Attached files

| file | filename |

|---|---|

| EX-32.2 - STL Marketing Group, Inc. | ex32-2.htm |

| EX-32.1 - STL Marketing Group, Inc. | ex32-1.htm |

| EX-31.2 - STL Marketing Group, Inc. | ex31-2.htm |

| EX-31.1 - STL Marketing Group, Inc. | ex31-1.htm |

| EXCEL - IDEA: XBRL DOCUMENT - STL Marketing Group, Inc. | Financial_Report.xls |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2014

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| STL MARKETING GROUP, INC. |

| (Exact name of registrant as specified in its charter) |

| Colorado | 000-55013 | 20-4387296 | ||

| (State or other jurisdiction of | (Commission | (I.R.S. Employer | ||

| incorporation or organization) | File Number) | Identification Number) |

10 Boulder Crescent, Suite 102

Colorado Springs, CO 80903

(Address of Principal Executive Offices)

(Former name or former address, if changed since last report)

(719) 219-5797

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.001 par value

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers in response to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | [ ] | Accelerated filer | [ ] |

| Non-accelerated filer | [ ] | Smaller reporting company | [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant on June 30, 2014, based on a closing price of .0255 was approximately $254,894 (reflecting the 1:15 reverse split effective March 5, 2015). As of April 15, 2015, the registrant had 145,697,286 shares of its common stock, 0.001 par value per share, outstanding.

Documents Incorporated By Reference: None.

STL MARKETING GROUP, INC.

INDEX TO REPORT ON FORM 10-K

| 2 |

FORWARD LOOKING STATEMENTS

Included in this Form 10-K are “forward-looking” statements, as well as historical information. Although we believe that the expectations reflected in these forward-looking statements are reasonable, we cannot assure you that the expectations reflected in these forward-looking statements will prove to be correct. Our actual results could differ materially from those anticipated in forward-looking statements as a result of certain factors, including matters described in the section titled “Risk Factors.” Forward-looking statements include those that use forward-looking terminology, such as the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “project,” “plan,” “will,” “shall,” “should,” and similar expressions, including when used in the negative. Although we believe that the expectations reflected in these forward-looking statements are reasonable and achievable, these statements involve risks and uncertainties and we cannot assure you that actual results will be consistent with these forward-looking statements. We undertake no obligation to update or revise these forward-looking statements, whether to reflect events or circumstances after the date initially filed or published, to reflect the occurrence of unanticipated events or otherwise.

General Information

Our business address is 10 Boulder Crescent, Suite 102, Colorado Springs, CO 80903. Our telephone number is (719) 219-5797 and our Internet website address is www.stlmarketinggroup.com. The information contained in, or that can be accessed through, our website is not part of this registration statement.

History

STL Marketing Group, Inc. (the “Company,” “our Company,” “we,” “us,” “our,” or “STL,” was incorporated under the laws of the State of Colorado on February 16, 1999 under the original name of Fountain Colony Ventures, Inc. Fountain Colony Ventures, Inc. changed its name to SGT Ventures, Inc. in March 2006. In June 2006, SGT Ventures, Inc. changed its name to Stronghold Industries, Inc. On October 30, 2007, Stronghold Industries, Inc. entered into a share purchase and exchange agreement with Image Worldwide, Inc. The Company name was officially changed with the Secretary of State to Image Worldwide, Inc. (“Image Worldwide”) on November 21, 2007. In 2008, Image Worldwide concentrated its business activities on helping clients create, market and promote their brands and image in print, online and at live events. Image Worldwide entered into a share exchange agreement with St. Louis Packaging Inc. on January 31, 2009. In April 2009, the Company changed its name to STL Marketing Group, Inc. On December 1, 2009, the Company sold majority of the STL Brands to Alliance Creative Group, Inc. In March of 2011, the Company entered into a distribution agreement with United Fuel Savers and entered into an option agreement to purchase land in Texas for a potential business opportunity. Prior to October 15, 2012, this distribution agreement and option agreement was canceled. On October 15, 2012, the Company agreed to merge with Versant Corporation, a Colorado based renewable energy company. On February 4, 2013 the Company entered into a share exchange agreement with Versant whereby Versant became the Company’s wholly owned operating subsidiary. The transaction is being accounted for as a reverse merger. Accordingly, the historical financial information going forward will be that of Versant Corporation and subsidiaries.

On May 29, 2014, the Board of Directors (the “Board”) of STL Marketing Group, Inc. (the “Company”) approved the formation of PhoneSuite Solutions, Inc. (“PSS”), as a Delaware corporation and a wholly owned subsidiary of the Company. On June 16, 2014, the Board approved the issuance of one-hundred (100) shares of common stock of PSS to the Company (the “Subsidiary Shares”). The Subsidiary Shares represent 100% of the authorized shares of common stock of PSS.

On June 24, 2014, PSS, as the Company’s wholly owned subsidiary, entered into a Strategic Alliance and Distribution Agreement (the “Agreement”) with Call Management Products, Inc. (“CMP”), a Colorado corporation in the business of designing, manufacturing, marketing, and selling telecommunications products. The Agreement provides that PSS will establish a dealer network and market and sell CMP’s products both internationally and in the United States (the “Territory”). In the domestic market PSS will market to the general business market, excluding the hospitality and assisted living verticals. Internationally, PSS may sell to all markets and develop both the hospitality and general business marketplaces.

Additionally, the Agreement provides that PSS will develop the Territories at its cost and promote CMP’s brands, name and products consistently across the globe. PSS is an exclusive Strategic Ally for CMP’s products in the Territory. The Agreement provides that, each year, PSS and CMP will mutually establish a sales quota for PSS to meet, with the first quota set for fiscal 2015.

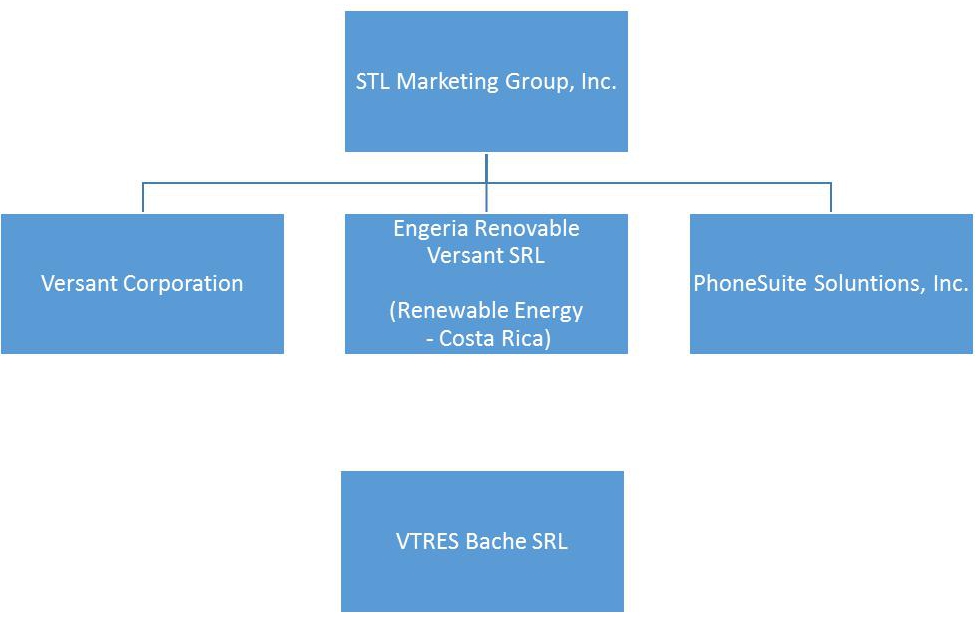

As a result, our business operations are currently (i) the sale and distribution of telecommunications under the brand name PhoneSuite; and (ii) the prospective sale of electricity through a planned wind park to a government owned utility company in Costa Rica. The Company continues to evaluate additional opportunities to bolster its revenue stream. Our corporate organization is as follows:

