Attached files

Net

Asset Valuation Presentation January 2015

Exhibit 99.3 |

General Notices

This is not an offer to sell nor a solicitation of an offer to buy shares of the REIT. The information

herein does not supplement or revise any information in the REIT's public filings made with the

U.S. Securities and Exchange Commission. To the extent information herein conflicts with the

REIT’s public filings, as supplemented, the information in the filings govern. This piece is for general information purposes only and does not constitute legal, tax, investment, or

other professional advice on any subject matter. Information provided is not all-inclusive

and should not be relied upon as being all-inclusive. This presentation includes forward-looking statements. Forward-looking statements are based on

current expectations and may be identified by words such as “believes,”

“expects,”, “anticipates”, “may,” “could” and terms of

similar substance, and speak only as of the date made. Actual results could differ materially

from those expressed or implied in the REIT’s forward-looking statements. Important factors,

among others, that could cause the REIT's actual results to differ materially from those in its

forward-looking statements include those identified in the Risk Factors described below.

Investors should not place undue reliance on forward-looking statements. The REIT is under

no obligation to, and expressly disclaims any obligation to update or alter its

forward-looking statements, whether as a result of new information, subsequent events or

otherwise, except as required by law.

An investment in the REIT is subject to significant risks, some of which are summarized below in the

“Risk Factors” section of this piece. See also, “Risk Factors” in the

REIT’s public filings for a more detailed description of the risks associated with an

investment in the REIT.

|

Risk

Factors Investing in a non-traded REIT is a higher-risk, longer term investment and is not suitable for

all investors. Due to the risks involved in the ownership of real estate, there is no guarantee

of any return on investment. The shares may lose value or investors could lose their entire

investment. The shares are not FDIC- insured, nor bank guaranteed. Non-traded REITs are illiquid. There is no public trading market for the shares. The REIT has no

obligation to list on any public securities market and does not expect to list the shares.

Stockholders will bear the economic risks of an investment in the shares for a substantial and

indefinite period. If investors are able to sell their shares, it would likely be at a

substantial loss of the amount invested.

The REIT relies on its advisor and the advisor’s affiliates to select the REIT’s properties

and to conduct the REIT’s operations. The REIT is obligated to pay substantial fees to its

advisor, managing dealer, property manager and their respective affiliates based upon

agreements which have not been negotiated at arm’s length, some of which are payable based

upon factors other than the quality of services. These fees could influence their advice and

judgment in performing services. Currently, the REIT is incurring fees and expenses, some of

which will need to be reimbursed to its advisor and affiliates. Certain officers and

directors of the advisor also serve as the REIT’s officers and directors, as well as officers and

directors of competing programs, and/or joint venture partners, resulting in conflicts of

interest. Those persons could take actions more favorable to other entities. The REIT has not identified all of the investments that it will make in the future, and investors will

not have the opportunity to evaluate future investments before they are made. Investors must

rely on the REIT’s advisor and board of directors to evaluate, structure and implement

future investments. |

Risk

Factors During the REIT's public offerings, the REIT made distributions to its stockholders in the form of

shares of its stock. Stock distributions served to provide early stockholders with additional

shares as compared to later stockholders for the same initial cash investment. As a result,

early stockholders are allocated greater percentages of any accretion in the value of the

REIT's early property developments and in any sales proceeds or liquidating distributions upon

the sale of such properties or occurrence of an exit event. The REIT believes its former stock

distribution policy aligned the age of the REIT's stockholder base with the long term

appreciation in the value of the REIT's assets. The REIT's board of directors will continue to

periodically review the REIT's distribution policy. If the REIT makes cash distributions from sources

other than from its cash flows or funds from operations, such as from borrowings, such

distributions could lower stockholders’ overall return on investment. The REIT has not

established a limit on the extent to which it may use borrowings or issue shares of common

stock to pay distributions. There is no assurance that the REIT will make any further

distributions. The amount or basis of distributions, if any, will be determined solely by

and at the discretion of the REIT’s board of directors. The distribution of new common stock is not

currently included as a component of the stockholder’s gross income under the IRS Code and is

therefore tax deferred and not taxable when received. Stockholders should consult with their

financial advisor, accountant and/or attorney for tax advice specific to their particular needs

and objectives.

