Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - ELECTRO RENT CORP | Financial_Report.xls |

| EX-32.2 - EXHIBIT - ELECTRO RENT CORP | ex-322.htm |

| EX-32.1 - EXHIBIT - ELECTRO RENT CORP | ex-321.htm |

| EX-10.21 - EXHIBIT - ELECTRO RENT CORP | ex1022fye14.htm |

| EX-10.36 - EXHIBIT - ELECTRO RENT CORP | ex1036fye14.htm |

| EX-10.21 - EXHIBIT - ELECTRO RENT CORP | ex1021fye14.htm |

| EX-10.35 - EXHIBIT - ELECTRO RENT CORP | ex-1035fye14.htm |

| EX-23 - EXHIBIT - ELECTRO RENT CORP | ex-23.htm |

| EX-10.18 - EXHIBIT - ELECTRO RENT CORP | ex1018fye14.htm |

| EX-31.2 - EXHIBIT - ELECTRO RENT CORP | ex-312.htm |

| EX-31.1 - EXHIBIT - ELECTRO RENT CORP | ex-311.htm |

| EX-10.18 - EXHIBIT - ELECTRO RENT CORP | ex1019fye14.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington DC 20549

FORM 10-K

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended May 31, 2014

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 000-09061

ELECTRO RENT CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

CALIFORNIA | 95-2412961 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

6060 Sepulveda Boulevard

Van Nuys, California 91411-2512

(Address of Principal Executive Offices and Zip Code)

(818) 786-2525

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock without par value | The NASDAQ Stock Market LLC | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

Large Accelerated Filer | ¨ | Accelerated Filer | ý | |||

Non-Accelerated Filer | ¨ | Smaller Reporting Company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

The aggregate market value of the registrant’s common stock held by non-affiliates, computed on the basis of the closing price as reported on the Nasdaq market as of November 30, 2013, was $408,047,552. Shares of common stock held by executive officers, directors and by persons who own 10% or more of the outstanding common stock of the registrant have been excluded for purposes of the foregoing calculation. This does not reflect a determination that such persons are affiliates for any other purpose.

Number of shares of the registrant’s common stock outstanding as of August 11, 2014: 24,008,489.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Annual Report on Form 10-K incorporates by reference certain information contained in the Proxy Statement for the registrant's Annual Meeting of Shareholders, which will be filed with the Securities and Exchange Commission not later than September 28, 2014.

EXPLANATORY NOTE

Unless otherwise noted, (1) the terms “we”, “us” and “our” refer to Electro Rent Corporation and its subsidiaries, and (2) the terms “Common Stock” and “shareholder(s)” refer to our common stock and the holders of that stock, respectively.

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. You can find many (but not all) of these statements by looking for words such as “approximates,” “believes,” “expects,” “anticipates,” “estimates,” “intends,” “plans,” “would,” “may” or other similar expressions in this Report. We claim the protection of the safe harbor contained in the Private Securities Litigation Reform Act of 1995. We caution investors that any forward-looking statements presented in this report, or that we may make orally or in writing from time to time, reflect our good faith estimations based on information currently available to us. Such statements are based on assumptions, and the actual outcome will be affected by known and unknown risks, trends, uncertainties and factors that are beyond our control or ability to predict. Although we believe that our assumptions are reasonable, they are not guarantees of future performance and some will inevitably prove to be incorrect. As a result, our actual future results can be expected to differ from our expectations, and those differences may be material.

Some of the risks and uncertainties that may cause our actual results, performance or achievements to differ materially from those expressed or implied by forward-looking statements include the following: Common Stock price fluctuations, fluctuations in operating results (including as a result of changing economic conditions), risks associated with technology changes, risks associated with customer solvency, competition, risks associated with international operations, risks associated with our manufacturers and suppliers, dependence on key personnel, control by management and others, risks associated with possible acquisitions and new business ventures and anti-takeover provisions. For further discussion of these and other factors, see Item 1A. “Risk Factors”; Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations”; and Item 7A. “Quantitative and Qualitative Disclosure about Interest Rates and Currency Rates,” in this report, and our other filings with the Securities and Exchange Commission.

This Annual Report on Form 10-K and all subsequent written and oral forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. We do not undertake any obligation to release publicly any revisions to our forward-looking statements to reflect events or circumstances after the date of this report.

2

PART I

Item 1. Business.

We are one of the largest global organizations devoted to the rental, lease and sale of new and used electronic test and measurement (“T&M”) equipment. We purchase that equipment from leading manufacturers such as Keysight Technologies, Inc. (formerly Agilent Technologies, Inc., “Keysight”), Anritsu, Inc. ("Anritsu"), and Tektronix Inc. (“Tektronix”) primarily for use by our customers in the aerospace, defense, telecommunications, electronics, and semiconductor industries. Although it represented only approximately 8% of our revenues in fiscal 2014, we believe our Data Products ("DP") division is one of the largest rental companies in the United States for personal computers and servers from manufacturers including Dell, HP/Compaq, IBM, Toshiba and Apple.

The Electro Rent Approach. For the most part, customers who rent, purchase, or lease equipment from us place orders through our inside sales force, which has access to our proprietary computer system that we update in real time for equipment availability and pricing. In the case of rentals and some leases, we generally use a pool of equipment we have previously purchased for that purpose, or we may add equipment to that pool to fill a lease or rental order if the addition makes economic sense. Our equipment fulfillment team typically can arrange delivery of equipment from our pool to our customers within one or two days of a request. Most of our equipment is technically complex and must be tested and serviced when returned to us. We do most of that testing in house, using a team of experienced technicians and our state of the art calibration laboratory.

Although our customers respond to equipment pricing and availability in making their decisions to choose to work with us, we believe that our success also depends on other factors:

• | Customer Service. Our customer service, responsiveness and expert technical staff provide us with a key competitive advantage. Our resale channel for Keysight T&M equipment in the United States and Canada has enabled us to substantially expand the number and technical expertise of our T&M sales force, which at approximately 100 persons is the largest among our principal competitors. |

• | Trusted Brand. We believe our management team is the most experienced and stable in the industry, with our executive officers averaging 30 years at Electro Rent. In 2008, 2009 and 2014, Forbes magazine named us as one of the “100 Most Trustworthy Companies” out of more than 8,000 publicly traded companies for “transparent and conservative accounting practices and solid corporate governance and management.” We were also honored as a Frost & Sullivan 2012 Company of the Year. |

• | Global Platform. As the largest T&M rental, leasing and sales company in North America, and one of the only T&M rental companies in the world with a global platform and key locations in the US, Canada, China and Europe, our size and reach appeals to our multinational customers and assists us in maximizing our equipment utilization and equipment pool management across different geographic markets. |

• | Multichannel Offerings. In the last two years, we have expanded our business to offer customers a single source for their equipment acquisitions, whether they want to rent, lease or buy new or used equipment. We believe that we offer the greatest breadth of acquisition options in the industry, allowing our customers to match the appropriate option to their usage and capital needs, budget and other factors, such as accounting rules and regulatory requirements. In addition, spreading costs over multiple channels allows us to maintain the largest sales force among our principal competitors, which in turn broadens and deepens our customer contacts and provides them more technical strength and assistance. |

• | Proprietary Equipment Management Systems. To maximize our overall profit, we manage our equipment pool on an on-going basis by controlling the timing, pricing and mix of our purchases and sales of equipment. We acquire new and used equipment to meet current and anticipated customer demand and stay abreast of current technical standards. We sell our used equipment when we believe that is the most lucrative option. We employ a complex equipment management strategy and our proprietary PERFECT software to adjust our equipment pool and pricing in order to maximize equipment availability, utilization and profitability. |

Strategic Growth Initiatives. We believe that our resources and financial infrastructure remain capable of handling a significantly greater volume of business activity without a proportionate increase in expenses. Based on this belief, we have been seeking ways to increase revenues and leverage that infrastructure through internal growth and external acquisitions. Despite continuing weakness in the economic environment, we have used our strong balance sheet to make significant equipment purchases to meet the T&M rental demand and support areas of potential growth. We paid $58.7 million for rental and lease equipment purchases during fiscal 2014, compared to $64.1 million during fiscal 2013, a decline of 8.4%. Our equipment purchases have allowed us to expand and upgrade our equipment base, enhancing our ability to meet the needs

3

of a wide range of customers, as well as expand our equipment pool offerings in some related areas such as telecommunications and industrial products.

