Attached files

| file | filename |

|---|---|

| EX-32 - GOLD LAKES CORP. | ex32.htm |

| EX-31 - GOLD LAKES CORP. | ex31.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES ACT OF 1934 |

For the fiscal year ended July 31, 2014

| [ ] | TRANSACTION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transaction period from ____________ to ____________

Commission File Number: 333-145879

TNX MAVERICK, CORP.

(Exact name of registrant as specified in charter)

| Nevada | 74-3207964 | |

| State

or other jurisdiction of incorporation or organization |

(I.R.S.

Employee I.D. No.) |

| 573 Monroe Blvd, Painesville, OH | 42077 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number 216-408-9423

Securities registered pursuant to Section 12(b) of the Act:

| Title of each share | Name of each exchange on which registered |

| None | None |

Securities registered pursuant to Section 12 (g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act [ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Act. [X] Yes [ ] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [ ] Yes [X] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [ ] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. See definition of “large accelerated filer”, “accelerated filer” and “small reporting company” Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [ ] (Do not check if a small reporting company) | Small reporting company | [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes [ ] No [X]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recent completed second fiscal quarter. On January 31, 2015, the market value of the 22,065,000 shares held by non-affiliates was $17,652.

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date:

July 14, 2015: 45,105,000 common shares Of these shares 22,065,000 are held by third parties. The market value of these shares is $63,989.

DOCUMENTS INCORPORATED BY REFERENCE

Listed hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; (3) Any prospectus filed pursuant to Rule 424 (b) or (c) under the Securities Act of 1933. The listed documents should be clearly described for identification purposes.

Contents

| 2 |

History and Organization

TNX Maverick, Corp. (“TNX”, the “company” or “we”) was incorporated in the State of Nevada on January 18, 2007, and established a fiscal year end of July 31. We do not have any subsidiaries or affiliated companies. On April 9, 2015, the Company has entered into a Letter of Intent with Flex Mining Ltd., whereby it will pay $10,000 within six months, and issue to Flex Mining Ltd. 1,800,000 shares of common stock of the Company, as compensation for entering into an earn-in agreement where, by making capital expenditure of up to $1,000,000 over three years on the Big Monty Claims. Flex Mining Ltd. owns 100% of six claims named the Big Monty Claims in the historic Abitibi Greenstone Belt. This earn-in agreement is subject to the Company reverse splitting the shares on the basis of one new share for every 200 existing shares and changing the name of the Company to Gold Lakes Corp. The Company is currently conducting its due diligence and the parties have agreed to enter into a Definitive Agreement by after the reverse split. Previously, the Company had two projects one the Valolo Claim in the Philippines, and the second a joint venture project on the Lucky Thirteen Claim.

We engaged in the search for gold and related minerals and have not generated any operating revenues since inception. We have not made our payments to secure our claim called the Lucky Thirteen Claim located in Hope, British Columbia, where we have completed exploration and testing work to see whether or not we have an economic resource. As we have not made the scheduled property payments we are in breach of our agreement to this claim we have defaulted on this claim.

With respect to the Valolo Claim in the Philippines, the Claim has expired.

We have incurred losses since inception and we must raise additional capital to fund our operations. There is no assurance we will be able to raise this capital or that if we raise the capital that the oral agreement to extend the payment terms will be honored.

There is no assurance that a commercially viable mineral deposit, a reserve, exists on our mineral claim or can be shown to exist until sufficient and appropriate exploration is done and a comprehensive evaluation of such work concludes economic and legal feasibility. Such work could take many years of exploration and would require expenditure of very substantial amounts of capital, capital we do not currently have and may never be able to raise.

Our initial holding was a 100% interest in the Valolo Gold Claim located in the Republic of Fiji. TNX acquired the Valolo Claim for the sum of $5,000.

TNX entered into a purchase agreement with Peter Osha on January 15, 2011 to earn a 100% interest in a placer gold project near Hope, British Columbia, Canada. Our investment is hereinafter referred to as the Lucky Thirteen Claim. TNX entered into a 50/50 joint venture on the Lucky Thirteen Claim with Big Rock Resources Inc. on May 2011 and TNX and commenced evaluating the Lucky Thirteen Property as the operator of the Joint Venture until February 2012 when Big Rock Resources Inc. announced that it would be unable to complete the promised financing. We are not proceeding with the purchase agreement with Peter Osha. We have spent through the joint venture approximately $400,000 on a work program on the Lucky Thirteen Claim.

As of the date of this Form 10K, we are planning on conducting exploration activities on the Big Monty Claims.

We have no full time employees and our management devotes a percentage of their time to the affairs of our Company. Our website is www.sigaresourcesinc.com

| 3 |

Our administrative office is located at 573 Monroe Blvd, Painesville, OH 44077. Our telephone number is 216-408-9423.

Presently our outstanding share capital is 45,105,000 common shares. We have no other type of shares either authorized or issued.

Our current auditors have expressed substantial doubt about our ability to continue as a going concern in their audit report attached to the financial statements. We have $nil cash as at July 31, 2014 and have liabilities of $282,925. Since our inception we have incurred accumulated losses of $661,275. We anticipate minimum operating expenses for the next twelve months of $210,300. It is extremely unlikely we will earn any revenue for a minimum of 5 years. We do not have any employees either full or part time.

TNX is responsible for filing various forms with the United States Securities and Exchange Commission (the “SEC”) such as Form 10-K and Form 10-Qs.

The shareholders may read and copy any material filed by TNX with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC, 20549. The shareholders may obtain information on the operations of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information which TNX has filed electronically with the SEC by assessing the website using the following address: http://www.sec.gov.

Planned Business

The following discussion should be read in conjunction with the information contained in the financial statements of TNX and the notes, which forms an integral part of the financial statements, which are attached hereto.

The financial statements mentioned above have been prepared in conformity with accounting principles generally accepted in the United States of America and are stated in United States dollars.

This Form 10-K also contains forward-looking statements that involve risks and uncertainties. If any of the events or circumstances described in the following risks actually occurs, our business, financial condition, or results of operations could be materially adversely affected and the price of our common stock could decline on the OTC Bulletin Board (the “OTCBB”).

Risks Associated with our Company:

| 1. | Because our auditors have issued a going concern opinion and because our officers and directors will not loan any money to us, we may not be able to achieve our objectives and may have to suspend or cease exploration activity. |

Our auditors’ report on our 2014 financial statements expressed an opinion that substantial doubt exists as to whether we can continue as an ongoing business for the next twelve months. Because our officers and directors are unwilling to commit to loan or advance capital to us, we believe that if we do not raise additional capital through the issuance of treasury shares, we will be unable to conduct exploration activity and may have to cease operations and go out of business.

| 4 |

| 2. | Because the probability of an individual prospect ever having reserves is extremely remote, in all probability our property does not contain any reserves, and any funds spent on exploration will be lost. |

Because the probability of an individual prospect ever having reserves is extremely remote, in all probability our properties, the Big Monty Claims, does not contain any reserves, and any funds spent on exploration will be lost. If we cannot raise further funds as a result, we may have to suspend or cease operations entirely which would result in the loss of our shareholders’ investment.

| 3. | We lack an operating history and have losses which we expect to continue into the future. As a result, we may have to suspend or cease exploration activity or cease operations. |

