Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - PASSPORT POTASH INC | Financial_Report.xls |

| EX-32.1 - EXHIBIT 32.1 - PASSPORT POTASH INC | exhibit32-1.htm |

| EX-31.2 - EXHIBIT 31.2 - PASSPORT POTASH INC | exhibit31-2.htm |

| EX-31.1 - EXHIBIT 31.1 - PASSPORT POTASH INC | exhibit31-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

FORM 10-Q

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended November 30, 2014

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____ to _____

Commission File Number: 000-54751

PASSPORT POTASH INC.

(Exact name of small business issuer as specified in its charter)

| British Columbia, Canada | Not Applicable |

| (State or other jurisdiction of incorporation or | (I.R.S. Employer Identification No.) |

| organization) | |

| 608 – 1199 West Pender Street | |

| Vancouver, BC, Canada | V6E 2R1 |

| (Address of principal executive offices) | (Zip Code) |

(604) 687-0300

Registrant’s telephone number,

including area code

N/A

(Former name, former address and former

fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all

reports required to be filed by Section 13 or 15(d) of the Exchange Act of

1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

Yes

[X] No [ ]

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files).

Yes

[X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] (do not check if a smaller reporting company) | Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell

company (as defined in Rule 12b-2 of the Exchange Act).

Yes [

] No [X]

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date. 109,490,859 shares of common stock as of January 15, 2015.

2

PASSPORT POTASH INC. AND SUBSIDIARY

Quarterly Report On Form 10-Q

For The Quarterly

Period Ended

November 30, 2014

INDEX

3

FORWARD-LOOKING STATEMENTS

This quarterly report on Form 10-Q contains forward-looking statements that involve risks and uncertainties. Any statements contained herein that are not statements of historical fact may be deemed to be forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “may”, “will”, “should”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “predict”, “potential” or “continue”, the negative of such terms or other comparable terminology. In evaluating these statements, you should consider various factors, including the assumptions, risks and uncertainties outlined in our annual report on Form 10-K for the fiscal year ended February 28, 2014 filed with the Securities and Exchange Commission (the “SEC”) on June 13, 2014, this quarterly report on Form 10-Q, and, from time to time, in other reports that we file with the SEC. These factors or any of them may cause our actual results to differ materially from any forward-looking statement. Given these uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. Forward-looking statements in this quarterly report include, among others, statements regarding:

- our capital needs;

- business plans; and

- expectations.

While these forward-looking statements, and any assumptions upon which they are based, are made in good faith and reflect our current judgment regarding future events, our actual results will likely vary, sometimes materially, from any estimates, predictions, projections, assumptions or other future performance suggested herein. Some of the risks and assumptions include:

- our need for additional financing;

- our limited operating history;

- our history of operating losses;

- our exploration activities may not result in commercially exploitable quantities of potash on our current or any future mineral properties;

- the risks inherent in the exploration for minerals such as geologic formation, weather, accidents, equipment failures and governmental restrictions;

- the competitive environment in which we operate;

- changes in governmental regulation and administrative practices;

- our dependence on key personnel;

- conflicts of interest of our directors and officers;

- our ability to fully implement our business plan;

- our ability to effectively manage our growth; and

- other regulatory, legislative and judicial developments.

We advise the reader that these cautionary remarks expressly qualify in their entirety all forward-looking statements attributable to us or persons acting on our behalf. Important factors that you should also consider, include, but are not limited to, the factors discussed under “Risk Factors” in our annual report on Form 10-K for the fiscal year ended February 28, 2014 filed with the SEC on June 13, 2014.

The forward-looking statements in this quarterly report are made as of the date of this quarterly report and we do not intend or undertake to update any of the forward-looking statements to conform these statements to actual results, except as required by applicable law, including the securities laws of the United States.

4

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

The following unaudited interim consolidated financial statements of Passport Potash Inc. (sometimes referred to as “we”, “us” or “our Company”) are included in this quarterly report on Form 10-Q:

It is the opinion of management that the unaudited interim consolidated financial statements for the three and nine months ended November 30, 2014 and 2013 include all adjustments necessary in order to ensure that the unaudited interim consolidated financial statements are not misleading. These unaudited interim financial statements reflect all adjustments which are, in the opinion of management, necessary to present fairly the financial position, results of operations and cash flows for the interim periods presented in accordance with accounting principles generally accepted in the United States of America. Except where noted, these unaudited interim consolidated financial statements follow the same accounting policies and methods of their application as our Company’s audited annual financial statements for the year ended February 28, 2014. All adjustments are of a normal recurring nature. These unaudited interim consolidated financial statements should be read in conjunction with our Company’s audited annual consolidated financial statements as of and for the year ended February 28, 2014.

5

Passport Potash Inc.

Consolidated Financial Statements

Nine months Ended November 30, 2014

Expressed in United States Dollars

(Unaudited)

| Passport Potash Inc. |

| Consolidated Balance Sheets |

| (Expressed in United States dollars) |

| Notes | November 31, | February 28, | |||||||

| 2014 | 2014 | ||||||||

| ASSETS | (unaudited) | ||||||||

| Current assets | |||||||||

| Cash | $ | 2,344 | $ | 49,062 | |||||

| Receivables | 11,671 | 4,853 | |||||||

| Prepaid expenses | 31,254 | 113,554 | |||||||

| Deferred issuance costs | 5,472 | 3,598 | |||||||

| Total current assets | 50,741 | 171,067 | |||||||

| Equipment | 2 | 561 | 660 | ||||||

| Unproven mineral properties | 3 | 1,600,000 | 1,600,000 | ||||||

| Reclamation deposits | 3 | 15,000 | 15,000 | ||||||

| Total non-current assets | 1,615,561 | 1,615,660 | |||||||

| TOTAL ASSETS | $ | 1,666,302 | $ | 1,786,727 | |||||

| LIABILITIES | |||||||||

| Current liabilities | |||||||||

| Trade payables and accrued liabilities | 6 | $ | 1,990,969 | $ | 980,983 | ||||

| Convertible debentures | 4 | - | 553,233 | ||||||

| Convertible debentures – subscriptions received | 4 | 112,250 | 95,000 | ||||||

| Derivative liability | 8 | 2,006 | 42,007 | ||||||

| Loans | 5 | 375,882 | 546,242 | ||||||

| Total current liabilities | 2,481,107 | 2,217,465 | |||||||

| Convertible debentures | 4 | 6,226,045 | 5,000,889 | ||||||

| Total non-current liabilities | 6,226,045 | 5,000,889 | |||||||

| TOTAL LIABILITIES | 8,707,152 | 7,218,354 | |||||||

| STOCKHOLDERS’ DEFICIENCY | |||||||||

| Common stock – Unlimited authorized without par value | 7 | 35,569,788 | 35,032,933 | ||||||

| Additional paid-in capital | 17,073,970 | 16,922,064 | |||||||

| Accumulated deficit | (59,684,608 | ) | (57,386,624 | ) | |||||

| TOTAL STOCKHOLDERS’ DEFICIENCY | (7,040,850 | ) | (5,431,627 | ) | |||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ DEFICIENCY | $ | 1,666,302 | $ | 1,786,727 |

Commitments and contingencies (Notes 1 and 3)

Subsequent

events (Note 10)

