Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT - Ocata Therapeutics, Inc. | ocata_ex2301.htm |

| EX-21.1 - SUBSIDIARIES OF THE REGISTRANT - Ocata Therapeutics, Inc. | ocata_ex2101.htm |

| EXCEL - IDEA: XBRL DOCUMENT - Ocata Therapeutics, Inc. | Financial_Report.xls |

| EX-31.1 - CERTIFICATION - Ocata Therapeutics, Inc. | ocata_ex3101.htm |

| EX-31.2 - CERTIFICATION - Ocata Therapeutics, Inc. | ocata_ex3102.htm |

| EX-23.1 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - Ocata Therapeutics, Inc. | ocata_ex2302.htm |

| EX-32.1 - CERTIFICATION - Ocata Therapeutics, Inc. | ocata_ex3201.htm |

| EX-32.2 - CERTIFICATION - Ocata Therapeutics, Inc. | ocata_ex3202.htm |

| EX-10.30 - 2014 STOCK OPTION AND INCENTIVE PLAN AND FORMS OF OPTION AGREEMENTS THEREUNDER - Ocata Therapeutics, Inc. | ocata_ex1030.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to _____________

Commission file number 0-50295

OCATA THERAPEUTICS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 87-0656515 |

| (STATE OR OTHER JURISDICTION OF | (I.R.S. EMPLOYER IDENTIFICATION NO.) |

| INCORPORATION OR ORGANIZATION) |

33 Locke Drive, Marlborough, Massachusetts

01752

(508) 756-1212

(Address and telephone number, including area code, of registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, $0.001 par value per share | The Nasdaq Stock Market |

| (Title of each class) | Name of each exchange on which registered |

Securities registered pursuant to Section

12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer x |

| Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes o No x

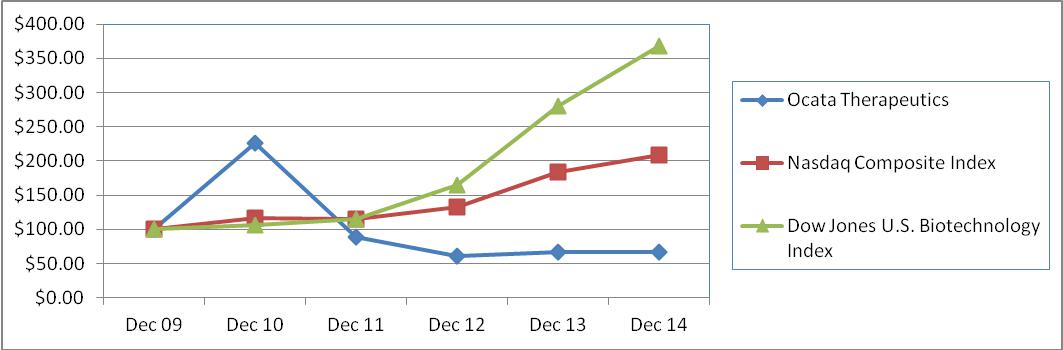

The aggregate market value of the registrant’s Common Stock held by non-affiliates of the registrant (based upon the closing price of $6.70 for the registrant’s Common Stock as of June 30, 2014) was approximately $222.6 million (based on 33,071,871 shares of common stock outstanding and held by non-affiliates on such date all on an 100:1 reverse split-adjusted basis). Shares of the registrant’s Common Stock held by each executive officer and director and by each entity or person that, to the registrant’s knowledge, owned 10% or more of the registrant’s outstanding Common Stock as of June 30, 2014 have been excluded in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of outstanding shares of the registrant’s Common Stock, $0.001 par value, was 35,042,363 shares as of March 1, 2015.

OCATA THERAPEUTICS, INC.

2014 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| Page | ||

| PART I | 1 | |

| Item 1. | Business | 1 |

| Item 1A. | Risk Factors | 13 |

| Item 1B. | Unresolved Staff Comments | 34 |

| Item 2. | Properties | 34 |

| Item 3. | Legal Proceedings | 34 |

| Item 4. | Mine Safety Disclosures | 34 |

| PART II | 35 | |

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 35 |

| Item 6. | Selected Financial Data | 36 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 37 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 44 |

| Item 8. | Financial Statements and Supplementary Data | 44 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 44 |

| Item 9A. | Controls and Procedures | 44 |

| Item 9B. | Other Information | 47 |

| PART III | 47 | |

| Item 10. | Directors, Executive Officers and Corporate Governance | 47 |

| Item 11. | Executive Compensation | 47 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 47 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 47 |

| Item 14. | Principal Accountant Fees and Services | 47 |

| Item 15. | Exhibits and Financial Statement Schedules | 47 |

CAUTIONARY STATEMENT RELATING TO FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the information incorporated by reference includes “forward-looking statements” All statements regarding our expected financial position and operating results, our business strategy, our financing plans and the outcome of any contingencies are forward-looking statements. Any such forward-looking statements are based on current expectations, estimates, and projections about our industry and our business. Words such as “anticipates,” “expects,” “intends,” “plans,” “believes,” “seeks,” “estimates,” or variations of those words and similar expressions are intended to identify such forward-looking statements. Forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those stated in or implied by any forward-looking statements.

Forward-looking statements are only current predictions and are subject to known and unknown risks, uncertainties, and other factors that may cause our or our industry’s actual results, levels of activity, performance, or achievements to be materially different from those anticipated by such statements. These factors include, among other things, the fact that we have no product revenue and no products approved for marketing; our limited operating history; the need for and limited sources of future capital; potential failures or delays in obtaining regulatory approval of products; risks inherent in the development and commercialization of potential products; reliance on new and unproven technology in the development of products; the need to protect our intellectual property; the challenges associated with conducting and enrolling clinical trials; the risk that the results of clinical trials may not support our product candidate claims; even if approved, the risk that physicians and patients may not accept or use our products; our reliance on third parties to conduct its clinical trials and to formulate and manufacture its product candidates; economic conditions generally; as well as those factors listed under “Risk Factors” in Item 1A of Part I of this Annual Report on Form 10-K and elsewhere in this Annual Report on Form 10-K. These and other factors could cause results to differ materially from those expressed in these forward-looking statements.

Although we believe that the expectations reflected in the forward-looking statements contained in this Annual Report on Form 10-K are reasonable, we cannot guarantee future results, performance, or achievements. Except as required by law, we are under no duty to update or revise any of such forward-looking statements, whether as a result of new information, future events or otherwise, after the date of this Annual Report on Form 10-K.

Unless otherwise indicated, information contained in this Annual Report on Form 10-K concerning our clinical trials, therapeutic candidates, number of patients that may benefit from these therapeutic candidates and the potential commercial opportunity for our therapeutic candidates, is based on information from independent industry analysts and third-party sources (including industry publications, surveys, and forecasts), our internal research, and management estimates. Management estimates are derived from publicly available information released by independent industry analysts and third-party sources, as well as data from our internal research, and based on assumptions made by us based on such data and our knowledge of such industry, which we believe to be reasonable. None of the sources cited in this Annual Report on Form 10-K has consented to the inclusion of any data from its reports, nor have we sought their consent. Our internal research has not been verified by any independent source, and we have not independently verified any third-party information. While we believe that such information included in this Annual Report on Form 10-K is generally reliable, such information is inherently imprecise. In addition, projections, assumptions, and estimates of our future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors” in Item 1A of Part I of this Annual Report on Form 10-K and elsewhere in this Annual Report on Form 10-K. These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

PART I

Item 1. Business.