We were incorporated in 2007, have not yet conducted any exploration activities and have not generated any revenues. We have an insufficient exploration history upon which to properly evaluate the likelihood of our future success or failure. Our net loss from inception to July 31, 2014, the date of our most recent unaudited financial statements, is $661,275. Our ability to achieve and maintain profitability and positive cash flow in the future is dependent upon:

| * | Our ability to locate a profitable mineral property | |

| * | Our ability to locate an economic ore reserve | |

| * | Our ability to generate revenues | |

| * | Our ability to reduce exploration costs. |

Based upon current plans, we expect to incur operating losses in future periods. This will happen because there are expenses associated with the research and exploration of our mineral property. We cannot guarantee we will be successful in generating revenues in the future. Failure to generate revenues will cause us to go out of business.

| 4. | We have no known ore reserves. Without ore reserves we cannot generate income and if we cannot generate income we will have to cease exploration activity which will result in the loss of our shareholders’ investment. |

We have no known ore reserves. Even if we find gold mineralization we cannot guarantee that any gold mineralization will be of sufficient quantity so as to warrant recovery. Additionally, even if we find gold mineralization in sufficient quantity to warrant recovery, we cannot guarantee that the ore will be recoverable. Finally, even if any gold mineralization is recoverable, we cannot guarantee that this can be done at a profit. Failure to locate gold deposits in economically recoverable quantities will mean we cannot generate income. If we cannot generate income we will have to cease exploration activity, which will result in the loss of our shareholders’ investment.

| 5. | If we don’t raise enough money for exploration, we will have to delay exploration or go out of business, which will result in the loss of our shareholders’ investment. |

We estimate that, with funding committed by our management combined, we do not have sufficient cash to continue operations for twelve months even if we only carry out Phase I of our planned exploration activity on the Big Monty Claims. We need to raise additional capital to undertake Phase I. We may not be able to raise additional funds. If that occurs we will have to delay exploration or cease our exploration activity and go out of business which will result in the loss of our shareholders’ entire investment in our Company.

| 6. | Because we are small and do not have much capital, we must limit our exploration and as a result may not find an ore body. Without an ore body, we cannot generate revenues and our shareholders will lose their investment. |

Any potential development of and production from our exploration property depends upon the results of exploration programs and/or feasibility studies and the recommendations of duly qualified engineers and geologists. Because we are small and do not have much capital, we must limit our exploration activity unless and until we raise additional capital. Any decision to expand our operations on our exploration property will involve the consideration and evaluation of several significant factors including, but not limited to:

| 5 |

| ● | Costs of bringing the property into production including exploration preparation of production feasibility studies, and construction of production facilities; |

| ● | Availability and cost of financing; |

| ● | Ongoing costs of production; |

| ● | Market prices for the minerals to be produced; |

| ● | Environmental compliance regulations and restraints; and |

| ● | Political climate and/or governmental regulations and controls. |

Such programs will require very substantial additional funds. Because we may have to limit our exploration, we may not find an ore body, even though our property may contain mineralized material. Without an ore body, we cannot generate revenues and our shareholders will lose their entire investment in our Company.

We may not have access to all of the supplies and materials we need to begin exploration which could cause us to delay or suspend exploration activity.

Competition and unforeseen limited sources of supplies in the industry could result in occasional spot shortages of supplies and certain equipment such as bulldozers and excavators that we might need to conduct exploration. We have not attempted to locate or negotiate with any suppliers of products, equipment or materials. We will attempt to locate products, equipment and materials as and when we are able to raise the requisite capital. If we cannot find the products and equipment we need, we will have to suspend our exploration plans until we do find the products and equipment we need.

| 7. | Because our officers and directors have other outside business activities and may not be in a position to devote a majority of their time to our exploration activity, our exploration activity may be sporadic which may result in periodic interruptions or suspensions of exploration . |

Our one officer, our President will be devoting only 15% of his time, approximately 24 hours per month, to our business. As a consequence of the limited devotion of time to the affairs of our Company expected from management, our business may suffer. For example, because our officers and directors have other outside business activities and may not be in a position to devote a majority of their time to our exploration activity, our exploration activity may be sporadic or may be periodically interrupted or suspended. Such suspensions or interruptions may cause us to cease operations altogether and go out of business.

| 8. | Because mineral exploration and development activities are inherently risky, we may be exposed to environmental liabilities. If such an event were to occur it may result in a loss of your investment. |

The business of mineral exploration and extraction involves a high degree of risk. Few properties that are explored are ultimately developed into production. At present, the Big Monty Claims, does not have a known body of commercial ore. Unusual or unexpected formations, formation pressures, fires, power outages, labor disruptions, flooding, explosions, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labor are other risks involved in extraction operations and the conduct of exploration programs. We do not carry liability insurance with respect to our mineral exploration operations and we may become subject to liability for damage to life and property, environmental damage, cave-ins or hazards. Previous mining exploration activities may have caused environmental damage to the Big Monty Claims. It may be difficult or impossible to assess the extent to which such damage was caused by us or by the activities of previous operators, in which case, any indemnities and exemptions from liability may be ineffective. If the Big Monty Claims is found to have commercial quantities of ore, we would be subject to additional risks respecting any development and production activities. Most exploration projects do not result in the discovery of commercially mineable deposits of ore.

| 6 |

| 9. | No matter how much money is spent on our Mineral Claim, the risk is that we might never identify a commercially viable ore reserve. |

No matter how much money is spent over the years on the Big Monty Claims, we might never be able to find a commercially viable ore reserve. Over the coming years, we could spend a great deal of money on the Big Monty Claims without finding anything of value. There is a high probability the Big Monty Claims do not contain any reserves so any funds spent on exploration will probably be lost.

| 10. | Even with positive results during exploration, the Mining Claims might never be put into commercial production due to inadequate tonnage, low metal prices or high extraction costs. |

We might be successful, during future exploration programs, in identifying a source of minerals of good grade but not in the quantity, the tonnage, required to make commercial production feasible. If the cost of extracting any minerals that might be found on the Big Monty Claims is in excess of the selling price of such minerals, we would not be able to develop the Big Monty Claims. Accordingly even if ore reserves were found on the Big Monty Claims, without sufficient tonnage we would still not be able to economically extract the minerals from the Big Monty Claims in which case we would have to abandon the Big Monty Claims and seek another mineral property to develop, or cease operations altogether.

Risks Associated with owning our Shares:

| 11. | We anticipate the need to issue and sell additional shares in the future meaning that there will be a dilution to our existing shareholders resulting in their percentage ownership in the Company being reduced accordingly. |

We expect that the only way we will be able to acquire additional funds is through the sale of our common stock. This will result in a dilution effect to our shareholders whereby their percentage ownership interest in the Company is reduced. The magnitude of this dilution effect will be determined by the number of shares we will have to issue in the future to obtain the funds required.

| 12. | We have settled liabilities of the Company by entering into Convertible Debentures and Settlement Agreements which have a significant dilution effect on our shareholders. |

We have entered into Convertible Debentures Agreements with our creditors which could result in the issuance of 116,000,000 additional shares. This will result in a dilution effect to our shareholders whereby their percentage ownership interest in the Company is reduced. Further agreements could be entered into.

| 13. | Because our securities are subject to penny stock rules, you may have difficulty reselling your shares. |

Our shares are “penny stocks” and are covered by Section 15(g) of the Securities Exchange Act of 1934 which imposes additional sales practice requirements on broker/dealers who sell the Company’s securities including the delivery of a standardized disclosure document; disclosure and confirmation of quotation prices; disclosure of compensation the broker/dealer receives; and, furnishing monthly account statements. For sales of our securities, the broker/dealer must make a special suitability determination and receive from its customer a written agreement prior to making a sale. The imposition of the foregoing additional sales practices could adversely affect a shareholder’s ability to dispose of his stock.

