Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - Borderfree, Inc. | Financial_Report.xls |

| EX-23.1 - EXHIBIT 23.1 - Borderfree, Inc. | ex231consent.htm |

| EX-32.1 - EXHIBIT 32.1 - Borderfree, Inc. | section906certs-20141231.htm |

| EX-31.1 - EXHIBIT 31.1 AND 31.2 - Borderfree, Inc. | section302certs-20141231.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2014

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 001-36359

BORDERFREE, INC.

(Exact name of registrant as specified in its charter)

Delaware | 52-2216062 | |||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||

292 Madison Avenue, 5th Floor

New York, New York 10017

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code:

(212) 299-3500

Securities Registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Stock, $0.01 par value per share | The NASDAQ Stock Market LLC | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | ¨ | |

Non-accelerated filer | x | (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of common stock held by non-affiliates of the registrant based on the closing price of the registrant’s common stock as reported on NASDAQ on June 30, 2014, was $167.5 million. Shares of voting and non-voting stock held by executive officers, directors and holders of more than 5% of the outstanding stock have been excluded from this calculation because such persons or institutions may be deemed affiliates. This determination of affiliate status is not a conclusive determination for other purposes.

The number of shares of common stock, par value $0.01 per share, outstanding as of February 25, 2014 was 31,961,225.

Documents Incorporated by Reference

Portions of the registrant’s definitive proxy statement for its annual meeting of stockholders, which the registrant intends to file pursuant to Regulation 14A with the Securities and Exchange Commission not later than 120 days after the registrant’s fiscal year end of December 31, 2014, are incorporated by reference into Part III of this Form 10-K.

BORDERFREE, INC.

INDEX TO FORM 10-K

Part I | Page | |

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Part II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Part III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Part IV | ||

Item 15. | ||

1

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. All statements other than statements relating to historical matters should be considered forward-looking statements. In addition, forward-looking statements may consist of statements including such words as “may,” “believe,” “could,” “anticipate,” “would,” “might,” “plan,” “expect,” and similar expressions or the negative of such terms or other comparable terminology. These forward-looking statements speak only as of the date of this Annual Report on Form 10-K and are subject to business and economic risks. These statements are not guarantees of future performance and involve certain risks, uncertainties, and assumptions that are difficult to predict, and you should not place undue reliance on our forward-looking statements. Our actual results could differ materially from those set forth in the forward-looking statements as a result of a number of important factors, including the factors set forth in Part I, Item 1A, “Risk Factors,” and elsewhere in this Annual Report on Form 10-K and in our other reports filed with the Securities and Exchange Commission, or SEC. We expressly disclaim any obligation to update the forward-looking statements to reflect events or circumstances that arise after the date hereof.

ITEM 1. BUSINESS

We are a market leader in global ecommerce, operating a proprietary technology and services platform to enable U.S. retailers to transact with consumers in more than 100 countries and territories worldwide. Borderfree delivers a comprehensive cross-border ecommerce solution available through a single unified platform enabling retailers to capitalize on the large cross-border market opportunity. Our customers, comprised of the retailers and brands that integrate our solution, use our highly scalable Borderfree platform to develop a seamless global ecommerce business across web, mobile and in-store channels to transact with international shoppers, who we refer to as consumers. Borderfree manages all aspects of the international shopping experience, including site localization, multi-currency pricing, payment processing, fraud management, landed cost calculation, customs clearance and brokerage, and global logistics services while maintaining the integrity of our customers’ brands and the consumer experience. Our integrated cross-border solution enables retailers to begin selling internationally typically within 90 days without the need to invest in expensive infrastructure, software, in-house compliance expertise or international vendor relationships. In addition, as a result of our scale and experience in international ecommerce, we have amassed a substantial amount of data that enables us to provide actionable marketing and merchandising insights to our customers to help grow their global sales.

Today, we are enabling the online international expansion initiatives of some of the largest U.S. retailers and brands, including J. Crew, Lands’ End, Macy’s, Neiman Marcus, Sephora, Under Armour, and Williams-Sonoma. We refer to U.S. retailers and brands as our customers and the shoppers transacting with them as consumers. As of December 31, 2014, our platform was powering the global expansion of 171 ecommerce sites for 96 customers.

We derive ecommerce revenue from fees paid to us by our customers based on a percentage of their sales generated through our platform and foreign exchange and other transaction related fees payable by consumers. We generate additional revenue from fulfillment services. We operate our business through an asset-light model, requiring minimal capital investment, which allows us to scale our business in a cost effective and efficient manner. Our customer contracts typically have multi-year initial terms ranging from one to four years, followed by one-year renewal periods.

Founded in 1999, we initially came to market with a patented foreign exchange technology solution that allowed ecommerce retailers to automatically present and settle transactions in the preferred currencies of their global consumers. As our business evolved, we realized that the problems retailers faced selling internationally went beyond foreign exchange to include localization, payments and logistical complexities. In response to these challenges we developed a comprehensive global ecommerce technology and service offering and renamed our company FiftyOne. The commercial launch of our global ecommerce platform occurred in 2008. In 2013, following the 2012 acquisition of the Borderfree business unit of Canada Post Corporation, we changed our name to Borderfree. In January 2015, we acquired Bundle Tech Limited, the operator of DutyCalculator, a provider of cloud-based global trade and customs compliance data services.

2

We processed $547 million, $448 million and $302 million of gross merchandise volume, or GMV, on our platform during 2014, 2013, and 2012, representing period over period growth of 22%, 48% and 120%, respectively. We experienced similar growth in revenue, generating revenue of $125 million, $110 million and $81 million in the same periods, representing period over period revenue growth of 14%, 36%, and 114% respectively. Additionally, global ecommerce services revenue grew 23%, 52%, and 111% over the same periods, respectively. We had net loss of $3.1 million and $0.7 million for the year ended December 31, 2014 and 2013, respectively, and net income of $0.2 million in 2012. For a definition of GMV see "Management's Discussion and Analysis of Financial Condition and Results of Operations" under Item 7 of this Annual Report on Form 10-K.

Market Opportunity

As a global ecommerce platform for online retailers, we benefit from international trends in ecommerce.

Ecommerce: a Large and Growing Global Market

The global mass migration of consumers from physical to online retail channels provides ecommerce retailers significant opportunities to serve markets outside the traditional scope of their business. Increasingly, consumers expect the ability to easily and seamlessly make online purchases from retailers without having to give much thought or consideration as to where that retailer is located, where the product is located, or how it will get to the consumer as long as the shopping experience is comfortable and the act of fulfilling the transaction is secure, timely, and problem free.

Strong demand for U.S. brands from global consumers provides U.S. retailers significant opportunities to serve markets outside the United States. Many U.S. brands have strong reputations internationally, with U.S. brands accounting for 54% of Interbrand’s Top 100 global brands in 2014. Prestige, product selection, price, and quality are just a few of the factors driving demand for U.S. brands by global consumers across the world. At the same time, technology trends such as broadband penetration and mobile device proliferation are making it easier for global consumers to purchase from brands located in the U.S. or other parts of the world.

