Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Acacia Diversified Holdings, Inc. | Financial_Report.xls |

| EX-32.1 - EX-32.1 - Acacia Diversified Holdings, Inc. | ex32-1.htm |

| EX-31.1 - EX-31.1 - Acacia Diversified Holdings, Inc. | ex31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

(Mark One)

|

|||

|

x

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

||

|

For the fiscal year ended December 31, 2014

|

|||

|

or

|

|||

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

||

|

For the transition period from _____________to ______________

|

|||

Commission file number: 1-14088

Acacia Diversified Holdings, Inc.

(Exact name of registrant as specified in its charter)

|

Texas

|

75-2095676

|

|

(State or other jurisdiction of incorporation or organization)

|

(IRS Employer Identification No.)

|

3512 East Silver Springs Boulevard - #243 Ocala, FL 34470

(Address of principal executive offices) (Zip Code)

Issuer’s telephone number: (877) 513-6294

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Name of each exchange on which registered

|

Securities registered pursuant to section 12(g) of the Act:

Common Stock

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. (1) Yes x No o (2) Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o (Not required) o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

|

|

Non-accelerated filer o (Do not check if a smaller reporting company)

|

Smaller reporting company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes o No o

Issuer’s revenues for its most recent fiscal year. $1,412,998

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold was $833,439 as of December 29, 2014 based on a value of $0.14 per share.

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date: 12,735,406 as of December 31, 2014.

TABLE OF CONTENTS

|

PAGE

|

||

|

PART I.

|

||

|

Item 1.

|

4

|

|

|

Item 1A.

|

7

|

|

|

Item 1B.

|

14

|

|

|

Item 2.

|

14

|

|

|

Item 3.

|

14

|

|

|

Item 4.

|

14

|

|

|

PART II.

|

||

|

Item 5.

|

15

|

|

|

Item 6.

|

16

|

|

|

Item 7.

|

16

|

|

|

Item 7A.

|

26

|

|

|

Item 8.

|

26

|

|

|

Item 9.

|

26

|

|

|

Item 9A (T).

|

26

|

|

|

Item 9B.

|

27

|

|

|

PART III.

|

||

|

Item 10.

|

28

|

|

|

Item 11.

|

30

|

|

|

Item 12.

|

32

|

|

|

Item 13.

|

32

|

|

|

Item 14.

|

33

|

|

|

Item 15.

|

34

|

|

|

35

|

||

PART I

Item 1. Business of the Company

Description of Historical Operations

Acacia Diversified Holdings, Inc. (“we”, “us”, the “Company”, or the “Parent Company”) was incorporated in Texas on October 1, 1984 as Gibbs Construction, Inc. (“Gibbs”). The Company changed its name from Gibbs Construction, Inc. to Acacia Automotive, Inc. effective February 20, 2007, and subsequently changed its name again from Acacia Automotive, Inc. to Acacia Diversified Holdings, Inc. effective October 18, 2012.

In the years following its incorporation, the Company grew to become a full service, national commercial construction company and completed an initial public offering of its common stock pursuant to a registration thereof on Form S-1 in January, 1996, and thereafter commenced trading on the NASDAQ Exchange under the symbol GBSE. In April, 2000, as a result of, in part, rising interest rates and a general decline in the United States economy, the Company was compelled to seek protection under Chapter 11 of the United States Bankruptcy Code. Despite various attempts to reorganize the Company’s affairs within the context of the Company’s bankruptcy, it ultimately was unsuccessful.

Initial Restructuring of the Company

The Company being unable to reorganize through bankruptcy, on August 15, 2006, the Company’s primary creditor sold 4,000,000 shares, or 46,7% of its then-issued and outstanding shares of common stock, to Mr. Steven L. Sample, its current Chief Executive Officer and Chairman of the Board of Directors. In addition, Mr. Sample personally satisfied several outstanding obligations of the Company relating to professional fees associated with its S.E.C. reporting obligations. As consideration for Mr. Sample’s contribution, on February 1, 200, a special meeting of the Company’s shareholders effectuated a one (1) for eight (8) reverse stock split and thereafter issued Mr. Sample an additional 8,117,500 shares of the Company’s common stock, making him the majority shareholder of the Company. In connection therewith, the Company changed its name to Acacia Automotive Holdings, Inc and caused its trading symbol to be changed to “ACCA”. Shortly thereafter, Mr. Sample Mr. Sample exchanged all his preferred shares for an equal number of common shares of the Company and a number of warrants to purchase Common shares. There are no preferred shares issued or outstanding as of December 31, 2014,

In that restructuring the Company retained its substantial tax loss carryforward, which has grown to become approximately $12,940,000 as of December 31, 2014. (See NOTE 5 to Financial Statements – “Income Taxes”)

Immediately following the approval of these amendments, the Company adopted its Acacia Automotive, Inc. 2007 Stock Incentive Plan, which was ratified by the Company’s stockholders in its Annual meeting held November 2007, initially reserving 1,000,000 shares thereunder. In subsequent actions, the shareholders of the Company approved amendments to the Acacia Automotive, Inc. 2007 Stock Incentive Plan (the “Plan”), renaming it the Acacia Diversified Holdings, Inc. 2012 Stock Incentive Plan and making that revised plan effective as of January 1, 2012. All material terms of the 2007 Plan remained in full force and effect as they were merged into the revised Plan.

In July 2007, the Company caused to be formed Acacia Augusta Vehicle Auction, Inc., a South Carolina corporation and wholly owned subsidiary of the Company. (“AAVA”), for the sole purposes of acquiring certain assets of the Augusta Auto Auction in Augusta, Georgia, and operating an auction at that same location. This became the Company’s first operating asset in the automotive auction industry and was the Company’s only revenue producing business at that time. Later, in 2009, the Company caused to be formed Acacia Chattanooga Vehicle Auction, Inc., a Tennessee corporation and wholly owned subsidiary of the Company. (“ACVA”), for the sole purposes of acquiring certain assets of the Chattanooga Vehicle Auction in Chattanooga, Tennessee, and operating an auction at that same location. The latter acquisition represented the Company’s second, and final, automotive auction acquisition.

Due a dispute that arose with the seller of the Chattanooga Vehicle Auction, the Company discontinued operations there effective August 31, 2010, accounting for those operations as discontinued effective that date, and first accounted for those as discontinued operations in its Quarterly Report on Form 10-Q for the period ended June 30, 2010. In late 2011, after successfully operating the Augusta auction for more than four years, the Company determined that it was in its best interests to sell the Augusta auction and thereafter entered into a Letter of Intent with two individuals for that purpose. The sale transaction was completed on July 31, 2012. (See Part II, Item 9B – “Other Information”) Those events were reported in their entirety by the Company on its Current Report on Form 8-K on August 27, 2012, which in incorporated herein by reference. Following the disposition of the Augusta Vehicle Auction in 2012, the Company lacked significant operations and thereafter sought to become a diversified holding company.