Forward Looking Statements

In addition to the other information contained in this Form 10-K, it contains forward-looking statements which involve risk and uncertainties. When used in this Form 10-K, the words “may”, “will”, “expect”, “anticipate”, “continue”, “estimate”, “project”, “intend”, “believe” and similar expressions are intended to identify forward-looking statements regarding events, conditions and financial trends that may affect our future plan of operations, business strategy, operating results and financial position. Readers are cautioned that any forward-looking statements are not guarantees of future performance and are subject to risks and uncertainties and that actual result could differ materially from the results expressed in or implied by these forward-looking statements as a result of various factors, many of which are beyond our control. Any reader should review in detail this entire Form 10-K including financial statements, attachments and risk factors before considering an investment.

| 7 |

ITEM 1B. UNRESOLVED STAFF COMMENTS

There are no unresolved staff comments outstanding at the present time.

Our mineral properties are a letter of intent to acquire the:

Big Monty Claims

We have entered into a letter of intent to with Gold Lakes Corp. (“Gold Lakes”). The LOI sets forth basic terms and conditions whereby the Company would acquire all of the issued and outstanding shares of Gold Lakes pursuant to a Share Exchange, which would result in Gold Lakes becoming a wholly owned subsidiary of the Company.

The Big Monty Claims consist of the following 6 mining claims in Northern Ontario:

| Mining Claim # | # of 16HA Claim Units | # of Hectares | # of Acres | |||||||||||

| 4256641 | 16 | 256 | 633 | |||||||||||

| 4256642 | 16 | 256 | 633 | |||||||||||

| 4256644 | 6 | 96 | 237 | |||||||||||

| 4256645 | 9 | 144 | 356 | |||||||||||

| 4256646 | 11 | 176 | 435 | |||||||||||

| 4256647 | 12 | 192 | 475 | |||||||||||

| 70 | 1,120 | 2,768 | ||||||||||||

Location and Access

The Big Monty Claims is located approximately 70 kilometers (44 miles) north of Kirkland Lake, Ontario, and 68 kilometers east of Timmins, Ontario (42 miles). It is located approximately 10 kilometers (6 miles) east of Matheson, Ontario. The area covered by the Claim is an active mineral exploration and development region with plenty of heavy equipment and operators available for hire. Both Kirkland Lake and Timmins can provide all necessary amenities and supplies including, fuel, helicopter services, hardware, drilling companies and assay services. Access to our Claim is via major highway east of Matheson. No water is required for the purposes of our planned exploration work. No electrical power is required at this stage of exploration. Any electrical power that might be required in the foreseeable future could be supplied by gas powered portable generators.

The claim’s terrain is rugged with mountain forests growth throughout.

| 8 |

Property Geology

Bedrock outcrops were found to be generally rare across all of the claims. This was due to vegetation and glacial till. Portions of the claims have been logged in recent years; particularly the northern portion of claim 4256645 and claims 4256646 and 4256647. However the logged areas have re-vegetated with first generation plants (grasses, pines, scrub oaks, sumac, etc.) making it difficult to find bedrock exposures. Also a significant portion of the claims area is covered with a veneer of glacial till of varying thicknesses. The till is described as a fine to medium grain arkosic sand with occasional pebble and gravel size clasts. This till dominates claims area south of the North Branch of the Porcupine-Destor Fault. The available bedrock outcrops are primarily found on claims 4255645, 4255646 and 4255647 due to recent logging and the glacial till being locally thinner at these claims. The observed bedrock is a massive fine-grained mafic volcanic rocks intruded with mafic rock characterized by pillow structures. Also observed was a northwest/southeast dike on claim 4255646. The dike rock is described as a medium-grain with visible feldspars and slightly magnetic. Finally, accessory minerals of pyrite and possible arsenopyrite were observed in several rocks. The general geochemistry is indicating the collect rocks are mafic being rich in iron and magnesium with low silica by weight. No significant concentrations of precious, base or rare earth elements were detected in the collected rocks. A belt of volcanic rocks, of the Savura Volcanic Group, underlies the property. These volcanic rocks are exposed along a wide axial zone of a broad complex. The presence of these rocks is on our property is relevant to us as gold mineralization, at the nearby (approximately 20 miles to the west of our claim) Nasoata Gold Mine, a past producer of gold in commercial quantities, is generally concentrated within extrusive volcanic rocks (of the Savura Volcanic Group) on the walls of large volcanic caldera.

| 9 |

The Big Monty Claims are located approximately 6 miles east of the town of Matheson (2,410 population)

| 10 |

Previous Exploration

On October 28, 2013, G3 - Gauvreau GeoEnvironmental Group Inc. prepared 2013 Claims Assessment Report. The work performed as part of the claims assessment necessary for the Big Monty Property to maintain the claims in good standing following the guidelines set forth by the Ontario Ministry of Northern Development and Mines (MNDM). The Big Monty Property is a northwest to southeast group of seven claims on Crown Land located west and south of Trollope Lake in Frecheville Township as illustrated on Figure 1. The claim numbers are the following: 4256641, 4256642, 4256644, 4256645, 4256646 and 4256647.

The assessment work for the claims is divided into three tasks:

1) Field Study performing geologic mapping and sampling

2) Magnetic Survey interpretation, and

3) Georeferencing.

The Big Monty claims were staked in September and October of 2010. These claims are geologically located in the Abitibi greenstone province. Structurally the claims lie along the central sector of the north branch of the Porcupine-Destor Fault. This Fault divides the claim’s lithostratographic assemblages north and south. The northern half of the claims has been mapped as Stoughton-Roquemaure Assemblage (27.25 to 27.20 Ma) (1). The southern and up side of the Fault has been mapped as the as the Kidd-Munro Assemblage (27.18 to 27.10 Ma) (1). The Stoughton-Roquemaure Assemblage is characterized by komatiitic basalt and low to high-Mg komatiite intrusives. Spinifex-textured and pillowed komatiites are common (2) while the Kidd-Monro Assemblage is described as assemblage as ultramafic and mafic, tholeiitic, metavolcanic rocks with minor high-silica rhyolite (1).

In the 2012 assessment period, an aerial magnetic survey was conducted on the Big Monty claims. The results from aerial magnetic survey produced a residual magnetic intensity map and a first vertical derivative of the residual magnetic intensity map. No corresponding geologic interpretation of the aerial magnetic survey was completed during that assessment period.

Field Study

A field study was performed beginning October 7 through October 11 and October 22, 2013. The purpose of the field study, where possible, was to complete the following:

| ● | geological mapping, | |

| ● | grab/hand rock sampling, | |

| ● | geochemical sampling, | |

| ● | structural mapping (faults, joints, fractures, etc.), and | |

| ● | GPS locating of control points including claim corner posts and claim boundaries. |

Nine rock samples were collected from various bedrock outcrops during the field study. These samples were submitted to an Agat Laboratories in Sudbury, Ontario for chemical analyses.

The field geological mapping and chemical analysis data is used to tie the aerial magnetometer survey to observable and mapable bedrock conditions along with structures the Porcupine-Destor Fault Zone.

Aerial Magnetometer Survey Interpretation

The interpretation of the aerial magnetic survey interpretation was conducted using the data collected in the field. The results from aerial magnetic survey produced a residual magnetic intensity map and a first vertical derivative of the residual magnetic intensity map. The reader is reminded that a magnetic field has a direction or vector. Residual magnetic intensity is the remnant magnetic field before the rock has cooled below the Curie point and the magnetic field has been removed (3). This magnetism can be in any direction. The residual magnetic intensity is not only the magnetism from the first cooling event but the residual magnetism can be affected but subsequent events (magmatic or hydrothermal intrusion) that will affect the magnetic minerals in that formation.

