Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Southcross Energy Partners, L.P. | d834804d8k.htm |

2014

Wells

Fargo

Energy

Symposium

December 9, 2014

Exhibit 99.1 |

2014 Wells Fargo Energy Symposium

Cautionary Statements

1

This presentation contains forward-looking statements and information. Forward-looking

statements include, without limitation, any statement that may project, indicate or imply future

results, events, performance or achievements, and may contain the words “expect,”

“intend,” “plan,” “anticipate,” “estimate,” “believe,” “will be,” “will continue,” “will likely result” and

similar expressions, or future conditional verbs such as “may,” “will,”

“should,” “would” and “could.” In addition, any statement concerning future financial performance (including future

revenues, earnings or growth rates), ongoing business strategies or prospects, and possible actions

taken by us, our subsidiaries or our affiliates, are also forward-looking statements. These

forward-looking statements involve external risks and uncertainties, including, but not limited to, those described under the section entitled “Risk Factors” included in our 2013

Annual Report on Form 10-K (as updated by our Quarterly Reports on Form 10-Q).

Forward-looking statements are based on current expectations and projections about future

events and are inherently subject to a variety of risks and uncertainties, many of which are

beyond the control of our management team. All forward-looking statements in this presentation and

in any other written or oral forward-looking statements attributable to us, or to

persons acting on our behalf, are expressly qualified in their entirety by these risks and

uncertainties. These risks and uncertainties include, among others: the volatility of natural gas, crude oil and NGL prices and the price and demand of products derived

from these commodities; competitive conditions in our industry and the extent and success of producers increasing production

or replacing declining production and our success in obtaining new sources of supply; industry conditions and supply of pipelines, processing and fractionation capacity relative to

available natural gas from producers; our dependence upon a relatively limited number of customers for a significant portion of our

revenues; actions taken, inactions or non-performance by third parties, including suppliers, contractors,

operators, processors, transporters and customers; our ability to effectively recover NGLs at a rate equal to or greater than our contracted rates with

customers; our ability to produce and market NGLs at the anticipated differential to NGL index pricing;

our access to markets enabling us to match pricing indices for purchases and sales of natural gas and

NGLs; our ability to complete projects within budget and on schedule, including but not limited to, timely

receipt of necessary government approvals and permits, our ability to control the costs of

construction and other factors that may impact projects;

our ability to consummate acquisitions, successfully integrate the acquired businesses and realize

anticipated cost savings and other synergies from any acquisitions, including in respect of our

acquisition of the TexStar rich gas system assets;

our ability to manage over time changing exposure to commodity price risk;

the effectiveness of our hedging activities or our decisions not to undertake hedging

activities; our access to financing and ability to remain in compliance with our financing covenants;

our ability to generate sufficient operating cash flow to fund our quarterly distributions;

changes in general economic conditions;

the effects of downtime associated with our assets or the assets of third parties interconnected with

our systems; operating hazards, fires, natural disasters, weather-related delays, casualty losses and other

matters beyond our control; the failure of our processing and fractionation plants to perform as expected, including outages for

unscheduled maintenance or repair; the effects of laws and governmental regulations and policies;

the effects of existing and future litigation; and

other financial, operational and legal risks and uncertainties detailed from time to time in our

filings with the U.S. Securities and Exchange Commission. Developments in any of these areas

could cause actual results to differ materially from those anticipated or projected, affect our ability to maintain distribution levels and/or access

necessary financial markets, or cause a significant reduction in the market price of our common

units. The foregoing list of risks and uncertainties may not contain all of the

risks and uncertainties that could affect us. In addition, in light of these risks and uncertainties, the matters referred

to in the forward-looking statements contained in this presentation may not, in fact, occur.

Accordingly, undue reliance should not be placed on these statements. We undertake no obligation

to publicly update or revise any forward-looking statements as a result of new information, future events or otherwise, except as otherwise required by law. |

2014 Wells Fargo Energy Symposium

Partnership Structure

Southcross Holdings LP

(“Holdings”)

Southcross Energy

Partners, L.P.

(NYSE: SXE)

Affiliate Assets

Public

43% LP Interest

2% GP Interest

57% LP Interest

Southcross Energy

Partners GP, LLC

Financial sponsor ownership through various holding companies

2

100% Interest |

2014 Wells Fargo Energy Symposium

3

30+ Years’

Experience

•

President & COO

Southcross Energy

•

President

NiSource Midstream Services

•

Owner, President

Ranger Interests, Inc.

