Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - Diplomat Pharmacy, Inc. | a2223651zex-23_2.htm |

| EX-23.1 - EX-23.1 - Diplomat Pharmacy, Inc. | a2223651zex-23_1.htm |

As filed with the Securities and Exchange Commission on March 13, 2015

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

DIPLOMAT PHARMACY, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Michigan (State or Other Jurisdiction of Incorporation or Organization) |

5122 (Primary Standard Industrial Classification Code Number) |

38-2063100 (I.R.S. Employer Identification Number) |

4100 S. Saginaw St.

Flint, MI 48507

(888) 720-4450

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices)

Sean Whelan

Chief Financial Officer

Diplomat Pharmacy, Inc.

4100 S. Saginaw St.

Flint, MI 48507

(888) 720-4450

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

| Copies to: | ||

Michael S. Ben, Esq. Honigman Miller Schwartz and Cohn LLP 2290 First National Building 660 Woodward Avenue Detroit, MI 48226-3506 Telephone: (313) 465-7000 Fax: (313) 465-8000 |

William J. Whelan, III, Esq. Cravath, Swaine & Moore LLP Worldwide Plaza 825 Eighth Avenue New York, NY 10019-7475 Telephone: (212) 474-1000 Fax: (212) 474-3700 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(3) |

||

|---|---|---|---|---|

Common Stock, no par value per share |

$200,000,000 | $23,240 | ||

|

||||

- (1)

- Includes

shares that the underwriters have the option to purchase.

- (2)

- Estimated

solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as

amended.

- (3)

- Calculated pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We and the selling shareholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MARCH 13, 2015

Shares

Diplomat Pharmacy, Inc.

Common Stock

This is a public offering of shares of common stock of Diplomat Pharmacy, Inc.

We are selling shares of common stock, and the selling shareholders identified in this prospectus are selling shares of common stock. We will not receive any proceeds from the sale of shares by the selling shareholders.

Our common stock is listed on the New York Stock Exchange under the symbol "DPLO." On March 12, 2015, the closing price of our common stock as reported on the NYSE was $28.04.

We and the selling shareholders have each granted the underwriters an option to purchase up to an additional shares of common stock (an aggregate of shares of common stock).

Investing in our common stock involves risks. See "Risk Factors" beginning on page 20.

| |

Price to Public |

Underwriting Discounts and Commissions(1) |

Proceeds to Diplomat Pharmacy, Inc. |

Proceeds to the Selling Shareholders |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Per Share | $ | $ | $ | $ | |||||||||

| Total | $ | $ | $ | $ | |||||||||

- (1)

- We have agreed to reimburse the underwriters for certain expenses in connection with this offering. See "Underwriting (Conflicts of Interest)".

Delivery of the shares of common stock will be made on or about , 2015.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| Credit Suisse | Morgan Stanley | |||

J.P. Morgan |

Wells Fargo Securities |

|||

William Blair |

Leerink Partners |

Raymond James |

The date of this prospectus is , 2015.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus or to which we have referred you. None of us, the selling shareholders or the underwriters have authorized anyone to provide you with information that is different from that contained in this prospectus or any free-writing prospectus prepared by us or on our behalf. We do not, and the selling shareholders and the underwriters do not, take any responsibility for, and can provide no assurances as to, the reliability of any information that others provide to you. We and the selling shareholders are offering to sell, and seeking offers to buy, shares of common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the common stock.

For investors outside the United States: none of we, the selling shareholders or any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions related to this offering and the distribution of this prospectus outside of the United States.

This prospectus includes our trademarks and trade names, such as DIPLOMAT® and DIPLOMAT SPECIALTY PHARMACY®, which are protected under applicable intellectual property laws and are our property. This prospectus also contains trademarks, trade names and service marks of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, trade names and service marks. We do not intend our use or display of other parties' trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, endorsement or sponsorship of us by these other parties.

i

Certain information contained in this prospectus concerning our industry and the markets in which we operate is based on information from publicly available independent industry and research organizations and other third-party sources, and management estimates. Management estimates are derived from publicly available information released by independent industry and research analysts and third-party sources, as well as data from our internal research, and are based on assumptions made by us upon reviewing such data and our knowledge of such industry and markets, which we believe to be reasonable. We believe the data from these third-party sources is reliable. In addition, projections, assumptions and estimates of the future performance of the industry in which we operate and our future performance are necessarily subject to uncertainty and risk due to a variety of factors, including those described under "Risk Factors" and "Special Note Regarding Forward-Looking Statements." These and other factors could cause results to differ materially from those expressed in the estimates made by these third-party sources.

ii

This summary highlights information appearing elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should read the entire prospectus carefully, including the sections titled "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes included elsewhere in this prospectus. Unless the context suggests otherwise, references in this prospectus to "Diplomat," "the Company," "we," "us" and "our" refer to Diplomat and its consolidated subsidiaries.

Business Overview

We are the largest independent specialty pharmacy in the United States, and are focused on improving lives of patients with complex chronic diseases. Our patient-centric approach positions us at the center of the healthcare continuum for the treatment of complex chronic diseases through partnerships with patients, payors, pharmaceutical manufacturers and physicians. We offer a broad range of innovative solutions to address the dispensing, delivery, dosing and reimbursement of clinically intensive, high-cost specialty drugs. We believe that we are a chosen partner for leading biotechnology and pharmaceutical companies based on our ability to deliver customized support services and dispense new drugs to complex chronic disease patient populations. As a result, we believe we are well positioned to continue expanding our market share in the high growth $78 billion specialty pharmacy industry.

Diplomat has a long track record of growth and innovation. We were founded in 1975 by our Chief Executive Officer and Chairman, Philip Hagerman, and his father, Dale, both trained pharmacists who transformed our business from a traditional pharmacy into a leading specialty pharmacy. In 2005, we began to expand the scope of our specialty pharmacy business from a small, regional operation to a large national enterprise, allowing us to capitalize on the growth of the specialty pharmacy market from approximately $20 billion in sales in 2005 to $78 billion in sales in 2014, representing a compounded annual growth rate of approximately 16%. As a result, we have grown our revenues to over $2.2 billion in 2014, achieving a compounded annual growth rate of over 60% since 2005, with a 3% overall market share (based on 2014 revenues from pharmacy-dispensed specialty drugs). To achieve this growth, we have consistently strengthened our clinical expertise in key therapeutic categories, such as oncology, immunology and more recently specialty infusion, broadened the scope of our services to retailers, hospitals and health systems, and strengthened our relationships with patients, payors, pharmaceutical manufacturers and physicians.

We focus on specialty drugs that are typically administered on a recurring basis to treat patients with complex chronic diseases that require specialized handling and administration as part of their distribution process. We have expertise across a broad range of high-growth specialty therapeutic categories, including oncology, immunology, hepatitis, multiple sclerosis, HIV and specialty infusion therapy (which involves infusing specialty pharmaceuticals for rare and chronic genetic disorders, primarily for hemophilia and immune globulin treatment). Our comprehensive, patient-focused services ensure that patients receive a superior standard of care, including assistance with complicated medication therapies, refill processing, third-party funding support programs, side effect management and adherence monitoring. We customize solutions for each patient based on the patient's overall health, disease and family history, lifestyle and financial means. Although generally we do not track or quantify specific cost savings for patients and payors, we believe we reduce long term costs for patients and payors by improving patient care, enhancing clinical outcomes, managing high risk members, monitoring patient adherence, and optimizing the utilization of specialty drugs, many of which can cost well over $100,000 per patient, per year. Our value proposition to payors and patients has helped us expand our managed lives under contract from approximately 5 million in 2009 to approximately 13 million as of December 31, 2014. We define managed lives under contract as patients enrolled in a

1

managed care organization network, including pharmacy benefit managers, health plans, state governments, employer groups and unions with whom we contract, through exclusive and preferred relationships with such organizations, whereby we are the only authorized or one of a few preferred specialty pharmacy providers to the patients in their system.

