Attached files

| file | filename |

|---|---|

| 8-K - 8-K - MIDDLEFIELD BANC CORP | d923423d8k.htm |

Exhibit 99.1

Middlefield

Banc

Corp.

Annual Shareholder Meeting

May

13,

2015 |

Forward Looking Statements

This presentation contains forward-looking statements within the

meaning of the Securities Exchange Act of 1934 and the Private

Securities Litigation Reform Act of 1995 concerning Middlefield

Banc Corp.’s plans, strategies, objectives, expectations, intentions,

financial condition and results of operations. These

forward-looking statements reflect management’s current

views and intentions and are subject to known and unknown risks,

uncertainties, assumptions and other factors that could cause the

actual results to differ materially from those contemplated by

the statements. The significant risks and uncertainties

related to Middlefield Banc Corp. of which management is aware are

discussed in detail in the periodic reports that Middlefield Banc Corp.

files with the Securities

and

Exchange

Commission

(the

“SEC”),

including

in

the

“Risk

Factors”

section

of its Annual Report on Form 10-K and its Quarterly Report on Form

10-Q. Investors are urged to review Middlefield Banc

Corp.’s periodic reports, which are available at no

charge

through

the

SEC’s

website

at

www.sec.gov

and

through

Middlefield

Banc

Corp.’s

website

at

www.middlefieldbank.com

on

the

“Investor

Relations”

page.

Middlefield

Banc

Corp. assumes no obligation to update any of these forward-looking

statements to reflect a change in its views or events or

circumstances that occur after the date of this presentation. 2

|

Board of Directors

3

Thomas G. Caldwell

James R. Heslop, II

Eric W. Hummel

Kenneth E. Jones

Darryl E. Mast

Clayton W. Rose, III

James J. McCaskey

William J. Skidmore

Joseph J. Thomas

Robert W. Toth

Carolyn J. Turk |

Experienced Management Team

Management

Position

Age

MBCN

Industry

Thomas G. Caldwell

President & CEO

57

28

38

James R. Heslop, II

EVP & COO

61

19

36

Donald L. Stacy

SVP & CFO

61

15

36

Jay P. Giles

SVP -

Senior Loan Officer

65

16

42

Teresa M. Hetrick

SVP -

Operations

51

18

27

Jeffrey N. Male

SVP -

Chief Residential Mortgage Officer

65

1

42

Kevin L. Miller

SVP -

Chief Information Officer

55

1

33

David G. Dalessandro

SVP -

Chief Credit Office

58

5

33

James L. Long

President, Central Ohio Region

64

6

42

Courtney M. Erminio

VP -

Risk Officer

33

5

12

Alfred F. Thompson, Jr.

VP -

Loan Administration

55

19

28

Thomas Caldwell serves on the Federal Delegate Board of the Independent Community Bankers of

America, having been elected in June 2010. He previously served

as Chairman of the Community

Bankers Association of Ohio.

4 |

Meeting Overview

Welcome to the Middlefield Banc Corp. 2015 Annual Shareholder

Meeting Company Snapshot

(1)(2)

NASDAQ:

MBCN

Stock Price:

$31.71

Market Cap:

$65.1 million

Dividend (yield):

$1.04 (3.3%)

Headquarters:

Middlefield, Ohio

Established:

Bank 1901/HC 1988

Branches:

10

Total Assets:

$699.9 million

Net Loans

$469.4 million

Total Deposits:

$617.1 million

(1)

Stock price, market cap and dividend yield as of April 22, 2015

(2)

Financial figures for the period ended March 31, 2015

5

Stock Price

$17.25

$25.25

$26.00

$33.61

12/31/2011

12/31/2012

12/31/2013

12/31/2014 |

6

Nasdaq Ceremony |

7

CEO Report |

Business Overview

Ended 2014 with record net loans

outstanding, net income, and

stockholders’