While Canada, Australia, the U.S. (for U.K. retailers) and the U.K. (for U.S. retailers) are natural markets for U.S. and U.K. retailers looking to expand internationally given the common language, cultural similarities, and an established ecommerce market, demand for goods from retailers based in these countries is significant throughout the world. Additional markets for our retailers include major non-English speaking developed economies such as France, Germany and Japan, and fast growing, emerging markets including China, Mexico, South Korea and the Middle East.

Given our focus on cross-border ecommerce, our addressable market is comprised of physical goods which can be shipped cost effectively, like apparel, handbags, jewelry, sporting goods, home décor, and toys, and therefore does not include digital goods and services, such as music downloads and travel. Many U.S. retailers are targeting faster growing international markets to boost the growth of their ecommerce businesses and take a larger share of the global ecommerce market.

The Under-monetized Cross Border Ecommerce Opportunity

We believe that the current cross-border ecommerce market is under-monetized and that U.S. and U.K. retailers not selling internationally today, or doing so in a non-optimized way, are missing out on significant demand from international consumers that, if served, could generate significant incremental ecommerce revenues for those retailers. We believe that the percentage of visitor traffic from international consumers will grow as internet penetration increases internationally, driving more global consumers to shop online with foreign retailers for the greater product selection from their favorite international brands.

We believe that a large opportunity exists globally for retailers and brands seeking to sell products to consumers outside of their home markets, which could represent an expansion of our total addressable market. We believe that by helping retailers everywhere export to anywhere in the world, we can tap into this large global market opportunity.

3

Challenges of Selling to Global Consumers

Challenges for Retailers

Selling globally can be expensive and complicated. There are currently two in-house alternatives to sell to global consumers, cross-border trading and establishing an in-country presence.

Cross-border Trading

Retailers selling to global consumers directly from their domestic website face challenges and risks including:

• | complicated import and export regulations and restrictions, which vary by country, product and quantity, and require costly resources to ensure compliance; |

• | an increased risk of credit card fraud; |

• | lower sales conversion rates due to factors including higher shipping costs, unexpected customs and duties, limited local currency payment options and narrower product selection; |

• | difficulty in tailoring the product offerings on its domestically-based website to global consumers in different markets; |

• | damage to their overall brand image if they provide a frustrating consumer experience; and |

• | foreign exchange volatility. |

Establishing an In-country Presence

Retailers setting up local operations face challenges and risks including:

• | investment of significant amounts of time and money to establish and maintain country-specific websites, order management systems, distribution centers, call centers, inventory, subsidiaries and other infrastructure such as local banking relationships and international shipping relationships; |

• | significant upfront investment with limited ability to assess local consumer demand before entering the market; |

• | exposure to foreign exchange and tax risk due to their investment and operations in the market; and |

• | inability to scale effectively, as each new market typically requires unique solutions which are not easily replicated from solutions in other markets. |

The challenges and risks posed by these alternatives cause many retailers to delay global expansion and miss the opportunity to generate additional revenue and further expand their brand awareness around the world.

4

Challenges for the Global Consumer

Global consumers are often faced with a disappointing customer experience whether they buy from a retailer’s local in-country website or a foreign website. In the case of local in-country websites of retailers, consumers are often faced with narrower product selection compared with what is available on the retailer’s domestic website. When ordering from a domestic website, international consumers often have to deal with high shipping costs, additional unexpected fees at the time of delivery related to taxes, customs and duties and long delivery times. They may also find that the domestic website does not translate the product prices into their local currency, has restrictive return policies, and lacks support for foreign credit cards or payment methods. In addition, many retailers fail to tailor their product catalogs to comply with export and import restrictions, presenting global consumers with products they cannot ultimately buy. We believe all of these limitations make it frustrating for the consumer and ultimately more difficult for an international consumer to buy from domestic retailers, thus contributing to the significant disparity between websites visited and transactions consummated by consumers outside the United States and the United Kingdom.

As a result, we believe the combination of the large international cross-border ecommerce opportunity and challenges of implementing an in-house solution create a significant opportunity for a differentiated third party solution.

The Borderfree Solution

The Borderfree solution is a proprietary ecommerce technology and services platform designed to remove the barriers to international cross-border ecommerce.

5

6

Key benefits of our platform include:

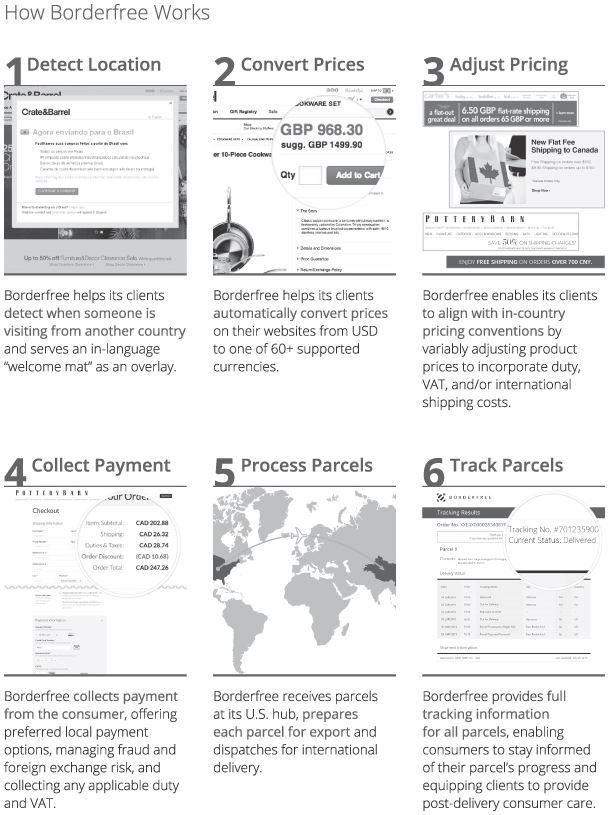

Comprehensive Solution. We believe Borderfree delivers the most comprehensive international ecommerce solution available through a single unified platform. Borderfree manages all aspects of the international sales process, including site localization, multi-currency pricing, payment processing, fraud management, landed cost calculation, customs clearance and brokerage and global logistics services while providing a high quality consumer experience throughout. In addition, our solution eliminates foreign exchange and credit card fraud exposure for our customers. Our solution combined with our experience in facilitating millions of international ecommerce transactions allows us to successfully navigate these challenges on behalf of our customers at low cost and risk to them.

High Return on Investment. We believe that the Borderfree platform offers a capital efficient, cost-effective and low-risk solution for retailers to compete in international markets. After a minimal initial investment for integration with our platform, which enables retailers to launch in all or select markets without any incremental cost, customers then pay us a percentage of the sales they generate through our platform. Retailers are typically able to start selling within 90 days in over 100 countries and territories and in more than 60 currencies. Retailers who implement our platform have the flexibility to launch in all or select markets, without any incremental cost or effort to activate additional markets. As we expand the available countries on our platform, our customers will gain access to these countries at no additional cost.

