Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(MARK ONE)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2014

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

COMMISSION FILE NUMBER 0-30961

SOHU.COM INC.

(Exact name of registrant as specified in its charter)

| Delaware | 98-0204667 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

Level 18, Sohu.com Media Plaza

Block 3, No. 2 Kexueyuan South Road, Haidian District

Beijing 100190

People’s Republic of China

(Address of principal executive offices)

(011) 8610-6272-6666

(Registrant’s Telephone Number, Including Area Code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Common Stock, $0.001 Par Value

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of common stock held by non-affiliates of the registrant, based upon the last sale price on June 30, 2014 as reported on the NASDAQ Global Select Market, was approximately $1.36 billion.

As of January 31, 2015, there were 38,517,892 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for Sohu’s 2015 Annual Meeting of Stockholders to be filed on or about April 28, 2015 are incorporated into Part III of this report.

SOHU.COM INC.

Table of Contents

As used in this report, references to “us,” “we,” “our,” “our company,” “our Group,” the “Sohu Group,” the “Group,” and “Sohu.com” are to Sohu.com Inc. and, except where the context requires otherwise, our wholly-owned and majority-owned subsidiaries and variable interest entities (“VIEs”) Sohu.com Limited, Sohu.com (Hong Kong) Limited (“Sohu Hong Kong”), All Honest International Limited (“All Honest”), Sohu.com (Game) Limited (“Sohu Game”), Go2Map Inc., Sohu.com (Search) Limited (“Sohu Search”), Sogou Inc. (“Sogou”), Sogou (BVI) Limited (“Sogou BVI”), Sogou Hong Kong Limited (“Sogou HK”), Vast Creation Advertising Media Services Limited (“Vast Creation”), Fox Video Investment Holding Limited (“Video Investment”), Fox Video Limited (“Sohu Video”), Fox Video (HK) Limited (“Video HK”), Focus Investment Holding Limited, Sohu Focus Limited, Sohu Focus (HK) Limited, Beijing Sohu New Era Information Technology Co., Ltd. (“Sohu Era”), Beijing Sohu Software Technology Co., Ltd., Beijing Sohu Interactive Software Co., Ltd., Go2Map Software (Beijing) Co., Ltd., Beijing Sogou Technology Development Co., Ltd. (“Sogou Technology”), Beijing Sogou Network Technology Co., Ltd (“Sogou Network”), Fox Information Technology (Tianjin) Limited (“Video Tianjin”), Beijing Sohu New Media Information Technology Co., Ltd. (“Sohu Media”), Beijing Focus Time Advertising Media Co., Ltd., Beijing Sohu New Momentum Information Technology Co., Ltd. (“Sohu New Momentum”), Beijing Century High Tech Investment Co., Ltd. (“High Century”), Beijing Heng Da Yi Tong Information Technology Co., Ltd. (“Heng Da Yi Tong”, formerly known as Beijing Sohu Entertainment Culture Media Co., Ltd.), Beijing Sohu Internet Information Service Co., Ltd. (“Sohu Internet”), Beijing GoodFeel Technology Co., Ltd., Beijing Sogou Information Service Co., Ltd. (“Sogou Information”), Beijing 21 East Culture Development Co., Ltd., Beijing Sohu Donglin Advertising Co., Ltd. (“Donglin”), Beijing Pilot New Era Advertising Co., Ltd. (“Pilot New Era”), Beijing Focus Yiju Network Information Technology Co., Ltd., SohuPay Science and Technology Co., Ltd., Beijing Sohu Dianjin Information Technology Co., Ltd., Beijing Yi He Jia Xun Information Technology Co., Ltd., Tianjin Jinhu Culture Development Co., Ltd. (“Tianjin Jinhu”), Guangzhou Qianjun Network Technology Co., Ltd. (“Guangzhou Qianjun”), Shenzhen Shi Ji Guang Su Information Technology Co., Ltd., Beijing Intelligence World Network Technology Co., Ltd., Chongqing Qogir Enterprise Management Consulting Co., Ltd., SendCloud Technology Co., Ltd., Beijing Focus Interactive Information Service Co., Ltd., Beijing Focus Xin Gan Xian Information Technology Co., Ltd., Beijing Focus Real Estate Agency Co., Ltd. and our independently-listed majority-owned subsidiary Changyou.com Limited (“Changyou,” formerly known as TL Age Limited) as well as the following direct and indirect subsidiaries and VIEs of Changyou: Changyou.com HK Limited (“Changyou HK”) formerly known as TL Age Hong Kong Limited), Changyou.com Webgames (HK) Limited (“Changyou HK Webgames”), Changyou.com Gamepower (HK) Limited, ICE Entertainment (HK) Limited (“ICE HK”), Changyou.com Gamestar (HK) Limited, Changyou.com (US) LLC. (formerly known as AmazGame Entertainment (US) Inc.), Changyou.com (UK) Company Limited, ChangyouMy Sdn. Bhd, Changyou.com Korea Limited, Changyou.com India Private Limited, Changyou BİLİŞİM HİZMETLERİ TİCARET LİMİTED ŞİRKETİ, Kylie Enterprises Limited, Mobogarden Enterprises Limited, Heroic Vision Holdings Limited, TalkTalk Limited, RaidCall (HK) Limited, 7Road.com Limited (“7Road”), 7Road.com HK Limited (“7Road HK”), Changyou.com (TH) Limited, Changyou.com Rus Limited, PT.CHANGYOU TECHNOLOGY INDONESIA, Changyou Middle East FZ-LLC, Changyou.com Technology Brazil Desenvolvimento De Programas LTDA, Greative Digital Limited, Glory Loop Limited (“Glory Loop”), MoboTap Inc. (“MoboTap”, a Cayman Islands company), MoboTap Inc. Limited (“MoboTap HK”), MoboTap Inc. (a Delaware corporation), Dolphin Browser Inc., Muse Entertainment Limited, Dstore Technology Limited, Mobo Information Technology Pte. Ltd., Global Cool Limited, Beijing AmazGame Age Internet Technology Co., Ltd. (“AmazGame”), Beijing Changyou Gamespace Software Technology Co., Ltd. (“Gamespace”), ICE Information Technology (Shanghai) Co., Ltd. (“ICE Information”), Beijing Changyou RaidCall Internet Technology Co., Ltd. (“RaidCall”), Beijing Yang Fan Jing He Information Consulting Co., Ltd. (“Yang Fan Jing He”), Shanghai Jingmao Culture Communication Co., Ltd. (“Shanghai Jingmao”), Shanghai Hejin Data Consulting Co., Ltd., Beijing Changyou Jingmao Film & Culture Communication Co., Ltd. (“Beijing Jingmao”), Beijing Gamease Age Digital Technology Co., Ltd. (“Gamease”), Beijing Guanyou Gamespace Digital Technology Co., Ltd. (“Guanyou Gamespace”), Beijing Doyo Internet Technology Co., Ltd., Beijing Zhi Hui You Information Technology Co., Ltd., Shanghai ICE Information Technology Co., Ltd. (“Shanghai ICE”), Shenzhen 7Road Network Technologies Co., Ltd. (“7Road Technology”), Shenzhen 7Road Technology Co., Ltd. (“Shenzhen 7Road”), Beijing Changyou e-pay Co. Ltd., Beijing Changyou Aishouxin Ecological Technology Co., Ltd., Shenzhen Brilliant Imagination Technologies Co., Ltd., Fujian Changyou Heguang Electronic Technology Co., Ltd., Beijing Baina Information Technology Co., Ltd., Baina Zhiyuan (Beijing) Technology Co., Ltd. (“Beijing Baina Technology”), Beijing Anzhuoxing Technology Co., Ltd., Baina Zhiyuan (Chengdu) Technology Co., Ltd., Chengdu Xingyu Technology Co., Ltd., Baina (Wuhan) Information Technology Co., Ltd. (“Wuhan Baina Information”), Wuhan Xingyu Technology Co., Ltd., Wuhan Hualian Chuangke Technology Co., Ltd., Beijing Changyou Ledong Internet Technology Co., Ltd., and Beijing Global Cool Technology Co., Ltd., and these references should be interpreted accordingly. Unless otherwise specified, references to “China” or “PRC” refer to the People’s Republic of China and do not include the Hong Kong Special Administrative Region, the Macau Special Administrative Region or Taiwan. This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, including, without limitation, statements regarding our expectations, beliefs, intentions or future strategies that are signified by the words “expect,” “anticipate,” “intend,” “believe,” or similar language. All forward-looking statements included in this document are based on information available to us on the date hereof, and we assume no obligation to update any such forward-looking statements. Our business and financial performance are subject to substantial risks and uncertainties. Actual results could differ materially from those projected in the forward-looking statements. In evaluating our business, you should carefully consider the information set forth under the heading “Risk Factors.” Readers are cautioned not to place undue reliance on these forward-looking statements.