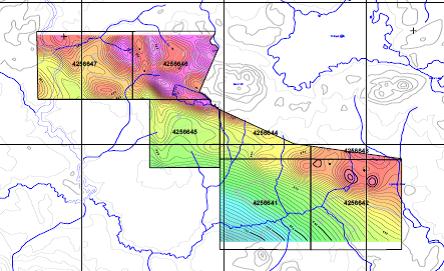

The first vertical derivative of the residual magnetic intensity emphasizes near surface features by mathematically removing the inclination and declination of the field from the data. The transformed data views the same geologic structures as the residual magnetic intensity map, but with the magnetic pole’s field induced vertical. The first vertical derivative is calculated by measuring the magnetic field simultaneously at two points vertically above each other and dividing the difference in the magnetic intensities by the distance between the two points. Figure 3 illustrates the residual magnetic intensity. The north branch of the Porcupine-Destor Fault is the dividing line between high and low magnetic intensity.

| 11 |

The magnetic intensity decreases to the southwest of the Fault. Correspondingly, the magnetic intensity is elevated on the claims northeast of the Fault. Interestingly, off set movement of the low magnetic intensity to the northeast is illustrated by the faults labeled 2 and 3 movement to the northeast. The low magnetic intensity located in the southeastern part of the Big Monty claims can be interpreted to be the lack of magnetic minerals which may possibly be due to an underlying felsic intrusive body. The mafic dike on claim 4255646 was expected to have a clear magnetic signature especially considering the rock sample collected from the dike was slightly magnetized and had the highest iron concentration however no geometric magnetic signature mimicking the dike was observed.

As with the residual magnetic intensity map, areas of north of the Porcupine-Destor Fault illustrate relatively higher general magnetic intensity than areas south of the Fault, and the southwestern portion of claim 4256641 is also an area of low magnetic intensity. Five near circular areas of elevated magnetic intensity are interpreted along or paralleling to the Northern Branch of the Porcupine- Destor Fault in claims 4256641, 4256642 and 4256645. These features are interpreted to be intrusions characterized by rocks with significant magnetic minerals. The relationship of the intrusions to the Fault can be interpreted as these intrusions having been injected into the Fault.

Georeferencing

MNDM requires the claims to be in spatially correct location. Georeferencing was planned as part of the field study following the MNDM guidelines. During the Field Study each claim corner was found using a GPS. Unfortunately no claims post were found at or surrounding these GPS locations. A request for extension has been filed to complete the georeferencing and re-posting of the claims.

Proposed Exploration Work – Plan of Operation

The ultimate goal of the assessment work is to identify locations of where to drill for precious metals. To achieve that goal from the available data, various assumptions must be made regarding the interpretation for the potential of mineralization. For example, if the assumption is that gold will be associated with quartz/felsic intrusions then the southwestern corner of claim 4256640 represents a reasonable target area. If it is further assumed that mineralization is associated with fault structures then the northeast trending Faults 3 and 4 should be focus areas for potential exploration locations.

However if the mineralization is associated with massive sulfide intrusions then the five elevated magnetic areas associated with the Fault are potential targets. Massive sulfides are usually associated with pyrite which is only slightly magnetic. The mineralization may be associated with pyrhhotite and magnetite which are common in sulfide intrusives. It should be noted that two of the elevated magnetic intensity areas are located at junction points between the Branch of the Porcupine-Destor Fault and the northeastern trending faults. The junction locations are ideal for intrusives and are recommended drilling locations.

Consequently, the proposed field work will be a phased exploration program to properly evaluate the potential of the Big Monty Claims. We must conduct exploration to determine what minerals exist on our property and whether they can be economically extracted and profitably processed. We plan to proceed with exploration of the Big Monty Claims by drilling the quartz/felsic intrusion as well as testing further the five elevated magnetic areas associated with the fault in order to begin determining the potential for discovering commercially exploitable deposits of gold on our claim.

We have not discovered any ores or reserves on the Big Monty Claims. Our planned work is exploratory in nature.

The goal of phase 1 is to utilize the current data base for the project, (an airborne mag survey and a brief geologic review done in 2013) to develop possible drill targets seeking precious and base metals on the 7 claims comprising the Monty Project.

| 12 |

The existing knowledge of geology and structure is insufficient to spot drill targets at this time. Only 9 rock samples were taken and none found more than trace values in precious or base metals. A problem was lack of outcrop, limiting knowledge of the actual rock types, including structure and geology. 10 outcrops were found and the geological evaluation was minimal. The report does not indicate that rock fabric or strike and dip of features was performed.

The Porcupine-Destor fault system is believed to run generally East-West through the property with numerous North East-South West cross faults providing several possible intersecting structural features which could possibly host economic mineralization.

Phase 1 will revisit outcrops for mapping and recording attitudes and fabric. Outcrop exposure will be attempted by stripping moss and vegetation from shallowly covered areas. This same effort will assess access for drill equipment, and determine if additional geophysics, either airborne or ground, would be valuable in determining more precisely the strike and dip of the major structures.

Competitive Factors

The mining industry is highly fragmented. We are competing with many other exploration companies looking for gold. We are among the smallest exploration companies in existence and are an infinitely small participant in the mining business which is the cornerstone of the founding and early stage development of the mining industry. While we generally compete with other exploration companies, there is no competition for the exploration or removal of minerals from our claims. Readily available markets exist for the sale of gold. Therefore, we will likely be able to sell any gold that we are able to recover, in the event commercial quantities are discovered on the Big Monty Claims. There is no ore body on the Big Monty Claims.

Government Regulation

Exploration activities are subject to various national and provincial laws which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances and other matters. We believe that we are in compliance in all material respects with applicable mining, health, safety and environmental statutes and the regulations passed there under in Ontario and Canada.

Environmental Regulation

Our exploration activities are subject to various federal, provincial and local laws and regulations governing protection of the environment. These laws are continually changing and, as a general matter, are becoming more restrictive. Our policy is to conduct business in a way that safeguards public health and the environment. We believe that our exploration activities are conducted in material compliance with applicable laws and regulations. Changes to current local, state or federal laws and regulations in the jurisdictions where we operate could require additional capital expenditures and increased operating and/or reclamation costs. Although we are unable to predict what additional legislation, if any, might be proposed or enacted, additional regulatory requirements could render certain exploration activities uneconomic.

Employees

Initially, we intend to use the services of subcontractors for labor exploration work on our claim. At present, we have no employees as such although our officer and director devotes a portion of their time to the affairs of the Company. Our officer and director does not have an employment agreement with us. We presently do not have pension, health, annuity, insurance, profit sharing or similar benefit plans; however, we may adopt such plans in the future. There are presently no personal benefits available to any employee.

| 13 |

As indicated above we will hire subcontractors on an as needed basis. We have not entered into negotiations or contracts with any of potential subcontractors. We do not intend to initiate negotiations or hire anyone until we are nearing the time of commencement of our planned exploration activities.

There are no permanent facilities, plants, buildings or equipment on our mineral claim.

Mineralization

No mineralization has been reported for the area of the property but structures and shear zones affiliated with mineralization on adjacent properties pass through it.

Exploration

Previous exploration work has not included any attempt to drill the structure on Big Monty Claims. Records indicate that no detailed exploration has been completed on the property.

Adjacent Properties

The adjacent properties are cited as examples of the type of deposit that has been discovered in the area and are not major facets to this report.