On behalf of the Board of Directors:

| “Joshua Bleak” | ”John

Eckersley” |

|

| Director |

Director |

| See accompanying notes to the consolidated financial statements | F-2 |

| Passport Potash Inc. |

| Consolidated statement of operations - unaudited |

| (Expressed in United States dollars) |

| Nine months periods | |||||||||||||

| Three months periods ended | ended | ||||||||||||

| November | November 30, | November | November 30, | ||||||||||

| Note | 30, 2014 | 2013 | 31, 2014 | 2013 | |||||||||

| Operating Expenses | |||||||||||||

| Administration | 6 | $ | 12,657 | $ | 15,036 | $ | 41,757 | $ | 100,496 | ||||

| Advertising | 3,093 | 11,201 | 13,854 | 83,744 | |||||||||

| Business development | 31,206 | 48,292 | 56,811 | 288,777 | |||||||||

| Consulting fees | 6 | 37,500 | 227,741 | 187,500 | 558,716 | ||||||||

| Depreciation | 2 | 33 | 41 | 99 | 123 | ||||||||

| Foreign exchange loss | (18,245 | ) | (9,912 | ) | 13,997 | 9,393 | |||||||

| Investor relations | 21,514 | 72,963 | 81,771 | 213,653 | |||||||||

| Management fees | 6 | 160,409 | 163,123 | 482,784 | 575,238 | ||||||||

| Mineral property impairment | - | - | - | - | |||||||||

| Mineral property option payments and exploration costs | 3, 6 | 88,712 | 323,603 | 450,184 | 1,399,961 | ||||||||

| Office and miscellaneous | 17,433 | 25,545 | 36,801 | 60,915 | |||||||||

| Professional fees | 24,605 | 18,779 | 58,165 | 294,636 | |||||||||

| Property investigation costs | - | - | - | - | |||||||||

| Transfer agent and filing fees | 6,706 | 19,058 | 44,363 | 78,158 | |||||||||

| (385,623 | ) | (915,470 | ) | (1,468,086 | ) | (3,663,810 | ) | ||||||

| Other items | |||||||||||||

| Accretion expense | 4 | (103,008 | ) | (1,035,052 | ) | (312,777 | ) | (3,111,452 | ) | ||||

| Change in fair value of | |||||||||||||

| derivative liability | 8 | 2,725 | 54,711 | 40,001 | 1,566,224 | ||||||||

| Interest income | - | - | - | - | |||||||||

| Interest expense on convertible debentures | 4 | (158,521 | ) | (216,363 | ) | (557,122 | ) | (649,310 | ) | ||||

| Gain (loss) on debt settlement | - | - | - | - | |||||||||

| Other income | - | - | - | - | |||||||||

| (258,804 | ) | (1,196,704 | ) | (829,898 | ) | (2,194,538 | ) | ||||||

| Net loss | $ | (644,427 | ) | $ | (2,112,174 | ) | $ | (2,297,984 | ) | $ | (5,858,348 | ) | |

| Loss per share – basic and diluted | $ | (0.01 | ) | $ | (0.02 | ) | $ | (0.02 | ) | $ | (0.06 | ) | |

| Weighted average number of shares outstanding– basic and diluted |

109,490,859 | 91,809,694 | 109,096,633 | 91,802,397 | |||||||||

| See accompanying notes to the consolidated financial statements | F-3 |

Passport Potash Inc.

Consolidated statement of

stockholders’ deficiency - Unaudited

(Expressed in United States dollars)

| Common Stock | |||||||||||||||

| Number of | Additional Paid-in | Accumulated | |||||||||||||

| shares | Amount | Capital | Deficit | Total | |||||||||||

| Balance at February 28, 2014 | 105,651,157 | $ | 35,032,933 | $ | 16,922,064 | $ | (57,386,624 | ) | $ | (5,431,627 | ) | ||||

| Net loss | - | - | - | (2,297,984 | ) | (2,297,984 | ) | ||||||||

| Rounding upon stock split | 140 | - | - | - | - | ||||||||||

| Shares issued for convertible debentures exercised | 3,839,562 | 460,748 | - | - | 460,748 | ||||||||||

| Amount allocated to share purchase warrants on re- issuance of debenture | - | - | 75,953 | - | 75,953 | ||||||||||

| Amount allocated to beneficial conversion feature on re- issuance of debenture | - | - | 75,953 | - | 75,953 | ||||||||||

| Accretion of discount for future periods on exercised convertible debentures | - | 58,052 | - | - | 58,052 | ||||||||||

| Accretion of beneficial conversion feature for future periods on exercised convertible debentures | - | 18,055 | - | - | 18,055 | ||||||||||

| Balance at November 30, 2014 | 109,490,859 | $ | 35,569,788 | $ | 17,073,970 | $ | (59,684,608 | ) | $ | (7,040,850 | ) | ||||

| See accompanying notes to the consolidated financial statements | F-4 |

| Passport Potash Inc. |

| Consolidated statements of cash flows - unaudited |

| (Expressed in United States dollars) |

| Nine month period ended | ||||||

| November 30, | November 30, | |||||

| 2014 | 2013 | |||||

| Operating activities | ||||||

| Net loss | $ | (2,297,984 | ) | $ | (5,858,348 | ) |

| Adjustments for: | ||||||

| Accretion | 312,777 | 3,111,452 | ||||

| Amortization of deferred issuance costs | 1,449 | 29,533 | ||||

| Depreciation | 99 | 123 | ||||

| Interest expense on convertible debentures | 557,122 | 649,310 | ||||

| Fair value adjustment on warrants | (40,001 | ) | (1,566,224 | ) | ||

| Foreign exchange | - | - | ||||

| Loss on debt settlement | - | - | ||||

| Mineral property impairment | - | - | ||||

| Mineral property option payments - shares | - | - | ||||

| Other income | - | - | ||||

| Stock-based compensation | - | 368,905 | ||||

| Changes in non-cash working capital items: | ||||||

| Receivables | (6,818 | ) | 37,618 | |||

| Injunction bond | - | 350,000 | ||||

| Prepaid expenses | 82,300 | 149,501 | ||||

| Trade payables and accrued liabilities | 1,005,196 | 546,010 | ||||

| Net cash flows used in operating activities | (385,860 | ) | (2,182,120 | ) | ||

| Investing activities | ||||||

| Reclamation deposits | - | - | ||||

| Long term deposits | - | - | ||||

| Mineral property acquisition costs | - | - | ||||

| Net cash flows used in investing activities | - | - | ||||

| Financing activities | ||||||

| Debentures - net of issue costs | 296,677 | 132,505 | ||||

| Proceeds on issuance of common shares - | ||||||

| net of issue costs | - | 8,157 | ||||

| Proceeds from Loans | 29,965 | 500,728 | ||||

| Subscriptions received | 12,500 | - | ||||

| Net cash flows from financing activities | 339,142 | 641,390 | ||||

| Decrease in cash | (46,718 | ) | (1,540,730 | ) | ||

| Cash, beginning | 49,062 | 1,643,771 | ||||

| Cash, ending | $ | 2,344 | $ | 103,041 | ||

| Supplemental disclosures: | ||||||

| Cash paid for: | ||||||

| Income tax | $ | - | $ | - | ||

| Interest | $ | - | $ | - | ||

See Note 9 for non-cash transactions.

| See accompanying notes to the consolidated financial statements | F-5 |

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 1 – ORGANIZATION AND BASIS OF PRESENTATION

Passport Potash Inc. (the “Company”) was incorporated on August 11, 1987. The Company’s corporate jurisdiction is the province of British Columbia, Canada. The Company is engaged in the acquisition and exploration of mineral properties. The Company’s shares are listed on the TSX-Venture Exchange (“TSX-V”).

The unaudited consolidated financial statements included herein have been prepared in accordance with accounting principles generally accepted in the United States for interim financial information and with the instructions to Form 10-Q and Regulation S-X. They do not include all information and notes required by generally accepted accounting principles for complete financial statements. However, except as disclosed herein, there has been no material change in the information disclosed in the notes to the financial for the year ended February 28, 2014. In the opinion of management, all adjustments (including normal recurring accruals) considered necessary for a fair presentation have been included. Operating results for the nine months ended November 30, 2014, are not necessarily indicative of the results that may be expected for any other interim period or the entire year. For further information, these unaudited consolidated financial statements and the related notes should be read in conjunction with the Company’s audited consolidated financial statements for the year ended February 28, 2014 included in the Company’s Form 10-K.

The Company’s unaudited consolidated financial statements are prepared on a going concern basis in accordance with US generally accepted accounting principles (“GAAP”) which contemplates the realization of assets and discharge of liabilities and commitments in the normal course of business. The Company is in the exploration stage. It has not generated operating revenues to date, and has accumulated losses of $59,684,608 since inception. The Company has funded its operations through the issuance of capital stock and debt. In the longer term, the Company will also need to repay outstanding convertible debentures if these are not converted which have a maturity date of August 19, 2016. At November 30, 2014, the Company had cash of $2,344 and a working capital deficit of $2,430,366. Management plans to raise additional funds through equity and/or debt financings. There is no certainty that further funding will be available as needed. These factors raise substantial doubt about the ability of the Company to continue operating as a going concern. The Company’s ability to continue its operations as a going concern, realize the carrying value of its assets, and discharge its liabilities in the normal course of business is dependent upon its ability to raise new capital sufficient to fund its commitments and ongoing losses, and ultimately on generating profitable operations.