1

| ITEM 1. | BUSINESS |

OUR COMPANY

Sohu.com Inc. (NASDAQ: SOHU), a Delaware corporation organized in 1996, is a leading Chinese online media, search and game service group providing comprehensive online products and services on PCs and mobile devices in the People’s Republic of China (the “PRC” or “China”). Our businesses are conducted by Sohu.com Inc. and its subsidiaries and VIEs (collectively referred to as the “Sohu Group”). The Sohu Group consists of Sohu, which when referred to in this report, unless the context requires otherwise, excludes the businesses and the corresponding subsidiaries and VIEs of Sogou Inc. (“Sogou”) and Changyou.com Limited (“Changyou”), Sogou and Changyou. Sogou and Changyou are indirect controlled subsidiaries of Sohu.com Inc. Sohu is a leading Chinese language online media content and services provider. Sogou is a leading online search, client software and mobile Internet product provider in China. Changyou is a leading online game developer and operator in China as measured by the popularity of its MMOG TLBB and its mobile game TLBB 3D, and engages primarily in the development, operation and licensing of online games for PCs and mobile devices. Most of our operations are conducted through our indirect wholly-owned and majority-owned china-based subsidiaries and variable interest entities (“VIEs”).

In August 1996, we were incorporated in Delaware as Internet Technologies China Incorporated, and in January 1997 we launched our original Website, itc.com.cn. In February 1998, we re-launched our Website under the domain name Sohu.com and, in September 1999, we renamed our company Sohu.com Inc. On July 17, 2000, we completed our initial public offering on NASDAQ.

OUR BUSINESS

Through the operation of Sohu, Sogou and Changyou, we generate online advertising revenues (including brand advertising revenues and search and Web directory revenues), online games revenues and others revenues. Online advertising and online games are our core businesses. In the year ended December 31, 2014, total revenues generated by Sohu, Sogou and Changyou were approximately $1.67 billion, including:

Sohu:

| - | $482.2 million in brand advertising revenues, of which $197.6 million was from Sohu Media Portal, $175.8 million was from Sohu Video, and $108.8 million was from Focus; and |

| - | $49.8 million in others revenues, mainly attributable to Sohu’s offering of mobile-related services and mobile products. |

Total revenues generated by Sohu were $532.0 million.

Sogou:

| - | $357.8 million in search and Web directory revenues (formerly referred to as “search and others” revenues); and |

| - | $28.6 million in others revenues attributable to Sogou’s offering of Internet value-added services (or “IVAS”) with respect to the operation of Web games and services provided to users. |

Total revenues generated by Sogou were $386.4 million.

Changyou:

| - | $652.0 million in online game revenues; |

| - | $59.0 million in brand advertising revenues, mainly attributable to Changyou’s 17173.com Website; and |

| - | $43.7 million in others revenues attributable to Changyou’s operation of the platform channel business, including the wan.com Website, RaidCall, the Dolphin Browser and other software applications; and Changyou’s cinema advertising revenues. |

Total revenues generated by Changyou were $754.7 million.

For the year ended December 31, 2014 our total brand advertising revenues were $541.2 million, total search and Web directory revenues were $357.8 million, total online game revenues were $652.0 million, and total others revenues were $122.1 million.

2

Sohu’s Business

Brand Advertising Business

Sohu’s main business is the brand advertising business, which offers to users, over our matrices of Chinese language online media, various content, products and services across multiple Internet-enabled devices, such as PCs, mobile phones and tablets. The majority of our products and services are provided through Sohu Media Portal, Sohu Video and Focus.

| • | Sohu Media Portal. Sohu Media Portal provides our users comprehensive online content, including news, entertainment, sports, automobile, business and finance, through www.sohu.com for PCs, the mobile portal m.sohu.com and the mobile phone application Sohu News APP; |

| • | Sohu Video. Sohu Video is a leading online video service provider in China through tv.sohu.com for PCs and the mobile phone application Sohu Video APP; and |

| • | Focus. Focus (www.focus.cn) is a leading online real estate information provider in China. |

Revenues generated by the brand advertising business are classified as brand advertising revenues in the Sohu Group’s consolidated statements of comprehensive income.

Others Business

Sohu also engages in the others business, which includes mobile-related services and mobile products offered in cooperation with China mobile network operators to mobile phone users and to China mobile network operators. Revenues generated by Sohu from the others business are classified as others revenues in the Sohu Group’s consolidated statements of comprehensive income.

Sogou’s Business

Search and Web Directory Business

The search and Web directory business primarily offers advertisers pay-for-click services, as well as online marketing services on Web directories operated by Sogou. Pay-for-click services enable advertisers’ promotional links to be displayed on the Sogou search result pages and Sogou Website Alliance members’ Websites where the links are relevant to the subject and content of such Web pages. Both pay-for-click services and online marketing services on Web directories operated by Sogou expand distribution of our advertisers’ Website links and advertisements by leveraging traffic on Sogou Website Alliance members’ Websites. Our search and Web directory business benefits significantly from our collaboration with Tencent Holdings Limited (together with its subsidiaries, “Tencent”), which provides us access to traffic generated from users of products and services provided by Tencent.

Revenues generated by the search and Web directory business are classified as search and Web directory revenues in the Sohu Group’s consolidated statements of comprehensive income.

Others Business

Sogou also engages in the others business by offering IVAS with respect to the operation of Web games developed by third parties and other services. Revenues generated by Sogou from the others business are classified as others revenues in the Sohu Group’s consolidated statements of comprehensive income.

Changyou’s Business

Changyou has three businesses, consisting of the online game business, the platform channel business and the others business.

Online Game Business

Changyou’s online game business offers to game players MMOGs, which are interactive online games that may be played simultaneously by hundreds of thousands of game players; mobile games, which are played on mobile devices with an Internet connection; and Web games, which are online games played over the Internet using a Web browser. All of Changyou’s games are operated under the item-based revenue model, where game players play the games for free but can purchase virtual items to enhance the game-playing experience. Revenues derived from the operation of online games are classified as online game revenues in our consolidated statements of comprehensive income.

3

Platform Channel Business

Changyou also owns and operates a number of Web properties and software applications for PCs and mobile devices (collectively referred to as “platform channels”), including the 17173.com Website, one of the leading information portals for game players in China; the wan.com Website, a games portal that provides to game players a collection of Web games of third-party developers; RaidCall, which provides online music and entertainment services, primarily in Taiwan; and the Dolphin Browser, a gateway to a host of user activities on mobile devices, with the majority of its users based in Europe, Russia and Japan. Changyou’s platform channels serve various needs of its users and help Changyou reach more user communities and conduct cross-promotions of its games and services. Revenues generated by 17173.com Website are classified as brand advertising revenues, and revenues generated by the wan.com Website, RaidCall and the Dolphin Browser are classified as others revenues in our consolidated statements of comprehensive income.

Others Business

Changyou also operates a cinema advertising business, which consists of Changyou offering slots for advertisements to be shown in cinemas before the screening of movies. Revenues generated by Changyou’s cinema advertising business are classified as others revenues in our consolidated statements of comprehensive income.

Business Transactions

Sogou Transactions

On October 22, 2010, Sogou issued and sold 24.0 million, 14.4 million and 38.4 million, respectively, of its newly-issued Series A Preferred Shares to Alibaba Investment Limited, a subsidiary of Alibaba Group Holding Limited (“Alibaba”); China Web Search (HK) Limited (“China Web”); and Photon Group Limited, the investment vehicle of the Sohu Group’s Chairman and Chief Executive Officer Dr. Charles Zhang (“Photon”), for $15 million, $9 million, and $24 million, respectively. On June 29, 2012, Sohu purchased Alibaba’s 24.0 million Sogou Series A Preferred Shares for a purchase price of $25.8 million.

