Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CECO ENVIRONMENTAL CORP | d924797d8k.htm |

| EX-99.1 - EX-99.1 - CECO ENVIRONMENTAL CORP | d924797dex991.htm |

Q1

2015 Financial Results Conference Call May 7, 2015

A global industrial technology company focused on

environmental, energy, fluid handling industries

Exhibit 99.2 |

Non-GAAP Financial Information

CECO is providing the non-GAAP historical financial measures in this

presentation, as the Company believes that these figures are helpful in allowing

individuals to better assess the ongoing nature of CECO’s core operations. A

"non-GAAP financial measure" is a numerical measure of a company's

historical financial performance that excludes amounts that are included in the

most directly comparable measure calculated and presented in the GAAP

statement of operations. Non-GAAP gross margin, non-GAAP operating

income, non-GAAP net income, non-GAAP adjusted EBITDA, non-GAAP gross profit margin, non-

GAAP

operating

margin,

non-GAAP

earnings

per

basic

and

diluted

share,

as

we

present

them

in

the

financial

data

included

in

this

presentation,

have

been adjusted to exclude the effects of expenses related to property, plant, and

equipment valuation adjustments, acquisition and integration expense

activities including retention, legal, accounting, banking, amortization and

earnout expenses, the impact of foreign currency remeasurement and the

associated tax benefit of these charges. Management believes that these items are

not necessarily indicative of the Company’s ongoing operations and

their exclusion provides individuals with additional information to compare the Company's results over multiple periods. Additionally, management

utilizes

this

information

to

evaluate

its

ongoing

financial

performance.

Our

financial

statements

may

continue

to

be

affected

by

items

similar

to

those

excluded in the non-GAAP adjustments described above, and exclusion of these

items from our non-GAAP financial measures should not be construed as an

inference that all such costs are unusual or infrequent. Non-GAAP gross

margin, non-GAAP operating income, non-GAAP net income, non-GAAP adjusted EBITDA, non-GAAP gross profit margin, non-

GAAP

operating

margin,

and

non-GAAP

earnings

per

basic

and

diluted

shares

are

not

calculated

in

accordance

with

GAAP,

and

should

be

considered

supplemental to, and not as a substitute for, or superior to, financial measures

calculated in accordance with GAAP. Non-GAAP financial measures have

limitations in that they do not reflect all of the costs associated with the operations of our business as determined in accordance with GAAP. As a

result, you should not consider these measures in isolation or as a substitute for

analysis of CECO’s results as reported under GAAP. In accordance with

the requirements of Regulation G issued by the Securities and Exchange Commission, non-GAAP gross margin, non-GAAP

operating income, non-GAAP net income, non-GAAP adjusted EBITDA,

non-GAAP gross profit margin, non-GAAP operating margin, and non-GAAP

earnings per basic and diluted share stated in the tables above are reconciled to

the most directly comparable GAAP financial measures. Free cash flow

has

limitations

due

to

the

fact

that

it

does

not

represent

the

residual

cash

flow

available

for

discretionary

expenditures,

since

it

does

not

take

into

account debt service requirements or other non-discretionary expenditures that

are not deducted from the measure. Adjusted EBITDA and Free Cash Flow

are not calculated in accordance with GAAP, and should be considered supplemental to, and not as a substitute for, or superior to, financial

measures calculated in accordance with GAAP Additionally, CECO cautions

investors that the non-GAAP financial measures used by the Company may

not be comparable to similarly titled measures of other companies. Safe Harbor

Statement 2 |

Forward-looking Statements

Any statements contained in this presentation other than statements of historical

fact, including statements about management’s beliefs and expectations,

are forward-looking statements and should be evaluated as such. These statements are made on the basis of

management’s

views

and

assumptions

regarding

future

events

and

business

performance.