STL Marketing Group, Inc. has been trading on the OTC Market Pink Sheets under the symbol ’STLK’ since April 2009.

| 3 |

OVERVIEW OF OUR RENEWABLE ENERGY BUSINESS

STL Marketing Group, Inc. (OTC: STLK), (the “Company”) is a Colorado corporation seeking to provide wind energy to the Costa Rican government from a wind power generation plant the Company intends to build and operate pursuant to a PPA (as defined below), which the Company expects to initiate in 2016. The Company has two wholly owned subsidiaries in Costa Rica that handle the development of the business and are expected to operate the power generation plant within the country. Energia Renovable Versant SRL (“ERV”) is a 100% owned subsidiary and is used as a holding company for potential future renewable energy operating companies. ERV intends to consolidate common tasks for the operating companies in Costa Rica. VTRES BACHE SRL (“VTRES”) is 100% owned by ERV. VTRES is the legal entity that we intend to operate the first proposed wind farm in the northern area of the province of Guanacaste, Costa Rica.

Costa Rica has a variety of laws that govern the generation of electricity. Due to the location of our primary site, we cannot use the existing law for private generation (Ley 7200/7508). This is a result of the lack of an existing sub-station of Grupo ICE in the vicinity. The lack of a sub-station requires us to partner with one of the various State-Owned Entities charged with the distribution and generation of electricity for their respective regions. Candidates for partnership include JASEC, CNFL, COOPELESCA, ESPH and COOPEGUANACASTE.

Under its proposed long-term land agreement, the Company is seeking to develop its first field on 270 hectares (the “primary site”). Due to the current political delays revolving around the eighteen-month review period for the generation of electricity by private entities, the Company is also working on alternatives for sites that are more amenable to the development under Costa Rica’s private generation law (Law 7200/ 7508) with proximity to existing substations. Law 7200/7508 is an existing process by which private generation companies can, and do, contract with Grupo ICE for the purchase of electricity. This process is well developed and has existed for several decades. As mentioned above, the lack of an existing sub-station at our proposed 270-hectare site requires a Power Purchase Agreement through other existing laws. The Company believes it is important to explore other potential sites during this review period to avoid any potential future delays.

In November 2013, President Luis Guillermo Solis was elected in Costa Rica. Initially, the Company believed that Mr. Solis was amicable to private entities generating electricity as part of an overall solution to the energy crisis in Costa Rica based on his campaign promises and positions. However, Mr. Solis has made various post election representations that would seem to indicate his non-approval of such a position, mainly the appointment of a new chairman for the country’s Grupo ICE committee. We believe the Grupo ICE appointee, and now CEO and Chairman of Grupo ICE, has a public position generally against private enterprise’s participation in the power generation spectrum. The Company believes that this appointment will likely trigger opposition by the Costa Rican government against companies such as ERV from establishing privatized energy solutions.

The Company is actively engaged in lobbying through different government channels. The Company will also be exploring alternatives to the previous government approval process, including the possibility of a 7200/7508 license, which allows the Company to produce up to 20MW of electricity. However, due to the preceding events in the Costa Rican government, we cannot state with any certainty or provide any assurances of an expected timeline for regulatory approval.

Energy Market in Costa Rica

Costa Rica is in need of inexpensive energy sources, as it does not possess any petroleum or coal and its natural gas reserves are, as of yet, untapped. As a result of this lack of fossil fuel, Costa Rica has had to develop new sources of renewable energy. As stated in the article, Environmental Entrepreneurs Update June 28, 2007, President Aims for Carbon Neutrality, Costa Rica already uses hydroelectric and geo thermal methods and, in 2007, set 2021 as the year to become carbon neutral. According to The Delhi Planet, Being Carbon Neutral- What It Means And Whats Being Done, July 16, 2008, “In 2004 itself, 46.7% of Costa Rica’s primary energy came from renewable sources, while 94% of its electricity was generated from hydroelectric power, wind farms and geothermal energy in 2006.” Costa Rica is pro-active about being carbon neutral. Currently, there is a 3.5% tax on gasoline in the country that is used for payments to compensate landowners for growing trees and protecting forests.”

Grupo ICE is the largest of the State Owned Enterprises in Costa Rica and is the institution that controls all of the country’s electrical distribution. According to the Business Wire article titled Fitch Affirms Instituto Costarricense de Electridad’s Ratings at BB+, The Instituto Costarricense de Electricidad (“ICE”) is the largest power generator and electric distribution utility company in the country. ICE’s role is to develop, operate and ensure that telecommunication and electric services and distributions are provided to the Country. ICE is a State Owned Enterprise and its revenues are approximately $1 billion per year, which includes telecommunications services (fixed, data and cellular).

| 4 |

Based on the experience of Ing. Pedro P. Quiros, our founding Chairman, and the previous Chief Executive Officer and Chairman of Grupo ICE, the Company believes, that as much as 90% of the country’s hydroelectric facilities are losing effectiveness because of variations in the rainfall in the past few decades in Costa Rica. Additionally, it is his opinion that most hydroelectric facilities are reaching their useful life (50 years) and will need replacement or major maintenance. We believe this will place a serious burden on the country’s electric providers, as it will take much needed infrastructure investment away from new developments. We believe these developments are already taking place, which is straining the country’s sole petroleum-based 200 MW facility (“Garabito”).

Based on Grupo ICE’s public reports and our founding Chairman’s knowledge, we believe that Costa Rica is 8-10 years behind in developing the necessary electrical infrastructure to maintain pace with its needs. Grupo ICE is working to develop various projects, however, over the past few decades, government funding support has been diverted to other governmental priorities, such as housing. We believe this has left the electrical development delayed and behind with the country’s needs and electrical projects are large, expensive, complicated, and time consuming. We believe this infrastructure delay is pitting electric rates against the country’s competitiveness. The Company believes that the government has a projected investment requirement of $10 billion for electric generation alone over the next decade (2010-2020) with a maximum investment capacity of $5 billion over the same time frame.

Law 8660 passed in large part due to the efforts of the former Chief Executive Officer and Chairman of Grupo ICE, Ing, Pedro P. Quiros, who regulated the possible maximum investment that can be made by Grupo ICE at approximately $5 billion. Based on their revenue, we believe ICE’s current legal framework allows it to invest about $850 million per year for its core businesses. This means that about $350 million per year is allocated for electric generation (the remainder is split between electrical distribution- $150 million- and telecommunications- $350 million). We believe that this leaves the government with an approximate, and very conservative, shortfall of $5 billion for electric generation in the next decade ($10 billion in required investment, less $350 million in electric generation plus $150 in electrical distribution times 10 years, equals a $5 billion shortfall). These internal forecasts do not take into account the possible reduced telecommunications revenues as a result of competition in the cellular market and possible credit issues due to the effect of the latest Moody’s downgrade of the country’s credit rating in September 2014 to Ba1 from Baa3, which was the downgrade given in 2010 from BB+.

Over approximately the last two years, numerous complaints by the Costa Rican public have been made and the local newspapers have covered the rate hikes Grupo ICE has instituted as a result of the very high use of its main 200 MW reserve facility, Garabito. Garabito uses petroleum-based fuel and runs continuously, primarily in the summer months (October-March) when the rains stop and hydro plants slow as a result of the lack of water. According to the article “Tarifa electrica impacta competitividad” dated March 26, 2013 in La Republica, one of the major newspapers in Costa Rica, electric rates have risen 50-60% since 2007 as a result of underdevelopment of infrastructure.

