 | |||||||||||

Income tax provision | — | (17 | ) | — | (34 | ) | |||||||||||

Change in unamortized prior service credits, net of tax | (3 | ) | 28 | (8 | ) | 52 | |||||||||||

Unamortized actuarial losses: | |||||||||||||||||

Change in unamortized actuarial losses | 19 | (4 | ) | 40 | (4 | ) | |||||||||||

Income tax (provision) benefit | (4 | ) | 2 | (9 | ) | 3 | |||||||||||

Change in unamortized actuarial losses, net of tax | 15 | (2 | ) | 31 | (1 | ) | |||||||||||

Foreign currency translation | (1 | ) | 1 | (2 | ) | — | |||||||||||

Other comprehensive income, net of tax | 11 | 27 | 21 | 51 | |||||||||||||

Comprehensive income (loss) including noncontrolling interests | 7 | 27 | (15 | ) | 1 | ||||||||||||

Comprehensive income attributable to noncontrolling interests | — | (2 | ) | (1 | ) | (2 | ) | ||||||||||

Comprehensive income (loss) attributable to Resolute Forest Products Inc. | $ | 7 | $ | 25 | $ | (16 | ) | $ | (1 | ) | |||||||

See accompanying notes to unaudited interim consolidated financial statements.

2

RESOLUTE FOREST PRODUCTS INC.

CONSOLIDATED BALANCE SHEETS

(Unaudited, in millions, except per share amount)

June 30, 2015 | December 31, 2014 | |||||||

Assets | ||||||||

Current assets: | ||||||||

Cash and cash equivalents | $ | 303 | $ | 337 | ||||

Accounts receivable, net: | ||||||||

Trade | 416 | 449 | ||||||

Other | 69 | 90 | ||||||

Inventories, net | 537 | 542 | ||||||

Deferred income tax assets | 65 | 70 | ||||||

Other current assets | 65 | 46 | ||||||

Total current assets | 1,455 | 1,534 | ||||||

Fixed assets, net | 1,944 | 1,985 | ||||||

Amortizable intangible assets, net | 61 | 62 | ||||||

Deferred income tax assets | 1,103 | 1,219 | ||||||

Other assets | 126 | 121 | ||||||

Total assets | $ | 4,689 | $ | 4,921 | ||||

Liabilities and equity | ||||||||

Current liabilities: | ||||||||

Accounts payable and accrued liabilities | $ | 471 | $ | 518 | ||||

Current portion of long-term debt | 1 | 1 | ||||||

Total current liabilities | 472 | 519 | ||||||

Long-term debt, net of current portion | 596 | 596 | ||||||

Pension and other postretirement benefit obligations | 1,474 | 1,616 | ||||||

Deferred income tax liabilities | 3 | 3 | ||||||

Other liabilities | 71 | 70 | ||||||

Total liabilities | 2,616 | 2,804 | ||||||

Commitments and contingencies | ||||||||

Equity: | ||||||||

Resolute Forest Products Inc. shareholders’ equity: | ||||||||

Common stock, $0.001 par value. 117.3 shares issued and 91.6 shares outstanding as of June 30, 2015; 117.3 shares issued and 94.8 shares outstanding as of December 31, 2014 | — | — | ||||||

Additional paid-in capital | 3,762 | 3,754 | ||||||

Deficit | (906 | ) | (869 | ) | ||||

Accumulated other comprehensive loss | (697 | ) | (718 | ) | ||||

Treasury stock at cost, 25.7 shares and 22.5 shares as of June 30, 2015 and December 31, 2014, respectively | (98 | ) | (61 | ) | ||||

Total Resolute Forest Products Inc. shareholders’ equity | 2,061 | 2,106 | ||||||

Noncontrolling interests | 12 | 11 | ||||||

Total equity | 2,073 | 2,117 | ||||||

Total liabilities and equity | $ | 4,689 | $ | 4,921 | ||||

See accompanying notes to unaudited interim consolidated financial statements.

3

RESOLUTE FOREST PRODUCTS INC.

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(Unaudited, in millions)

Six Months Ended June 30, 2015 | ||||||||||||||||||||||||||||

Resolute Forest Products Inc. Shareholders’ Equity | ||||||||||||||||||||||||||||

Common Stock | Additional Paid-In Capital | Deficit | Accumulated Other Comprehensive Loss | Treasury Stock | Non-controlling Interests | Total Equity | ||||||||||||||||||||||

Balance as of December 31, 2014 | $ | — | $ | 3,754 | $ | (869 | ) | $ | (718 | ) | $ | (61 | ) | $ | 11 | $ | 2,117 | |||||||||||

Share-based compensation costs for equity-classified awards | — | 8 | — | — | — | — | 8 | |||||||||||||||||||||

Net (loss) income | — | — | (37 | ) | — | — | 1 | (36 | ) | |||||||||||||||||||

Purchases of treasury stock (3.2 shares) (Note 11) | — | — | — | — | (37 | ) | — | (37 | ) | |||||||||||||||||||

Other comprehensive income, net of tax | — | — | — | 21 | — | — | 21 | |||||||||||||||||||||

Balance as of June 30, 2015 | $ | — | $ | 3,762 | $ | (906 | ) | $ | (697 | ) | $ | (98 | ) | $ | 12 | $ | 2,073 | |||||||||||

Six Months Ended June 30, 2014 | ||||||||||||||||||||||||||||

Resolute Forest Products Inc. Shareholders’ Equity | ||||||||||||||||||||||||||||

Common Stock | Additional Paid-In Capital | Deficit | Accumulated Other Comprehensive Loss | Treasury Stock | Non- controlling Interests | Total Equity | ||||||||||||||||||||||

Balance as of December 31, 2013 | $ | — | $ | 3,751 | $ | (592 | ) | $ | (271 | ) | $ | (61 | ) | $ | 12 | $ | 2,839 | |||||||||||

Share-based compensation costs for equity-classified awards | — | 2 | — | — | — | — | 2 | |||||||||||||||||||||

Net (loss) income | — | — | (52 | ) | — | — | 2 | (50 | ) | |||||||||||||||||||

Stock options exercised and stock unit awards vested (0.1 shares), net of shares forfeited for employee withholding taxes | — | — | — | — | — | — | — | |||||||||||||||||||||

Other comprehensive income, net of tax | — | — | — | 51 | — | — | 51 | |||||||||||||||||||||

Balance as of June 30, 2014 | $ | — | $ | 3,753 | $ | (644 | ) | $ | (220 | ) | $ | (61 | ) | $ | 14 | $ | 2,842 | |||||||||||

See accompanying notes to unaudited interim consolidated financial statements.

4

RESOLUTE FOREST PRODUCTS INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited, in millions)

Six Months Ended June 30, | ||||||||

2015 | 2014 | |||||||

Cash flows from operating activities: | ||||||||

Net loss including noncontrolling interests | $ | (36 | ) | $ | (50 | ) | ||

Adjustments to reconcile net loss including noncontrolling interests to net cash provided by operating activities: | ||||||||

Share-based compensation | 8 | 2 | ||||||

Depreciation and amortization | 117 | 124 | ||||||

Closure costs, impairment and other related charges | — | 54 | ||||||

Inventory write-downs related to closures | 1 | 4 | ||||||

Deferred income taxes | 23 | (8 | ) | |||||

Net pension contributions and other postretirement benefit payments | (27 | ) | (74 | ) | ||||

Net gain on disposition of assets | — | (2 | ) | |||||

Loss on translation of foreign currency denominated deferred income taxes | 89 | 6 | ||||||

Gain on translation of foreign currency denominated pension and other postretirement benefit obligations | (84 | ) | (6 | ) | ||||

Net planned major maintenance payments | (15 | ) | (6 | ) | ||||

Changes in working capital: | ||||||||

Accounts receivable | 53 | 36 | ||||||

Inventories | 3 | (55 | ) | |||||

Other current assets | (6 | ) | (9 | ) | ||||

Accounts payable and accrued liabilities | (41 | ) | 5 | |||||

Other, net | 5 | 1 | ||||||

Net cash provided by operating activities | 90 | 22 | ||||||

Cash flows from investing activities: | ||||||||

Cash invested in fixed assets | (79 | ) | (82 | ) | ||||

Disposition of assets | — | 2 | ||||||

Decrease in restricted cash | — | 1 | ||||||

Increase in deposit requirements for letters of credit, net | (4 | ) | (1 | ) | ||||

Net cash used in investing activities | (83 | ) | (80 | ) | ||||

Cash flows from financing activities: | ||||||||

Payments of debt | — | (1 | ) | |||||

Payments of financing and credit facility fees | (3 | ) | (1 | ) | ||||

Purchases of treasury stock | (37 | ) | — | |||||

Net cash used in financing activities | (40 | ) | (2 | ) | ||||

Effect of exchange rate changes on cash and cash equivalents | (1 | ) | 1 | |||||

Net decrease in cash and cash equivalents | (34 | ) | (59 | ) | ||||

Cash and cash equivalents: | ||||||||

Beginning of period | 337 | 322 | ||||||

End of period | $ | 303 | $ | 263 | ||||

See accompanying notes to unaudited interim consolidated financial statements.

5

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

Note 1. Organization and Basis of Presentation

Nature of operations

Resolute Forest Products Inc. (with its subsidiaries and affiliates, either individually or collectively, unless otherwise indicated, referred to as “Resolute Forest Products,” “we,” “our,” “us,” “Parent” or the “Company”) is incorporated in Delaware. We are a global leader in the forest products industry, with a diverse range of products, including newsprint, specialty papers, market pulp and wood products, which are marketed in close to 80 countries. We own or operate some 40 pulp and paper mills and wood products facilities in the United States, Canada and South Korea, and power generation assets in Canada.

Financial statements

Our interim consolidated financial statements are unaudited and have been prepared in accordance with the requirements of the United States Securities and Exchange Commission (the “SEC”) for interim reporting. Under those rules, certain footnotes and other financial information that are normally required by United States generally accepted accounting principles may be condensed or omitted. In our opinion, all adjustments (consisting of normal recurring adjustments) necessary for the fair statement of the unaudited interim consolidated financial statements have been made. All amounts are expressed in U.S. dollars, unless otherwise indicated. The results for the interim period ended June 30, 2015, are not necessarily indicative of the results to be expected for the full year. These unaudited interim consolidated financial statements should be read in conjunction with our Annual Report on Form 10-K for the year ended December 31, 2014, filed with the SEC on March 2, 2015.

New accounting pronouncements

In February 2015, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2015-02, “Amendments to the Consolidation Analysis,” which affects the variable interest entity and voting entity consolidation models for all companies. This update is effective for financial statements issued for fiscal years beginning after December 15, 2015. We are evaluating the impact of this update on our results of operations or financial position.

In April 2015, the FASB issued ASU 2015-03, “Simplifying the Presentation of Debt Issuance Costs,” which requires debt issuance costs to be presented in the balance sheet as a direct deduction from the carrying value of the associated debt liability, consistent with the presentation of a debt discount. This update is effective for financial statements issued for fiscal years beginning after December 15, 2015. The adoption of this accounting guidance will not materially impact our financial position.

