Attached files

| file | filename |

|---|---|

| 8-K - 8-K - NAUTILUS, INC. | d774080d8k.htm |

| Exhibit 99.1

|

Exhibit 99.1

Marketing Meetings

with Sidoti & Co

AUGUST 13-14, 2014

|

|

Safe Harbor Statement

This presentation includes forward-looking statements (statements which are not historical facts) within the meaning of the Private Securities Litigation Reform Act of 1995, including statements concerning the Company’s prospects, resources, capabilities, current or future financial trends or operating results, demand for the Company’s products, future plans for introduction of new products and the anticipated outcome of new business initiatives, estimates of market size and growth, planned capital expenditures and statements concerning our ability to finance growth plans with cash generated from our operations. Factors that could cause Nautilus, Inc.‘s actual results to differ materially from these forward-looking statements include our ability to acquire inventory from sole source foreign manufacturers at acceptable costs, within timely delivery schedules asnd that meet our quality control standards, availability and price of media time consistent with our cost and audience profile parameters, a decline in consumer spending due to unfavorable economic conditions in one or more of our current or target markets, an adverse change in the availability of credit for our customers who finance their purchases, our ability to pass along vendor raw material price increases and increased shipping costs, our ability to effectively develop, market and sell future products, our ability to protect our intellectual property, and the introduction of competing products. Additional assumptions, risks and uncertainties are described in detail in our registration statements, reports and other filings with the Securities and Exchange Commission, including the “Risk Factors” set forth in our Annual Report on Form 10-K, as supplemented by our quarterly reports on Form 10-Q. Such filings are available on our website or at www.sec.gov. You are cautioned that such statements are not guarantees of future performance and that actual results or developments may differ materially from those set forth in the forward-looking statements. We undertake no obligation to publicly update or revise forward-looking statements to reflect subsequent events or circumstances.

Unless otherwise indicated, all information regarding our operating results pertain to continuing operations.

© Nautilus, Inc. 2014

| 2 |

|

|

|

Presentation Overview

Who We Are: A team focused on providing innovative fitness solutions and superior results

Our Strategies: Strategic Innovation, Operational Excellence, Footprint Expansion

Our Results: Robust top and bottom line growth; Strong Balance Sheet

| 3 |

|

|

|

Who We Are Today

A leading provider of fitness equipment and related products for use in, and around, the home

Growing company which has dramatically improved profitability

Strong portfolio of brands, including #1 in the fitness industry (Bowflex)*

Industry leading capabilities in product quality and innovation

Revenue growth driven through expansion in three key channels: Direct to consumers, large and small Retail accounts, and Royalty revenue through licensing

An organization focused on increasing shareholder value

Our mission is to provide products which allow consumers to achieve their health and fitness goals

| * |

|

Based on 2012 National Consumer Research Study |

| 4 |

|

|

|

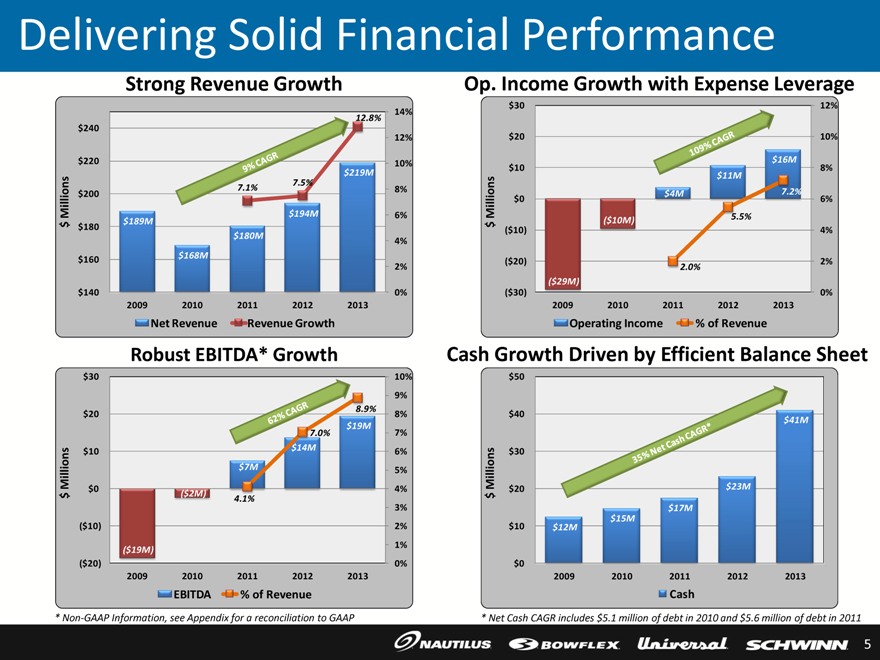

Delivering Solid Financial Performance

Strong Revenue Growth

Op. Income Growth with Expense Leverage

$240

$220

$200

$ Millions

$180

$160

$140

$189M

2009

$168M

7.1%

$180M

7.5%

$194M

12.8%

$219M

14%

12%

10%

8%

6%

4%

2%,9%, CAGR 0% 2009 2010 2011 2012 2013 Net Revenue Revenue Growth

$30 12%

$20 10%

$16M

$10 8%

$11M

$4M 7.2%

$0 6%

$ Millions ($10M) 5.5%

($10) 4%

($20) 2% 109% CAGR

2.0%

($29M)

0% ($30)

2009 2010 2011 2012 2013

operating Income % of Revenue

Robust EBITDA* Growth

Cash Growth Driven by Efficient Balance Sheet

$30

$20

$10

$7M

62% CAGR 8.9% 7.0% $19M< ($19M)

4.1%

$ Million s $0 ($2M)

($10)

($20)