Competition. We face different competition based on industry sector and geography. For T&M equipment, the North American market generates in excess of $300 million of rental and lease revenue annually. The market is characterized by intense competition from several large competitors, and no single competitor holds a dominant market share in North America. Our primary competitors in this market include McGrath RentCorp, Continental Resources, Inc., Test Equity LLC, and Microlease plc. In Europe, we compete for T&M rental business with Microlease plc and Livingston Group Ltd. In Asia we compete with a number of local operators. These entities also compete with us in leasing T&M equipment, as do banks,vendors and other financing sources. In selling used equipment, we may also compete with sales of new equipment by our suppliers, including Keysight, Tektronix and Anritsu, and their other distributors. Our competitors engage in aggressive pricing for both rentals and sales. In order to maintain or increase our market share, we may choose to lower our prices, resulting in lower revenues and decreased profitability.

For our DP division, the market for the lease and rental of computers and servers is highly fragmented. Our principal competitors in this area include SmartSource Rentals (“SmartSource”), Source One Rentals, Rentex and CRE Rentals. The computer rental market has been characterized by intense competition that has led to industry consolidation. We have acquired two competitors during the last seventeen years and SmartSource, our largest competitor in this market, has expanded primarily due to its numerous acquisitions. While we have focused on the rental of large quantities of computers to unique customers, SmartSource concentrates more on audio visual and trade show technology rentals.

Our Backlog. At May 31, 2014, we had a sales order backlog for new T&M equipment of $10.7 million, compared to $7.6 million at May 31, 2013 and $8.4 million at May 31, 2012. The increase in backlog is primarily due to longer manufacturing lead times for certain equipment as well as an increase in demand from our customers.

Backlog represents the cumulative balance, at a given point in time, of recorded customer sales orders that have not yet been shipped or recognized as sales. Backlog increases when an order is received, and declines when we recognize sales. Although backlog consists of firm orders for which goods and services are yet to be provided, customers can, and sometimes do, terminate or modify these orders. Backlog, on any particular date, while indicative of short-term revenue performance, is not necessarily a reliable indicator of medium or long-term revenue performance.

International Operations. We conduct rental, leasing and sales activity in foreign countries, which in the aggregate accounted for approximately 15.5% of our revenues in 2014, 14.9% in 2013 and 13.8% in 2012. Selected financial information regarding our international operations is presented below:

Fiscal Year ended May 31, (in thousands) | 2014 | 2013 | 2012 | ||||||||

Revenues: 1 | |||||||||||

U.S. | $ | 203,806 | $ | 211,745 | $ | 214,354 | |||||

Other 2 | 37,331 | 36,986 | 34,200 | ||||||||

Total | $ | 241,137 | $ | 248,731 | $ | 248,554 | |||||

As of May 31, (in thousands) | 2014 | 2013 | 2012 | ||||||||

Net Long Lived Assets: 3 | |||||||||||

U.S. | $ | 188,343 | $ | 198,956 | $ | 207,449 | |||||

Other 2 | 46,667 | 49,726 | 49,595 | ||||||||

Total | $ | 235,010 | $ | 248,682 | $ | 257,044 | |||||

1 | Revenues by country are based on the shipping destination. |

2 | Other consists of countries other than the United States. No single country outside the United States accounted for 10% or more of the total revenues and net long-lived assets. |

3 | Net long-lived assets include rental and lease equipment and other property, net of accumulated depreciation and amortization. |

For risks relating to our international operations, see “Item 1A. Risk Factors – Risks Associated with International Operations.”

4

Other Information. The following table shows, for each of the last three fiscal years, revenues from rentals and leases and sales of equipment and other revenues for our T&M and DP operating segments:

Fiscal Year ended May 31, (in thousands) | T&M | DP | Total | ||||||||

2014 | |||||||||||

Rentals and leases | $ | 120,629 | $ | 16,788 | $ | 137,417 | |||||

Sales of equipment and other revenues | 101,898 | 1,822 | 103,720 | ||||||||

$ | 222,527 | $ | 18,610 | $ | 241,137 | ||||||

2013 | |||||||||||

Rentals and leases | $ | 120,846 | $ | 15,745 | $ | 136,591 | |||||

Sales of equipment and other revenues | 109,700 | 2,440 | 112,140 | ||||||||

$ | 230,546 | $ | 18,185 | $ | 248,731 | ||||||

2012 | |||||||||||

Rentals and leases | $ | 113,540 | $ | 16,197 | $ | 129,737 | |||||

Sales of equipment and other revenues | 116,417 | 2,400 | 118,817 | ||||||||

$ | 229,957 | $ | 18,597 | $ | 248,554 | ||||||

The majority of our rental equipment not out on rent is located at our Van Nuys, California warehouse and is serviced by an ISO9001:2008 (DEKRA certified) and ISO17025:2005 (A2LA accreditation). We also service our customers through sales offices and calibration and service centers in the United States, Canada, China and Belgium, which are linked by a proprietary on-line computer system. These centers also function as depots for the sale of used equipment.

For additional financial information about our segments, see Note 14 to our consolidated financial statements included in this Annual Report on Form 10-K.

No single customer accounted for more than 10% of our total revenues during fiscal 2014, 2013 or 2012. We do not derive any significant portion of our revenues from direct United States government contracts.

Other than the license included in our reseller agreement with Keysight, we have no material patents, trademarks, licenses, franchises or concessions.

At May 31, 2014, we employed approximately 420 individuals. Except in China, where we have 13 employees, none of these employees are members of a labor union. None of our employees are subject to collective bargaining agreements. We believe that our employee relations are satisfactory.

Electro Rent Corporation was incorporated in California in 1965 and became a publicly held corporation in 1980.

Obtaining Additional Information. Our Internet address is www.electrorent.com. Copies of our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge on our website via links to the Securities and Exchange Commission’s website as soon as reasonably practicable after we electronically file those materials with the Securities and Exchange Commission. We provide paper copies of these reports to shareholders upon written request to Shareholder Relations, Electro Rent Corporation, 6060 Sepulveda Boulevard, Van Nuys, California 91411-2512.

Item 1A. Risk Factors.

Please carefully consider the following discussion of various risks and uncertainties, as well as the other information in this report and in other reports and documents we file with the Securities and Exchange Commission, when evaluating our business and future prospects. We believe that the following risk factors are the most relevant to our business, but they are not the only risk factors that we face. Additional risks and uncertainties, not presently known to us, or that we currently see as immaterial, may also occur. Our business, financial condition and results of operations could be seriously harmed if any of these risks or uncertainties actually occur or materialize. In that event, the market price for our Common Stock could decline, and our shareholders may lose all or part of their investment.

5

COMMON STOCK PRICE FLUCTUATIONS

The price of our Common Stock has fluctuated significantly in the past and may continue to do so in the future.

General Factors. We believe some of the reasons for past fluctuations in the price of our Common Stock have included:

• | announcements of developments related to our business; |

• | announcements concerning new products or enhancements in the equipment that we rent, or developments in our relationships with our customers; |

• | variations in our revenues, gross margins, earnings or other financial results from investors’ expectations; and |

• | fluctuations in results of our operations and general conditions in the economy, our market, and the markets served by our customers. |

In addition, prices in the stock market in general have been volatile in recent years. In many cases, the fluctuations have been unrelated to the operating performance of the affected companies. As a result, the price of our Common Stock could fluctuate in the future without regard to our operating performance.