Legal and Regulatory Framework

The situation related to the state of the energy market in Costa Rica has highlighted to the public the limited existing legal framework that allows the private generation and sale of electricity. As a result, there has been discussion in the legislature on how to expand and strengthen private rights and participation in the electric generation space. Currently, new laws are expected to improve the current legal framework in favor of private enterprise. However, these new laws are not expected for a few more years. Our business plan currently utilizes existing legislation and any future improvements would be a welcome benefit. However, the new government changes have delayed our progress and we may have to reinitiate the process to put the power purchase agreement in place. We cannot guarantee that any such future improvements will ever take place.

The current legal framework allows a few options to generate electric power. Law 7200/7508 controls the provision of concessions for private enterprises and specifically delineates the process by which any private enterprise receives, operates and commercializes its concession. This law is applicable to limited capacity facilities selling to ICE in amounts less than 20 MW. Law 8345 specifically grants the eight Costa Rican electric utility companies the right to generate power and specifies other rights like the “right of way” and the power to appropriate via “eminent domain”. There are various smaller electric utility companies (state cooperatives) in the country charged with other public services like street lighting, waste removal and sewage. These other electric utility companies bill their constituents directly, and as a group, handle half (50%) of the electrical distribution in the country with the other 50% handled by ICE. The bylaws as passed in Costa Rica for these utility companies allow them to enter into agreements with private entities to develop their services. These utility companies do not need further legislative approval or bidding to enter into these partnership agreements, so long as (i) Costa Rican ownership levels are within the law (35%), (ii) no Costa Rican government funds are used in the development, and that (iii) “a clear benefit is provided by entering into these arrangements” as stated in Law 8345.

Laws established for the Public Service companies such as Compañía Nacional Fuerza y Luz (an ICE subsidiary), JASEC (“Cartago”) and ESPH (“Heredia”), are similar to the one of four electric cooperatives regarding power generation and distribution. These entities have their own legal framework. All are allowed private partnerships to generate electricity and all have the credit rating of the Costa Rican government.

| 5 |

Off-Taker and Distribution Channel

An off-taker is a buyer of a resource to purchase and sell portions of a producer’s future production. An Off-Taker Agreement, or Power Purchase Agreement (“PPA”), is normally negotiated prior to the construction of a facility such as our proposed wind farm, in order to secure a market for the future output of the facility. On December 21, 2012, the Company received a Letter of Interest from the Compañia Nacional de Fuerza y Luz (“CNFL” or the proposed “Off-Taker”). CNFL is a private company 98% owned by Grupo ICE. Its market is “El Valle Central” or Central Valley, the area of San Jose and its environs. According to a public article published in Costa Rica, “El Potgam a la luz del censo 2011”, Central Valley is the largest market in the country with approximately 2 million customers in its general area.

The Company negotiated key terms and conditions with CNFL for a proposed PPA, including potential price and term. As a result of these negotiations, the Company tendered an official offer on April 16, 2013. The parties agreed in principle to a price (net of taxes) of $0.083/kWh and a term of twenty-five years. The price of electricity for wind, as many other services, is regulated by ARESEP and the above price is what we believe to be on the lower edge of the accepted pricing range in Costa Rica. Based on current information from the potential buyer, they delayed the internal process due to changes in regulation and later on due to new policies of the government winning the elections early in 2014. Currently, all private generation is on hold for an internal government review, which began in summer of 2014 and is expected to last through early 2016. In the event that the Off-Taker does not execute the PPA, there is no guarantee that the Company will be able to secure another Off-Taker on similar terms or at all. Should the Company not be able to secure another Off-Taker it would have a material adverse effect on our business and may cause us to cease operations entirely.

Costa Rica held elections in May 2014 and the new administration has advised, as of June 2014, that all projects for private generation are on hold until a review period of 18 months can be completed. Due to the delay presented by this review period, the Company is exploring 7200/7508 possibilities, the case being that these smaller plants are easier to accept within the existing legislation and are outside the current review process. We are currently pursuing alternative sites that allow us to utilize the 7200/7508 legislation, in the same area as our primary site. The Company will only seek alternative sites, compliant with Law 7200/7508, with existing sub-stations and access to high tension lines already provided by Grupo ICE. If successful, the ensuing PPA would be with Grupo ICE.

Interconnection

An “interconnection” is a power grid that operates at a synchronized frequency and is electrically tied together during normal system conditions. Synchronous grids with ample capacity facilitate electricity market trading across wide areas. Per the terms of our offer, CNFL intends to collect their electricity “at site” which means that they would be ensuring the interconnection and transport of the electricity generated by our wind farm to their substation. In our opinion this could greatly reduce our risk, as CNFL is an entity that has, as ICE’s subsidiary, full control and rights to the high-tension transmission lines of Costa Rica. ICE is the exclusive agent for high-tension lines including access to this network. This high-tension network is how electricity is delivered to CNFL’s grid and from there to its customers. The 7200/7508 contracts contemplate delivery at the substation and are by law with Grupo ICE, however, there is no existing substation at the primary site described above and therefore, we are looking for alternative smaller sites as well.

The substation in the primary site where the Company intends to connect to the high transmission lines to transport the electricity is less than 500 meters from the Sistema de Interconexion Electricapara America Central or Central American Electrical Interconnection System (“SIEPAC”). SIEPAC is a planned interconnection of the power grids of six Central American nations. In Central America, few electrical interconnections currently exist, and those that do are often old and unreliable. SIEPAC has been discussing plans to link the region’s electricity grids since 1987. The proposed project entails the construction of transmission lines connecting 37 million consumers in Panama, Costa Rica, Honduras, Nicaragua, El Salvador, and Guatemala. It is not clear if Belize, which buys much of its power from Mexico, will also be included. SIEPAC would cost about US$320 million without the interconnections with Mexico (US$40m), Belize (US$30m) and Panama (US$200m) and, back in 2003, was scheduled for completion in 2006. More recently, it has been estimated it would be completed in 2009. As of April 2013, all but about 20 km in southern Costa Rica is operating.

| 6 |

We believe because our proximity to the substation is so close to the SIEPAC transmission line that it may be possible to avoid paying the SIEPAC interconnection line costs and that an interagency arrangement could be handled under CNFL/ICE’s already existing agreements with SIEPAC. The Company and SIEPAC have entered into a non-binding letter of intent, whereby SIEPAC intends to serve as an interconnection and will provide the power generated, by the company’s proposed wind farm, to customers across Costa Rica. Please see a copy of the Letter of Intent between the Company and SIEPAC filed as Exhibit 10.1 to the amended registration statement on Form 10. Filed on December 4, 2013.

Wind Studies

Wind studies have been conducted on the primary site for the past several years. There are six active wind measurement towers on site, each 80 meters high, gradually built since 2007. In addition, there are two older towers of 50 meters high, which are out of service today, but have provided data along with neighboring MET masts for reference into the overall wind mapping conditions of the region. These stations offer different height levels of measurements for five years. The compiled data will be used for the revised Annual Energy Production Report (as defined below).

The Company engaged and paid GL Garrad Hassan approximately $80,000 to evaluate and generate an annual Energy Production Report (“AEP Report”) with five different wind turbine generators (WTGs). According to our current AEP Report, the Company can generate approximately 135,000,000 kWh per year (P75). The Company has moved the site slightly to the north (approximately 5 km) to gain access to the interconnection lines. Other benefits of this land include:

| ● | Large enough to increase capacity (5,300 hectares of land). | |

| ● | The land is level and generally flat. | |

| ● | The SIEPAC regional (Central America) grid traverses through the property. This allows us to transport electricity to the power grid and to our final customers. |

We have also commissioned a new AEP Report from Garrad Hassan for updated information. We have made a $20,000 payment to Garrad Hassan for the new AEP Report, and plan to pay the remaining $18,120 upon completion of certain amendments.

