Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - Trinseo S.A. | d820751dex991.htm |

| 8-K - 8-K - Trinseo S.A. | d820751d8k.htm |

| Exhibit 99.2

|

Exhibit 99.2

Third Quarter 2014 Earnings Summary

November 14, 2014

™ Trademark

|

|

Introductions & Disclosure Rules

Introductions

Chris Pappas, President & CEO

John Feenan, Executive Vice President & CFO

David Stasse, Vice President, Treasury & Investor Relations

Disclosure Rules

The forward looking statements contained in this presentation involve risks and uncertainties that may affect the Company’s operations, markets, products, services, prices and other factors. These risks and uncertainties include, but are not limited to, economic, competitive, legal, governmental and technological factors. Accordingly, there is no assurance that the Company’s expectations expressed in such forward looking statements will be realized. The Company assumes no obligation to provide revisions to any forward looking statements in this presentation should circumstances change.

This presentation contains financial measures that are not in accordance with generally accepted accounting principles in the US (“GAAP”) including Adjusted EBITDA, Adjusted Net Income and Adjusted EPS. We believe these measures provide relevant and meaningful information to investors and lenders about the ongoing operating results of the Company. Such measures when referenced herein should not be viewed as an alternative to GAAP measures of performance. We have provided a reconciliation of Adjusted EBITDA, Adjusted Net Income and Adjusted EPS in the Appendix section of this presentation.

2

|

|

Agenda

Business Overview Financial Review Forward Focus Q&A

3

|

|

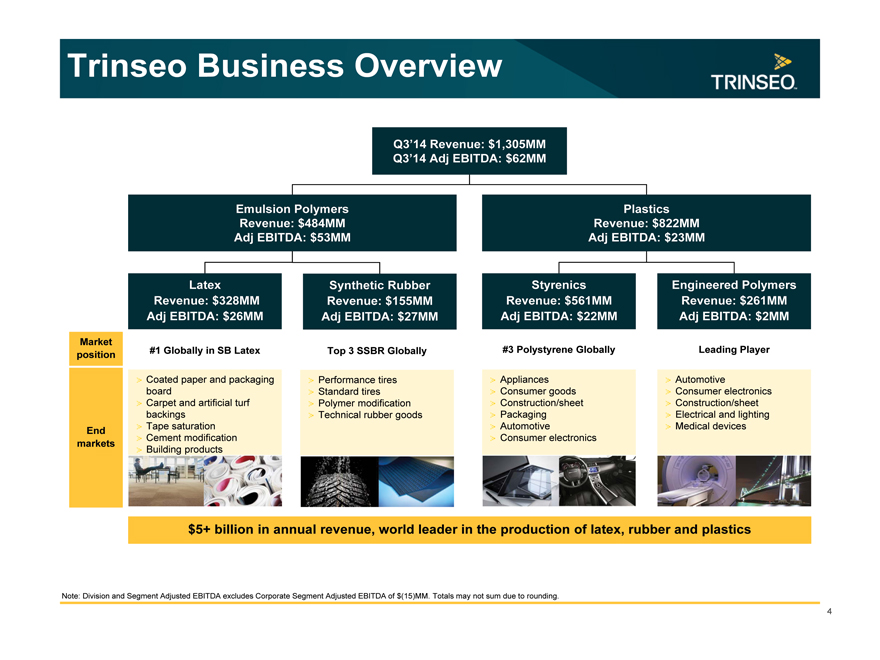

Trinseo Business Overview

Q3’14 Revenue: $1,305MM Q3’14 Adj EBITDA: $62MM

Emulsion Polymers Revenue: $484MM Adj EBITDA: $53MM

Plastics Revenue: $822MM Adj EBITDA: $23MM

Latex Revenue: $328MM

Adj EBITDA: $26MM

Synthetic Rubber Revenue: $155MM Adj EBITDA: $27MM

Styrenics Revenue: $561MM Adj EBITDA: $22MM

Engineered Polymers Revenue: $261MM

Adj EBITDA: $2MM

Market position

End markets

#1 Globally in SB Latex

Coated paper and packaging board Carpet and artificial turf backings Tape saturation Cement modification Building products

Top 3 SSBR Globally

Performance tires Standard tires Polymer modification Technical rubber goods

#3 Polystyrene Globally

Appliances Consumer goods Construction/sheet Packaging Automotive Consumer electronics

Leading Player

Automotive

Consumer electronics Construction/sheet Electrical and lighting Medical devices

$5+ billion in annual revenue, world leader in the production of latex, rubber and plastics

Note: Division and Segment Adjusted EBITDA excludes Corporate Segment Adjusted EBITDA of $(15)MM. Totals may not sum due to rounding.

4

|

|

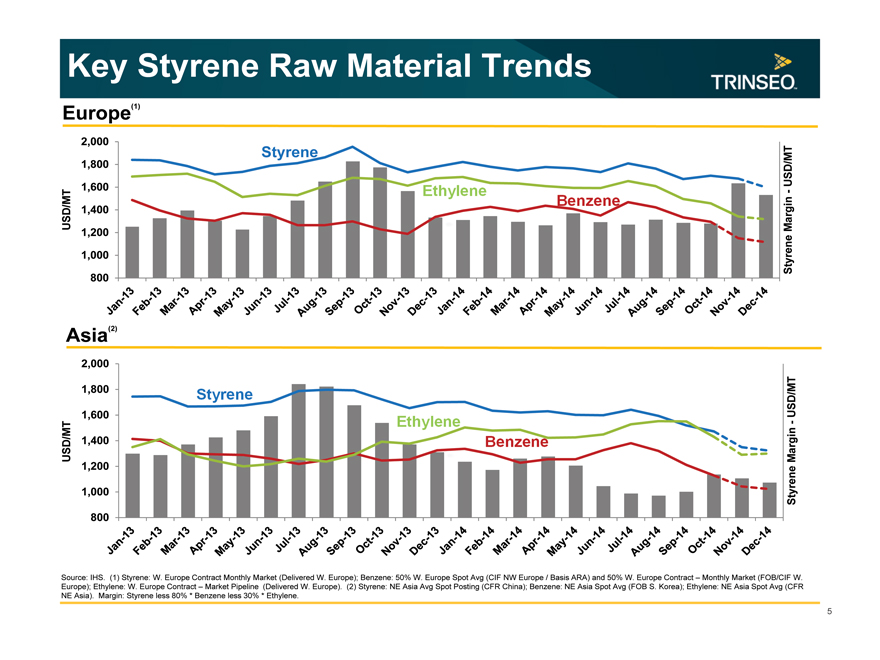

Key Styrene Raw Material Trends

Europe(1)

Styrene

Ethylene

Benzene

2,000

1,800

1,600 / MT USD 1,400 1,200

1,000

800

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

Styrene Margin—USD/MT

Asia(2)

Benzene

USD/MT

2,000 1,800 1,600 1,400 1,200 1,000 800

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

Styrene Margin—USD/MT

Source: IHS. (1) Styrene: W. Europe Contract Monthly Market (Delivered W. Europe); Benzene: 50% W. Europe Spot Avg (CIF NW Europe / Basis ARA) and 50% W. Europe Contract – Monthly Market (FOB/CIF W. Europe); Ethylene: W. Europe Contract – Market Pipeline (Delivered W. Europe). (2) Styrene: NE Asia Avg Spot Posting (CFR China); Benzene: NE Asia Spot Avg (FOB S. Korea); Ethylene: NE Asia Spot Avg (CFR NE Asia). Margin: Styrene less 80% * Benzene less 30% * Ethylene.

