Attached files

| file | filename |

|---|---|

| EX-31.02 - EXHIBIT 31.02 - Brooks Automation, Inc. | exhibit3102brks201310-k1.htm |

| EX-21.01 - EXHIBIT 21.01 - Brooks Automation, Inc. | exhibit21011.htm |

| EX-31.01 - EXHIBIT 31.01 - Brooks Automation, Inc. | exhibit3101brks201310-k1.htm |

| EX-23.01 - EXHIBIT 23.01 - Brooks Automation, Inc. | exhibit2301bdoconsent1.htm |

| EX-32 - EXHIBIT 32 - Brooks Automation, Inc. | exhibit32brks201310-k1.htm |

| EXCEL - IDEA: XBRL DOCUMENT - Brooks Automation, Inc. | Financial_Report.xls |

| EX-23.02 - EXHIBIT 23.02 - Brooks Automation, Inc. | exhibit2302pwcconsent1.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One) | ||

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For fiscal year ended September 30, 2014 | ||

or | ||

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the transition period from to . | ||

Commission File Number: 0-25434

Brooks Automation, Inc.

(Exact name of Registrant as Specified in Its Charter)

Delaware | 04-3040660 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

15 Elizabeth Drive Chelmsford, Massachusetts (Address of Principal Executive Offices) | 01824 (Zip Code) | |

978-262-2400

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.01 par value | The NASDAQ Stock Market LLC | |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Rule 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to the Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

(Do not check if a smaller reporting company) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ¨ No þ

The aggregate market value of the registrant's Common Stock, $0.01 par value, held by non-affiliates of the registrant as of March 31, 2014, was approximately $706,764,000 based on the closing price per share of $10.93 on that date on the Nasdaq Stock Market. As of March 31, 2014, 66,806,263 shares of the registrant's Common Stock, $0.01 par value, were outstanding. As of November 5, 2014, 66,927,388 shares of the registrant's Common Stock, $0.01, par value, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Proxy Statement involving the election of directors, which is expected to be filed within 120 days after the end of the registrant's fiscal year, are incorporated by reference in Part III of this Report.

BROOKS AUTOMATION, INC.

TABLE OF CONTENTS

PAGE NUMBER | ||

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

2

PART I

Item 1. | Business |

We are a leading worldwide provider of automation and cryogenic solutions for multiple markets including semiconductor manufacturing and life sciences. Our technologies, engineering competencies and global service capabilities provide customers speed to market and ensure high uptime and rapid response, which equate to superior value in our customers' mission-critical controlled environments. Since 1978, we have been a leading partner to the global semiconductor manufacturing markets and through product development initiatives and strategic business acquisitions we have expanded our products and services to meet the needs of customers in technology markets adjacent to semiconductor manufacturing and life sciences. We are headquartered in Chelmsford, Massachusetts and have full service operations in North America, Europe and Asia.

Our company initially developed and marketed automated handling equipment for front-end semiconductor manufacturing tools and became a publicly traded company in February 1995. Through both internal product development and business acquisitions we became the leading provider of these automation solutions in this market. Since that time, we have expanded both the markets we serve as well as our core product capabilities. A notable step in our expansion was the acquisition of Helix Technology Corporation in 2005, which provided us with leading technology solutions in vacuum equipment and allowed us to serve a broader set of markets. In 2011, we divested our contract manufacturing business to better focus on our core technology solutions.

In 2011, we identified life sciences as an underserved strategic market where our core competencies in automation and cryogenic solutions could provide enabling products and services to the market and favorable opportunities for growth of our business. Since 2011, we have made several strategic acquisitions to penetrate the automated sample storage system market, and we now are a leading worldwide provider of these solutions. In addition to automated sample management, our life sciences business offers related services, along with consumables and complementary bench-top instruments.

In addition to the acquisitions made to expand the non-semiconductor portions of our business, we have continued to make investments to maintain and grow our semiconductor product and service offerings. In 2012, we acquired Crossing Automation Inc., a Fremont, CA-based provider of automation solutions for the global semiconductor front-end market. In April 2014, we acquired Dynamic Micro Systems Semiconductor Equipment GmbH, or DMS, a German provider of automated contamination control solutions for front opening unified pod, or "FOUP," carriers and reticle storage.

In March 2014, we entered into an agreement to sell the Granville-Phillips Gas Analysis & Vacuum Measurement, or Granville-Phillips, business unit to MKS Instruments, Inc. for $87.0 million in cash and we completed this sale in May 2014. Unless otherwise noted, the description of our business relates solely to our continuing operations and does not include the operations of our former Granville-Phillips business unit.

We expect to continue our internal development efforts and seek acquisitions where we can expand or enhance our product and service offerings.

Markets

Our fiscal years 2014, 2013 and 2012 percentage of revenue by end market was as follows:

2014 | 2013 | 2012 | ||||||

Semiconductor capital equipment | 46 | % | 46 | % | 51 | % | ||

Service and spares | 19 | % | 21 | % | 17 | % | ||

Industrial capital equipment | 11 | % | 12 | % | 11 | % | ||

Other adjacent technology markets | 11 | % | 11 | % | 10 | % | ||

Life sciences | 13 | % | 10 | % | 11 | % | ||

100 | % | 100 | % | 100 | % | |||

The proportion of our revenue by end market is changing as a result of our internal product and sales initiatives, our acquisitions and divestitures and the cyclical nature of the semiconductor capital equipment market. Over time, we expect the percentage of revenue from our life science business to increase given its higher expected growth rate. Changes from year to year, however, will depend on a variety of factors, including the cyclicality of the semiconductor market.

Semiconductor capital equipment

The global semiconductor capital equipment industry is cyclical with a long term growth profile driven by the expanded use of semiconductor devices and the increase in device complexity, each necessitating incremental equipment purchases by manufacturers. This growth is increasingly focused in Asia. The production of advanced semiconductor chips is a complex and logistically challenging manufacturing activity. To create the tens of millions of microscopic transistors and connect them both

3

horizontally and in vertical layers in order to produce a functioning integrated circuit chip, or IC chip, silicon wafers must go through hundreds of process steps performed by complex processing equipment, or tools. A large production fabrication plant, or fab, may have more than 70 different types of process and metrology tools, totaling as many as 500 tools or more. Up to 40% of these tools perform processes in a vacuum, such as removing, depositing, or measuring material on wafer surfaces. Wafers can go through as many as 400 different process steps before fabrication is complete. These steps, which comprise the initial fabrication of the integrated circuit and are referred to in the industry as front-end processes, are repeated many times to create the desired pattern on the silicon wafer. As the complexity of semiconductors continues to increase, the number of process steps that occur in a vacuum environment have also increased, resulting in a greater need for both automation and vacuum technology solutions due to the sensitive handling requirements and increased number of tools. The requirement for efficient, higher throughput and extremely clean manufacturing for semiconductor wafer fabs and other high performance electronic-based products has created a substantial market for substrate handling automation (moving the wafers around and between tools in a semiconductor fab), tool automation (the use of robots and modules used in conjunction with and inside process tools that move wafers from station-to-station), and vacuum systems technology to create and sustain the clean environment necessary to fabricate various products. The use of advanced processing to form three dimensional structures of the previously patterned integrated circuits is emerging in the industry. This processing, often referred to as Wafer Level Packaging, or WLP, is typically performed at what would be considered the back-end processing of an IC chip. Some traditional front-end processes are being used in this back-end advance packaging, thereby increasing the market for automation solutions.