•

VP, Commercial (Western Region)

Enterprise Product Partners

•

Director, Commercial (Permian Basin)

GulfTerra Energy Partners

•

Director, Commercial

El Paso Field Services

•

Manager, Northeast Marketing

Delhi Gas Pipeline

•

VP, Business Development

Triumph Natural Gas

President & Chief Executive Officer

John E. Bonn

•

Bachelor of Science, Agricultural Engineering, Texas A&M

•

Officer, United States Army and Army Reserves

•

Board member, Texas Aggie Corps of Cadets Association

•

Past board member, Marcellus Shale Coalition

•

New Mexico Oil & Gas Association

•

Past president, Natural Gas Society of North Texas |

2014 Wells Fargo Energy Symposium

The Southcross Advantage

4

Significant

scale

of

pipeline

and

processing

assets

Operating

stability

through

interconnected

system

Extensive

footprint

in

the

prolific

Eagle

Ford and Gulf Coast area

Blue

chip,

active

producer

customer

base

Full

spectrum

of

services

creates

competitive and economic advantages

Fractionation

assets

are

a

significant

differentiator

Premium

and

growing

markets

for

gas,

NGLs and condensate

Corpus

Christi

region

is

growing

rapidly

and serving new export markets

Fully utilize existing capacity

Develop organic growth

projects

Drop-downs

Acquisitions

Premier Strategic Platform

in the Eagle Ford

Fully Integrated

Midstream Platform

Four Drivers of

Growth |

2014 Wells Fargo Energy Symposium

Premier Strategic Footprint with Scale to

Succeed in the Eagle Ford

Holdings

SXE

Sour Gas Treating Facility

Fractionator

Processing Plant

5

Corpus Christi

San Antonio

Houston

Conroe

Lone Star

Woodsboro

Bonnie View

Gregory

Robstown

South Texas Assets

Pipeline (miles)

Gas Processing Capacity (MMcf/d)

Fractionation Capacity (MBbls/d)

Holdings

655

-

63

SXE

3,030

685

27 |

2014 Wells Fargo Energy Symposium

Eagle Ford Highlights

6

Source: EIA

The Eagle Ford is a major driver of U.S. oil and natural gas production growth

U.S. Oil Production per Day

U.S. Natural Gas Production per Day |

2014 Wells Fargo Energy Symposium

Eagle Ford Has Attractive Producer

Economics

7

Eagle Ford

Permian Basin

Bakken

Marginal Economics

12-Month Strip

$/Bbl (WTI)

Source: RBC Capital Markets

U.S. Oil Play Break-Even Assessment at December 1, 2014 Forward Strip Prices |

2014 Wells Fargo Energy Symposium

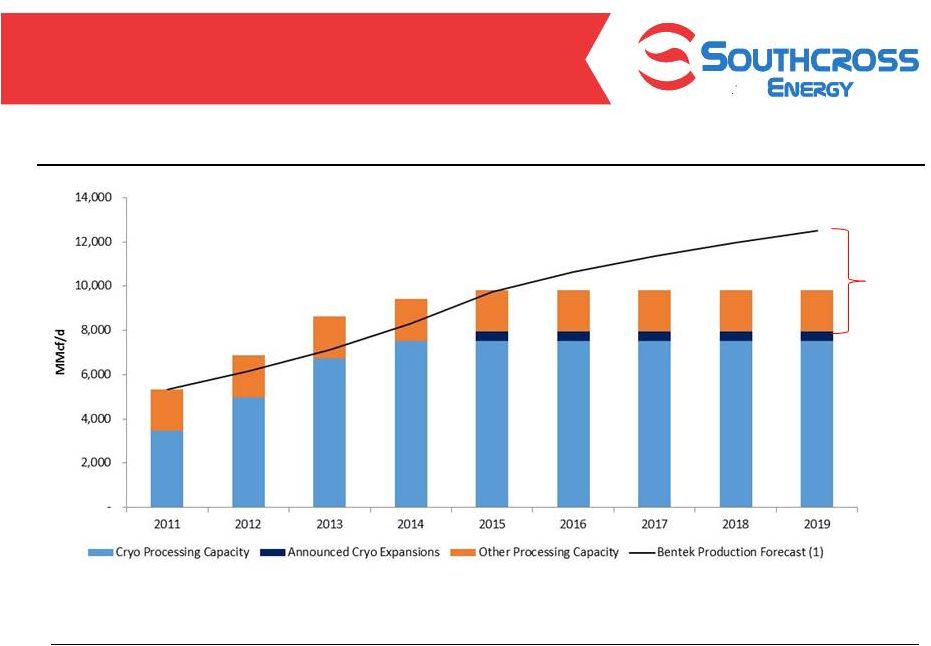

Request for Proposal Summary

Proposed Contract and Deal Terms

Texas Gulf Coast Production Expected to

Exceed Processing Capacity

8

(1) Bentek Eagle Ford and Texas Gulf Coast production estimates

Note: Excludes plant retirements.

