Attached files

| file | filename |

|---|---|

| 8-K - KAMAN CORPORATION FORM 8-K DATED AUGUST 13, 2014 - KAMAN Corp | form8-k.htm |

1

Investor Presentation

August 13, 2014

2

Forward Looking Statements

FORWARD-LOOKING STATEMENTS

This presentation contains "forward-looking statements" within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995.

Forward-looking statements also may be included in other publicly available documents issued by the company and in oral statements made by our officers and

representatives from time to time. These forward-looking statements are intended to provide management's current expectations or plans for our future operating and

financial performance, based on assumptions currently believed to be valid. They can be identified by the use of words such as "anticipate," "intend," "plan," "goal,"

"seek," "believe," "project," "estimate," "expect," "strategy," "future," "likely," "may," "should," "would," "could," "will" and other words of similar meaning in connection with

a discussion of future operating or financial performance. Examples of forward looking statements include, among others, statements relating to future sales, earnings,

cash flows, results of operations, uses of cash and other measures of financial performance.

Forward-looking statements also may be included in other publicly available documents issued by the company and in oral statements made by our officers and

representatives from time to time. These forward-looking statements are intended to provide management's current expectations or plans for our future operating and

financial performance, based on assumptions currently believed to be valid. They can be identified by the use of words such as "anticipate," "intend," "plan," "goal,"

"seek," "believe," "project," "estimate," "expect," "strategy," "future," "likely," "may," "should," "would," "could," "will" and other words of similar meaning in connection with

a discussion of future operating or financial performance. Examples of forward looking statements include, among others, statements relating to future sales, earnings,

cash flows, results of operations, uses of cash and other measures of financial performance.

Because forward-looking statements relate to the future, they are subject to inherent risks, uncertainties and other factors that may cause the company's actual results

and financial condition to differ materially from those expressed or implied in the forward-looking statements. Such risks, uncertainties and other factors include, among

others: (i) changes in domestic and foreign economic and competitive conditions in markets served by the company, particularly the defense, commercial aviation and

industrial production markets; (ii) changes in government and customer priorities and requirements (including cost-cutting initiatives, government and customer shut-

downs, the potential deferral of awards, terminations or reductions of expenditures to respond to the priorities of Congress and the Administration, or budgetary cuts

resulting from Congressional actions or automatic sequestration); (iii) changes in geopolitical conditions in countries where the company does or intends to do business;

(iv) the successful conclusion of competitions for government programs and thereafter contract negotiations with government authorities, both foreign and domestic; (v)

the existence of standard government contract provisions permitting renegotiation of terms and termination for the convenience of the government; (vi) the conclusion to

government inquiries or investigations regarding government programs, including the resolution of the Wichita subpoena matter; (vii) risks and uncertainties associated

with the successful implementation and ramp up of significant new programs; (viii) potential difficulties associated with variable acceptance test results, given sensitive

production materials and extreme test parameters; (ix) the receipt and successful execution of production orders for the JPF U.S. government contract, including the

exercise of all contract options and receipt of orders from allied militaries, as all have been assumed in connection with goodwill impairment evaluations; (x) the

continued support of the existing K-MAX® helicopter fleet, including sale of existing K-MAX® spare parts inventory; (xi) the accuracy of current cost estimates associated

with environmental remediation activities at the Bloomfield, Moosup and New Hartford, CT facilities and our U.K. facilities; (xii) the profitable integration of acquired

businesses into the company's operations; (xiii) the ability to implement our ERP systems in a cost-effective and efficient manner, limiting disruption to our business, and

to capture their planned benefits while maintaining an adequate internal control environment; (xiv) changes in supplier sales or vendor incentive policies; (xv) the effects

of price increases or decreases; (xvi) the effects of pension regulations, pension plan assumptions, pension plan asset performance and future contributions; (xvii) future

levels of indebtedness and capital expenditures; (xviii) the continued availability of raw materials and other commodities in adequate supplies and the effect of increased

costs for such items; (xix) the effects of currency exchange rates and foreign competition on future operations; (xx) changes in laws and regulations, taxes, interest rates,

inflation rates and general business conditions; (xxi) future repurchases and/or issuances of common stock; and (xxii) other risks and uncertainties set forth herein and in

our 2013 Form 10-K.