2010

EBITDA % of Revenue

$50

$40

$41M

$30

$ Million $20 $23M

$12M 35% Net Cash CAGR*

$17M

$14M

$15M

$10

$5

$0 $0

2009 2009 2010 2010 2011 2011 2012 2012 2013 2013

Cash Debt

| * |

|

Net Cash CAGR includes $5.1 million of debt in 2010 and $5.6 million of debt in 2011 |

| * |

|

Non-GAAP Information, see Appendix for a reconciliation to GAAP |

| 10% |

|

9% 8% 7% 6% 5% 4% 3% 2% 1% 0% |

| 5 |

|

|

|

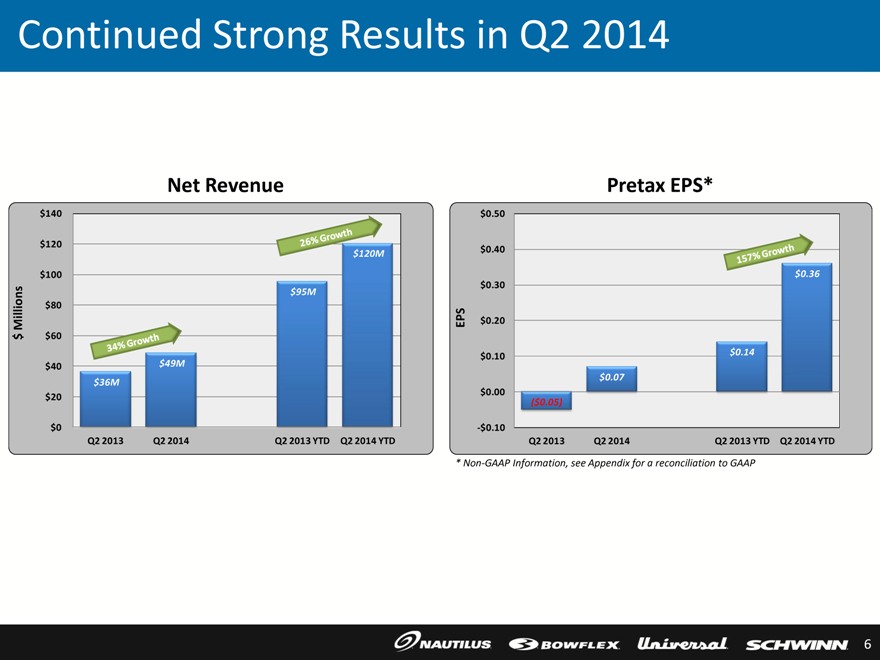

Continued Strong Results in Q2 2014

Net Revenue

$140

$120

$120M

$100

$95M

$80

$ Millions $60

$40 $49M

$36M

$20

$0

Q2 2013 Q2 2014 Q2 2013 YTD Q2 2014 YTD

Pretax EPS*

$ 0.50

$ 0.40

$ 0.36

$ 0.30

$ 0.10 $ 0.14

$ 0.07

$ 0.00

($ 0.05)

