Attached files

| file | filename |

|---|---|

| EX-4.3 - EXHIBIT 4.3 - RLJ ENTERTAINMENT, INC. | ex4_3.htm |

| EX-99.2 - EXHIBIT 99.2 - RLJ ENTERTAINMENT, INC. | ex99_2.htm |

| EX-23.2 - EXHIBIT 23.2 - RLJ ENTERTAINMENT, INC. | ex23_2.htm |

| EX-21.1 - EXHIBIT 21.1 - RLJ ENTERTAINMENT, INC. | ex21_1.htm |

| EX-23.1 - EXHIBIT 23.1 - RLJ ENTERTAINMENT, INC. | ex23_1.htm |

| EX-31.1 - EXHIBIT 31.1 - RLJ ENTERTAINMENT, INC. | ex31_1.htm |

| EX-31.2 - EXHIBIT 31.2 - RLJ ENTERTAINMENT, INC. | ex31_2.htm |

| EXCEL - IDEA: XBRL DOCUMENT - RLJ ENTERTAINMENT, INC. | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - RLJ ENTERTAINMENT, INC. | ex32_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the Fiscal Year Ended December 31, 2014 |

OR

|

£

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 for the Transition Period from…………To………… |

Commission File Number 001-35675

RLJ ENTERTAINMENT, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

45-4950432

|

|

|

(State or other jurisdiction of incorporation)

|

(I.R.S. Employer Identification Number)

|

8515 Georgia Avenue, Suite 650, Silver Spring, Maryland, 20910

(Address of principal executive offices, including zip code)

(301) 608-2115

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class:

|

Name of Each Exchange on Which Registered:

|

|

|

Common Stock, par value $0.001

|

NASDAQ Capital Market

|

Securities registered pursuant to Section 12(g) of the Act:

Warrants to purchase Common Stock

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES £ NO R

Indicate by check mark if the registrant is not required to file report pursuant to Section 13 or Section 15(d) of the Act. YES £ NO R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☑ NO £

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☑ NO £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer £

|

Accelerated filer £

|

Non- accelerated filer £

(Do not check if a smaller reporting company)

|

Smaller reporting company ☑

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES £ NO ☑

The aggregate market value of the voting stock held by non-affiliates computed on June 30, 2014, based on the sales price of $3.82 per share: Common Stock - $28,736,428. All directors and executive officers have been deemed, solely for the purpose of the foregoing calculation, to be “affiliates” of the registrant; however, this determination does not constitute an admission of affiliate status for any of these shareholders.

The number of shares outstanding of the registrant’s common stock as of April 30, 2015: 12,895,772

DOCUMENTS INCORPORATED BY REFERENCE

The registrant has incorporated by reference into Part III of this Annual Report on Form 10-K portions of its proxy statement for its 2015 Annual Meeting of Stockholders to be filed pursuant to Regulation 14A.

RLJ ENTERTAINMENT, INC.

Form 10-K Annual Report

For The Year Ended December 31, 2014

|

PART I

|

4 | ||

|

ITEM 1.

|

4 | ||

|

ITEM 1A.

|

20 | ||

|

ITEM 1B.

|

28 | ||

|

ITEM 2.

|

28 | ||

|

ITEM 3.

|

29 | ||

|

ITEM 4.

|

29 | ||

|

PART II

|

|||

|

ITEM 5.

|

30 | ||

|

ITEM 6.

|

31 | ||

|

ITEM 7.

|

32 | ||

|

ITEM 7A.

|

51

|

||

|

ITEM 8.

|

52

|

||

|

ITEM 9.

|

95 | ||

|

ITEM 9A.

|

95 | ||

|

ITEM 9B.

|

96 | ||

|

PART III

|

|||

|

ITEM 10.

|

97 | ||

|

ITEM 11.

|

97 | ||

|

ITEM 12.

|

97 | ||

|

ITEM 13.

|

97 | ||

|

ITEM 14.

|

97 | ||

|

PART IV

|

|||

|

ITEM 15.

|

98 | ||

| 102 | |||

|

CERTIFICATIONS

|

|||

|

FORWARD-LOOKING STATEMENTS

|

This Annual Report on Form 10-K for the year ended December 31, 2014 (or Annual Report) includes forward-looking statements that involve risks and uncertainties within the meaning of the Private Securities Litigation Reform Act of 1995. Other than statements of historical fact, all statements made in this Annual Report are forward-looking, including, but not limited to, statements regarding industry prospects, future results of operations or financial position, and statements of our intent, belief and current expectations about our strategic direction, prospective and future results and condition. In some cases, forward-looking statements may be identified by words such as “will,” “should,” “could,” “may,” “might,” “expect,” “plan,” “possible,” “potential,” “predict,” “anticipate,” “believe,” “estimate,” “continue,” “future,” “intend,” “project” or similar words.

Forward-looking statements involve risks and uncertainties that are inherently difficult to predict, which could cause actual outcomes and results to differ materially from our expectations, forecasts and assumptions. Factors that might cause such differences include, but are not limited to:

| § | Our financial performance, including our ability to achieve revenue growth, margins or earnings before income tax, depreciation, amortization, adjusted for cash investment in content, interest expense, loss on extinguishment of debt, transaction and severance costs, warrants and stock-based compensation (or Adjusted EBITDA); |

| § | The effects of limited cash liquidity on operational growth; |

| § | Our obligations under the Credit Agreement, including our principal repayment obligations; |

| § | Our ability to satisfy financial ratios; |

| § | Our ability to raise additional capital to reduce debt, improve liquidity and fund capital requirements; |

| § | Our ability to fund planned capital expenditures and development efforts; |

| § | Our inability to gauge and predict the commercial success of our programming; |

| § | The ability of our officers and directors to generate a number of potential investment opportunities; |

| § | Our ability to maintain relationships with customers, employees and suppliers; |

| § | Delays in the release of new titles or other content; |

| § | The effects of disruptions in our supply chain; |

| § | The loss of key personnel; |

| § | Our public securities’ limited liquidity and trading; or |

| § | Our ability to continue to meet the NASDAQ Capital Market continuing listing standards. |

You should carefully consider and evaluate all of the information in this Annual Report, including the risk factors listed above and elsewhere, including “Item 1A. Risk Factors” below. If any of these risks occur, our business, results of operations, and financial condition could be harmed, the price of our common stock could decline and you may lose all or part of your investment, and future events and circumstances could differ significantly from those anticipated in the forward-looking statements contained in this Annual Report. Unless otherwise required by law, we undertake no obligation to release publicly any updates or revisions to any such forward-looking statements that may reflect events or circumstances occurring after the date of this Annual Report.

