Attached files

| file | filename |

|---|---|

| EX-31.2 - CERTIFICATION - American Sands Energy Corp. | amse_10k-ex3102.htm |

| EX-31.1 - CERTIFICATION - American Sands Energy Corp. | amse_10k-ex3101.htm |

| EX-23.1 - CONSENT - American Sands Energy Corp. | amse_10k-ex2301.htm |

| EX-32.1 - CERTIFICATION - American Sands Energy Corp. | amse_10k-ex3201.htm |

| EX-32.2 - CERTIFICATION - American Sands Energy Corp. | amse_10k-ex3202.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended March 31, 2015 | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 000-53167

American Sands Energy Corp.

(Exact name of registrant as specified in its charter)

| Delaware | 87-0405708 |

| (State or other jurisdiction of incorporation or organization) | (IRS employer identification number) |

| 201 S. Main St., Suite 1800, Salt Lake City, UT | 84111 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (801) 536-6140

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, Par Value $0.001

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes x No o

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | |

| Non-accelerated filer | o | Smaller reporting company | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the average bid and asked price of such common equity as of the last business day of the registrant’s most recently completed second fiscal quarter was $10,521,622.

The number of shares outstanding of the registrant’s common stock on June 24, 2015, was 33,393,828.

DOCUMENTS INCORPORATED BY REFERENCE

| Document Description | 10-K Part | |

| Portions of the Registrant's proxy or information statement related to its 2015 Annual Meeting of Stockholders to be filed pursuant to Regulation 14A or 14C within 120 days after Registrant's fiscal year end of March 31, 2015 are incorporated by reference into Part III of this Report. | III |

Table of Contents

| Page | ||

| PART I | ||

| ITEM 1. BUSINESS | 2 | |

| ITEM 1A. RISK FACTORS | 8 | |

| ITEM 1B. UNRESOLVED STAFF COMMENTS | 16 | |

| ITEM 2. PROPERTIES | 16 | |

| ITEM 3. LEGAL PROCEEDINGS | 18 | |

| ITEM 4. MINE SAFETY DISCLOSURES | 18 | |

| PART II | ||

| ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 19 | |

| ITEM 6. SELECTED FINANCIAL DATA | 19 | |

| ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 19 | |

| ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 22 | |

| ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 22 | |

| ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 22 | |

| ITEM 9A. CONTROLS AND PROCEDURES | 22 | |

| ITEM 9B. OTHER INFORMATION | 23 | |

| PART III | ||

| ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 24 | |

| ITEM 11. EXECUTIVE COMPENSATION | 24 | |

| ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 24 | |

| ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE | 24 | |

| ITEM 14. PRINCIPAL ACCOUNTANT FEES AND SERVICES | 24 | |

| PART IV | ||

| ITEM 15. EXHIBITS, FINANCIAL STATEMENTS, SCHEDULES | 25 | |

| SIGNATURES | 28 | |

| i |

Forward-Looking Statements

The statements contained in this annual report on Form 10-K that are not historical facts represent management’s beliefs and assumptions based on currently available information and constitute “forward-looking statements.” All statements, other than statements of historical or present facts, including the information concerning our future operations, business strategies, need for financing, competitive position, potential growth opportunities, ability to retain and recruit personnel, the effects of competition and the effects of future legislation or regulations are forward-looking statements. Forward-looking statements can be identified by the use of forward-looking terminology such as the words “believes,” “intends,” “may,” “should,” “anticipates,” “expects,” “could,” “plans,” or comparable terminology or by discussions of strategy or trends. Although we believe that the expectations reflected in such forward-looking statements are reasonable, such statements by their nature involve risks and uncertainties that could significantly affect expected results, and actual future results could differ materially from those described in such forward-looking statements.

Among the factors that could cause actual future results to differ materially are the risks and uncertainties discussed in this report. While it is not possible to identify all factors, we continue to face many risks and uncertainties including, but not limited to, changes in the general economic environment; a downturn in the securities markets; and/or uncertainties associated with our ability to obtain operating capital. Should our underlying assumptions prove incorrect or the consequences of the aforementioned risks worsen, actual results could differ materially from those expected. We disclaim any intention or obligation to update publicly or revise such statements whether as a result of new information, future events or otherwise.

Throughout this report, unless otherwise designated, the terms “we,” “us,” “our,” “the Company” and “our company” refer to American Sands Energy Corp., a Delaware corporation, and its wholly owned subsidiary, Green River Resources, Inc., a Utah corporation.

PART I

ITEM 1. Business

Overview

American Sands Energy Corp. (“ASEC”) is a development stage company that proposes to engage in the clean extraction of bitumen from oil sands prevalent in the Mountain West region of North America using proprietary technology. Since the project’s inception, we have been engaged in the business of acquiring and developing oil sand assets and technologies used to separate the oil contained in oil sands. The Company anticipates that its primary operations will include the mining of oil sands, the separation of oil products therefrom and the sale of oil and oil by-products.

We have obtained a license for a hydrocarbon extraction process that separates oil and other hydrocarbons from sand, shale, dirt and other substances, without leaving behind toxins or other contaminants. We are currently developing our first project on certain hydrocarbon and mineral leases which cover approximately 1,760 acres near Sunnyside, Utah (the “Sunnyside Project”). We have filed an application for a Large Mine Permit with the Utah Department of Oil, Gas & Mining and an application for a Ground Water Discharge Permit (with related Construction Permit) with the Utah Department of Water Quality, which, if granted, will allow the Company to move forward with development of operations on the Sunnyside Project.

To date, we have acquired extensive bitumen resources, have successfully operated a pilot plant using our process technology on oil sands ore from our bitumen resources. This work included:

| · | retaining a leading engineering firm in the North American oil sands extraction industry, AMEC BDR Limited, to complete an engineering and feasibility study with respect to a pilot plant capable of producing 3,000 barrels of oil per day; |

| · | engaging a mining engineering firm to prepare a mine plan and feasibility study; |

| · | retaining an engineering firm to demonstrate the technology through the pilot plant; and |

| · | performing pilot test runs in our pilot plant. |

The pilot plant test runs were successful, removing in excess of 99% of the bitumen from the sand and leaving less than the two parts per million (“ppm”) of solvent in the sand. This means that the sand is suitable to be put back into the environment without tailing ponds or other environmental restrictions. Based on additional findings from the recent pilot plant tests and recommendations from our engineers and consultants, we working on the plans for building on to the pilot plant and completing a commercial plant capable of producing 10,000 barrels of oil per day (the “Commercial Facility”). We have submitted applications for mining, environmental and other permits required to operate a large mine on our leases to extract oil sand ore, and to build and operate the Commercial Facility. Based on the information from our consultants, we believe that additional financing of approximately $150 million will be required to procure and install the necessary equipment to begin operation of the Commercial Facility and related mining operations.