Overview

Ocata Therapeutics, Inc., a Delaware corporation formerly known as Advanced Cell Technology, Inc. (the “Company”, “Ocata”, “we”, “us”, or “our”) is a clinical stage biotechnology company focused on the development and commercialization of Regenerative Ophthalmology therapeutics. Ocata’s most advanced products are in clinical trials for the treatment of Stargardt’s macular degeneration, dry age-related macular degeneration, and myopic macular degeneration. We are also developing several pre-clinical terminally differentiated-cell therapies for the treatment of other ocular disorders. Additionally, we have a number of pre-clinical stage assets in disease areas outside the field of ophthalmology, including autoimmune, inflammatory and wound healing-related disorders. Our intellectual property portfolio includes pluripotent human embryonic stem cell, or hESC; induced pluripotent stem cell, or iPSC, platforms; and other cell therapy technologies. We have no therapeutic products currently available for sale and do not expect to have any therapeutic products commercially available for sale for a period of years, if at all. These factors indicate that our ability to continue research and development activities is dependent upon the ability of management to obtain additional financing as required.

We pursue a number of approaches to generating transplantable tissues both in-house and through collaborations with other researchers who have particular interests in, and skills related to, cellular differentiation. Our research in this area includes projects focusing on the development of many different cell types that may be used to treat a range of diseases within ophthalmology and other therapeutic areas. Control of cellular differentiation and the culture and growth of stem and differentiated cells are important areas of research and development for us.

Key Management Updates

During 2014 there were a number of key changes to our management team. In July 2014, Paul Wotton joined us as President and Chief Executive Officer and a member of our Board of Directors. In October 2014, LeRoux Jooste, joined our company as Senior Vice President of Business Development and Chief Commercial Officer.

An Overview of Regenerative Medicine

Our business focus is the development of new therapies in the field of regenerative medicine. Regenerative medicine is defined as the process of replacing or "regenerating" human cells, tissues or organs to restore or establish normal function and has been called the "next evolution of medical treatments" and “the vanguard of 21st century healthcare” by the U.S. Department of Health and Human Services.

Cell therapies, such as those we are developing, have the potential to offer a complete solution for complex physiologic processes in ways, or through mechanisms, which are not expected to be attainable using traditional small-molecule or protein therapeutics. This field holds the potential to therapeutically address damaged tissues and organs in the body by replacing damaged tissue or by stimulating the body's own repair mechanisms to heal tissues or organs. By altering the course of disease, regenerative medicine may make it possible to eliminate the need for daily therapies, reduce hospitalizations and avoid expensive medical procedures, thus enabling patients to lead healthier and more productive lives. Regenerative medicine, such as those therapies we are developing, could provide more effective solutions or potential cures for a broad range of conditions, and provide meaningful advances for a range of chronic, orphan, and aging-related conditions that traditional medicine has to date been unable to treat and that represent a quality-of-life and economic burden on society.

We believe that regenerative medicine, including Regenerative Ophthalmology ™ will become a highly relevant area of medicine as our population continues to age. Chronic diseases and impairments, which are among the leading causes of disability in older people, can negatively impact quality of life, lead to a decline in independent living, and impose an economic burden on patients and the healthcare system. About 80 percent of seniors in developed countries have at least one chronic health condition and 50 percent have at least two. According to the Centers for Disease Control, of the roughly 150,000 people who die each day, about two-thirds die of age-related causes. In industrialized nations, the proportion is much higher, reaching 90%. Concern is growing that medical advances leading to longevity will in turn lead to an older population who have a higher incidence of functional and cognitive impairment.

| 1 |

Figure 1 shows the projected growth of two groups of older people – those aged 65-79 and those 80 years and older.

By 2050, the number of people over the age of 65 living in developed countries is projected to exceed 325 million; when including developing countries, this number rises to 1.5 billion – a near tripling of the over 65 population as compared to today. In the United States, as an example, the number of Americans aged 65 and older is projected to be 88.5 million in 2050, more than double the population of 40.2 million in 2010. The U.S. population is projected to grow to 439 million by 2050, an increase of 42 percent relative to the 2010 census numbers of 310 million. The population is also expected to become much older. Those over the age of 85 accounted for 5.8 million Americans in the 2010 census, and are expected to reach 8.7 million by 2030 and then 19 million by 2050.

The majority of treatments available today for chronic and/or life-threatening diseases are palliative, meaning they merely treat the symptoms rather than cure the underlying cause. Others delay disease progression and the onset of complications associated with the underlying illness. Only a very limited number of these available therapies are capable of curing or significantly changing the course of disease. The result is a healthcare system burdened by costly treatments for an aging, increasingly ailing population, with few solutions for containing rising costs.

Regenerative medicine has the potential to change the thinking about disease and aging, as well as to help potentially reduce continuously growing health care costs. The best way to address the escalating economics of healthcare includes developing more effective treatments and cures for the most burdensome diseases (such as diabetes, neurodegenerative disorders, stroke and cardiovascular disease) which may help to facilitate longer, healthier and more productive lives.

We believe our therapeutic programs, such as our macular degeneration programs, will contribute to the medical community’s response to this growing problem. Our regenerative cell therapies currently in development may have both therapeutic benefit and provide meaningful reduction to the otherwise-predicted increase in healthcare costs resulting from aging. We believe those factors may help us obtain favorable pricing and reimbursement considerations for our therapies.

Pluripotent Stem Cell Platforms

There are two broad categories of stem cells: adult stem cells and pluripotent stem cells. The term “stem cells” is used to describe those cell types that can give rise to the different cells found in tissues. A common feature to all stem cells is the ability to both replicate (propagate) as well as differentiate into two or more different mature cell types. There are however, differences between adult and pluripotent stem cells. Adult stem cells are derived from various tissues in the human body and are typically limited in the diversity of other cell types they can become, usually only able to produce two or three different types of mature cells. Adult stem cells also are often limited in their ability to divide and renew in culture before ceasing to grow. In contrast, pluripotent stem cells are often termed “true” stem cells because they have the potential to differentiate into almost any cell in the body, and have a near infinite capacity to replicate. Pluripotent stem cells can potentially provide a renewable source of healthy cells and tissues to treat a wide array of diseases, making pluripotent stem cells a central aspect to our strategy in the development of effective cellular therapies that can be used in a commercially scalable manner.

From a single master stem cell bank the manufacturing of the therapeutic doses to be used can be readily controlled for consistency, lack of infectious agents and cleared by regulatory agencies to be used in an entire patient population. The pluripotent stem cell approach also permits the use of cell culturing and manufacturing techniques that we believe will prove to be less costly and intrinsically more scalable than the high-touch process that otherwise characterize the majority of “autologous” cell therapies.

Pluripotent stem cells presently include two distinct cell types: (1) embryonic stem, or ESCs, and (2) induced pluripotency stem cells, or iPSCs, which have ESC-like properties.

| 2 |

Embryonic Stem Cell Platform

A human ESC, or hESC, line represents a potentially inexhaustible supply of pluripotent cells. Derived from a single cell, the replicative capacity of an hESC line could be very significant. Embryonic stem cells have specific properties that make them particularly useful for cell-based therapies. Because they are able to differentiate into all of the more than 200 types of cells in the human adult body, they may offer substantial therapeutic potential. Our primary focus has been in the development of therapies that are terminally differentiated into the cells of interest, with hESCs representing the starting raw material for our therapeutic products.

iPSC Platform

iPSCs are adult cells that have been genetically or environmentally reprogrammed to an embryonic stem cell-like state by being genetically manipulated to express genes and factors important for maintaining the defining properties of embryonic stem cells. The reprogramming of adult cells into embryonic stem cell-like cells enables the generation of patient-specific stem cells and thus has potential for the treatment of degenerative diseases. Given that iPSCs can be made in a patient-specific manner, the ultimate goal for iPSC-derived tissues and differentiated cells is that these can be transplanted back into the same patient without rejection, and so might be used in treatment settings where donor-recipient matching would otherwise be necessary to prevent rejection of the transplanted cells.