Collectively, our ability to enhance patient adherence to complex drug regimens, collect and report data, and ensure effective dispensing of complex specialty medications supports the clinical and commercial needs of pharmaceutical manufacturers and physicians. Furthermore, our patient and provider support services ensure appropriate drug initiation, facilitate patient compliance and persistence, and capture important information regarding safety and effectiveness of the specialty medications that we dispense. Our services, together with our proactive engagement with pharmaceutical manufacturers early in the drug development process, have contributed to our current and growing access to limited distribution drugs, which we define as drugs that are only available for distribution by a select network of specialty pharmacies. Our inclusion in limited distribution networks provides critical sources of revenue growth and provides a catalyst for our future growth.

Our core revenues are derived from the customized care management programs we deliver to our patients, including the dispensing of their specialty medications. Because our core therapeutic categories generally require multi-year or life-long therapy, our singular focus on these complex chronic diseases helps drive recurring revenues and sustainable growth. Our revenues grow, in part, as we help more patients access the drugs they need in order to live longer and healthier lives. As a part of our mission to improve patient care, we provide specialty pharmacy support services to a national network of retailers and independent pharmacy groups, hospitals and health systems. For many of our retail, hospital and health system partners, we earn revenue by providing clinical and administrative support services on a fee-for-service basis to help them dispense specialty medications. Thus, our patient-focused solutions benefit multiple partners across the healthcare continuum, which we believe drives the sustainability of our business model.

Market Opportunity

Specialty pharmaceuticals represent a significant and growing total addressable market. The specialty pharmaceutical market has experienced significant growth in recent years as complex chronic conditions, care coordination, technology-enabled patient care, biotechnology research and outcomes-based healthcare have increased in focus. The total specialty pharmaceutical market represented approximately $92 billion in drug spend in 2012. We believe that our track record and leadership in limited distribution drug programs will create opportunities for us to gain market share in this growing segment of the specialty pharmacy market.

Specialty drugs are managed not only under the pharmacy benefit, but also under the medical benefit. Payors typically determine whether a particular specialty drug is covered under the pharmacy benefit versus the medical benefit based on such factors as the patient's ability to self-administer, the degree of clinical support required, the need for patient monitoring and the site of care (e.g., hospital or home). Total specialty pharmaceutical drug spend covered under the pharmacy benefit was approximately $51 billion in 2012 and is estimated to grow to $118 billion by 2018. Specialty drugs reimbursed under the medical benefit have also expanded rapidly in recent years and were approximately $39 billion, or approximately 45%, of the total specialty drug spend in 2012. Increasingly, drugs that have historically been reimbursed under the medical benefit are being moved to the pharmacy benefit by health plans and pharmacy benefit managers to better manage care and contain costs. While our historic focus has been pharmacy benefit, we believe that the medical benefit represents a significant additional revenue opportunity for us and expect it to have a bigger impact in our business going forward. Specifically, we view specialty infusion (which, for our purposes, includes infusion therapies for hemophilia, hereditary angioedema and immune globulins), with approximately 65% of the costs of such therapies covered under the medical benefit as of December 31, 2014, as an

2

attractive market due to significant projected growth and higher margins, and we intend to continue to invest in this important and growing area of our existing business.

Growth in specialty drug spend is significantly outpacing the broader pharmaceutical market. Specialty drugs are the fastest growing segment of the pharmaceutical market, and spend in this segment is estimated to grow at approximately 20% annually from 2013 to 2018, whereas traditional drug spend is expected to grow in the low to mid single digit percentage range. Specialty pharmaceutical products are targeted towards high-cost complex medical conditions, have fewer direct substitutes than traditional pharmaceuticals and face limited near-term generic market entry. These factors limit competition and drive higher prices. Additionally, specialty drug approvals comprised over 50% of all Federal Drug Administration ("FDA") drug approvals in 2013 as pharmaceutical and biotechnology companies have continued to invest in specialty drug development. This trend is expected to continue, driven by a robust pipeline of specialty drugs, which represent approximately 38% of the total number of drugs that we believe may receive FDA approval by March 2016.

Oncology and immunology, therapeutic categories in which we believe we are a leader, are large and growing therapeutic categories within the specialty pharmaceuticals industry. The oncology market represented 29% of specialty pharmaceutical sales in the U.S. in 2013. The immunology market, including the disease states rheumatoid arthritis, psoriasis and Crohn's disease, also represents a large and growing specialty market. Further, there are over 3,000 oncology and immunology drugs in global drug development. Given the chronic nature of these disease states, we provide recurring services to these patients over long periods of time. In 2014, we generated over 68% of our revenues in oncology and immunology, and our historical growth has largely been driven by our position as a leader in these categories.

Competitive Strengths

We are the nation's largest independent specialty pharmacy, with a 3% overall market share (based on 2014 revenues from pharmacy-dispensed specialty drugs). We believe we are well positioned to continue to increase our market share based on the following competitive strengths.

Adding value to all constituents. The value we deliver to all constituents is centered upon our core focus on patients. We help patients adhere to complicated medication therapies, process refills and manage any side effects and insurance concerns to ensure they get the best standard of care. The clinical efficacy of drug therapies, especially for acute and chronic conditions, is typically enhanced when patients precisely follow the prescribed treatment regimens (including dosing and frequency). We have achieved patient adherence rates of over 90% for the last six fiscal quarters. We believe our high adherence rates are due to, among other things, our patient training and education, compliance packaging, prophylactic starter kits and nurse adherence calls. We also help identify third-party funding support programs to help cover expensive out-of-pocket costs.

3

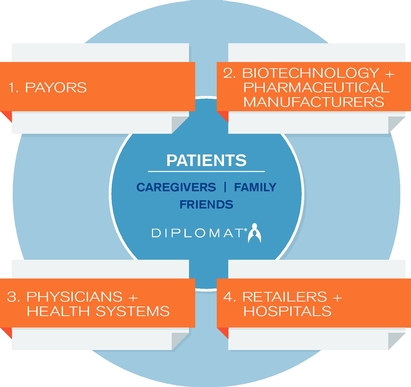

Supporting our core focus on patients, we also serve the following key constituents:

(1) Payors: We manage prescription regimens for chronically ill populations and help payors, which include insurance plans and pharmacy benefit managers, reduce costs through customized specialty pharmacy programs. Our electronic patient care platform, centered on our disease-specific technology solution, is customized for each payor's needs and is designed to improve efficiency and lower costs.

