Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - CADIZ INC | Financial_Report.xls |

| EX-10.35 - EXHIBIT 10.35 - CADIZ INC | exh10-35.htm |

| EX-23.1 - EXHIBIT 23.1 - CADIZ INC | exhibit_23-1.htm |

| EX-32.2 - EXHIBIT 32.2 - CADIZ INC | exhibit_32-2.htm |

| EX-31.1 - EXHIBIT 31.1 - CADIZ INC | exhibit_31-1.htm |

| EX-21.1 - EXHIBIT 21.1 - CADIZ INC | exhibit_21-1.htm |

| EX-31.2 - EXHIBIT 31.2 - CADIZ INC | exhibit_31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - CADIZ INC | exhibit_32-1.htm |

united states

Securities and Exchange Commission

Washington, D. C. 20549

FORM 10-K

þ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the fiscal year ended December 31, 2014

OR

þ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the transition period from ..... to .....

Commission File Number 0-12114

Cadiz Inc.

(Exact name of registrant specified in its charter)

|

DELAWARE

|

77-0313235

|

|

(State or other jurisdiction of

|

(I.R.S. Employer

|

|

incorporation or organization)

|

Identification No.)

|

|

550 S. Hope Street, Suite 2850

|

|

|

Los Angeles, CA

|

90071

|

|

(Address of principal executive offices)

|

(Zip Code)

|

(213) 271-1600

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

|

Common Stock, par value $0.01 per share

|

The NASDAQ Global Market

|

|

(Title of Each Class)

|

(Name of Each Exchange on Which Registered)

|

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in rule 405 under the Securities Act of 1933.

Yes ___ No √

Indicate by a check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes ___ No √

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes √ No ___

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes √ No ___

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§220.405 of this chapter) is not contained herein, and will not be contained to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment of this Form 10-K. [ ]

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as defined in Exchange Act Rule 12b-2).

Large accelerated filer ___ Accelerated filer √ Non-accelerated filer ___ Smaller Reporting Company ___

Indicate by check mark whether the Registrant is a shell company (as defined in Exchange Act Rule 12b-2).

Yes ___ No √

The aggregate market value of the common stock held by nonaffiliates as of June 30, 2014 was approximately $123,066,837 based on 14,773,930 shares of common stock outstanding held by nonaffiliates and the closing price on that date. Shares of common stock held by each executive officer and director and by each entity that owns more than 5% of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 4, 2015, the Registrant had 17,718,600 shares of common stock outstanding.

Documents Incorporated by Reference

Portions of the Registrant’s definitive Proxy Statement to be filed for its 2015 Annual Meeting of Stockholders are incorporated by reference into Part III of this Report. The Registrant is not incorporating by reference any other documents within this Annual Report on Form 10-K except those footnoted in Part IV under the heading “Item 15. Exhibits, Financial Statement Schedules”.

|

Part I

|

||

|

Item 1.

|

1

|

|

|

Item 1A.

|

14

|

|

|

Item 1B.

|

17

|

|

|

Item 2.

|

17

|

|

|

Item 3.

|

18

|

|

|

Item 4.

|

19

|

|

|

Part II

|

||

|

Item 5.

|

20

|

|

|

Item 6.

|

22

|

|

|

Item 7.

|

23

|

|

|

Item 7A.

|

39

|

|

|

Item 8.

|

39

|

|

|

Item 9.

|

39

|

|

|

Item 9A.

|

39

|

|

|

Item 9B.

|

40

|

|

|

Part III

|

||

|

Item 10.

|

41

|

|

|

Item 11.

|

41

|

|

|

Item 12.

|

41

|

|

|

Item 13.

|

41

|

|

|

Item 14.

|

41

|

|

|

Part IV

|

||

|

Item 15.

|

42

|

PART I

This Form 10-K contains forward-looking statements with regard to financial projections, proposed transactions such as those concerning the further development of our land and water assets, information or expectations about our business strategies, results of operations, products or markets, or otherwise makes statements about future events. Such forward-looking statements can be identified by the use of words such as “intends”, “anticipates”, “believes”, “estimates”, “projects”, “forecasts”, “expects”, “plans” and “proposes”. Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from these forward-looking statements. These include, among others, the cautionary statements under the caption “Risk Factors”, as well as other cautionary language contained in this Form 10-K. These cautionary statements identify important factors that could cause actual results to differ materially from those described in the forward-looking statements. When considering forward-looking statements in this Form 10-K, you should keep in mind the cautionary statements described above.

Overview

We are a land and water resource development company with 45,000 acres of land in three areas of eastern San Bernardino County, California. Virtually all of this land is underlain by high-quality, naturally recharging groundwater resources, and is situated in proximity to the Colorado River and the Colorado River Aqueduct (“CRA”), a major source of imported water for Southern California. Our main objective is to realize the highest and best use of our land and water resources in an environmentally responsible way.

For more than 20 years, we have maintained an agricultural development at our 34,000-acre property in the Cadiz and Fenner valleys of eastern San Bernardino County (the “Cadiz/Fenner Property”), relying upon groundwater from the underlying aquifer system for irrigation. In 1993, we secured permits to develop agriculture on up to 9,600 acres of the Cadiz/Fenner Property and withdraw more than one million acre-feet of groundwater from the underlying aquifer system. Since that time, we have maintained various levels of agriculture at the property and this operation has provided our principal source of revenue.

In addition to our sustainable agricultural operations, we believe that the long-term value of our land assets can best be derived through the development of a combination of water supply and storage projects at our properties. At present, Cadiz Inc. (“Cadiz” or the “Company”) is primarily focused on the development of the Cadiz Valley Water Conservation, Recovery and Storage Project (“Water Project” or “Project”), which will capture and conserve millions of acre-feet1 of native groundwater currently being lost to evaporation from the aquifer system beneath our Cadiz/Fenner Property and deliver it to water providers throughout Southern California (see “Water Resource Development”). We believe that the ultimate implementation of this Water Project will create the primary source of our future cash flow and, accordingly, our working capital requirements relate largely to the development activities associated with this Water Project.

1 One acre-foot is equal to approximately 326,000 gallons or the volume of water that will cover an area of one acre to a depth of one-foot. An acre-foot is generally considered to be enough water to meet the annual water needs of one average California household.

The primary factor driving the value of such projects is continuing pressure on water supplies throughout California which has led Southern California water providers to actively seek new, reliable supply solutions to plan for both short and long-term water needs. This includes environmental and regulatory restrictions on each of the State’s three main water sources: the State Water Project, which provides water supplies from Northern California to the central and southern parts of the state, the CRA and the Los Angeles Aqueduct. Southern California’s water providers rely on imports from these systems for a majority of their water supplies, but deliveries from all three into the region have been below capacity over the last several years.

Availability of supplies in California also differs greatly from year to year due to natural hydrological variability. In January 2014, California’s Governor declared a drought emergency for the entire state as a result of record-low winter precipitation and depleted reservoir storage levels. California continues to be mired in a long-term drought and January 2015 was one of the driest months on record for the state. According to the United States Drought Monitor, as of February 2015 more than 93% of California is in a severe drought condition. Further, deliveries from the State Water Project have been limited to just 15% of capacity.

In addition to our water resource development activities, we also continue to explore additional uses of our land and water resource assets, including new agricultural opportunities, the development of a land conservation bank on our properties outside the Water Project area and other long-term legacy uses of our properties, such as habitat conservation and cultural uses.

