Attached files

| file | filename |

|---|---|

| 8-K - 8-K - SunCoke Energy, Inc. | d93256d8k.htm |

| EX-99.1 - EX-99.1 - SunCoke Energy, Inc. | d93256dex991.htm |

Exhibit 99.2

SunCoke Energy, Inc.

Q2

2015 Earnings,

M&A Announcement

Conference Call

July 21, 2015

SunCoke Energy™

Forward-Looking Statements

TM

This slide presentation should be reviewed in conjunction with the Second

Quarter 2015 earnings release of SunCoke Energy, Inc. (SXC) and the conference call held on July 21, 2015 at 10:00 a.m. ET.

Some of the information included in

this presentation constitutes “forward-looking statements” as defined in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. All statements in this presentation that

express opinions, expectations, beliefs, plans, objectives, assumptions or projections with respect to anticipated future performance of SXC or SunCoke Energy Partners, L.P. (SXCP), in contrast with statements of historical facts, are

forward-looking statements. Such forward-looking statements are based on management’s beliefs and assumptions and on information currently available. Forward-looking statements include information concerning possible or assumed future results

of operations, business strategies, financing plans, competitive position, potential growth opportunities, potential operating performance improvements, the effects of competition and the effects of future legislation or regulations. Forward-looking

statements include all statements that are not historical facts and may be identified by the use of forward-looking terminology such as the words “believe,” “expect,” “plan,” “intend,” “anticipate,”

“estimate,” “predict,” “potential,” “continue,” “may,” “will,” “should” or the negative of these terms or similar expressions.

Although management believes that its plans, intentions and expectations reflected in or suggested by the forward-looking statements made in this presentation are reasonable, no

assurance can be given that these plans, intentions or expectations will be achieved when anticipated or at all. Moreover, such statements are subject to a number of assumptions, risks and uncertainties. Many of these risks are beyond the control of

SXC and SXCP, and may cause actual results to differ materially from those implied or expressed by the forward-looking statements. Each of SXC and SXCP has included in its filings with the Securities and Exchange Commission cautionary language

identifying important factors (but not necessarily all the important factors) that could cause actual results to differ materially from those expressed in any forward-looking statement. For more information concerning these factors, see the

Securities and Exchange Commission filings of SXC and SXCP. All forward-looking statements included in this presentation are expressly qualified in their entirety by such cautionary statements. Although forward-looking statements are based on

current beliefs and expectations, caution should be taken not to place undue reliance on any such forward-looking statements because such statements speak only as of the date hereof. SXC and SXCP do not have any intention or obligation to update

publicly any forward-looking statement (or its associated cautionary language) whether as a result of new information or future events or after the date of this presentation, except as required by applicable law.

This presentation includes certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures.

Reconciliations of non-GAAP financial measures to GAAP financial measures are provided in the Appendix at the end of the presentation. Investors are urged to consider carefully the

comparable GAAP measures and the reconciliations to those measures provided in the Appendix.

SXC Q2 2015 Earnings and M&A Announcements Call 1

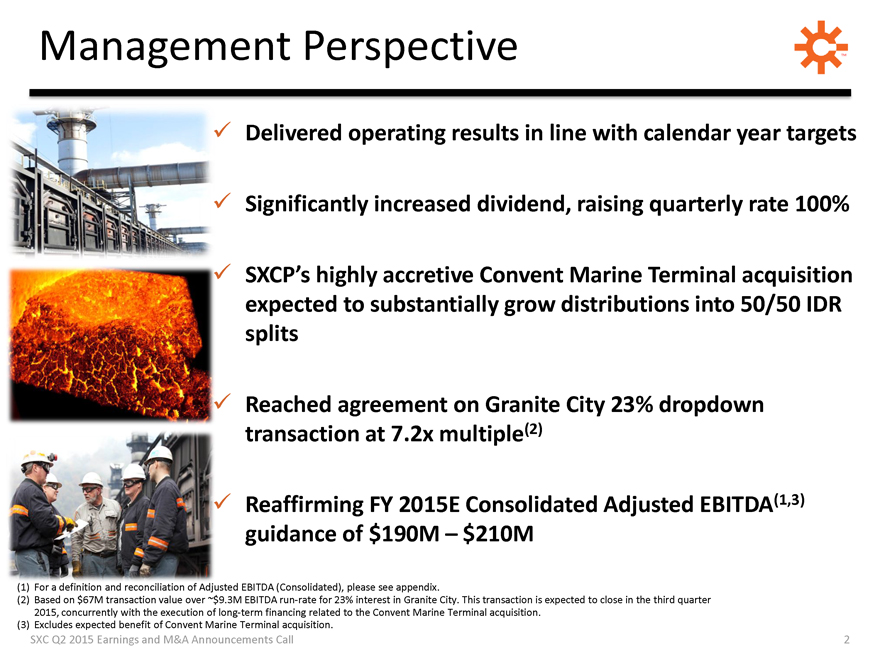

Management Perspective

Delivered operating results in line with calendar year targets

Significantly

increased dividend, raising quarterly rate 100%

SXCP’s highly accretive Convent Marine Terminal acquisition expected to substantially grow distributions into

50/50 IDR splits

Reached agreement on Granite City 23% dropdown transaction at 7.2x multiple(2)

Reaffirming FY 2015E Consolidated Adjusted EBITDA(1,3) guidance of $190M – $210M

(1) For

a definition and reconciliation of Adjusted EBITDA (Consolidated), please see appendix.

(2) Based on $67M transaction value over ~$9.3M EBITDA run-rate for 23%

interest in Granite City. This transaction is expected to close in the third quarter 2015, concurrently with the execution of long-term financing related to the Convent Marine Terminal acquisition.

(3) Excludes expected benefit of Convent Marine Terminal acquisition.