Service and spares

Whereas sales for production equipment are typically made to original equipment manufacturers (“OEMs”), the service and spares support of that equipment can be provided in collaboration with the OEMs, or through a relationship with the end-user manufacturer who is using that equipment in a productive capacity. While the majority of the market that we currently address with our service and spares activities is the semiconductor manufacturing market, we are actively looking to increase our service and spares offerings in the life science market.

Industrial capital equipment

In addition to semiconductor manufacturing, there are a variety of industrial manufacturing operations that require either a vacuum or significant cooling for effective deposition of films or coatings during the production process. The expansion of the use of mobile devices such as smart phones, tablets, and wearable technologies, and the resulting increase in the need for associated manufacturing equipment continues to drive demand for the use of vacuum solutions we provide. These deposition processes are typically performed on equipment that cycle from an uncontrolled atmospheric environment for loading and unloading to a controlled vacuum environment for processing. The transition to the controlled vacuum environment requires removal of large amounts of moisture inherent in the air by deep cooling of coils within the vacuum chamber. The increased need for the equipment necessary to deliver refrigerant to these coils has resulted in increased demand for our products.

Other adjacent technology markets

There are a variety of markets that have adopted, or are adopting, similar manufacturing methods to those utilized by the semiconductor industry. Frequently, these markets have common customers but technology applications in the end markets are still maturing. We serve a variety of these evolving markets including light emitting diode, or LED, applications. High Brightness LED, or HBLED, is a potential clean energy solution replacing incandescent lighting sources. We believe that the application of HBLED solutions will expand as manufacturing processes for these products advance, resulting in lower costs of production and more attractive pricing for these products. Organic LED, or OLED, solutions provide lower power consumption for high clarity still and video images. OLED applications are gaining traction in the mobile computing and telecommunications device markets. Other evolving markets which utilize our products include Micro-Electro-Mechanical Systems, or MEMS, manufacturing and solar panel manufacturing. MEMS applications, which include accelerometers, self tuning antennae and pressure gauges, are expanding in automotive, mobile computing and telecommunications device markets. We believe that solar panel production is also expanding, and our products are used in the production of thin film solar panels which require cooling to effectuate deposition and adhesion of the film on and to the panel.

Life Sciences

There is a broad market of devices, systems and consumables that support the pharmaceutical, biotechnology, healthcare research and diagnostics industries in the advanced handling, processing, storage and distribution of biological and compound samples. At the core of these activities is sample storage. Automated sample stores are generally more effective in maintaining a controlled environment, tracking samples, reliably processing and quickly handling samples, than are manual systems. These automated sample storage management systems are at the center of the complete sample handling process. With the advent of personalized medicine linking DNA to optimal treatment regimens, the expansion of mass storage of key biological material to support rapidly expanding comparative and longitudinal studies, and the accumulation of samples taken from surgical and other

4

procedures, we believe that the numbers of samples in storage is expanding between 25 and 30% per annum on a global basis. We believe that this expansion, together with the problems associated with traditional manual storage systems, will drive consistent growth in automated sample management equipment.

Products

In the semiconductor industry, wafer handling robotics have emerged as a critical technology in determining the efficacy and productivity of complex production tools in the world's most advanced 300mm wafer fabs. A tool is designed and built around a process chamber using automation technology to move wafers into and out of the chamber. Today, OEMs design and build their tools using a cluster architecture, whereby several process chambers are mounted to one central transfer module. High wafer throughput and new materials require advanced automation solutions to address the challenging equipment needs for multiple substrate sizes, including the emerging sub 20nm technology nodes, Thru Silicon Via, EUV Lithography and 450mm substrates. We specialize in developing and building the handling systems, as well as the vacuum technologies used in these tools. Our products can be utilized as individual components or as complete integrated handling systems. In addition, our automation products support both atmospheric and vacuum based processes and are designed to improve performance and productivity of the manufacturing process. The majority of our product revenue is derived from sales to OEMs and end-user semiconductor device manufacturers.

We provide high vacuum pumps which are required in certain process steps to create and to optimize the process environment by maintaining pressure consistency of the known process gas. To achieve optimal production yields, semiconductor manufacturers must ensure that each process operates at carefully controlled pressure levels. Impurities or incorrect pressure levels can lower production yields, thereby significantly increasing the cost per usable IC chip produced. Some key vacuum processes include: dry etching and dry stripping, chemical vapor deposition, or CVD, physical vapor deposition, or PVD, and ion implantation. Our cryogenic vacuum pumps are considered the industry standard by many leading semiconductor device manufacturers for ion implant and PVD applications.

In the HBLED market we have worked with leading manufacturers to develop advanced automation solutions that improve the productivity of processes that were previously manual. These LEDs are also made using vacuum processes for certain production steps, very similar to the steps used in semiconductor manufacturing. We have been successful in capturing LED market share for our vacuum product offerings and for high payload automated tool architectures. In other markets, such as MEMS and WLP applications, unique wafer handling and automation solutions are required to accommodate increasingly thinner and sometimes bowed substrates. We are developing differentiated solutions to address the requirements in these high growth market segments.

For the life science markets we provide automated sample management platforms that store samples (e.g., nucleic acid, blood, drug compounds, biological tissue, etc.) in a controlled environment and automate the process (vials are typically stored in racks or plates) of subsequently retrieving specifically selected samples from those racks or plates. The controlled storage environments ensure that samples are preserved within a narrow temperature band to maintain their integrity for long periods while providing absolute accuracy in the identification and selection of samples during the storage and retrieval processes.

In providing comprehensive solutions to the life science markets we also provide equipment for sealing and de-sealing samples stored on plates and automated cappers and de-cappers for samples stored in tubes. We also provide consumables in the form of sample plates, micro-plates and tubes and support services for many of the customers who have purchased our equipment.

Segments

We report financial results in three segments: Brooks Product Solutions; Brooks Global Services; and Brooks Life Science Systems.

The Brooks Product Solutions segment provides a variety of products and solutions that enable improved throughput and yield in controlled operating environments. Those products include atmospheric and vacuum robots, robotic modules, and tool automation systems that provide precision handling and clean wafer environments as well as vacuum pumping and thermal management solutions used to create and control critical process vacuum applications.

The Brooks Global Services segment provides an extensive range of support services, including repair services, diagnostic support services, and installation services in support of the base equipment installed by our Brooks Product Solutions segment, which enable our customers to maximize process tool uptime and productivity. This segment also provides end-user customers with spare parts to maximize customer tool productivity.

The Brooks Life Science Systems segment provides automated sample management systems for automated cold sample storage, equipment for sample preparation and handling, consumables, and parts and support services to a wide range of life science customers including pharmaceutical companies, biotechnology companies, national laboratories, research institutes and research hospitals.