In April 2015, the FASB issued ASU 2015-05, “Customer’s Accounting for Fees Paid in a Cloud Computing Arrangement,” which provides guidance to customers about whether a cloud computing arrangement includes a software license. If a cloud computing arrangement includes a software license, then the customer should account for the software license element of the arrangement consistent with the acquisition of other software licenses. If a cloud computing arrangement does not include a software license, the customer should account for the arrangement as a service contract. This update is effective for financial statements issued for fiscal years beginning after December 15, 2015, with early adoption permitted as of the beginning of an interim or annual reporting period. The adoption of this accounting guidance will not materially impact our financial position.

In July 2015, the FASB approved a one-year deferral of ASU 2014-09, “Revenue from Contracts with Customers,” deferring the effective date to fiscal years beginning after December 15, 2017. Early adoption is permitted for financial statements issued for fiscal years beginning after December 15, 2016. We are evaluating the impact of this update on our results of operations or financial position.

In July 2015, the FASB issued ASU 2015-11, “Simplifying the Measurement of Inventory,” which requires that inventory within the scope of this update, including inventory stated at average cost, be measured at the lower of cost and net realizable value. This update is effective for financial statements issued for fiscal years beginning after December 15, 2016, with early adoption permitted as of the beginning of an interim or annual reporting period. We are evaluating the impact of this update on our results of operations or financial position.

6

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

Note 2. Closure Costs, Impairment and Other Related Charges

Closure costs, impairment and other related charges for the three and six months ended June 30, 2015, were comprised of the following:

(Unaudited, in millions) | Accelerated Depreciation | Severance and Other Costs | Total | |||||||||

Permanent closures: | ||||||||||||

Paper mill in Iroquois Falls, Ontario | ||||||||||||

Second quarter | $ | — | $ | 1 | $ | 1 | ||||||

First six months | — | 5 | 5 | |||||||||

Paper machine in Clermont, Québec | ||||||||||||

Second quarter | — | — | — | |||||||||

First six months | 2 | — | 2 | |||||||||

Other | ||||||||||||

Second quarter | — | (1 | ) | (1 | ) | |||||||

First six months | — | (1 | ) | (1 | ) | |||||||

Total | ||||||||||||

Second quarter | $ | — | $ | — | $ | — | ||||||

First six months | 2 | 4 | 6 | |||||||||

Closure costs, impairment and other related charges for the three and six months ended June 30, 2014, were comprised of the following:

(Unaudited, in millions) | Impairment of Assets | Accelerated Depreciation | Severance and Other Costs | Total | ||||||||||||

Permanent closures: | ||||||||||||||||

Paper machine in Catawba, South Carolina | ||||||||||||||||

Second quarter | $ | — | $ | 45 | $ | — | $ | 45 | ||||||||

First six months | — | 45 | 1 | 46 | ||||||||||||

Pulp and paper mill in Fort Frances, Ontario | ||||||||||||||||

Second quarter | — | — | 2 | 2 | ||||||||||||

First six months | — | — | 8 | 8 | ||||||||||||

Paper machine in Iroquois Falls | ||||||||||||||||

Second quarter | — | — | — | — | ||||||||||||

First six months | — | 3 | — | 3 | ||||||||||||

Other | — | |||||||||||||||

Second quarter | 5 | — | — | 5 | ||||||||||||

First six months | 6 | — | (1 | ) | 5 | |||||||||||

Total | ||||||||||||||||

Second quarter | $ | 5 | $ | 45 | $ | 2 | $ | 52 | ||||||||

First six months | 6 | 48 | 8 | 62 | ||||||||||||

7

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

Note 3. Other Income, Net

Other income, net for the three and six months ended June 30, 2015 and 2014, was comprised of the following:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||

(Unaudited, in millions) | 2015 | 2014 | 2015 | 2014 | |||||||||||||

Foreign exchange gain | $ | 1 | $ | 17 | $ | 3 | $ | 3 | |||||||||

Miscellaneous income | — | 3 | 3 | 4 | |||||||||||||

$ | 1 | $ | 20 | $ | 6 | $ | 7 | ||||||||||

Note 4. Accumulated Other Comprehensive Loss

The change in our accumulated other comprehensive loss by component (net of tax) for the six months ended June 30, 2015, was as follows:

(Unaudited, in millions) | Unamortized Prior Service Credits | Unamortized Actuarial Losses | Foreign Currency Translation | Total | ||||||||||||

Balance as of December 31, 2014 | $ | 94 | $ | (812 | ) | $ | — | $ | (718 | ) | ||||||

Other comprehensive loss before reclassifications | — | — | (2 | ) | (2 | ) | ||||||||||

Amounts reclassified from accumulated other comprehensive loss (1) | (8 | ) | 31 | — | 23 | |||||||||||

Net current period other comprehensive (loss) income | (8 | ) | 31 | (2 | ) | 21 | ||||||||||

Balance as of June 30, 2015 | $ | 86 | $ | (781 | ) | $ | (2 | ) | $ | (697 | ) | |||||

(1) | See the table below for details about these reclassifications. |

The reclassifications out of accumulated other comprehensive loss for the six months ended June 30, 2015, were comprised of the following:

(Unaudited, in millions) | Amounts Reclassified From Accumulated Other Comprehensive Loss | Affected Line in the Consolidated Statements of Operations | |||

Unamortized Prior Service Credits | |||||

Amortization of prior service credits | $ | (8 | ) | Cost of sales, excluding depreciation, amortization and distribution costs (1) | |

— | Income tax (provision) benefit | ||||

$ | (8 | ) | Net of tax | ||

Unamortized Actuarial Losses | |||||

Amortization of actuarial losses | $ | 40 | Cost of sales, excluding depreciation, amortization and distribution costs (1) | ||

(9 | ) | Income tax (provision) benefit | |||

$ | 31 | Net of tax | |||

Total Reclassifications | $ | 23 | Net of tax | ||

(1) | These items are included in the computation of net periodic benefit cost related to our pension and other postretirement benefit (“OPEB”) plans summarized in Note 8, “Employee Benefit Plans.” |

8

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

Note 5. Net Loss Per Share

The weighted-average number of stock options and equity-classified restricted stock units, deferred stock units and performance stock units (collectively, “stock unit awards”) outstanding for the three and six months ended June 30, 2015 and 2014, was as follows:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||

(Unaudited, in millions) | 2015 | 2014 | 2015 | 2014 | |||||||||

Stock options | 1.5 | 1.8 | 1.6 | 1.8 | |||||||||

Stock unit awards | 1.2 | 1.0 | 1.2 | 1.0 | |||||||||

These stock options and stock unit awards were excluded from the calculation of diluted net loss per share as the impact would have been antidilutive for all periods presented.

Note 6. Inventories, Net

Inventories, net as of June 30, 2015 and December 31, 2014, were comprised of the following:

(Unaudited, in millions) | June 30, 2015 | December 31, 2014 | ||||||

Raw materials and work in process | $ | 144 | $ | 160 | ||||

Finished goods | 195 | 192 | ||||||

Mill stores and other supplies | 198 | 190 | ||||||

$ | 537 | $ | 542 | |||||

Note 7. Long-Term Debt

Overview

Long-term debt, including current portion, as of June 30, 2015 and December 31, 2014, was comprised of the following:

(Unaudited, in millions) | June 30, 2015 | December 31, 2014 | ||||||

5.875% senior notes due 2023: | ||||||||

Principal amount | $ | 600 | $ | 600 | ||||

Unamortized discount | (5 | ) | (5 | ) | ||||

Total senior notes due 2023 | 595 | 595 | ||||||

Capital lease obligation | 2 | 2 | ||||||

Total debt | 597 | 597 | ||||||

Less: Current portion of long-term debt | (1 | ) | (1 | ) | ||||

Long-term debt, net of current portion | $ | 596 | $ | 596 | ||||

5.875% senior notes due 2023

We issued $600 million in aggregate principal amount of 5.875% senior notes due 2023 (the “2023 Notes”) on May 8, 2013. Interest on the notes is payable semi-annually on May 15 and November 15, until their maturity date of May 15, 2023. The fair value of the 2023 Notes was $536 million and $571 million as of June 30, 2015 and December 31, 2014, respectively, and was determined by reference to over-the-counter prices (Level 1).

ABL Credit Facility

On May 22, 2015, we entered into a new five-year credit agreement for a senior secured asset-based revolving credit facility (the “ABL Credit Facility”), with an aggregate lender commitment of up to $600 million at any time outstanding, subject to borrowing base availability based on specified advance rates, eligibility criteria and customary reserves. This facility replaces our previous $665 million senior secured asset-based revolving credit facility, originally dated as of December 9, 2010. The ABL Credit Facility will mature on May 22, 2020.

9

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

The aggregate lender commitment under the facility includes a $60 million swingline sub-facility and a $200 million letter of credit sub-facility, and we may convert up to $50 million of the commitments under the facility to a first-in last-out facility (“FILO Facility”), subject to the consent of each converting lender. The ABL Credit Facility also provides for an uncommitted ability to increase the revolving credit facility by up to $500 million, subject to certain terms and conditions set forth in the agreement.

Revolving loan (and letter of credit) availability under the credit agreement is subject to a borrowing base, which at any time is equal to the sum of (i) 85% of eligible accounts receivable (or 90% with respect to certain insured or letter of credit backed accounts or with accounts owed by investment grade obligors), plus (ii) the lesser of (A) 70% of the lesser of the cost or market value of eligible inventory or (B) 85% of the net orderly liquidation value of eligible inventory, plus (iii) 100% of the value of eligible cash and 95% of the value of permitted investments held in deposit accounts controlled solely by the administrative and collateral agent (the “agent”). The FILO Facility will be subject to a borrowing base, which at any time will be equal to (i) 5% of the eligible accounts receivable, plus (ii) 10% of the appraised net orderly value of the eligible inventory (subject to reduction to 5% over the term of the facility). Each borrowing base described above is subject to customary reserves and eligibility criteria, in the exercise of the agent’s reasonable discretion.

The obligations under the credit agreement are guaranteed by certain material subsidiaries of the Company and are secured by first priority liens on and security interests in accounts receivable, inventory and related assets.

Borrowings under the credit agreement bear interest at a rate equal to the base rate, the London Interbank Offered Rate (“LIBOR”), or the Canadian banker’s acceptance (“BA”) rate, in each case plus an applicable margin. The applicable margin is between 0.00% and 0.75% with respect to base rate borrowings and between 1.00% and 1.75% with respect to LIBOR and Canadian BA borrowings, in each case based on availability under the credit facility and a leverage ratio.

Loans outstanding under the FILO Facility bear interest at a rate that is 1.25% per annum higher than the interest rate payable on revolving loans not made under the FILO Facility.

In addition to paying interest on outstanding principal under the credit agreement, we are required to pay fees of up to 0.30% in respect of unutilized commitments, as well as a fee in respect of outstanding letters of credit (equal to the applicable margin in respect of LIBOR and Canadian BA borrowings plus a fronting fee of 0.125% and certain administrative fees).

The Company is able to voluntarily repay outstanding loans and reduce unused commitments, in each case, in whole or in part, at any time without premium or penalty. However, no loans under the FILO Facility can be repaid unless all other loans under the credit agreement are repaid first. We are required to repay outstanding loans that exceed the maximum availability then in effect.