SXC Q2 2015 Earnings and

M&A Announcements Call 2

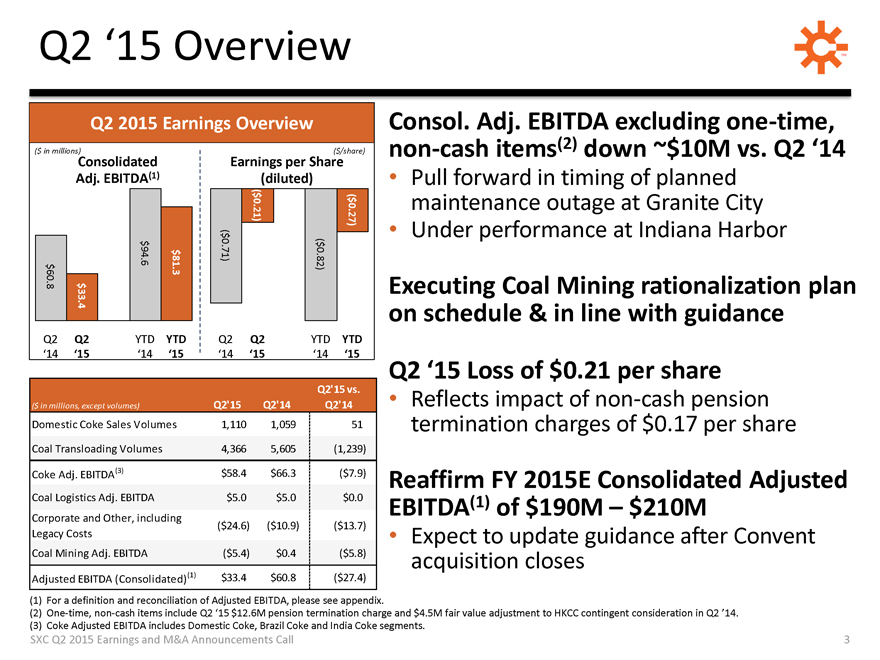

Q2 ‘15 Overview

Q2

2015 Earnings Overview

($ in millions)

Consolidated

Adj. EBITDA(1)

$60.8

$33.4

$94.6

$81.3

Q2

‘14

Q2

‘15

YTD

‘14

YTD

‘15

($/share)

Earnings per Share (diluted)

($0.71)

($0.21)

($0.82)

($0.27)

Q2

‘14

Q2

‘15

YTD

‘14

YTD

‘15

Q2’15 vs.

($ in millions, except volumes)

Q2’15

Q2’14

Q2’14

Domestic Coke Sales Volumes

1,110

1,059

51

Coal Transloading Volumes

4,366

5,605

(1,239)

Coke Adj. EBITDA(3)

$58.4

$66.3

($7.9)

Coal Logistics Adj. EBITDA

$5.0

$5.0

$0.0

Corporate and Other, including

($24.6)

($10.9)

($13.7)

Legacy Costs

Coal Mining Adj. EBITDA

($5.4)

$0.4

($5.8)

Adjusted EBITDA (Consolidated)(1)

$33.4

$60.8

($27.4)

(1) For a definition and reconciliation of Adjusted EBITDA, please see appendix.

(2) One-time, non-cash items include Q2 ‘15 $12.6M pension termination charge and $4.5M fair value adjustment to HKCC contingent consideration in Q2 ’14.

(3) Coke Adjusted EBITDA includes Domestic Coke, Brazil Coke and India Coke segments.

Consol. Adj. EBITDA excluding one-time, non-cash items(2) down ~$10M vs. Q2 ‘14

Pull

forward in timing of planned maintenance outage at Granite City

Under performance at Indiana Harbor

Executing Coal Mining rationalization plan on schedule & in line with guidance

Q2

‘15 Loss of $0.21 per share

Reflects impact of non-cash pension termination charges of $0.17 per share

Reaffirm FY 2015E Consolidated Adjusted EBITDA(1) of $190M – $210M

Expect to update

guidance after Convent acquisition closes

SXC Q2 2015 Earnings and M&A Announcements Call 3

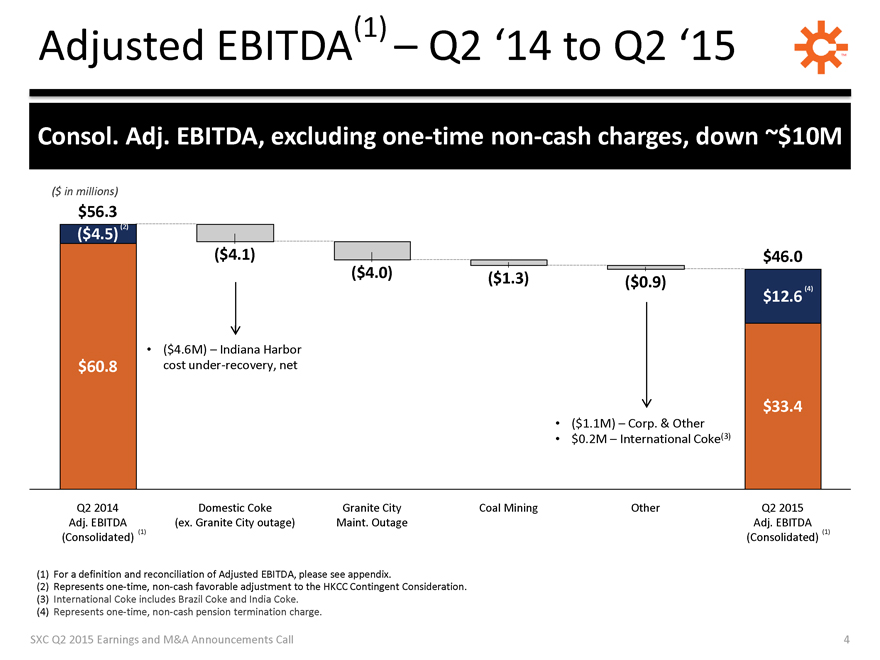

Adjusted EBITDA(1) – Q2 ‘14 to Q2 ‘15

Consol. Adj. EBITDA, excluding one-time non-cash charges, down ~$10M

($ in millions)

$56.3

($4.5) (2)

$60.8

($4.1)

($4.6M) – Indiana Harbor cost under-recovery, net

($4.0)

($1.3)

($0.9)

($1.1M) – Corp. & Other

$0.2M – International Coke(3)

$46.0

$12.6 (4)

$33.4

Q2 2014 Adj. EBITDA

(Consolidated) (1)

Domestic Coke (ex. Granite City outage)

Granite City

Maint. Outage

Coal Mining

Other

Q2 2015 Adj. EBITDA

(Consolidated) (1)

(1) For a definition and reconciliation of Adjusted EBITDA, please see appendix.

(2)

Represents one-time, non-cash favorable adjustment to the HKCC Contingent Consideration.

(3) International Coke includes Brazil Coke and India Coke.

(4) Represents one-time, non-cash pension termination charge.