High Quality Consumer Experience. Our platform enables our customers to provide a localized experience that maintains their brand integrity. Our platform geo-locates global consumers, and welcomes them in the local language to instill confidence at the outset of the shopping experience. All merchandise prices are converted to the consumer’s preferred currencies site-wide, and the consumer is presented with a landed cost calculation which is the transaction cost inclusive of all tariffs, value added tax, shipping costs, and clearance fees to ensure there are no surprise charges. In addition, the consumer can select from relevant local payment options, track purchases online with order update emails and a consolidated tracking link and benefit from the retailers’ international returns and other consumer service initiatives.

Customizable Pricing and Promotion Strategies. In addition to providing our market specific knowledge to retailers, we aggregate and analyze the data generated from the transactions processed on our platform. Our customers are able to leverage this data to create, test and deploy country-specific pricing and promotion strategies to maximize checkout conversion. For example, using our platform retailers can create and manage country specific pricing rules that optimize landed cost for conversion by adding margin into product prices to offset the cost of any combination of any shipping, duty or value added tax related promotions at checkout. Retailers can also display location based offers tailored to consumers visiting from specific countries such as dollar and percentage off discounts for merchandise product, shipping costs and duty and value added tax, order and item level discounts, coupons, as well as other specialized promotions.

Access to New Sales and Marketing Channels. We have formed strategic partnerships with global marketing partners, including those with payment processors. These partnerships can expand the marketing reach of retailers to many millions of qualified consumers through the variety of marketing channels offered by these partners. Additionally, these partnerships typically leverage our existing customer integration into our platform.

7

Our Competitive Strengths

As a result of our extensive experience in cross-border ecommerce and substantial data asset resulting from consumer interactions on our platform, we enjoy a strategic relationship with our customers. Our customers look to us for a technology solution to enable international ecommerce expansion as well as for strategic advice on how to best expand in markets around the world.

Our competitive strengths include:

Comprehensive and Scalable Platform. Our ecommerce platform enables retailers to begin selling internationally without requiring significant investment of time or resources. As the retailer’s global sales grow, our platform has the features and functionality to scale with them and effectively address their needs. As a result, we believe that we possess the most comprehensive platform for retailers looking to expand their ecommerce sales internationally, quickly and cost effectively.

Global Reach and Scale. In 2014 we facilitated approximately $547 million of GMV, shipping to over 100 countries and territories, and settling transactions in more than 60 currencies. We have a network of global and market-specific logistics vendors and payment providers. This network enables us to execute transactions and deliver products to both established markets and difficult to reach locations around the world. As a result of our scale and ability to consolidate volume we enjoy lower fulfillment costs and access to competitive foreign exchange rates.

Asset-light Business Model. Our model allows us to scale our business to serve additional customers, markets and GMV with minimal capital expenditures. We do not own or operate any distribution centers or warehouses. We work with third-party logistics providers for hub processing and international delivery services to process and transport products to the consumer, paying only a volume-based fee which varies in line with our customers’ sales volume. We also do not own or operate any consumer support centers, as our customers handle consumer service calls directly.

Branded Consumer Experience. We enable the retailer to provide a localized shopping experience that instills in international consumers the same level of trust and confidence in their brand as their U.S. consumers. Retailers who use our solution maintain full control of the consumer experience including the website presentation, customer service, product packaging and pre and post order related communications. All of these interactions are done in accordance with the brand and product objectives of our customers. By focusing on the immediacy, prominence and visibility of our customers’ brands, our solution is appealing to retailers who acquire and maintain customers through brand equity and customer service, especially large and iconic lifestyle and department store brands.

Substantial and Growing Data Asset. As the processor of consumer transactions on our platform, Borderfree possesses a substantial amount of data related to international consumer demand and purchasing behavior. With the growth in the number of customers operating their ecommerce sites on our platform, we have processed more than 7.0 million transactions since the launch of the Borderfree solution in the beginning of 2008. We collect data from the time a consumer initiates the check-out process to the time a consumer completes the transaction, providing retailers with a unique holistic view of the consumer’s preferences down to the SKU-level across multiple brands. This data, coupled with investment in advanced analytics and CRM capabilities, produces meaningful insights into international ecommerce marketing, merchandising and conversion strategies. In the years ended 2014, 2013 and 2012, we saw 2.6 million, 2.1 million and 1.4 million transactions on our platform, respectively.

Growing and Loyal Customer Base. Since we launched the Borderfree solution, we have experienced significant growth in our customer base, growing from a single customer in the beginning of 2008 to 96 as of December 31, 2014. We believe that our ability to retain customers is an indicator of the stability of our revenue base and the long-term value of our customer relationships. We assess our performance in this area using a metric we refer to as our global ecommerce services retention rate. We define this retention rate with respect to a given twelve-month period as (i) global ecommerce services revenue recognized within such period from customers that contributed global ecommerce services revenue in the prior twelve month period divided by (ii) global ecommerce services revenue recognized in such prior twelve month period. Our global ecommerce services retention rate was 122%, 144% and 197% for the years ended December 31, 2014, 2013 and 2012, respectively. We also gain valuable feedback from our existing customers, which helps enhance our platform with the most relevant features and functionality to stay current with our customers’ needs and attract prospective customers. As of December 31, 2014, we had 11 of the Internet Retailer Top 50 as our customers, and 61 of the Top 500. This loyal customer base of high profile retailers also serves to attract new customers as they see the tangible benefits realized by implementing our solution. In addition, once the Borderfree solution is deployed, GMV processed on customers’ collective ecommerce sites and average GMV per customer typically grows over time.

8

International Experience. We have developed market specific knowledge about ecommerce across a diverse group of markets and cultures. Our expertise helps our customers navigate local rules, regulations and compliance to sell to consumers in local markets more quickly and optimize market specific merchandising and marketing strategies to sell to these consumers more effectively.

9

Our Growth Strategy

Our mission is to be the leading provider of global ecommerce services, enabling retailers and brands located anywhere in the world to easily market and sell to consumers in every corner of the globe. Our strategies to achieve this goal include:

Grow GMV with our Existing Customers. While customers on our platform have rapidly grown their international ecommerce sales, international sales still represent only a small percentage of their domestic sales and international conversion on many sites remains a fraction of conversion on domestic sites. Therefore, we believe that there remains a significant opportunity for these customers to continue to grow their international sales volumes. We are pursuing a number of key initiatives to drive this growth including:

• | Improving Sales Conversion Through an Enhanced Shopping Experience for International Consumers. The cost of shipping is one of the largest obstacles to a global consumer completing an online purchase. Leveraging our scale, we have negotiated more favorable rates with our existing carriers to reduce shipping costs, which we believe has contributed to the improvement in our order submit rate. We intend to continue reducing the cost of logistics by expanding the number of hubs and carriers in our logistics network and introducing new lower cost delivery options, which we believe will improve our order submit rate. In addition to lower logistics costs, we are improving the localization capabilities of our technology platform, incorporating a variety of language, payment and cultural variables to provide as local a shopping experience as possible, no matter from where the consumer originates. |