equity

Profitable throughout the economic

cycle and never reported a quarterly

loss

History of quarterly cash dividend

payments, and maintained dividend

amount during recession

Excellent asset quality, strong liquidity

profile, and robust core deposit base

Strong returns and efficiency ratios

Two strong Ohio banking markets

For over 100 years, Middlefield Banc

Corp. has supported its communities

by offering customers superior

financial products, exceptional

service, and modern banking

amenities

8 |

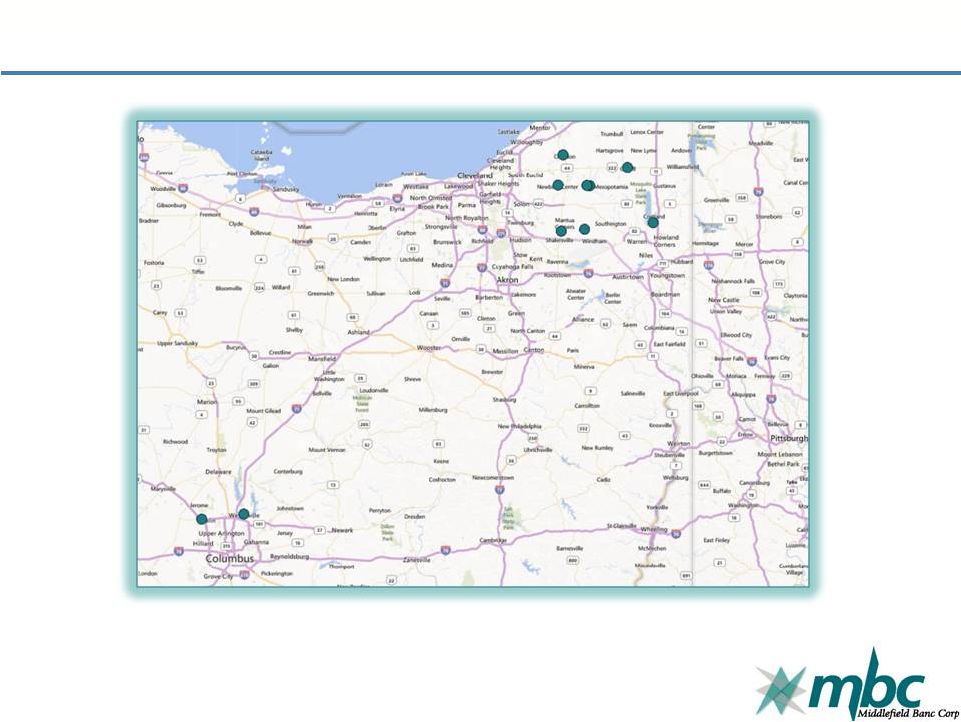

Branch Locations

9 |

Recent Rankings and Awards

SNL Financial

(3)

According

to

a

June

16,

2014

article

from

SNL

Financial,

Middlefield

Banc

Corp.

had

the

10

th

highest

ROAE

out

of

public community banks with under $1 billion in assets.

Independent Banker

(4)

According

to

May

30,

2014

study

from

Independent

Banker,

Middlefield

Banc

Corp.

had

the

21

st

highest

ROE

of

community banks with assets of $500 million to $1 billion

KBW

(2)

On April 13, 2015, Middlefield was named one of 25 U.S. banking institutions to KBW’s

coveted “Bank Honor Roll” of superior performers. Honor Roll members

are publicly traded banking institutions with more than $500 million in total assets

that have not reported an annual loss over the past 10 years, had 2014 annual EPS equal to or

greater than peak EPS over the past 10 years, and consecutive increases in EPS since

2009. American Banker

(1)

Middlefield

Banc

Corp.

was

ranked

38

th

out

of

the

top

200

community

banks

and

thrifts

by

3-year

Avg.

ROE

according to an April 27, 2015 American Banker article.

10

(1)

American Banker April 27, 2015

(2)

KBW April 13, 2015

(3)

SNL June 16, 2014

(4)

Independent Banker

Sources:

http://www.americanbanker.com/

http://www.kbw.com/content/the-firm-PDFs/press-releases/KBW-2015-Bank-Honor-Roll-04.13.15.pdf

http://independentbanker.org/2014/05/community-banks-with-assets-of-more-than-500-million-to-1-billion/