|

PART I

|

Overview

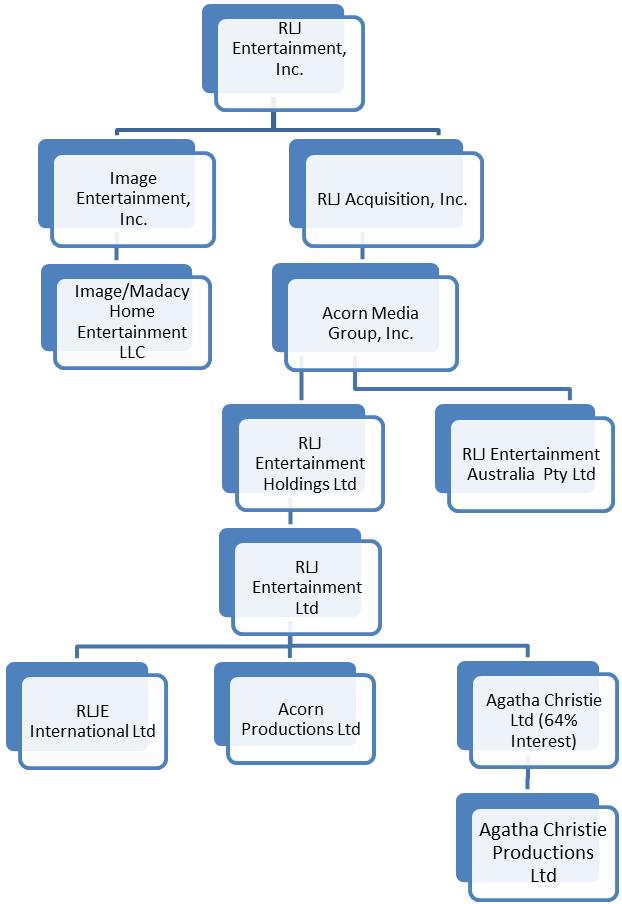

RLJ Entertainment, Inc. (or RLJE) is a global entertainment company with a direct presence in North America, the United Kingdom (or U.K.) and Australia with strategic sublicense and distribution relationships covering Europe, Asia and Latin America. RLJE was incorporated in Nevada in April 2012. On October 3, 2012, we completed the business combination of RLJE, Image Entertainment, Inc. (or Image) and Acorn Media Group, Inc. (or Acorn Media or Acorn), which is referred to herein as the “Business Combination.” The use of “we,” “our” or “us” within this Annual Report is referring to RLJE and its subsidiaries.

A summary of our significant corporate entities and structure is as follows:

We acquire content rights in various categories, with particular focus on British mysteries and dramas, urban programming, and full-length motion pictures. We acquire this content in two ways:

| § | Through long-term exclusive licensing agreements where we secure multiple rights to third-party programs. Generally, the rights we secure include broadcast, theatrical, digital and physical (DVD and Blu-ray), and; |

| § | Through development, production, and ownership of original drama television programming through our wholly-owned subsidiary, Acorn Productions Ltd. (or “Acorn Productions”) and our majority-owned subsidiary, Agatha Christie Limited (or ACL), as well as fitness programs through our Acacia brand. |

We control a program library in genres such as British mysteries and dramas, urban/African-American, action/thriller and horror, fitness/lifestyle, and documentaries.

We monetize our library content through carefully managed distribution windows across multiple platforms including broadcast/cable channels, digital distribution formats (which are subscription video on demand (or SVOD), free video on demand (or FVOD), download-to-own, and download-to-rental), and DVD and Blu-ray retail and online ecommerce.

We market our products through a multi-channel strategy encompassing:

|

§

|

The licensing of original program offerings through our wholly-owned subsidiary, Acorn Productions, and our majority-owned subsidiary, ACL (our Intellectual Property Licensing or IP Licensing segment);

|

| § | Wholesale through digital, mobile, broadcast, cable partners, ecommerce and brick and mortar (our Wholesale segment); and |

| § | Direct-to-consumer activities in the United States (or U.S.) and United Kingdom (or U.K.) including traditional and e-commerce offerings and our proprietary subscription-based digital platforms (our Direct-to-Consumer segment). |

Acorn Productions manages and develops our intellectual property rights on British drama and mysteries. These rights include our 64% ownership of ACL. ACL is home to some of the world’s greatest literary works of mystery fiction, including Murder on the Orient Express, Death on the Nile and And Then There Were None and includes publishing and TV/film rights to iconic sleuths such as Hercule Poirot and Miss Marple. The Agatha Christie library contains approximately 80 novels and short story collections, 19 plays and a film library of over 100 made-for-television films. In 2013, ACL commissioned a new writer to expand the Agatha Christie library and in the third quarter of 2014, ACL published its first book, The Monogram Murders, since the death of Agatha Christie. Our television productions are typically financed by the pre-sale of certain distribution rights, typically being international TV distribution rights, as well as tax credits. The pre-sale of these rights, alongside the realization of tax incentives, allows Acorn Productions to reduce production risks.

Our wholesale partners are broadcasters, digital outlets and major retailers in the U.S., Canada, U.K. and Australia, including, among others, Amazon, Netflix, Walmart, Target, Costco, Barnes & Noble, iTunes, BET, Showtime, PBS, DirecTV, and Hulu. We have a catalog of owned and long-term licensed content that is segmented into brands such as Acorn (British drama/mystery, including content produced by ACL), Image (independent feature films, action/thriller horror), Urban Movie Channel (or UMC) (urban), Acacia (fitness), and Athena (documentaries). Our owned content includes 28 Foyle’s War made for TV films; multiple instructional Acacia titles; and through our 64% ownership interest in ACL, the Agatha Christie branded library.

Our Direct-to-Consumer segment includes the continued roll-out of our proprietary subscription-based digital channels, such as our British mystery and drama network, Acorn TV, a fitness and lifestyle channel, Acacia TV, and a recently launched channel focused on providing entertainment to an African-American audience, UMC. As of December 31, 2014, Acorn TV had over 118,000 paying subscribers, compared to 57,000 as of the end of December 2013. We expect the subscriber base to grow in 2015 for all of our subscription-based digital channels as we add more exclusive content to the channels.

Acorn TV was launched in July 2011 and features British mysteries and dramas with exclusive streaming of certain series such as Agatha Christie’s Poirot, Foyle’s War, Doc Martin, Murdoch Mysteries and Midsomer Murders. Acorn TV can be accessed through the internet at www.acorn.tv by using computers, tablets and smartphones, or through Roku, iOS mobile, Samsung Smart TVs and Blu-ray players.

In the latter part of 2014, we launched UMC, a proprietary urban digital network targeting a broad range of urban/African-American households in the U.S. The content serves an underserved audience with a broad range of titles. The channel leverages our current urban content library from Image along with investments in new content in the form of licensing acquisitions such as: The Colony, Kevin Hart: I’m a Grown Little Man, Winnie Mandela, Jamie Foxx: I Might Need Security, Black Coffee and 35 & Ticking. Currently, UMC is offering a 14-day free trial to attract new subscribers and can be accessed through the internet at www.UrbanMovieChannel.com, Roku and through Chromecast. In the near future, this channel will be able to be accessed through applications such as Roku, iOS and Samsung Smart TVs and Blu-ray players.

Earlier in 2014, we also expanded our proprietary digital channels by launching Acacia TV in the U.S. and Europe. Acacia TV is a fitness and lifestyle channel promoting healthy, joyful lives. Subscribers to Acacia TV have access to the full catalog of Acacia fitness videos, customized fitness routines, and other wellness programming produced exclusively for Acacia TV such as nutritional information and food preparation videos. This new digital channel is available on computers, tablets and smartphones and can be accessed on the internet at www.us.acacia.tv. Currently, subscribers have access to fitness videos such as: Bethenny’s Skinny Girl Workout, Lisa Whelchel’s Everyday Workout for the Everyday Woman, RIPPED Total Body Challenge, Kenya Moore Booty Boot Camp and Shiva Rea Fluid Power. Our plan is to build content for Acacia TV that will be attractive to our existing and new Acacia customers within our direct-to-consumer segment, thus driving traffic to the Acacia website and increasing customer retention. By continuing to add content to this digital channel, we plan to build it into the flagship of the Acacia brand.