SXC Q2 2015 Earnings and M&A

Announcements Call 4

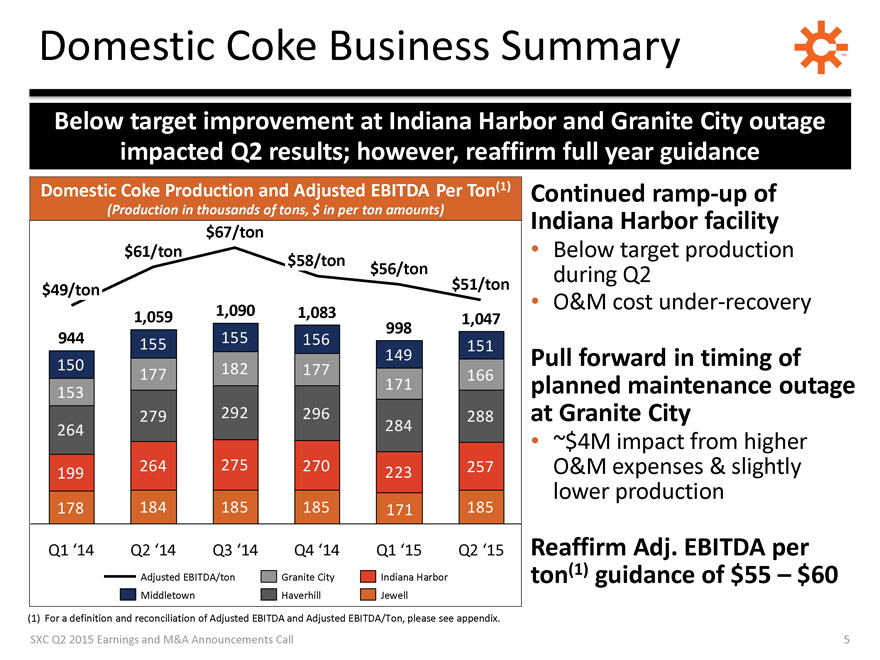

Domestic Coke Business Summary

Below target improvement at Indiana Harbor and Granite City outage impacted Q2 results; however, reaffirm full year guidance

Domestic Coke Production and Adjusted EBITDA Per Ton(1)

(Production in thousands of tons, $ in

per ton amounts)

$49/ton $61/ton $67/ton $58/ton $56/ton $51/ton

944 150 153

264 199 178

1,059 155 177 279 264 184

1,090 155 182 292 275 185

1,083 156 177 296 270 185

998 149 171 284 223 171

1,047 151 166 288 257 185

Q1 ‘14 Q2 ‘14 Q3 ‘14 Q4 ‘14 Q1 ‘15 Q2

‘15

Adjusted EBITDA/ton

Middletown

Granite City

Haverhill

Indiana Harbor

Jewell

(1) For a definition and reconciliation of Adjusted EBITDA and Adjusted EBITDA/Ton, please see appendix.

Continued ramp-up of Indiana Harbor facility

Below target production during Q2

O&M cost under-recovery

Pull forward in timing of planned maintenance outage at Granite

City

~$4M impact from higher O&M expenses & slightly lower production

Reaffirm Adj. EBITDA per ton(1) guidance of $55 – $60

SXC Q2 2015 Earnings and M&A

Announcements Call

5

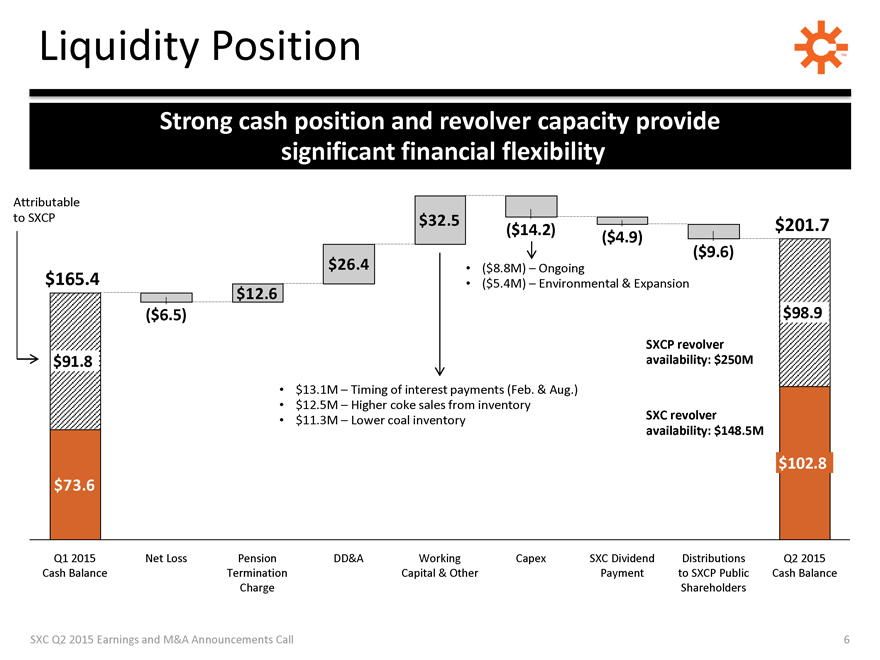

Liquidity Position

Strong

cash position and revolver capacity provide significant financial flexibility

Attributable to SXCP

$165.4 $91.8 $73.6

($6.5)

$12.6

$26.4

$32.5

($14.2)

($4.9)

($9.6)

$201.7 $98.9 $102.8

$13.1M – Timing of interest payments (Feb. & Aug.)

$12.5M – Higher coke sales from inventory

$11.3M – Lower coal

inventory

($8.8M) – Ongoing

($5.4M) – Environmental &

Expansion

SXCP revolver availability: $250M

SXC revolver availability:

$148.5M

Q1 2015 Cash Balance

Net Loss

Pension Termination Charge

DD&A

Working Capital & Other

Capex

SXC Dividend Payment

Distributions to SXCP Public Shareholders

Q2 2015 Cash Balance

SXC Q2 2015 Earnings and M&A Announcements Call

6

STRATEGIC UPDATES

SunCoke

Energy™

SXC Q2 2015 Earnings and M&A Announcements Call

7

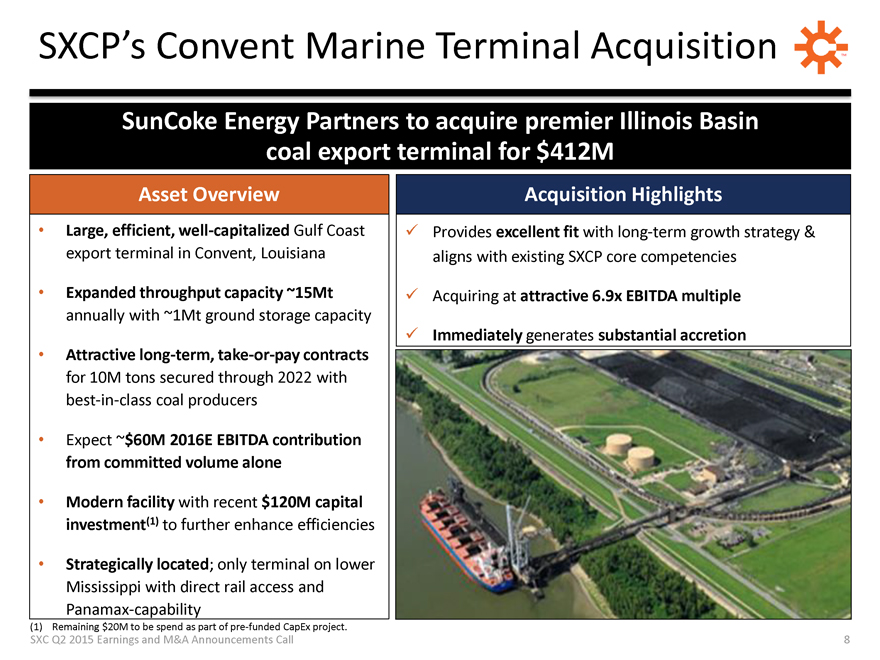

SXCP’s Convent Marine Terminal Acquisition

SunCoke Energy Partners to acquire premier Illinois Basin coal export terminal for $412M