Our Cell Therapy Research Programs

Our product development programs are based on our ability to induce hESCs to become a specific cell type of interest and to become this type of cell permanently. This is known as terminal differentiation and we believe it is a core competency of our research and development programs. We have demonstrated our ability to terminally differentiate hESCs into a wide variety of cell types. We have also demonstrated that many of these terminally differentiated cells may be safe, and, in some cases, potentially effective in treating human disease as in the case of our lead programs for macular degeneration. Our research with these terminally differentiated cells includes projects using many different cell types that may be used to treat a range of diseases across several therapeutic categories. We are pursuing a variety of approaches to generate transplantable tissues both through in-house and external collaborations with other researchers who have particular interests in, and skills related to, cellular differentiation. Control of differentiation and the culture and growth of stem and differentiated cells are also important current areas of research for us.

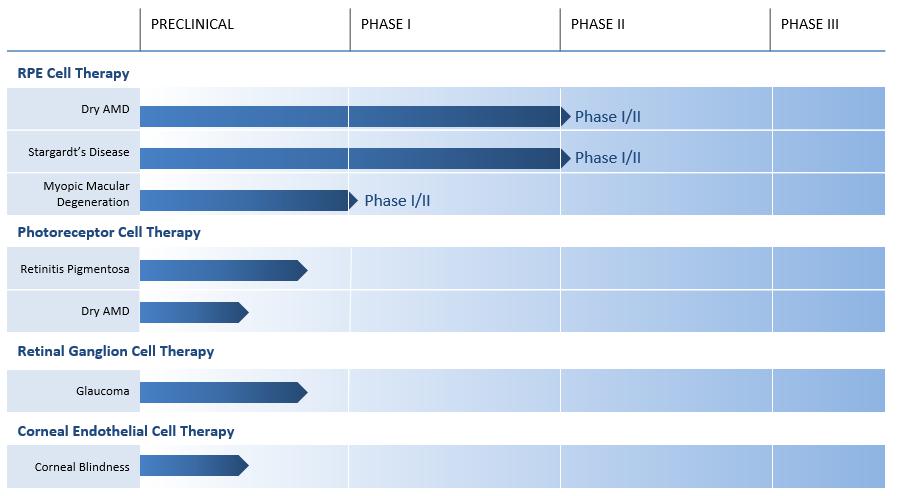

Based on the success to date of our Phase 1 clinical trials and what we see as favorable market dynamics of the ophthalmology sector, we have shifted our strategic priorities to focus primarily on the development, and ultimate commercialization of ophthalmology therapies. We believe that the eye is well suited for cellular transplantation for a number of reasons. First, the eye has relative immune privilege, which means that the body’s immune system is less likely to target a foreign substance, such as allogeneic cells, for rejection. Second, the eye is a compact structure and therefore the doses are relatively small (approximately 200,000-300,000 cells), which may enable relative ease of manufacturing scalability. Third, there are many well-known and validated tools that are accepted for measurement of clinical outcomes. Finally, the community of surgeons who will ultimately develop our back-of-the-eye therapies is small and highly concentrated. There are approximately 2,000 retinal surgeons in the United States, we believe we can access the majority of macular degeneration patients with a relatively small sales force to call on this concentrated physician base. Our current ophthalmology development pipeline is presented below:

| 3 |

Ophthalmology Programs

We are developing a pipeline of stem cell derived therapeutics which may have use as treatment for degenerative diseases of the eye. In some instances, stem cell derived therapies may repair and replace damaged tissue in the eye, permitting restoration of otherwise lost vision or prevention of further vision loss. As our understanding of the underlying pathophysiology of ocular disease increases, we believe we will have additional opportunities to develop other therapeutic products for the ophthalmology market.

Chronic diseases of the eye are common globally, particularly in aging populations. The recent success of palliative therapies in the wet age-related macular degeneration market highlights the therapeutic and commercial potential of this sector. This is underscored by large pharmaceutical and global biotech companies that have either recently repositioned themselves through further emphasis in funding and/or acquiring ophthalmology programs, or entering ophthalmology for the first time, as the industry comes to appreciate the potential size of this market and its projected growth rate, largely as a consequence of an aging population. These companies include, as examples, Bayer Healthcare, GlaxoSmithKline, Pfizer, Novartis and Roche. Despite this growing interest, several disease areas of ophthalmology remain underserved by prescription pharmaceuticals.

A significant unmet medical need relates to diseases affecting the back of the eye, such as age-related macular degeneration as well as other forms of macular degeneration, diabetic retinopathy and retinitis pigmentosa. Inflammatory diseases such as uveitis, and vision loss from photoreceptor and other neurosensory retinal damage due to glaucoma, also represent significant patient populations for which effective therapies have remained elusive. These conditions have been under-served primarily because of their pathophysiological complexity, which the development of new drugs – traditional small molecule and biologics – has been unable to solve. We are developing a pipeline of cell-based therapeutics which may have use as treatment for degenerative diseases of the eye. In some instances, stem cell derived therapies may repair and replace damaged tissue in the eye, permitting restoration of otherwise lost vision. As our understanding of the underlying pathophysiology of ocular disease increases, we believe we will have additional opportunities to develop other therapeutic products for the ophthalmology market.

Macular Degeneration Programs

The largest indication involving macular degeneration is “age-related macular degeneration”, or AMD. AMD is the leading cause of blindness and visual impairment in adults over fifty years of age. It is estimated that the clinically detectable AMD patient population in North America and Europe includes about 25-30 million people across the range of disease, from early-stage to late-stage, or legal blindness. Furthermore, it is estimated that there are nearly two million new diagnoses of AMD per year in the United States. AMD represents one of the largest unmet medical needs in medicine today in terms of the lack of useful therapeutics.

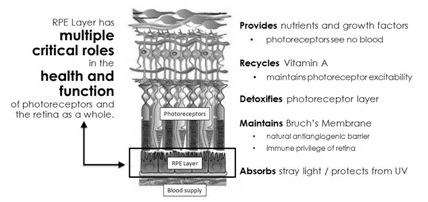

Retinal pigment epithelium, or RPE, is a single-cell-thick layer of pigmented cells that form part of the blood-ocular barrier. The presence and integrity of the RPE layer is required for normal vision. The RPE layer is positioned between the photoreceptor cell layer of the retina and the Bruch's membrane and choroid, a layer filled with blood vessels. Because the photoreceptors see no direct blood supply, it is the role of the RPE layer to transport nutrients and oxygen to the photoreceptor cells, as well as to supply, recycle, and detoxify products involved with the phototransduction process — the process by which the photoreceptors turn light into a signal to be propagated along the optic nerve to the brain. In particular, the RPE layer serves as the transport layer that maintains the structure of the photoreceptor environment by acting as an intermediary between the nerve layer and blood vessels, supplying small molecules, transporting ions and water from the blood vessels to the photoreceptor layer. The RPE cells take up nutrients such as glucose, retinol (Vitamin A), and fatty acids from the blood and deliver these nutrients to photoreceptors. The RPE layer also prevents the buildup of toxic metabolites around the nerve cells by transporting the metabolites to the blood. In addition, the RPE cells are able to secrete a variety of growth and survival factors helping to maintain the structural integrity and organization of the photoreceptors.

| 4 |

Maintenance of the Bruch’s membrane, which serves as a natural anti-angiogenic barrier that prevents the capillary bed of the choroid from invading and disrupting the photoreceptor and nerve microarchitecture of the retina, is also an important function of the RPE layer. RPE cells also recycle proteins and other components involved in a process is known as the visual cycle of retinal, which isomerizes all trans-retinol to 11-cis retinal – the latter of which is required by photoreceptors for vision. A failure of any one of these functions of the RPE layer can lead to degeneration of the retina, loss of visual function, and/or blindness. Dysfunction and degeneration of the RPE layer is in fact implicated in many disease processes, the most prominent being various forms of macular degeneration.