| 2 |

Test Results

We have performed lab and pilot plant tests on oil sands from the Utah Green River Formation in which the Sunnyside Project is located to prove the viability of the technology and to understand several key elements in the process. Initial pilot plant test runs were conducted in 2006-2007. We hired AMEC BDR, to witness the initial pilot plant tests and to manage the lab work and review the results. In addition to the initial pilot test, we have run pilot tests on a new system designed by SRS Engineering International during July through September of 2012, and May through June of 2013. In connection with those tests, we ran oil sands from Utah and Africa to acquire additional information on the efficiency of the solvent in removing the bitumen from the sand, the recovery of solvent from the bitumen and sand, and the overall efficiency and energy use of the system. The current test results are summarized as follows:

| · | Virtually all of the bitumen was separated from the sand, leaving the sand “oil” free. |

| · | The compositional characteristics of the bitumen were not altered by the process; therefore, management believes the bitumen will be suitable for upgrading and refining to saleable products by conventional refining technology. |

| · | The sand product contained less than 2 ppm of solvent residue, presents no environmental liability, and can be returned to the mine site or sold. |

| · | Solvent losses to the bitumen product were insignificant. Consequently, because the solvent is recycled with minimal loss in a closed loop system, make-up solvent costs should be minimal. |

| · | Our process works on oil sands from other locations in the world. This may allow us to use our process in other locations around the world where other “oil wet” oil sands are located. |

Leases and Resources

Of the 24 states in the United States that contain oil sand deposits, approximately 90% of the USGS mapped mineable resource is located in Utah, where in excess of 25 billion barrels of oil are in place. There are eleven oil sands deposit areas located in Utah. The seven major areas are Sunnyside, P. R. Spring, Asphalt Ridge, White Rocks, Tar Sand Triangle, Circle Cliffs, and Hill Creek. Three of these seven areas, Tar Sand Triangle, Circle Cliffs, and Hill Creek, have substantial constraints to resource development including environmental drawbacks related to their location on Indian Reservations and/or National Parks, significant overburden, lack of rich ore, and high sulfur content. The prime oil sand properties include Sunnyside, P. R. Spring, Asphalt Ridge and White Rocks.

We have obtained four leases in the Sunnyside area, on private property. We currently hold:

| · | two leases for an undivided 60% interest pursuant to two freehold hydrocarbon and mineral lease agreements in Section 2, East Half and North West quarters of Section 3 Township 14 South, Range 14 East, SLM containing approximately 1,120 acres; and |

| · | two leases for an undivided 21.67% interest pursuant to two freehold hydrocarbon and mineral lease agreements in the North West quarter of Section 3, East half and North West quarter of Section 10, Township 14, Range 14 East, SLM containing approximately 640 acres. |

The lease for an undivided 40% interest in the 1,120 acre property has a primary term ending December 31, 2020 while the lease for the remaining undivided 20% interest has a primary term ending on December 31, 2020. The lease for an undivided 16.67% interest in the 640 acre property has a primary term ending December 31, 2019 and the remaining 5% interest in the 640 acres has a primary term ending December 31, 2020. All leases are automatically extended thereafter for so long as an average of 500 barrels of oil is produced per day, subject to certain acceptable interruptions.

We have reviewed previous resource estimates prepared for Chevron and Amoco, as well as USGS estimates of mineable oil sands on our leases. In addition, we retained an outside firm to provide us with a Resource Audit and Classification report which was done in accordance with the provisions of the National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities (“NI 51-101”) and prepared as of May 29, 2009 (the “RAC Report”). Due to the nature of the resource and the stage of development, we do not have any proven reserves (within the meaning of Rule 4-10 of the SEC’s Regulation S-X) in Rule 4-10(a) of the SEC’s Regulation S-X to report.

| 3 |

The RAC Report prepared for us under NI 51-101 follows the standards set out in the Canadian Oil and Gas Evaluation (“COGE”) Handbook, prepared jointly by the Society of Petroleum Evaluation Engineers and the Canadian Institute of Mining, Metallurgy & Petroleum. Those standards require that the evaluator plan and perform an evaluation to obtain reasonable assurance as to whether the reserves are free of material misstatement. An evaluation must also include an assessment as to whether the reserves data are in accordance with the principles and definitions presented in the COGE Handbook. The estimate provided in the RAC Report is classified as contingent resources according to the guidelines set forth in NI 51-101 and COGE. The project resource calculation is contingent upon completion of additional exploration drilling, processing and extraction analysis, detailed economic analysis, evolution of legal mining rights, and environmental evaluations. There is no certainty that the project will be commercially viable to produce any portion of the resource. As a result of the differences between the U.S. rules and Canadian standards governing disclosure of reserve or resource estimates, differing estimates of reserves or resources available under our leases are reported, and may in the future be reported, between our website and our periodic reports filed with the SEC.

Our Process

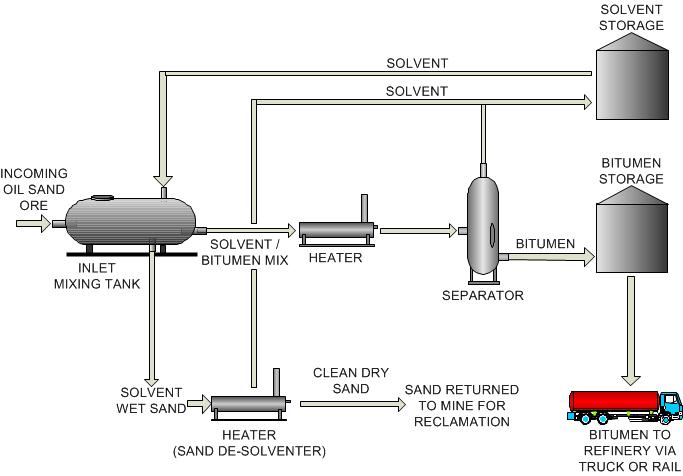

The following diagram demonstrates the stages of the process to remove bitumen from the oil sands using our proprietary bitumen recovery system:

Our process starts with the mixing of oil sand ore with a proprietary solvent. The solvent immediately separates the hydrocarbons contained in the ore from the inorganic insoluble material such as sand, rock and clay. We utilize much less heat than traditional or competing technologies.

The liquid hydrocarbon/solvent mix is then separated from the clean sand by gravity. The sand is heated to evaporate the solvent and the resulting solvent vapors are condensed and reused. The clean sand can be returned to the mine site as reclamation material or sold for industrial purposes.

The liquid hydrocarbon/solvent mix is subject to a simple, refluxed, low pressure, medium temperature distillation process to separate the solvent from the recovered hydrocarbon. The solvent distilled from the recovered hydrocarbon is condensed and reused. The extracted bitumen is transported to a refinery.

Since the process does not generate waste, tailing ponds and other environmental hazards are eliminated from the process, with the attendant reduction in costs and effects on the environment.

In connection with the engineering and development of the technology, we incurred costs of approximately $158,576 and $376,170 for the fiscal years ended March 31, 2015 and 2014, respectively.

| 4 |

Resource Base and Mine Plan

We have reviewed previous resource estimates prepared for Chevron and Amoco, as well as USGS estimates of mineable oil sands on our leases. In addition, we retained an outside firm to provide us with the RAC Report described above.

We also have access to and have reviewed detailed mining and operational plans prepared for Amoco in the mid-1990s with respect to our leases. These resources have been helpful in developing our mine and operational plan.