Future Sales of our Common Stock. Sales of our Common Stock by our officers, directors and employees could adversely and unpredictably affect the price of our shares. Additionally, the price could be affected by even the potential for sales by these persons. In addition to the 24,008,489 shares outstanding as of August 11, 2014, as of such date, up to 517,907 shares of Common Stock may be issued upon conversion of our vested and unvested stock units previously granted under our Equity Incentive Plan.

We cannot predict the effect that any future sales of our Common Stock, or the potential for those sales, will have on the share price for our Common Stock.

FLUCTUATIONS IN OPERATING RESULTS

Historically, our operating results have fluctuated from period to period, and we expect that fluctuations could continue in the future. The fluctuations in our past results have resulted from many factors, some of which are beyond our control. In the future, these or other factors could have a material impact on our operating results and the price of our Common Stock.

Timing of Equipment Purchases and Sales and Equipment Pool Management. The profitability of our business depends in part on controlling the timing, pricing and mix of purchases and sales of equipment and on managing our equipment pool. We seek to acquire new and used equipment at attractive prices, from which we feel we can make a profit as a result of a combination of renting, leasing and selling that equipment. We base expenditures for equipment purchases, sales and marketing and other items on our expectations of future customer demand. In order to maximize overall profit from the rental, leasing, and sales of equipment, we manage our equipment pool on an on-going basis by analyzing our product strategy for equipment in light of historical and projected lifecycles. In doing so, we compare our estimate of potential profit from rental with the potential profit from the product’s immediate sale and replacement with new or other equipment.

Our overall equipment management is complex and our equipment strategy can change during the equipment’s lifetime based upon numerous factors, including the U.S. and global economy, interest rates and new product launches. Our strategic equipment decisions are based on the following fundamentals:

• | our acquisition cost; |

• | our estimates of current and future market demand for rentals; |

• | our estimates of current and future supply of equipment; |

• | the book value of the equipment after depreciation and other impairment; |

• | our estimates of the effect of interest rates on rental and leasing fees as well as capital financing; and |

• | our estimates of the potential current and future sale prices of equipment. |

However, historical trends are not necessarily indicative of future trends. If our assumptions prove to be wrong, not only may our revenues fall short of our expectations, but we may not be able to adjust our equipment quickly enough to compensate for lower demand for one or more products in our equipment pool. In addition, as demand for a product falls, we may have

6

difficulty in selling any of our excess equipment at a favorable price or at all. Both of these factors can compound the impact of any revenue shortfall and further affect our operating results and the price of our Common Stock.

Global Economic Conditions. In recent years, our financial results have been impacted by competitive pressure on rental rates due in large part to the recession in the U.S. and our major international markets. Our customers historically have reduced their expenditures for T&M and DP equipment during economic downturns. Accordingly, when the domestic and/or international economy weakens, demand for our product offerings declines. A large part of our equipment pool is rented or leased to customers in the aerospace, defense, telecommunications, electronics, industrial and semiconductor industries. Continued weakness in the U.S. and global economy, or in one or more of these specific industries, may result in lower demand and increased pressure on prices and gross profit.

Economic uncertainty continues to impact our customers and competitors, resulting in more stringent credit requirements for our customers and reduced access to capital. We continue to focus on remaining profitable in the current conditions, as well as being prepared for the possibility that recessionary trends may return in future periods.

Seasonality. Regardless of the overall economic outlook domestically and globally, December, January and February typically reflect lower rental activity. In addition, because February is a short month, revenue billing in that month is reduced. The seasonal spending patterns of our customers are also affected by factors such as:

• | weather, holiday and vacation considerations; and |

• | fiscal budgetary cycles. |

Other Factors. Our quarterly operating results are subject to fluctuation based on a wide variety of factors. Other factors that may affect our operating results from one quarter to another include:

• | changes in customer demands and/or requirements; |

changes in pricing or maintenance policies of equipment manufacturers;

• | price competition from other rental, leasing and finance companies; |

• | the timing of new product announcements and launches; |

• | changes in interest rates; |

• | changes in product delivery dates; |

• | currency fluctuations and other risks of international operations; and |

• | changes and reductions to government spending that could negatively impact our customers in the aerospace and defense industry. |

All or any of these factors and similar factors could result in our operating results differing substantially from our expectations, as well as the expectations of public market analysts and investors, which would likely have a material adverse impact on our stock price.

RISKS ASSOCIATED WITH TECHNOLOGY CHANGES

We serve customers that operate in industries that are characterized by technological change, and accordingly must anticipate and respond to changes in technology in order to maintain competitiveness and successful operations.

Technological Advancements. We must anticipate and keep pace with the introduction of new hardware, software and networking technologies and acquire equipment that will be marketable to our current and prospective customers. The equipment that we acquire for our equipment pool can be subject to technological change, evolving customer demands and frequent new product announcements and enhancements. If we fail to adequately anticipate or adapt to new technological developments or to recognize changing market conditions, our operating results and stock price could be materially and adversely affected.

Expenses Resulting from Technological Advancements. As a result of technology developments, we may have to make substantial and unanticipated expenditures to acquire new equipment or invest in further staff education on operating and servicing the equipment we deliver to our customers. Further, we may not adequately anticipate or respond successfully to technological changes for many reasons, including misjudging the impact of technological changes as well as financial, technological or other constraints. If we do not adequately anticipate or respond to changes in technological advancements or customer preferences, it would likely have a material adverse impact on our operating results and stock price.

7

Introduction of New Products and Services. The markets in which we operate are characterized by changing technology, evolving industry standards and declining prices of certain products. Our operating results will depend to a significant extent on our ability to continue to introduce new services and to control and/or reduce costs on existing services. Whether we succeed in our new offerings depends on several factors such as:

• | proper identification of customer needs; |

• | appropriate control of costs; |

• | timely completion and introduction of products and services as compared to our competitors; |

• | our ability to differentiate our equipment and services from our competitors; and |

• | appropriate pricing and market acceptance of our solutions. |

RISKS ASSOCIATED WITH CUSTOMER SOLVENCY

Our customers may face liquidity issues, and if we make poor credit decisions or are unable to collect on contracts with customers, it could have a material adverse effect on our operating results and stock price.

One of the reasons some of our customers find it more attractive to rent or lease electronic equipment instead of owning that equipment is because renting or leasing enables them to deploy their capital elsewhere. This can be particularly true in industries with high growth rates such as the telecommunications industry. However, some of our customers have liquidity issues, which have been compounded by the recent slowness in the global economy, and ultimately may not be able to fulfill the terms of their agreements with us. If we are not able to manage credit risk issues, or if a large number of customers should have financial difficulties at the same time, our credit losses would increase above historical levels and may become material.

COMPETITION

If we do not compete effectively, we may lose market share and our revenues and profitability may decline.

The equipment rental, leasing and sales business is characterized by intense competition from several large competitors, some of which have access to greater financial and other resources than we do. We face competition from both established entities and new entries in the market. Our primary competitors in the North American T&M rental area include McGrath RentCorp, Continental Resources, Inc., Test Equity LLC and Microlease plc. Internationally, our largest competitors for rental business are Microlease plc and Livingston Group Ltd. in Europe. These entities also compete with us in leasing T&M equipment, as do banks, vendors and other financing sources. In addition, in equipment sale, we also compete with sales by our suppliers, including Keysight and Tektronix, and their other distributors. The market for the lease and rental of computers and servers is highly fragmented, and our principal competitors include SmartSource, Source One Rentals, Rentex and CRE Rentals.