5

|

|

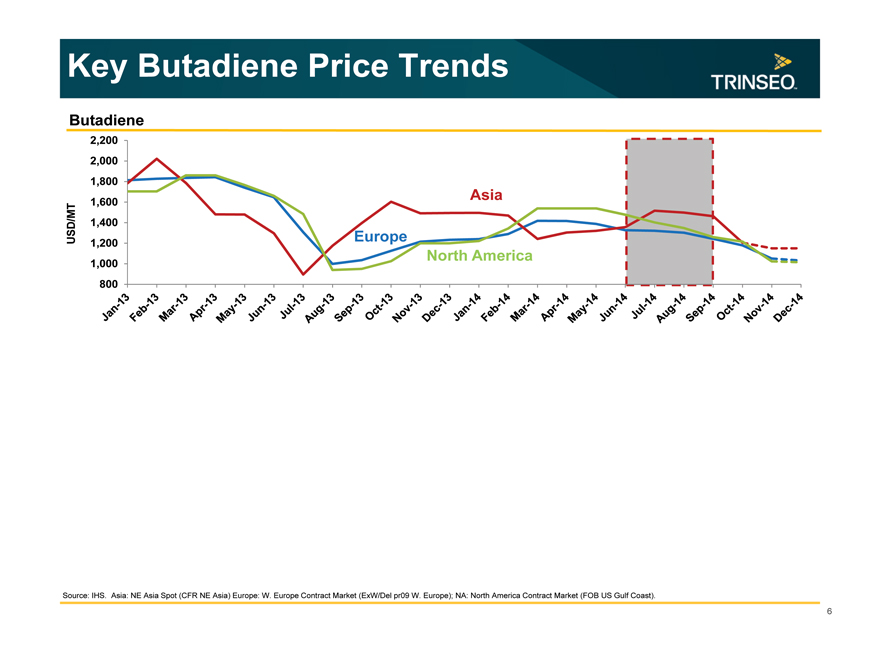

Key Butadiene Price Trends

Butadiene

USD/MT

2,200 2,000 1,800 1,600 1,400 1,200 1,000 800

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

Asia

Europe

North America

Source: IHS. Asia: NE Asia Spot (CFR NE Asia) Europe: W. Europe Contract Market (ExW/Del pr09 W. Europe); NA: North America Contract Market (FOB US Gulf Coast).

6

|

|

Financial Review

John Feenan EVP & CFO

™ Trademark

|

|

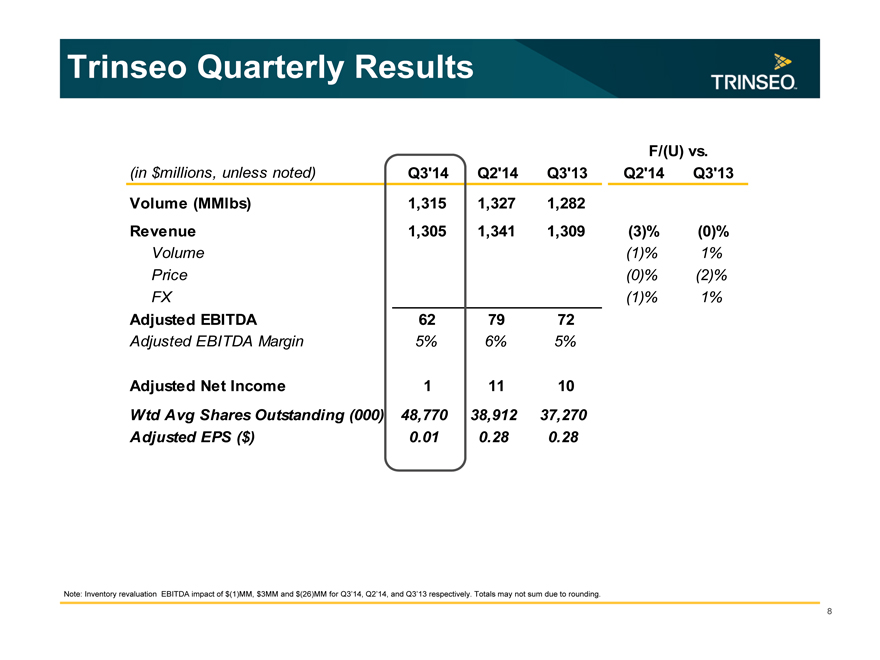

Trinseo Quarterly Results

F/(U) vs.

(in $millions, unless noted) Q3’14 Q2’14 Q3’13 Q2’14 Q3’13

Volume (MMlbs) 1,315 1,327 1,282

Revenue 1,305 1,341 1,309 (3)% (0)%

Volume (1)% 1%

Price (0)% (2)%

FX (1)% 1%

Adjusted EBITDA 62 79 72

Adjusted EBITDA Margin 5% 6% 5%

Adjusted Net Income 1 11 10

Wtd Avg Shares Outstanding (000) 48,770 38,912 37,270

Adjusted EPS ($) 0.01 0.28 0.28

Note: Inventory revaluation EBITDA impact of $(1)MM, $3MM and $(26)MM for Q3’14, Q2’14, and Q3’13 respectively. Totals may not sum due to rounding.