The credit agreement contains customary covenants for asset-based credit agreements of this type, including, among other things: (i) requirements to deliver financial statements, other reports and notices; (ii) restrictions on the existence or incurrence and repayment of indebtedness by the Company and its subsidiaries; (iii) restrictions on the existence or incurrence of liens by the Company and its subsidiaries; (iv) restrictions on the Company and certain of its subsidiaries making certain restricted payments; (v) restrictions on the Company and certain of its subsidiaries making certain investments; (vi) restrictions on certain mergers, consolidations and asset dispositions; (vii) restrictions on transactions with affiliates; (viii) restrictions on amendments or modifications to the Canadian pension and benefit plans; (ix) restrictions on modifications to material indebtedness; and (x) a springing requirement for the Company to maintain a minimum consolidated fixed charge coverage ratio, as determined under the credit agreement, of 1.0:1.0, anytime availability under the facility falls below the greater of $50 million or 10% of the maximum available borrowing amount for two consecutive business days. Subject to customary grace periods and notice requirements, the credit agreement also contains certain customary events of default.

As of June 30, 2015, we had no borrowings and $36 million of letters of credit outstanding under the ABL Credit Facility. As of June 30, 2015, we had $468 million of availability under the ABL Credit Facility.

Capital lease obligation

We have a capital lease obligation for a warehouse, which can be renewed for 20 years at our option. Minimum payments are determined by an escalatory price clause.

10

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

Note 8. Employee Benefit Plans

Pension and OPEB plans

The components of net periodic benefit cost relating to our pension and OPEB plans for the three and six months ended June 30, 2015 and 2014, were as follows:

Pension Plans:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||

(Unaudited, in millions) | 2015 | 2014 | 2015 | 2014 | |||||||||||||

Service cost | $ | 6 | $ | 7 | $ | 12 | $ | 14 | |||||||||

Interest cost | 58 | 69 | 116 | 138 | |||||||||||||

Expected return on plan assets | (67 | ) | (76 | ) | (134 | ) | (151 | ) | |||||||||

Amortization of actuarial losses | 20 | 2 | 42 | 3 | |||||||||||||

Amortization of prior service credits | — | (1 | ) | (1 | ) | (1 | ) | ||||||||||

$ | 17 | $ | 1 | $ | 35 | $ | 3 | ||||||||||

OPEB Plans:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||

(Unaudited, in millions) | 2015 | 2014 | 2015 | 2014 | |||||||||||||

Service cost | $ | — | $ | — | $ | — | $ | 1 | |||||||||

Interest cost | 2 | 3 | 4 | 6 | |||||||||||||

Amortization of actuarial gains | (1 | ) | (1 | ) | (2 | ) | (2 | ) | |||||||||

Amortization of prior service credits | (3 | ) | (2 | ) | (7 | ) | (4 | ) | |||||||||

$ | (2 | ) | $ | — | $ | (5 | ) | $ | 1 | ||||||||

Defined contribution plans

Our expense for the defined contribution plans totaled $4 million and $5 million for the three months ended June 30, 2015 and 2014, respectively, and $10 million and $11 million for the six months ended June 30, 2015 and 2014, respectively.

11

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

Note 9. Income Taxes

The income tax (provision) benefit attributable to income (loss) before income taxes differs from the amounts computed by applying the United States federal statutory income tax rate of 35% for the three and six months ended June 30, 2015 and 2014, as a result of the following:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||

(Unaudited, in millions) | 2015 | 2014 | 2015 | 2014 | |||||||||||||

Income (loss) before income taxes | $ | 6 | $ | 1 | $ | (16 | ) | $ | (57 | ) | |||||||

Income tax (provision) benefit: | |||||||||||||||||

Expected income tax (provision) benefit | (2 | ) | — | 6 | 20 | ||||||||||||

Changes resulting from: | |||||||||||||||||

Valuation allowance (1) | (8 | ) | (12 | ) | (27 | ) | (20 | ) | |||||||||

Foreign exchange | (2 | ) | 4 | (7 | ) | (2 | ) | ||||||||||

State income taxes and foreign tax rate differences | 2 | 9 | 5 | 11 | |||||||||||||

Other, net | — | (2 | ) | 3 | (2 | ) | |||||||||||

$ | (10 | ) | $ | (1 | ) | $ | (20 | ) | $ | 7 | |||||||

(1) | We recorded a net increase in our valuation allowance of $8 million and $12 million for the three months ended June 30, 2015 and 2014, respectively, and $27 million and $20 million for the six months ended June 30, 2015 and 2014, respectively, primarily related to our U.S. operations where we recognize a full valuation allowance against our net deferred income tax assets. |

Note 10. Commitments and Contingencies

Legal matters

We become involved in various legal proceedings and other disputes in the normal course of business, including matters related to contracts, commercial disputes, taxes, environmental issues, activists damages, employment and workers’ compensation claims, Aboriginal claims and other matters. Although the final outcome is subject to many variables and cannot be predicted with any degree of certainty, we regularly assess the status of the matters and establish provisions (including legal costs expected to be incurred) when we believe an adverse outcome is probable, and the amount can be reasonably estimated. Except as described below and for claims that cannot be assessed due to their preliminary nature, we believe that the ultimate disposition of these matters outstanding or pending as of June 30, 2015, will not have a material adverse effect on our consolidated financial statements.

Effective July 31, 2012, we completed the final step of the transaction pursuant to which we acquired the remaining 25.4% of the outstanding Fibrek Inc. (“Fibrek”) shares, following the approval of Fibrek’s shareholders on July 23, 2012, and the issuance of a final order of the Québec Superior Court in Canada approving the arrangement on July 27, 2012. Certain former shareholders of Fibrek exercised (or purported to exercise) rights of dissent in respect of the transaction, asking for a judicial determination of the fair value of their claim under the Canada Business Corporations Act. No consideration has to date been paid to the former Fibrek shareholders who exercised (or purported to exercise) rights of dissent. Any such consideration will only be paid out upon settlement or judicial determination of the fair value of their claims and will be paid entirely in cash. Accordingly, we cannot presently determine the amount that ultimately will be paid to former holders of Fibrek shares in connection with the proceedings, but we have accrued approximately Cdn $14 million ($11 million, based on the exchange rate in effect on June 30, 2015) for the eventual payment of those claims.

On June 12, 2012, we filed a motion for directives with the Québec Superior Court in Canada, the court with jurisdiction in the creditor protection proceedings under the Companies’ Creditors Arrangement Act (Canada), from which our predecessor entity and all but one of its affiliates emerged in 2010, seeking an order to prevent pension regulators in each of Québec, New Brunswick, and Newfoundland and Labrador from declaring partial wind-ups of pension plans relating to employees of former operations in New Brunswick, and Newfoundland and Labrador, or a declaration that any claim for accelerated reimbursements of deficits arising from a partial wind-up is a barred claim under the creditor protection proceedings. These plans are subject to the funding relief regulations described in Note 14, “Pension and Other Postretirement Benefit Plans - Canadian pension funding,” to our consolidated financial statements for the year ended December 31, 2014 and we contend, among other things, that any such declaration, if issued, would be inconsistent with the Québec Superior Court in Canada’s sanction order

12

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

confirming the plan of reorganization and the terms of our emergence from the creditor protection proceedings. A partial wind-up would likely shorten the period in which any deficit within those plans, which could reach up to Cdn $150 million ($120 million based on the exchange rate in effect on June 30, 2015), would have to be funded if we do not obtain the relief sought. No hearing date has been set to date.

Environmental matters

We are subject to a variety of federal, state, provincial and local environmental laws and regulations in the jurisdictions in which we operate. We believe our operations are in material compliance with current applicable environmental laws and regulations. Environmental regulations promulgated in the future could require substantial additional expenditures for compliance and could have a material impact on us, in particular, and the industry in general.

We may be a “potentially responsible party” with respect to four hazardous waste sites that are being addressed pursuant to the Comprehensive Environmental Response, Compensation and Liability Act of 1980 (commonly known as Superfund) or the Resource Conservation and Recovery Act corrective action authority. We believe we will not be liable for any significant amounts at any of these sites.

We have recorded $14 million and $18 million of environmental liabilities as of June 30, 2015 and December 31, 2014, respectively, primarily related to environmental remediation related to closed sites. The amount of these liabilities represents management’s estimate of the ultimate settlement based on an assessment of relevant factors and assumptions and could be affected by changes in facts or assumptions not currently known to management for which the outcome cannot be reasonably estimated at this time. These liabilities are included in “Accounts payable and accrued liabilities” or “Other liabilities” in our Consolidated Balance Sheets.

We have also recorded $24 million and $22 million of asset retirement obligations as of June 30, 2015 and December 31, 2014, respectively, primarily consisting of liabilities associated with landfills, sludge basins and the dismantling of retired assets. These liabilities are included in “Accounts payable and accrued liabilities” or “Other liabilities” in our Consolidated Balance Sheets.

Other matters

On October 30, 2014, we received a notice from the Ministry of Natural Resources and Forestry of Ontario (the “MNRF”) directing us to repay a conditional incentive of Cdn $23 million ($18 million based on the exchange rate in effect on June 30, 2015) offered in 2007 toward the construction of an electricity-producing turbine, should we fail to restart our Fort Frances pulp and paper mill or otherwise implement an alternative remedy that is acceptable to the MNRF. Several extensions to implement an alternative remedy have been granted to us by the MNRF, with the latest remedy date being October 31, 2015. We announced the permanent closure of the mill in the second quarter of 2014 and have been exploring a number of opportunities for the mill. We are not presently able to determine the outcome of this process, but we currently believe that we could reach an acceptable outcome for the MNRF within the time limit prescribed. Accordingly, we have recorded no contingent liability in respect of this notice in our Consolidated Balance Sheet as of June 30, 2015.

Note 11. Share Capital

On May 28, 2015, our board of directors authorized a $50 million increase to our existing $100 million share repurchase program, which was launched in May of 2012. As of December 31, 2014, we had repurchased 5.6 million shares, at a cost of $67 million. During the three and six months ended June 30, 2015, we repurchased 3.2 million shares, at a cost of $37 million. There remains $46 million under the program.

13

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

Note 12. Segment Information

We manage our business based on the products we manufacture. Accordingly, our reportable segments correspond to our principal product lines: newsprint, specialty papers, market pulp and wood products.

None of the income or loss items following “Operating income (loss)” in our Consolidated Statements of Operations are allocated to our segments, since those items are reviewed separately by management. For the same reason, closure costs, impairment and other related charges, inventory write-downs related to closures, start-up costs, net gain on disposition of assets, certain components of pension and OPEB costs and credits as well as other discretionary charges or credits are not allocated to our segments. We allocate depreciation and amortization expense to our segments, although the related fixed assets and amortizable intangible assets are not allocated to segment assets. Additionally, all selling, general and administrative expenses, excluding certain discretionary charges and credits, are allocated to our segments.

In the second quarter of 2015, we changed our presentation of segment operating income to reallocate certain components of pension and OPEB costs, which consist of interest cost, expected return on plan assets and amortization of actuarial losses and gains, from the reportable segments to “corporate and other” in the segment presentation of operating income. Current service costs and amortization of prior service credits will continue to be allocated to the reportable segments. This approach is consistent with the indicators management uses internally to evaluate performance, including those used by the chief operating decision maker. Prior period amounts have been reclassified to conform to the 2015 presentation.