Our competitors engage in aggressive pricing for both rentals and sales. In order to maintain or increase our market share, we may choose, or be compelled, to lower our prices, resulting in decreased revenues and profitability, which could materially and adversely affect our stock price.

RISKS ASSOCIATED WITH INTERNATIONAL OPERATIONS

Our international operations will continue to be a meaningful portion of our overall revenues and operations in the future. There are risks that are inherent to our international operations, and if we fail to manage them appropriately we may not meet our revenue expectations or may incur unanticipated expenses, either of which would adversely affect our operations.

Currency Risks. We generated 15.5% of our revenues from activity in foreign countries during the past fiscal year. Our contracts to supply equipment outside of the U.S. are generally priced in local currency. However, our consolidated financial statements are prepared in U.S. dollars. Consequently, changes in exchange rates can unpredictably and adversely affect our consolidated operating results, and could result in exchange losses. Although we use foreign currency forward contracts to mitigate the risks associated with fluctuations in exchange rates, we may not be able to eliminate or reduce the effects of currency fluctuations. Thus, exchange rate fluctuations could have a material adverse impact on our operating results and stock price.

Other Risks Associated with International Operations. Additionally, our financial results may be adversely affected by other international risks, such as:

• | international political and economic conditions; |

• | changes in government regulation in various countries; |

8

• | trade barriers; |

• | difficulty in staffing our foreign sales and service centers, and in training and retaining foreign employees; |

• | issues relating to the repatriation of any profits; |

• | adverse tax consequences; and |

• | costs associated with expansion into new territories. |

We expect to continue our international operations and that the revenues we derive from these activities will continue to be a meaningful portion of our total revenues. If we do not anticipate and respond to the risks associated with international operations, it could have a material adverse effect on our operating results and stock price.

RISKS ASSOCIATED WITH OUR MANUFACTURERS AND SUPPLIERS

Our business is dependent on our ability to purchase equipment for our equipment pool from third party manufacturers and suppliers at prices and on terms that allow us to meet our customers’ requirements. Any significant change in availability, pricing or terms for equipment from our manufacturers could have a substantial impact on our results of operations.

About 92% of our equipment portfolio at acquisition cost consists of general purpose T&M instruments purchased from leading manufacturers such as Keysight, Anritsu, and Tektronix. The remainder of our equipment pool consists of personal computers and workstations, which include personal computers from Dell, Apple, IBM and Toshiba and workstations primarily from HP/Compaq. We depend on these manufacturers and suppliers for our equipment. If, in the future, we are not able to purchase necessary equipment from one or more of these suppliers on favorable terms, we may not be able to meet our customers’ demands in a timely manner or for a price that generates a profit. Depending on the equipment required, or the customer’s specific requirements, there may not be suitable alternatives from other suppliers. Any inability to acquire equipment would adversely impact our revenues. Similarly, if we cannot increase our pricing commensurate with pricing changes from our customers our gross profit and income from operations will be adversely impacted.

If we are unable to renew our reseller agreement with Keysight when it expires on May 31, 2015 on acceptable terms, it could have a material adverse effect on our operating results and stock price.

Sales of new T&M equipment represent approximately 63.5% and 66.8% of our sales of equipment and other revenues for fiscal 2014 and 2013, respectively. Nearly all of our sales of new T&M equipment are in connection with our reseller agreement with Keysight, which expires on May 31, 2015. Keysight is a wholly-owned subsidiary of Agilent Technologies, Inc. (“Agilent”), with whom we originally entered into the reseller agreement. Agilent is currently in the process of spinning off Keysight into a separate publicly traded company, which Agilent has announced that it expects to complete by November 2014. We have renewed our reseller arrangement four times since we entered into the reseller agreement with Agilent in 2009. If we are unable to renew our reseller agreement with Keysight, or if the terms of any renewal are less favorable to us, our T&M equipment sales business may be materially and adversely affected.

Agilent's planned spin-off of Keysight (which manufactures T&M equipment) could impact our relationship with Keysight.

Agilent announced on September 19, 2013 that it plans to spin off its electronic measurement business (which manufactures the T&M equipment) into a separate company. Agilent is in the process of affecting the spin-off, and has assigned its rights to our reseller agreement to Keysight. Agilent has stated publicly that it expects to complete the spin-off by November, 2014. We do not know whether or how the spin-off will impact the renewal of our reseller agreement or other aspects of our relationship with Keysight. Sales of Keysight/Agilent T&M equipment constitutes a substantial portion of our overall revenues. Any material change in our relationship with Keysight, in Keysight’s sales strategy for T&M equipment, or our reseller agreement, may have a material and adverse effect on our business and operating prospects.

DEPENDENCE ON KEY PERSONNEL

If we are unable to recruit and retain qualified personnel, it could have a material adverse effect on our operating results and stock price.

Our success depends in large part on the continued services of our executive officers, our senior managers and other key personnel. Our executive officers, including our Chief Executive Officer, Daniel Greenberg, our President, Steven Markheim, and our Chief Financial Officer, Craig Jones, are each extremely experienced with a long history at the Company. The loss of any of these people could result in significant disruption to our operations. In addition, T&M equipment and solutions can be highly technical and complex, and typically require customizations to meet specific customer applications and needs. The

9

quality of our customer service and the knowledge of our personnel is a key competitive factor for our business. It is very important that we attract highly skilled personnel to accommodate growth and to replace personnel who leave. Competition for qualified personnel can be intense, especially in technology industries, and there are a limited number of people with the requisite knowledge and experience to market, sell and service our equipment. We must retain and recruit qualified personnel in order to maintain and grow our business.

CONTROL BY MANAGEMENT AND OTHERS

Senior management has significant influence over our policies and affairs and may be in a position to determine the outcome of corporate actions.

As of August 11, 2014, our executive officers and directors collectively owned approximately 21.2% of our Common Stock.

As of that date, (i) Mr. Daniel Greenberg, our Chairman and Chief Executive Officer, beneficially owned approximately 19.1% of our outstanding shares of Common Stock, and (ii) one other shareholder controlled 16.2% of our outstanding shares of Common Stock. As long as these shareholders own significant percentage of our Common Stock, they will be able to exert significant influence over our policies and affairs and may be in a position to determine the outcome of corporate actions requiring shareholder approval. These may include, for example, the election of directors, the adoption of amendments to our corporate documents and the approval of mergers and sales of our assets.

RISKS ASSOCIATED WITH POSSIBLE ACQUISITIONS AND NEW BUSINESS VENTURES

If we fail to accurately assess and successfully integrate any recent or future acquisitions or new business ventures, we may not achieve the anticipated benefits, which could result in lower revenues, unanticipated operating expenses, reduced profitability and dilution of our book value per share.

On occasion, we evaluate business opportunities that appear to fit within our overall business strategy. We have completed the following acquisitions and business ventures in recent years:

• | In fiscal 2012, we acquired certain assets and select post-closing liabilities of EMT, a private company based in Las Vegas, Nevada, and a provider of electronic T&M equipment. |

• | In fiscal 2010, we became a reseller of Agilent Technologies, Inc.’s (now Keysight Technologies, Inc.) new T&M equipment in the U.S. and Canada, resulting in the hiring of additional sales and support staff. |

We could decide to pursue one or more other opportunities by acquisition or internal development. Acquisitions and new business ventures, both domestic and foreign, involve many risks, including:

• | the difficulty of integrating acquired operations and personnel with our existing operations; |

• | the difficulty of developing and marketing new products and services; |

• | the diversion of our management’s attention as a result of evaluating, negotiating and integrating acquisitions or new business ventures; |

• | our exposure to unforeseen liabilities of acquired companies; and |

• | the loss of key employees of an acquired operation. |

In addition, an acquisition or new business venture could adversely impact cash flows and/or operating results, and dilute shareholder interests, for many reasons, including:

• | charges to our income to reflect the impairment of acquired intangible assets, including goodwill; |

• | interest costs and debt service requirements for any debt incurred in connection with an acquisition or new business venture; and |

• | any issuance of securities in connection with an acquisition or new business venture that dilutes or lessens the rights of our current shareholders. |

We have implemented various new business ventures in the past, and not all of such ventures have been successful. The risks associated with acquisitions and new business ventures could have a material adverse impact on our operating results and stock price.