8

|

|

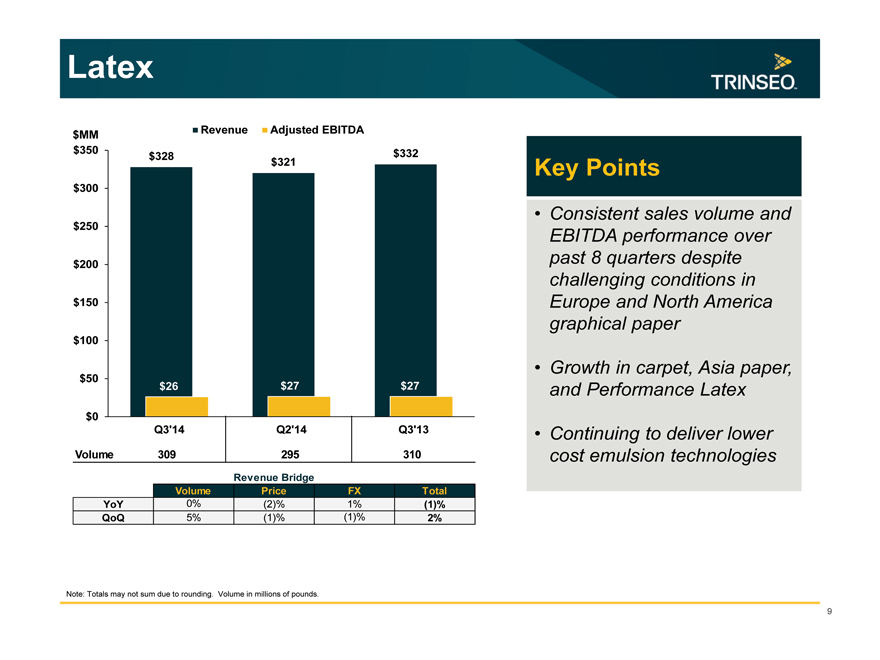

Latex

$MM $350

$300 $250 $200 $150 $100 $50 $0

Revenue Adjusted EBITDA

$328 $332 $321

$26 $27 $27 Q3’14 Q2’14 Q3’13

Volume 309 295 310

Revenue Bridge

Volume Price FX Total

YoY 0% (2)% 1% (1)%

QoQ 5% (1)% (1)% 2%

Key Points

Consistent sales volume and EBITDA performance over past 8 quarters despite challenging conditions in Europe and North America graphical paper

Growth in carpet, Asia paper, and Performance Latex

Continuing to deliver lower cost emulsion technologies

Note: Totals may not sum due to rounding. Volume in millions of pounds.

9

|

|

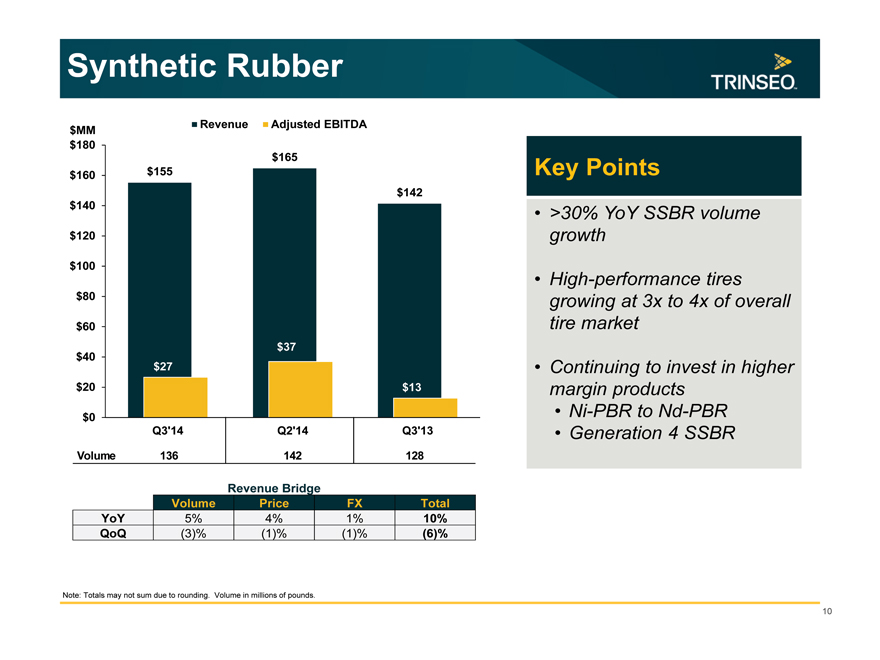

Synthetic Rubber

Revenue Adjusted EBITDA

$MM $180

$160 $140 $120 $100 $80 $60 $40 $20 $0

$165 $155 $142

$37 $27 $13

Q3’14 Q2’14 Q3’13

Volume 136 142 128

Revenue Bridge

Volume Price FX Total

YoY 5% 4% 1% 10%

QoQ (3)% (1)% (1)% (6)%

Key Points

>30% YoY SSBR volume growth

High-performance tires growing at 3x to 4x of overall tire market

Continuing to invest in higher margin products

Ni-PBR to Nd-PBR

Generation 4 SSBR

Note: Totals may not sum due to rounding. Volume in millions of pounds.

10

|

|

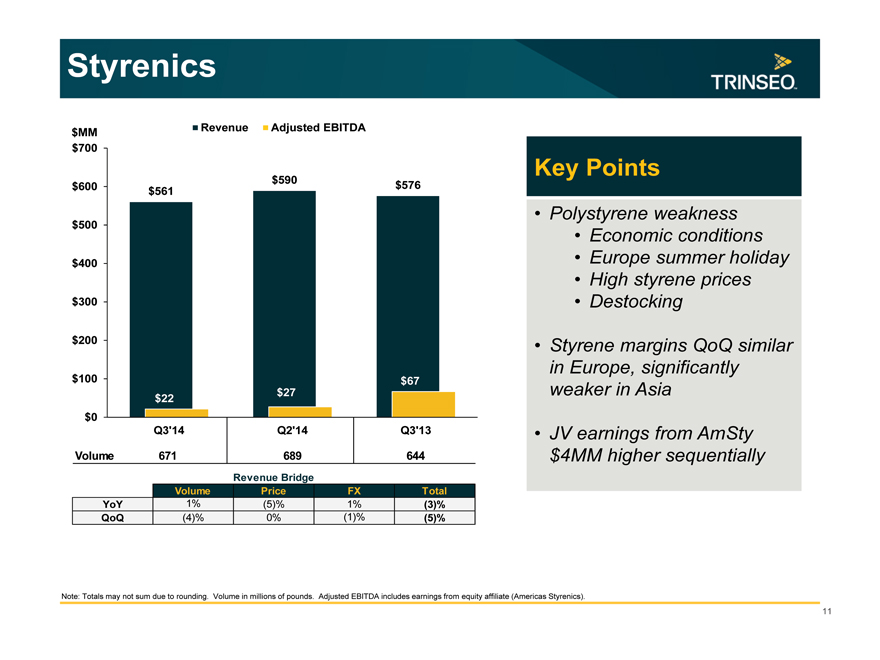

Styrenics

$MM Revenue Adjusted EBITDA

$700

$590

$600 $561 $576

$500

$400

$300

$200

$100 $67

$22 $27

$0

Q3’14 Q2’14 Q3’13

Volume 671 689 644

Revenue Bridge

Volume Price FX Total

YoY 1% (5)% 1% (3)%

QoQ (4)% 0% (1)% (5)%

Key Points

Polystyrene weakness

Economic conditions

Europe summer holiday

High styrene prices

Destocking

Styrene margins QoQ similar in Europe, significantly weaker in Asia

JV earnings from AmSty $4MM higher sequentially

Note: Totals may not sum due to rounding. Volume in millions of pounds. Adjusted EBITDA includes earnings from equity affiliate (Americas Styrenics).