Initially, we intend to obtain our oil sands through underground mining. We have completed an initial mine plan and cost estimate for the mine. The proposed mine plan layout is for an average daily production of 10,000 tons. Mining would occur year-round, with approximately one month overall allowed for shut-downs due to maintenance and repairs. Anticipated yearly mined tonnages include: 10,000 tons of oil sands mined per day; 2,700,000 tons per year (based on 270 days/year of production). Based upon the amount of estimated oil sands contained in the oil sand zone and expected grade, at this mining rate the life of the mine is expected to be between 20 and 30 years.

We intend to use a contract miner to initially mine the oil sands. Contract mining is an accepted practice in this area and has been used in coal mines as well as to mine tar sands for use in road paving. Because of recent coal mine shut downs, there is both excess capacity and excess mining equipment in the area. Mining equipment will consist of dozers, haul trucks, loaders, water trucks, and service trucks. Mined ore will be hauled by trucks via a haul road to the process area, where it can be either discharged directly to the inlet hopper or placed in a temporary storage pile adjacent to the processing facility for off-shift processing. Generally, a 3-day reserve supply of ore will be maintained in stockpiles at the processing facility.

The clean sand generated from processing the oil sands will be stored on surface (unless sold) under our mine plan. We have designated an area on surface to accommodate approximately 3 years of sand. The first 3 years of processed sand will be stored on surface. After that, we anticipate that the processed sand will be disposed of underground in mined out mining panels. The processed sand area will be designed to store approximately 6,000,000 cubic yard of processed sand. The processed sand will be transported to the storage site in the same trucks used for ore haulage.

Overall Market for Oil and Petroleum Products

According to the International Energy Agency (“IEA”), estimates of global petroleum and other liquid fuels consumption grew to 91.2 million bbl/d in 2013. IEA expected that world liquid fuels consumption would grow by 0.8 million bbl/d in 2014, followed by 1.0 million bbl/d growth in 2015, resulting in total world consumption of 93.1 million bbl/d in 2015. Countries outside the Organization for Economic Cooperation and Development (“OECD”) will make up almost all of the growth in consumption forecasted over the next two years, with the largest increases coming from China, other Asian countries, Latin America and the Middle East. The IEA believes 2014 marked the first time that non-OECD demand exceeded OECD demand.

The EIA expects non-OPEC production to grow by 0.7 million bbl/d in 2015 and by 0.4 million bbl/d in 2016, in part because of lower projected oil prices. The slower growth in total non-OPEC supply is largely attributable to slower production growth in the United States and Canada and declining production in Europe and Eurasia. After remaining relatively flat in 2015, production in Eurasia is projected to decline by more than 0.1 million bbl/d in 2016. The projected decline reflects reduced investment in Russia's oil sector stemming from low oil prices and international sanctions.

Projected Markets for the Company’s Oil

The primary product we will produce will be a heavy oil called bitumen. There are numerous refineries within our potential marketing area. Within 150 miles of the Salt Lake City area, there are a number of refineries with cumulative total daily capacity of approximately 175,000 barrels per day, according to the U.S. Energy Administration. These refineries are able to refine bitumen and have sufficient capacity to accept our product. Additionally, refineries in Colorado, Wyoming and New Mexico have daily combined capacity of approximately 417,000 barrels per day.

Pricing is typically benchmarked to leading crude price indices. Historically, bitumen has traded at a discount to West Texas Intermediate (“WTI”) of between 22-30%. Primary factors we will consider when going to market with our product are price and transportation costs. Because of the transportation cost associated with smaller volumes of product, we expect that our entire estimated output from our Commercial Facility will be delivered to the Salt Lake City refining center. If we are able to expand facilities and production, rail transport may become viable, which may open the opportunity for supplying product to multiple refineries with more distant locations versus Salt Lake City.

| 5 |

Government Regulation

We have commenced the process of obtaining the regulatory approvals required in connection with our project. We are committed to environmental responsibility and to meeting or exceeding best practices for environmental stewardship in our industry. We support the principle of sustainable development through adaptive management and we are working with stakeholders in the community, government and industry to protect and sustain air, land and aquatic resources in the region.

The key environmental issues to be managed in the development of our project encompass surface disturbance on the terrestrial ecosystem, effects on traditional land use and historical resources, and effects on wildlife populations and other natural resources. Because the commercial facility to be constructed will be a closed loop system, the only emissions anticipated will be from power generation. Only clean sand and bitumen will be produced.

We are committed to operating our project to achieve compliance with applicable statutes, regulations, codes, regulatory approvals and, to the extent practicable, government guidelines. Where the applicable laws are not clear or do not address all environmental concerns, management will apply appropriate internal standards and guidelines to address such concerns. In addition to complying with statutes, regulations, codes and regulatory approvals and exercising due diligence, we will strive to continuously improve the overall environmental performance of the operation and products.

There are a number of state and federal permits required in connection with the large permit necessary to commence principal operations. The Company has filed for the following permits, which, if granted, will allow the Company to move forward with development of operations on the Sunnyside Project:

| · | Notice of Intent to Commence Large Mining Operations including SWPPP (DOGM) |

| · | Utah Groundwater Discharge Permit including SAP and QAPP (DWQ) |

| · | Construction Permit (DWQ) |

| · | Air Small Source Exemption Registration (DAQ) |

These permits require a number of studies and/or clearances. The Large Mine Permit we applied for requires engineering and operation plans and posting of a reclamation bond. The Groundwater Discharge Permit and Construction permit we applied for requires engineering and operations plans to ensure that the Company does not contaminate ground water. We have contracted with an environmental consulting firm and a mine engineering firm to obtain the required studies and engineering and have filed applications for the above listed permits. The permits are currently being reviewed by the relevant agencies of the State of Utah. We also intend to seek the necessary business license from Carbon County and approvals of the county planning and zoning authorities and anticipate being able to obtain the necessary license and approval from Carbon County prior to receiving the large mining permit.

Competition

To our knowledge, there are currently two other companies intending to operate oil sands mining and extraction facilities in the State of Utah; U.S. Oil Sands, a Canadian company, which has publicly announced that it intends to commence operations on a 62-acre plant in eastern Utah to remove bitumen from oil sands using a citrus-based solvent in the fourth quarter of 2015, and MCW Oil Sands Recovery, LLC, which has announced its intention to operate a 250 barrel per day plant near Vernal, Utah. To our knowledge, these companies are not in production and may require significant capital to commence operations. Additionally, many of these companies are using processes that are unproven in commercial production.

