Attached files

| file | filename |

|---|---|

| EX-21.0 - EXHIBIT 21.0 - FlexShopper, Inc. | f10k2014ex21_flexshopper.htm |

| EX-32.1 - CERTIFICATION PURSUANT TO - FlexShopper, Inc. | f10k2014ex32i_flexshopper.htm |

| EX-14.1 - CODE OF ETHICS FOR SENIOR FINANCIAL OFFICERS - FlexShopper, Inc. | f10k2014ex14i_flexshopper.htm |

| EX-31.1 - CERTIFICATION PURSUANT TO - FlexShopper, Inc. | f10k2014ex31i_flexshopper.htm |

| EX-32.2 - CERTIFICATION PURSUANT TO - FlexShopper, Inc. | f10k2014ex32ii_flexshopper.htm |

| EX-31.2 - CERTIFICATION PURSUANT TO - FlexShopper, Inc. | f10k2014ex31ii_flexshopper.htm |

| EX-10.34 - FIRST AMENDMENT TO LEASE AGREEMENT - FlexShopper, Inc. | f10k2014ex1034_flexshopper.htm |

| EX-99.4 - PRESS RELEASE - MARCH 31, 2015 - FlexShopper, Inc. | f10k2014ex99iv_flexshopper.htm |

| EXCEL - IDEA: XBRL DOCUMENT - FlexShopper, Inc. | Financial_Report.xls |

| EX-10.30 - ASSET PURCHASE AGREEMENT DATED APRIL 30, 2014 - FlexShopper, Inc. | f10k2014ex10xxx_flexshopper.htm |

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2014 |

or

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 12 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____ to ___

| Commission File Number: 0-52589 | ||

| |

||

| FLEXSHOPPER, INC. | ||

| (Exact name of Registrant as specified in its charter) | ||

| Delaware | 20-5456087 | |

| (State of jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification Number) | |

| 2700 North Military Trail, Ste. 200 | ||

| Boca Raton, FL | 33431 | |

| (Address of principal executive offices) | (Zip Code) | |

| Registrant’s telephone number, including area code: | (866) 950-6669 | |

Securities registered pursuant to Section 12 (b) of the Act: None

Securities registered pursuant to Section 12 (g) of the Act: Common Stock, $.0001 Par Value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

| 1 |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K ☒.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act: smaller reporting company ☒.

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of June 30, 2014, the number of shares of Common Stock held by non-affiliates was approximately 16,908,000 shares (excluding 376,387 shares of Series A Preferred Stock convertible into 2,145,406 common shares). The approximate market value based on the last sale (i.e. $0.75 per share as of June 30, 2014) of the Company’s Common Stock held by non-affiliates was approximately $14,180,000.

The number of shares outstanding of the Registrant’s Common Stock, as of March 19, 2015, was 52,015,322. The Registrant also has outstanding 342,219 shares of Series 1 Preferred Stock convertible into 2,166,246 shares of Common Stock.

Documents incorporated by reference: None.

| 2 |

FORWARD-LOOKING STATEMENTS

We believe this annual report contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are subject to risks and uncertainties and are based on the beliefs and assumptions of our management, based on information currently available to our management. When we use words such as “believes,” “expects,” “anticipates,” “intends,” “plans,” “estimates,” “should,” “likely” or similar expressions, we are making forward-looking statements. Forward-looking statements include information concerning our possible or assumed future results of operations set forth under “Business” and/or “Management's Discussion and Analysis of Financial Condition and Results of Operations.”

Forward-looking statements reflect only our current expectations. We may not update these forward-looking statements, even though our situation may change in the future. In any forward-looking statement, where we express an expectation or belief as to future results or events, such expectation or belief is expressed in good faith and believed to have a reasonable basis, but there can be no assurance that the statement of expectation or belief will be achieved or accomplished. Our actual results, performance or achievements could differ materially from those expressed in, or implied by, the forward-looking statements due to a number of uncertainties, many of which are unforeseen, including those matters discussed in the “Risk Factors” section of this Form 10-K. As a result of these factors, we cannot assure you that the forward-looking statements in this Registration Statement will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame, if at all. Accordingly, you should not place undue reliance on these forward-looking statements.

We qualify all the forward-looking statements contained in this Form 10-K by the foregoing cautionary statements.

| 3 |

PART I

Item 1. Business

Introduction

FlexShopper, Inc. (“we,” “us,” “our” or the “Company”) is a corporation organized under the laws of the State of Delaware on August 16, 2006. FlexShopper owns 100% of FlexShopper, LLC, a limited liability company incorporated under the laws of North Carolina on June 24, 2013. Since the sale of the assets of Anchor Funding Services LLC, which sale was completed in a series of transactions between April and June 2014, FlexShopper, Inc. is a holding corporation with no operations except for those conducted by FlexShopper, LLC. FlexShopper LLC owns two wholly-owned Delaware subsidiaries, namely, FlexShopper 1, LLC and FlexShopper 2, LLC. All references to the business operations of FlexShopper refer to FlexShopper LLC and its wholly-owned subsidiaries, unless the context indicates otherwise.

Recent Developments

On March 6, 2015, FlexShopper entered into a credit agreement (the “Credit Agreement”) with a Lender. FlexShopper is permitted to borrow funds under the Credit Agreement based on FlexShopper’s cash on hand and the Amortized Order Value of its Eligible Leases (as such terms are defined in the Credit Agreement) less certain deductions described in the Credit Agreement. Under the terms of the Credit Agreement, subject to the satisfaction of certain conditions, FlexShopper may borrow up to $25,000,000 from the Lender for a term of two years. The borrowing term may be extended for an additional twelve months in the sole discretion of the Lender. The Credit Agreement contemplates that the Lender may provide additional debt financing to FlexShopper, up to $100 million in total, under two uncommitted accordions following satisfaction of certain covenants and other terms and conditions. The Lender will receive security interests in certain leases as collateral under the Credit Agreement. In connection with entering into the Credit Agreement, on March 6, 2015, FlexShopper raised approximately $8.6 million in net proceeds through direct sales of 17.0 million shares of FlexShopper common stock, par value $0.0001 per share, to certain affiliates of the Lender and other accredited investors for a purchase price of $0.55 per share.

Overview

In June 2013, we formed FlexShopper for the purpose of developing a business that provides certain types of durable goods to consumers on a lease-to-own basis and also provides lease-to-own terms to consumers of third party retailers and e-tailers. FlexShopper has been generating revenues from this new line of business since December 2013. Management believes that the introduction of FlexShopper's lease-to-own (“LTO”) programs support broad untapped expansion opportunities within the U.S. consumer e-commerce and retail marketplaces. FlexShopper and its online LTO products provide consumers the ability to acquire durable goods, including electronics, computers and furniture on an affordable payment, lease basis. Concurrently, e-tailers and retailers that work with FlexShopper may increase their sales by utilizing FlexShopper's online channels to connect with consumers that want to acquire products on an LTO basis.