Strategic Direction of the Company

RLJE’s management believes that the continued convergence of television and the internet will deepen competition for the attention of viewers and increase the value of content, in particular for scripted television, independent feature films and niche programming. RLJE intends to create long-term value for its shareholders by investing in its program library and building proprietary SVOD channels for its target audiences:

| § | Program library: RLJE intends to focus its content investments primarily in the development of IP rights for television dramas and the licensing of exclusive rights for scripted television, independent feature films, urban content, fitness/wellness programs and documentaries. |

| § | Proprietary SVOD channels: RLJE will continue to invest in the development of proprietary SVOD channels such as Acorn TV, UMC and Acacia TV in order to develop a direct and ongoing relationship with viewers with specific interests. We plan on increasing our subscriber base by utilizing exclusive windows with premier content. We are also exploring other potential SVOD channels using our existing library including such titles as: Rage, Odd Thomas, The Colony, and Creep Show for a Horror/Thriller channel; and titles such as: WW II: A Complete History, Ancient Secrets of the Bible, Power of Myth, Civil War: Untold Story and Baseball: Golden Age of America's Game from our Athena brand for a documentary channel. Management views these channels as a new window of exploitation that is complementary to our other current forms of distribution. |

| § | Other long-term growth strategies include: |

| Ø | The increased exploitation of our film and television library outside the U.S. with a particular emphasis on key markets such as Europe and Asia. |

| Ø | The acquisition of content libraries that either fits or complements our genre-based focus. |

| Ø | The continued expansion of our direct-to-consumer e-commerce business. |

| Ø | The evaluation and pursuit of opportunities to own broader digital distribution platforms, including cable/satellite networks or VOD providers, where we can directly distribute our content and expand our brands. |

Investments in Content

Our business model relies on developing and acquiring content that satisfies the desire of niche audiences for higher quality entertainment within specific genres. We then monetize content agnostically across all platforms through carefully orchestrated windows of distribution. When developing content, we develop new treatments from the intellectual property (or IP) we own. We also acquire finished programs through long-term exclusive contracts. We invest in content offerings that we believe will meet or exceed management’s 20% return-on-investment (or ROI) threshold. Our definition of ROI is the return on investment over the life of the investment (generally 7 - 10 years), and it is calculated by dividing estimated content earnings by its initial investment. Content earnings are calculated by estimating the future earnings, which is after subtracting costs (including overhead) necessary to maintain the investment, and discounting the earnings using a risk-appropriate rate.

RLJE invests approximately $45 - $60 million annually in content. These investments are added to our balance sheet as program rights and are expensed through the statement of operations as either amortization of advances or as overage royalty payments. During 2013 and 2014, management worked extensively on the reallocation of our content investments pursuing content with higher financial returns and strong strategic value. Management terminated content genres and content agreements that were either not profitable, not meeting our financial goals, or areas where we could not acquire comprehensive long-term distribution rights or control over the content. Additionally, Management re-aligned the Company’s investment across key genres, mainly British mystery and dramas, urban, action-thriller and horror, fitness, and documentaries.

Our investments in content provide us with significant cash flows and generate working capital, which are continuously redeployed to acquire or produce new content and fund strategic initiatives. Some of the key program releases in 2014, which generated a significant amount of revenues for us, and planned releases for 2015 and 2016 are as follows:

|

British Mystery and Drama:

§ Agatha Christie's Poirot, Series 11

§ Agatha Christie’s Poirot, Series 12

§ Agatha Christie’s Poirot, Series 13

§ Agatha Christie’s Poirot, Complete Cases Collection

§ Agatha Christie’s Poirot Fan Favorites Collection

§ Foyle's War, Set 7 (Series 8)

§ Doc Martin, Series 6

§ The Fall, Series 2 (UK)

§ Miss Fisher's Murder Mysteries, Series 2

§ Midsomer Murders, Set 23

§ Midsomer Murders, Set 24

§ Murdoch Mysteries, Season 7

§ New Tricks, Season 10

§ Vera, Set 3

§ Vera, Set 4

§ The Missing (UK)

§ George Gently, Series 6

§ Jack Taylor, Set 2

§ Agatha Christie's Marple, Series 6

§ Still Life: A Three Pines Mystery

§ Jeeves & Wooster Complete Collection

§ Upstairs, Downstairs: The Ultimate Collection

§ Case Histories, Series 2

§ Line of Duty, Series 2

§ Hinterland, Series 1

|

|

|

Urban:

§ Winnie Mandela

§ The Suspect

§ And Then There Was You

§ A Cross to Bear

§ Black Coffee

§ In God's Hands

§ Four of Hearts

§ Love the One You're With

§ The Divorce

§ Laughing to the Bank

|

|

|

Action/Thriller:

§ Rage

§ Devil's Knot

§ Odd Thomas

§ Drive Hard

§ The Outsider

§ The Colony

§ Way of the Wicked

§ Sparks

§ The Adventurer: The Curse of the Midas Box

|

|

|

Horror:

§ Wolf Creek 2

§ Cabin Fever: Patient Zero

§ All Cheerleaders Die

§ The Invoking

§ Aftermath

§ Paranormal Diaries

§ Werewolf Rising

§ Misfire

§ Devil Incarnate

§ Hunting the Legend

§ Tom Holland's Twisted Tales

§ Day of the Mummy

§ Camp Dread

§ Phobia

§ Varsity Blood

§ Blackwater Vampire

|

|

|

Fitness:

§ Exhale: Core Fusion Barre Basics for Beginners

§ Lisa Whelchel's Everyday Workout for Everyday Woman

§ Shiva Rea: Core Yoga

§ Tai Chi for Beginners with Grandmaster William C.C. Chen

§ R.I.P.P.E.D. Total Body Challenge

|

|

|

Documentaries:

§ Ancient Secrets of the Bible

§ Civil War: The Untold Story

§ David Suchet: In the Footsteps of St. Paul

|

|

|

2015/2016 Planned Releases

§ And Then There Were None

§ Partners in Crime

§ Foyle’s War, Set 8 (Series 9)

§ The Cobbler

§ Rewrite

§ Mysterious Ways

§ Blackbird

§ Hotel Rwanda

§ Barbershop

|

|

Growth Strategy

The last 12 months were primarily dedicated to cost containment, reallocation of content investments and the launching of our new proprietary digital channels, UMC and Acacia TV. Our growth strategy for the next 12 – 18 months is focused on revenue growth, improving net income and increasing EBITDA while keeping operating costs contained. We plan to achieve these goals through organic activities including:

| § | Acquisition of long-term and exclusive broad exploitation rights for finished programs across key genres that meet financial criteria of at least 20% targeted ROI including allocation of all direct and indirect costs through net income before taxes; |

| § | Production and purchase of new intellectual property rights, particularly for British scripted dramas and mysteries, and urban/African-American content; |

| § | Expansion of content offerings on all current and emerging digital platforms as consumers migrate from hard goods to digital consumption. In particular, we intend to grow our proprietary SVOD channels through new investments in exclusive content, promotion and improved information technology (or IT) infra-structure. Digital platforms also create opportunities for RLJE to improve gross margin as the cost to deliver can be considerably lower; |

| § | Expansion of international distribution footprint. Expand licensing and direct exploitation efforts in territories such as Europe and Asia. |

Our business model minimizes production and box-office risks by acquiring finished products with long-term rights over multiple platforms. In addition, our business is complemented, particularly in the British mystery and drama genre, by the development of our own IP, whereby we leverage the operations of Acorn Productions and our relationships in the U.K. including our 64% ownership of ACL. We strive to maximize the value of our program library by pursuing the development and acquisition of content with long-term value and by actively managing all windows of exploitation. Also, our brands and long-running franchises promote customer loyalty and lower our overall investment risk.