and financial condition to differ materially from those expressed or implied in the forward-looking statements. Such risks, uncertainties and other factors include, among

others: (i) changes in domestic and foreign economic and competitive conditions in markets served by the company, particularly the defense, commercial aviation and

industrial production markets; (ii) changes in government and customer priorities and requirements (including cost-cutting initiatives, government and customer shut-

downs, the potential deferral of awards, terminations or reductions of expenditures to respond to the priorities of Congress and the Administration, or budgetary cuts

resulting from Congressional actions or automatic sequestration); (iii) changes in geopolitical conditions in countries where the company does or intends to do business;

(iv) the successful conclusion of competitions for government programs and thereafter contract negotiations with government authorities, both foreign and domestic; (v)

the existence of standard government contract provisions permitting renegotiation of terms and termination for the convenience of the government; (vi) the conclusion to

government inquiries or investigations regarding government programs, including the resolution of the Wichita subpoena matter; (vii) risks and uncertainties associated

with the successful implementation and ramp up of significant new programs; (viii) potential difficulties associated with variable acceptance test results, given sensitive

production materials and extreme test parameters; (ix) the receipt and successful execution of production orders for the JPF U.S. government contract, including the

exercise of all contract options and receipt of orders from allied militaries, as all have been assumed in connection with goodwill impairment evaluations; (x) the

continued support of the existing K-MAX® helicopter fleet, including sale of existing K-MAX® spare parts inventory; (xi) the accuracy of current cost estimates associated

with environmental remediation activities at the Bloomfield, Moosup and New Hartford, CT facilities and our U.K. facilities; (xii) the profitable integration of acquired

businesses into the company's operations; (xiii) the ability to implement our ERP systems in a cost-effective and efficient manner, limiting disruption to our business, and

to capture their planned benefits while maintaining an adequate internal control environment; (xiv) changes in supplier sales or vendor incentive policies; (xv) the effects

of price increases or decreases; (xvi) the effects of pension regulations, pension plan assumptions, pension plan asset performance and future contributions; (xvii) future

levels of indebtedness and capital expenditures; (xviii) the continued availability of raw materials and other commodities in adequate supplies and the effect of increased

costs for such items; (xix) the effects of currency exchange rates and foreign competition on future operations; (xx) changes in laws and regulations, taxes, interest rates,

inflation rates and general business conditions; (xxi) future repurchases and/or issuances of common stock; and (xxii) other risks and uncertainties set forth herein and in

our 2013 Form 10-K.

Any forward-looking information provided in this presentation should be considered with these factors in mind. We assume no obligation to update any forward-looking

statements contained in this presentation.

statements contained in this presentation.

Contact: Eric Remington

V.P., Investor Relations

(860) 243-6334

Eric.Remington@kaman.com

3

Non-GAAP Figures

Certain measures presented in this presentation are “Non-GAAP”

items. These figures are denoted with an asterisk (*).

items. These figures are denoted with an asterisk (*).

Reconciliations from GAAP measures to the Non-GAAP measures are

presented in Appendix I to this presentation and our recent earnings

releases filed with the U.S. Securities and Exchange Commission.

presented in Appendix I to this presentation and our recent earnings

releases filed with the U.S. Securities and Exchange Commission.

