Attached files

| file | filename |

|---|---|

| EX-99.1 - EARNINGS RELEASE - OMNICOM GROUP INC. | e65188ex99-1.htm |

| 8-K - CURRENT REPORT - OMNICOM GROUP INC. | e65188_8k.htm |

Exhibit 99.2

Second Quarter 2015 Results July 21, 2015 Investor Presentation

2015 vs. 2014 P&L Summary – Second Quarter 1 (a) EBITA is a non - GAAP financial measure. See page 29 for the definition of this measure and page 24 for the reconciliation of non - GAAP measures. 2015 Reported 2014 Reported Revenue $ 3,805.3 $ 3,870.9 EBITA (a) 565.7 574.2 Margin % 14.9% 14.8% Amortization of Intangibles 27.1 25.8 Operating Income $ 538.6 $ 548.4 Margin % 14.2% 14.2% Second Quarter July 21, 2015

2015 vs. 2014 P&L Summary – Second Quarter 2 2015 Reported 2014 Reported 2014 Exclude Tax Benefit (a) Operating Income $ 538.6 $ 548.4 $ 548.4 Net Interest Expense 34.6 33.7 33.7 Income Taxes 165.3 160.3 171.5 (b) Tax Rate % 32.8% 31.1% 33.3% (b) Income from Equity Method Investments 4.0 4.0 4.0 Noncontrolling Interests 28.8 33.2 33.2 Net Income - Omnicom Group 313.9 325.2 314.0 Second Quarter (a) 2014 “Exclude Tax Benefit ”: Income Taxes and Tax Rate % amounts in this column are non - GAAP financial measures. See the 2014 “Reported” amounts on this page for the GAAP presentation and page 25 for the reconciliation of non - GAAP measures and footnote definitions . (b) Income Taxes and Tax Rate % amounts for the 3 months ended June 30, 2014 exclude the recognition of an income tax benefit of approximately $11 million related to expenses incurred in prior periods in connection with the proposed merger with Publicis Groupe S.A. (“ Publicis ”), which was terminated on May 8, 2014. Prior to the termination of the merger, the majority of the merger costs, which were incurred in 2013, were capitalized for income tax purposes and the related tax benefits were not recorded. Because the merger was terminated, t he merger costs were no longer required to be capitalized for income tax purposes. July 21, 2015

2015 vs. 2014 Earnings Per Share – Second Quarter 3 (a) 2014 “Exclude Tax Benefit ”: Net Income – Omnicom Group, Net Income available for common shares and EPS – Diluted amounts in this column are non - GAAP financial measures. See the 2014 “Reported” amounts on this page for the GAAP presentation and page 25 for the reconciliation of non - GAAP measures and footnote d efinitions. (b) Net Income – Omnicom Group, Net income available for common shares and EPS – Diluted figures for the 3 months ended June 30, 2014 exclude the net impact of the recognition of an income tax benefit of approximately $11 million as previously described on page 2. 2015 Reported 2014 Reported 2014 Exclude Tax Benefit (a) Net Income - Omnicom Group $ 313.9 $ 325.2 $ 314.0 (b) Net Income allocated to Participating Securities (3.9) (6.3) (6.1) Net Income available for common shares $ 310.0 $ 318.9 $ 307.9 (b) Diluted Shares (millions) 245.7 258.2 258.2 EPS - Diluted $ 1.26 $ 1.23 $ 1.19 (b) Dividend Declared per Share $ 0.50 $ 0.50 $ 0.50 Second Quarter July 21, 2015

2015 vs. 2014 P&L Summary – Year to Date 4 (a) EBITA is a non - GAAP financial measure. See page 29 for the definition of this measure and page 24 for the reconciliation of non - GAAP measures. 2015 Reported 2014 Reported Revenue $ 7,274.5 $ 7,373.0 EBITA (a) 970.8 981.3 Margin % 13.3% 13.3% Amortization of Intangibles 54.5 50.2 Operating Income $ 916.3 $ 931.1 Margin % 12.6% 12.6% Year to Date July 21, 2015