Our Primary Brands

We focus on high-quality British mystery and drama television, action and thriller independent feature films and diverse urban content, along with fitness and documentary lines. Titles are segmented into genre-based, franchise and content program lines and are exploited through our various brands. Our brands are as follows:

|

The bestselling novelist of all time, Agatha Christie has sold more than 2 billion books, and her work contains more than 80 novels and short story collections, 19 plays and a film library of over 100 TV productions. In February 2012, Acorn Media Group acquired a 64% stake in ACL. Known for specializing in the best of British television, Acorn monetizes high-quality dramas and mysteries to the broadcast/cable and home video windows within the North American, U.K. and Australian markets. Acorn is known for mystery and drama franchises and has been releasing TV movie adaptations featuring Agatha Christie’s two most famous characters, Hercule Poirot and Miss Marple, for over a decade; both series ranking among our all-time bestselling lines. Through Agatha Christie Limited, Acorn manages the vast majority of Agatha Christie publishing and television/film assets worldwide and across all mediums and actively develops new content and productions. In addition to film and television projects, in the third quarter of 2014, ACL published its first book, The Monogram Murders, since the death of Agatha Christie. The Agatha Christie family retains a 36% holding, and Mathew Prichard, Agatha Christie’s grandson, remains Chairman of ACL.

|

Acorn Productions provides us access to new content as a permanent presence in the U.K. television programming community. We further leverage the Acorn brand in our direct-to-consumer outlets in the U.S. and U.K. for our home-video releases and other complementary merchandise. With a mission to provide exceptional entertainment, imaginative gifts and uncommon quality, we market to consumers via two print catalogs, our online outlets, and our subscription digital television channel. The digital channel, Acorn TV, offers viewers over 1000 hours of high-quality British television programming, streaming 24/7 without commercials and on demand. New content is added on a weekly basis. Paid subscribers have access to all of the available programming, but Acorn TV offers several options to “try before you buy” through Apple TV, Apple iPhones, Apple iPads, Samsung mobile and tablets, YouTube and Roku. Some of the series currently airing on Acorn TV are Foyle’s War, Series 9, Poirot, Serangoon Road, The Palace, New Worlds, Secret State and The Blue Rose. As of December 31, 2014, Acorn TV surpassed 118,000 paid subscribers. The Acorn catalog (www.acornonline.com) focuses on British television, specialty programming and other distinctive merchandise. Our Acorn brand generates revenues that are reported in the IP Licensing (Agatha Christie revenues), Wholesale (DVD and digital download sales) and Direct-to-Consumer segments (catalog sales and digital channels revenues).

|

Image Entertainment (or Image) is a leading film and television licensee focusing on action, thriller, and horror independent feature films. Image licenses exclusive long-term exploitation rights across all distribution channels, with terms ranging generally from 5 to 25 years. Image content is currently distributed primarily in the U.S. and Canada through broadcast/cable, physical and digital platforms. In 2014, we began to exploit Image-branded content in the U.K. and Australia. Our Image titles that generated the highest amount of revenues in 2014 were Rage, Odd Thomas and Devil’s Knot. All of the revenues generated by the Image brand are included in our Wholesale segment.

|

|

The Urban Movie Channel (urbanmoviechannel.com) or UMC, launched in November 2014. UMC is a premium subscription-based streaming service exclusive to RLJ Entertainment, Inc. and it is devoted to the development, production, and acquisition of feature films, comedy specials, stage plays, documentaries, music, and entertainment for African American and urban audiences. New titles are added weekly in addition to the more than 150 titles in our UMC library, which include live stand-up performances featuring Academy Award® winner Jamie Foxx and comedic rock star Kevin Hart; documentaries Dark Girls and I Ain’t Scared of You: A Tribute to Bernie Mac; feature films All Things Fall Apart starring Grammy Award® winner 50 Cent and directed by Mario Van Peebles, The Last Fall starring budding superstars Lance Gross and Nicole Beharie, and The Colony starring Laurence Fishburne; and stage play productions including What My Husband Doesn’t Know by David E. Talbert, who is described by Variety as “the acknowledged kingpin of urban musicals.” Subscribers can access UMC from their tablet, phone and laptop to watch movies from today’s most recognizable talent available on demand and commercial-free.

|

Other Brands

|

Acacia is a healthy-living brand that encompasses original programming on DVD, a direct-to-consumer catalog and a recently launched digital channel called Acacia TV. Acacia provides distinctive, nature-oriented products to enhance customers’ enjoyment of their surroundings and to improve their appearance and well-being. We cater to customers seeking quality products that focus on physical and spiritual well-being, fitness and natural decor.

|

|

Athena is a branded line of home-video products providing a rich and enjoyable learning experience to intellectually curious consumers. These in-depth, entertaining, long-form documentaries facilitate the pursuit of lifelong learning on a diverse range of subjects. Programs include 8- to 20-page booklets with title-specific content, DVD extras and exclusive web content to enhance the learning experience and provide viewers with valuable supplementary information. Our Athena products are available through the Acorn direct-to-consumer catalog.

|

Image Madacy Entertainment

The Image Madacy Entertainment library includes classic television and historical footage, as well as numerous special-interest projects. Some of the widely distributed titles include The Three Stooges, The John Wayne Collection, The Lone Ranger Collection, Bonanza and The Beverly Hillbillies, as well as documentaries about World War I and II, the Civil War, the Vietnam War, NASA, dream cars, trains and various travel collections.

Trademarks

We currently use several registered trademarks including: RLJ Entertainment, Acorn, Acorn Media, Acacia, Athena, Yoga to the Rescue, Healthy Joyful Living, Keeping Fit, Keeping Fit in Your 50s, Engage Your Mind Expand Your World, The Best British TV, The Best British Television, Acorn TV, Image, Image Entertainment, One Village Entertainment, Image Madacy Entertainment, and Midnight Madness Series. We also currently use registered trademarks through our majority-owned subsidiary ACL including: Agatha Christie, Miss Marple and Poirot. Recently, we filed U.S. Federal trademarks for “UMC - Urban Music Channel” in May 2014 and “Acacia TV” in June 2014.

The above-referenced trademarks, among others, are registered with the U.S. Patent and Trademark Office and various international trademark authorities. In general, trademarks remain valid and enforceable as long as the marks are used in connection with the related products and services and the required registration renewals are filed. We believe our trademarks have value in the marketing of our products. It is our policy to protect and defend our trademark rights.

Segments

Management views the operations of the Company based on three distinct reporting segments: (1) Intellectual Property Licensing (or IP Licensing); (2) Wholesale; and (3) Direct-to-Consumer. Operations and net assets that are not associated with any of these operating segments are reported as “Corporate” when disclosing and discussing segment information. The IP Licensing segment includes intellectual property rights that we own, produce and then exploit worldwide in various formats including DVD, Blu-ray, digital, broadcast (including cable and satellite), VOD, streaming video, downloading and sublicensing. Our Wholesale and Direct-to-Consumer segments consist of the acquisition, content enhancement and worldwide exploitation of exclusive content in the same markets as our owned content. The Wholesale segment exploits the content to third parties such as Walmart, Best Buy, Target, Amazon and Costco while the Direct-to-Consumer segment distributes directly to the consumer through different exploitation channels. The Direct-to-Consumer segment distributes film and television content through our e-commerce websites, mail-order catalogs and our proprietary, subscription-based, digitally streaming channels (Acorn TV, UMC and Acacia TV). The segment also sells complementary merchandise through our mail-order catalogs: Acorn and Acacia.