(2) Biotechnology and Pharmaceutical Manufacturers: We offer specialized and highly customized prescription programs for pharmaceutical companies to help them optimize and track patient adherence which helps drive the clinical and commercial success of specialty drugs. In addition, we partner with pharmaceutical manufacturers early by helping them develop specialty pharmaceutical channel strategies as part of their commercial launch preparation.

(3) Physicians and Health Systems: Our team works with physician offices to manage prior-authorization and other managed care organization requirements, such as denial and appeal process, to ensure that complicated administrative tasks do not impair the delivery of quality patient care. Additionally, we provide risk evaluation services, implement risk mitigation strategies and collect patient adherence data to provide physicians and health systems with enhanced visibility.

(4) Retailers and Hospitals: We provide clinical and administrative support services for our retail and hospital partners on a fee-for-service basis. Based on our broad industry experience, infrastructure and treatment-tracking software, our retail specialty network solution provides customized clinical and administrative support services that help retailers and their specialty patients improve financial outcomes. We provide hospitals with unique solutions to maximize cost containment, improve efficiency and clinical outcomes from specialty pharmaceuticals.

Significant and longstanding payor relationships—approximately 13 million managed lives under contract. We partner with regional and mid-sized payors and independent pharmacy benefit managers to improve patient outcomes and lower costs by managing high-risk members and implementing

4

patient-focused specialty programs. We offer payors access to limited distribution drugs and cost containment programs, including partial refill programs, clinical management and motivational interviewing techniques for improving adherence. We believe that medication non-adherence is the largest avoidable cost in specialty pharmacy because it contributes to a substantial worsening of disease and death and significantly increases hospital and other health care costs, and that our strong adherence rates benefit patients and payors. We believe that our focus on high-touch patient care, reflecting our therapy management and support services through multiple interactions by our clinical, operational and administrative personnel, and our experience with high-risk populations makes us well-positioned for the anticipated growth in managed lives under the Affordable Care Act, particularly with respect to managed Medicaid coverage.

Partner of choice for biotechnology and pharmaceutical manufacturers. We believe that our role as the partner of choice for many biotechnology and pharmaceutical manufacturers is based on the following attributes:

- •

- Expertise in managing limited distribution drugs. We have

historically earned access to many limited distribution drugs, both at the time of their launch and post-launch. We actively monitor the drug pipeline and we maintain dialogue with many of the major

biotechnology and pharmaceutical manufacturers to identify opportunities in all pre-commercial stages of drug development. We believe that limited distribution is becoming the delivery system of

choice for many drug manufacturers because it facilitates high patient engagement, clinical expertise and elevated focus on service. Furthermore, we believe that our innovative solutions and

service-oriented culture set us apart from our competitors, have enabled us to win a large number of limited distribution contracts and is more appealing than our competitors' platforms to emerging

biotechnology firms and the boutique consulting firms that advise them. We believe that the trend toward limited distribution of specialty drugs will continue to expand in the future. As of

December 31, 2014, we had a portfolio of over 80 limited distribution drugs, all of which are post-launch.

- •

- Proven track record of adding value. We believe we

outperform our competitors in providing services that benefit specialty drug manufacturers. Our superior services are driven by our clinical expertise in oncology, immunology, hepatitis, multiple

sclerosis, HIV and specialty infusion. We offer targeted pilot programs, full reporting capabilities and a variety of additional services that support patients' medication adherence when clinically

appropriate.

- •

- Breadth of channel partners. In addition to maintaining

our strong relationships with payors, physicians, manufacturers and patients, we also partner with retailers, hospitals and health systems by providing critical patient-facing clinical and

administrative services that help support the specialty pharmacy capabilities of these constituents. These partnerships broaden our exposure and influence across the healthcare continuum.

- •

- Relationships with clinical experts and key opinion leaders. Our singular focus on specialty pharmacy and complex chronic diseases has enabled us to develop strong relationships with clinical experts and thought leaders in key therapeutic categories, such as oncology and immunology. We leverage these relationships to gain greater visibility into future drug launches and to stay current on the latest advances in patient care.

National footprint with highly scalable infrastructure. During the past several years, we have made significant investments to expand our capabilities and capacity, which we believe will help us to enhance sales volume, improve efficiency and create significant barriers to entry. In December 2010, we moved our corporate headquarters to a 550,000 square foot facility in Flint, Michigan. Our operations within this facility are highly scalable as we currently utilize approximately 40% of the facility, giving us significant capacity to execute our long term growth plan without significant additional capital expenditures. Our physical footprint has enabled us to develop a centralized infrastructure that we have

5

successfully scaled to dispense to all 50 states. We now have an advanced distribution center that enables us to ship medications nationwide as well as a centralized clinical call center that helps us deliver localized services on a national scale. We are fully accredited and licensed to conduct business in each of the states that require such licensure.

Strong financial profile combines sustainable growth and low capital intensity. Our financial profile is comprised of a recurring revenue model that is driven by the chronically ill populations we serve. As a result, we have demonstrated strong growth in revenue and profitability. We have achieved consistent revenue and Adjusted EBITDA growth with revenues increasing from $578 million in 2010 to $2,215 million in 2014 and Adjusted EBITDA increasing from $8 million in 2010 to $35 million in 2014, representing compound annual growth rates of 40% and 46%, respectively. Net loss was $(8) million in 2010, which includes non-operating expenses of $11 million, and net income attributable to the Company was $5 million in 2014, which includes non-operating expenses of $3 million. See "Selected Consolidated Financial Data" for our definition of Adjusted EBITDA, why we present Adjusted EBITDA and a reconciliation of our Adjusted EBITDA to net income (loss) attributable to the Company. We expect our growth to continue to be driven by a highly visible and recurring base of revenues, favorable demographic trends, advanced clinical developments, expanding drug pipelines, earlier detection of chronic diseases, improved access to medical care, manufacturer price increases and mix shift toward higher-cost specialty drugs. In addition, we believe that our expanding breadth of services, our growing penetration with new customers, and our access to limited distribution drugs, will help us achieve significant and sustainable growth and profitability in future.

Highly experienced and passionate management team. Our senior management team, which consists of five executives, has an average of over 30 years of experience in the pharmacy and specialty pharmacy industry and represents a group of highly recognized and respected industry veterans. Led by our Chief Executive Officer and Chairman Philip Hagerman, our management team is responsible for our proven track record of growth, consistent performance and industry leading service. Mr. Hagerman, a licensed pharmacist and recognized specialty pharmacy industry thought-leader, is a frequent speaker at state and national pharmacy conferences and has received several awards as a leading business executive in the country, including recognition by the White House Business Council for his leadership in job creation and community development. Our senior management team has an average tenure with Diplomat of over 15 years and brings a healthy balance of significant experience with Diplomat and with other companies in the industry, including public companies.

Growth Strategy

We plan to grow our business by continuing to execute on the following key growth strategies:

Capitalize on track record to expand leadership positions in high-growth oncology and limited distribution markets. We believe our track record of providing a customized, high level of service to our manufacturer partners in the oncology and immunology markets has led to repeat contract awards and initial limited distribution contracts related to new drugs our partners bring to market. In addition, our clinical and sales teams consistently engage our emerging biotechnology partners on commercialization strategy 12 to 18 months in advance of potential FDA approval. These pre-existing relationships position us to capture market share in these high-growth markets.