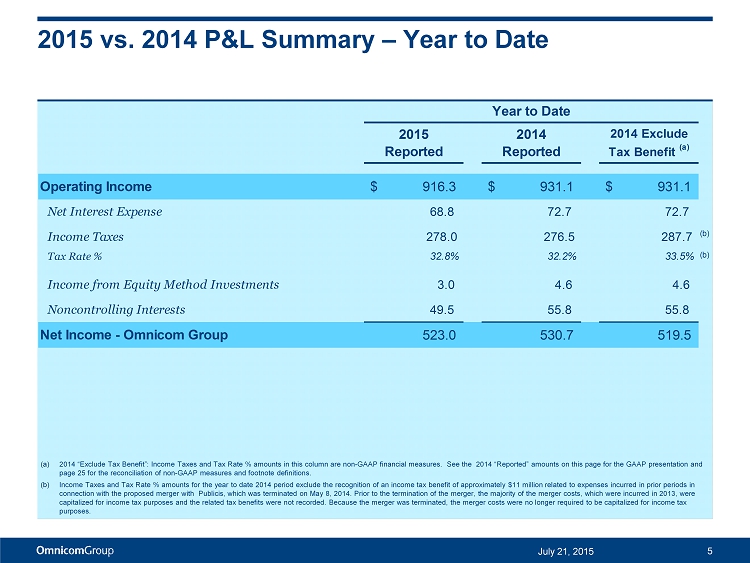

2015 vs. 2014 P&L Summary – Year to Date 5 2015 Reported 2014 Reported 2014 Exclude Tax Benefit (a) Operating Income $ 916.3 $ 931.1 $ 931.1 Net Interest Expense 68.8 72.7 72.7 Income Taxes 278.0 276.5 287.7 (b) Tax Rate % 32.8% 32.2% 33.5% (b) Income from Equity Method Investments 3.0 4.6 4.6 Noncontrolling Interests 49.5 55.8 55.8 Net Income - Omnicom Group 523.0 530.7 519.5 Year to Date (a) 2014 “Exclude Tax Benefit ”: Income Taxes and Tax Rate % amounts in this column are non - GAAP financial measures. See the 2014 “Reported” amounts on this pa ge for the GAAP presentation and page 25 for the reconciliation of non - GAAP measures and footnote definitions. (b) Income Taxes and Tax Rate % amounts for the year to date 2014 period exclude the recognition of an income tax benefit of approximately $11 million related to expenses incurred in prior periods in connection with the proposed merger with Publicis , which was terminated on May 8, 2014. Prior to the termination of the merger, the majority of the merger costs, which were inc urr ed in 2013, were capitalized for income tax purposes and the related tax benefits were not recorded. Because the merger was terminated, the me rge r costs were no longer required to be capitalized for income tax purposes. July 21, 2015

2015 vs. 2014 Earnings Per Share – Year to Date 6 2015 Reported 2014 Reported 2014 Exclude Tax Benefit (a) Net Income - Omnicom Group $ 523.0 $ 530.7 $ 519.5 (b) Net Income allocated to Participating Securities (6.7) (10.4) (10.2) Net Income available for common shares $ 516.3 $ 520.3 $ 509.3 (b) Diluted Shares (millions) 246.6 259.8 259.8 EPS - Diluted $ 2.09 $ 2.00 $ 1.96 (b) Dividend Declared per Share $ 1.00 $ 0.90 $ 0.90 Year to Date (a) 2014 “Exclude Tax Benefit ”: Net Income – Omnicom Group, Net Income available for common shares and EPS – Diluted amounts in this column are non - GAAP financi al measures. See the 2014 “Reported” amounts on this page for the GAAP presentation and page 25 for the reconciliation of non - GAAP measures and footnote d efinitions. (b) Net Income – Omnicom Group, Net income available for common shares and EPS – Diluted figures for the year to date 2014 period exclude the net impact of the recognition of an income tax benefit of approximately $11 million as previously described on page 5. July 21, 2015

2015 Total Revenue Change – Second Quarter 7 July 21, 2015 (a) To calculate the FX impact, we first convert the current period’s local currency revenue using the average exchange rates fro m t he equivalent prior period to arrive at constant currency revenue. The FX impact equals the difference between the current period revenue in U.S. dollars and the current period revenue in constant cu rrency. (b) Net acquisitions revenue is the aggregate of the applicable prior period revenue of the acquired businesses. Netted against thi s number is the revenue of any business included in the prior period reported revenue that was disposed of subsequent to the prior period. (c) Organic revenue is calculated by subtracting both the net acquisitions revenue and the FX impact from total revenue growth. 2Q '14 FX Impact Net Acquisitions Organic Revenue 2Q '15 $3,871 $3,805 $(275) $5 $204 (b) (c) (7.1)% 0.1% 5.3% (a)

2015 Total Revenue Change – Year to Date 8 July 21, 2015 (a) To calculate the FX impact, we first convert the current period’s local currency revenue using the average exchange rates fro m t he equivalent prior period to arrive at constant currency revenue. The FX impact equals the difference between the current period revenue in U.S. dollars and the current period revenue in constant cu rrency. (b) Net acquisitions revenue is the aggregate of the applicable prior period revenue of the acquired businesses. Netted against thi s number is the revenue of any business included in the prior period reported revenue that was disposed of subsequent to the prior period. (c) Organic revenue is calculated by subtracting both the net acquisitions revenue and the FX impact from total revenue growth. YTD '14 FX Impact Net Acquisitions Organic Revenue YTD '15 $7,373 $7,275 $(500) $19 $383 (b) (c) (6.8)% 0.3% 5.2% (a)

2015 Revenue by Region July 21, 2015 9 Second Quarter North America 59.9% UK 9.8% Euro Markets & Other Europe 15.9 % Asia Pacific 10.4% Latin America 2.2% Africa MidEast 1.8% Year to Date North America 59.8% UK 9.9% Euro Markets & Other Europe 16.0 % Asia Pacific 10.3% Latin America 2.3% Africa MidEast 1.7%

2015 Revenue by Region 10 Second Quarter Year to Date July 21, 2015 $ Mix % Growth % Organic Growth (a) North America 2,281.5$ 4.6% 5.9% UK 372.0 -3.0% 5.4% Euro & Other Europe 606.8 -16.6% 3.9% Asia Pacific 394.5 -1.8% 7.6% Latin America 82.6 -27.8% -9.6% Africa Mid East 67.9 7.6% 11.9% $ Mix % Growth % Organic Growth (a) North America 4,348.6$ 4.3% 5.4% UK 718.6 -0.5% 7.2% Euro & Other Europe 1,161.6 -16.7% 3.3% Asia Pacific 751.3 -1.3% 7.2% Latin America 166.4 -19.6% -3.7% Africa Mid East 128.0 7.7% 11.3% (a) “Organic Growth” reflects the year - over - year increase or decrease in revenue from the prior period, excluding the FX Impact and Net Acquisitions revenue, as defined on page 7.