NOTE 2 – EQUIPMENT

| Equipment | |||

| Cost: | |||

| At November 30, 2014 and February 28, 2014 | $ | 34,527 | |

| Depreciation: | |||

| At February 28, 2014 | $ | 33,867 | |

| Charge for the period | 99 | ||

| At November 30, 2014 | $ | 33,966 | |

| Net book value: | |||

| At February 28, 2014 | $ | 660 | |

| At November 30, 2014 | $ | 561 |

F-6

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 3 – UNPROVEN MINERAL PROPERTIES

Holbrook Basin Project

| November | February 28, | February 28, | |||||||||||||

| 30, 2014 | Additions | 2014 | Additions | 2013 | |||||||||||

| Property acquisition costs | |||||||||||||||

| $ | |||||||||||||||

| Cash paid for property | $ | 1,600,000 | $ | - | $ | 1,600,000 | - | $ | 1,600,000 | ||||||

| Option payments and exploration costs | |||||||||||||||

| Assay | $ | 309,680 | $ | - | $ | 309,680 | $ | 26,603 | $ | 283,077 | |||||

| Drilling and related costs | 8,992,677 | 12,843 | 8,979,834 | 456,640 | 8,523,194 | ||||||||||

| Geological consulting | 3,410,707 | 162,000 | 3,248,707 | 757,676 | 2,491,031 | ||||||||||

| License and filing | 700,208 | 55,558 | 644,650 | 200,974 | 443,676 | ||||||||||

| Option payments | 6,362,855 | - | 6,362,855 | - | 6,362,855 | ||||||||||

| Project administration | 3,380,604 | 219,783 | 3,160,821 | 482,375 | 2,678,446 | ||||||||||

| Recovery | (112,668 | ) | - | (112,668 | ) | - | (112,668 | ) | |||||||

| $ | 23,044,063 | $ | 450,184 | $ | 22,593,879 | $ | 1,924,268 | $ | 20,669,611 |

The Company acquired mineral claims in the Holbrook Basin Project through the following agreements:

South West Exploration Property, Arizona

On

September 30, 2008, as amended, the Company entered into an option agreement to

purchase 100% of certain mining claims located in the Holbrook Basin region of

Arizona, USA. In terms of the Southwest Option Agreement, the Company:

- made cash payments of $575,000 in stages;

- issued 1,000,000 share purchase options with a fair value of $61,152;

- issued 8,181,000 shares in stages with a fair value of $551,921; and

- incurred property expenditures of $200,000.

During the year ended February 29, 2012, the Company purchased the 1% Net Smelter Royalty (“NSR”) for $1 million. The Company now owns a 100% interest, with no NSR, in the South West Exploration Property.

At November 30, 2014, the Company had a reclamation bond of $15,000 (February 28, 2014: $15,000) for work done on the South West Exploration Property.

Twin Butte Ranch Property, Arizona

On August 28,

2009, as amended, the Company entered into a four year lease with an option to

purchase private deeded land within the Holbrook Basin. Under the terms of the

agreement the Company can earn a 100% undivided interest in the deeded land and

sub-surface mineral rights by making lease payments totaling $1,250,000 over

five and a half years and, upon exercising its option to purchase, by paying

$20,000,000 for the entire Twin Butte Ranch including all sub-surface mineral

rights except those pertaining to oil and gas, petrified wood and geothermal

resources. There are no royalties associated with the sub-surface mineral

rights.

F-7

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 3 – UNPROVEN MINERAL PROPERTIES (Cont’d)

Twin Butte Ranch Property, Arizona (cont’d)

Details of the payments under the agreement are as follows:

| a) | A payment of $50,000 and $10,000 legal costs on or before November 26, 2009 (paid); |

| b) | A payment of $25,000 on September 17, 2010 (paid); |

| c) | A payment of $75,000 on December 1, 2010 (paid); |

| d) | A payment of $150,000 on August 28, 2011 (paid); |

| e) | A payment of $200,000 on August 28, 2012 (paid); |

| f) | A payment of $250,000 on earlier of December 1, 2013 or within thirty days of closing a financing of at least $5,000,000 (not paid); |

| g) | A payment of $250,000 on August 28, 2014 (not paid); and |

| h) | A payment of $250,000 on May 1, 2015. |

The Company has not made the required $250,000 payments that were due on December 1, 2013 and August 28, 2014; therefore, there are past-due payment obligations. On April 17, 2014, the Company was served a notice of breach that it did not remedy within 30 days. The optionor may now terminate the option at their discretion.

The lease agreement and purchase option will expire on January 6, 2016 or such other time as is mutually acceptable and agreed to in writing by both parties.

Sweetwater/American Potash Property, Arizona

On

November 12, 2010, the Company entered into an option agreement to acquire 100%

of the right, title and interest in exploration permits within the Holbrook

basin region of Arizona, USA. In terms of the Sweetwater/American Potash option

agreement, the Company:

- made cash payments of $90,000 in stages;

- issued 500,000 shares of the Company with a fair value of $130,444; and

- paid all taxes and exploration work to keep the claims in good standing.

During the year ended February 28, 2013, the Company purchased the 2% NSR for $300,000. The Company now has a 100% interest, with no NSR, in the Sweetwater/American Potash Property.

Mesa Uranium, Arizona

On August 31, 2010, the

Company entered into an agreement to acquire 100% undivided interest in

exploration permits within the Holbrook basin region of Arizona, USA. In terms

of the Mesa Uranium option agreement, the Company:

- made cash payments of $20,000;

- issued 500,000 shares of the Company with a fair value of $40,625;

- competed $119,518 exploration expenditures in 2010; and

- obtained the maximum available assessment work credits or payments in lieu of the minimum requirements to keep the claims in good standing.

During the year ended February 29, 2012, the Company purchased the 2% NSR for $300,000. The Company now has a 100% interest, with no NSR, in the Mesa Property.

F-8

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 3 – UNPROVEN MINERAL PROPERTIES (Cont’d)

Ringbolt Property, Arizona

On March 28, 2011 the Company entered into an option agreement to acquire 90% undivided legal and beneficial interest in and to the Ringbolt Property free and clear of all encumbrances in exploration leases for the following consideration:

a)

$50,000 upon execution of the agreement (paid);

b) $250,000 upon

TSX-V approval on May 17, 2011 (paid) and 1,000,000 common shares (issued with a

fair value of $669,384);

c) Minimum

exploration expenditures within 1 year of TSX-V approval of $500,000

(completed);

d)

On or before the first anniversary of TSX-V approval $350,000 and 1,400,000

common shares (see

below);

e)

Minimum exploration expenditures within first year of first anniversary of TSX-V

approval of $750,000;

f) $350,000 upon

second anniversary of TSX-V approval and 1,600,000 common shares; and

g) Minimum

exploration expenditures within 1 year of second anniversary of TSX-V approval

of $1,000,000.

On completion of all terms above, the Company shall have earned a 90% interest and title of the permits shall be transferred to the Company. Upon exercise of the option agreement, the Company shall be deemed to be granted an option to purchase the remaining 10% interest in the Property for the payment of $5,000,000.

The Company paid a finder’s fee of $25,825 to a third party in connection with this option agreement.

During the year ended February 28, 2013, the Company became the subject to a civil action in the Third Judicial District court, Salt Lake County, State of Utah in connection with the Ringbolt Property option agreement. The optionors were seeking payment of $350,000, 1,400,000 of the Company’s shares and $20,716 in expenses related to the property, alternatively damages of $644,000. The Company did not make the required payment and did not issue the shares to the optionors as it contended that the optionors were in default of the option agreement. The Company counter claimed for specific performance under the option agreement and paid the $350,000 and issued the 1,400,000 shares into the Utah court.

The court ruled that tender to the court was not sufficient; therefore, the cash and shares were released to the optionors on July 10, 2012. The fair value of the 1,400,000 shares was $271,936. The Company deposited a bond in the amount of $350,000 with the Court as security for the preliminary injunction, which was disclosed on the balance sheet as an injunction bond. During the year ended February 28, 2014, the injunction bond was returned to the Company. On September 10, 2012, the court granted the motion for a preliminary injunction, which enjoined the optionors from terminating the Ringbolt option agreement based upon the grounds alleged by the optionors.