Expand clinical expertise to a broad range of therapeutic categories. We serve a broad range of therapeutic categories, and we believe we can expand our clinical expertise to increasingly penetrate additional markets such as hepatitis, multiple sclerosis, HIV and specialty infusion. We believe these categories will become increasingly important to our patient population in the coming years due to advancement of therapies and increased incidences of chronic illness and that our platform will allow us to grow with market expansion. Specifically, we view specialty infusion as an attractive market due to

6

significant projected growth and higher margins, and we intend to continue to invest in this important and growing area of our existing business. See "Recent Developments—Acquisitions."

Deepen and expand partner relationships. We currently contract with and support regional and mid-sized payors and independent pharmacy benefit managers, employer groups, and union groups representing approximately 13 million managed lives across the United States. We plan to continue to work with our current clients to grow their membership and are focused on expanding our client base nationally. In addition to providing specialty pharmacy services for self-administered medications covered under the pharmacy benefit, we also offer office-administered medications covered under the medical benefit to ensure that we provide a full spectrum of care to our specialty patients regardless of type of their benefit coverage and where they receive care. Further, our partnerships with retail pharmacies and hospitals allow us to serve specialty patients beyond the traditional specialty pharmacy approach. These partnerships allow patients to more easily access specialty medications in the retail setting and also positions Diplomat to be a key partner for Accountable Care Organizations, which are networks formed by groups of doctors, hospitals, and other health care providers that share financial and medical coordination of services to patients to limit unnecessary spending and to create an efficient patient care system.

Grow high-margin businesses and capitalize on investments to enhance key operating metrics. In May 2014, we contracted to significantly expand our retail customer base and expand our opportunities through a service contract with Novation, LLC (which includes Provista, LLC and VHA Inc.), one of the largest hospital networks and group purchasing organizations. In addition, our continued expansion into the infusion market will provide us with opportunities to capitalize on a market which historically has provided higher margins. We have made significant investments in our technology, infrastructure and service lines to build a scalable foundation for growth, which we believe provides meaningful opportunities to grow revenues and enhance key operating metrics.

Selectively pursue growth through strategic acquisitions. We believe the specialty pharmacy industry is highly fragmented and provides numerous opportunities to expand through acquisitions. While we will continue to focus on growing our business organically, we believe we can opportunistically enhance our competitive position through complementary acquisitions in both existing and new markets. For example, in December 2013, we completed the acquisition of American Homecare Federation, Inc. ("AHF"), a specialty infusion therapy provider focused primarily on hemophilia. In June 2014, we acquired MedPro Rx, Inc. ("MedPro"), a specialty pharmacy focused on specialty infusion therapies including hemophilia and immune globulin. In February 2015, we executed a definitive purchase agreement to acquire BioRx, LLC ("BioRx"), a highly specialized pharmacy and infusion services company that provides treatments for patients with ultra-orphan and rare, chronic diseases. We expect the BioRx acquisition to close shortly after this offering is completed. Additionally, we plan to selectively evaluate potential acquisition opportunities in other therapeutic categories, services and technologies, with the goal of preserving our culture, optimizing patient outcomes, enhancing value to other constituents and building long-term value for our shareholders.

Risk Factors

Investing in our common stock involves a high degree of risk. You should carefully consider the risks described under "Risk Factors" before making a decision to invest in our common stock. If any of these risks actually occurs, our business, results of operations, financial condition or prospects could be materially and adversely affected. Below is a summary of some of the principal risks we believe we face:

- •

- anticipating and adapting to significant changes, trends, consolidation and increasing participation in the specialty pharmacy industry could adversely impact our ability to compete;

7

- •

- pricing pressures from payors and pharmaceutical manufacturers may adversely affect our profitability;

- •

- failure to maintain our existing relationships, and build new relationships, with key pharmaceutical manufacturers, physicians,

payors, retailers, hospital and health systems would have a material and adverse effect on our business;

- •

- complying with, and changes to, significant state and federal regulations could restrict our ability to conduct our business or cause

us to incur significant costs;

- •

- we may not have the resources, purchasing power or operating efficiencies to compete successfully with leading specialty pharmacies;

- •

- any significant adverse matters regarding the top specialty drugs we dispense, or disruptions in the supply chain of these specialty

drugs, would have a material and adverse impact on our business and financial performance;

- •

- we may not be able to successfully implement our organic growth or acquisition strategy;

- •

- we may not be able to successfully consummate the pending acquisition of BioRx, LLC or realize the expected benefits therefrom;

and

- •

- our inability to identify and remediate any future material weaknesses in our internal control over financial reporting, which would impair our ability to produce accurate and timely financial statements.

Recent Developments

Initial Public Offering

In October 2014, we completed our initial public offering ("IPO") in which 15,333,333 shares of common stock were sold at a public offering price of $13.00 per share. We sold 11,000,000 shares of common stock and certain selling shareholders sold 4,333,333 shares of common stock. We did not receive any proceeds from the sale of common stock by the selling shareholders. We received net proceeds of $130.4 million after deducting underwriting discounts and commissions of $9.7 million, and other offering expenses of $2.9 million. Proceeds of $80.4 million were used to repay existing indebtedness to certain current or former shareholders and employees ($19.8 million), and borrowings under the revolving line of credit ($60.6 million). The remaining net proceeds of $50.0 million continue to be used for working capital and other general corporate purposes.

Acquisitions

On December 16, 2013, we acquired all of the outstanding stock of AHF, a specialty pharmacy focused on providing clotting medications, ancillaries and supplies to individuals with bleeding disorders, for a total acquisition price of approximately $13.4 million, excluding related acquisition costs. Included in the total acquisition price is $12.1 million in cash and contingent consideration with a maximum payout of $2.0 million (fair valued at $1.3 million as of the acquisition date and at $1.8 million as of December 31, 2014). The results of operations for AHF are included in our consolidated financial statements from the acquisition date.

On June 27, 2014, we acquired all of the outstanding stock of MedPro, a specialty pharmacy focused on specialty infusion therapies, including hemophilia and immune globulin, for a total acquisition price of approximately $68.5 million, excluding related acquisition costs. Included in the total acquisition price is $52.3 million in cash, 716,695 shares of our Class B Nonvoting Common Stock valued at approximately $12.0 million, and contingent consideration with a maximum payout of $11.5 million (fair valued at $4.2 million as of the acquisition date and at $9.9 million as of

8

December 31, 2014). The results of operations for MedPro are included in our consolidated financial statements from the acquisition date.

On February 26, 2015, we executed a definitive purchase agreement which provides that, upon the terms and conditions set forth therein, we will acquire all of the outstanding equity interests of BioRx. BioRx provides patients with personalized medication programs and services for a variety of complex disease states, including hemophilia, hereditary angioedema, immunology, nutrition and digestive disorders and alpha-1 antitrypsin deficiency. BioRx reaches patients in all 50 states and operates dispensing facilities in Ohio, Massachusetts, North Carolina, Iowa, Minnesota, Arizona and California. The acquisition is expected to close shortly after the completion of this offering in March or April 2015. In 2014, BioRx generated approximately $227 million in revenue and $23 million in EBITDA. Diplomat will purchase BioRx for $210 million cash and 4,050,926 shares of common stock upon the closing of the transaction. The transaction will provide Diplomat with an expected future tax benefit of approximately $50 million. Under the terms of a one year contingent earn out, BioRx can earn up to an additional 1,350,309 shares of common stock upon achieving an EBITDA-based metric. All recipients of common stock will be subject to certain lock-up restrictions on such shares for at least six months after the closing. See "Risk Factors—Risks Related to Our Pending Acquisition of BioRx."