Information about certain segment data for the three and six months ended June 30, 2015 and 2014, was as follows:

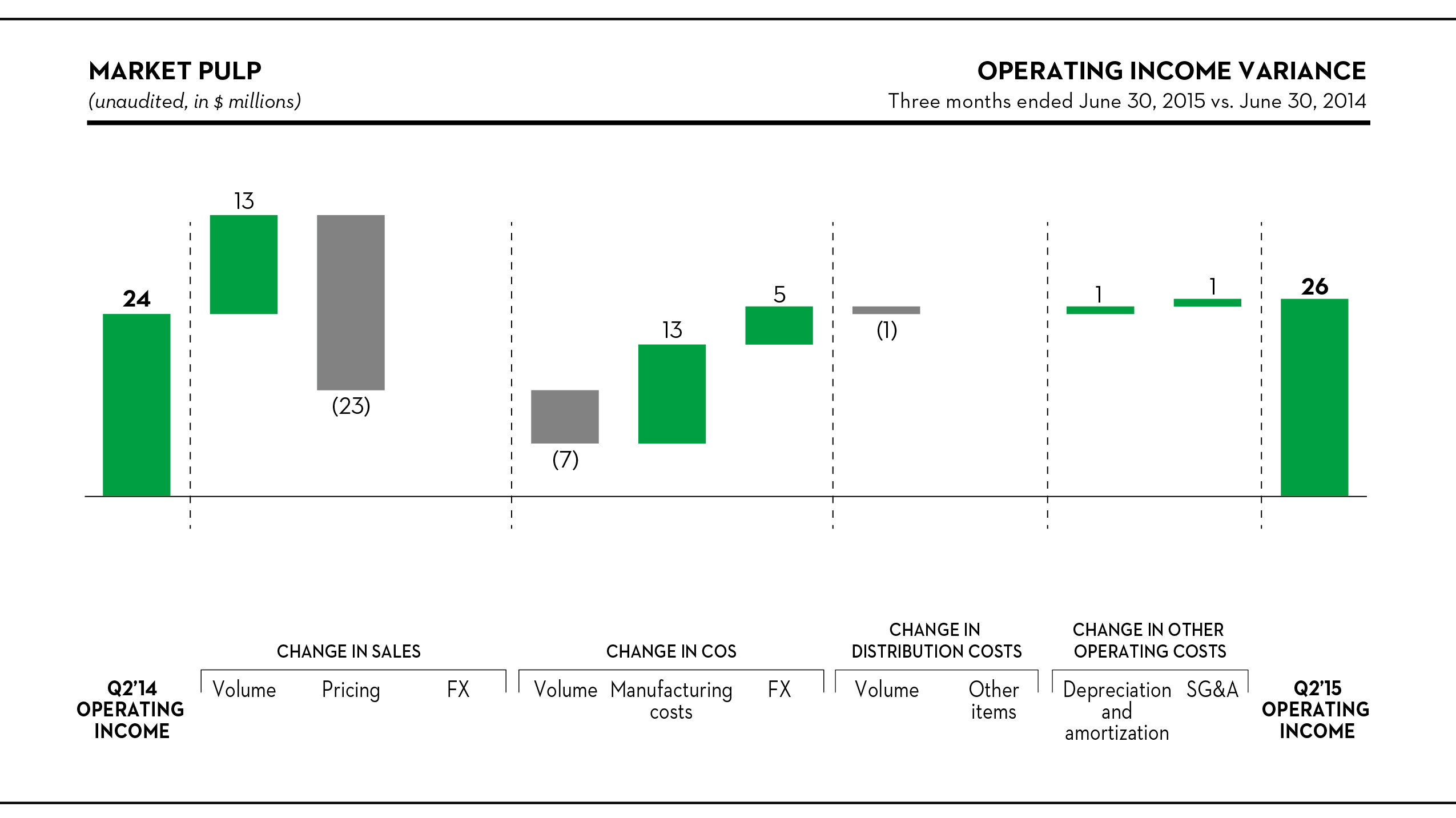

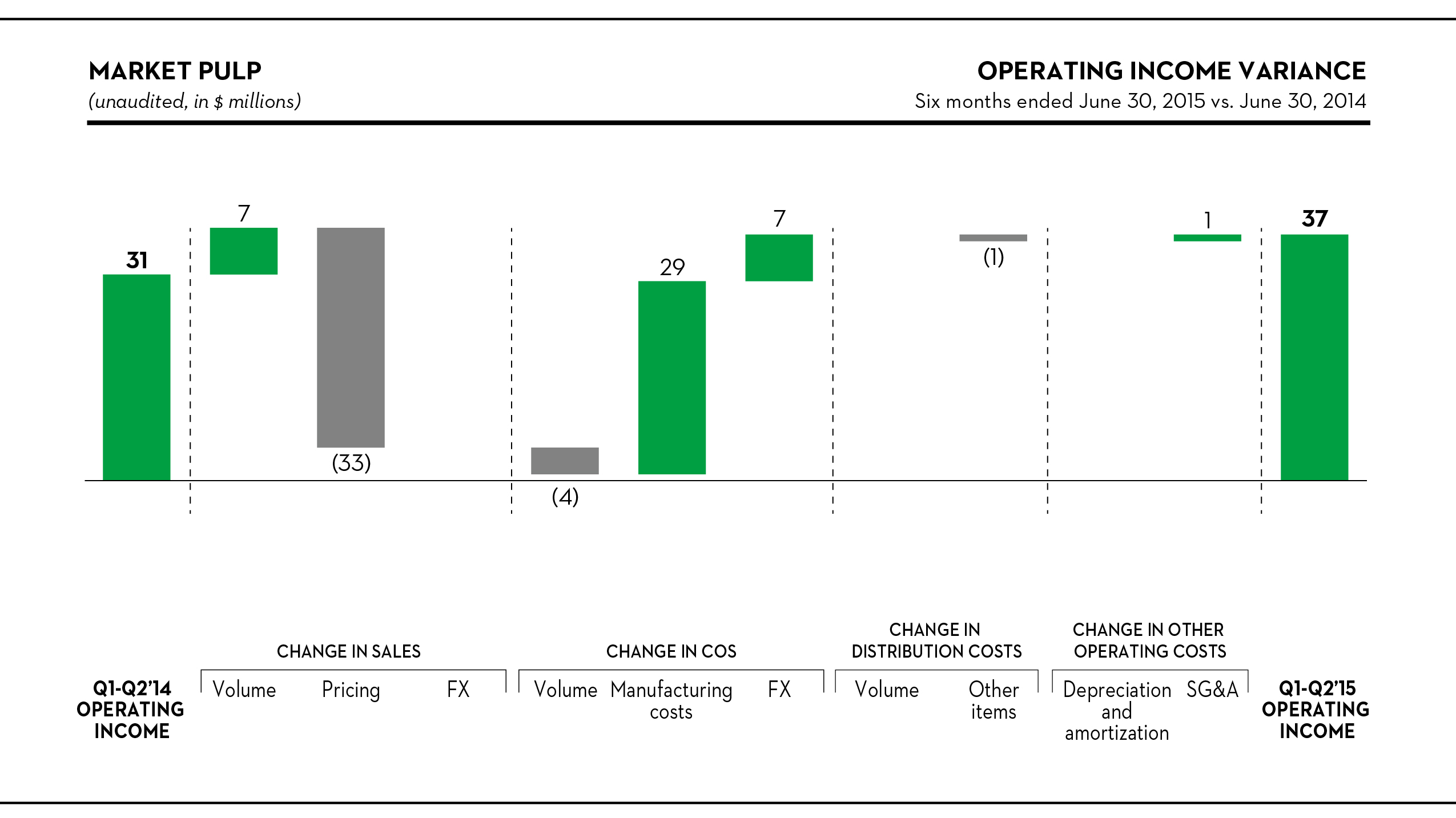

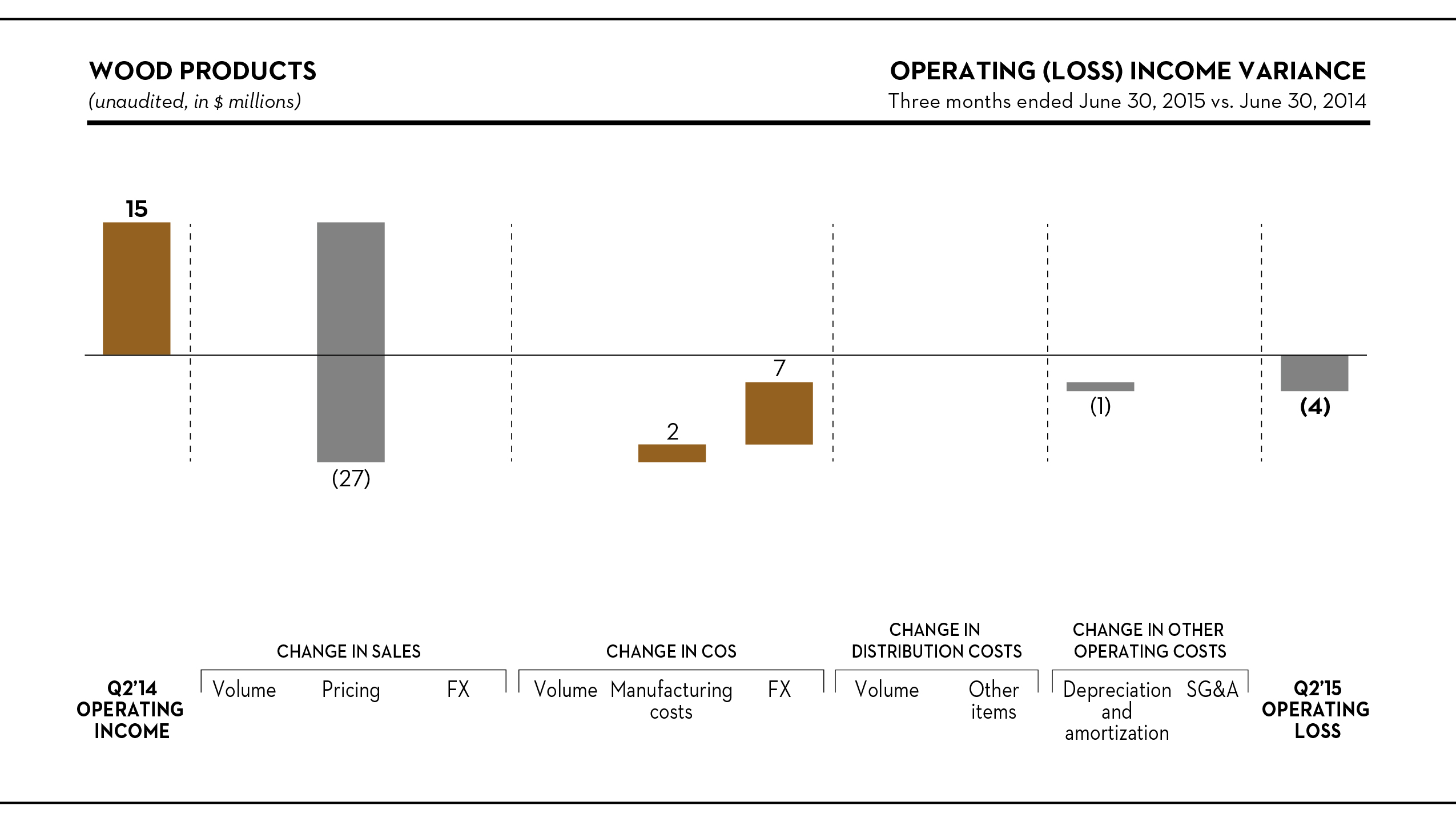

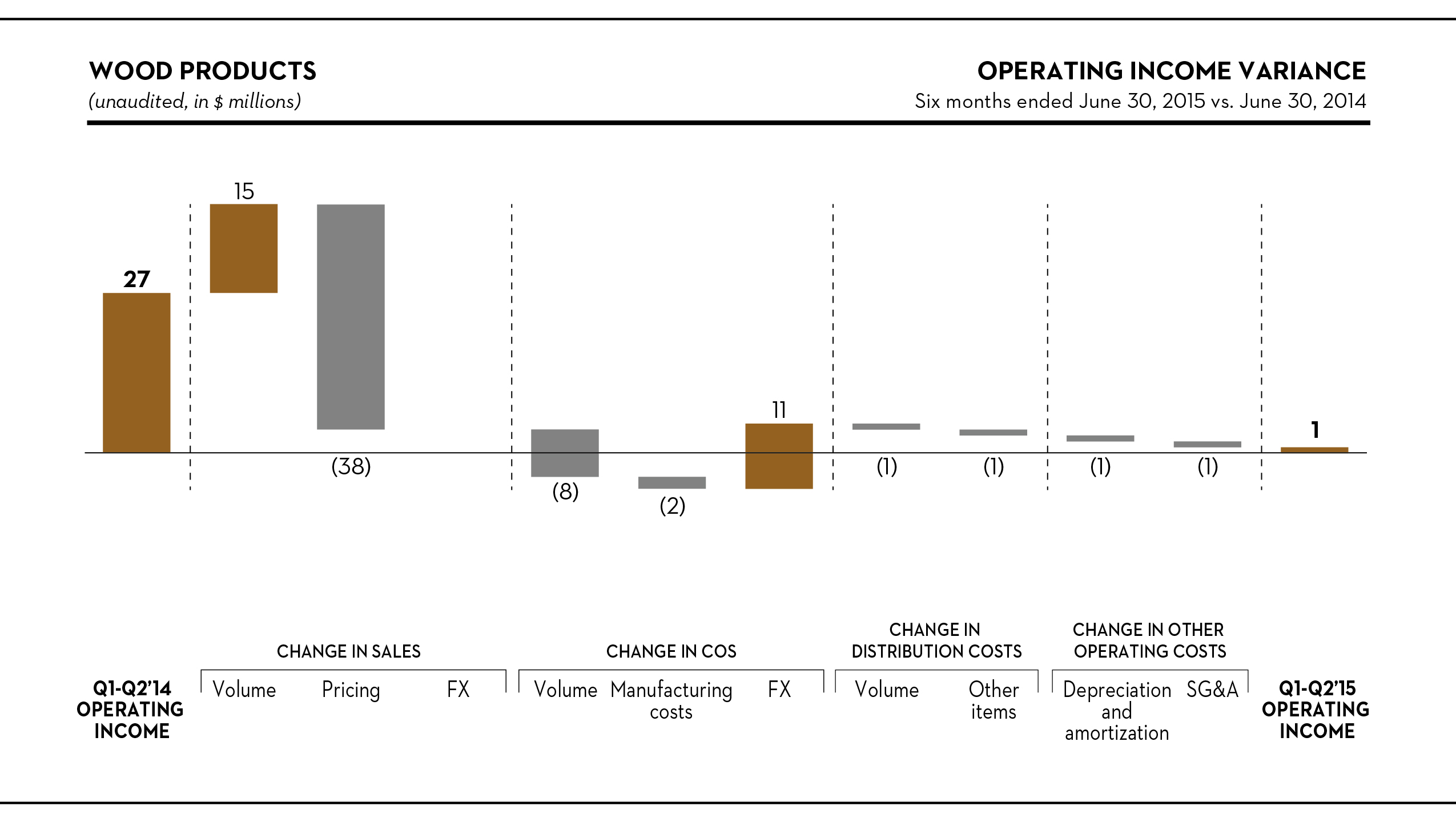

(Unaudited, in millions) | Newsprint | Specialty Papers | Market Pulp (1) | Wood Products | Segment Total | Corporate and Other | Total | |||||||||||||||||||||

Sales | ||||||||||||||||||||||||||||

Second quarter 2015 | $ | 289 | $ | 272 | $ | 231 | $ | 134 | $ | 926 | $ | — | $ | 926 | ||||||||||||||

Second quarter 2014 | 364 | 325 | 241 | 161 | 1,091 | — | 1,091 | |||||||||||||||||||||

First six months 2015 | 580 | 544 | 449 | 273 | 1,846 | — | 1,846 | |||||||||||||||||||||

First six months 2014 | 710 | 626 | 475 | 296 | 2,107 | — | 2,107 | |||||||||||||||||||||

Depreciation and amortization | ||||||||||||||||||||||||||||

Second quarter 2015 | $ | 16 | $ | 19 | $ | 12 | $ | 9 | $ | 56 | $ | 4 | $ | 60 | ||||||||||||||

Second quarter 2014 | 17 | 22 | 13 | 8 | 60 | 2 | 62 | |||||||||||||||||||||

First six months 2015 | 32 | 36 | 26 | 17 | 111 | 6 | 117 | |||||||||||||||||||||

First six months 2014 | 35 | 44 | 26 | 16 | 121 | 3 | 124 | |||||||||||||||||||||