In addition to these development efforts, we will also pursue strategic investments in complementary business or infrastructure to meet our objectives. We cannot predict with certainty when or if these objectives will be realized.

(a) General Development of Business

We are a Delaware corporation formed in 1992. As part of our historical business strategy, we have conducted our land acquisition, water development activities, agricultural operations, and land development initiatives to maximize the long-term value of our properties and future prospects (see “Narrative Description of Business”).

Our initial focus was on the acquisition of land and the assembly of contiguous land holdings through property exchanges to prove the quantity and quality of water resources in the Mojave Desert region of eastern San Bernardino County. We subsequently established agricultural operations on our properties in the Cadiz/Fenner Valley and sought to develop the water resources underlying that site. In 1993, we secured permits to develop up to 9,600 acres of agriculture at the Cadiz/Fenner Property and withdraw more than one million acre-feet of groundwater from the underlying aquifer system. The agricultural operations include vineyards, citrus orchards and seasonal vegetables.

The agricultural development demonstrated that the geology and hydrology of the property is also uniquely suited and able to support a project that could offer additional water supplies and water storage opportunities in Southern California.

In 1997, we entered into the first of a series of agreements with the Metropolitan Water District of Southern California (“Metropolitan”), the largest water wholesaler in the region and owner of the nearby Colorado River Aqueduct (“CRA”), to jointly design, permit, and build such a project (“2002 Project”). Between 1997 and 2002, we and Metropolitan received substantially all of the state and federal approvals required for the permits necessary to construct and operate the 2002 Project, including a Record of Decision (“ROD”) from the U.S. Department of the Interior, which approved the 2002 Project and offered a right-of-way for construction of facilities, including a 35-mile water conveyance pipeline from the Cadiz/Fenner Property to the CRA across federal lands. In October 2002, Metropolitan’s staff brought the right-of-way matter before its Board of Directors. By a very narrow margin, the Metropolitan Board voted not to accept the right-of-way grant nor proceed with the 2002 Project.

Following Metropolitan’s decision, we began to pursue new partnerships and redesigned the 2002 Project to meet the changing needs of Southern California’s water providers. We invested in significant scientific and technical analysis of the groundwater resources in the Cadiz/Fenner Valley as part of this effort, and focused on the safe and sustainable management of the aquifer system beneath our Cadiz/Fenner Property with the goal of providing a reliable, annual water supply for the region. In September 2008 we entered into a lease agreement with the Arizona & California Railroad Company (“ARZC”) to utilize its existing right-of-way between the Cadiz property and the Colorado River Aqueduct (“CRA”) to construct a pipeline able to deliver water from the property into the existing Southern California water transportation system. Between 2010 and 2011 six Southern California water providers executed option agreements to participate in the new Water Project. Under our lease agreement, the ARZC also reserved water from the Water Project to serve a variety of critical railroad purposes.

In accordance with the California Environmental Quality Act (“CEQA”), the Water Project began an environmental review and permitting process in 2011 led by Santa Margarita Water District (“SMWD”), one of the Project participants (see “Water Resource Development” below for a full description of the Water Project). After an extensive review process, the SMWD Board of Directors certified the Final Environmental Impact Report on July 31, 2012 and became the first participating agency to convert its option agreement to a Water Purchase and Sale Agreement for firm supplies from the Water Project. On October 1, 2012, San Bernardino County (“County”), a Responsible Agency under CEQA, also adopted CEQA findings and approved the Project’s Groundwater Monitoring, Management and Mitigation Plan (‘GMMMP”, “Plan”) and the withdrawal of 50,000 acre-feet (AF) of water per year for 50 years.

Following receipt of these critical approvals, we were named as a real-party-in-interest in nine lawsuits brought by parties seeking a reconsideration of the environmental documents and limitation of the Project approvals granted by SMWD and the County. Three of these cases were subsequently dismissed or otherwise settled and six lawsuits brought by two petitioners proceeded to trial in Orange County Superior Court (“Court”) before one judge in December 2013. In September 2014, the Court issued final signed judgments (“Judgments”) formally denying all claims brought in the six lawsuits. The Judgments upheld the environmental review and approvals of the Water Project and also awarded costs to SMWD, the County, Cadiz and Fenner Valley Mutual Water Company as the prevailing parties in the cases. The Judgments served as the Court’s final actions in the six cases.

Following receipt of the Judgments, we executed Letters of Intent (“LOIs”) and definitive contracts with additional water providers and agricultural entities and, combined with the option agreements entered into in 2010-2011, we have executed LOIs, option agreements and purchase agreements in excess of Project capacity. We expect to account for any oversubscription as we finalize the definitive purchase agreements prior to construction.

During the fourth quarter of 2014, the petitioners in the six original Court cases filed independent appeals of the six Judgments with the California Court of Appeals, Fourth District. These appeals were anticipated and are expected to be heard by the Appeals Court in 2015. The appeals process is not projected to have any impact on the Company’s ongoing implementation and pre-construction activities for the Water Project, including finalization of contracts with the California water providers and agricultural entities described above.

While the appeals process proceeds this year, we expect to continue final design of engineering plans, including arrangements with Metropolitan Water District of Southern California regarding conveyance of Project water in the Colorado River Aqueduct, begin further environmental review of Phase II of the Project, which would incorporate our 96-mile Cadiz to Barstow, California pipeline asset into our overall business plans, and progress construction financing arrangements for Phase 1. See “Narrative Description of Business” below for more detail.

(b) Financial Information about Industry Segments

Our primary business is to acquire and develop land and water resources. Our agricultural operations are confined to limited farming activities at the Cadiz/Fenner Property. As a result, our financial results are reported in a single segment. See Consolidated Financial Statements. See also Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”.

(c) Narrative Description of Business

Our business strategy is to pursue the development of our landholdings for their highest and best uses. At present, our development activities include water resource, land and agricultural development.

Water Resource Development

Our portfolio of water resources is located in proximity to the Colorado River and the Colorado River Aqueduct (“CRA”), the principal source of imported water for Southern California, and provides us with the opportunity to participate in a variety of water supply, water storage, and conservation programs with public agencies and other partners.

The Cadiz Valley Water Conservation, Recovery and Storage Project

We own approximately 34,000 acres of land and the subsurface strata, inclusive of the unsaturated soils and appurtenant water rights in the Cadiz and Fenner valleys of eastern San Bernardino County (the “Cadiz/Fenner Property”). The aquifer system underlying this property is naturally recharged by precipitation (both rain and snow) within a watershed of approximately 1,300 square miles. See Item 2, “Properties – The Cadiz/Fenner Valley Property”.

The Cadiz Valley Water Conservation, Recovery and Storage Project (the “Water Project” or “Project”) is designed to supply, capture and conserve billions of gallons of renewable native groundwater currently being lost annually to evaporation from the aquifer system underlying our Cadiz/Fenner Property, and provide a reliable water supply to water users in Southern California. By implementing established groundwater management practices, the Water Project will create a new, sustainable water supply for project participants without adversely impacting the aquifer system or the desert environment. The total quantity of groundwater to be recovered and conveyed to Water Project participants will not exceed a long-term annual average of 50,000 acre-feet per year for 50 years. The Project also offers participants the ability to carry-over their annual supply, and store it in the groundwater basin from year to year. A second phase of the Water Project, Phase II, will offer approximately one million acre-feet of underground storage capacity that can be used to hold imported water supplies at the Water Project area.

