Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - East Dubuque Nitrogen Partners, L.P. | Financial_Report.xls |

| EX-31.1 - EX-31.1 - East Dubuque Nitrogen Partners, L.P. | d824433dex311.htm |

| EX-32.1 - EX-32.1 - East Dubuque Nitrogen Partners, L.P. | d824433dex321.htm |

| EX-32.2 - EX-32.2 - East Dubuque Nitrogen Partners, L.P. | d824433dex322.htm |

| EX-21.1 - EX-21.1 - East Dubuque Nitrogen Partners, L.P. | d824433dex211.htm |

| EX-23.1 - EX-23.1 - East Dubuque Nitrogen Partners, L.P. | d824433dex231.htm |

| EX-31.2 - EX-31.2 - East Dubuque Nitrogen Partners, L.P. | d824433dex312.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Transition Period from to

Commission File No. 001-35334

RENTECH NITROGEN PARTNERS, L.P.

(Exact name of registrant as specified in its charter)

| Delaware | 45-2714747 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 10877 Wilshire Boulevard, 10th Floor Los Angeles, California |

90024 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (310) 571-9800

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Units Representing Limited Partner Interests | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates as of June 30, 2014, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $264.2 million (based upon the closing price of the common units on June 30, 2014, as reported by the New York Stock Exchange).

As of February 27, 2015, the registrant had 38,913,396 common units outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None

Table of Contents

2

Table of Contents

FORWARD-LOOKING STATEMENTS

Certain statements and information included in this Annual Report on Form 10-K, or this Annual Report, and other reports or materials that we have filed or will file with the Securities and Exchange Commission, or the SEC (as well as information included in oral statements or other written statements made or to be made by us or our management), contain or may contain “forward-looking statements.” Statements that are predictive in nature, that depend upon or refer to future events or conditions or that include the words “will,” “believe,” “expect,” “anticipate,” “intend,” “estimate” and other expressions that are predictions of or indicate future events and trends and that do not relate to historical matters identify forward-looking statements. Our forward-looking statements include statements about our business strategy, our industry, our future profitability, our expected capital expenditures (including for maintenance or expansion projects and environmental expenditures) and the impact of such expenditures on our performance, and our operating costs. These statements involve known and unknown risks, uncertainties and other factors, which may cause our actual results and performance to be materially different from any future results or performance expressed or implied by these forward-looking statements. Factors that could affect our results include the risk factors detailed in Part I—Item 1A “Risk Factors” and from time to time in our periodic reports and registration statements filed with the SEC. You should not place undue reliance on our forward-looking statements. Although forward-looking statements reflect our good faith beliefs, forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause our actual results, performance or achievements to differ materially from anticipated future results, performance or achievements expressed or implied by such forward-looking statements. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events, changed circumstances or otherwise, unless required by law.

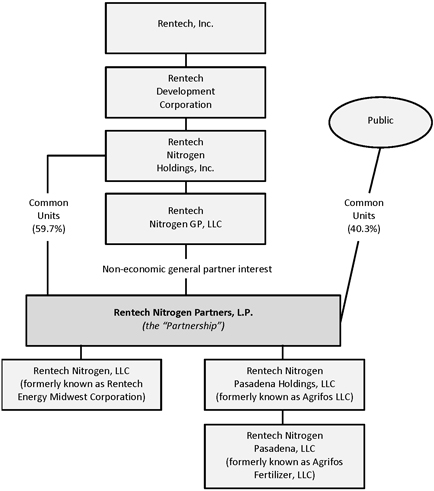

References in this report to “the Partnership,” “RNP,” “we,” “our,” “us” and like terms refer to Rentech Nitrogen Partners, L.P. and our subsidiaries, unless the context otherwise requires or where otherwise indicated. References in this report to “Rentech” refer to Rentech, Inc. and its subsidiaries other than us, unless the context otherwise requires or where otherwise indicated. References to “RDC” refer to Rentech Development Corporation, which is a wholly owned subsidiary of Rentech, references to “RNHI” refer to Rentech Nitrogen Holdings, Inc., which is a wholly owned subsidiary of RDC, and references to “Rentech Nitrogen GP” and “our general partner” refer to Rentech Nitrogen GP, LLC, which is our general partner and a wholly owned subsidiary of RNHI. References to “our operating companies” refer to Rentech Nitrogen, LLC, or RNLLC, which was formerly known as Rentech Energy Midwest Corporation, or REMC, and Rentech Nitrogen Pasadena, LLC, or RNPLLC, which was formerly known as Agrifos Fertilizer, LLC.

3

Table of Contents

Overview

We are a Delaware master limited partnership formed in July 2011 by Rentech, a company traded on the NASDAQ Stock Market under the symbol “RTK,” to own, operate and expand our fertilizer business. We own and operate two fertilizer facilities: our East Dubuque Facility and our Pasadena Facility. Our East Dubuque Facility produces primarily ammonia and urea ammonium nitrate solution, or UAN, using natural gas as the facility’s primary feedstock. Our Pasadena Facility produces ammonium sulfate, ammonium thiosulfate and sulfuric acid, using ammonia and sulfur as the facility’s primary feedstock.

On February 17, 2015, we announced that our general partner’s board has initiated a process to explore and evaluate potential strategic alternatives for the Partnership, which may include a sale of the Partnership, a merger with another party, a sale of some or all of our assets, or another strategic transaction. There can be no assurance that this strategic review process will result in a transaction.

Our East Dubuque Facility is located in the center of the Mid Corn Belt, the largest market in the United States for direct application of nitrogen fertilizer products. The Mid Corn Belt includes the States of Illinois, Indiana, Iowa, Missouri, Nebraska and Ohio. The States of Illinois and Iowa have been the top two corn producing states in the United States for the last 20 years according to the United States Department of Agriculture, or USDA. We consider the market for our East Dubuque Facility to be comprised of the States of Illinois, Iowa and Wisconsin.

Our East Dubuque Facility’s core market consists of the area located within an estimated 200-mile radius of the facility. In most instances, our customers take delivery of our nitrogen products at our East Dubuque Facility and then arrange and pay to transport them to their final destinations by truck. To the extent our products are picked up at our East Dubuque Facility, we do not incur any shipping costs, in contrast to nitrogen fertilizer producers located outside of the facility’s core market that must incur transportation and storage costs to transport their products to, and sell their products in, our market. In addition, our East Dubuque Facility does not maintain a fleet of trucks and, unlike some of our major competitors, our East Dubuque Facility does not maintain a fleet of rail cars because the facility’s customers generally are located close to the facility and prefer to be responsible for transportation. Having no need to maintain a fleet of trucks or rail cars lowers our East Dubuque Facility’s fixed costs. The combination of our East Dubuque Facility’s proximity to its customers and our storage capacity at the facility also allows for better timing of the pick-up and application of the facility’s products, as nitrogen fertilizer product shipments from more distant locations have a greater risk of missing the short periods of favorable weather conditions during which the application of nitrogen fertilizer may occur.

Our Pasadena Facility is the largest producer of synthetic ammonium sulfate and the third largest producer of ammonium sulfate in North America. We believe that our ammonium sulfate has several characteristics that distinguish it from competing products. In general, the ammonium sulfate that is available for sale in our industry is a byproduct of other processes and does not have certain characteristics valued by customers. Our ammonium sulfate is sized to the specifications preferred by customers and may more easily be blended with other fertilizer products. We also believe that our ammonium sulfate has a longer shelf-life, is more stable and is more easily transported and stored than many competing products.