Words

such

as

“estimate,”

“believe,”

“anticipate,”

“expect,”

“intend,”

“plan,”

“target,”

“project,”

“should,”

“may,”

“will”

and similar expressions are intended to identify forward-

looking statements. Forward-looking statements (including oral representations)

involve risks and uncertainties that may cause actual results to differ

materially from any future results, performance or achievements expressed or implied by such statements. These

risks

and uncertainties include, but are not limited to: our ability to successfully

complete the acquisition of PMFG; our ability to successfully integrate

acquired businesses and realize the synergies from acquisitions, including PMFG, as well as a number of factors related to our

business including economic and financial market conditions generally and economic

conditions in CECO’s service areas; dependence on

fixed

price

contracts

and

the

risks

associated

therewith,

including

actual

costs

exceeding

estimates

and

method

of

accounting

for

contract revenue; fluctuations in operating results from period to period due to

seasonality of the business; the effect of growth on CECO’s

infrastructure, resources, and existing sales; the ability to expand operations in both new and existing markets; the potential for

contract delay or cancellation; changes in or developments with respect to any

litigation or investigation; the potential for fluctuations in prices for

manufactured components and raw materials; the substantial amount of debt incurred in connection with our recent

acquisitions and our ability to repay or refinance it or incur additional debt in

the future; the impact of federal, state or local government regulations;

economic and political conditions generally; and the effect of competition in the product recovery, air pollution control and

fluid handling and filtration industries. These and other risks and uncertainties

are discussed in more detail in CECO’s filings with the Securities and

Exchange Commission, including our reports on Form 10-K and Form 10-Q. Many of these risks are beyond

management’s ability to control or predict. Should one or more of these risks

or uncertainties materialize, or should the assumptions prove incorrect,

actual results may vary in material aspects from those currently anticipated. Investors are cautioned not to place undue

reliance on such forward-looking statements as they speak only to our views as

of the date the statement is made. All forward-looking statements

attributable to CECO or persons acting on behalf of CECO are expressly qualified in their entirety by the cautionary

statements and risk factors contained in this presentation and CECO’s

respective filings with the Securities and Exchange Commission. Furthermore,

forward-looking statements speak only as of the date they are made. Except as required under the federal securities laws

or the rules and regulations of the Securities and Exchange Commission, CECO

undertakes no obligation to update or review any forward-looking

statements, whether as a result of new information, future events or otherwise.

Safe Harbor Statement

3 |

Important Information for Investors and Stockholders

This communication does not constitute an offer to sell or the solicitation of an

offer to buy securities or a solicitation of any vote or approval.

This

communication

is

not

a

substitute

for

the

prospectus/proxy

statement

that

CECO

and

PMFG

will

file

with

the

SEC.

Investors

in

CECO

or

PMFG

are

urged

to

read

the

prospectus/proxy

statement,

which

will

contain

important

information,

including

detailed risk factors, when it becomes available. The prospectus/proxy statement

and other documents that will be filed by CECO and PMFG with the SEC will be

available free of charge at the SEC’s website, www.sec.gov, or by directing a request when such a filing is

made to (1) CECO Environmental Corp., by mail at 4625 Red Bank Road Suite 200,

Cincinnati, Ohio 45227, Attention: Investor Relations, by telephone at

800-333-5475 or by going to CECO’s Investor page on its corporate website at www.cecoenviro.com; or (2)

PMFG, Inc. by mail at 14651 North Dallas Parkway Suite 500, Dallas, Texas 75254,

Attention: Investor Relations, by telephone at 877-

879-7634, or by going to PMFG, Inc.’s Investors page on its corporate

website at www.pmfginc.com. A final prospectus/proxy statement will be

mailed to CECO’s stockholders and shareholders of PMFG. Safe Harbor

Statement 4

Proxy Solicitation

CECO and PMFG, and certain of their respective directors, executive officers and

other members of management and employees may be deemed participants in the

solicitation of proxies in connection with the proposed transactions. Information about the directors and

executive officers of CECO is set forth in the proxy statement for CECO’s 2015

annual meeting of stockholders and CECO’s 10-K for the year

ended

December

31,

2014.

Information

about

the

directors

and

executive

officers

of

PMFG

is

set

forth

in

the

proxy

statement

for

PMFG’s 2014 annual meeting of shareholders and PMFG’s Form 10-K for

the year ended June 28, 2014. Investors may obtain additional information

regarding the interests of such participants in the proposed transactions by reading the prospectus/proxy

statement for such proposed transactions when it becomes available.

|

Jeff

Lang President and Chief Executive Officer

5 |

6

•

Revenue

–

Revenue of $81 million, up 41.6% year-over-year

–

Revenue on an organic basis is up 8.6% vs. 1Q14 using constant FX

•

Bookings / Backlog

–

1Q15 bookings of $93.9 million up 48% year-over-year

–

Organic bookings up 9.3% in Q1, $69.5 million vs. $63.6 million in prior

year

–

Record

backlog

of

$153.0

million

vs.