4

Distribution

Kaman Corporation - 2013 Sales Overview

Distribution

Aerospace

$1.7B Revenues

Aerospace

5

Kaman Corporation Overview

|

v

|

AEROSPACE

|

DISTRIBUTION

|

||

|

Integrated

Aerosystems

|

Specialty Bearings &

Engineered Products |

Fuzing & Precision

Products |

|

|

|

|

|

|

|

|

|

|

• Engineering design and

testing • Tooling design & manufacture

• Advanced machining and

composite aerostructure manufacturing • Complex assembly

• Helicopter MRO and support

|

• Self-lube airframe

bearings • Traditional airframe

bearings • Flexible drive systems

|

• Bomb safe and arm

fuzing devices • Missile safe and arm

fuzing devices • High precision measuring

systems • Memory products

|

• Bearing and power

transmission products • Fluid power products

• Automation, control and

energy products • Systems and services

across all product groups |

|

|

• Global commercial and defense OEM’s

• Super Tier I’s to subcontract manufacturers

• Aircraft operators and MRO

• Specialized aerospace distributors

|

• U.S. and allied militaries

• Weapon system OEMs

|

• Virtually every industry in

North America |

|

|

|

• “One Kaman” combines design and build capabilities

to provide customers with a global integrated solution • Bearing product lines strong commercial customer

base expected to provide growth from new program wins and increasing build rates |

• Exclusivity and

significant backlog provide a stable revenue base |

• Offers customers single-

source responsibility for a comprehensive portfolio of products |

|

Business

Dynamic

Customer

Product

6

Business Strengths

• Secular trends helping to drive significant long-term growth opportunities

in both Aerospace and Distribution segments

in both Aerospace and Distribution segments

• Improved balance across the Aerospace segment between commercial

and defense programs

and defense programs

– Increasing content of bearing products on new platforms

– Higher commercial build rates driving bearing and aerostructure sales

– New program ramp ups and wins provide offset to lower defense

spending

spending

• Distribution business gaining scale and capabilities via acquisitions and

enhancing complementary product platforms

enhancing complementary product platforms

• Investing in new product development and applications, acquisitions and

technology for long-term growth

technology for long-term growth

• Strong balance sheet to drive growth and strategic initiatives

• Experienced management team

7

2013 Sales: $614 million

Aerospace

37%

8

Aerospace Business Drivers

• Kaman is well positioned to further penetrate Commercial OEM’s and

Super Tier 1’s

Super Tier 1’s

– Proactive “One Kaman” business development efforts have increased

bid activity

bid activity

– Proven capability to provide flexible low cost solutions

– Broadening geographic footprint to better serve customers and to

provide lower cost manufacturing alternatives

provide lower cost manufacturing alternatives

• Increasing shared services across the organization and the introduction of

a common ERP system are expected to drive cost synergies

a common ERP system are expected to drive cost synergies

• Increasing production levels at Boeing and Airbus provide support for

near term specialty bearing & aerostructures growth

near term specialty bearing & aerostructures growth

• Defense platforms provide exposure to key vertical lift and reset programs

• Sole source long-term contractual position and solid backlog on key

fuzing program provide stable revenue base

fuzing program provide stable revenue base

9

Aerospace Strategy

10

Aerospace Sales Mix 2009 vs. 2013

2009

Sales = $501 million

2013

Sales = $614 million

Defense Aerospace

Fuzing

Commercial Aerospace

Significantly higher relative growth rates in our commercial aerospace portfolio have

resulted in improved balance. Commercial sales increased by 46% from 2009 to 2013.

resulted in improved balance. Commercial sales increased by 46% from 2009 to 2013.

11

Fixed trailing edge

Access doors

Top covers

Nose landing gear

Horizontal

stabilizer

stabilizer

Main landing gear

Flaps

Rudder

Door assemblies

Engine/thrust reverser

Aircraft Programs/Capabilities

Flight controls

Doors

Fixed leading edge

Red denotes bearing products

12

Manufacture of cockpit

Manufacture and assembly

of tail rotor pylon

of tail rotor pylon

Manufacture

subassembly

subassembly

Blade manufacture,

repair and overhaul

repair and overhaul

Driveline couplings

Bushings

Flight control bearings

Aircraft Programs/Capabilities

Red denotes bearing products

13

Market leading self lube airframe bearing product lines

• Products on virtually every aircraft

manufactured today - growing installed base

manufactured today - growing installed base

• Approximately 75% of sales are for

commercial applications

commercial applications

• Proprietary technology:

– KAron® bearing liner system

– KAflex® and Tufflex® flexible couplings

• Approximately 95% of sales are custom

engineered for the application

engineered for the application

• Operational excellence through lean

manufacturing

manufacturing

• World class engineers and material scientists

developing new products and applications

developing new products and applications

14

Fuzing Products

HARPOON

MAVERICK

FMU-139

TOMAHAWK

JPF

STANDARD

MISSILE

MISSILE

SLAM-ER

SLAM-ER

AMRAAM

TOMAHAWK

STANDARD

MISSILE

MISSILE

AGM-65M

AMRAAM

KPP Fuzes are on a majority of major U.S. weapons systems

15

• USAF bomb fuze of choice

• USAF inventory levels are less than half

desired quantity

desired quantity

• Recently awarded USAF contract extends

sole source position into 2017

sole source position into 2017

• Backlog of $108 million as of 6/27/2014

• Two orders totaling $14 million received in

July

July

• 27 foreign customers

• System reliability exceeds 98% and

operational reliability is greater than 99%

operational reliability is greater than 99%

Bomb Compatibility

- JDAM

- Paveway II and III

- GBU-10, 12, 16, 24, 27, 28, 31, 32,

38, 54

38, 54

- BLU-109, 110, 111, 113, 117, 121,

122, 126

122, 126

- MK82/BSU-49, MK83/BSU-85,

MK84/BSU-50

MK84/BSU-50

JPF Program

16

Driving Growth Through New Programs

New program activity is at unprecedented levels

17

Leveraging Customer Relationships - Bell/Textron Case Study

Continually providing quality value added solutions has led to a growing relationship

that is projected to exceed $40 million in sales annually

|

Early

1980’s

|

Developed a driveshaft for the U.S. Army’s UH-1 helicopter

|

|

|

Mid

1980’s

|

Developed technology to replace driveshaft's across the Bell

fleet of commercial and military aircraft |

|

|

2009

|

Awarded a five year $53M contract to build composite helo.

blade skins and skin core assemblies for eight Bell models |

|

|

2011

|

Awarded a contract with a potential value of more than $200

million to manufacture and assemble cabins for the AH-1Z - the largest structure ever outsourced by Bell

|

|

|

2013

|

Delivered significant structural components for the recently

introduced Textron AirLand Scorpion prototype aircraft |

|

18

Recent Global Aerospace Growth Investments

1. Lancashire, UK - new tooling facility

2. Höchstadt, Germany - new bearing manufacturing facility

3. Goa, India - composites manufacturing joint venture

19

Aerospace - Impact of Defense Spending

• We believe the diversity of our defense programs positions us well

to weather potential budget cuts

to weather potential budget cuts

– Joint Programmable Fuze - under contract into 2016, foreign

demand, continued sole source

demand, continued sole source

– A-10 re-wing program for Boeing - under contract through

shipset 173, 72% of the total program

shipset 173, 72% of the total program

– AH-1Z integrated fuselage for Bell/USMC - new business

• Improved commercial balance provides more stable Aerospace

revenue base

revenue base

20

New Zealand SH-2G(I)

• Entered into a $120 million

contract with the New Zealand

Ministry of Defence for the sale

of ten Kaman SH-2G(I) aircraft

contract with the New Zealand

Ministry of Defence for the sale

of ten Kaman SH-2G(I) aircraft

• Work under this program began

in 2013 and is on schedule

in 2013 and is on schedule

• Program is expected to

generate $60-65 million in cash

generate $60-65 million in cash

21

Unmanned K-MAX®

• Kaman/Lockheed teamed to

provide an unmanned military

version of the K-MAX helicopter

provide an unmanned military

version of the K-MAX helicopter

• K-MAX aircraft performed

unmanned cargo resupply missions

in Afghanistan from 2011 to 2014

and completed more than 1,950

missions and delivered more than

4.5 million pounds of cargo

unmanned cargo resupply missions

in Afghanistan from 2011 to 2014

and completed more than 1,950

missions and delivered more than

4.5 million pounds of cargo

• “The K-MAX and the team

operating the aircraft excelled

beyond anything I thought

possible.” - Captain Patrick Smith,

USN Program Manager

operating the aircraft excelled

beyond anything I thought

possible.” - Captain Patrick Smith,

USN Program Manager

Photograph by Corporal Lisa Tourtelot, United States Marine Corps.