We anticipate our future revenues derived from specialty infusion pharmacy services will increase significantly as a percentage of total revenues as a result of such acquisitions.

Debt

On June 26, 2014, we entered into an amended and restated credit agreement with GE Capital Bank, as agent, Comerica Bank, JP Morgan Chase Bank, N.A. and Wells Fargo Bank, N.A., as additional lenders. The amended and restated credit agreement provides an increase in our revolving line of credit (the "revolving line of credit" or "line of credit") to $120.0 million. The amount available for borrowing under the revolving line of credit is the lesser of $120.0 million and the sum of 85% of eligible accounts receivable and a portion of eligible inventory, less any outstanding letters of credit and swing loans. Additionally, our revolving line of credit permits incremental increases in the line of credit or issuance of term loans up to an aggregate amount of $25.0 million, subject to specified conditions.

In connection with the BioRx acquisition, we have obtained committed financing from GE Capital Bank to increase the line of credit to $150.0 million and to enter into a Term Loan A for $120.0 million (the "new credit facility"). We expect that the new credit facility will provide for the issuance of letters of credit up to $10.0 million and swingline loans up to $10.0 million, the issuance and incurrence of which will reduce the availability of the line of credit. We expect that the new credit facility will provide two interest rate options, (i) LIBOR (as defined) plus 3.00% or (ii) Base Rate (as defined) plus 2.00%, provided, however, that interest with respect to the revolving credit facility may reduce after a certain period of time based on changes in our leverage ratio. Subject to market conditions, we expect to fund the cash component of the BioRx purchase price with borrowings under the new credit facility.

For a further description of our debt, see "Description of Indebtedness."

Issuances of Preferred Stock

On January 23, 2014, we sold to certain funds of T. Rowe Price 2,986,228 shares of Series A Preferred Stock at a purchase price of $16.74 per share. We used $20.0 million of the $50.0 million investment proceeds for general corporate purposes, including fees associated with the transaction, and the remaining $30.0 million was used to redeem shares of common stock and common stock options.

On April 1, 2014, we sold to certain funds of Janus Capital Group 3,225,127 shares of Series A Preferred Stock at a purchase price of $16.74 per share. We used $25.2 million of the $54.0 million

9

investment proceeds for general corporate purposes, including fees associated with the transaction, and the remaining $28.8 million was used to redeem shares of common stock and common stock options.

All shares of Series A Preferred Stock converted into shares of our common stock on an one-for-one basis immediately prior to the completion of our IPO.

Our Corporate Information

Diplomat Pharmacy, Inc. is a Michigan corporation, and our principal executive offices are located at 4100 S. Saginaw St., Flint, Michigan 48507. Our telephone number is (888) 720-4450. Our website address is www.diplomat.is. The reference to our website is intended to be an inactive textual reference only. The information contained on, or accessible through, our website is not part of this prospectus or the registration statement of which this prospectus forms a part, and you should not rely on this information in making a decision to invest in our common stock in this offering.

10

Common stock offered by us |

shares(1) | |

Common stock offered by the selling shareholders |

shares(2) |

|

Common stock to be outstanding immediately after this offering |

shares |

|

Option to purchase additional shares from us and the selling shareholders |

The underwriters have an option to purchase a maximum of additional shares of common stock from us and an additional shares of common stock from the selling shareholders (an aggregate of shares of common stock). The underwriters may exercise this option at any time within 30 days from the date of this prospectus. |

|

Use of proceeds |

The net proceeds to us from this offering, after deducting the underwriting discount and estimated offering expenses, will be approximately $ million. We will not receive any proceeds from the sale of shares by the selling shareholders, including sales by the selling shareholders pursuant to the underwriters' option to purchase additional shares from them. The selling shareholders will not be responsible for any offering expenses, other than their proportionate share of the underwriting discounts and commissions. |

|

|

The principal purposes of this offering are to increase our capitalization and financial flexibility. We intend to use the net proceeds from this offering (including the net proceeds available in the event the underwriters exercise their option to purchase additional shares of our common stock from us) for working capital, other general corporate purposes and, if required by the terms of our new credit facility or at our option, to pay down future borrowings under our new credit facility. In addition, we may use a portion of the proceeds from this offering for future business acquisitions. |

|

|

In addition, we intend to use approximately $ million of the net proceeds from this offering to repurchase approximately options to purchase our common stock held by a number of our current and former employees, including certain of our executive officers (the "option repurchase"). The purchase price for the option repurchase will be based on the price per share of our common stock in this offering, net of the underwriting discount and exercise price. See "Use of Proceeds." |

(1)- We

have not determined the final allocation among us and the selling shareholders of the shares of common stock to be offered pursuant to this Registration Statement. We expect,

however, that we will offer approximately 65% of the shares. Of the primary proceeds, approximately $30 million (net of exercise price, and prior to application of the underwriting discount and

applicable withholding taxes) will be used to repurchase options as described herein. See "Use of Proceeds."

(2)- We have not determined the final allocation among us and the selling shareholders of the shares of common stock to be offered pursuant to this Registration Statement. We expect, however, that the selling shareholders will offer approximately 35% of the shares.

11

|

Because we expect to use a portion of the proceeds of this offering to pay down future borrowings under our new credit facility and certain affiliates of the underwriters are expected to be lenders under our new credit facility, we expect a "conflict of interest" may be deemed to exist under FINRA Rule 5121(f)(5)(C)(i), and this offering will be made in compliance with the applicable provisions of FINRA Rule 5121. See "Underwriting (Conflicts of Interest)—Conflicts of Interest". |

|

Dividend policy |

We expect to retain all future earnings, if any, for use in the operation and expansion of our business and do not anticipate paying any cash dividends in the foreseeable future. See "Dividend Policy." |

|

Risk factors |

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 20 of this prospectus for a discussion of the risks and uncertainties you should carefully consider before deciding to invest in our common stock. |

|

New York Stock Exchange symbol |

"DPLO" |

The number of shares of our common stock to be outstanding after the completion of this offering is based on 51,457,023 shares of our common stock outstanding as of December 31, 2014, and excludes:

- •

- 6,235,331 shares of our common stock issuable upon the exercise of options outstanding as of December 31, 2014 under the

Diplomat Pharmacy, Inc. 2007 Option Plan (the "2007 Option Plan"), with a weighted average exercise price of $6.69 per share (including approximately shares underlying the

option repurchase);

- •

- 982,000 shares of our common stock issuable upon the exercise of options outstanding as of December 31, 2014 under our 2014

Omnibus Incentive Plan (the "2014 Omnibus Plan" or the "omnibus plan"), with a weighted average exercise price of $13.00 per share (including approximately shares underlying the

option

repurchase);

- •

- 3,009,723 shares of our common stock reserved for future issuance under our 2014 Omnibus Plan;

- •

- 4,050,926 shares of our common stock issuable to certain equity owners of BioRx upon consummation of the BioRx acquisition; and

- •

- 1,350,309 shares of our common stock issuable to certain equity owners of BioRx in the event certain financial metrics are achieved within 12 months of the consummation of the BioRx acquisition.