• | Acquiring New Consumers and Driving Qualified Site Traffic Through Strategic Partnerships. By developing and leveraging in-market strategic partnerships with organizations that have deep relationships with global consumers, we believe we have a considerable opportunity to expand our business with our customers by deploying marketing solutions that acquire new consumer relationships and drive incremental international traffic to their ecommerce sites. We are partnering with our customers across a wide spectrum of marketing and promotional strategies including shipping promotions, e-mail marketing, search engine marketing, contextually relevant display advertising and social media. In addition, we plan to expand and strengthen our strategic alliances with loyalty, shopping comparison, and payment providers to provide our clients with new customer acquisition channels. For example we have strategic partnerships with payment processors that serve to expand the marketing reach of our customers. |

• | Leveraging Our Data Assets. We have recently invested in new business intelligence and database platforms to expand our analytics capabilities and enhance our own and our customers’ ability to analyze the aggregated information, and leverage it to formulate data driven marketing and merchandising strategies. Through our analytics capabilities and consumer information we expect to deliver insights on, and access to, the global consumer to help our clients increase international sales. We do not currently monetize our data asset beyond making our core products and services more attractive to our customers although we may attempt to do so in the future. |

Acquire More Customers. We believe there is significant opportunity for a variety of merchants to target global consumers. Currently, we target U.S. and U.K. retail brands with significant global appeal such as large department stores, established and emerging consumer brands, specialty retailers and online only retailers. We intend to expand our sales and marketing investments to focus on acquiring these customers and expand the geographic scope in which we operate to other parts of Europe and Asia. In addition, we believe that our addressable market opportunity includes many mid-size to smaller retailers based in these markets in which we plan to acquire by developing self-service options requiring limited integration time, effort and investment.

Continue to Innovate and Add New Functionality to Our Platform. We continually invest in additional platform features and functionality to address our customers’ current and long-term needs. Specifically, we are investing in enhanced integration technology to make it easier for new customers to come onto the platform, an upgraded customs classification and tariff quotation engine, new carrier and payment provider integrations, streamlining browsing and purchasing on mobile devices, supporting in-country multi-channel pricing strategies and fulfilling orders using regional inventory.

Pursue Strategic Acquisitions. We plan to pursue acquisitions that complement our existing business, represent a strong strategic fit and are consistent with our overall growth strategy. We may also target future acquisitions to expand or add functionality and capabilities to our platform.

10

Products and Services

Borderfree Ecommerce Platform

The Borderfree platform is comprised of technology, data, expertise and services that span:

• | consumer experience localization, |

• | payments, compliance and risk management, |

• | global transportation and logistics, |

• | post-delivery customer care, and |

• | global consumer insights and marketing. |

Our platform enables our customers to provide a localized shopping experience for global consumers based on the consumer’s IP geolocation. Conditional page manipulation based upon the consumer’s IP geolocation occurs within our customer’s IT environment and website. This is an alternative to the creation and hosting by Borderfree of international versions of the customer’s website or the customer building, hosting and maintaining separate country-specific websites. The effects of localization on transactions processed on our platform include the conversion of product prices to the appropriate currency, the suppression or filtering of merchandise subject to import or export restrictions, the substitution of the domestic checkout path with our international checkout and the introduction of visual welcoming elements such as flag icons, welcome messaging in the consumer’s language and international frequently asked questions.

Consumer Experience Localization

Localizing a consumer’s experience starts with the synchronization of Borderfree’s localization data with the retailer’s website environment. Localization data is comprised of IP geolocation tables, country-currency pairs, currency code information, country-specific price multipliers, customizable by a retailer based on their pricing strategy, currency rounding methods and foreign exchange rates. A retailer can either schedule the download of this localization data via application programming interfaces, or APIs, provided by Borderfree, or install our proprietary software tool called the Ambassador. The Ambassador automatically downloads new localization data sets and persists the data into the retailer’s website environment, transmits the retailer’s full or incremental product catalog updates to Borderfree, for estimating the duty of each new product, and screens for products that may be subject to import, export or shipping service restrictions. With localization data easily accessible by a retailer’s ecommerce website, the IP address of an incoming consumer’s location is identified, and the presentation of a retailer’s ecommerce pages are altered to be “localized” as they are delivered to the consumer’s browser.

11

Retailers have the flexibility with our solution to modify a variety of elements and features on their site to localize pages for international consumers, including:

• | Dynamic Suppression or Filtering of Restricted Merchandise. The retailer can automatically suppress or otherwise make unavailable from browse or search results any products or categories that are subject to licensing, shipping, export or import restrictions. |

• | Localized Greetings and International Icons. Upon detecting a first-time global consumer, the retailer can display Borderfree’s localized and customizable “Welcome Mat” in the consumer’s preferred language, and a flag icon corresponding to the country of the consumer in a prominent location within the global site header. |

• | Product Pricing Displayed in the Buyer’s Preferred Currency. Products are presented in the consumer’s preferred currency at the current exchange rate. |

• | Customizable Country-specific Price and Promotion Strategies. Retailers can create and manage country-specific pricing rules that optimize landed costs for conversion by adding margin into product prices to offset the cost of any combination of shipping, duty or VAT related promotions at checkout. Retailers can also display location-based offers tailored to consumers visiting from specific countries. |

• | International Checkout. We provide our customers with two convenient ways to integrate our international checkout capability. We offer a responsively designed HTML checkout hosted by Borderfree that is faster to implement, requires very little customization and which inherits new checkout features that may be introduced over time. We also offer an API-based checkout for retailers looking to control the entire presentation layer and unify their international and domestic checkout process. |

12

Payments, Compliance and Risk Management

Regardless of the international checkout method chosen, our platform offers preferred local payment options, fraud and foreign exchange risk management, VAT and duty collection and remittance and the management of all import and export restrictions.

• | Local Payment Options. We obtain international shipping information, billing information, and payment details from the consumer. International credit cards and other popular international tender forms are accepted. |

• | Fraud Prevention. When the consumer places an order, we authenticate and authorize their international payment information, perform an automated, real time fraud assessment using a payment gateway and denied party screening and fraud management tools incorporated into our platform from CyberSource Corporation, a wholly-owned subsidiary of Visa Inc. We can automatically accept or reject the order based on this assessment, or queue an order for manual review. |

• | Foreign Exchange Risk Management. We bill the consumer in their preferred currency, using real-time exchange rates, fixed at the time of the transaction, with no risk to the consumer. The retailer bills a Borderfree credit card or Borderfree account, in U.S. dollars, and therefore assumes no foreign exchange risk in the transaction. |

• | VAT and Duty Collection. We charge the consumer a guaranteed fully landed cost, covering payment of all duties, taxes and charges required to deliver the product, except when the consumer elects to pay the duties upon delivery. We contract with licensed customs brokers to manage the related VAT and duty collection related to our transactions with international consumers. All applicable local duties and VAT are calculated by the licensed customs broker and submitted for review and approval by the destination country’s customs authority. Upon approval by the destination country’s customs authority, the licensed customs broker pays the amounts due related to the parcel entry. The actual amount is billed back to us by the licensed customs broker. The consumer is the importer of record and, therefore, we do not have nexus in any foreign jurisdiction. |