Water Project facilities required for Phase I primarily include, among other things:

|

·

|

High yield wells designed to efficiently recover available native groundwater from beneath the Water Project area;

|

|

·

|

A water conveyance pipeline to deliver water from the well field to the CRA; and

|

|

·

|

An energy source to provide power to the well-field, pipeline and pumping plant;

|

If an imported water storage component of the Project is ultimately implemented in Phase II, the following additional facilities would be required, among other things:

|

·

|

A pumping plant to pump water through the conveyance pipeline from the CRA to the Project well-field; and

|

|

·

|

Spreading basins, which are shallow settling ponds that will be configured to efficiently percolate water from the ground surface down to the water table using subsurface storage capacity for the storage of water.

|

In general, several elements are needed to implement such a project: (1) a water conveyance pipeline right-of-way from the Water Project area to a delivery system; (2) storage and supply purchase agreements with one or more public water agencies or private water utilities; (3) environmental/regulatory permits; and (4) construction and working capital. As described below, the first three elements have been progressed on a concurrent basis. The fourth is dependent on actions arising from the completion of the first three.

|

(1)

|

A Water Conveyance Pipeline Right-of-Way from the Water Project Area to a Delivery System

|

In September 2008, we secured a right-of-way for the Water Project’s water conveyance pipeline by entering into a lease agreement with the Arizona & California Railroad Company (“ARZC”), which operates an active shortline railroad extending from Cadiz to Matthie, Arizona. The agreement allows for the use of a portion of the railroad’s right-of-way to construct and operate a water conveyance pipeline for a period up to 99 years. The buried pipeline would be constructed parallel to the railroad tracks and be used to convey water between our Cadiz/Fenner Property and the CRA in Freda, California.

Our lease agreement with the ARZC also expressly requires that the Project further several railroad purposes and, under the terms of the lease agreement, the ARZC reserved water supplies from the Project for its operational needs as well as access to Project facilities, such as roads and power appurtenances, for the benefit of its railroad operation. In September 2013, we also entered into a trackage rights agreement with the ARZC that would enable the operation of steam-powered, passenger excursion trains on the line powered by water made available from the pipeline.

The pipeline route was fully analyzed in the Water Project’s Final Environmental Impact Report (“EIR”) as part of the CEQA environmental review process completed in 2012 and was found to be the environmentally preferred route for the pipeline. Our plan to construct the Project pipeline within the railroad right-of-way is similar to, and modeled after, the thousands of other existing longitudinal uses of rail corridors in place across the United States today, such as telecommunications lines, natural gas and petroleum product lines and other water lines. Under the General Railroad Right-of-Way Act of March 3, 1875 (“1875 Act”), according to which many of these railroad corridors were established, a railroad can lease its property for third party uses without consent of the federal government so long as the use also serves railroad purposes.

In August 2014, the U.S. Bureau of Land Management issued guidance (Instruction Memorandum No. 2014-122) to its field offices requiring the evaluation of all existing and proposed uses of 1875 Act railroad rights-of-way to determine whether or not they further a railroad purpose. If the BLM determines that a third-party use does further a railroad purpose, then the railroad or third parties authorized by it may proceed with the activity without further federal consent or involvement. If BLM determines that the proposed activity does not further a railroad purpose, then the railroad or third parties authorized by it will have to obtain a permit from BLM in order to proceed. We are currently in communication with the BLM regarding its assessment of the Project’s proposed use of the ARZC right-of-way and the numerous railroad purposes served, as directed by the new guidance.

In addition to this planned pipeline, we also acquired an unused natural gas pipeline (as described in “Existing Pipeline Asset” below) that exists in the Water Project area as a means to access additional distribution systems in Phase II of the Water Project. Initial feasibility studies indicate that this pipeline could be used as a component of the Water Project to distribute water to participants or import water for storage at the Water Project area in Phase II. The potential use of this pipeline was preliminarily analyzed as part of the Water Project’s EIR. Additional environmental review would be required prior to converting this line for water distribution.

|

(2)

|

Storage and Supply Agreements with One or More Public Water Agencies or Private Water Utilities

|

In 2010 and 2011, we entered into option and environmental cost sharing agreements with six water providers: Santa Margarita Water District (“SMWD”), Golden State Water Company (a wholly owned subsidiary of American States Water [NYSE: AWR]), Three Valleys Municipal Water District, Suburban Water Systems (a wholly owned subsidiary of SouthWest Water Company), Jurupa Community Services District and California Water Service Company, the third largest investor-owned American water utility. The six water providers serve more than one million customers in cities throughout California’s San Bernardino, Riverside, Los Angeles, Orange, Imperial and Ventura Counties.

Following CEQA certification, SMWD was the first participant to convert its option agreement and adopt resolutions approving a Water Purchase and Sale Agreement for 5,000 acre-feet of water. The structure of the SMWD purchase agreement calls for an annually adjusted water supply payment, plus a pro rata portion of the capital recovery charge and operating and maintenance costs. The capital recovery charge is calculated by amortizing the total capital investment by the Company over a 30-year term. Under the terms of the option agreements with the other five water providers named above, each agency has the right to acquire an annual supply of 5,000 acre-feet of water at $775 per acre-foot (2010 dollars), which is competitive with their incremental cost of new water. In addition, these agencies have options to acquire storage rights in the Water Project to allow for the management of their Water Project supplies in complement with their other water resources. We are currently working with these water providers to convert their option agreements to definitive economic agreements.

In 2014, we also executed Letters of Intent (“LOIs”) with two California water providers and two California agricultural entities reserving up to 20,000 acre-feet of water per year from the Water Project at $960/acre-foot (2014 dollars) delivered to the Colorado River Aqueduct. In December 2014, we converted one of these LOIs with San Luis Water District (“San Luis”) to a Water Purchase and Sale Agreement (“PSA”) for 10,000 acre-feet per year. Under the terms of the PSA, San Luis will pay an initial price of $960 per acre-foot (“AF”)(2014 dollars) for water made available to it by the Project. The payment will be adjusted annually in accordance with the Bureau of Labor Statistics Water and Sewer Maintenance Index up to a maximum of five percent (5%) per year. San Luis also secured the right to acquire specified carry-over storage rights in the Water Project to achieve year-to-year flexibility in its use of water for $1,500 per AF and an annual management fee of $20 per AF of acquired storage capacity. Any delivery of the water from the Project to San Luis will be subject to an exchange with the Metropolitan Water District of Southern California or another eligible State Water Project contractor and terms of which will be finalized prior to commencement of Project construction.

We have executed LOIs, option agreements and purchase agreements that are in excess of Water Project capacity and are working collaboratively with the remaining water providers to account for any oversubscription as we progress final definitive PSAs.

|

(3)

|

Environmental/Regulatory Permits

|

In order to properly develop and quantify the sustainability of the Water Project, and prior to initiating the formal permitting process for the Water Project, we commissioned environmental consulting firm CH2M HILL to complete a comprehensive study of the water resources at the Project area. Following a year of analysis, CH2M HILL released its study of the aquifer system in February 2010. Utilizing new models produced by the U.S. Geological Survey in 2006 and 2008, the study estimated the total groundwater in storage in the aquifer system to be between 17 and 34 million acre-feet, a quantity on par with Lake Mead, the nation’s largest surface reservoir. The study also identified a renewable annual supply of native groundwater in the aquifer system currently being lost to evaporation. CH2M HILL’s findings, which were peer reviewed by leading groundwater experts, confirmed that the aquifer system could sustainably support the Water Project.