On October 30, 2012 the Company entered into an amended option agreement (the “Amendment Agreement”) to acquire 100% undivided legal and beneficial interest in and to the Ringbolt Property, free and clear of all encumbrances in exploration leases, according to the following terms:

| 1. | The Company will pay to the optionors a total of $3,850,000 according to the following schedule: |

| a) | $150,000 upon execution of the Amendment Agreement (paid); |

| b) | $2,450,000 upon TSX-V approval (paid); and |

| c) | $1,250,000 on or before October 31, 2014 (not paid). |

| 2. | The Company issue 750,000 common shares to the optionors upon TSX-V approval (issued with a fair value of $168,291). |

F-9

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 3 – UNPROVEN MINERAL PROPERTIES (Cont’d)

Ringbolt Property, Arizona (Cont’d)

| 3. | Upon written notice from the TSX-V that the Amendment Agreement has been approved, the parties shall simultaneously do the following: |

| a) | The optionors shall assign all of their right, title, and interest in and to the Ringbolt Property and will take all necessary action with the Arizona State Land Department to effect such assignment (completed); and |

| b) | The Company will place into escrow on behalf of the optionors the $2,450,000 cash payment and the 750,000 common shares (issued with a fair value of $168,291) of the Company. The cash payment and shares will be released to the optionors upon receipt of confirmation of the assignment of the Ringbolt Property to the Company (completed). |

| 4. | There will be no royalty attached to the transferred permits. |

| 5. | Should the Company sell or in any way transfer its interest in the Ringbolt Property, the optionors will receive a bonus payment in accordance with the following schedule: |

| a) | If the Company receives less than $30 million for the transaction, then no bonus payment shall be payable; |

| b) | If the Company receives greater than $30 million but less than $40 million the optionors would receive 20% of the gross consideration in excess of $30 million; |

| c) | If the Company receives greater than $40 million but less than $50 million the optionors would receive $2,000,000 plus 10% of the gross consideration in excess of $40 million, to a maximum of $1,000,000; or |

| d) | If the Company receives greater than $50 million the optionors would receive $3,000,000 plus 20% of the gross consideration received in excess of $50 million. |

Based upon the foregoing, the parties have agreed to a mutual release and settlement of any claims and causes of action between the parties as of the date of the Amended Agreement.

On December 8, 2012, the Company entered into a second amendment to the option agreement to acquire 100% of the Ringbolt Property. The amendment stipulates that in the event that the cash payment of $2,450,000 following TSX-V approval of the Amendment Agreement is delayed, the parties agree to extend the payment deadline for a period of 30 days from the date of final approval from the TSX-V with the payment of $100,000 to one of the optionors with this extension payment to be deducted from the $2,450,000 payment due following TSX-V approval. A payment of $100,000 was made to the optionor on December 20, 2012 and the balance of $2,350,000 on 28 February 2013.

On October 20, 2014, the Company provided formal written notice to the Optionors that it was abandoning the option granted to it in the option agreement. Therefore, the Company has no further obligations to make any option payments.

Cooperative Agreement and Joint Exploration Agreement

(“JEA”) with the Hopi Tribe

Effective November 1, 2012, the Company and

The Hopi Tribe, a federally recognized Indian Tribe, entered into a Joint

Exploration Agreement (the “JEA”) pursuant to which the parties agree to explore

the Hopi land sections (the “Hopi Property”) which are checker-boarded with the

Company’s southern landholdings in accordance with an exploration program.

Under the JEA, the Company is responsible for all costs, charges and expenses incurred in connection with the exploration program.

The JEA automatically terminated at 5:00 PM Arizona time on October 15, 2014.

F-10

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 3 – UNPROVEN MINERAL PROPERTIES (Cont’d)

Joint Exploration Agreement – HNZ Potash, LLC (“HNZ”)

On July 27, 2012 the Company entered into a Joint Exploration Agreement in

which the Company assigned 50% of their interest in twenty-one permitted parcels

within the Holbrook Basin Project (from Holbrook Basin Property and Twin Buttes

Ranch above) to HNZ. In return, HNZ reimbursed the Company for 50% of mineral

exploration costs previously incurred on the permits, ($112,668 received during

the year ended February 28, 2013), and the Company will be liable for 50% of the

future costs relating to the permits.

Fitzgerald Ranch, Arizona

On May 7, 2012, as

amended, the Company entered into an agreement to acquire the Fitzgerald Ranch

for $17,000,000 as follows:

| a) | A down payment of $500,000 (paid) ($25,000 was expensed in the year ended February 29,2012, and the remainder is included in long-term deposits); |

| b) | A payment of $500,000 (paid) upon execution of an amendment to the agreement in November 2012 (included in long-term deposits); |

| c) | A payment of $500,000 to be paid on the earlier of either October 31, 2013, or within 30 days of closing the Company’s next financing (not paid); |

| d) | A payment of $500,000 to be paid on or before December 31, 2013 (not paid); |

| e) | A payment of $1,000,000 to be paid on or before December 31, 2014 (not paid); and |

| f) | The balance of $14,000,000 to be paid on the closing of the sale which is on or before June 30, 2015. |

The Company has not made the required $500,000 payments that were due on October 31, 2013 and December 31, 2013 and $1,000,000 due on December 31, 2014; therefore, there are past-due payments and $975,000 capitalized to long-term deposits has been written-off as at the year ended February 28, 2014. The Company is currently in negotiations to amend the agreement.

NOTE 4 – CONVERTIBLE PROMISORY NOTES PAYABLE

Tranche I

On February 19, 2013, the Company issued

$5,305,540 of convertible debentures (of which $4,140,000 were to related

parties) which mature on February 19, 2014 (the “Maturity Date”) and bear

interest at 15% per annum which shall accrue and be payable on the earlier of

the Maturity Date, or the date the entire principal amount of the convertible

debentures is converted (the “Tranche I Debentures”). The principal amount of

the Tranche I Debentures is convertible into shares of common stock of the

Company at the option of the holder, in whole or in part, at a price of US$0.38

per share until the Maturity Date. The Tranches I Debentures are secured by a

first ranking floating charge security on all of the Company’s assets.

In addition, 2.5 common share purchase warrants were issued for each US$1.00 of principal amount of the Tranche I Debentures, entitling the holder to acquire one share of common stock of the Company for each warrant at an exercise price of US$0.38 per share for a period of one year from the date of issuance. 13,263,850 warrants were issued. The Company determined the fair value of the warrants to be $2,049,578 using the Black-Scholes Option Pricing Model with the following assumptions: Expected dividend yield – 0; Expected stock price volatility – 76%; Risk-free interest rate – 1.07%; Expected life – 1 year.

The proceeds were allocated to the Tranche I Debentures and the warrants based on their relative fair values and accordingly, $3,827,098 was allocated to the debentures and $1,478,442 was allocated to the warrants and recorded as a reduction in the liability and an increase in additional paid-in capital.

In accordance with ASC 470-20 “Debt with Conversion and Other Options”, the Company recognized the value of the embedded beneficial conversion feature of $2,316,159. This value was recorded as a reduction of the liability and an increase in additional paid-in capital.

F-11

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 4 – CONVERTIBLE PROMISORY NOTES PAYABLE (Cont’d)

Tranche I (Cont’d)

In connection with the

issuance of the Tranche I Debentures, the Company paid $73,958 in finder’s fees

and issued 101,882 finder’s warrants. Each finder’s warrant entitles the holder

to purchase one common share for US$0.19 per share for one year from the date of

issuance. The fair value of the finder’s warrant portion calculated using the

Black-Scholes Option Pricing Model was $5,770, recorded as a debenture issuance

cost. The Company also incurred legal and filing fee costs of $51,528, of which

$37,380 was recorded as deferred debt issuance costs and $93,876 was charged to

additional paid-in capital. (See also Tranche I - Amended)

Tranche II

On March 14, 2013, the Company issued

$285,000 of convertible debentures which mature on March 14, 2014 (the “Maturity

Date”), and bear interest at 15% per annum which shall accrue and be payable on

the earlier of the Maturity Date, or the date the entire principal amount of

each debenture is converted. The principal amount of the debentures is

convertible into shares of common stock of the Company at the option of the

holder, in whole or in part, at a price of US$0.38 per share until the Maturity

Date. The debentures are secured by a first ranking floating charge security on

all of the Company’s assets.