5

Customers

Within the semiconductor industry, we sell our products and services to most of the major semiconductor chip manufacturers and semiconductor equipment OEMs in the world. Our customers outside the semiconductor industry are broadly diversified. We have major customers in North America, Europe and Asia. Additionally, although much of our equipment sales ship to OEMs in the United States, many of our products are incorporated into equipment that is ultimately utilized outside of North America. See Part I, Item 1A, “Risk Factors” for a discussion of the risks related to foreign operations. The Brooks Global Services business provides support to leading OEMs, fabs and foundries across the globe.

Our life sciences systems solutions are used by pharmaceutical companies, biotechnology companies, national laboratories, research institutes and research hospitals. There is no continuing concentration of customers for the Brooks Life Science Systems segment although given the size of particular projects, an individual customer may be significant to the life science segment in a given quarter or fiscal year.

Relatively few customers account for a substantial portion of our revenue, with the top 10 customers accounting for approximately 37% of our business in fiscal year 2014. We have one customer, Applied Materials, Inc., that accounted for 11% of our overall revenue for the year.

For purposes of determining the percentage of revenue from any OEM customer, we do not include revenue from products sold to a contract manufacturer customer which in turn sells to the OEM. If we did include revenue from products sold to contract manufacturer customers supporting our OEM customers, the percentage of our total revenue derived from certain OEM customers would be higher.

Sales, Marketing and Customer Support

We market and sell most of our semiconductor, industrial and other adjacent technology market products and services in Asia, Europe, the Middle East and North America through our direct sales organization. The sales process for our products is often multilevel, involving a team comprised of individuals from sales, marketing, engineering, operations and senior management. In many cases we assign a team to a customer and that team engages the customer at different levels of its organization to facilitate planning, provide product customization when required, and ensure open communication and support. Some of our vacuum products and services are sold through local country distributors. Additionally, we serve the Japanese market for our robotics and automation products through Yaskawa Brooks Automation, our joint venture with Yaskawa Electric Corporation of Japan.

Much of our life sciences sales are completed through our direct Brooks Life Science Systems sales force, particularly our store systems and services. In addition, we facilitate the sale of consumables and instruments with distributors which reach a broader range of customers. In regions with emerging life science industries such as China, India and the Middle East, we leverage local distributors to assist in the sales process of stores. The sales process for our larger sample management systems may take 6-18 months to complete and it involves a team typically comprised of individuals from sales, marketing, engineering and senior management.

We typically provide warranties from one to two years, depending upon the type of product, with the average warranty on our products lasting for 15 months.

Our marketing activities include participation in trade shows, delivery of seminars, participation in industry forums, distribution of sales literature, publication of press releases and articles in business and industry publications. To enhance communication and support, particularly with our international customers, we maintain sales and service centers in Asia, Europe, the Middle East and North America. These facilities, together with our headquarters, maintain local support capabilities and demonstration equipment for customers to evaluate. Customers are encouraged to discuss features and applications of our demonstration equipment with our engineers located at these facilities.

Net revenue for the fiscal years ended September 30, 2014, 2013 and 2012 based upon the source of the order by geographic area is as follows (in thousands):

Year Ended September 30, | |||||||||||

2014 | 2013 | 2012 | |||||||||

North America | $ | 174,343 | $ | 177,779 | $ | 214,060 | |||||

Asia/Pacific | 198,695 | 154,358 | 183,406 | ||||||||

Europe | 109,810 | 90,303 | 91,517 | ||||||||

$ | 482,848 | $ | 422,440 | $ | 488,983 | ||||||

The geographic location of an OEM is not indicative of where our products will eventually be used. The geographic area for our orders is determined by the onward sale of an OEM system which incorporates our sub-systems and/or components.

6

Our property, plant and equipment as of September 30, 2014 and 2013 by geographic area is as follows (in thousands):

September 30, | |||||||

2014 | 2013 | ||||||

North America | $ | 40,232 | $ | 38,505 | |||

Asia/Pacific | 870 | 1,646 | |||||

Europe/Middle East | 9,081 | 7,355 | |||||

$ | 50,183 | $ | 47,506 | ||||

Competition

We operate in a variety of niches of varying breadth and with differing competitors and competitive dynamics. The semiconductor and adjacent technology markets, and process equipment manufacturing industries are highly competitive and characterized by continual changes and improvements in technology. A significant portion of equipment automation is still done in-house by OEMs. Our competitors among external vacuum automation suppliers are primarily Japanese companies such as Daihen Corporation, Daikin Industries, Ltd. and Rorze Corporation. Our competitors among vacuum components suppliers include Sumitomo Heavy Industries and Telemark, Inc. Atmospheric tool automation is typically less demanding, has fewer barriers to entry and has a larger field of competitors. We compete directly with other equipment automation suppliers of atmospheric modules and systems such as Hirata Corporation, Kawasaki Heavy Industries, Ltd., Genmark Automation, Inc., Rorze Corporation, Sankyo Seisakusho Co., Ltd., TDK Corporation and Sinfonia Technology Co., Ltd. Contract manufacturers such as Celestica Inc. and Flextronics International Ltd. also provide assembly and manufacturing services for atmospheric systems.

Our Life Science Systems business unit competes with a number of private companies in providing automated sample management systems. These competitors include Hamilton Company, Liconic AG and TTP LabTech, Ltd.

We believe our customers will purchase our equipment automation products and vacuum subsystems as long as our products continue to provide the necessary throughput, reliability, contamination control and accuracy at an acceptable price. We believe that we have competitive offerings with respect to all of these factors. We cannot guarantee, however, that we will be successful in selling our products to OEMs who currently satisfy a portion of their automation needs in-house or from other independent suppliers, regardless of the performance or price of our products.

Research and Development

Our research and development efforts are focused on developing new products and also enhancing the functionality, degree of integration, reliability and performance of our existing products. Our engineering, marketing, operations and management personnel leverage their close collaborative relationships with many of their counterparts in customer organizations in an effort to proactively identify market demands which helps us refocus our research and development investment to meet our customers' demands. With the rapid pace of change that characterizes the markets we serve, it is essential for us to provide high-performance and reliable products in order for us to maintain our leadership position.

Our research and development spending for fiscal years 2014, 2013 and 2012 was $52.6 million, $46.2 million and $44.7 million, respectively. The expansion in research and development spending primarily reflects our investment in life sciences as we have developed the Twinbank platform and continue to develop automated bio-sample storage solutions for environments operating at ultra-low temperatures.