$140.1

million

at

year

end,

up

9.2%

•

EPS

–

GAAP EPS for 1Q15 of $0.01 compared to $0.12 in 1Q14

–

Non-GAAP EPS for 1Q15 of $0.21 vs. $0.19 in 1Q14

1Q15 Quarterly Financial Highlights |

1Q15

Quarterly Financial Highlights 7

•

Non-GAAP Gross Margin

–

Gross margin of 26% compared to 35% in prior year, primarily

attributable to:

•

Expected shift in mix and 2014 acquisitions which have reshaped our gross

profit •

The large strategic energy job

•

Underperformance of Emtrol and Effox in Q1

•

Non-GAAP Operating Margin

–

The gross margin decrease adversely impacted operating margins,

–

However, SG&A declined as a percentage of sales to 17% from a little

over 20% last year, offsetting a portion of the gross profit decline

–

As such, operating margins decreased 520 bps to 9.3% over last year’s

14.5%

•

Adjusted EBITDA

–

Adjusted

EBITDA

of

$8.6

million,

down

from

$9.4

million

in

prior

year |

Business Conditions & Strategic Review

8

•

Overall end markets are unchanged; we are executing better on our Sales

Excellence

and

initiatives.

•

Environmental segment continues to gain momentum

•

Energy segment –

global natural gas power generation business is up.

Solid fuel is picking up globally but soft domestically; we are bolstering with

after-market strategies

•

Fluid Handling and Filtration is on track for a solid 2015

•

Integration of Zhongli and Emtrol are ahead of plan

•

Aftermarket sales continues to gain momentum

•

Acquisition of PMFG a significant strategic event |

9

Strong strategic fit

1.

Key step towards becoming market leader, including natural gas value chain

3.

Enhances global footprint, particularly in China and the Middle East

5.

4.

Provides access to attractive end markets to drive long-term growth

6.

Brings a leading portfolio of highly engineered product offerings

8.

Poised to benefit from a balanced portfolio and diverse end markets

7.

Grows aftermarket & recurring revenue opportunity

2.

Poised to achieve significant sales and cost synergies

Announcement of Proposed Acquisition of PMFG, Inc. -

Key Transaction Benefits & Strategic Rationale |

10

(1)

Pro forma for the full year impact of the Emtrol, Zhongli, HEE, and SAT

acquisitions. (2)

Includes $15M of synergies that are expected to be fully-realized in 2017.

(3)

See

Appendix

for

reconciliation

for

Adjusted

EBITDA

and

Adjusted

EBITDA

with

synergies

to

net

income

Illustrative 2014 Revenues & EBITDA Bridge

($ in millions)

Gross Margin (%)

Gross Profit

Revenues

Adj. EBITDA (w/ Syn.)

(3)

SG&A

SG&A (%)

Adj. EBITDA

(3)

30.0%

28.9%

29.6%

$98.4

$45.7

$144.1

$327.9

$158.1

$486.0

$60.0

(2)

$109.5

$58.0

$51.5

17.7%

32.6%

22.5%

$47.1

($2.1)

$45.0

Pro Forma

(12/31/2014)

(12/31/2014)

Standalone

(1) |

Ed

Prajzner Chief Financial Officer

11 |

12

•

Record revenue of $81.0 million, up 42% y/y and 6% sequentially

•

2014 acquisitions added approximately $20.5 y/y

•

On a constant currency basis, organic revenue grew 8.6%

($ in millions)

1Q15 Quarterly Financial Highlights

Revenue

$34.4

$44.4

$49.8

$68.7

$57.2

$66.6

$63.3

$76.1

$81.0

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15 |

Backlog

($ in millions)

13

1Q15 Quarterly Financial Highlights

Bookings

•

Solid 1Q15 backlog of $153.0 million, up 9.2% from year end

•

Strong 1Q15 bookings of $93.9 million, up 9.3% organically

$75.8

$77.9

$100.4

$98.5

$104.9

$96.0

$106.2

$140.1

$153.0

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

$37.6

$46.5

$48.0

$66.8

$63.6

$57.7

$69.9

$63.7

$93.9

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15 |

14

1Q15 Financial Highlights

Non-GAAP Gross Margin

•

Non-GAAP gross margin of 26.2% due to expected mix changes and

acquisitions

•

Operating margin of 9.3%, down 520 bps y/y and down 160 bps q/q

•

Good SG&A control

Non-GAAP Operating Margin

32.6%

32.2%

30.1%

32.4%

34.8%

32.3%

33.6%

29.8%

26.2%

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

13.4%

13.9%

11.4%

13.6%

14.5%

14.9%

12.9%

10.9%

9.3%

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15 |

15

Adjusted EBITDA

•

Adjusted EBITDA of $8.6 million vs. $9.4 million in the prior year

•

Non-GAAP EPS of $0.21, up from $0.19 in 1Q14

•

We have consistently excluded FX re-measurement in 2014 and 2013

Non-GAAP EPS

($ in millions)