In addition, 2.5 common share purchase warrants were issued for each US$1.00 of principal amount of the debentures, entitling the holder to acquire one share of common stock of the Company for each warrant at an exercise price of US$0.38 per share for a period of one year from the date of issuance. 712,500 warrants were issued. The Company determined the fair value of the warrants to be $130,826 using the Black-Scholes Option Pricing Model with the following assumptions: Expected dividend yield – 0; Expected stock price volatility – 75%; Risk-free interest rate – 0.97%; Expected life – 1 year.

The proceeds were allocated to the debentures and the warrants based on their relative fair values and accordingly, $195,334 was allocated to the debentures and $89,666 was allocated to the warrants and recorded as a reduction in the liability and an increase in additional paid-in capital.

In accordance with ASC 470-20 “Debt with Conversion and Other Options”, the Company recognized the value of the embedded beneficial conversion feature of $164,666. This value was recorded as a reduction of the liability and an increase in additional paid-in capital.

In connection with this private placement of debentures, the Company also incurred filing fee costs of $1,425, of which $353 was recorded as deferred debt issuance costs and $1,272 was charged to additional paid-in capital. (See also Tranche II - Amended)

Tranche III

On April 4, 2013, the Company issued

$200,000 of convertible debentures which will mature on April 4, 2014 (the

“Maturity Date”) and bear interest at 15% per annum which shall accrue and be

payable on the earlier of the Maturity Date, or the date the entire principal

amount of each debenture is converted. The principal amount of the debentures is

convertible into shares of common stock of the Company at the option of the

holder, in whole or in part, at a price of US$0.38 per share until the Maturity

Date. The Debentures are secured by a first ranking floating charge security on

all of the Company’s assets.

In addition, 2.5 common share purchase warrants were issued for each US$1.00 of principal amount of the debentures, entitling the holder to acquire one share of common stock of the Company for each warrant at an exercise price of US$0.38 per share for a period of one year from the date of issuance. 500,000 warrants were issued. The Company determined the fair value of the warrants to be $62,896 using the Black-Scholes Option Pricing Model with the following assumptions: Expected dividend yield – 0; Expected stock price volatility – 75%; Risk-free interest rate – 0.97%; Expected life – 1 year.

F-12

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 4 – CONVERTIBLE PROMISORY NOTES PAYABLE (Cont’d)

Tranche III (Cont’d)

The proceeds were

allocated to the debentures and the warrants based on their relative fair values

and accordingly, $152,151 was allocated to the debentures and $47,849 was

allocated to the warrants and recorded as a reduction in the liability and an

increase in additional paid-in capital.

The Company recognized the value of the embedded beneficial conversion feature of $58,375. This value was recorded as a reduction of the liability and an increase in additional paid-in capital.

In connection with this issuance of debentures, the Company also incurred filing fee costs of $1,070, of which $502 was recorded as deferred debt issuance costs and $568 was charged to additional paid-in capital. (See also Tranche III – Amended)

Amendment to Convertible Debentures – Tranche I to III

On February 6, 2014, the Company entered into agreements with all the

debenture holders to modify the terms of the convertible debentures as

follows:

| • | The maturity date is extended to August 19, 2016; |

| • | All interest due on the original maturity date is added to the principal of the convertible debentures; |

| • | The debt is now convertible to into common shares of the Company at $0.12 per share; and |

| • | The warrants will have a term of 42 months from the date of issuance and are exercisable to purchase one common share of the Company at $0.12 per share. |

All the amendments came into effect on the original maturity dates.

Tranche I - Amended

On February 19, 2014, the

amendments came into effect for the Tranche I Debentures. As a result, the

principal of the Tranche I Debentures increased to $6,095,894.

The Company determined the incremental fair value of the warrants issued with the Tranche I Debentures due to the modifications to be $866,295 using the Black-Scholes Option Pricing Model with the following assumptions: Expected dividend yield – 0; Expected stock price volatility – 93%; Risk-free interest rate – 1.16%; Expected life – 2.5 years.

The proceeds were allocated to the Tranche I Debentures and the warrants based on their relative fair values and accordingly, $5,258,905 was allocated to the Tranche I Debentures and $836,989 was allocated to the warrants and recorded as a reduction in the liability and an increase in additional paid-in capital.

In accordance with ASC 470-20 “Debt with Conversion and Other Options”, the Company recognized the value of the embedded beneficial conversion feature of $260,317. This value was recorded as a reduction of the liability and an increase in additional paid-in capital.

In connection with this amendment, the Company paid $4,379 issuance costs, of which $3,591 was recorded as deferred debt issuance costs and $788 was charged to additional paid-in capital.

Tranche II - Amended

On March 14, 2014, the

amendments came into effect for the Tranche II Debentures. As a result, the

principal of the Tranche II Debentures increased to $327,750.

The Company determined the incremental fair value of the warrants issued with the Tranche II Debentures due to the modifications to be $46,523 using the Black-Scholes Option Pricing Model with the following assumptions:

F-13

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 4 – CONVERTIBLE PROMISORY NOTES PAYABLE (Cont’d)

Tranche II - Amended (Cont’d)

Expected

dividend yield – 0; Expected stock price volatility – 94%; Risk-free interest

rate – 1.09%; Expected life – 2.44 years.

The proceeds were allocated to the Tranche II Debentures and the warrants based on their relative fair values and accordingly, $282,892 was allocated to the Tranche II Debentures and $44,858 was allocated to the warrants and recorded as a reduction in the liability and an increase in additional paid-in capital.

In accordance with ASC 470-20 “Debt with Conversion and Other Options”, the Company recognized the value of the embedded beneficial conversion feature of $44,858. This value was recorded as a reduction of the liability and an increase in additional paid-in capital.

Tranche III - Amended

On April 04, 2014, the

amendments came into effect for the Tranche III Debentures. As a result, the

principal of the Tranche III Debentures increased to $230,000.

The Company determined the incremental fair value of the warrants issued with the Tranche III Debentures due to the modifications to be $32,261 using the Black-Scholes Option Pricing Model with the following assumptions: Expected dividend yield – 0; Expected stock price volatility – 94%; Risk-free interest rate – 1.07%; Expected life – 2.38 years.

The proceeds were allocated to the Tranche III Debentures and the warrants based on their relative fair values and accordingly, $198,905 was allocated to the Tranche III Debentures and $31,095 was allocated to the warrants and recorded as a reduction in the liability and an increase in additional paid-in capital.

In accordance with ASC 470-20 “Debt with Conversion and Other Options”, the Company recognized the value of the embedded beneficial conversion feature of $31,095. This value was recorded as a reduction of the liability and an increase in additional paid-in capital.

Tranche V

On May 29, 2014, the Company issued

$500,000 of convertible debentures (the “Tranche V Debentures”) to a related

party (Note 6), which mature on May 29, 2018 and bear interest at 9.5% per annum

which shall accrue and be payable annually, as to 50% in cash and 50% in common

shares of the Company subject to the right of the holder to elect to have an

interest payment satisfied entirely in common shares. The issuance price of

common shares to pay accrued interest will be determined by the market price of

the common shares, as defined by the policies of the TSX-V. The principal amount

of the debenture is convertible at any time prior to the maturity date, in whole

or in part, at the option of the holder into either: (a) units of the Company at

a conversion price of US$0.12 per unit, with each unit being comprised of one

common share and one common share purchase warrant of the Company, with each

warrant exercisable into one common share at a price of US$0.12 per warrant

share until May 29, 2018, or (b) into 10% of the shares of the Company’s

wholly-owned subsidiary, PPI East Block Holding Corp., or pro rata portion thereof for any partial conversion. If option (a) is chosen, 4,166,667

shares and 4,166,667 warrants will be issued. The Tranches V Debentures are

secured by a first ranking floating charge security on all of the Company’s

assets. In accordance with ASC 470-20 “Debt with Conversion and Other Options”,

the Company determined the value of the embedded beneficial conversion feature

to be negative and as such no discount has been recorded.

In connection with this private placement of debentures, the Company paid $3,323 issuance costs which were recorded as deferred debt issuance costs.