On September 16, 2013, Sogou entered into a series of agreements with Tencent, Sohu Search and Photon pursuant to which Sogou issued Series B Preferred Shares and Class B Ordinary Shares to Tencent for a net amount of $448 million in cash and Tencent transferred its Soso search-related businesses and certain other assets to Sogou (collectively, the “Sogou-Tencent Transactions”). Also on that date, Sogou entered into Repurchase Option Agreements with Sohu Search and Photon, and a Repurchase/Put Option Agreement with China Web, with respect to all of the Series A Preferred Shares of Sogou held by Sohu Search and China Web, and a portion of the Series A Preferred Shares of Sogou held by Photon. Also on that date, Sogou, Sohu Search, Photon, Mr. Xiaochuan Wang, four other members of Sogou’s management (collectively, the “Sohu Parties”) and Tencent entered into a Shareholders Agreement (the “Shareholders Agreement”) under which the parties agreed to vote their Sogou voting shares in all elections of directors to elect three designees of Sohu Search and two designees of Tencent.

On September 17, 2013, Sogou paid a special dividend to the three holders of Series A Preferred Shares of Sogou in the aggregate amount of $300.9 million, of which Sohu Search received $161.2 million, Photon received $43.0 million, and China Web received $96.7 million.

On December 2, 2013, Tencent invested $1.5 million in cash in Sogou Information, which is a VIE of Sogou, as additional consideration in connection with the Sogou-Tencent Transactions, in return for a 45% equity interest in Sogou Information. Through a share pledge agreement and an exclusive equity interest purchase right agreement between Tencent and Sogou Technology, and similar agreements between the other two shareholders of Sogou Information, Sogou Technology controls all shareholder voting rights in Sogou Information, has the power to direct the activities of Sogou Information, and is the primary beneficiary of Sogou Information, and Tencent and the other two shareholders of Sogou Information act as Sohu Technology’s nominees.

On March 24, 2014, Sogou purchased from China Web, pursuant to the Repurchase/Put Option Agreement between Sogou and China Web, 14.4 million Series A Preferred Shares of Sogou, for an aggregate purchase price of $47.3 million.

In June 2014, Sogou repurchased approximately 4.2 million of its Class A Ordinary Shares from noncontrolling shareholders, a majority of whom were our employees, for an aggregate purchase price of $41.6 million.

Pursuant to the Shareholders Agreement, Sohu will hold approximately 52% of the total voting power and control the election of the Board of Directors of Sogou, assuming that the remaining repurchase options are exercised, Tencent’s non-voting Class B Ordinary Shares are converted to voting shares, and all share options under the Sogou 2010 Share Incentive Plan and all share options under an arrangement providing for Sogou share-based awards to be available for grants to Sohu management and key employees are granted and exercised. As Sohu is the controlling shareholder of Sogou, we consolidate Sogou in the Sohu Group’s consolidated financial statements, and recognize noncontrolling interest reflecting economic interests in Sogou held by shareholders other than Sohu.

4

Acquisition of RaidCall

On November 19, 2013, Changyou entered into an investment agreement with Beijing Kunlun Tech Co., Ltd. and certain of its affiliates (collectively, the “Kalends Group”), pursuant to which TalkTalk Limited (“TalkTalk”) was incorporated in the British Virgin Islands and initially wholly-owned by the Kalends Group, RaidCall (HK) Limited (“RaidCall HK”) was incorporated in Hong Kong as a wholly-owned subsidiary of TalkTalk, and Beijing Changyou RaidCall Internet Technology Co., Ltd.(“Changyou RaidCall”) was incorporated in the PRC as a wholly-owned subsidiary of RaidCall HK. The Kalends Group then transferred to RaidCall HK and Changyou RaidCall all of the assets associated with RaidCall. On December 24, 2013, pursuant to the investment agreement, Changyou acquired 62.5% of the equity interests, on a fully-diluted basis, in TalkTalk for cash consideration of $47.6 million. Of the total consideration, $27.6 million was paid to purchase from the Kalends Group a portion of the ordinary shares of TalkTalk held by the Kalends Group, and $20 million was injected for newly-issued ordinary shares of TalkTalk. Also effective upon the closing of the transaction, 15% of the equity interests of TalkTalk on a fully-diluted basis were reserved for grants of equity incentive awards to key employees associated with RaidCall, and the Kalends Group continued to hold the remaining 22.5% of the equity interests on a fully-diluted basis.

Acquisition of MoboTap

On July 16, 2014, Changyou, through a wholly-owned subsidiary, entered into an investment agreement with MoboTap, which is the mobile technology developer behind the Dolphin Browser, MoboTap’s subsidiaries and variable interest entities, and MoboTap’s shareholders pursuant to which Changyou agreed to purchase from existing shareholders of MoboTap shares of MoboTap representing 51% of the equity interests in MoboTap on a fully-diluted basis for approximately $90.8 million in cash.

On July 31, 2014, pursuant to the investment agreement, Changyou, MoboTap and the noncontrolling shareholders of MoboTap entered into a shareholder agreement pursuant to which Changyou has the right to designate three of the five directors of MoboTap, including the chairman of the board; Changyou’s approval will be required for any proposed transfers of equity interests in MoboTap held by the noncontrolling shareholders; and Changyou will be entitled to customary pre-emptive rights with respect to any new issuance of equity interests in MoboTap. Changyou has the right to purchase up to 10% of the equity interests in MoboTap from the noncontrolling shareholders, at a price of 20% below the initial public offering (“IPO”) price, before a qualified IPO of MoboTap. If MoboTap achieves specified performance milestones for 2016 and certain specified key employees continue their employment with MoboTap at the time the milestones are achieved, but there has not been an IPO by MoboTap, the noncontrolling shareholders of MoboTap will have a one-time right to put to Changyou shares of MoboTap held by them, representing up to 15% of the equity interests in MoboTap, for an aggregate price of up to $53 million.

PRODUCTS AND SERVICES

Sohu’s Business

Brand Advertising Business

Sohu’s main business is the brand advertising business, which offers to users, over Sohu’s matrices of Chinese language online media, various content, products and services across multiple Internet-enabled devices, such as PCs, mobile phones and tablets. The brand advertising business also offers advertisements on our Web properties to companies seeking to increase their brand awareness online.

Sources

The majority of Sohu’s products and services are provided through Sohu Media Portal, Sohu Video and Focus.

Sohu Media Portal

Sohu Media Portal provides our users comprehensive online content, including news, entertainment, sports, automobile, business and finance etc, through www.sohu.com on PCs, mobile portal m.sohu.com and mobile phone application Sohu News APP.

| • | Sohu News provides syndicated, partner and original news via texts, photos, and videos to engage users with wide-ranging, up-to-the-minute coverage and analysis of topical news events. |

| • | Sohu Entertainment contains extensive coverage of entertainment areas that are of interest to Chinese users. |

| • | Sohu Sports offers multimedia news and information on a wide range of sporting events, and broadcasts live and recorded domestic and international sports matches. |

| • | Sohu Auto provides a comprehensive database of car models. It also provides industry news and auto reviews. In addition, it offers automobile pricing and dealership information for certain local auto markets. |

| • | Sohu Business and Finance provides business and financial news coverage, financial product information, and real-time stock quotes from major stock exchanges. |

5

Sohu Video

Sohu Video is a leading online video service provider in China. We deliver licensed professionally-produced video content, original in-house produced video content, and user-generated content. We provide users free access to most of our extensive and comprehensive video content library, which includes popular domestic and overseas television dramas, movies, variety shows, in-house produced shows and programs, news, documentaries, animations, entertainment-related content, live television Webcasts, and user-generated content. We also offer selected fee-based video content, including movies and educational video content. Users can also access our video content via PCs through tv.sohu.com, or via mobile devices by visiting our mobile video site or installing Sohu Video App, our mobile video application.