11

|

|

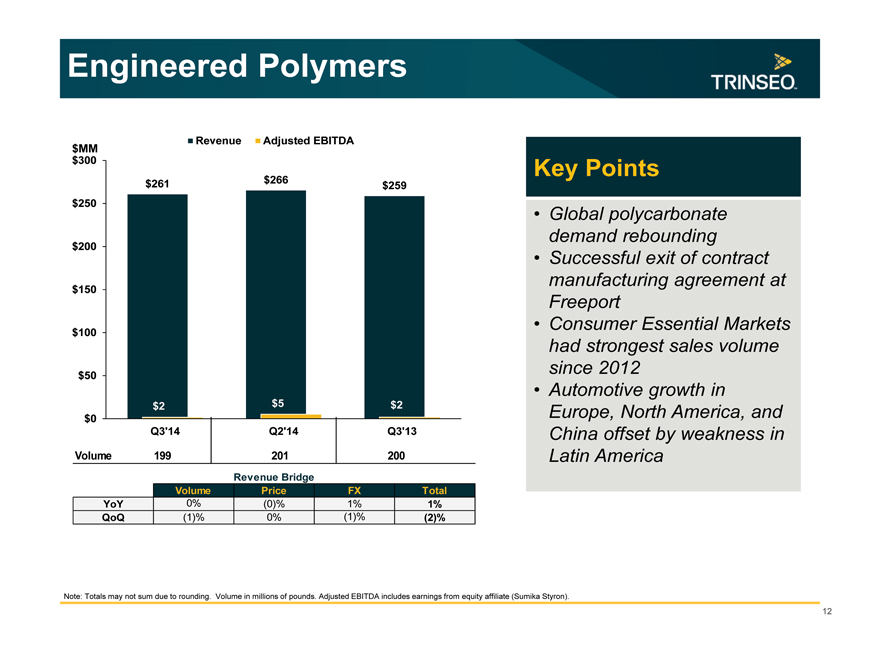

Engineered Polymers

Revenue Adjusted EBITDA

$MM

$300

$261 $266 $259

$250

$200

$150

$100

$50

$2 $5 $2

$0

Q3’14 Q2’14 Q3’13

Volume 199 201 200

Revenue Bridge

Volume Price FX Total

YoY 0% (0)% 1% 1%

QoQ (1)% 0% (1)% (2)%

Key Points

Global polycarbonate demand rebounding

Successful exit of contract manufacturing agreement at Freeport

Consumer Essential Markets had strongest sales volume since 2012

Automotive growth in Europe, North America, and China offset by weakness in Latin America

Note: Totals may not sum due to rounding. Volume in millions of pounds. Adjusted EBITDA includes earnings from equity affiliate (Sumika Styron).

12

|

|

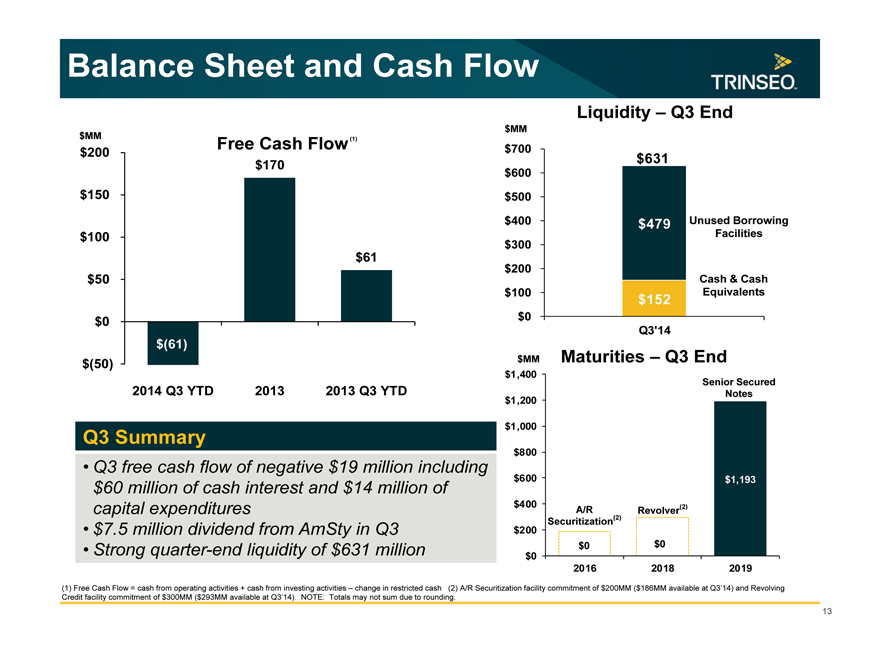

Balance Sheet and Cash Flow

$MM Free Cash Flow (1)

$200

$170

$150

$100

$61

$50

$0

$(61)

$(50)

2014 Q3 YTD 2013 2013 Q3 YTD

Q3 Summary

Q3 free cash flow of negative $19 million including $60 million of cash interest and $14 million of capital expenditures

$7.5 million dividend from AmSty in Q3

Strong quarter-end liquidity of $631 million

Liquidity – Q3 End

$MM

$700

$631

$600

$500

$400 $479 Unused Borrowing

Facilities

$300

$200

Cash & Cash

$100 Equivalents

$152

$0

Q3’14

$MM Maturities – Q3 End

$1,400

Senior Secured

$1,200 Notes

$1,000

$800

$600 $1,193

$400 (2)

A/R Revolver

Securitization(2)

$200

$0 $0

$0

2016 2018 2019

(1) Free Cash Flow = cash from operating activities + cash from investing activities – change in restricted cash (2) A/R Securitization facility commitment of $200MM ($186MM available at Q3’14) and Revolving Credit facility commitment of $300MM ($293MM available at Q3’14). NOTE: Totals may not sum due to rounding.