Except as otherwise indicated, information in this prospectus reflects or assumes no exercise by the underwriters of their option to purchase up to an additional shares of common stock in the aggregate from us and the selling shareholders in this offering.

All share and per share information referenced throughout this prospectus has been retroactively adjusted to reflect a series of transactions that occurred immediately prior to the closing of our IPO on

12

October 16, 2014: (i) the conversion of all shares of our Series A Preferred Stock into shares of our Class C Voting Common Stock on a one-for-one basis; (ii) the filing of our amended and restated articles of incorporation and the adoption of our amended and restated bylaws; (iii) the conversion of the Class A, Class B and Class C Common Stock into shares of our common stock on a one-for-one basis; (iv) the conversion of all options to acquire Class A Voting Common Stock and Class B Nonvoting Common Stock into options to acquire shares of our common stock on a one-for one basis; and (v) a stock split effected as a stock dividend of 8,500 shares for each share of our common stock, with proportionate adjustments to the number of options to acquire shares of our common stock and the exercise price therefor.

Accordingly, all share and per share amounts presented in this prospectus have been adjusted, where applicable, to reflect such conversions and stock dividend. Nevertheless, this prospectus retains references to terminology of Class A Voting Common Stock, Class B Nonvoting Common Stock, Class C Voting Common Stock and Series A Preferred Stock to the extent referring to transactions occurring prior to the closing of our IPO.

13

Summary Consolidated Financial Data

The following table summarizes our consolidated financial data and other data for the periods and at the dates indicated. We derived the consolidated statement of operations data for the years ended December 31, 2014, 2013 and 2012 and the consolidated balance sheet data as of December 31, 2014 and 2013 from our audited consolidated financial statements included elsewhere in this prospectus. We derived the consolidated balance sheet data as of December 31, 2012 from our audited consolidated financial statements that do not appear in this prospectus.

We derived the unaudited pro forma financial information for the year ended December 31, 2014 from the unaudited pro forma financial information included elsewhere in this prospectus.

Our historical results are not necessarily indicative of the results to be expected for any future period. The following information should be read together with the information under the headings "Capitalization" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes included elsewhere in this prospectus. The unaudited pro forma consolidated financial information does not necessarily represent what our financial position, results of operations and other data would have been if the transactions given effect to therein had actually been completed on the dates indicated, and is not intended to project such information for any future period. See "Use of Proceeds" and "Index to the Consolidated Financial Statements—Unaudited Pro Forma Consolidated Financial Information".

14

| |

For the year ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 Pro-Forma(1) |

2014(2) | 2013(3) | 2012 | |||||||||

| |

(Dollars in thousands, except per share and per prescription data) |

||||||||||||

| |

(Unaudited) |

|

|

|

|||||||||

Consolidated Statements of Operations Data |

|||||||||||||

Net sales |

$ | 2,485,898 | $ | 2,214,956 | $ | 1,515,139 | $ | 1,126,943 | |||||

Cost of goods sold |

(2,269,915 | ) | (2,074,817 | ) | (1,426,112 | ) | (1,057,608 | ) | |||||

| | | | | | | | | | | | | | |

Gross profit |

215,983 | 140,139 | 89,027 | 69,335 | |||||||||

Selling, general and administrative expenses |

(127,556 | ) | (77,944 | ) | (64,392 | ) | |||||||

| | | | | | | | | | | | | | |

Income from operations |

12,583 | 11,083 | 4,943 | ||||||||||

Interest expense |

(8,474 | ) | (2,528 | ) | (1,996 | ) | (1,086 | ) | |||||

Change in fair value of redeemable common shares |

— | 9,073 | (34,348 | ) | (6,566 | ) | |||||||

Termination of existing stock redemption agreement |

(4,842 | ) | (4,842 | ) | — | — | |||||||

Equity loss and impairment of non-consolidated entity |

(6,208 | ) | (6,208 | ) | (1,055 | ) | (267 | ) | |||||

Other income |

1,242 | 1,128 | 196 | 337 | |||||||||

| | | | | | | | | | | | | | |

Income (loss) before income taxes |

9,206 | (26,120 | ) | (2,639 | ) | ||||||||

Income tax expense(4) |

(4,655 | ) | — | — | |||||||||

| | | | | | | | | | | | | | |

Net income (loss) |

4,551 | (26,120 | ) | (2,639 | ) | ||||||||

Less: net loss attributable to noncontrolling interest |

(225 | ) | (225 | ) | — | — | |||||||

| | | | | | | | | | | | | | |

Net income (loss) attributable to Diplomat Pharmacy |

4,776 | (26,120 | ) | (2,639 | ) | ||||||||

Net income allocable to preferred shareholders(16) |

— | 458 | — | — | |||||||||

| | | | | | | | | | | | | | |

Net income (loss) allocable to common shareholders |

$ | $ | 4,318 | $ | (26,120 | ) | $ | (2,639 | ) | ||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Net income (loss) per common share(5): |

|||||||||||||

Basic |

$ | $ | 0.12 | $ | (0.79 | ) | $ | (0.08 | ) | ||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Diluted |

$ | $ | 0.11 | $ | (0.79 | ) | $ | (0.08 | ) | ||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Weighted average common shares outstanding(5): |

|||||||||||||

Basic |

35,990,122 | 33,141,500 | 33,141,500 | ||||||||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Diluted |

38,535,325 | 33,141,500 | 33,141,500 | ||||||||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Other Data (Unaudited) |

|||||||||||||

Adjusted EBITDA(6) |

$ | $ | 35,163 | $ | 18,970 | $ | 10,852 | ||||||

Prescriptions dispensed(7) |

894,000 |

797,000 |

722,000 |

680,000 |

|||||||||

Prescriptions serviced (not dispensed)(8) |

212,000 | 212,000 | 208,000 | 118,000 | |||||||||

| | | | | | | | | | | | | | |

Total prescriptions |

1,106,000 | 1,009,000 | 930,000 | 798,000 | |||||||||

| | | | | | | | | | | | | | |

Net sales per prescription dispensed(9) |

$ | 2,771 | $ | 2,770 | $ | 2,090 | $ | 1,652 | |||||

Gross profit per prescription dispensed(10) |

$ | 234 | $ | 167 | $ | 116 | $ | 97 | |||||

Net sales per prescription serviced (not dispensed)(11) |

$ | 27 | $ | 27 | $ | 27 | $ | 29 | |||||

Gross profit per prescription serviced (not dispensed)(11) |

$ | 27 | $ | 27 | $ | 27 | $ | 29 | |||||

Adjusted EBITDA per prescription(12) |

$ | $ | 35 | $ | 20 | $ | 14 | ||||||

15

| |

As of December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 Pro-Forma(13) |

2014 | 2013 | 2012 | |||||||||

| |

(Dollars in thousands) |

||||||||||||

| |

(Unaudited) |

|

|

|

|||||||||

Consolidated Balance Sheet Data |

|||||||||||||

Property and equipment, net |

$ | 14,447 | $ | 13,150 | $ | 12,378 | $ | 12,634 | |||||

Total assets |

390,086 | 211,777 | 139,595 | ||||||||||

Total debt (including short-term debt and current portion of long-term debt)(14)(15) |