Focus

Focus (www.focus.cn) is a leading online real estate information provider in China. With diversified online content of new homes, resale properties and home furnishing services, Focus provides comprehensive information and solutions for house seekers, homeowners and buyers of home furnishing services.

Business Model

In the brand advertising business, we enjoy a strong competitive position as one of the leading Internet companies in China. Through the platforms described above, we have built a sizeable user base through good user experiences provided by our products and services. This user base is appealing to advertisers. Through PCs and mobile devices, we provide advertisement placements to advertisers on our different Websites and in different formats, including banners, links, logos, buttons, full screen, pre-roll, mid-roll, post-roll video screens, and pause video screens, as well as loading page ads and news feed ads. We charge advertisers either on a time basis with fixed fees (the “Fixed Price model”) or on the Cost Per Impression model (“CPM”). For our real estate business operated by Focus, we apply the e-commerce model. For revenues under the Fixed Price model or the CPM model, our standard advertising charges vary depending on a number of factors, including the advertisement’s location within our Website, the content and the geographical location where the advertisement is displayed or broadcasted, and the devices that users employ. Discounts from standard rates are typically provided for higher-volume, longer-term advertising contracts, and may be provided for promotional purposes. Under the e-commerce model, Focus sells membership cards which allow potential home buyers to purchase specified properties from real estate developers at a discount greater than the price that Focus charges for the card. Membership fees are refundable until the potential home buyer uses the discounts to purchase properties. Focus recognizes such revenues upon obtaining confirmation that the membership card has been redeemed to purchase a property. Revenues generated under the e-commerce model are included in our brand advertising revenues.

We rely on both direct sales by our internal sales force and sales by advertising agents for advertising on our Websites. Our advertisers include multinational companies that have significant operations in Chinese markets, many of which are Fortune 500 companies, as well as numerous Chinese domestic companies. We continue focusing on multinational and Chinese domestic companies as our key advertisers.

Others Business

Sohu also engages in the others business, which includes mobile-related services and mobile products offered in cooperation with China mobile network operators to mobile phone users and to China mobile network operators.

Sogou’s Business

Search and Web Directory Business

Products and Services for Users

Sogou’s main business is the search and Web directory business. Sogou is a leading online search, client software and mobile Internet product provider in China. Sogou offers extensive products and services, including Sogou Input Method, Sogou Browser, Sogou Web Directory and Sogou Search to China’s online users.

6

Sogou Input Method

Sogou Input Method is in-house developed software to input Chinese characters on PCs and mobile devices. It is among the most popular Internet products in China and has a dominant market share. Sogou Input Method uses search engine technology to capture and generate vocabularies and language models and can present the latest trends in words used by Internet users. In December 2014, Sogou Input Method’s monthly active users on PCs reached 453 million, with a penetration rate of 85% in China, according to iResearch. Sogou Mobile Keyboard, the mobile version of Sogou Input Method, provides, in addition to character input, tailored features for smart phones, such as multimedia (audio and image) input, voice recognition, handwriting recognition, and vocabulary sync between mobile devices and PCs. Since September of 2014, Sogou Mobile Keyboard has been available in the App Store and became one of the most downloaded applications after Apple’s iOS system began to support third-party keyboards. In December 2014, Sogou Mobile Keyboard had approximately 210 million monthly active users.

Sogou Browser

Sogou Browser is our self-developed browser for both PCs and mobile devices that is designed with technologies to make the Web-navigation faster, safer, and easier. Sogou Browser for PCs has an originated dual-core network-layer system and a seven-stage acceleration mechanism, which can accelerate browsing speed and substantially enhance the experience of a user accessing the Internet. We also provide users with a mobile version of Sogou Browser. Our mobile browser has mobile-specific features, including file transfer from PC to mobile and smart detection of downloadable resources within the Webpage.

Sogou Web Directory

Sogou Web Directory is a popular Chinese Web directory navigation site for PCs which serves as a key access point to popular and preferred Websites.

Sogou Search

Sogou Search, which means “Search Dog,” is Sogou’s proprietary search engine and is conducted through Sogou.com. It performs interactive searches of billions of Web pages using advanced algorithms. Upon a search query, the user is taken through a fast and convenient interactive process to reach the most relevant selection of integrated Website and page search results through PCs and mobile devices. Sogou Search provides users with high updating speeds, short response times and accurate search results, based on a large database capacity of retrieved pages. We also provide mobile-specific search applications to mobile device users through Sogou Search App, a dedicated search application we rolled out in 2014. Sogou Search App embeds voice-activated search, intuitive display of search results and personalized features to retrieve search records so that it offers a productive and optimized mobile search experience. Under its agreements with Tencent, Sogou Search cooperates with Tencent in multiple respects. Sogou provides a full range of search services for the vast number of users of Tencent’s products and services on PCs and mobile devices. In addition, in 2014, Sogou launched a unique Weixin search function for both PCs and mobile devices, that allows users to search the enormous amount of content that is published on Weixin’s accounts.

Products and Services for Advertisers

Pay-for-click Services

Pay-for-click services are services that enable our advertisers’ promotional links to be displayed on Sogou’s search result pages and Sogou Website Alliance members’ Websites where the links are relevant to the subject and content of such Web pages. We introduce Internet users to our advertisers through our auction-based pay-for-click systems and charge advertisers on a per-click basis when the users click on the displayed links.

Online Marketing Services on Web Directories Operated by Sogou

Online marketing services mainly consist of displaying advertisers’ Website links on the Web pages of Web directories operated by Sogou. Sogou charges most of its advertisers based on the duration of the display of their Website links on the Web pages.

Sogou Website Alliance

Both pay-for-click services and online marketing services on Web directories operated by Sogou expand distribution of our advertisers’ Website links or advertisements by leveraging traffic on Sogou Website Alliance members’ Websites. Payments made to Sogou Website Alliance members are included in cost of search and Web directory revenues as traffic acquisition costs. We pay Sogou Website Alliance members based on either revenue-sharing arrangements, under which we pay a percentage of pay-for-click revenues generated from clicks by users of their properties, or a pre-agreed unit price.

7

Others

Sogou also engages in the others business by offering IVAS with respect to the operation of Web games developed by third parties and other services.

Changyou’s Business

Online Game Business

Changyou engages in the development, operation and licensing of online games for PCs and mobile devices, and is a leading online game developer and operator in China. Changyou’s online games include MMOGs, which are interactive online games that may be played simultaneously by hundreds of thousands of game players; mobile games, which are played on mobile devices and require an Internet connection; and Web games, which are played over the Internet using a Web browser.

Business Model

Changyou’s online games are operated under the item-based revenue model, meaning game players can play Changyou’s games for free, but may choose to pay for virtual items, which are non-physical items that game players can purchase and use within a game, such as gems, pets, fashion items, magic medicine, riding animals, hierograms, skill books and fireworks. Through virtual items, players are able to enhance or personalize their game environments or game characters, accelerate their progress in Changyou’s games and share and trade with friends.

For players who choose to purchase virtual goods, Changyou delivers enhanced gameplay experiences and benefits, such as:

Accelerated Progress. Many of Changyou’s games offer players the option to purchase items that can accelerate their progress in the game and increase their capabilities, so that they level up more quickly and compete more effectively against others in the game. While Changyou sells many items that accelerate progress in our games, Changyou monitors and carefully balances the disparity in capabilities between paying and non-paying game players to avoid discouraging non-paying game players and to keep the game challenging and interesting for paying game players.

Enhanced Social Interaction. Changyou uses a variety of virtual items to promote interaction and to facilitate relationship-building among game players in its games.

Personalized and Customized Appearance. Many of Changyou’s games offer players the option to purchase decorative and functional items to customize the appearance of their characters, pets, vehicles, houses and other in-game possessions to express their individuality.

Gifts. Many of Changyou’s games offer players the option to purchase gift items to send to their friends. Examples of gift items include decorative items and time-limited items for special holiday events and festivals, such as Valentine’s Day, Spring Festival (Chinese New Year) and Christmas.

Changyou’s online games include games that it self-operates and games that it licenses out to third-party operators.

