Attached files

| file | filename |

|---|---|

| 8-K - 8-K - Southcross Energy Partners, L.P. | d834295d8k.htm |

2014

Investor Day December 8, 2014

Exhibit 99.1 |

2014 Investor Day

Cautionary Statements

1

This presentation contains forward-looking statements and information. Forward-looking

statements include, without limitation, any statement that may project, indicate or imply future

results, events, performance or achievements, and may contain the words “expect,”

“intend,” “plan,” “anticipate,” “estimate,” “believe,” “will be,” “will continue,” “will likely result” and

similar expressions, or future conditional verbs such as “may,” “will,”

“should,” “would” and “could.” In addition, any statement concerning future financial performance (including future

revenues, earnings or growth rates), ongoing business strategies or prospects, and possible actions

taken by us, our subsidiaries or our affiliates, are also forward-looking statements. These

forward-looking statements involve external risks and uncertainties, including, but not limited to, those described under the section entitled “Risk Factors” included in our 2013

Annual Report on Form 10-K (as updated by our Quarterly Reports on Form 10-Q).

Forward-looking statements are based on current expectations and projections about future events and

are inherently subject to a variety of risks and uncertainties, many of which are beyond the

control of our management team. All forward-looking statements in this presentation and in any other written or oral forward-looking statements attributable to us, or to persons

acting on our behalf, are expressly qualified in their entirety by these risks and uncertainties. These

risks and uncertainties include, among others:

the volatility of natural gas, crude oil and NGL prices and the price and demand of products derived

from these commodities;

competitive conditions in our industry and the extent and success of producers increasing production

or replacing declining production and our success in obtaining new sources of supply;

industry conditions and supply of pipelines, processing and fractionation capacity relative to

available natural gas from producers;

our dependence upon a relatively limited number of customers for a significant portion of our

revenues; actions taken,

inactions or non-performance by third parties, including suppliers, contractors, operators, processors, transporters and customers;

our ability to effectively recover NGLs at a rate equal to or greater than our contracted rates with

customers; our ability to

produce and market NGLs at the anticipated differential to NGL index pricing;

our access to markets enabling us to match pricing indices for purchases and sales of natural gas and

NGLs; our ability to

complete projects within budget and on schedule, including but not limited to, timely receipt of necessary government approvals and permits, our ability to control the costs of

construction and other factors that may impact projects; our ability to consummate

acquisitions, successfully integrate the acquired businesses and realize anticipated cost savings and other synergies from any acquisitions, including in respect of our

acquisition of the TexStar rich gas system assets; our ability to manage over time

changing exposure to commodity price risk;

the effectiveness of our hedging activities or our decisions not to undertake hedging activities; our access to financing and

ability to remain in compliance with our financing covenants;

our ability to generate sufficient operating cash flow to fund our quarterly distributions; changes in general economic

conditions; the effects of

downtime associated with our assets or the assets of third parties interconnected with our systems;

operating hazards, fires, natural disasters, weather-related delays, casualty losses and other

matters beyond our control;

the failure of our processing and fractionation plants to perform as expected, including outages for

unscheduled maintenance or repair;

the effects of laws and governmental regulations and policies; the effects of existing and

future litigation; and

other financial, operational and legal risks and uncertainties detailed from time to time in our

filings with the U.S. Securities and Exchange Commission.

Developments in any of these areas could cause actual results to differ materially from those

anticipated or projected, affect our ability to maintain distribution levels and/or access

necessary financial markets, or cause a significant reduction in the market price of our common

units. The foregoing list of risks and uncertainties may not contain all of the risks and uncertainties that

could affect us. In addition, in light of these risks and uncertainties, the matters referred to

in the forward-looking statements contained in this presentation may not, in fact, occur.

Accordingly, undue reliance should not be placed on these statements. We undertake no obligation

to publicly update or revise any forward-looking statements as a result of new information, future

events or otherwise, except as otherwise required by law.

|

2014 Investor Day

We

believe

that

Adjusted

EBITDA

is

a

widely

accepted

financial

indicator

of

our

operational

performance

and

our

ability

to

incur

and

service

debt,

fund

capital expenditures and make distributions.

We define Adjusted EBITDA as net income/loss, plus interest expense, income tax

expense, depreciation and amortization expense, equity in losses of joint

venture investments, certain non-cash charges (such as non-cash unit-based compensation, impairments, loss on extinguishment of debt and

unrealized losses on derivative contracts), major litigation costs net of

recoveries, transaction-related costs, revenue deferral adjustment, loss on sale of

assets and selected charges that are unusual or non-recurring; less interest

income, income tax benefit, unrealized gains on derivative contracts, equity

in

earnings

of

joint

venture

investments

and

selected

gains

that

are

unusual

or

non-recurring.

Adjusted EBITDA is used as a supplemental measure by our management and by external

users of our financial statements, such as investors, commercial banks,

research analysts and others, to assess: •

the financial performance of our assets without regard to financing methods,

capital structure or historical cost basis; •

the

ability

of

our

assets

to

generate

cash

sufficient

to

support

our

indebtedness

and

make

future

cash

distributions;

•

operating

performance

and

return

on

capital

as

compared

to

those

of

other

companies

in

the

midstream

energy

sector,

without

regard

to financing or capital structure; and

•

the attractiveness of capital projects and acquisitions and the overall rates of

return on investment opportunities. Adjusted EBITDA is not a financial

measure presented in accordance with GAAP. We believe that the presentation of this non-GAAP financial measure

provides useful information to investors in assessing our financial condition,

results of operations and cash flows from operations. Net income/loss is the

GAAP

measure

most

directly

comparable

to

Adjusted

EBITDA,

and

a

reconciliation

of

Adjusted

EBITDA

to

net

income/loss

is

included

in

this

presentation.

Adjusted

EBITDA

should

not

be

considered

an

alternative

to

net

income,

operating

cash

flow

or

any

other

measure

of

financial

performance presented in accordance with GAAP. Non-GAAP financial

measures have important limitations as an analytical tool because each

excludes some but not all items that affect the most directly comparable GAAP

financial measure. You should not consider Adjusted EBITDA in isolation or

as a

substitute

for

analysis

of

our

results

as

reported

under

GAAP.

Because

Adjusted

EBITDA

may

be

defined

differently

by

other

companies

in

our

industry,

our

definition

of

this

non-GAAP

financial

measure

may

not

be

comparable

to

similarly

titled

measures

of

other

companies,

thereby

diminishing

its utility.

Non-GAAP Financial Measures

2 |

2014 Investor Day

Overview

David Biegler

Chairman

Operations and Strategy

John Bonn

President and Chief Executive

Officer

Financial Overview

and Outlook

Michael Anderson

SVP and Chief Financial Officer

Presenters

3 |

2014 Investor Day

David Ash

VP, Corporate Development

David Lawrence

VP, Treasury & Investor Relations

Corey Lothamer

VP, Gas Marketing & Supply

Other Management Team Attendees

4

David Mueller

VP, Commercial & Operations Support

Gerardo Rivera

VP, Natural Gas Liquids |

2014 Investor Day

5

30+ Years’

Experience

•

President & COO

Southcross Energy

•

President

NiSource Midstream Services

•

Owner, President

Ranger Interests, Inc.

•

VP, Commercial (Western Region)

Enterprise Product Partners

•

Director, Commercial (Permian Basin)

GulfTerra Energy Partners

•

Director, Commercial

El Paso Field Services

•

Manager, Northeast Marketing

Delhi Gas Pipeline

•

VP, Business Development

Triumph Natural Gas

President & Chief Executive Officer

John E. Bonn

•

Bachelor of Science, Agricultural Engineering, Texas A&M

•

Officer, United States Army and Army Reserves

•

Board member, Texas Aggie Corps of Cadets Association

•

Past board member, Marcellus Shale Coalition,

•

New Mexico Oil & Gas Association

•

Past president, Natural Gas Society of North Texas |

2014 Investor Day

Key Executive Management

6

John Bonn

President & CEO

Corey

Lothamer

VP

Gas Supply

& Marketing

Gerardo

Rivera

VP

NGLs

Gaylon

Gray

VP

Pipeline

Operations &

Engineering

David

Ishmael

VP

Plant

Operations &

Engineering

Michael

Anderson

Chief

Financial

Officer

Phil

Mezey

EVP

Business

Development

David

Ash

VP

Corporate

Development

David Biegler

Chairman |

2014 Investor Day

Name / Title

Years of

Experience

Previous Experience

David Biegler

Chairman

45+

•

Chairman and CEO

•

Chairman and Co-Founder

•

Vice Chairman, President and COO

•

Chairman, President and CEO

•

President and COO

Estrella Energy

Regency Gas Services

TXU Corp

ENSERCH Corp

Lone Star Gas Co.

John Bonn

President & CEO

30+

•

President

•

VP, Commercial (Western Region)

•

Director, Commercial (Permian Basin)

•

Director, Commercial

Nisource Midstream Services

Enterprise Product Partners

GulfTerra Energy Partners

El Paso Field Services

Michael Anderson

SVP & Chief Financial Officer

25+

•

SVP and CFO

•

CFO; later serving as Chairman and CEO

•

VP, M&A

Exterran and Exterran Partners

Azurix Corp.

JPMorgan Chase & Co.

Corey Lothamer

VP, Gas Marketing & Supply

10+

•

Gas Supply

•

Project Engineer

Crosstex Energy Services

Raytheon Company

Gerardo Rivera

VP, Natural Gas Liquids

25+

•

Strategy, Planning, Marketing and M&A

•

Director

Vermilion Energy, Inc.

ConocoPhilips

David Ash

13+

•

CFO

•

Partner

•

SVP

BlackBrush /

TexStar

Donovan

Capital

FBR Capital Markets

David Mueller

30+

•

VP, Finance &

Administration

•

VP,

Controller

•

VP

Texas Independent Energy

Enserch Energy Services

Enserch Development

David Lawrence

VP, Treasury & Investor Relations

15+

•

Managing

Director

•

Manager

FTI Consulting

Deloitte

Attending Management Team Bios

7

VP, Corporate Development

VP, Commercial & Operations Support |

Overview –

David Biegler |

2014 Investor Day

The Southcross Advantage

9

Significant

scale

of

pipeline

and

processing assets

Operating

stability

through

interconnected system

Extensive

footprint

in

the

prolific

Eagle

Ford and Gulf Coast area

Blue

chip,

active

producer

customer

base

Full

spectrum

of

services

creates

competitive and economic advantages

Fractionation

assets

are

a

significant

differentiator

Premium

and

growing

markets

for

gas,

NGLs and condensate

Corpus

Christi

region

is

growing

rapidly

and serving new export markets

Fully utilize existing capacity

Develop organic growth

projects

Drop-downs

Acquisitions

Premier Strategic Platform

in the Eagle Ford

Fully Integrated

Midstream Platform

Four Drivers of

Growth |

2014

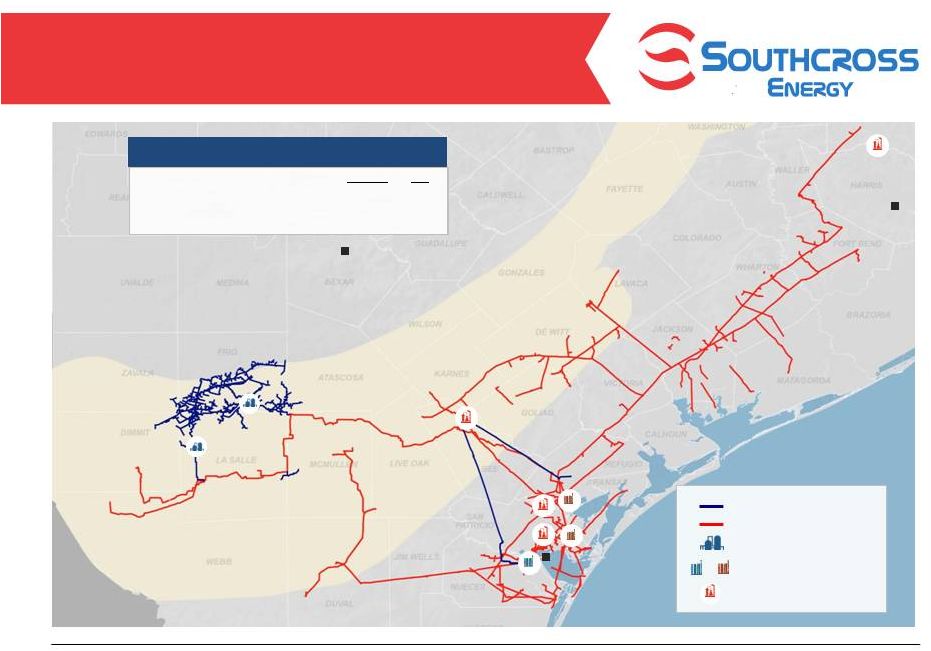

Investor Day Pipeline (miles)