• | Import and Export Restrictions Management. We use a combination of merchant provided data, internal import and external export compliance expertise and licensed compliance and restrictions data services to prevent a consumer from purchasing U.S. export restricted products or products that are restricted from import into the consumers’ country prior to checkout. |

• | Support for Split Shipments, Cancels, Backorders and Pre-orders. Funds are captured from consumers once parcels are shipped, and only for pro-rated amounts based on the value of a single parcel in the case of a partially shipped order or split shipment. Additionally, Borderfree guarantees its foreign exchange rates in pre-order scenarios. |

13

Global Transportation and Logistics Coordination

We contract with third-party hub facilities in Romulus, Michigan, Franklin Park, Illinois, Fort Worth, Texas, Carlstadt, New Jersey, and Etobicoke, Ontario, where we receive inbound parcels from customers and process them for export and international delivery. We also contract with a U.K.-based third-party hub facility in Colnbrook, U.K. We intend to contract with additional hub facilities to support the growing scale of our business, including international hub facilities to support geographical expansion. Our logistics platform provides significant advantages to our customers:

• | Simple for the Retailer. At its U.S. warehouse, the retailer picks and packs the parcel as a domestic shipment, with minimal change from its existing processes, and using its preferred U.S. carrier. Although the option exists to tender parcels to U.S. carriers as individual parcels, the retailer can also consolidate the parcel with other international orders bound for our hubs, which reduces shipping costs. |

• | Product Sorting and Classification. Once a shipment arrives at our hubs, it is sorted and an operator scans individual parcels. The operator inspects the merchandise for country of origin if it has not been provided from the merchant electronically, prints an international packing slip and commercial invoice, overlabels the parcel with a shipping label specific to the international destination, then aggregates freight by carrier and shipping method. Customs brokers perform item classification and assign the merchandise any and all harmonized systems codes required for efficient customs clearance. |

• | Error Reduction. Exceptions are also managed at our hubs, with operators separating out any parcels that are damaged, appear to contain an incorrect quantity or appear to contain the incorrect items. In the event that a parcel contains restricted items or an incorrect quantity of items, we coordinate with the retailer to either arrange for the timely return of the damaged or incorrect merchandise, or to resolve the exception while the merchandise is still at the hub so that it can continue to its destination. |

• | Full Track and Trace. As the parcel leaves our hubs, we send the consumer an international shipment confirmation e-mail, which includes a link to a page where the consumer can track his or her parcel’s progress and receive periodic delivery updates. |

• | Electronic Customs Declaration and Clearance. While the parcel is in transit, a customs declaration is electronically sent to customs officers in the receiving country, and duty and VAT are paid or remitted in the consumer’s name. Pre-clearance of shipments while in transit allows many shipments to be inducted directly into the local delivery network. |

• | Parcel Protection and Replacement Guarantee. Local, trusted delivery services are used in each international market to ensure a positive experience by the consumer. All parcels shipped by us have a parcel protection and replacement guarantee in case of any logistics issues that result in a lost or damaged parcel. |

• | Returns Managements. We process consumer returns in accordance with our retailers’ return policies and automatically refund to the consumer original landed costs upon receipt at one of our third-party hubs or upon final receipt at our retailers’ return centers. All returns that are consolidated at our third-party hubs are then returned to our retailers’ designated returns centers. |

Post-Delivery Consumer Care

We provide a web-based customer care and order management tool to a retailer’s consumer care representatives that allows them to provide international consumer service. These tools include international order data and search functionality, billing and crediting history, fraud disposition insights, and parcel-level tracking detail for consumers that make inquiries about delivery of their package. Also included are tools to allow a retailer to manage international returns and appeasements, as well as support case management and ticketing functionality. Together, our tools allow retailers to provide the same level of after-sales service to their global consumers as to their domestic consumers.

14

Global Consumer Insights and Marketing

As more international transactions flow through our platform, and more brands and retailers integrate with the platform, we are strategically positioned to provide data-driven marketing and merchandising expertise to our clients. Some of the services that we offer include:

• | Sales Reports, Consumer Insights and Best Practices. We leverage our proprietary data, consumer surveys, in-country focus groups and global research to spot emerging trends and identify best practices to help our customers grow their international business. |

• | Localized SEM / SEO Strategies. Through our data and analytics tools, our customers can develop local search engine marketing, or SEM, and search engine optimization, or SEO, strategies. |

• | Marketing Strategies. We work with our customers and third parties to create promotions tailored specifically for the customer’s brand and target markets, and provide greater visibility to their products. |

• | Promotion Campaigns. We can create country-specific coupons and promotions to engage and retain consumers. We also have percent and dollar off discount capabilities. With flexible options, a retailer can initiate multiple opportunities to keep consumers engaged. |

• | Localized Messaging. Retailers can personalize the consumer experience with localized checkout messages that connect consumers to a retailer’s brand. |

15

Customers

Our customers are U.S.-based retailers, department stores, apparel brands and lifestyle brands selling a variety of physical goods online including apparel, handbags, beauty and cosmetics, jewelry, sporting goods, home décor, and toys. As of December 31, 2014, we had 96 customers using our ecommerce platform, as compared to 91, 84 and 78 as of December 31, 2013, 2012 and 2011, respectively.

Some of our customers have multiple brands within their brand portfolio and/or multiple online ecommerce sites. As of December 31, 2014, there were 171 ecommerce sites on our platform, as compared to 158, 133 and 94 as of December 31, 2013, 2012 and 2011, respectively.

The following is a representative list of our customers by category:

• | Department Stores: Barneys New York, Bloomingdale’s, Macy’s, Neiman Marcus, Sears |

• | Brands: Aeropostale, Carter’s–OshKosh B’gosh, J.Crew, John Varvatos, Juicy, Lands' End, True Religion Brand Jeans, Under Armour, |

• | Specialty Retailers: Bed Bath & Beyond, Motosport, Orchard Brands, Pottery Barn, Pottery Barn Kids, Sephora, Tilly’s, Williams-Sonoma |

• | Online-only Retailers: Gilt Groupe, Shoes.com |

Our customer contracts typically have multi-year initial terms ranging from one to four years, followed by one-year renewal periods.

16

Sales and Marketing

We sell our solution and services primarily through our direct sales force. Our direct sales force is based in New York and is organized by prospect size and merchandise category. We target retailers and brands with global ambition, iconic and coveted merchandise, global brand recognition, high customer experience standards and who sell merchandise that is both cost-effective to ship worldwide and subject to limited licensing, export, import or other transportation restrictions. Our sales cycle can vary from customer to customer, but typically requires four to six months depending on the size of the organization and complexity of the opportunity.

We generate customer leads, accelerate sales opportunities and build brand awareness through our marketing programs. Our marketing programs target ecommerce executives, technology professionals and senior strategy leaders. Our principal marketing programs include:

• | our annual Global Ecommerce Forum; |

• | participation in, and sponsorship of, trade shows and industry events; |

• | public relations and social media; |

• | customer acquisition announcements; |

• | customer case studies; and |

• | email campaigns and newsletters. |

In April 2014, over 200 attendees representing more than 100 existing and potential customers attended our sixth annual Global Ecommerce Forum. We presented marketing, innovation, and strategic insights at this invite-only event.