Disproving the naysayers, some banks under $1B thrive

By Kiah Lau Haslett and Marshall Schraibman |

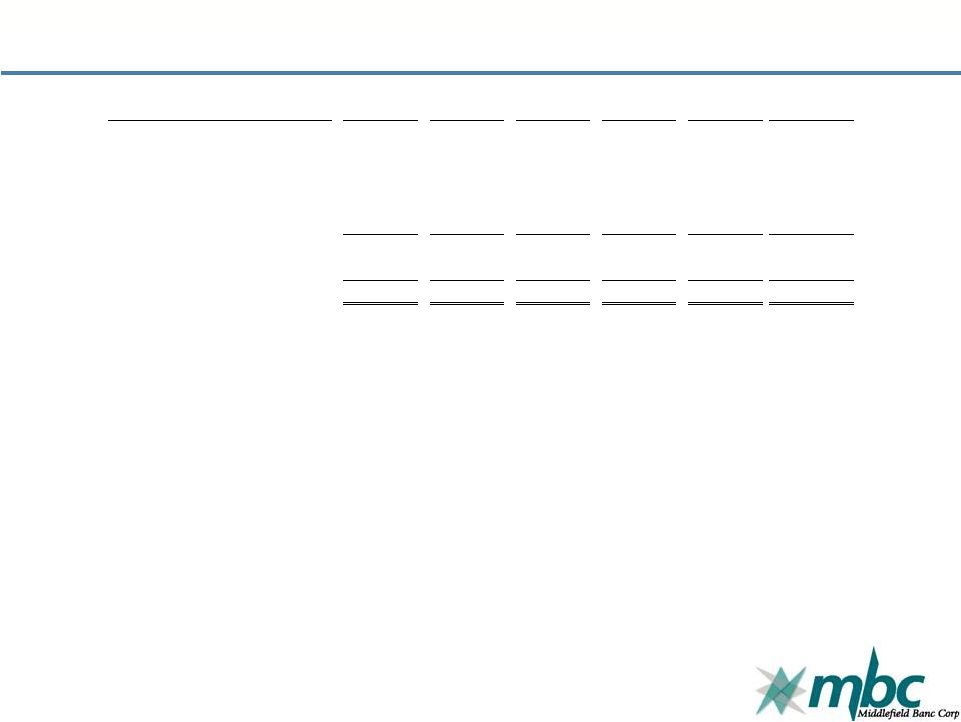

Financial Summary

Dollars in thousands

2009

2010

2011

2012

2013

2014

Net interest income

14,268

18,149

21,075

22,299

22,928

23,804

Provision for loan losses

2,578

3,580

3,085

2,168

196

370

Noninterest income

2,668

2,623

2,237

3,451

3,145

3,588

Noninterest expense

12,650

14,763

15,501

15,639

16,870

17,850

Income before income taxes

1,708

2,429

4,726

7,943

9,007

9,172

Income taxes

(73)

(88)

596

1,662

1,979

1,992

Net income

1,781

2,517

4,130

6,281

7,028

7,180

Net interest margin

3.30%

3.41%

3.65%

3.74%

3.85%

3.93%

Total assets

558,658

632,197

654,551

670,288

647,090

677,531

Loans outstanding, net

348,660

366,277

395,061

400,654

428,679

463,738

Deposits

487,106

565,251

580,962

593,335

568,836

586,112

Equity capital

36,707

38,022

47,253

55,437

53,473

63,867

Earnings per share

1.15

1.60

2.45

3.29

3.48

3.52

Cash dividend (per share)