Gas Processing Capacity (MMcf/d)

Fractionation Capacity (MBbls/d)

Holdings

655

-

63

SXE

3,030

685

27

South Texas Assets

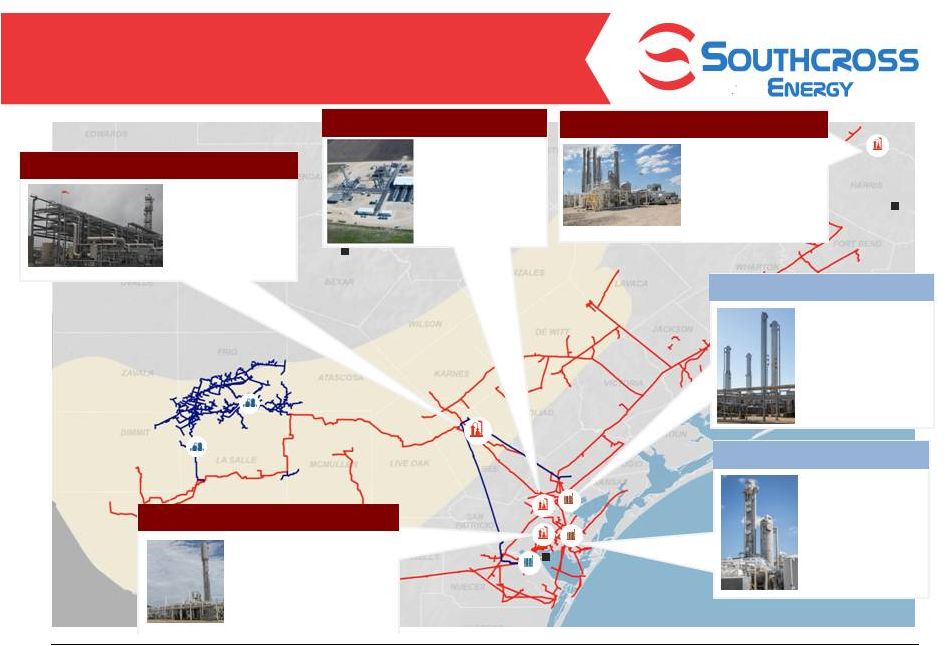

Premier Strategic Footprint with Scale to

Succeed in the Eagle Ford

10

Corpus Christi

San Antonio

Houston

Conroe

Lone Star

Woodsboro

Robstown

Pipeline (miles)

Gas Processing Capacity (MMcf/d)

Fractionation Capacity (MBbls/d)

Holdings

655

-

63

SXE

3,030

685

27

Bonnie View

Holdings

SXE

Sour Gas Treating Facility

Fractionator

Processing Plant

Gregory |

2014 Investor Day

2013

Bee Line

2013

Kenedy Line

2013

McMullen Lateral

2013

Bonnie View Plant

2013

Lone Star Plant

History of Growth

11

2012

Monco

Acquisition

2012

McMullen

Pipeline

2012

Woodsboro

Plant

2012-2014

Lancaster System

2012

T2 Pipeline

2014

Onyx Acquisition

2014

McMullen Lateral

McMullen Gathering

Acquisition

2014

Webb Pipeline

2014

Valley Wells

2011

Tennessee Pipeline

2015

NGL System

2012

T2 Pipeline

2015

Robstown

Fractionator

Holdings

SXE

Sour Gas Treating Facilities

Fractionator

Processing Plant |

2014 Investor Day

Partnership Structure

Southcross Holdings LP

(“Holdings”)

Southcross Energy

Partners, L.P.

(NYSE: SXE)

Affiliate Assets

Public

43% LP Interest

2% GP Interest

57% LP Interest

Southcross Energy

Partners GP, LLC

Financial sponsor ownership through various holding companies

12

100% Interest |

2014 Investor Day

13

Strong Equity Sponsors with a History

of Industry Success

Fund Description

Other Relevant Investments

•

$3.0 billion assets under management

•

Originally managed an investment portfolio solely for

Harvard University

•

Invested over $3.3 billion in 70 companies since 1991

•

Regency Gas Partners (realized)

•

Blueknight Energy Partners (current)

•

$15.1 billion assets under management

•

Solely invests in energy projects, companies and

related infrastructure

•

Invested $16.6 billion through 300 projects or

companies in 35 countries on six continents since 1982

•

BlackBrush Oil & Gas (realized)

•

Bolivia-Brazil Gas Pipeline (current)

•

FourPoint Energy (current)

•

Piñon Gathering Company (current)

•

$1.2 billion assets under management

•

Focused on midstream and upstream oil and gas

companies

•

Principals have invested over $1 billion the past 14

years in the space

•

Regency Gas Partners (realized)

•

TexStar Midstream I (realized)

•

BlackBrush Oil & Gas (realized)

•

Align Midstream Partners (current)

•

Pivotal Petroleum Partners (current)

•

Petro Waste Environmental Partners (current)

•

$13 billion in capital commitments

•

Focuses on investing in power generation, midstream

oil and gas, electric transmission, environmental

infrastructure and energy services sectors of North

America’s energy infrastructure

•

Cardinal Gas Storage Partners (realized)

•

Summit Midstream (current)

•

Alaska Midstream (current)

•

Rimrock Midstream (current)

•

Sendero Midstream Partners (current)

•

USD Group LLC (current)

•

Over $16 billion in assets under management with

over $2 billion in oil and gas infrastructure

•

300 person team dedicated to the business of energy

investment with over $25 billion in energy

transactions since 2004

•

Regency Gas Partners (realized)

•

Howard Energy Partners (realized)

•

Freeport LNG (current)

•

Summit Midstream Partners, LLC (current)

•

Harvest Pipeline (current) |

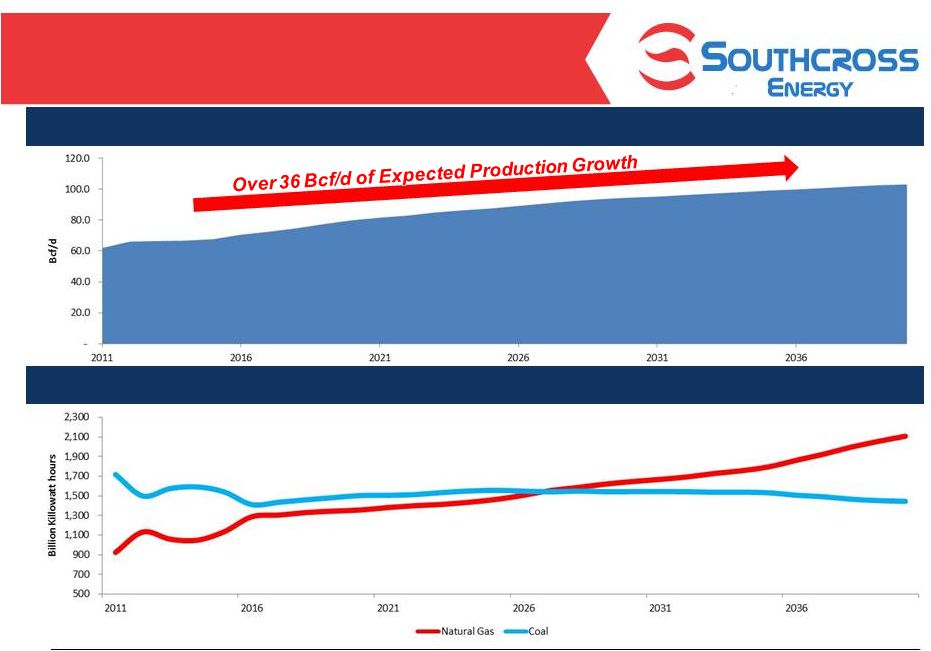

U.S.

Energy Highlights 14

Source: U.S. Energy Information Administration

Note: Petroleum production includes crude oil, natural gas liquids, condensates,

refinery processing gain, and other liquids, including biofuels; barrels per day oil equivalent were

calculated using a conversion factor of 1 barrel oil equivalent=5.55 million

British thermal units (Btu) The U.S. is the largest petroleum and natural

gas-producing country in the world 2008

2014E

Petroleum

Natural Gas

United States

Russia

Saudi Arabia

The U.S. is expected to produce more than 25

MMBOE in 2014, over 40% growth in 6 years

2014 Investor Day |

U.S.