GROWTH OPPORTUNITIES AND STRATEGIES

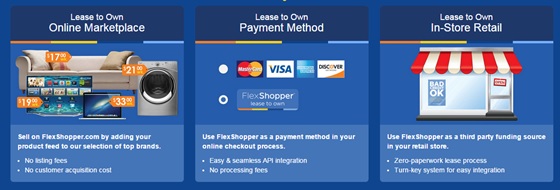

FlexShopper believes there is significant opportunity to expand the LTO industry online and into mainstream retail and e-tail. The LTO industry currently serves approximately six million consumers annually, generating approximately $8.5 billion in sales primarily through approximately 10,000 LTO brick and mortar stores. Through its strategic sales channels FlexShopper believes it will expand the LTO industry, also known as the rent-to-own or RTO industry. FlexShopper has successfully developed and is currently processing LTO transactions using its “LTO Engine.” The LTO Engine is FlexShopper’s proprietary technology that automates the process of consumers receiving spending limits and entering into leases for durable goods within a few minutes. The LTO engine is the basis for FlexShopper’s primary sales channels which provide consumers three distinct ways of obtaining brand name durable goods on an LTO basis: 1) At FlexShopper’s LTO e-commerce marketplace, www.flexshopper.com, consumers can choose from over 80,000 different items including electronics, furniture, musical instruments, and equipment. 2) On third party e-commerce sites featuring FlexShopper’s LTO payment method, consumers can activate FlexShopper’s payment button at checkout. 3) Consumers can use FlexShopper’s automated kiosk in certain retail locations.

FlexShopper launched its online LTO Marketplace in March 2014 and FlexShopper launched its LTO payment method in December 2014. Retailers and e-tailers that sell furniture, electronics, computers, appliances and other durable goods and partner with FlexShopper, will have three channels to increase their sales: in the store, online and on our marketplace. FlexShopper will enable merchants to sell to more than 50 million consumers that do not have sufficient credit or cash to buy from them. In addition, FlexShopper pays the merchant 100% pf the retail price. Our offerings to retail merchants are as follows as depicted in our marketing literature:

| 4 |

COMPETITIVE STRENGTHS

We believe the following competitive strengths differentiate us:

| · | We currently address the lease to own market through online channels which include our online marketplace and patent pending LTO payment method. These channels give us the ability to currently originate leases in forty five states without the operating expenses associated with having physical store-fronts in those states. |

| · | We believe our three channels described above, provide a compelling package for retailers to adopt to increase their sales with a vast customer base. |

| · | Our LTO online marketplace and patent pending payment method offer consumers more choices in products and retailers than traditional brick and mortar LTO storefronts. Our digital channels provide consumers with a selection of over 80,000 items including brand name products from recognized retailers. |

INDUSTRY OVERVIEW

The lease-to-own industry offers customers an alternative to traditional methods of obtaining electronics, computers, home furnishings and appliances. In a typical industry lease-to-own transaction, the customer has the option to acquire merchandise over a fixed term, usually 12 to 24 months, normally by making weekly lease payments. The customers may cancel the agreement as prescribed in the lease agreement by returning the merchandise, generally with no further lease obligation if their account is current. If customers lease the item to the full term, they obtain ownership of the item, though they can choose to buy it at any time. FlexShopper’s current fixed term to acquire ownership is fifty-two weeks.

The lease-to-own concept is particularly popular with consumers who cannot pay the full purchase price for merchandise at once or who lack the credit to qualify under conventional financing programs. Lease-to-own is also popular with consumers who, despite good credit, do not wish to incur additional debt, have only a temporary need for the merchandise or want to try out a particular brand or model before buying it.

We believe that there is significant market opportunity to expand the LTO market beyond brick and mortar stores by creating an online presence through an LTO e-commerce site and payment method. We believe that the segment of the population targeted by the industry comprises more than 50 million people in the United States and the needs of these consumers are generally underserved.

UNDERWRITING PROCESS AND RISK MANAGEMENT

FlexShopper has developed a proprietary decision engine that automates the process of consumers receiving spending limits and entering into leases for durable goods within a few minutes. Included in the determination of a consumer spending limit are factors such as income, frequency that they overdraw their bank account, fraud reports, repayment history and charge-off history. The Company obtains such consumer data from multiple third party sources which are monitored and analyzed by our risk department. We will continually update our underwriting models to manage risk of default. Our decision engine also includes fraud tools and information from third party data sources to combat online fraud. We will continuously develop and implement ongoing improvements to reduce losses due to fraudulent activity. In 2015, the Company has enhanced its risk department with two new hires including a Vice President of Risk and an Analytics Manager.

| 5 |

CUSTOMERS

FlexShopper’s customers typically do not have sufficient cash or credit to obtain durable goods. These consumers find the short-term nature and affordable payments of lease-to-own attractive. The lease-to-own industry serves a highly diverse customer base. According to the Association of Progressive Rental Organizations, approximately 83% of lease to-own customers have household incomes between $15,000 and $50,000 per year. We believe we can expand the LTO market beyond brick and mortar stores with our LTO e-commerce site and online payment method. These sales channels will enable us to serve and target more than 50 million people that we believe do not have sufficient cash or credit for durable goods.

SALES AND MARKETING

We plan to promote our FlexShopper products and services through print advertisements, Internet sites and direct response marketing, all of which are designed to increase our lease transactions and name recognition. Our advertisements emphasize such features as instant spending limit and affordable weekly payments. We believe that as the FlexShopper name gains familiarity and national recognition through our advertising efforts, we will continue to educate our customers and potential customers about the lease-to-own payment alternative as well as solidify our reputation as a leading provider of high quality branded merchandise and services.

For each sales channel FlexShopper has a marketing strategy that includes but is not limited to the following:

| Online LTO Marketplace | Patent pending LTO Payment Method | In-store LTO technology platform |

| Search engine optimization; pay-per click | Direct to retailers/etailers | Direct to retailers/etailers |

| Online affiliate networks | Partnerships with payment aggregators | Consultants & strategic relationships |

| Direct response television campaigns | Consultants & strategic relationships | |

| Direct mail |

MANAGEMENT INFORMATION SYSTEMS

FlexShopper uses computer-based management information systems to facilitate its entire business model including underwriting, processing transactions through its sales channels, managing collections and monitoring leased inventory. Through the use of our proprietary software developed in-house, each of our retail partners uses our online merchant portal that automates the process of consumers receiving spending limits and entering into leases for durable goods within a few minutes. The management information system generates reports which enable us to meet our financial reporting requirements.

GOVERNMENT REGULATIONS

The lease to own industry is regulated by and subject to the requirements of various federal, state and local laws and regulations, many of which are in place for consumer protection. In general such laws regulate applications for leases, late fees, other finance rates, the form of disclosure statements, the substance and sequence of required disclosures, the content of advertising materials and certain collection procedures. Violations of certain provisions of these laws may result in penalties ranging from nominal amounts up to and including forfeiture of fees and other amounts due on leases. We are unable to predict the nature or effect on our operations or earnings of unknown future legislation, regulations and judicial decisions or future interpretations of existing and future legislation or regulations relating to our operations, and there can be no assurance that future laws, decisions or interpretations will not have a material adverse effect on our operations and earnings. See “Risk Factors.”