Manufacturing

Our manufacturing operations are used for product assembly, integration and testing. We have implemented quality assurance procedures that include standard design practices including reliability testing and analysis, supplier and component selection procedures, vendor controls, manufacturing process controls, and service processes that ensure high-quality performance of our products. Our major manufacturing facilities are located in Chelmsford, Massachusetts; Poway, California; Spokane, Washington; Monterrey, Mexico; Yongin-City, South Korea; Manchester, UK; and Jena, Germany. We also provide service and spare parts support to end-users throughout the world. Many of our service customers are based outside of the United States, with many in Asia. We have service and support locations close to these customers to provide rapid response to their service needs. We have service and support locations in Chelmsford, Massachusetts; Poway, California; Fremont, California; Spokane, Washington; Chu Bei City, Taiwan; Yongin-City, South Korea; Yokohama, Japan; Shanghai, China; Singapore; Jena, Germany; Oberdiessbach, Switzerland; Manchester, UK; and Kiryat-Gat, Israel.

Our manufacturing operations are designed to provide high quality, low cost, differentiated products to our customers in short lead times through responsive and flexible processes and sourcing strategies. We utilize lean manufacturing techniques for a large portion of our manufacturing capabilities. This includes the outsourcing of assemblies and products to competitive regions, including Asia. We expect to continue to broaden our sourcing of certain portions of our manufacturing process to

7

ensure we continue to provide high quality products at competitive costs. We also believe the continued sourcing of portions of our manufacturing processes in these regions allows us to better serve our customers in these regions.

Patents and Proprietary Rights

We rely on patents, trade secret laws, confidentiality procedures, copyrights, trademarks and licensing agreements to protect our technology. Due to the rapid technological change that characterizes the life sciences, semiconductor, adjacent technology markets and related process equipment industries, we believe that the improvement of existing technology, reliance upon trade secrets and unpatented proprietary know-how and the development of new products may be as important as patent protection in establishing and maintaining a competitive advantage. To protect trade secrets and know-how, it is our policy to require all employees to enter into proprietary information and nondisclosure agreements. We cannot guarantee that these efforts will meaningfully protect our trade secrets.

As of September 30, 2014, we owned approximately 480 issued U.S. patents, with various corresponding patents issued in foreign jurisdictions. We also had approximately 140 pending U.S. patent applications, with foreign counterparts of certain of these applications having been filed or may be filed at the appropriate time. Our patents will expire at various dates through 2032.

Backlog

Total backlog for our products as of September 30, 2014, totaled $126.9 million as compared to $107.2 million at September 30, 2013. Backlog or total backlog, includes all purchase orders for which a customer has scheduled delivery, regardless of the expected delivery date, and consists principally of orders for products and service agreements. The backlog for our products within the next 12 months was $113.6 million and $104.9 million at September 30, 2014 and 2013, respectively. Twelve-month backlog includes orders scheduled to be delivered within the next 12 months. Backlog for products with scheduled deliveries beyond one year relate primarily to our life science products.

Backlog as of any particular date should not be relied upon as indicative of our revenue for any future period. A substantial percentage of current business generates no backlog because we deliver our products and services in the same period in which the order is received. The orders included in our backlog may also be canceled or rescheduled by customers without significant penalty.

Environmental Matters

We are subject to federal, state, and local environmental laws and regulations, as well as the environmental laws and regulations of the foreign national and local jurisdictions in which we have manufacturing facilities. We believe we are in material compliance with all such laws and regulations.

Compliance with foreign, federal, state, and local laws and regulations has not had, and is not expected to have, an adverse effect on our capital expenditures, competitive position, financial condition or results of operations.

Employees

At September 30, 2014, we had 1,455 full time employees. In addition, we employ part time workers and contractors. Approximately 45 employees in our facility in Jena, Germany are covered by a collective bargaining agreement. We consider our relationships with these and all employees to be good.

Available Information

We file annual, quarterly, and current reports, proxy statements, and other documents with the Securities and Exchange Commission, or SEC, under the Securities Exchange Act of 1934, as amended, or the Exchange Act. The public may read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Also, the SEC maintains an Internet website that contains reports, proxy and information statements, and other information regarding issuers, including Brooks Automation, Inc., that file electronically with the SEC. The public can obtain any documents that we file with the SEC at www.sec.gov.

Our internet website address is http://www.brooks.com. Through our website, we make available, free of charge, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports, as soon as reasonably practicable after such materials are electronically filed, or furnished to, the SEC. These SEC reports can be accessed through the investors section of our website. The information found on our website is not part of this or any other report we file with or furnish to the SEC.

8

Item 1A. | Risk Factors |

Factors That May Affect Future Results

You should carefully consider the risks described below and the other information in this report before deciding to invest in shares of our common stock. These are the risks and uncertainties we believe are most important for you to consider. Additional risks and uncertainties not presently known to us, which we currently deem immaterial or which are similar to those faced by other companies in our industry or business in general, may also impair our business operations. If any of the following risks or uncertainties actually occurs, our business, financial condition and operating results would likely suffer. In that event, the market price of our common stock could decline and you could lose all or part of your investment.

Risks Relating to Our Industry

Due in part to the cyclical nature of the semiconductor manufacturing industry and related industries, as well as due to volatility in worldwide capital and equity markets, we have previously incurred operating losses and may have future losses.

Our business is largely dependent on capital expenditures in the semiconductor manufacturing industry and other businesses employing similar manufacturing technologies. The semiconductor manufacturing industry in turn depends on current and anticipated demand for integrated circuits and the products that use them. In recent years, these businesses have experienced unpredictable and volatile business cycles due in large part to rapid changes in demand and manufacturing capacity for semiconductors, and these cycles have had an impact on our business, sometimes causing declining revenue and operating losses. We could experience future operating losses during an industry downturn. If an industry downturn continues for an extended period of time, our business could be materially harmed. Conversely, in periods of rapidly increasing demand, we could have insufficient inventory and manufacturing capacity to meet our customers' needs on a timely basis, which could result in the loss of customers and various other expenses that could reduce gross margins and profitability.

We face competition which may lead to price pressure and otherwise adversely affect our sales.

We face competition throughout the world in each of our product and service areas, including from the competitors discussed in Part I, Item 1, “Business - Competition” as well as from internal automation capabilities at larger OEMs. Many of our competitors have substantial engineering, manufacturing, marketing and customer support capabilities. We expect our competitors to continue to improve the performance of their current products and services and to introduce new products, services and technologies that could adversely affect sales of our current and future products and services. New products, services and technologies developed by our competitors or more efficient production of their products or provisions of their services could require us to make significant price reductions or decide not to compete for certain orders. If we fail to respond adequately to pricing pressures or fail to develop products with improved performance or developments or better quality services with respect to the other factors on which we compete, we could lose customers or orders. If we are unable to compete effectively, our business and prospects could be materially harmed.

Risks Relating to Our Operations

Our operating results could fluctuate significantly, which could negatively impact our business.