Energy Highlights 15

Source: EIA

Power Generation by Source

U.S. Natural Gas Production

Natural gas is surpassing coal as the main power

generation source

2014 Investor Day |

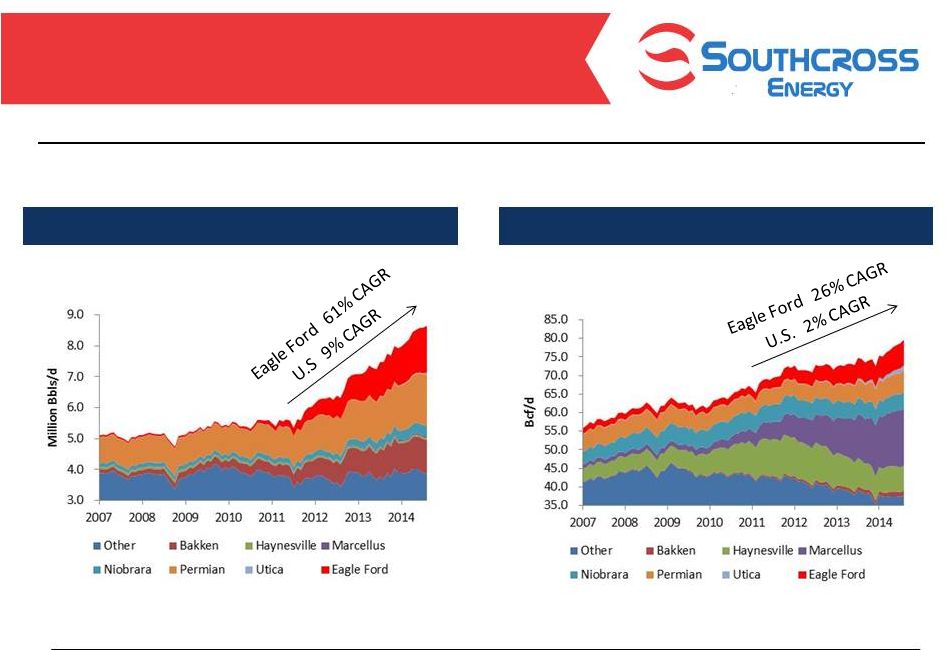

Eagle

Ford Highlights 16

Source: EIA

The Eagle Ford is a major driver of U.S. oil and natural gas production growth

U.S. Oil Production per Day

U.S. Natural Gas Production per Day

2014 Investor Day |

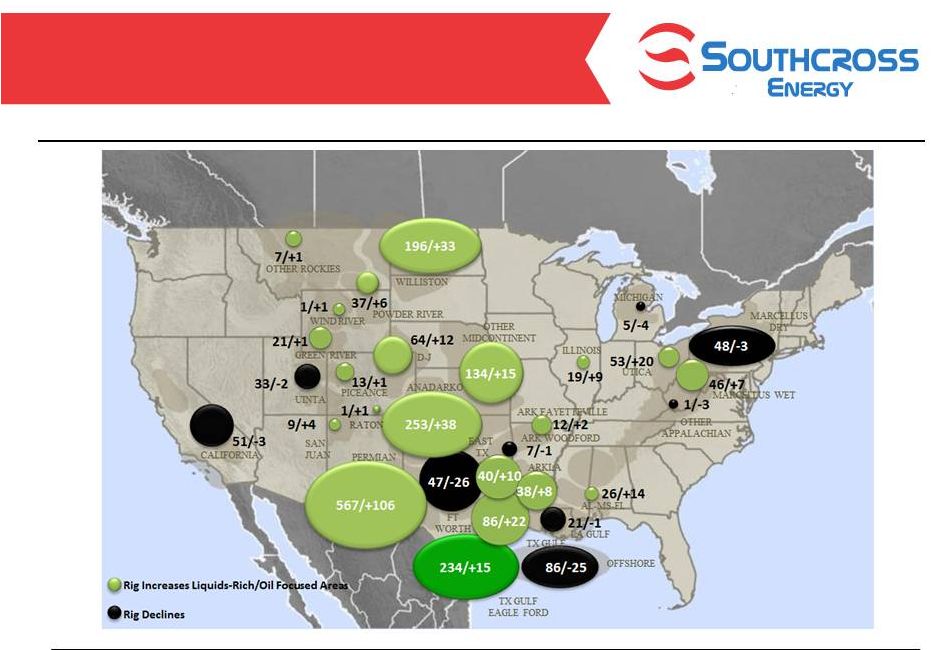

The

Eagle Ford is One of the Most Active Plays in the U.S.

17

Eagle Ford rig count is up 15 rigs since November 1, 2013

Active Rigs / Yearly Change

2014 Investor Day

Source: Bentek |

U.S.

Gas Production Growth Led by the Texas Gulf Coast Region

18

Source: Bentek

Texas Gulf Coast Region Gas Production per Day

2014 Investor Day

The Texas Gulf Coast Region is projected to account for an additional 4 Bcf/d U.S.

production by 2019 |

Request for Proposal Summary

Proposed Contract and Deal Terms

Texas Gulf Coast Production Expected to

Exceed Processing Capacity

19

(1) Bentek Eagle Ford and Texas Gulf Coast production estimates

Note: Excludes plant retirements.

Texas Gulf Coast Region is forecasted to need an additional 2.0 to 4.5 bcf/d of

processing capacity by 2019

Potential

4.5 Bcf/d

Shortfall

in Cryo

Capacity

2014 Investor Day |

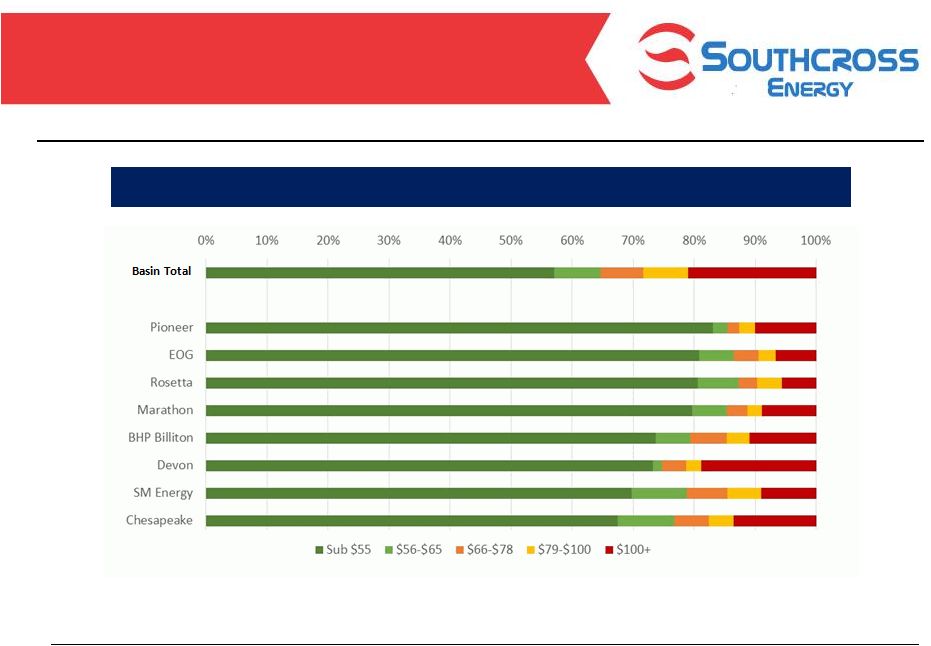

Eagle

Ford Has Attractive Producer Economics

20

U.S. Oil Play Break-Even Assessment at December 1, 2014 Forward Strip

Prices 2014 Investor Day

Eagle Ford

Permian Basin

Bakken

Marginal Economics

12-Month Strip

$/Bbl (WTI)

Source: RBC Capital Markets |

2014 Investor Day

Most Eagle Ford drilling since 2011 would have been economic under today’s lower

oil prices Note: All Horizontal wells drilled since 2011; assumes $7.5MM

D&C in East Eagle Ford and $6.8MM D&C in West Eagle Ford and $4/MMBtu natural gas price. Breakeven cost

estimated at 10% IRR.

Source: BTU Analytics, LLC, Data as of November 1, 2014

21

Percentage of Wells by Operator with a Greater than 10% IRR

Eagle

Ford

Breakeven

Price

at

10%

IRR |

2014 Investor Day

Gas Producers More Resistant to Current

Change in Commodity Landscape

22

Southcross Processed Volumes

% Change

Oct. 1

Nov. 1

Dec. 1

Oct. 1 - Dec. 1

Nov. 1 - Dec. 1

Commodity Prices:

Crude per Barrel

90.73

$

80.54

$

69.00

$

(24.0%)

(14.3%)

Condensate per Barrel

81.66

72.49

62.10

(24.0%)

(14.3%)

Natural Gas per MMbtu

4.05

3.63

4.14

2.2%

14.0%

NGL Basket per Gallon

0.77

0.68

0.57

(26.7%)

(16.9%)

Rich Gas Revenue to Producers per mcf

11.19

$

9.97

$

9.20

$

(17.8%)

(7.7%)

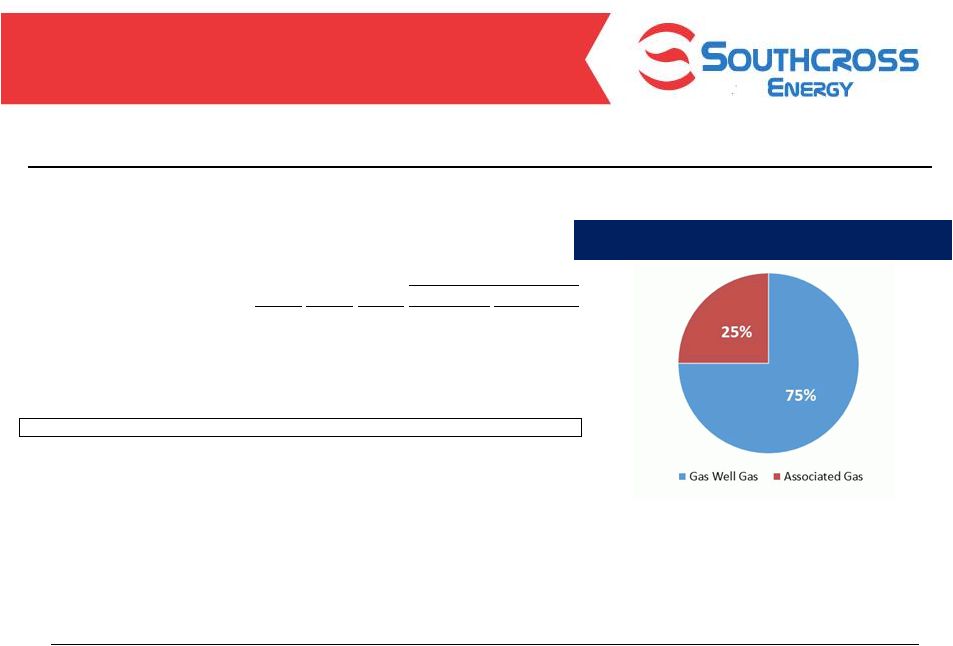

Gas well gas producers account for approximately 75% of Southcross’ processed volumes and have

seen their revenue decline approximately 8% over the last month compared to 14% for crude

producers

Note: Assumptions include, 5.75 GPM gas, normal processing plant recoveries, 57 barrels of condensate

per 1 MMcf and a condensate price equal to 90% of the crude price.

|

Operations and Strategy –

John Bonn |

2014 Investor Day

The Southcross Advantage

24

Significant

scale

of

pipeline

and

processing assets

Operating

stability

through

interconnected system

Extensive

Footprint

in

the

prolific

Eagle

Ford and Gulf Coast area

Blue

chip,

active

producer

customer

base

Full

spectrum

of

services

creates

competitive and economic advantages

Fractionation

assets

are

a

significant

differentiator

Premium

and

growing

markets

for

gas, NGLs and condensate

Corpus

Christi

region

is

growing

rapidly and serving new export markets

Fully utilize existing capacity

Develop organic growth

projects

Drop-downs

Acquisitions

Premier Strategic Platform

in the Eagle Ford

Fully Integrated

Midstream Platform

Four Drivers of

Growth |

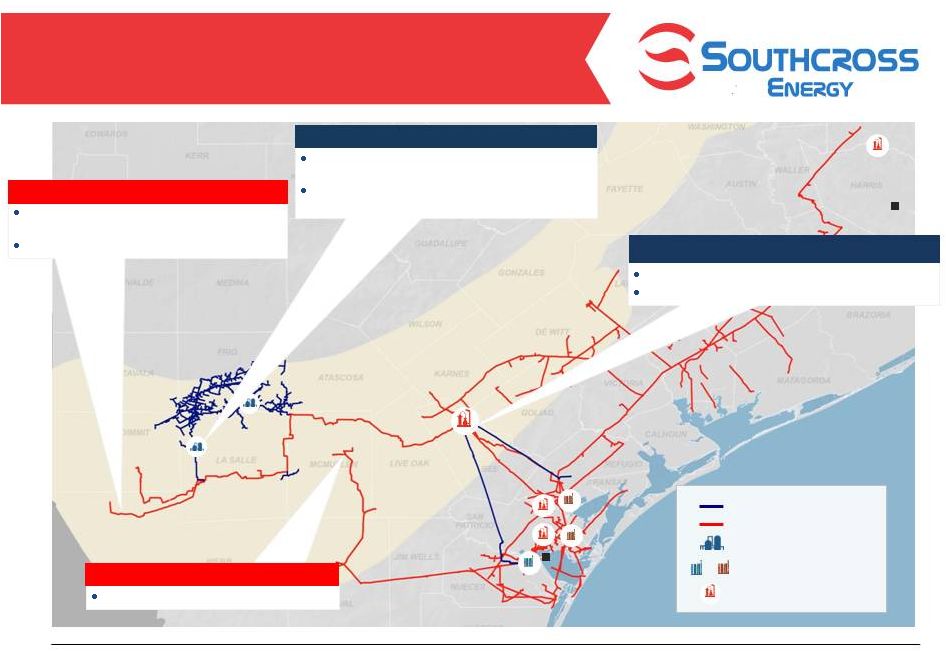

2014 Investor Day

Significant Scale of Pipeline and

Processing Assets

Corpus Christi

San Antonio

Houston

Conroe

Lone Star

Woodsboro

Bonnie View

Gregory

Robstown

•

Year Built:

2012

•

Capacity:

200 MMcf/d

Woodsboro Processing Plant

Lone Star Processing Plant

•

Year Built:

2013

•

Capacity:

300 MMcf/d

•

Year Enhanced:

2012

•

Capacity:

50 MMcf/d

Conroe Processing Plant

•

Year Refurbished:

2013

•

Capacity:

135 MMcf/d

Gregory Processing Plant

Bonnie View Fractionator

•

Year Built:

2013

•

Capacity:

22.5 MBbls/d

•

Year Refurbished:

2013

•

Capacity:

4.8 MBbls/d

Gregory Fractionator

25 |

2014 Investor Day

Source: BENTEK Energy

Major Eagle Ford Midstream Company

26

2,230

1,575

1,525

1,100

685

500

400

340

200

200

200

175

150

135

0

500

1,000

1,500

2,000

EPD

DPM

ETP

KMP

SXE

XOM

APL

WMB

Formosa

WES

Howard

RGP

BWP

Hilcorp

Southcross is the 5

largest Eagle Ford midstream company by processing capacity

th |

2014 Investor Day

Operating Stability through

Interconnected System

27

Gregory

Robstown

Corpus Christi

Bonnie View

Woodsboro

Gregory

Corpus Christi

Lone Star

Y-Grade Flow

Lone Star

Woodsboro

Rich Gas Flow

Holdings

SXE

Fractionator

Processing Plant |

2014 Investor Day

Well Positioned for Current Eagle Ford

Activity

28

Permits 2012-2014 |

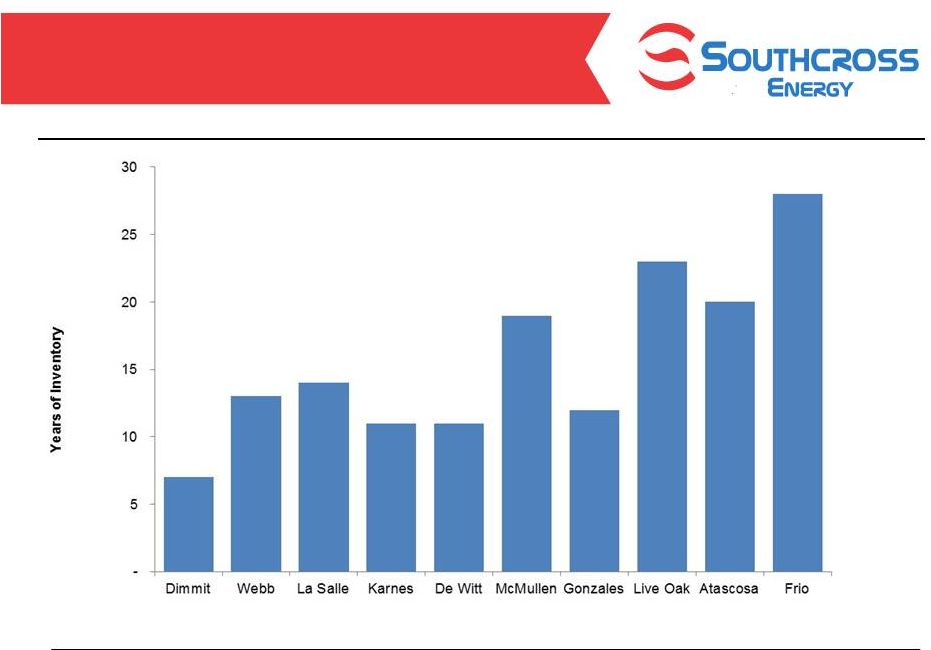

Attractive Supply Sourcing

29

Source: BTU Analytics, Drillinginfo

Note: Shading indicates counties where Southcross has operations

Production (MMcf/d)

Inventory

Y/Y

Eagle Ford Total

Eagle Ford Cumulative

County

2014 YTD

Growth

Locations

Wells Drilled

% Drilled

Webb

1,795

11%

8,309

1,499

18%

De Witt

645

31%

4,662

709

15%

Dimmit

746

32%

6,570

1,513

23%

La Salle

642

13%

11,034

1,096

10%

Karnes

639

20%

7,716

1,019

13%

McMullen

390

22%

9,921

672

7%

Live Oak

328

26%

3,452

386

11%

Gonzales

171

15%

3,424

501

15%

Lavaca

101

30%

2,484

101

4%

Atascosa

58

59%

6,254

351

6%

Bee

53

-9%

225

24

11%

Frio

29

10%

2,792

185

7%

Grimes

34

-5%

N/A

N/A

N/A

Duval

43

-12%

230

6

3%

Brazos

26

65%

1,180

130

11%

Fayette

53

-5%

1,229

76

6%

Zavala

15

27%

3,204

135

4%

Maverick

11

19%

1,272

68

5%

Burleson

25

152%

N/A

N/A

N/A

2014 Investor Day

Southcross’ footprint is in prolific gas production counties with significant drilling inventory

|

30

The major producing Eagle Ford counties have a weighted average inventory of 13

years Source: BTU Analytics, Drillinginfo.

Note: Production data listed is 2014 YTD average; years of inventory equals

drilling locations divided by current pace of drilling. 746

MMcf/d

1,795

MMcf/d

642

MMcf/d

639

MMcf/d

645

MMcf/d

390

MMcf/d

171

MMcf/d

328

MMcf/d

58

MMcf/d

29

MMcf/d

2014 Investor Day

Lengthy Gas Supply Inventory in Eagle

Ford |

2014 Investor Day

solid and growing base of gas supply

31

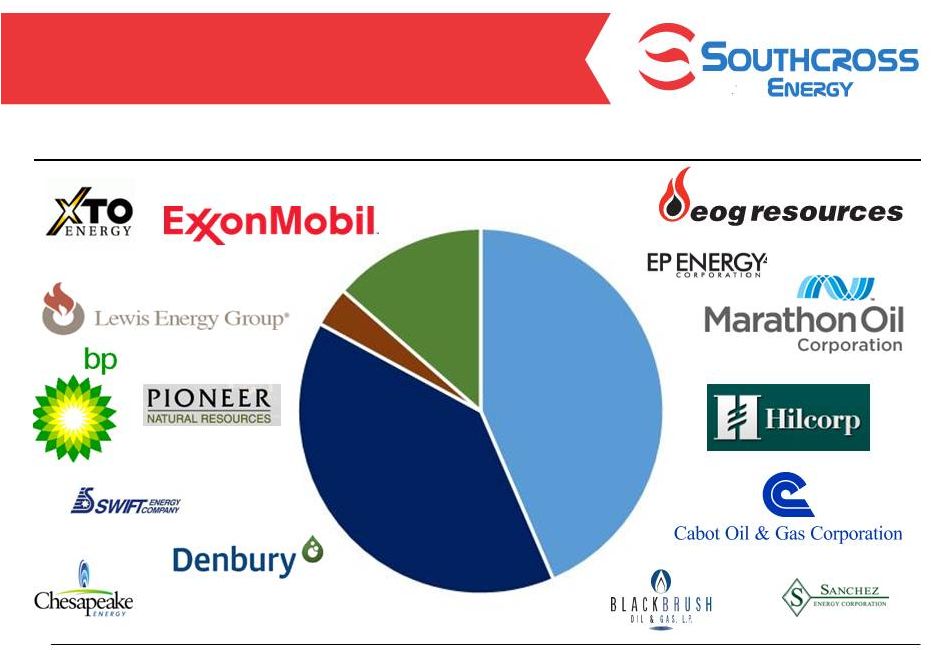

Blue Chip Customer and Contract Base

Minimum

Volume

Commitments

44%

Acreage

Dedications

39%

Captive

Volumes

14%

Minimum volume commitments, acreage dedications and captive volumes should provide

a (1) Data from processed gas volumes for the Q4 guidance range.

Other

3%

(1) |

2014 Investor Day

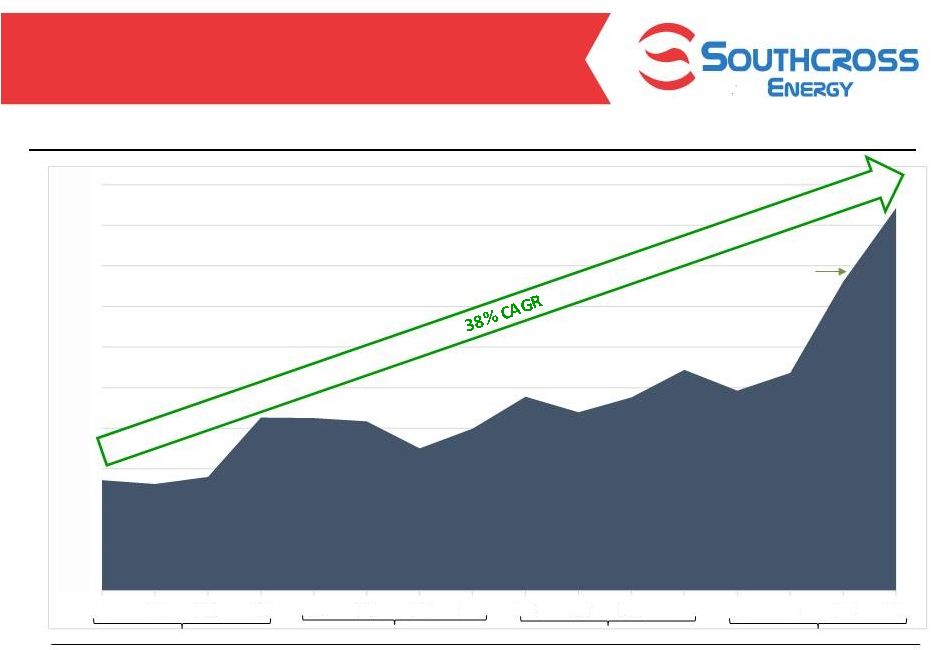

Rapid Growth of Southcross Processed

Gas Volumes

32

Average Processed Gas Volumes (MMBtu/d)

29% Organic

CAGR (excluding

acquisition)

2011

2012

2013

2014

38% compound annual growth rate in average daily processed gas volumes since

2011 -

50

100

150

200

250

300

350

400

450

500

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Oct. |

2014 Investor Day

Focus on Eagle Ford Region

33

Karnes / De Witt

Region

Frio / La Salle

Region

Webb /

Dimmit

Region

McMullen

Region

Corpus Christi

Region

Pipeline (miles)

Gas Processing Plant Capacity (MMcf/d)

Fractionation Capacity (MBbls/d)