1.04

1.04

1.04

1.04

1.04

1.04

Dividend pay-out ratio

90.28%

65.04%

42.71%

31.87%

29.84%

29.54%

Return on average assets

0.36%

0.41%

0.65%

0.95%

1.06%

1.07%

Return on average equity

4.90%

6.44%

10.24%

11.98%

13.17%

12.17%

11 |

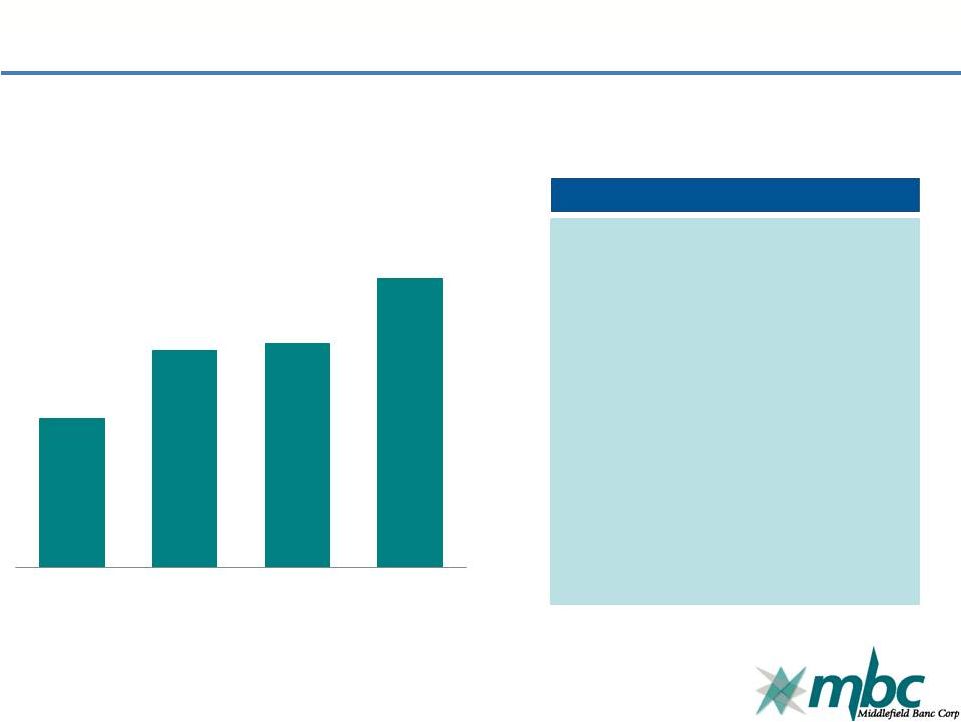

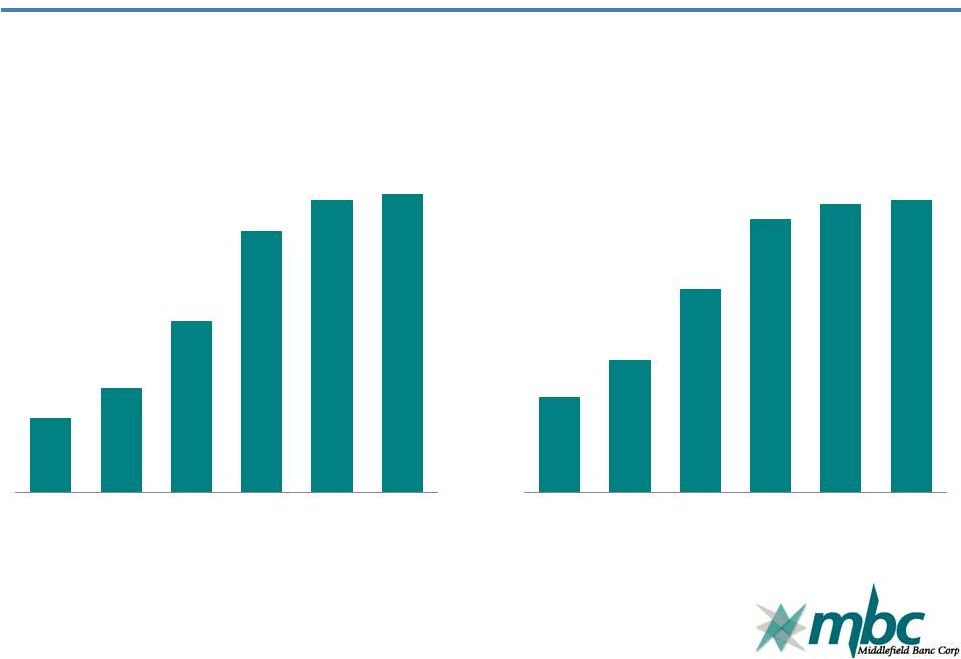

Annual Profitability

Net Income

(In millions)

Diluted EPS

MBCN has been consistently profitable through the economic cycle

and has never reported a quarterly loss.