As the name implies, age-related macular degeneration usually affects older adults, with loss of central vision required for reading, driving and other important activities of daily living due to chronic damage of the central retina. It occurs in "dry" (aka "atrophic" or "geographic") and "wet" (aka "neovascular" or "exudative") forms. In the case of dry AMD, the disease process appears to begin with loss (death) of RPE cells followed by some period of photoreceptor atrophy and inactivity, and eventually, photoreceptor death. For most dry AMD patients, gradual loss of central vision occurs first. Wet AMD is often an end-stage manifestation seen in approximately 10% - 15% of dry AMD patients, with the loss of the RPE layer and its ability to maintain the Bruch's membrane function as a barrier resulting in failure of the membrane's integrity and abnormal blood vessels penetrating into the subretinal space with ensuing rapid loss of vision. In addition to AMD, other forms of macular degenerative diseases exist which, even if the underlying causes are different, appear to follow a similar course of RPE cell loss followed by atrophy, inactivity and ultimately death of the photoreceptor. These include, for example, an inherited juvenile onset form of macular degeneration called Stargardt's Macular Degeneration, or SMD.

Our research has indicated that RPE cells generated from pluripotent stem cell sources, such as our hESC lines, may potentially solve the sourcing of transplantable RPE cells for treating macular degenerative conditions. It is possible that the area in which the RPE layer exists will maintain its relative immune-privilege in dry AMD patients. If so, the need for donor matching is not likely to be a significant limitation and a single and scalable allogeneic source of RPE cells, one that can be manufactured in culture, might provide a therapeutic solution for the millions of patients affected by this disease. We have created GMP-compliant hESC master stem cell banks and a GMP protocol for manufacturing of human RPE cells from our hESC master banks. Extensive animal testing of the human RPE cells generated in culture has been conducted and has established that when injected into the eyes of test animals as a suspension of cells, the human RPE cells were able to home to areas of damage in the RPE layer, with engraftment and recapitulation of the correct anatomical structure in the back of the eye of the animals. As published in 2006 the journal Cloning and Stem Cells , we have also demonstrated that in animal models of macular degeneration, not only did the human RPE cells reform the correct structure, but also that the injection of the cells resulted in preservation of the photoreceptor layer and its function. That is, the injected human RPE cells repaired and restored the function of the RPE layer in animal models of disease.

This data, along with safety data we collected on the human RPE cells, or our RPE Program, formed the basis of several Investigational New Drug applications filed with the U.S. Food and Drug Administration and an Investigational Medicinal Product Dossier, or IMPD, relied upon by the U.K. Medicines and Healthcare Products Regulatory Agency. It also served as the basis of our clinical trials using RPE cells in patients with SMD and dry AMD.

| 5 |

We believe that the results from the SMD and dry AMD clinical trials are promising. Preliminary results for the first dry AMD and first SMD patient were published in January 2012 in The Lancet. This publication followed two patients who were treated with our RPE therapy for at least three months of post-transplant follow up and the study reported that there were no serious adverse events due to the injected RPE cells, which is the primary endpoint of the trials. The trial sites have provided regular follow-up on all of the patients, and have been able to include data relating to the engraftment and persistence of the injected cells as well the impact on visual acuity. The preliminary data suggest that the injected cells are well tolerated and appear generally to be capable of engrafting at the site of injection, forming the appropriate anatomical monolayer structure around the injected area. Visual acuity improvement has been observed to varying degrees in several of these very late-stage patients, a result that was not anticipated in the original design of these studies.

In October 2014, we announced that Phase 1/2 clinical data published online in The Lancet demonstrate positive long-term safety results using our RPE cells for the treatment of SMD and AMD (nine patients from each study). The publication features data from 18 U.S.-based patients with at least six months of post-transplant follow-up. These two studies provide the first evidence of the mid- to long-term safety, survival, and potential biologic activity of pluripotent stem cell progeny into humans with any disease. In addition to showing no adverse safety issues related to the transplanted tissue, anatomic evidence confirmed successful engraftment of the RPE cells, which included increased pigmentation at the level of the RPE layer after transplantation in 13 of 18 patients. The publication also noted that ten of the 18 patients experienced clinically significant (greater than 15 letters on the standard EDTRS charts) improvements in best corrected visual acuity. We have subsequently updated the visual acuity data, as patients have continued their post-transplant follow up measurements, and have noted that visual acuity gains have persisted in several patients for more than 2 years.

Based on the data published in The Lancet in October 2014, and the continued safety profile observed in all 38 patients that have been treated, to date, with our experimental therapy, we plan to advance our programs to Phase 2 clinical proof-of-concept trials. To this end, we have met with regulatory agencies, including the US Food and Drug Administration (FDA), the European Medicines Agency (EMA) and the United Kingdom Medicines Healthcare Products Regulatory Agency (“MHRA”), to obtain feedback on our Phase 2 study designs. Based on this feedback and in consultation with our clinical investigators and other external consultants, we believe we have developed a set of clinical studies that will achieve our development objectives over the next several years.

We plan to initiate our Phase 2 trial for dry AMD in the second quarter of this year. The purpose of the dry AMD trial is to evaluate the safety and exploratory efficacy of our hESC-derived RPE cells. This Phase 2 study will include three cohorts of 20 subjects each, 15 who will be treated with our RPE therapy and 5 untreated control subjects. Each of the three cohorts will be treated with different immune suppression regimens. We intend to complete the first cohort during 2015 and the second two cohorts by the end of 2016.

The purpose of our pivotal SMD trial will be to evaluate the safety and efficacy of our hESC-derived RPE cells. This trial will include 100 subjects, 50 who will be treated with our RPE therapy and 50 untreated control subjects.

To support these plans we intend to expand our clinical operations capabilities. We currently work with four clinical sites in the US and two in the UK. In addition, we are expanding the network of contract service providers and also plan to expand our internal workforce. These expansions and the increased spending that will result from these expanded capabilities is consistent with our previously stated plans to transition into a late-stage clinical development company.

In February 2013, we announced that our clinical partner, the Jules Stein Eye Institute at the University of California, Los Angeles had received approval of its Investigator IND Application to initiate a Phase 1/2 study using our RPE cells to treat myopic macular degeneration, or MMD, a form of macular degeneration that can occur in association with severe forms of myopia. Myopia, or nearsightedness, is the most common eye disorder in the world, and is a significant global public health concern. Myopic macular degeneration seems to be associated with stress on the RPE layer as a consequence of pathological elongation of the eye in myopic patients. The apparent stress can induce fissures in the RPE layer, leading to RPE cell death and ultimately macular dystrophy and degeneration. It is an important public health issue lacking safe and effective treatments. Overall, MMD is reported to be the seventh-ranking cause of legal blindness in the United States, the fourth-ranking cause in Hong Kong and the second in parts of China and Japan. In June 2014, we announced that Jules Stein Eye Institute has initiated the trial. The actual enrollment of patients in this trial has been delayed by technical considerations to maximize patient safety.