F-14

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 4 – CONVERTIBLE DEBENTURES (Cont’d)

| November 30, | February 28, | |||||

| Convertible Debentures – Tranche I to III & Tranche V | 2014 | 2014 | ||||

| Opening balance | $ | 5,554,122 | $ | 1,624,128 | ||

| Subscriptions received | 500,000 | 485,000 | ||||

| Detachable share purchase warrants – amended | (75,953 | ) | (974,504 | ) | ||

| Intrinsic beneficial conversion feature - amended | (75,953 | ) | (483,358 | ) | ||

| Exercised – transfer to share capital | (536,855 | ) | (5,000 | ) | ||

| Accretion | 312,777 | 4,049,613 | ||||

| Interest | 552,372 | 858,243 | ||||

| Interest payable and transferred to accounts payable | (4,465 | ) | - | |||

| Closing balance | $ | 6,226,045 | $ | 5,554,122 |

The difference between the amount recorded to the convertible debentures on initial recognition and the value at maturity will be accreted using the effective interest rate method. During the period ended November 30, 2014, $552,372 (year ended February 28, 2014 - $4,049,613) was expensed as a non-cash interest charge.

Subscriptions Received

The Company holds

subscriptions of $112,250 (2014 - $95,000) towards convertible debenture

offerings.

NOTE 5 – LOANS

Loans comprise certain advances from

third parties and related parties (Note 6). As at November 30, 2014, the loans

have no fixed repayment terms, are unsecured and do not bear interest.

NOTE 6 – RELATED PARTY TRANSACTIONS

Related party balances

The following amounts due to

related parties are included in trade payables and accrued liabilities:

| November | ||||||

| 30, | February 28, | |||||

| 2014 | 2014 | |||||

| Directors, officers and companies controlled by directors and officers of the Company | $ | 1,306,776 | $ | 434,838 |

The following amounts due to related parties are included in loans:

| November 30, | February 28, | ||||||||

| Note | 2014 | 2014 | |||||||

| Director | 5 | $ | 215,000 | $ | 200,000 | ||||

| Companies controlled by directors and officers of the Company | 5 | 43,292 | 46,264 | ||||||

| $ | 258,292 | $ | 246,264 |

F-15

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 6 – RELATED PARTY TRANSACTIONS (Cont’d)

Related party balances (Cont’d)

The following

convertible debentures are outstanding to:

| November 30, | February 28, | ||||||||

| Note | 2014 | 2014 | |||||||

| Companies controlled by directors and officers of the Company | 4 | $ | 230,000 | $ | 200,000 | ||||

| Significant investor of the Company | 4 | $ | 4,410,000 | $ | - | ||||

| $ | 4,640,000 | $ | 200,000 |

Related party transactions

The Company incurred the following transactions with directors, officers, significant investors and companies that are controlled by directors and officers of the Company.

| Nine month period ended | ||||||

| November 30, | November 30, | |||||

| 2014 | 2013 | |||||

| Administration | $ | - | $ | 54,266 | ||

| Consulting fees | 112,500 | 388,811 | ||||

| Management fees | 360,000 | 575,238 | ||||

| Mineral exploration costs | 333,000 | 660,034 | ||||

| Convertible Debenture V issued | 500,000 | - | ||||

| $ | 1,305,500 | $ | 1,678,349 | |||

NOTE 7 – COMMON STOCK

Share Issuances:

During the period ended November

30, 2014, the Company issued 3,839,562 shares pursuant to $460,748 of

convertible debentures being converted to shares at a price of $0.12 per share.

Stock options :

The Board of Directors has adopted a new fixed share option plan (the “2014 Plan”) that provides the maximum aggregate number of common shares that may be reserved for issuance under the 2014 Plan at any point in time is 9,180,969, which represents 10% of the Company’s issued and outstanding common shares as at the date of the Company’s last annual shareholders meeting on September 12, 2013. All stock options outstanding under the previous 2011 rolling stock option plan were rolled into the 2014 Plan. The 2014 Plan is subject to TSX Venture Exchange approval, however, shareholder approval is not required as the 2014 Plan will not result at any time in the number of shares reserved for issuance under stock options exceeding 10% of the Company’s issued shares.

F-16

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 7 – COMMON STOCK (Cont’d)

Stock options

: (Cont’d)

At November 30, 2014 and February 28, 2014 the following stock options were outstanding:

| Number of | Exercise price | |

| Options | CDN$ | Expiry date |

| 72,812 | 0.20 | November 16, 2015 |

| 725,000 | 0.64 | January 10, 2016 |

| 2,513,500 | 0.40 | February 11, 2016 |

| 460,750 | 0.40 | March 03, 2016 |

| 750,500 | 1.18 | June 21, 2016 |

| 745,250 | 0.84 | September 12, 2016 |

| 1,900,000 | 0.76 | January 20, 2017 |

| 234,000 | 0.42 | February 19, 2018 |

| 500,000 | 0.10 | February 19, 2018 |

| 1,265,000 | 0.36 | July 02, 2018 |

| 9,166,812 |

All options outstanding are exercisable. The weighted average remaining contractual life of the outstanding stock options is 0.96 years and the weighted average exercise price is CDN$0.57.

Share purchase warrants

At November 30, 2014 and

February 28, 2014 the following share purchase warrants were outstanding:

| Number of | Exercise price | Expiry date | ||

| Warrants | CDN$ | USD$ | ||

| 561,013 | 0.50 | February 19, 2018 | ||

| 14,476,350 | 0.12 | August 19, 2016 | ||

| 15,037,363 * | ||||

* There is a potential for additional 4,166,667 Warrants to be issued exercisable at $0.12 until May 29, 2018 upon the exercise of the convertible debenture described under convertible debenture V option (a) – Note 4.

NOTE 8 – DERIVATIVE LIABILITY

| Nine months | Year ended | |||||

| ended | ||||||

| November 30, | February 28, | |||||

| 2014 | 2014 | |||||

| Balance, beginning | $ | 42,007 | $ | 1,619,786 | ||

| Fair value of warrants exercised | - | (2,813 | ) | |||

| Fair value change of warrants | (40,001 | ) | (1,574,966 | ) | ||

| Balance, ending | $ | 2,006 | $ | 42,007 |

The derivative liability consists of the fair value of share purchase warrants that were issued in unit private placements that have an exercise price in a currency (Canadian dollars) other than the functional currency of the Company. The derivative liability is a non-cash liability and the Company is not required to expend any cash to settle this liability.

F-17

| Passport Potash Inc. |

| Notes to the consolidated financial statements - unaudited |

| (Expressed in United States dollars) |

| For the nine months ended November 30, 2014 |

NOTE 8 – DERIVATIVE LIABILITY (Cont’d)

Details of these warrants and their fair values are as follows:

| November 30, 2014 | February 28, 2014 | ||||||||||||||

| Exercise | |||||||||||||||

| Price | Number | Number | |||||||||||||

| Issued | ($CDN) | Outstanding | Fair Value | Outstanding | Fair Value | ||||||||||

| February 19, 2013 | $0.50 | 556,249 | $ | 2,006 | 556,250 | $ | 42,007 | ||||||||

The fair value of the share purchase warrants was calculated using the Black-Scholes Option Pricing Model using the following assumptions: Expected dividend yield – 0% (2014: 0%); Expected stock price volatility – 118% (2014: 119%) Risk-free interest rate – 1.25% (2014: 1.52%); Expected life of share purchase warrants – 3.22 years (2014: 0.87 -3.97 years).

NOTE 9 – NON CASH TRANSACTIONS

The Company incurred the following non-cash transactions that are not reflected in the statements of cash flows:

| Year ended | ||||||

| November 30, | February 28, | |||||

| 2014 | 2014 | |||||

| Fair value of shares issued for debt | $ | - | $ | 1,367,499 | ||

| Shares issued for convertible debentures exercised | 460,748 | 5,000 | ||||

| $ | 460,748 | $ | 1,372,499 | |||

NOTE 10 – SUBSEQUENT EVENTS

The Company has evaluated all events that occurred after the balance sheet date through the date when the financial statements were issued to determine if they must be reported. The Management of the Company determined that there were no reportable subsequent events.

F-18

Item 2. Management’s Discussion and Analysis of Financial Conditions and Results of Operations

The following discussion of our financial condition, changes in financial condition and results of operations for the three and nine months ended November 30, 2014 and 2013 should be read in conjunction with our unaudited interim consolidated financial statements and related notes for the three and nine months ended November 30, 2014 and 2013. The following discussion contains forward-looking statements that involve risks, uncertainties and assumptions. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of many factors, including, but not limited to, those set forth under the section entitled “Risk Factors” in our annual report on Form 10-K for the fiscal year ended February 28, 2014 filed with the SEC on June 13, 2014.

