Attached files

| file | filename |

|---|---|

| EX-23.2 - EXHIBIT 23.2 - TRIBUNE MEDIA CO | ex232deloitteconsent.htm |

| EX-23.1 - EXHIBIT 23.1 - TRIBUNE MEDIA CO | ex-231pwcconsent.htm |

| EX-21.1 - EXHIBIT 21.1 - TRIBUNE MEDIA CO | ex-21subsidiaries.htm |

| EX-10.21 - EXHIBIT 10.21 - TRIBUNE MEDIA CO | ex-1021formrsuagreement.htm |

| EX-10.22 - EXHIBIT 10.22 - TRIBUNE MEDIA CO | ex-1022formpsuagreement.htm |

| EX-32.1 - EXHIBIT 32.1 - TRIBUNE MEDIA CO | ex-321906certificationceo.htm |

| EX-31.2 - EXHIBIT 31.2 - TRIBUNE MEDIA CO | ex-312302certificationcfo.htm |

| EX-10.20 - EXHIBIT 10.20 - TRIBUNE MEDIA CO | ex-1020formstockoptionagr.htm |

| EX-31.1 - EXHIBIT 31.1 - TRIBUNE MEDIA CO | ex-311302certificationceo.htm |

| EX-32.2 - EXHIBIT 32.2 - TRIBUNE MEDIA CO | ex-322906certificationcfo.htm |

| EX-99.1 - EXHIBIT 99.1 - TRIBUNE MEDIA CO | ex-991foodnetworkfinancials.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 28, 2014

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-8572

TRIBUNE MEDIA COMPANY

(Exact name of registrant as specified in its charter)

Delaware | 36-1880355 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

435 North Michigan Avenue, Chicago, Illinois | 60611 | |

(Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (212) 210-2786

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Class A Common Stock, par value $0.001 per share | The New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K (Check box if no delinquent filers). x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | o | Accelerated filer | o | Non-accelerated filer | x | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the voting common equity held by non-affiliates of the registrant based on the closing sales prices of the registrant’s Class A Common Stock and Class B Common Stock as reported on the OTC Bulletin Board (“OTC”) market on June 29, 2014, was $6,612,289,792.

As of February 28, 2015, 92,076,777 shares of the registrant’s Class A Common Stock and 2,433,292 shares of the registrant’s Class B Common Stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The definitive proxy statement relating to the registrant’s Annual Meeting of Shareholders to be held on May 20, 2015 is incorporated by reference in Part III to the extent described therein.

TRIBUNE MEDIA COMPANY

INDEX TO 2014 FORM 10-K

Item No. | Page | |

Part I | ||

1. | Business | |

1A. | Risk Factors | |

1B. | Unresolved Staff Comments | |

2. | Properties | |

3. | Legal Proceedings | |

4. | Mine Safety Disclosures | |

Part II | ||

5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

6. | Selected Financial Data | |

7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |

7A. | Quantitative and Qualitative Disclosures about Market Risk | |

8. | Financial Statements and Supplementary Data | |

9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

9A. | Controls and Procedures | |

9B. | Other Information | |

Part III | ||

10. | Directors, Executive Officers and Corporate Governance | |

11. | Executive Compensation | |

12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

13. | Certain Relationships and Related Transactions, and Director Independence | |

14. | Principal Accountant Fees and Services | |

Part IV | ||

15. | Exhibits and Financial Statement Schedules | |

Signatures | ||

Index to Consolidated Financial Statements | ||

Report of Independent Registered Public Accounting Firm | ||

Consolidated Financial Statements and Notes | ||

Exhibits | ||

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K for the fiscal year ended December 28, 2014 (the “Annual Report”) contains “forward-looking statements” within the meaning of the federal securities laws, including, without limitation, statements concerning the conditions in our industry, our operations, our economic performance and financial condition, including, in particular, statements relating to our business and growth strategy and product development efforts under “Item 1. Business” and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements include all statements that do not relate solely to historical or current facts, and can be identified by the use of words such as “may,” “might,” “will,” “should,” “estimate,” “project,” “plan,” “anticipate,” “expect,” “intend,” “outlook,” “believe” and other similar expressions. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of their dates. These forward-looking statements are based on estimates and assumptions by our management that, although we believe to be reasonable, are inherently uncertain and subject to a number of risks and uncertainties. These risks and uncertainties include, without limitation, those identified under “Item 1A. Risk Factors” and elsewhere in this Annual Report.

The following list represents some, but not necessarily all, of the factors that could cause actual results to differ from historical results or those anticipated or predicted by these forward-looking statements:

• | competition and other economic conditions including incremental fragmentation of the media landscape and competition from other media alternatives; |

• | changes in advertising demand and audience shares; |

• | changes in the overall market for broadcast and cable television advertising, including through regulatory and judicial rulings; |

• | our ability to protect our intellectual property and other proprietary rights; |

• | our ability to adapt to technological changes; |

• | our ability to develop and grow or maintain our online businesses; |

• | availability and cost of quality network, syndicated and sports programming affecting our television ratings; |

• | the loss, cost and / or modification of our network affiliation agreements; |

• | our ability to renegotiate retransmission consent agreements with multichannel video programming distributors (“MVPDs”); |

• | our ability to expand our metadata business operations internationally; |

• | the incurrence of costs to address contamination issues at physical sites owned, operated or used by our businesses; |

• | adverse results from litigation, governmental investigations or tax-related proceedings or audits; |

• | our ability to settle unresolved claims filed in connection with the Debtors’ Chapter 11 cases and resolve the appeals seeking to overturn the Confirmation Order (as defined and described below in “Item 1A. Risk Factors—Risks Related to Our Emergence from Bankruptcy”); |

• | our ability to satisfy pension and other postretirement employee benefit obligations; |

• | our ability to attract and retain employees; |

• | the effect of labor strikes, lock-outs and labor negotiations; |

• | our ability to realize benefits or synergies from acquisitions or divestitures or to operate our businesses effectively following acquisitions or divestitures; |

• | the financial performance of our equity method investments; |

• | the impairment of our existing goodwill and other intangible assets; |

3

• | changes in accounting standards; |

• | impact of increases in interest rates on our variable rate indebtedness or refinancings thereof; |

• | our indebtedness and ability to comply with covenants applicable to our debt financing and other contractual commitments; |

• | our ability to satisfy future capital and liquidity requirements; |

• | our ability to access the credit and capital markets at the times and in the amounts needed and on acceptable terms; |

• | the factors discussed in “Item 1A. Risk Factors” of this Annual Report; and |

• | other events beyond our control that may result in unexpected adverse operating results. |

We caution you that the foregoing list of important factors is not exclusive. In addition, in light of these risks and uncertainties, the matters referred to in the forward-looking statements contained in this Annual Report may not in fact occur. We undertake no obligation to publicly update or revise any forward-looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

PART I

ITEM 1. BUSINESS

Company Overview

Tribune Media Company is a diversified media and entertainment business. It is comprised of 42 television stations that are either owned by us or owned by others, but to which we provide certain services, which we refer to as “our television stations,” along with a national general entertainment television network, a radio station, a production studio, a digital and data technology business, a portfolio of real estate assets and investments in a variety of media, websites and other related assets. We believe our diverse portfolio of assets distinguishes us from traditional pure-play broadcasters through our ownership of high-quality original and syndicated programming, our ability to capitalize on revenue growth from our data and real estate assets, and cash distributions from our equity investments. Unless otherwise indicated, references in this Annual Report to “Tribune Media,” “Tribune,” “we,” “our,” “us” and the “Company” refer to Tribune Media Company and its consolidated subsidiaries.