As we continue to manage our clinical trials and expand the indications for which our RPE cell therapy is being investigated, we have also begun to take the steps to define our final product formulation, as well as to lay the early ground work to support appropriate pricing, coverage and reimbursement programs. We believe that our RPE therapy provides pricing justification across all categories of consideration by Medicare, Medicaid, National Health Service (UK) and private payers. Our program related to RPE cell therapy for the treatment of SMD has been granted Orphan Drug status in both the U.S. and Europe, which could accordingly lead to provide regulatory market exclusivity and potential FDA grant opportunities.

| 6 |

Photoreceptor Progenitor Program

Photoreceptors mediate the first step in vision, capturing light which, in turn, is converted into nerve signals to the brain. Photoreceptor atrophy, and subsequent cell death and permanent loss of photoreceptors, is seen as a consequence of degenerative diseases including AMD, and SMD as well as various inherited retinopathies. Loss of photoreceptors is also a consequence of acquired conditions such as diabetes. We recognize the potential value of being able to repair the retina with replacement photoreceptor cells derived from pluripotent stem cell sources such as iPSCs and hESCs. We believe those therapies can provide the basis for new approaches for treating a wide variety of retinal degenerations in diseases where photoreceptors malfunction and/or die, either alone or in combination with our RPE therapy.

We have developed a human photoreceptor progenitor cell which we believe is unique with respect to both the markers they express as well as their plasticity, meaning that they can differentiate into both rods and cones, and therefore provide a viable source of new photoreceptors for retinal repair. In addition, our photoreceptor progenitors appear to secrete neuroprotective factors, and have the ability to phagocytose (digest) such materials as the drusen deposits that build up in the eyes of dry AMD patients, and so may provide additional benefits beyond forming new photoreceptors when injected into the subretinal space in the eyes of patients. We will continue our pre-clinical investigation in animal models, establish appropriate correlation between integration of the transplanted cells and visual function in the animals, and then consider preparation of an IND and/or IMPD application to commence clinical studies with these cells. As part of our evaluation of this program, we will consider, among other things, the data generated from pre-clinical studies, our understanding of the potential market opportunity, and our ability to allocate capital resources to adequately fund the program to the next milestone.

Retinal Ganglion Cell Progenitor Program

In the United States alone, approximately 100,000 people are legally blind from glaucoma. Proven treatments include drug therapy or surgery to lower intraocular pressure; however, many patients lose vision despite receiving these treatments. In glaucoma, retinal ganglion cells degenerate before photoreceptors are lost. We are currently conducting pre-clinical research and development activities regarding differentiation of stem cells into retinal ganglion cells and demonstration of the ability of those cells to protect against elevated intraocular pressure in glaucoma models. We have succeeded in generating a unique human ganglion progenitor cell which, when injected in animal models of glaucoma, appear to protect against damage. We will continue our pre-clinical investigation in animal models, establish appropriate correlation between integration and visual function in the animals, and then consider preparation of an IND and/or IMPD application to commence clinical studies with these cells. As part of our evaluation of this program, we will consider, among other things, the data generated from pre-clinical studies, our understanding of the potential market opportunity, and our ability to allocate capital resources to adequately fund the program to the next milestone.

Corneal Endothelial Program

Diseases and injuries affecting the cornea are another major cause of blindness worldwide. Although the cornea is clear and seems to lack substance, it is actually a highly organized group of cells and proteins. To see well, all layers of the cornea must be free of any cloudy or opaque areas which can be caused by, among other reasons, swelling of the cornea due loss of the corneal endothelial cells (CECs). The CECs are single layer of cells required to maintain the health and clarity of the cornea and are not know to regenerate spontaneously. In instances where the cornea is damaged or scarred, such as due to chemical injury or infection or thinning as a consequence of aging or an inherited disorder, the current standard of care is a cornea transplant, also referred to as a keratoplasty or corneal graft. The graft replaces damaged corneal tissue with healthy corneal tissue donated from an eye bank. In the past, full thickness corneal transplants were used as part of the procedure. However, a newer version of corneal transplant, known as Descemet's Stripping Endothelial Keratoplasty, (DSEK), is gaining prominence as the surgical method for visual rehabilitation of secondary to corneal pathology [gReg1] . DSEK utilizes the innermost layers, i.e., the endothelial layer and Descemet membrane, for transplant. While corneal transplants are performed routinely (more than 40,000 corneal transplants are performed in the U.S. each year), there is still a pressing need for transplantable corneal tissue. The cadaveric source of donor eyes in the eye banks in the U.S. is not sufficient to meet the demand for the number of patients in need of the surgery, and the corneal tissue being used is often from older donors and hence not as dense or robust as might be desired. We believe that corneal blindness is a significant unmet medical need.

We have been able to generate sheets of corneal endothelial cells, with Descemet membrane, from hESCs. These endothelial sheets, which resemble fetal cornea in cell density, and thickness and durability of the tissue graft, could serve as the transplanted tissue in DSEK. In culture, our corneal endothelial cells have all the hallmarks, both marker expression and morphology, of native human corneal endothelium. We have tested these cells in several animal models of corneal diseases. As part of our evaluation of this program, we will consider, among other things, the data generated from pre-clinical studies, our understanding of the potential market opportunity, and our ability to allocate capital resources to adequately fund the program to the next milestone.

Other Programs

In addition to our ophthalmology programs, we are investing a limited portion of our resources to advance other programs where we feel that we can leverage our expertise in cellular and developmental biology to generate therapies that have the potential to improve health care in other prevalent degenerative diseases and diseases of aging. At the core of our pipeline planning are approaches intended to address large unmet medical needs with allogeneic stem cell-derived therapeutics. The criteria for prioritizing and allocating resources to these programs include stem cell capability, competitive landscape within the therapeutic area, severity/prevalence of the therapeutic need and our perceived ability to out-license these non-core programs to, or otherwise collaborate with third parties that may be able to help advance these programs more efficiently than we can on our own. We utilize a proof-of-concept approach in our product development process, testing our candidate therapies in relevant animal models of human disease in order to assess the likelihood of success when it comes time to try those therapies in human patients.

| 7 |

Hemangio-derived Mesenchymal Cells™

Pluripotent stem-cell derived mesenchymal stem cells (MSCs) regulate immune and inflammatory responses, making them an attractive tool for the treatment of autoimmunity and inflammation. Their underlying molecular mechanisms of action together with their clinical benefit — for example, in autoimmunity — are, in our opinion, being revealed by an increasing number of clinical trials and pre-clinical studies of MSCs. The immunosuppressive/ immunomodulatory activity of these cells allows MSCs to be transplanted nearly universally, i.e., as an allogeneic cell therapy, without matching between donors and recipients. This versatility, along with the ability to manufacture and store these cells, presents a unique opportunity to produce an "off-the-shelf" cellular therapy ready for treatment of diseases in both acute and chronic settings.

Current competitive MSC products for therapeutic applications are isolated from donor-dependent primary tissue sources such as umbilical cord, bone marrow, and adipose (fat) tissue. To achieve commercial scale quantities, MSCs isolated from these tissues need to be expanded in culture, yet the process of expansion compromises the therapeutic potency of these cells. Accordingly, the number of doses of MSCs that can be generated from each donor must be limited in order to preserve potency. Multiple donors must therefore be used to achieve large scale manufacturing required for an off-the-shelf therapy. The use of multiple donors introduces variability in the final MSC product and also drives up costs as pathogen screening must be performed for each new donor.