10

RISKS ASSOCIATED WITH FLUCTUATING INTEREST RATES

Interest rate fluctuations could have a material adverse effect on our operating results and stock price.

Our leasing yields tend to correlate with market interest rates. When interest rates are higher, our leasing terms incorporate a higher financing charge. However, in times of relatively lower interest rates our financing charges also decrease, and some of our customers choose to purchase new equipment, rather than leasing equipment at all. Lower leasing yields result in lower rental and lease revenues, which could have a material adverse impact on our operating results and stock price.

RISKS ASSOCIATED WITH CHANGES IN GOVERNMENT SPENDING

We have customers in the aerospace and defense industry that derive a significant amount of revenue from the U.S. government. If the U.S. government were to substantially curtail spending for the aerospace and defense industry, it would have a significant negative effect on our revenues and profitability.

The U.S. federal government has implemented significant changes and reductions to government spending and programs. In addition, uncertainty resulting from previously announced defense spending reductions and the potential future additional reductions have impacted, and are likely to continue to impact, the manner in which our customers in the aerospace and defense industry make procurement decisions, resulting in reduced demand by such customers in our rental services and resale business. A shift in government priorities to government programs in which our customers do not participate and/or reductions in funding for or the termination of government programs in which our customers do participate, unless offset by other programs and opportunities, could have a material adverse effect on the demand of our services and products and, as a consequence, our revenues, operating results and stock price.

ANTI-TAKEOVER PROVISIONS

The anti-takeover provisions contained in our Articles of Incorporation and Bylaws and in California law could materially and adversely impact the value of our Common Stock.

Certain provisions of our Articles of Incorporation, our Bylaws and California law could, together or separately, discourage, delay or prevent a third party from acquiring us, even if doing so might benefit our shareholders. This may adversely impact the interests of our shareholders with respect to a potential acquisition and may also affect the price investors would receive for their shares of Common Stock. Some examples of these provisions in our Articles of Incorporation and Bylaws are:

• | the right of our board of directors to issue preferred stock with rights and privileges that are senior to the Common Stock, without prior shareholder approval; and |

• | certain limitations of the rights of shareholders to call a special meeting of shareholders. |

Item 1B: Unresolved Staff Comments.

None.

Item 2. Properties.

We own a building that houses our corporate headquarters and Los Angeles sales office located at 6060 Sepulveda Boulevard, Van Nuys, California. The building contains approximately 84,500 square feet of office space. Approximately 16,000 square feet are currently leased to others. These tenant arrangements provide for all of the leased property to be available for our future needs.

We own a building at 15385 Oxnard Street, Van Nuys, California, which contains approximately 68,200 square feet. We use all of this space, except for 1,000 square feet that are currently being leased to others. This building houses our California warehouse and equipment calibration center.

We own a facility in Wood Dale, Illinois, containing approximately 30,750 square feet. This facility houses our Illinois warehouse and service center.

As of May 31, 2014, we had sales offices in the metropolitan areas of Atlanta and Los Angeles. We also have service centers in Chicago, Dallas, Los Angeles, New York/Newark, San Francisco, Charlotte, Orlando, Toronto, Seattle and Washington/Baltimore. We have foreign sales offices and warehouses in Mechelen, Belgium, and Beijing, China.

Our facilities aggregate approximately 271,000 square feet as of May 31, 2014. Except for the corporate headquarters, the Wood Dale, Illinois facilities and the Oxnard Street building, each of which we own, all of our facilities are rented pursuant to leases for up to seven years for aggregate annual rentals of approximately $1.2 million in fiscal 2014. Most of our leases provide us with the option of renewing our leases at the end of the initial lease term, at the then-existing fair rental value, for periods of up to five years. We do not consider any rented facility essential to our operations. We consider our facilities to be in good condition, well maintained and adequate for our needs.

Item 3. Legal Proceedings.

We are subject to legal proceedings and business disputes involving ordinary routine legal matters and claims incidental to our business. The ultimate legal and financial liability with respect to such matters generally cannot be estimated with certainty and requires the use of estimates in recording liabilities for potential litigation settlements or awards against us. Estimates for losses

11

from litigation are made after consultation with outside counsel. If estimates of potential losses increase or the related facts and circumstances change in the future, we may be required to record either more or less litigation expense. At May 31, 2014 we are not involved in any pending or threatened legal proceedings that we believe could reasonably be expected to have a material adverse effect on our financial condition, results of operations or cash flows.

Item 4. Mine Safety Disclosures.

Not applicable.

PART II

Item 5. Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market for Common Stock; Holders.

Our Common Stock is quoted on the NASDAQ stock market under the symbol ELRC. There were 307 shareholders of record at August 11, 2014. The following table sets forth, for the periods shown, the high and low sale prices of our Common Stock as reported by NASDAQ.

Fiscal Year 2014 | Fiscal Year 2013 | ||||||||||||||

High | Low | High | Low | ||||||||||||

First Quarter | $ | 19.41 | $ | 16.31 | $ | 18.10 | $ | 13.61 | |||||||

Second Quarter | 21.58 | 17.00 | 18.23 | 13.56 | |||||||||||

Third Quarter | 21.25 | 15.68 | 16.39 | 13.93 | |||||||||||

Fourth Quarter | 19.29 | 14.76 | 18.73 | 15.91 | |||||||||||

Sales of Unregistered Securities.

We did not make any unregistered sales of our securities in fiscal 2014.

Securities Authorized for Issuance Under Equity Compensation Plans.

The following table provides information as of May 31, 2014 with respect to shares of our Common Stock that may be issued under our existing stock incentive plans, all of which were approved by our shareholders:

EQUITY COMPENSATION PLAN INFORMATION

Number of shares of Common Stock to be issued upon exercise of outstanding options, warrants and rights (a) | Weighted-average exercise price of outstanding options, warrants and rights (b) | Number of shares of Common Stock remaining available for future issuance under equity compensation plans (excluding shares reflected in column (a)) (c) | ||

0 | 0 | 498,130 | ||

Stock Repurchases.

We have from time to time repurchased shares of our Common Stock under an authorization from our Board of Directors. Shares repurchased by us are retired and returned to the status of authorized but unissued stock. We did not repurchase any shares during fiscal 2014, 2013 or 2012. We may choose to make additional open market or other purchases of our Common Stock in the future, but we have no commitment to do so.

Dividends.

Since July 2007, we have been paying quarterly dividends each January, April, July and October. For fiscal 2014, we paid total dividends of $0.80 per common share (representing a quarterly dividend of $0.20 per common share), compared to a total of $1.80 per common share in fiscal 2013 (which included a special dividend of $1.00 per common share) and a total of $0.80 per common share in fiscal 2012 amounting to an aggregate of $19.7 million, $43.8 million and $19.4 million for fiscal 2014, 2013 and 2012, respectively. We expect to continue paying a quarterly dividend in future quarters, although the amount and timing of dividends, if any, will be determined by our Board of Directors in each quarter, subject to compliance with applicable law.