Our business operates in the following two reportable segments:

• | Television and Entertainment: Provides audiences across the country with news, entertainment and sports programming on Tribune Broadcasting local television stations and distinctive, high quality television series and movies on WGN America, including through content produced by Tribune Studios and its production partners. |

• | Digital and Data: Provides innovative technology and services that collect and distribute video, music and entertainment data primarily through wholesale distribution channels to consumers globally. |

In addition, we report and include under Corporate and Other certain administrative activities associated with operating our corporate office functions and managing our predominantly frozen company-sponsored defined benefit pension plans, as well as the management of certain of our real estate assets, including revenues from leasing office and production facilities. We also currently hold a variety of investments in cable and digital assets, including equity investments in Television Food Network, G.P. (“TV Food Network”) and CareerBuilder, LLC (“CareerBuilder”).

4

Organizational Structure and History

Tribune Media Company is a holding company that does business through its direct and indirect operating subsidiaries. Previously known as Tribune Company, we were founded in 1847 and incorporated in Delaware in 1968. Throughout the 1980s and 1990s, we grew rapidly through a series of broadcasting acquisitions and strategic investments in companies such as TV Food Network, CareerBuilder and Classified Ventures, LLC (“CV”). On December 20, 2007, we completed a series of transactions (collectively, the “Leveraged ESOP Transactions”) which culminated in the cancellation of all issued and outstanding shares of the Company’s common stock as of that date and with the Company becoming wholly-owned by the Tribune Company employee stock ownership plan (the “ESOP”).

As a result of severe declines in advertising and circulation revenues leading up to and during the recession that followed the global financial crisis of 2007-2008, as well as the general deterioration of the publishing and broadcasting industries during such time, we faced significant constraints on our liquidity, including our ability to service our indebtedness. Due to these factors, in December 2008 we filed for protection under chapter 11 (“Chapter 11”) of title 11 of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court of the District of Delaware (the “Bankruptcy Court”). From December 2008 through December 2012, we operated our businesses under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the Bankruptcy Code, the Federal Rules of Bankruptcy Procedure and applicable orders of the Bankruptcy Court.

As our emergence from bankruptcy was subject to the consent of the Federal Communications Commission (“FCC”) to the assignment of our FCC broadcast and auxiliary station licenses as part of our reorganization, in April 2010 we filed applications with the FCC to obtain FCC approval for such assignments.

In April 2012, we filed our final plan of reorganization which was the result of extensive negotiations and contested proceedings before the Bankruptcy Court, principally related to the resolution of certain claims and causes of action arising between certain of our creditors in connection with the Leveraged ESOP Transactions. In July 2012, the Bankruptcy Court issued an order confirming our plan of reorganization.

In November 2012, the FCC granted the applications to assign our broadcast and auxiliary station licenses to our licensee subsidiaries. We emerged from Chapter 11 on December 31, 2012.

After the confirmation of our bankruptcy plan and the receipt of the FCC’s consent to its implementation, we consummated an internal restructuring pursuant to the terms of our bankruptcy plan. For further details, see Note 3 to our audited consolidated financial statements.

On December 27, 2013, pursuant to a securities purchase agreement dated as of June 29, 2013, we acquired all of the issued and outstanding equity interests in Local TV, including the subsidiaries Local TV, LLC and FoxCo Acquisition, LLC, for $2.8 billion in cash, net of working capital and other closing adjustments (the “Local TV Acquisition”). As a result of the acquisition, we became the owner of 16 of the 19 television stations in Local TV’s portfolio. Concurrently with the Local TV Acquisition, Dreamcatcher Broadcasting LLC (“Dreamcatcher”), acquired the FCC licenses and certain other assets and liabilities of Local TV’s television stations WTKR-TV, Norfolk, VA, WGNT-TV, Portsmouth, VA and WNEP-TV, Scranton, PA (collectively, the “Dreamcatcher Stations”) (the “Dreamcatcher Transaction”). We subsequently entered into shared services agreements (“SSAs”) with Dreamcatcher to provide technical, promotional, back-office, distribution and certain programming services to the Dreamcatcher Stations consistent with current FCC rules and policies.

On August 4, 2014, we completed a separation transaction (the “Publishing Spin-off”), resulting in the spin-off of the assets and certain liabilities of the businesses primarily related to our principal publishing

operations, other than owned real estate and certain other assets (the “Publishing Business”), through a tax-free,

pro rata dividend to our stockholders and warrantholders of 98.5% of the shares of common stock of Tribune

Publishing Company (“Tribune Publishing”), and we retained 1.5% of the outstanding common stock of Tribune Publishing. The Publishing Business consisted of newspaper publishing and local news and information gathering functions that operated daily newspapers and related websites, as well as a number of ancillary businesses that leveraged certain of the assets of those businesses. As a result of the completion of the Publishing Spin-off, Tribune Publishing operates the Publishing Business as an independent, publicly-traded company.

5

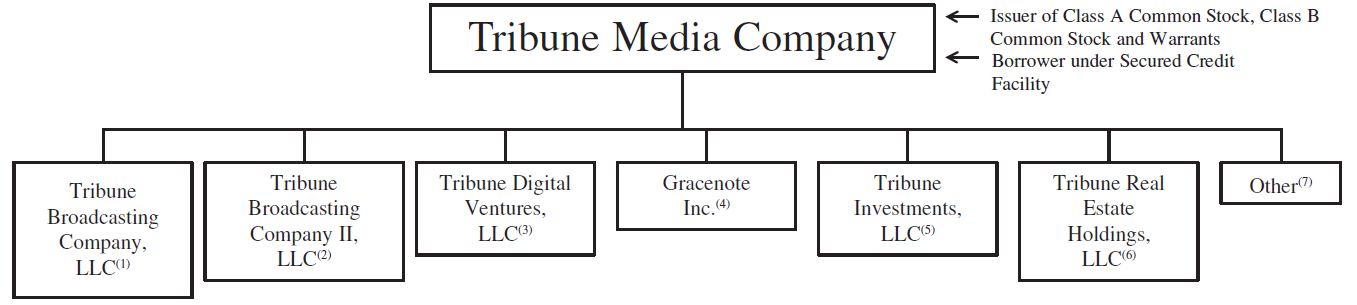

The following chart illustrates our organizational structure as of the date hereof:

(1) This entity and its direct and indirect subsidiaries hold our broadcasting businesses (with the exception of the broadcasting businesses that we acquired through our acquisition of Local TV), including WGN America, and our equity method investment in TV Food Network.

(2) This entity and its direct and indirect subsidiaries hold our broadcasting businesses that we acquired through our acquisition of Local TV.

(3) This entity and its direct and indirect subsidiaries hold our digital and data businesses (with the exception of our Gracenote Music businesses).

(4) This entity and its direct and indirect subsidiaries hold our Gracenote Music businesses.

(5) This entity and its direct and indirect subsidiaries hold certain of our other equity method investments, including our investment in CareerBuilder.

(6) This entity and its direct and indirect subsidiaries hold the majority of our real estate assets.

(7) Other direct and indirect subsidiaries that hold various broadcasting and other Company assets, including certain cost method investments and international businesses.

Competitive Strengths

We believe that we benefit from the following competitive strengths:

Geographically diversified media properties in attractive U.S. markets.