Further, and also prior to beginning the formal environmental permitting process, we entered into a Memorandum of Understanding (“MOU”) with the Natural Heritage Institute (“NHI”), a leading global environmental organization committed to protecting aquatic ecosystems, to assist with our efforts to sustainably manage the development of our Cadiz/Fenner Property. As part of this “Green Compact”, we will follow stringent plans for groundwater management and habitat conservation.

As discussed in (2), above, we entered into environmental cost-sharing agreements with all participating water providers creating a framework for funds to be committed by each participant to share in the costs associated with the CEQA review work. SMWD served as the lead agency for the review process, which began in February 2011 with SMWD’s issuance of a Notice of Preparation (“NOP”) of a Draft Environmental Impact Report (“Draft EIR”).

Following two NOP public scoping meetings, SMWD released the Draft EIR in December 2011. The Draft EIR analyzed potential impacts to environmental resources at the Water Project area, including critical resources of the desert environment such as vegetation, mountain springs, and water and air quality. The analysis of the Water Project considered peer-reviewed technical reports, independently collected data, existing reports and the Project’s state of the art Groundwater Management, Monitoring and Mitigation Plan (“GMMMP”). SMWD held a 100-day public comment period for the Draft EIR, during which SMWD hosted two public comment meetings and an informational workshop.

In May 2012, SMWD, Cadiz and the County of San Bernardino also entered into a Memorandum of Understanding creating the framework for finalizing the GMMMP in accordance with the County’s desert groundwater ordinance.

In July 2012, SMWD released the Final EIR and responses to public comments. The Final EIR summarized that, with the exception of unavoidable short-term construction emissions, by implementing the measures developed in the GMMMP, the Project will avoid significant impacts to desert resources. A public hearing was held on July 25, 2012 by the SMWD Board of Directors to take public testimony and consider certification of the Final EIR. On July 31, 2012, the SMWD Board of Directors certified the Final EIR.

Following SMWD’s certification of the Final EIR, the San Bernardino County Board of Supervisors voted on October 1, 2012 to approve the GMMMP for the Project and adopted certain findings under CEQA, becoming the first Responsible Agency to take an approving action pursuant to the certified EIR. San Bernardino County served as a Responsible Agency in the CEQA review process as the local government entity responsible for oversight over groundwater resources in the Cadiz Valley.

Third parties in California have the ability to challenge CEQA approvals in State Court and, in 2012, the Company was named as a real-party-in-interest in nine lawsuits challenging the various Water Project approvals granted by SMWD and San Bernardino County. In 2013, three cases were dismissed or otherwise settled. Trial in the six remaining cases, which were brought by two petitioners, began in December 2013 and concluded in February 2014. In September 2014, the Court issued final signed judgments (“Judgments”) formally denying all claims brought in the six lawsuits. The Judgments upheld the environmental review and approvals of the Water Project and also awarded costs to SMWD, the County, Cadiz and Fenner Valley Mutual Water Company as the prevailing parties in the cases. The Judgments served as the Court’s final actions in the six cases.

During the fourth quarter of 2014, the petitioners filed independent appeals of the six Judgments in the California Court of Appeals, Fourth District. See Item 3, “Legal Proceedings” for more information. These appeals were anticipated and are expected to be heard by the Appeals Court in 2015. The appeals process is not projected to have any impact on the Company’s ongoing implementation and pre-construction activities for the Water Project.

Because Water Project supplies must enter and be transported within the CRA to reach the Project’s customers, Metropolitan must also take action as a responsible agency under CEQA prior to construction of the Project regarding the terms and conditions of the Project’s use of the CRA. Water Project supplies will enter Metropolitan’s CRA in accordance with its published engineering and design standards and subject to all applicable fees and charges routinely established by Metropolitan for the conveyance of water within its service territory. We expect Metropolitan to consider the terms and conditions of transportation for our customers’ water later this year.

|

(4)

|

Construction and Working Capital

|

As part of the Water Purchase and Sale Agreement with SMWD referred to in (2), above, SMWD is further authorized to continue next steps with the Company, which includes final permitting, design and construction.

As described above, construction of Phase I of the Water Project would primarily consist of wellfield facilities at the Project site, a conveyance pipeline extending approximately 43 miles along the right-of-way described in (1), above, from the wellfield to the CRA, and an energy source to pump water through the conveyance pipeline between the Project well-field and the CRA. The construction of these facilities will require capital financing, which is expected to be entirely provided with lower-cost senior debt, secured by the new facility assets. The Company’s existing corporate term debt (see Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources”) provides us the flexibility to incorporate Water Project construction financing within our current debt structure.

Existing wells at the Cadiz/Fenner Property currently in use for our agricultural operations will be integrated into the Water Project well-field, reducing the number of wells that must be constructed prior to Project implementation.

Existing Pipeline Asset

As described above (see “Water Resource Development”), we currently hold ownership rights to a 96-mile existing idle natural gas pipeline from the Cadiz/Fenner Property to Barstow, California that would be converted for the transportation of water.

In September 2011, we entered into an agreement with El Paso Natural Gas (“EPNG”), a subsidiary of Kinder Morgan Inc., providing us with rights to purchase approximately 220-miles of idle, natural gas pipelines between Bakersfield and Cadiz, California for $40 million.

Initial feasibility studies indicated that, upon conversion, the 30-inch line could transport between 20,000 and 30,000 acre-feet of water per year between the Water Project area and various points along the Central and Northern California water transportation network. In February 2012, we made a $1 million payment to EPNG to extend our option to purchase the 220-mile line until April 2013.

In December 2012, we entered into a new agreement with EPNG dividing the 220-mile pipeline in Barstow, California, with the Company gaining ownership rights to the 96-mile eastern segment between Barstow and the Cadiz Valley and returning to EPNG rights to the 124-mile western segment for its own use. The 96-mile eastern portion from the Cadiz Valley to Barstow was identified as the most critical segment of the line for accessing the state’s water transportation infrastructure. The Barstow area serves as a hub for water delivered from northern and central California to communities in Southern California’s High Desert.

In consideration of the new agreement, EPNG reduced the purchase price of the 96-mile eastern segment to $1 (one dollar), plus previous option payments totaling $1.07 million already made by the Company. On April 11, 2014, the Company paid the remaining purchase price of $1 (one dollar) and secured ownership of the asset. In addition, the agreement provides that if EPNG files for regulatory approval of any new use of the 124-mile western segment by December 2015, EPNG will make a payment of $10 million to the Company on the date the application for regulatory approval is filed.

The 96-mile Cadiz-Barstow pipeline creates significant opportunities for our water resource development efforts. Once converted to water use, the pipeline can be used to directly connect the Cadiz area to northern and central California water sources, serving a growing need for additional locations for storage of water south of the Bay Delta region. In addition, the 96-mile pipeline creates new opportunities to deliver water, either directly or via exchange, to potential customers in San Bernardino and Kern Counties, areas which do not currently have an interconnection point with the Project. When both the 96-mile line and the 43-mile pipeline to the CRA become operational, Cadiz would link the two major water delivery systems in California providing flexible opportunities for both supply and storage.

The entire EPNG pipeline was evaluated in the Water Project’s EIR during the CEQA process at a programmatic level. Any use of the line would be conducted in conformity with the Project’s GMMMP and is subject to further CEQA evaluation (see “Cadiz Valley Water Conservation, Recovery and Storage Project” above).