12

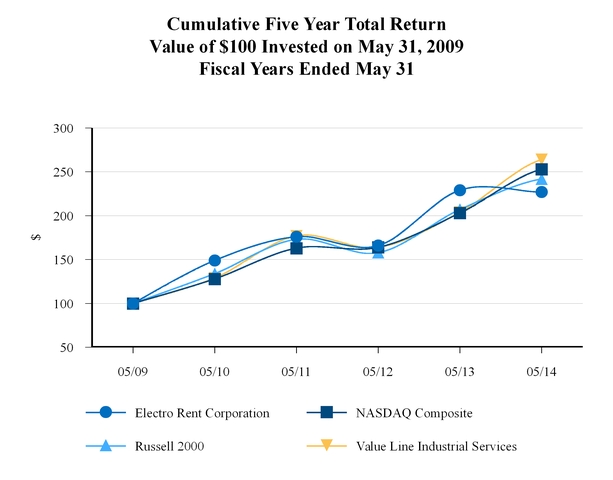

Performance Graph.

The graph below compares our total shareholder return with (1) the NASDAQ Composite Index, (2) the Russell 2000 Index, and (3) the composite prices of the companies listed by Value Line, Inc. in its Industrial Services Industry Group. Our Common Stock is listed in both the Russell 2000 Index and the Industrial Services Industry Group. The comparison is over a five year period, beginning May 31, 2009 and ending May 31, 2014. The total shareholder return assumes $100 invested at the beginning of the period in our Common Stock and in each index. It also assumes reinvestment of all dividends.

2009 | 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||

Electro Rent Corporation | 100 | 149 | 176 | 166 | 229 | 227 | |||||||||||

NASDAQ Composite | 100 | 128 | 163 | 164 | 203 | 253 | |||||||||||

Russell 2000 | 100 | 134 | 173 | 158 | 207 | 242 | |||||||||||

Value Line Industrial Services | 100 | 129 | 177 | 164 | 204 | 264 | |||||||||||

Item 6. Selected Financial Data.

(in thousands, except per share amounts)

The following selected consolidated financial data should be read in conjunction with our audited consolidated financial statements and the accompanying notes included in “Item 8. Financial Statements and Supplementary Data” below and other financial and statistical information included in this Annual Report on Form 10-K.

13

Fiscal year ended May 31, | |||||||||||||||||||

2014 | 2013 | 2012 (1) | 2011 | 2010 (2) | |||||||||||||||

Operations data: | |||||||||||||||||||

Revenues | $ | 241,137 | $ | 248,731 | $ | 248,554 | $ | 228,729 | $ | 145,867 | |||||||||

Costs of revenues and depreciation | 150,078 | 155,477 | 159,218 | 144,582 | 90,319 | ||||||||||||||

Selling, general and administrative expenses | 58,920 | 56,543 | 53,250 | 47,412 | 37,794 | ||||||||||||||

Operating profit | 32,139 | 36,711 | 36,086 | 36,735 | 17,754 | ||||||||||||||

Bargain purchase gain, net (3) | — | — | 3,435 | 202 | 679 | ||||||||||||||

Interest and other, net | 387 | 402 | 484 | 352 | 1,599 | ||||||||||||||

Income before income taxes | 32,526 | 37,113 | 40,005 | 37,289 | 20,032 | ||||||||||||||

Income tax provision | 12,118 | 14,359 | 14,233 | 13,533 | 8,435 | ||||||||||||||

Net income | $ | 20,408 | $ | 22,754 | $ | 25,772 | $ | 23,756 | $ | 11,597 | |||||||||

Earnings per share: | |||||||||||||||||||

Basic | $ | 0.84 | $ | 0.94 | $ | 1.07 | $ | 0.99 | $ | 0.48 | |||||||||

Diluted | $ | 0.84 | $ | 0.94 | $ | 1.07 | $ | 0.99 | $ | 0.48 | |||||||||

Shares used in per share calculation: | |||||||||||||||||||

Basic | 24,325 | 24,226 | 23,983 | 23,974 | 23,932 | ||||||||||||||

Diluted | 24,357 | 24,269 | 24,152 | 24,072 | 24,004 | ||||||||||||||

Balance sheet data (at end of year): | |||||||||||||||||||

Total assets | $ | 302,058 | $ | 318,926 | $ | 329,831 | $ | 305,927 | $ | 276,068 | |||||||||

Bank borrowings | $ | — | $ | 10,000 | $ | — | $ | — | $ | — | |||||||||

Shareholders’ equity | $ | 230,958 | $ | 228,549 | $ | 248,131 | $ | 240,375 | $ | 229,962 | |||||||||

Shareholders’ equity per common share | $ | 9.62 | $ | 9.52 | $ | 10.34 | $ | 10.02 | $ | 9.60 | |||||||||

Cash dividends declared per common share | $ | 0.80 | $ | 1.80 | $ | 0.80 | $ | 0.60 | $ | 0.45 | |||||||||

(1) | Includes the post-acquisition operating results and year-end balance sheet information for the assets acquired from EMT on August 24, 2011. (See Note 3 to the consolidated financial statements included in this Annual Report on Form 10-K). |

(2) | Includes the post-acquisition operating results and year-end balance sheet information for the assets acquired from Telogy on March 31, 2010. |

(3) | The estimated fair value of the net assets acquired from EMT in fiscal 2012 and Telogy in fiscal 2010 (further adjusted in fiscal 2011) exceeded the acquisition cost, resulting in bargain purchase gains with respect to these transactions. |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion of our financial condition and results of operations should be read in conjunction with the consolidated financial statements and the notes thereto and the other financial and statistical information appearing elsewhere in this Annual Report on Form 10-K.

OVERVIEW

We are one of the largest global organizations devoted to the rental, lease and sale of new and used electronic T&M equipment. We purchase that equipment from leading manufacturers such as Keysight, Anritsu, and Tektronix primarily for use by our customers in the aerospace, defense, telecommunications, electronics, industrial and semiconductor industries.

In addition, although it represented only approximately 8%, 7% and 7% of our revenues in fiscal 2014, 2013 and 2012, respectively, we believe our DP division is one of the largest rental businesses in the United States for personal computers and servers from manufacturers including Dell, HP/Compaq, IBM, Toshiba and Apple.

In fiscal 2010, we became a reseller for Agilent, the largest T&M equipment manufacturer in North America. On May 29, 2014, we entered into a new agreement with Agilent, pursuant to which we were appointed as a reseller for certain new and premium used T&M products and services in the United States and Canada. This agreement replaced and superseded the previous agreement dated December 1, 2009, which expired according to its terms on May 31, 2014. Agilent has, effective August 1, 2014, assigned our reseller agreement to its wholly-owned subsidiary, Keysight, in connection with the planned spin-off by Agilent of Keysight into a separate publicly traded company, which Agilent has announced it expects to complete by November

14

2014. Our reseller agreement with Keysight provides us with the exclusive right to sell Keysight’s more complex T&M equipment to small and medium size customers (who previously purchased directly from Agilent/Keysight).

We do not currently have reseller agreements with any other manufacturers for equipment similar to that included in our Keysight reseller agreement. In addition, we sell used equipment from a variety of manufacturers that was previously in our rental and lease pool.

We have a focused sales strategy, using a direct sales force to meet our customers’ needs in our T&M equipment rental, lease and sales business. We have a large technical sales force that consists primarily of field engineers and applications engineers, each of whom specializes in all the products and services offered by our company. Our sales force is usually assigned to specific territories, and identifies potential customers through coordinated efforts with our marketing organization. Our marketing organization is staffed by professionals with many years of industry-related experience. As our customers have a wide range of requirements for equipment, our sales force is able to leverage our extensive knowledge of the test and measurement equipment environment to determine the right product to rent, lease or sell to the customer to meet the customer’s specific needs.

Our sales force also specializes in configuring new Keysight equipment to sell to our customers that is tailored to the customer’s need. These configurations typically start with a base model, which is frequently upgraded through an extensive list of options in order to perform the customer’s specific test or measurement. Once the configuration is determined, it serves as the basis for our orders to Keysight, who builds the product accordingly. We order equipment from Keysight once the customer has placed an order with us. Equipment is typically shipped directly to the customer by Keysight at our request. Occasionally, equipment is shipped to our warehouse prior to delivery to the customer. Inventory held for sale is immaterial and is therefore included in other assets in our consolidated balance sheets. Each order and sales invoice is subject to our standard sales terms and conditions, which include provisions covering equipment delivery delays and warranty services.