-$ 0.10

26% Growth 34% Growth 157% Growth $0.20 EPS

Q2 2013 Q2 2014 Q2 2013 YTD Q2 2014 YTD

* Non-GAAP Information, see Appendix for a reconciliation to GAAP

| 6 |

|

|

|

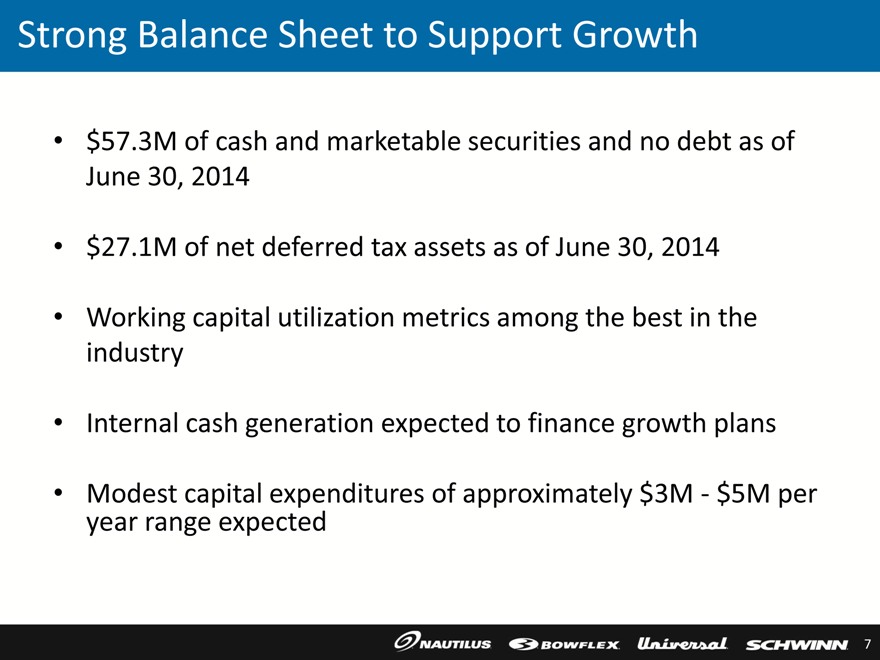

Strong Balance Sheet to Support Growth

$57.3M of cash and marketable securities and no debt as of June 30, 2014

$27.1M of net deferred tax assets as of June 30, 2014

Working capital utilization metrics among the best in the industry

Internal cash generation expected to finance growth plans

Modest capital expenditures of approximately $3M - $5M per year range expected

| 7 |

|

|

|

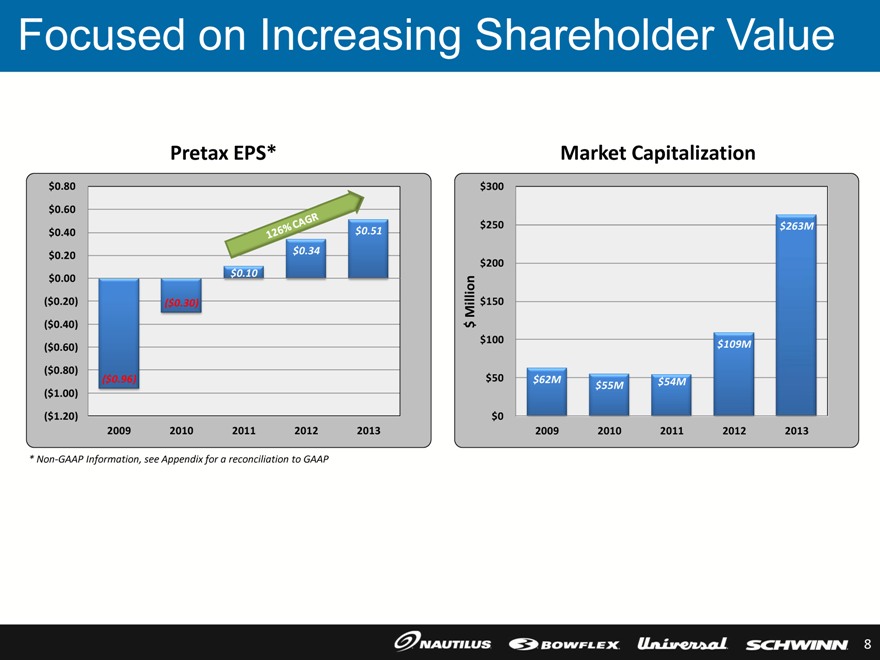

Focused on Increasing Shareholder Value

Pretax EPS*

$0.80

$0.60

$0.40 $ 0.51

$0.20 $ 0.34

$0.00 $ 0.10

($ 0.20) ($ 0.30)

($ 0.40)

($ 0.60)

($ 0.80)

($ 0.96)

($ 1.00)

($ 1.20)