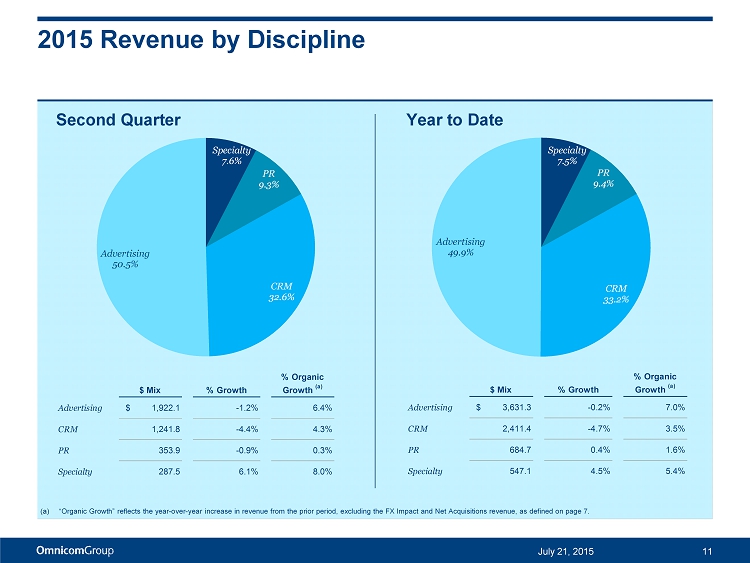

2015 Revenue by Discipline July 21, 2015 11 Second Quarter Specialty 7.6% PR 9.3% CRM 32.6% Advertising 50.5% Specialty 7.5% PR 9.4% CRM 33.2% Advertising 49.9% $ Mix % Growth % Organic Growth (a) Advertising $ 1,922.1 -1.2% 6.4% CRM 1,241.8 -4.4% 4.3% PR 353.9 -0.9% 0.3% Specialty 287.5 6.1% 8.0% $ Mix % Growth % Organic Growth (a) Advertising $ 3,631.3 -0.2% 7.0% CRM 2,411.4 -4.7% 3.5% PR 684.7 0.4% 1.6% Specialty 547.1 4.5% 5.4% (a) “Organic Growth” reflects the year - over - year increase in revenue from the prior period, excluding the FX Impact and Net Acquisitions revenue, as defined on page 7. Year to Date

Revenue by Industry July 21, 2015 12 Auto 8% Consumer Products 9% Financial Services 7% Food & Beverage 13% Other 25% Pharma & Health 11% Retail 7% Tech 9% Telcom 5% T&E 6% Auto 8% Consumer Products 9% Financial Services 7% Food & Beverage 13% Other 26% Pharma & Health 10% Retail 7% Tech 9% Telcom 5% T&E 6% Year to Date – 2015 Year to Date – 2014

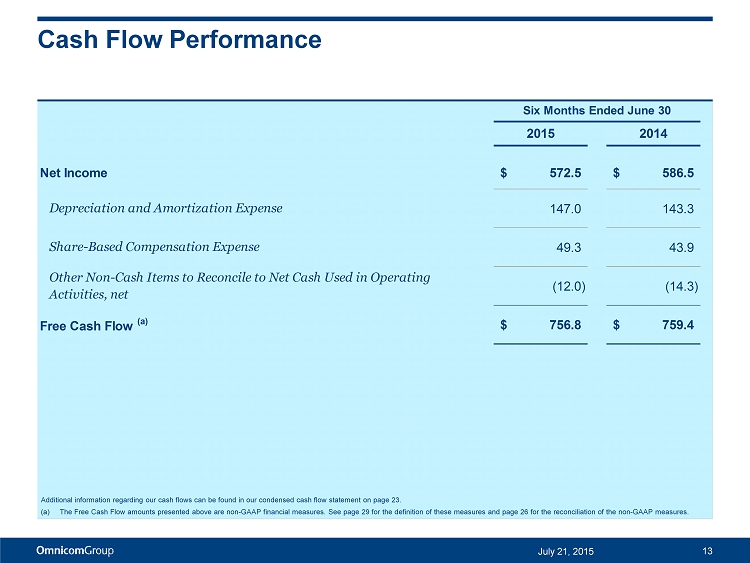

Cash Flow Performance 13 July 21, 2015 2015 2014 Net Income 572.5$ 586.5$ Depreciation and Amortization Expense 147.0 143.3 Share-Based Compensation Expense 49.3 43.9 Other Non-Cash Items to Reconcile to Net Cash Used in Operating Activities, net (12.0) (14.3) Free Cash Flow (a) 756.8$ 759.4$ Six Months Ended June 30 Additional information regarding our cash flows can be found in our condensed cash flow statement on page 23. (a) The Free Cash Flow amounts presented above are non - GAAP financial measures. See page 29 for the definition of these measures and page 26 for the reconciliation of the non - GAAP measures.

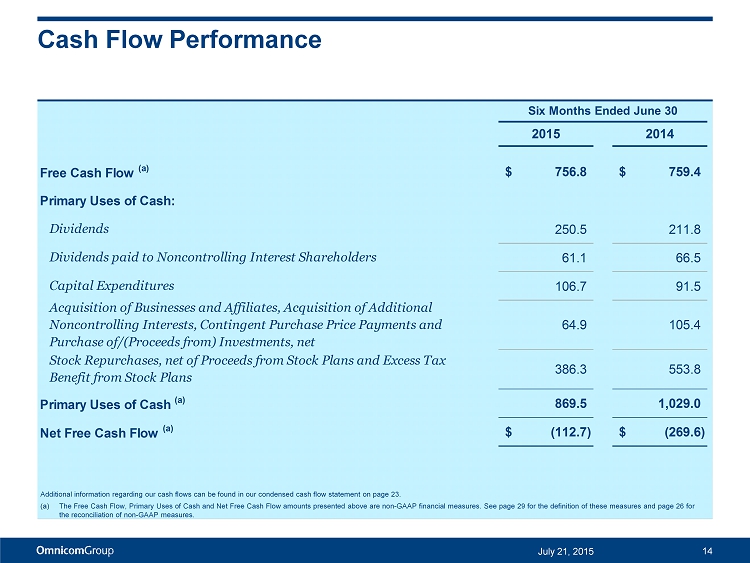

Cash Flow Performance 14 July 21, 2015 2015 2014 Free Cash Flow (a) 756.8$ 759.4$ Primary Uses of Cash: Dividends 250.5 211.8 Dividends paid to Noncontrolling Interest Shareholders 61.1 66.5 Capital Expenditures 106.7 91.5 Acquisition of Businesses and Affiliates, Acquisition of Additional Noncontrolling Interests, Contingent Purchase Price Payments and Purchase of/(Proceeds from) Investments, net 64.9 105.4 Stock Repurchases, net of Proceeds from Stock Plans and Excess Tax Benefit from Stock Plans 386.3 553.8 Primary Uses of Cash (a) 869.5 1,029.0 Net Free Cash Flow (a) (112.7)$ (269.6)$ Six Months Ended June 30 Additional information regarding our cash flows can be found in our condensed cash flow statement on page 23. (a) The Free Cash Flow, Primary Uses of Cash and Net Free Cash Flow amounts presented above are non - GAAP financial measures. See pag e 29 for the definition of these measures and page 26 for the reconciliation of non - GAAP measures.