Net revenues by reporting segment for the periods presented are as follows:

|

Years Ended

December 31,

|

||||||||

|

(In thousands)

|

2014

|

2013

|

||||||

|

IP Licensing

|

$

|

8,752

|

$

|

8,019

|

||||

|

Wholesale

|

91,379

|

115,397

|

||||||

|

Direct-to-Consumer

|

37,558

|

41,414

|

||||||

|

Total revenues

|

$

|

137,689

|

$

|

164,830

|

||||

Assets for each reporting segment and Corporate as of December 31, 2014 and 2013 are as follows:

|

(In thousands)

|

December 31,

|

|||||||

|

2014

|

2013

|

|||||||

|

IP Licensing

|

$

|

30,197

|

$

|

36,127

|

||||

|

Wholesale

|

140,935

|

160,968

|

||||||

|

Direct-to-Consumer

|

12,049

|

15,964

|

||||||

|

Corporate

|

8,873

|

7,211

|

||||||

|

$

|

192,054

|

$

|

220,270

|

|||||

IP Licensing

A summary of the IP Licensing segment’s revenues and expenses is as follows:

|

Years Ended

December 31,

|

||||||||

|

(In thousands)

|

2014

|

2013

|

||||||

|

Revenue

|

$

|

8,752

|

$

|

8,019

|

||||

|

Operating costs and expenses

|

(6,662

|

)

|

(7,967

|

)

|

||||

|

Depreciation and amortization

|

(115

|

)

|

(89

|

)

|

||||

|

Share in ACL earnings

|

2,580

|

3,296

|

||||||

|

IP Licensing segment contribution

|

$

|

4,555

|

$

|

3,259

|

||||

Our IP Licensing segment includes owned intellectual property that is either acquired or created by us and is licensed for exploitation worldwide. The operating activities consist of our 100% interest in Foyle’s War Series 8 and Series 9. Our IP Licensing segment does not include revenues generated or costs incurred from the exploitation of Foyle’s War Series by our Wholesale segment. Also included is our 64% majority interest in ACL. ACL is accounted for using the equity method of accounting given the voting control of the Board of Directors by the minority shareholder. Gross margin percentages generated from content that is owned is generally higher than margins realized from content that is not owned.

As part of our growth strategy, we plan to continue to produce and own more intellectual property with an emphasis in British mysteries and dramas and urban programming.

Wholesale

A summary of the Wholesale segment’s revenues and expenses is as follows:

|

Years Ended

December 31,

|

||||||||

|

(In thousands)

|

2014

|

2013

|

||||||

|

Revenue

|

$

|

91,379

|

$

|

115,397

|

||||

|

Operating costs and expenses

|

(85,595

|

)

|

(118,455

|

)

|

||||

|

Depreciation and amortization

|

(1,684

|

)

|

(3,115

|

)

|

||||

|

Wholesale segment contribution

|

$

|

4,100

|

$

|

(6,173

|

)

|

|||

The Wholesale segment consists of acquisition of content, content enhancement and worldwide exploitation of exclusive content in various formats to third parties such as Walmart, Best Buy, Target, Amazon and Costco. We market and exploit our exclusive content through agreements that generally range from 5 to 25 years in duration. The revenues generated in our Wholesale segment are historically our most consistent revenue stream.

While standard DVD comprise a majority of our revenues within this segment, Blu-ray titles and related revenues continue to increase given the format’s growing acceptance. We believe that the affordability of larger screen high-definition television (or HDTV) and ease of use as an entertainment hub in consumer households will continue to accelerate the conversion from standard DVD to Blu-ray formats for all demographics. We also believe there is a significant opportunity for us to realize increased revenues from customers of Acorn branded British mystery and drama product who will be converting their standard DVD collection to Blu-ray. It is expected that future revenues generated from DVD and Blue-ray sales will decline and sale of content to consumers through digital, streaming video and downloading will increase in future years.

We engage in the exclusive licensing of the digital rights to our library of audio and video content. The demand for the types of programming found in our library continues to increase as new digital retailers enter the online marketplace. We seek to differentiate ourselves competitively by being a one-stop source for these retailers who desire a large and diverse collection of entertainment represented by our digital library. We enter into non-exclusive arrangements with retail and consumer-direct entities whose business models include the digital delivery of content. We continue to add video and audio titles to our growing library of exclusive digital rights. The near-term challenges faced by all digital retailers are to develop ways to increase consumer awareness and integrate this awareness into their buying and consumption habits. Some of our digital retailers include Netflix, iTunes, Amazon, Hulu, Microsoft Xbox Live Marketplace, Sony PlayStation, YouTube/Google, Vudu, Vevo, Intel, Roku and Samsung.

We further exploit our product in the ‘traditional’ VOD channels, wherein consumers pay a fee to watch programming via their cable or satellite operators. This business model has expanded in recent years to include exclusive windows for VOD monetization prior to other channels of exploitation. For example, a high-profile release may be released on VOD prior to theatrical exploitation. In that instance, we would receive higher price points and better placement with our VOD providers. Our partners in the VOD space include DirecTV, Dish, inDemand, AT&T Uverse, Vubiquity and Warner Digital Distribution. We also exploit our product to cable networks in the United States. Traditionally, our Acorn product has been sold to PBS or its affiliated stations, while our feature-length product has been sold to a wide array of customers. These cable networks include BET, Chiller, Fearnet, SyFy, CW, Disney, and Lifetime.

Outside North America and the U.K., we sublicense distribution in the areas of home entertainment, television and digital through distribution partners such as Universal Music Group International, BET International, Warner Music Australia and Universal Pictures Australia, each of which pays us a royalty for their distribution of our products.

Direct-to-Consumer

A summary of the Direct-to Consumer segment’s revenues and expenses is as follows:

|

Years Ended

December 31,

|

||||||||

|

(In thousands)

|

2014

|

2013

|

||||||

|

Revenue

|

$

|

37,558

|

$

|

41,414

|

||||

|

Operating costs and expenses

|

(41,413

|

)

|

(44,762

|

)

|

||||

|

Depreciation and amortization

|

(3,415

|

)

|

(2,931

|

)

|

||||

|

Goodwill impairment

|

(981

|

)

|

—

|

|||||

|

Direct-to-Consumer segment contribution

|

$

|

(8,251

|

)

|

$

|

(6,279

|

)

|

||

The Direct-to-Consumer segment exploits the same film and television content as the Wholesale segment but exploits the content directly in the U.S. and the U.K. to consumers through various proprietary SVOD channels and in our catalogs (Acorn and Acacia) and our e-commerce websites. To date, we have three proprietary digital subscription channels, which are Acorn TV, UMC and Acacia TV. We are continually rolling-out new content on our digital channels and attracting new subscribers. As of December 31, 2014, Acorn TV had over 118,000 subscribers compared to 57,000 subscribers at December 31, 2013.

During 2014, we delivered 21.5 million catalogs and flyers of which 20.4 million were delivered in the U.S. and 900,000 were delivered in the U.K. We had approximately 4.4 million visitors in 2014 to our e-commerce websites with 4.7% of the visitors purchasing our products. The catalogs and online businesses have diverse product offerings marketed to a select audience. Through our brands, Acorn and Acacia, our product offering includes DVDs, lifestyle products for the discerning British mystery consumer, apparel, jewelry, and decorative household items. The Direct-to-Consumer segment achieved record sales of proprietary DVDs to consumers in 2014.

During 2011, Acorn Media launched its first online paid subscription channel, Acorn TV, with the stated goal of being a distinctive point for consumers with interest in high-quality British TV programming. Viewership continues to grow with free subscriptions offered over a 30-day period. Acorn TV is currently available through the branded Acorn website and through applications currently with YouTube and Roku consumers. New applications were launched in 2014 and include iOS application for iPhones, iPads and Samsung devices. During 2015, we plan on investing in more exclusive content for our digital channels and establishing partnerships with device manufactures and other third-party digital platforms to assist with increasing viewership and subscribers during 2015.

In late 2014, we launched UMC, an urban digital proprietary network targeting a broad range of the African-American households in the U.S. The network is anticipated to skew towards a younger demographic versus our Acorn TV offering. The content will leverage our current urban content library from Image along with investments in new content in the form of co-productions and acquisitions.

In early 2014, we expanded our proprietary digital channels by launching Acacia TV in the U.S. and Europe. Acacia TV is a fitness and lifestyle channel with the primary goal of assisting viewers in living healthy, joyful lives. Subscribers to Acacia TV have access to the full catalog of Acacia fitness videos, customized fitness routines for adding variety, and video content produced exclusively for Acacia TV such as nutritional information and food preparation videos.