22

Aerospace - Key Operational Objectives

23

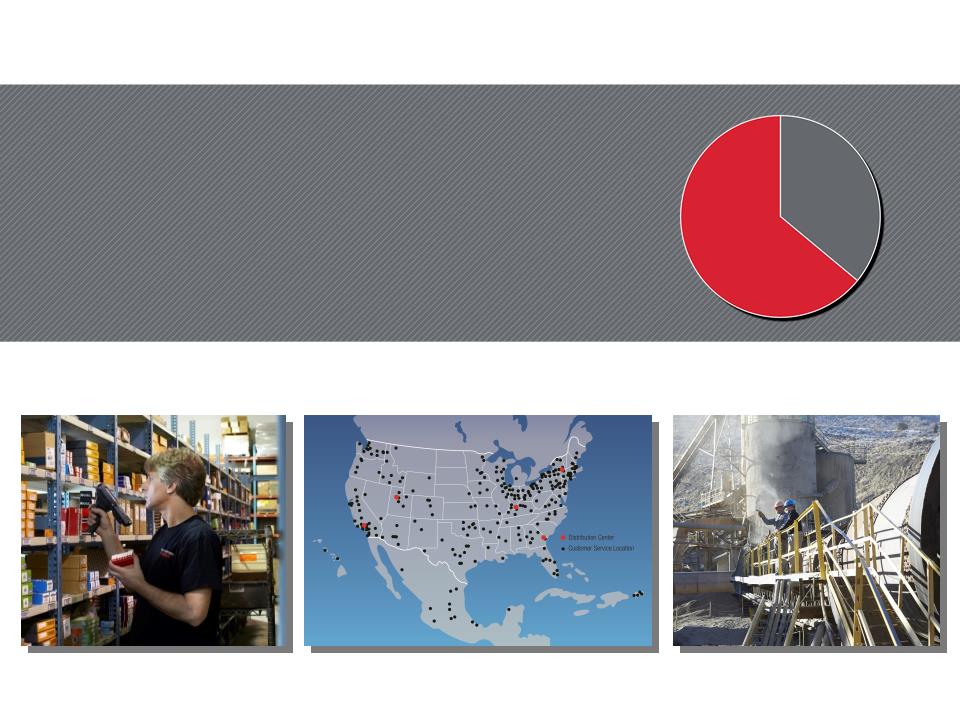

Distribution

2013 Sales: $1.07 Billion

63%

24

Distribution Overview

Major product categories

•Bearings

•Power Transmission

•Fluid Power

•Motion Control

•Automation

•Material Handling

•Electrical control and power

distribution

distribution

25

Distribution Business Drivers

• Industrial customers increasing use of national contracts to

consolidate supply of MRO goods and driving compliance with

suppliers

consolidate supply of MRO goods and driving compliance with

suppliers

• Increased residential construction expected to drive demand across

numerous industries served by Kaman

numerous industries served by Kaman

• Hydraulic, automation and motion control products add content to

MRO customers and meet trend of customers transitioning to higher-

technology applications

MRO customers and meet trend of customers transitioning to higher-

technology applications

• Unique products to service municipalities in water, wastewater, and

supporting control system infrastructure

supporting control system infrastructure

• OEMs looking for more value-add and integration services

26

Distribution Strategy

27

Improved Diversification of Distribution Served End Markets

Bearings and Mechanical Power Transmission

Automation, Control and Energy

Fluid Power

up 40%

up 203%

up 97%

28

Distribution - Major Product Platforms

|

PRODUCT

PLATFORM |

BEARINGS &

MECHANICAL POWER

TRANSMISSION (BPT)

|

FLUID POWER

|

AUTOMATION, CONTROL &

ENERGY (ACE) |

|

% of 2013

Sales |

61%

|

14%

|

25%

|

|

Market Size

|

$12.5 Billion

|

$7.2 Billion

|

$15.0 Billion

|

|

Acquisitions

since 2008 |

• Industrial Supply Corp

• Allied Bearings Supply

• Plains Bearing

• Fawick de Mexico

• Florida Bearings Inc.