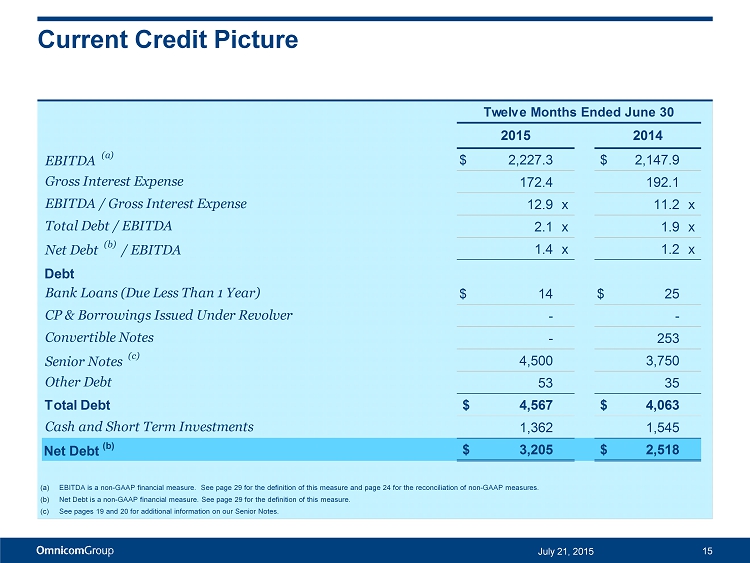

Current Credit Picture 15 July 21, 2015 (a) EBITDA is a non - GAAP financial measure. See page 29 for the definition of this measure and page 24 for the reconciliation of no n - GAAP measures. (b) Net Debt is a non - GAAP financial measure. See page 29 for the definition of this measure. (c) See pages 19 and 20 for additional information on our Senior Notes. 2015 2014 EBITDA (a) $ 2,227.3 $ 2,147.9 Gross Interest Expense 172.4 192.1 EBITDA / Gross Interest Expense 12.9 x 11.2 x Total Debt / EBITDA 2.1 x 1.9 x Net Debt (b) / EBITDA 1.4 x 1.2 x Debt Bank Loans (Due Less Than 1 Year) $ 14 $ 25 CP & Borrowings Issued Under Revolver - - Convertible Notes - 253 Senior Notes (c) 4,500 3,750 Other Debt 53 35 Total Debt $ 4,567 $ 4,063 Cash and Short Term Investments 1,362 1,545 Net Debt (b) $ 3,205 $ 2,518 Twelve Months Ended June 30

Historical Returns 16 July 21, 2015 Return on Invested Capital (ROIC) (a) : Twelve Months Ended June 30, 2015 17.6% Twelve Months Ended June 30, 2014 16.9% Return on Equity (b) : 15 Twelve Months Ended June 30, 2015 35.9% Twelve Months Ended June 30, 2014 31.5% (a) Return on Invested Capital is After Tax Reported Operating Income (a non - GAAP measure – see page 29 for the definition of this m easure and page 26 for the reconciliation of non - GAAP measures) divided by the average of Invested Capital at the beginning and the end of the period (book value of all long - term liabilities and short - term interest bearing debt plus shareholders’ equity less cash, cash equivalents and short term investments). (b) Return on Equity is Reported Net Income for the given period divided by the average of shareholders’ equity at the beginning and end of the period.

Net Cash Returned to Shareholders through Dividends and Share Repurchases 17 July 21, 2015 0.5 0.7 0.9 1.1 1.3 1.6 2.0 2.3 2.8 3.0 2.1 2.9 3.7 3.6 4.8 5.6 6.5 7.0 8.0 8.4 $0.7 $1.5 $2.4 $3.3 $4.3 $5.1 $5.9 $6.9 $7.9 $8.9 $10.0 $10.5 76 % 92 % 110% 108% 105% 92 % 103 % 103% 107% 104% 108% 109% $ - $2.0 $4.0 $6.0 $8.0 $10.0 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD 2015 Cumulative Dividends Paid Cumulative Cost of Net Shares Repurchased - Payments for repurchases of common stock less proceeds from stock plans. Cumulative Net Income - Omnicom Group Inc. % of Cumulative Net Income Returned to Shareholders - Cumulative Dividends Paid plus Cumulative Cost of Net Shares Repurchased divided by Cumulative Net Income. From 2004 through June 30, 2015, Omnicom distributed over 100% of Net Income to shareholders through Dividends and Share Repurchases . $ In Billions

Supplemental Financial Information July 21, 2015 18

Omnicom Debt Structure Bank Loans $14 2024 Senior Notes $750 2022 Senior Notes $1,250 2020 Senior Notes $1,000 2019 Senior Notes $500 2016 Senior Notes $1,000 19 July 21, 2015 The above chart sets forth Omnicom’s debt outstanding at June 30, 2015. The amounts reflected above for the 2016, 2019, 2020, 2022 and 2024 Senior Notes represent the principal amount of these notes at maturity on April 15, 2016, July 15, 2019, August 15, 2020, May 1, 2022 and November 1, 2024, respectively.