Outsourced Services

In 2013, we consolidated our Wholesale fulfillment partners to better manage capital and reduce costs. Under a Distribution Services and License Agreement with Sony Pictures Home Entertainment (or SPHE), SPHE acts as our exclusive manufacturer in North America to meet our hard good manufacturing requirements (DVD and Blue-ray) and to provide related fulfillment and other logistics services in exchange for certain fees. Our agreement with SPHE expires in August 2019. Under our relationship with SPHE, we are responsible for the credit risk from the end customer with respect to accounts receivable and also the risk of inventory loss with respect to the inventory they manage on our behalf.

In addition to conventional manufacturing, we also utilize SPHE’s capability to manufacture-on-demand (or MOD). MOD services are provided for replication of slower moving titles, which helps avoid replicating larger minimum quantities of certain titles, and can be used for direct-to-consumer sales as needed. Under our agreement, SPHE also provides certain operational services at our direction, including credit and collections, merchandising, returns processing and certain IT functions.

We believe the SPHE agreement provides us with several significant advantages, including:

| § | The ability to sell directly to key accounts such as Walmart, Best Buy and Costco, which eliminates other third-party distributor fees, provides incremental revenues, higher gross margins and the ability to better manage retail inventories; |

| § | Access SPHE’s point-of-sale reporting systems to better manage replenishment of store inventories on a daily basis; and |

| § | Access SPHE’s extensive scan-based trading network that features product placement in over 20,000 drug and grocery outlets. |

We also outsource certain post-production and creative services necessary to prepare a disc master for manufacturing and packaging/advertising materials for marketing of our products. Such services include:

| § | Packaging design; |

| § | DVD/Blu-ray authoring and compression; |

| § | Menu design; |

| § | Video master quality control; |

| § | Music clearance; and |

| § | For some titles, the addition of enhancements, such as: |

| Ø | multiple audio tracks; |

| Ø | commentaries; |

| Ø | foreign language tracks; |

| Ø | behind-the-scenes footage; and |

| Ø | interviews. |

In the U.K., we have a fulfillment and logistics services arrangement with Sony DADC UK Limited, which is similar to the arrangement we have with SPHE in North America.

In the U.S., Trade Global is our outsourced fulfillment partner that assists with managing our Direct-to-Consumer segment’s catalog business. They provide the following services: customer service, order management and fulfillment, cash collection, credit card processing, merchandise return processing and inventory management.

Marketing and Sales

Our in-house marketing department manages promotional efforts across a wide range of off-line and online platforms. Our marketing efforts include:

| § | Point-of-sale advertising; |

| § | Print advertising in trade and consumer publications; |

| § | Television, outdoor, in-theater and radio advertising campaigns; |

| § | Internet advertising, including viral and social network marketing campaigns; |

| § | Direct-response campaigns; |

| § | Dealer incentive programs; |

| § | Trade show exhibits; |

| § | Bulletins featuring new releases and catalog promotions; and |

| § | Public relations outreach programs. |

RLJE maintains its own sales force and has a direct selling relationship with the majority of its broadcast and cable/satellite partners, and retail customers. We sell our programs to broadcasters, cable and satellite providers, traditional and specialty retailers, internet retailers, rental outlets, wholesale distributors and through alternative exploitation efforts, which includes direct-to-consumer print catalogs, proprietary e-commerce websites, direct-response campaigns, subscription service/club sales, proprietary SVOD subscription channels, home shopping television channels, other non-traditional sales channels, kiosks and sub-distributors. Examples of our key broadcast/cable/satellite partners are DirecTV, Starz, BET and public television stations. Examples of our key customers are Amazon.com, Walmart, Best Buy Co., Target, Costco and HMV. Examples of our key distribution partners are Video Products Distributors, Ingram Entertainment, ITV Global Enterprises and All3Media. Examples of key rental customers are Netflix and Redbox.

We also focus on special-market sales channels, to take advantage of our large and diverse catalog and to specifically target niche sales opportunities. Examples of our key customers within special markets are Midwest Tapes and Waxworks. Another special-market channel is scanned-based trading in conjunction with SPHE.

Additionally, in connection with our Distribution Services and License Agreement with SPHE, SPHE agreed to perform certain sales and inventory management functions at Walmart, Best Buy and Target. By using SPHE, we benefit from having a major studio present RLJE’s product alongside its own releases, which include well known motion pictures. SPHE is our primary vendor of record for shipments of physical product to North American retailers and wholesalers, and as the vendor of record, they are responsible for collecting these receivables and remitting these proceeds to us. In the U.K., similar services are provided by Sony DADC UK Limited.

Customer Concentration

Amazon accounted for approximately 19.0% of our net revenues for the year ended December 31, 2014. We do not have any other customers which accounted for more than 10.0% of our net revenues for the year. Our top five customers accounted for approximately 46.2% of our net revenues for 2014, which includes Amazon. At December 31, 2014, SPHE and Netflix accounted for approximately 44.0% and 21.4%, respectively, of our gross accounts receivables.

Competition

We face competition from other independent distribution companies, major motion picture studios and broadcast and internet outlets in securing exclusive content distribution rights. We also face competition from online and direct-to-consumer retailers, as well as alternative forms of leisure entertainment, including video games, the internet and other computer-related activities. The success of any of our products depends upon consumer acceptance of a given program in relation to current events as well as the other products released into the marketplace at or around the same time. Consumers can choose from a large supply of competing entertainment content from other suppliers. Many of these competitors are larger than us. Our DVD and Blu-ray products compete for a finite amount of brick-and-mortar retail and rental shelf space. Sales of digital downloading, streaming, VOD and other broadcast formats are largely driven by what is visually available to the consumer, which can be supported by additional placement fees or previous sales success. Programming is available online, delivered to smart phones, tablets, laptops personal computers, or direct to the consumers’ TV set through multiple internet-ready devices and cable or satellite VOD. Digital and VOD formats are growing as an influx of new delivery devices, such as the Apple iPad and the Microsoft Xbox, gain acceptance in the marketplace. According to ABI Research, as of December 31, 2013, there were approximately 70 million name-brand tablets owned in the U.S., and the number is rapidly growing. We face increasing competition as these platforms continue to grow and programming providers enter into distribution agreements for a wider variety of formats.

Our ability to continue to successfully compete in our markets is largely dependent upon our ability to develop and secure unique and appealing content, and to anticipate and respond to various competitive factors affecting the industry, including new or changing product formats, changes in consumer preferences, regional and local economic conditions, discount pricing strategies and competitors’ promotional activities.

Industry Trends

According to The Digital Entertainment Group (or DEG), consumer home entertainment spending in calendar 2014 exceeded $17.8 billion, or a year-over-year decline of 1.8%. This slight decrease was driven by the continued decrease in physical format sales (led by the maturing of DVD’s), which decreased year-over-year by 10.9%. Offsetting this decrease was a 16.1% year-over-year increase in digital-format revenues to over $7.5 billion in 2014.

Digital-format revenues include electronic sell-through (or EST), VOD and subscription-based streaming. Subscription-based programing revenues increased by 25.8% in 2014 compared to 2013, while revenues from other digital formats increased by 6.7%.

DEG reported that in 2014 the number of homes with Blu-ray playback devices, including set-top boxes, game consoles and home-theater-in-a-box systems, was 70 million. DEG also reported that the number of households with HDTV is now more than 95 million.