13

|

|

2014 Focus

Chris Pappas President & CEO

™ Trademark

|

|

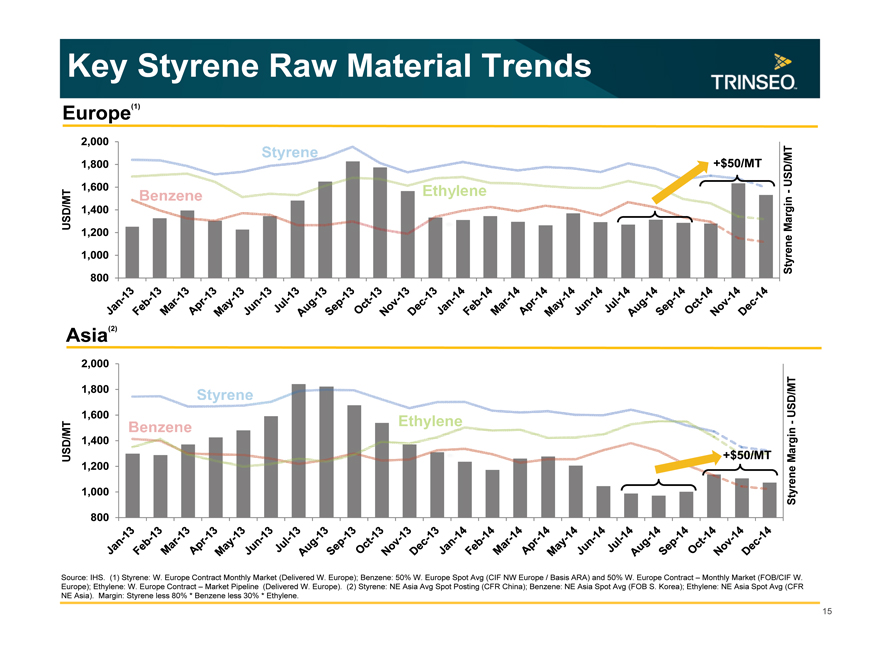

Key Styrene Raw Material Trends

Europe(1)

2,000

Benzene Styrene Ethylene

1,800 +$50/MT USD/MT

1,600

-

1,400

1,200

1,000 Styrene Margin - USD/MT

800

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

Asia(2)

2,000

1,800 USD/MT

1,600

Ethylene

1,400

+$50/MT

1,200

1,000 Styrene

Margin - USD/MT

800

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

Benzene Styrene

Source: IHS. (1) Styrene: W. Europe Contract Monthly Market (Delivered W. Europe); Benzene: 50% W. Europe Spot Avg (CIF NW Europe / Basis ARA) and 50% W. Europe Contract – Monthly Market (FOB/CIF W. Europe); Ethylene: W. Europe Contract – Market Pipeline (Delivered W. Europe). (2) Styrene: NE Asia Avg Spot Posting (CFR China); Benzene: NE Asia Spot Avg (FOB S. Korea); Ethylene: NE Asia Spot Avg (CFR NE Asia). Margin: Styrene less 80% * Benzene less 30% * Ethylene.

15

|

|

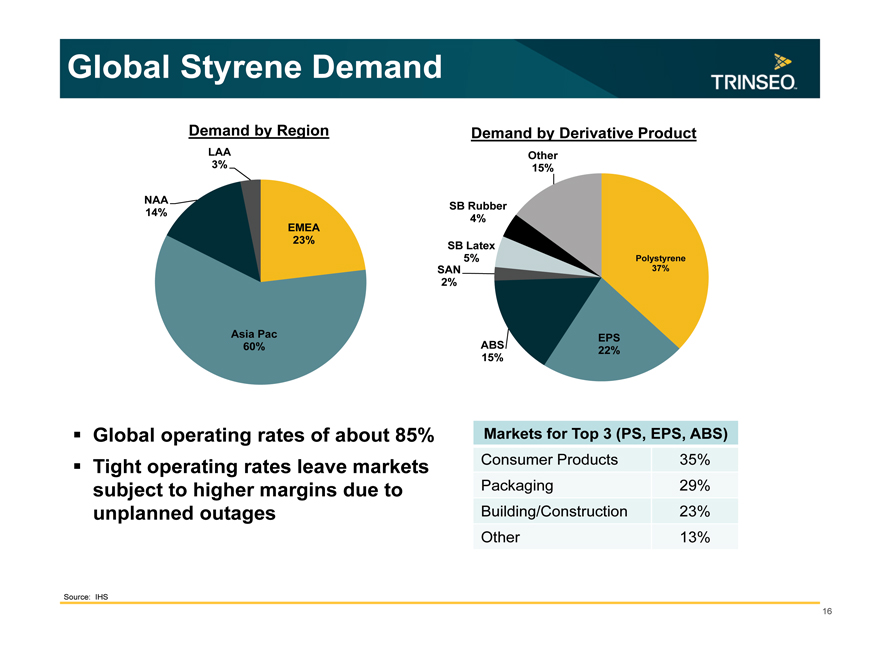

Global Styrene Demand

Demand by Region Demand by Derivative Product

LAA Other

3% 15%

NAA SB Rubber

14% 4%

EMEA

23% SB Latex

5% Polystyrene

SAN 37%

2%

Asia Pac EPS

60% ABS 22%

15%

Global operating rates of about 85% Tight operating rates leave markets subject to higher margins due to unplanned outages

Markets for Top 3 (PS, EPS, ABS)

Consumer Products 35%

Packaging 29%

Building/Construction 23%

Other 13%

Source: IHS

16

|

|

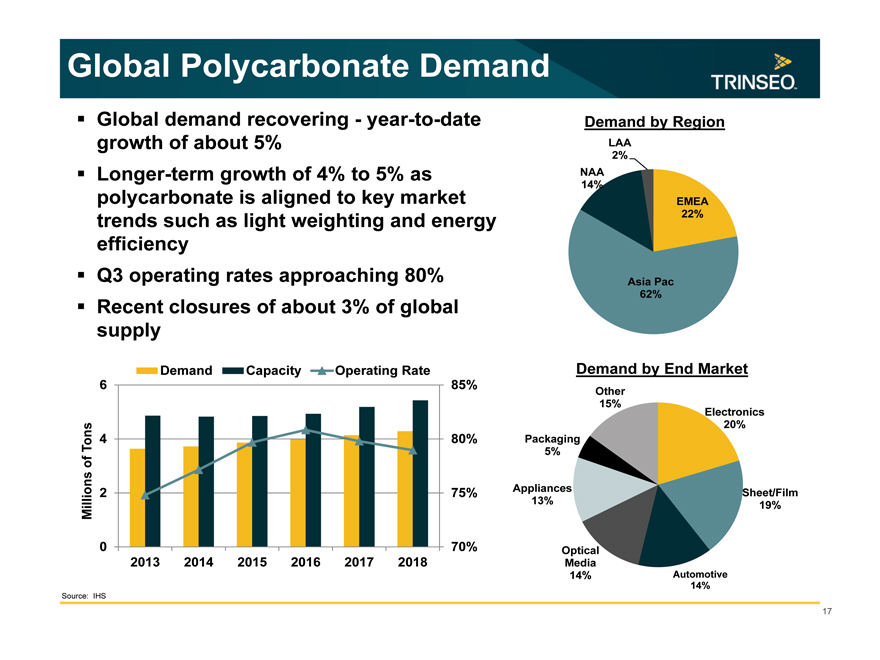

Global Polycarbonate Demand

Global demand recovering—year-to-date growth of about 5% Longer-term growth of 4% to 5% as polycarbonate is aligned to key market trends such as light weighting and energy efficiency Q3 operating rates approaching 80% Recent closures of about 3% of global supply