Planned Exploration Program

| Description of Phase 1 Expenses | Cost | |||

| Air travel | $ | 3,000 | ||

| Fees for field crews for 3 weeks | 24,000 | |||

| Transportation | 2,000 | |||

| Equipment rental | 6,000 | |||

| Ground transportation (ATV rental) | 1,500 | |||

| Sampling and assaying | 6,000 | |||

| Trenching and possible short-hole drillin | 25,000 | |||

| TOTAL PHASE ONE | $ | 67,500 | ||

If phase 1 is successful, and time/weather is acceptable drilling can be commenced:

| Description of Phase 2 Expenses | Cost | |||

| Ground/air geophysics over fault zones | $ | 30,000 | ||

| Fees for field crews for 2 months | 48,000 | |||

| Drilling 3,300 meter holes if warranted | 108,000 | |||

| TOTAL PHASE TWO | $ | 186,000 | ||

| TOTAL FOR PHASES ONE AND TWO | $ | 253,500 | ||

| 14 |

There are no permanent facilities, plants, buildings or equipment on the Big Monty Claims.

We intend to complete the exploration work on the Big Monty Claims. No exact date has been determined for the commencement of exploration work on the Big Monty Claims.

Particularly since we have a limited operating history, no reserves and no revenue, our ability to raise additional funds might be limited. If we are unable to raise the necessary funds, we would be required to suspend Siga’s operations and liquidate our company.

There are no permanent facilities, plants, buildings or equipment on the Big Monty Claims.

Investment Policies

Siga does not have an investment policy at this time. Any excess funds it has on hand will be deposited in interest bearing notes such as term deposits or short term money instruments. There are no restrictions on what the directors are able to invest.

There are no legal proceedings to which we are a party or to which the Big Monthly Claims is subject, nor to the best of management’s knowledge are any material legal proceedings contemplated.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITIES HOLDERS

There has been no Annual General Meeting of Stockholders since our date of inception. Management hopes to hold an Annual General Meeting of Stockholders during 2015.

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASE OF EQUITY SECURITIES

Since inception, we have not paid any dividends on our common stock, and we do not anticipate that it will pay dividends in the foreseeable future. As at July 31, 2014, we had 11 shareholders; none of these shareholders are an officer and director. The Company trades under the symbol SGAE during the years ended July 31, 2014 and 2013 as follows:

| Quarter ended | High | Low | Volume | |||||||||

| 31-Oct-12 | $ | 0.4500 | $ | 0.007 | 1,192,000 | |||||||

| 31-Jan-13 | $ | 0.045 | $ | 0.0108 | 2,858,000 | |||||||

| 30-Apr-13 | $ | 0.0270 | $ | 0.018 | 1,215,000 | |||||||

| 31-Jul-13 | $ | 0.0140 | $ | 0.0024 | 3,501,000 | |||||||

| 15 |

| Quarter ended | High | Low | Volume | |||||||||

| 31-Oct-13 | $ | 0.0287 | $ | 0.0025 | 24,167,000 | |||||||

| 31-Jan-14 | $ | 0.0025 | $ | 0.0020 | 23,180,000 | |||||||

| 30-Apr-14 | $ | 0.0100 | $ | 0.0030 | 6,301,000 | |||||||

| 31-Jul-14 | $ | 0.0049 | $ | 0.0033 | 22,790,000 | |||||||

Option Grants and Warrants outstanding since Inception.

No stock options have been granted since our inception.

There are no outstanding warrants.

There is conversion privileges on approximately $116,000 of our debt. This could result in additional shares of 116,000,000 being issued through conversion of this debt.

ITEM 6. SELECTED FINANCIAL INFORMATION

The following summary financial data was derived from our financial statements. This information is only a summary and does not provide all the information contained in our financial statements and related notes thereto. You should read the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes included elsewhere in this Form 10-K.

Operation Statement Data

| For the year ended | For the year ended | |||||||

| July 31, 2014 | July 31, 2013 | |||||||

| Interest Expense | $ | 14,158 | $ | 129,925 | ||||

| General and Administrative | 9,000 | 34,750 | ||||||

| Net loss | $ | 23,158 | $ | 164,675 | ||||

| Weighted average shares outstanding (basic and fully diluted | 45,105,000 | 45,105,000 | ||||||

| Net loss per share (basic and fully diluted) | $ | 0.00 | $ | 0.00 | ||||

| 16 |

Balance Sheet Data

| Cash and cash equivalent | $ | Nil | $ | Nil | ||||

| Total assets | $ | Nil | $ | Nil | ||||

| Total liabilities | $ | 282,925 | $ | 259,767 | ||||

| Total Stockholders’ deficiency | $ | (282,925 | ) | $ | (259,767 | ) |

Our historical results do not necessary indicate results expected for any future periods.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONS AND RESULTS OF OPERATIONS

Corporate Organization and History within the Last Three years

We were incorporated under the laws of the State of Nevada on January 18, 2007 under the name TNX Maverick, Corp. We do not have any subsidiaries or affiliated companies. Since our default have defaulted on payments to keep the ownership in the Lucky Thirteen Claim intact. Consequently, we have lost our interest in the Lucky Thirteen Claim entirely.

We have not been involved in any bankruptcy, receivership or similar proceedings since inception nor have we been party to a reclassification, merger, consolidation, or purchase or sale of a significant amount of assets not in the ordinary course of business. We have no intention of entering into a corporate merger or acquisition.

Business Development since Inception

There is no historical financial information about us upon which to base an evaluation of our performance as an exploration corporation. We are a pre-exploration stage company and have not generated any revenues from our exploration activities. Further, we have not generated any revenues since our formation on January 18, 2007. We cannot guarantee we will be successful in our exploration activities. Our business is subject to risks inherent in the establishment of a new business enterprise, including limited capital resources, possible delays in the exploration of our properties, and possible cost overruns due to price and cost increases in services.

To become profitable and competitive, we first complete our acquisition of the Big Monty Claims or resurrect our ownership interest in the Lucky Thirteen Claim by making the requisite payments; or we must find an alternate mining claim. We must obtain equity or debt financing to provide the capital required implement our phased exploration program. We have no assurance that financing will be available to us on acceptable terms. If financing is not available on satisfactory terms, we will be unable to commence, continue, develop or expand our exploration activities. Even if available, equity financing could result in additional dilution to existing shareholders.

Our auditors have issued a going concern opinion. This means that our auditors believe there is substantial doubt that we can continue as an on-going business for the next twelve months unless we obtain additional capital to pay our bills. This is because we have not generated any revenues and no revenues are anticipated until we begin removing and selling minerals. Accordingly, we must raise cash from other sources. Our only other source for cash at this time is investments by others in the Company.

To meet our need for cash we must raise additional capital. We will attempt to raise additional money through a private placement, public offering or through loans. We have discussed this matter with our officers and directors. However, our officers and directors are unwilling to make any commitments to loan us any money at this time. At the present time, we have not made any arrangements to raise additional cash. We require additional cash to continue operations. Such operations could take many years of exploration and would require expenditure of very substantial amounts of money, money we do not presently have and may never be able to raise. If we cannot raise it we will have to abandon our planned exploration activities and go out of business.