Holdings

655

-

63

SXE

3,030

685

27

South Texas

Holdings

SXE

Sour Gas Treating Facilities

Fractionator

Processing Plant |

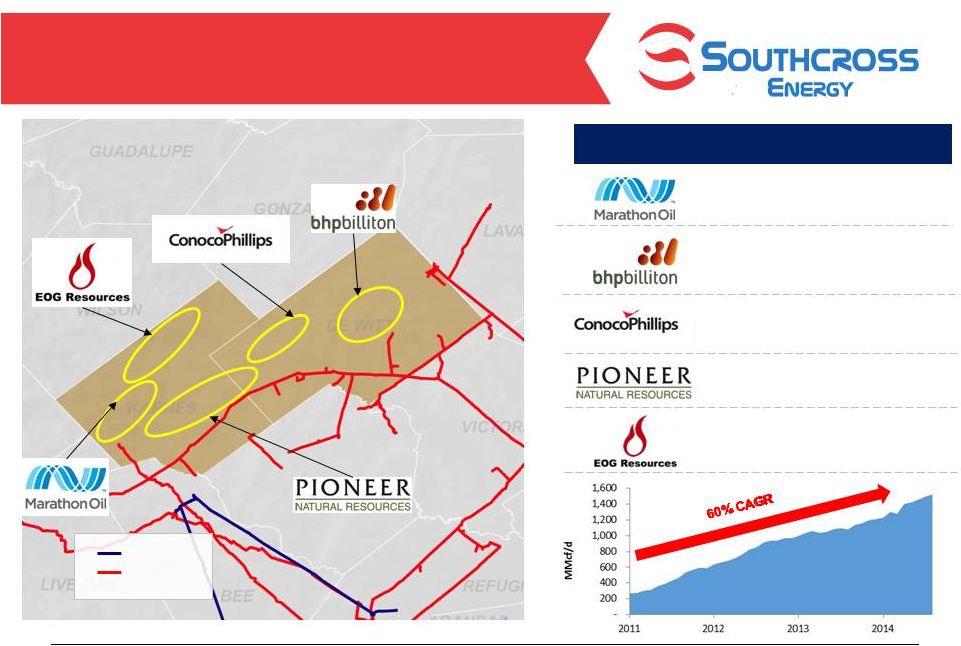

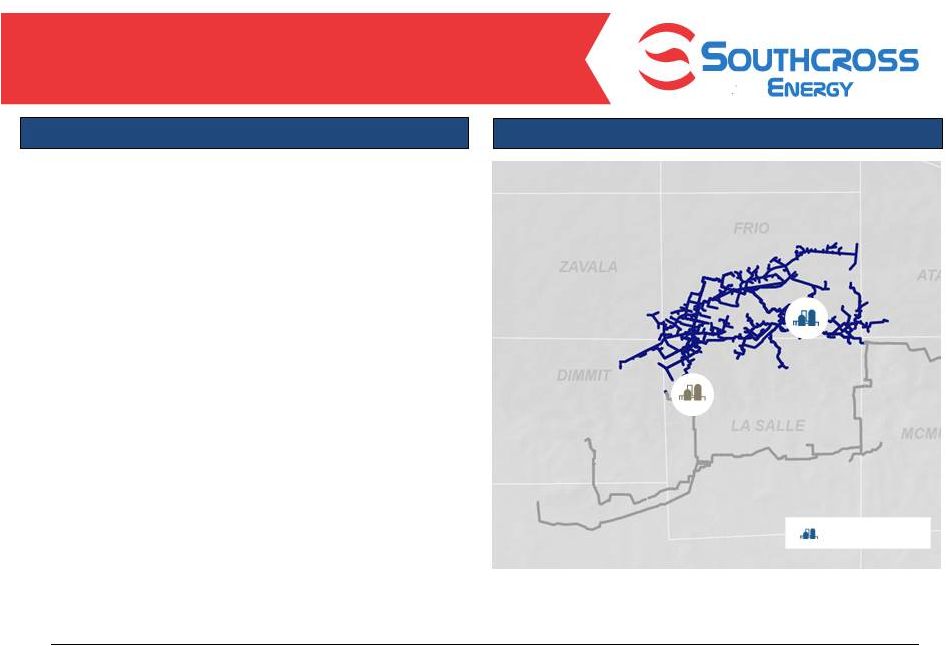

2014 Investor Day

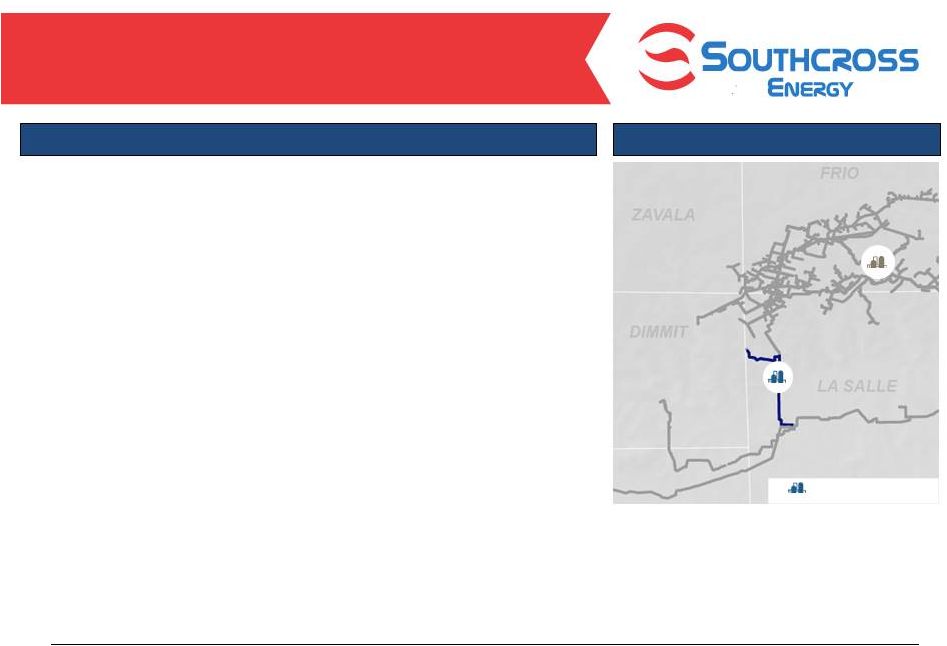

Frio / La Salle Region

34

Selected Producer Highlights

•

100 MMcf/d of current production

•

Operating 4 rigs in La Salle

•

Breakeven oil price of $50 per barrel

•

50% of 3Q14 capex spend in the Eagle

Ford

•

12 MMcf/d of current production

•

Operating 4 rigs in Frio

•

Estimated $700 million 2015 capex spend

in the Eagle Ford

•

21 MMcf/d of current production

•

Operating 3 rigs in Frio/LaSalle/Dimmitt

•

25 MMcf/d of current production

•

Operating 4 rigs in the area

•

Recently acquired by Ares Capital

Note: Monthly producer data from Drilling Info and relates to their production in

the noted counties. Holdings

SXE |

2014 Investor Day

Webb / Dimmit Region

35

Selected Producer Highlights

•

525 MMcf/d of current production

•

Operating more than 1,400 wells, primarily

focused on Eagle Ford

•

150 MMcf/d of current production

•

More than 2,800 net drilling locations in the

Eagle Ford

•

Purchased Shell acreage

•

Operating 7 rigs in the Eagle Ford

•

439 MMcf/d of current production

•

3 rigs operating in the area

•

223 MMcf/d of current production

•

3 rigs operating in the area

Holdings

SXE

Note: Monthly producer data from Drilling Info and relates to their production in

the noted counties. |

2014 Investor Day

McMullen Region

36

•

51 MMcf/d of current production

•

82% of 2014 capex has been spent in the

Eagle Ford

•

Completed 10 wells in 3Q 14

•

Operating 1 rig in McMullen

•

15 MMcf/d of current production

•

Operating 2 rigs in McMullen

•

21 MMcf/d of current production

•

Operating 1 rig in McMullen

•

28 MMcf/d of current production

•

Operating 1 rig in McMullen

Holdings

SXE

•

173 MMcf/d of current production

•

Operating 2 rigs in McMullen

Note: Monthly producer data from Drilling Info and relates to their production in

the noted counties. Selected Producer Highlights

|

2014 Investor Day

Karnes / Dewitt Region

37

Selected Producer Highlights

•

200 MMcf/d of current production

•

Operating 15 rigs in Karnes

•

$2.3 billion in capex has been spent in the

Eagle Ford in 2014

•

18 MMcf/d of current production

•

13 active rigs in the area

•

232 MMcf/d of current production

•

10 active rigs in the area

•

266 MMcf/d of current production

•

5 active rigs in the area

Holdings

SXE

•

80 MMcf/d of current production

•

5 active rigs in the area

Note: Monthly producer data from Drilling Info and relates to their production in

the noted counties. |

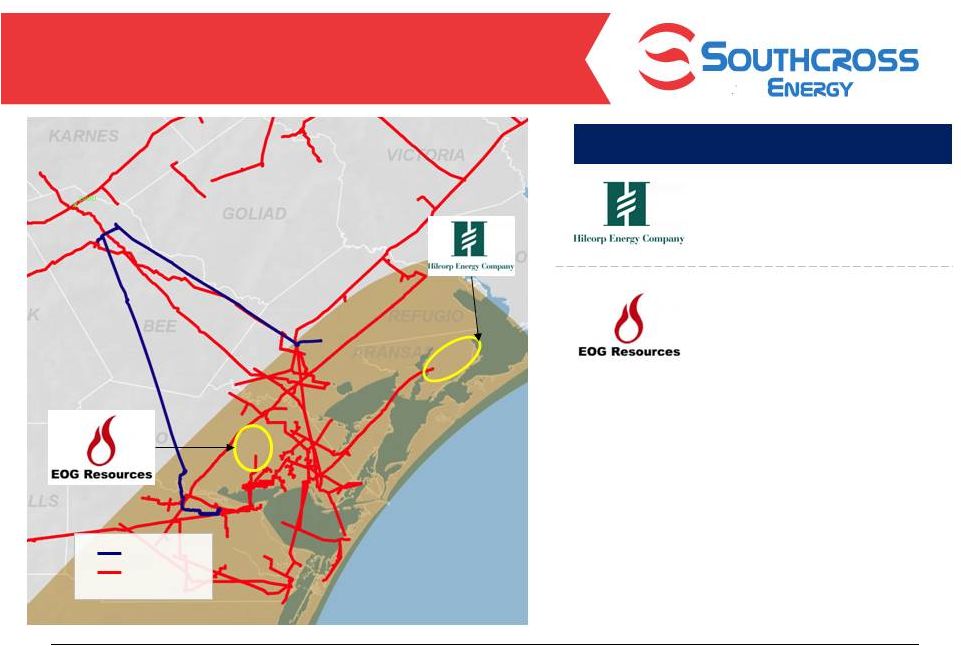

2014 Investor Day

Corpus Christi Region

38

Selected Producer Highlights

•

33 MMcf/d of current production

•

Operating 3 rigs in the area

•

27 MMcf/d of current production

•

Operating 1 rig in San Patricio

county

Holdings

SXE

Note: Monthly producer data from Drilling Info and relates to their production in