Our process is efficient, cost effective, and has a small environmental footprint when compared to other technologies currently known or used for the separation of oil sands. By comparison, the processes utilized in Canada for the extraction of bitumen from oil sand consume significant amounts of water and have a significant environmental impact. In comparing our process to known oil sands extraction systems, we believe our licensed proprietary system offers a significantly reduced operating environmental impact. Our process significantly mitigates or eliminates environmental impacts typically associated with oil sand projects including:

| o | Release of Volatile Organic Hydrocarbons (“VOC’s”): The solvent losses resulting from the operation of our system are minor. The system does not release any solvent to the environment. Solvent consumed by the process is recovered and conserved during the processing of the oil sands. In addition the process does not produce gases to a flare or vent system of any kind. |

| o | Substantial Water consumption/contamination: Our process neither consumes nor produces any water. It is a dry process and therefore no water is taken from or returned to the environment. |

| o | Emissions: The process can be powered by natural gas or electricity. If it were powered by electricity, emissions associated with the energy consumption of the process could be controlled through standard power plant emission control systems. As noted above, the deposit under lease to GRI is currently serviced by electrical power lines. |

| o | Hydrocarbon and water wet tailings stream: Typical oil sands operations produce a waste stream of spent sand that contains a significant amount of residual hydrocarbons and water. The sand product from our process is dry and essentially free of hydrocarbons, either natural or induced through the solvent wetting process. It is directly suitable for use in reclamation efforts or can be sold as a value added product without further processing. Use of the sand in the reclamation process provides for the return of the mined material to the mine site (less the naturally occurring hydrocarbons) with no loss of material. |

| 6 |

We believe our process is efficient, cost effective, and simple when compared to other technologies currently known or used for the separation of oil sands. By comparison, the processes utilized in Canada for the extraction of bitumen from oil sand consume significant amounts of water and, therefore, have a significant environmental impact. Approximately 3/4 of a barrel of tailings is produced for every barrel of bitumen produced by Canadian oil sands producers. Consequently, there are thousands of acres of tailing ponds located at Canadian oil sands operations produced as a direct result of the oil sand extraction process. This is one reason why oil sands are being questioned as a source of energy for the United States. Our process uses little or no water, and recaptures virtually all of the solvent used, resulting in only clean sand as a byproduct.

Production costs using our method to recover bitumen are believed to be significantly lower than those used by established producers of bitumen from oil sands in Canada. In addition, the projected capital cost for our Commercial Facility would be significantly lower than the cost of capital for a traditional oil sands project. Thus, our competitive advantages are an environmentally superior process and the ability to be a low-cost producer of high demand energy.

Recent Developments Affecting the Company

Effective January 24, 2012, the Company entered into a License, Development and Engineering Agreement with Universal Oil Recovery Corp. and SRS International (the “License Agreement”) whereby the Company was granted an exclusive non-transferable license to use certain technology in its proposed business to extract bitumen from oil sands. The territory covered by the agreement includes the State of Utah and any other geographic location in which a future designated project is commenced by or through the Company. In conjunction with the License Agreement, the Company terminated its operating agreement with Bleeding Rock. On November 18, 2013, the Company entered into an Amended and Restated License, Development and Engineering Agreement with Universal Oil Recovery LLC (“Amendment”). The Amendment amends and restates the License Agreement. Pursuant to the terms of the Amendment, the previous royalties of 75% on projects outside of Utah and the minimum royalty of $1,000,000 per year on such agreements have been eliminated. Pursuant to the Amendment, the Company will now pay royalties on projects outside of Utah of 15% of the net fees (net of all costs other than general and administrative expenses) collected by the Company on any license of the technology. In addition, the $25,000 per month management fee is eliminated until a permanent financing is closed (minimum of $25,000,000), at which time the payment will be reinstated. In consideration of the amendment, the Company issued to Universal Oil Recovery LLC (“UOR”), 575,000 warrants to purchase common stock of the Company for $0.01 per share, exercisable for ten years (see Note 11). The Company agreed to make certain payments to UOR. The term of the License Agreement is for 20 years and thereafter so long as production of products using the technology is commercially and economically feasible.

In conjunction with entering into the License Agreement, we also entered into a Termination Agreement dated January 24, 2012, with Bleeding Rock (the “Termination Agreement”). The purpose of the Termination Agreement was to terminate the Operating Agreement dated May 31, 2005, as amended, between Bleeding Rock and GRI (the “Operating Agreement”). Pursuant to the Operating Agreement GRI had obtained the rights through Bleeding Rock to utilize a process for the development, engineering and extraction of hydrocarbons from oil sands. In light of conversations with potential investors, management determined that having the technology licensed directly to the Company rather than through Bleeding Rock would be beneficial to fund raising prospects. As a result, the Company entered into the License Agreement described above. In partial consideration for Bleeding Rock agreeing to terminate the Operating Agreement, we entered into a royalty agreement with Bleeding Rock. Under the terms of the Gross Royalty Agreement we are obligated to pay a royalty equal to 1.5% of the gross receipts from future projects using the technology, excluding the current project in Sunnyside, Utah. Bleeding Rock subsequently assigned all of its interest in the Gross Royalty Agreement to Hidden Peak Partners LC (“Hidden Peak”), an entity managed and partially owned by Mr. Gibbs. The Termination Agreement also contains mutual releases by the parties relating to the Operating Agreement.

Employees

We currently have three employees; namely, our CEO, William C. Gibbs; our COO, Robin Gereluk; and our CFO, David B. Hardman. Mr. Gibbs and Mr. Gereluk work full time for the Company. Mr. Hardman works part-time on an hourly basis. We also engage consultants and independent contractors as needed.

| 7 |

ITEM 1A. Risk Factors

Our business activities and the oil and gas industry in general, are subject to a variety of risks. If any of the following risk factors should occur, our profitability, financial condition or liquidity could be materially impacted. As a result, holders of our securities could lose part or all of their investment in American Sands Energy Corp.

Risks Related to Our Company and Its Business

Because of our historic losses from operations since inception, there is substantial doubt about our ability to continue as a going concern.

We have incurred recurring losses since the date of inception that have resulted in an accumulated deficit attributable to common stockholders of approximately $$18,000,000 as of March 31, 2015. Although we had approximately $191,000 of available cash as of March 31, 2015, that amount is not adequate to meet our capital expenditure and operating requirements over the next 12 months. In addition, we estimate that we will require approximately $150,000,000 in capital expenditures and working capital to place our properties into production. These factors raise substantial doubt about our ability to continue as a going concern or to commence principal operations. We are dependent upon obtaining funds from investors to meet our cash flow requirements. If we are unsuccessful in doing so, we will be required to substantially revise our business plan or our proposed business could fail.

The impact of disruptions in the global financial and capital markets may significantly affect our ability to obtain financing.

International economic and political conditions, fluctuations in capital markets, changes in production by oil producing countries, and other events have historically caused volatility in commodity prices. We will continue to need further funding to achieve our business objectives. In the past, the issuance of equity or debt securities has been the major source of capital and liquidity for us. Changes in commodity prices as a result of global conditions has a direct impact on our ability to obtain capital. With the recent substantial volatility in oil prices we are finding limited sources of capital for oil development and, as a result, financing may not be available to us on acceptable terms, if at all. If we are unable to fund future operations by way of financing, including public or private offerings of equity or debt securities, our financial condition and results of operations will be adversely impacted. Additionally, these factors, as well as other related factors, may cause decreases in asset values that are deemed to be other than temporary, which may result in impairment losses.

We have not commenced principal operations and have a limited operating history and therefore we cannot ensure the long-term successful operation of our business or the execution of our business plan.