12

$1.8

$2.5

$4.1

$6.3

$7.0

$7.2

09

10

11

12

13

14

$1.15

$1.60

$2.45

$3.29

$3.48

$3.52

09

10

11

12

13

14 |

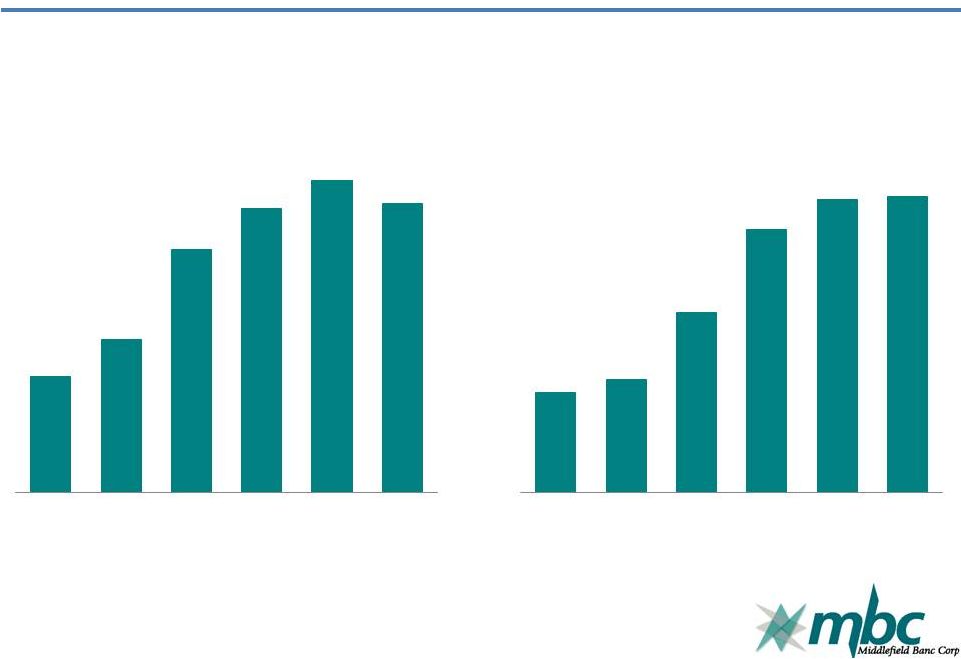

Annual Returns

Return on Average Equity

Return on Average Assets

13

4.90%

6.44%

10.24%

11.98%

13.17%

12.17%

09

10

11

12

13

14

0.36%

0.41%

0.65%

0.95%

1.06%

1.07%

09

10

11

12

13

14 |

Market Demographics Stronger than State

Market

Rank

Company

Total

Median

Median Value

Unemployment

Based on

Deposits in

Population

Household

Owner-Occupied

Rate

Share of

Market

2013

Income

Housing Units

December

County

Deposits

($000)

(1)

(est.)

(2)

2013 ($)

(2)

2013 ($)

(2)

2014 (%)

(3)

Geauga

1

360,742

93,972

66,428

224,700

4.3

Geauga County

has the 3rd highest

Portage

6

92,232

163,862

52,337

150,300

4.8

median household

income in the State.

Franklin

25

61,079

1,212,263

51,460

150,800

3.8

Trumbull

10

48,954

206,442

41,798

97,400

7.5

Ashtabula

8

26,837

101,497

40,839

110,800

5.8

Aggregate: Entire State of Ohio

11,570,808

48,308

130,800

4.8

Aggregate: National

316,128,839

53,046

176,700

5.6

(1)

Obtained from the FDIC's Summary of Deposits data, as of June 30, 2014

(www.fdic.gov). (2)

Information from the U. S. Census Bureau

(www.quickfacts.census.gov). (3)

Sourced from Ohio Department of Job and Family Services and the Bureau

of Labor Statistics. Eight of the bank's 10 offices (and more

than 86% of its deposits) are located in counties that have

stronger demographics than the State averages (median household

income, median value of owner-occupied housing, and

employment rates).

14 |

Deposit Market Share

Ashtabula, Geauga, Portage & Trumbull Counties

June 30, 2014

Rank in

Market

Institution

Number of

Branches

Total Market

Share (%)

1

The Huntington National Bank

38

1,532,821

20.60

2

JP Morgan Chase Bank, N.A.