Our Pasadena Facility is located on the Houston Ship Channel with access to transportation at favorable prices. The facility has two deep-water docks and access to the Mississippi waterway system and key international waterways. The facility is also connected to key domestic railways, which permit the efficient, cost-effective distribution of its products west of the Mississippi River. Our Pasadena Facility’s distributors purchase our products at our facility and then arrange and pay to transport them to their final destinations by truck, rail car or vessel. Our Pasadena Facility’s products are sold primarily through distributors to customers in the United States, and are applied to many types of crops including soybeans, potatoes, cotton, canola, alfalfa, corn and wheat.

Our Pasadena Facility purchases ammonia as a feedstock at contractual prices based on the monthly Tampa Index market, while our East Dubuque Facility sells ammonia at prevailing prices in the Mid Corn Belt region. Ammonia prices are typically significantly higher in the Mid Corn Belt than in Tampa.

Overview of Certain Significant Events that Occurred during 2014

During 2014, we (i) completed the urea expansion project at our East Dubuque Facility; (ii) substantially completed the power generation project and completed the sulfuric acid converter project at our Pasadena Facility; (iii) wrote off the remaining $27.2 million of goodwill relating to the acquisition of Agrifos LLC, or the Agrifos Acquisition; and (iv) reached an agreement with the seller in the Agrifos Acquisition to settle all existing and future indemnity claims relating to the Agrifos Acquisition, which resulted in income to us of $5.6 million.

4

Table of Contents

Several negative factors affected our operating results in 2014. Sales volumes were lower than we had expected due to both unplanned downtime at our East Dubuque Facility and a decision to reduce output and sales from our Pasadena Facility in order to improve the profitability of that facility. As discussed above, we also wrote down all of the remaining goodwill at our Pasadena Facility as a result of the continued outlook for profits to be lower than we had foreseen at the time of the Agrifos Acquisition.

We seek to continue to organically expand capacity at our fertilizer facilities, although any such expansion projects are likely to be smaller than the ongoing or recently-completed capacity expansions at each facility. We expect any expansion project to require new capital as we do not expect to use our operating cash flow to invest in any new growth projects. Expansion projects involve numerous risks and uncertainties, and there can be no assurance that we will be able to complete any expansion projects on a timely basis or at all.

Organizational Structure

The following diagram depicts our organizational structure as of February 27, 2015 (all percentage ownership interests are 100% unless otherwise noted):

Business

Our East Dubuque Facility

Our East Dubuque Facility is located on 210 acres in the northwest corner of Illinois on a 140-foot bluff above the Upper Mississippi River. Our East Dubuque Facility produces ammonia, urea ammonium nitrate solution, or UAN, liquid and granular urea, nitric acid and food-grade carbon dioxide, or CO2, using natural gas as its primary feedstock. We sell such products to customers located in the Mid Corn Belt region of the United States, the largest market in the United States for direct application of nitrogen fertilizer products. Our East Dubuque Facility operates continuously, except for planned shutdowns for maintenance and efficiency improvements, and unplanned shutdowns. Our East Dubuque Facility can optimize its product mix according to changes in demand and pricing for its various products. Some of these products are final products sold to customers, and others, including ammonia, are both final products and feedstocks for other products, such as UAN, nitric acid, liquid urea and granular urea.

5

Table of Contents

The following table sets forth our East Dubuque Facility’s current rated production capacity for the listed products in tons per day and tons per year, and its product storage capacity.

| Product |

Approximate Production Capacity | Product Storage Capacity | ||||||||

| Tons /Day | Tons /Year(1) | |||||||||

| Ammonia |

1,025 | 374,125 | 60,000 tons (3 tanks); 15,000 tons(2) | |||||||

| UAN |

1,100 | 401,500 | 80,000 tons (2 tanks) | |||||||

| Urea (liquid) |

484 | 176,660 | Limited capacity is not a factor | |||||||

| Urea (granular) |

140 | 51,100 | 12,000 granular ton warehouse | |||||||

| Nitric acid |

380 | 138,700 | Limited capacity is not a factor | |||||||

| CO2 |

350 | 127,750 | 1,900 tons | |||||||

| (1) | Production capacity for the year is based on daily rated production capacity times 365 days. The number of actual operating days will vary from year to year. |

| (2) | Represents 15,000 tons of storage capacity at the terminal of Agrium U.S.A., Inc., or Agrium, in Niota, Illinois where we have the right to store ammonia pursuant to our distribution agreement with Agrium. Our right to store ammonia at this terminal expires on June 30, 2016, but automatically renews for successive one year periods, unless we deliver a termination notice to Agrium with respect to such storage rights at least three months prior to an automatic renewal. Notwithstanding the foregoing, our right to use the storage space immediately terminates if the distribution agreement terminates in accordance with its terms. See “—Marketing and Distribution.” |

The following table sets forth the amount of products produced by, and shipped from, the East Dubuque Facility for the years ended December 31, 2014, 2013 and 2012:

| For the Years Ended December 31, |

||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| (in thousands of tons) | ||||||||||||

| Products Produced |

||||||||||||

| Ammonia(1) |

324 | 244 | 293 | |||||||||

| UAN |

269 | 262 | 301 | |||||||||

| Urea (liquid) |

150 | 137 | 139 | |||||||||

| Urea (granular) |

25 | 22 | 23 | |||||||||

| Nitric acid |

105 | 106 | 122 | |||||||||

| CO2 |

82 | 69 | 76 | |||||||||

| Products Shipped |

||||||||||||

| Ammonia |

153 | 103 | 149 | |||||||||

| UAN |

267 | 269 | 291 | |||||||||

| Urea (liquid) |

30 | 21 | 13 | |||||||||

| Urea (granular) |

25 | 22 | 22 | |||||||||

| Nitric acid |

11 | 14 | 14 | |||||||||

| CO2 |

81 | 71 | 76 | |||||||||

| (1) | Ammonia is used in the production of all other products produced by our East Dubuque Facility, except CO2. |

Expansion Projects

In 2014, we completed the urea expansion project at our East Dubuque Facility. As part of the project, we installed an additional CO2 compressor, which increased liquid urea production capacity at our East Dubuque Facility from 460 tons per day to 484 tons per day, or from 167,900 tons annually to 176,660 tons annually. We spent $3.2 million on this project.

We are regularly evaluating or pursuing opportunities to increase our profitability by expanding the East Dubuque Facility’s production capabilities and product offerings, including with the following expansion projects:

| • | Nitric Acid Expansion Project. In 2014, we commenced the replacement of a compressor train in one of our nitric acid plants at our East Dubuque Facility. This project is expected to increase nitric acid production at the facility by 30 tons per day or 11,000 tons annually, and decrease electric power usage. We expect to complete this project during the second quarter of 2015 at a cost of $7.0 million. This project will be funded initially with borrowings under the credit agreement we entered into in July 2014 with General Electric Capital Corporation, or the GE Credit Agreement. |

| • | Ammonia Synthesis Converter Project. We plan to replace the ammonia synthesis converter at our East Dubuque Facility, which is expected to increase reliability, production and plant efficiency. The project is expected to cost approximately $30.0 million and to be completed by the end of 2016. This project will be funded initially with borrowings under the GE Credit Agreement. |

6

Table of Contents

Products

Our East Dubuque Facility’s product sales are heavily weighted toward sales of ammonia and UAN, which together made up 80% or more of our East Dubuque Facility’s total revenues for the years ended December 31, 2014, 2013 and 2012. A majority of our East Dubuque Facility’s products are sold through our distribution agreement with Agrium as described below under “—Marketing and Distribution,” with the exception of CO2, which we sell directly to customers in the food and beverage market at negotiated contract prices. Ammonia and UAN are each sources of nitrogen, but each has its own characteristics, and customers’ preferences for each product vary according to the crop planted, soil and weather conditions, regional farming practices, relative prices and the cost and availability of storage, transportation, handling and application equipment. During the years ended December 31, 2014, 2013 and 2012, we sold more than 90% of our East Dubuque Facility’s nitrogen products to customers for agricultural application, with the remaining portion sold to customers for industrial uses.