We are one of the largest independent station owner groups in the United States based on household reach, and we own or operate local television stations in each of the nation’s top five markets by population and seven of the top ten markets. We have network affiliations with all of the major over-the-air networks, including American Broadcasting Company (“ABC”), CBS Corporation (“CBS”), FOX Broadcasting Company (“FOX”), National Broadcasting Company (“NBC”) and The CW Network, LLC (“CW”). We provide must-see programming, including the National Football League and other live sports, on many of our stations and local news to over 50 million U.S. households in the aggregate, as measured by Nielsen Media Research (“Nielsen”), representing approximately 44% of all U.S. households.

In addition, we own a national general entertainment network, WGN America, which is distributed to approximately 73 million households nationally, as measured by Nielsen. WGN America provides us with a platform for launching original programming and exclusive syndication content. We believe that the combination of our broadcast stations and WGN America creates a unique distribution platform.

Core competency in metadata.

Our metadata powers the television listings and schedules for on-screen Electronic Program Guides (“EPG”) through cable and satellite providers via set-top boxes or other means and makes it possible to search for specific television episodes and series and set digital video recorder (“DVR”) recordings. It also powers the algorithms that make movie and music recommendations possible for popular streaming music and on-demand video services.

The demand from consumers and, therefore, distributors has grown for the metadata we have historically provided through our Tribune Media Services business. Data is becoming more vital to businesses as it is used to make smarter decisions about investing in content and provide enhanced measurement tools to drive advertising efficiency and effectiveness.

As consumer demand continues to increase, we are well positioned to take advantage of this trend by adding scale to our existing business. The industry is highly fragmented by data set, region and service layer.

6

Strong and diverse cash flow generation.

Our core businesses have historically generated strong cash flows from operations. In 2014, our net cash provided by operating activities was $378 million, which includes $190 million of cash distributions received from our equity investments. In addition to the cash distributions accounted for within net cash provided by operating activities, cash flows from investing activities included $181 million of cash distributions from our equity investments, of which $160 million was from CV related to the sale of its Apartments.com business. Our equity investments have historically provided substantial cash distributions annually. These strong cash flows provide us with the financial flexibility to pursue our strategies both through organic investments in our existing businesses and through accretive acquisition opportunities. We are making investments across our businesses, including in the acquisition of original content and the expansion of our digital and data businesses.

Valuable real estate holdings.

We own attractive real estate in key markets, including development rights for certain of our real estate assets. We actively manage our portfolio of real estate assets to drive value through the following initiatives:

• | Maximize utility of our existing real estate footprint; |

• | Generate revenues on excess space by leasing to third parties; |

• | Opportunistically dispose of underutilized or non-essential properties; and |

• | Develop vacant properties or properties with redevelopment options. |

Experienced management team with demonstrated industry experience.

Our senior management team has broad and diverse experience across their respective disciplines, with proven track records of success in the industry. Peter Liguori, our President and Chief Executive Officer, is an experienced media industry leader with a background in developing successful programming. Our organization consists of talented executives with expertise across finance, strategy, operations, regulatory matters and human resources. Our management team has a unified vision for the Company, which includes capitalizing on our current strengths and strategically investing in new initiatives and businesses to generate increased value for our stockholders.

Strategies

Our mission is to create, produce and distribute outstanding entertainment, news and sports content and digital data that inform, entertain, engage, and inspire millions of people every day. To achieve this mission, we are pursuing the following strategies:

Utilize the scale and quality of our operating businesses to increase value to all of our partners: advertisers, MVPDs, network affiliates and consumers.

Our television station group reaches over 50 million households nationally, as measured by Nielsen, representing approximately 44% of all U.S. households. WGN America, our national general entertainment network, reaches approximately 62% of U.S. households and the digital networks we operate, Antenna TV and THIS TV, collectively reach approximately 90% of U.S. households. We also operate approximately 50 websites primarily associated with our television stations, which, in 2014, reached an average of 63 million unique visitors monthly. Our metadata businesses feature information and content for more than 6.7 million TV shows and movies and 200 million song tracks.

Through our extensive distribution network, we can deliver content through a multitude of channels. This ability to reach consumers across a broad geographical footprint is valuable for advertisers, MVPDs and affiliates alike as we connect consumers with their messaging and quality content.

WGN America is currently undergoing a transformation from a superstation to a fully distributed general entertainment cable channel. Our strategy is to build a network that combines high quality, original programming as well as exclusive, highly-rated syndicated programming and feature films.

7

Be the most valued source of local news and information in the markets in which we operate.

Local news is a cornerstone of our local television stations. We believe local news enjoys a competitive advantage relative to national news outlets due to its ability to generate immediate reporting, which is especially valuable when a breaking news story develops in a local market. We are also able to utilize our breadth of coverage to distribute local content on a national scale by sharing news stories on-air and digitally across Tribune-covered markets. Annually, we produce approximately 75,000 hours of news in our 33 U.S. markets. We also operate approximately 50 websites and approximately 125 mobile applications.

Continue to shift to a content ownership model that will result in both the retention of a greater share of advertising revenue and allow us to participate in the longer tail of programming monetization.

As competition for media advertising spend continues to increase, we are focused on developing our Tribune Studios business to drive future growth by creating original content to be distributed across our WGN America and television station platforms, as well as on other streaming platforms such as Hulu or Netflix. We believe that retaining the rights associated with our content will provide us with a competitive advantage relative to broadcasters that rely primarily on licensed programming acquired from third-party syndicators. A shift away from licensing content from third parties to content ownership will provide us with new outlets, such as over-the-top (“OTT”), subscription video on demand (“SVOD”) and international rights through which to monetize programming. Owned programming that airs across our station group further allows us to retain a greater share of overall advertising revenue generated from such content.

Develop a leading global metadata business.

Having started with Tribune Media Services as our core metadata asset, we have been selectively acquiring both domestic and foreign metadata businesses in order to capitalize on our core competency in data and technology by driving increased scale in our business and providing deeper and richer global content solutions. Through such acquisitions, we expect to be able to provide improved services for current domestic customers and to compete for international customers through the use of innovative technologies that will generate increased monetization opportunities of our data assets.

Strategically identify and pursue acquisition opportunities to complement our organic growth strategy.

As a complement to our organic growth initiatives, we intend to continue to pursue a selective acquisition strategy that seeks to enhance our offerings and increase our scale. In evaluating prospective investment decisions, we assess the strategic fit, including application of our core competencies and projected cash returns, taking into consideration relevant regulations applicable to owners of broadcast television stations, but which do not apply to cable networks. We also believe there will be opportunities for us to continue to build scale and technology capabilities in our data businesses.

Maximize the long term value of our real estate assets.

We intend to maximize the long term value of our real estate assets primarily by employing best practices in the operation and management of our holdings and selectively forming strategic partnerships with knowledgeable local developers in certain markets where our assets are located.

Segments

We operate our business through two reportable segments: (1) Television and Entertainment and (2) Digital and Data. In addition, certain administrative activities associated with operating our corporate office functions and managing our predominantly frozen company-sponsored defined benefit pension plans, as well as the management of certain of our real estate assets, including revenues from leasing office and production facilities, are reported under Corporate and Other. We also currently hold a variety of minority investments in cable and digital assets, including TV Food Network and CareerBuilder.