1Q15 Quarterly Financial Highlights

$5.0

$6.7

$6.4

$9.7

$9.4

$11.0

$9.4

$8.9

$8.6

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

$0.18

$0.30

$0.24

$0.23

$0.19

$0.25

$0.25

$0.22

$0.21

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

See supplemental slide for adjusted EBITDA reconciliation and important disclosures regarding

CECO’s use of adjusted EBITDA.

Note: |

16

Environmental Segment

Revenue

•

Revenue of $41.7 million was up 56% y/y

•

Bookings of $51.2 million in 1Q15, up 66% y/y with >15%

due to organic

•

The OneCECO systems approach is gaining traction with creating

customer value

•

Aftermarket continues to gain momentum to bolster our P&L

•

Overall a solid quarter in our Environmental segment

Bookings

($ in millions)

First Quarter Results

$26.7

$32.9

$27.7

$40.3

$41.7

1Q14

2Q14

3Q14

4Q14

1Q15

$30.9

$26.4

$24.6

$33.3

$51.2

1Q14

2Q14

3Q14

4Q14

1Q15 |

17

Revenue

•

Revenue of $24.3 million was up 59% y/y

•

Bookings of $26.5 million in 1Q15, up 81.5% sequentially

•

Aftermarket and retrofit opportunities continue to grow

Bookings

Energy Segment

($ in millions)

First Quarter Results

$15.3

$16.8

$18.0

$20.2

$24.3

1Q14

2Q14

3Q14

4Q14

1Q15

$17.8

$14.8

$28.4

$14.6

$26.5

1Q14

2Q14

3Q14

4Q14

1Q15 |

18

Revenue

Revenue of $15.2 million, down 4.4% sequentially

Bookings of $16.2 million, up 2.5% sequentially

Margin expansion and operational excellence continuing on plan

Added strategic Sales leadership resources during Q1

Bookings

Fluid Handling & Filtration Segment

($ in millions)

First Quarter Results

$15.5

$16.7

$17.6

$15.9

$15.2

1Q14

2Q14

3Q14

4Q14

1Q15

$15.1

$16.6

$16.7

$15.8

$16.2

1Q14

2Q14

3Q14

4Q14

1Q15 |

19

12/31/2011

12/31/2012

12/31/2013

12/31/2014

3/31/2015

Cash & Equivalents

$ 12.7

$

23.0

$ 22.7

$ 19.4

$ 19.0

Total Assets

$ 79.3

$ 94.1

$348.5

$414.4

$417.4

Total Bank Debt

$ 0.0

$

0.0

$ 89.1

$112.4

$112.9

Convertible Debt

$ 9.6

$

0.0

$ 0.0

$ 0.0

$ 0.0

Shareholders’

Equity

$ 43.0

$

62.0

$170.4

$181.2

$179.3

Current Asset

Current Liabilities

Net Working Capital

$ 53.5

$(23.6)

$ 29.9

$ 64.3

$(27.5)

$ 36.8

$124.8

$(59.3)

$ 65.5

$143.0

$(75.4)

$ 67.6

Balance Sheet

.

Selected Balance Sheet

Information

Note: Balance Sheet figures presented as reported in Company filings

$151.0

$(83.9)