We believe we have succeeded at creating a unique cellular product, which we refer to as Hemangio-derived Mesenchymal Cells™ (“HMC’s) with attributes similar to MSCs but that circumvent the issues encountered with donor-dependent sources, Our HMCs are produced from a single, pluripotent stem cell source, the renewable nature of which, permits us to manufacture large scale quantities of HMCs without the need for extensive in vitro culture, thus preserving their potency. The stem-cell-sourced manufacturing process may be scalable for global commercialization and therefore may prove to be less costly (particularly at commercial scale) than the primary tissue-sourced MSC products in development by other companies.

Pre-clinical testing of our stem cell-derived HMCs has demonstrated their therapeutic efficacy in various autoimmune disease models. During the course of this testing, we noted another differentiating feature of our cells: the HMCs generated using our proprietary manufacturing approach appear to be more potent with respect to suppressing autoimmune disease than equivalent doses of bone marrow MSCs. This potency was dependent on the number of passages in culture, with the earlier passage HMCs retaining the greatest potency. This correlates with reports in the scientific literature which suggest that not only does the time in culture affect MSC potency but the age of the tissue source affects its potency as well. Evidence in the field suggests that MSCs from young tissue sources, such as embryonic, may be more potent than those from adult (e.g., bone marrow or adipose) tissue sources. Being derived from embryonic stem cells, the early-passage HMCs we are testing for potential therapeutic use are both youthful and replenishable, representing the earliest and most potent stage of biological development.

Our goal is to conduct a limited number of pre-clinical proof-of-concept studies, and based on those results, advance certain of these HMC discovery programs into IND-enabling pre-clinical studies and perhaps file IND applications, as circumstances dictate. In parallel, we are evaluating opportunities for strategic partnering relationships, out-licensing or other commercial transactions with outside parties, such as large pharmaceutical and biotech companies, with the objective of obtaining external funding for these programs so they may continue to be advanced with minimal costs to our company.

Neuroprotective Biologics

In the course of our work with various progenitor cells for treating ocular degenerative diseases, we have discovered that certain progenitor cells not only have the ability to participate directly in the formation of new tissue in the eye, but also were able to exert a neuroprotective effect that reduces the rate of degeneration of native photoreceptors in the animals’ eyes, for example, in animal models of macular degeneration. These cells appeared to also be a source of neuroprotective paracrine factors; biological agents which may themselves be useful as drugs. Further, we observed that these protective effects were uniquely produced by particular progenitor cell sub-types. The restriction of this protective activity to only a certain progenitor cell type permits us to examine which factors are differentially produced by these cells as compared with other closely related progenitor cells which do not seem to secrete any protective agents. We anticipate that the neuroprotective agent(s) that we may ultimately develop as drug candidates may be useful not only in retinal diseases and dystrophies, but may have broader applications in central nervous system and peripheral nervous system diseases and disorders, including diseases causing cognitive function impairment, movement disorders such as Parkinson’s Disease, and ischemic events such as caused by stroke.

| 8 |

Platelets

Platelets are key elements in maintaining blood vessel integrity, or hemostasis, and are therefore central to wound healing and tissue regeneration after injury or surgery. Platelets are a mainstay in treating trauma, and are increasingly being used to promote healing from a wide range of surgeries. When platelet levels decrease and result in thrombocytopenia, such as when bone marrow is destroyed or suppressed, the decrease in platelet function is often a leading cause of morbidity.

Platelets are the most difficult blood product to maintain. They cannot be frozen or refrigerated. Instead, they must be stored at room temperature which limits the shelf life of platelets to five to seven days both because of loss of activity and risk of bacterial contamination during storage. Accordingly, it is our belief that the practical use of platelets is limited by availability. Our estimates are that, but for limitations on donated platelet supplies, there would be a demand for a substantial number of additional units of platelets each year beyond the current platelet usage, particularly for expanded use in surgical settings such as joint replacement or to prevent scarring.

We have developed a manufacturing process for generating megakaryocytes, proplatelet forming cells and ultimately platelets using either hESCs or iPSCs as the starting materials. This process can be carried out under GMP conditions, and we are approaching the ability to produce clinical doses of platelets. We have also solved an important problem in this process, in that we have developed a feeder-free process for making platelets from start to finish. This means our process may be portable into a continuous flow bioreactor to permit large-scale manufacturing.

Overall, we observe that the platelets made by our stem cell process have ultrastructural and morphological features that are indistinguishable from normal blood platelets. We believe our platelets function appropriately as well, both in vitro and in vivo. They respond to thrombin stimulation, form micro-aggregates, and facilitate clot formation and retraction. In animal models of injury, our stem cell derived platelets contribute to developing thrombi at sites of vascular injury.

While the early data that we have generated are encouraging, we believe that our limited resources are best allocated to our other programs, at this time. In the future we may look to partner this program, pursue government funding or permanently cancel the program.

Our Intellectual Property

Our research and development is supported by a robust intellectual property portfolio, including pending patent applications and issued patents. As of February 11, 2015, we have 58 issued patents and 180 pending patent applications filed worldwide, of which 13 issued patents and 82 pending patent applications pertain to our active product development programs. Any patents that may issue from our pending patent applications and which are directed to our current clinical and pre-clinical therapeutic programs would expire between 2025 and 2035, excluding any patent term extension. These patents and patent applications disclose compositions of matter, pharmaceutical compositions, methods of use and manufacturing methods. For instance, we already have issued patents with broad reaching claims in the U.S. and other major markets around our RPE clinical programs, and continue to actively improve our existing portfolio with filings around the improvements we make as we have translated the use of RPE cells from the bench to a regulated manufacturing and human therapy program. To illustrate, over the past few years, the United States Patent and Trademark Office, and other patent offices in major market countries, have granted several of our patents covering the methods we use to derive and produce our RPE cell therapy, as well as patents that cover the use of the RPE cells for formulating pharmaceutical preparations for use in human patients and for treating various macular degenerative diseases such as dry AMD and SMD.

With respect to our therapeutic programs generally, we have filed a number of patent applications, including broad omnibus patent applications, intended to cover the generation of transplantable cells and tissues from any pluripotent stem cell source including hESC, iPSC and other pluripotent stem cell sources as may be identified. Our patent strategy has been to protect the method of manufacturing these transplantable cells and tissues, as well as pharmaceutical preparations of the cells/tissues and the use of those pharmaceutical preparations in patient treatment settings. Our patent strategy includes very broad claims, as well as claims more narrowly directed to our actual processes and formulations. In the case of our RPE Program, to illustrate, we have pursued layers of various independent and dependent claims that range from very broad methods and formulations, to narrower claims which further define and protect the methods and compositions we actually use; as for example, the particular steps in our derivation process, defining the resulting RPE cells by marker and/or functional characteristics, the format of the RPE cells in the final formulation (cell suspension, sheet of cells, cells on a matrix support), etc. In the course of pursuing broad claims with the intention of covering not only our business but creating a barrier to entry to potential competitors who wish to use similar though not identical technology, we have focused on both literal claim scope as well as claims intended to provide additional coverage under the doctrine of equivalents.