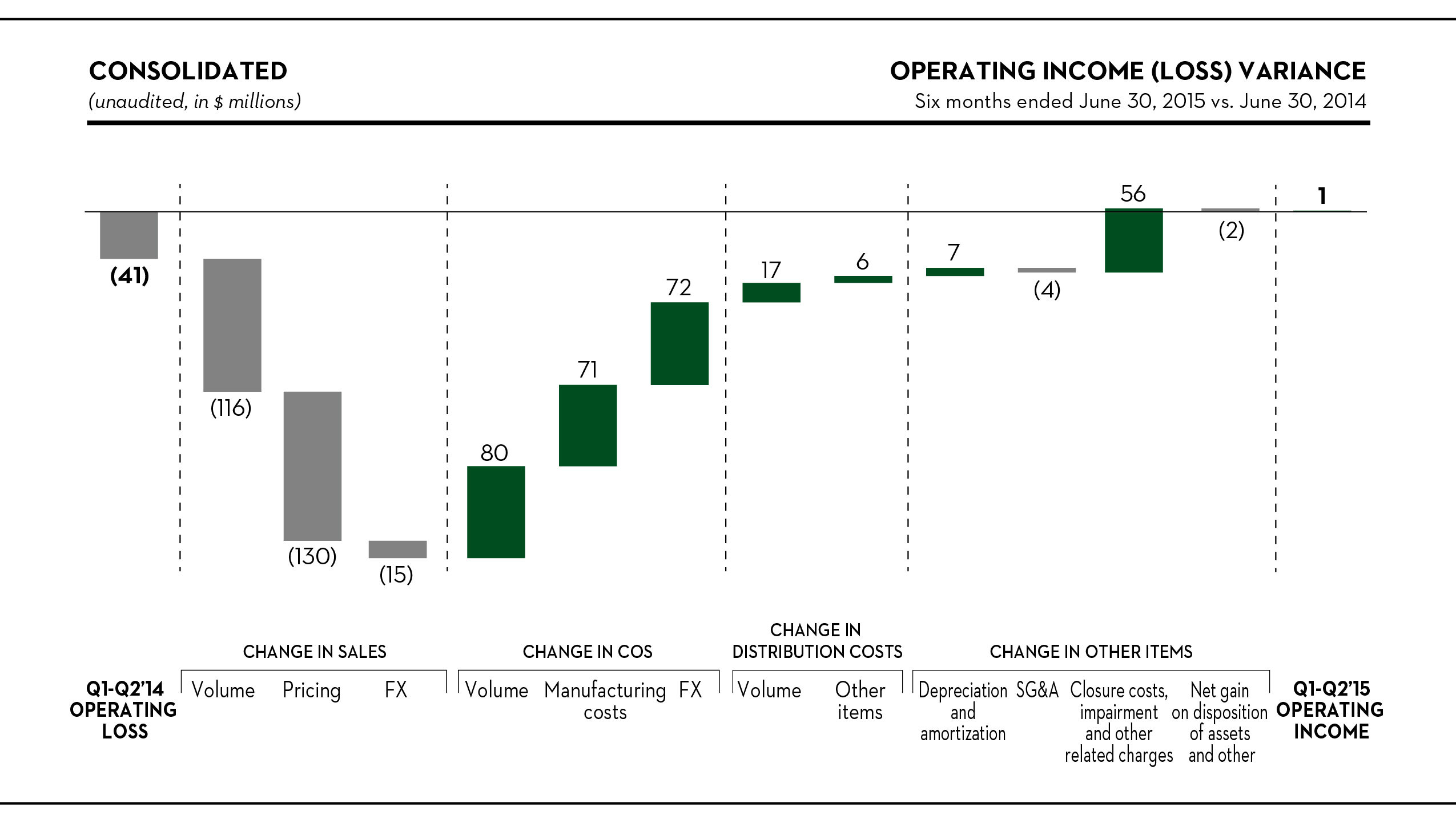

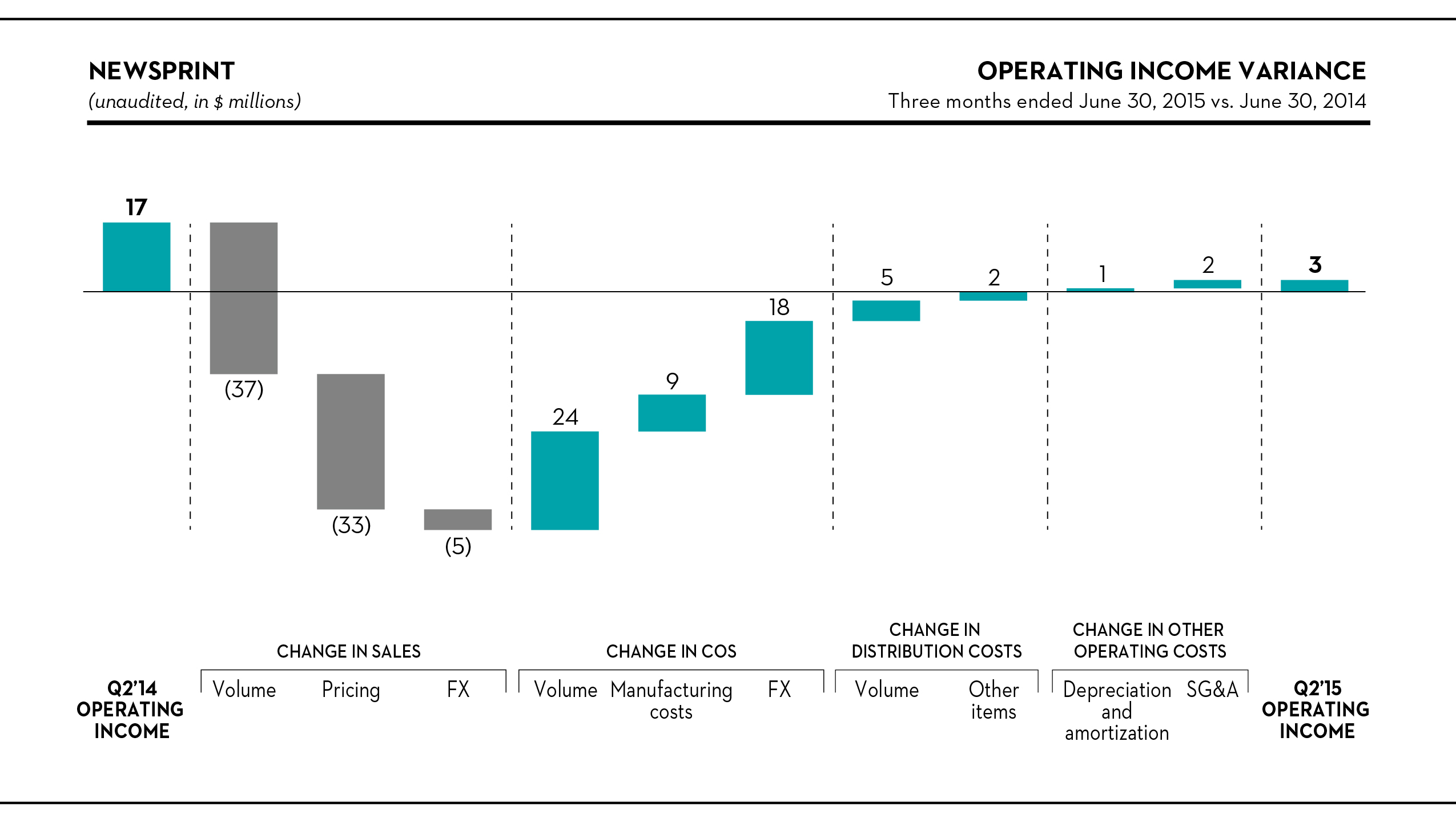

Operating income (loss) | ||||||||||||||||||||||||||||

Second quarter 2015 | $ | 3 | $ | 17 | $ | 26 | $ | (4 | ) | $ | 42 | $ | (26 | ) | $ | 16 | ||||||||||||

Second quarter 2014 | 17 | (4 | ) | 24 | 15 | 52 | (60 | ) | (8 | ) | ||||||||||||||||||

First six months 2015 | — | 22 | 37 | 1 | 60 | (59 | ) | 1 | ||||||||||||||||||||

First six months 2014 | 1 | (29 | ) | 31 | 27 | 30 | (71 | ) | (41 | ) | ||||||||||||||||||

(1) | Market pulp sales excluded inter-segment sales of $5 million and $7 million for the three months ended June 30, 2015 and 2014, respectively, and $8 million and $10 million for the six months ended June 30, 2015 and 2014, respectively. |

14

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

Note 13. Condensed Consolidating Financial Information

The following information is presented in accordance with Rule 3-10 of Regulation S-X and the public information requirements of Rule 144 promulgated pursuant to the Securities Act of 1933 in connection with Resolute Forest Products Inc.’s 2023 Notes that are fully and unconditionally guaranteed, on a joint and several basis, by all of our 100% owned material U.S. subsidiaries (the “Guarantor Subsidiaries”). The 2023 Notes are not guaranteed by our foreign subsidiaries and our less than 100% owned U.S. subsidiaries (the “Non-guarantor Subsidiaries”).

The following condensed consolidating financial information sets forth the Statements of Operations and Comprehensive Income (Loss) for the three and six months ended June 30, 2015 and 2014, the Balance Sheets as of June 30, 2015 and December 31, 2014, and the Statements of Cash Flows for the six months ended June 30, 2015 and 2014 for the Parent, the Guarantor Subsidiaries on a combined basis, and the Non-guarantor Subsidiaries on a combined basis. The condensed consolidating financial information reflects the investments of the Parent in the Guarantor Subsidiaries and Non-guarantor Subsidiaries, as well as the investments of the Guarantor Subsidiaries in the Non-guarantor Subsidiaries, using the equity method of accounting. The principal consolidating adjustments are elimination entries to eliminate the investments in subsidiaries and intercompany balances and transactions.

CONDENSED CONSOLIDATING STATEMENT OF OPERATIONS AND COMPREHENSIVE INCOME | ||||||||||||||||||||

For the Three Months Ended June 30, 2015 | ||||||||||||||||||||

(Unaudited, in millions) | Parent | Guarantor Subsidiaries | Non-guarantor Subsidiaries | Consolidating Adjustments | Consolidated | |||||||||||||||

Sales | $ | — | $ | 747 | $ | 559 | $ | (380 | ) | $ | 926 | |||||||||

Costs and expenses: | ||||||||||||||||||||

Cost of sales, excluding depreciation, amortization and distribution costs | — | 676 | 397 | (381 | ) | 692 | ||||||||||||||

Depreciation and amortization | — | 23 | 37 | — | 60 | |||||||||||||||

Distribution costs | — | 41 | 76 | 1 | 118 | |||||||||||||||

Selling, general and administrative expenses | 3 | 14 | 23 | — | 40 | |||||||||||||||

Operating (loss) income | (3 | ) | (7 | ) | 26 | — | 16 | |||||||||||||

Interest expense | (18 | ) | (1 | ) | (2 | ) | 10 | (11 | ) | |||||||||||

Other income, net | — | 9 | 2 | (10 | ) | 1 | ||||||||||||||

Parent’s equity in income of subsidiaries | 17 | — | — | (17 | ) | — | ||||||||||||||

(Loss) income before income taxes | (4 | ) | 1 | 26 | (17 | ) | 6 | |||||||||||||

Income tax provision | — | — | (10 | ) | — | (10 | ) | |||||||||||||

Net (loss) income including noncontrolling interests | (4 | ) | 1 | 16 | (17 | ) | (4 | ) | ||||||||||||

Net income attributable to noncontrolling interests | — | — | — | — | — | |||||||||||||||

Net (loss) income attributable to Resolute Forest Products Inc. | $ | (4 | ) | $ | 1 | $ | 16 | $ | (17 | ) | $ | (4 | ) | |||||||

Comprehensive income attributable to Resolute Forest Products Inc. | $ | 7 | $ | 1 | $ | 27 | $ | (28 | ) | $ | 7 | |||||||||

15

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

CONDENSED CONSOLIDATING STATEMENT OF OPERATIONS AND COMPREHENSIVE (LOSS) INCOME | ||||||||||||||||||||