$ 67.1

Net Debt to Pro Forma EBITDA = 2.03 Leverage Ratio

Balance Sheet Detail

($ Millions) |

Supplemental

20 |

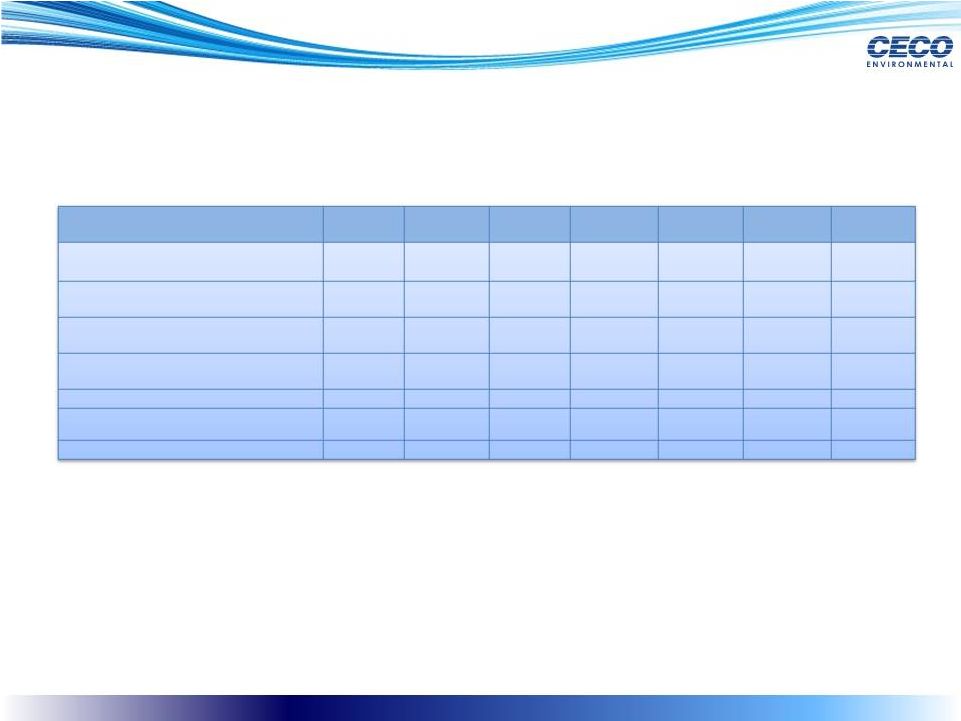

21

Non-GAAP Gross Margin

($ in millions)