Our success will likely depend upon our ability to preserve our proprietary technologies as well as operate without infringing the proprietary rights of other parties. However, we may also need to rely on certain proprietary technologies and know-how that are not patentable. With regard to our own proprietary information, we seek to protect such information, in part, by the use of confidentiality agreements with our employees, consultants and certain of our contractors.

| 9 |

We maintain a strategic patent policy and, when appropriate, seek patent protection for inventions in our core technologies and in ancillary technologies that support our core technologies, or which we otherwise believe will provide us with a competitive advantage. We pursue this strategy by filing patent applications for discoveries we make, either alone or in collaboration with scientific collaborators and strategic partners. Typically, although not always, we file patent applications both in the United States and in select international markets. In addition, we sometimes obtain licenses or options, if available, to acquire licenses to patent filings from other individuals and organizations that we anticipate could be useful in advancing our research, development and commercialization initiatives and our strategic business interests.

Our patents do have a finite life with respect to enforcement against third parties and will eventually expire. The fundamental consequence of patent expiration is that the invention covered by that patent will enter the public domain. However, the expiration of patent protection, or anticipated patent protection, for the bulk of our portfolio is not scheduled to begin for approximately ten to fifteen years. In some instances, we believe that patent term extensions and adjustments, or other forms of exclusivity dependent on our patent rights, may be available in particular instances, such as by operation of patent and/or regulatory laws and regulations. As we make improvements to formulations and dosage amounts, find new combinations of cells and combinations of cells and other therapeutics, refine manufacturing, and elucidate new indications for which our therapies can be used, we expect that we will continue to file additional patent applications covering these new inventions in the future. Any actual products that we develop are expected to be supported by intellectual property covered by granted patents or current patent applications that, if granted, would not expire for 20 years from the date first filed. For example, the granted United States patents covering our RPE cell therapy do not begin to expire until 2025 at the earliest, and then only if no patent term extensions and adjustments are provided. As we have made improvements to our RPE program, particularly arising from the translation of the cell therapy into a human patient treatment setting, we have diligently filed on those improvements. These additional patent filings may prove to be significant barriers to entry for third parties wishing to compete, and would extend the patent portfolio well into the 2030's.

Research and License Agreements

Stem Cell & Regenerative Medicine International

On December 1, 2008, we formed an international joint venture with CHA Biotech. The new company, SCRMI, was tasked with developing human blood cells and other clinical therapies based on our hemangioblast program, one of our core technologies. Under the terms of this agreement, we received a 33% interest in the joint venture upfront, and another 7% interest upon fulfilling certain obligations under the agreement over a period of 3 years. Our contribution included (a) the uninterrupted use of a portion of our leased facility at our expense, (b) the uninterrupted use of certain equipment in the leased facility, and (c) the release of certain of our research and science personnel who were subsequently employed by the joint venture. In return, for a 60% interest, CHA Biotech contributed $150,000 cash upfront and funded operational costs thereafter. Additionally, SCRMI paid us a fee of $500,000 for an exclusive, worldwide license to the hemangioblast program. In parallel, SCRMI granted an exclusive license to CHA Biotech for the commercialization of products arising from the hemangioblast in the territory of South Korea. As of December 31, 2014, we hold a 40% interest in the joint venture and CHA Biotech owns a 60% interest.

In July 2011, we entered into a binding term sheet with CHA Biotech in which SCRMI was realigned around both product development rights and research responsibilities. Under the terms of the binding term sheet, SCRMI exclusively licensed the rights to the hemangioblast program to us for United States and Canada and expanded the jurisdictional scope of the license to CHA Biotech to include Japan (in addition to South Korea, which was already exclusively licensed to CHA Biotech). As part of the agreement, the scientists at SCRMI involved in the hemangioblast program were transferred to us, and SCRMI discontinued its research activity and became solely a licensing entity. In order to maintain our exclusive license, we are obligated to satisfy certain diligence requirements relating to licensed products, defined in the license agreement as “any therapeutic, diagnostic, bioinformatics or other human or veterinarian health care product and/or service and or research reagent utilizing or derived in any manner whatsoever from the Technology”. By filing the investigational new animal drug application on September 12, 2013, with the U.S. FDA, we met the commitment required to maintain its exclusive license. Intellectual property rights created by us in the course of our research are subject to a non-exclusive license to CHA Biotech for Japan and South Korea, and to SCRMI to be sub-licensable under certain circumstances for countries other than the United States, Canada, Japan and South Korea.

CHA Biotech

On March 31, 2009, we entered into a licensing agreement under which we have licensed our RPE technology, for the treatment of diseases of the eye, to CHA Biotech for development and commercialization exclusively in Korea. We are eligible to receive up to $1.9 million in fees based upon achieving certain milestones, including us making an IND submission to the U.S. FDA to commence clinical trials in humans using the technology, which we completed during the second half of 2009. We received an up-front fee of $250,000 and additional consideration under the agreement in the amount of $850,000. Under the terms of the agreement, CHA Biotech will incur all of the cost associated with RPE clinical trials in Korea.

On May 21, 2009, we entered into a licensing agreement under which we licensed our proprietary single blastomere technology, which has the potential to generate stable cell lines, including RPE cells for the treatment of diseases of the eye, to CHA Biotech for development and commercialization exclusively in Korea. We received a $300,000 up-front license fee, and received an additional $300,000 in December 2009.

| 10 |

Embryome Sciences, Inc.

In 2008, we entered into three license agreements whereby we licensed to Embryome Sciences certain cell processing technologies, including technology licensed from Kirin Beer. We received up-front payments of $470,000 and will receive royalties from future sales, if any, of product that utilizes the technologies from the licenses.

Regulations

Our research and development activities and the future manufacturing and marketing of our potential therapeutic products are, and will continue to be, subject to regulation for safety and efficacy by numerous governmental authorities in the United States and other countries.

In the United States, pharmaceuticals, biologicals and medical devices are subject to rigorous regulation by the FDA. The Federal Food, Drug and Cosmetic Act, the Public Health Service Act, applicable FDA regulations, and other federal and state statutes and regulations govern, among other things, the testing, manufacture, labeling, storage, export, record keeping, approval, marketing, advertising, and promotion of our potential products. Product development and approval within this regulatory framework takes a number of years and involves significant uncertainty combined with the expenditure of substantial resources.

The steps required before our potential therapeutic products may be marketed in the United States include: pre-clinical laboratory and animal tests; submission and acceptance of an IND application; safe and efficacious human clinical trials; submission of a Biologics Licensing Application; and Regulatory Approval.

The testing and approval process will require substantial time, effort and expense. The time for approval is affected by a number of factors, including relative risks and benefits demonstrated in clinical trials, the availability of alternative treatments and the severity of the disease. Additional animal studies or clinical trials may be requested during the FDA review period, which might add to that time. FDA approval of the application(s) is required prior to any commercial sale or shipment of the therapeutic product. Biologic product manufacturing facilities located in certain states also may be subject to separate regulatory and licensing requirements.

In addition, the FDA may require post-marketing studies. After receiving FDA marketing approval for a product for an initial indication, further clinical trials may be required to gain approval for the use of the product for additional indications. The FDA may also require post-marketing testing and surveillance to monitor for adverse effects, which could involve significant expense, or the FDA may elect to grant only conditional approvals subject to collection of post-marketing data.

Among the conditions for product licensure is the requirement that the prospective manufacturer’s quality control and manufacturing procedures conform to the FDA’s current good manufacturing practice (GMP) requirements. Even after a product’s licensure approval, its manufacturer must comply with GMP on a continuing basis, and what constitutes GMP may change as the state of the art of manufacturing changes. Domestic manufacturing facilities are subject to regular FDA inspections for GMP compliance, which are normally held at least every two years. Foreign manufacturing facilities are subject to periodic FDA inspections or inspections by the foreign regulatory authorities. Domestic manufacturing facilities may also be subject to inspection by foreign authorities.