the noted counties. |

2014 Investor Day

The Southcross Advantage

39

Significant scale

of pipeline and processing

assets

Operating stability

through interconnected

system

Extensive

footprint

in

the

prolific

Eagle

Ford and Gulf Coast area

Blue

chip

active

producer

customer

base

Full spectrum of services

creates

competitive and economic advantages

Fractionation assets

are a significant

differentiator

Premium

and

growing

markets

for

gas,

NGLs and condensate

Corpus

Christi

region

is

growing

rapidly

and serving new export markets

Fully utilize existing capacity

Develop organic growth

projects

Drop-downs

Acquisitions

Premier Strategic Platform

in the Eagle Ford

Fully Integrated

Midstream Platform

Four Drivers of

Growth

, |

2014 Investor Day

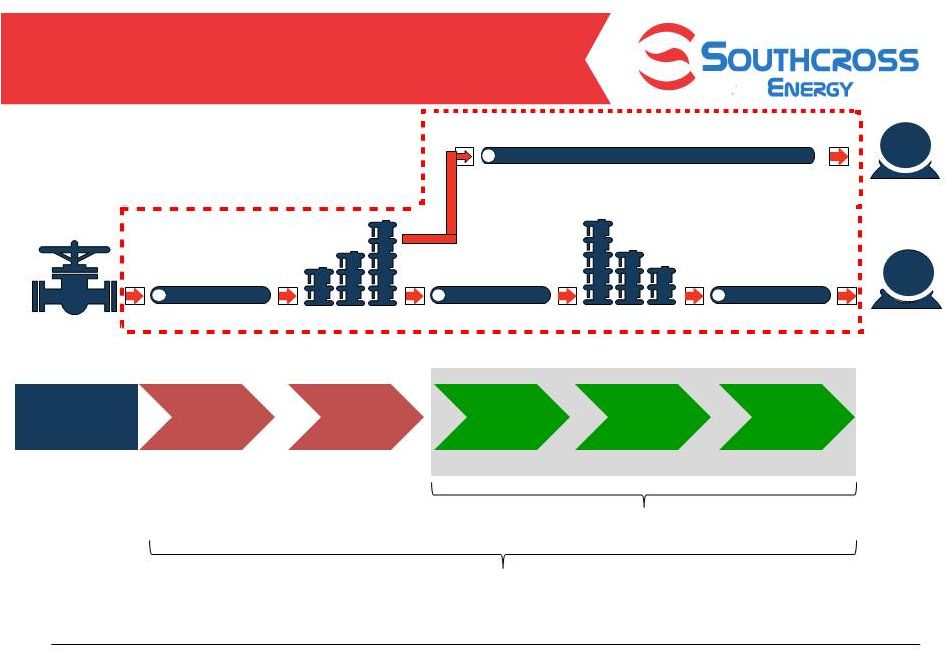

Full Spectrum of Services Creates

Competitive and Economic Advantages

40

Wellhead

Gathering and Compression

Gas Processing Plants

Y-Grade

Fractionation Facilities

Natural Gas

End Users

Transportation Lines / Storage

NGL End Users

NGL & Residue Marketing

20%

30%

5%

35%

10%

Midstream

Margin Stream

Southcross participates in 100% of the midstream margin stream

~50% of Margin Stream from Fractionation

and NGL Marketing

Note: Treating fees, when applicable, further supplement the margin stream

|

2014 Investor Day

Fractionation Assets Create a Significant

Service and Margin Advantage

•

Fractionation increases the full value service offering

enabling Southcross to achieve higher margins and be

more competitive winning new gas supply

•

Wellhead to end-use NGL marketing provides

convenience to producers by avoiding the need to

negotiate multiple long term transportation and

fractionation agreements and provides a secure off-take

for NGLs

•

The location of Southcross’

fractionators in Corpus

Christi enables producers to avoid bottlenecks at Mt.

Belvieu, reduces transport costs and provides direct

access to end-use markets and key export facilities

Bonnie View & Gregory

27,300 Bbls/d

Robstown

63,000 Bbls/d

41

Fractionation Capacity |

Request for Proposal Summary

Proposed Contract and Deal Terms

The Gulf Coast is the Hub for NGL

Production and End-Use

42

The increasing shift to the Gulf Coast for both production and end-use markets is

fueling a heavy demand for midstream infrastructure in the area

Source: INGAA Foundation, Inc.

2014 Investor Day |

2014 Investor Day

Growing LPG Export Market

43

•

Propane export terminal capacity is expected to

double in 2015 to nearly 840 MBbls/d

•

The anticipated 2015 propane export terminal

capacity represents over 50% of current propane

production in the U.S.

•

The majority of the LPG terminal capacity is on the

Gulf Coast of Texas

Source: EIA

49.5%

Asia Pacific

27.9%

Europe/North

Africa

10.2%

12.4%

South America

Mexico, Caribbean and Central

America

U.S. LPG Exports by Destination Region

Source: Enterprise Product Partners, LP

U.S. LPG Supply, Demand and Exports (MMBbls/d)

U.S. LPG Export Forecast (MBbls/d)

Propane

Propane

Butane

Butane

14%

CAGR

Source: Wells Fargo

Source: Oxford Institute for Energy Studies |

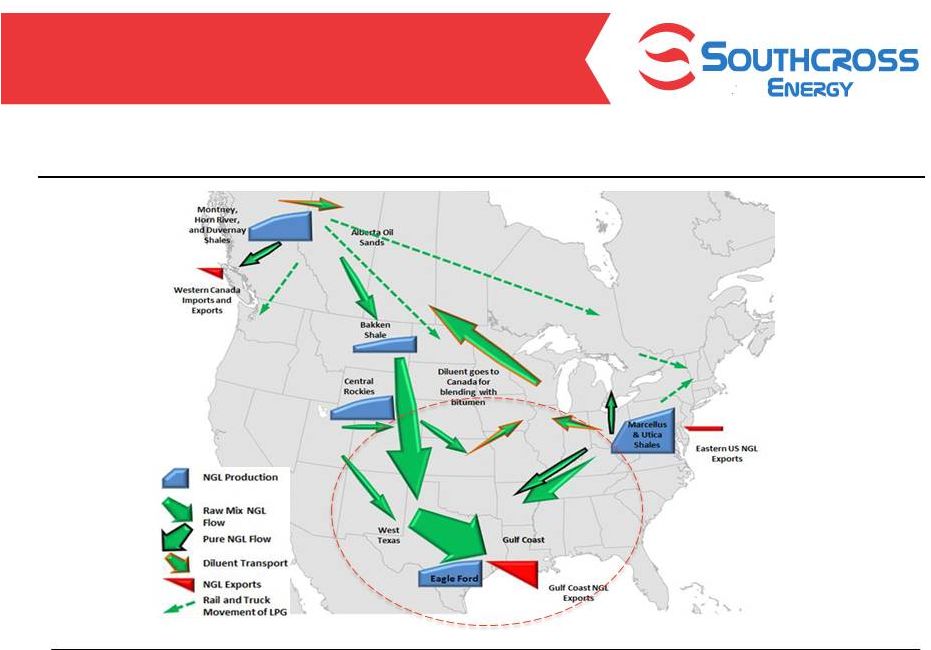

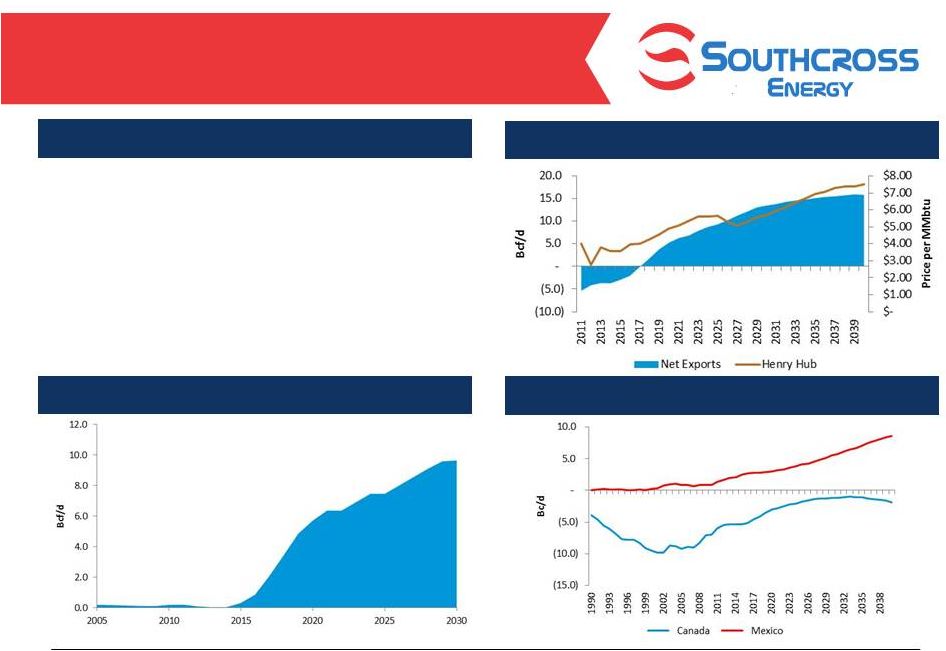

Growing Exports of U.S. Natural Gas

44

Source: EIA

•

The United States is transitioning from being a net

importer of 1.5 Tcf of natural gas in 2012 to a net

exporter of 5.8 Tcf in 2040

•

In 2012, U.S. natural gas exports to Mexico

accounted for over 38% of total U.S. natural gas

exports, and nearly 80% of Mexico's natural gas

imports

•

Net LNG exports, primarily to Asia, are expected to

increase by 3.5 Tcf from 2012 to 2030

U.S. Liquefied Natural Gas Export Projection

U.S. Net Exports by Counterparty

Overview

U.S. Natural Gas Net Export Projection

2014 Investor Day |

2014 Investor Day

Refining Projects

•

Valero upgrading 325kb/d Corpus Christi refinery

•

Flint Hills plans to reconfigure 230kb/d Corpus Christi West Refinery

•

Martin Midstream, Magellan Midstream and Trafigura constructing condensate

splitters at facilities in Corpus Christi Lyondell / Equistar Ethylene

Capacity Expansion •

Lyondell to add 800 million lbs/year of ethylene capacity at Corpus Christi plant

by 2016 •

20,000 Bbl/d of estimated increase in ethane demand by 2016

Cheniere

–

April

7,

2014,

July

17,

2014

and

October

8,

2014

Press

Releases

•

Entered into 20 year LNG supply agreements with Endesa

•

Signed agreement to supply EDF with 380,000 tons / year of LNG from Train 3 as

early as 2019 •

Expect to complete steps to final investment decision and construction by early

2015 •

FERC issues final Environmental Impact Statement for project on October 8, 2014

Trafigura

–

November 14, 2013 and September 11, 2014 Press Release

•

Trafigura spending $500 million to expand dock facilities at Corpus Christi

•

Expansion to meet increasing demand for water access for Eagle Ford

production •

Buckeye

Partners

LP

completes

$860

million

acquisition

of

80%

of

Corpus

Christi

midstream

business

from

Trafigura

NET

Midstream

Pipeline

to

Mexico

–

November

17,

2014

Press

Release

•

•

45

Lower Gulf Coast Projects Fuel Growth

OxyChem Corpus Christi Development Projects

•

OxyChem 110,000 Bbl/d propane export facility at Ingleside expected to begin

operations in 2015 •

OxyChem

and

MexiChem

to

build

1.2

billion

lbs/year

ethylene

cracker

in

2017

(34,000

Bbl/d

ethane

demand)