We have not commenced principal mining and production operations. As a result, we have a limited operating history upon which to evaluate our proposed business and prospects. Our proposed business operations will be subject to numerous risks, uncertainties, expenses and difficulties associated with early stage enterprises. Such risks include but are not limited to the following:

| · | the absence of a lengthy operating history; |

| · | insufficient capital to fully realize our operating plan; |

| · | our ability to purchase or lease necessary equipment when required and at reasonable prices; |

| · | our ability to obtain regulatory and environmental approvals of our proposed mines and facilities; |

| · | expected continual losses for the foreseeable future; |

| · | social and political unrest; |

| · | disruptions to transportation routes; |

| · | our ability to anticipate and adapt to developing markets; |

| · | acceptance of our product by consumers; |

| · | limited marketing experience; |

| · | a competitive environment characterized by well-established and well-capitalized competitors; |

| · | the ability to identify, attract and retain qualified personnel; and |

| · | reliance on key personnel. |

Because we are subject to these risks, evaluating our business may be difficult. We may be unable to successfully overcome these risks which could harm our business. Our business strategy may be unsuccessful and we may be unable to address the risks we face in a cost-effective manner, if at all. If we are unable to successfully address these risks our business will be harmed.

| 8 |

Compliance with government regulations and delays in obtaining necessary mining permits and licenses could delay or otherwise adversely affect our proposed business operations.

Our proposed plan to mine and process oil sands is subject to substantial regulation under federal, state and local laws relating to the exploration for, and the development, upgrading, marketing, pricing, taxation, and transportation of oil sands bitumen and related products and other matters. Amendments to current laws and regulations governing operations and activities of oil sands exploration and development operations could have a material adverse impact on our business. In addition, there can be no assurance that income tax laws, royalty regulations, environmental regulations and government incentive programs related to our permits and oil sands exploration licenses, and the oil sands industry generally, will not be changed in a manner which may adversely affect our progress and cause delays, or cause the inability to explore and develop, resulting in the abandonment of these interests.

Permits, licenses and approvals are required from a variety of regulatory authorities at various stages of exploration and development. There can be no assurance that the various government permits, leases, licenses and approvals sought will be granted, that they will be granted in a timely manner, or, if granted, that they will not be cancelled or will be renewed upon expiration. There is no assurance that such permits, leases, licenses and approvals will not contain terms and provisions which may adversely affect our exploration and development activities.

Environmental groups or other third parties may oppose our project

Permits, licenses and approvals are required from a variety of regulatory authorities in connection with the development of our project. In connection with these permits, regulatory agencies often solicit public comment with respect to a proposed project and take into consideration comments received. In addition, third parties in the area of our project, such as property owners, may also object to the project. Objections from these parties may adversely affect our progress and cause delays, result in litigation and/or cause the inability to explore and develop our property or project, resulting in the abandonment of these interests. In addition, there is also no assurance that objections by such parties to our permits, leases, licenses and other required approvals will not result in terms and provisions which may adversely affect the economics of our project or our exploration and development activities.

On May 28, 2015, the Department of Water Quality received a comment letter from Western Resources Associates and Living Rivers, expressing concerns and objecting to the draft Water Discharge Permit published by the Utah Division of Water Quality. The Division of Water Quality will evaluate these comments and concerns and may require amendments to the proposed permit or may decide not to issue the permit. Any amendments to the permit could adversely affect the feasibility and/or economics of the project.

The exploration for and development of oil sands properties is highly competitive.

Oil sands exploration and development involves many risks that even a combination of experience, knowledge and careful evaluation may not be able to overcome. We have no proven or probable reserves of oil sands on our properties. As with any petroleum property, there can be no assurance that commercial deposits of bitumen will be produced from our leased lands in Utah.

Furthermore, the marketability of any resource will be affected by numerous factors beyond our control. These factors include, but are not limited to, market fluctuations of prices, proximity and capacity of processing equipment, equipment and labor availability and government regulations (including, without limitation, regulations relating to prices, taxes, royalties, land tenure, allowable production, importing and exporting of oil and gas, land use and environmental protection). The extent of these factors cannot be accurately predicted, but the combination of these factors may result in us not receiving an adequate return on invested capital.

If we are unable to hire and retain key personnel, we may not be able to implement our plan of operation and our business may fail.

Our success is largely dependent on our ability to continue to hire and retain highly qualified personnel in both management and operations. These individuals may be in high demand and we may not be able to attract the management staff we need. In addition, we may not be able to afford the high salaries and fees demanded by qualified personnel, including fees associated with persons employed by us, or we may fail to retain such employees after they are hired. Our failure to hire and retain key personnel as needed will have a significant negative effect on our business.

We are dependent upon a few key people and the loss of current management would make it difficult for us to implement our current business plan.

Investors must rely upon the ability, expertise, judgment, discretion, integrity and good faith of our management and directors. Our success is dependent upon our management and key personnel. We do not maintain key-man insurance for any of our employees. The unexpected loss or departure of any of our key officers and employees could be detrimental to our future success.

| 9 |

Environmental and regulatory compliance may impose substantial costs on us.

Our proposed operations will be subject to stringent federal, state, and local laws and regulations relating to improving or maintaining environmental quality. Environmental laws often require parties to pay for remedial action or to pay damages regardless of fault. Environmental laws also often impose liability with respect to divested or terminated operations, even if the operations were terminated or divested many years ago.

Our exploration activities are or will be subject to extensive laws and regulations governing prospecting, development, production, exports, taxes, labor standards, occupational health, waste disposal, land use, protection and remediation of the environment, protection of endangered and protected species, operational safety, toxic substances and other matters. Exploration is also subject to risks and liabilities associated with pollution of the environment and disposal of waste products. Compliance with these laws and regulations will impose substantial costs on us and will subject us to significant potential liabilities. In addition, should there be changes to existing laws or regulations, our competitive position within the oil sands industry may be adversely affected, as many industry players have greater resources than we do.

We are required to obtain and are in various stages of obtaining necessary regulatory permits and approvals in order to explore and develop our properties. The absence of a distinct overlying shale formation on portions of our leases may make it more difficult or costly to obtain regulatory approvals. There is no assurance that regulatory approvals for exploration and development of our properties will be obtained at all or with terms and conditions acceptable to us.

We could encounter third-party liability or environmental liability in connection with our proposed operations.

Our proposed operations could result in liability for personal injuries, property damage, oil spills, discharge of hazardous materials, remediation and clean-up costs and other environmental damages. We could be liable for environmental damages caused by previous owners. As a result, substantial liabilities to third parties or governmental entities may be incurred, and the payment of such liabilities could have a material adverse effect on our financial condition and results of operations. The release of harmful substances in the environment or other environmental damages caused by our activities could result in us losing our operating and environmental permits or inhibit us from obtaining new permits or renewing existing permits. We currently have a limited amount of insurance and, at such time as we commence additional operations, we expect to be able to obtain and maintain additional insurance coverage for our operations, including limited coverage for sudden environmental damages, but we do not believe that insurance coverage for environmental damage that occurs over time is available at a reasonable cost. Moreover, we do not believe that insurance coverage for the full potential liability that could be caused by environmental damage is available at a reasonable cost. Accordingly, we may be subject to liability or may lose substantial portions of our properties in the event of certain environmental damage. We could incur substantial costs to comply with environmental laws and regulations which could affect our ability to operate as planned.

The early stage of our bitumen extraction technology increases the risk that we may not be able to successfully implement an oil sands recovery program using this technology.