19

894,279

12.02

3

8

528,765

7.11

4

KeyBank, National Association

15

522,389

7.02

5

PNC Bank, National Association

11

506,911

6.81

6

Talmer Bank and Trust

9

464,660

6.24

7

Cortland Savings & Banking Co.

10

385,484

5.18

8

FirstMerit Bank, N. A.

12

347,397

4.67

Total for institutions in Market

190

7,441,520

15

Total Deposits in

Market ($M)

The Middlefield Banking Company |

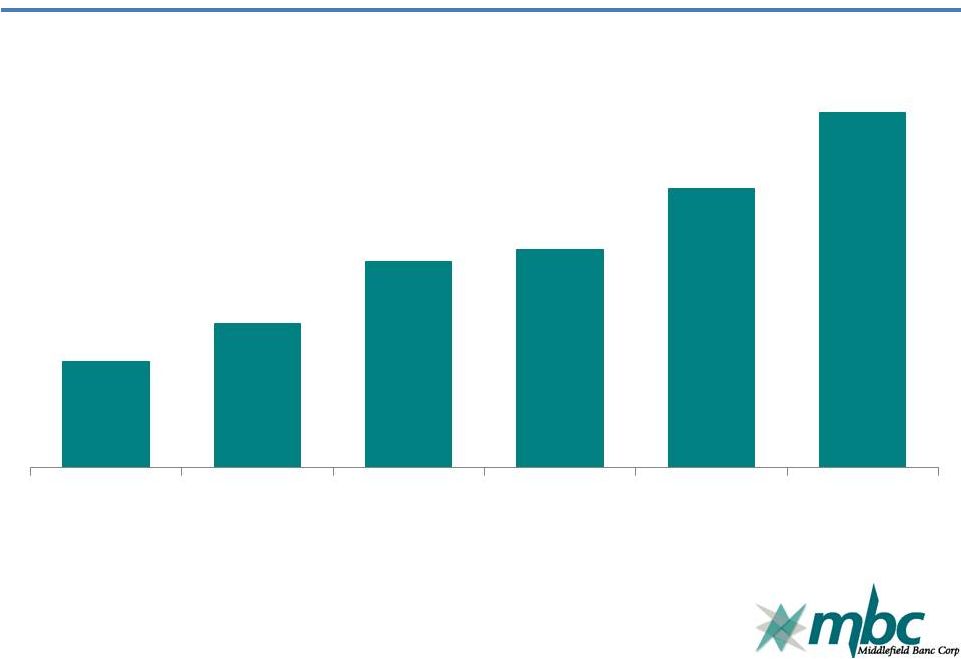

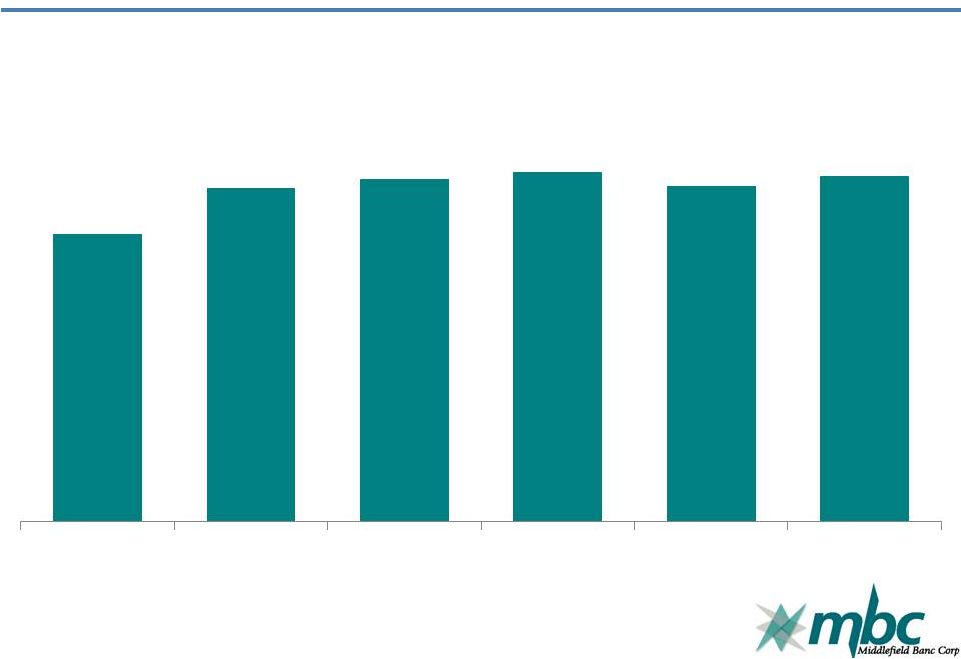

Annual

Loan

Growth

(1)