Omnicom Debt Maturity Profile 20 July 21, 2015 Other borrowings at June 30, 2015 include short - term borrowings of $14 million which are due in less than one year. For purposes of this presentation we have included these borrowings as outstandi ng through July 31, 2019, the date of expiration of our five - year credit facility. $0 $250 $500 $750 $1,000 $1,250 2016 Senior Notes Other Borrowings 2019 Senior Notes 2022 Senior Notes 2020 Senior Notes 2024 Senior Notes

Historical Return Trends 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 LTM 6/30/15 July 21, 2015 21 (a) Return on Equity (“ROE”) is Reported Net Income for the given period divided by the average shareholders’ equity at the begin nin g and end of the period. (b) Return on Invested Capital (“ROIC”) is After Tax Reported Operating Income (a non - GAAP measure – see page 29 for the definition of this measure and page 26 for the reconciliation of non - GAAP measure for LTM 6/30/15) divided by the average of Invested Capital at the beginning and end of the period (book value of all long - term liabilities and short - term interest bearing debt plus shareholders’ equity less cash, cash equivalents and short term investments). Return on Equity Average through June 30, 2015 – 25.9% Return on Invested Capital Average through June 30, 2015 - 20.4% ROE (a) ROIC (b)

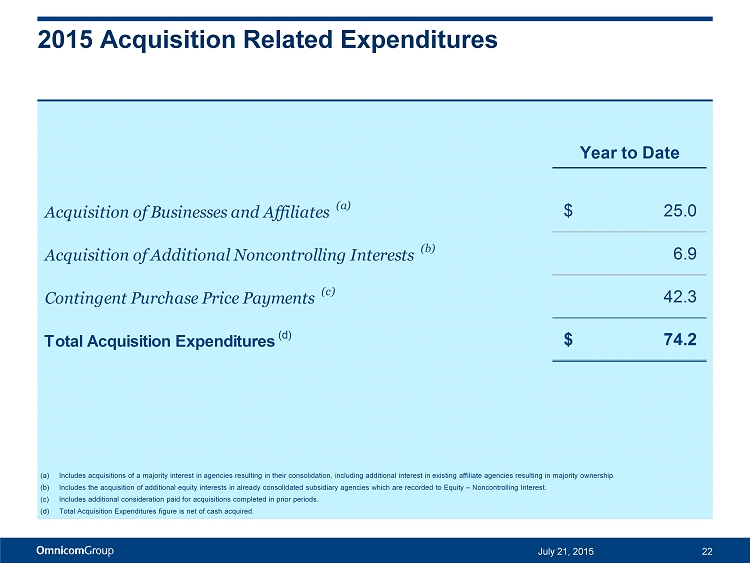

2015 Acquisition Related Expenditures 22 July 21, 2015 (a) Includes acquisitions of a majority interest in agencies resulting in their consolidation, including additional interest in e xis ting affiliate agencies resulting in majority ownership. (b) Includes the acquisition of additional equity interests in already consolidated subsidiary agencies which are recorded to Equ ity – Noncontrolling Interest. (c) Includes additional consideration paid for acquisitions completed in prior periods. (d) Total Acquisition Expenditures figure is net of cash acquired. Year to Date Acquisition of Businesses and Affiliates (a) 25.0$ Acquisition of Additional Noncontrolling Interests (b) 6.9 Contingent Purchase Price Payments (c) 42.3 Total Acquisition Expenditures (d) 74.2$

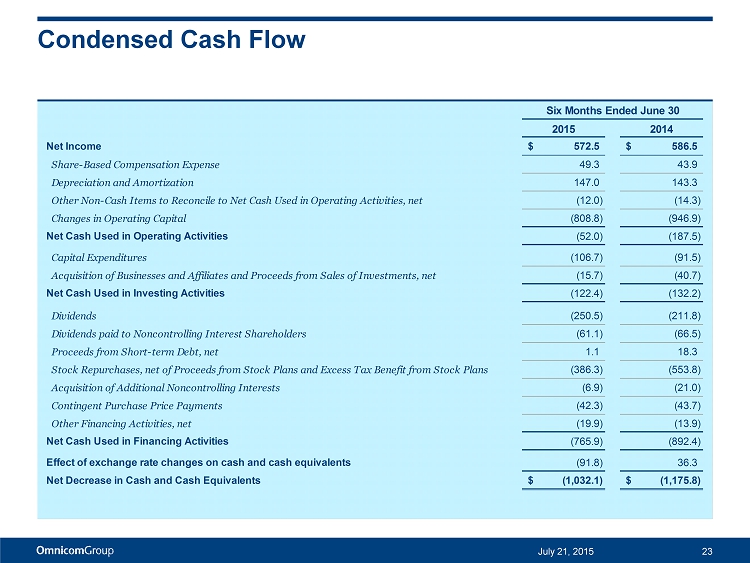

Condensed Cash Flow 23 July 21, 2015 2015 2014 Net Income 572.5$ 586.5$ Share-Based Compensation Expense 49.3 43.9 Depreciation and Amortization 147.0 143.3 Other Non-Cash Items to Reconcile to Net Cash Used in Operating Activities, net (12.0) (14.3) Changes in Operating Capital (808.8) (946.9) Net Cash Used in Operating Activities (52.0) (187.5) Capital Expenditures (106.7) (91.5) Acquisition of Businesses and Affiliates and Proceeds from Sales of Investments, net (15.7) (40.7) Net Cash Used in Investing Activities (122.4) (132.2) Dividends (250.5) (211.8) Dividends paid to Noncontrolling Interest Shareholders (61.1) (66.5) Proceeds from Short-term Debt, net 1.1 18.3 Stock Repurchases, net of Proceeds from Stock Plans and Excess Tax Benefit from Stock Plans (386.3) (553.8) Acquisition of Additional Noncontrolling Interests (6.9) (21.0) Contingent Purchase Price Payments (42.3) (43.7) Other Financing Activities, net (19.9) (13.9) Net Cash Used in Financing Activities (765.9) (892.4) Effect of exchange rate changes on cash and cash equivalents (91.8) 36.3 Net Decrease in Cash and Cash Equivalents (1,032.1)$ (1,175.8)$ Six Months Ended June 30