Our revenue, operating margins and other operating results could fluctuate significantly from quarter to quarter depending upon a variety of factors, including:

• | demand for our products as a result of the cyclical nature of the semiconductor manufacturing industry and the markets upon which the industry depends or otherwise; |

• | changes in the timing and terms of product orders by our customers as a result of our customer concentration or otherwise; |

• | changes in the mix of products and services that we offer; |

• | changes in the demand for the mix of products and services that we offer; |

• | timing and market acceptance of our new product and services introductions; |

• | delays or problems in the planned introduction of new products or service, or in the performance of any such products following delivery to customers or the quality of such services; |

• | new products, services or technological innovations by our competitors, which can, among other things, render our products less competitive due to the rapid technological changes in the markets in which we provide products and services; |

• | the timing and related costs of any acquisitions, divestitures or other strategic transactions; |

9

• | our ability to reduce our costs in response to decreased demand for our products and services; |

• | our ability to accurately estimate customer demand, including the accuracy of demand forecasts used by us; |

• | disruptions in our manufacturing process or in the supply of components to us; |

• | write-offs for excess or obsolete inventory; and |

• | competitive pricing pressures. |

As a result of these risks, we believe that quarter-to-quarter comparisons of our revenue and operating results may not be meaningful, and that these comparisons may not be an accurate indicator of our future performance.

If we do not continue to introduce new products and services that reflect advances in technology in a timely and effective manner, our products and services may become obsolete and our operating results will suffer.

Our success is dependent on our ability to respond to the technological change present in the markets we serve. The success of our product development and introduction depends on our ability to:

• | accurately identify and define new market opportunities, products and services; |

• | obtain market acceptance of our products and services; |

• | timely innovate, develop and commercialize new technologies and applications; |

• | adjust to changing market conditions; |

• | differentiate our offerings from our competitors' offerings; |

• | obtain and maintain intellectual property rights where necessary; |

• | continue to develop a comprehensive, integrated product and service strategy; |

• | properly price our products and services; and |

• | design our products to high standards of manufacturability so that they meet customer requirements. |

If we cannot succeed in responding in a timely manner to technological and/or market changes or if the new products and services that we introduce do not achieve market acceptance, our competitive position would diminish which could materially harm our business and our prospects.

The global nature of our business exposes us to multiple risks.

For the fiscal years ended September 30, 2014 and 2013, approximately 64% and 58%, respectively, of our revenue was derived from sales outside North America. We expect that international sales, including increased sales in Asia, will continue to account for a significant portion of our revenue. We maintain a global footprint of sales, service and repair operations. As a result of our international operations, we are exposed to many risks and uncertainties, including:

• | longer sales-cycles and time to collection; |

• | tariff and international trade barriers; |

• | fewer or less certain legal protections for intellectual property and contract rights abroad; |

• | different and changing legal and regulatory requirements in the jurisdictions in which we operate; |

• | government currency control and restrictions on repatriation of earnings; |

• | fluctuations in foreign currency exchange and interest rates, particularly in Asia and Europe; and |

• | political and economic instability, changes, hostilities and other disruptions in regions where we operate. |

Negative developments in any of these areas in one or more countries could result in a reduction in demand for our products, the cancellation or delay of orders already placed, threats to our intellectual property, difficulty in collecting receivables, and a higher cost of doing business, any of which could materially harm our business and profitability.

Our business could be materially harmed if we fail to adequately integrate the operations of the businesses that we have acquired or may acquire.

We have made in the past, and may make in the future, acquisitions or significant investments in businesses with complementary products, services and/or technologies. Our acquisitions present numerous risks, including:

• | difficulties in integrating the operations, technologies, products and personnel of the acquired companies and realizing the anticipated synergies of the combined businesses; |

• | defining and executing a comprehensive product strategy; |

• | managing the risks of entering markets or types of businesses in which we have limited or no direct experience; |

10

• | the potential loss of key employees, customers and strategic partners of ours or of acquired companies; |

• | unanticipated problems or latent liabilities, such as problems with the quality of the installed base of the target company's products or infringement of another company's intellectual property by a target company's activities or products; |

• | problems associated with compliance with the acquired company's existing contracts; |

• | difficulties in managing geographically dispersed operations; and |

• | the diversion of management's attention from normal daily operations of the business. |

If we acquire a new business, we may be required to expend significant funds, incur additional debt or issue additional securities, which may negatively affect our operations and be dilutive to our stockholders. In periods following an acquisition, we will be required to evaluate goodwill and acquisition-related intangible assets for impairment. When such assets are found to be impaired, they will be written down to estimated fair value, with a charge against earnings. The failure to adequately address these risks or the impairment of any assets could materially harm our business and financial results.

Entering new markets introduces new competitors and commercial risks.

A key part of our growth strategy is to continue expanding beyond the semiconductor manufacturing market into semiconductor adjacent and life sciences markets. As part of this strategy, we expect to diversify our product sales and service revenue by leveraging our core technologies, which requires investments and resources which may not be available as needed. We cannot guarantee that we will be successful in leveraging our capabilities into the life sciences market to meet all the needs of these new customers and to compete favorably. Because a significant portion of our growth potential may be dependent on our ability to increase sales to markets beyond semiconductor manufacturing, our inability to successfully enter new markets may adversely impact future financial results.

Changes in key personnel could impair our ability to execute our business strategy.

The continuing service of our executive officers and essential engineering, technical and management personnel, together with our ability to attract and retain such personnel, is an important factor in our continuing ability to execute our strategy. There is substantial competition to attract such employees and the loss of any such key employees could have a material adverse effect on our business and operating results. The same could be true if we were to experience a high turnover rate among engineering and technical personnel and we were unable to replace them.

Our failure to protect our intellectual property could adversely affect our future operations.

Our ability to compete is significantly affected by our ability to protect our intellectual property. We rely upon patents, trade secret laws, confidentiality procedures, copyrights, trademarks and licensing agreements to protect our technology. Existing trade secret, trademark and copyright laws offer only limited protection. Our success depends in part on our ability to obtain and enforce patent protection for our products both in the United States and in other countries. We own numerous U.S. and foreign patents, and we intend to file additional applications, as appropriate, for patents covering our products and technology. Any issued patents owned by or licensed to us may be challenged, invalidated or circumvented, and the rights under these patents may not provide us with competitive advantages. In addition, the laws of some countries in which our products are or may be developed, manufactured or sold may not fully protect our products. Due to the rapid technological change that characterizes the semiconductor and adjacent technology markets, we believe that the improvement of existing technology, reliance upon trade secrets and unpatented proprietary know-how and the development of new products may be as important as patent protection in establishing and maintaining competitive advantage. To protect trade secrets and know-how, it is our policy to require all technical and management personnel to enter into nondisclosure agreements.

We cannot guarantee that the steps we have taken to protect our intellectual property will be adequate to prevent the misappropriation of our technology. Other companies could independently develop similar or superior technology without violating our intellectual property rights. In the future, it may be necessary to engage in litigation or like activities to enforce our intellectual property rights, to protect our trade secrets or to determine the validity and scope of proprietary rights of others, including our customers. This could require us to incur significant expenses and to divert the efforts and attention of our management and technical personnel from our business operations.

The expiration of our patents over time could lead to an increase of competition and a decline in our revenue.

One of our main competitive strengths is our technology and we are dependent on our patent rights and other intellectual property rights to maintain our competitive position. While our current patents will expire from time to time through 2032, certain significant patents will expire within two years, including a patent related to technology in one of our core automation products expiring in 2015 and patents which we license to third parties in exchange for agreed upon royalties expiring in 2016. In addition to the loss of revenue from royalties, the expiration of patents could result in increased competition and declines in product and service revenue.