Texas Gulf Coast Region is forecasted to need an additional 2.0 to 4.5 bcf/d of

processing capacity by 2019

Potential

4.5 Bcf/d

Shortfall

in Cryo

Capacity |

2014 Wells Fargo Energy Symposium

Well Positioned for Current Eagle Ford

Activity

9

Permits 2012-2014 |

2014 Wells Fargo Energy Symposium

Full Spectrum of Services Creates

Competitive and Economic Advantages

10

Wellhead

Gathering and Compression

Gas Processing Plants

Y-Grade

Fractionation Facilities

Natural Gas

End Users

Transportation Lines / Storage

NGL End Users

NGL & Residue Marketing

20%

30%

5%

35%

10%

Midstream

Margin Stream

Southcross participates in 100% of the midstream margin stream

~50% of Margin Stream from Fractionation

and NGL Marketing

Note: Treating fees, when applicable, further supplement the margin stream

|

2014 Wells Fargo Energy Symposium

Refining Projects

•

Valero upgrading 325kb/d Corpus Christi refinery

•

Flint Hills plans to reconfigure 230kb/d Corpus Christi West Refinery

•

Martin Midstream, Magellan Midstream and Trafigura constructing condensate

splitters at facilities in Corpus Christi Lyondell / Equistar Ethylene

Capacity Expansion •

Lyondell to add 800 million lbs/year of ethylene capacity at Corpus Christi plant

by 2016 •

20,000 Bbl/d of estimated increase in ethane demand by 2016

Cheniere

–

April

7,

2014,

July

17,

2014

and

October

8,

2014

Press

Releases

•

Entered into 20 year LNG supply agreements with Endesa

•

Signed agreement to supply EDF with 380,000 tons / year of LNG from Train 3 as

early as 2019 •

Expect to complete steps to final investment decision and construction by early

2015 •

FERC issues final Environmental Impact Statement for project on October 8, 2014

Trafigura

–

November

14,

2013

and

September

11,

2014

Press

Release

•

Trafigura spending $500 million to expand dock facilities at Corpus Christi

•

Expansion to meet increasing demand for water access for Eagle Ford

production •

Buckeye

Partners

LP

completes

$860

million

acquisition

of

80%

of

Corpus

Christi

midstream

business

from

Trafigura

NET

Midstream

Pipeline

to

Mexico

–

November

17,

2014

Press

Release

•

120-mile, 42”

and 48”

natural gas pipeline with 2.3 Bcf/d of initial capacity (expandable to 3.0 Bcf/d)

was completed ahead of schedule and is now operational

•

Long-term firm gas transportation agreement with MexGas Supply Ltd., a

subsidiary of Pemex 11

Lower Gulf Coast Projects Fuel Growth

OxyChem Corpus Christi Development Projects

•

OxyChem 110,000 Bbl/d propane export facility at Ingleside expected to begin

operations in 2015 •

OxyChem and MexiChem to build 1.2 billion lbs/year ethylene cracker in 2017

(34,000 Bbl/d ethane demand) |

2014 Wells Fargo Energy Symposium

•

System provides interconnects to every interstate pipeline in the region and

diverse market outlets; both are an advantage in attracting producer

contracts •

Local markets provide incremental downstream margins

•

Multiple gas sale outlets including direct connections to industrial and electric