Agricultural Development

Within the Cadiz/Fenner Property, 9,600 acres have been zoned for agriculture and the Company has developed a total of 1,920 acres of the property for agricultural operations. The infrastructure currently includes six wells that are interconnected within a portion of this acreage for current agricultural use, and three additional production wells, with the nine wells together having total annual production capacity of approximately 20,000 acre-feet of water. Additionally, there are housing and kitchen facilities that support up to 300 employees. If the entire 9,600 acres were developed and irrigated, total water usage would be approximately 40,000 – 50,000 acre-feet per year depending on the crop mix. The underlying groundwater, fertile soil, and desert temperatures are well suited for a wide variety of fruits and vegetables.

Permanent crops in production currently include 160 acres of vineyard used to produce dried-on-the-vine raisins and 340 acres of lemon orchards. All crops are farmed using sustainable agricultural practices.

We currently derive our agricultural revenues through direct farming and sale of our products into the market or through the lease of our agricultural properties to third parties for farming. The entire organic raisin crop grown at the property is farmed by the Company and we incur all of the costs required to produce and harvest the crop. The harvested raisins are then sold in bulk to a raisin processing facility.

Approximately 340 acres of lemons are presently being farmed under a 2013 lease agreement with Limoneira Company (“Limoneira”). Limoneira has planted 140 acres of new lemons since 2013 under the lease agreement. In January 2015, Limoneira also acquired 200 acres of young lemon trees and associated irrigation lines from the Company and one of its leasing tenants for approximately $1.2 million and amended its lease with us to include the additional 200 acres. Under the amended lease agreement, Limoneira now has the right to plant up to an additional 1,140 acres of lemons over the next three years. In conjunction with the new plantings of lemons, the Company elected to remove its existing older 240 acres of lemons that had reached the end of their commercial life. All lemons grown on the property are now pursuant to the lease with Limoneira.

In consideration for the lease arrangement, Limoneira provides an annual base rent and will also provide a profit-sharing payment once its lemon orchards reach commercial production.

Agricultural revenues will vary from year to year based on the number of acres in development, crop yields, and prices. We do not expect that our agricultural revenues will be material to our overall results of operations once the Water Project is fully operational. However, our agricultural operations are expected to be maintained in complement with the Water Project to provide added value to Project operations.

Additional Eastern Mojave Properties

We also own approximately 11,000 acres outside of the Cadiz/Fenner Valley area in other parts of the Mojave Desert in eastern San Bernardino County.

Our primary landholding outside of the Cadiz area is approximately 9,000 acres in the Piute Valley. This landholding is located approximately 15 miles from the resort community of Laughlin, Nevada, and about 12 miles from the Colorado River town of Needles, California. Extensive hydrological studies, including the drilling and testing of a full-scale production well, have demonstrated that this landholding is underlain by high-quality groundwater. The aquifer system underlying this property is naturally recharged by precipitation (both rain and snow) within a watershed of approximately 975 square miles and could be suitable for a water supply project, agricultural development or solar energy production. Certain of these properties are located in or adjacent to areas designated by the federal government as Critical Desert Tortoise Habitat and/or Desert Wilderness Areas and are also suitable candidates for preservation and conservation (see “Land Conservation Bank” below).

Additionally, we own acreage located near Danby Dry Lake, approximately 30 miles southeast of our Cadiz/Fenner Valley properties. The Danby Dry Lake property is located approximately 10 miles north of the CRA. Initial hydrological studies indicate that the area has excellent potential for a water supply project. Certain of the properties in this area may also be suitable for agricultural development and/or preservation and conservation.

Land Conservation Bank

As stated above, approximately 10,000 acres of our properties outside of the Cadiz/Fenner Valley area are located within terrain designated by the federal government as Critical Desert Tortoise Habitat and/or Desert Wilderness Areas and have limited development opportunities. In February 2015, the California Department of Fish and Wildlife approved our establishment of the Fenner Valley Desert Tortoise Conservation Bank (“Fenner Bank”), a land conservation bank that makes available approximately 7,500 acres of our properties located within Critical Desert Tortoise Habitat for mitigation of impacts to tortoise and other sensitive species that would be caused by development in the Southern California desert. Under its enabling documents, the Fenner Bank will offer credits that can be acquired by entities that must mitigate or offset impacts linked to planned development. For example, this bank could potentially service the mitigation requirements of numerous utility-scale solar development projects being considered throughout Riverside and San Bernardino Counties, or military, residential and commercial development in approved areas throughout the desert. Credits sold by the Fenner Bank will fund our permanent preservation of the land as well as research by outside entities into desert tortoise health and species protection.

Other Opportunities

Other opportunities in the water and agricultural or related infrastructure business complementary to our current objectives could provide new opportunities for our Company.

Over the longer-term, we believe the population of Southern California, Nevada and Arizona will continue to grow, and that, in time, the economics of commercial and residential development at our properties may become attractive.

We remain committed to the sustainable use of our land and water assets, and will continue to explore all opportunities for environmentally responsible development of these assets. We cannot predict with certainty which of these various opportunities will ultimately be utilized.

Seasonality

Our water resource development activities are not seasonal in nature.

Our farming operations are limited to the cultivation of lemons and grapes/raisins and spring and fall plantings of vegetables on the Cadiz Valley properties. These operations are subject to the general seasonal trends that are characteristic of the agricultural industry.

Competition

We face competition for the acquisition, development and sale of our properties from a number of competitors. We may also face competition in the development of water resources and siting of renewable energy facilities associated with our properties. Since California has scarce water resources and an increasing demand for available water, we believe that location, price and reliability of delivery are the principal competitive factors affecting transfers of water in California.

Employees

As of December 31, 2014, we employed 10 full-time employees (i.e. those individuals working more than 1,000 hours per year). We believe that our employee relations are good.

Regulation

Our operations are subject to varying degrees of federal, state and local laws and regulations. As we proceed with the development of our properties, including the Water Project, we will be required to satisfy various regulatory authorities that we are in compliance with the laws, regulations and policies enforced by such authorities. Groundwater development, and the export of surplus groundwater for sale to entities such as public water agencies, is subject to regulation by specific existing statutes, in addition to general environmental statutes applicable to all development projects. Additionally, we must obtain a variety of approvals and permits from state and federal governments with respect to issues that may include environmental issues, issues related to special status species, issues related to the public trust, and others. Because of the discretionary nature of these approvals and concerns, which may be raised by various governmental officials, public interest groups and other interested parties during both the development and the approval process, our ability to develop properties and realize income from our projects, including the Water Project, could be delayed, reduced or eliminated.

Access to Our Information

Our annual, quarterly and current reports, proxy statements and other information are filed with the Securities and Exchange Commission (“SEC”) and are available free of charge through our web site, www.cadizinc.com, as soon as reasonably practical after electronic filing of such material with the SEC.

Our SEC filings are also available to the public at the SEC website at www.sec.gov. You may also read and copy any document we file at the SEC’s public reference room located at 100 F Street N.E., Washington D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the operation of the public reference room.

Our business is subject to a number of risks, including those described below.

Our Development Activities Have Not Generated Significant Revenues

At present, our development activities include water resource and agricultural development at our San Bernardino County properties. We have not received significant revenues from our development activities to date and we do not know when, if ever, we will receive operating revenues sufficient to offset the costs of our development activities. As a result, we continue to incur a net loss from operations.