2009 2010 2011 2012 2013

Market Capitalization

$300s

$250 $263M

$200

$109M

$

$55M $54M

$0

2009 2010 2011 2012 2013

126% CAGR

$ Million 150 & 50 & 62M

| * |

|

Non-GAAP Information, see Appendix for a reconciliation to GAAP |

| 8 |

|

|

|

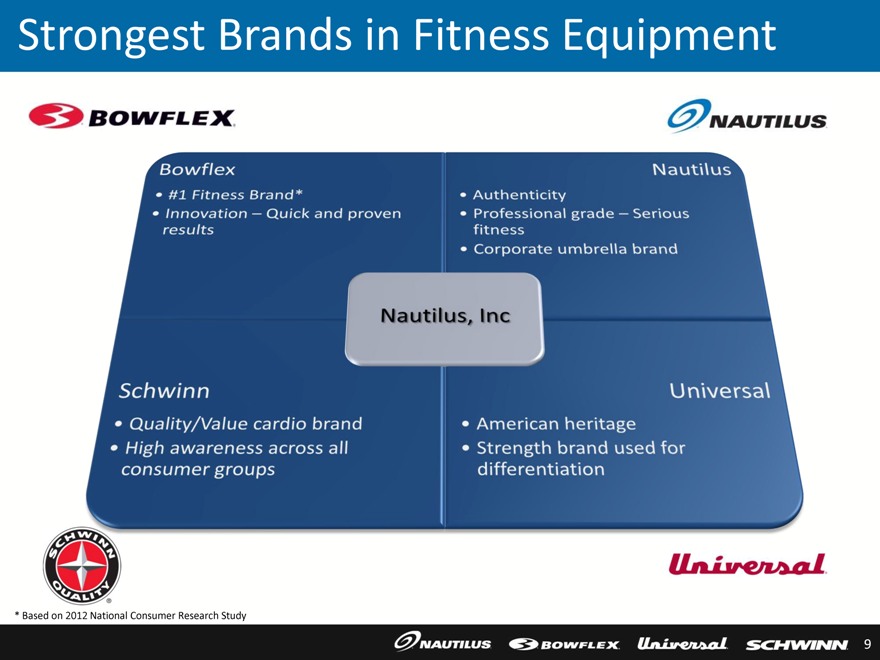

Strongest Brands in Fitness Equipment

Bowflex

#1 Fitness Brand*

Innovation – Quick and proven results

Schwinn

Quality/Value cardio brand

High awareness across all consumer groups

Nautilus, Inc

Authenticity

Professional grade – Serious fitness

Corporate umbrella brand

sAmerican heritage Universal Nautilus

Strength brand used for differentiation

9

|

|

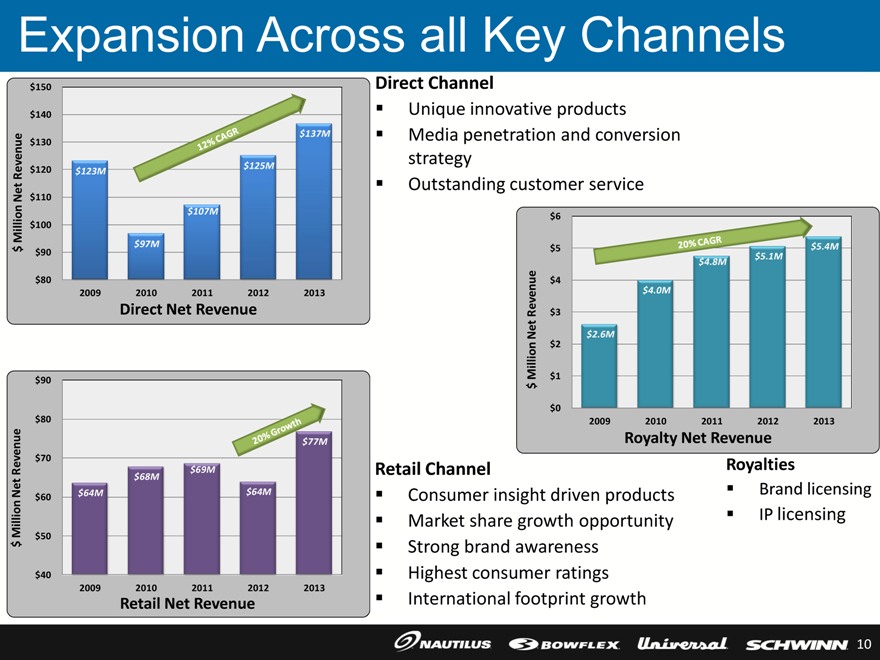

Expansion Across all Key Channels

$150

$140

$137M

$130

$120 $123M $125M

$110

$107M

$100

$ Million Net Revenue $97M

$90

$80

2009

$90

$80

$70

$60 $64M

$ Million Net Revenue $50

$40

2009 2010 2011 2012 2013

Retail Net Revenue

Direct Channel

Unique innovative products

Media penetration and conversion strategy

Outstanding customer service

$6

$5 $5.4M

$4.8M $5.1M

$4

$4.0M

$3

$2.6M

$2

$ Million Net Revenue $1

$0

2009 2010 2011 2012 2013

Royalty Net Revenue

Retail Channel

Consumer insight driven products

Royalties

Brand licensing Market share growth opportunity

IP licensing Strong brand awareness

Highest consumer ratings

International footprint growth

12% CAGR Direct Revenue 20% Growth $69M $ 64M $ 77M $68M 20% CAGR

10

|

|

Industry Leading Product Quality & Innovation

11

|

|

Retail Channel

12

|

|

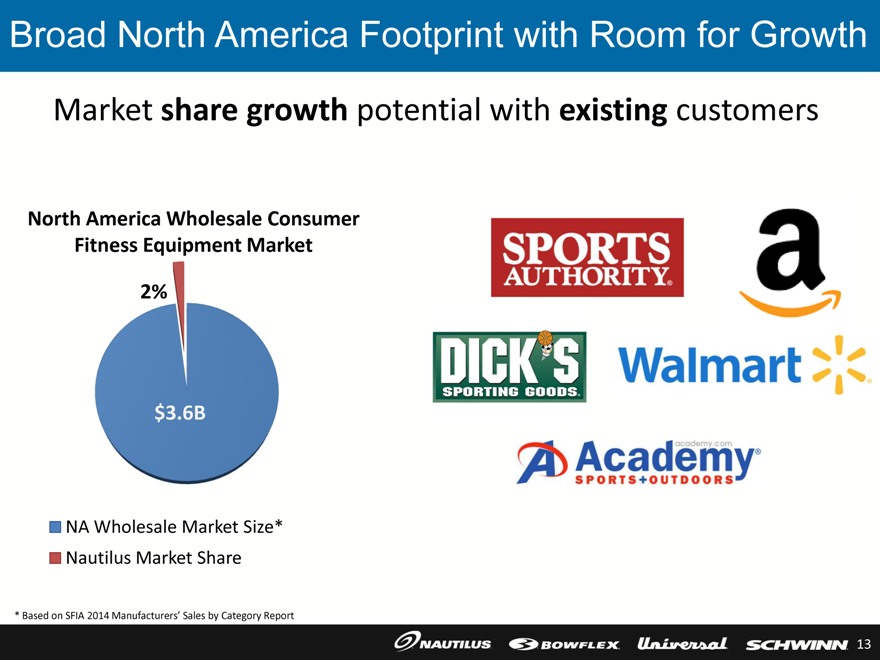

Broad North America Footprint with Room for Growth

Market share growth potential with existing customers

North America Wholesale Consumer Fitness Equipment Market

2%

$3.6B

NA Wholesale Market Size* Nautilus Market Share

| * |

|

Based on SFIA 2014 Manufacturers’ Sales by Category Report |

13

|

|

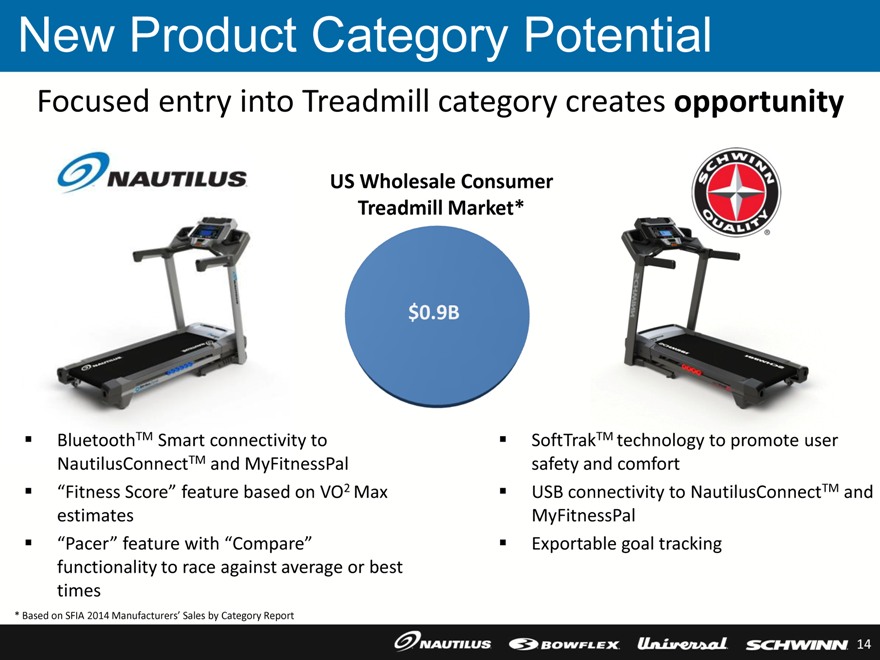

New Product Category Potential

Focused entry into Treadmill category creates opportunity

US Wholesale Consumer Treadmill Market*

$0.9B

BluetoothTM Smart connectivity to NautilusConnectTM and MyFitnessPal

“Fitness Score “ feature based on VO2 Max estimates

“Pacer “ feature with “Compare” functionality to race against average or best times