We have entered into a license agreement under which the licensing entities have agreed to provide technical and engineering assistance in building an oil sands recovery plant based upon their proprietary solvent. This solvent process has not been installed on a project which meets the projected recovery amounts in our business plan. In addition, the process has only been tested in a pilot plant setting and not in full commercial production facility, so that there is limited experience with the technology on which we are basing our plans to develop the Commercial Facility. There is a risk that the Commercial Facility will not be completed on time or on budget or at all. Additionally, there is a risk that the program may have delays, interruption of operations or increased costs due to many factors, including, without limitation: breakdown or failure of equipment or processes; construction performance falling below expected levels of output or efficiency; design errors; challenges to, or inability to access in a timely or economic fashion; contractor or operator errors; non-performance by third-party contractors; labor disputes, disruptions or declines in productivity; increases in materials or labor costs; inability to attract sufficient numbers of workers; delays in obtaining, or conditions imposed by, regulatory approvals; changes in program scope; violation of permit requirements; disruption in the supply of energy; transportation accidents, disruption or delays in availability of transportation services or adverse weather conditions affecting transportation; unforeseen site surface or subsurface conditions; and catastrophic events such as fires, earthquakes, storms or explosions. There is also a risk that the manufacturer of the equipment and components for our Commercial Facility could fail in production due to labor shortages, price increases, or better opportunities with other customers, which would frustrate and delay our effort to build the Commercial Facility and begin production.

| 10 |

We have significant financial obligations under our mining leases, and if we fail to meet those obligations we would lose the mineral resource on which our business plan depends.

Our interest in certain mining leases is conditioned upon the payments of annual rentals, of royalties, minimum yearly investment in development, tax payments, and other obligations to the owners of the leases. If we are unable to make the required payments or meet the necessary obligations, we could default on our lease agreements which could be terminated and which would void our interest in the leases. There is no certainty we will be able to make every payment and meet all obligations required under the respective lease agreements.

If we do not reach production levels by December 31, 2019, our leases may be terminated.

Two of our four leases are conditioned upon reaching the production stage by December 31, 2020 and other two leases require production by December 31, 2019. If we do not attain average productivity of at least 500 bbl/d by these dates, our interest in the leases may be terminated. The ability to attain productivity is conditioned upon factors of which we are not within complete control such as those listed in this Annual Report. There is no certainty we will ever reach the level of production required to keep our interest in these mining leases from becoming void.

We have no proven or probable reserves or resources.

We have not yet established any reserves. There are numerous uncertainties inherent in estimating quantities of bitumen resources and reserves, including many factors beyond our control, and no assurance can be given that the recovery of bitumen will be realized. In general, estimates of resources and reserves are based upon a number of factors and assumptions made as of the date on which the resources and reserves estimates were determined, such as geological and engineering estimates which have inherent uncertainties, the assumed effects of regulation by governmental agencies and estimates of future commodity prices and operating costs, all of which may vary considerably from estimated results. All such estimates are, to some degree, uncertain and classifications of resources and reserves are only attempts to define the degree of uncertainty involved. For these reasons, estimates of reserves and resources, the classification of such resources and reserves based on risk of recovery, prepared by different engineers or by the same engineers at different times, may vary substantially.

Investors are cautioned not to assume that all or any part of a resource is economically or legally extractable.

We may participate in joint ventures and/or strategic alliances to develop and operate our planned business. These partnerships or the failure to establish them could have a material adverse effect on our ability to develop and manage our business. In addition, such undertakings may not be successful.

Our strategy may include plans to participate in joint ventures and other strategic alliances to develop and operate our business and sell our products. We may develop mining operations in part through joint ventures and strategic alliances with other parties as well as with additional outside funding. Joint ventures and strategic alliances may expose us to new operational, regulatory and market risks, as well as risks associated with additional capital requirements. Additionally, we may not be able to identify and secure suitable alliance partners. Even if we identify suitable partners, we may be unable to consummate alliances on terms commercially acceptable to us. If we fail to identify appropriate partners, we may not be able to implement our strategies effectively or efficiently.

In addition to joint venture and strategic alliances, we may raise additional debt and/or equity financing to build and operate our proposed operations. Such capital raises could result in significant dilution to the percentage ownership held by existing stockholders or the failure to secure such capital could impair our ability to execute our business plan.

We anticipate that the cost to build operations on our existing or future properties will be approximately $150,000,000 and we have no current sources for this funding. Offerings using our equity securities or debt instruments convertible into our common stock could require the issuance of a substantial number of additional shares of common stock. These potential offerings and the issuance of additional shares of common stock would have the effect of diluting the percentage ownership of existing stockholders. Moreover, there can be no assurance that such financing will be available, or, if available, that such financing will be at a price that will be acceptable or favorable to us. Failure to generate sufficient revenue or raise additional capital would have an adverse impact on our ability to achieve our longer-term business objectives, and would adversely affect our ability to continue operating as a going concern.

| 11 |

We do not insure against all potential operating risks. We may incur losses and be subject to liability claims as a result of our operations.

We maintain insurance for some, but not all, of the potential risks and liabilities associated with our business. For some risks, we may not obtain insurance if we believe the cost of available insurance is excessive relative to the risks presented. As a result of market conditions, premiums and deductibles for certain insurance policies can increase substantially, and in some instances, certain insurance may become unavailable or available only for reduced amounts of coverage. As a result, we may not be able to renew our existing insurance policies or procure other desirable insurance on commercially reasonable terms, if at all. Although we maintain insurance at levels we believe are appropriate and consistent with industry practice, we are not fully insured against all risks. In addition, pollution and environmental risks generally are not fully insurable. Losses and liabilities from uninsured and underinsured events and delay in the payment of insurance proceeds could have a material adverse effect on our financial condition, results of operations and cash flows.

American climate change legislation could negatively affect markets for crude and synthetic crude oil.

Environmental legislation regulating carbon fuel standards in the United States could result in increased costs and/or reduced revenue. For example, both California and the federal governments have passed legislation which, in some circumstances, considers the lifecycle greenhouse gas emissions of purchased fuel and which may negatively affect our business, or require the purchase of emissions credits, which may not be economically feasible.

Our mining production and delivery operations are subject to conditions and events that are beyond our control, which could result in higher operating costs and decreased production levels.