Recent Operations of the Company

The Company was without revenue-producing operations from July 31, 2012 until July 10, 2013, when it, through its new wholly-owned subsidiary Citrus Extracts, Inc., entered into a definitive agreement to acquire certain assets and assumed liabilities related to those assets from Red Phoenix Extracts, Inc. (“RPE”), a corporation located in Fort Pierce, Florida. The assets included, among other things, furnishings, machinery, and equipment. As consideration for the assets, the Company issued to the holders of RPE nine hundred thousand (900,000) restricted shares of its common stock. There was no cash consideration in the transaction, which was more particularly described in the Company’s Current Report on Form 8-K dated July 10, 2013.

In that transaction, the Company also assumed certain liabilities of RPE, including indebtedness and trade payables in the amount of $519,493 for certain loan and payable obligations and responsibility for a forklift lease in the amount of $465 per month for the remaining 16 months of the lease. That forklift lease expired in October of 2014, and the Company exercised its option to purchase at that time. As a part of the assumed indebtedness the Company accepted responsibility for payment of the remaining $226,100 due on an SBA equipment loan at $5,205.46 per month.

In that same transaction, the Company also assumed responsibility for two leases for a facility of approximately 14,525 square feet consisting of two adjacent building units located at 3495 S. U.S. Hwy.1, Bldgs. 12-E and 12-W. The Company pays a combined $4,691 per month for the two leased units to the to the Fort Pierce State Farmer’s Market in Fort Pierce, Florida. The Farmers Market is owned and operated by the State of Florida, and the leases are subject to additional 1-year lease renewals, that being the maximum term allowed by the Florida authority operating the facility.

Current Operations of the Company

The Company’s current business operations are conducted through two (2) wholly-owned subsidiaries and a new operation that is not yet segregated as a subsidiary or division. They include:

Citrus Extracts, Inc.

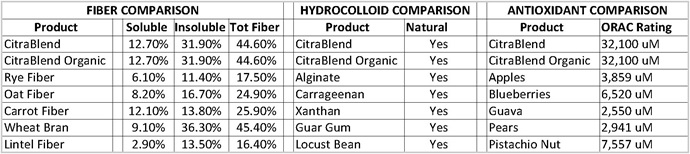

Citrus Extracts, Inc. (“CEI”) is a business in the food manufacturing industry subsector that transforms livestock and agricultural products into products for intermediate or final consumption. The industry groups are distinguished by the raw materials (generally of animal or vegetable origin) processed into food products. CEI utilizes our proprietary chemical-free, 100% natural processes in the manufacturing, sale, and distribution of all-natural, food-grade ingredients from raw, fresh, natural citrus peel resulting from citrus juicing operations. Through these controlled methods, CEI processes and dehydrates orange, lemon, grapefruit and tangerine peel into its “CitraBlend” and “CitraBlend Organic” products and then mills those products to varying sizes ranging from larger “cut & sift flakes” to 40+ mesh powders (or smaller sizes for custom orders). These ingredients, both organic and non-organic, find their way into many regional and national brand-name products commonly found on America’s kitchen tables in the form of spices, teas and otherwise. Our CitraBlend products are also utilized in brewing many local and regional craft beers in addition to nationally-recognized beer brands, and because we have only recently addressed that market it remains largely untapped. At this time CitraBlend is primarily sold through a network of distributors who blend our products and sell them as ingredients included in many well-known consumer products.

On July 2014, RPE reacquired $113,597 of the original debt transferred to the Company in the asset acquisition agreement and reacquired the $69,950 in trade obligations, thereafter becoming a creditor to the Company in those amounts replacing others. It further extended a new advance to the Company in the amount of $65,000 cash, resulting in total obligations to RPE of $248,547.

Following those actions, on August 20, 2014 the Company issued 108,597 new common shares to RPE in extinguishment of a portion of its obligations, those shares being valued at $1.00 each. Following the issuance of those shares, the Company’s debt obligation to RPE from the original acquisition transaction was reduced to $139,950 and its remaining debt obligations to others from that transaction was reduced to $109,846.

Thus, in 2013 the Company issued 934,285 new restricted shares of its Common stock. Of those shares issued in 2013, 900,000 shares were issued to RPE for assets acquired, 20,000 shares were issued to the Company’s securities attorney for services, and 14,285 shares were issued for services related to website and logo design. In 2014 the Company issued 238,597 new restricted shares of its Common stock. Of those shares issued in 2014, 108,597 shares were issued in extinguishment of obligations to RPE, 20,000 shares were issues for services related to the company’s computer servers and websites, 5,000 shares were issued for legal services, and 105,000 shares were issued to others for miscellaneous services.

Acacia Transport Services, Inc.

Acacia Transport Services, Inc. (“ATS”) is a business in the transportation industry that hauls fresh, raw, citrus peel resulting from the juice extraction process at juice plants. ATS has an exclusive contract to remove all the remediated raw citrus peel from Lambeth Groves Juice Company in Vero Beach, Florida, about 20 miles from the CEI manufacturing plant. In July and August of 2014 Acacia Transport acquired three tandem-axle diesel road tractors, five tandem-axle aluminum end-dump trailers, one 53 foot tandem axle closed van trailer, one straight truck with a stainless steel tank for small peel-hauling operations, as well as other spare parts and support equipment to accommodate its obligations to Lambeth Groves and Citrus Extracts. Under the terms of the contract, ATS, at its option, can bill Lambeth Groves for removing the raw peel, but has thus far elected not to do so. A portion of the raw peel ATS hauls from Lambeth Groves is taken to CEI for use in its manufacturing processes, and AST delivers excess peel to local farmers for use as livestock feed, charging only for those transport services on a per-load basis.

Acacia Transport Services transported its first load of raw peel from Lambeth Groves on August 7, 2014 and transported subsequent loads going forward from that date. Full-scale transport operations finally began with the onset of the 2015 citrus season that again started later than anticipated at approximately the beginning of December, 2014, the number of loads transported “in season” generally being maximized during the period of December through March or April.

Acacia Milling Services, Inc.

Acacia Milling Services (“AMS”) is a developmental stage business in the milling or grinding industry that mills finished citrus ingredient products rendered by Citrus Extracts into smaller, finer particles. These milling services vary from simple sifting operations that separate the various sizes of materials to creating specific cuts from the original material, such as “tea bag cut” size, granulated materials of various sizes, or “powders” of various mesh sizes. Generally the greater the mesh size (higher mesh sizes referring to finer, smaller, particle size) requested by the customer, the higher the milling charges per pound. The Company does not currently maintain separate accounting functions for its new milling operations, but intends to further segregate those milling operations later in 2015 and to implement a new system of segregated financial reporting for those operations, should the operations of AMS increase as expected. The Company also intends to expand its offerings of those milling services to outside parties for the generation of additional revenues in the future.

Thus, Acacia Diversified Holdings, Inc., now (i) through its Citrus Extracts, Inc. subsidiary is now engaged in operating an agricultural processing and manufacturing business concentrating on optimizing citrus biomass (waste) materials into food, beverage, spice, nutraceutical, skin care, cosmetics, and botanical products; (ii) through its wholly-owned Acacia Transport Services, Inc. subsidiary in Fort Pierce, Florida is now engaged in the transportation industry; and, (iii) through its Acacia Milling Services operations is engaged in milling finished products for the Company’s Citrus Extracts, Inc. subsidiary and ultimately other clients.