SoftTrakTM technology to promote user safety and comfort

USB connectivity to NautilusConnectTM and MyFitnessPal

Exportable goal tracking

| * |

|

Based on SFIA 2014 Manufacturers’ Sales by Category Report |

14

|

|

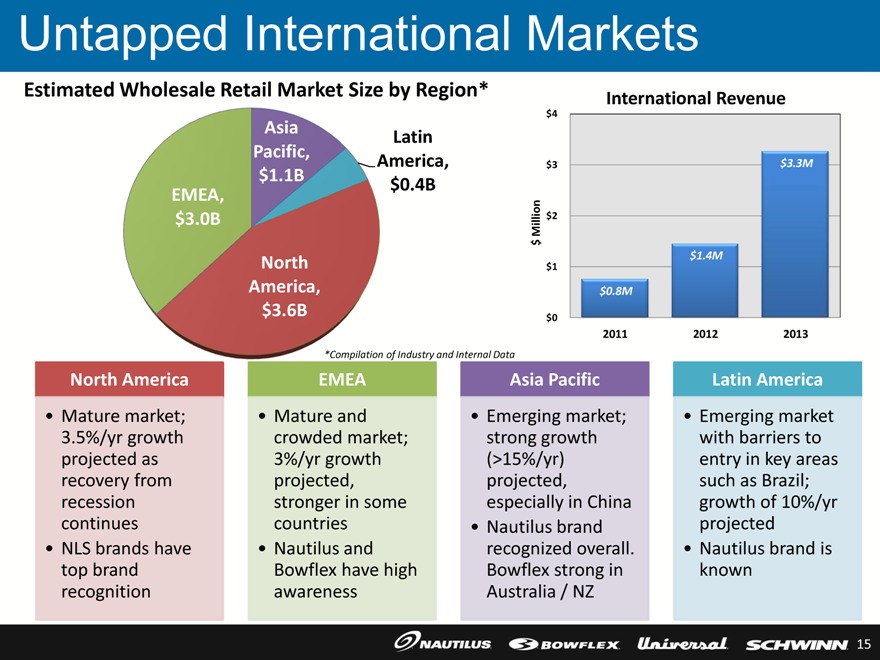

Untapped International Markets

Estimated Wholesale Retail Market Size by Region* International Revenue

$4

Asia Latin

Pacific, America, $3 $3.3M

$1.1B $0.4B

EMEA,

$3.0B $ Millions $2

North $1 $1.4M

America,s $0.8M

$3.6B $0

2011 2012 2013

*Compilation of Industry and Internal Data

North America

Mature market; 3.5%/yr growth projected as recovery from recession continues

NLS brand have top brand recognition

EMEA

Mature and crowded market; 3%/yr growth projected, stronger in some countries

Nautilus and Blowflex have high awareness

Asia pacific

Emerging market strong growth(15%/yr) projected especially in China

Nautilus brand recognized overall. Bowflex strong in Australia / NZ

Latin America

Emerging market with barriers to entry in key areas such as Brazil; growth of 10%/yr projected

Nautilus brand is known

15

|

|

Direct Channel

16

|

|

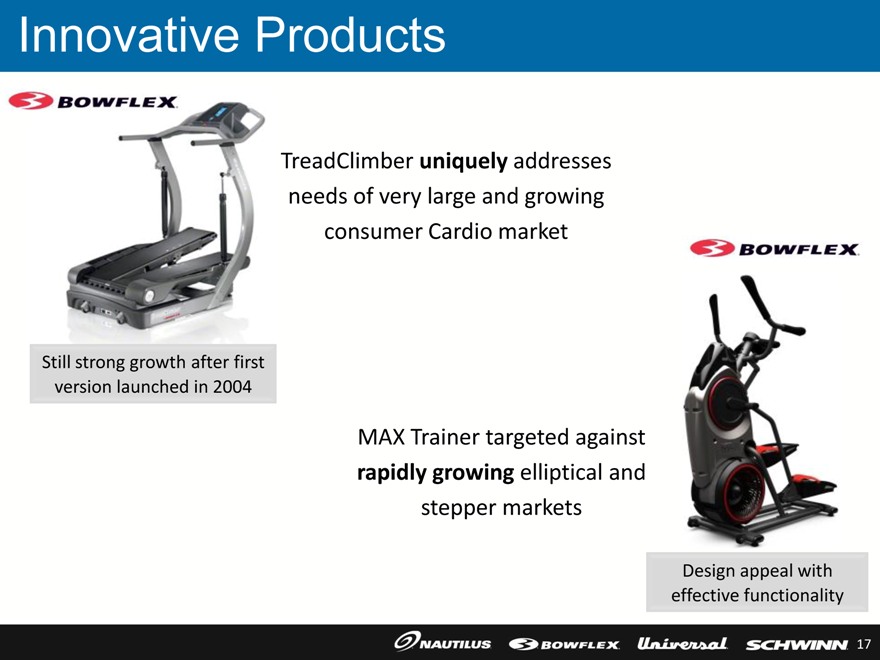

Innovative Products

TreadClimber uniquely addresses needs of very large and growing consumer Cardio market

Still strong growth after first version launched in 2004

MAX Trainer targeted against rapidly growing elliptical and stepper markets

Design appeal with effective functionality

17

|

|

Building on Strong Legacy of TV Marketing

TV remains the core channel to reach a mass audience

In 2013, we invested > $20 million in Short Form and Long Form television resulting in over 5 billion impressions

Magazines capture an engaged, niche audience

Top titles were Weight Watchers, Woman’s Day, Health

Ran Full-Page ads and advertorials during the peak season

18

|

|

Rapidly Expanding Digital Media Presence

Our Online Media spend was > $10 million and delivered nearly

| 3 |

|

billion impressions |

Resulting in over 15 million visitors to our 30+ US & Canada ecommerce & content sites

Active presence across 17 social media platforms

19

|

|

Large Opportunity for Cross-selling

Database of over 12 million customer names

Communicate to several million annually

Deep Conversion Stream

Includes an information kit, self mailers, postcards and emails that incentivize conversion to sale

Large campaigning tool used to support print, promotions, retention, and content as well as lead, sales and testimonial prospecting

Catalog

| 3 |

|

drops a year – Summer, Holiday and Winter |

Use complex consumer modeling & segmentation

Kit Information

Modeling

20

|

|

Long-term Goals

21

|

|

Our Five Management Principles

| 1. |

|

Focus on profitable growth while leveraging and tightly controlling expenses |

| 2. |

|

Deliver a steady flow of consumer-insight driven innovations |

| 3. |

|

Continue investing in our brands and new product launches |

Longer term view

| 4. |

|

Apply sense of urgency and intense focus on strategy and execution |

Achieve what we say we’re going to do

| 5. |

|

Support and nurture our vibrant culture of organizational excellence |

Continue to drive positive shareholder return!