On August 24, 2011, we completed the acquisition of certain assets (including accounts receivable and rental equipment but excluding certain designated assets) and the assumption of specified post-closing liabilities of EMT, for $10.7 million in cash, of which $0.5 million was deposited into an escrow account for any post-closing adjustments. The purchase price was reduced by $0.3 million reflecting the final determination of the post-closing adjustment of the purchase price in accordance with the asset purchase agreement with EMT. (See Note 3 to the consolidated financial statements included in this Annual Report on Form 10-K).

In recent years, our financial results have been impacted by competitive pressure on rental rates due in large part to the recession and subsequent weakness in the U.S. economy and our major international markets. During fiscal 2013, our revenues were flat compared to fiscal 2012 as growth in our rental and leasing business and increased sales of used equipment, in part due to a large buyout of used equipment by a customer in the third fiscal quarter of 2013, was offset by a decline in sales of new equipment. Our operating profit increased modestly for fiscal 2013 as compared to fiscal 2012, as growth in our higher margin rental and lease revenues and used equipment sales offset declines in our sales of new equipment, which typically have lower operating margins. During fiscal 2014, our revenues declined slightly and our operating profit declined moderately as compared to fiscal 2013, primarily due to a decline in our new equipment sales revenue, partially offset by growth in our higher margin rental and lease revenues. Our new equipment sales continue to be affected by delays in our customers’ procurement decisions, resulting in decreased demand, particularly in the aerospace and defense sector due to uncertainty regarding U.S. government defense spending. We have also seen a softening in the telecommunications and semiconductor manufacturing sectors. We experienced an increase in our selling, general and administrative expenses as a result of our infrastructure investment which began in fiscal 2011 and continued throughout fiscal 2012, 2013 and 2014 in support of our continued investment in our oversees operations, the strengthening of our IT and financial infrastructure and the expansion of our sales and marketing organization in support of future opportunities.

Economic uncertainty continues to impact certain industries that we serve. We will continue to focus on remaining profitable in the current conditions, as well as being prepared for the possibility that recessionary trends may return in future periods.

To maximize our overall profit from the rental, leasing, and sales of equipment, we manage our equipment pool on an on-going basis by controlling the timing, pricing and mix of our purchases and sales of equipment. We acquire new and used equipment to meet current technological standards and current and anticipated customer demand, and we sell our used equipment where we believe that is the most lucrative option. We employ a complex equipment management strategy and our proprietary PERFECT software to adjust our equipment pool and pricing on a dynamic basis in order to maximize equipment availability, utilization and profitability. If we do not accurately predict market trends, or if demand for the equipment we supply declines, we can be left with equipment that we are unable to rent or sell for a profit. We assess the carrying value of the equipment pool on an annual basis or more frequently when factors indicating potential impairment are present.

15

We have revenues, expenses, assets and liabilities in foreign currencies, primarily the euro, the Canadian dollar and the Chinese yuan, due to our foreign operations. We enter into forward contracts to hedge against unfavorable currency fluctuations in our monetary assets and liabilities in our European and Canadian operations. Our exposure to fluctuations in the Chinese yuan is not significant. These contracts are designed to minimize the effect of fluctuations in foreign currencies. As a result of these forward contracts, as well as the relative stability of these foreign currencies, the impact on our operating results from foreign currency fluctuations has been insignificant. See “Item 7A-Quantitative and Qualitative Disclosures about Market Risk-Changes in Foreign Currencies” for additional information about our exposure to foreign currency exchange risk.

Profitability and Key Business Trends

Comparing fiscal 2014 to fiscal 2013, our revenues decreased by 3.1% from $248.7 million to $241.1 million, our operating profit decreased 12.5% from $36.7 million to $32.1 million and our net income decreased by 10.3% from $22.8 million to $20.4 million.

Our rental and lease revenues increased by 0.6%, from $136.6 million for fiscal 2013 to $137.4 million for fiscal 2014. For fiscal 2014 and 2013, 88% of our rental and lease revenues were derived from T&M equipment. Our T&M rental revenues decreased $0.1 million due to a decrease in demand of $2.2 million offset by an increase in rental rates of $2.1 million. Our T&M lease revenues decreased $0.1 million due to a decrease in lease rates of $0.4 million offset by an increase in demand of $0.3 million. Rental and lease revenues in our DP segment increased $0.6 million and $0.4 million, respectively, due to an increase in rental and lease rates.

Our sales of equipment and other revenues decreased 7.5%, from $112.1 million for fiscal 2013 to $103.7 million for fiscal 2014. This decrease was primarily due to a decline in new equipment sales, which continue to be affected by delays in our customers’ procurement decisions, resulting in decreased demand, particularly in the aerospace and defense sector due to uncertainty regarding U.S. government defense spending. We have also seen a softening in the telecommunications and semiconductor manufacturing sectors.

For fiscal 2014, our operating profit decreased 12.5% compared to fiscal 2013. Our rental and lease business contributed an additional $0.1 million in operating profit resulting from a) a $0.8 million, or 0.6%, increase in rental and lease revenues, b) an offsetting increase in depreciation expense of $0.2 million, or 0.4%, due to a higher average rental equipment pool, and c) an offsetting increase in our costs of rentals and leases, excluding depreciation, of $0.5 million, or 2.8%. Sales of equipment and other revenues decreased $8.4 million, or 7.5%, resulting in a decline of $2.3 million in operating profit. Although our higher margin used equipment sales contributed an additional $1.7 million in revenue, this was offset by a $9.1 million decline in revenue from sales of our lower margin new equipment. The remaining decrease in sales of equipment and other revenues is attributable to a $1.0 million decrease in other revenue. Our selling, general and administrative expenses increased by 4.2% from $56.5 million in fiscal 2013 to $58.9 million in fiscal 2014, primarily due to our continued investment in our oversees operations, the strengthening of our IT and financial infrastructure and the expansion of our sales and marketing organization in support of future opportunities. Our net income for fiscal 2012 included a bargain purchase gain, net of deferred taxes, of $3.4 million as a result of our acquisition of EMT.

Some of our key profitability measurements are presented below:

Fiscal 2014 | Fiscal 2013 | Fiscal 2012 | |||||||||

Net income per diluted common share (EPS) | $ | 0.84 | $ | 0.94 | $ | 1.07 | |||||

Net income as a percentage of average assets | 6.5 | % | 7.0 | % | 8.1 | % | |||||

Net income as a percentage of average equity | 8.8 | % | 9.6 | % | 10.7 | % | |||||

Our average acquisition cost of equipment for rent and lease in our equipment pool is presented below:

Average acquisition cost of equipment (in millions) | Fiscal 2014 vs. Fiscal 2013 | Fiscal 2013 vs. Fiscal 2012 | |||||||||||||||||||

2014 | 2013 | Change | 2013 | 2012 | Change | ||||||||||||||||

On rent | $ | 238.6 | $ | 245.5 | (2.8 | )% | $ | 245.5 | $ | 234.1 | 4.9 | % | |||||||||

On lease | $ | 37.2 | $ | 35.0 | 6.3 | % | $ | 35.0 | $ | 31.7 | 10.4 | % | |||||||||

The decrease in our average equipment on rent is due to a decline in demand in our T&M North American operations, in particular in the aerospace and defense sector, partially offset by increased demand in our T&M foreign operations. Our average equipment on lease increased due to higher demand in North American operations.

16

Average rental rates increased by 2.8% in fiscal 2014 as compared to fiscal 2013 and 2.7% as compared to fiscal 2012. Our average lease rates decreased by 0.8% in fiscal 2014 as compared to fiscal 2013, and 3.4% as compared to fiscal 2012. The increase in rental rates is the result of growth in industries where we realize higher rental rates.