Our mining operations are planned to be conducted primarily in underground mines and possibly in surface mines. The level of our production is subject to operating conditions or events beyond our control that could disrupt operations, decrease production and affect the cost of mining at particular mines for varying lengths of time. Adverse operating conditions and events that oil and gas producers have experienced in the past include:

| · | unfavorable geologic conditions, such as the thickness of the oil and gas deposits and the amount of rock embedded in or overlying the oil and gas deposit; |

| · | poor mining conditions resulting from geological conditions or the effects of prior mining; |

| · | inability to acquire or maintain, or unexpected delays or difficulties in obtaining, necessary permits or mining or surface rights; |

| · | changes in governmental regulation of the mining industry or the utility industry; |

| · | market conditions could change and mean the sale of the type of oil and gas being produced from our concessions is no longer saleable at an economic price; |

| · | adverse weather conditions and natural disasters; |

| · | accidental mine water flooding; |

| · | labor-related interruptions; |

| · | interruptions due to transportation delays; |

| · | mining and processing equipment unavailability and failures and unexpected maintenance problems; |

| · | accidents, including fire and explosions from methane and other sources; |

| · | surface subsidence from underground mining, which could result in collapsed roofs at our underground mines, among other difficulties; |

| · | unavailability of mining equipment and supplies and increases in the price of mining equipment and supplies; |

| · | unexpected maintenance problems or key equipment failures; and |

| · | increased or unexpected reclamation costs. |

If any of these or similar conditions or events occur in the future at any of the mines we plan to develop or affect deliveries of our product to customers, they may increase our costs of mining and delay or halt production at particular mines or sales to our customers, either permanently or for varying lengths of time, which could adversely affect our results of operations, cash flows and financial condition. Our current insurance coverage would cover some but not all of these risks.

| 12 |

A substantial or extended decline in oil and gas prices could reduce our revenues and the value of our oil and gas resources.

Our results of future operations will be dependent upon the prices we receive for our oil and gas and other products as well as our ability to improve productivity and control costs. Declines in prices could adversely affect our results of operations. The prices charged for oil and gas depend upon factors beyond our control, including:

| · | the supply of, and demand for, domestic and foreign oil and gas; |

| · | the price elasticity of supply; |

| · | the demand for oil and gas; |

| · | the proximity to and the capacity and cost of transportation facilities; |

| · | governmental regulations and taxes; |

| · | air emission standards for oil refineries; |

| · | regulatory, legislative, administrative and judicial decisions; |

| · | the price and availability of alternative fuels, including the effects of technological developments; and |

| · | the effect of worldwide energy conservation measures. |

Decreased demand for oil and gas could result in declines in oil and gas prices and require us to increase productivity and lower costs in order to maintain our margins. If we are not able to maintain our margins, our operating results could be adversely affected. Therefore, price declines may adversely affect our operating results for future periods and our ability to generate cash flows necessary to improve productivity and invest in operations.

Inaccuracies in our estimates of oil sands deposits could result in lower than expected revenues and higher than expected costs.

We will base our oil sands deposit information on engineering, economic and geological data assembled and analyzed by various engineers and geologists we retain for that purpose. The estimates of oil sands deposits as to both quantity and quality will be continually updated to reflect the production of bitumen from the deposits and new drilling or other data received. There are numerous uncertainties inherent in estimating quantities and qualities of oil sands deposits and costs to process these deposits, including many factors beyond our control. Estimates of economically recoverable bitumen and net cash flows necessarily depend upon a number of variable factors and assumptions, all of which may vary considerably from actual results, such as:

| · | geological and mining conditions and/or effects from prior mining activities that may not be fully identified by available exploration data or that may differ from experience, in current operations; | |

| · | the assumed effects of regulation, including the issuance of required permits, and taxes by governmental agencies and assumptions concerning oil and gas prices, operating costs, mining technology improvements, severance and excise tax, development costs and reclamation costs; | |

| · | historical production from the area compared with production from other similar producing areas; and | |

| · | assumptions concerning future oil and gas prices, operating costs, capital expenditures, severance taxes and development and reclamation costs. |

For these reasons, estimates of the economically recoverable quantities and qualities attributable to any particular group of properties, classifications of reserves and non-reserve deposits based on risk of recovery and estimates of net cash flows expected from particular reserves prepared by different engineers or by the same engineers at different times may vary substantially and vary materially from estimates. As a result, these estimates may not accurately reflect actual reserves or non-reserve deposits. Any inaccuracy in our estimates related to our deposits could result in lower than expected revenues, higher than expected costs and decreased profitability.

We compete with numerous alternative and “green” energy industries.

The U.S. and international petroleum industry is highly competitive in all aspects, including the exploration for, and the development of, new sources of supply, the acquisition of oil interests and the distribution and marketing of petroleum products.

The petroleum industry also competes with other industries in supplying energy, fuel and related products to consumers. Some of these industries benefit from lighter regulation, lower taxes and subsidies. In addition, certain of these industries are less capital intensive.

A number of competing companies are engaged in the oil sands business and are actively exploring for and delineating their resource bases. Some of our competitors have announced plans to begin production of synthetic crude oil, or to expand existing operations. If these plans are effected, they could materially increase the supply of synthetic crude oil and other competing crude oil products in the marketplace and adversely affect plans for development of our lands.

| 13 |

We may be subject to unexpected operational hazards based upon the remote location of our properties.

Our exploration and development activities are subject to the customary hazards of operation in remote areas, such as fires, explosions, migration of harmful substances, and spills. A casualty occurrence might result in the loss of equipment or life, as well as injury, property damage or other liability. While we maintain limited insurance to cover current operations, our property and liability insurance may not be sufficient to cover any such casualty occurrences or disruptions. Equipment failures could result in damage to our facilities and liability to third parties against which we may not be able to fully insure or may elect not to insure because of high premium costs or for other reasons. Our operations could be interrupted by natural disasters such as forest fires or other events beyond our control. Losses and liabilities arising from uninsured or under-insured events could have a material adverse effect on our business, our financial condition and results of our operations.

Risks Related to Our Common Stock

Because our shares are designated as “penny stock,” broker-dealers will be less likely to trade in our stock due to, among other items, the requirements for broker-dealers to disclose to investors the risks inherent in penny stocks and to make a determination that the investment is suitable for the purchaser.

Our shares are designated as “penny stock” as defined in Rule 3a51-1 promulgated under the Exchange Act and thus may be more illiquid than shares not designated as penny stock. The SEC has adopted rules which regulate broker-dealer practices in connection with transactions in “penny stocks.” Penny stocks are defined generally as: non-Nasdaq equity securities with a price of less than $5.00 per share; not traded on a “recognized” national exchange; or in issuers with net tangible assets less than $2,000,000, if the issuer has been in continuous operation for at least three years, or $10,000,000, if in continuous operation for less than three years, or with average revenues of less than $6,000,000 for the last three years. The penny stock rules require a broker-dealer to deliver a standardized risk disclosure document prepared by the SEC, to provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction, monthly account statements showing the market value of each penny stock held in the customer’s account, to make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity, if any, in the secondary market for a stock that is subject to the penny stock rules. Since our securities are subject to the penny stock rules, investors in the shares may find it more difficult to sell their shares. Many brokers have decided not to trade in penny stocks because of the requirements of the penny stock rules and, as a result, the number of broker-dealers willing to act as market makers in such securities is limited. The reduction in the number of available market makers and other broker-dealers willing to trade in penny stocks may limit the ability of purchasers in this offering to sell their stock in any secondary market. These penny stock regulations, and the restrictions imposed on the resale of penny stocks by these regulations, could adversely affect our stock price.

Future sales of our common stock may cause our stock price to decline.

Our stock price may decline due to future sales of our shares or the perception that such sales may occur. The board of directors has discretion to determine the issue price and the terms of issue of shares of our common stock. Such future issuances may be dilutive to investors. Holders of shares of common stock have no pre-emptive rights under our Certificate of Incorporation to participate in any future offerings of securities.