In addition to the foregoing, the Company will continue to seek and evaluate other acquisition, business combination or merger opportunities. Such opportunities need not be in our current area of operations and may be more consistent with our objective to become a holding company with a diverse array of businesses. There can be no assurance that any such evaluations will result in viable acquisition opportunities, or that any viable acquisition opportunities could result in a formal business combination or relationship. Moreover, there can be no assurances that if we are able to identify a suitable opportunity, that we will have the financial ability to close such contemplated transaction or that the target will accept any bona fide offer made by us. Should the Company require additional capital to close such a transaction, that may require us to offer to sell and sell either our debt or equity securities. There can be no assurances, however, that any such efforts would be successful. There have been no tentative or definitive plans for acquisition or merger agreements resulting from any evaluations.

Employees

The Parent Company had two officers in 2014, being Steven L. Sample, its Chairman, President and Chief Executive Officer, and Patricia Ann Arnold, its Secretary. Ms. Arnold serves in her capacity as a non-employee, while Mr. Sample serves as a full-time employee of the Company. Ms. Arnold spends less than full time on the affairs of the Parent Company. The Parent Company also had one other full time senior accounting employee in 2014.

Our wholly-owned operating subsidiaries, Citrus Extracts, Inc. and Acacia Transport Services, Inc., have a total of approximately 20 full-time and part-time employees.

The Company, should it be successful in executing its business plan, believes that it may be required to expand its staff to implement the controls necessary to manage a larger organization. This would likely result in the need for a Chief Financial Officer or Corporate Controller or other officers and managers and basic support personnel. The Company will endeavor to operate with the smallest corporate management staff possible so as to maintain the lowest overhead possible while still effecting sufficient management processes to properly guide the company.

Governmental Regulation

The Company, as with most companies, is subject to various business regulations, permits and licenses. The Company believes that it has complied with appropriate requirements and obtained all permits necessary to function under the current state and federal regulations.

Available Information

Our Web address is www.acacia.bz. The Company attempts to make its electronic filings with the Securities and Exchange Commission (“SEC”), including all Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and if applicable, amendments to those reports, available free of charge on its Web site as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. In addition, information regarding our board of directors is available on our Web site. The information posted on our Web site is not incorporated into this Annual Report on Form 10-K.

Any materials that we file with the SEC may be read and copied at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet Web site that contains reports, proxy statements and other information about issuers, like us, that file electronically with the SEC. The address of that site is www.sec.gov.

Item 1A. Risk Factors

Our auditors have issued a going concern opinion with respect to our consolidated financial statements although our financial statements are prepared using generally accepted accounting principles applicable to a going concern.

While the Company’s Citrus Extracts subsidiary is profitable, and while its Augusta Auto Auction operations were profitable as well, the Company has incurred significant losses as a consolidated entity since July 2007, losses that have continued since that time through the close of fiscal 2014. These continuing losses raise substantial doubt about our ability to continue as a going concern, and our auditor's opinion with respect to our financial statements contain a going concern opinion. The accompanying audited consolidated financial statements do not include any adjustments relating to the recoverability and classification of asset carrying amounts or the amount and classification of liabilities that might result from the outcome of this uncertainty.

Because We Have Limited Operating History, it is Difficult to Evaluate Our Business.

On July 10, 2013 the Company acquired certain assets that it utilized to begin revenue-producing operations under a new food grade citrus byproducts subsidiary. On March 1, 2014 the Company began milling products under the name Acacia Milling Services in preparation to create a stand-alone billing entity in the future. In July and August of 2014 the Company acquired vehicles and implemented operations at its new Acacia Transport, Inc. subsidiary. As a result of our limited operating history in these businesses, you have very little operating and financial data about us upon which to base an evaluation. You should consider our prospects in light of the risks, expenses and difficulties we may encounter, including those frequently encountered by new companies. If we are unable to execute our plans and grow our business, either as a result of the risks identified in this section or for any other reason, this failure would have a material adverse effect on our results of operations, business prospects, and financial condition.

The purchase of our securities is a purchase of an interest in what should be considered as a high risk venture or in a new or “start-up” venture with all the unforeseen costs, expenses, problems, and difficulties to which such ventures are subject.

We plan to grow through acquisitions

We plan to grow through expansion of our new operations, creation of new businesses, acquisitions, and/or mergers, and investors have little current basis to evaluate the possible merits or risks of the target businesses' operations or our ability to identify and integrate acquired operations into our company. Because we intend to develop and expand our business at least in part through selective acquisitions of or mergers with other businesses, there are significant risks that we may not be successful. We may not be able to identify, acquire or profitably manage additional companies or assets or successfully integrate such additional companies or assets into our Company without substantial costs, delays or other problems. In addition, companies we may acquire may not be profitable at the time of their acquisition or may not achieve levels of profitability that would justify our investment. Acquisitions may involve a number of special risks, including but not limited to:

|

Ø

|

adverse short-term effects on our reported operating results,

|

|

Ø

|

diversion of management's attention,

|

|

Ø

|

dependence hiring, training, and retaining key personnel,

|

|

Ø

|

risks associated with unanticipated problems or legal liabilities,

|

|

Ø

|

amortization of acquired intangible assets, some or all of which could reflect poorly on our operating results and financial reports,

|

|

Ø

|

implementation or remediation of controls, procedures and policies appropriate for a public company at companies that, prior to the acquisition, lacked these controls, procedures and policies; and,

|

|

Ø

|

incursion of debt to make acquisitions or for other operating uses.

|

To the extent we complete a business combination with a financially unstable company or an entity in its development stage, we may be affected by numerous risks inherent in the business operations of those entities. Although our management will endeavor to evaluate the risks inherent in a particular target business, we cannot assure you that we will properly ascertain or assess all of the significant risk factors.

We will seek to implement our acquisition strategy in certain industries that may be considered as mature

We may acquire a business in what may be considered a mature industry in which single-digit or low double-digit growth may occur. Most growth for our Company would, accordingly, occur largely through acquisitions. To the extent that competitors are also seeking to grow through acquisitions, we could encounter competition for those acquisitions or a generally increasing price to acquire going concerns.

A primary part of the Company’s strategy is to establish revenue through the acquisition of or merger with additional companies or operations. There can be no assurance that the Company will be able to identify, acquire, combine with, or profitably manage additional companies or successfully integrate the operations of additional companies into those of the Company without encountering substantial costs, delays or other problems. In addition, there can be no assurance that companies acquired in the future will achieve or maintain profitability that justify liabilities that could materially adversely affect the Company's results of operations or financial condition. The Company may compete for acquisition, merger, and expansion opportunities with companies that have greater resources than the Company. There can be no assurance that suitable acquisition or merger candidates will be available, that purchase terms or financing for acquisitions or mergers will be obtainable on terms acceptable to the Company, that acquisitions or mergers can be consummated, or that acquired businesses can be integrated successfully and profitability into the Company’s operations. Further, the Company's results of operations in fiscal quarters immediately following a material acquisition or merger could be materially adversely affected while the Company integrates the acquired business into its existing structure.