11

We may be subject to claims of infringement of third-party intellectual property rights, or demands that we license third-party technology, which could result in significant expense and prevent us from using our technology.

There has been substantial litigation regarding patent and other intellectual property rights in the semiconductor-related industries. We have in the past been, and may in the future be, notified that we may be infringing intellectual property rights possessed by third parties. We cannot guarantee that infringement claims by third parties or other claims for indemnification by customers or end-users of our products resulting from infringement claims will not be asserted in the future or that such assertions, whether or not proven to be true, will not materially and adversely affect our business, financial condition and results of operations.

We cannot predict the extent to which we might be required to seek licenses or alter our products so that they no longer infringe the rights of others. We also cannot guarantee that licenses will be available or the terms of any licenses we may be required to obtain will be reasonable. Similarly, changing our products or processes to avoid infringing the rights of others may be costly or impractical and could detract from the value of our products. If a judgment of infringement were obtained against us, we could be required to pay substantial damages and a court could issue an order preventing us from selling one or more of our products. Further, the cost and diversion of management attention brought about by such litigation could be substantial, even if we were to prevail. Any of these events could result in significant expense to us and may materially harm our business and our prospects.

If our manufacturing sites were to experience a significant disruption in operations, our business could be materially harmed, while the failure to estimate customer demand accurately could result in excess or obsolete inventory.

We have a limited number of manufacturing facilities for our products and we have moved portions of our manufacturing to third parties, including some in lesser developed countries. If the operations at any one of these facilities were disrupted as a result of a natural disaster, fire, power or other utility outage, work stoppage or other similar event, our business could be seriously harmed because we may be unable to manufacture and ship products and parts to our customers in a timely fashion. The impact of any disruption at one of our facilities may be exacerbated if the disruption occurs at a time when we need to rapidly increase our manufacturing capabilities to meet increased demand or expedited shipment schedules.

Moreover, if actual demand for our products is different than expected, we may purchase more/fewer component parts than necessary or incur costs for canceling, postponing or expediting delivery of such parts. If we purchase inventory in anticipation of customer demand that does not materialize, or if our customers reduce or delay orders, we may incur excess inventory charges. Any or all of these factors could materially and adversely affect our business, financial condition and results of operations.

Our business could be materially harmed if one or more key suppliers fail to continuously deliver key components of acceptable cost and quality.

We currently obtain many of our key components on an as-needed, purchase order basis from numerous suppliers. In some cases we have only a single source of supply for necessary components and materials used in the manufacturing of our products. Further, we are increasing our sourcing of products in Asia, and particularly in China, and we do not have a previous course of dealing with many of these suppliers. We do not generally have long-term supply contracts with any of these suppliers, and many of them underwent cost-containment measures in light of the last significant industry downturn in 2008 and 2009. As the industry has recovered, these suppliers have faced challenges in delivering components on a timely basis. The volatility in demand of these components has led some of our vendors to exit the semiconductor market, and other vendors may also decide to exit this market. Our inability to obtain components or materials in required quantities or of acceptable cost and quality and with the necessary continuity of supply could result in delays or reductions in product shipments to our customers. In addition, if a supplier or sub-supplier suffers a production stoppage or delay for any reason, including natural disasters such as the tsunamis that affected Japan and Thailand, this could result in a delay or reduction in our product shipments to our customers. Any of these contingencies could cause us to lose customers, result in delayed or lost revenue and otherwise materially harm our business.

Our outsource providers may fail to perform as we expect.

Outsource providers have played and will continue to play a key role in our manufacturing operations and in many of our transactional and administrative functions, such as information technology and facilities management. Although we attempt to select reputable providers and secure their performance on terms documented in written contracts, it is possible that one or more of these providers could fail to perform as we expect and such failure could have an adverse impact on our business.

12

Our business relies on certain critical information systems and a failure or breach of such a system could harm our business and results of operations and, in the event of unauthorized access to a customer’s data or our data, incur significant legal and financial exposure and liabilities.

We maintain and rely upon certain critical information systems for the effective operation of our business. These information systems include telecommunications, the internet, our corporate intranet, various computer hardware and software applications, network communications and e-mail. These information systems may be owned and maintained by us, our outsource providers or third parties such as vendors and contractors. These information systems are subject to attacks, failures, and access denials from a number of potential sources including viruses, destructive or inadequate code, power failures, and physical damage to computers, hard drives, communication lines and networking equipment. To the extent that these information systems are under our control, we have implemented security procedures, such as virus protection software and emergency recovery processes, to mitigate the outlined risks. However, security procedures for information systems cannot be guaranteed to be failsafe and our inability to use or access these information systems at critical points in time, or unauthorized releases of confidential information, could unfavorably impact the timely and efficient operation of our business.

Confidential information stored on these information systems could also be compromised. If a third party gains unauthorized access to our data, including any information regarding our customers, such security breach could expose us to a risk of loss of this information, loss of business, litigation and possible liability. These security measures may be breached as a result of third-party action, including intentional misconduct by computer hackers, employee error, malfeasance or otherwise. Additionally, third parties may attempt to fraudulently induce employees or customers into disclosing sensitive information such as user names, passwords or other information in order to gain access to our customers' data or our data, including our intellectual property and other confidential business information, or our information technology systems. Because the techniques used to obtain unauthorized access, or to sabotage systems, change frequently and generally are not recognized until launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. Any security breach could result in a loss of confidence by our customers, damage our reputation, disrupt our business, lead to legal liability and negatively impact our future sales.

Our intangible assets may become impaired.

As of September 30, 3014, we had $109.5 million of goodwill and $59.6 million in net intangible assets as a result of our acquisitions. We periodically review our goodwill and the estimated useful lives of our identifiable intangible assets, taking into consideration any events or circumstances that might result in either a diminished fair value, or for intangible assets, a revised useful life. These events and circumstances include significant changes in the business climate, legal factors, operating performance indicators, advances in technology and competition. Any impairment or revised useful life could have a material and adverse effect on our financial position and results of operations, and could harm the trading price of our common stock.

Changes in tax rates or tax regulation could affect results of operations.

As a global company, we are subject to taxation in the United States and various other countries. Significant judgment is required to determine and estimate worldwide tax liabilities. Our future annual and quarterly effective tax rates could be affected by numerous factors, including changes in the: applicable tax laws; composition of pre-tax income in countries with differing tax rates; and/or valuation of our deferred tax assets and liabilities. In addition, we are subject to regular examination by the Internal Revenue Service and state, local and foreign tax authorities. We regularly assess the likelihood of favorable or unfavorable outcomes resulting from these examinations to determine the adequacy of our provision for income taxes. Although we believe our tax estimates are reasonable, there can be no assurance that any final determination will not be materially different from the treatment reflected in our historical income tax provisions and accruals, which could materially and adversely affect our financial condition and results of operations.

We are subject to numerous governmental regulations.