Ammonia. Our East Dubuque Facility produces ammonia, the simplest form of nitrogen fertilizer and the feedstock for the production of other nitrogen fertilizers. The ammonia processing unit at our East Dubuque Facility has a current rated capacity of 1,025 tons per day. Our East Dubuque Facility’s ammonia product storage consists of three 20,000 ton tanks and 15,000 tons of leased storage in Niota, Illinois.

UAN. UAN is a liquid fertilizer that has a slight ammonia odor but, unlike ammonia, it does not need to be refrigerated or pressurized when transported or stored. Our East Dubuque Facility has two UAN storage tanks with a combined capacity of 80,000 tons.

Urea. Our East Dubuque Facility’s urea solution is (i) sold in its liquid state, (ii) processed into granular urea through the facility’s urea granulation plant to create dry granular urea, (iii) upgraded into UAN or (iv) upgraded into diesel exhaust fluid, or DEF. We assess market demand for each of these four end products and allocate our East Dubuque Facility’s urea solution as appropriate. We sell liquid urea, including DEF, primarily to industrial customers in the power, ethanol and diesel emissions markets. DEF is a urea-based chemical reactant that is intended to reduce nitrogen oxide emissions in the exhaust systems of certain diesel engines of trucks and off-road farm and construction equipment. Although we believe that there is high demand for our granular urea in agricultural markets, we sell it primarily to customers in specialty urea markets where the spherical shape and consistent size of the granules produced by our curtain granulation technology generally command a premium price. Our East Dubuque Facility has a 12,000 ton capacity bulk warehouse that can be used for storage of dry bulk granular urea.

Nitric Acid. Our East Dubuque Facility produces nitric acid through two separate nitric acid plants at the facility. Nitric acid is either sold to third parties or used within the facility for the production of ammonium nitrate solution, as an intermediate from which UAN is produced. We believe that our East Dubuque Facility currently has sufficient storage capacity available for the nitric acid produced at the facility.

CO2. CO2 is a gaseous product that is co-manufactured with ammonia, with 1.1 tons of CO2 produced per ton of ammonia produced. Our East Dubuque Facility utilizes CO2 in its urea production and has developed a market for CO2 through purification to a food grade liquid CO2. Our East Dubuque Facility has storage capacity for 1,900 tons of CO2. We have multiple CO2 sales agreements that allow for regular shipment of CO2 throughout the year, and our current storage capacity is sufficient to support our CO2 delivery commitments.

Marketing and Distribution

In 2006, we entered into a distribution agreement with Agrium under which a majority of our East Dubuque Facility’s products, including ammonia and UAN, are sold. Pursuant to the distribution agreement, Agrium is obligated to use commercially reasonable efforts to promote the sale of, and to solicit and secure orders from its customers for, ammonia, liquid and granular urea, UAN and nitric acid. Under the distribution agreement, Agrium bears the credit risk on products sold through Agrium pursuant to the agreement. The distribution agreement has a term that ends in April 2016, but automatically renews for subsequent one-year periods, unless either party delivers a termination notice to the other party at least three months prior to an automatic renewal.

7

Table of Contents

During the years ended December 31, 2014, 2013 and 2012, 78% or more of our East Dubuque Facility product sales were through Agrium pursuant to the distribution agreement, and the remainder sold directly to other customers. Our management approves price, quantity and other terms for each sale through Agrium, and we pay Agrium a commission for its services. Our rights under the distribution agreement include the right to store specified amounts of our ammonia for a monthly fee at Agrium’s ammonia terminal in Niota, Illinois, which serves as a distribution point where ammonia produced at our East Dubuque Facility is sold. Our right to store ammonia at Agrium’s terminal expires on June 30, 2016, but automatically renews for successive one year periods, unless we deliver a termination notice to Agrium with respect to such storage rights at least three months prior to an automatic renewal. Notwithstanding the foregoing, our right to use the storage space immediately terminates if the distribution agreement terminates in accordance with its terms. Outside of the distribution agreement, we also sell our East Dubuque Facility’s nitrogen products and CO2 directly to our customers.

Under the distribution agreement, we pay commissions to Agrium on applicable gross sales during the first 10 years of the agreement, not to exceed $5 million during each contract year. The commission rate is 5%. The effective commission rate associated with sales under the distribution agreement was 3.4% for the year ended December 31, 2014, 3.6% for the year ended December 31, 2013 and 2.7% for the year ended December 31, 2012.

Customers

We sell a majority of our East Dubuque Facility’s nitrogen products to customers located in the facility’s core market, which is the area located within an estimated 200-mile radius of the facility. Given the nature of our business, and consistent with industry practice, we generally do not have long-term minimum sales contracts for fertilizer products with any of our customers. The following table shows for the periods presented the percentage of our sales of products to our top five customers and sales to certain specific customers:

| For the Years Ended December 31, |

||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| Sales of Products to Top 5 Customers |

||||||||||||

| Ammonia, as a % of total ammonia sales |

62 | % | 57 | % | 54 | % | ||||||

| UAN, as a % of total UAN sales |

58 | % | 59 | % | 38 | % | ||||||

| Sales to Customers, as a % of total sales |

||||||||||||

| Agrium (as a direct customer) |

— | 2 | % | 2 | % | |||||||

| Crop Production Services, Inc., or CPS |

12 | % | 12 | % | 9 | % | ||||||

Seasonality and Volatility

Ammonia, UAN and other nitrogen based fertilizer sales are seasonal, based upon planting, growing and harvesting cycles, and product availability. Inventories are accumulated to allow for shipments to customers during the spring and fall fertilizer application seasons, which require significant storage capacity. The accumulation of inventory to be available for seasonal sales creates significant seasonal working capital requirements. This seasonality generally results in higher fertilizer prices during peak fertilizer application periods, with prices normally reaching their highest point in the spring, decreasing in the summer, and increasing again in the fall. Our East Dubuque Facility’s products are sold both on the spot market for immediate delivery and under prepaid contracts for future delivery of products at fixed prices. The terms of the prepaid contracts, including the percentage of the purchase price paid as a down payment, can vary from season to season. Variations in the proportion of product sold through forward sales contracts and variations in the terms of such contracts can increase the seasonal volatility of our cash flows and cause changes in the patterns of seasonal volatility from year-to-year. The cash from prepaid contracts is included in our operating cash flow in the quarter in which the cash is received, while revenue and cost of sales related to prepaid contracts are recognized when products are picked up or delivered and the customer takes title. As a result, the timing of cash received under prepaid contracts may be very different from the timing of recognition of income and expense under those same contracts; significant amounts of profit may be related to cash collected in earlier periods and recorded profits may not be accompanied by a corresponding collection of cash in a particular reporting period. See “Part II—Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Another seasonal factor affecting our industry is the effect of weather-related conditions on the ability to transport products by barge on the Upper Mississippi River. During certain times of the winter, the Upper Mississippi River cannot be used for transport due to lock closures, which could preclude the transportation of nitrogen products by barge during this period and may increase transportation costs. The following table sets forth the percentage of ammonia and UAN tonnage sold that was transported from our East Dubuque Facility by barge:

| For the Years Ended December 31, |

||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| Ammonia |

— | 4.8 | % | 5.6 | % | |||||||

| UAN |

4.5 | % | — | 1.7 | % | |||||||

8

Table of Contents

The following table shows total tons of our East Dubuque Facility’s products shipped for each quarter presented below:

| For the Years Ended December 31, |

||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| (in thousands of tons) | ||||||||||||

| Ammonia |

||||||||||||

| Quarter ended March 31 |

7 | 11 | 30 | |||||||||

| Quarter ended June 30 |

72 | 41 | 40 | |||||||||

| Quarter ended September 30 |

27 | 24 | 31 | |||||||||

| Quarter ended December 31 |

47 | 27 | 48 | |||||||||

| UAN |

||||||||||||

| Quarter ended March 31 |

49 | 61 | 34 | |||||||||

| Quarter ended June 30 |

82 | 59 | 92 | |||||||||

| Quarter ended September 30 |

83 | 117 | 110 | |||||||||

| Quarter ended December 31 |

53 | 32 | 55 | |||||||||

| Other Nitrogen Products |

||||||||||||

| Quarter ended March 31 |

16 | 15 | 13 | |||||||||

| Quarter ended June 30 |

17 | 20 | 13 | |||||||||

| Quarter ended September 30 |

16 | 14 | 14 | |||||||||

| Quarter ended December 31 |

17 | 8 | 9 | |||||||||

| CO2 |

||||||||||||

| Quarter ended March 31 |

20 | 23 | 15 | |||||||||

| Quarter ended June 30 |

22 | 24 | 15 | |||||||||

| Quarter ended September 30 |

19 | 21 | 25 | |||||||||

| Quarter ended December 31 |

20 | 3 | 21 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total Tons Shipped |

567 | 500 | 565 | |||||||||

|

|

|

|

|

|

|

|||||||

We typically ship the highest volume of tons from our East Dubuque Facility during the spring planting season, which occurs during the quarter ending June 30 of each year. The next highest volume of tons shipped is typically after the fall harvest during the quarter ending December 31 of each year. However, as reflected in the table above, the seasonal patterns may change substantially from year to year due to various circumstances, including timing of or changes in weather. These seasonal increases and decreases in demand also can cause fluctuations in sales prices. In winter seasons with warmer weather, early planting may shift significant ammonia sales into the quarter ending March 31. Wet or cold weather during the normal spring application season can delay deliveries that would normally occur in the spring. Weather conditions can also affect the mix of demand for our products at various times in the year. Certain weather and soil conditions favor the application of ammonia, while other conditions favor the application of UAN solution.

Raw Materials

The principal raw material used to produce nitrogen fertilizer products at our East Dubuque Facility is natural gas. We have historically purchased natural gas in the spot market, through the use of forward purchase contracts, or a combination of both. We use forward purchase contracts to lock in pricing for a portion of our East Dubuque Facility’s natural gas requirements. These forward purchase contracts are generally either fixed-price or index-price, short term in nature and for a fixed supply quantity. Our general policy is to purchase enough natural gas under fixed-price forward contracts to manufacture the products that have been sold under prepaid contracts for future delivery, effectively fixing a substantial portion of the gross margin on pre-sold product. We sometimes also purchase or fix prices on natural gas in excess of those requirements, when we believe that gas prices are attractive enough to lock in even without matching product pre-sales. We are able to purchase natural gas at competitive prices due to our East Dubuque Facility’s connection to the Northern Natural Gas interstate pipeline system, which is within one mile of the facility, and the facility’s connection to the ANR Pipeline Company, or ANR, pipeline. The pipelines are connected to Nicor Inc.’s, or Nicor’s, distribution system at the Chicago Citygate receipt point and at the Hampshire interconnect, respectively, from which natural gas is transported to the facility. Though we do not typically purchase natural gas for the purpose of resale, we occasionally sell natural gas when purchase commitments exceed production requirements and/or storage capacities, or

9

Table of Contents

when the margin from selling natural gas significantly exceeds the margin from producing additional ammonia. The East Dubuque Facility’s receipt point locations and access to the Chicago Citygate receipt point has allowed us to obtain relatively favorable natural gas prices for sales of our excess natural gas due to our proximity to the stable residential demand for the commodity in Chicago, Illinois. The following table shows the natural gas purchased and used in production:

| For the Years Ended December 31, |

||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| Volume (MMBtu, or million British thermal units) |

11,487,000 | 8,942,000 | 10,644,000 | |||||||||

We plan to continue to operate our East Dubuque Facility with natural gas as its primary feedstock. Competitors may have access to cheaper natural gas or other feedstocks that could provide them with a cost advantage. Depending on its magnitude, the amount of this cost advantage could offset our savings on transportation and storage costs as a result of our East Dubuque Facility’s location. The following table shows the average prices for natural gas in our cost of sales for the periods presented:

| For the Years Ended December 31, |

||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| Cost of natural gas ($ per MMBtu) |

$ | 5.00 | $ | 4.16 | $ | 3.59 | ||||||

Changes in the levels of natural gas prices and market prices of nitrogen-based products can materially affect our financial position and results of operations. Natural gas prices in the United States have experienced significant fluctuations over the last several years, increasing substantially in 2008 and subsequently declining to the current lower levels. Several recent discoveries of large natural gas deposits in North America, combined with advances in technology for natural gas production have caused large increases in the estimates of available natural gas reserves and production in the United States, contributing to significant reductions in the market price of natural gas.

In 2014, we entered into fixed-quantity forward purchase contracts at fixed and indexed prices for various delivery dates through June 30, 2015. As of December 31, 2014, the total MMBtus associated with these forward purchase contracts are 3.7 million and the total amount of the purchase commitments are $15.6 million, resulting in a weighted average rate per MMBtu of $4.18 in these commitments. During January and February 2015, we entered into additional fixed-quantity forward purchase contracts at fixed and indexed prices for various delivery dates through December 31, 2015. The total MMBtus associated with these additional forward purchase contracts are 2.7 million and the total amount of the purchase commitments is $7.7 million, resulting in a weighted average rate per MMBtu of $2.88 in these new commitments.

Transportation

In most instances, our East Dubuque Facility’s customers take delivery of nitrogen products at the facility, and then arrange and pay to transport the products to their final destinations by truck. Similarly, under the distribution agreement, neither we nor Agrium is responsible for transportation, and customers that purchase our East Dubuque Facility’s products through Agrium also take delivery of such products at the facility. When products are purchased for delivery at the facility, the customer is responsible for all costs of, and bears all risks associated with, the transportation of products from the facility.

In certain instances, customers take delivery of products at the final destination. In these circumstances, we are responsible for the associated transportation costs. In order to accommodate barge and rail deliveries, we own and operate a barge dock on the Mississippi River, and a rail spur that connects to the Burlington Northern Santa Fe Railway and the Canadian National Railway Company, or Canadian National. We also ship products by barge to our leased storage facility in Niota, Illinois, which provides another distribution point from which our customers may pick up our East Dubuque Facility’s products by truck.

Competition

Our East Dubuque Facility competes with a number of domestic and foreign producers of nitrogen fertilizer products, many of which are larger than us and have significantly greater financial and other resources than we do.