Competition

We face competition from other wind energy companies, renewable energy generators, and traditional energy companies in our bidding and signing for a long-term PPA with the government of Costa Rica. However, if we are successful in signing the PPA, we believe we will have no competition for the wind energy generated by our anticipated wind farm. This is not to say that Costa Rica does not have other wind farms or sources of renewable energy but rather that once the wind farm is completed, the sales will be guaranteed for the term of the PPA, which is currently proposed as twenty-five (25) years. If the PPA is signed, our proposed contract covers our entire production and the Off-Taker is committed to buying this electricity over the 25-year term. Additionally, each government utility in Costa Rica has exclusive territory to its client base by law.

The Company would not make any sales without the execution of the PPA. Should the PPA be cancelled or otherwise terminated, it would have a material adverse effect on the Company and may force us to cease our business operations entirely.

Going Concern

Our financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying financial statements, we incurred a net operating loss in the years ended December 31, 2014 and 2013, have a working capital deficit of approximately $5,108,000 at December 31, 2014 and have no revenues at this time. These conditions raise substantial doubt about the Company’s ability to continue as a going concern.

| 7 |

The ability of the Company to continue as a going concern is dependent upon the Company’s ability to further implement its business plan, generate revenues, and continue to raise additional investment capital. No assurance can be given that the Company will be successful in these efforts. The lack of additional capital could force the Company to curtail or cease operations and would, therefore, have a material adverse effect on its business.

Employees

As of April 15, 2015 the Company had two full-time employees and one consultant.

OVERVIEW OF OUR TELECOMMUNICATIONS BUSINESS

On May 29, 2014, the Board of Directors (the “Board”) of STL Marketing Group, Inc. (the “Company”) approved the formation of PhoneSuite Solutions, Inc. (“PSS”), as a Delaware corporation and a wholly owned subsidiary of the Company. On June 16, 2014, the Board approved the issuance of one-hundred (100) shares of common stock of PSS to the Company (the “Subsidiary Shares”). The Subsidiary Shares represent 100% of the authorized shares of common stock of PSS.

On June 24, 2014, PSS, as the Company’s wholly owned subsidiary, entered into a Strategic Alliance and Distribution Agreement (the “Agreement”) with Call Management Products, Inc. (“CMP”), a Colorado corporation in the business of designing, manufacturing, marketing, and selling telecommunications products. The Agreement provides that PSS will establish a dealer network and market and sell CMP’s products both internationally and in the United States (the “Territory”). In the domestic market PSS will market to the general business market, excluding the hospitality and assisted living verticals. Internationally, PSS may sell to all markets and develop both the hospitality and general business marketplaces.

Additionally, the Agreement provides that PSS will develop the Territories at its cost and promote CMP’s brands, name and products consistently across the globe. PSS is an exclusive Strategic Ally for CMP’s products in the Territory. The Agreement provides that, each year, PSS and CMP will mutually establish a sales quota for PSS to meet, with the first quota set for fiscal 2015.

At this time, internal work has been completed on both the structural necessities for this type of transactional business and the necessary training and certifications processes to ensure the proper infrastructure in instituting a process to establish dealers. Internal review of our accounting systems has also been completed and is now loaded and adapted to quoting, entering orders, and invoicing.

To date, the Company has issued quotes to interested, potential customers for VoIP equipment. While there is no guarantee these quotes will be sold, it is an important milestone, as we believe this sales funnel does begin to indicate that we may have revenue in the near term, which we believe will help to establish a baseline to provide future goals based on previous sales.

To ensure an active and successful dealer program and sales funnel, we have begun the process of establishing our dealer network. In this area, we are actively working with a handful of potential dealers that we believe will execute dealer agreements in the short term. We have announced one partnership with VTECH’s CALA hospitality division whereby VTECH will provide us leads for the PhoneSuite product line and vice versa. This also provides us access to their dealer network if applicable. Additionally, we have had preliminary discussions with UNIDEN to explore providing business telephones with the IP PBX as a whole solution. All of this is underway as we await progress on the energy front. We can provide no assurances that these dealer agreements will be successful in generating sales for our business operations.

The Company has successfully signed three distribution agreements covering the United Arab Emirates and India, Barbados and Nigeria and currently has six additional and active overseas distribution possibilities. These possible partners are located in Australia, Bangladesh, Guatemala, Saipan, Malta, and Mexico. Active quotes to potential customers are significant for our current stage. We can provide no assurances that these distribution agreements will lead to sales.

In 2015, we believe PhoneSuite Solutions, Inc. will begin to generate revenue, add dealers, and follow through with our goal to gain financial independence. We believe that this should ease dependence on fundraising over the near term and lessen our need for the current funding mechanisms.

| 8 |

Competition

Competitors vary by region. However, we believe our major competitors include Avaya, Shoretel, NEC, Mitel and Cisco. PSS is focused on providing newer technologies such as Voiceware (full VoIP) and the Series 2 (VoIP/ Analog hybrid) for its dealer business vertical.

Business Plan

PSS is focused on the promotion, marketing, and sales of two of PhoneSuite’s core products (i) Voiceware and (ii) the Series2. These products are already deployed in the United States, with PSS now developing the dealer channel to achieve sales revenues overseas. These products are VoIP Private Branch Exchange products, designed to provide a feature rich communications system to businesses.

| 1. | Voiceware - Voiceware is a VoIP phone system (IP-PBX) application designed for today’s hospitality voice communication needs. The server-based core makes Voiceware extremely flexible, and enables PhoneSuite to continually enhance and improve a hotel PBX feature set without expensive equipment upgrades. | |

| 2. | Series 2 - Series2 VoIP combines a traditional telephone platform (analog room phones and digital and analog telephone lines) with a Voiceware server. This converts traditional analog and digital end points to be compatible with VoIP technology. With this technology a customer will be able to use existing wiring plans and phones without potentially expensive upgrades. |

PSS is the exclusive distributor of PhoneSuite branded products to both the international market, as well as the Small Business Market (SMB) here in the United States. PSS currently has plans to offer products in geographic areas including, but not limited to: Asia, the Caribbean, Africa, Australia, the Middle East and India, Europe, Central America, and South America.

Going Concern

Our financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying financial statements, we incurred a net operating loss in the years ended December 31, 2014 and 2013, have a working capital deficit of approximately $5,108,000 at December 31, 2014 and have no revenues at this time. These conditions raise substantial doubt about the Company’s ability to continue as a going concern.

The ability of the Company to continue as a going concern is dependent upon the Company’s ability to further implement its business plan, generate revenues, and continue to raise additional investment capital. No assurance can be given that the Company will be successful in these efforts. The lack of additional capital could force the Company to curtail or cease operations and would, therefore, have a material adverse effect on its business.

Reports to Security Holders.

| 1. | The Company will file with the SEC reports as required under the Exchange Act and comply with the requirements of the Exchange Act. | |

| 2. | The public may read and copy any materials the Company files with the SEC in the SEC’s Public Reference Section, Room 1580, 100 F Street N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Section by calling the SEC at 1-800-SEC-0330. Additionally, the SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, which can be found at http://www.sec.gov. |

| 9 |

Where You Can Find More Information

The public may read and copy any materials the Company files with the U.S. Securities and Exchange Commission (the “SEC”) at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0030. The SEC maintains an Internet website (http://www.sec.gov) that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

OUR AUDITORS HAVE EXPRESSED SUBSTANTIAL DOUBT ABOUT OUR ABILITY TO CONTINUE AS A GOING CONCERN.

As of December 31, 2014, we had a net loss of $771,742. A significant amount of capital will be necessary to advance the development of our projects to the point at which they will become commercially viable, and these conditions raise substantial doubt about our ability to continue as a going concern.