Demand Capacity Operating Rate

6 85%

Tons 4 80%

of

Millions 2 75%

0 70%

2013 2014 2015 2016 2017 2018

Demand by Region

LAA

2%

NAA

14%

EMEA

22%

Asia Pac

62%

Demand by End Market

Other

15%

Electronics

20%

Packaging

5%

Appliances Sheet/Film

13% 19%

Optical

Media

14% Automotive

14%

Source: IHS

17

|

|

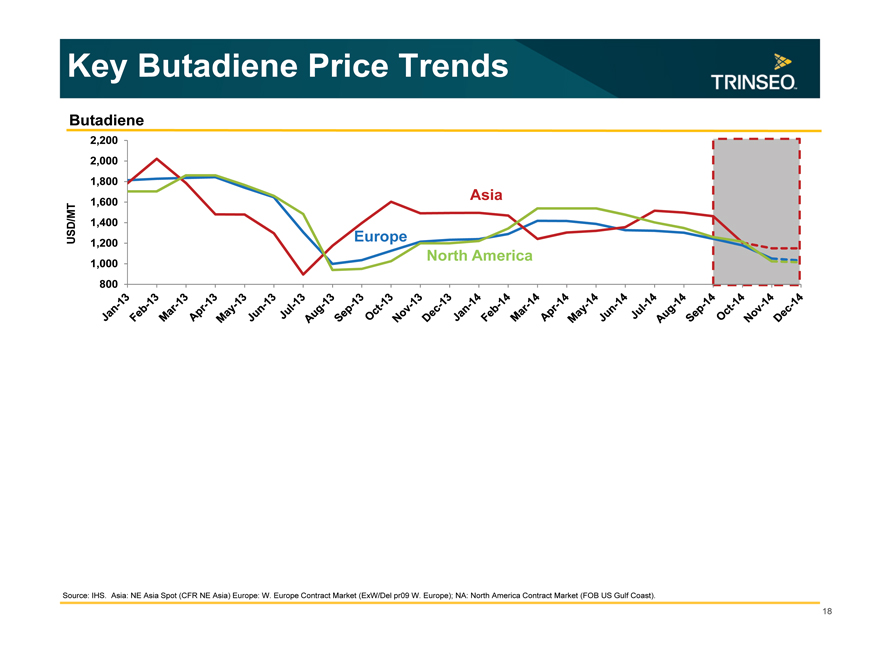

Key Butadiene Price Trends

Butadiene

2,200

2,000

1,800

1,600 Asia

1,400

USD/MT Europe

1,200

1,000 North America

800

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

Source: IHS. Asia: NE Asia Spot (CFR NE Asia) Europe: W. Europe Contract Market (ExW/Del pr09 W. Europe); NA: North America Contract Market (FOB US Gulf Coast).

18

|

|

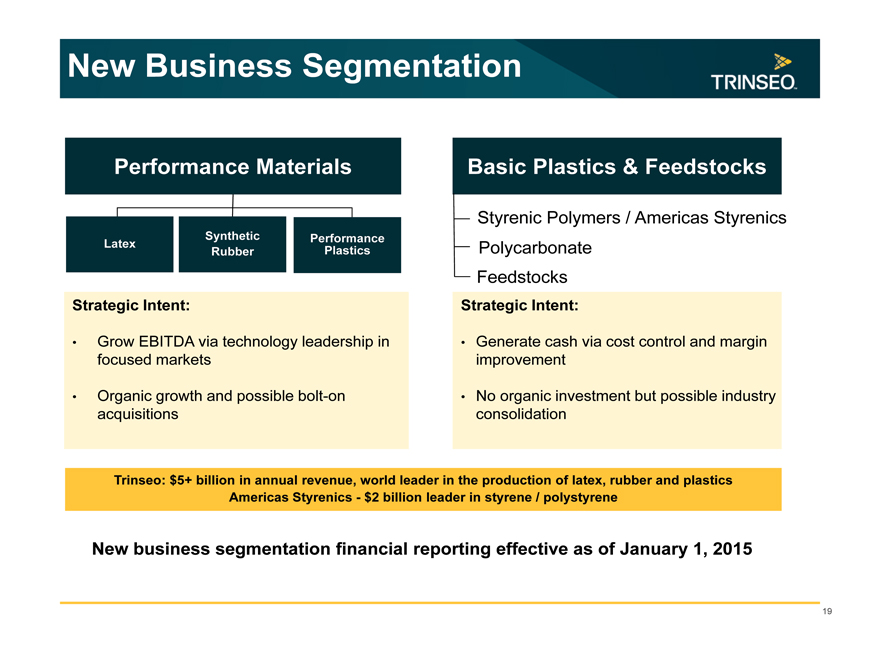

New Business Segmentation

Performance Materials

Latex Synthetic Performance

Rubber Plastics

Strategic Intent:

Grow EBITDA via technology leadership in focused markets

Organic growth and possible bolt-on acquisitions

Basic Plastics & Feedstocks

Styrenic Polymers / Americas Styrenics Polycarbonate Feedstocks

Strategic Intent:

Generate cash via cost control and margin improvement

No organic investment but possible industry consolidation

Trinseo: $5+ billion in annual revenue, world leader in the production of latex, rubber and plastics Americas Styrenics—$2 billion leader in styrene / polystyrene