We are subject to federal, state, local and foreign regulations, including environmental regulations and regulations relating to the design and operation of our products and control systems. We might incur significant costs as we seek to ensure that our products meet safety and emissions standards, many of which vary across the states and countries in which our products are used. In the past, we have invested significant resources to redesign our products to comply with these directives. Compliance with future regulations, directives, and standards could require us to modify or redesign some products, make capital expenditures, or incur substantial costs. If we do not comply with current or future regulations, directives, and standards:

• | we could be subject to fines; |

• | our production or shipments could be suspended; and |

• | we could be prohibited from offering particular products in specified markets. |

Any of these events could materially and adversely affect our business, financial condition and results of operations.

13

New regulations and customer demands related to conflict minerals may adversely affect us.

The Dodd-Frank Wall Street Reform and Consumer Protection Act imposes new disclosure requirements regarding the use in our products of “conflict minerals” mined from the Democratic Republic of Congo and adjoining countries, whether or not the components of our products are manufactured by us or third parties. This new requirement could affect the pricing, sourcing and availability of minerals used in the manufacture of components we use in our products. In addition, there are additional costs associated with complying with the disclosure requirements and customer requests, such as costs related to our due diligence to determine the source of any conflict minerals used in our products. We may face difficulties in satisfying customers who may require that all of the components of our products are certified as conflict mineral free and/or free of numerous other hazardous materials.

Unfavorable currency exchange rate fluctuations may lead to lower operating margins, or may cause us to raise prices, which could result in reduced sales.

Currency exchange rate fluctuations could have an adverse effect on our sales and results of operations and we could experience losses with respect to forward exchange contracts into which we may enter. Unfavorable currency fluctuations could require us to increase prices to foreign customers, which could result in lower net sales by us to such customers. Alternatively, if we do not adjust the prices for our products in response to unfavorable currency fluctuations, our results of operations could be materially and adversely affected. In addition, most sales made by our foreign subsidiaries are denominated in the currency of the country in which these products are sold and the currency they receive in payment for such sales could be less valuable as compared to the U.S. dollar at the time of receipt as a result of exchange rate fluctuations. From time to time, we enter into forward exchange contracts to reduce currency exposure. However, we cannot be certain that our efforts will be adequate to protect us against significant currency fluctuations or that such efforts will not expose us to additional exchange rate risks, which could materially and adversely affect our results of operations.

Risks Relating to Our Customers

Because we rely on a limited number of customers for a large portion of our revenue, the loss of one or more of these customers could materially harm our business.

We receive a significant portion of our revenue in each fiscal period from a relatively limited number of customers, and that trend is likely to continue. Sales to our ten largest customers accounted for approximately 37%, 40% and 45% of our total revenue in the fiscal years ended September 30, 2014, 2013 and 2012, respectively. The loss of one or more of these major customers, a significant decrease in orders from one of these customers, or the inability of one or more customers to make payments to us when they are due could materially affect our revenue, business and reputation. In addition, there has been and may continue to be significant consolidation among some of our largest OEM customers, which could lead to increased pressure to reduce the price of our products and/or decreased market share of our products with the combined companies.

Because of the lengthy sales cycles of many of our products, we may incur significant expenses before we generate any revenue related to those products.

Our customers may need several months to test and evaluate our products. This increases the possibility that a customer may decide to cancel an order or change its plans, which could reduce or eliminate our sales to that customer. The impact of this risk can be magnified during the periods in which we introduce a number of new products, as has been the case in recent years. As a result of this lengthy sales cycle, we may incur significant research and development expenses, and selling, general and administrative expenses before we generate the related revenue for these products, and we may never generate the anticipated revenue if our customer cancels an order or changes its plans.

In addition, many of our products will not be sold directly to the end-user but will be components of other products manufactured by OEMs. As a result, we rely on OEMs to select our products from among alternative offerings to be incorporated into their equipment at the design stage; so-called design-ins. The OEMs' decisions often precede the generation of volume sales, if any, by a year or more. Moreover, if we are unable to achieve these design-ins from an OEM, we would have difficulty selling our products to that OEM because changing suppliers after design-ins involves significant cost, time, effort and risk on the part of that OEM.

Customers generally do not make long term commitments to purchase our products and our customers may cease purchasing our products at any time.

Sales of our products are often made pursuant to individual purchase orders and not under long-term commitments and contracts. Our customers frequently do not provide any assurance of minimum or future sales and are not prohibited from purchasing products from our competitors at any time. Accordingly, we are exposed to competitive pricing pressures on each order. Our customers also engage in the practice of purchasing products from more than one manufacturer to avoid dependence on sole-source suppliers for certain of their needs. The existence of these practices makes it more difficult for us to increase price, gain new customers and win repeat business from existing customers.

14

We may face claims for liability related to damages of customer materials attributed to the failure of our products, exposing us to significant financial or reputational harm.

Our automation products for the semiconductor manufacturing market are used in the handling and movement of silicon wafers at various points in the production process, and our automated cold storage systems for the life sciences market are used in the handling, movement and storage of biological and chemical samples. In either case, damage to our customers' materials may be attributed to a failure of our products which could lead to claims for damages made by our customers and could also harm our relationship with our customers and damage our reputation in each of these industries, resulting in material harm to our business.

Risks Relating to Owning Our Securities

Our stock price is volatile.

The market price of our common stock has fluctuated widely. From the beginning of fiscal year 2013 through the end of fiscal year 2014, our stock price fluctuated between a high of $11.64 per share and a low of $7.00 per share. Consequently, the current market price of our common stock may not be indicative of future market prices, and we may be unable to sustain or increase the value of an investment in our common stock. Factors affecting our stock price may include:

• | variations in operating results from quarter to quarter; |

• | changes in earnings estimates by analysts or our failure to meet analysts' expectations; |

• | changes in the market price per share of our public company customers; |

• | market conditions in the semiconductor and other industries into which we sell products and services; |

• | global economic conditions; |

• | political changes, hostilities or natural disasters such as hurricanes and floods; |

• | low trading volume of our common stock; and |

• | the number of firms making a market in our common stock. |

In addition, the stock market has in the past experienced significant price and volume fluctuations. These fluctuations have particularly affected the market prices of the securities of high technology companies like ours. These market fluctuations could adversely affect the market price of our common stock.

We may not pay dividends on our common stock.

Holders of our common stock are only entitled to receive dividends when and if they are declared by our Board of Directors. Although we have declared cash dividends on our common stock for the past few years, we are not required to do so and may reduce or eliminate our cash dividends in the future. This could adversely affect the market price of our common stock.

Provisions in our charter documents and, Delaware law may delay or prevent an acquisition of us, which could decrease the value of your shares.

Our restated certificate of incorporation and by-laws and Delaware law contain provisions that could make it harder for a third party to acquire us without the consent of our Board of Directors. These provisions include limitations on actions by our stockholders by written consent, the inability of stockholders to call special meetings and the potential for super majority votes of our stockholders in certain circumstances. In addition, our Board of Directors has the right to issue preferred stock without stockholder approval, which could be used to dilute the stock ownership of a potential hostile acquirer.