Our independent auditors included an explanatory paragraph regarding this uncertainty in their report on our financial statements as of December 31, 2014. The Company plans to raise additional debt and/or equity financing to allow us the ability to cover our current cash flow requirements and meet our obligations as they become due. There can be no assurances that financing will be available or if available, that it will be under favorable terms. In the event that we are unable to generate adequate revenues to cover expenses and cannot obtain additional financing in the near future, we may need to cease operations or seek protection under bankruptcy laws. These financial statements do not include any adjustments that might result from the uncertainty as to whether we will continue as a “going concern”. Our ability to continue status as a “going concern” is dependent upon our generating cash flow sufficient to fund operations. If we continue incurring losses and fail to achieve profitability, we may have to cease our operations. Our business plan may not be successful in addressing these issues.

RISKS RELATED TO OUR BUSINESSES

WE HAVE GENERATED SUBSTANTIAL NET LOSSES AND NEGATIVE OPERATING CASH FLOWS SINCE OUR INCEPTION AND EXPECT TO CONTINUE TO DO SO AS WE BEGIN TO DEVELOP AND CONSTRUCT OUR FUTURE ENERGY AND TELECOMMUNICATIONS PROJECTS.

We have generated substantial net losses and negative operating cash flows from operating activities since our operations commenced.

We expect that our net losses will continue and our cash used in operating activities will grow during the next several years, as compared with prior periods, as we increase our development activities. Energy and telecommunications projects typically incur operating losses prior to commercial operation at which point the projects begin to generate positive operating cash flow. We also expect to incur additional costs, contributing to our losses and operating uses of cash, as we incur the incremental costs of operating as a fully reporting public company. Our costs may also increase due to factors such as higher than anticipated financing and other costs; increases in the costs of labor or materials; and major incidents or catastrophic events. If any of those factors occurs, our losses could increase significantly and the value of our common stock could decline. As a result, our net losses and accumulated deficit could increase significantly.

WE DO NOT HAVE SUFFICIENT CASH ON HAND. IF WE DO NOT GENERATE SUFFICIENT REVENUES FROM SALES, AMONG OTHER FACTORS, WE WILL BE UNABLE TO CONTINUE OUR OPERATIONS.

There is limited history upon which to base any assumption as to the likelihood that we will prove to be successful, and we may not be able to generate enough operating revenues or ever achieve profitable operations. If we are unsuccessful in addressing these risks, our business will be adversely affected.

| 10 |

WE HAVE A LIMITED OPERATING HISTORY. IF WE ARE NOT SUCCESSFUL IN CONTINUING TO GROW THE BUSINESS, THEN WE MAY HAVE TO SCALE BACK OR EVEN CEASE ONGOING BUSINESS OPERATIONS.

We have no history of revenues from operations. We have yet to generate positive earnings and there can be no assurance that we will ever operate profitably. Operations will be subject to all the risks inherent in the establishment of a developing enterprise, such as difficulties in commercializing our wind energy power generation plant and telecommunications business, and the uncertainties arising from the absence of a significant operating history. We may be unable to sign customer contracts or operate on a profitable basis. If the business plan is not successful, and we are not able to operate profitably, investors may lose some or all of their investment.

IF WE ARE UNABLE TO OBTAIN ADDITIONAL FUNDING, BUSINESS OPERATIONS WILL BE HARMED, AND IF WE DO OBTAIN ADDITIONAL FINANCING THEN EXISTING SHAREHOLDERS MAY SUFFER SUBSTANTIAL DILUTION.

Additional capital will be required to effectively support the operations and otherwise implement overall business strategy. We currently do not have any contracts or commitments for additional financing. There can be no assurance that financing will be available in amounts or on terms acceptable to us, if at all. The inability to obtain additional capital will restrict our ability to grow and may reduce our ability to continue to conduct business operations. If we are unable to obtain additional financing, we will likely be required to curtail and possibly cease operations. Any additional equity financing may involve substantial dilution to then existing shareholders.

THE LOSS OF ONE OR MORE MEMBERS OF OUR SENIOR MANAGEMENT OR KEY EMPLOYEES MAY ADVERSELY AFFECT OUR ABILITY TO IMPLEMENT OUR STRATEGY.

We depend on our experienced management team and the loss of one or more key executives could have a negative impact on our business. Our success depends to a significant extent upon the continued services of Mr. Jose P. Quiros, our Chief Executive Officer. The loss of the services of Mr. Quiros could have a material adverse effect on our growth, revenues, and prospective business. Mr. Quiros does have an employment agreement with the Company.

In order to successfully implement and manage our business plan, we will be dependent upon, among other things, successfully recruiting qualified managerial and company personnel having experience in the small wind turbine and telecommunications business. Competition for qualified individuals is intense. Additionally, because the wind industry is relatively new, there is a scarcity of top-quality employees with experience in the wind industry, including qualified technical personnel with significant experience in the design, development, manufacture and construction of wind power generation plants, and we may face challenges hiring and retaining these types of employees.

We also depend on our ability to retain and motivate key employees and attract qualified new employees. There can be no assurance that we will be able to retain existing employees or that we will be able to find, attract and retain qualified personnel on acceptable terms. If we lose a member of the management team or a key employee, we may not be able to replace him or her. Integrating new employees into our management team and training new employees with no prior experience in the wind industry could prove disruptive to our operations, require a disproportionate amount of resources and management attention and ultimately prove unsuccessful. An inability to attract and retain sufficient technical and managerial personnel could limit or delay our development efforts, which could have a material adverse effect on our business, financial condition and results of operations.

| 11 |

WE NEED TO ESTABLISH AND MAINTAIN REQUIRED DISCLOSURE CONTROLS AND PROCEDURES AND INTERNAL CONTROLS OVER FINANCIAL REPORTING AND TO MEET THE PUBLIC REPORTING AND THE FINANCIAL REQUIREMENTS FOR OUR BUSINESS, WHICH WILL BE TIME CONSUMING FOR OUR MANAGEMENT.

Our management has a legal and fiduciary duty to establish and maintain disclosure controls and control procedures in compliance with the securities laws, including the requirements mandated by the Sarbanes-Oxley Act of 2002. The standards that must be met for management to assess the internal control over financial reporting as effective are new and complex, and require significant documentation, testing and possible remediation to meet the detailed standards. Because we have limited resources, we may encounter problems or delays in completing activities necessary to make an assessment of our internal control over financial reporting, and other disclosure controls and procedures. In addition, the attestation process by our independent registered public accounting firm is new and we may encounter problems or delays in completing the implementation of any requested improvements and receiving an attestation of our assessment by our independent registered public accounting firm. If we cannot assess our internal control over financial reporting as effective or provide adequate disclosure controls or implement sufficient control procedures, or our independent registered public accounting firm is unable to provide an unqualified attestation report on such assessment, investor confidence and share value may be negatively impacted.

IF WE CANNOT EFFECTIVELY MANAGE OUR INTERNAL GROWTH, OUR POTENTIAL BUSINESS PROSPECTS, REVENUES AND PROFIT MARGINS MAY SUFFER.

If we fail to effectively manage our internal growth in a manner that minimizes strains on our resources, we could experience disruptions in our operations and ultimately be unable to generate revenues or profits. We expect that we will need to significantly expand our operations to successfully implement our business strategy. As we add manufacturing, marketing, sales and installation and build our infrastructure, we expect that our operating expenses and capital requirements will increase. To effectively manage our growth, we must continue to expend funds to improve our operational, financial and management controls and our reporting systems and procedures. In addition, we must effectively expand, train and manage our employee base. If we fail in our efforts to manage our internal growth, our prospects, revenue and profit margins may suffer.

THE PRODUCTION OF WIND ENERGY DEPENDS HEAVILY ON SUITABLE WIND CONDITIONS. IF WIND CONDITIONS ARE UNFAVORABLE OR BELOW OUR ESTIMATES, OUR ELECTRICITY PRODUCTION, AND THEREFORE OUR REVENUES, MAY BE SUBSTANTIALLY BELOW OUR EXPECTATIONS.