generation markets Southcross Delivers Gas to Attractive

End-use Markets

12

YTD 2014 residue gas sales

Corpus Christi

Woodsboro

Gregory

NET Midstream

2.3 Bcf/d Mexico

Pipeline

Cheniere LNG

2.6 Bcf/d facility

Processing Plant

Markets

LNG Facility

82%

Direct End-use

Markets

18%

Pipelines |

2014 Wells Fargo Energy Symposium

Multiple NGL Markets in Corpus Christi

Area

13

Corpus Christi

Fractionator

Markets

Export Terminal

Bonnie View

Gregory

Trafigura Export

Active

Oxy Export

Approved

Martin Export

Active

Robstown

•

Advantaged Southcross footprint in expanding Gulf Coast

petrochemical infrastructure and NGL markets

•

End-use NGL markets provide attractive pricing and

market outlets

•

New NGL export terminals near Corpus Christi

•

Most North American ethane cracking is on the Gulf

Coast and is expanding

•

Attractive NGL customer base in the Corpus Christi

market |

2014 Wells Fargo Energy Symposium

14

Blue Chip Customer and Contract Base

Minimum

Volume

Commitments

44%

Acreage

Dedications

39%

Captive

Volumes

14%

Minimum volume commitments, acreage dedications and captive volumes should provide a

solid

and

growing

base

of

gas

supply

(1)

(1) Data from processed gas volumes for the Q4 guidance range.

Other

3% |

2014 Wells Fargo Energy Symposium

Updates on Recent Key Projects

15

Corpus Christi

Houston

Conroe

Lone Star

Woodsboro

Bonnie View

Gregory

Robstown

45 mile pipeline extending from Webb County

to rich gas system

35 MMcf/d MVC started November 2014

Webb Pipeline

100 MMcf/d sour gas treating facility; treated gas

flows into SXE rich gas system

Dedicated acreage in Dimmit and La Salle

counties producing sour gas

Valley Wells System

4 mile gathering pipeline

McMullen Lateral

9 mile pipeline extending into Karnes County

27 MMcf/d MVC started December 2014

Karnes Gathering

Holdings

SXE

Sour Gas Treating Facility

Fractionator

Processing Plant |

2014 Wells Fargo Energy Symposium

Rapid Growth of Southcross Processed

Gas Volumes

16

Average Processed Gas Volumes (MMBtu/d)

29% Organic

CAGR (excluding

acquisition)

38% compound annual growth rate in average daily processed gas volumes since

2011 2011

2012

2013

2014

-

50

100

150

200

250

300

350

400

450

500

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Oct. |

2014 Wells Fargo Energy Symposium

Significant Growth Achievable From

Existing Capacity

17

332

MMcf/d

381

MMcf/d

404

MMcf/d

440

MMcf/d

August

September

October

November

MTD

Southcross

Processing

Capacity

685

MMcf/d

1

As discussed on the November 7, 2014 SXE earnings call.

2

At margin of $0.50 to $0.75 per mcf/d.

Significant available processing capacity presents cash flow growth opportunity

Adding 200 MMcf/d of

gas represents $36

million to $55 million of

additional potential

annual margin

2014 Avg. Daily Processed Volumes

(MMcf/d) 0

50

100

150

200

250

300

350

400

450

500

550

600

650

2

1 |

2014 Wells Fargo Energy Symposium

600 miles of sweet and sour gas gathering lines

28,000 hp of compression

100 MMcf/d sour gas treating facility; expandable to

300 MMcf/d

~300,000 acres dedicated from 18 producers

Lancaster System

NGL Pipeline System

100 MMcf/d sour gas

treating facility

25,000 hp of compression

Valley Wells System

Drop-Down Inventory

18

Sour Gas Treating Facilities

Robstown Fractionator

63,000 Bbls/d NGL

fractionation facility

Long-term purity product

off-take agreements with

blue chip customers and

exporters under long term

contracts

Robstown Fractionator

Corpus Christi

70,000 Bbls/d Y-grade

pipeline 60,000 Bbls/d

Y-grade pipeline and

20,000 Bbls/d propane pipeline from Woodsboro Plant

to Robstown Fractionator

(under construction) |

2014 Wells Fargo Energy Symposium

•

Expected near-term path to 1.0x distribution coverage

–

Recent new minimum volume commitment contracts are expected to add

$7 million to $8 million in full quarter Adjusted EBITDA

–

Existing base of strong producer customers is expected to continue to

grow production at current commodity price levels

•

Existing commitment from Holdings to forgo subordinated unit distributions

while coverage is less than 1.0x provides support for common units

•

Expect to fill processing plant capacity within 12 to 18 months

–

Potential to start-up new processing plant in 2016

•

Supplement organic growth through expected drop-downs

Enable Consistent Distribution Growth

19

Expect to

achieve at

least 1.0x

coverage of

common units

in Q1 2015

Expect to grow

distributions

in 2015

Expect further

growth

through filling

asset capacity

& completing

drop-downs |

2014 Wells Fargo Energy Symposium

20

NYSE Ticker

Total Units

Unit Price

Market Capitalization

SXE

50.9 million units

(1)