• Ohio Gear and Transmission

|

• INRUMEC

• Catching

• Northwest Hose & Fittings

• Westerns Fluid Components

• B. W. Rogers

|

• Zeller

• Minarik

• Target Electronic Supply

• B. W. Rogers

|

|

Major

Suppliers |

|

|

|

29

Executing Strategy and Building Network

30

Distribution - ERP Technology Investments

• Consolidate 12 disparate business systems and numerous sub-systems

to a standard state-of-the-art enterprise-wide business system

to a standard state-of-the-art enterprise-wide business system

• Infor’s Distribution SX.e is the leading distribution ERP solution

Increased customer satisfaction

CRM will provide critical info to sales teams driving higher sales volume

Reduced transaction and response times will drive productivity gains

Ability to consolidate and analyze purchasing requirements will lower

procurement costs and increase profitability

procurement costs and increase profitability

BENEFITS

31

B.W. Rogers Acquisition - Overview

32

B.W. Rogers - Background

• Tri-motion Parker distributor

• Acquisition creates contiguous

Parker territory from

Pennsylvania to Chicago

Parker territory from

Pennsylvania to Chicago

• 21 locations across seven

states including 20 authorized

Parker locations and 12

ParkerStores

states including 20 authorized

Parker locations and 12

ParkerStores

• Approximately 240 employees

33

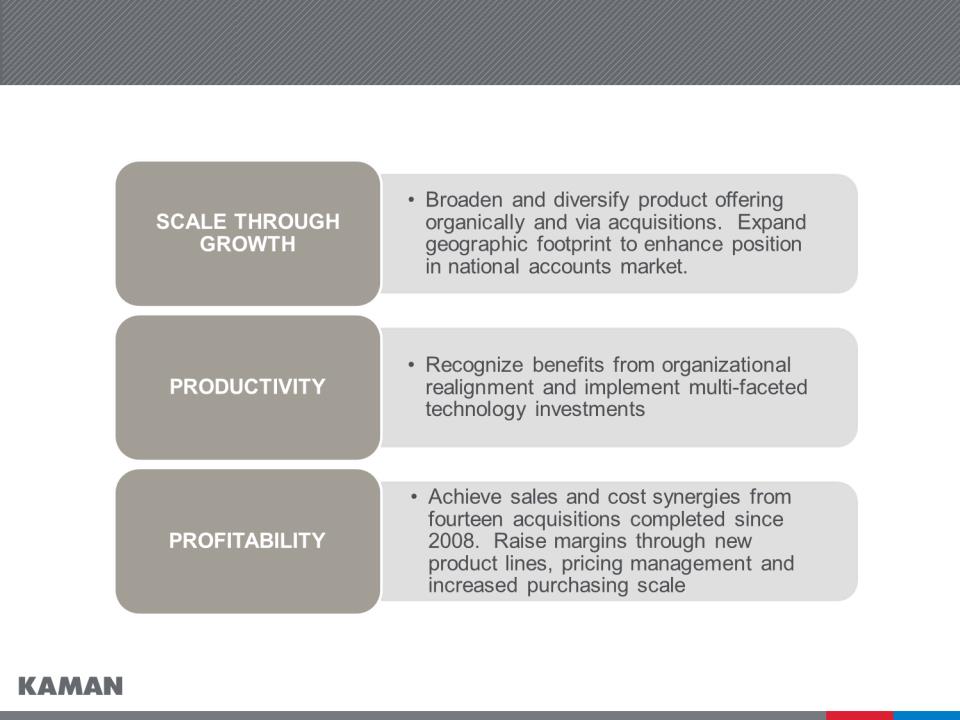

Distribution - Key Operational Objectives

34

Kaman Investment Merits

Focus

Market

Position