We estimate we will require $210,300 in cash over the next twelve months. For a detailed breakdown refer to “Liquidity and Capital Reserves”. In addition cash will be required to cover the phase one cost of completing the exploration work for the Big Monty Claims during that period is estimated at $67,500; and, if required the phase two costs estimated at $186,000.

| 17 |

Comparison of Operations for the year ended July 31, 2014 (YE2014) compared to year ended July 31, 2013 (YE2013)

| Expense | 7/31/2014 | 7/31/2013 | Difference | Reference | ||||||||||||

| Accounting and auditing | $ | 9,000 | $ | 25,050 | $ | (16,050 | ) | |||||||||

| Bank charges | - | 205 | (205 | ) | ||||||||||||

| Management fees | + | 9,000 | (9,000 | ) | (i) | |||||||||||

| News Releases | - | 370 | (370 | ) | ||||||||||||

| Telephone | - | 125 | (125 | ) | ||||||||||||

| Interest | 14,158 | 129,925 | (115,767 | ) | (ii) | |||||||||||

| TOTAL EXPENSES | 23,158 | 164,675 | (141,157 | ) |

| (i) | Management fees |

| In YE2014, for 9 months the Director was paid $0 per month. The previous Directors of the Company were paid $1,500 per month each during the 2013 year end until they resigned late in 2012. Consequently director fees reduced by $9,000 from YE2014 over YE2013. | |

| (ii) | Interest |

Interest in YE2014 was $14,158 due to the interest earned on the Convertible Notes. The balance of $129,925 interest expense in YE2013 included the amortization of the Discount of the Convertible Notes $116,000. |

| 18 |

Balance Sheets

Total cash and cash equivalents, as of July 31, 2014 and 2013 was $Nil. Our working capital deficiency as at July 31, 2014 was a $282,925 and as of July 31, 2013, $259,767.

Total stockholders’ deficiency as of July 31, 2014 was $282,925 and $259,767 as at July 31, 2013. Total shares outstanding as at July 31, 2014 and 2013 was 45,105,000.

Our mineral properties are a letter of intent to acquire the:

Big Monty Claims

We have entered into a letter of intent to enter into an earn-in agreement to earn a 100% interest in the Big Monty Claims. Please see ITEM 2. PROPERTIES for a full description of these properties.

Critical Accounting Policies

Our discussion and analysis of our financial condition and results of operations, including the discussion on liquidity and capital resources, are based upon our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of these financial statements requires us to make estimates and judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. On an ongoing basis, management re-evaluates its estimates and judgments.

| 19 |

The going concern basis of presentation assumes we will continue in operation throughout the next fiscal year and into the foreseeable future and will be able to realize our assets and discharge our liabilities and commitments in the normal course of business. Certain conditions, discussed below, currently exist which raise substantial doubt upon the validity of this assumption. The financial statements do not include any adjustments that might result from the outcome of the uncertainty.

Liquidity and Capital Resources

As of July 31, 2014 our total assets were $Nil and our total liabilities were $282,925.

Not including the cost of completing the exploration phase of our Big Monty Claims, our non-elective expenses over the next twelve months, are expected to be as follows:

| Expense | Ref. | Estimated Amount | ||||

| Accounting and audit | (i) | $ | 15,500 | |||

| Edgar filing fees | (ii) | 6,000 | ||||

| Filing fees – Nevada; Securities of State | (ii) | 375 | ||||

| Office and general expenses | (iv) | 43,000 | ||||

| Estimated expenses for the next twelve months | 64,875 | |||||

| Account payable as at July 31, 2014 | 145,425 | |||||

| Cash required for the next twelve months | $ | 210,300 | ||||

| (i) | Accounting and audit |

| We will have to continue to prepare consolidated financial statements for submission with the various 10-K and 10-Q as follows: |

| Period | Form | Accountant | Auditor | Amount | ||||||||||||

| October 31, 2013 | 10-Q | 1,500 | 1,500 | 3,000 | ||||||||||||

| January 31, 2014 | 10-Q | 1,500 | 1,500 | 3,000 | ||||||||||||

| April 30, 2014 | 10-Q | 1,500 | 1,500 | 3,000 | ||||||||||||

| July 31, 2014 | 10-K | 3,000 | 3,500 | 6,500 | ||||||||||||

| Estimated total | $ | 7,500 | $ | 8,000 | $ | 15,500 | ||||||||||

| (ii) | Edgar filing fees |

| We will be required to file the annual Form 10-K estimated at $250 and the three Form 10-Qs at $250 each for a total cost of $1,000. Additional Form 8-K should cost an additional $1,000. The conversion costs to XBLR is estimated at $4,000. | |

| (iii) | Filing fees in Nevada |

| To maintain the Company in good standing in the State of Nevada an annual fee of approximately $375 has been paid to the Secretary of State. | |

| (iv) | Office and general |

| We have estimated a cost of approximately $25,000 for photocopying, printing, fax and delivery, travel, transfer agent and entertainment. Director Fees total $1,500 per month or $18,000. Total Office and General is estimated to be $43,000. |

| 20 |

Our future operations are dependent upon our ability to obtain third party financing in the form of debt and equity and ultimately to generate future profitable operations or income from investments. As of July 31, 2014, we have not generated revenues, and have experienced negative cash flow from operations. We may look to secure additional funds through future debt or equity financings. Such financings may not be available or may not be available on reasonable terms.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURE ABOUT MARKET RISK

Market Information

There are no common shares subject to outstanding options, warrants or securities convertible into common equity of our Company.

The number of shares subject to Rule 144 is 23,925,000.

Presently, there are no shares being offered to the public and no shares have been offered pursuant to an employee benefit plan or dividend reinvestment plan.

Our shares are traded on the OTCBB. Although the OTCBB does not have any listing requirements per se, to be eligible for quotation on the OTCBB, we must remain current in our filings with the SEC; being as a minimum Forms 10-Q and 10-K. Securities already quoted on the OTCBB that become delinquent in their required filings will be removed following a 30 or 60 day grace period if they do not make their filing during that time.

In the future our common stock trading price might be volatile with wide fluctuations. Things that could cause wide fluctuations in our trading price of our stock could be due to one of the following or a combination of several of them:

| ● | our variations in our operations results, either quarterly or annually; |

| ● | trading patterns and share prices in other exploration companies which our shareholders consider similar to ours; |

| ● | the exploration results on the Big Monty Claims, and |

| ● | other events which we have no control over. |

In addition, the stock market in general, and the market prices for thinly traded companies in particular, have experienced extreme volatility that often has been unrelated to the operating performance of such companies. These wide fluctuations may adversely affect the trading price of our shares regardless of our future performance. In the past, following periods of volatility in the market price of a security, securities class action litigation has often been instituted against such company. Such litigation, if instituted, whether successful or not, could result in substantial costs and a diversion of management’s attention and resources, which would have a material adverse effect on our business, results of operations and financial conditions.

| 21 |

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

The financial statements attached to this Form 10-K for the year ended July 31, 2014 have been examined by our independent accountants, ZBS Group LLP. and attached hereto.

ITEM 9. CHANGES IN AND DISAGREEMENT WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

There are no disagreements with accountants on accounting and financial disclosure. During the year ended December 31, 2013, the Company changed its auditors from Sadler Gibbs & Associates, LLC, the auditors for the year ended July 31, 2012, initially to Messineo & Co. CPAs., who was appointed on November 6, 2014, and subsequently to ZBS Group, LLP, on April 1, 2015.

ITEM 9A. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

We carried out an evaluation, under the supervision and with the participation of our management, including our principal executive officer and principal financial officer, of the effectiveness of the design of our disclosure controls and procedures (as defined by Exchange Act Rules 13a-15(e) or 15d-15(e)) as of July 31, 2014 pursuant to Exchange Act Rule 13a-15. Based upon that evaluation, our Principal Executive Officer and Principal Financial Officer concluded that our disclosure controls and procedures are not effective as of July 31, 2014 as a result of material weaknesses in internal controls over financial reporting. A material weakness is a deficiency, or a combination of control deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of the Company’s interim financial statements will not be prevented or detected on a timely basis. Our management, on behalf of the Company, has considered certain internal control procedures as required by the Sarbanes-Oxley (“SOX”) Section 404 A which accomplishes the following:

Internal controls are mechanisms to ensure objectives are achieved and were under the supervision of the Company’s former Chief Executive Officer, being Edwin Morrow, and former Chief Financial Officer, being Robert Malasek until their withdrawal of services on November 7, 2012 and subsequently Bob Hogarth as President and Director who was replaced on September 3, 2014 by Christopher Vallos. Good controls encourage efficiency, compliance with laws and regulations, sound information, and seek to eliminate fraud and abuse.