17

Technology, Operations, and Development

Technology

Our platform has been designed to support many merchants on a single service architecture across mobile and web technologies. We have a common distributed deployment of our core platform supporting all current merchants over a variety of integration methods. Some key considerations of our platform include:

• | Scalability. All components of the Borderfree platform were built to scale horizontally, allowing for additional capacity to handle large traffic events. We offload significant amounts of workload from our core infrastructure to third-parties. Additionally, we utilize virtualization technologies from VMWare to allow for rapid infrastructure adjustments in the case of unexpected workload. |

• | Reliability. We utilize nationally recognized third-parties for all areas of infrastructure, network, and software. We constantly invest in both internal and external monitoring capabilities to provide a complete picture of platform health. |

• | Security. We are a PCI-DSS Level 1 certified merchant, adhering to a set of standards that ensure that proper measures are in place to secure networks, data, architecture, and access to systems while also ensuring controls and process around cadence of testing, policy development, and change control are followed. This certification is a multifaceted security standard, monitored by the payment card industry, and includes external audits of business and technology functions to ensure compliance and maintain a company’s certification rating. We have an external certified PCI Qualified Security Assessor who performs a full audit annually and as needed support continuously. |

• | Ease of Deployment. Merchants can choose between prebuilt plugins for major platforms, hosted services, or deep API integrations depending on needs. Individual customer integrations do not require changes or releases in our core platform which means our platform can be easily deployed. We also have strong documentation and a hands-on approach to implementation with a dedicated technical implementations team to ensure high quality and efficient deployment. |

• | Open Platform. We built our platform with a modular, API driven approach. This model enables both internal teams and customers to build novel functionality extending our core platform to serve our customers’ business objectives. |

Operations

We operate and host our platform in two secure facilities located in New Jersey and California. We contract with Equinix Operating Co. and Atlantic Metro Communications for these facilities. We operate a 24 hour a day, seven day a week operations center from Tel Aviv, Israel and New York, New York to monitor and respond to automated alerts and customer support issues. Our operations group also provides ongoing administration, security, and deployment capabilities to the rest of the organization. As of December 31, 2014 we had 53 employees in our operations group, an increase from 47 employees as of December 31, 2013 and 46 employees as of December 31, 2012.

Research and Development

Our research and development organization is responsible for all new product development, quality assurance, and core platform improvements. We operate under an agile methodology and perform test-driven development, allowing for rapid product development while maintaining a high level of quality. Our research and development organization is located in both Tel Aviv, Israel, and New York, New York. We typically release new versions of our software monthly which our customers can easily access through web-based APIs. As of December 31, 2014 we had 67 employees in our product and research and development groups, an increase from 49 employees as of December 31, 2013 and 40 employees as of December 31, 2012.

18

Competition

The market for ecommerce technology and services is intensely competitive, subject to rapid technological change and significantly affected by new product introductions and other market activities. Our primary competition are retailers who choose to develop an in-house solution working directly with international third party payment partners, carriers and distribution center operators. The market for international ecommerce software and fulfillment services is highly fragmented and contains well-funded competitors. The market includes companies of various sizes, as well as large companies, that specialize in third-party point solutions or freight forwarding services, full-service ecommerce business process outsourcers and online marketplaces with international logistics support.

• | Third-party Point Solutions or Freight Forwarding Services. Our competitors in this category are typically not integrated with U.S. retailer websites, but instead offer international customers freight forwarding, consolidation, repackaging and temporary storage services as well as give member consumers the ability to purchase products from many U.S. websites, consolidate or repackage resulting parcels and have the service export the products to them at a later date. We compete with this category of competitors by focusing on an integrated and elevated consumer experience, providing visibility into consumer buying activity and our comprehensive set of merchandising and pricing capabilities that allows our customers to provide the international consumer with a localized experience and the ability to ship direct. |

• | Full-service Ecommerce Business Process Outsourcers. Our competitors in this category are integrated with U.S. retailer websites as we are, with landed cost calculation, payment management and logistics orchestration being core elements of the service, but with the international consumer generally having to leave the retailer’s website to complete the transaction. We compete primarily with this category of competitors by focusing on letting the retailer control the entire order life cycle without disintermediation, the protection of the prominence of the retailer’s brand at all times, the reliability and scalability of our platform, our comprehensive set of merchandising and pricing capabilities and reduced shipping and other transactional costs that we are able to take advantage of as a result of our scale, volume and customer relationships. |

• | Large Online Marketplaces Which Provide Retailers with International Logistics Support. Our competitors in this category offer expansive marketplaces for retailers to create storefronts within certain markets with access to consumers that have previously frequented or purchased through that marketplace. These marketplaces are generally localized and tailored to the respective markets. We compete with these competitors by maintaining our customer’s brand and logo throughout the international order lifecycle and allow our customers to control the consumer’s experience. |

We compete primarily on the basis of the comprehensiveness of our platform and services, our focus on the consumer experience and maintaining the retailer’s brand identity, our robust set of merchandising capabilities and features, the reliability and scalability of our platform, and the speed and cost of deploying our solution.

19

Intellectual Property and Proprietary Rights

Our intellectual property and proprietary rights are important to our business. To safeguard them, we rely on a combination of patent, copyright, trade secret, trademark and other rights in the United States and other jurisdictions, as well as confidentiality procedures and contractual provisions to protect our proprietary technology, processes and other intellectual property. We have one issued U.S. patent. We have confidentiality and license agreements with employees, contractors, customers, distributors and other third parties, which limit access to and use of our proprietary information and software. Though we rely in part upon these legal and contractual protections, we believe that factors such as the skills and ingenuity of our employees and the functionality and frequent enhancements to our solutions are larger contributors to our success in the marketplace.

Despite our efforts to preserve and protect our intellectual property and proprietary rights, unauthorized third parties may attempt to copy, reverse engineer, or otherwise obtain portions of our solutions. Competitors may attempt to develop similar products that could compete in the same market as our product. Unauthorized disclosure of our confidential information by our employees or third parties could occur. Laws of other jurisdictions may not protect our intellectual property and proprietary rights from unauthorized use or disclosure in the same manner as the United States. The risk of unauthorized use of our proprietary and intellectual property rights may increase as our company continues to expand outside of the United States.

Third-party infringement claims are also possible in our industry, especially as software functionality and features expand, evolve, and overlap with other industry segments. Third parties, including non-practicing patent holders, have from time to time claimed, and could claim in the future, that our activities or our customers’ ecommerce sites infringe patents they now hold or might obtain in the future, and, in most cases, we have agreed to indemnify our customers against claims that our products or the use of our products infringe the intellectual property rights of third parties. See “Risk Factors—We could be required to stop selling or using a product or service and/or incur substantial costs as a result of any claim of violation of another party’s intellectual property or proprietary rights.”