COMPETITION

The lease-to-own industry is highly competitive. Our operation competes with other national, regional and local lease-to-own businesses, as well as with rental stores that do not offer their customers a purchase option. Some of these companies have, or may develop, systems that enable consumers to obtain through online facilities spending limits and payment terms and to enter into leases nearly instantaneously, in a manner similar to that provided by FlexShopper’s proprietary technology. Many of our competitors have substantially more resources and greater experience in the lease-to-own business than FlexShopper. With respect to customers desiring to purchase merchandise for cash or on credit, we also compete with retail stores. Competition is based primarily on store location, product selection and availability, customer service, and lease rates and terms. We believe that currently we do not have significant competition for our on-line LTO marketplace and patent pending LTO payment method, however there is no assurance that other companies may not develop similar or competing concepts that could adversely impact the usage or value of our online LTO marketplace or our LTO payment method.

| 6 |

INTELLECTUAL PROPERTY

FlexShopper has filed a provisional patent for a system that enables consumers to obtain products on an LTO basis using mobile devices and tablets and for a lease-to-own method of payment at check-out on e-commerce sites. We can provide no assurances that FlexShopper will be granted any patents by the U.S. Patent and Trademark Office. We regard our pending patents, trademarks, service marks, copyrights, trade dress, trade secrets, proprietary technology, and similar intellectual property as critical to our success. In particular, we believe certain proprietary information, including but not limited to our underwriting model, and patent pending systems are central to our business model and we believe give us a key competitive advantage. We rely on trademark and copyright law, trade secret protection, and confidentiality, license and work product agreements with our employees, customers, and others to protect our proprietary rights. See “Risk Factors.”

Operations and Employees of FlexShopper

Brad Bernstein, our Chief Executive Officer manages our day-to-day operations and internal growth and oversees our growth strategy. FlexShopper’s management includes an Executive Vice President of Operations, Chief Financial Officer, Chief Technology Officer with oversight of the Company’s development team and a Vice President of e-commerce. In addition, FlexShopper has a customer service and collections call center. As of December 31, 2014, FlexShopper had 44 full-time employees.

DISCONTINUED OPERATIONS OF ANCHOR

Anchor Funding Services LLC was incorporated under the laws of the State of South Carolina in January 2003 and later reincorporated under the laws of the State of North Carolina in August 2005. Anchor operated its factoring business for approximately 10 years until the assets were sold in a series of closings between April and June, 2014. Anchor purchased clients’ accounts receivable which provided businesses with critical working capital so it could meet their operational costs and obligations while waiting to receive payments from its customers. Anchor also provided purchase order financing.

During 2013, FlexShopper decided to concentrate its efforts on the operations of FlexShopper and subsequently on April 30, 2014, we entered into an Asset Purchase and Sale Agreement (the “Purchase Agreement”) with a Bank, pursuant to which Anchor Funding Services LLC sold to the Bank substantially all of its assets (the “Anchor Assets”), consisting primarily of its factoring portfolio (the “Portfolio Accounts”). The purchase price for the Anchor Assets was equal to (1) 110% of the total funds outstanding associated with the Portfolio Accounts plus (2) an amount equal to 50% of the factoring fee and interest income earned by the Portfolio Accounts during the 12 month period following acquisition (“Earnout Payments”). The sale of the Anchor Assets was made in a series of closings through June 16, 2014. In connection with each closing, Anchor used the proceeds thereof to pay to Bank all amounts due for factor advances associated with the Portfolio Accounts acquired pursuant to such closing under Anchor’s Rediscount Facility Agreement with the Bank dated November 30, 2011. In accordance with the Purchase Agreement, following the final closing thereunder all obligations of Anchor under the Rediscount Facility Agreement (and the associated Validity Warranty) were paid and satisfied in full and the agreement was terminated to have no further force and effect.

Item 1A. Risk Factors

You should carefully consider the following risk factors, in addition to the other information presented in this Form 10-K, in evaluating us and our business. Any of the following risks, as well as other risks and uncertainties, could harm our business and financial results and cause the value of our securities to decline, which in turn could cause you to lose all or part of your investment.

An investment in our common stock involves a high degree of risk. You should consider carefully the following risks and other information contained in this Form 10-K before you decide whether to buy our common stock. If any of the events contemplated by the following discussion of risks should occur, our business, results of operations and financial condition could suffer significantly. As a result, the market price of our common stock could decline, and you may lose all or part of the money you paid to buy our common stock. In addition, the risks described below are not the only ones facing our company. Additional risks and uncertainties of which we are unaware or currently deem immaterial may also become important factors that may harm our business.

Business Risks

Limited operating history. FlexShopper, LLC, which was formed in June 2013 to enter the lease-to-own business, has a limited operating history upon which investors may judge our performance. Our new FlexShopper business has generated revenues over a limited operating history and has incurred net losses. Our ability to achieve profitability in this business will depend upon many factors, including, without limitation, our ability to execute our growth strategy and technology development, obtain sufficient capital, develop relationships with third party retail partners, adapt to fluctuations in the economy and modify our strategy based on the degree and nature of competition. Our senior management team has very limited experience in the lease-to-own industry. While we believe our FlexShopper business model will be successful, prior success of our senior management in other businesses should not viewed as an indication that we will be profitable. We can provide no assurances that our operations will ever be profitable.

| 7 |

Our business liquidity and capital resources are dependent upon our credit agreement with an institutional lender and our compliance with the terms thereof. On March 6, 2015, FlexShopper, through a wholly-owned subsidiary (the “Borrower”), entered into a credit agreement (the “Credit Agreement”) with a lender (the “Lender”). The Borrower is permitted to borrow funds under the Credit Agreement based on the Borrower’s cash on hand and the Amortized Order Value of the Borrower’s Eligible Leases (as such terms are defined in the Credit Agreement) less certain deductions described in the Credit Agreement. Under the terms of the Credit Agreement, subject to the satisfaction of certain conditions, the Borrower may borrow up to $25,000,000 from the Lender for a term of two years. The borrowing term may be extended for an additional twelve months in the sole discretion of the Lender. The Credit Agreement contemplates that the Lender may provide additional debt financing to the Borrower, up to $100 million in total, under two uncommitted accordions following satisfaction of certain covenants and other terms and conditions. The Lender will receive security interests in certain leases as collateral under the Credit Agreement. For the term of the Credit Agreement, FlexShopper and its subsidiaries may not incur additional indebtedness (other than certain indebtedness expressly permitted under the Credit Agreement) without the permission of the Lender. The Lender and its affiliates will have a right of first refusal on certain subsequent FlexShopper transactions involving leases or other financial products during the term of the Credit Agreement and up to three months following the termination thereof. The Credit Agreement includes customary events of default, including, among others, failures to make payment of principal and interest, breaches or defaults under the terms of the Credit Agreement and related agreements entered into with the Lender, breaches of representations, warranties or certifications made by or on behalf of the Borrower in the Credit Agreement and related documents (including certain financial and expense covenants), deficiencies in the borrowing base, certain judgments against the Borrower and bankruptcy events. If an event of default occurs and is continuing, the Lender may, among other things, terminate any remaining commitments available to the Borrower, declare all outstanding principal and interest immediately due and payable and enforce any and all liens created in connection with the Credit Agreement. The occurrence of an event of default under the terms of our Credit Agreement may materially and adversely affect our operations.