We May Never Generate Significant Revenues or Become Profitable Unless We Are Able to Successfully Implement Programs to Develop Our Land Assets and Related Water Resources

We do not know the terms, if any, upon which we may be able to proceed with our water and other development programs. Regardless of the form of our water development programs, the circumstances under which supplies or storage of water can be developed and the profitability of any supply or storage project are subject to significant uncertainties, including the risk of variable water supplies and changing water allocation priorities. Additional risks include our ability to obtain all necessary regulatory approvals and permits, litigation by environmental or other groups, unforeseen technical difficulties, general market conditions for water supplies, and the time needed to generate significant operating revenues from such programs after operations commence.

The Development of Our Properties Is Heavily Regulated, Requires Governmental Approvals and Permits That Could Be Denied, and May Have Competing Governmental Interests and Objectives

In developing our land assets and related water resources, we are subject to local, state, and federal statutes, ordinances, rules and regulations concerning zoning, resource protection, environmental impacts, infrastructure design, subdivision of land, construction and similar matters. Our development activities are subject to the risk of adverse interpretations or changes to U.S. federal, state and local laws, regulations and policies. Further, our development activities require governmental approvals and permits. If such permits were to be denied or granted subject to unfavorable conditions or restrictions, our ability to successfully implement our development programs would be adversely impacted.

The opposition of government officials may adversely affect our ability to obtain needed government approvals and permits upon satisfactory terms in a timely manner. In this regard, federal government appropriations currently preclude spending for “any proposal to store water for the purpose of export or for any activities associated with the approval of rights-of-way on lands managed by the Needles Field Office of the U.S. Bureau of Land Management” (the “BLM”). Federal government appropriations also direct the U.S. Department of the Interior (the “DOI”) to confirm that the Water Project’s proposed use of a portion of the right-of-way of the ARZC for the Project’s conveyance pipeline is within the scope of ARZC’s right-of-way. According to existing federal law and direction from the DOI in Memorandum Opinion M-23075, a railroad has the authority to grant third party uses within its rights-of-way without BLM approval if those uses will serve a railroad purpose. The Project and pipeline will further numerous railroad purposes, including fire suppression, access to water for business operations, hydropower generation creating additional transloading opportunities, as well as increased traffic among other benefits, and the ARZC has provided information regarding these purposes to the BLM. As a result, we do not believe federal right-of-way approval is required to implement the Project; however, this may be subject to challenge.

Additionally, the statutes, regulations and ordinances governing the approval processes provide third parties the opportunity to challenge proposed plans and approvals. Opposition from third parties will cause delays and increase the costs of our development efforts or preclude such development entirely. In California, third parties have the ability to file litigation challenging the approval of a project, which they usually do by alleging inadequate disclosure and mitigation of the environmental impacts of the project. We expect to be party to various legal proceedings arising in the general course of our business related to the development of the Water Project. We are currently named as a real-party-in-interest in six lawsuits before the California Court of Appeals, 4th District. These lawsuits seek to overturn the rulings issued by Orange County Superior Court in October 2014 which upheld all of the Water Project approvals granted to date and denied all claims against the Project. While we have worked with representatives of various environmental and third party interests and agencies to minimize and mitigate the impacts of our planned projects, certain groups may remain opposed to our development plans and pursue legal action.

Our Failure to Make Timely Payments of Principal and Interest on Our Indebtedness May Result in a Foreclosure on Our Assets

As of December 31, 2014, we had indebtedness outstanding to our senior secured lenders of approximately $106.2 million. Approximately $45.7 million of our indebtedness is secured by our assets, $34.7 million of which is due in March 2016 (see Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources”). To the extent that we do not make principal and interest payments on the indebtedness when due at maturity, or if we otherwise fail to comply with the terms of agreements governing our indebtedness, we may default on our obligations.

The Conversion of Our Outstanding Convertible Notes into Common Stock Would Dilute the Percentage of Our Common Stock Held by Current Stockholders

In connection with our March 2013 debt refinance (see Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources”), we issued approximately $53.5 million in convertible notes (the “Convertible Notes”) Principal and accrued interest under the Convertible Notes can be converted into common stock at $8.05 per share at the election of our lenders. An election by our lenders to convert all or a portion of principal and accrued interest under these Convertible Notes into common stock will dilute the percentage of our common stock held by current stockholders up to 7.6 million shares as of March 5, 2015, and up to an additional 1.8 million shares if held to maturity.

We May Not Be Able To Obtain the Financing We Need To Implement Our Asset Development Programs

Based upon our current and anticipated usage of cash resources, we have sufficient funds to meet our expected working capital needs through the first quarter of 2016. We will continue to require additional working capital to meet our cash resource needs until such time as our asset development programs produce revenues. If we cannot raise funds if and when needed, we might be forced to make substantial reductions in our operating expenses, which could adversely affect our ability to implement our current business plan and ultimately our viability as a company. We cannot assure you that our current lenders, or any other lenders, will give us additional credit should we seek it. If we are unable to obtain additional credit, we may engage in further financings. Our ability to obtain financing will depend, among other things, on the status of our asset development programs and general conditions in the capital markets at the time funding is sought. Although we currently expect our capital sources to be sufficient to meet our near term liquidity needs, there can be no assurance that our liquidity requirements will continue to be satisfied. Any further equity or convertible debt financings would result in the dilution of ownership interests of our current stockholders.

The Issuance of Equity Securities Under Management Equity Incentive Plans Will Impact Earnings

Our compensation programs for management emphasize long-term incentives, primarily through the issuance of equity securities and options to purchase equity securities. It is expected that plans involving the issuance of shares, options, or both will be submitted from time to time to our stockholders for approval. In the event that any such plans are approved and implemented, the issuance of shares and options under such plans may result in the dilution of the ownership interest of other stockholders and will, under currently applicable accounting rules, result in a charge to earnings based on the value of our common stock at the time of issue and the fair value of options at the time of their award. The expense would be recorded over the vesting period of each stock and option grant.

The Volatility of Our Stock Price Could Adversely Affect Current and Future Stockholders

The market price of our common stock is volatile and fluctuates in response to various factors which are beyond our control. Such fluctuations are particularly common in companies such as ours, which have not generated significant revenues. The following factors, in addition to other risk factors described in this section, could cause the market price of our common stock to fluctuate substantially:

|

·

|

developments involving the execution of our business plan;

|

|

·

|

disclosure of any adverse results in litigation;

|

|

·

|

regulatory developments affecting our ability to develop our properties;

|

|

·

|

the dilutive effect or perceived dilutive effect of additional debt or equity financings;

|

|

·

|

perceptions in the marketplace of our company and the industry in which we operate; and

|

|

·

|

general economic, political and market conditions.

|

In addition, the stock markets, from time to time, experience extreme price and volume fluctuations that may be unrelated or disproportionate to the operating performance of companies. These broad fluctuations may adversely affect the market price of our common stock. Price volatility could be worse if the trading volume of our common stock is low.

Not applicable at this time.

Following is a description of our significant properties.

The Cadiz/Fenner Valley Property

Since 1983, we have acquired approximately 34,000 acres of largely contiguous land in the Cadiz and Fenner valleys of eastern San Bernardino County, California (the “Cadiz/Fenner Property”). This area is located approximately 30 miles north of the Colorado River Aqueduct (“CRA”). In 1984, we conducted investigations into the feasibility of agricultural development of this land. These investigations confirmed the availability of high-quality groundwater in quantities appropriate for agricultural development.

Additional independent geotechnical and engineering studies conducted since 1985 have confirmed that the Cadiz/Fenner Property overlies an aquifer system that is ideally suited for the conservation, recovery and delivery of indigenous groundwater, as well as the storage of conserved or imported water, as contemplated by the Water Project. See Item 1, “Business – Narrative Description of Business – Water Resource Development”.