Employees

As of December 31, 2014 we had 231 employees of which 28 were in transaction processing, 53 were in technology and operations, 67 were in research and development, 45 were in sales and marketing and 38 were in general and administrative positions. None of our employees are covered by a collective bargaining agreement. We have never experienced a strike or similar work stoppage, and we consider our relations with our employees to be good.

Properties

Our principal corporate offices are located in New York, New York. We currently occupy three floors in New York approximating 28,000 square feet of space under an agreement that expires in November 2020. We occupy an additional leased facility, approximating 12,000 square feet of space, in Tel Aviv, Israel for our research and development operations. We also lease office space in Dublin, Ireland and Shanghai, China. We believe that our facilities are suitable for our current needs and that additional or substitute space will be readily available, on commercially reasonable terms, as needed to support the expansion of our business.

Legal Proceedings

We are subject to various legal proceedings that have arisen or may arise in the ordinary course of business. Although some of these proceedings may result in adverse decisions or settlements, we believe that the final disposition of such matters will not have a material effect on our business or consolidated financial statements. For information concerning our indemnification obligations to customers against which patent infringement claims have been or may be asserted, see “Risk Factors under Item 1A of this Annual Report on Form 10-K—We could be required to stop selling or using a product or service and/or incur substantial costs as a result of any claim of violation of another party’s intellectual property or proprietary rights.”

20

Available Information

We maintain an internet website at www.borderfree.com. The information on our website is not incorporated by reference into this Annual Report on Form 10-K and should not be considered to be a part of this Annual Report on Form 10-K. Our website address is included in this Annual Report on Form 10-K as an inactive technical reference only. Our reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, including our Annual Reports on Form 10-K, our Quarterly Reports on Form 10-Q and our Current Reports on Form 8-K, and amendments to those reports, are accessible through our website, free of charge, as soon as reasonably practicable after these reports are filed electronically with, or otherwise furnished to, the SEC. We also make available on our website the charters of our audit committee, compensation committee and nominating and corporate governance committee, as well as our corporate governance guidelines

21

ITEM 1A—Risk Factors

You should carefully consider the risks described below and the other information in this Annual Report on Form 10-K and in our other public filings. Our business, prospects, financial condition, or operating results could be harmed by any of these risks, as well as other risks not currently known to us or that we currently consider immaterial. If any of such risks and uncertainties actually occurs, our business, financial condition or operating results could differ materially from the plans, projections and other forward-looking statements included in the section titled "Management's Discussion and Analysis of Financial Condition and Results of Operations" and elsewhere in this report and in our other public filings. The trading price of our common stock could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

Risks Related to Our Business and Our Industry

We have incurred operating losses in recent fiscal periods and may be unable to sustain profitability, which may negatively impact our ability to achieve our business objectives.

We incurred operating losses in certain recent fiscal periods. We reported net loss of $3.1 million and $0.7 million for 2014 and 2013, respectively, however, we cannot assure you that we will be profitable in the future. As of December 31, 2014, our accumulated deficit was $19.5 million. We expect to continue to make future expenditures to develop and expand our business that may result in us incurring future losses. In addition, as a public company we will incur significant legal, accounting and other expenses that we did not incur as a private company. These increased expenditures will make it harder for us to sustain future profitability. Our recent growth in revenue and number of customers may not be sustainable, and we may not achieve sufficient revenue to maintain profitability if our growth slows or we lose customers or have customers reduce their sales volume on our platform. We may incur significant losses in the future for a number of reasons, including the other risks described in these Risk Factors, and we may encounter unforeseen expenses, difficulties, complications and delays and other unknown events. For example, one of our strategies is to substantially increase the number of carriers and logistics hubs. If we fail to manage growth and additional complexity in our logistics network, our ability to reduce our fulfillment costs and increase sales conversion could be adversely affected. Additionally, we may experience fluctuations in foreign currencies which could reduce cross-border trade which in turn could adversely affect the sales volume on our platform. Accordingly, we may not be able to maintain profitability and we may incur significant losses for the foreseeable future.

Our limited history as a comprehensive global ecommerce platform makes it difficult to evaluate our current business and future prospects.

In 2008, we changed our business and began offering a comprehensive solution that allows U.S. retailers to transact with consumers worldwide. We have a limited operating history with respect to our current business, which may make it difficult for you to evaluate our current business and our future prospects. For example, the results for the set of customers that we launch each year inherently reflect a distinct group of retailers and consumers and may not be representative of our current or future composite group of retailers and consumers, particularly as we grow and our customer base broadens. In addition, the results for each such customer cohort may reflect unique market and consumer dynamics during the periods covered and may not be indicative of the future performance of such cohort or other cohorts. In recent periods we have experienced significant growth, and have encountered, and will continue to encounter, risks and difficulties frequently experienced by growing companies in rapidly changing industries, including increasing and unforeseen expenses as we continue to grow our business. If we do not manage these risks successfully, our business may be adversely impacted.

22

We depend on a limited number of customers for a substantial portion of our revenue. The loss of a key customer or the significant reduction of business from our largest customers could significantly reduce our revenue.

We have derived, and we believe that we will continue to derive, a substantial portion of our revenue from a limited number of customers, many of whom can terminate their agreements with us upon 30 to 90 days prior written notice. For example, for the year ended December 31, 2014 transactions with our largest ten customers accounted for an aggregate of approximately 67% our global ecommerce revenue. No individual customer accounted for more than 10% of our total revenue for the years ended December 31, 2014, 2013 and 2012. Additionally, transactions with our top three customers generated approximately 26% of our global ecommerce revenue for the year ended December 31, 2014, approximately 27% for the year ended December 31, 2013 and approximately 31% for the year ended December 31, 2012.

Because the primary driver of global ecommerce services and fulfillment services revenue are the international cross-border sales processed through our platform, our total revenue is dependent on a relatively small number of customers and their end consumers who will continue to account for a significant portion of our revenue for the foreseeable future. As a result, our operating results for the foreseeable future will continue to depend on our ability to provide our ecommerce solutions to this small number of customers. Any revenue growth will depend on our success in retaining our customers, growing our customers’ sales processed on our platform and acquiring additional customers. The loss of one or more of our customers, particularly the loss of any of our larger customers, whether through change in customer strategy, acquisitions, consolidations, bankruptcies, terminations for convenience or otherwise, or the failure to retain a significant amount of business from our customers, could harm our business, growth prospects, operating results and financial condition.

If we are unable to retain our existing customers, or the sales volumes generated by them on our platform decline, or does not increase, our business, operating results and financial condition would be adversely affected.

Our customer contracts typically have initial multi-year terms ranging from one to four years, followed by one-year renewal periods. We generate a significant portion of revenue from fees paid to us by our customers based on a percentage of their total gross international sales revenue processed through our platform. We also generate revenue from consumers for fulfillment services, including revenue related to international shipping, handling, and other efforts associated with delivering global logistics services, and foreign exchange and other transaction related fees. These contributors to our revenue are driven by international ecommerce sales generated on our platform.