Position

Financial

Profile

Acquisition

Strategy

Strategy

Management

Team

Team

Leader in Both Business Segments

Earnings Growth, Cash Flow Generation,

Strengthening Market Position

Strengthening Market Position

Strong Liquidity and Conservative Practices

Disciplined and Focused

Proven track record

35

Financial Information

36

Financial Highlights - Q2 2014

37

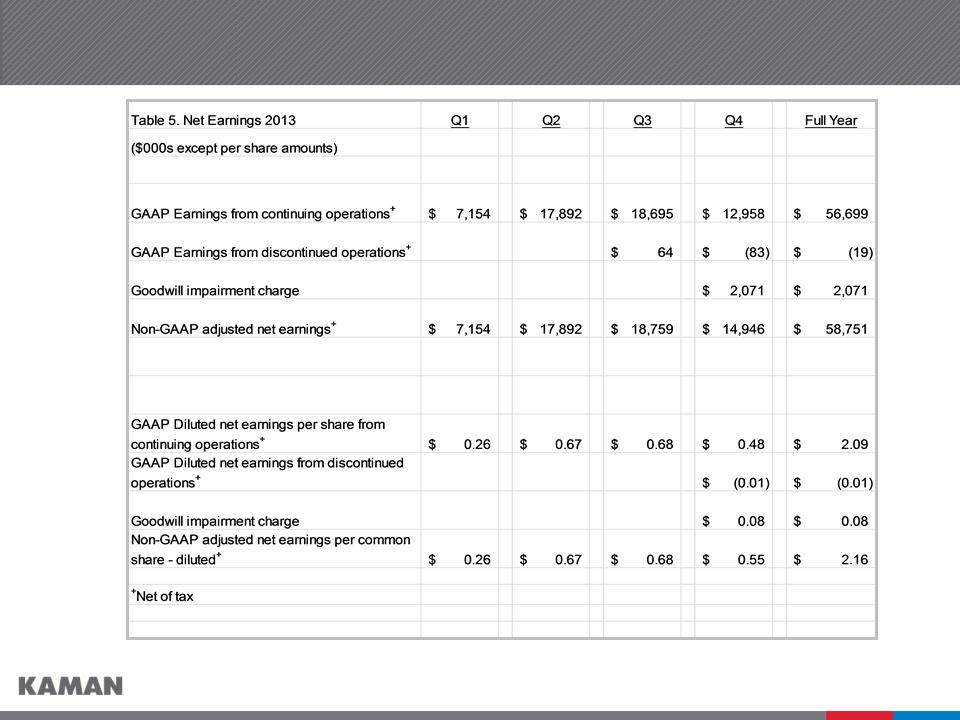

Financial Highlights - Full Year 2013

38

Balance Sheet, Capital Factors, and Cash Flow Items

|

(In Millions)

|

As of 6/27/14

|

As of 12/31/13

|

As of 12/31/12

|

|

Cash and Cash Equivalents

|

$ 11.7

|

$ 10.4

|

$ 16.6

|

|

Notes Payable and Long-term Debt

|

$ 362.9

|

$ 275.2

|

$ 259.6

|

|

Shareholders’ Equity

|

$ 540.6

|

$ 511.3

|

$ 420.2

|

|

Debt as % of Total Capitalization

|

40.2%

|

35.0%

|

38.2%

|

|

Capital Expendituresa

|

$ 18.1

|

$ 40.9

|

$ 32.6

|

|

Depreciation & Amortizationa

|

$ 17.1

|

$ 31.9

|

$ 28.4

|

|

Free Cash Flow*a

|

$ 6.3

|

$ 21.6

|

$ 52.0

|

)

(

aYTD 6/27/2014

39

Appendix I

Non-GAAP Reconciliations

Non-GAAP Reconciliations

40

Reconciliation of Non-GAAP Financial Information

41

Reconciliation of Non-GAAP Financial Information

42

Reconciliation of Non-GAAP Financial Information

43

Reconciliation of Non-GAAP Financial Information

44

Reconciliation of Non-GAAP Financial Information

45

Reconciliation of Non-GAAP Financial Information

46

Reconciliation of Non-GAAP Financial Information