FlexShopper LTO revenue and earnings growth depend on our ability to execute our growth strategies. Our primary growth strategies are our FlexShopper LTO online products to consumers and utilization by retailers of FlexShopper’s online channels to connect with customers that want to acquire products on a LTO basis. Effectively managing the development and growth can be challenging, particularly as we develop the management and operational systems necessary to develop this line of business. If we are unable to successfully execute these growth strategies, revenue from this line of business will grow slowly or not at all, and we may never achieve profitability.

Our LTO business depends on the success of our third-party retail partners and our continued relationships with them. Our LTO revenues depend in part on the ability of unaffiliated third-party retailers to attract customers. In addition, in most cases, our agreements with such third-party retailers may be terminated at the retailer's election. The failure of our third-party retail partners to maintain quality and consistency in their operations and their ability to continue to provide products and services, or the loss of the relationship with any of these third-party retailers and an inability to replace them, could cause our LTO business to lose customers, substantially decreasing the revenues and earnings growth in our LTO business.

Our growth will depend on our ability to develop our brands, and these efforts may be costly. Our ability to develop the FlexShopper brand will be critical to achieving widespread acceptance of our services, and will require a continued focus on active marketing efforts. We will need to continue to spend substantial amounts of money on, and devote substantial resources to, advertising, marketing, and other efforts to create and maintain brand loyalty among our customers. If we fail to promote and maintain our brand, or if we incur substantial expenses in an unsuccessful attempt to promote and maintain our brand, our business would be harmed.

Our LTO business will depend on the continued growth of online and mobile commerce. The business of selling goods over the Internet and mobile networks is dynamic and relatively new. Concerns about fraud, privacy and other problems may discourage additional consumers from adopting the Internet or mobile devices as modes of commerce, or may prompt consumers to offline channels. In order to expand our user base, we must appeal to and acquire consumers who historically have used traditional means of commerce to purchase goods and may prefer Internet analogues to such traditional retail means, such as the retailer's own website, to our offerings. If these consumers prove to be less active than we expect due to lower levels of willingness to use the Internet or mobile devices for commerce for any reason, including lack of access to high-speed communications equipment, traffic congestion on the Internet or mobile network outages or delays, disruptions or other damage to users' computers or mobile devices, and we are unable to gain efficiencies in our operating costs, including our cost of acquiring new users, our business could be adversely impacted.

| 8 |

Our customer base presents significant risk of default for non-payment. We bear the risk of non-payment or slow payment by our customers. The nature of our customer base makes it sensitive to adverse economic conditions and less likely to meet our prevailing underwriting standards, which may be more restrictive in an adverse economic environment. As a result, during such periods we may experience decreases in the growth of new customers, and we may curtail spending limits to existing customers, which may adversely affect our net sales and potential profitability.

Our customers can return merchandise without penalty. When our customers acquire merchandise through the FlexShopper LTO program, we actually purchase the merchandise from the retailer and enter the lease-to-own relationship with the customer. Because our customers can return merchandise without penalty, there is risk that we may end up owning a significant amount of merchandise that is difficult to monetize. While we have factored customer returns into our business model, customer return volume may exceed the levels we expect, which could adversely impact our collections, revenues and our financial performance. Returns totaled approximately $77,000 carrying value of leased merchandise during the twelve months ended December 31, 2014.

We rely on third party credit/debit card and ACH (Automated Clearing House) processors to process collections from customers on a weekly basis. Our ability to collect from customers could be impaired if these processors did not work with us. These third-party payment processors may consider our business a high risk since our customer base could have a high incidence of insufficient funds and rejected payments. This could cause a processor to discontinue its services to us, and we may not be able to find a replacement processor. If this occurred, we would have to collect from our customers using less efficient methods, which could adversely impact our collections, revenues and our financial performance.

We rely on internal models to manage risk, to provide accounting estimates and to make other business decisions. Our results could be adversely affected if those models do not provide reliable estimates or predictions of future activity. The accurate modeling of risks is critical to our business, particularly with respect to managing underwriting and spending limits for our customers. Our expectations regarding customer repayment levels, as well as our allowances for doubtful accounts and other accounting estimates, are based in large part on internal modeling. We also rely heavily on internal models in making a variety of other decisions crucial to the successful operation of our business. It is therefore important that our models are accurate, and any failure in this regard could have a material adverse effect on our results. Models are inherently imperfect predictors of actual results because they are based on historical data available to us and our assumptions about factors such as demand, payment rates, default rates, delinquency rates and other factors that may overstate or understate future experience. Our models could produce unreliable results for a number of reasons, including the limitations or lack of historical data to predict results, invalid or incorrect assumptions underlying the models, the need for manual adjustments in response to rapid changes in economic conditions, incorrect coding of the models, incorrect data being used by the models or inappropriate application of a model to products or events outside of the model’s intended use. In particular, models are less dependable when the economic environment is outside of historical experience, as has been the case recently. Due to the factors described above, unanticipated and excessive default and charge-off experience can adversely affect our profitability and financial condition, breach covenants in future credit facilities, limit our ability to secure a credit facility and adversely affect our ability to finance our business.

Our operations are regulated by and subject to the requirements of various federal and state laws and regulations. These laws and regulations, which may be amended or supplemented or interpreted by the courts from time to time, could expose us to significant compliance costs or burdens or force us to change our business practices in a manner that may be materially adverse to our operations, prospects or financial condition. Currently, 47 states and the District of Columbia specifically regulate rent-to-own, lease-to-own transactions. At the present time, no federal law specifically regulates the rent-to-own industry, although federal legislation to regulate the industry has been proposed from time to time. Any adverse changes in existing laws, or the passage of new adverse legislation by states or the federal government could materially increase both our costs of complying with laws and the risk that we could be sued or be subject to government sanctions if we are not in compliance. In addition, new burdensome legislation might force us to change our business model and might reduce the economic potential of our sales and lease ownership operations. Most of the states that regulate rent-to-own transactions have enacted disclosure laws that require rent-to-own companies to disclose to their customers the total number of payments, total amount and timing of all payments to acquire ownership of any item, any other charges that may be imposed and miscellaneous other items. The more restrictive state lease purchase laws limit the total amount that a customer may be charged for an item, or regulate the "cost-of-rental" amount that rent-to-own companies may charge on rent-to-own transactions, generally defining "cost-of-rental" as lease fees paid in excess of the “retail” price of the goods. There has been increased legislative attention in the United States, at both the federal and state levels, on consumer debt transactions in general, which may result in an increase in legislative regulatory efforts directed at the rent-to-own industry. We cannot guarantee that the federal government or states will not enact additional or different legislation that would be disadvantageous or otherwise materially adverse to us. In addition to the risk of lawsuits related to the laws that regulate rent-to-own and consumer lease transactions, we could be subject to lawsuits alleging violations of federal and/or state laws and regulations and consumer tort law, including fraud, consumer protection, information security and privacy laws, because of the consumer-oriented nature of the rent-to-own industry. A large judgment against FlexShopper could adversely affect our financial condition and results of operations. Moreover, an adverse outcome from a lawsuit, even one against one of our competitors, could result in changes in the way we and others in the industry do business, possibly leading to significant costs or decreased revenues or profitability.