Self-Operated Games

For self-operated games, Changyou determines the price of virtual items based on the demand or expected demand for such virtual items. Changyou may change the pricing of certain virtual items based on their consumption patterns. Changyou hosts the games on its own servers and is responsible for the sales and marketing of the games as well as customer service. Changyou’s self-operated games include MMOGs, mobile games and Web games developed in house and MMOGs and mobile games that Changyou licensed from or jointly developed with third-party developers.

For self-operated MMOGs, Changyou collects proceeds from players and third-party game card distributors through sale of its game points on its online payment platform and prepaid game cards. For self-operated mobile games, Changyou sells game points to its game players via third-party mobile app stores. The mobile app stores in turn pay Changyou proceeds after deducting their share of pre-agreed revenue-sharing amounts. For self-operated Web games, Changyou collects proceeds from players through sale of its game points on its online payment platform. For self-operated games that are licensed from or jointly developed with third-party developers, Changyou pays the developers license fees for the exclusive right to operate the games domestically or globally, as well as revenue-sharing payments over the duration of the licenses.

8

Licensed Out Games

Changyou also authorizes third-parties to operate its online games. Licensed-out games include MMOGs, mobile games and Web games developed in house and mobile games jointly developed with third-party developers. For licensed -out games, the licensee operators pay Changyou license fees, as well as revenue-sharing payments over the duration of the licenses.

Online Games in Operation

MMOGs — TLBB

TLBB is Changyou’s flagship MMOG. TLBB is a popular martial arts MMOG in China that is adapted from the popular Chinese martial arts novel “Tian Long Ba Bu,” which means “Novel of Eight Demigods,” written by the famous writer Louis Cha. TLBB features a combination of martial arts-style-fighting and community-building among its game players with a variety of interesting and interactive gameplay. Players can join a clan, make friends within it, and engage in other interactive events with their friends. In addition, TLBB features new cross-server gameplay designed for clans. With different levels of cross-server games, all levels of players can play with opponents at comparable levels. Since TLBB’s launch in May 2007, we have regularly developed new content and released game updates in the form of expansion packs for the game. TLBB has won various awards in China, including the 2008 “Best Self-Developed Online Games (First Place)” and the 2008 and 2009 “Most Liked Online Games by Game Players (First Place)” awards at the China Digital Entertainment Expo and Conference, or ChinaJoy. Its expansion packs, TLBB2, TLBB3 and New TLBB, won the 2010 “Most Liked Online Games by Game Players” award, the 2011 “Best Self-Developed Online Games” award, and the 2013 “Most Liked Online Games by Game Players” award, respectively, at ChinaJoy. TLBB was chosen as one of the 2012 “Most Liked Online Games by Game Players” at ChinaJoy.

For 2014, revenues from TLBB were $411.9 million, accounting for approximately 63% of Changyou’s online game revenues, approximately 55% of Changyou’s total revenues and 25% of the Sohu Group’s total revenues.

Mobile game — Tian Long Ba Bu 3D (“TLBB 3D”)

TLBB 3D is an in-house developed mobile 3D martial arts MMO role-playing game. Adapted from Louis Cha’s novel of the same name, the game re-enacts the story of the original novel and blends in some of the elements of the PC version of the game, including its gameplay, social elements, and multiple gaming systems, enabling players to enjoy exciting battles and interesting real-time interaction with other players. Changyou launched this game in October 2014.

Web games — Wartune and DDTank

Wartune is a 2.5D role-playing and quasi real-time strategy Web game launched in December 2011 in China. Wartune is set in a mythical western universe where players build their own kingdoms in a virtual world where they must fight against a demonic race by developing their own villages and armies. Wartune has been launched in 18 different language versions.

DDTank is a 2D multi-player, combat and role-playing Web game in which players control avatars to compete with other game players. Avatars can earn or buy various weapons, potions, magic rings, rockets and other items to increase competitiveness and enhance the game experience. DDTank has been launched in 13 different language versions.

Online Games in Pipeline

Changyou has several MMOGs and mobile games in its pipeline with different graphic styles, themes and features to appeal to different segments of the online game player community. Games in Changyou’s pipeline include, among others:

| • | MMOGs — an in-house developed MMOG, Steel Ocean; |

| • | Mobile games — an in-house developed mobile game, Dash fire, and two jointly developed mobile games, Xuan Yuan Jian and Twins of Brothers. |

Platform Channel Business

Changyou also owns and operates a number of Web properties and software applications for PCs and mobile devices (collectively referred to as “platform channels”), including the 17173.com Website, one of the leading information portals for game players in China; the wan.com Website, a games portal that provides to game players a collection of Web games of third-party developers; RaidCall, which provides online music and entertainment services, primarily in Taiwan; and the Dolphin Browser, a gateway to a host of user activities on mobile devices, with the majority of its users based in Europe, Russia and Japan. Changyou’s platform channels serve various needs of its users and help Changyou reach more user communities and conduct cross-promotions of its games and services.

9

Others Business

Changyou also operates a cinema advertising business, which consists of Changyou offering slots for advertisements to be shown in cinemas before the screening of movies.

COMPETITION

The Internet and Internet-related markets in China are rapidly evolving. There are many companies in the domestic and international markets that distribute online content, online games, and value-added telecommunications services targeting Chinese users. We now are facing more intense competition from both domestic and international competitors for providing content and services over the Internet.

We believe the rapid increase in China’s online population will draw more attention to the PRC Internet market from both domestic and multinational competitors. Our existing competitors may in the future achieve greater market acceptance and gain additional market share. It is also possible that new competitors may emerge and acquire significant market share. In addition, our competitors may leverage their existing Internet platforms to cross-sell newly launched products and services. It is also possible that, as a result of deficiencies in legal protections afforded intellectual property in the Internet industry in China, or inadequate enforcement of existing PRC laws protecting such intellectual property, we may not be able to prevent existing or new competitors from accessing and using our in-house developed Web content or technologies.

In recent years there have emerged three large conglomerates, Tencent, Alibaba and Baidu, Inc. (“Baidu”), that have a wide reach in the Internet industry in China, and between them tend to dominate key aspects of the industry through their own operations or through strategic investments in other companies. Each of these companies is in a position to compete very effectively against us. For example, Alibaba alone competes with us in almost every key aspect of our business, competing with us in media through its investment in Sina Corporation (“Sina”), in online video through its investment in Youku Tudou Inc. (“Youku Tudou”), and in online search through its investment in UCWeb Inc. (“UCWeb).

Sohu’s Business

In the PRC Internet space, competition for brand advertising business is intense and is expected to increase significantly in the future. We compete with our peers and competitors in China primarily on the following basis:

| • | access to financial resources; |

| • | gateway to host of Internet users activities; |

| • | technological advancements; |

| • | attractiveness of products; |

| • | brand recognition; |

| • | volume of traffic and users; |

| • | quality of Websites and content; |

| • | quality and quantity of professionally-made and licensed video content; |

| • | strategic relationships; |

| • | quality of services; |

| • | effectiveness of sales and marketing efforts; |

| • | talent of staff; and |

| • | pricing. |

Over time, our competitors may gradually build certain competitive advantages over us in terms of:

| • | greater brand recognition among Internet users and clients; |

| • | better products and services; |

| • | larger user and advertiser bases; |

10

| • | more extensive and well developed marketing and sales networks; and |

| • | substantially greater financial and technical resources. |

There are a number of existing or new PRC Internet companies, including those controlled or sponsored by private entities and by PRC government entities. As an Internet portal, we compete with various portals, including Tencent, Sina, NetEase.com, Inc. (“NetEase”), and Phoenix New Media Limited (“Phoenix”), and vertical sites, such as Autohome Inc.(“Autohome”), Bitauto Holdings Limited (“BitAuto”), Youku Tudou”, Beijing Xin Lian Xin De Advertising Media Co., Ltd. (“iQIYI”), SouFun Holdings Limited (“SouFun”), Leju Holdings Limited (“Leju”), and YY Inc. (“YY”).

We also compete with traditional forms of media, such as newspapers, magazines, radio and television, for advertisers, advertising revenues and content. Some of these traditional media, such as CCTV, Xinhua News Agency and People’s Daily, have extended their businesses into the Internet market. As a result, we expect to face more intense competition with traditional media companies in both their traditional media and in the Internet-related markets.