The Company will attempt to acquire or merge with business entities that are going and functioning concerns with a trailing history of profitability, but may acquire or merge with certain businesses that have either been unprofitable, have had inconsistent profitability prior to their acquisition or combination therewith, or that have had no operating history. An inability of the Company to improve the profitability of these acquired businesses could have a material adverse effect on the Company. Finally, the Company's acquisition and merger strategy places significant demands on the Company's resources and there can be no assurance that the Company's management and operational systems and structure can be expanded to effectively support the Company's acquisition strategy. If the Company is unable to successfully implement its acquisition and merger strategy, this inability could have a material adverse effect on the Company's business, results of operations, or financial condition. The Company may face the opportunity to enhance shareholder value by being acquired by another company. Upon any acquisition of the Company, the Company would be subject to various risks, including the replacement of its management by persons currently unknown. There can also be no assurance that, if acquired, new management will be successfully integrated or can profitably manage the Company. In addition, any acquisition or merger of or by the Company may involve immediate dilution to existing shareholders of the Company. No assurances can be given that the Company will be able to or desire to be acquired, or be able to acquire or merge with additional companies.

Need for Additional Financing

The Company does not have adequate capital or resources to fund its operations and other capital needs for the next six months without new revenue sources or additional capital infusion, and there can be no assurance that such funds will become available in amounts sufficient to meet the obligations of our business. The Company may require additional amounts of capital for its future expansion and working capital, possibly from private placements of its common stock or borrowing, but there can be no assurance that such financing will be available, or that such financing will be available on acceptable terms.

Dependence on Key Personnel

Our future performance depends in significant part upon the continued service of our Chief Executive Officer, Steven L. Sample and now upon the continued service of William J. Howe, the President of the Company’s new Citrus Extracts, Inc. subsidiary in Fort Pierce, Florida. The loss of either of their services could have a material adverse effect on our business, prospects, financial condition and results of operations. The Company does not presently maintain key man life insurance on Mr. Sample or Mr. Howe, but may obtain such insurance at the discretion of its board of directors for such term as it may deem suitable or desirable. Our future success may depend on our ability to attract and retain highly qualified technical, sales and managerial personnel. The competition for such personnel can be intense, and there can be no assurance that we can attract, assimilate or retain highly qualified technical, sales and managerial personnel for favorable compensations in the future.

Technological Change

Technology, particularly the ability to use the Internet to conduct business and allow several management functions, is characterized by rapidly changing technology, evolving industry standards, frequent new product and service announcements, introductions and enhancements, and changing customer demands. Our future success will to some degree depend on our ability to adapt to rapidly changing technologies, our ability to adapt its solutions to meet evolving industry standards and our ability to improve continually the performance, features and reliability of its solutions. Similarly, the Company must also continue to examine new processes and technologies related to its new citrus byproducts subsidiary. The failure of the Company to adapt successfully to such changes in a timely manner could have a material adverse effect on the Company's business, results of operations and financial condition. Furthermore, there can be no assurance that the Company will not experience difficulties that could delay or prevent the successful implementation of solutions, or that any new solutions or enhancements to existing solutions will adequately meet the requirements of its current and prospective customers and achieve any degree of significant market acceptance. If the Company is unable, for technological or other reasons, to develop and introduce new solutions or enhancements to existing solutions in a timely manner or in response to changing market conditions or customer requirements, or if its solutions or enhancements do not achieve a significant degree of market acceptance, the Company's business, results of operations and financial condition could be materially and adversely affected.

Competition

Any industry served by the Company is likely to be highly competitive across the entire United States and the rest of the world. The Company has elected to devote the majority of its efforts on sales within the continental United States, but does compete with other companies in diverse countries than can potentially produce and sell its products at lower prices. While the Company believes that there are other hurdles for those foreign entities to scale, including the high cost of international shipping to U.S. buyers, we believe that they nonetheless can compete with us in our markets. We will potentially compete with a variety of companies, both domestic and international, and as such will be subject to various levels of competition. There is no assurance the Company will be able to adhere to its plans or to engage in any acquisitions or mergers at all. As a result of its agreement with Uncle Matt’s Organic, Inc., Florida’s largest organic Juice producer, the Company believes it can compete as a manufacturer and supplier of organic food grade citrus peel products. The Company has several buyers of its product in diverse areas of the United States, and is currently fielding opportunities to sell or distribute its products to other buyers. In addition, the Company attended an organic trade show in Europe in early 2014 in an effort to establish clients in Europe and other venues, although it does not expend great energies in those areas and does not expect to see a significant amount of international business in its portfolio.

Control

Our Chief Executive Officer and Chairman of the Board of Directors owns a significant percentage of our outstanding voting securities which could reduce the ability of minority shareholders to effect certain corporate actions.

Our Chief Executive Officer and Director, Steven Sample, owned 43.27% of the Company’s issued and outstanding common stock as of December 31, 2013. As a result, currently, and after an offering by the Company of its equity securities, he will possess significant influence and can elect a majority of our board of directors and authorize or prevent proposed significant corporate transactions. His effective control may also have the effect of delaying or preventing a future change in control, impeding a merger, consolidation, takeover or other business combination or discourage a potential acquirer from making a tender offer.

As of that same date, all officers and directors of the Company owned a combined 45.58% of the Company’s issued and outstanding common stock. Based upon the Company's current business plan, it is anticipated that Mr. Sample will continue to have substantial influence over, if not effective control over the Company’s operations in the near future, including the election of a majority of its board of directors, the issuance of additional shares of equity securities, and other matters of corporate governance, perhaps even after some potential subsequent issuances by the Company of new common shares for capital raising activities, acquisitions, or merger activities.

We may, in the future, issue additional shares of common stock, which would reduce investors’ percent of ownership and may dilute our share value.

Our Articles of Incorporation, as amended, authorize the issuance of 150,000,000 shares of common stock. The future issuance of common stock may result in substantial dilution in the percentage of our common stock held by our then existing shareholders. We may value any common stock issued in the future on an arbitrary basis. The issuance of common stock for future services or acquisitions or other corporate actions may have the effect of diluting the value of the shares held by our investors, and might have an adverse effect on any trading market for our common stock

Management of Growth

The Company is continually seeking to identify and acquire viable businesses. As a result, the Company must manage relationships with a growing number of third parties as it seeks to accommodate this goal. The Company's management, personnel, systems, procedures and controls may not be adequate to support the Company’s future operations. The Company's ability to manage its growth effectively will require it to continue to expand its operating and financial procedures and controls, to replace or upgrade its operational, financial and management information systems and to attract, train, motivate, manage and retain key employees. If the Company's executives are unable to manage growth effectively, the Company's business, results of operations and financial condition could be materially adversely affected. If successful in acquiring or combining with other operations, the Company anticipates it may inherit a substantial portion of the staff necessary to operate the new entities, but there is no assurance that will happen, or that if it does happen, that the staff will remain employed by the Company for any period of time. We may find that some of the personnel and management of any acquisition target(s) may not be suitable for continued employment, while other suitable candidates may elect to discontinue their employment or affiliation with the Company for various reasons. This can create a burden on the Company’s management as it seeks to fill key positions. Failure of the Company to do so in a timely manner can result in disruption of operations, loss of revenues, and an attendant reduction in profits or even substantial losses.