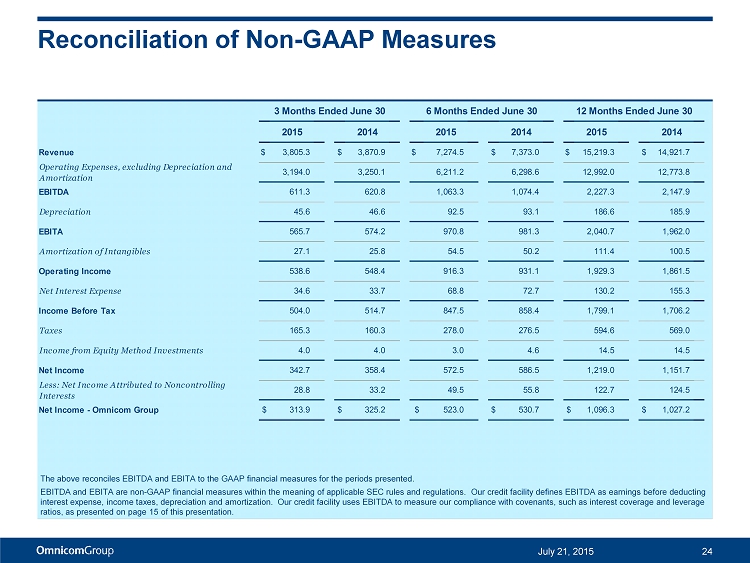

Reconciliation of Non - GAAP Measures 24 July 21, 2015 The above reconciles EBITDA and EBITA to the GAAP financial measures for the periods presented. EBITDA and EBITA are non - GAAP financial measures within the meaning of applicable SEC rules and regulations. Our credit facilit y defines EBITDA as earnings before deducting interest expense, income taxes, depreciation and amortization. Our credit facility uses EBITDA to measure our compliance wit h c ovenants, such as interest coverage and leverage ratios, as presented on page 15 of this presentation. 2015 2014 2015 2014 2015 2014 Revenue $ 3,805.3 $ 3,870.9 $ 7,274.5 $ 7,373.0 $ 15,219.3 $ 14,921.7 Operating Expenses, excluding Depreciation and Amortization 3,194.0 3,250.1 6,211.2 6,298.6 12,992.0 12,773.8 EBITDA 611.3 620.8 1,063.3 1,074.4 2,227.3 2,147.9 Depreciation 45.6 46.6 92.5 93.1 186.6 185.9 EBITA 565.7 574.2 970.8 981.3 2,040.7 1,962.0 Amortization of Intangibles 27.1 25.8 54.5 50.2 111.4 100.5 Operating Income 538.6 548.4 916.3 931.1 1,929.3 1,861.5 Net Interest Expense 34.6 33.7 68.8 72.7 130.2 155.3 Income Before Tax 504.0 514.7 847.5 858.4 1,799.1 1,706.2 Taxes 165.3 160.3 278.0 276.5 594.6 569.0 Income from Equity Method Investments 4.0 4.0 3.0 4.6 14.5 14.5 Net Income 342.7 358.4 572.5 586.5 1,219.0 1,151.7 Less: Net Income Attributed to Noncontrolling Interests 28.8 33.2 49.5 55.8 122.7 124.5 Net Income - Omnicom Group $ 313.9 $ 325.2 $ 523.0 $ 530.7 $ 1,096.3 $ 1,027.2 3 Months Ended June 30 12 Months Ended June 306 Months Ended June 30