New business segmentation financial reporting effective as of January 1, 2015

19

|

|

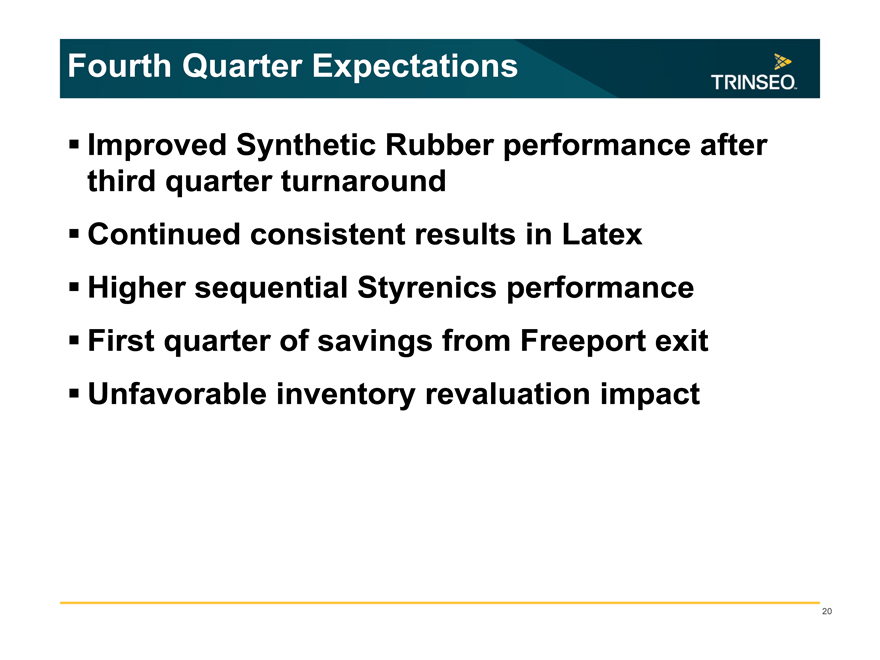

Fourth Quarter Expectations

Improved Synthetic Rubber performance after third quarter turnaround Continued consistent results in Latex Higher sequential Styrenics performance First quarter of savings from Freeport exit Unfavorable inventory revaluation impact

20

|

|

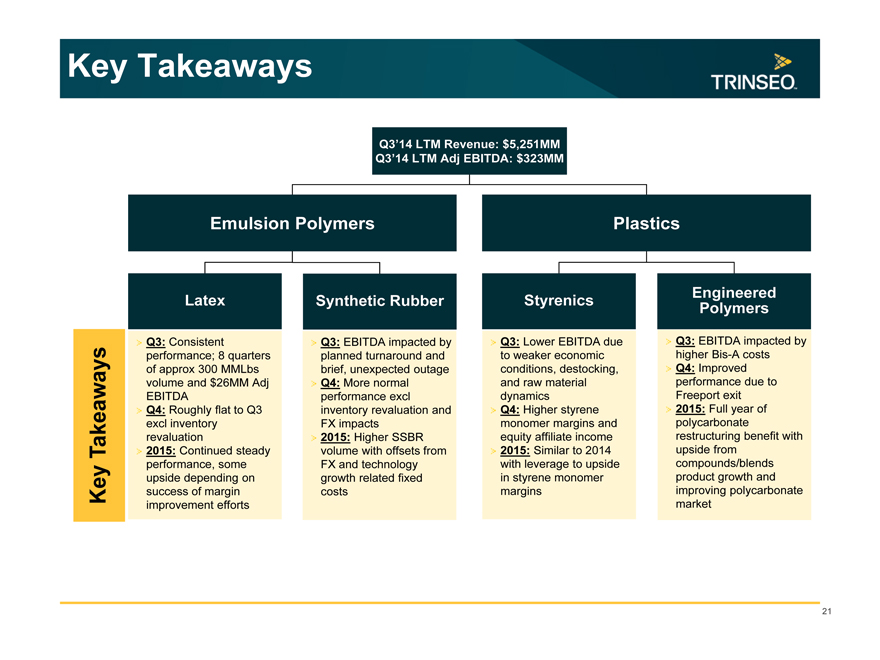

Key Takeaways

Q3’14 LTM Revenue: $5,251MM Q3’14 LTM Adj EBITDA: $323MM

Emulsion Polymers

Plastics

Latex Synthetic Rubber Styrenics

Engineered Polymers

Key Takeaways

Q3: Consistent performance; 8 quarters of approx 300 MMLbs volume and $26MM Adj EBITDA

Q4: Roughly flat to Q3 excl inventory revaluation 2015: Continued steady performance, some upside depending on success of margin improvement efforts

Q3: EBITDA impacted by planned turnaround and brief, unexpected outage Q4: More normal performance excl inventory revaluation and FX impacts 2015: Higher SSBR volume with offsets from FX and technology growth related fixed costs

Q3: Lower EBITDA due to weaker economic conditions, destocking, and raw material dynamics Q4: Higher styrene monomer margins and equity affiliate income 2015: Similar to 2014 with leverage to upside in styrene monomer margins

Q3: EBITDA impacted by higher Bis-A costs Q4: Improved performance due to Freeport exit 2015: Full year of polycarbonate restructuring benefit with upside from compounds/blends product growth and improving polycarbonate market

21

|

|

Q&A

™ Trademark

|

|

Appendix

™ Trademark

|

|

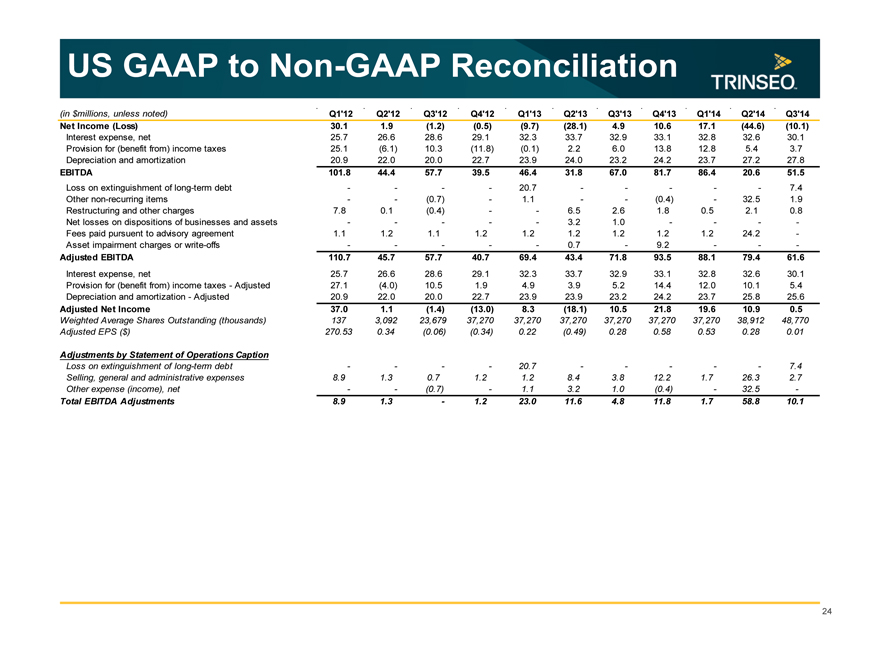

US GAAP to Non-GAAP Reconciliation

(in $millions, unless noted) Q1’12 Q2’12 Q3’12 Q4’12 Q1’13 Q2’13 Q3’13 Q4’13 Q1’14 Q2’14 Q3’14