Risks Associated with Expansion

The Company desires to start, acquire or combine with other businesses, perhaps in diverse locations and markets. To date, the Company does not have substantial experience in developing services on a regional or national scale. There can be no assurance that the Company will be able to deploy successfully its goods or services in those markets. There are certain risks inherent in doing business in several diverse markets, such as; unexpected changes in regulatory requirements, potentially adverse tax consequences, local restrictions, controls relating to inter-company communications and technology, difficulties in staffing and managing distant operations, fluctuations in manpower availability, effects of local competition, weather and climactic trends, and customer preferences, any of which could have a material adverse effect on the success of the Company's operations and, consequently, on the Company's business, results of operations, and financial condition.

Product and Service Offerings

On July 10, 2013, the Company acquired certain assets and, though its Citrus Extracts, Inc. (“CEI”) subsidiary, entered the citrus peel byproducts manufacturing business. The Company’s CEI subsidiary utilizes our chemical-free, 100% natural processes in the manufacturing, sale, and distribution of all-natural food-grade ingredients made from raw, fresh, natural citrus peel resulting from citrus juicing operations. Through its trade secret processes, CEI processes and dehydrates orange, lemon, grapefruit and tangerine peel as CitraBlend and CitraBlend then mills it to varying sizes from “cut & sift flakes” to 40+ mesh powders (or smaller sizes for custom orders). These ingredients, both organic and non-organic, find their ways into many national brand-name products commonly found on America’s kitchen tables in the form of spices, teas, national brand beer, specialty beverages, and otherwise. In addition to a national label beer, our products are found in many craft beers, and because we have only recently addressed that market it remains largely untapped. CitraBlend is currently primarily sold through a distributor network with emphasis on those industries.

In addition to our standard non-organic line of products, our Citrus Extracts subsidiary began manufacturing organic citrus ingredient products in larger quantities effective with the beginning of January 2014. The Company secures it source material (fresh citrus peel) directly from a citrus peel processor less than 20 miles from its manufacturing facility, also obtaining is fresh organic peel from that plant in conjunction with its juice processing operations for Uncle Matt’s Organic Juice Company-Florida’s largest organic juice manufacturer. All our food grade products are gluten free, non-gmo, certified Kosher, and in the case our organic products, bear our USDA National Organic Certification.

On January 15, 2014, the Company formed a new Florida corporation, Acacia Transport Services, Inc. (“ATS”), for the purposes of utilizing that corporation to house new subsidiary operations and to receive certain acquired assets. On July 2, 2014, ATS executed an exclusive agreement with Lambeth Groves Juice Company in Vero Beach, Florida to obtain all the raw citrus peel resulting from its juice extraction operations beginning July 30, 2014, and concomitant with that same time the Company acquired several road tractors and trailers for use in transporting the raw citrus peel for use at the Company’s Citrus Extracts, Inc. manufacturing subsidiary and for disposing of excess peel to farmers. ATS hauled its first loads of raw citrus peel from Lambeth Groves on August 7, 2014 and thereafter as it became available.

On March 1, 2014 the Company began performing milling operations using the trade name Acacia Milling Services at the Fort Pierce location for its Citrus Extracts subsidiary. Milling is the term applied to grinding or refining the finished citrus ingredient products rendered by Citrus Extracts into smaller, finer particles. These services vary from simple sifting operations that separate the various sizes of materials to creating specific cuts from the original material, such as “tea bag cut” size, granulated materials of various sizes, or “powders” of various mesh sizes. Generally the greater the mesh size (finer, smaller, particle size) requested by the customer, the higher the milling charges per pound. The Company does not currently maintain separate accounting functions for its new milling operations, but intends to further segregate those milling operations in 2015 and to implement a new system of segregated financial reporting for those operations. The Company also intends to expand its offerings of those milling services to outside parties for the generation of additional revenues in the future.

The Company may seek to start, acquire, or combine with other service or non-service entities, including those involved in manufacturing, transportation, distribution, chemical products, or otherwise. It is important to our future success to expand the breadth and depth of our offerings to be competitive and to enhance our potentials for growth of revenues and profits. Expansion of our categories and offerings in this manner will require significant additional expenditures and could strain our management, financial and operational resources. For example, we may find it prudent to acquire or build, outfit, and operate a new manufacturing facility or to initiate a new transport subsidiary where one is not currently available. We cannot be certain that we would be able to do so in a cost-effective or timely manner or that we would be able to offer certain products or services in demand by our customers, or to do so in a quality manner. Furthermore, any new product or service offering that is not favorably received by the Company’s clients could damage our reputation. The lack of market acceptance of new products or services or our inability to generate satisfactory revenues from expanded product or service offerings to offset their costs could harm our business. If we do not successfully expand our sales operations, our revenues may fall below expectations. If we do not successfully expand our operations on an ongoing basis to accommodate increases in demand, we will not be able to fulfill our customers’ needs in a timely manner, which would harm our business. Most of our product or service operations are anticipated to be handled at our facilities, but some services may be performed at offsite locations or by approved vendors or contractors. Any future expansion may cause disruptions in our business and may be insufficient to meet our ongoing requirements. The Company may move into various businesses as sales, manufacturing, transport, marketing, or otherwise, and is not limited to considering only product or service business offering. There can be no assurance that the Company will be successful in identifying new businesses, or if it can be successful in acquiring or merging with any new business if identified.

Government Regulation and Legal Uncertainties

Any new legislation or regulation, or the application of laws or regulations from jurisdictions whose laws do not currently apply to the Company's business could have a material adverse effect on the Company's business, results of operations and financial condition.

Check, Credit Card, and Other Fraud

Our business could be harmed if we experience significant credit, wire transfer, draft, check, credit card, or other fraud. If we fail to adequately control fraudulent transactions, our revenues and results of operations could be harmed. The Company may attempt to obtain insurance as partial protections from such potential losses, but even while the Company’s exposure to loss in this event may be limited by the purchase of any such insurance, losses could nonetheless occur. Any losses sustained as a result of fraud or fraudulent activity would adversely affect the Company's business and results of operations, and its financial condition could be materially adversely affected.

Liability Claims

The Company may face costly liability claims by consumers or other businesses. Any claim of liability by a client, employee, consumer or other entity against us, regardless of merit, could be costly financially and could divert the attention of our management. It could also create negative publicity, which would harm our business. Although we maintain certain forms of liability insurance, it may not provide protections in the event of certain liability claims, or may not be sufficient to cover a covered claim if one is made.

The Company may not be able to attain profitability without additional funding, which may be unavailable.