$14.30

(2)

$728 million

(2)

$458 million

Debt at Sept 30, 2014

Quarterly Distribution

$0.40 per unit ($1.60 per unit on an annualized basis)

Current Yield

11.2%

(2)

(1)

Includes 14.9 million Class B convertible units; excludes GP units

(2)

As of December 5, 2014

Southcross Fact Sheet |

2014 Wells Fargo Energy Symposium

We

believe

that

Adjusted

EBITDA

is

a

widely

accepted

financial

indicator

of

our

operational

performance

and

our

ability

to

incur

and

service

debt,

fund

capital expenditures and make distributions.

We define Adjusted EBITDA as net income/loss, plus interest expense, income tax

expense, depreciation and amortization expense, equity in losses of joint

venture investments, certain non-cash charges (such as non-cash unit-based compensation, impairments, loss on extinguishment of debt and

unrealized losses on derivative contracts), major litigation costs net of

recoveries, transaction-related costs, revenue deferral adjustment, loss on sale of

assets and selected charges that are unusual or non-recurring; less interest

income, income tax benefit, unrealized gains on derivative contracts, equity

in

earnings

of

joint

venture

investments

and

selected

gains

that

are

unusual

or

non-recurring.

Adjusted EBITDA is used as a supplemental measure by our management and by external

users of our financial statements, such as investors, commercial banks,

research analysts and others, to assess: •

the financial performance of our assets without regard to financing methods,

capital structure or historical cost basis; •

the

ability

of

our

assets

to

generate

cash

sufficient

to

support

our

indebtedness

and

make

future

cash

distributions;

•

operating

performance

and

return

on

capital

as

compared

to

those

of

other

companies

in

the

midstream

energy

sector,

without

regard

to financing or capital structure; and

•

the attractiveness of capital projects and acquisitions and the overall rates of

return on investment opportunities. Adjusted EBITDA is not a financial

measure presented in accordance with GAAP. We believe that the presentation of this non-GAAP financial measure

provides useful information to investors in assessing our financial condition,

results of operations and cash flows from operations. Net income/loss is the

GAAP

measure

most

directly

comparable

to

Adjusted

EBITDA,

and

a

reconciliation

of

Adjusted

EBITDA

to

net

income/loss

is

included

in

this

presentation.

Adjusted

EBITDA

should

not

be

considered

an

alternative

to

net

income,

operating

cash

flow

or

any

other

measure

of

financial

performance presented in accordance with GAAP. Non-GAAP financial

measures have important limitations as an analytical tool because each

excludes some but not all items that affect the most directly comparable GAAP

financial measure. You should not consider Adjusted EBITDA in isolation

or

as

a

substitute

for

analysis

of

our

results

as

reported

under

GAAP.

Because

Adjusted

EBITDA

may

be

defined

differently

by

other

companies

in

our

industry,

our

definition

of

this

non-GAAP

financial

measure

may

not

be

comparable

to

similarly

titled

measures

of

other

companies,

thereby

diminishing

its utility.

Non-GAAP Financial Measures

21 |

2014 Wells Fargo Energy Symposium

22

Reconciliation to Adjusted EBITDA

(Dollars in Thousands)

Three Months Ended,

9/30/2013

12/31/2013

3/31/2014

6/30/2014

9/30/2014

Reconciliation of net loss to Adjusted EBITDA:

Net (loss) income

$

(4,069)

$

674

$

(1,289)

$

(2,961)

$

(24,778)

Add (deduct):

Depreciation and amortization expense

9,447

8,590

8,528

8,978

11,629

Interest expense

3,587

3,855

2,973

1,771

4,596

Loss on extinguishment of debt

-

-

-

-

2,316

Unit-based compensation

552

542

529

1,082

609

Income tax (benefit) expense

125

(19)

8

56

69

Unrealized (gain) loss

-

(120)

(32)

175

207

Revenue deferral adjustment

-

-

1,182

444

444

Gain on sale of assets

-

(25)

-

(45)

-

Loss on asset disposal

-

-

4

-

334

Major litigation costs, net of recoveries

-

517

273

630

488

Transaction-related costs

-

-

303

4

10,506

Equity in losses of joint venture investments

-

-

-

-

3,308

Impairment of assets

-

-

-

-

1,556

Other, net

20

24

18

44

-

Adjusted EBITDA

$

9,662

$

14,038

$

12,497

$

10,178

$

11,284 |