Asset

Overview

Large, efficient, well-capitalized Gulf Coast export terminal in Convent, Louisiana

Expanded throughput capacity ~15Mt annually with ~1Mt ground storage capacity

Attractive

long-term, take-or-pay contracts for 10M tons secured through 2022 with best-in-class coal producers

Expect ~$60M 2016E EBITDA contribution from committed volume

alone

Modern facility with recent $120M capital investment(1) to further enhance efficiencies

Strategically located; only terminal on lower Mississippi with direct rail access and Panamax-capability

(1) Remaining $20M to be spend as part of pre-funded CapEx project.

Acquisition Highlights

Provides excellent fit with long-term growth strategy & aligns with existing SXCP core competencies

Acquiring at attractive 6.9x EBITDA multiple

Immediately generates substantial accretion

SXC Q2 2015 Earnings and M&A Announcements Call

8

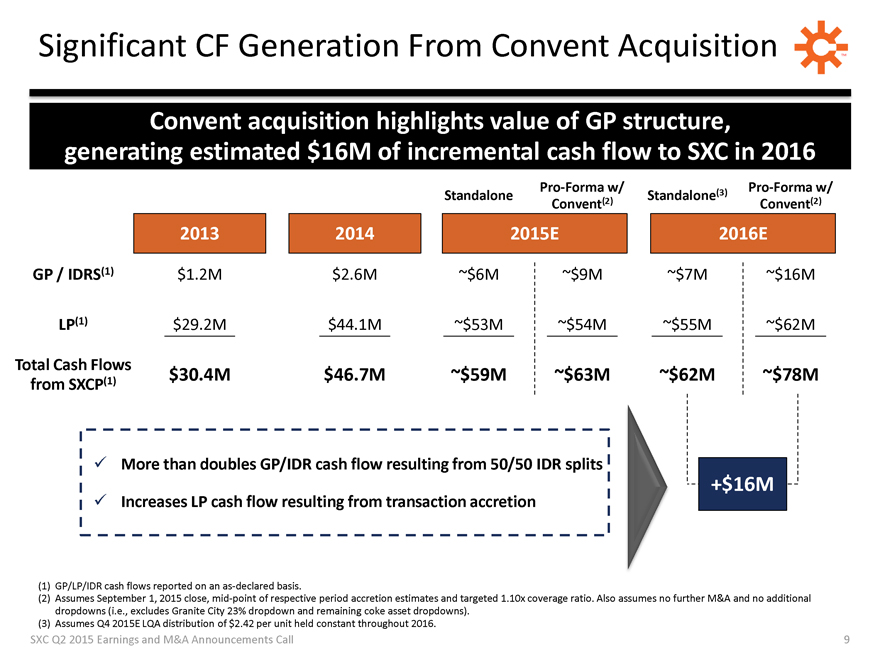

Significant CF Generation From Convent Acquisition

Convent acquisition highlights value of GP structure, generating estimated $16M of incremental cash flow to SXC in 2016

GP / IDRS(1) LP(1) Total Cash Flows from SXCP(1)

2013 $1.2M $29.2M $30.4M

2014 $2.6M $44.1M $46.7M

Standalone Pro-Forma w/ Convent(2)

2015E

~$6M ~$53M ~$59M

~$9M ~$54M ~$63M

Standalone(3)

Pro-Forma w/ Convent(2)

2016E

~$7M ~$55M ~$62M

~$16M ~$62M ~$78M

+$16M

More than doubles GP/IDR cash flow resulting from 50/50 IDR splits

Increases LP cash flow resulting from transaction accretion

(1) GP/LP/IDR cash flows reported

on an as-declared basis.

(2) Assumes September 1, 2015 close, mid-point of respective period accretion estimates and targeted 1.10x coverage ratio. Also

assumes no further M&A and no additional dropdowns (i.e., excludes Granite City 23% dropdown and remaining coke asset dropdowns).

(3) Assumes Q4 2015E LQA

distribution of $2.42 per unit held constant throughout 2016.

SXC Q2 2015 Earnings and M&A Announcements Call

9

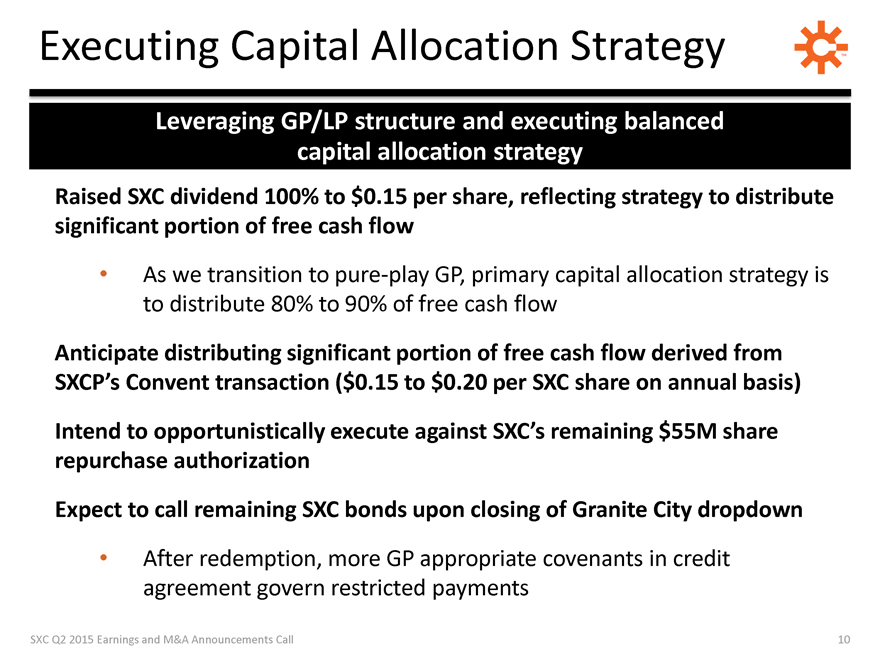

Executing Capital Allocation Strategy

Leveraging GP/LP structure and executing balanced capital allocation strategy

Raised SXC

dividend 100% to $0.15 per share, reflecting strategy to distribute significant portion of free cash flow