| 9 |

If we fail to protect the integrity and security of customer and employee information, we could be exposed to litigation or regulatory enforcement, and our business could be adversely impacted. We collect and store certain personal information provided to us by our customers and employees in the ordinary course of our business. Despite instituted safeguards for the protection of such information, we cannot be certain that all of our systems are entirely free from vulnerability to attack. Computer hackers may attempt to penetrate our network security and, if successful, misappropriate confidential customer or employee information. In addition, one of our employees, contractors or other third party with whom we do business may attempt to circumvent our security measures in order to obtain such information, or inadvertently cause a breach involving such information. Loss of customer or employee information could disrupt our operations, damage our reputation and expose us to claims from customers, employees, regulators and other persons, any of which could have an adverse effect on our business, financial condition and results of operations. In addition, the costs associated with information security, such as increased investment in technology, the costs of compliance with privacy laws and costs incurred to prevent or remediate information security breaches, could adversely impact our business.

The loss of any of our key personnel could harm our business. Our future financial performance will depend to a significant extent on our ability to motivate and retain key management personnel. Further, FlexShopper is seeking to hire additional qualified management for its FlexShopper business. Competition for qualified management personnel is intense, and there can be no assurance that we will be able to hire additional qualified management on terms satisfactory to FlexShopper. Further, in the event we experience turnover in our senior management positions, we cannot assure you that we will be able to recruit suitable replacements. We must also successfully integrate all new management and other key positions within our organization to achieve our operating objectives. Even if we are successful, turnover in key management positions may temporarily harm our financial performance and results of operations until new management becomes familiar with our business. At present, we do not maintain key-man life insurance on any of our executive officers, although we entered into an employment contract with Brad Bernstein, Chief Executive Officer and President. Our Board of Directors is responsible for approval of all future employment contracts with our executive officers. We can provide no assurances that said future employment contracts and/or their current compensation is or will be on commercially reasonable terms to us in order to retain our key personnel. The loss of any of our key personnel could harm our business.

Competition in the LTO business is intense. The lease-to-own industry is highly competitive. Our operation will compete with other national, regional and local lease-to-own businesses, as well as with rental stores that do not offer their customers a purchase option. Some of these companies have, or may develop, systems that enable consumers to obtain through online facilities spending limits and payment terms and to enter into leases nearly instantaneously, in a manner similar to that provided by FlexShopper’s proprietary technology. Many of our competitors will have substantially more resources and greater experience in the lease-to-own business of FlexShopper. With respect to customers desiring to purchase merchandise for cash or on credit, we also compete with retail stores. Competition is based primarily on store location, product selection and availability, customer service and lease rates and terms. We believe we do not currently have significant competition for our on-line LTO marketplace and patent pending LTO payment method. However, such competition is likely to develop over time, and we may be unable to successfully compete in our target markets. We can provide no assurances that we will be able to successfully compete in the LTO industry.

Worsening of current economic conditions could result in decreased revenues or increased costs. Although we believe an economic downturn can result in increased business in the lease-to-own market as consumers increasingly find it difficult to purchase home furnishings, electronics and appliances from traditional retailers on store installment credit, it is possible that if the conditions continue for a significant period of time, or get worse, consumers may curtail spending on all or some of the types of merchandise we offer, in which event our revenues may suffer.

Changes in regulations or customer concerns, in particular as they relate to privacy and protection of customer data, could adversely affect our business. Our business is subject to laws relating to the collection, use, retention, security and transfer of personally identifiable information about our customers. The interpretation and application of privacy and customer data protection laws are in a state of flux and may vary from jurisdiction to jurisdiction. These laws may be interpreted and applied inconsistently and our current data protection policies and practices may not be consistent with those interpretations and applications. Complying with these varying requirements could cause us to incur substantial costs or require us to change our business practices in a manner adverse to our business. Any failure, or perceived failure, by us to comply with our own privacy policies or with any regulatory requirements or orders or other privacy or consumer protection related laws and regulations could result in proceedings or actions against us by governmental entities or others, subject us to significant penalties and negative publicity and adversely affect our operating results.

System interruption and the lack of integration and redundancy in our order entry and online systems may adversely affect our net sales. Customer access to our customer service center and websites is key to the continued flow of new orders. Anything that would hamper or interrupt such access could adversely affect our net sales, operating results and customer satisfaction. Examples of risks that could affect access include problems with the Internet or telecommunication infrastructure, limited web access by our customers, local or more systemic impairment of computer systems due to viruses or malware, or impaired access due to breaches of Internet security or denial of service attacks. Changes in the policies of service providers or others that increase the cost of telephone or Internet access could inhibit our ability to market our products or transact orders with customers. In addition, our ability to operate our business from day-to-day, largely depends on the efficient operation of our computer hardware and software systems and communications systems. Our computer and communications systems and operations could be damaged or interrupted by fire, flood, power loss, telecommunications failure, earthquakes, acts of war or terrorism, acts of God, computer viruses, physical or electronic break-ins or denial of service attacks, improper operation by employees and similar events or disruptions. Any of these events could cause system interruption, delays and loss of critical data and could prevent us from accepting and fulfilling customer orders and providing services, which would impair our operations. Certain of our systems are not redundant, and we have not fully implemented a disaster recovery plan. In addition, we may have inadequate insurance coverage to compensate us for any related losses. Interruptions to customer ordering, particularly if prolonged, could damage our reputation and be expensive to remedy and have significant adverse effects on our financial results.

| 10 |

We face risk related to the strength of our operational, technological and organizational infrastructure. We are exposed to operational risks that can be manifested in many ways, such as errors related to failed or inadequate processes, faulty or disabled computer systems, fraud by employees, contractors or third parties and exposure to external events. In addition, we are heavily dependent on the strength and capability of our technology systems that we use to manage our internal financial, credit and other systems, interface with our customers and develop and implement effective marketing campaigns. Our ability to operate our business to meet the needs of our existing customers and attract new ones and to run our business in compliance with applicable laws and regulations depends on the functionality of our operational and technology systems. Any disruptions or failures of our operational and technology systems, including those associated with improvements or modifications to such systems, could cause us to be unable to market and manage our products and services and to report our financial results in a timely and accurate manner, all of which could have a negative impact on our results of operations. In some cases, we outsource delivery, maintenance and development of our operational and technological functionality to third parties. These third parties may experience errors or disruptions that could adversely impact us and over which we may have limited control. Any increase in the amount of our infrastructure that we outsource to third parties may increase our exposure to these risks.