If the REIT fails to maintain its qualification as a REIT for any taxable year, it will be subject to

federal income tax on taxable income at regular corporate rates. In such an event, net earnings

available for investment or distributions would be reduced.

|

Risk

Factors The REIT has incurred debt to make its investments. The use of leverage to acquire assets may hinder

the REIT’s ability to pay distributions and/or decrease the value of stockholders’

investment in the event income from, or the value of the property securing the debt

declines. The REIT made only a limited number of investments resulting in a less diversified portfolio in terms

of the number of investments owned and their geographic locations. All of the REIT’s

current investments are in multifamily development properties in the Southeast and Sun Belt

regions of the United States. An investment in the REIT’s shares is subject to greater

risk to the extent that the REIT has limited geographic and sector diversification in its

portfolio of investments.

If sales of our properties or other assets not owned by a TRS are deemed prohibited transactions, we

may be subject to a 100% penalty federal tax on the gains resulting from those sales. A

“prohibited transaction” is a sale by a REIT of real property or other assets held

primarily for sale in the ordinary course of the REIT’s trade or business (i.e., real

property or other assets that are not held for investment but are held as inventory for sale by

the REIT). Under existing law, whether property is held as inventory or primarily for sale to customers

in the ordinary course of a trade or business is a question of fact that depends on all the facts and

circumstances surrounding the particular transaction. |

Valuation Disclosures

Our estimated net asset value per share is based upon subjective judgments, assumptions and opinions

which may or may not turn out to be correct. You should not rely upon our estimated net asset

value as representative of the amount that might be paid to you for your shares in a market

transaction, or in a liquidity event.

In determining our estimated net asset value per share, we relied upon a valuation of our portfolio

of properties as of Dec. 31, 2014. Valuations and appraisals of our properties are

estimates of fair value and may not necessarily correspond to realizable value upon the sale

of such properties. Therefore, the estimated present value to the Company of our equity in our

portfolio may not reflect the amount that would be realized upon a sale of each of our

properties.

We intend to conduct annual year end valuations in accordance with our valuation policy, if we do not

perform a subsequent calculation of the net asset value per share of our shares, you may not

be able to determine the net asset value of your shares on an ongoing basis.

This valuation represents the estimated net asset value per share as a snapshot in time, will

fluctuate over time, and should not be relied upon as representative of the amount a

stockholder could expect to receive now or in a future liquidation event. CBRE Cap, the

independent valuation firm, made numerous assumptions with respect to industry, business,

economic and regulatory conditions, all of which are subject to changes beyond the control of

CBRE Cap or the Company. CBRE Cap is not responsible for our estimated net asset value per

share as of Dec. 31, 2014. Throughout the valuation process, the valuation committee, our

advisor and senior members of management reviewed, confirmed and approved the processes

and methodologies and their consistency with real estate industry standards and best

practices.

|

7

CNL Growth Properties is a non-traded real estate investment trust

(REIT)

The REIT seeks commercial real estate investment opportunities in

growth-oriented markets, with a focus on Multifamily Development.

CNL Growth Properties |

8

Highlights

Commenced initial offering in October 2009

Launched follow-on offering in August 2013

Closed second offering in April 2014

Raised approximately $559 million in equity since initial offering

Invested in 16 assets as of the valuation date

16 multifamily development projects

8 operating, 7 in development, 1 operating & held for sale

Asset Held-for-Sale

Woodfield Long Point, Charleston County, SC

Distribution Policy, Distribution Reinvestment Plan, Redemption Plan

Stock distributions terminated October 1, 2014

Distribution Reinvestment Plan (DRP) terminated October 1, 2014

Redemption Plan suspended October 1, 2014

Completed independent valuation of portfolio as of December 31, 2014

|

9

Sale of Woodfield Long Point

Entered Purchase & Sale Agreement November 25, 2014

258-Unit Class A Garden Style Community in Mount Pleasant

(Charleston County), South Carolina

Sale Price: $55.5 million

Closed: January 15, 2015 |

10

Estimated Net Asset Value (“NAV”)

Consistent with methodologies prescribed by IPA

Valuation Guidelines

1

Individual MAI property appraisals (no enterprise/portfolio

premiums)