Sogou’s Business

Our search and Web directory business mainly consists of pay-for-click services, as well as online marketing services on the Web directories operated by Sogou. Pay-for-click services face intense competition from other search engines, powered by Baidu, Inc. (“Baidu”), Qihoo 360 Technology Co., Ltd. (“Qihoo”), UCWeb, Google Inc. (“Google”), and Microsoft. Online marketing services on Web directories operated by Sogou also face intense competition from other Chinese Web directories, such as the 360 Personal Start-up Page of Qihoo, Hao123.com of Baidu, 2345.com of Shanghai Ruichuang Internet Technology Development Co., Ltd. and duba.com of Cheetah Mobile Inc. (“Cheetah”).

Moreover, we compete with other technology-driven companies on developing and promoting client-end software and mobile Internet products. For example, we launched our self-developed Sogou Input Method and Sogou Browser on both PCs and mobile devices in 2006, and have provided regular upgrades since then. However, many companies, such as Baidu, Google, Tencent, Qihoo, Microsoft, Maxthon International Limited, Mozilla Corporation and Cheetah have presented their own input methods or browsers that compete with us.

Our existing and potential competitors compete with us for users and advertisers on the basis of the quality and quantity of search results, the features, availability and ease of use of products and services, and the number of marketing and distribution channels. They also compete with us for talent with technological expertise, which is critical to the sustained development of our products and services. We also face competition from traditional forms of media.

Changyou’s Business

Online Game Business

In the online games industry, we compete principally with the following three groups of competitors in China:

| • | online game developers and operators in China, including Tencent, NetEase, Shanda Games Limited (“Shanda”), Perfect World Co., Ltd. (“Perfect World”), Giant Interactive Group Inc. (“Giant”), Kalends Inc., iDreamsky Technology Ltd. NetDragon Websoft Inc. (“NetDragon”), Kingsoft Corporation Limited (“Kingsoft”), and various mobile game developers and operators who recently entered into this emerging market; |

| • | other private companies in China devoted to game development or operation, many of which are backed by venture capital; and |

| • | international competitors. |

Our existing and potential competitors in the online games industry compete with us for talent, game player spending, time spent on game playing, marketing activities, quality of games, and distribution network.

Platform Channel Business

In the platform channel business, we primarily compete with PRC-based and international Internet companies that build Internet platforms to offer online advertising and value-added services similar to those that we offer.

11

Changyou’s game information portal operated through the 17173.com Website currently competes in China with, among others, the following game information portals:

| • | Duowan.com, operated by YY; and |

| • | game.qq.com, operated by Tencent. |

Our existing and potential competitors in the online advertising industry compete with us for talent, advertiser spending, number of unique visitors, number of page views, visitors’ time spent on Website, and quality of service.

For Changyou’s other platform products, such as the Dolphin Browser, Changyou generally competes with other PC and mobile application developers, including developers who promote their products as offering similar functions to those offered by Changyou’s products. In addition, Changyou competes with all major Internet companies for users.

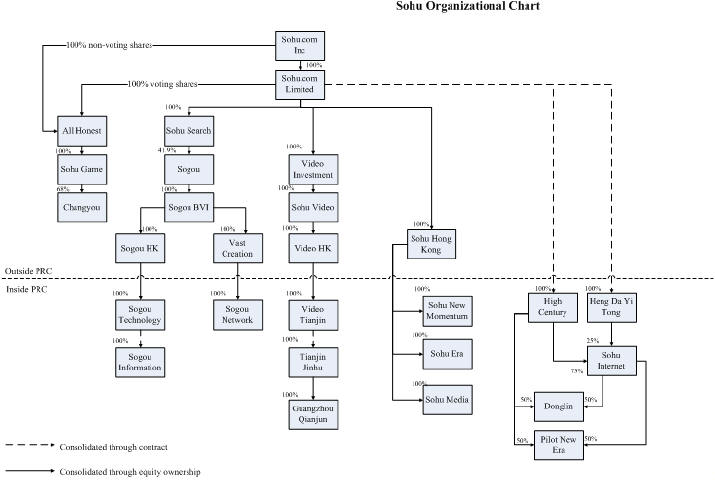

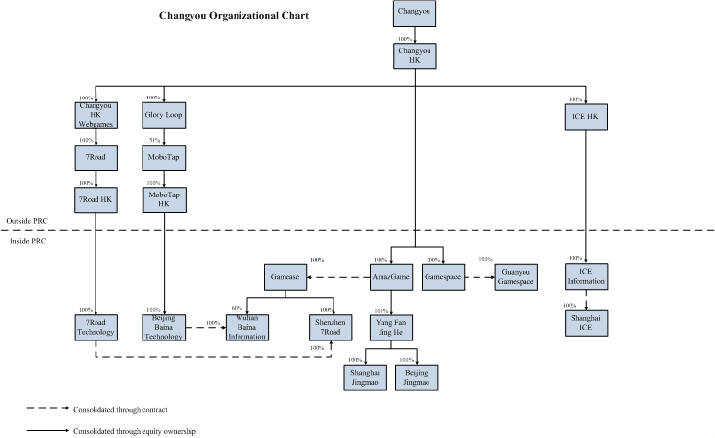

OUR CORPORATE STRUCTURE

The charts below present the principal consolidated entities of Sohu.com Inc. not including our consolidated Changyou entities, and our principal consolidated Changyou entities.

12

Principal Subsidiaries

The following are our China-based principal direct or indirect operating subsidiaries, all of which were established as wholly foreign-owned enterprises (or “WFOEs”) under PRC law (collectively the “China-Based Subsidiaries,” or the “PRC Subsidiaries”):

For Sohu’s Business

| • | Sohu Era, established in 2003 as a WFOE of Sohu Hong Kong; |

| • | Sohu Media, established in 2006 as a WFOE of Sohu Hong Kong; |

| • | Sohu New Momentum, established in 2010 as a WFOE of Sohu Hong Kong; and |

| • | Video Tianjin, established in 2011 as a WFOE of Video HK. |

For Sogou’s Business

| • | Sogou Technology, established in 2006 as a WFOE of Sogou HK; and |

| • | Sogou Network, established in 2012 as a WFOE of Vast Creation. |

For Changyou’s Business

| • | AmazGame, established in 2007 as a WFOE of Changyou HK; |

| • | Gamespace, established in 2009 as a WFOE of Changyou HK; |

| • | ICE Information, acquired in 2010 as a WFOE as a result of the acquisition of ICE Entertainment (HK) Limited; |

| • | Yang Fan Jing He, established in 2010 by AmazGame; |

13

| • | Shanghai Jingmao, acquired in 2010 by Yang Fan Jing He; |

| • | Beijing Jingmao, established in 2010 by Shanghai Jingmao and acquired in 2012 by Yang Fan Jing He; |

| • | 7Road Technology, organized in 2012 as a WFOE of 7Road.com HK, which is a wholly-owned subsidiary of 7Road; and |

| • | Beijing Baina Technology, acquired in July 2014 as a WFOE of MoboTap HK; |

Principal Variable Interest Entities

The following are our principal VIEs, which we established or acquired in China to perform value-added telecommunications services because of PRC restrictions on direct foreign investment in and operation of value-added telecommunications businesses, which restrictions are discussed further below under the heading “Government Regulation and Legal Uncertainties-Specific Regulations-Regulation of Foreign Direct Investment in Value-Added Telecommunications Companies.” We entered into contractual arrangements between our VIEs and our PRC Subsidiaries that govern a substantial portion of our operations, including those of the brand advertising business, the search and Web directory business, the online game business and the others business. These entities are consolidated in Sohu’s consolidated financial statements, and noncontrolling interest is recognized when applicable.