According to PricewaterhouseCoopers LLP’s Global Entertainment and Media Outlook for 2014-2018, consumer spending for the overall physical home entertainment segment in the U.S. is projected to decline at a 6.5% compound annual rate over the 2014-2018 period to approximately $8.7 billion in 2018. While the decline in consumer spending on physical home entertainment continues, although at a lower rate than in past years, it is substantially offset by the increase in consumer spending on electronic home video. Consumer spending in the U.S. on electronic distribution, driven primarily by SVOD, will surge from $7.3 billion in 2013 to $17.0 billion in 2018, compounded annual rate of 18.3% over the 2014-2018 period as a result of growth in existing services (e.g., Netflix, Apple, Microsoft, etc.), augmented with new download service providers, growth in video-friendly hardware (e.g., tablets) and growing consumer acceptance of digital lockers. By 2018, the electronic home video segment is projected to be the main contributor to total filmed entertainment revenue at 43%, overtaking the box office in 2017.

Employees

As of February 13, 2015, we had 109 U.S.-based employees at our Maryland, California and Minnesota locations. We had 38 employees at our U.K. and Australia locations. Our employees are primarily employed on a full-time basis.

Available Information

Under the menu “Investors—SEC Filings” on our website at www.rljentertainment.com, we provide free access to our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. The information contained on our website is not incorporated herein by reference and should not be considered part of this Annual Report.

Risks Relating to Our Liquidity and Credit Agreement

We may not be able to generate sufficient cash to service all of our indebtedness, and we may be forced to take other actions, which may or may not be successful, to satisfy our obligations under our indebtedness. Our ability to make scheduled payments depends on our financial and operating performance, which is subject to prevailing economic and competitive conditions and to certain financial, business and other factors beyond our control. We cannot assure you that we will maintain a level of cash flows from operating activities sufficient to permit us to pay the principal, premium, if any, and interest on our indebtedness. If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell assets or operations, seek additional capital or restructure or refinance our indebtedness. We cannot assure you that we would be able to take any of these actions, that these actions would be successful and permit us to meet our scheduled debt service obligations or that these actions would be permitted under the terms of our existing or future debt agreements, including our Credit Agreement with certain lenders and McLarty, as Administrative Agent. In the absence of such cash flows or capital resources, we could face substantial liquidity problems and might be required to dispose of material assets or operations to meet our debt service and other obligations. Our senior secured Credit Agreement and the indenture governing our senior secured notes restrict our ability to dispose of assets and use the proceeds from such dispositions. We may not be able to consummate those dispositions or to obtain the proceeds which we could realize from them and these proceeds may not be adequate to meet any debt service obligations then due.

If we cannot make scheduled payments on our debt, we will be in default and, as a result:

| § | Our debt holders could declare all outstanding principal and interest to be due and payable; and |

| § | We could be forced into bankruptcy or liquidation. |

Our Credit Agreement contains covenants that may limit the way we conduct business. Our Credit Agreement contains various covenants limiting our ability to:

| § | incur or guarantee additional indebtedness; |

| § | pay dividends and make other distributions; |

| § | pre-pay any subordinated indebtedness; |

| § | make investments and other restricted payments; |

| § | make capital expenditures; |

| § | enter into merger or acquisition transactions; and |

| § | sell assets. |

These covenants may prevent us from raising additional debt or equity financing, competing effectively or taking advantage of new business opportunities.

Our Credit Agreement includes covenants that require us to maintain specified financial ratios. Our ability to satisfy those financial ratios can be affected by events beyond our control, and we cannot be certain we will satisfy those ratios. As of March 31, 2015, we were not in compliance with our minimum cash balance requirement, which was waived by our lenders on April 15, 2015.

Our Credit Agreement provides that the failure to comply with the financial ratios or other covenants or a material adverse change in our business, assets or prospects constitutes an “event of default.” If we are unable to comply with the financial ratios, comply with other covenants as specified in the Credit Agreement, our lenders may choose to assert an event of default under our Credit Agreement. In this event, unless we are able to negotiate an amendment, forbearance or waiver, we could be required to repay all amounts then outstanding, which would have a material adverse effect on our liquidity, business, results of operations, and financial condition.

We may not be able to generate the amount of cash needed to fund our future operations. Our ability either to fund planned capital expenditures and development efforts will depend on our ability to generate cash in the future. Our ability to generate cash is in part subject to general economic, financial, competitive, regulatory and other factors that are beyond our control. We cannot assure you, however, that our business will generate sufficient cash flow from operations to fund our liquidity needs.

Our liquidity depends on our cash-on-hand, operating cash flows and ability to collect cash receipts. At March 31, 2015, our cash and cash equivalents were approximately $3.1 million and, in accordance with the April 15, 2015 amendment to the Credit Agreement, we are required to maintain $1.0 million of cash at all times. We rely on our cash-on-hand, operating cash flows and ability to collect cash receipts to fund our operations and meet our financial obligations. Delays or any failure to collect our trade accounts receivable would have a negative effect on our liquidity.

We have pledged our intellectual property assets to secure our Credit Agreement, and this represents a risk to our business, results of operations and financial condition. In order to secure the financing necessary to operate our business, we pledged all of our intellectual property rights as collateral to our Credit Agreement. If we were to default on our obligations under the Credit Agreement, we could forfeit our intellectual property and, thereby, a primary source of revenue. This could have a material adverse effect on our business, results of operations and financial condition.

We are seeking additional capital funding and such capital may not be available to us. We are exploring various equity financing alternatives. If we are unable to obtain additional capital, we may be required to delay or reduce our operations. We cannot assure you that any necessary additional financing will be available on terms favorable to us, or at all. If we raise additional funds through the issuance of securities convertible into or exercisable for common stock, the percentage ownership of our stockholders could be significantly diluted, and these newly issued securities may have rights, preferences or privileges senior to those of existing stockholders. Market and industry factors may harm the market price of our common stock and may adversely impact our ability to raise additional funds. Similarly, if our common stock is delisted from the NASDAQ Capital Market, it may limit our ability to raise additional funds.

Risks Relating to Our Business

We have limited working capital and limited access to financing. Our cash requirements, at times, may exceed the level of cash generated by operations. Accordingly, we may have limited working capital.

Our ability to obtain adequate additional financing on satisfactory terms may be limited and our Credit Agreement prevents us from incurring additional indebtedness. Our ability to raise financing through sales of equity securities depends on general market conditions, including the demand for our common stock. We may be unable to raise adequate capital through the sale of equity securities, and if we were able to sell equity, our existing stockholders could experience substantial dilution. If adequate financing is not available at all or it is unavailable on acceptable terms, we may find we are unable to fund expansion, continue offering products and services, take advantage of acquisition opportunities, develop or enhance services or products, or respond to competitive pressures in the industry.

Our business requires a substantial investment of capital. The production, acquisition and distribution of programming require a significant amount of capital. Capital available for these purposes will be reduced to the extent that we are required to use funds otherwise budgeted for capital investment to fund our operations and/or make scheduled payments on our debt obligations. Curtailed content investment over a sustained period could have a material adverse effect on future operating results and cash flows. Further, a significant amount of time may elapse between our expenditure of funds and the receipt of revenues from our television programs or motion pictures. This time lapse requires us to fund a significant portion of our capital requirements from our operating cash flow and from other financing sources. Although we intend to continue to mitigate the risks of our production exposure through pre-sales to broadcasters and distributors, tax credit programs, government and industry programs, co-financiers and other sources, we cannot assure you that we will continue to successfully implement these arrangements or that we will not be subject to substantial financial risks relating to the production, acquisition, completion and release of new television programs and motion pictures. In addition, if we increase (through internal growth or acquisition) our production slate or our production budgets, we may be required to increase overhead and/or make larger up-front payments to talent and, consequently, bear greater financial risks. Any of the foregoing could have a material adverse effect on our business, financial condition, operating results, liquidity and prospects.