We believe that customers for nitrogen fertilizer products make purchasing decisions principally on the delivered price and availability of the product at the critical application times. Our East Dubuque Facility’s proximity to its customers provides us with a

10

Table of Contents

competitive advantage over producers located further away from those customers. The nitrogen fertilizer facilities closest to our East Dubuque Facility are located about 190 miles away in Fort Dodge, Iowa; 275 miles away in Creston, Iowa; 300 miles away in Port Neal, Iowa; and 350 miles away in Lima, Ohio. Our East Dubuque Facility’s physical location in the center of the Mid Corn Belt provides the facility with a transportation cost advantage compared to other producers who must ship their products over greater distances to our East Dubuque Facility’s market area. The combination of our East Dubuque Facility’s proximity to its customers and our storage capacity at the facility allows customers to better time the pick-up and application of our products, as deliveries from more distant locations have a greater risk of missing the short periods of favorable weather conditions during which the application of nitrogen fertilizer and planting may occur. However, other producers of nitrogen fertilizer products are constructing or contemplating the construction of new nitrogen fertilizer facilities in North America, including in the Mid Corn Belt. For example, Orascom Construction Industries Company, or OCI, an Egyptian producer of fertilizer products, has announced that a wholly owned subsidiary of OCI is constructing a facility located 165 miles away from our East Dubuque Facility that is designed to produce between 1.5 to 2.0 million metric tons per year of ammonia, urea, UAN and DEF and that it expects the facility to be operational in late 2015. If a new nitrogen fertilizer facility is completed in our East Dubuque Facility’s core market, it could benefit from the same competitive advantage associated with the location of our East Dubuque Facility. The completion of such a facility could have a material adverse effect on our results of operations, financial condition and ability to make cash distributions to our unitholders.

Our Pasadena Facility

On November 1, 2012, we completed our acquisition of 100% of the membership interests of Agrifos LLC, or Agrifos, from Agrifos Holdings Inc., or the Seller, pursuant to a Membership Interest Purchase Agreement, or the Purchase Agreement. Upon the closing of this transaction, or the Agrifos Acquisition, Agrifos became our wholly owned subsidiary and its name changed to Rentech Nitrogen Pasadena Holdings, LLC. Rentech Nitrogen Pasadena Holdings, LLC owns all of the member interests in RNPLLC, which owns and operates the Pasadena Facility.

Our Pasadena Facility is located on an 85 acre site located on the Houston Ship Channel which includes 2,700 linear feet of water frontage and two deep-water docks. The property also includes 415 acres of land, which contains phosphogypsum stacks. In early 2011 prior to our ownership, the Pasadena Facility ceased production of diammonium phosphate and monoammonium phosphate. Agrifos undertook major capital and maintenance projects at the Pasadena Facility, including decommissioning certain phosphate production assets, and converting a portion of the Pasadena Facility’s assets to the production of ammonium sulfate fertilizer. Ammonium sulfate is now the primary product of the Pasadena Facility. Following the conversion, the Pasadena Facility continues to produce sulfuric acid and ammonium thiosulfate.

Our Pasadena Facility is the largest producer of synthetic ammonium sulfate and the third largest producer of ammonium sulfate in North America. We believe that our ammonium sulfate has several characteristics that distinguish it from competing products. In general, the ammonium sulfate that is available for sale in our industry is a byproduct of other processes and does not have certain characteristics valued by customers. Our ammonium sulfate is sized to the specifications preferred by customers and may more easily be blended with other fertilizer products. We also believe that our ammonium sulfate has a longer shelf-life, is more stable and is more easily transported and stored than many other competing products.

In late 2014, we restructured operations at our Pasadena Facility. As part of the restructuring, our Pasadena Facility reduced expected annual production of ammonium sulfate by approximately 25 percent, to 500,000 tons. We intend to sell approximately 70 percent of the 500,000 tons in the domestic market and the remaining tons in New Zealand and Australia, which are the international markets with the highest net prices for ammonium sulfate. Our sales plan eliminates historically low-margin sales to Brazil, other than modest amounts expected during peak seasons when higher margins may be achievable. Our restructuring plan provides us the flexibility to increase ammonium sulfate production above the 500,000 ton rate, if market conditions are favorable.

We are evaluating opportunities to build terminalling assets on the site of our Pasadena Facility. We do not expect to invest significant amounts of our own capital in such assets, but expect to work with a joint venture partner on any such development.

The following table sets forth our Pasadena Facility’s current rated production capacity for the listed products in tons per day and tons per year, and our product storage capacity.

| Approximate Production Capacity | ||||||||||||

| Product |

Tons /Day | Tons /Year(1) | Product Storage Capacity | |||||||||

| Ammonium sulfate |

2,100 | 693,000 | 60,000 tons | |||||||||

| Sulfuric acid |

1,750 | 638,750 | 27,000 tons | |||||||||

| Ammonium thiosulfate |

220 | 80,300 | 14,000 tons | |||||||||

| (1) | Ammonium sulfate production capacity for the year is based on daily rated production capacity times 330 days given regular required cleanings of the granulator. Actual production, based on the restructuring plan, is expected to be 500,000 tons per year. Sulfuric acid and ammonium thiosulfate production capacities for the year are based on daily rated production capacity times 365 days. The number of actual operating days will vary from year to year. |

11

Table of Contents

The following table sets forth the amount of products produced by, and shipped from, our Pasadena Facility for the years ended December 31, 2014 and 2013 and the period beginning November 1, 2012 (the closing date of the Agrifos Acquisition) through December 31, 2012:

| For the Years Ended December 31, |

For the Period November 1, 2012 Through December 31, |

|||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| (in thousands of tons) | ||||||||||||

| Products Produced |

||||||||||||

| Ammonium sulfate |

522 | 465 | 88 | |||||||||

| Sulfuric acid(1) |

447 | 478 | 69 | |||||||||

| Ammonium thiosulfate |

63 | 60 | 9 | |||||||||

| Products Shipped |

||||||||||||

| Ammonium sulfate |

572 | 428 | 115 | |||||||||

| Sulfuric acid |

112 | 148 | 27 | |||||||||

| Ammonium thiosulfate |

67 | 54 | — | |||||||||

| (1) | Our Pasadena Facility produces sulfuric acid primarily for the production of ammonium sulfate. |

Expansion Projects and Other Significant Capital Projects

In 2014, we substantially completed the power generation project and completed the sulfuric acid converter project at our Pasadena Facility. In the power generation project, we installed a steam turbine/generator set that uses excess steam produced from the sulfuric acid plant at the facility to produce electrical power. We expect that a portion of the power will be used in our Pasadena Facility, reducing electricity expenses, and the remaining power will be sold in the deregulated Texas power market, creating an additional revenue stream. We spent $30.8 million on this project through December 31, 2014. We replaced the sulfuric acid converter for a cost of $16.7 million.

Products

Our Pasadena Facility’s products are applied to many types of crops including soybeans, potatoes, cotton, canola, alfalfa, corn and wheat. Our Pasadena Facility’s product sales are heavily weighted toward sales of ammonium sulfate, which made up 80% or more of our Pasadena Facility’s total revenues for the years ended December 31, 2014 and 2013. Our Pasadena Facility’s products are sold primarily through distribution agreements as described below under “—Marketing and Distribution.”

Ammonium Sulfate. Ammonium sulfate is a solid dual-nutrient fertilizer produced by combining ammonia and sulfuric acid. The sulfur derived from ammonium sulfate is the form of sulfur most available as a nutrient for crops. Our Pasadena Facility produces ammonium sulfate that is sized to the specifications of other nitrogen, phosphate and potash fertilizer products which results in less segregation in blended products. The ammonium sulfate plant at our Pasadena Facility has a current rated capacity of 2,100 tons per day. Our Pasadena Facility has storage capacity for 60,000 tons of ammonium sulfate. In addition, we have an arrangement with Interoceanic Corporation, or IOC, that permits us to store approximately 60,000 tons of ammonium sulfate at IOC-controlled terminals, which are located near end customers of our Pasadena Facility’s ammonium sulfate.