Our restated certificate of incorporation makes us subject to the anti-takeover provisions of Section 203 of the Delaware General Corporation Law. In general, Section 203 prohibits publicly held Delaware corporations to which it applies from engaging in a “business combination” with an “interested stockholder” for a period of three years after the date of the transaction in which the person became an interested stockholder, unless the business combination is approved in a prescribed manner. This provision could discourage others from bidding for our shares of common stock and could, as a result, reduce the likelihood of an increase in the price of our common stock that would otherwise occur if a bidder sought to buy our common stock.

Delaware law also imposes restrictions on mergers and other business combinations between us and any holder of 15% or more of our outstanding common stock. Although we believe these provisions provide for an opportunity to receive a higher bid by requiring potential acquirers to negotiate with our Board of Directors, these provisions apply even if the offer may be considered beneficial by stockholders. If a change of control or change in management is delayed or prevented, the market price of our common stock could decline.

15

Our certificate of incorporation authorizes the issuance of shares of blank check preferred stock.

Our certificate of incorporation provides that our Board of Directors is authorized to issue from time to time, without further stockholder approval, up to 1,000,000 shares of preferred stock in one or more series and to fix and designate the rights, preferences, privileges and restrictions of the preferred stock, including dividend rights, conversion rights, voting rights, redemption rights and terms of redemption and liquidation preferences. Such shares of preferred stock could have preferences over our common stock with respect to dividends and liquidation rights. Our issuance of preferred stock may have the effect of delaying or preventing a change in control. Our issuance of preferred stock could decrease the amount of earnings and assets available for distribution to the holders of common stock or could adversely affect the rights and powers, including voting rights, of the holders of common stock. The issuance of preferred stock could have the effect of decreasing the market price of our common stock.

Item 1B. | Unresolved Staff Comments |

None.

Item 2. | Properties |

Our corporate headquarters and primary manufacturing/research and development facilities are currently located in three buildings in Chelmsford, Massachusetts, where we own two buildings and are committed to purchase the third under a long term purchase option. In summary, we maintain the following active principal facilities:

Location | Functions | Square Footage (Approx.) | Ownership Status/Lease Expiration | ||||

Chelmsford, Massachusetts | Corporate headquarters, training, manufacturing, R&D and sales & support | 201,000 | Owned | ||||

Chelmsford, Massachusetts | Manufacturing | 97,000 | Committed to purchase | ||||

Poway, California | Manufacturing, R&D and sales & support | 67,600 | July 2015 | ||||

Fremont, California | R&D and sales & support | 44,900 | August 2018 | ||||

Manchester, UK | Manufacturing, R&D and sales & support | 42,000 | December 2019 | ||||

Yongin-City, South Korea | Manufacturing, R&D and sales & support | 34,100 | August 2019 | ||||

Jena, Germany | Manufacturing, R&D and sales & support | 30,100 | January 2017 | ||||

Chu Bei City, Taiwan | Sales & support | 28,600 | June 2016 | ||||

Our Brooks Product Solutions segment utilizes the facilities in Massachusetts, Fremont, California, South Korea and Germany. Our Brooks Global Services segment utilizes the facilities in Massachusetts, South Korea, Germany and Taiwan. Our Brooks Life Science Systems segment utilizes the facilities in Poway, California and the UK as well as an additional facility in Spokane, Washington.

We maintain additional sales and support and training offices in Texas and overseas in Europe (France, Germany and Switzerland), as well as in Asia (Japan, China, Singapore and Taiwan) and the Middle East (Israel).

We utilize a third party to manage our manufacturing operation in Mexico. As part of our arrangement with this third party, we guarantee a lease for a 56,100 square foot manufacturing facility. The remaining payments under this lease, which expires in 2018, are approximately $1.4 million.

Item 3. | Legal Proceedings |

We are subject to various legal proceedings, both asserted and unasserted, that arise in the ordinary course of business. We cannot predict the ultimate outcome of such legal proceedings or in certain instances provide reasonable ranges of potential losses. However, as of the date of this report, we believe that none of these claims will have a material adverse effect on our consolidated financial condition or results of operations. In the event of unexpected subsequent developments and given the inherent unpredictability of these legal proceedings, there can be no assurance that our assessment of any claim will reflect the ultimate outcome and an adverse outcome in certain matters could, from time-to-time, have a material adverse effect on our consolidated financial condition or results of operations in particular quarterly or annual periods.

16

Item 4. | Mine Safety Disclosures |

Not applicable.

PART II

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is traded on the NASDAQ Stock Market LLC under the symbol “BRKS.” The following table sets forth the high and low intraday sales prices per share of our common stock as reported by the NASDAQ Stock Market LLC and the cash dividends declared per common share for the periods indicated:

Market Price | Dividends Declared | ||||||||||

High | Low | ||||||||||

Fiscal year ended September 30, 2014 | |||||||||||

First quarter | $ | 10.75 | $ | 9.01 | $ | 0.08 | |||||

Second quarter | 11.64 | 9.43 | 0.08 | ||||||||

Third quarter | 11.50 | 8.75 | 0.08 | ||||||||

Fourth quarter | 11.53 | 9.86 | 0.10 | ||||||||

Fiscal year ended September 30, 2013 | |||||||||||

First quarter | $ | 8.24 | $ | 7.00 | $ | 0.08 | |||||

Second quarter | 10.50 | 8.23 | 0.08 | ||||||||

Third quarter | 10.97 | 8.78 | 0.08 | ||||||||

Fourth quarter | 10.56 | 8.74 | 0.08 | ||||||||

Number of Holders

As of November 5, 2014, there were 672 holders of record of our common stock.

Dividend Policy

Dividends are declared at the discretion of our Board of Directors and depend on actual cash from operations, our financial condition and capital requirements and any other factors our Board of Directors may consider relevant. Future dividend declarations, as well as the record and payment dates for such dividends, will be determined by our Board of Directors on a quarterly basis.

On November 5, 2014, our Board of Directors approved a cash dividend of $0.10 per share payable on December 26, 2014 to common stockholders of record on December 5, 2014.

17

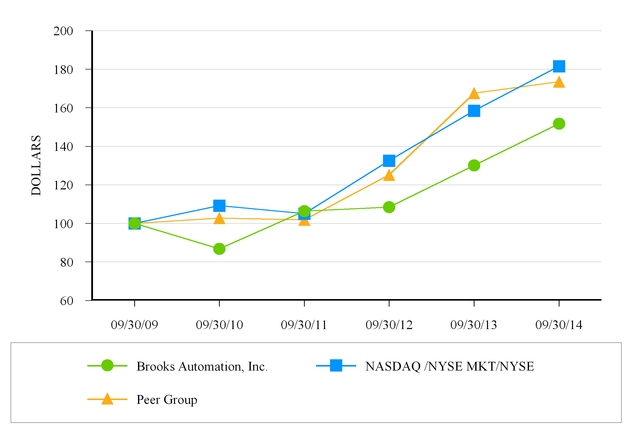

Comparative Stock Performance