8

Television and Entertainment

Our Television and Entertainment reportable segment consists of the following businesses:

• | Television broadcasting services through Tribune Broadcasting, which owns or provides services to 42 broadcast television stations located in 33 U.S. markets; |

• | Digital multicast network services through Antenna TV and through the operation and distribution of THIS TV, both of which are digital networks that air in households nationally; |

• | National program services through WGN America, a national general entertainment network; |

• | Tribune Studios, a development and production studio; and |

• | Radio program services on WGN, a Chicago radio station. |

Tribune Broadcasting

Our broadcast television stations serve the local communities in which they operate by providing locally produced news and special interest broadcasts as well as syndicated programming.

Tribune Broadcasting owns or provides certain services to 42 local television stations, reaching more than 50 million households nationally, as measured by Nielsen, making us one of the largest independent station groups in the United States based on household reach. Currently, our television stations, including the 3 stations to which we provide certain services under SSAs with Dreamcatcher, consist of 14 FOX television affiliates, 13 CW television affiliates, 6 CBS television affiliates, 3 ABC television affiliates, 2 NBC television affiliates and 4 independent television stations. Our affiliates represent all of the major over-the-air networks, and we own or operate local television stations in each of the nation’s top five markets and seven of the top ten markets.

9

The following chart provides additional information regarding our television stations:

Stations | Market | Market Rank(1) | % of U.S. Households | Primary Network Affiliations | Affiliation Expiration | |||||

WPIX | New York | 1 | 6.5% | CW | 2016 | |||||

KTLA | Los Angeles | 2 | 4.9% | CW | 2016 | |||||

WGN | Chicago | 3 | 3.1% | CW | 2016 | |||||

WPHL | Philadelphia | 4 | 2.6% | MY | 2015 | |||||

KDAF | Dallas | 5 | 2.3% | CW | 2016 | |||||

WDCW | Washington | 8 | 2.1% | CW | 2016 | |||||

KIAH | Houston | 10 | 2.0% | CW | 2016 | |||||

KCPQ / KZJO | Seattle | 14 | 1.6% | FOX / MY | 2018/2015 | |||||

WSFL | Miami | 16 | 1.4% | CW | 2016 | |||||

KDVR / KWGN | Denver | 17 | 1.4% | FOX / CW | 2018/2016 | |||||

WJW | Cleveland | 19 | 1.3% | FOX | 2018 | |||||

KTXL | Sacramento | 20 | 1.2% | FOX | 2016(4) | |||||

KTVI / KPLR | St. Louis | 21 | 1.1% | FOX / CW | 2018/2016 | |||||

KRCW | Portland | 23 | 1.0% | CW | 2016 | |||||

WXIN / WTTV | Indianapolis | 27 | 1.0% | FOX / CBS(2) | 2016(4)/2019 | |||||

KSWB | San Diego | 28 | 0.9% | FOX | 2017(4) | |||||

WTIC / WCCT | Hartford | 30 | 0.9% | FOX / CW | 2016(4)/2016 | |||||

WDAF | Kansas City | 31 | 0.8% | FOX | 2018 | |||||

KSTU | Salt Lake City | 34 | 0.8% | FOX | 2018 | |||||

WITI | Milwaukee | 35 | 0.8% | FOX | 2018 | |||||

WXMI | Grand Rapids | 40 | 0.6% | FOX | 2016(4) | |||||

WTKR(3) / WGNT(3) | Norfolk | 42 | 0.6% | CBS / CW | 2019/2016 | |||||

KFOR / KAUT | Oklahoma City | 44 | 0.6% | NBC / IND | 2015/NA | |||||

WPMT | Harrisburg | 45 | 0.6% | FOX | 2016(4) | |||||

WGHP | Greensboro | 46 | 0.6% | FOX | 2018 | |||||

WREG | Memphis | 50 | 0.6% | CBS | 2019 | |||||

WGNO / WNOL | New Orleans | 51 | 0.6% | ABC / CW | 2019/2016 | |||||

WNEP(3) | Wilkes Barre | 55 | 0.5% | ABC | 2019 | |||||

WTVR | Richmond | 57 | 0.5% | CBS | 2019 | |||||

WHO | Des Moines | 72 | 0.4% | NBC | 2015 | |||||

WHNT | Huntsville | 79 | 0.3% | CBS | 2019 | |||||

WQAD | Davenport | 100 | 0.3% | ABC | 2019 | |||||

KFSM / KXNW | Ft. Smith | 101 | 0.3% | CBS / MY | 2019/2016 | |||||

(1) Market rank refers to ranking the size of the Designated Market Area (“DMA”) in which the station is located in relation to other DMAs. Source: Local Television Market Universe Estimates for 2014-2015, as published by Nielsen.

(2) Under the terms of our comprehensive long-term agreement to renew our existing CBS affiliation agreements, beginning on January 1, 2015, our WTTV-Indianapolis station became the CBS affiliate in the Indianapolis market. At the same time, our CW network affiliation in Indianapolis, which was broadcast on WTTV-Indianapolis through December 31, 2014, was relinquished for compensation.

(3) Stations owned by Dreamcatcher to which we provide certain services under SSAs. See Note 5 to our audited consolidated financial statements for further information.

(4) These FOX affiliation agreements include an early termination provision that permits FOX, upon notice, to reclaim the affiliation if FOX purchases a station within the corresponding DMA.

10

Our television and radio stations are operated pursuant to licenses granted by the FCC. Under rules promulgated and enforced by the FCC, each of our television stations has 6 megahertz of spectrum. Our television and radio operations are broadly regulated by the FCC, subject to ongoing rule changes, and subject to periodic renewal, as discussed further in “—Regulatory Environment” below.

A majority of U.S. households receive our broadcast programming through at least one of our television stations via MVPDs, which include cable television systems, direct broadcast satellite providers and wireline providers who pay us to offer our programming to their customers. We refer to such fees paid to us by MVPDs as retransmission consent revenues.

Programming

We source programming for our 39 Tribune Broadcasting-owned stations from the following sources:

• | News and entertainment programs that are developed and executed by the local television stations; |

• | Acquired and original syndicated programming; |

• | Programming received from our network affiliates that is retransmitted by our local television stations (primarily prime time and sports programming); and |

• | Paid programming. |

We produce approximately 75,000 hours of news annually in our 33 U.S. markets. Many of our newscasts are critically acclaimed.

Acquired syndicated programming, including both television series and movies, are purchased on a group basis for use by our owned stations. Contracts for purchased programming generally cover a period of up to five years, with payments typically made over several years.

For those stations with which we have a network affiliation, certain programming is acquired from the affiliated network, including FOX, CW, CBS, NBC and ABC. Network affiliation agreements dictate what programs are aired at specific times of the day, primarily during prime time. Our network affiliated stations are largely dependent upon the performance of network provided programs in order to attract viewers. Those day parts which do not contain network-provided content are programmed by the stations, primarily with syndicated programs purchased for cash, cash and barter or barter-only, as well as through self-produced news, live local sporting events, and other entertainment programming. We are also pursuing a strategy through Tribune Studios whereby we intend to develop more of our own first run, or original syndicated programming, for air on our owned stations. This could include owning the programming outright or being a partner with other media companies.

In addition, our stations air paid-programming whereby third parties pay our local television stations for a block of time to air long-form advertising. The content is a commercial message designed to represent the viewpoints and to serve the interest of the sponsor.

The programming sources described above relate to our 39 owned television stations. In compliance with FCC regulations, Dreamcatcher maintains complete responsibility for and control over programming, finances, personnel and operations of the three Dreamcatcher Stations. We provide technical, promotional, back-office, distribution and limited programming services for the Dreamcatcher Stations.