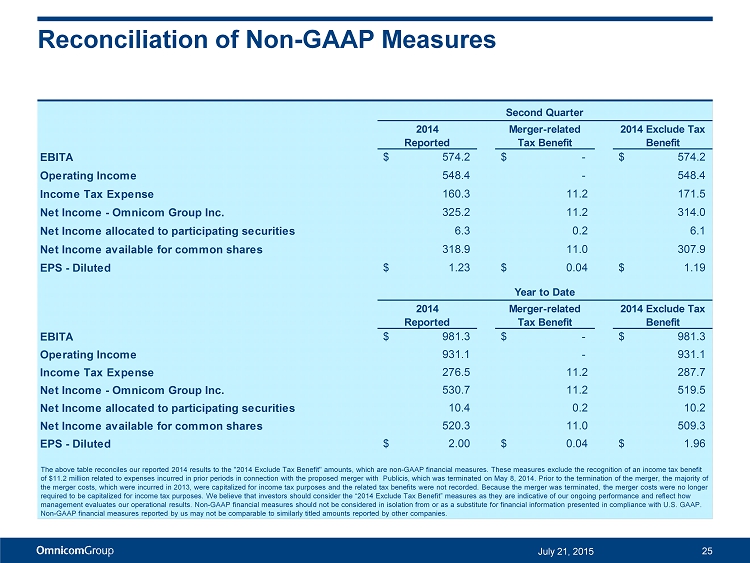

Reconciliation of Non - GAAP Measures 25 July 21, 2015 2014 Reported Merger-related Tax Benefit 2014 Exclude Tax Benefit EBITA $ 574.2 $ - $ 574.2 Operating Income 548.4 - 548.4 Income Tax Expense 160.3 11.2 171.5 Net Income - Omnicom Group Inc. 325.2 11.2 314.0 Net Income allocated to participating securities 6.3 0.2 6.1 Net Income available for common shares 318.9 11.0 307.9 EPS - Diluted $ 1.23 $ 0.04 $ 1.19 2014 Reported Merger-related Tax Benefit 2014 Exclude Tax Benefit EBITA $ 981.3 $ - $ 981.3 Operating Income 931.1 - 931.1 Income Tax Expense 276.5 11.2 287.7 Net Income - Omnicom Group Inc. 530.7 11.2 519.5 Net Income allocated to participating securities 10.4 0.2 10.2 Net Income available for common shares 520.3 11.0 509.3 EPS - Diluted $ 2.00 $ 0.04 $ 1.96 Second Quarter Year to Date The above table reconciles our reported 2014 results to the " 2014 Exclude Tax Benefit" amounts, which are non - GAAP financial measures. These measures exclude the recognition of an income tax benefit of $11.2 million related to expenses incurred in prior periods in connection with the proposed merger with Publicis , which was terminated on May 8, 2014. Prior to the termination of the merger, the majority of the merger costs, which were incurred in 2013, were capitalized for income tax purposes and the related tax benefits were not re corded. Because the merger was terminated, the merger costs were no longer required to be capitalized for income tax purposes. We believe that investors should consider the “2014 Exclude Tax Benefit” measures as they are indicative of our ongoing performance and reflect how management evaluates our operational results. Non - GAAP financial measures should not be considered in isolation from or as a sub stitute for financial information presented in compliance with U.S. GAAP. Non - GAAP financial measures reported by us may not be comparable to similarly titled amounts reported by other companies.

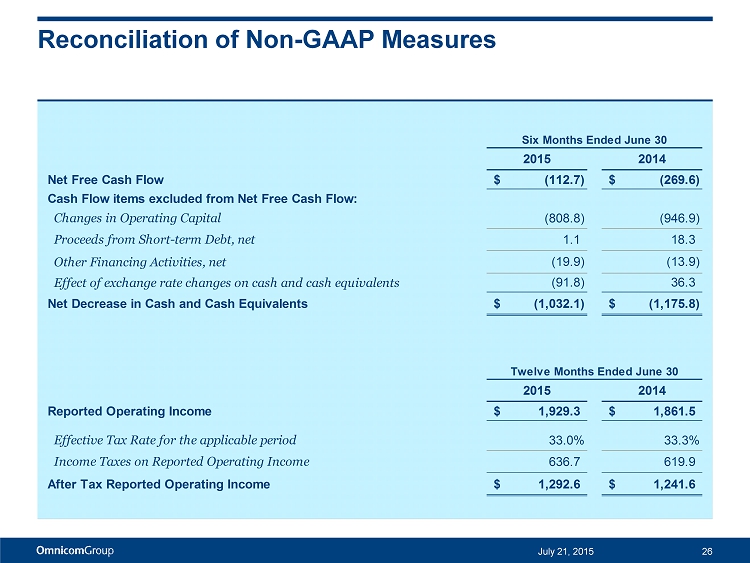

Reconciliation of Non - GAAP Measures July 21, 2015 26 2015 2014 Net Free Cash Flow (112.7)$ (269.6)$ Cash Flow items excluded from Net Free Cash Flow: Changes in Operating Capital (808.8) (946.9) Proceeds from Short-term Debt, net 1.1 18.3 Other Financing Activities, net (19.9) (13.9) Effect of exchange rate changes on cash and cash equivalents (91.8) 36.3 Net Decrease in Cash and Cash Equivalents (1,032.1)$ (1,175.8)$ Six Months Ended June 30 2015 2014 Reported Operating Income 1,929.3$ 1,861.5$ Effective Tax Rate for the applicable period 33.0% 33.3% Income Taxes on Reported Operating Income 636.7 619.9 After Tax Reported Operating Income 1,292.6$ 1,241.6$ Twelve Months Ended June 30

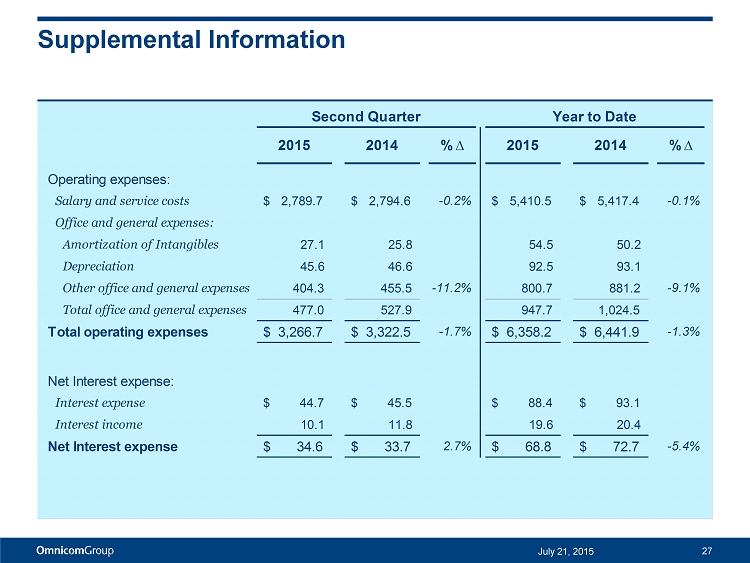

Supplemental Information 27 July 21, 2015 2015 2014 % ∆ 2015 2014 % ∆ Operating expenses: Salary and service costs $ 2,789.7 $ 2,794.6 -0.2% $ 5,410.5 $ 5,417.4 -0.1% Office and general expenses: Amortization of Intangibles 27.1 25.8 54.5 50.2 Depreciation 45.6 46.6 92.5 93.1 Other office and general expenses 404.3 455.5 -11.2% 800.7 881.2 -9.1% Total office and general expenses 477.0 527.9 947.7 1,024.5 Total operating expenses $ 3,266.7 $ 3,322.5 -1.7% $ 6,358.2 $ 6,441.9 -1.3% Net Interest expense: Interest expense $ 44.7 $ 45.5 $ 88.4 $ 93.1 Interest income 10.1 11.8 19.6 20.4 Net Interest expense $ 34.6 $ 33.7 2.7% $ 68.8 $ 72.7 -5.4% Second Quarter Year to Date

Second Quarter Acquisition July 21, 2015 28 Established in 2009 with a focus on search and web analytics, Semetis is a market leader in optimizing digital advertising campaigns (search, branding, RTB, mobile, social, local, remarketing ), utilizing analytics , digital business intelligence and custom technology. Semetis is located in Brussels, Belgium and will operate within the Omnicom Media Group network.