As we transition to pure-play GP, primary capital

allocation strategy is to distribute 80% to 90% of free cash flow

Anticipate distributing significant portion of free cash flow derived from

SXCP’s Convent transaction ($0.15 to $0.20 per SXC share on annual basis)

Intend to

opportunistically execute against SXC’s remaining $55M share repurchase authorization

Expect to call remaining SXC bonds upon closing of Granite City dropdown

After redemption, more GP appropriate covenants in credit agreement govern restricted payments

SXC Q2 2015 Earnings and M&A Announcements Call

10

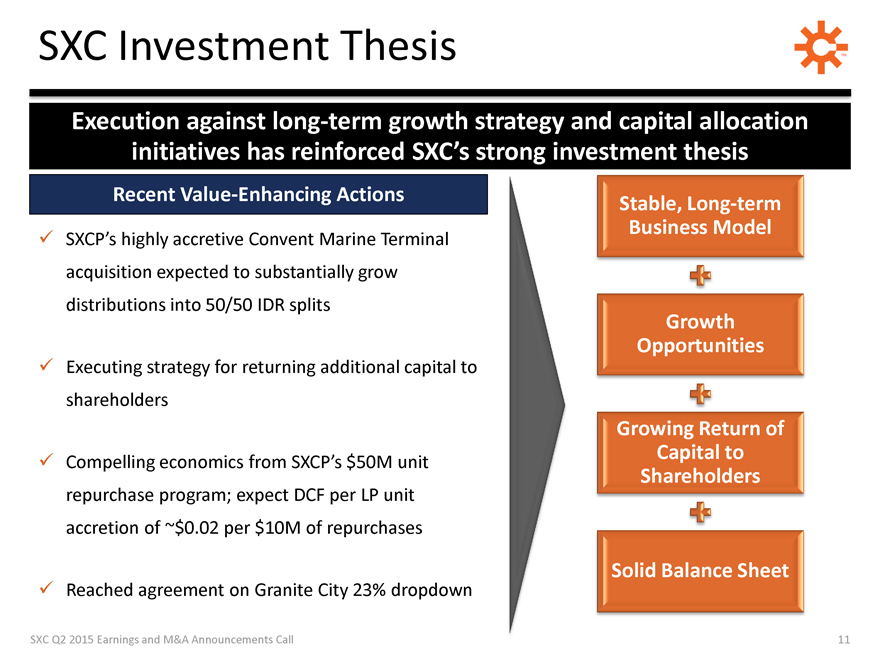

SXC Investment Thesis

Execution against long-term growth strategy and capital allocation initiatives has reinforced SXC’s strong investment thesis

Recent Value-Enhancing Actions

SXCP’s highly accretive Convent Marine Terminal

acquisition expected to substantially grow distributions into 50/50 IDR splits

Executing strategy for returning additional capital to shareholders

Compelling economics from SXCP’s $50M unit repurchase program; expect DCF per LP unit accretion of ~$0.02 per $10M of repurchases

Reached agreement on Granite City 23% dropdown

Stable, Long-term Business Model

Growth Opportunities

Growing Return of Capital to Shareholders

Solid Balance Sheet

SXC Q2 2015 Earnings and M&A Announcements Call 11

QUESTIONS

SunCoke

Energy™

SXC Q2 2015 Earnings and M&A Announcements Call

12

Investor Relations

630-824-1907 www.suncoke.com

SunCoke Energy™

APPENDIX

SunCoke

Energy™

SXC Q2 2015 Earnings and M&A Announcements Call 14

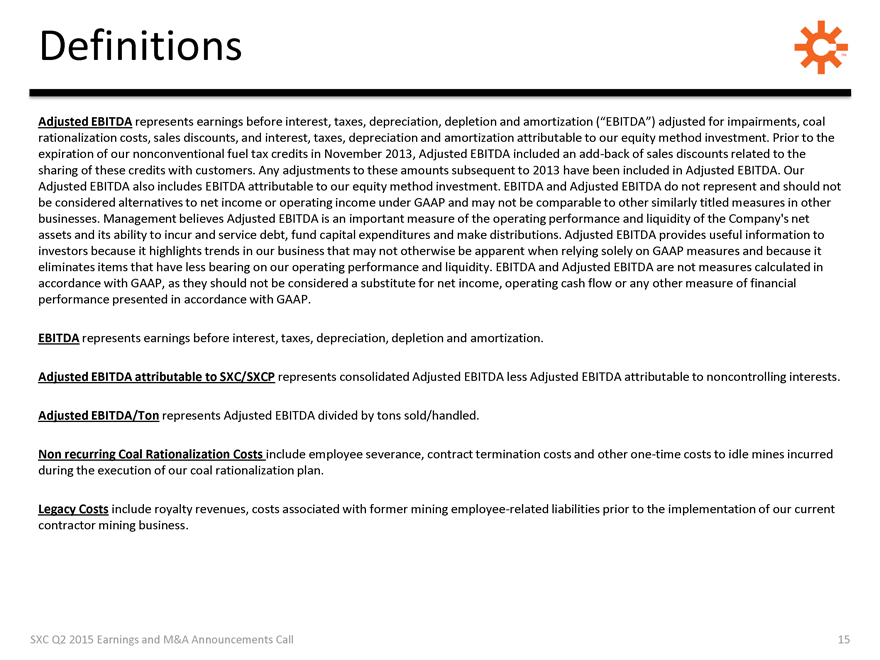

Definitions

Adjusted

EBITDA represents earnings before interest, taxes, depreciation, depletion and amortization (“EBITDA”) adjusted for impairments, coal rationalization costs, sales discounts, and interest, taxes, depreciation and amortization attributable

to our equity method investment. Prior to the expiration of our nonconventional fuel tax credits in November 2013, Adjusted EBITDA included an add-back of sales discounts related to the sharing of these credits with customers. Any adjustments to

these amounts subsequent to 2013 have been included in Adjusted EBITDA. Our Adjusted EBITDA also includes EBITDA attributable to our equity method investment. EBITDA and Adjusted EBITDA do not represent and should not be considered alternatives to

net income or operating income under GAAP and may not be comparable to other similarly titled measures in other businesses. Management believes Adjusted EBITDA is an important measure of the operating performance and liquidity of the Company’s

net assets and its ability to incur and service debt, fund capital expenditures and make distributions. Adjusted EBITDA provides useful information to investors because it highlights trends in our business that may not otherwise be apparent when

relying solely on GAAP measures and because it eliminates items that have less bearing on our operating performance and liquidity. EBITDA and Adjusted EBITDA are not measures calculated in accordance with GAAP, as they should not be considered a

substitute for net income, operating cash flow or any other measure of financial performance presented in accordance with GAAP.

EBITDA represents earnings before

interest, taxes, depreciation, depletion and amortization.