Sources of Revenue and Expenses

Tribune Broadcasting

Our television stations derive a majority of their revenue from local and national broadcasting advertising and retransmission consent revenues. Other sources of revenue include barter/trade revenues and copyright royalties. Barter revenue is the exchange of advertising airtime in lieu of cash payments for the rights to programming, equipment, merchandise or services. Copyright royalties represent distributions collected from satellite and cable

11

companies and distributed by the U.S. Copyright Office for programming created by us that is broadcast outside of the local market in which it is intended to air.

While serving the programming interests and needs of our television audiences, we also seek to meet the needs of our advertising customers by delivering significant audiences in key demographics. Our strategy is to achieve this objective by providing quality local news programming and popular network and syndicated programs to our viewing audience. We attract most of our national television advertisers through a retained national marketing representation firm. Our local television advertisers are attracted through the use of a local sales force at each of our television stations. We also derive advertising revenue from our television stations’ corresponding websites and mobile applications. In total, we currently operate approximately 50 websites and approximately 125 mobile applications. As consumers continue to turn to online resources for news and entertainment content, we are adapting and expanding our digital presence in each of the local markets where we operate.

Advertising revenues have historically been seasonal, with higher revenues generated in the second and fourth quarters of the year. Political advertising revenues are also cyclical, with a significant increase in spending in even numbered election years and disproportionate amounts being spent every four years during presidential campaign years.

We generate retransmission consent revenues from MVPDs in exchange for their right to carry our stations in their pay-television services to consumers. Retransmission rates are governed by multi-year agreements negotiated with each MVPD and are generally based on the number of monthly subscribers in each MVPD’s respective coverage area.

Expenses at our Tribune Broadcasting stations primarily consist of compensation and programming costs associated with producing local news and acquiring syndication rights to other content. Programming fees are also paid to our affiliate partners who typically provide prime time and sports programming to be carried in the local markets in which we operate.

Antenna TV and THIS TV

Antenna TV, which is owned and operated by Tribune Broadcasting, is a digital multicast network airing on television stations across the United States. The network features classic television programs and movies. Local television stations air Antenna TV as a digital multicast channel, often on a .2 or .3 channel depending on the city and the station, using data compression techniques that allow a television station to transmit more than one independent program channel at the same time. Antenna TV is free and available over-the-air using a traditional broadcast television or rooftop antenna. In addition, most major cable companies across the United States carry local affiliate feeds of Antenna TV. In some cities, stations run alternative local programming at various points throughout the day. Currently, the network is available in 97 markets, including markets in which Tribune owns or provides services to a television station. The primary source of revenue is advertising, both at the network level as well as the locally sold advertising for those markets in which we operate.

THIS TV is a digital multicast network airing on certain television stations across the United States. It is owned by Metro-Goldwyn-Mayer Studios, Inc. (“MGM”) and operated by Tribune Broadcasting. The network programming largely consists of movies, limited classic television series and children’s programming. Local television stations air THIS TV as a digital multicast channel often on a .2 or .3 channel, depending on the city and the station. THIS TV is free and available over-the-air using a traditional broadcast television or rooftop antenna. In addition, most major cable companies across the United States carry local affiliate feeds of THIS TV. Currently, the network is available in 123 markets, including markets in which Tribune owns or provides services to a television station. Revenue consists of locally sold advertising for those markets in which we operate, a fee from MGM for operating the network as well as profit participation.

WGN America

WGN America is our national, general entertainment network. The channel is currently available in approximately 73 million households as measured by Nielsen. WGN America programming is delivered by our MVPD partners and consists primarily of syndicated series and movies, and first-run original programming. Content

12

contracts are typically signed with the major studios and program distributors and cover a period of one to five years, with payment typically made over several years.

WGN America is currently undergoing a transformation from a superstation to a fully distributed general entertainment cable channel. To achieve this transformation, we are:

• | Negotiating with MVPDs to facilitate the conversion of WGN America’s signal from a superstation to a cable network, which commenced, in part, in December 2014; |

• | Negotiating with MVPDs to expand the household reach of the station (as measured by Nielsen) from approximately 73 million households today; and |

• | Improving the overall quality of programming on WGN America through greater investments in original scripted and unscripted content, exclusive syndication deals and premiere feature films. |

If successful, we anticipate that the change in status of WGN America to a fully distributed cable channel will improve advertising revenues and subscriber (carriage) fees received from MVPDs.

WGN America’s primary sources of revenue are:

• | Advertising revenues—We sell national advertising, with pricing based on audience size, the demographics of our audiences and the demand for our limited inventory of commercial time. |

• | Paid Programming—Third parties pay for a block of time to air long-form advertising, typically in overnight time blocks. |

• | Subscriber (carriage) fees—We earn revenues from agreements with MVPDs. The revenue we receive is typically based on the number of subscribers the MVPD has in their franchise area. |

• | Copyright revenue—We receive fee revenues distributed by the U.S. Copyright Office based on original programming that is retransmitted and not directly paid for by MVPDs. As MVPDs switch to a cable signal from the superstation signal, we will no longer receive copyright revenue. |

The primary expenses for WGN America are programming costs associated with new productions and marketing and promotion costs that are incurred as we launch new original series.

Tribune Studios

In March 2013, Tribune Studios was launched to source and produce original and exclusive content for WGN America and our local television stations, providing alternatives to acquired programming across a variety of daypart segments. We believe that a shift away from traditional syndication towards content ownership will provide meaningful value as we participate in the revenue streams from digital rights deals, domestic and foreign syndication rights and other monetization opportunities for our programming.

The below table presents our roster of new original and syndicated series developed, or in development, by Tribune Studios and its production partners as of the date of this filing:

Name of Series | Type | Network/ Station Aired | Air Date | |||

Salem | WGN America Licensed Original | WGN America | Spring 2015 (season 2) | |||

Manhattan | WGN America Co-owned Original | WGN America | Fall 2015 (season 2) | |||

Outsiders | WGN America Co-owned Original Ordered to Series | WGN America | TBD | |||

Underground | WGN America Co-owned Original Ordered to Series | WGN America | TBD | |||

Wrestling with Death | WGN America Owned Original | WGN America | January 2015 | |||

Outlaw Country | WGN America Owned Original | WGN America | February 2015 | |||

Celebrity Name Game | First-run Syndication-Equity Participant | Local Stations | Ongoing | |||

Bill Cunningham | First-run Syndication-Owned | Local Stations | Ongoing | |||

13

In addition to programming that is developed by Tribune Studios, our strategy for WGN America also includes obtaining rights for off-network syndication, many of which are exclusive. Our syndication programming includes the popular television series Blue Bloods, Elementary and Person of Interest.

Through our ownership of a national channel and the extensive footprint of our local television stations, we are uniquely positioned to leverage the scale of this distribution model to cross-promote our content, which we believe will provide an advantage to WGN America and our Tribune Broadcasting stations to build further awareness of our content and brands that will drive viewership across both networks.

When appropriate, we distribute Tribune Studios programming to our Tribune Broadcasting stations, as well as offer for license to third-party networks.

We expect to continue to make sizable investments in developing, creating and producing original programming content for both WGN America and our owned television stations.

Radio Station

We own WGN 720 AM, a radio station based in Chicago, Illinois. WGN 720 AM is a high-powered clear channel AM station, which has the highest protection from interference from other stations, and features talk-radio programs that host local personalities and provide sports play-by-play commentary.