Average utilization for our T&M equipment pool, calculated based on average acquisition cost of equipment on rent and lease compared to the average total equipment pool, decreased to 64.9% for fiscal 2014, compared to 66.9% for fiscal 2013 and 67.7% for fiscal 2012. The average utilization of our DP equipment pool, based on the same method of calculation, was 35.7% for fiscal 2014, compared to 35.6% for fiscal 2013 and 38.1% for fiscal 2012. Our utilization rate fluctuates frequently, and is impacted by new equipment purchases in support of existing and potential business, and sales of used equipment.

As of May 31, 2014, we had a sales order backlog for new T&M equipment of $10.7 million, compared to $7.6 million as of May 31, 2013 and $8.4 million as of May 31, 2012. The increase in backlog is primarily due to longer manufacturing lead times on certain products as well as an increase in demand.

RESULTS OF OPERATIONS

Fiscal 2014 Compared with Fiscal 2013

Total Revenues: Total revenues for fiscal 2014 and 2013 were $241.1 million and $248.7 million, respectively. The 3.1% decrease in total revenues was due to a 7.5% decrease in sales of equipment and other revenues offset by a 0.6% increase in rental and lease revenues.

Rental and lease revenues for fiscal 2014 were $137.4 million, compared to $136.6 million for the prior fiscal year. This increase is due to an increase in rental rates in our T&M and DP segments, due to our growth in industries where we realize higher rental rates, and increased demand in our Chinese and European operations. This increase was offset, in part, by a decrease in demand in our North American operations due to softening in the aerospace and defense and semiconductor industries. Our lease revenues increased primarily due to higher demand for T&M equipment, while our DP lease revenues increased slightly.

Sales of equipment and other revenues decreased to $103.7 million for fiscal 2014 from $112.1 million in the prior year. Sales of used equipment, including finance leases, increased to $32.8 million for fiscal 2014, compared to $31.0 million for fiscal 2013 while sales of new equipment decreased to $65.8 million for fiscal 2014 compared to $74.9 million for fiscal 2013. Our new equipment sales continue to be affected by delays in our customers’ procurement decisions, resulting in decreased demand, particularly in the aerospace and defense sector due to uncertainty regarding U.S. government defense spending. We have also seen a softening in the telecommunications and semiconductor manufacturing sectors.

Operating expenses

Depreciation of Rental and Lease Equipment: Depreciation of rental and lease equipment remained relatively consistent at $57.0 million, or 41.5% of rental and lease revenues in fiscal 2014 compared to $56.8 million, or 41.6% of rental and lease revenues in fiscal 2013. The depreciation ratio stayed consistent due to increases in our rental rates of our DP equipment offset by decreases in our lease and utilization rates of our T&M equipment.

Costs of Rentals and Leases, Excluding Depreciation: Costs of rentals and leases, excluding depreciation, which primarily includes labor related costs of our operations personnel, supplies, repairs, and insurance and warehousing costs associated with our rental and lease equipment, increased to $18.3 million for fiscal 2014 compared to $17.8 million for fiscal 2013, primarily due to higher labor related costs to support growth in our rental and lease business. This expense is not expected to significantly fluctuate from period to period, as only moderate changes are required from time to time to handle changes in rental and lease activity.

Costs of Sales of Equipment and Other Revenues: Costs of sales of equipment and other revenues, which primarily include the costs of equipment sales, decreased to $74.8 million for fiscal 2014 from $80.9 million in fiscal 2013. Costs of sales of equipment and other revenues as a percentage of sales of equipment and other revenues remained flat at 72.1% in fiscal 2014 and fiscal 2013. Our sales margin percentage is expected to fluctuate depending on the mix of used and new equipment sales. Our sales margin is also impacted by competition, economic uncertainty, changes in U.S. governmental policies, and customer requirements and funding.

Selling, General and Administrative Expenses: Selling, general and administrative expenses increased 4.2% to $58.9 million in fiscal 2014 compared to $56.5 million in fiscal 2013. As a percentage of total revenues, selling, general and administrative expenses increased modestly to 24.4% in fiscal 2014 from 22.7% in fiscal 2013. The increase in selling, general, and administrative reflects our continued investment in our oversees operations, the strengthening of our IT and financial infrastructure and the expansion of our sales and marketing organization in support of future opportunities.

17

Income Tax Provision: Our effective tax rate was 37.3% for fiscal 2014, compared to 38.7% for fiscal 2013. The decrease for fiscal 2014 is due to more income being apportioned to states with lower tax rates resulting in a lower effective state rate as well as the recognition of certain Belgian tax credits which had no impact in fiscal 2013.

Fiscal 2013 Compared with Fiscal 2012

Total Revenues: Total revenues for fiscal 2013 and 2012 were $248.7 million and $248.6 million, respectively. The 0.1% increase in total revenues was due to a 5.3% increase in rental and lease revenues offset by a 5.6% decrease in sales of equipment and other revenues.

Rental and lease revenues for fiscal 2013 were $136.6 million, compared to $129.7 million for the prior fiscal year. This increase was due to an increase in T&M rental and lease demand, in particular in our North American operations, due in part to the acquisition of EMT, and the integration of our resale organization and T&M sales force, which began in the first quarter of fiscal 2012, providing additional rental opportunities to an expanding customer base, and higher demand from our customers in lieu of new equipment purchases. This increase was partially offset by a decline in rental and lease revenues in our DP business, due to a decrease in demand.

Sales of equipment and other revenues decreased to $112.1 million for fiscal 2013 from $118.8 million in the prior year. Sales of used equipment, including finance leases, increased to $31.0 million for fiscal 2013, compared to $24.9 million for fiscal 2012, in part due to a large buyout by a customer in the third quarter of fiscal 2013, while sales of new equipment decreased to $75.0 million for fiscal 2013 compared to $88.4 million for fiscal 2012, as our customers that traditionally purchase new equipment delayed procurement decisions due to changes in the U.S. national budgetary policy and uncertainty in the global economy.

Operating expenses

Depreciation of Rental and Lease Equipment: Depreciation of rental and lease equipment increased in fiscal 2013 to $56.8 million, or 41.6% of rental and lease revenues, from $53.7 million, or 41.4% of rental and lease revenues, in fiscal 2012. The increased depreciation expense in fiscal 2013 was due to a higher average rental and lease equipment pool. The depreciation ratio, as a percentage of rental and lease revenues, marginally increased due to a moderate decline in utilization rates while rental rates were flat.

Costs of Rentals and Leases, Excluding Depreciation: Costs of rentals and leases, excluding depreciation, which primarily include labor related costs of our operations personnel, supplies, repairs, and insurance and warehousing costs associated with our rental and lease equipment, increased to $17.8 million for fiscal 2013 compared to $17.3 million for fiscal 2012, primarily due to higher labor related costs to support growth in our rental and lease business. This expense is not expected to significantly fluctuate from period to period, as only moderate changes are required from time to time to handle changes in rental and lease activity.

Costs of Sales of Equipment and Other Revenues: Costs of sales of equipment and other revenues, which primarily include the costs of equipment sales, decreased to $80.9 million for fiscal 2013 from $88.2 million in fiscal 2012. Costs of sales of equipment and other revenues decreased as a percentage of sales of equipment and other revenues to 76.3% in fiscal 2013 from 77.8% in fiscal 2012. This decrease is due to a decline in sales of new T&M equipment, which generally carry a lower margin than used equipment sales, while higher margin used equipment sales increased. Our sales margin percentage is expected to fluctuate depending on the mix of used and new equipment sales. Our sales margin is also impacted by competition, economic uncertainty, changes in U.S. governmental policies, and customer requirements and funding.