If we issue additional shares of common stock in private financings under an exemption from the registration requirements, then those shares will constitute “restricted shares” as defined in Rule 144 under the Securities Act. The restricted shares may only be sold if they are registered under the Securities Act, or sold under Rule 144, or another exemption from registration under the Securities Act.

Some of our outstanding restricted shares of common stock are either eligible for sale pursuant to Rule 144 or have been registered under the Securities Act for resale by the holders. We are unable to estimate the amount, timing, or nature of future sales of outstanding common stock. Sales of substantial amounts of our common stock in the public market may cause the stock’s market price to decline.

The public trading market for our common stock is volatile and may result in higher spreads in stock prices.

Our common stock trades in the over-the-counter (“OTC”) market and is quoted on the OTC Markets. The over-the-counter market for securities has historically experienced extreme price and volume fluctuations during certain periods. These broad market fluctuations and other factors, as well as economic conditions and quarterly variations in our results of operations, may adversely affect the market price of our common stock. In addition, the spreads on stock traded through the over-the-counter market are generally unregulated and higher than on stock exchanges, which means that the difference between the price at which shares could be purchased by investors in the over-the-counter market compared to the price at which they could be subsequently sold would be greater than on these exchanges. Significant spreads between the bid and asked prices of the stock could continue during any period in which a sufficient volume of trading is unavailable or if the stock is quoted by an insignificant number of market makers. Historically our trading volume has been insufficient to significantly reduce this spread and we have had a limited number of market makers sufficient to affect this spread. These higher spreads could adversely affect investors who purchase the shares at the higher price at which the shares are sold, but subsequently sell the shares at the lower bid prices quoted by the brokers. Unless the bid price for the stock exceeds the price paid for the shares by the investor, plus brokerage commissions or charges, the investor could lose money on the sale. For higher spreads such as those on over-the-counter stocks, this is likely a much greater percentage of the price of the stock than for exchange listed stocks. There is no assurance that at the time an investor in our common stock wishes to sell the shares, the bid price will have sufficiently increased to create a profit on the sale.

| 14 |

We have not paid, and do not intend to pay, dividends on our common stock and therefore, unless our common stock appreciates in value, our investors may not benefit from holding our common stock.

We have not paid any cash dividends on our common stock since inception. We do not anticipate paying any cash dividends on our common stock in the foreseeable future. As a result, investors in our common stock will not be able to benefit from owning our common shares unless the market price of our common stock becomes greater than the price paid for the stock by these investors.

There are a large number of restricted shares and shares issuable upon exercise of our outstanding options, warrants, or other convertible instruments that may be available for future sale, or which may be resold pursuant to Rule 144, the sale of which into our trading market may depress the market price of our common stock.

As of March 31, 2015, we had 33,393,828 shares of common stock issued and outstanding, of which 26,106,281 were designated by our transfer agent as restricted shares pursuant to Rule 144 promulgated by the SEC. In addition, as of March 31, 2015, we had outstanding warrants to purchase up to 16,697,936 shares of common stock, outstanding options to purchase up to 6,522,500 (including 600,000 options granted that vest upon completion of certain future financings) shares of common stock, and Series A Convertible Preferred shares convertible into 16,472,839 common shares. The sale of these shares into the open market may adversely affect the market price of our common stock.

Our board of directors can, without stockholder approval, cause preferred stock to be issued on terms that adversely affect common stockholders.

Under our Certificate of Incorporation, our board of directors is authorized to issue up to 10,000,000 shares of preferred stock, of which none are issued and outstanding as of the date of this registration statement. Also, our board of directors, without stockholder approval, may determine the price, rights, preferences, privileges and restrictions, including voting rights, of those shares. If the board of directors causes additional shares of preferred stock to be issued, the rights of the holders of our common stock could be adversely affected. The board of directors’ ability to determine the terms of preferred stock and to cause its issuance, while providing desirable flexibility in connection with possible acquisitions and other corporate purposes, could have the effect of making it more difficult for a third party to acquire a majority of our outstanding voting stock. Preferred shares issued by the board of directors could include voting rights, or even super voting rights, which could shift the ability to control us to the holders of the preferred stock. Preferred shares could also have conversion rights into shares of common stock at a discount to the market price of the common stock which could negatively affect the market for our common stock. In addition, preferred shares would have preference in the event of liquidation of the corporation, which means that the holders of preferred shares would be entitled to receive the net assets of the corporation distributed in liquidation before the common stockholders receive any distribution of the liquidated assets. We have no current plans to issue any shares of preferred stock.

We are an “emerging growth company” and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our common stock less attractive to investors.

The JOBS Act permits “emerging growth companies” like us to rely on some of the reduced disclosure requirements that are already available to smaller reporting companies, which are companies that have a public float of less than $75,000,000. As long as we qualify as an emerging growth company or a smaller reporting company, we would be permitted to omit the auditors’ attestation on internal control over financial reporting that would otherwise be required by Section 404 of the Sarbanes-Oxley Act, and are also exempt from the requirement to submit “say-on-pay”, “say-on-pay frequency” and “say-on-parachute” votes to our stockholders and may avail ourselves of reduced executive compensation disclosure that is already available to smaller reporting companies.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the exemption from complying with new or revised accounting standards provided in Section 7(a)(2)(B) of the Securities Act as long as it is an emerging growth company. An emerging growth company can therefore delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to take advantage of these benefits until we are no longer an emerging growth company or until we affirmatively and irrevocably opt out of this exemption. Our financial statements may therefore not be comparable to those of companies that comply with such new or revised accounting standards.

We will cease to be an emerging growth company at such time as described in the risk factor immediately above. Until such time, however, we cannot predict if investors will find our common stock less attractive because we may rely on these exemptions. If some investors find our common stock less attractive as a result, there may be a less active trading market for our common stock and our stock price may be more volatile and could cause our stock price to decline.

| 15 |

Some provisions of our charter documents may have anti-takeover effects that could discourage an acquisition of us by others, even if an acquisition would be beneficial to our stockholders and may prevent attempts by our stockholders to replace or remove our current management.

Provisions in our Certificate of Incorporation and bylaws could make it more difficult for a third party to acquire us or increase the cost of acquiring us, even if doing so would benefit our stockholders, or remove our current management. These provisions:

| · | authorize the issuance of “blank check” preferred stock, the terms of which may be established and shares of which may be issued without stockholder approval; | |

| · | do not provide for cumulative voting in the election of directors, which would otherwise allow for less than a majority of stockholders to elect director candidates; | |

| · | prohibit stockholder action for the election of directors by written consent, thereby requiring all stockholder actions to elect directors to be taken at a meeting of our stockholders; and | |

| · | limit the ability of our stockholders to call meetings of stockholders. |

These provisions may frustrate or prevent any attempts by our stockholders to replace or remove our current management by making it more difficult for stockholders to replace members of our board of directors, who are responsible for appointing the members of our management. Any provision of our certificate of incorporation or bylaws or Delaware law that has the effect of delaying or deterring a change in control could limit the opportunity for our stockholders to receive a premium for their shares of our common stock, and could also affect the price that some investors are willing to pay for our common stock.

ITEM 1B. Unresolved Staff Comments