Digital and Data

Our Digital and Data reportable segment operates under our business unit Tribune Digital Ventures (“TDV”). TDV was established in 2013 as a vehicle to manage and develop our digital products and services that leverage our content and data. Today, TDV is primarily focused on operating the following businesses:

• | Gracenote Video: Powering television and video listings on mobile applications, streaming devices and televisions through leading video metadata and other video services and technologies; |

• | Gracenote Music: Offering leading music, metadata and recognition and discovery technologies; and |

• | Entertainment Websites: Providing powerful entertainment resources to consumers. |

Gracenote Video, formerly known as TMS, historically operated primarily in the television metadata industry. Through the acquisition of Gracenote, Inc. (“Gracenote”) in early 2014, the combined business is also now a leader in music metadata and recognition and discovery technology, and has expanded into high growth areas, such as streaming music services, mobile devices, automotive infotainment and the television data market in key international markets.

Metadata powers the television listings, schedules and other content in on-screen EPG offered through cable and satellite providers via set-top boxes or other means and makes it possible to search for specific television episodes and series, as well as set DVR recordings. It also powers the algorithms that make movie and music recommendations possible for popular streaming music and on-demand video services. Demand has grown from consumers, and therefore distributors, for the metadata we have provided for decades through our TMS business and now provide through Gracenote Video and Gracenote Music. Distributors include companies that deliver music and video content to consumers through devices, platforms and applications, including pay-TV operators, streaming music services, online music stores, TV and consumer electronics manufacturers, over-the-top services and automakers and related suppliers.

Gracenote Video

Gracenote Video, whose roots originated in 1918, began operations in the publishing industry by syndicating columns, comic strips and other content items to newspapers. In addition to its syndication operations, with the birth of television and its wide adoption by consumers in the United States, it began creating and aggregating television listing information to provide to newspapers. Today, Gracenote Video collects and licenses entertainment data and reaches more than 100 million households through television, online and in print channels. Gracenote Video data is used daily in millions of homes in the United States and more than 50 other countries, including across Europe, Mexico, Latin America, India, the Middle East and parts of Africa. Gracenote Video provides TV listings and

14

associated metadata to many of the largest media, entertainment and technology companies in the world in order to power their EPGs.

Video metadata includes TV and movie descriptions, genres, cast and crew details, TV schedules and listings, TV episode and season numbers, unique program IDs and sports data. Video metadata consists of content sourced through a variety of means, including data produced, edited and curated by Gracenote’s editorial staff and technology, as well as data collected through broadcasters, studios and content creators and feeds from regional data providers.

Gracenote Video derives the majority of its revenue from cable, online, consumer electronics and other business-to-business (“B2B”) channels. Gracenote Video products include:

• | Gracenote On Entertainment: TV metadata, schedules, and other content carefully organized and delivered in a cloud-based API to power television on-screen guides, second screen apps and discovery platforms. |

• | ResearchTV: A web-based measurement tool that tracks TV show airings in order to provide valuable insights for studios analyzing royalties, broadcasters evaluating programming line-ups and advertisers looking to make quick decisions on media buys. |

• | Baseline’s The Studio System: A leading business intelligence platform, with the most comprehensive database of historical and forward-looking television and film data, deeply embedded in the daily workflow of film studios, television networks, talent agencies and production companies. |

• | What’s ON EPG Engine: TV and EPG data and services for pay-TV operators in India, the Middle East and other regions. |

• | What’s ON TV Street Maps: A broadcast TV monitoring service that provides TV channel placement and availability reports to broadcaster customers. Spanning approximately 2,400 pay-TV operators in approximately 2,000 towns and cities across India, TV Street Maps provides broadcasters and content distributors insight into where their channels are placed in pay-TV line-ups throughout the country. |

Schedule based television information and related content has historically been Gracenote Video’s largest component of revenue, but the increase in on-demand and online viewing is driving an increasing demand for non-linear information. Gracenote Video’s services support a variety of its customers’ consumer-facing products, including cable and satellite on-screen guides, smart TVs, mobile applications and online websites. In addition, it provides data to major research, royalty and reporting agencies. Revenues are primarily generated by multi-year subscriptions, which typically renew automatically.

While automation has allowed us to keep pace with the rapid proliferation of entertainment content worldwide, the strength of our technology and databases rely on an experienced and specialized workforce spread across offices in the United States, Europe, India and the Middle East. As such, compensation expense is the main component of Gracenote Video’s cost base, with occupancy and infrastructure costs accounting for much of the remainder.

As part of this strategy, Gracenote Video has made strategic investments to grow its video metadata business internationally. We expanded our data and geographic footprint with the acquisition of What’s On India Media Private Limited (“What’s ON”), a leading television search and EPG data provider for India and the Middle East in July 2014. What’s ON delivers data for more than 2,000 television channels and helps populate the data of more than 60 million set-top boxes through the regions’ top cable and internet protocol video systems (“IPTV”) services. What’s ON customers include some of the most-viewed television networks, service providers, and consumer electronics manufacturers.

In August 2014, we acquired Baseline LLC (“Baseline”), a movie and TV data services company. The acquisition of Baseline deepens Gracenote’s existing video metadata by adding more descriptive information about TV and movie productions as far back as 1896. Additionally, Baseline’s The Studio System platform expands Gracenote’s reach into the studio and TV network communities with data and subscription-based services geared towards entertainment industry professionals.

15

In October 2014, we acquired HWW Pty Ltd (“HWW”), Australia’s leading provider of TV and movie data. HWW syndicates TV and movie data to leading Australian broadcasters, pay-TV operators and on-demand services for program guides on a wide range of devices, including IPTV, cable & satellite set-top boxes, smart TVs and mobile apps. HWW has data describing millions of TV programs and movies across more than 500 national and local TV channels in Australia and its DataGenius software platform is used to support entertainment data services across Australasia, Africa and the Middle East.

Gracenote Music

Gracenote Music is one of the largest sources of music data in the world, featuring metadata for more than 200 million tracks as of December 28, 2014, which helps power nearly a billion mobile devices including smart phones, tablets and laptops, and many of the world’s most popular streaming music services. Gracenote Music technology is also featured in mobile applications as well as millions of smart TVs. Its music recognition technology is part of the audio systems in approximately 63 million cars from major automakers.

Metadata for music includes a variety of content such as artist name, album name, track name, music genre, origin, era, tempo and mood, as well as album cover art and artist images. The metadata consists of content sourced through various means, including data produced, edited and curated by Gracenote’s editorial staff and data derived from machine learning technology as well as data received from direct feeds from record labels and user submissions via software featuring Gracenote MusicID technology.

Gracenote Music products include:

• | Gracenote MusicID®: enables the identification of CDs, digital music files and music streams by a variety of devices and applications. MusicID delivers relevant music metadata, links to streaming music services, and cover art upon identification. |

• | Scan and Match: advanced form of music recognition technology that helps music fans identify and migrate their local music collections, stored on laptops and mobile devices, to the cloud. |

• | Gracenote Rhythm™: music discovery platform that enables the creation of internet radio and music recommendation services. |

Gracenote Music derives the majority of its revenue from licensing its metadata and technologies in the B2B segment. Gracenote Music licenses its products to customers on either a flat fee basis (“subscription”) or on a per-unit fee (“royalty based”). License agreements are non-exclusive and typically range from 24 to 36 months for non-automotive customers and 60 months for customers in the automotive business.

Gracenote Music also licenses certain content from third-party providers on a flat fee or use-based royalty basis. Gracenote Music’s primary expenses are compensation, occupancy and infrastructure, as well as research and development. Gracenote Music has operations in the United States, Europe and Asia.