The Company has limited capital resources. Unless the Company begins to generate sufficient revenues to finance operations as a going concern, the Company may experience liquidity and solvency problems. Such liquidity and solvency problems may force the Company to cease operations if additional financing is not available. No known alternative resources of funds are available in the event we do not generate sufficient funds from operations.

Our lack of history in our current industry makes evaluating our business difficult.

We have a limited operating history in our current industry and we may not sustain profitability in the future.

To sustain profitability, we must:

|

Ø

|

develop and identify new clients in need of our product;

|

|

Ø

|

economically increase production output;

|

|

Ø

|

compete with larger, more established competitors in our industry;

|

|

Ø

|

maintain and enhance our brand recognition; and

|

|

Ø

|

adapt to meet changes in our markets and competitive developments.

|

We may not be successful in accomplishing these objectives. Further, our lack of operating history makes it difficult to evaluate our business and prospects. Our prospects must be considered in light of the risks, uncertainties, expenses and difficulties frequently encountered by companies in their early stages of development, particularly companies in highly competitive industries. The historical information in this report may not be indicative of our future financial condition and future performance. For example, we expect that our future annual growth rate in revenues will be moderate and likely be less than the growth rates experienced in the early part of our history.

If we fail to effectively manage our growth, our business, brand and reputation, results of operations and financial condition may be adversely affected.

We may experience a rapid growth in operations, which may place significant demands on our management team and our operational and financial infrastructure. As we continue to grow, we must effectively identify, integrate, develop and motivate new employees, and maintain the beneficial aspects of our corporate culture. To attract top talent, we believe we will have to offer attractive compensation packages. The risks of over-hiring or over compensating and the challenges of integrating a rapidly growing employee base may impact profitability.

Additionally, if we do not effectively manage our growth, the quality of our services could suffer, which could adversely affect our business, brand and reputation, results of operations and financial condition. If operational, technology and infrastructure improvements are not implemented successfully, our ability to manage our growth will be impaired and we may have to make significant additional expenditures to address these issues. To effectively manage our growth, we will need to continue to improve our operational, financial and management controls and our reporting systems and procedures. This will require that we refine our information technology systems to maintain effective online services and enhance information and communication systems to ensure that our employees effectively communicate with each other and our growing base of customers. These system enhancements and improvements will require significant incremental and ongoing capital expenditures and allocation of valuable management and employee resources. If we fail to implement these improvements and maintenance programs effectively, our ability to manage our expected growth and comply with the rules and regulations that are applicable to publicly reporting companies will be impaired and we may incur additional expenses.

We may be subject to regulatory inquiries, claims, suits, or prosecutions which may impact our profitability.

Any failure or perceived failure by us to comply with applicable laws and regulations may subject us to regulatory inquiries, claims, suits and prosecutions. We can give no assurance that we will prevail in such regulatory inquiries, claims, suits and prosecutions on commercially reasonable terms or at all. Responding to, defending and/or settling regulatory inquiries, claims, suits and prosecutions may be time-consuming and divert management and financial resources or have other adverse effects on our business. A negative outcome in any of these proceedings may result in changes to or discontinuance of some of our services, potential liabilities or additional costs that could have a material adverse effect on our business, results of operations, financial condition and future prospects.

Expanding our product offerings or number of offices may not be profitable.

We may choose to develop new products to offer. Developing new offerings involves inherent risks, including:

|

Ø

|

our inability to estimate demand for the new offerings;

|

|

Ø

|

our inability to perfect the new products;

|

|

Ø

|

our ability to locate and identify new buyers for those products;

|

|

Ø

|

competition from more established market participants; and

|

|

Ø

|

a lack of market understanding.

|

In addition, expanding into new geographic areas and/or expanding current service offerings is challenging and may require integrating new employees into our culture as well as assessing the demand in the applicable market.

Risks of Low Priced Stocks

Following its initial public offering of its common stock in 1996, the Company’s shares were originally traded on the NASDAQ Exchange into 2000 as Gibbs Construction, Inc. under the trading symbol GBSE. Gibbs encountered severe financial difficulties in 2000, after which it was moved from the NASDAQ Capital Markets to the OTC Pink Sheets. Following the resurrection of the Company’s operations in 2007 through the intervention and assistance of the Company’s current CEO, Mr. Sample, its stock currently trades on the OTCQB exchange under the trading symbol ACCA. Most of the Company’s issued and outstanding common shares continue to be restricted shares resulting in a small “float”. For that and other reasons the Company’s securities have been thinly traded, and while a trading market for the Company's common stock could develop further with its current or new operations and the further release of restrictions on registered shares, there can be no assurance that it will do so. The Company returned to the OTC Pink Sheets following a delinquency in filing required reports, but anticipates returning to the OTCQB market immediately following the filings if this Annual Report for 2014 on Form 10-K.

The Securities and Exchange Commission (the “SEC” or “Commission”) has adopted regulations which define a “penny stock” to be any equity security, such as those of the Company, that has a market price of less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. In the event the Company determined to offer its common stock for sale, or elected to utilize its common stock in an acquisition of merger transaction, it would be required to advise the potential purchasers or parties to any such acquisition or merger transaction of the risks of penny stocks. For any transaction involving a penny stock, unless exempt, the rules require the delivery, prior to any transaction involving a penny stock by a retail customer, of a disclosure schedule prepared by the Securities and Exchange commission relating to the penny stock market. Disclosure is also required to be made about commissions payable to both the broker/dealer and the registered representative and current quotations for the securities. Accordingly, market makers may be less inclined to participate in marketing the Company’s securities, which may have an adverse impact upon the liquidity of the Company’s securities.

If the Company were successful in identifying a new business opportunity and/or identifying an acquisition or merger target, became successful in actually launching a new business or acquiring or merging with any such target, and was successful in bringing profitable operations to the Company, it would intend to seek to meet the new listing requirements of the NASDAQ Capital market and attempt to return to that Exchange, which listing requirements include minimal capitalization, share price, and other benchmark requirements. There is no assurance the Company can successfully identify any suitable new business opportunity, acquisition or merger candidate, or if successful in identifying a new business opportunity or merger/acquisition candidate, that it can be successful in developing a new business or completing any acquisition or merger, or if successful in developing a new business or completing any acquisition or merger that the Company could be successful in meeting the new listing requirements of the NASDAQ, or if successful in meeting those requirements, that the NASDAQ would accept the Company as a member, or that if the Company were successful in achieving a listing on the NASDAQ exchange that its share values would improve. Any attempt to return to the NASDAQ Exchange, even if the Company were successful in meeting the requirements to do so, could take as long as two years to complete.

We are subject to penny stock regulations and restrictions and you may have difficulty selling shares of our common stock.

The SEC has adopted regulations which generally define so-called “penny stocks” to be an equity security that has a market price less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exemptions. Our common stock is a “penny stock”, and we are subject to Rule 15g-9 under the Exchange Act, or the “Penny Stock Rule”. This rule imposes additional sales practice requirements on broker-dealers that sell such securities to persons other than established customers. For transactions covered by Rule 15g-9, a broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction prior to sale. As a result, this rule may affect the ability of broker-dealers to sell our securities and may affect the ability of purchasers to sell any of our securities in the secondary market.