Certain information and footnote disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been condensed or omitted. It is suggested that these financial statements be read in conjunction with the financial statements and notes thereto included in the Company’s February 28, 2014 audited financial statements, which were attached to our annual report on Form 10-K for the fiscal year ended February 28, 2014 filed with the SEC on June 13, 2014. The results of operations for the periods ended November 30, 2014 and the same period last year are not necessarily indicative of the operating results for the full years.

Overview of our Business

We were incorporated on August 11, 1987 under the laws of Québec, Canada under the name “Bakertalc Inc.” On January 21, 1994, we changed our name to “Palace Explorations Inc.” On November 11, 1996, we changed our name to “X-Chequer Resources Inc.” On September 29, 2004 we changed our name to “International X-Chequer Resources Inc.” On October 18, 2007, we changed our name to “Passport Metals Inc.” On November 10, 2009 we changed our name to “Passport Potash Inc.” Effective April 26, 2011, we continued our governing corporate jurisdiction from the Province of Québec to the Province of British Columbia under the name “Passport Potash Inc.”

Effective September 29, 2004, we effected a share consolidation (reverse stock split) of our issued and outstanding shares of common stock on a basis of twelve (12) old shares for one (1) new share.

Effective October 18, 2007, we effected a forward stock split of our issued and outstanding shares of common stock on a basis of one (1) old share for three (3) new shares.

Effective March 13, 2014, we effected a share consolidation (reverse stock split) of our issued and outstanding shares of common stock on a basis of two (2) old shares for one (1) new share.

We are a reporting issuer in the Canadian Provinces of British Columbia, Alberta, Ontario and Québec and our common shares are listed for trading on the TSX Venture Exchange (the “TSX-V”) under the trading symbol “PPI”.

Our head and principal office is located at 608 - 1199 West Pender Street, Vancouver, British Columbia, Canada, V6E 2R1.

We are an exploration stage company engaged in the acquisition, exploration and development of mineral resource properties. We currently have an interest in or have the right to earn an interest in seven properties: Southwest Exploration Property, Twin Butte Ranch, Sweetwater/American Potash, Mesa Uranium, Joint Exploration Agreement with the Hopi Tribe, Fitzgerald Ranch and Joint Exploration Agreement with HNZ Potash, which are all located in Arizona. We are currently in default under the option agreement to acquire the Twin Buttes Ranch and in arrears under the purchase agreement to acquire the Fitzgerald Ranch, however, we are in continuing negotiations to either amend these agreements or enter into new agreements. We have not established any proven or probable reserves on our mineral property interests and we are not in actual development or production of any mineral deposit at this time. We are an exploration stage enterprise, as defined in FASB ASC 915 “Development Stage Entities.”

Our independent auditors’ report accompanying our February 28, 2014 and February 28, 2013 financial statements contains an explanatory paragraph expressing substantial doubt about our ability to continue as a going concern.

6

Our financial statements have been prepared assuming that we will continue as a going concern, which contemplates that we will realize our assets and satisfy our liabilities and commitments in the ordinary course of business.

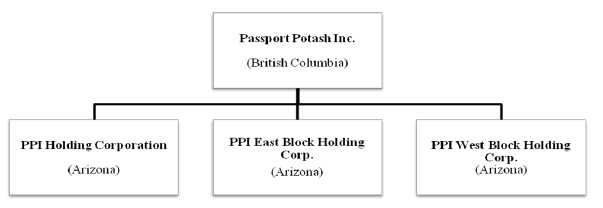

Subsidiaries

The chart below illustrates our corporate structure, including our subsidiaries, which are all wholly owned, and the jurisdictions of incorporation.

Mineral Properties/Agreements

Southwest Exploration Property

On September 30, 2008 we entered into a mineral property option agreement (the “Southwest Option Agreement”) with Southwest Exploration Inc. (“Southwest”) to acquire an undivided 100% interest in 13 Arizona State Land Department exploration permits (“ASLD Exploration Permits”) comprising 8,413.3 acres (3,404.76 ha) of mineral exploration property located in Navajo County, in the Holbrook Basin, Arizona. Under the terms of the Southwest Option Agreement, any after acquired permits within the area of common interest may be made part of the property. Pursuant to this clause, 32 additional ASLD Exploration Permits were made part of the property for a total of 45 ASLD Exploration Permits.

Under the terms of the Southwest Option Agreement, as amended, we could acquire a 100% interest in the Southwest mining claims, subject to a 1% NSR retained by Southwest, in exchange for the following considerations:

| (a) |

$100,000 on execution of the agreement (paid); | |

| (b) |

1,000,000 options (issued) upon receipt of TSX-V approval of the agreement; | |

| (c) |

$125,000 from 90 days following issuance of a drilling permit from the Arizona State Land Department. This permit was received on June 11, 2009 and $125,000 was paid July 23, 2009; | |

| (d) |

250,000 shares on April 1, 2009 (issued); | |

| (e) |

2,681,000 shares on October 1, 2009 (issued); |

7

| (f) |

5,000,000 shares on November 1, 2010 (issued); | |

| (g) |

$350,000 from six months following TSX-V approval of the issuance of 5,000,000 shares (paid); | |

| (h) |

Funding of $200,000 in exploration expenditures pursuant to the completion of a NI 43-101 technical report (completed); | |

| (i) |

250,000 shares upon completion of a NI 43-101 technical report after drilling (issued); and | |

| (j) |

Southwest shall retain a 1% NSR (purchased by the Company). |

Currently, we have a blanket bond with the Arizona State Land Department in the amount of $15,000 for the ASLD Exploration Permits. In addition, we also have a bond with the Arizona Oil and Gas Conservation Commission in the amount of $55,000 for drilling permits.

We entered into an amendment to the Southwest Option Agreement, dated September 18, 2009, whereby the parties agreed to settle the October 1, 2009 scheduled cash payment of $225,000 with the issuance of 2,681,000 shares of the Company.

We entered into a second amendment to the Southwest Option Agreement, dated April 1, 2010, whereby the parties agreed to extend the due date for the payment of $250,000 to Southwest until October 1, 2010. As we had not satisfied this payment obligation by October 1, 2010, we issued 5,000,000 shares of our common stock to Southwest on November 8, 2010 in full satisfaction of the outstanding payment.

We completed the exercise of our option to purchase the 100% interest in the Southwest claims and the purchase of the 1% net smelter royalty in an agreement dated February 13, 2012. The Southwest permits are held by PPI Holding Corporation, our wholly owned subsidiary.

Twin Buttes Ranch Property

On August 28, 2009, as amended, we entered into a four-year lease with an option to purchase (the “Lease & Option Agreement”) with Twin Buttes Ranch, LLC respecting the Twin Buttes Ranch located in the potash-bearing Holbrook Basin of east-central Arizona. The Twin Buttes Ranch comprises some 28,526 acres (11,544 hectares) of private deeded land with 76.7% or approximately 21,894 acres (8,860 hectares) overlying the potash horizons within the Holbrook Basin.

Under the terms of the Lease & Option Agreement, we may acquire a 100% undivided interest in the deeded land and sub-surface mineral rights comprising the Twin Buttes Ranch property by making lease payments totaling $1,250,000 over five and a half years and, upon exercising our option to purchase, by paying $20,000,000 for the entire Twin Buttes Ranch including all sub-surface mineral rights except those pertaining to oil and gas, petrified wood and geothermal resources. There are no royalties associated with the sub-surface mineral rights.

On December 4, 2009, we entered into an amendment to the Lease & Option Agreement whereby we signed a mining lease with Twin Buttes Ranch, LLC on the Twin Buttes Ranch with a term from December 4, 2009 through August 28, 2013 subject to early termination as provided in the Lease & Option Agreement. Under the mining lease, we are entitled to explore, develop, mine, remove, treat and produce all ores, minerals and metals on Twin Buttes Ranch solely for the purpose of determining the existence of potash and the economic feasibility of the purchase and development of the property. In consideration, we shall remain current in our option payments under the Lease & Option Agreement and keep all terms of the Lease & Option Agreement in good standing.

On September 7, 2010, we amended the terms of the Lease & Option Agreement to provide for an extension of a portion of the initial cash payment until December 1, 2010.