(1) Dollars in millions

16

$463.8

$428.7

$400.7

$395.1

$366.3

$348.7

14

13

12

11

10

09 |

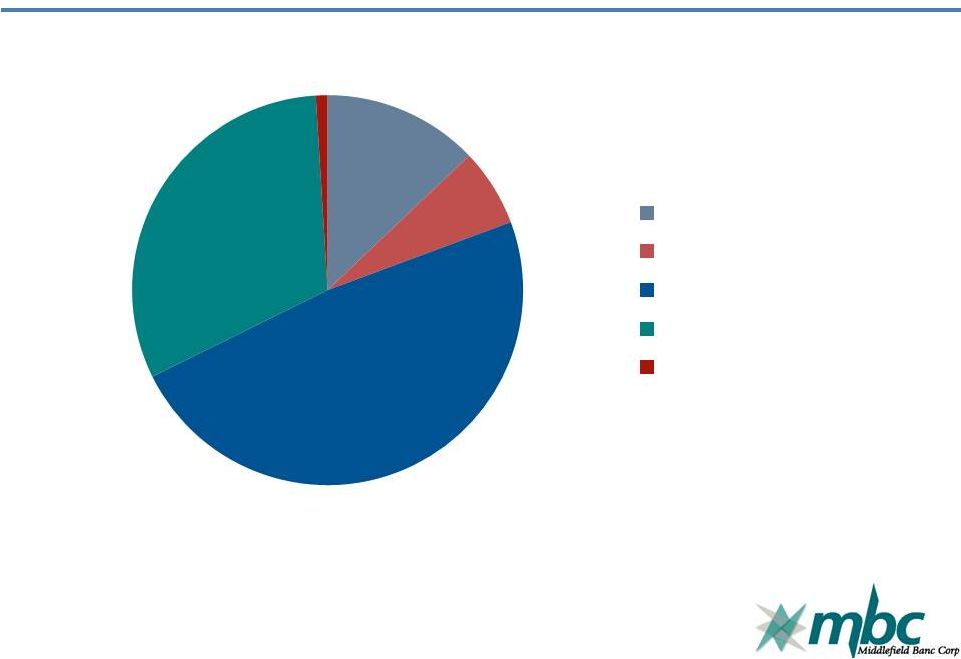

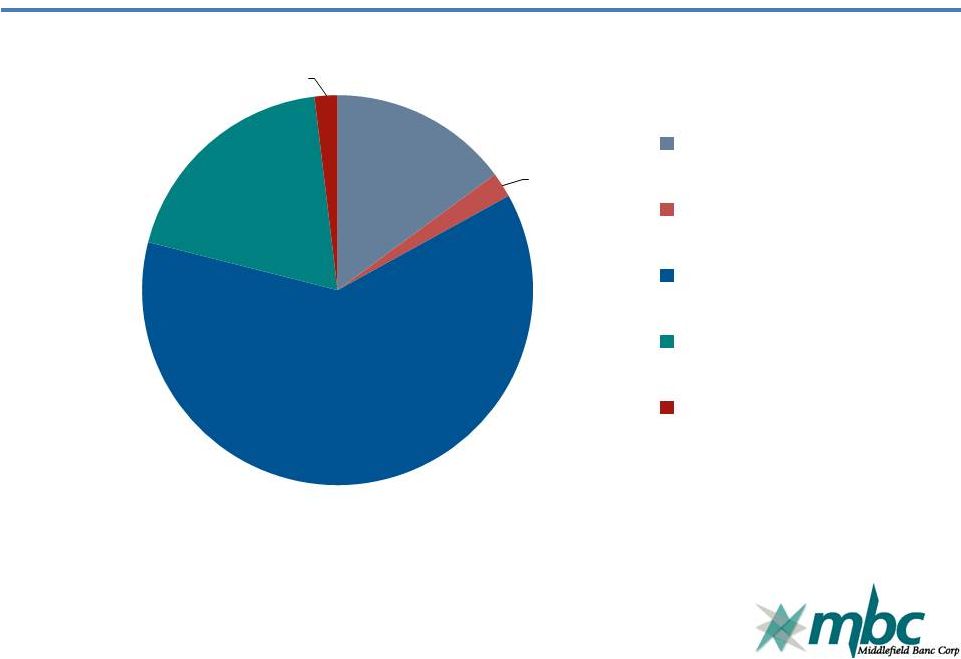

Loan Portfolio at December 31, 2014

17

13%

7%

48%

31%

1%

Commercial & Industrial

Real Estate -

Construction

Residential Mortgage

Commercial Mortgage

Consumer Installment |

Asset Quality

2010

2011

2012

2013

2014

Nonperforming Loans

$19,986

$24,546

$14,224

$12,290

$9,048

Real Estate Owned

2,302

2,196

1,846

2,698

2,590

Nonperforming Assets

$22,288

$26,742

$16,070

$14,988

$11,638

Nonperforming Assets/

Total Assets (%)

3.52%

4.09%

2.40%

2.32%

1.72%

Allowance for Loan Losses

$6,221

$6,819

$7,779

$7,046

$6,846

Allowance/Total Loans (%)

1.67%

1.70%

1.90%

1.62%

1.45%

Net Charge-off Ratio (%)

0.63%

0.65%

0.30%

0.19%

0.38%

-

Problem

assets

peaked

in

2011,

primarily

driven

by

non-owner

occupied

1

-

4

family

in

Central

Ohio

market.

-

Net charge-offs returned to normalized levels in 2012.

-

Strong reserve coverage provides flexibility in managing potential losses

with reduced impact on net income. 18 |

Managed

Deposit

Growth

(1)

Cost of deposits declined from 2.69% in 2009 to 0.74% in 2014

(1) Dollars in millions

19

$487.1

$565.3

$581.0

$593.3

$568.8

$586.1

09

10

11

12

13

14 |

Strong Core Deposit Base at December 31, 2014

20

15%

2%

62%

19%

2%

Non-interest bearing

Demand

Money Market

Time

Interest-bearing Demand

Savings |

Capital Ratios at December 31, 2014

To Be Well

Capitalized