Other Eastern Mojave Properties

In addition to the Cadiz/Fenner Valley property, we also own approximately 11,000 additional acres in the eastern Mojave Desert portion of San Bernardino County, California at two separate properties.

The first property consists of approximately 9,000 acres in the Piute Valley. This landholding is located approximately 15 miles from the resort community of Laughlin, Nevada, and about 12 miles from the Colorado River town of Needles, California. Extensive hydrological studies, including the drilling and testing of a full-scale production well, have demonstrated that this landholding is underlain by high-quality groundwater. The aquifer system underlying this property is naturally recharged by precipitation (both rain and snow) within a watershed of approximately 975 square miles and could be suitable for a water supply project, agricultural development or solar energy production. Certain of these properties are located in or adjacent to areas designated by the federal government as Critical Desert Tortoise Habitat and/or Desert Wilderness Areas and are suitable candidates for preservation and conservation.

Additionally, we own nearly 2,000 acres near Danby Dry Lake, approximately 30 miles southeast of our Cadiz/Fenner landholdings. Our Danby Dry Lake property is located approximately 10 miles north of the Colorado River Aqueduct. Initial hydrological studies indicate that it has excellent potential for water supply, agricultural development and related uses. Certain of the properties in this area may also be suitable for agricultural development and/or preservation and conservation.

Executive Offices

We lease approximately 7,200 square feet of office space in Los Angeles, California for our executive offices. The lease terminates in January 2016. Current base rent under the lease is approximately $14,500 per month.

Cadiz Real Estate

In December 2003, we transferred substantially all of our assets (with the exception of our office sublease, and certain office furniture and equipment) to Cadiz Real Estate LLC, a Delaware limited liability company (“Cadiz Real Estate”). We hold 100% of the equity interests of Cadiz Real Estate and, therefore, we continue to hold 100% beneficial ownership of the properties that we transferred to Cadiz Real Estate. The Board of Managers of Cadiz Real Estate currently consists of two managers appointed by us.

Cadiz Real Estate is a co-obligor under our senior secured term loan, for which assets of Cadiz Real Estate have been pledged as security.

Because the transfer of our properties to Cadiz Real Estate has no effect on our ultimate beneficial ownership of these properties, we refer throughout this Report to properties owned of record either by Cadiz Real Estate or by us as “our” properties.

Debt Secured by Properties

Our assets have been pledged as collateral for $45.7 million of senior secured debt outstanding as of December 31, 2014. Information regarding interest rates and principal maturities is provided in Note 6 to the Consolidated Financial Statements.

CEQA Claims Challenging Water Project Approvals

As noted under Item 1A, Risk Factors, third parties have the ability in California to file litigation challenging the approval of a project.

In 2012, the Company was named as a real-party-in-interest in nine lawsuits related to the Water Project approvals granted in 2012 by the Santa Margarita Water District (“SMWD”) and the County of San Bernardino (“County”) in accordance with the California Environmental Quality Act (“CEQA”). In 2013, three cases were dismissed or otherwise settled. Trial in the six remaining cases, which were brought by two petitioners, began in December 2013 and concluded in February 2014.

The six lawsuits challenged the following three (3) separate Project approvals:

|

(1)

|

MOU Approval – two cases filed by Tetra Technologies, Inc. (“Tetra”) (NYSE: TTI) challenging the May 2012 approvals of the Memorandum of Understanding between Cadiz, SMWD and the County related to the Project’s Groundwater Management, Monitoring & Mitigation Plan (“GMMMP”).

|

|

(2)

|

EIR Approval – two cases filed by Tetra and Center for Biological Diversity, et al (“CBD”) challenging the adequacy of the EIR certified by SMWD on July 31, 2012.

|

|

(3)

|

GMMMP Approval – two cases filed by Tetra and CBD challenging the approval of the GMMMP by the County Board of Supervisors on October 1, 2012:

|

In September 2014, the Orange County Superior Court (“Court”) issued final signed judgments (“Judgments”) formally denying all claims brought in the six lawsuits and upholding the environmental review and the approvals described above. The Judgments also awarded costs to SMWD, the County, Cadiz and Fenner Valley Mutual Water Company as the prevailing parties in the cases and served as the Court’s final actions in the six cases.

During the fourth quarter of 2014, the petitioners in these cases filed independent appeals of the six Judgments with the California Court of Appeals, Fourth District. These appeals were anticipated and are expected to be heard by the Appeals Court in 2015. The appeals process is not projected to have any impact on the Company’s ongoing implementation and pre-construction activities for the Water Project. We cannot predict with certainty the timing or outcome of any of the proceedings.

Other Proceedings

There are no other material legal proceedings pending to which we are a party or of which any of our property is the subject.

PART II

Our common stock is currently traded on The NASDAQ Global Market ("NASDAQ") under the symbol "CDZI." The following table reflects actual sales transactions for the dates that we were trading on NASDAQ, as reported by NASDAQ.

|

High

|

Low

|

|||||||

|

Quarter Ended

|

Sales Price

|

Sales Price

|

||||||

|

2013:

|

||||||||

|

March 31

|

$

|

6.79

|

$

|

6.69

|

||||

|

June 30

|

$

|

4.83

|

$

|

4.58

|

||||

|

September 30

|

$

|

5.15

|

$

|

5.05

|

||||

|

December 31

|

$

|

7.22

|

$

|

6.74

|

||||

|

2014:

|

||||||||

|

March 31

|

$

|

7.10

|

$

|

6.91

|

||||

|

June 30

|

$

|

8.48

|

$

|

8.29

|

||||

|

September 30

|

$

|

10.63

|

$

|

9.87

|

||||

|

December 31

|

$

|

11.69

|

$

|

11.09

|

||||

On March 4, 2015, the high, low and last sales prices for the shares, as reported by Bloomberg, were $11.33, $11.06, and $11.18, respectively.

As of December 31, 2014, the number of stockholders of record of our common stock was 97.

To date, we have not paid a cash dividend on our common stock and do not anticipate paying any cash dividends in the foreseeable future. Our senior secured term loan has covenants that prohibit the payment of dividends.

All securities sold by us during the three years ended December 31, 2014, which were not registered under the Securities Act of 1933, as amended, have been previously reported in accordance with the requirements of Rule 12b-2 of the Securities Exchange Act of 1934, as amended.