Annual

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Annual

2014

Q1

2015

$ 61.6

$ 19.7

$ 21.4

$ 21.1

$ 22.6

$ 84.8

$ 21.0

31.2%

34.4%

32.1%

33.3%

29.7%

32.2%

25.9%

1.1

-

-

-

-

$

- -

0.2

0.2

0.1

0.2

0.1

$

0.6

0.2

$ 62.9

$ 19.9

$ 21.5

$ 21.3

$ 22.7

$ 85.4

$ 21.2

31.9%

34.8%

32.3%

33.6%

29.8%

32.4%

26.2%

with GAAP

with GAAP

Gross profit as reported in accordance

Gross profit margin in accordance

Inventory valuation adjustment

Plant, property and equipment

Non-GAAP gross margin

Non-

GAAP Gross profit margin

valuation adjustment |

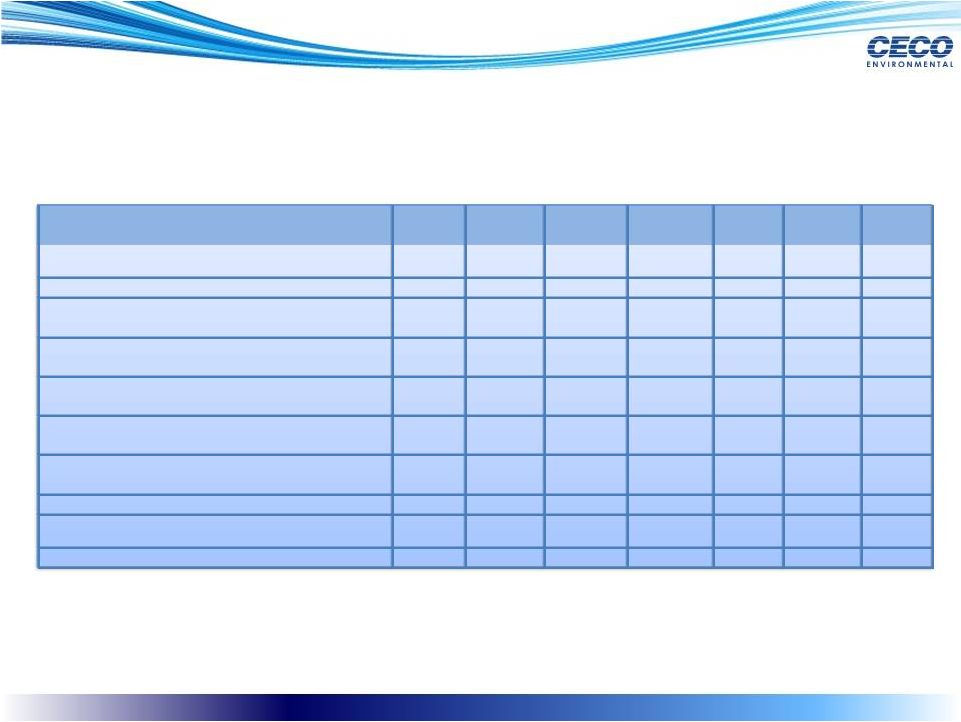

22

Non-GAAP Operating Margin

($ in millions)

Operating income as reported in accordance with GAAP

$ 7.0

$ 5.5

$ 7.2

$ 5.2

$ 3.8

$ 21.7

$ 3.0

Operating margin in accordance with GAAP

3.5%

9.6%

10.8%

8.2%

5.0%

8.2%

3.7%

Inventory valuation adjustment

1.1

-

-

-

-

-

-

Plant, property and equipment valuation

adjustment

0.2

0.2

0.1

0.2

0.1

0.6

0.2

Acquisition and integration expenses

7.2

0.1

0.2

0.1

0.9

1.3

0.3

Amortization and earn-out expenses

6.8

2.5

2.4

2.4

2.8

10.1

4.0

Legal reserves

3.5

-

-

0.3

-

0.3

-

Non-GAAP operating income

$

25.8

$ 8.3

$ 9.9

$

8.2

$ 7.6

$ 34.0

$ 7.5

Non-GAAP Operating margin

13.1%

14.5%

14.9%

12.9%

10.0%

12.9%

9.3%

Annual

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Annual

2014

Q1

2015 |

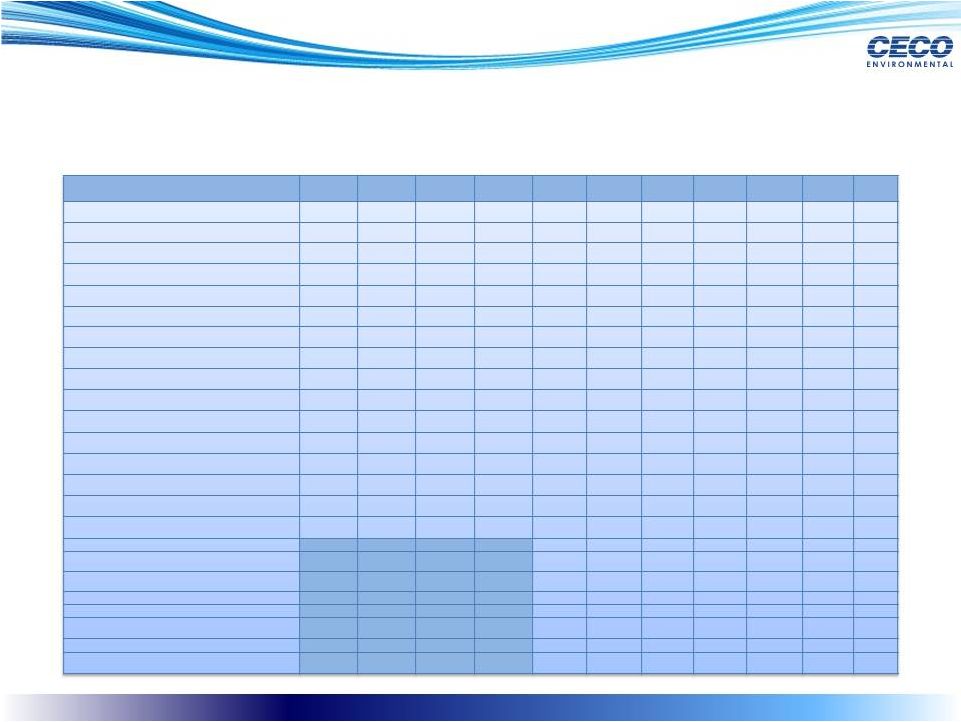

23

Non-GAAP NI & EBITDA

($ in millions)

Annual

2009

Annual

2010

Annual

2011

Annual

2012

Annual

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

Annual

2014

Q1

2015

Net income as reported in accordance with GAAP

$ (15.0)