Net Income (Loss) 30.1 1.9 (1.2) (0.5) (9.7) (28.1) 4.9 10.6 17.1 (44.6) (10.1)

Interest expense, net 25.7 26.6 28.6 29.1 32.3 33.7 32.9 33.1 32.8 32.6 30.1

Provision for (benefit from) income taxes 25.1 (6.1) 10.3 (11.8) (0.1) 2.2 6.0 13.8 12.8 5.4 3.7

Depreciation and amortization 20.9 22.0 20.0 22.7 23.9 24.0 23.2 24.2 23.7 27.2 27.8

EBITDA 101.8 44.4 57.7 39.5 46.4 31.8 67.0 81.7 86.4 20.6 51.5

Loss on extinguishment of long-term debt ———— 20.7 ————— 7.4

Other non-recurring items —— (0.7) — 1.1 —— (0.4) — 32.5 1.9

Restructuring and other charges 7.8 0.1 (0.4) —— 6.5 2.6 1.8 0.5 2.1 0.8

Net losses on dispositions of businesses and assets ————— 3.2 1.0 ——— -

Fees paid pursuent to advisory agreement 1.1 1.2 1.1 1.2 1.2 1.2 1.2 1.2 1.2 24.2 -

Asset impairment charges or write-offs ————— 0.7 — 9.2 —— -

Adjusted EBITDA 110.7 45.7 57.7 40.7 69.4 43.4 71.8 93.5 88.1 79.4 61.6

Interest expense, net 25.7 26.6 28.6 29.1 32.3 33.7 32.9 33.1 32.8 32.6 30.1

Provision for (benefit from) income taxes—Adjusted 27.1 (4.0) 10.5 1.9 4.9 3.9 5.2 14.4 12.0 10.1 5.4

Depreciation and amortization—Adjusted 20.9 22.0 20.0 22.7 23.9 23.9 23.2 24.2 23.7 25.8 25.6

Adjusted Net Income 37.0 1.1 (1.4) (13.0) 8.3 (18.1) 10.5 21.8 19.6 10.9 0.5

Weighted Average Shares Outstanding (thousands) 137 3,092 23,679 37,270 37,270 37,270 37,270 37,270 37,270 38,912 48,770

Adjusted EPS ($) 270.53 0.34 (0.06) (0.34) 0.22 (0.49) 0.28 0.58 0.53 0.28 0.01

Adjustments by Statement of Operations Caption

Loss on extinguishment of long-term debt ———— 20.7 ————— 7.4

Selling, general and administrative expenses 8.9 1.3 0.7 1.2 1.2 8.4 3.8 12.2 1.7 26.3 2.7

Other expense (income), net —— (0.7) — 1.1 3.2 1.0 (0.4) — 32.5 -

Total EBITDA Adjustments 8.9 1.3 — 1.2 23.0 11.6 4.8 11.8 1.7 58.8 10.1

24

|

|

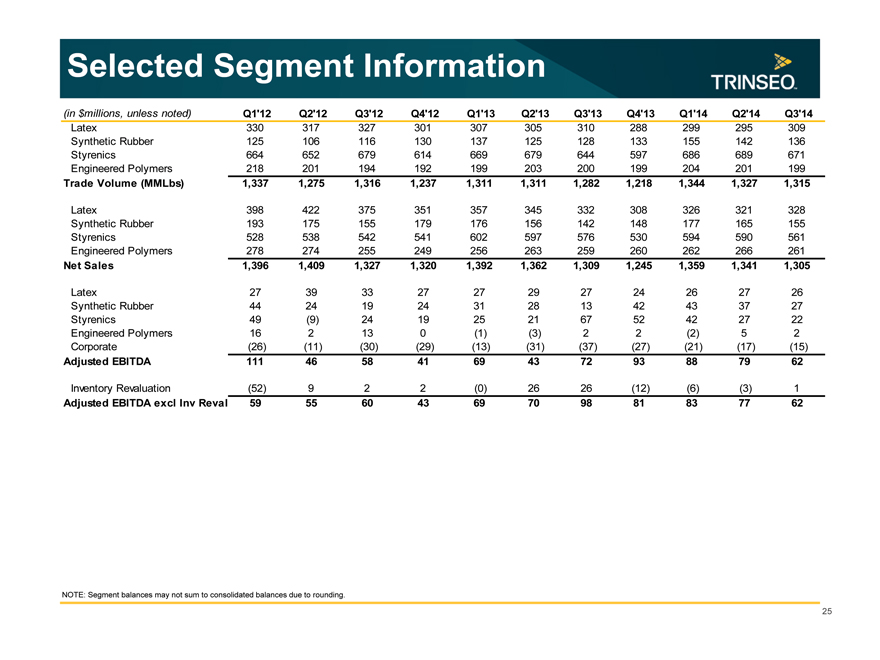

Selected Segment Information

(in $millions, unless noted) Q1’12 Q2’12 Q3’12 Q4’12 Q1’13 Q2’13 Q3’13 Q4’13 Q1’14 Q2’14 Q3’14

Latex 330 317 327 301 307 305 310 288 299 295 309

Synthetic Rubber 125 106 116 130 137 125 128 133 155 142 136

Styrenics 664 652 679 614 669 679 644 597 686 689 671

Engineered Polymers 218 201 194 192 199 203 200 199 204 201 199

Trade Volume (MMLbs) 1,337 1,275 1,316 1,237 1,311 1,311 1,282 1,218 1,344 1,327 1,315

Latex 398 422 375 351 357 345 332 308 326 321 328

Synthetic Rubber 193 175 155 179 176 156 142 148 177 165 155

Styrenics 528 538 542 541 602 597 576 530 594 590 561

Engineered Polymers 278 274 255 249 256 263 259 260 262 266 261

Net Sales 1,396 1,409 1,327 1,320 1,392 1,362 1,309 1,245 1,359 1,341 1,305

Latex 27 39 33 27 27 29 27 24 26 27 26

Synthetic Rubber 44 24 19 24 31 28 13 42 43 37 27

Styrenics 49 (9) 24 19 25 21 67 52 42 27 22

Engineered Polymers 16 2 13 0 (1) (3) 2 2 (2) 5 2

Corporate (26) (11) (30) (29) (13) (31) (37) (27) (21) (17) (15)

Adjusted EBITDA 111 46 58 41 69 43 72 93 88 79 62

Inventory Revaluation (52) 9 2 2 (0) 26 26 (12) (6) (3) 1

Adjusted EBITDA excl Inv Reval 59 55 60 43 69 70 98 81 83 77 62

NOTE: Segment balances may not sum to consolidated balances due to rounding.

25