If we do not respond to technological changes, our services could become obsolete, and we could lose customers. To remain competitive, we must continue to enhance and improve the functionality and features of our e-commerce websites and other technologies. We may face material delays in introducing new products and enhancements. If this happens, our customers may forego the use of our websites and use those of our competitors. The Internet and the online commerce industry are rapidly changing. If competitors introduce new products and services using new technologies or if new industry standards and practices emerge, our existing websites and our proprietary technology and systems may become obsolete. Our failure to respond to technological change or to adequately maintain, upgrade and develop our computer network and the systems used to process customers’ orders and payments could harm our business, prospects, financial condition and results of operations.

We may not be able to adequately protect our intellectual property rights or may be accused of infringing intellectual property rights of third parties. We have filed provisional patents for a system that enables consumers to buy products on a LTO basis using mobile devices and tablets and for a lease-to-own method of payment at check-out on e-commerce sites. We can provide no assurances that we will be granted any patents by the U.S. Patent and Trademark Office. We regard our pending patents, trademarks, service marks, copyrights, trade dress, trade secrets, proprietary technology, and similar intellectual property as critical to our success. In particular, we believe certain proprietary information, including but not limited to our underwriting model, and patent pending systems are central to our business model, and we believe give us a key competitive advantage. We rely on trademark and copyright law, trade secret protection, and confidentiality, license and work product agreements with our employees, customers and others to protect our proprietary rights. We may be unable to prevent third parties from acquiring trademarks, service marks and domain names that are similar to, infringe upon, or diminish the value of our trademarks and other proprietary rights. Failure to protect our domain names could affect adversely our reputation and brand, and make it more difficult for users to find our website. We may be unable to discover or determine the extent of any unauthorized use of our proprietary rights. The protection of our intellectual property may require the expenditure of significant financial and managerial resources. In addition, the steps we take to protect our intellectual property may not adequately protect our rights or prevent parties from infringing or misappropriating our proprietary rights. We can be at risk that others will independently develop or acquire equivalent or superior technology or other intellectual property rights. The use of our technology or similar technology by others could reduce or eliminate any competitive advantage we have developed, cause us to lose sales or otherwise harm our business.

We cannot be certain that the intellectual property used in our business does not and will not infringe the intellectual property rights of others, and we are from time to time subject to third party infringement claims. Due to recent changes in patent law, we face the risk of a temporary increase in patent litigation due to new restrictions on including unrelated defendants in patent infringement lawsuits in the future particularly from entities that own patents but that do not make products or services covered by the patents. Any third party infringement claims against us, whether or not meritorious, may result in the expenditure of significant financial and managerial resources, injunctions against us or the payment of damages. Moreover, should we be found liable for infringement, we may be required to seek to enter into licensing agreements, which may not be available on acceptable terms or at all.

In deciding whether to provide a spending limit to customers, we rely on the accuracy and completeness of information furnished to us by or on behalf of our customers. If we and our systems are unable to detect any misrepresentations in this information, this could have a material adverse effect on our results of operations and financial condition. In deciding whether to provide a customer with a spending amount, we rely heavily on information furnished to us by or on behalf of our customers and our ability to validate such information through third-party services, including personal financial information. If a significant percentage of our customers intentionally or negligently misrepresent any of this information, and we or our systems do not or did not detect such misrepresentations, it could have a material adverse effect on our ability to effectively manage our risk, which could have a material adverse effect on our results of operations and financial condition.

| 11 |

If we fail to timely contact delinquent customers, then the number of delinquent customer receivables eventually being charged off could increase. We contact customers with delinquent account balances soon after the account becomes delinquent. During periods of increased delinquencies it is important that we are proactive in dealing with these customers rather than simply allowing customer receivables to go to charge-off. During periods of increased delinquencies, it becomes extremely important that we are properly staffed and trained to assist customers in bringing the delinquent balance current and ultimately avoiding charge-off. If we do not properly staff and train our collections personnel, or if we incur any downtime or other issues with our information systems that assist us with our collection efforts, then the number of accounts in a delinquent status or charged-off could increase. In addition, managing a substantially higher volume of delinquent customer receivables typically increases our operational costs. A rise in delinquencies or charge-offs could have a material adverse effect on our business, financial condition, liquidity and results of operations.

Our management information systems may not be adequate to meet our evolving business and emerging regulatory needs and the failure to successfully implement them could negatively impact the business and its financial results. We are investing significant capital in new information technology systems to support our growth plan. These investments include redundancies, and acquiring new systems and hardware with updated functionality. We are taking appropriate actions to ensure the successful implementation of these initiatives, including the testing of new systems, with minimal disruptions to the business. These efforts may take longer and may require greater financial and other resources than anticipated, may cause distraction of key personnel, may cause disruptions to our systems and our business, and may not provide the anticipated benefits. The disruption in our information technology systems, or our inability to improve, integrate or expand our systems to meet our evolving business and emerging regulatory requirements, could impair our ability to achieve critical strategic initiatives and could adversely impact our sales, collections efforts, cash flows and financial condition.

If we fail to maintain adequate systems and processes to detect and prevent fraudulent activity, our business could be adversely impacted. Criminals are using increasingly sophisticated methods to engage in illegal activities such as paper instrument counterfeiting, fraudulent payment or refund schemes and identity theft. As we make more of our services available over the internet and other media we subject ourselves to consumer fraud risk. We use a variety of tools to protect against fraud; however, these tools may not always be successful.

Our failure to maintain an effective system of internal controls could result in inaccurate reporting of financial results and harm our business. We are required to comply with a variety of reporting, accounting and other rules and regulations. As such, we maintain a system of internal control over financial reporting, but there are limitations inherent in internal control systems. A control system can provide only reasonable, not absolute, assurance that the objectives of the control system are met. In addition, the design of a control system must reflect the fact that there are resource constraints and the benefit of controls must be appropriate relative to their costs. Furthermore, compliance with existing requirements is expensive and we may need to implement additional finance and accounting and other systems, procedures and controls to satisfy our reporting requirements. If our internal control over financial reporting is determined to be ineffective, such failure could cause investors to lose confidence in our reported financial information, negatively affect the market price of our common stock, subject us to regulatory investigations and penalties, and adversely impact our business and financial condition.

Lack of Board Committees. Currently we have no audit, compensation, nominating or other committees of the board of directors. In the future, we may establish committees at such time as the board deems it to be in the best interest of our stockholders or when it is required under the rules of an exchange on which we may seek to list our Common Stock. We can provide no assurances that our lack of committees will not continue in future operating periods. Since we have no audit committee composed solely of independent directors, as required by the Sarbanes-Oxley Act of 2002, as amended, our board of directors has all the responsibilities of the audit committee.