Our customers often have the right to terminate their agreements for convenience by providing 30 to 90 days prior written notice, and have no obligation to renew their agreements with us after their terms expire. Even if these agreements are renewed, they may not be renewed on the same or on more profitable terms. We expect to continue to derive a significant portion of our revenue from our existing customers’ total sales on our platform and we expect our future revenue growth to be driven by increases in our existing customers’ sales. Despite such expectations, we cannot guarantee that our customers process a minimum volume of sales using our ecommerce solutions. As a result, if existing customers terminate their agreements with us, elect to operate their cross-border trading in certain markets by setting up local operations, do not renew their agreements with us, renew on less favorable terms, do not generate their current volume of sales using our solutions, or demand a fixed pricing per transaction model, our operating results and financial condition will suffer. In addition, the rate at which our customers increase their sales volumes on our platform, and the rate at which new customers adopt our ecommerce solutions is critical to our future growth. Factors that may affect sales volumes processed on our platform, and the adoption rate for our solution include:

• | the price, performance and functionality of our solutions; |

• | the availability, price performance and functionality of competing solutions; |

• | the effectiveness of our logistics and customer support services; |

• | the degree and the rate to which our customers adopt our marketing programs and solutions to drive additional traffic to their ecommerce sites; and |

• | the strengthening of the U.S. dollar against other currencies, which may affect international end consumers' ability or willingness to purchase our customers' products |

23

If our efforts to attract new customers are not successful, our revenue growth will be adversely affected, and the new customers we do attract may not generate revenue comparable to our current or historical customers.

One of our growth strategies is to acquire new customers. There is no guarantee that we can sustain our historical acquisition rates. Our ability to attract new customers will depend in large part on the success of our sales and marketing efforts, which may not be successful. Our prospective customers may not be familiar with our solution, or may have traditionally used other products and services for their international ecommerce needs. Our prospective customers may develop their own solutions to address their international ecommerce needs, purchase competitive product offerings, or engage third-party providers of services that do not use our solution to provide their services. In addition, attracting new customers requires substantial time and expense. It may be difficult to identify, engage and market to customers who do not currently have ecommerce needs or are unfamiliar with our solution, and many of our customers typically require input from one or more internal levels of approval. This requires us to spend substantial time and effort assisting potential customers in evaluating our solution including providing demonstrations. If our prospective customers do not perceive our solution to be of sufficiently high value and quality, we may not be able to attract new customers and our business, operating results and financial condition would be adversely affected. Additionally, even if we are successful in attracting new customers, such new customers may not generate comparable revenue relative to our current or historical customers, which could materially adversely affect our operating results and our growth.

24

Fluctuations in exchange rates of foreign currencies, which may reduce cross-border trade, could harm our business.

International sales generated by our customers processing transactions through our platform are the primary source of both revenue and profit for us. The operating results of, and sales generated from, many of our customers’ internationally focused websites running on our platform are exposed to foreign exchange rate fluctuations. For example, for a U.S. retailer running on our platform, if the U.S. dollar weakens against foreign currencies, the translation of the prices of the retailer’s products into foreign currency denominated transactions would decrease, which may result in increased international sales volumes, revenue and net income for us. Conversely, to the extent the U.S. dollar strengthens against foreign currencies, as experienced in 2014 with the Canadian dollar, Australian dollar, euro and Russian Ruble, and in 2013 with the Australian dollar and the Japanese yen, cross-border trade related to purchases of dollar-denominated goods from our U.S.-based retailers running on our platform by non-U.S. purchasers will likely decrease, which would adversely affect our business, operating results and financial condition. As exchange rates in foreign currencies vary, our net revenue and other operating results may differ materially from expectations. For example, during the second half of 2014, our sales volumes were negatively impacted by the U.S. dollar which strengthened against most major currencies, including the Canadian dollar and Australian dollar, our two largest individual markets in terms of international sales volumes. In addition, if the U.S. dollar continues to strengthen against major currencies (for example, the Canadian dollar, Australian dollar, euro and pound sterling), due to worsening economic conditions, divergence in monetary policies or for any other reasons, our revenue and operating results would be adversely impacted.

Our operating results are subject to seasonal fluctuations that could adversely affect the market price of our common stock.

Our business is seasonal in nature and the fourth quarter is a significant period for our operating results due to the holiday season. In 2014, 2013 and 2012, fourth quarter revenue represented approximately 29%, 32% and 36% of our total annual revenue, respectively. As a result, revenue and income (loss) from operations generally decline (increase) in the first quarter sequentially from the fourth quarter of the previous year.

Any disruption in our ability to process and fulfill consumer orders in the fourth quarter could have a negative effect on our quarterly and annual operating results. For example, if a large number of end consumers access our customers’ websites that operate on our platform in a short period of time due to increased holiday demand, we may experience system interruptions that prevent us from efficiently fulfilling orders, which may reduce the volume of goods we sell through, and the attractiveness of, our platform. In addition, we may experience an increase in our net shipping cost due to complimentary upgrades, split-shipments, and additional long-zone shipments necessary to ensure timely delivery for the holiday season. Additionally, any disruption in our business operations or the operations of our customers or logistics providers or other factors that could lead to a material shortfall compared with our expectations for the fourth quarter could result in a significant shortfall in revenue and operating cash flows for the full year.

If we do not successfully optimize and operate our logistics network, our business and growth strategy could be harmed.

The cost of shipping is one of the largest obstacles to a global consumer completing an online purchase. An important part of our strategy is to improve order submit rates through our efficiencies and cost reductions via improvements and expansion of our logistics and distribution infrastructure and our supply chain. As part of this strategy, we intend to continue reducing the cost of logistics by expanding the number of hubs and carriers in our logistics network. As we continue to expand the number of hubs and carriers, our logistics network will become increasingly complex and operating it may become more challenging. If one or more service providers in our logistics network on whom we rely fail to perform adequately, our ability to optimize and operate our logistics network will be impaired. If we are unsuccessful in continuing to optimize and operate, our logistics network, our fulfillment costs, operating results, financial condition and growth prospects will be adversely affected.

25

If we experience delays in the customer implementation process, it could delay our ability to recognize revenue, increase our costs and otherwise negatively impact our business.

In the initial stage of implementation our ecommerce solution is configured and integrated based on the customer’s needs. It may be difficult for us to manage the timeliness of these implementations and the allocation of personnel and resources by us or our customers. If our infrastructure capacity is insufficient to meet our needs, we may experience delays in deploying our solution to new customers, or expanding the solutions we offer to existing customers. We do not recognize significant revenue from customers until their ecommerce solution is launched. If the launch of our solution with a new customer is delayed or an expansion of our solution with an existing customer is delayed due to complications in the implementation process caused by us or our customers, our recognition of revenue for the deployment or expansion with such customer will be delayed. Therefore, failure to successfully manage customer implementations could result in a delay in our ability to recognize revenue. In the past, delays in customer implementation have also resulted in unexpected variances in our results. Delays in implementation could also increase costs, harm our reputation, cause us to lose existing customers, lead to potential customer disputes or limit the adoption rate of our solutions, and our business, operating results and financial condition could be materially and adversely affected.

26

Our lengthy sales cycle makes it difficult to predict our future revenue and causes variability in our operating results.