$

2.1

$

8.3

$ 10.9

$

6.6

$

3.0

$ 4.5

$

3.7 $

1.9 $ 13.1

$ 0.2

Inventory valuation adjustment

-

-

-

-

1.1

-

-

-

-

-

-

Plant, property and equipment valuation adjustment

-

-

-

-

0.2

0.2

0.1

0.2

0.1

0.6

0.2

Acquisition and integration expenses

-

-

-

-

7.2

0.1

0.2

0.1

0.9

1.3

0.3

Amortization and earn-out expenses

-

-

-

-

6.8

2.5

2.4

2.4

2.8

10.1

4.0

Legal reserves

-

-

-

-

3.5

-

-

0.3

-

0.3

-

Foreign currency remeasurement

-

-

-

-

(1.1)

-

-

1.7

1.2

2.9

2.7

Tax benefit of expenses

-

-

-

-

(4.6)

(0.8)

(0.7)

(1.2)

(1.0)

(3.7)

(1.7)

Non-GAAP net income

$ (15.0)

$

2.1

$

8.3

$ 10.9

$ 19.7

$

5.0

$ 6.5

$

7.2

$

5.9

$

24.6

$

5.7

Depreciation

2.5

1.8

1.4

1.2

1.6

0.8

0.7

0.8

0.8

3.1

0.7

Non-cash stock compensation

1.0

0.9

0.7

0.7

1.1

0.3

0.4

0.5

0.5

1.7

0.4

Goodwill impairment

17.1

-

-

-

-

-

-

-

-

-

-

Other (income)/expense

0.8

0.1

(0.5)

0.1

0.1

0.1

0.1

(0.2)

(0.6)

(0.6)

(1.0)

Interest expense

1.3

1.2

1.1

1.2

1.5

0.7

0.8

0.7

0.9

3.1

1.0

Income tax expense

(3.1)

1.4

3.4

4.5

4.5

2.5

2.5

0.4

1.4

6.8

1.8

Non-GAAP EBITDA

$

4.6

$

7.5

$ 14.4

$

18.6 $

28.5

$

9.4 $ 11.0

$ 9.4

$

8.9

$ 38.7

$

8.6

Basic Shares Outstanding

20,116,991

25,606,352

25,643,508

25,691,884

26,057,831

25,750,972

26,271,316

Diluted Shares Outstanding

20,719,951

26,115,512

26,107,648

26,129,427

26,467,984

26,196,901

26,598,799

Earnings (loss) per share:

Basic

$ 0.33

$ 0.12

$ 0.18

$ 0.14

$

0.07

$ 0.51

$ 0.01

Diluted

$ 0.32

$ 0.12

$ 0.17

$ 0.14

$ 0.50

$ 0.01

$

0.07 |

24

($ in Millions)

CECO

Reported

Pro-forma

(Recent

Acquisitions)

CECO

Standalone

PMFG

Pro-forma

CECO

Combined

GAAP Revenues

$263.2

$64.7

$327.9

$158.1

$ 486.0

GAAP Gross profit

$84.8

$13.6

$98.4

$45.7

$144.1

SG&A as reported in accordance with GAAP

$51.4

$6.6

$58.0

$51.5

$109.5

GAAP Net income

$13.1

$8.1

$21.2

($33.1)

($11.9)

Amortization and earn-out expenses

$10.1

-

$10.1

$0.9

$11.0

Other

(1)

$5.1

$0.3

$5.4

$26.5

$31.9

Tax benefit of expenses

($3.7)

-

($3.7)

($2.2)

($5.9)

Non-GAAP net income

$24.6

$8.4

$33.0

($7.8)

$25.2

Depreciation

$3.1

-

$3.1

$1.8

$4.9

Non-cash stock compensation

$1.7

-

$1.7

$1.1

$2.8

Other (income)/expense

($0.6)

-

($0.6)

($0.1)

($0.7)

Interest expense

$3.1

-

$3.1

$1.8

$4.9

Income tax expense

$6.8

-

$6.8

1.1

$7.9

Non GAAP Adjusted EBITDA

$38.7

$8.4

$47.1

($2.1)

$45.0

Non-GAAP Adjusted EBITDA (with Synergies)

$60.0

GAAP to Non-GAAP Adjusted EBITDA Reconciliation

(Twelve Months ended 12/31/2014)

(1) Includes

plant,

property

and

equipment

(PPE)

valuation

adjustments,

acquisition

and

integration

expenses,

legal

reserves

and

foreign

currency

remeasurement |