For the Six Months Ended June 30, 2015 | ||||||||||||||||||||

(Unaudited, in millions) | Parent | Guarantor Subsidiaries | Non-guarantor Subsidiaries | Consolidating Adjustments | Consolidated | |||||||||||||||

Sales | $ | — | $ | 1,498 | $ | 1,140 | $ | (792 | ) | $ | 1,846 | |||||||||

Costs and expenses: | ||||||||||||||||||||

Cost of sales, excluding depreciation, amortization and distribution costs | — | 1,380 | 821 | (791 | ) | 1,410 | ||||||||||||||

Depreciation and amortization | — | 46 | 71 | — | 117 | |||||||||||||||

Distribution costs | — | 82 | 149 | — | 231 | |||||||||||||||

Selling, general and administrative expenses | 6 | 26 | 49 | — | 81 | |||||||||||||||

Closure costs, impairment and other related charges | — | — | 6 | — | 6 | |||||||||||||||

Operating (loss) income | (6 | ) | (36 | ) | 44 | (1 | ) | 1 | ||||||||||||

Interest expense | (36 | ) | (2 | ) | (4 | ) | 19 | (23 | ) | |||||||||||

Other (expense) income, net | (1 | ) | 21 | 5 | (19 | ) | 6 | |||||||||||||

Parent’s equity in income of subsidiaries | 6 | — | — | (6 | ) | — | ||||||||||||||

(Loss) income before income taxes | (37 | ) | (17 | ) | 45 | (7 | ) | (16 | ) | |||||||||||

Income tax benefit (provision) | — | 4 | (24 | ) | — | (20 | ) | |||||||||||||

Net (loss) income including noncontrolling interests | (37 | ) | (13 | ) | 21 | (7 | ) | (36 | ) | |||||||||||

Net income attributable to noncontrolling interests | — | — | (1 | ) | — | (1 | ) | |||||||||||||

Net (loss) income attributable to Resolute Forest Products Inc. | $ | (37 | ) | $ | (13 | ) | $ | 20 | $ | (7 | ) | $ | (37 | ) | ||||||

Comprehensive (loss) income attributable to Resolute Forest Products Inc. | $ | (16 | ) | $ | (13 | ) | $ | 41 | $ | (28 | ) | $ | (16 | ) | ||||||

16

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

CONDENSED CONSOLIDATING STATEMENT OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS) | ||||||||||||||||||||

For the Three Months Ended June 30, 2014 | ||||||||||||||||||||

(Unaudited, in millions) | Parent | Guarantor Subsidiaries | Non-guarantor Subsidiaries | Consolidating Adjustments | Consolidated | |||||||||||||||

Sales | $ | — | $ | 892 | $ | 732 | $ | (533 | ) | $ | 1,091 | |||||||||

Costs and expenses: | ||||||||||||||||||||

Cost of sales, excluding depreciation, amortization and distribution costs | — | 830 | 507 | (525 | ) | 812 | ||||||||||||||

Depreciation and amortization | — | 23 | 39 | — | 62 | |||||||||||||||

Distribution costs | — | 42 | 93 | (1 | ) | 134 | ||||||||||||||

Selling, general and administrative expenses | 4 | 13 | 24 | — | 41 | |||||||||||||||

Closure costs, impairment and other related charges | — | 48 | 4 | — | 52 | |||||||||||||||

Net gain on disposition of assets | — | — | (2 | ) | — | (2 | ) | |||||||||||||

Operating (loss) income | (4 | ) | (64 | ) | 67 | (7 | ) | (8 | ) | |||||||||||

Interest expense | (18 | ) | (1 | ) | (1 | ) | 9 | (11 | ) | |||||||||||

Other income, net | 1 | 8 | 20 | (9 | ) | 20 | ||||||||||||||

Parent’s equity in income of subsidiaries | 19 | — | — | (19 | ) | — | ||||||||||||||

(Loss) income before income taxes | (2 | ) | (57 | ) | 86 | (26 | ) | 1 | ||||||||||||

Income tax benefit (provision) | — | 15 | (18 | ) | 2 | (1 | ) | |||||||||||||

Net (loss) income including noncontrolling interests | (2 | ) | (42 | ) | 68 | (24 | ) | — | ||||||||||||

Net income attributable to noncontrolling interests | — | — | (2 | ) | — | (2 | ) | |||||||||||||

Net (loss) income attributable to Resolute Forest Products Inc. | $ | (2 | ) | $ | (42 | ) | $ | 66 | $ | (24 | ) | $ | (2 | ) | ||||||

Comprehensive income (loss) attributable to Resolute Forest Products Inc. | $ | 25 | $ | (16 | ) | $ | 67 | $ | (51 | ) | $ | 25 | ||||||||

17

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

CONDENSED CONSOLIDATING STATEMENT OF OPERATIONS AND COMPREHENSIVE (LOSS) INCOME | ||||||||||||||||||||

For the Six Months Ended June 30, 2014 | ||||||||||||||||||||

(Unaudited, in millions) | Parent | Guarantor Subsidiaries | Non-guarantor Subsidiaries | Consolidating Adjustments | Consolidated | |||||||||||||||