The preceding materials have been prepared for use in the July 21, 2015 conference call on Omnicom’s results of operations fo r t he period ended June 30, 2015. The call will be archived on the Internet at http://www.omnicomgroup.com/financialwebcasts. Forward - Looking Statements Certain statements in this presentation constitute forward - looking statements, including statements within the meaning of the Private Securities Litigation Reform Act of 1995. In addition, from time to time, the Company or its representatives have made, or may make, forward - looking statements, orally or in writing. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial condition, or otherwise, based on current beliefs of the Company’s management as well as assumptions made by, and information currently available to, the Company’s management. Forward - looking statements may be accompanied by words such as “aim,” “anticipate,” “believe,” “plan,” “could,” “wou ld,” “should,” “estimate,” “expect,” “forecast,” “future,” “guidance,” “intend,” “may,” “will,” “possible,” “potential,” “predict,” “project” or similar words, phrases or expressions. The se forward - looking statements are subject to various risks and uncertainties, many of which are outside the Company’s control. Therefore, you should not place undue reliance on such statements. Factors that could cause actual results to differ ma terially from those in the forward - looking statements include: international, national or local economic, social or political conditions that could adversely affect the Company or it s clients; losses on media purchases and production costs incurred on behalf of clients; reductions in client spending, a slowdown in client payments and changes in client advertising, marketing and corporate communications requirements; failure to manage potential conflicts of interest between or among clients; unanticipated changes relating to competitive factors in the advertising, marketing and corporate communications industries ; ability to hire and retain key personnel; ability to attract new clients and retain existing clients in the manner anticipated; reliance on information technology systems; changes in legislation or governmental regulations affecting the Company or its clients; conditions in the credit markets; risks associated with assumptions the Company makes in connection with its critical accounting estimates and legal proceedings; and the Company’s international operations, which are subject to the risks of currency fluctuation and currency repatriation restrictions. The foregoing list of factors is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties that may affect the Company’s business, including those described in the “Risk Factors” in Omnicom’s Annual Report on Form 10 - K for the year ended December 31, 2014. Except as required under applicable law, the Company does not assume any obligation to update these forward - looking statements . Non - GAAP Financial Measures We present financial measures determined in accordance with generally accepted accounting principles in the United States (“G AAP ”) and adjustments to the GAAP presentation (“Non - GAAP”), which we believe are meaningful for understanding our performance. Non - GAAP financial measures should not be considered in isolation f rom, or as a substitute for, financial information presented in compliance with GAAP. Non - GAAP financial measures as reported by us may not be comparable to similarly titled amounts reported b y other companies. We provide a reconciliation of non - GAAP measures to the comparable GAAP measures on pages 24, 25 and 26. The Non - GAAP measures used in this presentation include the following: 2014 Exclude Tax Benefit, which excludes the impact of the tax benefit related to expenses incurred in 2013 related to the proposed merger with Publicis . We believe that this presentation allows for a more meaningful understanding of our performance. Net Free Cash Flow, defined as Free Cash Flow (defined below) less the Primary Uses of Cash (defined below). Net Free Cash Fl ow is one of the metrics used by us to assess our sources and uses of cash and was derived from our consolidated statements of cash flows. We believe that this presentation is meaningful for unde rst anding our primary sources and primary uses of that cash flow. Free Cash Flow, defined as net income plus depreciation, amortization, share based compensation expense less other non - cash items to reconcile to net cash provided by operating activities. Primary Uses of Cash, defined as dividends to common shareholders, dividends paid to non - controlling interest shareholders, capital expenditures , cash paid on acquisitions, payments for additional interest in controlled subsidiaries and stock repurchases, net of the proceeds and excess tax benefit from our stock plans, and excludes changes in wor king capital and other investing and financing activities, including commercial paper issuances and redemptions used to fund working capital changes. EBITDA, defined as operating income before interest, taxes, depreciation and amortization. We believe EBITDA is meaningful be cau se the financial covenants in our credit facilities are based on EBITDA. EBITA, defined as operating income before interest, taxes and amortization. We use EBITA as an additional operating performan ce measure, which excludes acquisition - related amortization expense, because we believe that EBITA is a useful measure to evaluate the performance of our businesses. Net Debt, defined as total debt less cash, cash equivalents and short - term investments. We believe net debt, together with the c omparable GAAP measures, reflects one of the metrics used by us to assess our cash management. After Tax Reported Operating Income, defined as reported operating income less income taxes calculated using the effective ta x r ate for the applicable period. Other Information All dollar amounts are in millions except for per share amounts and figures shown on pages 3, 6 and 25 and the net cash retur ned to shareholders figures on page 17. The information contained in this document has not been audited, although some data has been derived from Omnicom’s historical financial statements, including its audited financial statements. In addition, industry, operational and other non - financial data contained in this document have been derived from sources that we believe to be reliable, but we have n ot independently verified such information, and we do not, nor does any other person, assume responsibility for the accuracy or completeness of that information. Certain amounts in prior periods ha ve been reclassified to conform to our current presentation. The inclusion of information in this presentation does not mean that such information is material or that disclosure of such inf ormation is required. Disclosure July 21, 2015 29