210,000 | — | 88,164 | 63,102 | |||||||||

Total liabilities |

492,927 | 221,359 | 289,559 | 191,157 | |||||||||

Shareholders' equity (deficit)(14)(16) |

168,727 | (77,782 | ) | (51,562 | ) | ||||||||

- (1)

- The

unaudited pro forma consolidated financial information for the year ended December 31, 2014 gives effect to: (A) the January and April

2014 issuance of preferred stock and the use of a portion of the proceeds therefrom to redeem outstanding shares of common stock and common stock options, (B) our acquisition of MedPro in June

2014 and related borrowings under our line of credit, (C) our conversion from an S-corporation to a C-corporation on January 23, 2014, (D) the conversion of all outstanding shares

of our capital stock into shares of our common stock, and immediately thereafter a stock split effected as a stock dividend of 8,500 shares for each share of our common stock, (E) our IPO on

October 9, 2014 and the use of proceeds therefrom, (F) our probable acquisition of BioRx and related borrowings under the new credit facility as currently contemplated and

(G) this offering and the use of proceeds therefrom, assuming in each case that such event occurred on January 1, 2014. See "Index to the Consolidated Financial

Statements—Unaudited Pro Forma Combined Consolidated Financial Information".

- (2)

- We

acquired MedPro on June 27, 2014 and its financial results have been included in our historical financial statements since such date.

- (3)

- We

acquired AHF on December 16, 2013 and its financial results have been included in our historical financial statements since that date.

- (4)

- Prior

to January 23, 2014, we had elected to be taxed under the provisions of Subchapter S of the Internal Revenue Code. Therefore, we did not

pay corporate income taxes on our taxable income. Instead, our shareholders were liable for individual income taxes on their respective shares of our taxable income. On January 23, 2014, we

changed from an S-corporation to a C-corporation, and therefore we now pay corporate income taxes on our taxable income for periods after January 23, 2014.

- (5)

- All

share and per share amounts presented have been adjusted to reflect the applicable conversions of capital stock and the 8,500 to one stock split,

effected in the form of a stock dividend, occurring immediately prior to the completion of the IPO.

- (6)

- See

"—Adjusted EBITDA" below for our definition of Adjusted EBITDA, why we present Adjusted EBITDA and a reconciliation of net income (loss)

attributable to the Company to Adjusted EBITDA.

- (7)

- Prescriptions

dispensed (rounded to nearest thousand) represents actual prescriptions filled and dispensed by Diplomat.

- (8)

- Prescriptions

serviced (not dispensed) (rounded to nearest thousand) represents prescriptions filled and dispensed by a non-Diplomat pharmacy, including

retailers and health systems, for which we provide support services required to assist patients and pharmacies with the complexity of filling specialty medications, and for which we earn a fee.

- (9)

- Net sales per prescription dispensed represents total prescription revenue from prescriptions dispensed by Diplomat, divided by the number of prescriptions dispensed by Diplomat. Total prescription revenue from prescriptions dispensed includes all revenue collected from patients, third party payors and various

16

patient assistance programs, as well as revenue collected from pharmaceutical manufacturers for data and other services directly tied to the actual dispensing of their drug(s).

- (10)

- Gross

profit per prescription dispensed represents gross profit from prescriptions dispensed by Diplomat, divided by the number of prescriptions dispensed

by Diplomat. Gross profit represents total prescription revenue from prescriptions dispensed less the cost of the drugs purchased.

- (11)

- Net

sales per prescription serviced (not dispensed) represents total prescription revenue from prescriptions serviced divided by the number of

prescriptions serviced for the non-Diplomat pharmacies. Gross profit per prescription serviced (not dispensed) is equal to net sales per prescription serviced because there is no Diplomat drug cost of

goods sold associated with such transactions. Total prescription revenue from prescriptions serviced includes revenue collected from partner pharmacies, including retailers and health systems, for

support services rendered to their patients.

- (12)

- Adjusted

EBITDA per prescription is Adjusted EBITDA divided by the total number of prescriptions dispensed or serviced.

- (13)

- The

unaudited pro forma consolidated financial information as of December 31, 2014 gives effect to: (A) our probable acquisition of

BioRx and related borrowings under the new credit facility as currently contemplated and (B) this offering and the use of proceeds therefrom, assuming in each case that such event occurred on

December 31, 2014. See "Index to the Consolidated Financial Statements—Unaudited Pro Forma Combined Consolidated Financial Information".

- (14)

- We

received net proceeds of $130,440 from our IPO that were credited to shareholders' equity in October 2014. Proceeds of $80,458 were used to repay

outstanding indebtedness to certain current or former stakeholders and employees, and borrowings under the revolving line of credit.

- (15)

- In

2012, we entered into settlement agreements with current or former shareholders whereby we purchased shares of common stock formerly owned by the

shareholders for consideration of $29,393 of which $2,851 was paid in cash, forgiveness of note of $196 and the remaining $26,346 was payable in full, as per the terms of an executed promissory note,

maturing 2017, which were repaid using IPO proceeds.

- (16)

- In January 2014, we sold to certain funds of T. Rowe Price, 2,986,228 shares of Series A Preferred stock at a purchase price of $16.74 per share. We used $20,000 of the $50,000 investment proceeds for general corporate purposes, including fees associated with the transaction, and the remaining $30,000 was used to redeem shares of common stock and common stock options. Further, in April 2014, we sold to certain funds of Janus Capital Group 3,225,127 shares of Series A preferred stock at a purchase price of $16.74 per share. We used $25,200 of the $54,000 investment for general corporate purposes, including fees associated with the transaction, and the remaining $28,800 was used to redeem shares of common stock and common stock options. These redemptions decreased our shareholders' equity by $58,800 in the year ended December 31, 2014. All shares of Series A Preferred Stock converted into common stock on a one-for-one basis immediately prior to the completion of our IPO.

Adjusted EBITDA

We define Adjusted EBITDA as net income (loss) before interest expense, income taxes, depreciation and amortization, share-based compensation, restructuring and impairment charges, equity loss and impairment of non-consolidated entities, and certain other items that we do not consider indicative of our ongoing operating performance (which items are itemized below). Adjusted EBITDA is a non-GAAP financial measure.

We consider Adjusted EBITDA to be a supplemental measure of our operating performance. We present Adjusted EBITDA because it is used by our Board of Directors (the "Board of Directors" or "Board") and management to evaluate our operating performance. It is also used as a factor in determining incentive compensation, for budgetary planning and forecasting overall financial and operational expectations, for identifying underlying trends and for evaluating the effectiveness of our

17

business strategies. Further, we believe it assists us, as well as investors, in comparing performance from period to period on a consistent basis. Adjusted EBITDA is not in accordance with, or an alternative to, measures prepared in accordance with accounting principles generally accepted in the United States ("GAAP"). In addition, this non-GAAP measure is not based on any comprehensive set of accounting rules or principles.