These control procedures provide reasonable assurance regarding the reliability of financial reporting and the preparation of the Company’s financial statements for external purposes in accordance with U.S. generally accepted accounting principles.

Internal control is “everything that helps one achieve one’s goals - or better still, to deal with the risks that stop one from achieving one’s goals.”

Internal controls are mechanisms that are there to help the Company manage risks to success.

Internal controls is about getting things done (performance) but also about ensuring that they are done properly (integrity) and that this can be demonstrated and reviewed (transparency and accountability).

In other words, control activities are the policies and procedures that help ensure the Company’s management directives are carried out. They help ensure that necessary actions are taken to address risks to achievement of the Company’s objectives. Control activities occur throughout the Company, at all levels and in all functions. They include a range of activities as diverse as approvals, authorizations, verifications, reconciliations, reviews of operating performance, security of assets and segregation of duties.

As of July 31, 2014, the management of the Company assessed the effectiveness of the Company’s internal control over financial reporting based on the criteria for effective internal control over financial reporting established in Internal Control—Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”) and SEC guidance on conducting such assessments. Management concluded, during the year ended July 31, 2014, internal controls and procedures were not effective to detect the inappropriate application of US GAAP rules. Management realized there are deficiencies in the design or operation of the Company’s internal control that adversely affected the Company’s internal controls which management considers to be material weaknesses.

| 22 |

In the light of management’s review of internal control procedures as they relate to COSO and the SEC the following were identified:

| ● | The Company’s Audit Committee does not function as an Audit Committee should since there is a lack of independent directors on the Committee, |

| ● | The Company has limited segregation of duties which is not consistent with good internal control procedures. |

| ● | The Company does not have a written internal control procedurals manual which outlines the duties and reporting requirements of the Directors and any staff to be hired in the future. This lack of a written internal control procedurals manual does not meet the requirements of the SEC or good internal control. |

| ● | There are no effective controls instituted over financial disclosure and the reporting processes. |

Management feels the weaknesses identified above, being the latter three, have not had any effect on the financial results of the Company. Management will have to address the lack of independent members on the Audit Committee and identify an “expert” for the Committee to advise other members as to correct accounting and reporting procedures.

The Company and its management will endeavor to correct the above noted weaknesses in internal control once it has adequate funds to do so. By appointing independent members to the Audit Committee and using the services of an expert on the Committee will greatly improve the overall performance of the Audit Committee. With the addition of other Board Members and staff the segregation of duties issue will be address and will no longer be a concern to management. By having a written policy manual outlining the duties of each of the officers and staff of the Company will facilitate better internal control procedures.

Management will continue to monitor and evaluate the effectiveness of the Company’s internal controls and procedures and its internal controls over financial reporting on an ongoing basis and are committed to taking further action and implementing additional enhancements or improvements, as necessary and as funds allow.

ITEM 9A (T). CONTROLS AND PROCEDURES

There were no changes in the Company’s internal controls or in other factors that could affect its disclosure controls and procedures subsequent to the Evaluation Date, nor any deficiencies or material weaknesses in such disclosure controls and procedures requiring corrective actions.

There are no matters required to be reported upon under this Item.

| 23 |

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

Each of our Directors serves until his successor is elected and qualified. Each of our officers is elected by the Board of Directors to a term of one (1) year and serves until his successor is duly elected and qualified, or until he is removed from office. The Board of Directors has no nominating or compensation committees.

The name, address, age and position of our officers and directors is set forth below:

| Name and Address | Position(s ) | Age | ||

Christopher P. Vallos 573 Monroe Blvd Painesville OH 42077 |

Chief Executive Officer, Chief Financial Officer, President and Director (1) | 35 |

| (1) | Christopher Vallos, was appointed as the sole director by the Shareholders on September 3, 2014. Bob Hogarth and Richard W Markle were appointed as directors on November 7, 2012 as, President and the Chief Executive Officer, and Secretary Treasurer, respectively on the same day. Mr. Markle has subsequently resigned. Mr. Hogarth was not reappointed by the Shareholders as a Director. Effective September 3, 2014, Christopher Vallos was appointed Chief Executive Officer, Chief Financial Officer, President, and Secretary-Treasurer of the Company. |

The percentage of common shares beneficially owned, directly or indirectly, or over which control or direction are exercised by the directors and officers of our Company, collectively, is nil.

Background of officers and directors

CHRISTOPHER VALLOS was appointed as sole director of the Company on September 3, 2014, and subsequently made the Chief Executive Officer, Chief Financial Officer, President, and Secretary-Treasurer of the Company on that date.

Mr. Vallos has been the Director of Finance and Marketing for NYC Marketing since 2010. NYC Marketing is a national investor relation and marketing firm that provides comprehensive customized services for publicly traded companies. Mr. Vallos responsibilities included corporate finance, budgeting, forecasting, and business analysis. Prior to joining NYC Marketing, Mr. Vallos was a product manager at Steris Corporation for 3 years.

Board of Directors

Below is a description of the Audit Committee of the Board of Directors. The Charter of the Audit Committee of the Board of Directors sets forth the responsibilities of the Audit Committee. The primary function of the Audit Committee is to oversee and monitor the Company’s accounting and reporting processes and the audits of the Company’s financial statements.

| 24 |

Our audit committee is comprised of Christopher Vallos, our President and Chairman of the Audit Committee whom is not independent. Christopher Vallos cannot be considered an “audit committee financial expert” as defined in Item 401 of Regulation S-B.

Apart from the Audit Committee, the Company has no other Board committees.

Since inception on January 18, 2007, our Board has conducted its business entirely by consent resolutions and has not met, as such.

Significant Employees

We have not paid employees as such. Our Officers and Directors fulfill many of the functions that would otherwise require TNX to hire employees or outside consultants.

We will have to engage the services of certain consultants to assist in continuation of the exploration of our previous mineral claims and to prepare a report on the Lucky Thirteen Claim. Such consultant will responsible for hiring and supervising, the exploration work on the Company’s claims in the near future. This individual will be responsible for the completion of the geological work and, therefore, will be an integral part of our operations although he or she will not be considered an employee either on a full time or part time basis. This is because our exploration programs will not last more than a few weeks and once completed this individual will no longer be required. We have not identified any individual who would work as a consultant for us.