For any transaction involving a penny stock, unless exempt, the rules require delivery, prior to any transaction in a penny stock, of a disclosure schedule prepared by the SEC relating to the penny stock market. Disclosure is also required to be made about sales commissions payable to both the broker-dealer and the registered representative and current quotations for the securities. Finally, monthly statements are required to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stock.

No Assurance of Payment of Dividends

Should the Company acquire additional operations, and should the operations of the Company become profitable, it is likely that the Company would retain much or all of its earnings in order to finance future growth and expansion. Therefore, the Company does not presently intend to pay dividends, and it is not likely that any dividends will be paid in the foreseeable future.

Potential Future Capital Needs

The Company may not be successful in generating sufficient cash from its new operations or in raising capital in sufficient amounts or on acceptable terms to meet its capital needs. The failure to generate sufficient cash flows or to raise sufficient funds may require the Company to delay or abandon some or all of its development and expansion plans or otherwise forego market opportunities, and may make it difficult for the Company to respond to competitive pressures, any of which could have a material adverse effect on the Company's business, results of operations, and financial condition. While the Company may seek to raise capital through the offering of common stock, there can be no assurance that it will be successful in doing so, or if successful in raising capital that the proceeds in any such offering will be sufficient to permit the Company to implement its proposed business plan, or that any assumptions relating to the implementation of such plan will prove to be accurate. To the extent that the proceeds of any such offering are not sufficient to enable the Company to generate sufficient revenues or achieve profitable operations, the inability to obtain additional financing will have a material adverse effect on the Company. There can be no assurance that any such financing will be available to the Company on commercially reasonable terms, or at all, or that the Company will be successful in finding new operations.

Implementation of Business Plan

The Company currently does not have sufficient working capital to pursue our business plan in its entirety as described herein. Our ability to implement our business plan will depend on our ability to obtain sufficient working capital and to execute its business plans. No assurance can be given that we will be able to obtain additional capital, or, if available, that such capital will be available at terms acceptable to us, or that we will be able to generate profit from operations, or if profits are generated, that they will be sufficient to carry out our business plans, or that the plans will not be modified.

Item 1B. Unresolved Staff Comments

None.

Item 2. Description of Properties

The Company’s Citrus Extracts, Inc. subsidiary leases manufacturing and administrative facilities in Ft. Pierce, Florida for a combined rent of $4,691 per month on a year-to-year lease – the maximum allowed by Florida state law in this facility. The leased premises consists of two buildings of approximately 15,000 combined square feet indoors housing its manufacturing operations, warehouse space, elevated loading docks, and office space. The lease also provides for sufficient outdoor parking and operating space such as to accommodate the Company’s needs. The Company also currently maintains office and administrative space in Ocala, Florida, at a cost of approximately $600 per month, which it may cancel at any time. The Company also rents on a month-to-month basis an additional warehouse in the Fort Pierce State Farmers Market consisting of approximately 1,900 square feet for $838.50 per month for additional temporary warehouse space.

Item 3. Legal Proceedings

None.

Item 4. Submission of Matters to a Vote of Security Holders

None.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities

Our stock has been thinly traded during the past five fiscal years. Moreover, we do not believe that any institutional or other large scale trading of our stock has occurred, or will in fact occur in the near future. We are presently traded on the Over the Counter QB Market under the ticker symbol ACCA. There were seven market makers who commonly made markets in our stock as of December 31, 2014. The following table sets forth information as reported by the National Association of Securities Dealers Composite Feed or Other Qualified Interdealer Quotation Medium for the high and low bid and ask prices for each of the twelve quarters ending December 31, 2014. The following prices reflect inter-dealer prices without retail markup, markdown or commissions and may not reflect actual transactions.

|

Closing Bid

|

Closing Ask

|

|||||||||||||||

|

High

|

Low

|

High

|

Low

|

|||||||||||||

|

Quarters ending in 2012

|

||||||||||||||||

|

March 31

|

$

|

0.25

|

$

|

0.03

|

$

|

1.96

|

$

|

1.20

|

||||||||

|

June 30

|

0.51

|

0.05

|

1.20

|

0.51

|

||||||||||||

|

September 30

|

0.10

|

0.03

|

0.99

|

0.99

|

||||||||||||

|

December 31

|

$

|

0.10

|

$

|

0.01

|

$

|

0.99

|

$

|

0.75

|

||||||||

|

Quarters ending in 2013

|

||||||||||||||||

|

March 31

|

$

|

0.01

|

$

|

0.01

|

$

|

1.80

|

$

|

0.69

|

||||||||

|

June 30

|

0.25

|

0.15

|

1.80

|

0.80

|

||||||||||||

|

September 30

|

0.65

|

0.20

|

1.80

|

0.55

|

||||||||||||

|

December 31

|

$

|

0.51

|

$

|

0.36

|

$

|

1.00

|

$

|

0.51

|

||||||||

|

Quarters ending in 2014

|

||||||||||||||||

|

March 31

|

$

|

0.55

|

$

|

0.06

|

$

|

1.41

|

$

|

0.70

|

||||||||

|

June 30

|

0.20

|

0.06

|

0.70

|

0.70

|

||||||||||||

|

September 30

|

0.20

|

0.06

|

0.70

|

0.65

|

||||||||||||

|

December 31

|

$

|

0.13

|

$

|

0.10

|

$

|

0.65

|

$

|

0.51

|

||||||||

As of December 31, 2014 the Company had 191 stockholders of record. The Company believes that it may also have as many as 200 or more additional beneficial shareholders. The number of both shareholders of record and beneficial shareholders may change on a daily basis and without the Company’s immediate knowledge.

Holders of common stock are entitled to receive dividends as may be declared by our board of directors and, in the event of liquidation, to share pro rata in any distribution of assets after payment of liabilities. The board of directors has sole discretion to determine: (i) whether to declare a dividend; (ii) the dividend rate, if any, on the shares of any class of series of our capital stock, and if so, from which date or dates; and (iii) the relative rights of priority of payment of dividends, if any, between the various classes and series of our capital stock. We have not paid any dividends and do not have any current plans to pay any dividends.