As a non-GAAP measure, Adjusted EBITDA has limitations in that it does not reflect all of the amounts associated with our results of operations as determined in accordance with GAAP and therefore you should not consider Adjusted EBITDA in isolation from, or as a substitute for, financial information prepared in accordance with GAAP. You should be aware that in the future we may incur expenses that are the same as or similar to some of the adjustments in the presentation, and we do not infer that our future results will be unaffected by unusual or non-recurring items. Adjusted EBITDA does not:

- •

- include depreciation expense from property and equipment or amortization expense from acquired intangible assets (and although they

are non-cash charges, the assets being depreciated/amortized will often have to be replaced in the future);

- •

- reflect interest expense on our debt and capital leases or interest income we earn on cash and cash equivalents;

- •

- reflect the amounts we paid in taxes or other components of our tax provision (which reduces cash available to us);

- •

- reflect certain expenses associated with our acquisition activities;

- •

- include the impact of share-based compensation (which is a recurring expense that will remain a key element of our long-term incentive

compensation package, although we exclude it when evaluating our operating performance for a particular period); or

- •

- include the restructuring and impairment charges, equity income or loss of our non-consolidated entity, or other matters we do not consider to be indicative of our ongoing operations.

Further, other companies in our industry may calculate Adjusted EBITDA differently than we do and these calculations may not be comparable to our Adjusted EBITDA metric. Because of these limitations, you should consider Adjusted EBITDA alongside other financial performance measures, including net income (loss) attributable to the Company and our financial results presented in accordance with GAAP.

18

The table below presents a reconciliation of net income (loss) attributable to the Company to Adjusted EBITDA for the periods indicated:

| |

For the year ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 Pro-Forma |

2014 | 2013 | 2012 | |||||||||

| |

(Dollars in thousands) |

||||||||||||

| |

(Unaudited) |

|

|

|

|||||||||

Net income (loss) attributable to Diplomat |

$ | $ | 4,776 | $ | (26,120 | ) | $ | (2,639 | ) | ||||

Depreciation and amortization |

30,495 | 8,139 | 3,934 | 3,842 | |||||||||

Interest expense |

8,474 | 2,528 | 1,996 | 1,086 | |||||||||

Income tax expense |

4,655 | — | — | ||||||||||

| | | | | | | | | | | | | | |

EBITDA |

20,098 | (20,190 | ) | 2,289 | |||||||||

| | | | | | | | | | | | | | |

Share-based compensation expense(1) |

2,954 | 2,871 | 886 | 915 | |||||||||

Change in fair value of redeemable common shares |

— | (9,073 | ) | 34,348 | 6,566 | ||||||||

Restructuring and impairment charges(2) |

— | — | 1,033 | 424 | |||||||||

Equity loss and impairment of non-consolidated entities(3) |

6,208 | 6,208 | 1,055 | 267 | |||||||||

Severance and related fees(4) |

363 | 363 | 205 | 412 | |||||||||

Contingent consideration and merger and acquisition related fees(5) |

12,256 | 7,238 | 677 | — | |||||||||

Private company expenses(6) |

180 | 180 | 222 | — | |||||||||

Other taxes and credits(7) |

1,005 | 1,005 | — | (148 | ) | ||||||||

Termination of existing stock redemption agreement |

4,842 | 4,842 | — | — | |||||||||

Other items(8) |

1,431 | 1,431 | 734 | 127 | |||||||||

| | | | | | | | | | | | | | |

Adjusted EBITDA |

$ | $ | 35,163 | $ | 18,970 | $ | 10,852 | ||||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

- (1)

- Share-based

compensation expense relates to director and employee share-based awards.

- (2)

- Restructuring

and impairment charges reflect decreases in the fair market value of non-core property and assets, or actual losses on disposal of such

assets. 2013 charges primarily relate to the $932 write-down of our former Swartz Creek, Michigan headquarters facility to its fair value, after we vacated it in favor of our present Flint, Michigan

facility. 2012 charges primarily relate to our write-down of an externally purchased software package we no longer utilize, as well as sales of Company-owned vehicles.

- (3)

- During

the fourth quarter of 2014, we reassessed the recoverability of our investment in our non-consolidated entity, Ageology. Based upon this assessment,

we determined that a full impairment of $4,869 was warranted, primarily due to updated projections of continuing losses into the foreseeable future. The remaining amounts in 2014, 2013 and 2012

represents our share of losses recognized by Ageology, using the equity method of accounting. We first invested in Ageology, an anti-aging physician network dedicated to nutrition, fitness and

hormones, in October 2011, in connection with its formation.

- (4)

- Employee

severance and related fees primarily relates to severance for former management.

- (5)

- Fees

and expenses directly related to merger and acquisition activities, including our acquisitions of AHF and MedPro and the impact of changes in the fair

value of related contingent consideration liabilities.

- (6)

- Primarily

includes philanthropic activities performed at the direction of our majority shareholder.

- (7)

- Represents

(a) various tax credits received from the state of Michigan for facility improvement and employee hiring initiatives, (b) the

one-time costs associated with converting from an S-corporation to a C-corporation, and (c) a 2014 charge of $1,825 related to non-income tax obligations.

- (8)

- Includes other expenses, including information technology ("IT") operating leases. These operating leases were initiated, in lieu of purchases or capital leases for a subset of our IT spend, for a short period of time in 2013 and 2014 for liquidity purposes. We have since discontinued the practice of leasing IT equipment. The cost of purchased IT equipment is reflected in depreciation and amortization.

19

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, together with the other information in this prospectus, including "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and related notes, before deciding whether to invest in shares of our common stock. If any of the following risks actually occurs, our business, results of operations, financial condition or prospects could be materially and adversely affected. In that event, the trading price of our common stock could decline and you could lose part or all of your investment.

Risks Related to Our Business and Industry

Our failure to anticipate or appropriately adapt to changes or trends within the specialty pharmacy industry could have a significant negative impact on our ability to compete successfully.

The specialty pharmacy industry is growing and evolving rapidly. Any significant shifts in the structure of the specialty pharmacy industry or the healthcare products and services industry in general could alter the industry dynamics and adversely affect our ability to attract or retain customers. These changes or trends could result from, among other things, a large intra- or inter-industry merger, a new entrant in the specialty pharmacy business, changes in the distribution model for specialty drugs, a slowdown in the biotechnology pharmaceutical pipeline in our areas of expertise, consolidation of shipping carriers or the necessary changes or unintended consequences of the federal Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act of 2010 (the "Health Reform Laws") or future regulatory changes. Our failure to anticipate or appropriately adapt to any of these changes or trends, none of which are within our control, could have a significant negative impact on our competitive position and materially adversely affect our business.

Significant and increasing pressure from third-party payors to limit reimbursements and the impact of high cost specialty drugs could materially adversely impact our profitability, results of operations and financial condition.

The continued efforts of health maintenance organizations, managed care organizations, pharmacy benefit managers, government programs (such as Medicare, Medicaid and other federal and state funded programs) and other third-party payors to limit pharmacy reimbursements may adversely impact our profitability. While manufacturers have increased the price of drugs, payors have generally decreased reimbursement rates as a percentage of drug cost. We expect pricing pressures from third-party payors to continue given the high and increasing costs of specialty drugs. Given the significant competition in the industry, we have limited bargaining power to counter payor demands for reduced reimbursement rates. If a significant number of patients cannot afford to cover the portions of specialty drug costs not covered by payors as a result of limited reimbursements, and we are unable to find other sources of funding for such patients, those patients may not fill their prescriptions and our revenues and business could be adversely affected.