Use of independent investment banking firm

Engaged CBRE Capital Advisors, Inc. (“CBRE Cap”) an independent

investment banking firm as valuation expert

Disclosure of key assumptions & methodology

Utilized discounted cash flow method

Range provided by adjusting key assumptions

Discount rates, terminal capitalization (“terminal cap”) rates

1

There is no assurance that IPA Guidelines are acceptable to FINRA or under ERISA

for compliance with reporting requirements. |

11

Methodology

Valuation based on cash flow projections and a four year

discounted cash flow analysis (expected hold period) for each

property from actual cash flows based on realized rent, and

the Company’s development budgets and cash flow

projections

The Company’s real estate properties were categorized into three

classifications

Operating Assets (8 properties)

Development Projects (7 properties)

Operating Asset Held For Sale (1 property)

Terminal capitalization rate was used to calculate terminal

value (stabilized NOI/terminal capitalization rate) of the assets

at stabilization

Terminal capitalization rate sourced from MAI appraisals and vary by

location, asset quality and supply/demand metrics |

12

CBRE Cap created a valuation range by varying the discount rate

utilized and the terminal cap rate of each real estate asset

The

range

was

set

at

50bps

on

the

discount

rate

and

30bps

on

the

terminal

capitalization rate of each asset

Represents an approximate 5% sensitivity on the discount rate and terminal

capitalization rate ranges consistent with IPA guidelines

CBRE Cap utilized a December 31, 2014, share count of 22,526,171

CBRE Cap Valuation (discount and terminal capitalization rates

based on CBRE appraisals)

Weighted avg. discount rate: 10.5%

Weighted avg. terminal rate:

6.03%

Valuation Summary |

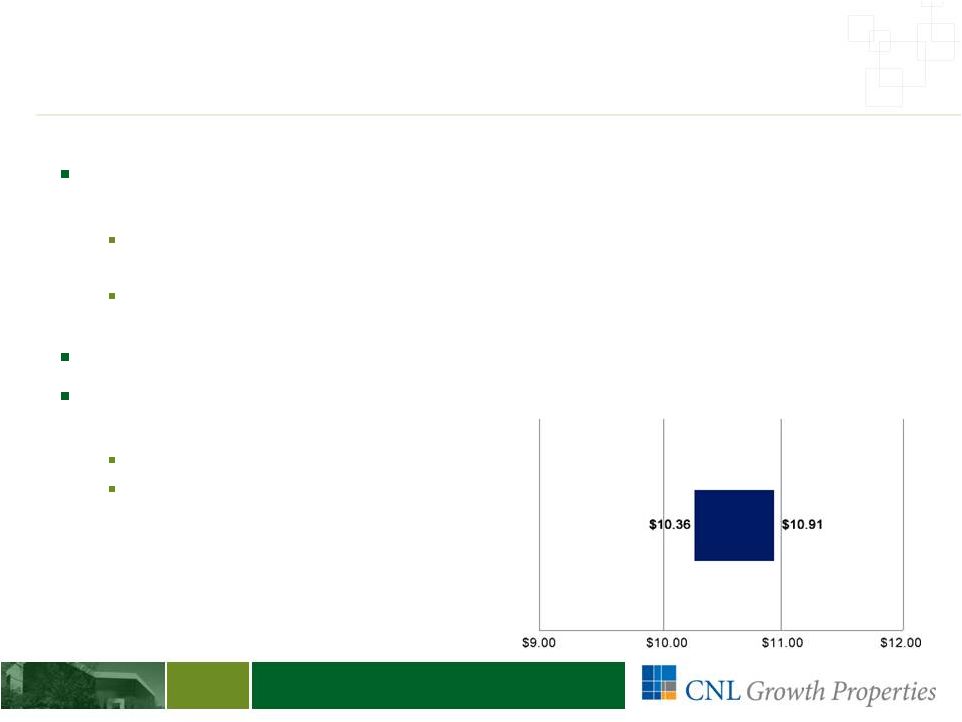

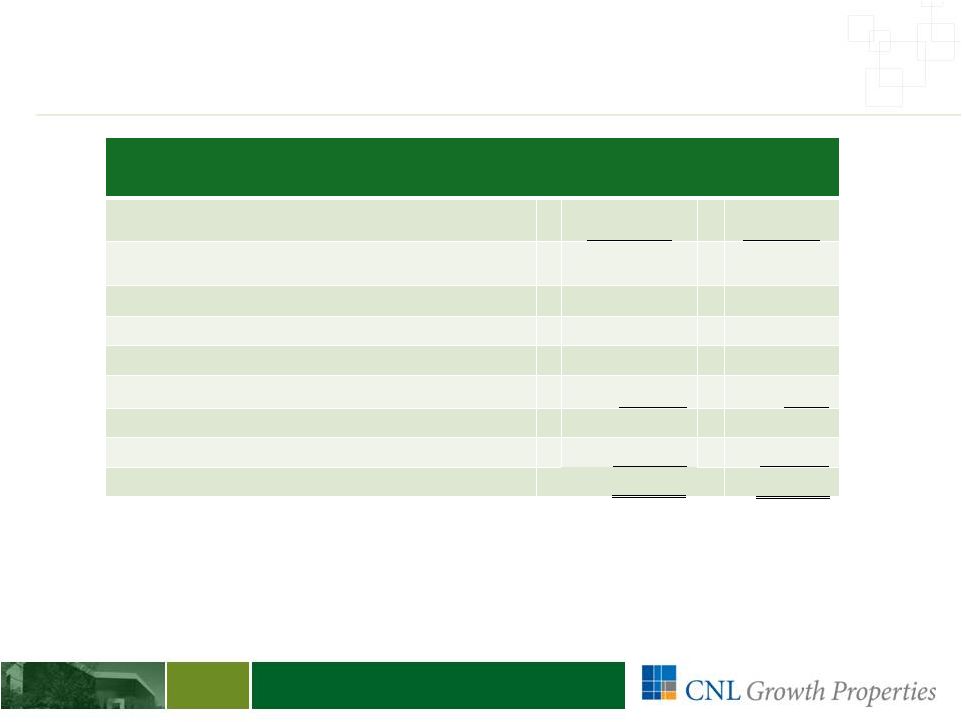

13

Estimated NAV Per Share Build-Up

Table of Value Estimates for Components of Net Asset Value

(as of Dec. 31, 2014)

Value

($

in

000’s)

Per

Share

$199,439

$8.85

Cash

and

cash

equivalents

2

46,854

2.08

Other

assets

2

638

0.03

Accounts

payable

and

other

accrued

expenses

2

(4,607)

(0.20)

Other

liabilities

2

(1,492)

(0.07)

Estimated

NAV

before

incentive

fee

$240,832

$10.69

Less:

Incentive

Fee

to

Advisor

(1,393)

(0.06)

Estimated

NAV

3

1

The company’s share of equity including promote structure in each

venture. 2

Based on the Company’s preliminary balance sheet as of Dec. 31, 2014.

3

The

estimated

NAV

per

share

is

a

snapshot

in

time

and

should

not

be

relied

upon

as

indicative

of

the

value

the

company

or

stockholders

may receive now or in a future liquidation event.

$239,439

$10.63

Present value of equity in operating assets,

development

projects

and

asset

held

for

sale

1 |

14

Looking Ahead

1

Evaluate monetization opportunities as

properties become stabilized

Execute on existing pipeline of multifamily

development opportunities

1

There is no assurance these objectives will be met. Forward-looking statements

are based on current expectations and may be identified by words such as

“believes,” “expects,”

“may,”

“could”

and terms of similar substance, and speak only as of the date made. Actual results

could differ materially due to risks and uncertainties that are beyond the

REIT’s ability to control or accurately predict. Investors should not

place undue reliance on forward-looking statements.

|

15

For More Information

Investors

To obtain additional information about CNL Growth Properties,

please consult your Financial Advisor or visit

CNLGrowthProperties.com.

Financial Professionals

For more information about CNL Growth Properties, please

contact our managing dealer, CNL Securities, Member

FINRA/SIPC at 866-650-0650 or CNLSecurities.com.

This is not an offer. Dissemination to investors is prohibited. Investments in non-traded

real estate investment trusts (REITs) are subject to significant risks. These risks include

limited operating histories, reliance on the advisors, conflicts of interests, use of leverage, payment of

substantial fees to the advisors and their affiliates, illiquidity and liquidations at less than the

original amounts invested. © 2015 CNL Global Growth Advisor, LLC. All Rights Reserved. CNL® and the Squares Within

Squares design trademarks are used under license from CNL Intellectual Properties, Inc.

|

16

Questions & Answers |