Sulfuric Acid. Sulfuric acid not used for production of ammonium sulfate is sold to third parties. The majority of the sulfuric acid sold by our Pasadena Facility is sold through a distributor to industrial consumers. Our Pasadena Facility has storage capacity for 27,000 tons of sulfuric acid.

Ammonium Thiosulfate. Ammonium thiosulfate is a liquid fertilizer. Ammonium thiosulfate typically is combined with UAN to help increase the efficiency of nitrogen in crops. Our Pasadena Facility has storage capacity for 14,000 tons of ammonium thiosulfate.

12

Table of Contents

Marketing and Distribution

We sell substantially all of our Pasadena Facility’s products through marketing and distribution agreements. Pursuant to an exclusive marketing agreement we have entered into with IOC, IOC has the exclusive right and obligation to market and sell all of our Pasadena Facility’s ammonium sulfate product. Under the marketing agreement, IOC is required to use commercially reasonable efforts to market the product to obtain the most advantageous price. We compensate IOC for transportation and storage costs relating to the ammonium sulfate product it markets through the pricing structure under the marketing agreement. The marketing agreement has a term that ends December 31, 2016, but automatically renews for subsequent one-year periods (unless either party delivers a termination notice to the other party at least 210 days prior to an automatic renewal). The marketing agreement may be terminated prior to its stated term for specified causes. During the years ended December 31, 2014 and 2013, the marketing agreement with IOC accounted for all of our Pasadena Facility’s ammonium sulfate revenues. The ammonium sulfate storage arrangement with IOC currently is not governed by a written contract. We also have marketing and distribution agreements to sell other products that automatically renew for successive one year periods.

Customers

We sell substantially all of the products from our Pasadena Facility to IOC and our other distributors, and we do not have direct contact with our distributors’ customers. Our distributors sell a majority of our Pasadena Facility’s products to customers located west of the Mississippi River. Through our distributors, we sold all of our Pasadena Facility’s nitrogen products to customers for agricultural uses during the years ended December 31, 2014 and 2013 . Given the nature of our business, and consistent with industry practice, we do not have direct sales contracts for fertilizer products with any of our end customers. The majority of the sulfuric acid our Pasadena Facility sells to its distributor is placed with industrial consumers.

Seasonality and Volatility

Significant seasonal weather factors have affected demand for and timing of deliveries for our Pasadena Facility’s domestic agricultural products. Domestic prices for ammonium sulfate and ammonium thiosulfate normally reach their highest point in the spring, decreasing in the summer, and increasing again in the fall. Sales prices of these products are adjusted seasonally in order to facilitate distribution of the products throughout the year. Sales to Australia, Brazil and New Zealand may partially offset this domestic seasonal pattern because they are in the southern hemisphere. We operate the ammonium sulfate plant at our Pasadena Facility throughout the year to the extent that there is available storage capacity for this product. We manage our storage capacity by distributing the product through IOC to customers in both domestic and offshore markets throughout the year. If storage capacity were to be insufficient, we would be forced to cease or reduce production of the product until storage capacity became available. Our Pasadena Facility’s ammonium sulfate product is delivered to IOC and sold at prevailing market prices. See “Part II—Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Because we sell sulfuric acid through a distributor to industrial consumers, demand for this product generally is constant during the year. Sales of industrial products, such as sulfuric acid, are generally not impacted by seasons and weather. We typically ship sulfuric acid from our Pasadena Facility each month of the year with the majority of the product sold under annual contracts.

Raw Materials

The principal raw materials used to produce nitrogen fertilizer products at our Pasadena Facility are ammonia and sulfur. We purchase ammonia for use at the facility from OCI Beaumont, LLC, or OCI Beaumont. OCI Beaumont operates an ammonia and methanol production facility on the Neches River in Nederland, Texas just outside of Beaumont, Texas. Ammonia pricing is based on a published Tampa, Florida market index that is set on a quarterly basis through negotiations between large industry producers and consumers, or the Tampa Index. The Tampa Index is commonly used in annual contracts for both the agricultural and industrial sectors, and is based on the most recent major industry transactions in the Tampa market. Pricing considerations for ammonia incorporate international supply-demand, ocean freight and production factors. An 1,800 short ton ammonia barge delivers ammonia from Beaumont, Texas to our Pasadena Facility, pursuant to a long term lease we entered into with Port Arthur Towing Company. Ammonia purchased and used in production at our Pasadena Facility was 155,000 tons in the year ended December 31, 2014 and 128,000 tons in the year ended December 31, 2013.

We obtain sulfur for our Pasadena Facility primarily by truck from local refineries in the Houston area and, to a lesser extent, by rail car. Major suppliers of sulfur to our Pasadena Facility include refiners, such as Phillips 66 Company, Shell Oil Products U.S. and Valero Energy Corporation. Our contracts with these refiners generally have a term of one year. Once pricing for the first quarter of a year is negotiated, the price then fluctuates up or down each subsequent quarter based on changes to the Tampa Index. Sulfur purchased and used in production at our Pasadena Facility was 194,000 tons in the year ended December 31, 2014 and 172,000 tons in the year ended December 31, 2013.

13

Table of Contents

Transportation

Our Pasadena Facility is located on the Houston Ship Channel with access to various modes of transportation at favorable prices. The facility has two deep-water docks and access to the Mississippi waterway system and key international waterways. The docks at the facility are suitable for loading and unloading bulk or liquid barges with payloads of up to 35,000 tons. The facility is also connected to key domestic railways which permit the efficient, cost-effective distribution of its products west of the Mississippi River. We believe this provides a significant cost advantage relative to producers located on the East Coast that are forced to switch railways when shipping product to this region. Our location on the Houston Ship Channel allows our distributors or us to use low cost barge and vessel transport when selling products and purchasing feedstocks.

Competition

Our Pasadena Facility competes with a number of domestic and foreign producers of nitrogen fertilizer products, many of which are larger than we are and have significantly greater financial and other resources than we do. We believe that customers who purchase the product make purchasing decisions based, in part, on the product’s size and shelf life. The majority of ammonium sulfate produced in North America and globally is generated as a byproduct of another process. We believe that our ammonium sulfate (which we refer to as synthetic ammonium sulfate) is made specifically for fertilizer, is sized to the specifications preferred by customers, is more easily blended with other fertilizer products and is better suited for use in agricultural application equipment. We also believe that our ammonium sulfate has a longer shelf-life, is more stable and is more easily transported and stored than many other competing products. Honeywell International Inc., or Honeywell, the largest producer of ammonium sulfate in the United States is located in Hopewell, Virginia, about 1,350 miles away from our Pasadena Facility. BASF AG, the second largest producer of ammonium sulfate, is located in Freeport, Texas, about 60 miles away from our Pasadena Facility. Our Pasadena Facility has access to transportation at favorable prices, such as low cost barge and vessel. We believe that our close proximity to sources of our primary feedstocks and access to low-cost transportation enables the facility to offer competitive pricing to customers adjacent to and west of the Mississippi River.

We also face competition from numerous regional producers of sulfuric acid, including E. I. du Pont de Nemours and Company located in El Paso and La Porte, Texas and Burnside, Louisiana, Eco Services located in Baytown and Houston, Texas and Chemtrade Logistics Inc., located in Beaumont, Texas.

Growth Plans

We seek to continue to organically expand capacity at our Fertilizer Facilities, although any such expansion projects are likely to be smaller than the ongoing or recently-completed capacity expansions at each facility. We expect any expansion project to require new capital as we do not expect to use our operating cash flow to invest in any new growth projects. Expansion projects involve numerous risks and uncertainties, and there can be no assurance that we will be able to complete any expansion projects on a timely basis or at all.