Our inability to gauge and predict the commercial success of our programming could adversely affect our business, results of operations and financial condition. Operating in the entertainment industry involves a substantial degree of risk. Each video program or feature film is an individual artistic work, and its commercial success is primarily determined by unpredictable audience reactions. The commercial success of a title also depends upon the quality and acceptance of other competing programs or titles released into the marketplace, critical reviews, the availability of alternative forms of entertainment and leisure activities, general economic conditions and other tangible and intangible external factors, all of which are subject to change and cannot be predicted. Timing is also sometimes relevant to a program’s success, especially when the program concerns a recent event or historically relevant material (e.g., an anniversary of a historical event which focuses media attention on the event and accordingly spurs interest in related content). Our success depends in part on the popularity of our content and our ability to gauge and predict it. Even if a film achieves success during its initial release, the popularity of a particular program and its ratings may diminish over time. Our inability to gauge and predict the commercial success of our programming could materially adversely affect our business, results of operations and financial condition.

We may be unable to recoup advances paid to secure exclusive distribution rights. Our most significant costs and cash expenditures relate to acquiring content for exclusive distribution. Most agreements to acquire content require upfront advances against royalties or net profits participations expected to be earned from future distribution. The amount we are willing to advance is derived from our estimate of net revenues that will be realized from our distribution of the title. Although these estimates are based on management’s knowledge of current events and actions management may undertake in the future, actual results will differ from those estimates. If sales do not meet our original estimates, we may (i) not recognize the expected gross margin or net profit, (ii) not recoup our advances or (iii) record accelerated amortization and/or fair value write-downs of advances paid. We recorded impairments of $4.8 million and $6.4 million during 2014 and 2013, respectively, related to our investments in content.

Our inability to maintain relationships with our program suppliers and vendors may adversely affect our business. We receive a significant amount of our revenue from the distribution of content for which we already have exclusive agreements with program suppliers. However, titles which have been financed by us may not be timely delivered as agreed or may not be of the expected quality. Delays or inadequacies in delivery of titles, including rights clearances, could negatively affect the performance of any given quarter or year. In addition, results of operations and financial condition may be materially adversely affected if:

| § | We are unable to renew our existing agreements as they expire; |

| § | Our current program suppliers do not continue to support digital, DVD or other applicable format in accordance with our exclusive agreements; |

| § | Our current content suppliers do not continue to license titles to us on terms acceptable to us; or |

| § | We are unable to establish new beneficial supplier relationships to ensure acquisition of exclusive or high-profile titles in a timely and efficient manner. |

Disputes over intellectual property rights could adversely affect our business, results of operations and financial condition. Our sales and net revenues depend heavily on the exploitation of intellectual property owned by us or third parties from whom we have licensed intellectual property. Should a dispute arise over, or a defect be found in, the chain of title in any of our key franchises, this could result in either a temporary suspension of distribution or an early termination of our distribution license. This could have a material adverse impact on our business, results of operations and financial condition.

We, and third parties that manage portions of our secure data, are subject to cybersecurity risks and incidents. Our direct-to-consumer business involves the storage and transmission of customers' personal information, shopping preferences and credit card information, in addition to employee information and our financial and strategic data. The protection of our customer, employee and company data is vitally important to us. While we have implemented measures to prevent security breaches and cyber incidents, any failure of these measures and any failure of third parties that assist us in managing our secure data could materially adversely affect our business, financial condition and results of operations.

A high rate of product returns may adversely affect our business, results of operations and financial condition. As with the major studios and other independent companies in this industry, we experience a relatively high level of product returns as a percentage of our revenues. Our allowances for sales returns may not be adequate to cover potential returns in the future, particularly in the case of consolidation within the home-video retail marketplace, which when it occurs tends to result in inventory consolidation and increased returns. We have experienced a high rate of product returns over the past three years. We expect a relatively high rate of product returns to continue, which may materially adversely affect our business, results of operations and financial condition.

We depend on third-party shipping and fulfillment companies for the delivery of our products. If these companies experience operational difficulties or disruptions, our business could be adversely affected. We rely on SPHE, our distribution facilitation and manufacturing partner in North America, Sony DADC UK Limited in the U.K, and Trade Global, our fulfillment partner in the U.S. for a majority of our Direct-to-Consumer sales, to determine the best delivery method for our products. These partners rely entirely on arrangements with third-party shipping companies, principally Federal Express and UPS, for small package deliveries and less-than-truckload service carriers for larger deliveries, for the delivery of our products. The termination of arrangements between our partners and one or more of these third-party shipping companies, or the failure or inability of one or more of these third-party shipping companies to deliver products on a timely or cost-efficient basis from our partners to our customers, could disrupt our business, reduce net sales and harm our reputation. Furthermore, an increase in the amount charged by these shipping companies could negatively affect our gross margins and earnings.

Economic weakness may continue to adversely affect our business, results of operations and financial condition. The global economic downturn had a significant negative effect on our revenues and may continue to do so. As consumers reduced spending and scaled back purchases of our products, we experienced higher product returns and lower sales, which adversely affected our revenues and results of operations in previous years. Although consumer spending has improved over the last few years, weak consumer demand for our products may occur and may adversely affect our business, results of operations and financial condition.

Our high concentration of sales to and receivables from relatively few customers (and use of a third-party to manage collection of substantially all packaged goods receivables) may result in significant uncollectible accounts receivable exposure, which may adversely affect our liquidity, business, results of operations and financial condition. During 2014, our net revenues from Amazon were 19.0% of our net revenues. Our top five customers accounted for approximately 46.2% of our net revenues for 2014. SPHE and Netflix accounted for approximately 44.0% and 21.4%, respectively, of our gross accounts receivable as of December 31, 2014.

We may be unable to maintain favorable relationships with our retailers and distribution facilitators including SPHE and Sony DADC UK Limited. Further, our retailers and distribution facilitators may be adversely affected by economic conditions. If we lose any of our top customers or distribution facilitators, or if any of these customers reduces or cancels a significant order, it could have a material adverse effect on our liquidity, business, results of operations and financial condition.

We face credit exposure from our retail customers and may experience uncollectible receivables from these customers should they face financial difficulties. If these customers fail to pay their accounts receivable, file for bankruptcy or significantly reduce their purchases of our programming, it would have a material adverse effect on our business, financial condition, results of operations and liquidity.

A high concentration of our gross accounts receivables is attributable to SPHE and Sony DADC UK Limited, as they are our vendor of record for shipments of physical product to North American and U.K. retailers and wholesalers. As part of our arrangement with our distribution facilitation partners, SPHE and Sony DADC UK Limited collect the receivables from our end customers, provide us with monthly advance payments on such receivables (less a reserve), and then true up the accounts receivables accounting quarterly. While we remain responsible for the credit risk from the end customer, if SPHE or Sony DADC UK Limited should fail to adequately collect and pay us the accounts receivable they collect on our behalf, whether due to inadequate processes and procedures, inability to pay, bankruptcy or otherwise, our financial condition, results of operations and liquidity would be materially adversely affected.

We do not control the timing of dividends paid by ACL, which could negatively impact our cash flow. Although we hold a 64% interest in ACL, we do not control the board of directors of ACL. The members of the Agatha Christie family, who hold the remaining 36% interest in ACL, have the right to appoint the same number of directors as us and, in the event of deadlock on any decision of the board, also have a second or casting vote exercised by their appointee as chairman of ACL, which allows them to exercise control of ACL’s board of directors.

Under English law, the amount, timing and form of payment of any dividends or other distributions is a matter for ACL’s board of directors to determine, and, as a result, we cannot control when these distributions are made. If ACL’s board of directors decides not to authorize distributions, our revenue and cash flow may decrease, materially adversely affecting our business, results of operations, liquidity and financial condition.