At its meeting of directors on February 1, 2007, the Company’s board of directors approved the Acacia Automotive, Inc. 2007 Stock Incentive Plan1 (the “Plan”), which was approved by our stockholders on November 2, 2007, reserving 1,000,000 shares to be issued thereunder in the form of common stock or common stock purchase options. On July 26, 2012, our shareholders voted to update and extend the Acacia Automotive, Inc. 2007 Stock Incentive Plan, renaming it the Acacia Diversified Holdings, Inc. 2012 Stock Incentive Plan. Warrants, which may be included as equity compensation of used in other manners, are not a component of the Plan. In resolutions since the implementation of the Plan, the directors granted restricted stock, warrants, and options for compensation summarized as follows as of December 31, 2014:

SUMMARY OF EQUITY COMPENSATION PLANS

|

Plan Description at December 31, 2013 and 2014

|

Number of

Shares to be

Issued Upon

Exercise of

Outstanding

Options

|

Weighted

Average

Exercise Price

of

Outstanding

Options

|

Number of

Shares

Remaining

Available for

Future

Issuance

|

||||||

|

Initial Number of Securities Available for Issue Under the Plan (1)

|

-

|

-

|

1,000,000

|

||||||

|

Total Options approved and issued through 12-31-2013 (2)

|

735,000

|

0.43

|

-

|

||||||

|

Options forfeited by former holders through 12-31-2013 (2)

|

(645,000

|

) |

|

0.44

|

-

|

||||

|

Total Equity Plan Options outstanding at December 31, 2013

|

90,000

|

0.34

|

3,743,200

|

||||||

|

Total options approved and issued in 2014 (2)

|

-

|

-

|

-

|

||||||

|

Options forfeited by former holders in 2014 (2)

|

-

|

-

|

-

|

||||||

|

Total Equity Plan Options outstanding at December 31, 2014 (2)

|

90,000

|

0.34

|

4,243,072

|

||||||

|

(1)

|

The Company’s Acacia Automotive, Inc. 2007 Stock Incentive Plan began with 1,000,000 authorized securities, to which were added 4% of the issued and outstanding shares of stock of the Company on the first calendar day of each year, but not to exceed 1,000,000 shares added in any calendar year. In 2012, the Company made certain revisions to and changed the name of its plan to the Acacia Diversified Holdings, Inc. 2012 Stock Incentive Plan.

|

|

(2)

|

The number of Options issued and forfeited under the Plan in the years 2007 through 2014 and the increases in securities added to the Plan for each year are as follows:

|

|

Year

|

Options Granted

|

Options Forfeited

|

Securities added to Plan

|

Securities available* at December 31st

|

||||||||||||

|

2007

|

155,000 | -0- | -0- | 845,000 | ||||||||||||

|

2008

|

240,000 | -0- | 479,900 | 1,084,900 | ||||||||||||

|

2009

|

195,000 | -0- | 482,500 | 1,372,400 | ||||||||||||

|

2010

|

145,000 | (255,000 | ) | 483,300 | 1,965,700 | |||||||||||

|

2011

|

-0- | (390,000 | ) | 462,500 | 2,818,200 | |||||||||||

|

2012

|

-0- | -0- | 462,500 | 3,280,700 | ||||||||||||

|

2013

|

-0- | -0- | 462,500 | 3,743,200 | ||||||||||||

|

2014

|

-0- | -0- | 499,872 | 4,243,072 | ||||||||||||

* This number will increase on January 1, 2015 by 509,416 securities, bringing the total securities authorized for issuance under the plan as of that date to 4,752,488.

Item 6. Selected Financial Data

Not Applicable

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Forward-Looking Statements

This Management's Discussion and Analysis of Financial Condition and Results of Operations (MD&A) contains forward-looking statements that involve known and unknown risks, significant uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed, or implied, by those forward-looking statements. You can identify forward-looking statements by the use of the words such as "expects", "anticipates", "intends", "plans", "believes", "seeks", "estimates", “may”, “will”, “should”, “could”, “predicts”, “potential”, “proposed”, or “continue” or the negative of those terms. These statements are only predictions. In evaluating these statements, you should consider various factors which may cause our actual results to differ materially from any forward-looking statements. Although we believe that the exceptions reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Therefore, actual results may differ materially and adversely from those expressed in any forward-looking statements due to numerous factors, including, but not limited to, availability of financing for operations, successful performance of operations, impact of competition and other risks detailed below as well as those discussed elsewhere in this Form 10-K and from time to time in the Company's Securities and Exchange Commission filings and reports. In addition, general economic and market conditions and growth rates could affect such statements. We undertake no obligation to revise or update publicly any forward-looking statements for any reason.

Executive Overview

With the acquisition of the Augusta Auto Auction on July 10, 2007, the Company commenced revenue-producing at that location and conducted its first weekly auction under the Company's ownership and management on July 11th of that year. The Company's Augusta auction sold vehicles and equipment for automotive dealers and commercial accounts, including banks and finance companies, as well as for the United States Marshals Service. The Company sold the business and related assets of the Augusta auction on July 31, 2012, and first accounted for those operations as discontinued on its Annual Report of Form 10-K for the year ended December 31, 2011.

The Company acquired its second auto auction in December 2009, located in Chattanooga, Tennessee. Following disputes with the seller of those operations and certain related parties, the Company discontinued operations at that location effective August 31, 2010, after which the Company and its CEO, the Seller of the Chattanooga auction, and its related parties entered into litigation in September of that same year. The ongoing litigation between the parties was settled on February 28, 2012. Accordingly, the Company considered those as discontinued operations effective August 31, 2010, as first accounted for them as discontinued in the Company’s Quarterly Report on Form 10-Q for the period ended June 30, 2010. These events were further reported in the Company’s Current Report on Form 8-K filed on November 19, 2012, its Amended Annual Report on Form 10-K /A for the period ended December 31, 2009, and its Annual Report on Form 10-K for the period ended December 31, 2010, which described those events in detail, and which reports are incorporated herein by reference.

On July 10, 2013 the Company, through its wholly-owned subsidiary Citrus Extracts, Inc., entered into a definitive agreement to acquire certain assets (the “Assets”) of Red Phoenix Extracts, Inc., a Florida corporation (“RPE” or the “Seller”) in Fort Pierce, Florida. The transaction is more particularly described in the Company’s Current Report on Form 8-K dated July 10, 2013.

The Company on January 15, 2014 formed Acacia Transport Services, Inc. as a wholly-owned subsidiary for the primary purpose of providing transportation and a continuous source of raw citrus peel materials for its sister Citrus Extracts, Inc. manufacturing plant, and for the secondary purpose of generating transport revenues in hauling excess raw citrus peel materials to local farmers for use as feed for livestock. On July 2, 2014, that subsidiary entered into an Agreement for Citrus Peel Hauling Services with Lambeth Groves Juice Company, a juice extraction company located in Vero Beach, Florida, some 20 miles from Citrus Extracts, Inc. That contract called for Acacia Transport to assume all responsibilities for hauling the raw, remediated citrus peel products from Lambeth Groves by July 30, 2014, and actual transport operations from Lambeth Groves commenced on August 7, 2014.

On March 1, 2014 the Company began performing milling operations using the trade name Acacia Milling Services at the Fort Pierce location for its Citrus Extracts subsidiary. Milling is the term applied to grinding or refining the finished citrus ingredient products rendered by Citrus Extracts into smaller, finer particles. These services vary from simple sifting operations that separate the various sizes of materials to creating specific cuts from the original material, such as “tea bag cut” size, granulated materials of various sizes, or “powders” of various mesh sizes. Generally the greater the mesh size (finer, smaller, particle size) requested by the customer, the higher the milling charges per pound. The Company does not currently maintain separate accounting functions for its new milling operations, but intends to further segregate those milling operations in 2015 and to implement a new system of segregated financial reporting for those operations. The Company also intends to expand its offerings of those milling services to outside parties for the generation of additional revenues in the future.

Discussion Regarding Management Fees