The electricity produced and revenues generated by a wind energy project depend heavily on wind conditions, which are variable and difficult to predict. Operating results for projects vary significantly from period to period depending on the wind resource during the periods in question. We base our decisions about which sites to develop in part on the findings of long-term wind and other meteorological studies conducted in the proposed area, which measure the wind’s speed, prevailing direction and seasonal variations. Actual wind conditions, however, may not conform to the measured data in these studies and may be affected by variations in weather patterns, including any potential impact of climate change. Therefore, the electricity generated by our projects may not meet our anticipated production levels or the rated capacity of the turbines located there, which could adversely affect our business, financial condition and results of operations. If the wind resources at a project are below the average level we expect, our rate of return for the project would be below our expectations and we would be adversely affected. Projections of wind resources also rely upon assumptions about turbine placement, interference between turbines and the effects of vegetation, land use and terrain, which involve uncertainty and require us to exercise considerable judgment. We or our consultants may make mistakes in conducting these wind and other meteorological studies. Any of these factors could cause us to develop sites that have less wind potential than we had expected, or to develop sites in ways that do not optimize their potential, which could cause the return on our investment in these projects to be lower than expected.

If our wind energy assessments turn out to be wrong, our business could suffer a number of material adverse consequences, including:

| ● | our energy production and sales may be significantly lower than we predict; |

| ● | any future hedging arrangements may be ineffective or more costly; |

| ● | we may not produce sufficient energy to meet future commitments to sell electricity as a result, we may have to pay damages; and |

| ● | our projects may not generate sufficient cash flow to make payments of principal and interest as they become due on any future project-related debt, and we may have difficulty obtaining financing for future projects. |

| 12 |

NATURAL EVENTS MAY REDUCE ENERGY PRODUCTION BELOW OUR EXPECTATIONS.

A natural disaster, severe weather or an accident that damages or otherwise adversely affects any of our operations could have a material adverse effect on our business, financial condition and results of operations. Lightning strikes, icing, earthquakes, tornados, extreme wind, severe storms, wildfires and other unfavorable weather conditions or natural disasters could damage or require us to shut down our turbines or related equipment and facilities, impeding our ability to maintain and operate our facilities and decreasing electricity production levels and our revenues. Operational problems, such as degradation of turbine components due to wear or weather or capacity limitations on the electrical transmission network, can also affect the amount of energy we are able to deliver. Any of these events, to the extent not fully covered by insurance, could have a material adverse effect on our business, financial condition and results of operations.

OPERATIONAL PROBLEMS MAY REDUCE ENERGY PRODUCTION BELOW OUR EXPECTATIONS.

Spare parts for wind turbines and key pieces of electrical equipment may be hard to acquire or unavailable to us. Sources for some significant spare parts and other equipment are located outside of North America. If we were to experience a shortage of or inability to acquire critical spare parts, we could incur significant delays in returning facilities to full operation. In addition, we may not hold spare substation main transformers. These transformers are designed specifically for each wind energy project, and the current lead time to receive an order for this type of equipment is over eight months. If we had to replace any future substation main transformers, we could be unable to sell electricity from the affected wind energy project until a replacement is installed. That interruption to our business might not be fully covered by insurance.

WE FACE COMPETITION PRIMARILY FROM OTHER RENEWABLE ENERGY SOURCES AND, IN PARTICULAR, OTHER WIND ENERGY COMPANIES.

We believe our primary competitors are developers and operators focused on renewable energy generation, specifically wind energy companies. We will compete with other wind energy companies primarily for sites with good wind resources that can be built in a cost-effective manner. We will also compete for access to transmission or distribution networks. Because the wind energy industry in the United States is at an early stage, we will also compete with other wind energy developers for the limited pool of personnel with requisite industry knowledge and experience. Furthermore, in recent years, there have been times of increased demand for wind turbine related components, causing turbine suppliers to have difficulty meeting the demand. If these conditions return in the future, component manufacturers may give priority to other market participants, including our competitors, who may have resources greater than ours.

We compete with other renewable energy companies (and energy companies in general) for the financing needed to pursue our development plan. Once we have developed a project and put a project into operation, we may compete on price if we sell electricity into power markets at wholesale market prices. Depending on the regulatory framework and market dynamics of a region, we may also compete with other wind energy companies, as well other renewable energy generators, when we bid on or negotiate for a long-term PPA.

WE WILL ALSO COMPETE WITH TRADITIONAL ENERGY COMPANIES.

We will also compete with traditional energy companies. For example, depending on the regulatory framework and market dynamics of a region, we also compete with traditional electricity producers when we bid on or negotiate for a long-term PPA. Furthermore, technological progress in traditional forms of electricity generation (including technology that reduces or sequesters greenhouse gas emissions) or the discovery of large new deposits of traditional fuels could reduce the cost of electricity generated from those sources or make them more environmentally friendly, and as a consequence reduce the demand for electricity from renewable energy sources or render existing or future wind energy projects uncompetitive. Any of these developments could have a material adverse effect on our business, financial condition and results of operations.

| 13 |

NEGATIVE PUBLIC OR COMMUNITY RESPONSE TO WIND ENERGY PROJECTS IN GENERAL OR OUR PROJECTS SPECIFICALLY CAN ADVERSELY AFFECT OUR ABILITY TO DEVELOP OUR WIND FARM PROJECTS.

Negative public or community response to our wind energy projects can adversely affect our ability to develop, construct and operate our projects. This type of negative response can lead to legal, public relations and other challenges that impede our ability to meet our development and construction targets, achieve commercial operations for a project on schedule, address the changing needs of our projects over time, and generate revenues. If we are unable to develop, construct and operate the production capacity that we expect from our future development projects in our anticipated timeframes, it could have a material adverse effect on our business, financial condition and results of operations.

WE NEED GOVERNMENTAL APPROVAL FROM THE COSTA RICAN GOVERNMENT AND PERMITS TO CONSTRUCT AND OPERATE OUR PROJECTS. ANY FAILURE TO PROCURE AND/OR MAINTAIN NECESSARY PERMITS WOULD ADVERSELY AFFECT ONGOING DEVELOPMENT, CONSTRUCTION AND CONTINUING OPERATION OF OUR PROJECTS.

The design, construction and operation of wind energy projects are highly regulated, require various approvals from the government of Costa Rica and permits, including environmental approvals and permits, and may be subject to the imposition of related conditions that vary by jurisdiction. In some cases, these approvals and permits require periodic renewal, which we may not be able to successfully obtain. We cannot predict whether all permits required for a given project will be granted or whether the conditions associated with the permits will be achievable. The denial of a permit essential to a project or the imposition of impractical conditions would impair our ability to develop the project. In addition, we cannot predict whether the permits will attract significant opposition or whether the permitting process will be lengthened due to complexities and appeals. Delay in the review and permitting process for a project can impair or delay our ability to develop that project or increase the cost so substantially that the project is no longer attractive to us. In the future, we may experience delays in developing our future projects due to delays in obtaining non-appealable permits. If we were to commence construction in anticipation of obtaining the final, non-appealable permits needed for a project, we would be subject to the risk of being unable to complete the project if all the permits were not obtained. If this were to occur, we would likely lose a significant portion of our investment in the project and could incur a loss as a result. Any failure to procure and maintain necessary permits would adversely affect ongoing development, construction and continuing operation of our projects.

OUR DEVELOPMENT ACTIVITIES AND OPERATIONS ARE SUBJECT TO NUMEROUS ENVIRONMENTAL, HEALTH AND SAFETY LAWS AND REGULATIONS.