Entertainment Websites

We operate a website, www.zap2it.com, dedicated to entertainment content which has two primary revenue streams: Zap2it and Zap2it Entertainment.

Zap2it offers television viewers a powerful resource for in-depth information on all aspects of their favorite television shows through a user interface compatible with all connected devices. It is an integrated TV discovery and editorial source that enables universal search capabilities across platforms by providing TV listings information for linear TV programming and direct links to movies and TV programs on popular streaming services, including Netflix, Amazon and Hulu. Content includes entertainment news relevant to the TV and celebrity world as well as TV listings information.

Zap2it Entertainment, formerly known as TV by the Numbers, is a leading editorial content provider dedicated to breaking news and analysis of television ratings data and network programming news from Hollywood. Zap2it Entertainment powers the TV Ratings editorial content on our Zap2it.com site.

16

Users of this website include consumers of entertainment content, television listing information and content regarding television ratings information. In 2014, Zap2it attracted approximately 6 million unique users monthly, as well as over 34 million monthly page views.

The primary source of revenue for the Zap2it.com website is direct and indirect display advertising.

Corporate and Other

The remaining activities that fall outside of our reportable segments consist of the following areas:

• | Costs associated with operating the corporate office functions and our predominantly frozen company-sponsored defined benefit pension plans; and |

• | Management of real estate assets, including revenues from leasing office space and operating facilities. |

We own the majority of the real estate and facilities used in the operations of our business. A large percentage of those facilities which house Tribune Publishing’s businesses are subject to operating leases. Our real estate holdings comprise 78 real estate assets, representing approximately 7.5 million square feet of office, studio, industrial and other buildings on land totaling approximately 1,100 acres. Certain of these properties and land are available for redevelopment. These include excess land, underutilized buildings, and older facilities located in urban centers. We estimate that approximately 4.7 million square feet and approximately 293 acres are available for full or partial redevelopment. See “Item 2. Properties” for further information on our real estate holdings.

We intend to maximize the long term value of our real estate assets primarily by employing best practices in the operation and management of our holdings and forming strategic partnerships with knowledgeable local developers in the various markets where our assets are located.

Investments

We hold a variety of investments, which include cable and digital assets. Currently, we derive significant cash flows from our two largest investments, which are a 31% interest in TV Food Network and a 32% interest in CareerBuilder.

TV Food Network operates two 24-hour television networks, Food Network and Cooking Channel, as well as their related websites. Our partner in TV Food Network is Scripps Networks Interactive, Inc. (“Scripps”), which owns a 69% interest in TV Food Network and operates the networks on behalf of the partnership. Food Network engages audiences by creating original programming that is entertaining, instructional and informative. Food Network is a fully distributed network in the United States with content distributed internationally. Cooking Channel caters to avid food lovers by focusing on food information and instructional cooking programming. Cooking Channel is a digital-tier network, available nationally and airs popular off-Food Network programming as well as originally produced programming.

CareerBuilder is a global leader in human capital solutions, helping companies target, attract and retain talent. Its website, CareerBuilder.com, is the largest job website in North America on the basis of traffic and revenue. CareerBuilder operates websites in the United States, Europe, Canada, Asia and South America. CareerBuilder is continuing to expand its international operations both organically and through acquisitions, including beyond its traditional business, such as recruitment solutions, which includes talent and compensation intelligence and target and niche websites.

On October 1, 2014, we completed the sale of our entire 27.8% equity interest in CV to Gannett Co., Inc. (“Gannett”). Our after-tax proceeds were approximately $426 million. As part of the transaction, Gannett also acquired the equity interests of the other partners and thereby acquired full ownership of CV.

We also hold a number of other smaller investments in private companies as well as a 1.5% interest in Tribune Publishing. See Note 8 to our audited consolidated financial statements for further information on our investments.

17

Competition

Television and Entertainment

The advertising marketplace has become increasingly fragmented as new forms of media vie for share of advertiser wallet. Our Television and Entertainment segment competes for audience share and advertising revenue with other broadcast television and radio stations, cable television and other media serving the same markets. Competition for audience share and advertising revenue is based upon various interrelated factors including programming content, audience acceptance and price. Our broadcast television stations compete for audience share and advertising revenue with other television stations in their respective DMAs, as well as with other advertising media such as MVPDs, radio, newspapers, magazines, outdoor advertising, transit advertising, telecommunications providers, internet and broadband and direct mail. Some competitors are part of larger organizations with substantially greater financial, technical and other resources than we have.

Other factors that are material to a television station’s competitive position include signal coverage, local program acceptance, network affiliation or program service, audience characteristics and assigned broadcast frequency. Competition in the television broadcasting industry occurs primarily in individual DMAs, which are generally highly competitive. Generally, a television broadcasting station in one DMA does not compete with stations in other DMAs. MVPDs can increase competition for a broadcast television station by bringing additional cable network channels into its market.

Television stations compete for audience share primarily on the basis of program popularity, which has a direct effect on advertising rates. Our network affiliated stations are largely dependent upon the performance of network provided programs in order to attract viewers. Non-network time periods are programmed by the station primarily with syndicated programs purchased for cash, cash and barter or barter-only, as well as through self-produced news, live local sporting events, paid-programming and other entertainment programming. Television advertising rates are based upon factors which include the size of the DMA in which the station operates, a program’s popularity among the viewers that an advertiser wishes to attract, the number of advertisers competing for the available time, the demographic makeup of the DMA served by the station, the availability of alternative advertising media in the DMA, the productivity of the sales forces in the DMA and the development of projects, features and programs that tie advertiser messages to programming.

We also compete for programming, which involves negotiating with national program distributors or syndicators that sell first-run and rerun packages of programming. Our stations compete for access to those programs against in-market broadcast stations for syndicated products and with national cable networks. Public broadcasting stations generally compete with commercial broadcasters for viewers, but not for advertising dollars.

Lastly, our Tribune Broadcasting and WGN America businesses also compete with new distribution technologies for viewers and for content acquisition, including SVOD and OTT outlets.

Major competitors include broadcast owners and operators, namely FOX, ABC, CBS and NBC, as well other major broadcast television station owners, including Gannett, Nexstar, Sinclair and Raycom.

Digital and Data

Gracenote Video and Gracenote Music operate in the metadata and digital entertainment technology industries and compete against other providers of content and data to music and online video services, cable companies, connected devices and consumer electronics manufacturers, as well as those companies with content recognition services that enable the recognition of audio and video data via mobile applications or televisions. Competition tends to be regional, with many competitors offering solutions in only one of the verticals we offer, or even a single competitive product. The industry is highly fragmented by data set, region and service layer. A major competitor for both Gracenote Video and Gracenote Music is Rovi. Other competitors of Gracenote Music include but are not limited to Echonest and Shazam, while Digitalsmiths is also a major competitor for Gracenote Video.

18

Customers and Contracts

No single customer accounted for more than 10% of our consolidated operating revenues in 2014, 2013 or 2012. Our Digital and Data segment has one customer that accounted for approximately 11% of its 2014 revenue.

We are a party to multiple contractual arrangements with several program distributors for their respective programming content. In addition, we have affiliation agreements with our television affiliates, such as FOX, CBS, ABC, NBC and CW.