On August 20, 2013, we further amended the Lease & Option Agreement to extend the term of the option agreement from August 28, 2013 to January 6, 2016 and provide for the payments of:

8

| (a) |

$250,000 on the earlier of (i) within 30 days of closing our next round of financing which is a minimum $5 million, or (ii) December 1, 2013 (this payment obligation survives any early termination of the Lease & Option Agreement by us or a termination resulting from an uncured breach by us), | |

| (b) |

$250,000 on August 28, 2014; and | |

| (c) |

$250,000 on May 1, 2015. |

Concurrently with the amendment to the Lease & Option Agreement, we also amended the mining lease to provide that the term of the lease will end on the expiration or earlier termination of the Lease & Option Agreement, except in the event that we exercise our option pursuant to the Lease & Option Agreement in which event the term shall end on the closing date of the Lease & Option Agreement, and any subsequent amendments thereto.

Details of the payments under the Lease & Option Agreement, as amended, are as follows:

| (a) |

A payment of $50,000 and $10,000 legal costs on or before November 26, 2009 (paid); | |

| (b) |

A payment of $25,000 on September 17, 2010 (paid); | |

| (c) |

A payment of $75,000 on December 1, 2010 (paid); | |

| (d) |

A payment of $150,000 on August 28, 2011 (paid); | |

| (e) |

A payment of $200,000 on August 28, 2012 (paid); | |

| (f) |

A payment of $250,000 on the earlier of (a) within 30 days of closing our next round of financing which is a minimum $5 million, or (b) December 1, 2013 (not paid); | |

| (g) |

A payment of $250,000 on August 28, 2014 (not paid); and | |

| (h) |

A payment of $250,000 on May 1, 2015. |

The Company has not made the required $250,000 payments that were due on December 1, 2013 and August 28, 2014; therefore, there are past-due payment obligations. On April 17, 2014, we were served a notice of breach that we did not remedy within 30 days. Therefore, Twin Buttes Ranch, LLC may now terminate the option at its discretion, which would also terminate the Lease, however, we have not received notice of termination from Twin Buttes Ranch, LLC. We are continuing negotiations to either amend the Option Agreement or enter into a new option agreement, however, the risk remains that we may not be successful in completing either an amendment to the Option Agreement or entering into a new option agreement.

The Option Agreement currently provides that upon exercise to purchase the entire Twin Butte Ranch, we must deliver a certified cheque in the amount of $1,000 on or before 5pm (Arizona time), January 6, 2016 (the option expiry date), followed by a payment of $19,999,000 within thirty days.

Sweetwater/American Potash Property

On November 12, 2010 we entered into an option of Arizona exploration leases (the “Sweetwater Option Agreement”) with Sweetwater River Resources, LLC (“Sweetwater”) and American Potash, LLC (“American Potash”) to acquire the right, title and interest in five mineral exploration permits within the Holbrook Basin. The five permits consist of Arizona State Land Department exploration permits that cover more than 3,200 acres.

Pursuant to the terms of the Sweetwater Option Agreement, we could acquire a 100% interest in the exploration permits for the consideration of: (i) issuing 500,000 shares of our common stock by December 15, 2010; (ii) cash payment of CAD$90,000 payable in three installments of $30,000 each at 12 months, 18 months and 24 months from the date of signing the Sweetwater Option Agreement; and (iii) meeting the exploration expenditures a required by the Arizona State Land Department. We are responsible for payment of all exploration expenditures on the permits. Pursuant to the Sweetwater Option Agreement, the property was subject to a 2% net smelter royalty in favor of American Potash which we had the option to purchase at a price of $150,000 for 1% or $300,000 for the full 2%.

9

On March 27, 2012, we completed the exercise of the option under the Sweetwater Option Agreement and the repurchase of the 2% NSR royalty in respect of the Sweetwater exploration permits. The permits are held by PPI Holding Corporation, our wholly owned subsidiary.

Mesa Uranium Property

On August 31, 2010 we entered into a mineral property option agreement (the “Mesa Option Agreement”) with Mesa Uranium Corp. (“Mesa”) in respect of three Arizona State Land Department exploration permits covering approximately 1,950 acres, which are wholly owned by Mesa. Pursuant to the terms of the agreement, we had the right to acquire a 75% interest in the Mesa permits in consideration for the issuance of 500,000 shares of our common stock to Mesa, the payment of $20,000.00 cash to Mesa and meeting the minimum exploration expenditures as required by the Arizona State Land Department. Upon earning a 75% interest in the permits, we had the right to acquire the remaining 25% interest in the Mesa permits by paying $100,000 in cash, stock equivalent or work expenditures. Under the terms of the agreement, we are responsible for payment of all exploration expenditures on the leases. The property was subject to a 2% net smelter royalty which we had the option to purchase at a price of $150,000 per 1% or $300,000 for the full 2%.

On February 13, 2012, we exercised our option to acquire a 75% interest in the Mesa permits. On March 9, 2012, we announced that we had exercised our option to acquire the remaining 25% interest in the Mesa properties under the Mesa Option Agreement and to acquire the 2% NSR on those properties thereby acquiring a royalty-free, 100% interest in the Mesa properties. The permits are held by PPI Holding Corporation, our wholly owned subsidiary.

Ringbolt Property

On March 28, 2011 we entered into an option agreement (the “Ringbolt Option Agreement”) with Ringbolt Ventures Ltd., Potash Green, LLC, Wendy Walker Tibbetts and Joseph J. Hansen (collectively, the “Optionor”) pursuant to which we acquired the right to acquire a 100% interest in the Ringbolt potash property located in the Holbrook Basin of southeast Arizona. The Ringbolt property is comprised of 15,994.32 acres of mineral exploration permits on land managed by the Arizona State Land Department.

Pursuant to the terms of the Ringbolt Option Agreement, we may acquire a 90% interest in the property by: (i) making cash payments totaling $1.0 million ($50,000 upon execution of the agreement, $250,000 upon TSX Venture Exchange approval, $350,000 on or before the 1st anniversary of TSX Venture Exchange approval, and $350,000 on or before the 2nd anniversary of TSX Venture Exchange approval), (ii) incurring a total of $2.25 million in exploration expenditures on the property over three years ($500,000 within 1 year of TSX Venture Exchange approval, $750,000 within 1 year of the 1st anniversary of TSX Venture Exchange approval, and $1,000,000 within 1 year of the 2nd anniversary of TSX Venture Exchange approval), and (iii) issuing four million common shares over a three-year period (1,000,000 shares upon TSX Venture Exchange approval, 1,400,000 shares on or before the 1st anniversary of TSX Venture Exchange approval, and 1,600,000 shares on or before the 2nd anniversary of TSX Venture Exchange approval). Upon satisfaction of these terms, we will have the right to purchase the remaining 10% interest for a cash payment of $5 million, which shall remain exercisable until the Ringbolt property goes into commercial production (defined as the sale of any mineral products from the property). In addition, pursuant to the Ringbolt Option Agreement, the Ringbolt property will be subject to a 1% gross overriding royalty on production from the property.

On October 30, 2012, as part of a settlement agreement between us and the Optionor, we entered into an amendment agreement to the Ringbolt Option Agreement pursuant to which we will pay to the Optionor a total of $3,850,000, $150,000 of which was paid upon execution of the amendment agreement, $2,450,000 will be paid upon TSX Ventures Exchange approval of the amendment agreement, and the remaining $1,250,000 on or before October 31, 2014. In addition, upon TSX Venture Exchange approval of the amendment agreement, we will issue 750,000 shares of common stock to the Optionor and the Optionor will assign to us all of its right, title and interest in and to the property and will take all necessary action with the ASLD to effect such assignment. The cash payment of $2,450,000 and 750,000 shares of our common stock will be placed into escrow and will be released to the Optionor upon receipt of confirmation of the assignment of the property to us from the ASLD. There will be no royalty attached to the transferred mineral exploration permits.

10

Should we sell or in any way transfer our interest in the property, the Optionor will receive 20% of the gross consideration in excess of $30 million to a maximum of $2,000,000 if the aggregate consideration received for the transfer of the interest in the property is greater than $30 million and less than $40 million; or $2,000,000 plus 10% of the gross consideration in excess of $40 million to a maximum of $1,000,000 if the aggregate consideration is greater than $40 million and less than $50 million; or $3,000,000 plus 20% of the gross consideration in excess of $50 million if the aggregate consideration is greater than $50 million.

If we sell or transfer less than a 100% interest in the property, then the aforementioned bonus payments shall be ratably reduced by multiplying the bonus payment by the percentage of interest subject to the transfer transaction. The sale or transfer of the remainder of the interest in the property held by us will continue to be subject to the aforementioned bonus payment provisions.