We are subject to numerous environmental, health and safety laws and regulations in each of the jurisdictions in which we intend to operate. These laws and regulations will require us to obtain approvals and maintain permits, undergo environmental impact assessments and review processes and implement environmental, health and safety programs and procedures to control risks associated with the citing, construction, operation and decommissioning of wind energy projects. For example, to obtain permits we could be required to undertake expensive programs to protect and maintain local endangered species. If such programs are not successful, we could be subject to penalties or to revocation of our permits. In addition, permits frequently specify permissible sound levels.

If we do not comply with applicable laws, regulations or permit requirements, we may be required to pay penalties or fines or curtail or cease operations of the affected projects. Violations of environmental and other laws, regulations and permit requirements, including certain violations of laws protecting migratory birds and endangered species, may also result in criminal sanctions or injunctions.

Environmental, health and safety laws, regulations and permit requirements may change or become more stringent. Any such changes could require us to incur materially higher costs than we have incurred to date. Our costs of complying with current and future environmental, health and safety laws, regulations and permit requirements, and any liabilities, fines or other sanctions resulting from violations of them, could adversely affect our business, financial condition and results of operations.

| 14 |

WE WILL RELY ON TRANSMISSION LINES AND OTHER TRANSMISSION FACILITIES THAT ARE OWNED AND OPERATED BY THIRD PARTIES. WHEREVER WE DEVELOP OUR OWN GENERATOR LEADS, WE WILL BE EXPOSED TO TRANSMISSION FACILITY DEVELOPMENT AND CURTAILMENT RISKS, WHICH MAY DELAY AND INCREASE THE COSTS OF OUR PROJECTS OR REDUCE THE RETURN TO US ON THOSE INVESTMENTS.

We will depend on electric transmission lines owned and operated by third parties to deliver the electricity we generate. Some of our projects may have limited access to interconnection and transmission capacity because there can be many parties seeking access to the limited capacity that may be available. We may not be able to secure access to this limited interconnection or transmission capacity at reasonable prices or at all. Moreover, a failure in the operation by third parties of these transmission facilities could result in our losing revenues because such a failure could limit the amount of electricity we deliver. In addition, our production of electricity may be curtailed due to third-party transmission limitations, reducing our revenues and impairing our ability to capitalize fully on a particular project’s potential. Such a failure could have a material adverse effect on our business, financial condition and results of operations.

In certain circumstances, we may develop our own generator leads in the future from our projects to available electricity transmission or distribution networks when such facilities do not already exist. In some cases, these facilities may cover significant distances. To construct such facilities, we need approvals, permits and land rights, which may be difficult or impossible to acquire or the acquisition of which may require significant expenditures. We may not be successful in these activities, and our projects that rely on such generator lead development may be delayed, have increased costs or not be feasible. Our failure in operating these generator leads could result in lost revenues because it could limit the amount of electricity we are able to deliver. In addition, we may be required by law or regulation to provide service over our facilities to third parties at regulated rates, which could constrain transmission of our power from the affected facilities, or we could be subject to additional regulatory risks associated with being considered the owner of a transmission line.

WE MAY BE UNABLE TO CONSTRUCT OUR WIND ENERGY PROJECTS ON TIME, AND OUR CONSTRUCTION COSTS COULD INCREASE TO LEVELS THAT MAKE A PROJECT TOO EXPENSIVE TO COMPLETE OR MAKE THE RETURN ON OUR INVESTMENT IN THAT PROJECT LESS THAN EXPECTED.

There may be delays or unexpected developments in completing our future wind energy projects, which could cause the construction costs of these projects to exceed our expectations. We may suffer significant construction delays or construction cost increases as a result of a variety of factors, including, without limitation:

| ● | failure to manufacture turbines on the required schedule; | |

| ● | failure to receive other critical components and equipment, including batteries, that meet our design specifications on schedule; | |

| ● | failure to complete interconnection to transmission networks; | |

| ● | failure to obtain all necessary rights to land access and use; | |

| ● | failure to receive quality and timely performance of third-party services; | |

| ● | failure to secure and maintain environmental and other permits or approvals; | |

| ● | appeals of environmental and other permits or approvals that we obtain; | |

| ● | failure to obtain capital to develop our planned wind farm projects; | |

| ● | shortage of skilled labor; | |

| ● | inclement weather conditions; | |

| ● | adverse environmental and geological conditions; and | |

| ● | force majeure or other events out of our control. |

| 15 |

Any of these factors could give rise to construction delays and construction costs in excess of our expectations. This could prevent us from completing construction of a project, cause defaults under any potential financing agreements or under PPAs that require completion of project construction by a certain time, cause the project to be unprofitable for us, or otherwise impair our business, financial condition and results of operations.

FUTURE LITIGATION OR ADMINISTRATIVE PROCEEDINGS RELATED TO OUR WIND FARM PROJECTS COULD HAVE A MATERIAL ADVERSE EFFECT ON OUR BUSINESS, FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

In the future, we may be involved in legal proceedings, administrative proceedings, claims and/or litigation that arise in the ordinary course of business of wind farm projects. Individuals and interest groups may sue to challenge the issuance of a permit for a wind energy project or seek to enjoin construction of a wind energy project. In addition, we may be subject to legal proceedings or claims contesting the construction or operation of future wind energy projects. Unfavorable outcomes or developments relating to any such proceedings, such as judgments for monetary damages, injunctions or denial or revocation of permits, could have a material adverse effect on our business, financial condition and results of operations.

WE ARE NOT ABLE TO INSURE AGAINST ALL POTENTIAL RISKS AND MAY BECOME SUBJECT TO HIGHER INSURANCE PREMIUMS.

Our wind energy division will be exposed to the risks inherent in the construction and operation of wind energy projects, such as breakdowns, manufacturing defects, natural disasters, terrorist attacks and sabotage, not all of which is insurable. We may also be exposed to environmental risks. We will have insurance policies covering certain risks associated with our business. However, any such insurance policies will not cover losses as a result of force majeure, natural disasters, terrorist attacks or sabotage, among other things. We do not expect to maintain insurance for certain environmental risks, such as environmental contamination with respect to our wind energy business. In addition, our insurance policies may be subject to annual review by our insurers and may not be renewed at all or on similar or favorable terms. A serious uninsured loss or a loss significantly exceeding the limits of our future insurance policies could have a material adverse effect on our business, financial condition and results of operations.

WE FACE FORMIDABLE COMPETITION FROM NUMEROUS ESTABLISHED FIRMS THAT PROVIDE BOTH TRADITIONAL ENTERPRISE VOICE COMMUNICATIONS SOLUTIONS AS WELL AS PROVIDERS OF TECHNOLOGY RELATED TO BUSINESS COLLABORATION AND CONTACT CENTER SOLUTIONS; AS THESE MARKETS EVOLVE, WE EXPECT COMPETITION TO INTENSIFY AND EXPAND TO INCLUDE COMPANIES THAT DO NOT CURRENTLY COMPETE DIRECTLY AGAINST US.

We compete against providers of both traditional enterprise voice communications solutions, as well as providers of technology related to business collaboration and contact center solutions. In addition, because the business collaboration market continues to evolve and technology continues to develop rapidly, we may face competition in the future from companies that do not currently compete against us, but whose current business activities may bring them into competition with us in the future. In particular, information technology and communications applications deployed on converged networks become more integrated to support business collaboration. We may face increased competition from current leaders in information technology infrastructure, information technology, consumer products companies, personal and business applications and the software that connects the network infrastructure to those applications. Several of our existing competitors have, and many of our future competitors may have, greater financial, personnel, technical, research and development and other resources, more well-established brands or reputations and broader customer bases and, as a result, these competitors may be in a stronger position to respond quickly to potential acquisitions and other market opportunities, new or emerging technologies and changes in customer requirements. Some of these competitors may have customer bases that are more geographically balanced and therefore, may be less affected by an economic downturn in a particular region. Other competitors may have deeper expertise in a particular stand-alone technology that develops more quickly than we anticipate. Competitors with greater resources also may be able to offer lower prices, additional products or services or other incentives. Industry consolidations may also create competitors with broader and more geographic coverage and the ability to reach enterprises through communications service providers. Existing customers of data networking companies that compete against us may be inclined to purchase enterprise communications solutions from their current data networking or software vendors. Additionally, as communications and data networks converge, we may face competition from systems integrators that traditionally have been focused on data network integration.

| 16 |

RISKS RELATED TO THE TELECOMMUNICATIONS INDUSTRY - REGULATION OF IP-BASED NETWORKS AND COMMERCE IN THE UNITED STATES AND ELSEWHERE MAY INCREASE, COMPLIANCE WITH THESE REGULATIONS MAY BE TIME-CONSUMING, DIFFICULT AND COSTLY AND, IF WE FAIL TO COMPLY, OUR SALES MIGHT DECREASE.