In addition to safety regulations enforced by the FDA, we are also subject to regulations under the Occupational Safety and Health Act, the Environmental Protection Act, the Toxic Substances Control Act and other present and potential future and federal, state, local, and foreign regulations.

Outside the United States, we will be subject to regulations that govern the import of drug products from the United States or other manufacturing sites and foreign regulatory requirements governing human clinical trials and marketing approval for our products. The requirements governing the conduct of clinical trials, product licensing, pricing and reimbursements vary widely from country to country.

The United States Congress, several states and foreign countries have considered legislation banning or restricting human application of ESC-based and nuclear transfer based technologies. No assurance can be given regarding future restrictions or prohibitions that might affect our technology and business. In addition, we cannot assure you that future judicial rulings with respect to nuclear transfer technology or hESCs will not have the effect of delaying, limiting or preventing the use of nuclear transfer technology or ESC-based technology or delaying, limiting or preventing the sale, manufacture or use of products or services derived from nuclear transfer technology or ESC-derived material. Any such legislative or judicial development would harm our ability to generate revenues and operate profitably.

For additional information about governmental regulations that will affect our planned and intended business operations, see the section entitled “Risk Factors” beginning below.

| 11 |

Competition

We are engaged in activities in the biotechnology field, which is characterized by extensive research efforts and rapid technological progress. If we fail to anticipate or respond adequately to technological developments, our ability to operate profitably could suffer. Many of our competitors have substantially greater financial, technical and other resources, such as larger research and development staff and experienced marketing and manufacturing organizations. Competition may increase further as a result of advances in the commercial applicability of technologies and greater availability of capital for investment in these industries. Our competitors may succeed in developing, acquiring or licensing on an exclusive basis, products that are more effective or less costly than any product candidate that we may develop, or achieve earlier patent protection, regulatory approval, product commercialization and market penetration than us. Additionally, technologies developed by our competitors may render our potential product candidates uneconomical or obsolete, and we may not be successful in marketing our product candidates against competitors. We cannot assure you that research and discoveries by other biotechnology, agricultural, pharmaceutical or other companies will not render our technologies or potential products or services uneconomical or result in products superior to those we develop or that any technologies, products or services we develop will be preferred to any existing or newly-developed technologies, products or services.

We are aware that several companies and non-profit entities are working on various RPE formulations for treating macular degeneration. For example, Pfizer, Regenerative Patch Technologies and the Riken Center for Developmental Biology (Japan) have publicly stated that each is working towards clinical trials of RPE patches (sheets of cells) for treating wet AMD, and have also stated that they believe their formulations of RPE cells could potentially be used for treating dry AMD. Cell Cure Neurosciences Ltd. (Israel) has previously announced that it is developing RPE cell formulations for dry AMD.

Other cell types are also being developed for subretinal use in treating various forms of macular degeneration. StemCells Inc. recently commenced treating dry AMD patients with purified human neural stem cells. Bioheart, Inc. sponsors an active clinical trial for treating dry AMD with adipose stem cell (ASC), while the University of California Davis and Retinal Associates of South Florida are the sponsors of FDA approved pilot studies to determine whether it would be safe and feasible to inject CD34+ stem cells from bone marrow into the eye as treatment for patients who are irreversibly blind from various retinal conditions including dry AMD. Neurotech, Inc. recently completed a phase I study testing the safety of injecting encapsulated cells that express CNTF in dry AMD patients, while Janssen Research & Development, LLC suspended temporarily its safety study of umbilical cord stem cells administered subretinally in dry AMD patients.

Research and Development Expenditures

We spent the following amounts on company-sponsored research and development activities during each of the last three fiscal years:

| Fiscal Year | Research and Development Expenditures | |||

| 2014 | $10,529,321 | |||

| 2013 | $11,564,768 | |||

| 2012 | $14,158,936 |

Employees

As of March 1, 2015, we had 37 full-time employees, of whom 10 hold Ph.D. or M.D. degrees. Twenty-six employees are directly involved in research and development activities and 11 are engaged in business development and administration. We also use the services of numerous outside consultants in business and scientific matters. We believe that we have good relations with our employees and consultants.

Corporate Information

We were incorporated in Nevada under the name Two Moon Kachinas Corp. on May 18, 2000. On December 30, 2004, we changed our corporate name to A.C.T. Holdings, Inc. On January 31, 2005, we completed the acquisition of Advanced Cell Technology, Inc., a Delaware corporation, or ACT, pursuant to the terms of an Agreement and Plan of Merger dated December 31, 2004. On June 17, 2005, we changed our corporate name to Advanced Cell Technology, Inc. On November 18, 2005, we consummated a merger with and into our wholly-owned subsidiary ACT. As a result of the reincorporation, we became a Delaware corporation. On November 12, 2014, we changed our corporate name to Ocata Therapeutics, Inc.

| 12 |

Item 1A. Risk Factors.

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below, including information in the section of this document entitled “Forward Looking Statements.” The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties not presently known to us or that we currently believe are immaterial may also impair our business operations. If any of the following risks actually occur, our business, financial condition or results of operations could be materially adversely affected, the value of our common stock could decline, and you may lose all or part of your investment.

Risks Relating to our Early Stage of Development and Capital Resources

We have a history of operating losses and we may not achieve future revenues or operating profits.

We have generated modest revenue to date from our operations. Historically, we have had net operating losses each year since our inception. As of December 31, 2014, we have an accumulated deficit of $349,134,225 and a stockholders’ deficit of $2,735,545. We incurred net losses of $34,748,945, $31,022,248, and $34,584,115 for the years ended December 31, 2014, 2013, and 2012, respectively. We have limited current potential sources of income from licensing fees and we do not generate significant revenue from any other source. We have no therapeutic products currently available for sale and do not expect to have any therapeutic products commercially available for sale for a period of years, if at all. Additionally, even if we are able to commercialize our technologies or any products or services related to our technologies if approved, it is not certain that they will result in revenue or profitability.

Our business is at an early stage of development and we may not develop therapeutic products that can be commercialized.

Our most advanced product candidates are being prepared for use in Phase 2 clinical trials and we do not have any products that are currently in the marketplace. Though we have recently released clinical data from our Phase I/II clinical trial regarding the safety and tolerability of sub-retinal transplantation of hESC-derived RPE cells transplanted into patients with SMD and dry AMD, our potential therapeutic products will require additional extensive pre-clinical and clinical testing prior to any possible regulatory approval in the United States and other countries and may additionally require post-authorization outcome studies. We may not be able to obtain regulatory approvals for any of our products (see the subsection entitled “Regulatory Risks” below), or commence or continue clinical trials for any of our products, or commercialize any products. Any of our therapeutic and product candidates may prove to have undesirable and unintended side effects or other characteristics that could cause adverse effects on patient safety, efficacy or cost-effectiveness that could prevent or limit their therapeutic use, commercialization or acceptance in the medical community. Clinical trial results that we view as positive or proof of safety and/or efficacy may not be viewed in the same manner by regulators or potential collaborators. Any product using any of our technologies may fail to provide the intended therapeutic benefits, or even achieve therapeutic benefits equal to or better than the standard of treatment at the time of testing or production, or may not be safe for use in humans. In addition, we will need to determine whether any of our potential products can be manufactured in commercial quantities or at an acceptable cost, with or without third-party support. Our efforts may not result in a product that can be or will be marketed successfully. Physicians may not prescribe our products, patients may not use our products, or third-party payors may not cover or provide adequate reimbursement for our products. For these reasons and others, we may not be able to generate product revenues.

We have never generated any revenue from product sales and may never be profitable.