120-mile, 42”

and 48”

natural gas pipeline with 2.3 Bcf/d of initial capacity (expandable to 3.0 Bcf/d)

was completed ahead of schedule and is now operational

Long-term firm gas transportation agreement with MexGas Supply Ltd., a

subsidiary of Pemex |

2014 Investor Day

•

System

provides

interconnects

to

every

interstate

pipeline

in

the

region

and

diverse

market

outlets;

both

are

an

advantage

in attracting producer contracts

•

Local markets provide incremental downstream margins

•

Multiple

gas

sale

outlets

including

direct

connections

to

industrial

and

electric

generation

markets

Southcross Delivers Gas to Attractive

End-use Markets

46

YTD 2014 residue gas sales

18%

Pipelines

Corpus Christi

Woodsboro

Gregory

NET Midstream

2.3 Bcf/d Mexico

Pipeline

Cheniere LNG

2.6 Bcf/d facility

Processing Plant

Markets

LNG Facility

82%

Direct End-use

Markets |

2014 Investor Day

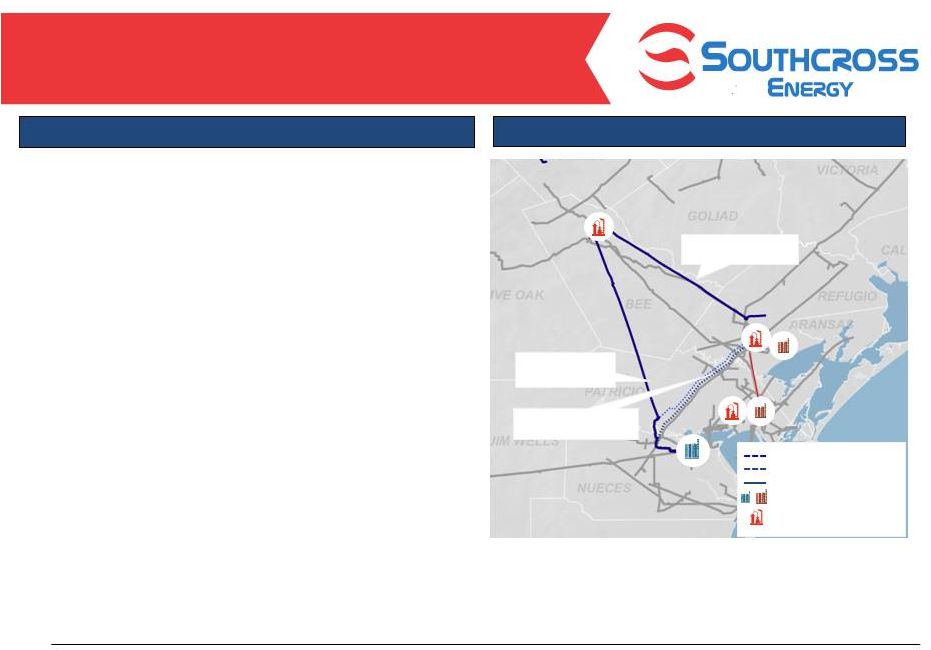

Multiple NGL Markets in Corpus Christi

Area

47

Corpus Christi

Bonnie View

Gregory

Trafigura Export

Active

Oxy Export

Approved

Martin Export

Active

Robstown

•

Advantaged Southcross footprint in expanding Gulf Coast

petrochemical infrastructure and NGL markets

•

End-use NGL markets provide attractive pricing and

market outlets

•

New NGL export terminals near Corpus Christi

•

Most North American ethane cracking is on the Gulf

Coast and is expanding

•

Attractive NGL customer base in the Corpus Christi

market

Fractionator

Markets

Export Terminal |

2014 Investor Day

Strategic End-use Market Position in

Mississippi and Alabama

48

Gross Margin

($ in millions)

Mississippi System

626 mile intrastate pipeline system

End-use driven business with 85% of gas sold to on-system end-users

and only 15% sold to other pipelines

High quality end-user customer base including:

–

SMEPA

–

Georgia Pacific

–

CF Industries

Alabama System

519 mile intrastate pipeline system

Gas supply primarily from low-decline coal bed methane under life of

lease transportation agreements, fortified by interconnections with long-

line pipelines

Long-term gas sales contract with Alagasco

Overview of Mississippi and Alabama

Largest intrastate pipeline in each state

Provides consistent cash flow

Periodic growth opportunities to expand in the region

Vicksburg

Jackson

MISSISSIPPI

Fayette

Tuscaloosa

ALABAMA

Hattiesburg

$8

$8

$8

$9

$9

$9

$-

$5

$10

$15

$20

2012

2013

LTM 9/30/2014

Mississippi

Alabama |

2014 Investor Day

The Southcross Advantage

49

Significant

scale

of

pipeline

and

processing assets

Operating

stability

through

interconnected system

Extensive

footprint

in

the

prolific

Eagle

Ford and Gulf Coast area

Blue

chip,

active

producer

customer

base

Full

spectrum

of

services

creates

competitive and economic advantages

Fractionation

assets

are

a

significant

differentiator

Multiple

and

growing

markets

for

gas, NGLs and condensate

Corpus

Christi

complex

is

growing

rapidly and serving new export markets

Fully utilize existing capacity

Develop organic growth

projects

Drop-downs

Acquisitions

Premier Strategic Platform

in the Eagle Ford

Fully Integrated

Midstream Platform

Four Drivers of

Growth |

2014 Investor Day

Significant Growth Achievable From

Existing Capacity

50

332

MMcf/d

381

MMcf/d

404

MMcf/d

440

MMcf/d

August

September

October

November

MTD

1

Southcross

Processing

Capacity

685

MMcf/d

1

As discussed on the November 7, 2014 SXE earnings call.

2

At margin of $0.50 to $0.75 per mcf/d.

Significant available processing capacity presents cash flow growth opportunity

Adding 200 MMcf/d of

gas represents $36

million to $55 million of

additional potential

annual margin

2014 Avg. Daily Processed Volumes

(MMcf/d) 0

50

100

150

200

250

300

350

400

450

500

550

600

650

2 |

2014 Investor Day

Fully Utilize Existing Capacity

51

SXE Y-Grade

Production

October 2014 Avg.

36 MBbls/d

SXE Y-grade

Production at Full

Processing Capacity

64 MBbls/d

SXE Fractionation

Capacity

27 MBbls/d

63 MBbls/d

Holdings

Robstown Fractionation

Capacity

90 MBbls/d

Significant available fractionation capacity to accommodate a new processing

plant Fractionation Capacity

Used as Processing

Capacity is Filled

Fractionation Capacity

Available for Future

Processing Plant

-

10

20

30

40

50

60

70

80

90 |

2014 Investor Day

•

Business Development team is focused on:

o

Full utilization of existing asset processing and fractionation facilities

o

Adding to rich gas network to accelerate growth

o

Optimization of extensive pipeline and asset base in South Texas

•

Currently pursuing projects including:

o

Repurposing pipelines for higher value uses of crude and condensate

transports o

Exploiting NGL position to add NGL pipeline transportation services

o

Serving new gas and NGL export opportunities

Develop Organic Growth Projects

52

The Southcross business development team has been enhanced through the TexStar

combination and possesses experienced and talented professionals

|

2014 Investor Day

Updates on Recent Key Projects

53

Corpus Christi

Houston

Conroe

Lone Star

Woodsboro

Bonnie View

Gregory

Robstown

45 mile pipeline extending from Webb County

to rich gas system

35 MMcf/d MVC started November 2014

Webb Pipeline

100 MMcf/d sour gas treating facility; treated gas

flows into SXE rich gas system

Dedicated acreage in Dimmit and La Salle

counties producing sour gas

Valley Wells System

4 mile gathering pipeline

McMullen Lateral

9 mile pipeline extending into Karnes County

27 MMcf/d MVC started December 2014

Karnes Gathering

Holdings

SXE

Sour Gas Treating Facility

Fractionator

Processing Plant |

2014 Investor Day

Growth Through Acquisitions

54

Near-Term

•

Near-term focus is on opportunities to enhance our position in the Eagle

Ford –

Primarily targeting bolt-on acquisitions and other opportunities to enhance

our capacity and volumes in South Texas

–

Expect consolidation to continue

Long-Term

•

Long-term focus includes opportunities beyond existing operating areas

Summary of Acquisitions

•

Crosstex Pipelines and Plants (2009)

•

Enterprise Alabama (2011)

•

Tennessee Pipeline Assets (2011)

•

Monco Pipeline System (2012)

•

Valero Pipeline (2012)

•

Tierra Pipelines (2013)

•

Onyx Pipelines (2014)

•

TexStar Rich Gas System (2014)

•

McMullen Gathering System (2014) |

2014 Investor Day

Overview

•

Well in excess of $1 billion of asset value expected to be dropped down to SXE over

time •

Timing and size of each drop-down based upon maturity of asset and capital

market conditions •

Expect to drop down assets that have achieved some maturity of cash flow

•

Expect to fund drop-downs with prudent mix of debt and equity

•

Holdings is incentivized to drop down assets to SXE and grow distributions

•

Holdings

owns

approximately

57%

of

the

SXE

LP

interests

and

100%

of

the

GP

interests

•

Drop-down outlook:

•

Expect to complete at least one drop-down during 2015

•

Expect to drop down assets through a greater number of transactions in smaller

asset packages

Drop-Down Opportunities

55 |

2014 Investor Day

NGL Pipeline System

Drop-Down Inventory

56

63,000 Bbls/d NGL

fractionation facility

Long-term purity product

off-take agreements with

blue chip customers and

exporters under long term

contracts

Robstown Fractionator

Corpus Christi

70,000 Bbls/d Y-grade pipeline

60,000 Bbls/d Y-grade pipeline

and 20,000 Bbls/d propane

pipeline from Woodsboro Plant

to Robstown Fractionator

(under construction)

600 miles of sweet and sour gas gathering lines

28,000 hp of compression

100 MMcf/d sour gas treating facility; expandable to

300 MMcf/d

~300,000 acres dedicated from 18 producers

Lancaster System

100 MMcf/d sour gas

treating facility

25,000 hp of compression

Valley Wells System

Sour Gas Treating Facilities

Robstown Fractionator |

2014 Investor Day

Overview

•

Holdings is completing construction of the 63,000 Bbl/d

Robstown Fractionator with an expected in-service date

during Q1 2015

–

The fractionator will be connected via pipeline to

over 1 Bcf/d of processing capacity and to the DCP

Sandhills Y-grade pipeline

•

Delivers a substantial portion of purity NGL products to

Equistar’s Olefins Facility in Corpus Christi

•

Primary purity pipeline connections are:

–

Equistar

–

Dow

–

Trafigura

–

Citgo

•

Location near Corpus Christi provides access to

international markets

Robstown Fractionator

57 |

2014 Investor Day

Overview

•

56 mile 70,000 Bbls/d 12”

Y-grade pipeline extending from

the Lone Star Plant to the Robstown Fractionator in

Corpus Christi

•

49 mile 12”

pipeline extending from Pettus to Refugio

County

•

Currently constructing two additional pipelines:

–

37 mile 20,000 Bbls/d 6”

propane pipeline to

connect Bonnie View to Robstown and Trafigura

–

27 mile 60,000 Bbls/d 10”

Y-grade pipeline to

connect Woodsboro to Robstown and DCP

Sandhills

•

The NGL Pipeline System connects Y-grade from the Lone

Star, Woodsboro and Gregory processing plants to

multiple outlets including:

–

Robstown Fractionator

–

Bonnie View Fractionator

–

Gregory Fractionator

–

Multiple Mont Belvieu fractionators via DCP

Sandhills Pipeline

NGL Pipeline System Map

Lone Star to Robstown

Y-Grade Pipeline

Lone Star to Refugio Y-Grade

or Residue Gas Pipeline

Y-grade Line under construction

Propane Line under construction

NGL System

Fractionator

Processing Plant

NGL Pipeline System

58

Woodsboro

Bonnie View

Gregory

Lone Star

Robstown

Woodsboro to Robstown

Y-grade and propane pipelines |

2014 Investor Day

Overview

Gathering and Treating Systems

•

Holdings currently owns two sour gas gathering systems

and two sour gas treating plants

–

Lancaster System

–

Valley Wells System

•

At Lancaster, Holdings owns and operates an acid gas

injection well, providing a unique disposal service and

meaningful competitive advantage with up to 300 MMcf/d

of inlet treating capacity

–

Valley Wells is able to send its recovered H2S

back to Lancaster via pipeline for injection

•

Sour gas treating plants are a key strategic advantage

–

Limited amount of sour gas gathering and treating

service available in the area

–

Producer activity is driven by oil wells

–

Increasing sour gas production trends

Sour Gas Gathering and Treating

59

Sour Gas Treating Facility |

2014 Investor Day

Overview

Lancaster Gathering and Treating System

•

Holdings operates approximately 600 miles of sweet and

sour gas gathering lines located in Frio, La Salle, Zavala,

Dimmit, Atascosa and McMullen Counties

–

28,000 HP of compression

–

Acid gas injection well with ability to serve up to

300 MMcf/d of treating capacity

–

Current treating capacity of approximately 100

MMcf/d being expanded to approximately 250

MMcf/d

•

Holding’s Lancaster gathering system connects to the

SXE rich gas system

•

Significant acreage dedications totaling approximately

300,000 acres from 18 producers

Lancaster Treating Facility and Pipelines

60

Sour Gas Treating Facility |

2014 Investor Day

Valley Wells Treating Facility

•

Built to serve acreage located between Lancaster System and the rich gas

system in Dimmit and La Salle Counties

–

25,000 horsepower of compression

–

Proven

ability

to

build

and

operate

sour

gas

treating

facilities

and

the

existing acid gas injection well are significant competitive advantages

–

Current treating capacity of approximately 100 MMcf/d

•

Valley Wells gathering system connects to the SXE rich gas system

•

Received firm volume commitment of 35 MMcf/d which began in October

2014

Asset Map

Valley Wells Treating Facility and

Pipelines

61

Sour Gas Treating Facility |

2014 Investor Day

Employee and Customer Focus

62

Our commercial success is centered around our

customers

Southcross employees and customers are at the

heart of our operational success

Creativity

Responsiveness

Accountability

Customer

Service

Safety

Reliability

Experience

Performance

Teamwork

Integrity

Employees

Customers |

2014 Investor Day

Fill Capacity

Organic

Projects

Drop-downs

Acquisitions

Growth Strategy

63

SXE

Holdings

•

Fully utilize processing capacity

in 12 to 18 months

•

Optimization of asset base

•

Potential new processing plant

in 2016

•

Expect drop-down transaction

in 2015

•

Focus on bolt-on assets in

existing markets

•

Fill fractionator with system

volumes and potential third

party volumes; add sour gas to

treating and gathering system

•

Larger projects with significant

development time and ramp

•

Recycle capital from drop-

downs to further growth

•

Focus on larger and/or less

developed acquisitions in

existing markets; potentially

move to other areas later |

Financial

Overview

&

Outlook

–

Michael

Anderson |

2014 Investor Day

Financial Strategy

65

Provide solid

financial

foundation

Generate

predictable

and growing

cash flow

Enable

consistent

distribution

growth

Ensure strong

base of capital

for growth

through

market cycles |

2014 Investor Day

•

Attractive credit facilities with long-dated maturities

–

Corporate family credit rating of B1 / B

–

$450 million term loan B facility

•

August 2021 maturity; borrowing rate of LIBOR plus 4.25% (1.00% LIBOR floor)

–

$200 million revolving credit facility

•

August 2019 maturity; current borrowing rate of LIBOR plus 3.25%

–

Existing debt balance is over 50% hedged

•

Expect near term de-leveraging

–

Benefits from expected cash flow growth related to recent projects and

acquisitions –

Limited required growth capital expenditures in 2015

–

Adjusted

EBITDA

growth

expected

from

filling

existing

processing

capacity

•

Access to capital for growth

–

Recently implemented ATM equity program

–

Expect to fund drop-downs with prudent debt/equity mix

–

Flexibility through Holding’s asset and capital base

Provide Solid Financial Foundation

66

Targeting 3.0x to 4.0x leverage ratio and 1.1x to 1.2x distribution coverage

with prudent use of equity to fund growth |

2014 Investor Day

•

Attractive contract mix with large base of minimum volume commitment contracts and

producer customers driven by attractive Eagle Ford economics

•

Gross

operating

margin

1

is

becoming

increasingly

fixed

fee

oriented

•

Anticipate ability to grow Adjusted EBITDA without significant growth capital

–

Filling 200 MMcf/d of current processing space can generate meaningful

incremental Adjusted EBITDA:

•

$36 million at $0.50 per mcf/d

•

$55 million at $0.75 per mcf/d

•

$73 million at $1.00 per mcf/d

•

Access to potential drop-down assets at Holdings that are already integrated

with South Texas asset base

Generate Predictable and

Growing Cash Flow

67

1

We

define

gross

operating

margin

as

the

sum

of

revenues

less

the

cost

of

natural

gas

and

NGLs

sold. |

2014 Investor Day

•

Largely fixed fee contracts with producers provide attractive mix of fixed fee

margins with some commodity sensitive upside

•

Commodity price exposure primarily from NGL equity barrels created through fixed

recovery processing contracts

•

Commodity sensitive margins expected to decline as a portion of gross operating

margin •

Recently acquired and new contracts are largely fixed fee margins

Low Commodity Price Sensitivity

68

Analysis based upon Q4 2014 guidance forecast

Change in Commodity Price

(20.0%)

(10.0%)

10.0%

20.0%

Natural Gas

1.5%

0.8%

(0.8%)

(1.5%)

NGLs

(5.3%)

(2.7%)

2.7%

5.3%

Change in Gross Operating Margin

vs. Change in Commodity Prices

% of Commodity Sensitive Gross Margin

24%

15-20%

10-15% |

2014 Investor Day

•

Expected near-term path to 1.0x distribution coverage

–

Recent new minimum volume commitment contracts are expected to add

$7 million to $8 million in full quarter Adjusted EBITDA

–

Existing base of strong producer customers is expected to continue to

grow production at current commodity price levels

•

Existing commitment from Holdings to forgo subordinated unit distributions

while coverage is less than 1.0x provides support for common units

•

Expect to fill processing plant capacity within 12 to 18 months

–

Potential to start-up new processing plant in 2016

•

Supplement organic growth through expected drop-downs

Enable Consistent Distribution Growth

69

Expect to

achieve at

least 1.0x

coverage of

common units

in Q1 2015

Expect to grow

distributions in

2015

Expect further

growth

through filling

asset capacity

& completing

drop-downs |

2014 Investor Day

Expected Path to Distribution Coverage

70

$11.3 Million

Guidance Range

$20-$24 Million

Future Growth

Through Filling Asset

Capacity and

Completing Drop-

Downs

Quarterly Adjusted EBITDA

Distributions Covered

$19.0 Million

$10.0 million in quarterly distributions

25.0 million common units / GP units

$23.9 Million

$14.9 million in quarterly distributions

25.0 million common units / GP units

12.2 million subordinated units |

2014 Investor Day

•

29.2 million SXE common / Class B Convertible PIK units

•

100% of SXE General Partner units

•

Operating assets with estimated value well in excess of $1 billion

•

Approximately $100 million in cash

•

$50 million from unfunded revolving credit facility

•

Additional capital from unfunded preferred equity commitment

•

Future potential investments from strong base of private equity investors

Holdings Profile

71

Holdings provides an ideal platform for potential growth through

existing assets and an enviable cadre of private equity energy investors

Holdings Asset Composition

Holdings Capital Available for Growth

•

Market value of approximately $440 million at $15 per unit |

2014 Investor Day

Compelling Valuation

72

Attractive Yield vs.

Gathering / Processing

Peers

Large Base of

Potential Drop-

Down Assets vs.

Current Adjusted

EBITDA

Potential

Distribution

Growth Heavily

Discounted in

Current Market

Price |

2014 Investor Day

Company

Drop Down

Opportunities

EBITDA

2014E EBITDA

Drop Down

EBITDA / 2014E

EBITDA

LQA Yield

Southcross

$150.0

$56.0

2.7x

11.4%

Valero

850.0

69.0

12.4x

2.0%

Phillips 66

1,500.0

136.0

11.0x

2.5%

MPLX

800.0

168.0

4.8x

2.0%

Western Refining Logistics

175.0

72.0

2.4x

3.7%

Midcoast Energy

200.0

94.0

2.1x

8.2%

Summit

350.0

201.0

1.7x

4.8%

Oiltanking

300.0

188.0

1.6x

2.1%

QEP Midstream

150.0

93.0

1.6x

7.2%

EQT Midstream

325.0

256.0

1.3x

2.3%

DCP Midstream

555.0

519.0

1.1x

6.4%

Rose Rock

115.0

117.0

1.0x

3.8%

EnLink

400.0

511.0

0.8x

5.1%

Western Gas

400.0

649.0

0.6x

3.7%

Tesoro

150.0

308.0

0.5x

1.4%

Attractive Yield Versus Drop-Down Peers

73

(1)

(2)

SXE

+

Source: Goldman Sachs; company research

(1)

Company estimates of Adjusted EBITDA at time of potential drop-down

(2)

2014E Adjusted EBITDA based upon mid-point of $20 - $24 million Q4 Adjusted EBITDA guidance

range |

2014 Investor Day

Note: As of market close December 4, 2014; gold shading denotes peers with

significant assets at GP level Opportunity for Unit Price Appreciation

74 |

Summary –

David Biegler |

2014 Investor Day

The Southcross Advantage

76

Significant

scale

of

pipeline

and

processing assets

Operating

stability

through

interconnected system

Extensive

footprint

in

the

prolific

Eagle

Ford and Gulf Coast areas

Blue

chip

active

producer

customer

base

Full

spectrum

of

services

creates

competitive and economic advantages

Fractionation

assets

are

a

significant

differentiator

Premium

and

growing

markets

for

gas, NGLs and condensate

Corpus

Christi

region

is

growing

rapidly and serves new export markets

Fully utilize existing capacity

Develop organic growth

projects

Drop-downs

Acquisitions

Premier Strategic Platform

in the Eagle Ford

Fully Integrated

Midstream Platform

Four Drivers of

Growth

, |

Appendix |

2014 Investor Day

78

Reconciliation to Adjusted EBITDA

(Dollars in Thousands)

Three Months Ended,

9/30/2013

12/31/2013

3/31/2014

6/30/2014

9/30/2014

Reconciliation of net loss to Adjusted EBITDA:

Net (loss) income

$

(4,069)

$

674

$

(1,289)

$

(2,961)

$

(24,778)

Add (deduct):

Depreciation and amortization expense

9,447

8,590

8,528

8,978

11,629

Interest expense

3,587

3,855

2,973

1,771

4,596

Loss on extinguishment of debt

-

-

-

-

2,316

Unit-based compensation

552

542

529

1,082

609

Income tax (benefit) expense

125

(19)

8

56

69

Unrealized (gain) loss

-

(120)

(32)

175

207

Revenue deferral adjustment

-

-

1,182

444

444

Gain on sale of assets

-

(25)

-

(45)

-

Loss on asset disposal

-

-

4

-

334

Major litigation costs, net of recoveries

-

517

273

630

488

Transaction-related costs

-

-

303

4

10,506

Equity in losses of joint venture investments

-

-

-

-

3,308

Impairment of assets

-

-

-

-

1,556

Other, net

20

24

18

44

-

Adjusted EBITDA

$

9,662

$

14,038

$

12,497

$

10,178

$

11,284 |