Control of FlexShopper. Our secured lender described under Item 1, Item 7 and Item 13 beneficially owns 28.0% of our outstanding Common Stock as of the filing date of this Form 10-K. Also, our executive officers and directors beneficially own an additional 27.7% of our Common Stock as of the same date. In the event that they act in concert on future stockholder matters, such persons may have the ability to affect the election of all of our directors and the outcome of all issues submitted to our stockholders. Such concentration of ownership could limit the price that certain investors might be willing to pay in the future for shares of Common Stock and could have the effect of making it more difficult for a third party to acquire, or of discouraging a third party from attempting to acquire, control of us.

We have no established public market for our Securities. Our outstanding Common Stock does not have an established trading market, although our Common Stock has been quoted on the OTCQB under the symbol “FPAY.” Trading in our Common Stock has been sporadic in the Over-the-Counter Market since it began in December 2007. The availability for sale of restricted securities pursuant to Rule 144 or otherwise could adversely affect the market for our Common Stock, if any. We can provide no assurances that an established public market will ever develop or be sustained for our Common Stock in the future. Therefore, investors in this Offering may find it difficult to sell their Shares, whether pursuant to an effective registration statement, under Rule 144 or otherwise.

| 12 |

The price of our Common Stock may fluctuate significantly. The market price for our Common Stock, if any, can fluctuate as a result of a variety of factors, including the factors listed above, many of which are beyond our control. These factors include: actual or anticipated variations in quarterly operating results; announcements of new services by our competitors or us; announcements relating to strategic relationships or acquisitions; changes in financial estimates or other statements by securities analysts; and other changes in general economic conditions. Because of this, we may fail to meet or exceed the expectations of our stockholders or others, and the market price for our Common Stock could fluctuate as a result. In addition, the securities markets have from time to time experienced significant price and volume fluctuations that are unrelated to the operating performance of particular companies. These market fluctuations may also materially and adversely affect the market price of our Common Stock.

Our Common Stock is considered to be a “penny stock” and, as such, the market for our Common Stock, should one develop, may be further limited by certain SEC rules applicable to penny stocks. To the extent the price of our Common Stock remains below $5.00 per share or we have net tangible assets of $2,000,000 or less, our shares of Common Stock will be subject to certain “penny stock” rules promulgated by the SEC. Those rules impose certain sales practice requirements on brokers who sell penny stock to persons other than established customers and accredited investors (generally institutions with assets in excess of $5,000,000 or individuals with net worth in excess of $1,000,000). For transactions covered by the penny stock rules, the broker must make a special suitability determination for the purchaser and receive the purchaser’s written consent to the transaction prior to the sale. Furthermore, the penny stock rules generally require, among other things, that brokers engaged in secondary trading of penny stocks provide customers with written disclosure documents, monthly statements of the market value of penny stocks, disclosure of the bid and asked prices and disclosure of the compensation to the brokerage firm and disclosure of the sales person working for the brokerage firm. These rules and regulations could adversely affect the ability of brokers to sell our Common Stock in the public market should one develop, and they limit the liquidity of our Shares.

We have never declared or paid cash dividends on our Common Stock, and we do not anticipate paying any cash dividends on our Common Stock in the foreseeable future. We currently intend to retain future earnings, if any, to fund the development and growth of our FlexShopper business. Any future determination to pay cash dividends will be dependent upon our financial condition, operating results, capital requirements, applicable contractual restrictions and other such factors as our Board of Directors may deem relevant.

Increased costs associated with corporate governance compliance may significantly impact our results of operations. Changing laws, regulations and standards relating to corporate governance, public disclosure and compliance practices, including the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the Sarbanes-Oxley Act of 2002, and new SEC regulations, may create difficulties for companies such as ours in understanding and complying with these laws and regulations. As a result of these difficulties and other factors, devoting the necessary resources to comply with evolving corporate governance and public disclosure standards has resulted in and may in the future result in increased general and administrative expenses and a diversion of management time and attention to compliance activities. We also expect these developments to increase our legal compliance and financial reporting costs. In addition, these developments may make it more difficult and more expensive for us to obtain director and officer liability insurance, and we may be required to accept reduced coverage or incur substantially higher costs to obtain coverage. Moreover, we may be unable to comply with these new laws and regulations on a timely basis.

These developments could make it more difficult for us to retain qualified members of our board of directors, or qualified executive officers. We are presently evaluating and monitoring regulatory developments and cannot estimate the timing or magnitude of additional costs we may incur as a result. To the extent these costs are significant, our general and administrative expenses are likely to increase.

If we sell shares of our common stock or securities convertible into our common stock in future financings, the ownership interest of existing shareholders will be diluted and, as a result, our stock price may go down. We may from time to time issue additional shares of common stock at a discount from the current trading price of our common stock. As a result, our existing shareholders will experience immediate dilution upon the purchase of any shares of our common stock sold at a discount. For example, between May 8, 2014 and October 9, 2014, we sold 13,638,368 shares of our common stock in a private placement offering (and to two principal stockholders who are officers and/or directors) at a price of $.55 per share, at a time when the market price of our common stock was above this level. As other capital raising opportunities present themselves, we may enter into financing or similar arrangements in the future. If we issue common stock or securities convertible into common stock, our shareholders will experience dilution and this dilution will be greater if we find it necessary to sell securities at a discount to prevailing market prices.

| 13 |

In January 2015, we filed a registration statement with the Securities and Exchange Commission to register the resale of 13,593,214 shares of our common stock. As of the filing date of this Form 10-K, this registration statement has not been declared effective. Such a large number of shares registered for resale may depress the market price of our common stock. In January 2015, we filed a registration statement with the Securities and Exchange Commission to register the resale of 13,593,214 shares of our common stock. As of the filing date of this Form 10-K, this registration statement has not been declared effective. Such a large number of shares registered for resale may depress the market price of our common stock. Further, substantially all the remaining outstanding common shares not registered in this offering are either free trading shares in the public float or shares available for sale pursuant to Rule 144 of the Securities Act of 1933, as amended. Sales of a substantial number of shares of our common stock in the public market could cause the market price of our common stock to decline. If there are more shares of common stock offered for sale than buyers are willing to purchase, then the market price of our common stock may decline to a market price at which buyers are willing to purchase shares.

Item 1B. Unresolved Staff Comments

None

Item 2. Properties

On August 1, 2013, FlexShopper entered into a 39 month lease for additional office space in Boca Raton, Florida to accommodate FlexShopper’s business and its employees. The monthly rent was approximately $6,800. This lease agreement was amended in January 2014 to reflect a 63 month term for a larger suite in an adjoining building. Upon commencement the monthly base rent including operating expenses for the first year will be approximately $9,600 with annual three percent increases throughout the lease term.

Item 3. Legal Proceedings

We are not a party to any pending material legal proceedings except as described below. To our knowledge, no governmental authority is contemplating commencing a legal proceeding in which we would be named as a party.