22

|

|

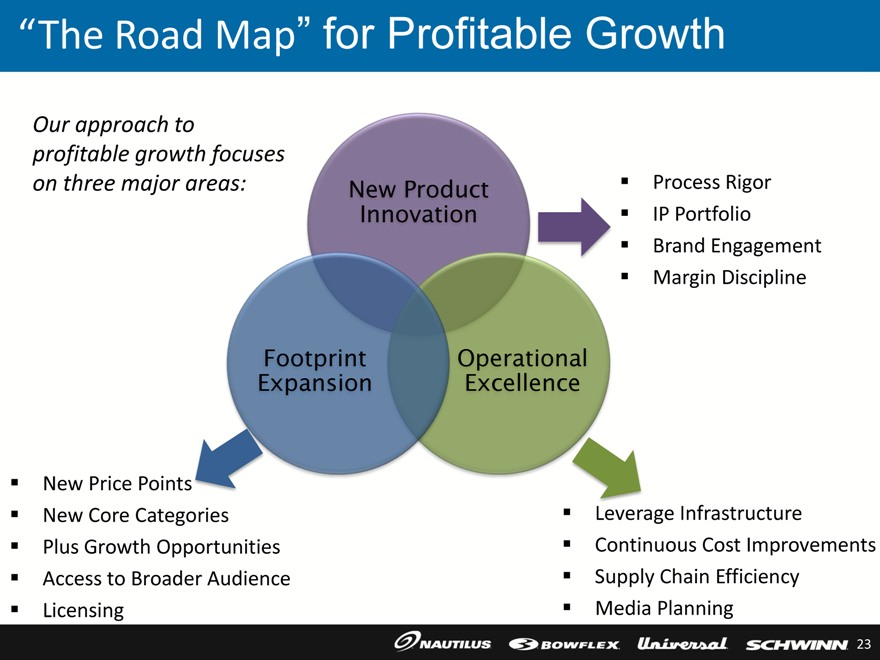

“The Road Map” for Profitable Growth

Our approach to profitable growth focuses on three major areas:

New Product Innovation

Process Rigor

IP Portfolio

Brand Engagement

Margin Discipline

Footprint Expansion

New Price Points

New Core Categories

Plus Growth Opportunities

Access to Broader Audience

Licensing

Operational Excellence

Leverage Infrastructure

Continuous Cost Improvements

Supply Chain Efficiency

Media Planning

23

|

|

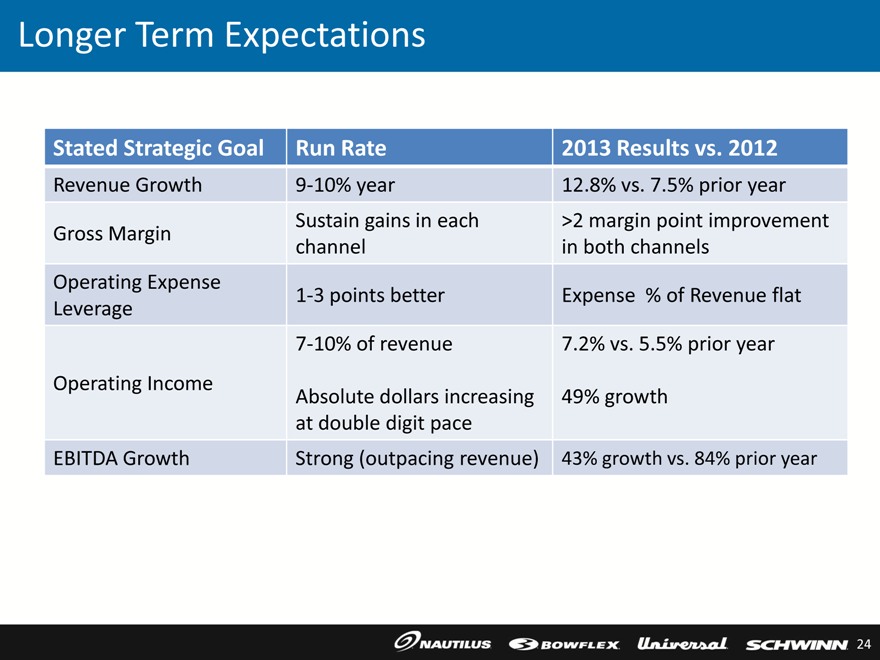

Longer Term Expectations

Stated Strategic Goal

Run Rate

2013 Results vs. 2012

Revenue Growth

Gross Margin

9-10% year

12.8% vs. 7.5% prior year

Sustain gains in each channel >2 margin point improvement in both channels

Operating Expense Leverage

1-3 points better

Expense % of Revenue flat

7-10% of revenue 7.2% vs. 5.5% prior year

Operating Income

Absolute dollars increasing 49% growth

at double digit pace

EBITDA Growth Strong (outpacing revenue) 43% growth vs. 84% prior year

24

|

|

Key Take Aways

Our company is achieving growth and significantly improved profitability

Capabilities have been built to deliver long-term profitability

Strategic growth drivers and opportunities have been identified and are being pursued

Strong asset position is unique and leverage-able

“Brands, IP, balance sheet, business model, human capital

Our team is highly skilled and motivated behind a solid plan .....s and the plan is working