For Sohu’s Business

| • | High Century, a PRC company that we established in 2001. High Century is a holding company. Dr. Charles Zhang, our Chairman of the Board and Chief Executive Officer, and Wei Li held 80% and 20% interests, respectively, in High Century as of December 31, 2014; |

| • | Heng Da Yi Tong, formally known as Beijing Sohu Entertainment Culture Media Co., Ltd., a PRC company that we established in 2002. Dr. Charles Zhang and Wei Li held 80% and 20% interests, respectively, in Heng Da Yi Tong as of December 31, 2014; |

| • | Sohu Internet, a PRC company that we established in 2003. High Century and Heng Da Yi Tong held 75% and 25% interests, respectively, in Sohu Internet as of December 31, 2014; |

| • | Donglin, a PRC company that we established in 2010. Donglin engages in the advertising business. High Century and Sohu Internet each held 50% interest in Donglin as of December 31, 2014; |

| • | Pilot New Era, a PRC company that we established in 2010. Pilot New Era engages in the advertising and real estate business. High Century and Sohu Internet each held 50% interest in Pilot New Era as of December 31, 2014; |

| • | Tianjin Jinhu, a PRC company that we established in November 2011. Tianjin Jinhu provides video program production and performance and artist agency services in China. Ye Deng and Xuemei Zhang each held 50% interest in Tianjin Jinhu as of December 31, 2014; and |

| • | Guangzhou Qianjun, a PRC company that we acquired in November 2014. Tianjin Jinhu held a 100% interest in this entity as of December 31, 2014. |

For Sogou’s Business

| • | Sogou Information, a PRC company that we established in December 2005. Sogou Information provides Search and other Internet information services in China. As of December 31, 2014, Xiaochuan Wang, Sogou’s Chief Executive Officer, High Century and Tencent held 10%, 45% and 45% interests, respectively, in Sogou Information. Sogou Information is indirectly controlled by Sogou Inc., our controlled search subsidiary. |

For Changyou’s Business

| • | Gamease, a PRC company that we established in August 2007. Gamease provides online game services in China. Tao Wang, the former Chief Executive Officer of Changyou, and Dewen Chen, the Co-Chief Executive Officer of Changyou, held 60% and 40% interests, respectively, in Gamease as of December 31, 2014; |

14

| • | Guanyou Gamespace, a PRC company that we established in August 2010. Guanyou Gamespace provides online game services in China. Tao Wang and Dewen Chen held 60% and 40% interests, respectively, in Guanyou Gamespace as of December 31, 2014; |

| • | Shanghai ICE, a PRC company that we acquired in May 2010. Shanghai ICE provides online game services in China. Runa Pi and Rong Qi each held a 50% interest in Shanghai ICE as of December 31, 2014; |

| • | Shenzhen 7Road, a PRC company that was established in January 2008. Gamease, which is one of Changyou’s VIEs, acquired 68.258% of the equity interests in Shenzhen 7Road in May 2011 and acquired the remaining 31.742% of the equity interests in June 2013. Shenzhen 7Road engages in Web game development and operations in China and internationally. Gamease held 100% of the equity interest in Shenzhen 7Road as of December 31, 2014; |

| • | Wuhan Baina Information, a PRC company acquired by Gamease in July 2014. Wuhan Baina Information engages in the Internet information services business. Gamease and a third-party individual held 60% and 40% interests, respectively, in this entity as of December 31, 2014. |

As of the date of this report, Changyou is in the process of transferring each of the individual shareholders’ ownership interests in Gamease, Guanyou Gamespace and Shanghai ICE to entities that are affiliates of the Sohu Group.

We have extended interest-free loans to the individual shareholders of the VIEs to fund their capital investment in the VIEs. The loans are secured by pledges of the shareholders’ equity interests in the VIEs, and can only be repaid by the shareholders by surrender of those equity interests to us. We have also entered into a series of agreements with the individual shareholders to transfer their equity interests in the VIEs to us when required to do so.

GOVERNMENT REGULATION AND LEGAL UNCERTAINTIES

The following description of PRC laws and regulations is based upon the opinion of Haiwen & Partners, or Haiwen, our PRC legal counsel. The laws and regulations affecting China’s Internet industry and other aspects of our business are at an early stage of development and are evolving. There are substantial uncertainties regarding the interpretation and enforcement of PRC laws and regulations. We cannot assure you that the PRC regulatory authorities would find that our corporate structure and business operations strictly comply with PRC laws and regulations. If we are found to be in violation of PRC laws and regulations by the PRC government, we may be required to pay fines, obtain additional or different licenses or permits, and/or change, suspend or discontinue our business operations until we are found to comply with applicable laws. For a description of legal risks relating to our ownership structure and business, see “Risk Factors.”

Overview

The Chinese government has enacted an extensive regulatory scheme governing Internet-related areas, such as telecommunications, Internet information services, international connections to computer information networks, online game services, information security and censorship.

Various aspects of the PRC Internet industry are regulated by various PRC governmental authorities, including:

| • | the Ministry of Industry and Information Technology (“MIIT”); |

| • | the Ministry of Culture (“MOC”); |

| • | the Ministry of Public Security (“MPS”); |

| • | the Ministry of Commerce (“MOFCOM”); |

| • | the State Administration of Industry and Commerce (“SAIC”); |

| • | the State Administration of Press, Publication, Radio, Film and Television (“SAPPRFT”), which resulted from the merger of the former General Administration of Press and Publication, or (“GAPP”), with the former State Administration of Radio, Film and Television (“SARFT”), in March 2013. The “SAPPRFT” as used in this report refers to the governmental authority that resulted from the merger, as well as to the GAPP and the SARFT separately for periods prior to the merger; |

| • | the PRC State Council Information Office (“SCIO”); and |

| • | the State Administration of Foreign Exchange (“SAFE”). |

15

Specific Statutes and Regulations

Requirements for Establishment of WFOEs

Under current PRC laws, the establishment of a WFOE must be approved by MOFCOM or one its local branches. Each of our WFOEs was established with such approval.

Requirements for Obtaining Business Licenses

All China-based companies may commence operations only upon the issuance of a business license by the relevant local branch of the SAIC. All of our China-Based Subsidiaries and VIEs have been issued business licenses by the relevant local branches of the SAIC.

In the opinion of Haiwen, our principal China-Based Subsidiaries and principal VIEs have satisfied the requirements for business licenses.

Regulation of Value-added Telecommunications Services

The Telecommunications Regulations of the People’s Republic of China (“Telecom Regulations”), implemented on September 25, 2000 and amended on July 29, 2014, are the primary PRC law governing telecommunication services, and set out the general framework for the provision of telecommunication services by domestic PRC companies. The Telecom Regulations require that telecommunications service providers procure operating licenses prior to commencing operations. The Telecom Regulations draw a distinction between “basic telecommunications services,” which we generally do not provide, and “value-added telecommunications services.” The Telecom Regulations define value-added telecommunications services as telecommunications and information services provided through public networks. The Catalogue of Telecommunications Business (“Catalogue”), which was issued as an attachment to the Telecom Regulations and updated in February 2003, identifies online data and transaction processing, on-demand voice and image communications, domestic Internet virtual private networks, Internet data centers, message storage and forwarding (including voice mailbox, e-mail and online fax services), call centers, Internet access, and online information and data search as value-added telecommunications services. We engage in various types of business activities that are value-added telecommunications services as defined and described by the Telecom Regulations and the Catalogue.

On March 1, 2009, the MIIT issued the Measures on the Administration of Telecommunications Business Operating Permits (the “Telecom License Measures”), which became effective on April 10, 2009, to supplement the Telecom Regulations and replace the previous Administrative Measures for Telecommunications Business Operating Licenses. The Telecom License Measures confirm that there are two types of telecom operating licenses for operators in China, one for basic telecommunications services and one for value-added telecommunications services. A distinction is also made as to whether a license is granted for “intra-provincial” or “trans-regional” (inter-provincial) activities. An appendix to each license granted will detail the permitted activities of the enterprise to which it was granted. An approved telecommunication services operator must conduct its business (whether basic or value-added) in accordance with the specifications recorded in its Telecommunications Services Operating License.

The business activities of Sohu Internet include the provision of mobile-related services and mobile products offered in cooperation with China mobile network operators to mobile phone users and to China mobile network operators. Most of the mobile revenues are derived through products such as SMS, RBT and IVR. On April 25, 2004, the MIIT issued a notice stating that China mobile network operators may only provide mobile network access to those mobile Internet service providers which have obtained licenses from the relevant local arm of the MIIT before conducting operations, and that such carriers must terminate mobile network access for those providers who have not secured the required licenses within a thirty-day grace period. On the basis of the notice, China Mobile has required each of its mobile Internet service providers to first obtain a license for trans-regional value-added telecommunications services in order to gain full access to its mobile network, which is a nationwide policy in line with a similar notice issued by the Beijing branch of China Mobile on April 12, 2004.