On October 22, 2010, Anchor filed a complaint in the Superior Court of Stamford/Norwalk, Connecticut against the Administrators of the Estate of David Harvey ("Harvey") to recoup a credit loss incurred by FlexShopper’s former subsidiary, Brookridge Funding Services, LLC. Harvey was the owner of a Company that caused the credit loss, and FlexShopper is pursuing its rights under the personal guarantee that Harvey provided. The Complaint is demanding principal of approximately $485,000 plus interest and damages. During the twelve months ended December 31, 2014, there were no current developments involving the current legal proceeding.

Item 4. Mine Safety Disclosures

Not applicable

| 14 |

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our Common Stock is quoted on the OTCQB under the symbol “FPAY.” The following table sets forth the range of high and low closing sale prices of our Common Stock for our last two fiscal periods.

| High | Low | |||

| 2013 - Quarter Ended | ||||

| December 31 | $0.63 | $0.63 | ||

| September 30 | 0.50 | 0.50 | ||

| June 30 | 0.35 | 0.35 | ||

| March 31 | 0.22 | 0.22 | ||

| 2014 Quarter Ended | ||||

| December 31 | 1.00 | $0.40 | ||

| September 30 | 0.90 | 0.69 | ||

| June 30 | 0.94 | 0.65 | ||

| March 31 | 0.95 | 0.42 |

Our Common Stock has a limited public market. All quotations reflect inter-dealer prices, without retail mark-up, markdown or commissions and may not necessarily represent actual transactions.

Holders of Record

As of December 31, 2014, there were 707 holders of record of shares of Common Stock and 65 holders of record of our Series 1 Preferred Stock. FlexShopper's transfer agent is Continental Stock Transfer & Trust Company, 17 Battery Place, New York, NY 10004.

Dividend Policy

The holders of our Series 1 Preferred Stock were entitled to receive dividends from issuance in 2007 through December 31, 2009 as more fully described below. We have not paid or declared any cash dividends on our Common Stock. We currently intend to retain any earnings for future growth and, therefore, do not expect to pay cash dividends on our Common Stock in the foreseeable future. Cumulative annual dividends were payable in shares of Series 1 Preferred Stock or, in certain instances in cash, at an annual rate of 8% ($.40 per share of Series 1 Preferred Stock), on December 31 of each year commencing December 31, 2007 through December 31, 2009.

| 15 |

Recent Sales of Unregistered Securities

The following sales of unregistered securities took place during the quarter ended December 31, 2014:

| Date of Sale | Title of Security | Number Sold | Consideration Received | Purchasers | Exemption from Registration Claimed |

|

October 2014 |

Common Stock | 245,456 shares and placement agent warrants to purchase 1,773,027 shares (4) | $135,000 before placement agent compensation of $17,550 | Accredited Investors | Section 4(2) and/or Rule 506 promulgated thereunder |

|

October 2014 |

Common Stock | 194,758 shares | 34,168 Preferred Stock conversion; no commissions paid | Accredited Investors | Section 3(a)(9) |

|

October 2014 |

Common Stock Options(1) | Options to purchase 1,121,000 shares | Services rendered; no commissions paid | Officers, directors and employees | Section 4(2) |

| (1) | Options are exercisable at prices ranging from $0.17 to $1.25 per share. A Form S-8 Registration Statement is anticipated to be filed with the SEC to register the shares issuable upon exercise of options under our 2007 Stock Option Plan. |

Item 6. Selected Financial Data

Not applicable.

| 16 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion should be read in conjunction with our consolidated financial statements and the notes thereto appearing elsewhere in this Form 10-K.

Forward-Looking Statements

The Private Securities Litigation Reform Act of 1995 (the Act) provides a safe harbor for forward-looking statements made by or on behalf of our Company. Our Company and its representatives may from time to time make written or verbal forward-looking statements, including statements contained in this report and other Company filings with the Securities and Exchange Commission and in our reports to stockholders. Statements that relate to other than strictly historical facts, such as statements about the Company's plans and strategies and expectations for future financial performance are forward-looking statements within the meaning of the Act. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “will” and other similar expressions identify forward-looking statements. The forward-looking statements are and will be based on management's then current views and assumptions regarding future events and operating performance, and speak only as of their dates. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. See “Risk Factors” for a discussion of events and circumstances that could affect our financial performance or cause actual results to differ materially from estimates contained in or underlying our forward-looking statements.

Executive Overview

The results of operations from continuing operations below principally reflect the operations of FlexShopper, LLC which provides certain types of durable goods to consumers on a lease-to-own basis and also provides lease-to-own terms to consumers of third party retailers and e-tailers. FlexShopper began generating revenues from this line of business in December 2013. Management believes that the introduction of FlexShopper's Lease-to-own (LTO) programs support broad untapped expansion opportunities within the U.S. consumer e-commerce and retail marketplaces. FlexShopper and its online LTO platforms provide consumers the ability to acquire durable goods, including electronics, computers and furniture on an affordable payment, lease basis. Concurrently, e-tailers and retailers that work with FlexShopper may increase their sales by utilizing FlexShopper's online channels to connect with consumers that want to acquire products on an LTO basis. FlexShopper’s sales channels include 1) serving as the financial and technology partner for durable goods retailers and etailers 2) selling directly to consumers via the online FlexShopper LTO Marketplace featuring thousands of durable goods and 3) utilizing FlexShopper’s patent pending LTO payment method at check out on e-commerce sites.

Summary of Critical Accounting Policies

Management’s Discussion and Analysis of Financial Condition and Results of Operations discusses our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. On an on-going basis, management evaluates its estimates and judgments, including those related to credit provisions, intangible assets, contingencies, litigation and income taxes. Management bases its estimates and judgments on historical experience as well as various other factors that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions. Management believes the following critical accounting policies, among others, reflect the more significant judgments and estimates used in the preparation of our financial statements.

Accounts Receivable and Allowance for Doubtful Accounts – The Company seeks to collect amounts owed under its leases from each customer on a weekly basis by charging their bank account or credit card. Accounts receivable are principally comprised of lease payments currently owed to the Company which are past due as the Company has been unable to successfully collect in the manner described above. As of December 31, 2014, approximately 60% of the Company’s leases were current and did not have a past due balance and an additional 15% were past due with balances of one to four payments. An allowance for doubtful accounts is estimated by reserving all accounts in excess of four payments in arrears, adjusted for subsequent collections. The Company is developing historical data to assess the estimate of the allowance in the future. The accounts receivable balances consisted of the following as of December 31, 2014 and 2013.

| 17 |

| December 31, 2014 | December 31, 2013 | |||||||

| Accounts receivable | $ | 1,509,736 | $ | 119 | ||||

| Allowance for doubtful accounts | 1,380,902 | - | ||||||

| Accounts receivable, net | $ | 128,834 | $ | 119 | ||||

The Company’s reserve is 91.4% of the accounts receivable balance as of December 31, 2014. The reserve is a significant percentage of the balance because the Company has not charged off any customer accounts since inception to assure that it has exhausted all collection efforts with respect to each account including attempts to repossess items. In addition, the same delinquent customers will continue to accrue weekly charges until they are charged off or the Company has exhausted collection efforts and the company will charge off accounts once it estimates there is no chance of recovery.