Adjusted EBITDA attributable to SXC/SXCP represents consolidated Adjusted EBITDA less Adjusted EBITDA

attributable to noncontrolling interests.

Adjusted EBITDA/Ton represents Adjusted EBITDA divided by tons sold/handled.

Non recurring Coal Rationalization Costs include employee severance, contract termination costs and other one-time costs to idle mines incurred during the execution of our coal

rationalization plan.

Legacy Costs include royalty revenues, costs associated with former mining employee-related liabilities prior to the implementation of our

current contractor mining business.

SXC Q2 2015 Earnings and M&A Announcements Call 15

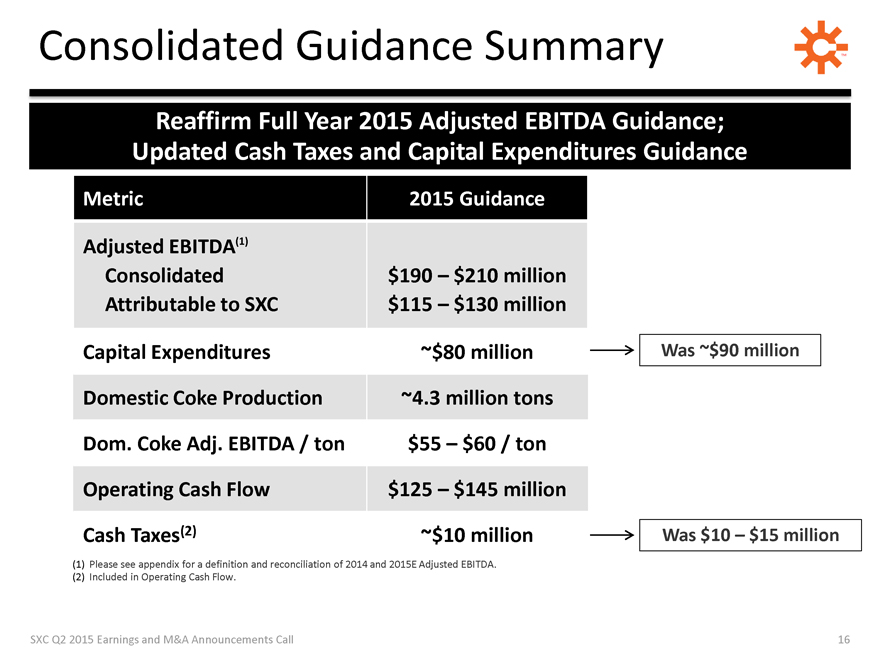

Consolidated Guidance Summary

Reaffirm Full Year 2015 Adjusted EBITDA Guidance; Updated Cash Taxes and Capital Expenditures Guidance

Metric

2015 Guidance

Adjusted EBITDA(1)

Consolidated

$190 – $210 million

Attributable to SXC

$115 – $130 million

Capital Expenditures

~$80 million

Was ~$90 million

Domestic Coke Production

~4.3 million tons

Dom. Coke Adj. EBITDA / ton

$55 – $60 / ton

Operating Cash Flow

$125 – $145 million

Cash Taxes(2)

~$10 million

Was $10 – $15 million

(1) Please see appendix for a definition and reconciliation of 2014

and 2015E Adjusted EBITDA.

(2) Included in Operating Cash Flow.

SXC Q2 2015

Earnings and M&A Announcements Call

16

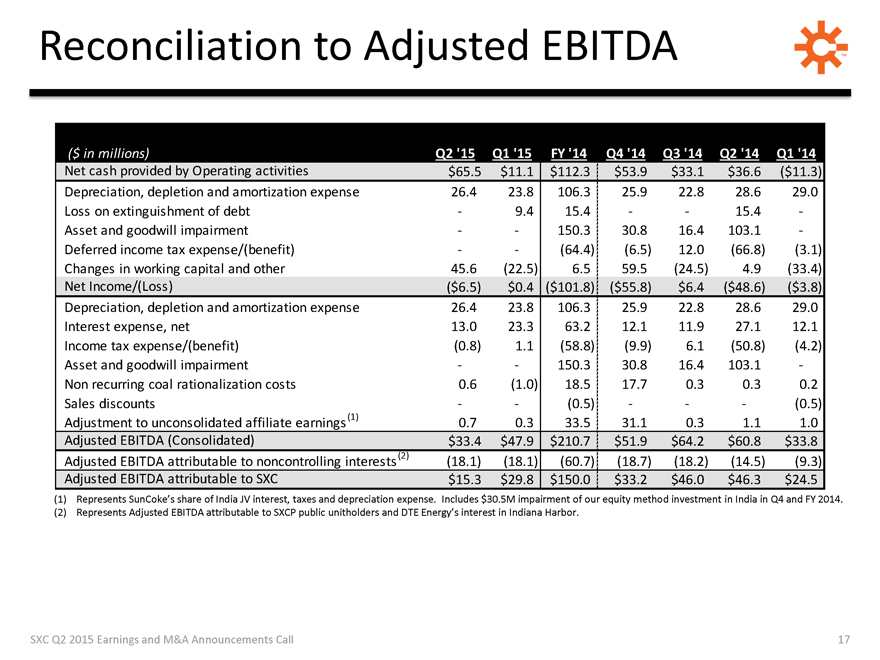

Reconciliation to Adjusted EBITDA

($ in millions)

Q2 ‘15 Q1 ‘15 FY ‘14 Q4 ‘14 Q3 ‘14 Q2 ‘14 Q1

‘14

Net cash provided by Operating activities

$65.5 $11.1 $112.3 $53.9

$33.1 $36.6 ($11.3)

Depreciation, depletion and amortization expense

26.4

23.8 106.3 25.9 22.8 28.6 29.0

Loss on extinguishment of debt

- 9.4 15.4 - -

15.4 -

Asset and goodwill impairment

- - 150.3 30.8 16.4 103.1 -

Deferred income tax expense/(benefit)

- - (64.4) (6.5) 12.0 (66.8) (3.1)

Changes in working capital and other

45.6 (22.5) 6.5 59.5 (24.5) 4.9 (33.4)

Net Income/(Loss)

($6.5) $0.4 ($101.8) ($55.8) $6.4 ($48.6) ($3.8)

Depreciation, depletion and amortization expense

26.4 23.8 106.3 25.9 22.8 28.6 29.0

Interest expense, net

13.0 23.3 63.2 12.1 11.9 27.1 12.1

Income tax expense/(benefit)

(0.8) 1.1 (58.8) (9.9) 6.1 (50.8) (4.2)

Asset and goodwill impairment

- - 150.3 30.8 16.4 103.1 -

Non recurring coal rationalization costs

0.6 (1.0) 18.5 17.7 0.3 0.3 0.2

Sales discounts

- - (0.5) - - - (0.5)

Adjustment to unconsolidated affiliate earnings (1)

0.7 0.3 33.5 31.1 0.3 1.1 1.0

Adjusted EBITDA (Consolidated)

$33.4 $47.9 $210.7 $51.9 $64.2 $60.8 $33.8

Adjusted EBITDA attributable to noncontrolling interests (2)

(18.1) (18.1) (60.7) (18.7)

(18.2) (14.5) (9.3)

Adjusted EBITDA attributable to SXC

$15.3 $29.8 $150.0

$33.2 $46.0 $46.3 $24.5

(1) Represents SunCoke’s share of India JV interest, taxes and depreciation expense. Includes $30.5M impairment of our equity method

investment in India in Q4 and FY 2014.