In general, the telecommunications industry is highly regulated. Regulatory treatment of VoIP telephony outside the United States varies from country to country and often the laws are unclear. We currently plan to distribute our products and services directly through resellers that may be subject to telecommunications regulations in their home countries. The failure by us or our resellers to comply with these laws and regulations could impact our business operations. Such regulations could include matters such as using or providing VoIP services or protocols, encryption technology and access charges for service providers. The adoption of such regulations could prohibit entry into a target market or force us to withdraw products in one or more jurisdictions. As a result, overall demand for our products could decrease and, at the same time, the cost of selling our products could increase, either of which, or the combination of both, could have a material adverse effect on our business, operating results and financial condition.

In addition, the convergence of the public switched telephone network, or PSTN, and IP-based networks could become subject to governmental regulation, including the imposition of access fees or other tariffs, and such regulation could adversely affect the market for our products and services. User uncertainty regarding future policies and regulations may also affect demand for communications products such as ours. We may be required, or we may otherwise deem it necessary or advisable, to alter our products to address actual or anticipated changes in the regulatory environment. Our inability to timely alter our products or address any regulatory changes may have a material adverse effect on our financial condition, results of operations or cash flows.

WE MAY NOT BE ABLE TO COMPETE SUCCESSFULLY IN OUR HIGHLY COMPETITIVE INDUSTRIES, WHICH COULD ADVERSELY AFFECT OUR BUSINESS, RESULTS OF OPERATIONS AND FINANCIAL CONDITION.

We face significant competition in many of the markets in which we do business and expect that this competition will intensify. The principal competitive factors in our business are range of service offerings, global capabilities and price and quality of services. In addition, we believe there has been an industry trend to move agent-based operations toward offshore sites. The trend toward international expansion by foreign and domestic competitors and continuous technological changes may erode profits by bringing new competitors into our markets and reducing prices. Our competitors’ products, services and pricing practices, as well as the timing and circumstances of the entry of additional competitors into our markets, could adversely affect our business, results of operations and financial condition.

We rely on a combination of an internal sales effort and third party relationships to market our services. If we are unable to offset pricing declines through increased transaction volume and greater efficiency due to a failure of our sales efforts or otherwise, our business, results of operations and financial condition could be adversely affected.

THE LOSS OF ONE OR MORE MEMBERS OF OUR SENIOR MANAGEMENT OR KEY EMPLOYEES MAY ADVERSELY AFFECT OUR ABILITY TO IMPLEMENT OUR STRATEGY.

We depend on our experienced management team and the loss of one or more key executives could have a negative impact on our business. Our success depends to a significant extent upon the continued services of Mr. Jose P. Quiros, our Chief Executive Officer. The loss of the services of Mr. Quiros could have a material adverse effect on our growth, revenues, and prospective business. Mr. Quiros does have an employment agreement with the Company.

We also depend on our ability to retain and motivate key employees and attract qualified new employees. There can be no assurance that we will be able to retain existing employees or that we will be able to find, attract and retain qualified personnel on acceptable terms. If we lose a member of the management team or a key employee, we may not be able to replace him or her. Integrating new employees into our management team and training new employees with no prior experience in the wind industry could prove disruptive to our operations, require a disproportionate amount of resources and management attention and ultimately prove unsuccessful. An inability to attract and retain sufficient technical and managerial personnel could limit or delay our development efforts, which could have a material adverse effect on our business, financial condition and results of operations.

| 17 |

RISKS RELATED TO COMMON STOCK

POTENTIAL FUTURE FINANCINGS MAY DILUTE THE HOLDINGS OF OUR CURRENT SHAREHOLDERS.

In order to provide capital for the operation of our business, in the future we may enter into financing arrangements. These arrangements may involve the issuance of new shares of common stock, preferred stock that is convertible into common stock, debt securities that are convertible into common stock or warrants for the purchase of common stock. Any of these items could result in a material increase in the number of shares of common stock outstanding, which would in turn result in a dilution of the ownership interests of existing common shareholders. In addition, these new securities could contain provisions, such as priorities on distributions and voting rights, which could affect the value of our existing common stock.

WE CURRENTLY DO NOT INTEND TO PAY DIVIDENDS ON OUR COMMON STOCK. AS A RESULT, YOUR ONLY OPPORTUNITY TO ACHIEVE A RETURN ON YOUR INVESTMENT IS IF THE PRICE OF OUR COMMON STOCK APPRECIATES.

We currently do not expect to declare or pay dividends on our common stock. In addition, in the future we may enter into agreements that prohibit or restrict our ability to declare or pay dividends on our common stock. As a result, your only opportunity to achieve a return on your investment will be if the market price of our common stock appreciates and you sell your shares at a profit.

YOU MAY EXPERIENCE DILUTION OF YOUR OWNERSHIP INTEREST DUE TO THE FUTURE ISSUANCE OF ADDITIONAL SHARES OF OUR COMMON STOCK.

We are in a capital intensive business and we do not have sufficient funds to finance the growth of our natural gas, oil and wind energy divisions of our business or the construction costs of our development projects or to support our projected capital expenditures. As a result, we will require additional funds from future equity or debt financings, including tax equity financing transactions or sales of preferred shares or convertible debt, to complete the development of new projects and pay the general and administrative costs of our business. We may in the future issue our previously authorized and unissued securities, resulting in the dilution of the ownership interests of holders of our common stock. We are currently authorized to issue 2,600,000,000 shares of common stock and 1,401,925,000 shares of preferred stock with preferences and rights as determined by our board of directors. The potential issuance of such additional shares of common stock or preferred stock or convertible debt may create downward pressure on the trading price of our common stock. We may also issue additional shares of common stock or other securities that are convertible into or exercisable for common stock in future public offerings or private placements for capital raising purposes or for other business purposes. The future issuance of a substantial number of common shares into the public market, or the perception that such issuance could occur, could adversely affect the prevailing market price of our common shares. A decline in the price of our common shares could make it more difficult to raise unds through future offerings of our common shares or securities convertible into common shares.

| 18 |

THERE IS CURRENTLY A LIMITED PUBLIC MARKET FOR OUR COMMON STOCK. FAILURE TO DEVELOP OR MAINTAIN A TRADING MARKET COULD NEGATIVELY AFFECT ITS VALUE AND MAKE IT DIFFICULT OR IMPOSSIBLE FOR YOU TO SELL YOUR SHARES.

There has been a limited public market for our common stock and an active public market for our common stock may never develop. Failure to develop or maintain an active trading market could make it difficult for you to sell your shares or recover any part of your investment in us. Even if a market for our common stock does develop, the market price of our common stock may be highly volatile. In addition to the uncertainties relating to future operating performance and the profitability of operations, factors such as variations in interim financial results or various, as yet unpredictable, factors, many of which are beyond our control, may have a negative effect on the market price of our common stock.

“PENNY STOCK” RULES MAY MAKE BUYING OR SELLING OUR COMMON STOCK DIFFICULT.