Sales | $ | — | $ | 1,737 | $ | 1,433 | $ | (1,063 | ) | $ | 2,107 | |||||||||

Costs and expenses: | ||||||||||||||||||||

Cost of sales, excluding depreciation, amortization and distribution costs | — | 1,650 | 1,039 | (1,056 | ) | 1,633 | ||||||||||||||

Depreciation and amortization | — | 48 | 76 | — | 124 | |||||||||||||||

Distribution costs | — | 79 | 177 | (2 | ) | 254 | ||||||||||||||

Selling, general and administrative expenses | 8 | 22 | 47 | — | 77 | |||||||||||||||

Closure costs, impairment and other related charges | — | 50 | 12 | — | 62 | |||||||||||||||

Net gain on disposition of assets | — | — | (2 | ) | — | (2 | ) | |||||||||||||

Operating (loss) income | (8 | ) | (112 | ) | 84 | (5 | ) | (41 | ) | |||||||||||

Interest expense | (35 | ) | (2 | ) | (4 | ) | 18 | (23 | ) | |||||||||||

Other income, net | — | 19 | 6 | (18 | ) | 7 | ||||||||||||||

Parent’s equity in loss of subsidiaries | (9 | ) | — | — | 9 | — | ||||||||||||||

(Loss) income before income taxes | (52 | ) | (95 | ) | 86 | 4 | (57 | ) | ||||||||||||

Income tax benefit (provision) | — | 30 | (24 | ) | 1 | 7 | ||||||||||||||

Net (loss) income including noncontrolling interests | (52 | ) | (65 | ) | 62 | 5 | (50 | ) | ||||||||||||

Net income attributable to noncontrolling interests | — | — | (2 | ) | — | (2 | ) | |||||||||||||

Net (loss) income attributable to Resolute Forest Products Inc. | $ | (52 | ) | $ | (65 | ) | $ | 60 | $ | 5 | $ | (52 | ) | |||||||

Comprehensive (loss) income attributable to Resolute Forest Products Inc. | $ | (1 | ) | $ | (15 | ) | $ | 61 | $ | (46 | ) | $ | (1 | ) | ||||||

18

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

CONDENSED CONSOLIDATING BALANCE SHEET | ||||||||||||||||||||

As of June 30, 2015 | ||||||||||||||||||||

(Unaudited, in millions) | Parent | Guarantor Subsidiaries | Non-guarantor Subsidiaries | Consolidating Adjustments | Consolidated | |||||||||||||||

Assets | ||||||||||||||||||||

Current assets: | ||||||||||||||||||||

Cash and cash equivalents | $ | — | $ | 261 | $ | 42 | $ | — | $ | 303 | ||||||||||

Accounts receivable, net | — | 348 | 137 | — | 485 | |||||||||||||||

Accounts receivable from affiliates | 3 | 406 | 176 | (585 | ) | — | ||||||||||||||

Inventories, net | — | 252 | 295 | (10 | ) | 537 | ||||||||||||||

Deferred income tax assets | — | — | 65 | — | 65 | |||||||||||||||

Advance and interest receivable from parent | — | 40 | — | (40 | ) | — | ||||||||||||||

Notes receivable from affiliates | — | 324 | — | (324 | ) | — | ||||||||||||||

Other current assets | — | 33 | 32 | — | 65 | |||||||||||||||

Total current assets | 3 | 1,664 | 747 | (959 | ) | 1,455 | ||||||||||||||

Fixed assets, net | — | 732 | 1,212 | — | 1,944 | |||||||||||||||

Amortizable intangible assets, net | — | — | 61 | — | 61 | |||||||||||||||

Deferred income tax assets | — | — | 1,101 | 2 | 1,103 | |||||||||||||||

Notes receivable from parent | — | 690 | — | (690 | ) | — | ||||||||||||||

Investments in consolidated subsidiaries and affiliates | 4,123 | 2,028 | — | (6,151 | ) | — | ||||||||||||||

Other assets | 7 | 52 | 67 | — | 126 | |||||||||||||||

Total assets | $ | 4,133 | $ | 5,166 | $ | 3,188 | $ | (7,798 | ) | $ | 4,689 | |||||||||

Liabilities and equity | ||||||||||||||||||||

Current liabilities: | ||||||||||||||||||||

Accounts payable and accrued liabilities | $ | 5 | $ | 194 | $ | 272 | $ | — | $ | 471 | ||||||||||

Current portion of long-term debt | — | 1 | — | — | 1 | |||||||||||||||

Accounts payable to affiliates | 406 | 176 | 3 | (585 | ) | — | ||||||||||||||

Advance and interest payable to subsidiaries | 40 | — | — | (40 | ) | — | ||||||||||||||

Notes payable to affiliate | — | — | 324 | (324 | ) | — | ||||||||||||||

Total current liabilities | 451 | 371 | 599 | (949 | ) | 472 | ||||||||||||||

Long-term debt, net of current portion | 595 | 1 | — | — | 596 | |||||||||||||||

Notes payable to subsidiaries | 690 | — | — | (690 | ) | — | ||||||||||||||

Pension and other postretirement benefit obligations | — | 408 | 1,066 | — | 1,474 | |||||||||||||||

Deferred income tax liabilities | — | — | 3 | — | 3 | |||||||||||||||

Other liabilities | 1 | 30 | 40 | — | 71 | |||||||||||||||

Total liabilities | 1,737 | 810 | 1,708 | (1,639 | ) | 2,616 | ||||||||||||||

Total equity | 2,396 | 4,356 | 1,480 | (6,159 | ) | 2,073 | ||||||||||||||

Total liabilities and equity | $ | 4,133 | $ | 5,166 | $ | 3,188 | $ | (7,798 | ) | $ | 4,689 | |||||||||

19

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

CONDENSED CONSOLIDATING BALANCE SHEET | ||||||||||||||||||||

As of December 31, 2014 | ||||||||||||||||||||

(Unaudited, in millions) | Parent | Guarantor Subsidiaries | Non-guarantor Subsidiaries | Consolidating Adjustments | Consolidated | |||||||||||||||

Assets | ||||||||||||||||||||

Current assets: | ||||||||||||||||||||

Cash and cash equivalents | $ | — | $ | 257 | $ | 80 | $ | — | $ | 337 | ||||||||||

Accounts receivable, net | — | 383 | 156 | — | 539 | |||||||||||||||

Accounts receivable from affiliates | — | 384 | 95 | (479 | ) | — | ||||||||||||||

Inventories, net | — | 251 | 300 | (9 | ) | 542 | ||||||||||||||

Deferred income tax assets | — | — | 70 | — | 70 | |||||||||||||||

Note and interest receivable from parent | — | 287 | — | (287 | ) | — | ||||||||||||||

Notes receivable from affiliates | — | 318 | — | (318 | ) | — | ||||||||||||||

Other current assets | — | 20 | 26 | — | 46 | |||||||||||||||

Total current assets | — | 1,900 | 727 | (1,093 | ) | 1,534 | ||||||||||||||

Fixed assets, net | — | 742 | 1,243 | — | 1,985 | |||||||||||||||

Amortizable intangible assets, net | — | — | 62 | — | 62 | |||||||||||||||

Deferred income tax assets | — | — | 1,217 | 2 | 1,219 | |||||||||||||||

Note receivable from parent | — | 388 | — | (388 | ) | — | ||||||||||||||

Investments in consolidated subsidiaries and affiliates | 4,096 | 2,020 | — | (6,116 | ) | — | ||||||||||||||

Other assets | 7 | 49 | 65 | — | 121 | |||||||||||||||

Total assets | $ | 4,103 | $ | 5,099 | $ | 3,314 | $ | (7,595 | ) | $ | 4,921 | |||||||||

Liabilities and equity | ||||||||||||||||||||

Current liabilities: | ||||||||||||||||||||

Accounts payable and accrued liabilities | $ | 5 | $ | 193 | $ | 320 | $ | — | $ | 518 | ||||||||||

Current portion of long-term debt | — | 1 | — | — | 1 | |||||||||||||||

Accounts payable to affiliates | 386 | 93 | — | (479 | ) | — | ||||||||||||||

Note and interest payable to subsidiary | 287 | — | — | (287 | ) | — | ||||||||||||||

Notes payable to affiliate | — | — | 318 | (318 | ) | — | ||||||||||||||

Total current liabilities | 678 | 287 | 638 | (1,084 | ) | 519 | ||||||||||||||

Long-term debt, net of current portion | 595 | 1 | — | — | 596 | |||||||||||||||

Note payable to subsidiary | 388 | — | — | (388 | ) | — | ||||||||||||||

Pension and other postretirement benefit obligations | — | 414 | 1,202 | — | 1,616 | |||||||||||||||

Deferred income tax liabilities | — | — | 3 | — | 3 | |||||||||||||||

Other liabilities | 1 | 29 | 40 | — | 70 | |||||||||||||||

Total liabilities | 1,662 | 731 | 1,883 | (1,472 | ) | 2,804 | ||||||||||||||

Total equity | 2,441 | 4,368 | 1,431 | (6,123 | ) | 2,117 | ||||||||||||||

Total liabilities and equity | $ | 4,103 | $ | 5,099 | $ | 3,314 | $ | (7,595 | ) | $ | 4,921 | |||||||||

20

RESOLUTE FOREST PRODUCTS INC.

Notes to Unaudited Interim Consolidated Financial Statements

CONDENSED CONSOLIDATING STATEMENT OF CASH FLOWS | ||||||||||||||||||||

For the Six Months Ended June 30, 2015 | ||||||||||||||||||||

(Unaudited, in millions) | Parent | Guarantor Subsidiaries | Non-guarantor Subsidiaries | Consolidating Adjustments | Consolidated | |||||||||||||||

Net cash provided by operating activities | $ | — | $ | 80 | $ | 10 | $ | — | $ | 90 | ||||||||||

Cash flows from investing activities: | ||||||||||||||||||||

Cash invested in fixed assets | — | (37 | ) | (42 | ) | — | (79 | ) | ||||||||||||

Increase in deposit requirements for letters of credit, net | — | — | (4 | ) | — | (4 | ) | |||||||||||||

Advance to parent | — | (37 | ) | — | 37 | — | ||||||||||||||

Net cash used in investing activities | — | (74 | ) | (46 | ) | 37 | (83 | ) | ||||||||||||

Cash flows from financing activities: | ||||||||||||||||||||

Payments of financing and credit facility fees | — | (2 | ) | (1 | ) | — | (3 | ) | ||||||||||||

Purchases of treasury stock | (37 | ) | — | — | — | (37 | ) | |||||||||||||

Advance from subsidiary | 37 | — | — | (37 | ) | — | ||||||||||||||

Net cash used in financing activities | — | (2 | ) | (1 | ) | (37 | ) | (40 | ) | |||||||||||

Effect of exchange rate changes on cash and cash equivalents | — | — | (1 | ) | — | (1 | ) | |||||||||||||

Net increase (decrease) in cash and cash equivalents | — | 4 | (38 | ) | — | (34 | ) | |||||||||||||

Cash and cash equivalents: | ||||||||||||||||||||

Beginning of period | — | 257 | 80 | — | 337 | |||||||||||||||

End of period | $ | — | $ | 261 | $ | 42 | $ | — | $ | 303 | ||||||||||

CONDENSED CONSOLIDATING STATEMENT OF CASH FLOWS | ||||||||||||||||||||

For the Six Months Ended June 30, 2014 | ||||||||||||||||||||

(Unaudited, in millions) | Parent | Guarantor Subsidiaries | Non-guarantor Subsidiaries | Consolidating Adjustments | Consolidated | |||||||||||||||