25

|

|

THANK YOU

26

|

|

Appendix

27

|

|

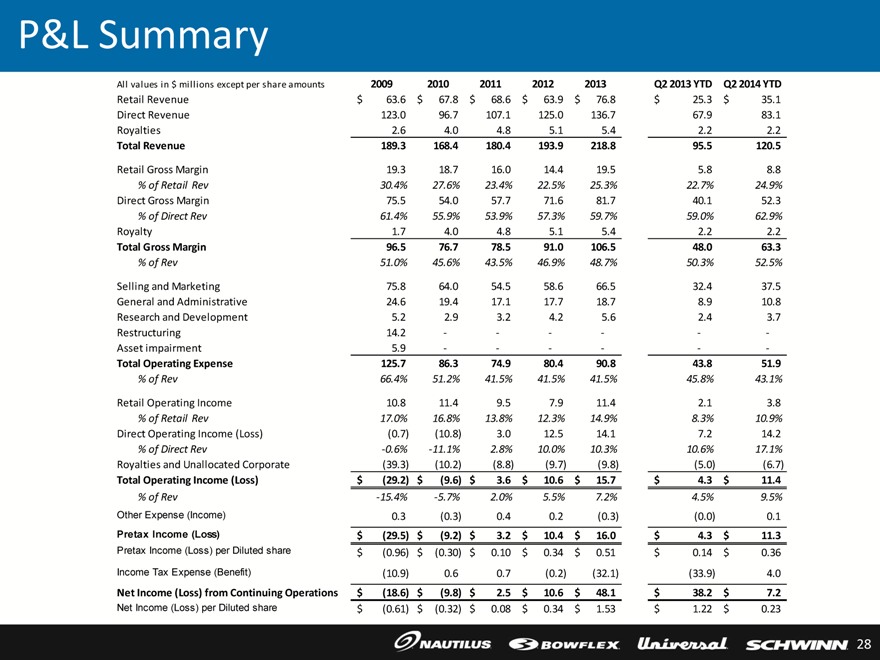

P&L Summary

All values in $ millions except per share amounts 2009 2010 2011 2012 2013 Q2 2013 YTD Q2 2014 YTD

Retail Revenue $ 63.6 $ 67.8 $ 68.6 $ 63.9 $ 76.8 $ 25.3 $ 35.1

Direct Revenue 123.0 96.7 107.1 125.0 136.7 67.9 83.1

Royalties 2.6 4.0 4.8 5.1 5.4 2.2 2.2

Total Revenue 189.3 168.4 180.4 193.9 218.8 95.5 120.5

Retail Gross Margin 19.3 18.7 16.0 14.4 19.5 5.8 8.8

% of Retail Rev 30.4% 27.6% 23.4% 22.5% 25.3% 22.7% 24.9%

Direct Gross Margin 75.5 54.0 57.7 71.6 81.7 40.1 52.3

% of Direct Rev 61.4% 55.9% 53.9% 57.3% 59.7% 59.0% 62.9%

Royalty 1.7 4.0 4.8 5.1 5.4 2.2 2.2

Total Gross Margin 96.5 76.7 78.5 91.0 106.5 48.0 63.3

% of Rev 51.0% 45.6% 43.5% 46.9% 48.7% 50.3% 52.5%

Selling and Marketing 75.8 64.0 54.5 58.6 66.5 32.4 37.5

General and Administrative 24.6 19.4 17.1 17.7 18.7 8.9 10.8

Research and Development 5.2 2.9 3.2 4.2 5.6 2.4 3.7

Restructuring 14.2 — — — — — —

Asset impairment 5.9 — — — — — —

Total Operating Expense 125.7 86.3 74.9 80.4 90.8 43.8 51.9

% of Rev 66.4% 51.2% 41.5% 41.5% 41.5% 45.8% 43.1%

Retail Operating Income 10.8 11.4 9.5 7.9 11.4 2.1 3.8

% of Retail Rev 17.0% 16.8% 13.8% 12.3% 14.9% 8.3% 10.9%

Direct Operating Income (Loss) (0.7) (10.8) 3.0 12.5 14.1 7.2 14.2

% of Direct Rev -0.6% -11.1% 2.8% 10.0% 10.3% 10.6% 17.1%

Royalties and Unallocated Corporate (39.3) (10.2) (8.8) (9.7) (9.8) (5.0) (6.7)

Total Operating Income (Loss) $ (29.2) $ (9.6) $ 3.6 $ 10.6 $ 15.7 $ 4.3 $ 11.4

% of Rev -15.4% -5.7% 2.0% 5.5% 7.2% 4.5% 9.5%

Other Expense (Income) 0.3 (0.3) 0.4 0.2 (0.3) (0.0) 0.1

Pretax Income (Loss) $ (29.5) $ (9.2) $ 3.2 $ 10.4 $ 16.0 $ 4.3 $ 11.3

Pretax Income (Loss) per Diluted share $ (0.96) $ (0.30) $ 0.10 $ 0.34 $ 0.51 $ 0.14 $ 0.36

Income Tax Expense (Benefit) (10.9) 0.6 0.7 (0.2) (32.1) (33.9) 4.0

Net Income (Loss) from Continuing Operations $ (18.6) $ (9.8) $ 2.5 $ 10.6 $ 48.1 $ 38.2 $ 7.2

Net Income (Loss) per Diluted share $ (0.61) $ (0.32) $ 0.08 $ 0.34 $ 1.53 $ 1.22 $ 0.23