Environmental Matters

Our business is subject to extensive and frequently changing federal, state and local, environmental, health and safety regulations governing a wide range of matters, including the emission of air pollutants, the release of hazardous substances into the environment, the treatment and discharge of waste water and the storage, handling, use and transportation of our fertilizer products, raw materials, and other substances that are part of our operations. These laws include the Clean Air Act, or the CAA, the federal Water Pollution Control Act, or the Clean Water Act, the Resource Conservation and Recovery Act, or RCRA, the Comprehensive Environmental Response, Compensation and Liability Act, or CERCLA, the Toxic Substances Control Act, or the TSCA, and various other federal, state and local laws and regulations. These laws, their underlying regulatory requirements and the enforcement thereof impact us by imposing:

| • | restrictions on operations or the need to install enhanced or additional controls; |

| • | the need to obtain and comply with permits and authorizations; |

| • | liability for the investigation and remediation of contaminated soil and groundwater at current and former facilities (if any) and off-site waste disposal locations; and |

| • | specifications for the products we market. |

14

Table of Contents

These laws significantly affect our operating activities as well as the level of our operating costs and capital expenditures. Failure to comply with environmental laws, including the permits issued to us thereunder, generally could result in substantial fines, penalties or other sanctions, court orders to install pollution-control equipment, permit revocations and facility shutdowns. The following table shows capital expenditures related to environmental, health and safety at the East Dubuque Facility and the Pasadena Facility:

| For the Years Ended December 31, |

||||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| (in millions) | ||||||||||||

| East Dubuque Facility |

$ | 0.2 | $ | 0.2 | $ | 0.3 | ||||||

| Pasadena Facility |

0.2 | 0.3 | 1.0 | |||||||||

Our operations require numerous permits and authorizations. A decision by a governmental regulator to revoke or substantially modify an existing permit or authorization could have a material adverse effect on our ability to continue operations at the impacted facility. Expansion of our operations is predicated upon obtaining the necessary environmental permits and authorizations. We may experience delays in obtaining or be unable to obtain required permits, which may delay or interrupt our operations and limit our growth and revenue.

In addition, environmental, health and safety laws may impose joint and several liability, without regard to fault, for cleanup of a contaminated site on current owners and operators of the site, former owners and operators of the site at the time of the disposal of the hazardous substances, any person who arranges for the transportation, disposal or treatment of the hazardous substances, and the transporters who select the disposal and treatment facilities, regardless of the care exercised by such persons. Private parties, including the owners of properties adjacent to other facilities where our wastes are taken for disposal, also may have the right to pursue legal actions to enforce compliance as well as to seek damages for non-compliance with environmental laws and regulations or for personal injury or property or natural resource damages. In addition, the risk of accidental spills or releases could expose us to significant liabilities that could have a material adverse effect on our business, financial condition or results of operations.

The laws and regulations to which we are subject are complex, change frequently and have tended to become more stringent over time. The ultimate impact on our business of complying with existing laws and regulations is not always clearly known or determinable due in part to the fact that our operations may change over time and certain implementing regulations for laws, such as the CAA, have not yet been finalized, are under governmental or judicial review or are being revised. These laws and regulations could result in increased capital, operating and compliance costs.

Our facilities have experienced some level of regulatory scrutiny in the past, and we may be subject to further regulatory inspections, future requests for investigation or assertions of liability relating to environmental issues. In the future, we could incur material liabilities or costs related to environmental matters, and these environmental liabilities or costs (including fines or other sanctions) could have a material adverse effect on our results of operations, financial condition and ability to make cash distributions.

Certain environmental regulations and risks associated with our business are outlined below. We strive to maintain compliance with these regulations; however, they are complex and varied, and our operations are heavily regulated, and we may, from time to time, fall out of compliance. For example, the Pasadena Facility may not comply with wastewater and stormwater discharge requirements and solid and hazardous waste requirements. As another example, the Illinois Environmental Protection Agency, or the IEPA, alleged that an ammonia release at our East Dubuque Facility violated environmental laws, and we entered into a settlement agreement with the IEPA in August 2013 requiring us to connect a device at the facility to an ammonia safety flare by December 1, 2015.

The Federal Clean Air Act. The CAA and its implementing regulations, as well as the corresponding state laws and regulations that regulate emissions of pollutants into the air, impose permitting and emission control requirements relating to specific air pollutants, as well as the requirement to maintain a risk management program to help prevent accidental releases of certain substances. Standards promulgated pursuant to the CAA may require that we install controls at or make other changes to our facilities. If new controls or changes to operations are needed, the costs could be significant. In addition, failure to comply with the requirements of the CAA and its implementing regulations could result in substantial fines, civil or criminal penalties, or other sanctions.

The regulation of air emissions under the CAA requires that we obtain various construction and operating permits, including Title V air permits and incur capital expenditures for the installation of certain air pollution control devices at our facilities. Measures have been taken to comply with various regulations specific to our operations, such as National Emission Standard for Hazardous Air Pollutants, New Source Performance Standards and New Source Review. We have incurred, and expect to continue to incur, substantial capital expenditures to maintain compliance with these and other air emission regulations that have been promulgated or may be promulgated or revised in the future. As one example, we entered into a consent decree that required us to take action to achieve compliance with the emissions limits and other requirements applicable to our East Dubuque Facility.

15

Table of Contents

In July 2011, we voluntarily began operating what we believe is the first tertiary nitrous oxide, or N2O, catalytic converter in the United States on one of our nitric acid plants at our East Dubuque Facility. This converter is designed to convert approximately 90% of the N2O generated in our production of nitric acid into nitrogen and oxygen at that one plant. During the year ended December 31, 2014, 91%, or 331 metric tonnes, of N2O generated by that plant was converted into nitrogen and oxygen. In late December 2013, we installed a N2O abatement catalyst in the other nitric acid plant at our East Dubuque Facility. This catalyst is also designed to convert approximately 90% of the N2O generated in our production of nitric acid into nitrogen and oxygen. During the year ended December 31, 2014, 93%, or 340 metric tonnes, of N2O generated by that plant was converted into nitrogen and oxygen. We monitor and record the reduction in N2O emissions, which is verified by a third party. We have listed the credits on an active registry, such as the Climate Registry maintained by the Climate Action Reserve, and sell the credits for a profit. We have entered into a five-year agreement to supply emission reduction credits with sales totaling $0.5 million for the year ended December 31, 2014 and $0.1 million during each of the years ended December 31, 2013 and 2012.

Release Reporting. The release of hazardous substances or extremely hazardous substances into the environment is subject to release reporting requirements under federal and state environmental laws, including the Emergency Planning and Community Right-to-Know Act. We occasionally experience releases of hazardous or extremely hazardous substances from our operations or properties. We report such releases to the EPA, the IEPA, the Texas Commission on Environmental Quality, and other relevant federal, state and local agencies as required by applicable laws and regulations. If we fail to properly report a release, or if the release violates the law or our permits, it could cause us to become the subject of a governmental enforcement action or third-party claims. Government enforcement or third-party claims relating to releases of hazardous or extremely hazardous substances could result in significant expenditures and liability.

Clean Water Act. The Clean Water Act and analogous state laws impose restrictions and strict controls with respect to the discharge of pollutants, including spills and leaks of oil and other substances, into waters of the United States. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the EPA or an analogous state agency. The Clean Water Act and regulations implemented thereunder also prohibit the discharge of dredge and fill material into regulated waters, including wetlands, unless authorized by an appropriately issued permit. In addition, the Clean Water Act and analogous state laws require individual permits or coverage under general permits for discharges of storm water runoff from certain types of facilities. Spill prevention, control and countermeasure requirements of federal laws require appropriate containment berms and similar structures to help prevent the contamination of navigable waters by a petroleum hydrocarbon tank spill, rupture or leak. Federal and state regulatory agencies can impose administrative, civil and criminal penalties for non-compliance with discharge permits or other requirements of the Clean Water Act and analogous state laws and regulations.