(2) Represents Adjusted EBITDA attributable to SXCP public unitholders and DTE Energy’s interest in Indiana Harbor.

SXC Q2 2015 Earnings and M&A Announcements Call

17

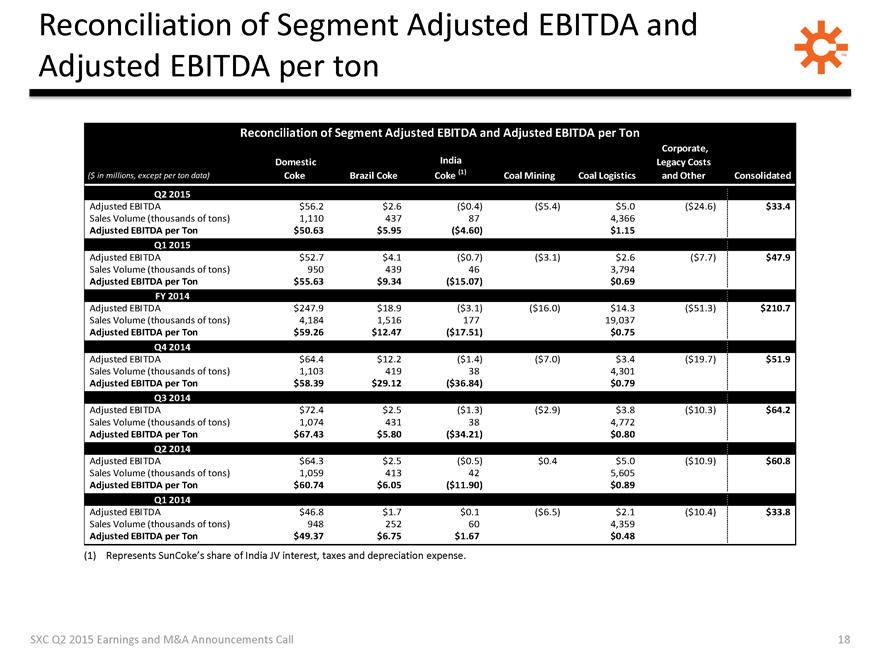

Reconciliation of Segment Adjusted EBITDA and Adjusted EBITDA per ton

Reconciliation of Segment Adjusted EBITDA and Adjusted EBITDA per Ton

($ in millions, except

per ton data)

Domestic Coke

Brazil Coke

India Coke (1)

Coal Mining

Coal Logistics

Corporate, Legacy Costs and Other

Consolidated

Q2 2015

Adjusted EBITDA

$56.2 $2.6 ($0.4) ($5.4) $5.0 ($24.6) $33.4

Sales Volume (thousands of tons)

1,110 437 87 4,366

Adjusted EBITDA per Ton

$50.63 $5.95 ($4.60) $1.15

Q1 2015

Adjusted EBITDA

$52.7 $4.1 ($0.7) ($3.1) $2.6 ($7.7) $47.9

Sales Volume (thousands of tons)

950 439 46 3,794

Adjusted EBITDA per Ton

$55.63 $9.34 ($15.07) $0.69

FY 2014

Adjusted EBITDA

$247.9 $18.9 ($3.1) ($16.0) $14.3 ($51.3) $210.7

Sales Volume (thousands of tons)

4,184 1,516 177 19,037

Adjusted EBITDA per Ton

$59.26 $12.47 ($17.51) $0.75

Q4 2014

Adjusted EBITDA

$64.4 $12.2 ($1.4) ($7.0) $3.4 ($19.7) $51.9

Sales Volume (thousands of tons)

1,103 419 38 4,301

Adjusted EBITDA per Ton

$58.39 $29.12 ($36.84) $0.79

Q3 2014

Adjusted EBITDA

$72.4 $2.5 ($1.3) ($2.9) $3.8 ($10.3) $64.2

Sales Volume (thousands of tons)

1,074 431 38 4,772

Adjusted EBITDA per Ton

$67.43 $5.80 ($34.21) $0.80

Q2 2014

Adjusted EBITDA

$64.3 $2.5 ($0.5) $0.4 $5.0 ($10.9) $60.8

Sales Volume (thousands of tons)

1,059 413 42 5,605

Adjusted EBITDA per Ton

$60.74 $6.05 ($11.90) $0.89

Q1 2014

Adjusted EBITDA

$46.8 $1.7 $0.1 ($6.5) $2.1 ($10.4) $33.8

Sales Volume (thousands of tons)

948 252 60 4,359

Adjusted EBITDA per Ton

$49.37 $6.75 $1.67 $0.48

(1) Represents SunCoke’s share of India JV interest, taxes and depreciation expense.

SXC

Q2 2015 Earnings and M&A Announcements Call

18

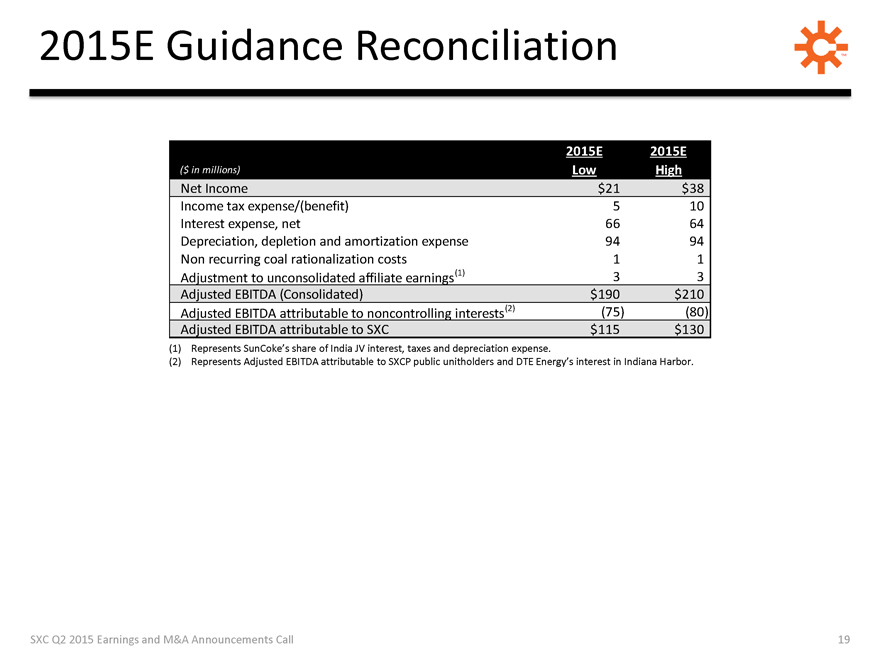

2015E Guidance Reconciliation

2015E

2015E

($ in millions)