Net cash (used in) provided by operating activities | $ | — | $ | (70 | ) | $ | 92 | $ | — | $ | 22 | |||||||||

Cash flows from investing activities: | ||||||||||||||||||||

Cash invested in fixed assets | — | (38 | ) | (44 | ) | — | (82 | ) | ||||||||||||

Disposition of assets | — | — | 2 | — | 2 | |||||||||||||||

Decrease in restricted cash | — | — | 1 | — | 1 | |||||||||||||||

Increase in deposit requirements for letters of credit, net | — | — | (1 | ) | — | (1 | ) | |||||||||||||

Net cash used in investing activities | — | (38 | ) | (42 | ) | — | (80 | ) | ||||||||||||

Cash flows from financing activities: | ||||||||||||||||||||

Payments of debt | — | (1 | ) | — | — | (1 | ) | |||||||||||||

Payments of financing and credit facility fees | — | (1 | ) | — | — | (1 | ) | |||||||||||||

Net cash used in financing activities | — | (2 | ) | — | — | (2 | ) | |||||||||||||

Effect of exchange rate changes on cash and cash equivalents | — | — | 1 | — | 1 | |||||||||||||||

Net (decrease) increase in cash and cash equivalents | — | (110 | ) | 51 | — | (59 | ) | |||||||||||||

Cash and cash equivalents: | ||||||||||||||||||||

Beginning of period | — | 165 | 157 | — | 322 | |||||||||||||||

End of period | $ | — | $ | 55 | $ | 208 | $ | — | $ | 263 | ||||||||||

21

ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following management’s discussion and analysis is intended to help the reader understand Resolute Forest Products, our results of operations, cash flows and financial condition. The discussion is provided as a supplement to, and should be read in conjunction with, our consolidated financial statements and the accompanying notes contained in Item 1 – Financial Statements.

When we refer to “Resolute Forest Products,” “we,” “our,” “us” or the “Company,” we mean Resolute Forest Products Inc. with its subsidiaries and affiliates, either individually or collectively, unless otherwise indicated.

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING INFORMATION AND USE OF THIRD-PARTY DATA

Statements in this quarterly report on Form 10-Q that are not reported financial results or other historical information of Resolute Forest Products are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. They include, for example, statements relating to our: efforts to continue to reduce costs and increase revenues and profitability, including our cost-reduction initiatives; business and operating outlook; future pension funding obligations; assessment of market conditions; prospects, growth strategies and the industry in which we operate; and strategies for achieving our goals generally. Forward-looking statements may be identified by the use of forward-looking terminology such as the words “should,” “would,” “could,” “will,” “may,” “expect,” “believe,” “anticipate,” “attempt,” “project” and other terms with similar meaning indicating possible future events or potential impact on our business or Resolute Forest Products’ shareholders.

The reader is cautioned not to place undue reliance on these forward-looking statements, which are not guarantees of future performance. These statements are based on management’s current assumptions, beliefs and expectations, all of which involve a number of business risks and uncertainties that could cause actual results to differ materially. The potential risks and uncertainties that could cause our actual future financial condition, results of operations and performance to differ materially from those expressed or implied in this quarterly report on Form 10-Q include, but are not limited to, developments in alternative media, which are expected to adversely affect the demand for some of our key products, and the effectiveness of our responses to these developments; the impact of any additional closure costs and long-lived asset impairment or accelerated depreciation charges; the impact of currency fluctuations on our competitive position, selling prices and manufacturing costs; the impact of global economic conditions; intense competition in the forest products industry and our ability to compete effectively; negative publicity, even if unjustified, which could have a negative impact on our brand and the marketability of our products; the highly cyclical nature of the forest products industry, which could impact the prices of and demand for our products, which could result in small or negative profit margins, lower sales volumes and curtailment or closure of operations; the impact of contributions to our Canadian pension plans, which could be at levels significantly higher than expected; the impact of the terms of our outstanding indebtedness, which could restrict our current and future operations, particularly our ability to respond to changes and take certain actions; our ability to maintain adequate capital resources to provide for all of our capital requirements, which are substantial; any inability to successfully implement our strategies to increase our earnings power; the impact of changes in laws or regulations, including environmental regulations and liabilities and the impact of future regulation of our Canadian softwood lumber exports to the United States; any difficulties in obtaining wood fiber at favorable prices, or at all; the impact of changes in the cost of purchased energy and other raw materials, which could lead to higher manufacturing costs and reduce our margins; the impact of changes in political or economic conditions in Canada, the United States or other countries in which our products are manufactured or sold; physical and financial risks associated with climate change; the impact of any labor disputes; extreme weather conditions or natural or man-made disasters, which could disrupt our supply chain and delivery of our products; cyber security risks; the impact of acquisitions, divestitures or other strategic transactions we may pursue; and the potential risks and uncertainties set forth under Part I, Item 1A, “Risk Factors,” of our annual report on Form 10-K for the year ended December 31, 2014, filed with the U.S. Securities and Exchange Commission, or the “SEC”, on March 2, 2015 (the “2014 Annual Report”).

All forward-looking statements in this quarterly report on Form 10-Q are expressly qualified by the cautionary statements contained or referred to in this section and in our other filings with the SEC and the Canadian securities regulatory authorities. We disclaim any obligation to publicly update or revise any forward-looking information, whether as a result of new information, future events or otherwise, except as required by law.

Market and industry data

The information on industry and general economic conditions in this quarterly report on Form 10-Q was derived from third-party sources and trade publications we believe to be widely accepted and accurate. We have not independently verified the information and cannot assure you of its accuracy.

22

OVERVIEW

Resolute Forest Products is a global leader in the forest products industry, with a diverse range of products, including newsprint, specialty papers, market pulp and wood products, which are marketed in close to 80 countries. We own or operate some 40 pulp and paper mills and wood products facilities in the U.S., Canada and South Korea, and power generation assets in Canada. We’re the biggest Canadian producer of wood products east of the Rockies and one of the most significant pulp producers in North America. By capacity, we are the number one producer of newsprint in the world and the largest producer of uncoated mechanical papers in North America.

We report our activities in four business segments: newsprint, specialty papers, market pulp and wood products.

We are guided by our vision and values, focusing on safety, profitability, accountability, sustainability and teamwork. These are the elements that we believe best define us:

• | Competitive cost structure - as a result of aggressive cost reductions and mill rationalizations, today we compete as a leading, lower-cost North American producer. Maintaining this competitive advantage is our key focus. We are committed to maximizing shareholder value and earnings power by: stressing our guiding principles of operational excellence in everything we do; pushing to optimize our asset base in order to maximize the utilization of our most cost-effective mills; and streamlining production to adapt to changing market dynamics. |

• | Synergistic and diversified asset base - we apply our principles of operational excellence to our synergistic and diversified asset base, one that has evolved with time as we execute our profitable retreat from paper toward more sustainable long-term businesses. Put simply, our optimized paper segments generate significant cash flow, which we use to grow our business for the long-term, including: the tissue manufacturing and converting facility scheduled for ramp-up in 2017; the three pulp mills we acquired in 2012; the capacity enhancement initiatives in wood products; and the continuous pulp digester project at the Calhoun, Tennessee, pulp and paper facility. This synergistic and complementary asset base also offers the fiber management advantage of integration and earnings diversification. |

• | Financial strength - we make disciplined capital management a priority; we believe in maintaining a flexible and conservative capital structure. Our financial strength gives us the ability to consider a range of suitable opportunities, and the patience to make sure the valuation is right. |

Our Business

For information relating to our business, including our products, strategy, sustainable performance and development, and power generation assets, refer to our 2014 Annual Report.

Second Quarter Overview

In the second quarter of 2015, we changed our presentation of segment operating income to reallocate the net financing and remeasurement components of pension and other postretirement benefit, or “OPEB”, costs from the reportable segments to “corporate and other” in the segment presentation of operating income. We refer to these components, which consist of interest cost, expected return on plan assets and amortization of actuarial losses and gains, as “non-operating pension and OPEB costs or credits.” Current service costs and amortization of prior service credits will continue to be allocated to the reportable segments.

We now also treat non-operating pension and OPEB costs as a special item to be adjusted for purposes of establishing our non-GAAP performance measures, as further described below. We believe that reallocating the non-operating pension and OPEB costs to “corporate and other” and removing them from non-GAAP performance measures better reflects our ongoing operating results and improves their comparability between periods, and will therefore be more useful to investors. This approach is consistent with the indicators management uses internally to evaluate performance, including those used by the chief operating decision maker, and also consistent with a number of industry peers.

Prior period amounts have been reclassified to conform to the 2015 presentation.

Three months ended June 30, 2015 vs. June 30, 2014

Excluding special items, we generated operating income of $29 million in the quarter, compared to $43 million in the second quarter of 2014. Unadjusted for special items, operating income was $16 million, compared to an operating loss of $8 million in the year-ago period. Special items are described below.

23

Our net income in the quarter, excluding special items, was $7 million, or $0.07 per share, down from net income, excluding special items, of $17 million, or $0.18 per share, in the year-ago period. Unadjusted for special items, our net loss in the quarter was $4 million, or $0.04 per share, compared to $2 million, or $0.02 per share, in the year-ago period.

Three Months Ended June 30, 2015 | Operating Income (Loss) | Net Income (Loss) | EPS | |||||||||

(unaudited, in millions, except per share amounts) | ||||||||||||

GAAP, as reported | $ | 16 | $ | (4 | ) | $ | (0.04 | ) | ||||

Adjustments for special items (1): | ||||||||||||

Foreign exchange translation gain | — | (1 | ) | (0.01 | ) | |||||||

Start-up costs | 1 | 1 | 0.01 | |||||||||

Non-operating pension and OPEB costs | 12 | 12 | 0.12 | |||||||||

Income tax effect of special items | — | (1 | ) | (0.01 | ) | |||||||

GAAP, as adjusted for special items | $ | 29 | $ | 7 | $ | 0.07 | ||||||

Three Months Ended June 30, 2014 | Operating Income (Loss) | Net Income (Loss) | EPS | |||||||||

(unaudited, in millions, except per share amounts) | ||||||||||||

GAAP, as reported | $ | (8 | ) | $ | (2 | ) | $ | (0.02 | ) | |||

Adjustments for special items (1): | ||||||||||||

Foreign exchange translation gain | — | (17 | ) | (0.18 | ) | |||||||

Closure costs, impairment and other related charges | 52 | 52 | 0.55 | |||||||||

Inventory write-downs related to closures | 3 | 3 | 0.03 | |||||||||

Start-up costs | 1 | 1 | 0.01 | |||||||||

Net gain on disposition of assets | (2 | ) | (2 | ) | (0.02 | ) | ||||||

Non-operating pension and OPEB credits | (3 | ) | (3 | ) | (0.03 | ) | ||||||

Other income, net | — | (3 | ) | (0.03 | ) | |||||||

Income tax effect of special items | — | (12 | ) | (0.13 | ) | |||||||

GAAP, as adjusted for special items | $ | 43 | $ | 17 | $ | 0.18 | ||||||