Middlefield Banc

Corp.

The Middlefield

Banking Company

Tier 1 Risk-Based

Capital

6.00%

13.38%

12.95%

Total Risk-Based

Capital

10.00%

14.64%

14.19%

Tier 1 Leverage

Capital

5.00%

9.60%

9.25%

All capital ratios exceed regulatory requirements to qualify as well

capitalized. 21 |

2014 Initiatives

Personnel/Talent

Strong management to drive performance growth

Sales-orientation and cultural fit

Operations/Risk Management

Expanded technology

Scaled to support growth initiatives

Diligent risk management incorporating regulatory

environment

Expand Share of Market/Share of Customer

Identify target markets and customer segments

Commercial relationship opportunities

De novo expansion and strategic acquisitions

22 |

Today’s Banking Landscape

High level of competition for share of wallet

Increasing regulatory concerns with added costs

for smaller banks

Economic challenges with a continued low rate

environment and slow growth

Uncertain loan demand

23 |

2015 and Forward

Grow Secondary Mortgage Offering

2015 Strategic Planning Exercise Provides Confidence in

Middlefield’s:

Market position

Product and service offerings

Growth initiatives

Continue to Expand Share of Market/Share of Customer

Identify target markets and customer segments

Commercial relationship opportunities

De novo expansion and strategic acquisitions

24 |

Questions, Comments,

and Discussion

25 |

Voting Results

Election of three Directors

Non-binding proposal on compensation

Ratification of appointment of S.R. Snodgrass, P.C.

26 |

Thank you for your support!

May 13, 2015

27 |