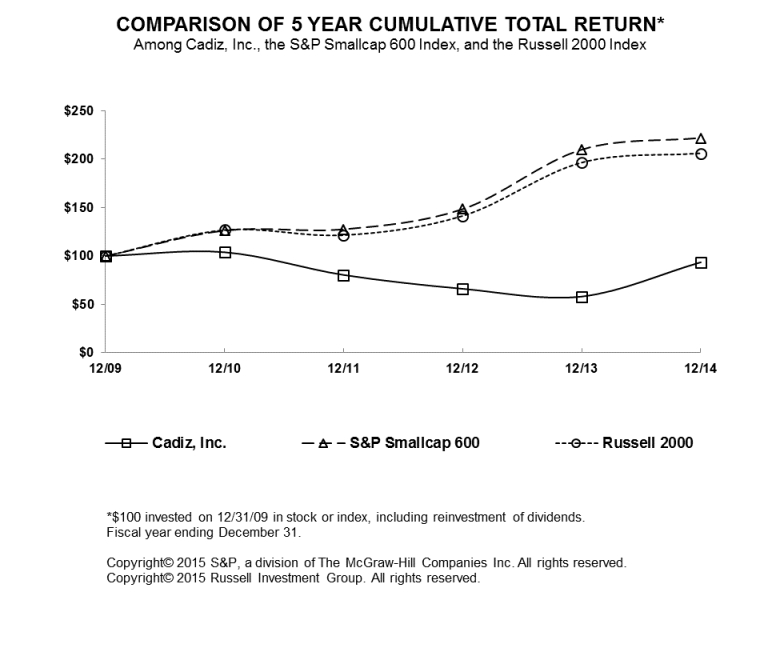

STOCK PRICE PERFORMANCE

The stock price performance graph below compares the cumulative total return of Cadiz Inc. common stock against the cumulative total return of the Standard & Poor’s Small Cap 600 NASDAQ U.S. index and the Russell 2000® index for the past five fiscal years. The graph indicates a measurement point of December 31, 2009, and assumes a $100 investment on such date in Cadiz Inc. common stock, the Standard & Poor’s Small Cap 600 and the Russell 2000® indices. With respect to the payment of dividends, Cadiz Inc. has not paid any dividends on its common stock, but the Standard & Poor’s Small Cap 600 and the Russell 2000® indices assume that all dividends were reinvested. The stock price performance graph shall not be deemed incorporated by reference by any general statement incorporating by reference this annual report on Form 10-K into any filing under the Securities Act of 1933, as amended, except to the extent that Cadiz Inc. specifically incorporates this graph by reference, and shall not otherwise be deemed filed under such acts.

The following selected financial data insofar as it relates to the years ended December 31, 2014, 2013, 2012, 2011, and 2010 has been derived from our audited financial statements. The information that follows should be read in conjunction with the audited consolidated financial statements and notes thereto for the period ended December 31, 2014 included in Part IV of this Form 10-K. See also Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations".

($ in thousands, except for per share data)

|

Year Ended December 31,

|

|||||||||||||||||||

|

2014

|

2013

|

2012

|

2011

|

2010

|

|||||||||||||||

|

Statement of Operations Data:

|

|||||||||||||||||||

|

Total revenues

|

$

|

336

|

$

|

301

|

$

|

362

|

$

|

1,019

|

$

|

1,023

|

|||||||||

|

Net loss

|

$

|

(18,881

|

)

|

$

|

(22,677

|

) |

$

|

(19,574

|

)

|

$

|

(16,837

|

)

|

$

|

(15,899

|

)

|

||||

|

Net loss applicable to common stock

|

$

|

(18,881

|

)

|

$

|

(22,677

|

) |

$

|

(19,574

|

)

|

$

|

(16,837

|

)

|

$

|

(15,899

|

)

|

||||

|

Per share:

|

|||||||||||||||||||

|

Net loss (basic and diluted)

|

$

|

(1.15

|

)

|

$

|

(1.46

|

) |

$

|

(1.27

|

)

|

$

|

(1.20

|

)

|

$

|

(1.16

|

)

|

||||

|

Weighted-average common shares outstanding

|

16,370

|

15,570

|

15,438

|

14,082

|

13,672

|

||||||||||||||

|

December 31,

|

|||||||||||||||||||

|

2014

|

2013

|

2012

|

2011

|

2010

|

|||||||||||||||

|

Balance Sheet Data:

|

|||||||||||||||||||

|

Total assets

|

$

|

68,212

|

$

|

64,174

|

$

|

50,518

|

$

|

57,998

|

$

|

48,936

|

|||||||||

|

Long-term debt

|

$

|

104,384

|

$

|

96,417

|

$

|

63,250

|

$ |

52,032

|

$ |

44,403

|

|||||||||

|

Common stock and additional paid-in capital

|

$

|

319,781

|

$

|

304,140

|

$

|

301,193

|

$

|

300,317

|

$

|

282,496

|

|||||||||

|

Accumulated deficit

|

$

|

(359,519

|

)

|

$

|

(340,638

|

) |

$

|

(317,961

|

)

|

$

|

(298,387

|

)

|

$

|

(281,550

|

)

|

||||

|

Stockholders' (deficit) equity

|

$

|

(39,738

|

)

|

$

|

(36,498

|

) |

$

|

(16,768

|

)

|

$

|

1,930

|

$

|

946

|

||||||

Common shares issued and outstanding have increased from 13,677,772 in 2010 to 17,681,274 as of December 31, 2014. The increase is primarily due to the issuance of shares to investors in private placements, the issuance of shares to investors upon warrant exercises, and the issuance of shares to employees, vendors and lenders.

In connection with the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995, the following discussion contains trend analysis and other forward-looking statements. Forward-looking statements can be identified by the use of words such as "intends", "anticipates", "believes", "estimates", "projects", "forecasts", "expects", "plans" and "proposes". Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from these forward-looking statements. These include, among others, our ability to maximize value from our land and water resources and our ability to obtain new financings as needed to meet our ongoing working capital needs. See additional discussion under the heading "Risk Factors” above.

Overview

We are a land and water resource development company with 45,000 acres of land in three areas of eastern San Bernardino County, California. Virtually all of this land is underlain by high-quality, naturally recharging groundwater resources, and is situated in proximity to the Colorado River and the Colorado River Aqueduct (“CRA”), a major source of imported water for Southern California. Our main objective is to realize the highest and best use of these land and water resources in an environmentally responsible way.

For more than 20 years, we have maintained an agricultural development at our 34,000-acre property in the Cadiz and Fenner valleys of eastern San Bernardino County (the “Cadiz/Fenner Property”), relying upon groundwater from the underlying aquifer system for irrigation. In 1993, we secured permits to develop agriculture on up to 9,600 acres of the Cadiz/Fenner Property and withdraw more than one million acre-feet of groundwater from the underlying aquifer system. Since that time, we have maintained various levels of agriculture at the property and this operation has provided our principal source of revenue.

In addition to our sustainable agricultural operations, we believe that the long-term value of our land assets can best be derived through the development of a combination of water supply and storage projects at our properties. The primary factor driving the value of such projects is continuing pressure on water supplies throughout California, which has led Southern California water providers to actively seek new, reliable supply solutions to plan for both short and long-term water needs. This includes environmental and regulatory restrictions on each of the State’s three main water sources: the State Water Project, which provides water supplies from Northern California to the central and southern parts of the state, the CRA and the Los Angeles Aqueduct. Southern California’s water providers rely on imports from these systems for a majority of their water supplies, but deliveries from all three in the region have been below capacity over the last several years. Availability of supplies in California also differs greatly from year to year due to natural hydrological variability.

At present, our water development efforts are primarily focused on the Cadiz Valley Water Conservation, Recovery and Storage Project (“Water Project” or “Project”), which will capture and conserve millions of acre-feet of native groundwater currently being lost to evaporation from the aquifer system beneath our Cadiz/Fenner Property and deliver it to water providers throughout Southern California (see “Water Resource Development” below). We believe that the ultimate implementation of this Water Project will create the primary source of our future cash flow and, accordingly, our working capital requirements relate largely to the development activities associated with this Water Project.

We also continue to explore additional uses of our land and water resource assets, including new agricultural opportunities, the development of a land conservation bank on our properties outside the Water Project area and other long-term legacy uses of our properties, such as habitat conservation and cultural uses.

In addition to these development efforts, we will also pursue strategic investments in complementary business or infrastructure to meet our objectives. We cannot predict with certainty when or if these objectives will be realized.

Water Resource Development