Family Relationships

None

Involvement in Certain Legal Proceedings

To the knowledge of the Company, during the past five years, none of our directors or executive officers:

| (1) | has filed a petition under the federal bankruptcy laws or any state insolvency law, nor had a receiver, fiscal agent or similar officer appointed by the court for the business or property of such person, or any partnership in which he was a general partner at or within two years before the time of such filings; |

| (2) | was convicted in a criminal proceeding or named subject of a pending criminal proceeding (excluding traffic violations and other minor offenses); |

| (3) | was the subject of any order, judgment or decree, not subsequently reversed, suspended or vacated, of any court of competent jurisdiction, permanently or temporarily enjoining him from or otherwise limiting, the following activities: |

(i) acting as a futures commission merchant, introducing broker, commodity trading advisor, commodity pool operator, floor broker, leverage transaction merchant, associated person of any of the foregoing, or as an investment advisor, underwriter, broker or dealer in securities, or as an affiliate person, director or employee of any investment company, or engaging in or continuing any conduct or practice in connection with such activity;

(ii) engaging in any type of business practice; or

(iii) engaging in any activities in connection with the purchase or sale of any security or commodity or in connection with any violation of federal or state securities laws or federal commodities laws;

| 25 |

| (4) | was the subject of any order, judgment, or decree, not subsequently reversed, suspended, or vacated, of any federal or state authority barring, suspending or otherwise limiting for more than 60 days the right of such person to engage in any activity described above under this Item, or to be associated with persons engaged in any such activities; |

| (5) | was found by a court of competent jurisdiction in a civil action or by the SEC to have violated any federal or state securities law, and the judgment in such civil action or finding by the SEC has not been subsequently reversed, suspended, or vacated. |

| (6) | was found by a court of competent jurisdiction in a civil action or by the Commodity Futures Trading Commission to have violated any federal commodities law, and the judgment in such civil action or finding by the Commodity Futures Trading Commission has not been subsequently reversed, suspended or vacated. |

ITEM 11. EXECUTIVE COMPENSATION

Compensation to our directors and officers was paid as follows:

Summary Compensation Table

| Long Term Compensation | ||||||||||||||||||||||||||||

| Annual Compensation | Awards | Payouts | ||||||||||||||||||||||||||

| (a) | (b) | (c) | (e) | (f) | (g) | (h) | (i) | |||||||||||||||||||||

| Name

and Principal position | Year | Salary | Other annual Comp. ($) | Restricted stock awards ($) | Options/ SAR (#) | LTIP payouts ($) | All other compensation ($) | |||||||||||||||||||||

| Christopher Vallos | 2014 | -0- | -0- | -0- | -0- | -0- | -0- | |||||||||||||||||||||

| Bob Hogarth | 2014 | -0- | -0- | -0- | -0- | -0- | -0- | |||||||||||||||||||||

| 2013 | -0- | -0- | -0- | -0- | -0- | -0- | ||||||||||||||||||||||

| Richard W. Markle | 2013 | -0- | -0- | -0- | -0- | -0- | -0- | |||||||||||||||||||||

| 2012 | -0- | -0- | -0- | -0- | -0- | -0- | ||||||||||||||||||||||

| Edwin G. Morrow | 2011 | -0- | 16,500 | 45,000 | -0- | -0- | -0- | |||||||||||||||||||||

| President, CEO and | 2012 | -0- | 16,000 | -0- | -0- | -0- | -0- | |||||||||||||||||||||

| Director | 2013 | -0- | 4,500 | -0- | -0- | -0- | -0- | |||||||||||||||||||||

| Robert Malasek | 2011 | -0- | 16,500 | 45,000- | -0- | -0- | -0- | |||||||||||||||||||||

| Secretary Treasurer, | 2012 | -0- | 16,000 | -0- | -0- | -0- | -0- | |||||||||||||||||||||

| CFO and Director | 2013 | -0- | 4,500 | -0- | -0- | -0- | -0- | |||||||||||||||||||||

| 26 |

Compensation of Directors

We have no standard arrangement to compensate directors for their services in their capacity as directors. Directors are not paid for meetings attended. All travel and lodging expenses associated with corporate matters are reimbursed by us, if and when incurred.

Consulting Agreements with Executive Officers and Directors

There is no consulting agreement with the Company’s director. The previous director, Bob Hogarth was unpaid. There were consulting agreements with both of the previous officers or directors. Under their respective agreements with Ed Morrow and Richard Malasek, the directors were to be paid $1,500 per month each and each received 100,000 shares upon entering into these agreements.

Stock Option Plan

We have never established any form of stock option plan for the benefit of our directors, officers or future employees. We do not have a long-term incentive plan nor do we have a defined benefit, pension plan, profit sharing or other retirement plan.

Bonuses and Deferred Compensation

None

Compensation Pursuant to Plans

None

Pension Table

None

Termination of Employment

There are no compensatory plans or arrangements, including payments to be received from us, with respect to any person named in Summary of Compensation set out above which would in any way result in payments to any such person because of his resignation, retirement, or other termination of such person’s employment with us, or any change in control of us, or a change in the person’s responsibilities following a change in control of us.

Compliance with Section 16 (a) of the Exchange Act

We know of no director or officer, (“Reporting Person”) that failed to file any reports required to be furnished pursuant to Section 16(a). We do not know whether the beneficial owner of more than ten percent of any class of equity securities of our stock registered pursuant to Section 12 (“Reporting Person”) has filed any reports required to be furnished pursuant to Section 16(a).

ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

The following table sets forth, as at May 1, 2015, the total number of shares owned beneficially by each of our directors, officers and key employees, individually and as a group, and the present owners of 5% or more of our total outstanding shares. The shareholders listed below have direct ownership of his shares and possesses sole voting and dispositive power with respect to the shares.

| 27 |

| Title or Class | Name and Address of Beneficial Owner (1) | Amount of Beneficial Ownership (2) | Percent of Class | |||||||

| Common Stock | NMM Consulting, Ltd.(2) 400-116 Cambie Street, Vancouver, BC V6B 2M8 Canada | 23,625,000 | 52.4 | % | ||||||

| Common Stock | Greater than 5% shareholders as a Group (1 person) | 23,625,000 | 52.4 | % | ||||||

| (1) | Unless otherwise noted, the security ownership disclosed in this table is of record and beneficial. |

| (2) | Beneficially owned by Tyler Powell, of the same address |

| (3) | Under Rule 13-d of the Exchange Act, shares not outstanding but subject to options, warrants, rights, conversion privileges pursuant to which such shares may be acquired in the next 60 days are deemed to be outstanding for the purpose of computing the percentage of outstanding shares owned by the person having such rights, but are not deemed outstanding for the purpose of computing the percentage for such other persons. None of our officers or directors has options, warrants, rights or conversion privileges outstanding. |

We do not know of any other shareholder who has more than 5 percent of the issued shares.

The number of shares under Rule 144 is 23,925,000.

Our largest shareholders, NMM Consulting Ltd, own, 23,625,000 issued and outstanding shares of our common stock. All of these shares are “restricted shares” as that term is defined in Rule 144 of the Rules and Regulations of the SEC promulgated under the Securities Act. Under Rule 144, shares can be publicly sold, subject to volume restrictions and restrictions on the manner of sale, commencing one year after their acquisition.

There are no voting trusts or similar arrangements known to us whereby voting power is held by another party not named herein. We know of no trusts, proxies, power of attorney, pooling arrangements, direct or indirect, or any other contract arrangement or device with the purpose or effect of divesting such person or persons of beneficial ownership of our common shares or preventing the vesting of such beneficial ownership.

Description of Our Securities

We have only common shares authorized and there are no preferred shares or other forms of shares. Our authorized common stock consists of 500,000,000 shares of common stock, par value $0.001 per share. The holders of our common stock:

| ● | have equal ratable rights to dividends from funds legally available therefore, when, as, and if declared by our Board of Directors; |

| ● | are entitled to share ratably in all of our assets available for distribution upon winding up of our affairs; and |

| ● | do not have preemptive, subscription or conversion rights and there are no redemption or sinking fund provisions or rights; and |

| ● | are entitled to one non-cumulative vote per share on all matters on which shareholders may vote at all meetings of shareholders. |

| 28 |

The shares of common stock do not have any of the following rights:

| ● | preference as to dividends or interest; |

| ● | preemptive rights to purchase in new issues of shares; |

| ● | preference upon liquidation; or |

| ● | any other special rights or preferences. |