Greenhouse Gas Emissions. Legislative and regulatory measures to address greenhouse gas, or GHG, emissions (including CO2, methane and N2O) are in various phases of discussion or implementation. At the federal legislative level, Congress has previously considered legislation requiring a mandatory reduction of GHG emissions. Although Congressional passage of such legislation does not appear imminent at this time, it could be adopted at a future date. It is also possible that Congress may pass alternative climate change bills that do not mandate a nationwide cap-and-trade program and instead focus on promoting renewable energy and energy efficiency or impose a carbon fee.

Management of Hazardous Substances and Contamination. Under CERCLA and related state laws, certain persons may be liable at sites where or from release or threatened release of hazardous substances has occurred or is threatened. These persons can include the current owner or operator of property where a release or threatened release occurred, any persons who owned or operated the property when the release occurred, and any persons who disposed of, or arranged for the transportation or disposal of, hazardous substances at a contaminated property. Liability under CERCLA is strict, retroactive and, under certain circumstances, joint and several, so that any responsible party may be held liable for the entire cost of investigating and remediating the release of hazardous substances. RCRA regulates the generation, treatment, storage, handling, transportation and disposal of solid waste and requires states to develop programs to ensure the safe disposal of solid waste. Under RCRA, persons may be liable at sites where the past or present storage, handling, treatment, transportation, or disposal of any solid or hazardous waste may present an imminent and substantial endangerment to health or the environment. These persons can include the current owner or operator of property where disposal occurred, any persons who owned or operated the property when the disposal occurred, and any persons who disposed of, or arranged for the transportation or disposal of, hazardous substances at a contaminated property. Liability under RCRA is strict and, under certain circumstances, joint and several, so that any responsible party may be held liable for the entire cost of investigating and remediating the release of hazardous substances. As is the case with all companies engaged in similar industries, depending on the underlying facts and circumstances we face potential exposure from future claims and lawsuits involving environmental matters, including soil and water contamination, personal injury or property damage allegedly caused by hazardous substances that we manufactured, handled, used, stored, transported, spilled, disposed of or released. We cannot assure you that we will not become involved in future proceedings related to our release of hazardous or extremely hazardous substances or that, if we were held responsible for damages in any existing or future proceedings, such costs would be covered by insurance or would not be material. For a discussion of hazardous substances management at the Pasadena Facility, see the risk factor captioned “There are phosphogypsum

16

Table of Contents

stacks located at the Pasadena Facility that will require closure. In the event we become financially obligated for the costs of closure, this would have a material adverse effect on our business, cash flow and ability to make cash distributions to our unitholders.” For a discussion of releases at the Pasadena Facility, see the risk factor captioned “Soil and groundwater at the Pasadena Facility is pervasively contaminated, and we may incur costs to investigate and remediate known or suspected contamination at the Pasadena Facility. We may also face legal actions or sanctions or incur costs related to contamination or noncompliance with environmental laws at the facility.”

Underground Injection Operations. Underground injection operations are subject to the Safe Drinking Water Act, or SWDA, as well as analogous state laws and regulations. Under the SWDA, the EPA established the underground injection control, or UIC program, which includes requirements for permitting, testing, monitoring, record keeping, and reporting of injection well activities, as well as a prohibition against the migration of fluid containing any contaminant into underground sources of drinking water. ExxonMobil Corporation (a former owner of the Pasadena Facility), or ExxonMobil, operates injection wells located at or surrounded by our Pasadena Facility for the disposal of wastewater related to the phosphogypsum stacks. State regulations require that a permit be obtained from the applicable regulatory agencies to operate underground injection wells. Any leakage from the subsurface portions of the injection wells could cause degradation of fresh groundwater resources, potentially resulting in suspension of ExxonMobil’s UIC permit, which could adversely impact the closure of the phosphogypsum stacks.

Environmental Insurance. We have a premises pollution liability insurance policy which covers third party bodily injury and property damages claims, remediation costs and associated legal defense expenses for pollution conditions at or migrating from our facilities and the transportation risks associated with moving waste from our facilities to offsite locations for unloading or depositing waste. The policy also covers business interruptions and non-owned disposal sites. Our policy is subject to a limit and self-insured retention and contains other terms, exclusions, conditions and limitations that could apply to a particular pollution condition claim, including the closure post closure of the gypsum stacks (the responsibility of ExxonMobil) and we cannot guarantee that a claim will be adequately insured for all potential damages.

Safety, Health and Security Matters

We are subject to a number of federal and state laws and regulations related to safety, including the federal Occupational Safety and Health Act, or OSHA, and comparable state statutes, the purpose of which are to protect the health and safety of workers. Various OSHA standards may apply to our operations, including standards concerning notices of hazards, safety in excavation and demolition work, the handling of asbestos and asbestos-containing materials and worker training and emergency response programs. We also are subject to OSHA Process Safety Management regulations, which are designed to prevent or minimize the consequences of catastrophic releases of toxic, reactive, flammable or explosive chemicals. These regulations apply to any process that involves a chemical at or above the specified thresholds or any process that involves flammable liquid or gas, pressurized tanks, caverns and wells in excess of 10,000 pounds at various locations. We have an internal safety, health and security program designed to monitor and enforce compliance with worker safety requirements. We also are subject to EPA Chemical Accident Prevention Provisions, known as the Risk Management Plan requirements, which are designed to prevent the accidental release of toxic, reactive, flammable or explosive materials, and the United States Coast Guard’s Maritime Security Standards for Facilities, which are designed to regulate the security of high-risk maritime facilities.

Employees

As of December 31, 2014, we had 101 non-unionized and salaried employees, and 166 unionized employees. We believe that we have good relations with our employees. We have collective bargaining agreements in place covering unionized employees at our East Dubuque Facility and our Pasadena Facility. The agreement for the East Dubuque Facility expires on October 17, 2016. There are two agreements for the Pasadena Facility. One agreement expires on March 28, 2016 and the other expires on April 30, 2016. We have not experienced work stoppages in the recent past.

Financial Information

We operate in two business segments. All of our properties are located in the United States and all of the related revenues are derived from purchasers located in the United States. Our financial information is included in “Part II—Item 8. Financial Statements and Supplementary Data.”

Properties

We operate our East Dubuque Facility on a 210 acre site in East Dubuque, Illinois adjacent to the Mississippi River. We own the land, buildings, several special purpose structures, equipment, storage tanks and specialized truck, rail and river barge loading facilities, and hold easements for the roadways, wells, the rail track and the barge dock. We also have the right to store 15,000 tons of ammonia at Agrium’s terminal in Niota, Illinois. See “—Our East Dubuque Facility—Marketing and Distribution.”

17

Table of Contents

We operate our Pasadena Facility on an 85 acre site in Pasadena, Texas located on the Houston Ship Channel which includes 2,700 linear feet of water frontage and two deep-water docks. The property also includes 415 acres of unused land which contains phosphogypsum stacks. In addition, we have an arrangement with IOC that permits us to store approximately 60,000 tons of ammonium sulfate at IOC-controlled terminals, which are located near end customers of our Pasadena Facility’s ammonium sulfate. This arrangement currently is not governed by a written contract. See “—Our Pasadena Facility—Marketing and Distribution.”

Available Information