Low

High

Net Income

$21

$38

Income tax expense/(benefit)

5

10

Interest expense, net

66

64

Depreciation, depletion and amortization expense

94

94

Non recurring coal rationalization costs

1

1

Adjustment to unconsolidated affiliate earnings(1)

3

3

Adjusted EBITDA (Consolidated)

$190

$210

Adjusted EBITDA attributable to noncontrolling interests(2)

(75)

(80)

Adjusted EBITDA attributable to SXC

$115

$130

(1) Represents SunCoke’s share of India JV interest, taxes and depreciation expense.

(2) Represents Adjusted EBITDA attributable to SXCP public unitholders and DTE Energy’s interest in Indiana Harbor.

SXC Q2 2015 Earnings and M&A Announcements Call

19

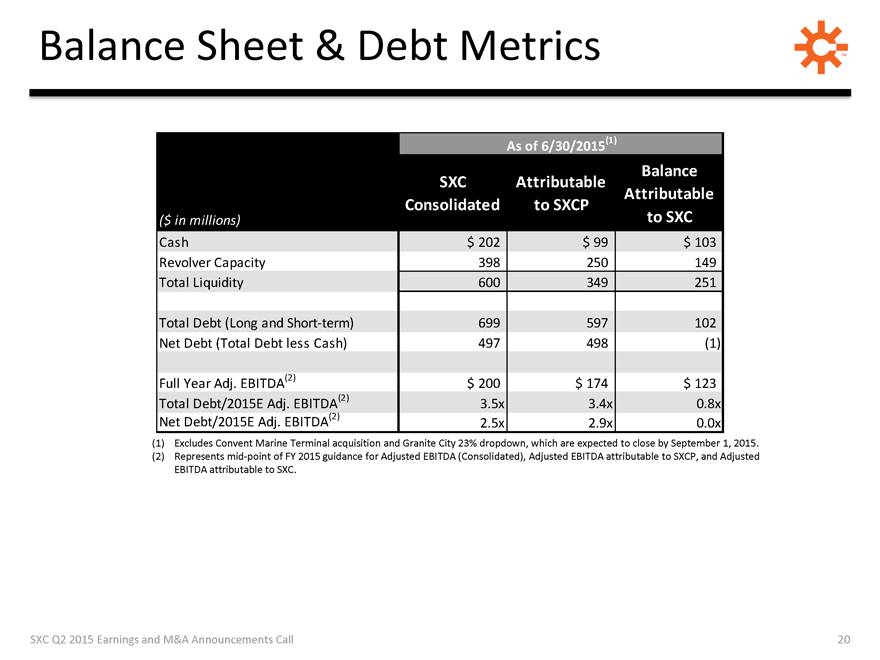

Balance Sheet & Debt Metrics

As of 6/30/2015(1)

($ in millions)

SXC Consolidated

Attributable to SXCP

Balance Attributable to SXC

Cash

$ 202

$ 99

$ 103

Revolver Capacity

398

250

149

Total Liquidity

600

349

251

Total Debt (Long and Short-term)

699

597

102

Net Debt (Total Debt less Cash)

497

498

(1)

Full Year Adj. EBITDA(2)

$ 200

$ 174

$ 123

Total Debt/2015E Adj. EBITDA(2)

3.5x

3.4x

0.8x

Net Debt/2015E Adj. EBITDA(2)

2.5x

2.9x

0.0x

(1) Excludes Convent Marine Terminal acquisition and Granite City 23%

dropdown, which are expected to close by September 1, 2015.

(2) Represents mid-point of FY 2015 guidance for Adjusted EBITDA (Consolidated), Adjusted EBITDA

attributable to SXCP, and Adjusted EBITDA attributable to SXC.

SXC Q2 2015 Earnings and M&A Announcements Call

20

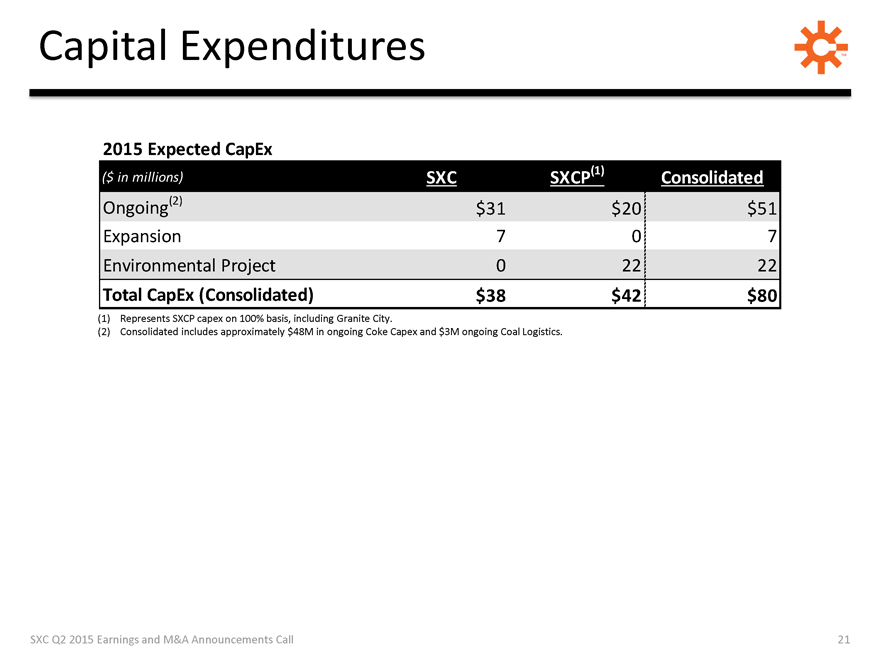

Capital Expenditures

2015

Expected CapEx

($ in millions)

SXC

SXCP(1)

Consolidated

Ongoing(2)

$31

$20

$51

Expansion

7

0

7

Environmental Project

0

22

22

Total CapEx (Consolidated)

$38

$42

$80

(1) Represents SXCP capex on 100% basis, including Granite City.

(2)

Consolidated includes approximately $48M in ongoing Coke Capex and $3M ongoing Coal Logistics.

SXC Q2 2015 Earnings and M&A Announcements Call

21