28

|

|

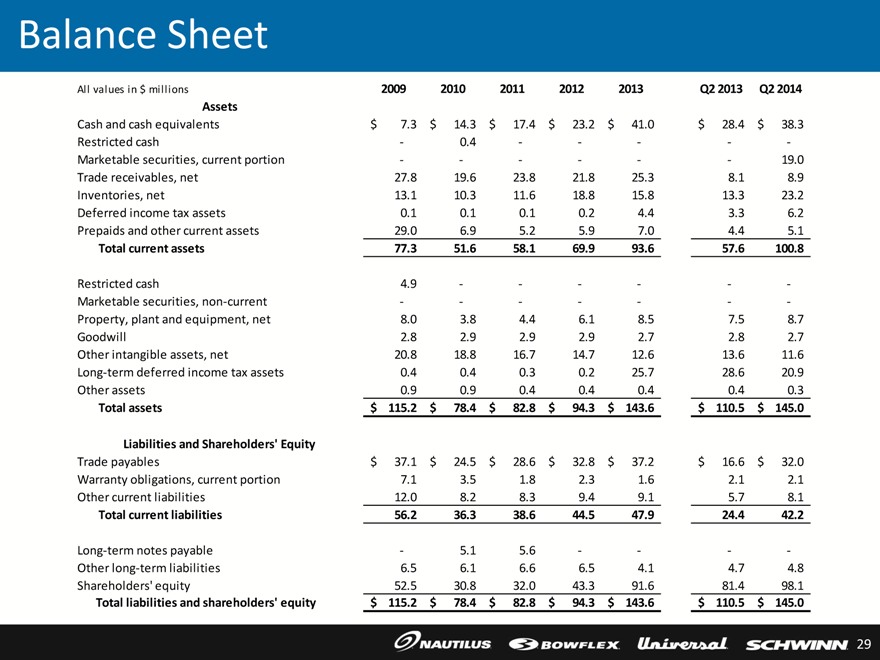

Balance Sheet

All values in $ millions 2009 2010 2011 2012 2013 Q2 2013 Q2 2014

Assets

Cash and cash equivalents $ 7.3 $ 14.3 $ 17.4 $ 23.2 $ 41.0 $ 28.4 $ 38.3

Restricted cash — 0.4 — — — — —

Marketable securities, current portion — — — — — — 19.0

Trade receivables, net 27.8 19.6 23.8 21.8 25.3 8.1 8.9

Inventories, net 13.1 10.3 11.6 18.8 15.8 s13.3 23.2

Deferred income tax assets 0.1 0.1 0.1 0.2 4.4 3.3 6.2

Prepaids and other current assets 29.0 6.9 5.2 5.9 7.0 4.4 5.1

Total current assets 77.3 51.6 58.1 69.9 93.6 57.6 100.8

Restricted cash 4.9 — — — — — —

Marketable securities, non-current — — — — — — —

Property, plant and equipment, net 8.0 3.8 4.4 6.1 8.5 7.5 8.7

Goodwill 2.8 2.9 2.9 2.9 2.7 2.8 2.7

Other intangible assets, net 20.8 18.8 16.7 14.7 12.6 13.6 11.6

Long-term deferred income tax assets 0.4 0.4 0.3 0.2 25.7 28.6 20.9

Other assets 0.9 0.9 0.4 0.4 0.4 0.4 0.3

Total assets $ 115.2 $ 78.4 $ 82.8 $ 94.3 $ 143.6 $ 110.5 $ 145.0

Liabilities and Shareholders’ Equity

Trade payables $ 37.1 $ 24.5 $ 28.6 $ 32.8 $ 37.2 $ 16.6 $ 32.0

Warranty obligations, current portion 7.1 3.5 1.8 2.3 1.6 2.1 2.1

Other current liabilities 12.0 8.2 8.3 9.4 9.1 5.7 8.1

Total current liabilities 56.2 36.3 38.6 44.5 47.9 24.4 42.2

Long-term notes payable — 5.1 5.6 — — — —s

Other long-term liabilities 6.5 6.1 6.6 6.5 4.1 4.7 4.8

Shareholders’ equity 52.5 30.8 32.0 43.3 91.6 81.4 98.1

Total liabilities and shareholders’ equity $ 115.2 $ 78.4 $ 82.8 $ 94.3 $ 143.6 $ 110.5 $ 145.0

29

|

|

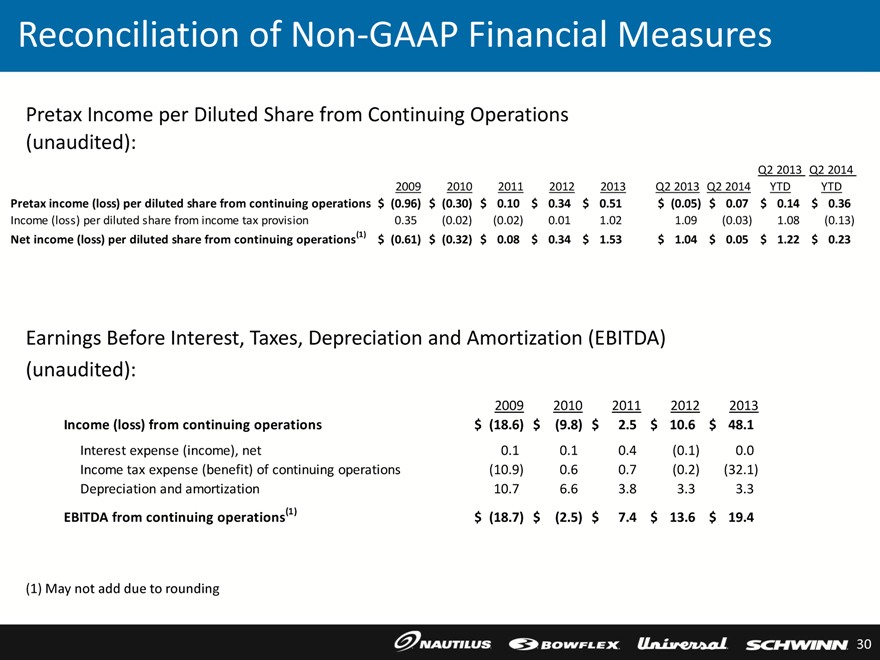

Reconciliation of Non-GAAP Financial Measures

Pretax Income per Diluted Share from Continuing Operations

(unaudited):

Q2 2013 Q2 2014

2009 2010 2011 2012 2013 Q2 2013 Q2 2014 YTD YTD

Pretax income (loss) per diluted share from continuing operations $ (0.96) $ (0.30) $ 0.10 $ 0.34 $ 0.51 $ (0.05) $ 0.07 $ 0.14 $ 0.36

Income (loss) per diluted share from income tax provision 0.35 (0.02) (0.02) 0.01 1.02 1.09 (0.03) 1.08 (0.13)

Net income (loss) per diluted share from continuing operations(1) $ (0.61) $ (0.32) $ 0.08 $ 0.34 $ 1.53 $ 1.04 $ 0.05 $ 1.22 $ 0.23

Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA)

(unaudited):

2009 2010 2011 2012 2013

Income (loss) from continuing operations $ (18.6) $ (9.8) $ 2.5 $ 10.6 $ 48.1

Interest expense (income), net 0.1 0.1 0.4 (0.1) 0.0

Income tax expense (benefit) of continuing operations (10.9) 0.6 0.7 (0.2) (32.1)

Depreciation and amortization 10.7 6.6 3.8 3.3 3.3

EBITDA from continuing operations(1) $ (18.7) $ (2.5) $ 7.4 $ 13.6 $ 19.4

| (1) |

|

May not add due to rounding |

30