On August 8, 2014 and November 3, 2014, respectively, the MIIT issued to Sohu Internet and Guangzhou Qianjun renewed Value-Added Telecommunications Services Operating Licenses, which authorize the provision of trans-regional mobile services classified as value-added telecommunication services. The licenses are subject to annual inspection.

Regulation of Foreign Direct Investment in Value-Added Telecommunications Companies

Various PRC regulations currently restrict foreign-invested entities from engaging in value-added telecommunication services, including providing Internet information services and operating online games. Foreign direct investment in telecommunications companies in China is regulated by the Regulations for the Administration of Foreign-Invested Telecommunications Enterprises (“FITE Regulations”), which were issued by the PRC State Council, or State Council, on December 11, 2001, became effective on January 1, 2002 and were amended on September 10, 2008. The FITE Regulations stipulate that foreign invested telecommunications enterprises in the PRC (“FITEs”) must be established as Sino-foreign equity joint ventures. Under the FITE Regulations and in accordance with WTO-related agreements, the foreign party to a FITE engaging in value-added telecommunications services may hold up to 50% of the equity of the FITE, with no geographic restrictions on its operations.

16

For a FITE to acquire any equity interest in a value-added telecommunications business in China, it must satisfy a number of stringent performance and operational experience requirements, including demonstrating a track record and experience in operating a value-added telecommunications business overseas. FITEs that meet these requirements must obtain approvals from the MIIT and the MOFCOM or their authorized local counterparts, which retain considerable discretion in granting approvals.

On July 13, 2006, the MIIT issued the Notice of the Ministry of Information Industry on Intensifying the Administration of Foreign Investment in Value-added Telecommunications Services (the “MIIT Notice”),which reiterates certain provisions of the FITE Regulations. Under the MIIT Notice, if a FITE intends to invest in a PRC value-added telecommunications business, the FITE must be established and must apply for a telecommunications business license applicable to the business. Under the MIIT Notice, a domestic company that holds a license for the provision of Internet content services, or an ICP license, is considered to be a type of value-added telecommunications business in China, and is prohibited from leasing, transferring or selling the license to foreign investors in any form, and from providing any assistance, including providing resources, sites or facilities, to foreign investors to conduct value-added telecommunications businesses illegally in China. Trademarks and domain names that are used in the provision of Internet content services must be owned by the ICP license holder. The MIIT Notice requires each ICP license holder to have appropriate facilities for its approved business operations and to maintain such facilities in the regions covered by its license. In addition, all value-added telecommunications service providers are required to maintain network and information security in accordance with standards set forth in relevant PRC regulations. Our VIEs, rather than our subsidiaries, hold ICP licenses, own our domain names, and hold or have applied for registration in the PRC of trademarks related to our business and own and maintain facilities that we believe are appropriate for our business operations.

In view of these restrictions on foreign direct investment in the value-added telecommunications sector, we established or acquired several domestic VIEs to engage in value-added telecommunications services. For a detailed discussion of our VIEs, please refer to “Our Corporate Structure” above. Due to a lack of interpretative materials from the relevant PRC authorities, there are uncertainties regarding whether PRC authorities would consider our corporate structure and contractual arrangements to constitute foreign ownership of a value-added telecommunications business. See “Risks Related to Our Corporate Structure.” In order to comply with PRC regulatory requirements, we operate our main business through companies with which we have contractual relationships but in which we do not have an actual ownership interest. If our current ownership structure is found to be in violation of current or future PRC laws, rules or regulations regarding the legality of foreign investment in the PRC Internet sector, we could be subject to severe penalties.

In the opinion of Haiwen, subject to the uncertainties and risks disclosed elsewhere in this report under the heading “Risk Factors” and “Government Regulation and Legal Uncertainties”, the ownership structures of our principal PRC Subsidiaries and our principal VIEs comply with all existing laws, rules and regulations of the PRC and each of such companies has the full legal right, power and authority, and has been duly approved, to carry on and engage in the business described in its business license.

Regulation of the Provision of Internet Content

Internet Information Services

On September 25, 2000, the State Council issued the Measures for the Administration of Internet Information Services (“ICP Measures”). Under the ICP Measures, entities that provide information to online users on the Internet, or ICPs, are obliged to obtain an operating license from the MIIT or its local branch at the provincial or municipal level in accordance with the Telecom Regulations described above.

The ICP Measures further stipulate that entities providing online information services regarding news, publishing, education, medicine, health, pharmaceuticals and medical equipment must procure the consent of the national authorities responsible for such areas prior to applying for an operating license from the MIIT or its local branch at the provincial or municipal level. Moreover, ICPs must display their operating license numbers in conspicuous locations on their home pages. ICPs are required to police their Websites and remove certain prohibited content. Many of these requirements mirror Internet content restrictions that have been announced previously by PRC ministries, such as the MIIT, the MOC, and the SAPPRFT, that derive their authority from the State Council.

Most importantly for foreign investors, the ICP Measures stipulate that ICPs must obtain the prior consent of the MIIT prior to establishing an equity or cooperative joint venture with a foreign partner.

On July 2, 2014 , October 10, 2014, the Beijing Telecom Administration (“BTA”) issued to Sogou Information, and Sohu Internet a renewed Telecommunications and Information Services Operating Licenses (each an “ICP license”). On August 13, 2012, the Shanghai Telecom Administration issued a renewed ICP license to Shanghai ICE. On October 17, 2012, the BTA issued to Guanyou Gamespace a renewed ICP license. On July 19, 2011, the Guangdong Telecom Administration issued to Shenzhen 7Road an ICP license. On May 22, 2014, the BTA issued to Gamease a renewed ICP license. All of these ICP licenses are subject to annual inspection.

17

In 2000, the MIIT promulgated the Internet Electronic Bulletin Service Administrative Measures (“BBS Measures”). The BBS Measures required ICPs to obtain specific approvals before they provided BBS services, which included electronic bulletin boards, electronic forums, message boards and chat rooms. On September 23, 2014, the MIIT abolished the BBS Measures in a Decision on Abolishment and Amendment Certain Regulations and Rules. However, in practice certain local authorities still require operating companies to obtain approvals or make filings for the operation of BBS services. The ICP licenses held by Sohu Internet, Sogou Information, Gamease and Guanyou Gamespace include such specific approval of the BBS services that they provide. However, although Shenzhen 7Road provides BBS services, its ICP license does not specifically permit the operation of BBS services. It is unclear whether Shenzhen 7Road’s provision of BBS services is in violation of applicable regulations or local practice. In order to avoid the possibility of being challenged by the relevant local authorities with respect to the absence of approval for its BBS services, Shenzhen 7Road has applied to the Guangdong Communications Administration for amendments of its ICP license to permit operation of BBS services. Shenzhen 7Road has been orally informed by Guangdong Communications Administration that currently there are no specific governmental entities with the authority to approve BBS services in Shenzhen and that new regulations regarding the provision of BBS services may be released in 2015. If relevant PRC authorities were to determine that Shenzhen 7Road’s provision of BBS services is prohibited due to the absence of such specific approval or filings, Shenzhen 7Road might be subject to fines up to five times the income it generated from such services and other penalties, such as the shutdown of its Websites.

On December 29, 2011, the MIIT issued Several Provisions for Standardizing the Market Order of Internet Information Services (the “Several Provisions”) which took effect on March 15, 2012. With the aim of promoting the healthy development of the Internet information services market in China, the Several Provisions strengthen the regulation of the operations of Internet information service providers, including prohibiting Internet information service providers from infringing the rights and interests of other Internet information service providers, regulating evaluations provided by Internet information service providers regarding the services and products of other Internet information service providers, and regulating the installation and running of software by Internet information service providers. The Several Provisions also provide various rules to protect the interests of Internet information users, such as requesting Internet information service providers to take measures to protect the privacy information of their users and prohibiting Internet information service providers from cheating and misleading their users.

Online News Dissemination