Intellectual Property

With respect to our Television and Entertainment segment, we do not face major barriers to our operations from patents owned by third parties. However, we view continuous innovation with respect to our technology as being one of our key competitive advantages. Our Television and Entertainment segment maintains a growing patent and patent application portfolio with respect to our technology, owning, as of December 28, 2014, approximately 10 U.S. and foreign issued patents and approximately 60 pending patent applications in the U.S. and foreign jurisdictions. Generally, the duration of issued patents in the U.S. is 20 years from filing of the earliest patent application to which an issued patent clams priority. We also maintain, for our Television and Entertainment segment, federal, international, and state trademark registrations and applications that protect, along with common law rights, our brands, certain of which are long-standing and well known, such as WGN, WPIX, and KTLA. Generally, the duration of a trademark registration is perpetual, if it is renewed on a timely basis and continues to be used properly as a trademark. We also own a large number of copyrights, none of which individually is material to the business. Further, we maintain certain licensing and content sharing relationships with third-party content providers that allow us to produce the particular content mix we provide to our viewers and consumers in our markets and across the country. Other than the foregoing and commercially available software licenses, we do not believe that any of our licenses to third-party intellectual property are material to our business as a whole.

With respect to our Digital and Data segment, Tribune Digital Ventures’ and/or its subsidiaries’ and other companies’, including Gracenote’s, operations have been and continue to be the subject, from time to time, of patent litigation brought by both competitors in the space and non-practicing entities. Given the duration of patents noted above, our ability to defend patent litigation brought by competitors and non-practicing entities is important to our ability to operate, although any current patent infringement dispute is not material to our business as a whole. As part of defending and monetizing its innovation in the space, Tribune Digital Ventures and/or its subsidiaries and other companies, including Gracenote, own, as of December 28, 2014, approximately 100 U.S. and foreign issued patents and approximately 90 pending patent applications in the U.S. and foreign jurisdictions. We also maintain, for our Digital and Data segment, federal, international and state trademark registrations and applications that protect, along with common law rights, our brands, such as GRACENOTE. Given the B2B nature of much of the Digital and Data segment, however, many of the trademark registrations and applications are not material to our business as a whole. We also own a large number of copyrights, none of which individually is material to the business. Further, we maintain certain licensing and content sharing relationships with third-party content providers that allow us to produce the particular content mix we provide to our customers and consumers. Other than the foregoing and commercially available software licenses, we do not believe that any of our licenses to third-party intellectual property are material to our business.

In connection with the Publishing Spin-off, on August 4, 2014, all of the service marks, trademarks and trade names exclusively related to the Publishing Business were transferred to Tribune Publishing and its subsidiaries.

Employees

As of December 28, 2014, we employed approximately 7,600 employees, approximately 1,400 of which were represented by labor unions. Approximately 550 of our employees were employed in international locations. We believe that our relations with our employees are satisfactory.

19

Regulatory Environment

Various aspects of our operations are subject to regulation by governmental authorities in the United States. Our television and radio broadcasting operations are subject to FCC jurisdiction under the Communications Act of 1934, as amended (the “Communications Act”). FCC rules, among other things, govern the term, renewal and transfer of radio and television broadcasting licenses and limit the number and type of media interests in a local market that may be owned by a single person or entity. Our stations must also adhere to various statutory and regulatory provisions that govern, among other things, political and commercial advertising, payola and sponsorship identification, contests and lotteries, television programming and advertising addressed to children, and obscene and indecent broadcasts. The FCC may impose substantial penalties for violation of its regulations, including fines, license revocations, denial of license renewal or renewal of a station’s license for less than the normal term.

Each television and radio station that we own must be licensed by the FCC. Television and radio broadcast station licenses are granted for terms of up to eight years and are subject to renewal by the FCC in the ordinary course. As of February 28, 2015, renewal applications for 11 of those stations were pending. Two additional renewal applications are expected to be filed with the FCC before the end of 2015. We must also obtain FCC approval prior to the acquisition or disposition of a station, the construction of a new station or modification of the technical facilities of an existing station. Interested parties may petition to deny such applications and the FCC may decline to renew or approve the requested authorization in certain circumstances. Although we have generally received such renewals and approvals in the past, there can be no assurance that we will continue to do so in the future.

The FCC’s substantive media ownership rules generally limit or prohibit certain types of multiple or cross ownership arrangements. However, not every interest in a media company is treated as a type of ownership triggering application of the substantive rules. Under the FCC’s “attribution” policies the following relationships and interests generally are cognizable for purposes of the substantive media ownership restrictions: (1) ownership of 5% or more of a media company’s voting stock (except for investment companies, insurance companies and bank trust departments, whose holdings are subject to a 20% voting stock benchmark); (2) officers and directors of a media company and its direct or indirect parent(s); (3) any general partnership or limited liability company manager interest; (4) any limited partnership interest or limited liability company member interest that is not “insulated,” pursuant to FCC-prescribed criteria, from material involvement in the management or operations of the media company; (5) certain same-market time brokerage agreements; (6) certain same-market joint sales agreements; and (7) under the FCC’s “equity/debt plus” standard, otherwise non-attributable equity or debt interests in a media company if the holder’s combined equity and debt interests amount to more than 33% of the “total asset value” of the media company and the holder has certain other interests in the media company or in another media property in the same market.

Under the FCC’s “Local Television Multiple Ownership Rule” (the “Duopoly Rule”), a person may have attributable interests in up to two television stations within the same Nielsen DMA (i) provided certain specified signal contours of the stations do not overlap, (ii) where certain specified signal contours of the stations overlap but, at the time the station combination was created, no more than one of the stations was a top 4-rated station and the market would continue to have at least eight independently-owned full power stations after the station combination is created or (iii) where certain waiver criteria are met. We own duopolies permitted under the “top-4/8 voices” test in the Seattle, Denver, St. Louis, Indianapolis, Oklahoma City and New Orleans DMAs. The Indianapolis duopoly is permitted under the Duopoly Rule because it met the top-4/8 voices test at the time we acquired WTTV(TV)/WTTK(TV) in July 2002. For our other duopoly markets, the FCC granted Duopoly Rule waivers on November 16, 2012, by the FCC’s Memorandum Opinion and order (the “Exit Order”) granting our applications to assign our broadcast and auxiliary station licenses from the debtors-in-possession to our licensee subsidiaries in connection with the FCC’s approval of the Fourth Amended Joint Plan of Reorganization for Tribune Company and its Subsidiaries (subsequently amended and modified, the “Plan”) and in connection with the Local TV Acquisition (the “Local TV Transfer Order”). These Duopoly Rule waivers authorize our ownership of duopolies in the New Haven-Hartford and Fort Smith-Fayetteville DMAs, and full power “satellite” stations in the Denver and Indianapolis DMAs. The Local TV Acquisition was completed on December 27, 2013. On January 22, 2014, Free Press filed an Application for Review seeking review by the full Commission of the Local TV Transfer Order. We filed an Opposition to the Application for Review on February 21, 2014, and Free Press filed a reply on March 6, 2014. The matter is pending.

20

The FCC’s “National Television Multiple Ownership Rule” prohibits a person from having an attributable interest in television stations that, in the aggregate, reach more than 39% of total U.S. television households, subject to a 50% discount of the number of television households attributable to UHF stations (the “UHF Discount”). Our current national reach would exceed the 39% cap on an undiscounted basis. In a pending rulemaking proceeding the FCC has proposed to repeal the UHF Discount but to grandfather existing combinations that exceed the 39% cap. Under the FCC’s proposal, absent a waiver, a grandfathered station group would have to come into compliance with the modified cap upon a sale or transfer of control. If adopted as proposed, the elimination of the UHF Discount would affect our ability to acquire additional television stations (including the Dreamcatcher stations that are the subject of certain option rights held by us).